Form N-CSR FORUM FUNDS For: Jun 30

Tweet

Tweet Share

Share

AUXIER FOCUS FUND

Annual Report

June 30, 2018

Fund Adviser:

Auxier Asset Management LLC

15668 NE Eilers Road

Aurora, Oregon 97002

Toll Free: (877) 3AUXIER or (877) 328-9437

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2018

Market Commentary

In the second quarter, the US enjoyed improving fundamentals in terms of GDP1, employment, service sector and manufacturing gains. Home equity continues to increase, hitting records. Rising interest rates are pressuring bonds, bond surrogates and businesses with poor balance sheets. Lower taxes and regulation rollbacks are being offset somewhat over the worries of escalating trade tensions. The tax act expensing allowance is stimulating capital spending which in turn should improve overall productivity. While earnings in general are rising so are input costs like labor, fuel and transportation. Tariffs are leading to steep price increases in goods like steel and lumber. There continues to be a growing and acute shortage of truckers with a projected shortfall of over 50,000 drivers. We are seeing rolling industry corrections with increased volatility, in part due to tightened liquidity and the concentration of high frequency exchange-traded funds (ETFs). Higher interest rates and a strong US dollar have led to a sharp correction in emerging market currencies where low rates have led to a borrowing binge the last few years. Higher rates expose bad behavior and poor investment decisions.

Performance Update

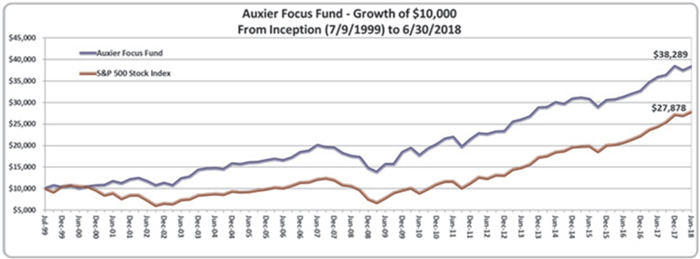

Auxier Focus Fund’s Investor Class returned 6.97% for the year ended June 30, 2018 vs. 14.37% for the S&P 500 Index. The stocks in the Fund returned 8.7%. Domestic stocks comprised 81% and foreign 15%, with cash and “workouts” 4%. From inception at the top of the market in 1999 to June 30, 2018, a hypothetical $10,000 investment in the Fund has grown to $38,289, with an average equity exposure of 78% compared to $27,878 for the fully invested S&P 500. When we started the Fund, General Electric was one of the most highly valued and popular companies in the world. $10,000 invested in General Electric back then is worth less than $6,500 as of June 30. Buy, hold and forget, without aggressive research, can be costly.

Contributors:

UnitedHealth Group (UNH)

Revenues grew 13.3% to $55.2 billion. Earnings from operations increased 18.8% to $4.1 billion. Every business segment reported double-digit earnings growth. Cash flows from operations for the quarter

Auxier Focus Fund – Investor Class

Average Annual Total Returns (6/30/2018)

Since Inception (07/09/1999) 7.33%

10-year 8.13%

5-year 8.09%

1-year 6.97%

3-month 2.39%

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than original cost. As stated in the current prospectus, the Fund’s Investor Class Share’s annual operating expense ratio (gross) is 1.10%. The Fund’s adviser has contractually agreed to waive a portion of its fee and/or reimburse Fund expenses to limit total annual operating expenses at 0.98%, which is in effect until October 31, 2018. Other share classes may vary. The Fund charges a 2.0% redemption fee on shares redeemed within six months of purchase. For the most recent month-end performance, please call (877) 328-9437 or visit the Adviser’s website at www.auxierasset.com. The recent growth rate in the stock market has helped to produce short-term returns that are not typical and may not continue in the future.

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2018

were $8.37 billion, up 29.63%. UnitedHealth repurchased 11.6 million shares for $2.65 billion during the first quarter. They also paid $722 million in dividends, an increase of 21.1%. UnitedHealth ended its exclusivity deal with Lab Corp this quarter and added Quest Diagnostics as one of its diagnostic service providers. This will provide their customers with more diverse diagnostic options in the future.

