Form N-CSR UNIFIED SERIES TRUST For: Aug 31

Tweet

Tweet Share

Shareunited

states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

| Investment Company Act file number | 811-21237 |

| Unified Series Trust |

| (Exact name of registrant as specified in charter) |

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Address of principal executive offices)

(Zip code)

Zachary P. Richmond

Ultimus Fund Solutions, LLC

225 Pictoria Drive. Suite 450

Cincinnati, OH 45246

(Name and address of agent for service)

| Registrant’s telephone number, including area code: | 513-587-3400 |

Date of fiscal year end: 8/31

Date of reporting period: 8/31/23

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| (a) |

| Tactical Multi-Purpose Fund |

| Annual Report |

| August 31, 2023 |

| Fund Adviser: |

| Fisher Asset Management, LLC |

| 6500 International Parkway, Suite 2050 |

| Plano, Texas 75093 |

| (800) 550-1071 |

Tactical

Multi-Purpose Fund

Management’s Discussion of Fund Performance

(Unaudited)

Dear Shareholder:

Market Commentary and Outlook

Last year, we expected an early grind with a rally late. But the negative drumbeat of war, inflation, interest rate hikes, political rancor and more dragged stocks down into a minor bear market. Usually, stocks move past such widely known factors quickly. But 2022’s constant drip of negatives created a year-long fog of uncertainty. Even when reality turned out to be better than feared—like second-half economic data—pessimists dismissed it, warning worse was still ahead, a classic sign of “the pessimism of disbelief.” However, markets appear to have reckoned with many of these concerns, and improvement on some—like inflation—made the last year a good one for global equities. Stocks rose +15.6% since a year ago and +28.0% since the October 12th 2022 low.

The Q2 2023 end closes a nearly picture-perfect example of the nine-month “Midterm Miracle.” This stretch is history’s most consistently positive, up 91.7% of the time and averaging +19.6% gains. On cue, the S&P 500 surged 25.7% from last September 30 through June. The Midterm Miracle might be over but the positivity party isn’t. In our view, gridlock should remain a tailwind for stocks in the second half—and into 2024. Third years’ second halves aren’t as consistently positive or strong as the first, but gains tend to continue.

Despite these positives, the bull market features a classic “wall of worry”—a barrage of investor fears tamping down sentiment as stocks climb higher. Nearly a year since stocks’ low, the rally is getting a bit more love, but not much. Some don’t acknowledge a new bull market. Many who do see little reason stocks can keep thriving. Today’s wide gulf between sentiment and reality is a classic early bull market feature. The “wall” has many bricks.

The springtime batch of regional bank failures is a big brick in this bull market’s worry wall. It bridged Q1 and Q2, from Silicon Valley Bank’s March failure through First Republic’s travails and sale to JPMorgan Chase in May. In between, headlines painted a dire picture akin to 2008. While lending has slowed—as we expected—it remains healthy at 5.8% y/y as of June 28. Emergency bank borrowing from the Fed has flattened, and new borrowings from the Discount Window—its traditional crisis facility—have tanked. As for the Bank Term Funding Program created early this year, use is up, but this doesn’t seem like a sign of systemic stress, given friendly collateral terms and rates banks can lock in for a year. While more small banks could fail or face profit headwinds and industry consolidation might loom, we think systemic crisis fears have, rightly, evaporated.

1

Tactical

Multi-Purpose Fund

Management’s Discussion of Fund Performance

(Unaudited) (continued)

Of all the drags on sentiment since early 2022, none has dug in quite like inflation. Companies might be coping relatively well, with robust profit margins and a 28.0% MSCI World return from last October’s low, but people are weary. The US inflation rate has slowed markedly since June 2022’s peak, yet many only noticed recently and complain core prices are still rising too fast. People see more stubborn prices in the UK and Europe, worrying stickier inflation there necessitates even more rate hikes, rendering a recession that infects the world. Yet on both sides of the Atlantic, there are many encouraging signs. Sentiment has fallen too far, vastly underrating improvements and creating a big inflation wall of worry.

As for short rates, again, central banks are unpredictable. But this rate hike cycle looks close to done. After slowing its rate hike pace to a quarter point in March and April, the Fed paused in June. This doesn’t preclude more hikes, a possibility many focus on. With inflation moderating, this seems rational.

Not that stocks need a rate pause or cuts, as many argue today. Pundits who focus on this are hyperventilating unnecessarily, considering there is ample evidence stocks already overcame rate hikes. The S&P 500 is up nicely since June 2022, despite most of the Fed’s rate hikes (and their biggest moves) occurring since then. The ECB started hiking last July. Eurozone stocks? Up double digits since then in euros and dollars. UK stocks were among the MSCI World’s best performers in 2022 despite the BoE starting its tightening cycle in December 2021. They hit all-time highs in February amid more hiking.

If all of these rate hikes didn’t prevent stocks from rising over the last year, it seems pretty clear rate hikes aren’t driving markets. It is also clear stocks aren’t waiting for pauses or rate cuts. They are doing what they always do, pricing in expected earnings over the next 3 – 30 months. Those will likely hinge on far more than interest rates.

Expectations for China’s economy were high entering Q2 2023. Fiscal and monetary stimulus was kicking in, the weather was warming up, and people were free to shop and travel. The stage seemed set for a newly reopened economy to roar back. Yet hope got a bit too lofty, and April and May economic data didn’t quite meet it—see widely watched retail sales and industrial production.

Retail sales illustrate the trend. After March’s sales beat expectations, many extrapolated red-hot growth forward. Yet April and May’s growth, while faster than March’s, missed forecasts. We suspect complicated year-over-year comparisons played a role here. April and May 2022 were when Shanghai and other major metro areas were locked down. Analysts rightly factored in a low base. But perhaps they underestimated how society

2

Tactical

Multi-Purpose Fund

Management’s Discussion of Fund Performance

(Unaudited) (continued)

had already learned to adapt to restrictions two years into the pandemic. Perhaps it was because the growth rates in those quarters had their own upward base-effect skew from 2021’s initial reopening boost. Regardless, the miss discouraged those with high hopes for China’s economy.

Tepid data drove fears of China lapsing into an unprecedented economic malaise, with high debt, prolonged property market weakness and poor demographics stymieing growth. However, it looks like China is returning to longer-term economic trends. Slower growth would also match the government’s long-term goal of transitioning away from heavy industry- and export-driven growth to a model buttressed by domestic demand and services—akin to major Western economies. Note, too, a decelerating China still contributes mightily to the global economy: Last year’s 3.0% annual real growth added nearly $490 billion to global GDP when measured in constant 2015 US dollars.

Performance Attribution

The Tactical Multi-Purpose Fund (the “Fund”) seeks positive total returns over the long-term regardless of market conditions in the U.S. and foreign equity markets. The Fund is designed to be used by the Adviser to facilitate moving groups of clients into and out of defensive and special situation investments efficiently, based on the Adviser’s perceptions of market risks and opportunities.

