Form N-CSR Nuveen Corporate Income For: Dec 31

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number |

811-23075 |

Nuveen Corporate Income November 2021 Target Term Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Mark L. Winget

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: December 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Closed-End Funds

31 December

2020

Nuveen Closed-End Funds

| JHB | Nuveen Corporate Income November 2021 Target Term Fund | |

| JHAA | Nuveen Corporate Income 2023 Target Term Fund |

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will not be sent to you by mail unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares or, if you are a direct investor, by enrolling at www.nuveen.com/e-reports.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary or, if you are a direct investor, by calling 800-257-8787 and selecting option #2 or (ii) by logging into your Investor Center account at www.computershare.com/investor and clicking on “Communication Preferences”. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary or, if you are a direct investor, to all your directly held Nuveen Funds and any other directly held funds within the same group of related investment companies.

Annual Report

Life is Complex

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready—no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your email!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

| 4 | ||||

| 5 | ||||

| 12 | ||||

| 14 | ||||

| 16 | ||||

| 20 | ||||

| 21 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| 38 | ||||

| 40 | ||||

| 50 | ||||

| 71 | ||||

| 72 | ||||

| 73 | ||||

3

Chair’s Letter to Shareholders

4

Nuveen Corporate Income November 2021 Target Term Fund (JHB)

Nuveen Corporate Income 2023 Target Term Fund (JHAA)

Nuveen Corporate Income November 2021 Target Term Fund (JHB) and Nuveen Corporate Income 2023 Target Term Fund (JHAA) are closed-end funds that feature portfolio management by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisors, LLC, the Funds’ investment adviser. The Funds’ portfolio managers are Kevin Lorenz, CFA, Jacob J. Fitzpatrick, CFA, and Christopher Williams.

Fund Name and Investment Policy Changes

Effective August 24, 2020, Nuveen Corporate Income November 2021 Target Term Fund changed from Nuveen High Income November 2021 Target Term Fund, and Nuveen Corporate Income 2023 Target Term Fund changed from Nuveen High Income 2023 Target Term Fund. Each Fund’s investment policy to invest at least 80% of its managed assets in securities that, at the time of investment, are rated below investment grade or are unrated but judged by the portfolio managers to be of comparable quality was also eliminated.

Here the Funds’ portfolio management team reviews U.S. economic and market conditions, key investment strategies and the performance of the Funds for the twelve-month reporting period ended December 31, 2020.

What factors affected the U.S. economy and financial markets during the twelve-month reporting period ended December 31, 2020?

The U.S. economy rebounded more quickly than expected from the deep downturn caused by the COVID-19 crisis and containment measures, but it was not fully recovered by the year’s end. U.S. gross domestic product (GDP) grew 4.0% on an annualized basis in the fourth quarter of 2020 and 33.1% (annualized) in the third quarter, but remained down 3.5% in 2020 overall (from the 2019 annual level to the 2020 annual level) as measured by the Bureau of Economic Analysis “advance” estimate. GDP measures the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. The economy fell into a deep recession in February 2020 due to the restrictions on business and social activity to mitigate the COVID-19 spread. In the first and second quarters of 2020, annualized GDP shrank 5% and 31.4%, respectively. Government relief programs provided significant aid to individuals and businesses as the economy began reopening in May 2020, which helped the economy bounce back strongly over the second half of the year.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

5

Portfolio Managers’ Comments (continued)

Consumer spending, the largest driver of the economy, remained resilient despite the disruption caused by the health and economic crisis. Consumer spending declined significantly and unemployment rose sharply starting in March 2020. These measures rebounded markedly in the second half of the year, although the momentum slowed toward year end amid a resurgence of coronavirus infections. The Bureau of Labor Statistics said the unemployment rate rose to 6.7% in December 2020 from 3.6% in December 2019. As of December 2020, slightly more than half of the 22 million jobs lost in March and April 2020 have been recovered. The average hourly earnings rate appeared to increase, growing at an annualized rate of 5.1% in December 2020, despite the spike in unemployment. Earnings data was skewed by the concentration of job losses in lower-wage work, which effectively eliminated most of the low-wage data, resulting in an average of mostly higher numbers. The overall trend of inflation remained muted, as decreases in gasoline, apparel and transportation prices offset an increase in food prices. The Bureau of Labor Statistics said the Consumer Price Index (CPI) increased 1.4% over the twelve-month reporting period ended December 31, 2020 before seasonal adjustment.

Prior to the COVID-19 crisis recession, the U.S. Federal Reserve (the Fed) had reduced its benchmark interest rate to support the economy’s slowing growth. The Fed also stopped shrinking its bond portfolio sooner than scheduled and began buying short-term Treasury bills to help money markets operate smoothly and maintain short-term borrowing rates at low levels. As the health and economic crisis deepened, the Fed enacted an array of emergency measures in March 2020 to stabilize the financial system and support the markets, including cutting its main interest rate to near zero, offering lending programs to aid small and large companies and allowing unlimited bond purchases, known as quantitative easing. In August 2020, the Fed announced a change in inflation policy to average inflation targeting. Under this regime, the Fed will tolerate the inflation rate temporarily overshooting the target rate to offset periods of below-target inflation, so that inflation averages a 2% rate over time. Fed officials remained cautious, acknowledging the economy’s improvement but concerned about near-term weakness, and left policy unchanged over the remainder of their meetings in 2020.

In March and April 2020, the U.S. government approved three aid packages. These included $2 trillion allocated across direct payments to Americans, an expansion of unemployment insurance, loans to large and small businesses, funding to hospitals and health agencies and support to state and local governments, and more than $100 billion in funding to health agencies and employers offering paid leave. In December 2020, the government enacted a $900 billion relief package extending some of these programs. With Joe Biden winning the U.S. presidential election in November 2020, more fiscal stimulus is anticipated in 2021.

The COVID-19 crisis rapidly dwarfed all other market concerns starting in late February 2020. Equity and commodity markets sold off and safe-haven assets rallied in March 2020 as China, other countries and then the United States initiated quarantines, restricted travel and shuttered factories and businesses. The potential economic shock was particularly difficult to assess, which amplified market volatility. An ill-timed oil price war between the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC member Russia, which caused oil prices to plunge in March 2020, exacerbated the market sell-off. At year end, the announcement of high efficacy rates in several COVID-19 vaccine trials, followed by regulatory authorizations and public vaccination drives across Western countries, improved the outlook for 2021 and led to risk-on sentiment in the markets.

Geopolitical uncertainty remained elevated during 2020 in anticipation of the U.S. presidential election in November 2020 and the Brexit transition period set to expire in December 2020. Political risks eased somewhat toward the end of the reporting period, as markets ultimately viewed a Biden administration positively and the European Union (EU) and United Kingdom (U.K.) finalized a trade deal in the final days of the transition period. Although China and the U.S. signed a “phase one” trade deal in January 2020, tensions continued to flare over other trade and technology/security issues, Hong Kong’s sovereignty and the management of the COVID-19 crisis.

6

Nuveen Corporate Income November 2021 Target Term Fund (JHB)

What key strategies were used to manage the Fund during the twelve-month reporting period ended December 31, 2020?

The Fund seeks to provide a high level of current income and to return the original $9.85 net asset value (NAV) per common share on or about November 1, 2021. The Fund will seek to achieve its investment objectives by investing primarily in shorter maturity, high yield (below investment grade) corporate debt securities. High yield bonds typically offer higher yields than investment grade bonds, in exchange for greater credit risk. Bonds with shorter maturities have lower duration (or interest rate sensitivity) than longer maturity bonds, which may help mitigate price declines if rates rise.

The Fund may invest in other types of securities including senior loans, convertible securities and other types of debt instruments and derivatives that provide comparable economic exposure to the corporate debt market. At least 80% of the Fund’s managed assets will be in corporate debt securities. No more than 15% will be in securities rated CCC+/Caa1 or lower at the time of investment. Up to 30% may be in securities of non-U.S. issuers, including up to 20% in emerging market issuers and up to 10% may be in non- U.S. dollar denominated securities.