Valero Energy Corp. (VLO)

Valero saw revenues of $26.44 billion, up 21.44%. EPS2 was $1.09, up 60.29%. Net income for the quarter was $469 million, up 112.79%. Net cash flow from operating activities was $138 million, down 86.03%. The decrease in cash flow was due largely in part to the company’s continued investments in the future growth of the business. Capital investment plans for 2018 remain at $2.7 billion. $1 billion of this amount is for growth projects and the remaining $1.7 billion is for sustaining the business. Continued increase in US oil production and the decision to increase OPEC3 production by 1 million barrels per day will increase Valero’s earning potential. Growth prospects for Valero include renewable energy ventures such as a wind farm in Texas and a renewable diesel plant in Louisiana that will produce 10,000 barrels per day. Valero plans to increase production in this plant by 70% by the end of 2018.

Anthem Inc. (ANTM)

Total operating revenues remained flat at $22.3 billion. The total operating margin increased by 130 basis points to 8.4%. Net income increased by 30% to $1.31 billion. The increase in net income was driven by improved cost management and a lower tax rate. Anthem paid dividends of $0.75 per share in both Q1 and Q2 which equates to an annual dividend of $3.00 per share.

Becton Dickinson (BDX)

Becton Dickinson saw strong revenue growth in all three of their main segments leading to overall revenue growth of 47.2%. The continuing integration of Bard is going faster than expected.

| Top Holdings on 6/30/2018 | % Assets |

| UnitedHealth Group, Inc. | 4.3 |

| Bank of New York Mellon Corp. | 4.1 |

| Mastercard, Inc. Class A | 4.1 |

| Microsoft Corp. | 3.7 |

| Medtronic PLC | 3.4 |

| PepsiCo, Inc. | 3.3 |

| Johnson & Johnson | 2.9 |

| Phillip Morris International, Inc. | 2.9 |

| BP PLC | 2.8 |

|

Merck & Co, Inc. New |

2.5 |

Express Scripts (ESRX)

Cigna is acquiring Express Scripts for $48.75 in cash and 0.2434 of Cigna stock per share, which is over $90 a share. The deal is expected to close by the end of 2018.

Kroger (KR)

Kroger has focused on staying ahead of competitors as it adds three automatic warehouses for grocery delivery via robots this year. Their investments prove worthwhile, as their digital sales grew by 66% last quarter. In the next few years they expect their warehouse number to reach 20 and to benefit from their recently announced partnership with Nuro, an autonomous driving company. In terms of products, Kroger’s Simple Truth brand has reached $2 billion in annual sales, helping drive their adjusted net earnings up 14%.

Mastercard (MA)

Both transaction numbers and gross dollar volume were up for Mastercard, with net revenue rising 27% this past quarter to $3.6 billion. They have exemplified a strong push for growth in emerging markets with the recent acquisition of Oltio, which resides in South Africa. Acquiring Oltio enables Mastercard to introduce digital payments to even the smallest of local businesses to accelerate growth. In addition, their VocaLink subsidiary continues to drive their “Other Revenues” category, which was up 33% via its real time payments. As cash still makes up 80% of world’s total transactions, many believe Mastercard has plenty of room to grow even as an established company.

Biogen (BIIB)

Biogen saw revenues increase by 9% to $3.4 billion. Revenue growth was driven by Spinal Muscular Atrophy drug Spinraza which saw a 108% increase in revenue. Spinraza is Biogen’s fastest growing drug which they hope will be able to offset the slowing Multiple Sclerosis product line. Biogen presented the detailed results for the phase II trials of their Alzheimer’s drug BAN2401 on July 25th. The results of the trial were positive with tested patients showing 30% less cognitive decline over 18 months than those who received the placebo, but the presentation garnered a mixed reception and caused Biogen’s stock to fall 9% in after-hours trading. Earlier in July, Biogen announced that the trials of the drug were looking very positive without giving any details, and this announcement may have caused many to anticipate that the results would be better than what was ultimately shown. Currently, Biogen’s stock is hurting from the results announcement, but their outlook is still positive in the long-run due to the strength of their pipeline. Another Alzheimer’s drug in Biogen’s pipeline, Aducanumab, just finished its enrollment for two phase III trials. This drug has been regarded as more promising than BAN2401, and if it is successful Biogen will have the only drug in a $12 billion market.