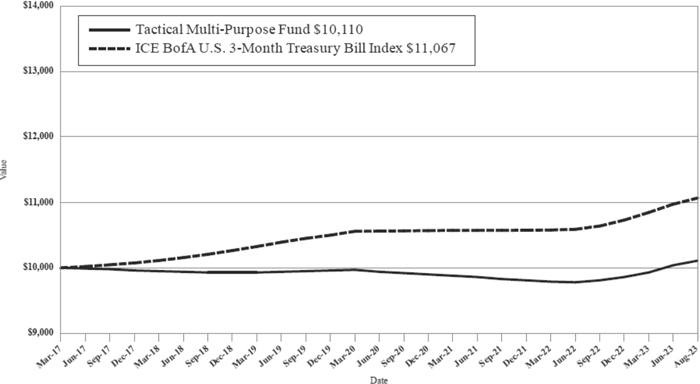

During the fiscal year ended August 31, 2023, the Adviser did not take a defensive position; therefore the Fund was limited in size, with its assets invested mostly in T-Bills and cash equivalents. The Fund returned +3.16% during the fiscal year ended August 31, 2023. During the same period, the Fund’s primary benchmark, the ICE BofA 3-month U.S. Treasury Bill Index, returned 4.28%.

The Fund’s relative underperformance is reflective of its modest investment in T-Bills and cash equivalents for the period, which generated minimal interest. Underperformance as compared to the index is also in part due to the Fund’s 1.00% expense ratio (the performance of the index does not reflect the deduction of expenses). Due to the size of the investment, the Fund maintained a sizeable portion of the investments in cash equivalents to meet expense obligations. However, T-Bills were purchased throughout the period to opportunistically benefit from changes by the Fed to short rates. It is anticipated that similar positioning will continue until the Adviser utilizes the Fund for defensive purposes or prevailing short-term interest rates meaningfully change.

Portfolio Shifts

No portfolio shifts have been made to the Fund.

3

Investment Results (Unaudited)

Average Annual Total Returns(a)

as of August 31, 2023

| Since Inception | |||||

| Fund/Index | One Year | Five Year | (3/30/17) | ||

| Tactical Multi-Purpose Fund | 3.16% | 0.36% | 0.17% | ||

| ICE BofA 3-Month U.S. Treasury Bill(b) | 4.28% | 1.66% | 1.59% |

Total annual operating expenses, as disclosed in the Tactical Multi-Purpose Fund (the “Fund”) prospectus dated December 29, 2022, were 644.33% of average daily net assets (1.14% after fee waivers/expense reimbursements). Fisher Asset Management, LLC, d/b/a Fisher Investments (the “Adviser”) is contractually obligated to limit the Fund’s total annual operating expenses to 1.00% of the Fund’s average daily net assets through December 31, 2027 (excluding portfolio transaction and other investment-related costs (including brokerage fees and commissions); taxes; borrowing costs (such as interest and dividend expenses on securities sold short); acquired fund fees and expenses; fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example option and swap fees and expenses); any amounts payable pursuant to a distribution or service plan adopted in accordance with Rule 12b-1 under the Investment Company Act of 1940, as amended, any administrative and/or shareholder servicing fees payable pursuant to a plan adopted by the Board of Trustees; expenses incurred in connection with any merger or reorganization; extraordinary expenses (such as litigation expenses, indemnification of Trust officers and Trustees and contractual indemnification of Fund service providers); and other expenses that the Trustees agree have not been incurred in the ordinary course of the Fund’s business). This expense cap may not be terminated prior to this date except by the Board of Trustees upon 60 days’ written notice to the Adviser. Each expense payment by the Adviser (but not management fee waiver) is subject to recoupment by the Adviser from the Fund in the three years following the date the particular expense payment occurred, but only if such recoupment can be achieved without exceeding the annual expense limitation in effect at the time of the expense payment and any expense limitation in effect at the time of recoupment. Additional information pertaining to the Fund’s expense ratios as of August 31, 2023 can be found in the financial highlights.

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance of the Fund may be lower or higher than the performance quoted. The Fund’s investment objective, risks, charges and expenses should be considered carefully before investing. Performance data current to the most recent month-end may be obtained by calling (800) 550-1071.

| (a) | Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. |

| (b) | The ICE BofA 3-Month U.S. Treasury Bill Index (the “Index”) is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the Index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date. The Index returns assume reinvestment of all distributions and do not reflect the deduction of taxes and fees. Individuals cannot invest directly in the Index. However, an individual may invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

4

Investment Results (Unaudited) (continued)

You should consider the Fund’s investment objective, risks, charges and expenses carefully before you invest. The Fund’s prospectus contains important information about the Fund’s investment objective, potential risks, management fees, charges and expenses, and other information and should be read carefully before investing. You may obtain a current copy of the Fund’s prospectus or performance data current to the most recent month-end by calling (800) 550-1071.

Comparison of the Growth of a $10,000 Investment in the Tactical Multi-Purpose Fund and the ICE BofA U.S. 3-Month Treasury Bill Index.

This graph shows the value of a hypothetical initial investment of $10,000 made on March 30, 2017 (commencement of operations) and held through August 31, 2023. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The ICE BofA 3-Month U.S. Treasury Bill Index is an unmanaged index of Treasury securities that assumes reinvestment of all income. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call (800) 550-1071. You should carefully consider the investment objective, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

The Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

5

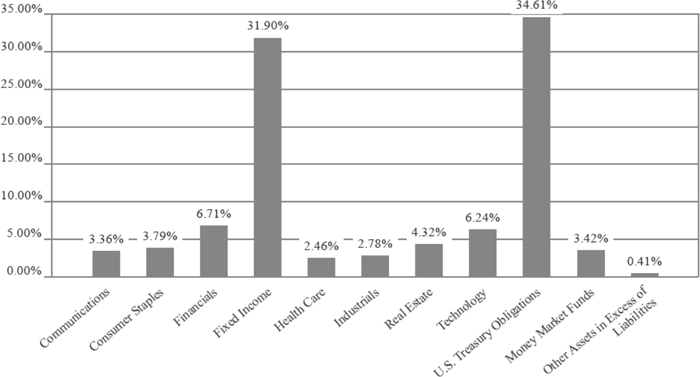

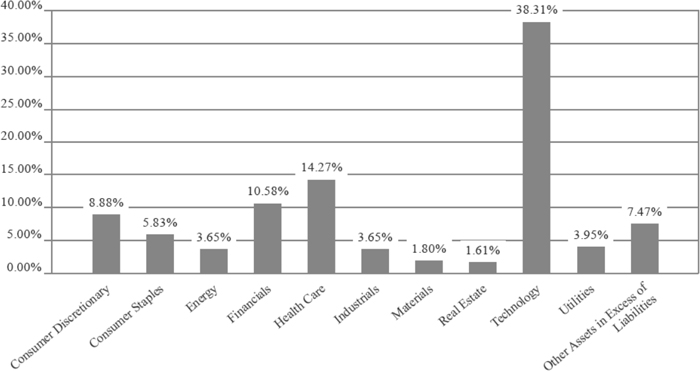

Fund Holdings (Unaudited)

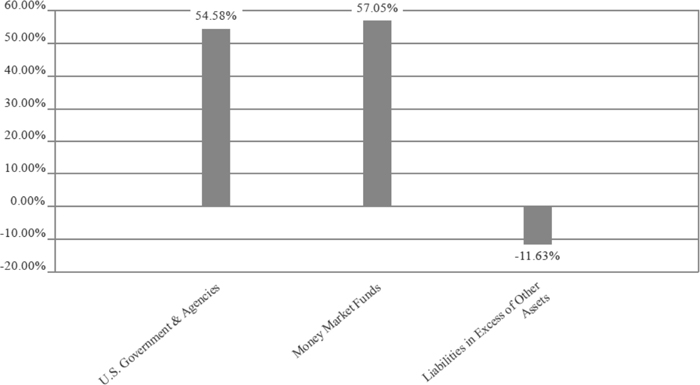

Tactical Multi-Purpose Fund Holdings as of August 31, 2023*

| * | As a percentage of net assets. |

The investment objective of the Fund is to seek positive total returns over the long-term regardless of market conditions in the U.S. and foreign equity markets.