The Fund seeks to identify securities across diverse sectors and industries that the portfolio managers believe are undervalued or mispriced. In seeking to return the original NAV on or about November 1, 2021, the Fund intends to utilize various portfolio and cash flow management techniques, including setting aside a portion of its net investment income, possibly retaining gains and limiting the longest maturity of any holding to no later than May 1, 2022. The Fund also uses leverage.

Recent market conditions have materially increased the risk associated with achieving the Fund’s objective to return original NAV. This objective is not a guarantee and is dependent on a number of factors including the extent of market recovery and the cumulative level of income retained in relation to cumulative portfolio gains net of losses.

How did the Fund perform during the twelve-month reporting period ended December 31, 2020?

The table in the Performance Overview and Holding Summaries section of this report provides total returns at net asset value (NAV) for the period ended December 31, 2020. The Fund’s total returns on NAV are compared with the performance of a corresponding market index.

For the twelve-month reporting period ended December 31, 2020, the Fund underperformed the Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index (Bloomberg Barclays U.S. High Yield 1-5 Year Index).

The high yield market started 2020 supported by dovish central banks and stable credit fundamentals, while capital from around the globe continued to flow into the asset class in the hunt for yield. However, the full-scale global pandemic led to a near complete shutdown of the capital markets in March 2020, which was exacerbated by the sharp drop in crude oil prices. Together these forces drove a spike in risk premiums and high yield outflows, with the spread of the Bloomberg Barclays U.S. High Yield 1-5 Year Index peaking at 1,387 basis points over Treasuries at the reporting period’s widest point in March 2020. However, the immediate response by policymakers to support healthy market and economic functioning helped stabilize the high yield market. Investors took courage from these steps resulting in sizable inflows back into the high yield market over the remainder of the reporting period. These inflows were met with the largest net new issuance on record as companies aimed to optimize their capital structure, although approximately two-thirds of 2020’s new issuance was related to refinancings. Over the remainder of the reporting period, the high yield market continued to be supported by accommodative policies, gradual re-openings and falling unemployment, helping default activity to ease substantially from the elevated levels seen earlier in 2020. After the segment’s significant underperformance in March 2020, high yield spreads retraced to 398 basis points over Treasuries by the end of the reporting period and the Bloomberg Barclays U.S. High Yield 1-5 Year Index ended the reporting period with a 4.49% annual return.

7

Portfolio Managers’ Comments (continued)

During the volatile market conditions, the Fund underperformed the benchmark on a total return basis mainly due to its more conservative positioning as it approaches the termination date. Also, because of these conditions, the Fund’s NAV fell quite significantly, hitting its lowest level during the March 2020 sell-off. Over the remainder of the reporting period, the Fund’s NAV recovered much of the reporting period’s earlier losses, ending the reporting period $0.50 per share lower at $9.47 per share.

The Fund’s much shorter duration than its benchmark detracted from relative results because the more pronounced price appreciation in longer duration assets produced a higher total return. Fund holdings are more anchored to par price as their near-term maturity dates approach so they had less room for appreciation versus the benchmark constituents.

Carrying a cash balance, which was in large part due to the heavy refinancing activity in the high yield segment, hindered the Fund’s performance given the strong rally in the high yield market and the pace of refinancings. Companies are refinancing their short-term debt into much longer maturity profiles than the termination date of this Fund allows. This weighed on the Fund’s total return, particularly in the highest quality BB rated issuers, the best performing rating category over the course of the reporting period.

Security selection in the transportation sector detracted from performance. As airlines and transportation service companies burned through cash at an unsustainable rate, the market was generally supportive of extending liquidity to select companies, many times in exchange for added collateral or on other favorable terms. However, foreign airlines received less support than U.S. carriers from local governments and markets, which forced their hand in restructuring or liquidating assets. The Fund had a modest position in Virgin Australia Holdings Ltd., which was among a sizeable group of foreign airlines that filed for bankruptcy during the COVID-19 crisis.

The Fund’s security selection in consumer cyclicals proved beneficial to performance. Over the course of the reporting period, credits in gaming, leisure, quick-service restaurants and autos steadily rallied due to the increasing potential for broad reopening of the economy. Also, companies in the sector took the opportunity to redress their balance sheets to improve their capital structures.

Performance was also aided by the Fund’s underweight and security selection among CCC rated issues, which was the worst performing benchmark ratings category. The Fund had overweights in several issuers including APX Group in the residential security service area, Realogy Group LLC in real estate brokerage, relocation and title services; and GFL Environmental in waste management. These positions all rallied based on improved fundamental outlooks while investors searched for yield, causing CCC valuations to compress later in the reporting period.

Another favorable factor in the Fund’s performance was its significant underweight to the energy sector. During the drop in commodity prices, companies found themselves searching for liquidity and redressing capital structures to withstand the sustained lockdowns. Although energy credits experienced a rally late in the reporting period after OPEC and other oil-producing nations agreed to adjustments to production, it was not enough to make up for the reporting period’s earlier weakness.

To reduce risk as the Fund approaches its 2021 termination, we have increased exposure to higher quality BB credits and reduced CCC rated exposure. In terms of other portfolio changes, we increased communications exposure by redeploying cash from refinancings into companies that still had outstanding debt that fit the Fund’s term and where we were constructive on fundamental outlooks. We believe the sector will continue to benefit from the high demand for connectivity. We also increased exposure to banking and other financials as the COVID-19 vaccine rollouts and further stimulus measures point toward reopening, higher economic growth expectations and continued demand for credit creation. The Fund’s consumer cyclical exposure decreased as bonds in the sector were called by issuers or matured in 2020. At the end of the reporting period, the Fund’s overweights included financial companies (loan servicing, business development companies, specialty lenders), banks and communications. The Fund remained underweight in the energy

8

and in non-cyclicals (health care, food and beverage, consumer products) sectors, given a lack of available bonds or loans that fit its approaching termination parameters.

We continue to position the portfolio in high income producing investments that we expect to make timely interest and principal payments as we attempt to meet the objective of returning the original NAV on the final term date of the Fund. However, the universe of available issues that fit the Fund’s term parameters has been materially reduced as companies have refinanced and extended their maturity walls while the low yield environment still persists. We continue to position in credits whose competitive positions and balance sheets are able to withstand a prolonged disruption in activity, or those that may be beneficiaries of supportive policy. We are decreasing exposures to companies that will likely run into additional challenges making it to the other side of the current health crisis in the event a return to normalcy takes longer than anticipated. We continue to manage calls, maturities and the cash flow profile of the Fund with the target of managing principal preservation and yield in light of the Fund’s termination date.

Nuveen Corporate Income 2023 Target Term Fund (JHAA)

What key strategies were used to manage the Fund during the twelve-month reporting period ended December 31, 2020?

The Fund seeks to provide a high level of current income and to return the original $9.875 net asset value (NAV) per common share on or about December 1, 2023. The Fund invests in a portfolio of primarily corporate debt securities, including bonds and senior loans. The Fund may invest in other types of securities including convertible securities and other types of debt instruments and derivatives that provide comparable economic exposure to the corporate debt market. Under normal circumstances, up to 30% of its managed assets may be in securities of non-U.S. issuers, including up to 20% of managed assets in emerging market issuers, and up to 10% of managed assets may be in non-U.S. dollar denominated securities. No more than 15% will be in securities rated CCC+/Caa1 or lower at the time of investment.

In seeking to return the original NAV on or about December 1, 2023, the Fund intends to utilize various portfolio and cash flow management techniques, including setting aside a portion of its net investment income, possibly retaining gains, and limiting the longest maturity of any holding to no later than June 1, 2024.

The Fund’s objective is not a guarantee and is dependent on a number of factors including the extent of market recovery and the cumulative level of income retained in relation to cumulative portfolio gains net of losses.

How did the Fund perform during the twelve-month reporting period ended December 31, 2020?

The table in the Performance Overview and Holding Summaries section of this report provides total returns at net asset value (NAV) for the period ended December 31, 2020. The Fund’s total returns on NAV are compared with the performance of a corresponding market index.