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2018

Twenty-First Century Fox (FOXA)

Twenty-First Century Fox has been in the news recently due to the bidding war between Disney and Comcast. The merger that was eventually approved by shareholders, between Disney and Twenty-First Century Fox, will give Twenty-First Century Fox shareholders $38 a share or stock consideration. The collar on the stock consideration gives Twenty-First Century Fox shareholders an exchange ratio of 0.3324 if Disney stock is above $114.32. At the current price of $115.62 a share, the value on the consideration is about $38.50 a share. In addition to the deal with Disney, Twenty-First Century Fox will spin-off their news, sports, and broadcast businesses to create a new "Fox". The new "Fox" will include Fox News Channel, Fox Business Network, Fox Broadcasting Company, Fox Sports, Fox Television Stations Group, and sports cable networks. The deal has already been approved by the DOJ4 but still awaits approval in foreign markets.

Detractors:

Johnson & Johnson (JNJ)

One of only 22 companies to increase dividends every year for at least 50 consecutive years, Johnson & Johnson increased total sales 12.6% to over $20 billion. As the world’s largest medical conglomerate, they are well positioned to provide medicine and care for aging Baby Boomers.

Travelers (TRV)

Travelers is coming back down from historic highs early this year. Last quarter they posted revenue gains of 5% and net income gains of 12%. Hurricane losses in 2017 exceeded $200 billion. In 2018 losses have continued to be severe in hail and fires. This could further reduce capacity which should benefit premium pricing.

Philip Morris (PM) and Altria (MO)

Both stocks are starting to move higher after Q2 results came out for PM. Shipments on their “reduced risk products” were up, boosting their revenue. With the ability to raise prices, popularity of vaping and their inevitable entry into the marijuana market (anticipated to be a $50 billion market by 2026), the long-term fundamentals look solid. Both companies are structured to take advantage of developing trends.

Molson Coors (TAP)

Coors stock has struggled with 10% tariffs on aluminum, increasing competition from micro-breweries and a roaring marijuana market cutting into the overall beer market. Trying to take advantage of this growing market, Coors has assembled a team in Canada to find a way to best tap into the cannabis industry.

Inflation

The US employment-cost index, which measures wages and benefits, rose 2.8% in the twelve months ended in June. According to Standard and Poor’s, strong employment gains could lead to a further drop in the unemployment rate, to 3.6% over the next few months. Historically, in a more normalized interest rate environment, the 10-year Treasury would yield 2% higher than the prevailing inflation rate. This makes bonds vulnerable with the current rate under 3%. Through six months the Barclays intermediate bond index has declined 2.63%. Higher inflation rates tend to compress stock price-earnings ratios making high expectation momentum strategies vulnerable to sharp corrections on earnings disappointments. One of the best inflation hedges I have seen in the past thirty-five years is a well nurtured business, with disciplined capital allocation, that earns high returns on capital, enjoys rapid inventory turns and has the ability to raise prices while requiring little in mandatory capital expenditure to grow. We strive to be long term owners of such enterprises. Conversely, utilities have high mandatory cash needs and can suffer if faced with large construction projects. In the 1980s I remember watching utilities get crushed in the market as higher inflation led to cost overruns on the construction of nuclear power plants. In our research we have not been able to identify one utility in the US that currently has positive cash flow.

In socialist Venezuela, inflation rates are running more than 40,000%, yet stock returns in local terms have still exceeded inflation. Bonds have been wiped out. There is a misperception that government bonds are safe. Argentina has defaulted over six times and recently raised interest rates 40% to defend their currency.

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2018

Risks

Technological disruption is a constant threat as the economy digitizes. Platform changes need to be scrutinized. The move from 3G to 4G decimated phone companies like Nokia, Blackberry and Motorola leading to a duopoly with Android and Apple. 5G could be as equally disruptive. Voice enabled assistants, artificial intelligence and augmented reality are potential platforms that could change the status quo. The growth of the cloud has led to centralized market power with Amazon, Microsoft and Google. However, blockchain technology decentralizes the internet through digital ledgers and could prove to be a powerful disrupter that claims to be less corruptible.