Availability of Portfolio Schedule (Unaudited)

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (the “SEC”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Fund’s Form N-PORT reports are available on the SEC’s website at www.sec.gov.

6

| Tactical Multi-Purpose Fund |

| Schedule of Investments |

| August 31, 2023 |

| Principal | ||||||||

| Amount | Fair Value | |||||||

| U.S. GOVERNMENT & AGENCIES — 54.58% | ||||||||

| United States Treasury Bill, 5.50%, 12/12/2023 | $ | 14,000 | $ | 13,790 | ||||

| Total U.S. Government & Agencies (Cost $13,834) | 13,790 | |||||||

| Shares | ||||||||

| MONEY MARKET FUNDS - 57.05% | ||||||||

| First American Government Obligations Fund, Class X, 5.25%(a) | 14,416 | 14,416 | ||||||

| Total Money Market Funds (Cost $14,416) | 14,416 | |||||||

| Total Investments — 111.63% (Cost $28,250) | 28,206 | |||||||

| Liabilities in Excess of Other Assets — (11.63)% | (2,939 | ) | ||||||

| NET ASSETS — 100.00% | $ | 25,267 | ||||||

| (a) | Rate disclosed is the seven day effective yield as of August 31, 2023. |

See accompanying notes which are an integral part of these financial statements.

7

| Tactical Multi-Purpose Fund |

| Statement of Assets and Liabilities |

| August 31, 2023 |

| Assets | ||||

| Investments in securities at fair value (cost $28,250) | $ | 28,206 | ||

| Interest receivable | 105 | |||

| Receivable from Adviser | 9,115 | |||

| Prepaid expenses | 2,191 | |||

| Total Assets | 39,617 | |||

| Liabilities | ||||

| Payable to affiliates | 2,788 | |||

| Other accrued expenses | 11,562 | |||

| Total Liabilities | 14,350 | |||

| Net Assets | $ | 25,267 | ||

| Net Assets consist of: | ||||

| Paid-in capital | $ | 24,520 | ||

| Accumulated earnings | 747 | |||

| Net Assets | $ | 25,267 | ||

| Shares outstanding (unlimited number of shares authorized, no par value) | 2,500 | |||

| Net asset value, offering and redemption price per share | $ | 10.11 |

See accompanying notes which are an integral part of these financial statements.

8

| Tactical Multi-Purpose Fund |

| Statement of Operations |

| For the year ended August 31, 2023 |

| Investment Income | ||||

| Dividend income | $ | 1,038 | ||

| Interest income | 29 | |||

| Total investment income | 1,067 | |||

| Expenses | ||||

| Fund accounting | 30,002 | |||

| Administration | 30,000 | |||

| Legal | 22,990 | |||

| Trustee | 16,636 | |||

| Compliance services | 12,031 | |||

| Transfer agent | 12,000 | |||

| Audit and tax | 11,076 | |||

| Custodian | 5,000 | |||

| Report printing | 3,367 | |||

| Registration | 391 | |||

| Adviser | 62 | |||

| Miscellaneous | 19,560 | |||

| Total expenses | 163,115 | |||

| Fees waived and/or expenses reimbursed by Adviser | (156,166 | ) | ||

| Fees reduced by Administrator | (6,701 | ) | ||

| Net operating expenses | 248 | |||

| Net investment income | 819 | |||

| Net change in unrealized depreciation of investment securities | (42 | ) | ||

| Net realized and change in unrealized loss on investments | (42 | ) | ||

| Net increase in net assets resulting from operations | $ | 777 |

See accompanying notes which are an integral part of these financial statements.

9

| Tactical Multi-Purpose Fund |

| Statements of Changes in Net Assets |

| August 31, 2023 |

| For the | For the | |||||||

| Year Ended | Year Ended | |||||||

| August 31, | August 31, | |||||||

| 2023 | 2022 | |||||||

| Increase (Decrease) in Net Assets due to: | ||||||||

| Operations | ||||||||

| Net investment income (loss) | $ | 819 | $ | (108 | ) | |||

| Net change in unrealized depreciation of investment securities | (42 | ) | (2 | ) | ||||

| Net increase (decrease) in net assets resulting from operations | 777 | (110 | ) | |||||

| Capital Transactions | ||||||||

| Amount paid for shares redeemed | — | (10 | ) | |||||

| Net decrease in net assets resulting from capital transactions | — | (10 | ) | |||||

| Total Increase (Decrease) in Net Assets | 777 | (120 | ) | |||||

| Net Assets | ||||||||

| Beginning of year | 24,490 | 24,610 | ||||||

| End of year | $ | 25,267 | $ | 24,490 | ||||

| Share Transactions | ||||||||

| Shares redeemed | — | (1 | ) | |||||

| Net decrease in shares | — | (1 | ) | |||||

See accompanying notes which are an integral part of these financial statements.

10

| Tactical Multi-Purpose Fund |

| Financial Highlights |

| (For a share outstanding during each year) |

| For the | For the | For the | For the | For the | ||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| August 31, | August 31, | August 31, | August 31, | August 31, | ||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Selected Per Share Data: | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 9.80 | $ | 9.84 | $ | 9.93 | $ | 9.95 | $ | 9.93 | ||||||||||

| Investment operations: | ||||||||||||||||||||

| Net investment income (loss) | 0.33 | (0.04 | ) | (0.09 | ) | (0.02 | ) | 0.02 | ||||||||||||

| Net realized and unrealized loss | (0.02 | ) | — | (a) | — | — | (a) | — | (a) | |||||||||||

| Total from investment operations | 0.31 | (0.04 | ) | (0.09 | ) | (0.02 | ) | 0.02 | ||||||||||||

| Net asset value, end of year | $ | 10.11 | $ | 9.80 | $ | 9.84 | $ | 9.93 | $ | 9.95 | ||||||||||

| Total Return(b) | 3.16 | % | (0.41 | )% | (0.91 | )% | (0.20 | )% | 0.20 | % | ||||||||||

| Ratios and Supplemental Data: | ||||||||||||||||||||

| Net assets, end of year (000 omitted) | $ | 25 | $ | 24 | $ | 25 | $ | 25 | $ | 25 | ||||||||||

| Ratio of net expenses to average net assets | 1.00 | % | 1.00 | % | 1.00 | % | 1.00 | % | 1.00 | % | ||||||||||

| Ratio of gross expenses to average net assets before waiver and reimbursement | 657.38 | % | 644.19 | % | 635.29 | % | 596.00 | % | 589.45 | % | ||||||||||

| Ratio of net investment income (loss) to average net assets | 3.30 | % | (0.44 | )% | (0.91 | )% | (0.20 | )% | 0.15 | % | ||||||||||

| Portfolio turnover rate | 0 | % | 0 | % | 0 | % | 0 | % | 0 | % | ||||||||||

| (a) | Rounds to less than $0.005 per share. |

| (b) | Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

See accompanying notes which are an integral part of these financial statements.