For the twelve-month reporting period ended December 31, 2020, the Fund underperformed the Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index (Bloomberg Barclays U.S. High Yield 1-5 Year Index).

The high yield market started 2020 supported by dovish central banks and stable credit fundamentals, while capital from around the globe continued to flow into the asset class in the hunt for yield. However, the full-scale global pandemic led to a near complete shutdown of the capital markets in March 2020, which was exacerbated by the sharp drop in crude oil prices. Together these forces drove a spike in risk premiums and high yield outflows, with the spread of the Bloomberg Barclays U.S. High Yield 1-5 Year Index peaking at 1,387 basis points over Treasuries at the reporting period’s widest point in March 2020. However, the immediate response by policymakers to support healthy market and economic functioning helped stabilize the high yield market. Investors took courage from these steps resulting in sizable inflows back into the high yield market over the remainder of the reporting period. These inflows were met with the largest net new issuance on record as companies aimed to optimize their capital structure, although approximately two-thirds of 2020’s new issuance was related to refinancings. Over the remainder of the reporting period, the high

9

Portfolio Managers’ Comments (continued)

yield market continued to be supported by accommodative policies, gradual re-openings and falling unemployment, helping default activity to ease substantially from the elevated levels seen earlier in 2020. After the segment’s significant underperformance in March 2020, high yield spreads retraced to 398 basis points over Treasuries by the end of the reporting period and the Bloomberg Barclays U.S. High Yield 1-5 Year Index ended the reporting period with a 4.49% annual return.

During the volatile market conditions during the reporting period, the Fund underperformed the benchmark on a total return basis. Also because of these conditions, the Fund’s NAV fell quite significantly, hitting its lowest level during the March 2020 sell-off. Over the remainder of the reporting period, the Fund’s NAV recovered much of the reporting period’s earlier losses, ending the reporting period $0.33 per share lower at $10.03 per share.

As it gets closer to termination, the Fund’s shorter duration than its benchmark detracted from relative results because the more pronounced price appreciation in longer duration assets produced a higher total return. Fund holdings are more anchored to par price as their maturity dates approach and issuers are in the market to refinance their outstanding shorter-dated debt maturities at or near par. Therefore, the Fund’s holdings have less room for appreciation versus the benchmark constituents.

Security selection within the consumer non-cyclicals sector detracted, specifically in the health care subsector. The Fund was underweight in some hospital and physician staffing credits that rallied. More broadly, consumer non-cyclicals benefited more from stay-at-home orders than other benchmark sectors.

The Fund was also hindered by an underweight stance in the technology sector. Over the course of the reporting period, technology credits benefited from increased IT spending at the enterprise and consumer level. At the same time, demand for remote connectivity and various methods of communication increased due to social distancing orders.

The Fund’s performance benefited from security selection among CCC rated issues, despite this being the worst performing benchmark ratings category. The Fund had overweights in several issuers including nThrive Inc., a company that offers advisory expertise, services, analytics, and education programs to health care organizations; SM Energy Co, oil and gas exploration and production; and Realogy Group LLC, real estate brokerage, relocation and title services. These positions all rallied based on improved fundamental outlooks while investors searched for yield, causing CCC valuations to compress later in the reporting period.

Another favorable factor in the Fund’s performance was its significant underweight to the energy sector, which was among the worst performing benchmark sectors in 2020. During the drop in commodity prices earlier, companies found themselves searching for liquidity and redressing capital structures to withstand the sustained lockdowns. Although energy credits experienced a rally later in the reporting period after OPEC and other oil-producing nations agreed to adjustments to production, it was not enough to make up for the earlier weakness. The sector is likely to remain volatile until commuter and commercial traffic returns to a more normal level.

Also, the Fund’s security selection in the transportation sector benefited performance. As airlines and transportation service companies burned through unsustainable amounts of cash, the market was supportive of extending liquidity to select companies, many times in exchange for added collateral or on other favorable terms. Hertz Corp, for example, sold vehicles from its fleet and is in the process of modifying its capital structure while the company continues to operate. The first lien debt owned by the Fund benefited from the favorable terms of the modification, which aided outperformance. The unsecured debt, which is not owned by the Fund, underperformed the benchmark as a result of the modification. Delta Air Lines Inc and United Airlines Holding Inc secured debt using mileage/customer loyalty programs, which helped their debt trade well throughout the remainder of the reporting period.

In terms of portfolio changes, the Fund increased its communications exposure by redeploying cash from refinancings into companies that still had outstanding debt that fit the Fund’s term and where we were constructive on fundamental outlooks. We believe the sector will continue to benefit from the high demand for connectivity. We also increased

10

health care exposure in the consumer non-cyclical area as elective procedures began increasing, while reducing consumer cyclicals. Because of attractive relative values in the CCC segment, we increased exposure there while still maintaining the Fund’s underweight in lower rated credits. At the same time, we reduced exposure to BB rated credits due to high valuations or refinancings. At the end of the reporting period, the Fund’s overweights included transportation (secured airline debt, rail, truck and travel services), consumer non-cyclicals and utilities sector exposure. The Fund remained underweight in the energy, consumer cyclicals and real estate investment trusts (REIT) sectors where valuations may be stretched relative to current fundamentals in those sectors.

We continue to position the portfolio in high income producing investments that we expect to make timely interest and principal payments as we attempt to meet the objective of returning the original NAV on the final term date of the Fund. However, the universe of available issues that fit the Fund’s term parameters has been materially reduced as companies have refinanced and extended their maturity walls while the low yield environment still persists. We continue to position in credits whose competitive positions and balance sheets are able to withstand a prolonged disruption in activity, or those that may be beneficiaries of supportive policy. We are decreasing exposures to companies that will likely run into additional challenges making it to the other side of the current health crisis in the event a return to normalcy takes longer than anticipated. We continue to manage calls, maturities and the cash flow profile of the Fund with the target of managing principal preservation and yield in light of the Fund’s termination date in 2023.

11

IMPACT OF THE FUNDS’ LEVERAGE STRATEGIES ON PERFORMANCE

One important factor impacting the returns of the Funds’ common shares relative to their comparative benchmarks was the Funds’ use of leverage through the use of bank borrowings as well as the use of reverse repurchase agreements for JHAA. As of the end of the reporting period, JHB is no longer using bank borrowings and JHAA is no longer using reverse repurchase agreements. The Funds use leverage because our research has shown that, over time, leveraging provides opportunities for additional income. The opportunity arises when short-term rates that the Fund pay on its leveraging instruments are lower than the interest the Fund earns on its portfolio securities that it has bought with the proceeds of that leverage. This has been particularly true in the recent market environment where short-term rates have been low by historical standards.

However, use of leverage can expose Fund common shares to additional price volatility. When a Fund uses leverage, the Fund’s common shares will experience a greater increase in their net asset value if the securities acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the bonds acquired through leverage decline in value. All this will make the shares’ total return performance more variable, over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when short-term interest rates increase and increase when short-term interest rates decrease. In recent quarters, fund leverage expenses have generally tracked the overall movement of short-term tax-exempt interest rates. While fund leverage expenses are somewhat higher than their recent lows, leverage nevertheless continues to provide the opportunity for incremental common share income, particularly over longer-term periods.

JHB’s use of leverage had a negative impact on total return performance during this reporting period. The negative impact of leverage during the brief but severe COVID-19 induced market downturn in March was greater than the positive impact of leverage during the remainder of the reporting period as the Fund continued to lower its leverage ratio driven by the limited options to reinvest shorter dated cash proceeds in securities that paid more than the cost of leverage amid the shrinking investable universe. The Fund fully de-levered subsequent to the reporting period.

JHAA’s use of leverage had a negligible impact on total return performance during this reporting period. The negative impact of leverage during the brief but severe COVID-19 induced market downturn in March was greater than the positive impact of leverage during the remainder of the reporting period. Management believes, however, that the potential benefits from leverage continue to outweigh the associated increase in risk and total return variability previously described.