The popularity and performance of many technology stocks is acting as a magnet for enormous flows of capital which can lead to supply gluts. We are seeing exuberance in venture funding from Japan, China and Silicon Valley. This happened in the late 1990s when the rage was internet hosting and fiberoptic. Massive capacity was built for businesses losing money and when interest rates rose a crash followed. Telecom companies like Lucent and Level 3 lost over 85% of their value. It is estimated by the venture firm Benchmark that today the top 200 Silicon Valley start-ups have cash burn rates 5 to 10 times 1999 levels. The potential problem, like 1999, is that much of the technology infrastructure is being built for businesses losing money and with interest rates rising the funding can cease abruptly. Softbank is driving crazy valuations in businesses like WeWork, which provides basic workspaces. Softbank is seeking a valuation in excess of $20 billion for this company that lost over $900 million last year. Many venture firms will often set private market pricing far higher than underlying fundamentals warrant. In addition, record amounts of money have been raised in private equity (leveraged buyouts). Carlyle Group recently raised a record $18.5 billion. Many of our portfolio companies are attractive to these leveraged buyout firms because of their high free cash flow characteristics. However, bond protection via debt covenants has never been this poor. This is a new cyclical low in the quality of covenant protection, which is common near the end of booms.

Opportunities

We are seeing exciting innovations in medtech and biotech. Many of the larger companies’ stocks trade at very reasonable valuations by historic standards. Fred Hutchinson Cancer Research Center out of Seattle has stated cures for cancer are in sight as “immunotherapies” that unleash the body’s own immune system to seek out and destroy cancer cells have “shown mind-blowing results in early testing on blood cancers.” CAR T cell therapies are being developed by companies like Celgene and Gilead. Merck’s KEYTRUDA has shown good potential for the treatment of lung cancer. Companies like Alkermes, led by founder CEO Richard Pops, are at the forefront in the treatment of opioid addictions, which have led to over 50 million deaths this past year. Exciting strides are being made in transaortic valve replacement led by Medtronic. Cerner is an attractive leader in digitizing hospitals and doctors’ offices. They recently landed a major multiyear contract with the Veteran’s Administration.

Alphabet is taking a leadership in artificial intelligence and predictive data analytics. YouTube, with over 1.8 billion users has grown over 20% this past year and has an annual growth rate nearly twice as fast as Facebook’s. YouTube users spend over an hour a day on the YouTube mobile app alone. Waymo is a leader in self-driving car technology. It took Waymo six years to test their first one million miles, this year they went from seven to eight million in one month.

In the industrial sector, fears over deepening trade wars have led to more attractive prices for quality franchises like Parker Hannifin and Caterpillar. Higher short-term interest rates will help earnings for companies and households with high cash balances which have suffered under central bank interest rate suppression over the past decade.

We are looking for management teams focused on using predictive data analytics and the “customer experience.” Those on the right side of digital are being rewarded with premium valuations. With internet transparency, high-grade ethics are more important than ever in building intrinsic value. We strongly believe that the best way to enjoy high compounded returns over long periods is through the well-researched selection of high return businesses that are ideally founder or family controlled and where the management is diligent in capital allocation and relentlessly focused on improving value. Usually the best buys have been when there is a plethora of negative headlines and the consensus is “this is no time to buy stocks.” Those purchased at an attractive price can reward investors with the double-triple play over years while deferring taxes and providing more than adequate compensation for the risk taken.