11

Tactical

Multi-Purpose Fund

Notes to the Financial Statements

August 31, 2023

NOTE 1. ORGANIZATION

The Tactical Multi-Purpose Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified series of Unified Series Trust (the “Trust”) on November 14, 2016. The Trust is an open-end investment company established under the laws of Ohio by an Agreement and Declaration of Trust dated October 14, 2002, as amended (the “Trust Agreement”). The Trust Agreement permits the Board of Trustees of the Trust (the “Board”) to issue an unlimited number of shares of beneficial interest of separate series without par value. The Fund is one of a series of funds currently authorized by the Board. The Fund commenced operations on March 30, 2017. The investment adviser to the Fund is Fisher Asset Management, LLC, d/b/a Fisher Investments (the “Adviser”). The investment objective of the Fund is to seek positive total returns over the long-term regardless of market conditions in the U.S. and foreign equity markets.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”, including Accounting Standards Update 2013-08. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Regulatory update – Tailored Shareholder Reports for Mutual Funds and Exchange-Traded Funds (“ETFs”) – Effective January 24, 2023, the Securities and Exchange Commission (the “SEC”) adopted rule and form amendments to require mutual funds and ETFs to transmit concise and visually engaging streamlined annual and semiannual reports to shareholders that highlight key information. Other information, including financial statements, will no longer appear in a streamlined shareholder report but must be available online, delivered free of charge upon request, and filed on a semiannual basis on Form N-CSR. The rule and form amendments have a compliance date of July 24, 2024. At this time, management is evaluating the impact of these amendments on the shareholder reports for the Fund.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

12

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net realized capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

As of and during the fiscal year ended August 31, 2023, the Fund did not have any liabilities for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations when incurred. During the year, the Fund did not incur any interest or penalties. Management of the Fund has reviewed tax positions taken in tax years that remain subject to examination by all major tax jurisdictions, including federal (i.e., the previous three tax year ends and the interim tax period since then, as applicable) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements and does not expect this to change over the next twelve months.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds of the Trust based on each fund’s relative net assets or another appropriate basis (as determined by the Board).

Security Transactions and Related Income – The Fund follows industry practice and records security transactions on the trade date for financial reporting purposes. The specific identification method is used for determining gains or losses for financial statement and income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis.

Dividends and Distributions – The Fund intends to distribute its net investment income and net realized long-term and short-term capital gains, if any, at least annually. Dividends and distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the period from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified among the components of net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset value (“NAV”) per share of the Fund.

13

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

NOTE 3. NON-DIVERSIFICATION RISK

The Fund is non-diversified, which means it may invest a greater percentage of its assets in a limited number of issuers as compared to other mutual funds that are more broadly diversified. As a result, the Fund’s share price may be more volatile than the share price of some other mutual funds, and the poor performance of an individual holding in the Fund’s portfolio may have a significant negative impact on the Fund’s performance.

NOTE 4. SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS

The Fund values its portfolio securities at fair value as of the close of regular trading on the New York Stock Exchange (“NYSE”) (normally 4:00 p.m. Eastern Time) on each business day the NYSE is open for business. Fair value is defined as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. GAAP establishes a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes.

Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk (the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique). Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained and available from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| ● | Level 1 – unadjusted quoted prices in active markets for identical investments and/or registered investment companies where the value per share is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date |

| ● | Level 2 – other significant observable inputs (including, but not limited to, quoted prices for an identical security in an inactive market, quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

14

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

| ● | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy which is reported is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

Equity securities that are traded on any stock exchange are generally valued at the last quoted sale price on the security’s primary exchange. Lacking a last sale price, an exchange-traded security is generally valued at its last bid price. Securities traded in the Nasdaq over-the-counter market are generally valued at the Nasdaq Official Closing Price. When using market quotations and when the market is considered active, the security is classified as a Level 1 security. In the event that market quotations are not readily available or are considered unreliable due to market or other events, securities are valued in good faith by the Adviser, as Valuation Designee, under oversight of the Board’s Pricing & Liquidity Committee. The Adviser has adopted written policies and procedures for valuing securities and other assets in circumstances where market quotes are not readily available in conformity with guidelines adopted by the Board. In the event that market quotes are not readily available, and the security or asset cannot be valued pursuant to one of the valuation methods, the value of the security or asset will be determined in good faith by the Valuation Designee pursuant to its policies and procedures. Any fair value provided by the Valuation Designee, is subject to the ultimate review of the pricing methodology by the Pricing & Liquidity Committee of the Board on a quarterly basis. Under these policies, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used.

Investments in mutual funds, including money market mutual funds, are generally priced at the ending NAV provided by the service agent of the mutual funds. These securities are categorized as Level 1 securities.

Debt securities are valued by using the mean between the closing bid and ask prices provided by a pricing service. If the closing bid and ask prices are not readily available, the pricing service may provide a price determined by a matrix pricing method. Matrix pricing is a mathematical technique used to value fixed income securities without relying exclusively on quoted prices. Matrix pricing takes into consideration recent transactions, yield, liquidity, risk, credit quality, coupon, maturity, type of issue and any other factors or market data the pricing service deems relevant for the actual security being priced and for other securities with similar characteristics. These securities will generally be categorized as Level 2 securities. If the Valuation Designee decides that a price provided by the pricing service does not accurately reflect the fair value of the securities or when prices are not

15

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

readily available from a pricing service, securities are valued at fair value as determined by the Valuation Designee, in conformity with guidelines adopted by and subject to review of the Board through its Pricing & Liquidity Committee. These securities will generally be categorized as Level 3 securities.

In accordance with the Trust’s valuation policies and fair value determinations pursuant to Rule 2a-5 under the 1940 Act, the Valuation Designee is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single method exists for determining fair value because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of a security being valued by the Valuation Designee would be the amount that the Fund might reasonably expect to receive upon the current sale. Methods that are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market prices of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. Fair-value pricing is permitted if, in the Valuation Designee’s opinion, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before the Fund’s NAV calculation that may affect a security’s value, or the Valuation Designee is aware of any other data that calls into question the reliability of market quotations. The Valuation Designee may obtain assistance from others in fulfilling its duties. For example, it may seek assistance from pricing services, fund administrators, sub-advisers, accountants, or counsel; it may also consult the Trust’s Fair Value Committee. The Valuation Designee, however, remains responsible for the final fair value determination and may not designate or assign that responsibility to any third party.