As of December 31, 2020, the Funds’ percentages of leverage are shown in the accompanying table.

| JHB | JHAA | |||||||

| Effective Leverage* |

0.00 | % | 23.80 | % | ||||

| Regulatory Leverage* |

0.00 | % | 23.80 | % | ||||

| * | Effective Leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of reverse repurchase agreements, certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. A Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

12

THE FUNDS’ REGULATORY LEVERAGE

Bank Borrowings

As noted previously, the Funds employ leverage through the use of bank borrowings. The Funds’ bank borrowing activities are as shown in the accompanying table.

| Current Reporting Period | Subsequent to the Close of the Reporting Period |

|||||||||||||||||||||||||||||||||||

| Fund | Outstanding Balance as of January 1, 2020 |

Draws | Paydowns | Outstanding Balance as of December 31, 2020 |

Average Balance Outstanding |

Draws | Paydowns | Outstanding Balance as of February 25, 2021 |

||||||||||||||||||||||||||||

| JHB |

$ | 192,000,000 | $ | — | $ | (192,000,000 | ) | $ | — | $ | 98,862,245 | * | $ | — | $ | — | $ | — | ||||||||||||||||||

| JHAA |

$ | 27,025,000 | $ | — | $ | (2,500,000 | ) | $ | 24,525,000 | $ | 25,706,694 | $ | — | $ | — | $ | 24,525,000 | |||||||||||||||||||

| * | For the period January 1, 2020 through July 14, 2020. |

Refer to Notes to Financial Statements, Note 8 – Fund Leverage, for further details.

Reverse Repurchase Agreements

As noted previously, JHAA used reverse repurchase agreements, in which the Fund sells to a counterparty a security that it holds with a contemporaneous agreement to repurchase the same security at an agreed-upon price and date. The Fund’s transactions in reverse repurchase agreements are as shown in the accompanying table.

| Current Reporting Period | Subsequent to the Close of the Reporting Period |

|||||||||||||||||||||||||||||||||||

| Fund | Outstanding January 1, 2020 |

Sales | Purchases | Outstanding December 31, 2020 |

Average Balance Outstanding |

Sales | Purchases | Outstanding Balance as of February 25, 2021 |

||||||||||||||||||||||||||||

| JHAA |

$ | 490,000 | $ | — | $ | (490,000 | ) | $ | — | $ | 490,000 | ** | $ | — | $ | — | $ | — | ||||||||||||||||||

| ** | For the period January 1, 2020 through June 19, 2020. |

Refer to Notes to Financial Statements, Note 8 – Fund Leverage, for further details.

13

COMMON SHARE DISTRIBUTION INFORMATION

The following information regarding the Funds’ distributions is current as of December 31, 2020. Each Fund’s distribution levels may vary over time based on each Fund’s investment activity and portfolio investment value changes.

During the current reporting period, the Funds’ distributions to common shareholders were as shown in the accompanying table.

| Monthly Distributions (Ex-Dividend Date) | JHB | JHAA | ||||||

| January 2020 |

$ | 0.0415 | $ | 0.0520 | ||||

| February |

0.0415 | 0.0520 | ||||||

| March |

0.0370 | 0.0480 | ||||||

| April |

0.0370 | 0.0480 | ||||||

| May |

0.0370 | 0.0480 | ||||||

| June |

0.0315 | 0.0430 | ||||||

| July |

0.0315 | 0.0430 | ||||||

| August |

0.0315 | 0.0430 | ||||||

| September |

0.0245 | 0.0430 | ||||||

| October |

0.0245 | 0.0430 | ||||||

| November |

0.0245 | 0.0430 | ||||||

| December 2020 |

0.0205 | 0.0395 | ||||||

| Total Distributions from Net Investment Income |

$ | 0.3825 | $ | 0.5455 | ||||

| Current Distribution Rate* |

2.67 | % | 4.95 | % | ||||

| * | Current distribution rate is based on the Fund’s current annualized monthly distribution divided by the Fund’s current market price. The Fund’s monthly distributions to its shareholders may be comprised of ordinary income, net realized capital gains and, if at the end of the fiscal year the Fund’s cumulative net ordinary income and net realized gains are less than the Fund’s distributions, a return of capital for tax purposes. |

Each Fund seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit each Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. Distributions to common shareholders are determined on a tax basis, which may differ from amounts recorded in the accounting records. In instances where the monthly dividend exceeds the earned net investment income, the Fund would report a negative undistributed net ordinary income. Refer to Note 6 – Income Tax Information for additional information regarding the amounts of undistributed net ordinary income and undistributed net long-term capital gains and the character of the actual distributions paid by the Fund during the period.

All monthly dividends paid by each Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions is sourced or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders will be notified of those sources. For financial reporting purposes, the per share amounts of each Fund’s distributions for the reporting period are presented in this report’s Financial Highlights. For income tax purposes, distribution information for each Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

NUVEEN CLOSED-END FUND DISTRIBUTION AMOUNTS

The Nuveen Closed-End Funds’ monthly and quarterly periodic distributions to shareholders are posted on www.nuveen.com and can be found on Nuveen’s enhanced closed-end fund resource page, which is at https://www.nuveen.com/resource-center-closed-end-funds, along with other Nuveen closed-end fund product

14

updates. To ensure timely access to the latest information, shareholders may use a subscribe function, which can be activated at this web page (https://www.nuveen.com/subscriptions).

COMMON SHARE REPURCHASES

During August 2020, the Funds’ Board of Trustees reauthorized an open-market share repurchase program, allowing each Fund to repurchase an aggregate of up to approximately 10% of its outstanding shares.

As of December 31, 2020, and since the inception of the Funds’ repurchase programs, the Funds have cumulatively repurchased and retired their outstanding common shares as shown in the accompanying table.

| JHB | JHAA | |||||||

| Common shares cumulatively repurchased and retired |

0 | 0 | ||||||

| Common shares authorized for repurchase |

5,590,000 | 780,000 | ||||||

During the current reporting period, the Funds did not repurchase any of their outstanding common shares.

OTHER COMMON SHARE INFORMATION

As of December 31, 2020, and during the current reporting period, the Funds’ common share prices were trading at a premium/(discount) to their common share NAVs as shown in the accompanying table.

| JHB | JHAA | |||||||

| Common share NAV |

$ | 9.47 | $ | 10.03 | ||||

| Common share price |

$ | 9.20 | $ | 9.58 | ||||

| Premium/(Discount) to NAV |

(2.85 | )% | (4.49 | )% | ||||

| 12-month average premium/(discount) to NAV |

(2.62 | )% | 0.30 | % | ||||

JHB and JHAA each have an investment objective to return $9.85 and $9.875, respectively (the original net asset value following each Fund’s initial public offering (the “Original NAV”)) to shareholders on or about the end of the Fund’s term. There can be no assurance that the Funds will be able to return the Original NAV to shareholders, and such return is not backed or otherwise guaranteed by the Funds’ investment adviser, Nuveen Fund Advisors, LLC (the “Adviser”), or any other entity.

In connection with the objective of returning Original NAV, each Fund currently intends to set aside and retain in its net assets a portion of its net investment income and possibly all or a portion of its gains. This will reduce the amounts otherwise available for distribution prior to the liquidation of each Fund, and the Fund may incur taxes on such retained amount, which will reduce the overall amounts that the Fund would have otherwise been able to distribute. Such retained income or gains, net of any taxes, would constitute a portion of the liquidating distribution returned to investors at the end of each Fund’s term. In addition, each Fund’s investment in shorter term and lower yielding securities, especially as the Fund nears the end of its term, may reduce investment income and, therefore, the monthly dividends during the period prior to termination. Investors that purchase shares in the secondary market (particularly if their purchase price differs meaningfully from the Original NAV) may receive more or less than their original investment.

Each Fund’s ability to return Original NAV to common shareholders on or about the termination date will depend on market conditions and the success of various portfolio and cash flow management techniques.