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2018

Trade

It appears the Trump administration is using tariffs as a tool to bring countries to the negotiating table on a more bilateral basis. Negotiations surrounding Europe and The North American Free Trade Agreement (NAFTA) appear to be moving forward. China is tougher. What is needed is a united front by allies to increase the leverage for a level playing field respecting intellectual property rights. We see President Trump as resolute with China. On the downside, the Smoot-Hawley Tariff Act of 1930 raised tariffs on over 20,000 imported goods which led to a drop of American exports and imports by over half. So free trade is the obvious choice vs protectionism. Given China’s growing debt load, nearly 300% of GDP, steep stock market correction and surplus trade position, it looks like a good time for the US and Europe to push for meaningful reforms. We are hopeful that this is a bargaining stance to ultimately lead to lower overall global tariffs. While there is immediate pain in the farm sector, negative headlines create opportunities to add to world class business franchises that rarely trade at bargain prices.

China has been a big creditor to Venezuela where the Maduro policies have led to starvation, human rights atrocities and hyperinflation. The “Black Book on Communism” published by Harvard University Press in France illustrated work carried out by a team of professors and researchers from the National Center for Scientific Research—the most important scientific institution in France. They listed the number of people killed by communism. China led the list with an estimated 82 million dead under communist rule. Since 1999 Venezuela, where the leadership follows Marxism-Leninism, they figure more than 252,000 dead. That is why we put so much time into daily research to identify facts and fundamentals and those policies that can destroy intrinsic value. Integrity in financial markets, political checks and the rule of law are all critical to enduring long term. The only constant in investing is change and the key to risk management continues to be a rational approach rooted in a daily tenacious research effort.

I sought for the greatness and genius of America in her commodious harbors and her ample rivers—and it was not there .... in her fertile fields and boundless forests—and it was not there .... in her rich mines and her vast world commerce—and it was not there .... in her democratic Congress and her matchless Constitution—and it was not there. Not until I went into the churches of America and heard her pulpits flame with righteousness did I understand the secret of her genius and power. America is great because she is good, and if America ever ceases to be good, she will cease to be great. - Alexis de Tocqueville.

We appreciate your trust.

Jeff Auxier

Fund returns (i) assume the reinvestment of all dividends and capital gain distributions and (ii) would have been lower during the period if certain fees and expenses had not been waived. Performance shown is for the Fund’s Investor Class shares; returns for other share classes will vary. Performance for Investor Class shares for periods prior to December 10, 2004 reflects performance of the applicable share class of Auxier Focus Fund, a series of Unified Series Trust (the “Predecessor Fund”). Prior to January 3, 2003, the Predecessor Fund was a series of Ameriprime Funds. The performance of the Fund’s Investor Class shares for the period prior to December 10, 2004 reflects the expenses of the Predecessor Fund.

The Fund may invest in value and/or growth stocks. Investments in value stocks are subject to risk that their intrinsic value may never be realized and investments in growth stocks may be susceptible to rapid price swings, especially during periods of economic uncertainty. In addition, the Fund may invest in mid-sized companies which generally carry greater risk than is customarily associated with larger companies. Moreover, if the Fund’s portfolio is overweighted in a sector, any negative development affecting that sector will have a greater impact on the Fund than a fund that is not overweighted in that sector. An increase in interest rates typically causes a fall in the value of a debt security (Fixed-Income Securities Risk) with corresponding changes to the Fund’s value.

| 1 | Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country's borders in a specific time period. |

| 2 | Earnings per share (EPS) is the portion of a company's profit allocated to each outstanding share of common stock. Earnings per share serves as an indicator of a company's profitability. EPS is calculated as: EPS = (Net Income - Dividends on Preferred Stock) / Average Outstanding Shares. |

| 3 | OPEC is an abbreviation for Organization of Petroleum Exporting Countries, which is a union of oil producing countries that regulate the amount of oil each country is able to produce. |

| 4 | DOJ is an abbreviation for The Department of Justice, a department of the federal executive branch, headed by the attorney general, which administers the Federal Bureau of Investigation (FBI), prosecutes violations of federal law, and is responsible for enforcing all civil rights legislation. |

AUXIER FOCUS FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

JUNE 30, 2018

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on 500 widely held common stocks. One cannot invest directly in an index or average.

The views in this shareholder letter were those of the Fund Manager as of the letter’s publication date and may not reflect his views on the date this letter is first distributed or anytime thereafter. These views are intended to assist readers in understanding the Fund’s investment methodology and do not constitute investment advice.