The following is a summary of the inputs used to value the Fund’s investments as of August 31, 2023:

| Valuation Inputs | ||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| U.S. Government & Agencies | $ | — | $ | 13,790 | $ | — | $ | 13,790 | ||||||||

| Money Market Funds | 14,416 | — | — | 14,416 | ||||||||||||

| Total | $ | 14,416 | $ | 13,790 | $ | — | $ | 28,206 | ||||||||

The Fund did not hold any investments at the end of the reporting period for which significant unobservable inputs (Level 3) were used in determining fair value; therefore,

16

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

no reconciliation of Level 3 securities is included for this reporting period. The Fund did not hold any derivative instruments during the reporting period.

NOTE 5. FEES AND OTHER TRANSACTIONS WITH AFFILIATES AND OTHER SERVICE PROVIDERS

The Adviser, under the terms of the management agreement (the “Agreement”) with the Trust with respect to the Fund, manages the Fund’s investments. As compensation for its management services, the Fund is obligated to pay the Adviser a management fee computed and accrued daily and paid monthly at an annual rate of 0.25% of the Fund’s average daily net assets. For the fiscal year ended August 31, 2023, the Adviser earned management fees of $62 from the Fund before the waiver and reimbursement described below.

The Adviser has contractually agreed to limit the Fund’s total annual operating expenses to 1.00% of the Fund’s average daily net assets through December 31, 2027 (excluding portfolio transaction and other investment-related costs (including brokerage fees and commissions); taxes; borrowing costs (such as interest and dividend expenses on securities sold short); acquired fund fees and expenses; fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example option and swap fees and expenses); any administrative and/or shareholder servicing fees payable pursuant to a plan adopted by the Board; expenses incurred in connection with any merger or reorganization; extraordinary expenses (such as litigation expenses, indemnification of Trust officers and Trustees and contractual indemnification of Fund service providers); and other expenses that the Trustees agree have not been incurred in the ordinary course of the Fund’s business). This expense cap may not be terminated prior to this date except by the Board upon 60 days’ written notice to the Adviser.

Each expense payment by the Adviser (but not management fee waiver) is subject to recoupment by the Adviser from the Fund in the three years following the date the particular expense payment occurred, but only if such recoupment can be achieved without exceeding the annual expense limitation in effect at the time of the expense payment and any expense limitation in effect at the time of the recoupment. As of August 31, 2023, the Adviser may seek repayment of expense reimbursements in amounts as follows:

| Recoverable Through | ||||

| August 31, 2024 | $ | 155,999 | ||

| August 31, 2025 | 155,959 | |||

| August 31, 2026 | 156,166 | |||

17

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting and transfer agent services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services.

The Administrator has agreed to waive fees to the extent necessary that the Fund’s total annual operating expenses (excluding taxes, borrowing costs such as interest and dividend expenses on securities sold short, brokerage commissions, acquired fund fees and expenses, shareholder servicing fees paid to financial intermediaries, extraordinary expenses and expenses outside the normal course of business) do not exceed $156,000 annually, based on a twelve-month period commencing April 1 and ending March 31 (the “Annual Period”). The waiver will accrue on a monthly basis such that the Fund’s operating expenses for any month during the Annual Period will not exceed the sum of $13,000 (the “Monthly Expense Cap”), provided that Ultimus may recoup any fees waived by Ultimus in a prior month during the Annual Period to the extent of any unused amount of the Monthly Expense Cap in the current month. The waiver will be suspended and forfeited in any month that the Adviser is not the sole shareholder of the Fund. During the fiscal year ended August 31, 2023, the total amount waived by the Administrator was $6,701.

Northern Lights Compliance Services, LLC (“NLCS”), an affiliate of Ultimus, provides a Chief Compliance Officer to the Trust, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Trust. Under the terms of such agreement, NLCS receives fees from the Fund, which are approved annually by the Board.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

Certain officers of the Trust are also employees of Ultimus and such persons are not paid by the Fund for serving in such capacities. One Trustee is a former employee of Ultimus who is not currently paid by the Fund for serving in such capacity.

The Board supervises the business activities of the Trust. Each Trustee serves as a trustee until termination of the Trust unless the Trustee dies, resigns, retires, or is removed. The Chair of the Board and more than 75% of the Trustees are “Independent Trustees,” which means that they are not “interested persons” as defined in the 1940 Act. The Independent Trustees review and establish compensation at least annually. Each Independent Trustee of the Trust receives annual compensation, which is an established amount paid quarterly per fund in the Trust at the time of the regular quarterly Board meetings. The Chair of the Board receives the highest compensation, commensurate with his additional duties

18

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

and each Chair of a committee receives additional compensation as well. Independent Trustees also receive additional fees for attending any special meetings. In addition, the Trust reimburses Independent Trustees for out-of-pocket expenses incurred in conjunction with attendance at meetings.

NOTE 6. INVESTMENT TRANSACTIONS

For the fiscal year ended August 31, 2023, there were no purchases or sales of investment securities, other than short-term investments.

There were no purchases or sales of long-term U.S. government obligations during the fiscal year ended August 31, 2023.

NOTE 7. BENEFICIAL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a)(9) of the 1940 Act. As of August 31, 2023, the Adviser owned 100% of the Fund’s outstanding shares. As a result, the Adviser may be deemed to control the Fund.

NOTE 8. FEDERAL TAX INFORMATION

At August 31, 2023, the net unrealized appreciation (depreciation) and tax cost of investments for tax purposes was as follows:

| Gross unrealized appreciation | $ | — | ||

| Gross unrealized depreciation | (44 | ) | ||

| Net unrealized depreciation on investments | $ | (44 | ) | |

| Tax cost of investments | $ | 28,250 |

At August 31, 2023, the components of accumulated earnings (deficit) on a tax basis were as follows:

| Undistributed Ordinary Income | $ | 791 | ||

| Unrealized depreciation on investments | (44 | ) | ||

| Total accumulated earnings | $ | 747 |

For tax purposes no distributions were paid by the Fund for the fiscal years 2022 and 2023.

Certain capital losses and specified gains realized after October 31, and net investment losses realized after December 31 of the Fund’s fiscal year may be deferred and treated as occurring on the first business day of the Fund’s following taxable year. For the tax year

19

Tactical

Multi-Purpose Fund

Notes to the Financial Statements (continued)

August 31, 2023

ended August 31, 2023, the Fund deferred qualified late year ordinary losses in the amount of $0.

NOTE 9. COMMITMENTS AND CONTINGENCIES

The Trust indemnifies its officers and Trustees for certain liabilities that may arise from their performance of their duties to the Trust or the Fund. Additionally, in the normal course of business, the Trust enters into contracts that contain a variety of representations and warranties which provide general indemnifications. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred.

NOTE 10. SUBSEQUENT EVENTS

Management of the Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date at which these financial statements were issued. Based upon this evaluation, management has determined there were no items requiring adjustment of the financial statements or additional disclosure.