Recent market conditions have materially increased the risk associated with achieving JHB’s objective to return Original NAV. This objective is not a guarantee and is dependent on a number of factors including the extent of market recovery and the cumulative level of income retained in relation to cumulative portfolio gains net of losses. JHAA’s objective is not a guarantee and is dependent on a number of factors including market conditions and the cumulative level of income retained in relation to cumulative portfolio gains net of losses.

15

15

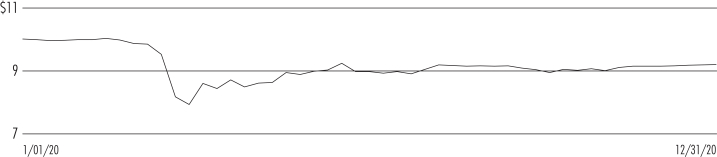

| JHB | Nuveen Corporate Income November 2021 Target Term Fund Performance Overview and Holding Summaries as of December 31, 2020 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of December 31, 2020

| Average Annual | ||||||||

| 1-Year | Since Inception |

|||||||

| JHB at Common Share NAV | (1.07)% | 4.35% | ||||||

| JHB at Common Share Price | (4.17)% | 3.40% | ||||||

| Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index | 4.49% | 5.57% | ||||||

Since inception returns are from 8/23/16. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Common Share Price Performance — Weekly Closing Price

16

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

| 1 | Includes 14.2% (as a percentage of total investments) in emerging markets countries. |

| 2 | See Portfolio of Investments for details on “other” Portfolio Composition. |

17

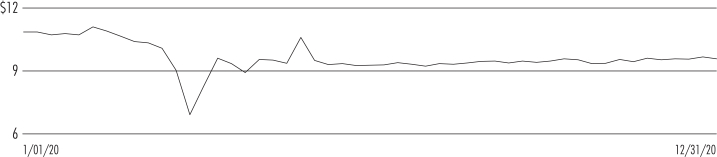

| JHAA | Nuveen Corporate Income 2023 Target Term Fund Performance Overview and Holding Summaries as of December 31, 2020 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of December 31, 2020

| Average Annual | ||||||||

| 1-Year | Since Inception |

|||||||

| JHAA at Common Share NAV | 2.51% | 6.48% | ||||||

| JHAA at Common Share Price | (6.43)% | 3.54% | ||||||

| Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index | 4.49% | 6.31% | ||||||

Since inception returns are from 12/18/18. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Common Share Price Performance — Weekly Closing Price

18

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

| 1 | Includes 9.1% (as a percentage of total investments) in emerging markets countries. |

| 2 | See Portfolio of Investments for details on “other” Portfolio Composition. |

19

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees

Nuveen Corporate Income November 2021 Target Term Fund

Nuveen Corporate Income 2023 Target Term Fund:

Opinion on the Financial Statements

We have audited the accompanying statements of assets and liabilities of Nuveen Corporate Income November 2021 Target Term Fund (formerly known as Nuveen High Income November 2021 Target Term Fund) and Nuveen Corporate Income 2023 Target Term Fund (formerly known as Nuveen High Income 2023 Target Term Fund) (the Funds), including the portfolios of investments, as of December 31, 2020, the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the related notes (collectively, the financial statements) and the financial highlights for each of the years in the four-year period then ended and the period from August 23, 2016 (commencement of operations) to December 31, 2016 for Nuveen Corporate Income November 2021 Target Term Fund, and each of the years in the two-year period then ended and the period from December 18, 2018 (commencement of operations) to December 31, 2018 for Nuveen Corporate Income 2023 Target Term Fund. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Funds as of December 31, 2020, the results of their operations and cash flows for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the four-year period then ended and the period from August 23, 2016 to December 31, 2016 for Nuveen Corporate Income November 2021 Target Term Fund, and each of the years in the two-year period then ended and the period from December 18, 2018 to December 31, 2018 for Nuveen Corporate Income 2023 Target Term Fund, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Such procedures also included confirmation of securities owned as of December 31, 2020, by correspondence with custodians and brokers or other appropriate auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the auditor of one or more Nuveen investment companies since 2014.