AUXIER FOCUS FUND

PERFORMANCE CHART AND ANALYSIS (Unaudited)

JUNE 30, 2018

The following chart reflects the change in the value of a hypothetical $10,000 investment in Investor Shares, including reinvested dividends and distributions, in the Auxier Focus Fund (the “Fund”) compared with the performance of the benchmark, the S&P 500 Index (“S&P 500”), over the past ten fiscal years. The S&P 500 is a broad-based measurement of the U.S. stock market based on the performance of 500 widely held large capitalization common stocks. The total return of the Fund's classes includes the maximum sales charge of 5.75% (A Shares only) and operating expenses that reduce returns, while the total return of the S&P 500 does not include the effect of sales charges and expenses. A Shares are subject to a 1.00% contingent deferred sales charge on shares purchased without an initial sales charge and redeemed less than one year after purchase. The total return of the index includes the reinvestment of dividends and income. The total return of the Fund includes operating expenses that reduce returns, while the total return of the index does not include expenses. The Fund is professionally managed, while the index is unmanaged and is not available for investment.

Comparison of Change in Value of a $10,000 Investment

Investor Shares vs. S&P 500 Index

|

Average Annual Total Returns Periods Ended June 30, 2018 |

One Year | Five Years | Ten Years | Since Inception(1) |

| Investor Shares | 6.97% | 8.09% | 8.13% | 7.33% |

| S&P 500® Index (Since July 9, 1999) | 14.37% | 13.42% | 10.17% | 5.55% |

| A Shares (with sales charge)(2),(3) | 0.55% | 6.68% | 7.42% | 6.96% |

| Institutional Shares(3) | 7.20% | 8.31% | 8.27% | 7.40% |

| (1) | Investor, A Shares and Institutional Shares commenced operations on July 9, 1999, July 8, 2005 and May 9, 2012, respectively. |

| (2) | Due to shareholder redemptions on August 21, 2005, net assets of the class were zero from the close of business on that date until September 22, 2005. Financial information presented for the period August 21, 2005 to September 22, 2005 reflects performance of Investor Shares of the Fund. |

| (3) | For Institutional Shares, performance for the 10-year and since inception periods are blended average annual returns which include the returns of the Investor Shares prior to commencement of operations of the Institutional Shares. For A Shares, performance for the since inception period is a blended average annual return which includes the return of the Investor Shares prior to commencement of operations of the A Shares. |

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than original cost. As stated in the Fund’s prospectus, the annual operating expense ratios (gross) for Investor Shares, A Shares and Institutional Shares are 1.10%, 1.54% and 1.10%, respectively. However, the Fund’s Adviser has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, dividend expenses on short sales, and extraordinary expenses) to 0.98%, 1.25% and 0.80% of the Investor Shares, A Shares and Institutional Shares, respectively, through October 31, 2018 (the “Expense Cap”). The Adviser may be reimbursed by the Fund for fees waived and expenses reimbursed by the Adviser pursuant to the Expense Cap if such payment is made within three years of the fee waiver or expense reimbursement, and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current Expense Cap, or (ii) the Expense Cap in place at the time the fees/expenses were waived/reimbursed. Shares redeemed or exchanged within 180 days of purchase will be charged a 2.00% redemption fee. The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns greater than one year are annualized. For the most recent month-end performance, please call (877) 328-9437 or visit www.auxierasset.com.

Performance for Investor Shares for periods prior to December 10, 2004, reflects performance and expenses of Auxier Focus Fund, a series of Unified Series Trust (the “Predecessor Fund”). Prior to January 3, 2003, the Predecessor Fund was a series of Ameriprime Funds.