20

Report of Independent Registered Public Accounting Firm

To

the Shareholders of Tactical Multi-Purpose Fund and

Board of Trustees of Unified Series Trust

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Tactical Multi-Purpose Fund (the “Fund”), a series of Unified Series Trust, as of August 31, 2023, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the related notes, and the financial highlights for each of the five years in the period then ended (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of August 31, 2023, the results of its operations for the year then ended, the changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of August 31, 2023, by correspondence with the custodian. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more investment companies advised by Fisher Asset Management, LLC since 2017.

COHEN & COMPANY, LTD.

Chicago, Illinois

October 27, 2023

21

Liquidity Risk Management Program (Unaudited)

The Trust has adopted and implemented a written liquidity risk management program (the “Program”) as required by Rule 22e-4 (the “Liquidity Rule”) under the 1940 Act. The Program is reasonably designed to assess and manage the Fund’s liquidity risk, taking into consideration, among other factors, the Fund’s investment strategy and the liquidity of its portfolio investments during normal and reasonably foreseeable stressed conditions; its short and long-term cash flow projections; and its cash holdings and access to other funding sources. The Board approved the appointment of the Liquidity Administrator Committee, comprising certain Trust officers and employees of the Adviser. The Liquidity Administrator Committee maintains Program oversight and reports to the Board on at least an annual basis regarding the Program’s operational effectiveness through a written report (the “Report”). The Program’s most recent Report, which was presented to the Board for consideration at its meeting held on August 14-15, 2023, outlined the operation of the Program and the adequacy and effectiveness of the Program’s implementation. During the review period, the Fund did not experience unusual stress or disruption to their operations related to purchase and redemption activity. Also, during the review period the Fund held adequate levels of cash and highly liquid investments to meet shareholder redemption activities in accordance with applicable requirements. The Report concluded that the Program is reasonably designed to prevent violation of the Liquidity Rule and has been effectively implemented.

22

Summary of Fund Expenses (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction and (2) ongoing costs, including management fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other funds. You may pay brokerage commissions on purchases and sales of exchange-traded fund shares, which are not reflected in the example. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from March 1, 2023 through August 31, 2023.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if transaction costs were included, your costs would have been higher.

| Beginning Account Value March 1, 2023 | Ending Account Value August 31, 2023 | Expenses Paid During Period(a) | Annualized Expense Ratio | ||||||||||||

| Actual | $ | 1,000.00 | $ | 1,021.20 | $ | 5.10 | 1.00% | ||||||||

| Hypothetical(b) | $ | 1,000.00 | $ | 1,020.15 | $ | 5.10 | 1.00% | ||||||||

| (a) | Expenses are equal to the Fund’s annualized expense ratios, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| (b) | Hypothetical assumes 5% annual return before expenses. |

23

Trustees and Officers (Unaudited)

GENERAL QUALIFICATIONS. The Board supervises the business activities of the Trust. Each Trustee serves as a trustee until termination of the Trust unless the Trustee dies, resigns, retires, or is removed. The Chair of the Board and more than 75% of the Trustees are “Independent Trustees”, which means that they are not “interested persons” (as defined in the 1940 Act) of the Trust or any adviser, sub-adviser or distributor of the Trust.

The following table provides information regarding the Independent Trustees.

| Name,

Address*, (Year of Birth), Position with Trust**, Term of Position with Trust |

Principal

Occupation During Past 5 Years and Other Directorships |

| Daniel

J. Condon (1950) Chair, May 2022 to present; Chair of the Audit Committee; Chair of the Governance & Nominating Committee, May 2020 to May 2022; Independent Trustee, December 2002 to present |

Current:

Retired (2017 – present). Previous: Peak Income Plus Fund (May 2022 – February 2023). |

| Kenneth

G.Y. Grant (1949) Chair of the Governance & Nominating Committee, May 2022 to present; Chair, January 2017 to May 2022; Independent Trustee, May 2008 to present |

Current:

Director, Standpoint Multi-Asset (Cayman) Fund, Ltd. (2019 – present); Director, Advisors Charitable Gift Fund (2020 –

present), a Donor Advised Fund; Trustee. Trustee, Peak Income Plus Fund (May 2022 – present). Previous: EVP, Benefit Plans Administrative Services, Inc., provider of retirement benefit plans administration (2019 – 2020); Director, Northeast Retirement Services (NRS) LLC, a transfer agent and fund administrator; and Director, Global Trust Company (GTC), a non-depository trust company sponsoring private investment products (2003 – 2019); EVP, NRS (2003 – 2019); GTC, EVP (2008 – 2019); EVP, Savings Banks Retirement Association (2003 – 2019), provider of qualified retirement benefit plans. |

| Ronald

C. Tritschler (1952) Chair of the Audit Committee, May 2022 to present; Independent Trustee, January 2007 to present; Interested Trustee, December 2002 to December 2006 |

Current:

Chief Executive Officer, Director and Legal Counsel of The Webb Companies, a national real estate company, (2001– present);

Director, Standpoint Multi- Asset (Cayman) Fund, Ltd. (2020 – present); Director of First State Bank of the Southeast (2000

– present). Previous: Trustee, Peak Income Plus Fund (May 2022 – February 2023). |

| Catharine

B. McGauley (1977) Chair of the Pricing & Liquidity Committee, November 2022 to present; Independent Trustee, September 2022 to present |

Current:

Lead Portfolio Manager of Atlantic Charter Insurance, a workers’ compensation insurer, (2010 – present); Investment

Advisor for a Family Office (2015 – present); Senior Analyst/Advisor for a Boston real estate company and related family (2010

– present). Previous: Trustee, Peak Income Plus Fund (May 2022 – February 2023). |

| Freddie

Jacobs, Jr. (1970) Independent Trustee, September 2022 to present |

Current:

Chief Operating Officer and Chief Risk Officer Northeast Retirement Services LLC (NRS), and its subsidiary, Global Trust Company

(GTC). NRS is a transfer agent and fund administrator, GTC is a non- depository trust company sponsoring private investment products

(2021 – present); Chair, Board of Crispus Attucks Fund (2020 – present); Board Member of Camp Harbor View (2020 –

present); Director, Sportsmen’s Tennis and Education Center (2019 – present). Previous: SVP, Senior Risk Officer NRS (2013 – 2021); Trustee, Peak Income Plus Fund (May 2022 – February 2023); Trustee of Buckingham Browne & Nichols (2017 - June 2023). |

| * | The address for each Trustee is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. |

| ** | As of the date of this report, the Trust consists of 29 series. |

24

Trustees and Officers (Unaudited) (continued)

The following table provides information regarding the Interested Trustees and Officers of the Trust.

| Name,

Address*, (Year of Birth), Position with Trust, Term of Position with Trust |

Principal

Occupation During Past 5 Years and Other Directorships |

| David

R. Carson (1958) Interested Trustee, August 2020 to present; President, January 2016 to August 2021 |

Current:

Retired (2023 – present); Interested Trustee, Mammoth Institutional Credit Access Fund and Mammoth Institutional Equity