Chicago, Illinois

February 25, 2021

20

| JHB | Nuveen Corporate Income

Portfolio of Investments December 31, 2020 |

| Principal Amount (000) |

Description (1) | Coupon | Maturity | Ratings (2) | Value | |||||||||||||||||||

| LONG-TERM INVESTMENTS – 74.3% (100.0% of Total Investments) |

| |||||||||||||||||||||||

| CORPORATE BONDS – 68.8% (92.6% of Total Investments) |

| |||||||||||||||||||||||

| Aerospace & Defense – 0.5% | ||||||||||||||||||||||||

| $ | 2,750 | Bombardier Inc, 144A |

5.750% | 3/15/22 | B | $ | 2,805,742 | |||||||||||||||||

| Airlines – 2.2% | ||||||||||||||||||||||||

| 3,019 | Air Canada, 144A |

7.750% | 4/15/21 | B+ | 3,034,095 | |||||||||||||||||||

| 12 | Continental Airlines 2007-1 Class B Pass-Through Trust |

6.903% | 4/19/22 | Ba1 | 12,292 | |||||||||||||||||||

| 8,000 | Delta Air Lines Inc |

3.625% | 3/15/22 | Baa3 | 8,230,261 | |||||||||||||||||||

| 6,700 | Virgin Australia Holdings Ltd, 144A |

7.875% | 10/15/21 | N/R | 536,000 | |||||||||||||||||||

| 17,731 | Total Airlines |

11,812,648 | ||||||||||||||||||||||

| Auto Components – 2.1% | ||||||||||||||||||||||||

| 2,000 | Icahn Enterprises LP / Icahn Enterprises Finance Corp |

6.250% | 2/01/22 | BB | 2,005,000 | |||||||||||||||||||

| 8,650 | ZF North America Capital Inc, 144A |

4.500% | 4/29/22 | BB+ | 8,896,092 | |||||||||||||||||||

| 10,650 | Total Auto Components |

10,901,092 | ||||||||||||||||||||||

| Automobiles – 2.8% | ||||||||||||||||||||||||

| 5,000 | Ford Motor Credit Co LLC |

3.813% | 10/12/21 | BB+ | 5,056,250 | |||||||||||||||||||

| 5,055 | Ford Motor Credit Co LLC |

3.339% | 3/28/22 | BB+ | 5,105,550 | |||||||||||||||||||

| 4,945 | Ford Motor Credit Co LLC |

1.521% | 3/28/22 | BB+ | 4,860,707 | |||||||||||||||||||

| 15,000 | Total Automobiles |

15,022,507 | ||||||||||||||||||||||

| Banks – 2.3% | ||||||||||||||||||||||||

| 2,000 | Banco Nacional de Costa Rica, 144A |

5.875% | 4/25/21 | B2 | 2,007,500 | |||||||||||||||||||

| 7,410 | CIT Group Inc |

4.125% | 3/09/21 | BBB– | 7,432,230 | |||||||||||||||||||

| 825 | Ukreximbank Via Biz Finance PLC, 144A |

9.625% | 4/27/22 | B | 859,303 | |||||||||||||||||||

| 1,844 | UniCredit SpA, 144A |

3.750% | 4/12/22 | Baa1 | 1,910,915 | |||||||||||||||||||

| 12,079 | Total Banks |

12,209,948 | ||||||||||||||||||||||

| Chemicals – 0.3% | ||||||||||||||||||||||||

| 1,353 | CF Industries Inc, 144A |

3.400% | 12/01/21 | Baa2 | 1,384,710 | |||||||||||||||||||

| Consumer Finance – 5.6% | ||||||||||||||||||||||||

| 4,585 | Ally Financial Inc |

4.125% | 2/13/22 | BBB– | 4,761,355 | |||||||||||||||||||

| 14,100 | Navient Corp |

6.625% | 7/26/21 | Ba3 | 14,399,625 | |||||||||||||||||||

| 6,225 | Navient Corp |

7.250% | 1/25/22 | Ba3 | 6,505,125 | |||||||||||||||||||

| 3,000 | OneMain Finance Corp |

7.750% | 10/01/21 | BB– | 3,157,500 | |||||||||||||||||||

| 995 | SLM Corp |

5.125% | 4/05/22 | BB+ | 1,017,388 | |||||||||||||||||||

| 28,905 | Total Consumer Finance |

29,840,993 | ||||||||||||||||||||||

| Diversified Financial Services – 1.3% | ||||||||||||||||||||||||

| 2,798 | Park Aerospace Holdings Ltd, 144A |

3.625% | 3/15/21 | BBB– | 2,805,550 | |||||||||||||||||||

| 4,280 | PHH Corp |

6.375% | 8/15/21 | N/R | 4,215,800 | |||||||||||||||||||

| 7,078 | Total Diversified Financial Services |

7,021,350 | ||||||||||||||||||||||

| Diversified Telecommunication Services – 3.2% | ||||||||||||||||||||||||

| 11,195 | CenturyLink Inc |

5.800% | 3/15/22 | BB | 11,670,787 | |||||||||||||||||||

| 5,000 | Cogent Communications Group Inc, 144A |

5.375% | 3/01/22 | Ba3 | 5,143,750 | |||||||||||||||||||

| 16,195 | Total Diversified Telecommunication Services |

16,814,537 | ||||||||||||||||||||||

| Electric Utilities – 1.1% | ||||||||||||||||||||||||

| 3,625 | Eskom Holdings SOC Ltd, 144A |

5.750% | 1/26/21 | BBB+ | 3,610,500 | |||||||||||||||||||

| 2,000 | Instituto Costarricense de Electricidad, 144A |

6.950% | 11/10/21 | B1 | 1,992,500 | |||||||||||||||||||

| 5,625 | Total Electric Utilities |

5,603,000 | ||||||||||||||||||||||

21

| JHB | Nuveen Corporate Income November 2021 Target Term Fund (continued) | |

| Portfolio of Investments December 31, 2020 | ||

| Principal Amount (000) |

Description (1) | Coupon | Maturity | Ratings (2) | Value | |||||||||||||||||||

| Food & Staples Retailing – 0.2% | ||||||||||||||||||||||||

| $ | 1,010 | Smithfield Foods Inc, 144A |

3.350% | 2/01/22 | BBB | $ | 1,023,863 | |||||||||||||||||

| Health Care Providers & Services – 0.1% | ||||||||||||||||||||||||

| 310 | Fresenius Medical Care US Finance II Inc, 144A |

5.875% | 1/31/22 | BBB | 326,475 | |||||||||||||||||||

| Hotels, Restaurants & Leisure – 3.3% | ||||||||||||||||||||||||

| 9,112 | International Game Technology PLC, 144A |

6.250% | 2/15/22 | BB | 9,408,049 | |||||||||||||||||||

| 5,000 | MGM Resorts International |

7.750% | 3/15/22 | BB | 5,325,000 | |||||||||||||||||||

| 2,900 | Yum! Brands Inc |

3.750% | 11/01/21 | B+ | 2,929,000 | |||||||||||||||||||

| 17,012 | Total Hotels, Restaurants & Leisure |

17,662,049 | ||||||||||||||||||||||

| Household Durables – 4.6% | ||||||||||||||||||||||||

| 5,460 | KB Home |

7.000% | 12/15/21 | BB | 5,651,100 | |||||||||||||||||||

| 1,250 | Lennar Corp |

6.250% | 12/15/21 | Baa3 | 1,280,000 | |||||||||||||||||||

| 450 | Lennar Corp |

4.125% | 1/15/22 | Baa3 | 460,688 | |||||||||||||||||||

| 6,432 | Meritage Homes Corp |

7.000% | 4/01/22 | Ba1 | 6,834,000 | |||||||||||||||||||

| 5,000 | Newell Brands Inc |

3.650% | 4/01/21 | BB+ | 4,987,500 | |||||||||||||||||||

| 4,525 | PulteGroup Inc |

4.250% | 3/01/21 | Baa3 | 4,536,312 | |||||||||||||||||||

| 500 | Toll Brothers Finance Corp |

5.875% | 2/15/22 | BBB– | 520,000 | |||||||||||||||||||

| 23,617 | Total Household Durables |

24,269,600 | ||||||||||||||||||||||

| Insurance – 1.1% | ||||||||||||||||||||||||

| 5,897 | Genworth Holdings Inc |

7.625% | 9/24/21 | B– | 5,985,455 | |||||||||||||||||||

| Internet & Direct Marketing Retail – 1.3% | ||||||||||||||||||||||||

| 6,655 | Netflix Inc |

5.500% | 2/15/22 | BB | 6,962,794 | |||||||||||||||||||

| Machinery – 0.4% | ||||||||||||||||||||||||

| 1,850 | CNH Industrial Capital LLC |

3.875% | 10/15/21 | BBB | 1,893,413 | |||||||||||||||||||

| Media – 5.3% | ||||||||||||||||||||||||

| 10,770 | CSC Holdings LLC |

6.750% | 11/15/21 | B | 11,254,650 | |||||||||||||||||||

| 11,485 | DISH DBS Corp |

6.750% | 6/01/21 | B2 | 11,717,112 | |||||||||||||||||||

| 5,146 | Nielsen Finance LLC / Nielsen Finance Co, 144A |

5.000% | 4/15/22 | BB– | 5,159,534 | |||||||||||||||||||

| 27,401 | Total Media |

28,131,296 | ||||||||||||||||||||||

| Metals & Mining – 3.5% | ||||||||||||||||||||||||

| 748 | Anglo American Capital PLC, 144A |

4.125% | 4/15/21 | BBB | 753,964 | |||||||||||||||||||

| 5,534 | Freeport-McMoRan Inc |

3.550% | 3/01/22 | Ba1 | 5,630,845 | |||||||||||||||||||

| 1,500 | Glencore Finance Canada Ltd, 144A |

4.950% | 11/15/21 | BBB+ | 1,559,888 | |||||||||||||||||||

| 3,825 | Howmet Aerospace Inc |

5.870% | 2/23/22 | BBB– | 4,001,906 | |||||||||||||||||||

| 3,250 | Petra Diamonds US Treasury PLC, 144A, (3) |

7.250% | 5/01/22 | D | 1,267,500 | |||||||||||||||||||

| 5,324 | Teck Resources Ltd |

4.750% | 1/15/22 | BBB– | 5,435,884 | |||||||||||||||||||

| 20,181 | Total Metals & Mining |

18,649,987 | ||||||||||||||||||||||

| Mortgage Real Estate Investment Trust – 1.7% | ||||||||||||||||||||||||

| 9,000 | Starwood Property Trust Inc |

5.000% | 12/15/21 | Ba3 | 9,150,930 | |||||||||||||||||||

| Oil, Gas & Consumable Fuels – 10.0% | ||||||||||||||||||||||||

| 9,250 | Calumet Specialty Products Partners LP / Calumet Finance Corp |

7.625% | 1/15/22 | B– | 9,157,500 | |||||||||||||||||||

| 3,000 | Occidental Petroleum Corp |

2.600% | 8/13/21 | Ba2 | 3,026,250 | |||||||||||||||||||

| 10,000 | Occidental Petroleum Corp |

3.125% | 2/15/22 | Ba2 | 10,075,000 | |||||||||||||||||||

| 2,172 | Ovintiv Exploration Inc |

5.750% | 1/30/22 | BBB– | 2,255,903 | |||||||||||||||||||

| 3,000 | Petroleos Mexicanos |

4.875% | 1/24/22 | BBB | 3,084,900 | |||||||||||||||||||

| 4,000 | Petroleos Mexicanos |

5.375% | 3/13/22 | BBB | 4,132,040 | |||||||||||||||||||

| 2,059 | Sabine Pass Liquefaction LLC |

6.250% | 3/15/22 | BBB– | 2,166,941 | |||||||||||||||||||

| 4,000 | Southwestern Energy Co |

4.100% | 3/15/22 | BB | 4,020,000 | |||||||||||||||||||

| 9,920 | Western Midstream Operating LP |

5.375% | 6/01/21 | Baa3 | 9,969,600 | |||||||||||||||||||

| 5,000 | WPX Energy Inc |

6.000% | 1/15/22 | BBB– | 5,075,050 | |||||||||||||||||||

| 52,401 | Total Oil, Gas & Consumable Fuels |

52,963,184 | ||||||||||||||||||||||

22

| Principal Amount (000) |

Description (1) | Coupon | Maturity | Ratings (2) | Value | |||||||||||||||||||

| Pharmaceuticals – 1.9% | ||||||||||||||||||||||||

| $ | 3,750 | Teva Pharmaceutical Finance Co BV |

3.650% | 11/10/21 | Ba2 | $ | 3,796,875 | |||||||||||||||||

| 6,199 | Teva Pharmaceutical Finance IV BV |

3.650% | 11/10/21 | BBB | 6,276,487 | |||||||||||||||||||

| 9,949 | Total Pharmaceuticals |

10,073,362 | ||||||||||||||||||||||

| Real Estate Management & Development – 0.9% | ||||||||||||||||||||||||

| 2,900 | China Evergrande Group, Reg S |

8.250% | 3/23/22 | B2 | 2,718,685 | |||||||||||||||||||

| 2,000 | RKPF Overseas 2019 B Ltd |

7.750% | 4/18/21 | BB– | 2,027,500 | |||||||||||||||||||

| 4,900 | Total Real Estate Management & Development |

4,746,185 | ||||||||||||||||||||||

| Semiconductors & Semiconductor Equipment – 0.2% | ||||||||||||||||||||||||

| 850 | Microchip Technology Inc |

3.922% | 6/01/21 | Baa3 | 862,066 | |||||||||||||||||||

| Specialty Retail – 1.5% | ||||||||||||||||||||||||

| 7,000 | Foot Locker Inc |

8.500% | 1/15/22 | BB+ | 7,446,250 | |||||||||||||||||||

| 448 | L Brands Inc |

5.625% | 2/15/22 | B+ | 464,240 | |||||||||||||||||||

| 7,448 | Total Specialty Retail |

7,910,490 | ||||||||||||||||||||||

| Technology Hardware, Storage & Peripherals – 1.5% | ||||||||||||||||||||||||

| 7,938 | Dell International LLC / EMC Corp, 144A |

5.875% | 6/15/21 | BB+ | 7,952,288 | |||||||||||||||||||

| Thrifts & Mortgage Finance – 0.6% | ||||||||||||||||||||||||

| 3,280 | Ladder Capital Finance Holdings LLLP / Ladder Capital Finance Corp, 144A |

5.250% | 3/15/22 | Ba2 | 3,296,400 | |||||||||||||||||||

| Trading Companies & Distributors – 2.3% | ||||||||||||||||||||||||

| 2,000 | AerCap Ireland Capital DAC / AerCap Global Aviation Trust |

3.950% | 2/01/22 | BBB | 2,056,493 | |||||||||||||||||||

| 7,000 | Aircastle Ltd |

5.500% | 2/15/22 | BBB | 7,290,312 | |||||||||||||||||||

| 2,809 | Fortress Transportation and Infrastructure Investors LLC, 144A |

6.750% | 3/15/22 | Ba3 | 2,816,023 | |||||||||||||||||||

| 11,809 | Total Trading Companies & Distributors |

12,162,828 | ||||||||||||||||||||||

| Transportation Infrastructure – 0.6% | ||||||||||||||||||||||||

| 3,000 | Adani Ports & Special Economic Zone Ltd, Reg S |

3.950% | 1/19/22 | BBB– | 3,067,049 | |||||||||||||||||||

| Wireless Telecommunication Services – 6.4% | ||||||||||||||||||||||||

| 11,495 | Hughes Satellite Systems Corp |

7.625% | 6/15/21 | BB | 11,782,375 | |||||||||||||||||||

| 3,000 | MTN Mauritius Investments Ltd, 144A |

5.373% | 2/13/22 | Ba2 | 3,088,950 | |||||||||||||||||||

| 1,475 | Sprint Communications Inc |

9.250% | 4/15/22 | N/R | 1,612,736 | |||||||||||||||||||

| 11,375 | Sprint Corp |

7.250% | 9/15/21 | BB+ | 11,835,687 | |||||||||||||||||||

| 5,429 | T-Mobile USA Inc |

4.000% | 4/15/22 | BB+ | 5,598,656 | |||||||||||||||||||

| 32,774 | Total Wireless Telecommunication Services |

33,918,404 | ||||||||||||||||||||||

| $ | 364,648 | Total Corporate Bonds (cost $367,073,864) |

364,424,645 | |||||||||||||||||||||

| Principal Amount (000) |

Description (1) | Coupon | Maturity | Ratings (2) | Value | |||||||||||||||||||

| SOVEREIGN DEBT – 2.7% (3.6% of Total Investments) |

| |||||||||||||||||||||||

| Argentina – 0.1% | ||||||||||||||||||||||||

| $ | 35 | Argentine Republic Government International Bond |

1.000% | 7/09/29 | CCC+ | $ | 15,298 | |||||||||||||||||

| 582 | Argentine Republic Government International Bond |

0.125% | 7/09/30 | CCC+ | 235,710 | |||||||||||||||||||

| 617 | Total Argentina |

|

251,008 | |||||||||||||||||||||

| Egypt – 1.3% | ||||||||||||||||||||||||

| 6,750 | Egypt Government International Bond, 144A |

6.125% | 1/31/22 | B+ | 7,042,235 | |||||||||||||||||||

| Nigeria – 0.3% | ||||||||||||||||||||||||

| 1,750 | Nigeria Government International Bond, 144A |

6.750% | 1/28/21 | B | 1,753,549 | |||||||||||||||||||

| Sri Lanka – 0.3% | ||||||||||||||||||||||||

| 2,100 | Sri Lanka Government International Bond, 144A |

5.750% | 1/18/22 | CCC+ | 1,626,051 | |||||||||||||||||||

23

| JHB | Nuveen Corporate Income November 2021 Target Term Fund (continued) | |

| Portfolio of Investments December 31, 2020 | ||

| Principal Amount (000) |

Description (1) | Coupon | Maturity | Ratings (2) | Value | |||||||||||||||||||||||

| Turkey – 0.7% | ||||||||||||||||||||||||||||

| $ | 3,625 | Turkey Government International Bond |

|

5.125% | 3/25/22 | BB– | $ | 3,712,000 | ||||||||||||||||||||

| $ | 14,842 | Total Sovereign Debt (cost $14,675,927) |

|

14,384,843 | ||||||||||||||||||||||||

| Principal Amount (000) |

Description (1) | Coupon (4) | Reference Rate (4) |

Spread (4) | Maturity (5) | Ratings (2) | Value | |||||||||||||||||||||

| VARIABLE RATE SENIOR LOAN INTERESTS – 1.5% (2.1% of Total Investments) (4) |

| |||||||||||||||||||||||||||

| Specialty Retail – 1.5% | ||||||||||||||||||||||||||||

| $ | 8,102 | Petsmart Inc., Term Loan B, First Lien |

4.500% | 3-Month LIBOR | 3.500% | 3/11/22 | B1 | $ | 8,121,987 | |||||||||||||||||||

| $ | 8,102 | Total Variable Rate Senior Loan Interests (cost $8,025,206) |

|

8,121,987 | ||||||||||||||||||||||||

| Principal Amount (000) |

Description (1) | Coupon | Maturity | Ratings (2) | Value | |||||||||||||||||||||||

| CONVERTIBLE BONDS – 1.3% (1.7% of Total Investments) |

| |||||||||||||||||||||||||||

| Interactive Media & Services – 1.0% | ||||||||||||||||||||||||||||

| $ | 5,000 | Twitter Inc |

|

1.000% | 9/15/21 | N/R | $ | 5,090,085 | ||||||||||||||||||||

| Pharmaceuticals – 0.3% |

| |||||||||||||||||||||||||||

| 1,706 | Teva Pharmaceutical Finance Co LLC |

|

0.250% | 2/01/26 | Ba2 | 1,697,470 | ||||||||||||||||||||||

| $ | 6,706 | Total Convertible Bonds (cost $6,637,068) |

|

6,787,555 | ||||||||||||||||||||||||

| Total Long-Term Investments (cost $396,412,065) |

|

393,719,030 | ||||||||||||||||||||||||||

| Other Assets Less Liabilities – 25.7% |

|

135,863,664 | ||||||||||||||||||||||||||

| Net Assets Applicable to Common Shares – 100% |

|

$ | 529,582,694 | |||||||||||||||||||||||||

For Fund portfolio compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications into sectors for reporting ease.