Access Fund (November 2022 – present); Interested Trustee, Peak Income Plus Fund (May 2022 – present). Previous: Interested Trustee of Ultimus Managers Trust, (January 2021 – April 2023); Senior Vice President Client Strategies of Ultimus Fund Solutions, LLC, (2013 – April 2023). |

| Martin

R. Dean (1963) President, August 2021 to present; Vice President, November 2020 to August 2021; Chief Compliance Officer, April 2021 to August 2021; Assistant Chief Compliance Officer, January 2016 to April 2021 |

Current:

President, Northern Lights Compliance Services (2023 – present). Previous: Senior Vice President, Head of Fund Compliance of Ultimus Fund Solutions, LLC (2016 – January 2023). |

| Zachary

P. Richmond (1980) Treasurer and Chief Financial Officer, November 2014 to present |

Current: Vice President, Director of Financial Administration for Ultimus Fund Solutions, LLC, (2015 – present). |

| Gweneth

K. Gosselink (1955) Chief Compliance Officer, August 2021 to present |

Current:

Assistant Vice President, Senior Compliance Officer of Ultimus Fund Solutions, LLC, since 2019. Previous: Chief Operating Officer & CCO at Miles Capital, Inc. (2013 – 2019). |

| Elisabeth

Dahl (1962) Secretary, May 2017 to present; Assistant Secretary, March 2016 to May 2017 |

Current: Attorney, Ultimus Fund Solutions, LLC since March 2016. |

| Timothy

J. Shaloo (1970) AML Compliance Officer, August 2023 to present |

Current:

AVP, Compliance Officer (September 2023 – present). Previous: Senior Compliance Analyst, Northern Lights Compliance Services, LLC (2021 – August 2023); Compliance Specialist, Ultimus Fund Solutions, LLC (2016 – 2020). |

| * | The address for each Officer is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. |

Other Information (Unaudited)

The Fund’s Statement of Additional Information (“SAI”) includes additional information about the trustees and is available without charge, upon request. You may call toll-free at (800) 550-1071 to request a copy of the SAI or to make shareholder inquiries.

25

PRIVACY NOTICE

Rev: January 2020

| FACTS | WHAT DOES TACTICAL MULTI-PURPOSE FUND (THE “FUND”) DO WITH YOUR PERSONAL INFORMATION? |

| Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. |

| What? | The types of personal information we collect and share depend on the product or service you have with us. This information can include:

■ Social Security number

■ account balances and account transactions

■ transaction or loss history and purchase history

When you are no longer our customer, we continue to share your information as described in this notice. |

| How? | All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons the Fund chooses to share; and whether you can limit this sharing. |

| Reasons we can share your personal information | Does

the Fund share? |

Can

you limit this sharing? |

| For

our everyday business purposes— such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus |

Yes | No |

| For

our marketing purposes— to offer our products and services to you |

No | We

don’t share |

| For joint marketing with other financial companies | No | We

don’t share |

| For

our affiliates’ everyday business purposes— information about your transactions and experiences |

No | We

don’t share |

| For

our affiliates’ everyday business purposes— information about your creditworthiness |

No | We

don’t share |

| For nonaffiliates to market to you | No | We

don’t share |

| Questions? | Call (800) 550-1071 |

26

| Who we are | |

| Who is providing this notice? | Tactical Multi-Purpose Fund

Ultimus Fund Distributors, LLC (Distributor)

Ultimus Fund Solutions, LLC (Administrator) |

| What we do | |

| How

does the Fund protect my personal information? |

To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings. Our service providers are held accountable for adhering to strict policies and procedures to prevent any misuse of your nonpublic personal information. |

| How

does the Fund collect my personal information? |

We collect your personal information, for example, when you

■ open an account or deposit money

■ make deposits or withdrawals from your account or provide account information

We also collect your personal information from other companies. |

| Why can’t I limit all sharing? | Federal law gives you the right to limit only

■ sharing for affiliates’ everyday business purposes — information about your creditworthiness

■ affiliates from using your information to market to you

■ sharing for nonaffiliates to market to you

State laws and individual companies may give you additional rights to limit sharing. |

| Definitions | |

| Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies.

■ Fisher Asset Management, LLC, d/b/a Fisher Investments, the investment adviser to the Fund, could be deemed to be an affiliate. |

| Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies.

■ The Fund does not share your personal information with nonaffiliates so they can market to you |

| Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you.

■ The Fund does not jointly market. |

27

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities and information regarding how the Fund voted those proxies during the most recent twelve month period ended June 30, are available (1) without charge upon request by calling the Fund at (800) 550-1071 and (2) in Fund documents filed with the SEC on the SEC’s website at www.sec.gov.

| TRUSTEES | INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

| Daniel J. Condon, Chair | Cohen & Company, Ltd. |

| David R. Carson | 151 North Franklin Street, Suite 575 |

| Kenneth G.Y. Grant | Chicago, IL 60606 |

| Freddie Jacobs, Jr. | |

| Catharine B. McGauley | |

| Ronald C. Tritschler | |

| OFFICERS | LEGAL COUNSEL |

| Martin R. Dean, President | Thompson Hine LLP |

| Gweneth K. Gosselink, Chief Compliance Officer | 312 Walnut Street, 20th Floor |

| Zachary P. Richmond, Treasurer and Chief Financial Officer | Cincinnati, OH 45202 |

| INVESTMENT ADVISER | CUSTODIAN |

| Fisher Asset Management, LLC | U.S. Bank, N.A. |

| 6500 International Parkway, Suite 2050 | 425 Walnut Street |

| Plano, TX 75093 | Cincinnati, OH 45202 |

| DISTRIBUTOR | ADMINISTRATOR, TRANSFER AGENT AND FUND ACCOUNTANT |

| Ultimus Fund Distributors, LLC | Ultimus Fund Solutions, LLC |

| 225 Pictoria Drive, Suite 450 | 225 Pictoria Drive, Suite 450 |

| Cincinnati, OH 45246 | Cincinnati, OH 45246 |

This report is intended only for the information of shareholders or those who have received the Fund’s prospectus which contains information about the Fund’s management fee and expenses. Please read the prospectus carefully before investing.

Distributed by Ultimus Fund Distributors, LLC

Member FINRA/SIPC

FISHER INVESTMENTS INSTITUTIONAL GROUP FUND FAMILY |

Annual Report

August 31, 2023

Fisher Investments Institutional Group

Stock Fund for Retirement Plans

Fisher Investments Institutional Group

ESG Stock Fund for Retirement Plans

Fisher Investments Institutional Group

Fixed Income Fund for Retirement Plans

Fisher Investments Institutional Group

ESG Fixed Income Fund for Retirement Plans

Fund Adviser:

Fisher Asset Management, LLC

6500 International Parkway, Suite 2050

Plano, Texas 75093

(800) 851-8845

Management Discussion of Fund Performance – (Unaudited)

Dear Shareholder:

Market Outlook

Developed world equities finished solidly positive in both Q2 and 2023’s first half. The main force behind the positive year-to-date return, in our view, is that reality exceeded expectations. We think equities are likely to end the year higher as that force is expected to continue.

Elevated inflation has dominated headlines over the past year, and the UK has been among the developed world’s hardest hit. Though the headline consumer price index (including owner occupiers’ housing costs, or CPI-H) sped up from 7.8% y/y to 7.9% in May, most worry centered on the reacceleration in core CPI-H (which excludes energy, food, alcohol and tobacco prices) to 6.5% y/y, its fastest rate in over 30 years. Separately, UK wage growth jumped 7.2% y/y in the three months through April. These developments spurred conversation that the Bank of England (BoE) has yet to tamp down inflation—and will need to keep hiking rates to do so, which many fear is a headwind for equities.

However, in our view, May’s core CPI acceleration appears tied largely to one-time developments, specifically, a big acceleration in recreation and culture prices related to some live music events and the release of a popular video game. These are one-off events, not permanent changes. We also think the theory that wages drive inflation is a misperception. Rather, the former trails the latter since employers typically factor in living costs when setting wages, making them a late-lagging price that responds to inflationary conditions. Data supports this notion lately in other major economies, including the US and Japan—and in our view, it isn’t any different in the UK.

UK equities have lagged the benchmark in Q2 and for the year, but in our view, their relative struggles appear tied to sentiment more than fundamentals. Several fears, from stubbornly high inflation to recession worries, have taken turns weighing on sentiment. However, we don’t think reality is as poor as perceived. Producer prices are close to a zero percent inflation rate, and broad money supply has contracted in five of the past seven months. These developments suggest inflation should broadly keep easing, regardless of whether the BoE hikes or not, and 13 straight BoE hikes haven’t halted GDP growth. That so many remain dour towards British equities despite this resilience is bullish, in our view.

In continental Europe, more recent data suggest the eurozone’s economic backdrop is mixed. The eurozone composite Purchasing Managers’ Index, which aggregates services and manufacturing, fell to 49.9 in late Q2—right below the level dividing expansion and contraction. However, by sector, services showed growth (52.0) while manufacturing stayed in contraction (43.4). This split has persisted throughout the year, and while heavy industry’s weakness weighs on growth, services comprise the majority of output in the eurozone—so the latter’s prospects have more sway on the region’s economy. Regarding prices, though June headline inflation slowed to 5.5% y/y from 6.1%, core CPI picked up

1

Management Discussion of Fund Performance – (Unaudited)

(continued)

from 5.3% to 5.4% y/y, which was tied partly to a low base effect from a price assistance measure last year (e.g., German transport ticket discounts). However, the pickup in core inflation is consistent with the UK’s minor reacceleration, a reminder that inflation trends are global, and one month’s uptick doesn’t negate broader disinflationary trends.

Germany is another place where reality is not as poor as feared, in our view. Since late 2021, economists have been predicting a German recession, and that oft-forecast downturn appeared to manifest in revised GDP data. Q1 GDP was revised down from flat to -0.3% q/q. Following Q4 2022’s -0.5% q/q dip, the two straight quarterly dips meet one popular definition of recession. Some argue German equities outperformance since last September has been disconnected from fundamentals—and now they point to technical recession and other alleged headwinds (e.g., ongoing ECB rate hikes) to claim the outlook is negative. These worries are likely why German equities have lagged throughout Q2.

In our view, forward-looking equities have moved on from these developments, as recession discussion didn’t prevent Italy, Spain, France and even Germany from outperforming in late Q2. Now, it is always possible developments weigh on returns in the near term. For example, Dutch equities have been a top performer year to date but matched the benchmark in June. The cool down comes as Holland’s Information Technology sector only rose slightly, trailing the MSCI’s Information Technology sector in June, which we believe looks tied to minor political uncertainty. The Dutch government detailed export restrictions on machines that make advanced semiconductor processor chips, impacting Dutch semiconductor firm ASML—which comprises nearly all of the Netherlands’ Information Technology sector by market capitalization. We don’t think this restriction significantly disrupts ASML—the company said it did not expect restrictions to have a material impact on its financial outlook—but the news likely weighed on sentiment.

In Asia, sentiment toward Japanese markets still seems relatively optimistic—especially compared to Western Europe. Many high-profile investors have talked up Japanese markets’ prospects recently, pointing to Japanese firms’ cheap valuations and Q1 GDP improvement (1.9% annualized growth) as reasons to be bullish. But valuations aren’t predictive. Despite arguably being attractive for most of the last decade, Japan’s 12-month forward price-to-earnings (P/E) ratio was continuously lower than the broader index from 2014 – 2019.

Investors also point to Japan’s economic recovery, as growth looks stronger relative to other developed markets. For example, May retail sales rose 1.3% m/m, beating expectations, and have risen five of the past six months. In contrast, eurozone retail sales were flat on a monthly basis in May (latest data available). However, Japan’s recent growth is largely tied to its reopening-related boost and tourism recovery. In our view, that likely tapers off and the country will return to its pre-pandemic growth rates.

2

Management Discussion of Fund Performance – (Unaudited)

(continued)

In Japanese politics, Prime Minister Fumio Kishida announced he won’t dissolve the National Diet nor call a snap election. Some observers thought PM Kishida may seek to take advantage of recent optimism by calling for an early election, with the goal of solidifying his power within the ruling Liberal Democratic Party (LDP). But some issues arose, including snags with the national ID card rollout and controversy surrounding a party hosted by PM Kishida’s son at the official residence. Those stories dented his popularity recently, so PM Kishida appears to be holding off from calling a snap vote—and for now, that reduces some political uncertainty. In our view, Japan remains a mixed bag, but sentiment still seems a bit more optimistic than warranted given ongoing headwinds on domestic demand, arguing for a selective approach.

Gridlock looks prevalent throughout the developed world, particularly in Europe—an underappreciated positive for equities, since it decreases the likelihood of major, uncertainty-inducing legislative changes. Another underappreciated eurozone development: cooling inflation. Eurozone inflation hit 6.1% y/y in May, down from April’s 7.0%, as prices continued to slow from October 2022’s 10.6% rate. Though eurozone inflation remains well above its pre-pandemic rate, the price pressures plaguing businesses and households over the past 12 months continue to ease. That said, over the longer term, broader economic and political conditions swamp country-specific issues—and in the eurozone’s case, even mild growth is likely to exceed low expectations, a bullish force for eurozone equities.

Several developed world central banks hiked rates in Q2. Some met expectations, including the 25 basis-point hikes from Sweden’s Riksbank, the ECB and the Swiss National Bank. Others, however, surprised. Norway’s Norges Bank and the BoE hiked by more than anticipated (50 bps instead of 25 bps). The Reserve Bank of Australia and Bank of Canada resumed rate increases after a pause, which caught observers off guard—the former hiked in May and June (25 bps each time) after an April break while the latter had been on hold since January.

For all the attention rate hikes receive, however, they don’t have a preset market impact. Yes, some countries’ markets are down in US dollar terms ever since their central banks began hiking, including Norway, Canada and Australia. Yet other markets are positive: See the eurozone, Switzerland, the UK and Sweden. In our view, this mixed bag illustrates that rate hikes aren’t automatically bad for equities. Monetary policy is just one factor, among many, that markets consider—worth keeping in mind given all the attention on monetary policy globally.

3

Management Discussion of Fund Performance – (Unaudited)

(continued)

Fisher Investments Institutional Group Stock Fund for Retirement Plans Performance Attribution