| (1) | All percentages shown in the Portfolio of Investments are based on net assets applicable to common shares unless otherwise noted. |

| (2) | For financial reporting purposes, the ratings disclosed are the highest of Standard & Poor’s Group (“Standard & Poor’s”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch, Inc. (“Fitch”) rating. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Ratings below BBB by Standard & Poor’s, Baa by Moody’s or BBB by Fitch are considered to be below investment grade. Holdings designated N/R are not rated by any of these national rating agencies. Ratings are not covered by the report of independent registered public accounting firm. |

| (3) | Defaulted security. A security whose issuer has failed to fully pay principal and/or interest when due, or is under the protection of bankruptcy. |

| (4) | Senior loans generally pay interest at rates which are periodically adjusted by reference to a base short-term, floating lending rate (Reference Rate) plus an assigned fixed rate (Spread). These floating lending rates are generally (i) the lending rate referenced by the London Inter-Bank Offered Rate (“LIBOR”), or (ii) the prime rate offered by one or more major United States banks. Senior loans may be considered restricted in that the Fund ordinarily is contractually obligated to receive approval from the agent bank and/or borrower prior to the disposition of a senior loan. The rate shown is the coupon as of the end of the reporting period. |

| (5) | Senior loans generally are subject to mandatory and/or optional prepayment. Because of these mandatory prepayment conditions and because there may be significant economic incentives for a borrower to prepay, prepayments of senior loans may occur. As a result, the actual remaining maturity of senior loans held may be substantially less than the stated maturities shown. |

| 144A | Investment is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These investments may only be resold in transactions exempt from registration, which are normally those transactions with qualified institutional buyers. |

| LIBOR | London Inter-Bank Offered Rate |

| Reg S | Regulation S allows U.S. companies to sell securities to persons or entities located outside of the United States without registering those securities with the Securities and Exchange Commission. Specifically, Regulation S provides a safe harbor from the registration requirements of the Securities Act for the offers and sales of securities by both foreign and domestic issuers that are made outside the United States. |

See accompanying notes to financial statements.

24

| JHAA | Nuveen Corporate Income 2023 Target

Portfolio of Investments December 31, 2020 |

| Principal Amount (000) |

Description (1) | Coupon | Maturity | Ratings (2) | Value | |||||||||||||||||||

| LONG-TERM INVESTMENTS – 122.3% (92.7% of Total Investments) |

||||||||||||||||||||||||

| CORPORATE BONDS – 79.4% (60.1% of Total Investments) |

||||||||||||||||||||||||

| Aerospace & Defense – 0.8% | ||||||||||||||||||||||||

| $ | 600 | Bombardier Inc, 144A |

6.125% | 1/15/23 | B | $ | 586,500 | |||||||||||||||||

| Air Freight & Logistics – 1.6% | ||||||||||||||||||||||||

| 1,200 | XPO Logistics Inc, 144A |

6.125% | 9/01/23 | BB– | 1,221,000 | |||||||||||||||||||

| Airlines – 1.3% | ||||||||||||||||||||||||

| 1,000 | United Airlines Holdings Inc |

5.000% | 2/01/24 | Ba3 | 992,500 | |||||||||||||||||||

| Auto Components – 1.6% | ||||||||||||||||||||||||

| 975 | Icahn Enterprises LP / Icahn Enterprises Finance Corp |

6.750% | 2/01/24 | BB | 991,555 | |||||||||||||||||||

| 250 | ZF North America Capital Inc, 144A |

4.500% | 4/29/22 | BB+ | 257,113 | |||||||||||||||||||

| 1,225 | Total Auto Components |

|

1,248,668 | |||||||||||||||||||||

| Automobiles – 4.2% | ||||||||||||||||||||||||

| 375 | Fiat Chrysler Automobiles NV |

5.250% | 4/15/23 | BBB– | 402,187 | |||||||||||||||||||

| 2,000 | Ford Motor Credit Co LLC |

3.370% | 11/17/23 | BB+ | 2,039,580 | |||||||||||||||||||

| 800 | Ford Motor Credit Co LLC |

5.584% | 3/18/24 | BB+ | 862,920 | |||||||||||||||||||

| 3,175 | Total Automobiles |

|

3,304,687 | |||||||||||||||||||||

| Chemicals – 2.0% | ||||||||||||||||||||||||

| 1,525 | NOVA Chemicals Corp, 144A |

4.875% | 6/01/24 | BB– | 1,587,906 | |||||||||||||||||||

| Commercial Services & Supplies – 2.5% | ||||||||||||||||||||||||

| 1,475 | ADT Security Corp |

4.125% | 6/15/23 | BB– | 1,572,571 | |||||||||||||||||||

| 400 | Pitney Bowes Inc |

5.950% | 4/01/23 | BB | 408,000 | |||||||||||||||||||

| 1,875 | Total Commercial Services & Supplies |

|

1,980,571 | |||||||||||||||||||||

| Communications Equipment – 1.0% | ||||||||||||||||||||||||

| 750 | CommScope Inc, 144A |

5.500% | 3/01/24 | Ba3 | 773,250 | |||||||||||||||||||

| Consumer Finance – 3.7% | ||||||||||||||||||||||||

| 500 | Navient Corp |

5.500% | 1/25/23 | Ba3 | 522,500 | |||||||||||||||||||

| 800 | Navient Corp |

7.250% | 9/25/23 | Ba3 | 876,784 | |||||||||||||||||||

| 1,300 | OneMain Finance Corp |

8.250% | 10/01/23 | BB– | 1,491,750 | |||||||||||||||||||

| 2,600 | Total Consumer Finance |

|

2,891,034 | |||||||||||||||||||||

| Containers & Packaging – 2.1% | ||||||||||||||||||||||||

| 237 | Berry Global Inc |

5.125% | 7/15/23 | BB+ | 239,963 | |||||||||||||||||||

| 500 | OI European Group BV, 144A |

4.000% | 3/15/23 | B+ | 510,000 | |||||||||||||||||||

| 28 | Reynolds Group Issuer Inc / Reynolds Group Issuer LLC / Reynolds Group Issuer Lu, 144A |

5.125% | 7/15/23 | B+ | 28,344 | |||||||||||||||||||

| 850 | Sealed Air Corp, 144A |

5.250% | 4/01/23 | BB+ | 903,125 | |||||||||||||||||||

| 1,615 | Total Containers & Packaging |

|

1,681,432 | |||||||||||||||||||||

| Diversified Financial Services – 2.0% | ||||||||||||||||||||||||

| 500 | Navient Corp |

6.125% | 3/25/24 | Ba3 | 533,750 | |||||||||||||||||||

| 300 | Park Aerospace Holdings Ltd, 144A |

4.500% | 3/15/23 | BBB– | 314,357 | |||||||||||||||||||

| 350 | Park Aerospace Holdings Ltd, 144A |

5.500% | 2/15/24 | BBB– | 381,671 | |||||||||||||||||||

| 300 | Sasol Financing International Ltd |

4.500% | 11/14/22 | BB | 305,910 | |||||||||||||||||||

| 1,450 | Total Diversified Financial Services |

|

1,535,688 | |||||||||||||||||||||

| Diversified Telecommunication Services – 2.1% | ||||||||||||||||||||||||

| 1,500 | CenturyLink Inc |