AUXIER FOCUS FUND

SCHEDULE OF INVESTMENTS

JUNE 30, 2018

| Shares | Security Description | Value | ||||||

| Equity Securities - 96.8% | ||||||||

| Common Stock - 96.8% | ||||||||

| Communications - 2.7% | ||||||||

| 222,375 | America Movil SAB de CV, ADR | $ | 3,704,767 | |||||

| 1,719 | Cisco Systems, Inc. | 73,969 | ||||||

| 221,738 | Telefonica SA, ADR | 1,891,425 | ||||||

| 8,446 | Twenty-First Century Fox, Inc., Class A | 419,682 | ||||||

| 8,845 | Viacom, Inc., Class B | 266,765 | ||||||

| 6,356,608 | ||||||||

| Consumer Discretionary - 6.2% | ||||||||

| 27,700 | Arcos Dorados Holdings, Inc., Class A | 192,515 | ||||||

| 34,000 | Becle SAB de CV | 49,300 | ||||||

| 54,160 | Comcast Corp., Class A | 1,776,990 | ||||||

| 9,990 | CVS Health Corp. | 642,856 | ||||||

| 114,077 | Discovery Communications, Inc., Class A (a) | 3,137,117 | ||||||

| 4,641 | Discovery Communications, Inc., Class C (a) | 118,345 | ||||||

| 16,250 | General Motors Co. | 640,250 | ||||||

| 36,712 | H&R Block, Inc. | 836,299 | ||||||

| 186,701 | Lincoln Educational Services Corp. (a) | 324,860 | ||||||

| 18,550 | Lowe's Cos., Inc. | 1,772,824 | ||||||

| 6,156 | McDonald's Corp. | 964,584 | ||||||

| 38,150 | Sally Beauty Holdings, Inc. (a) | 611,545 | ||||||

| 1,176 | The Andersons, Inc. | 40,219 | ||||||

| 4,725 | The Home Depot, Inc. | 921,847 | ||||||

| 19,150 | Walmart, Inc. | 1,640,198 | ||||||

| 7,050 | Yum China Holdings, Inc. | 271,143 | ||||||

| 7,050 | Yum! Brands, Inc. | 551,451 | ||||||

| 14,492,343 | ||||||||

| Consumer Staples - 18.3% | ||||||||

| 62,500 | Altria Group, Inc. | 3,549,375 | ||||||

| 30,200 | British American Tobacco PLC, ADR | 1,523,590 | ||||||

| 13,200 | Coca-Cola HBC AG, ADR (a) | 442,332 | ||||||

| 5,135 | Diageo PLC, ADR | 739,491 | ||||||

| 2,225 | Dr. Pepper Snapple Group, Inc. | 271,450 | ||||||

| 15,378 | Lamb Weston Holdings, Inc. | 1,053,547 | ||||||

| 50,327 | Molson Coors Brewing Co., Class B | 3,424,249 | ||||||

| 35,300 | Monster Beverage Corp. (a) | 2,022,690 | ||||||

| 70,820 | PepsiCo., Inc. | 7,710,173 | ||||||

| 83,725 | Philip Morris International, Inc. | 6,759,956 | ||||||

| 160,871 | Tesco PLC, ADR | 1,629,623 | ||||||

| 57,300 | The Coca-Cola Co. | 2,513,178 | ||||||

| 2,845 | The J.M. Smucker Co. | 305,781 | ||||||

| 203,368 | The Kroger Co. | 5,785,820 | ||||||

| 20,525 | The Procter & Gamble Co. | 1,602,182 | ||||||

| 67,900 | Unilever NV, ADR | 3,783,388 | ||||||

| 43,116,825 | ||||||||

| Consumer, Cyclical - 0.4% | ||||||||

| 20,475 | DR Horton, Inc. | 839,475 | ||||||

| Energy - 4.8% | ||||||||

| 144,810 | BP PLC, ADR | 6,612,025 | ||||||

| 9,430 | Chevron Corp. | 1,192,235 | ||||||

| 14,600 | ConocoPhillips | 1,016,452 | ||||||

| 7,800 | Phillips 66 | 876,018 | ||||||

| 14,415 | Valero Energy Corp. | 1,597,614 | ||||||

| 11,294,344 | ||||||||

| Financials - 21.8% | ||||||||

| 57,260 | Aflac, Inc. | 2,463,325 | ||||||

| 49,445 | American International Group, Inc. | 2,621,574 | ||||||

| 1,280 | Ameriprise Financial, Inc. | 179,046 | ||||||

| 201,699 | Bank of America Corp. | 5,685,895 | ||||||

| 16,545 | Berkshire Hathaway, Inc., Class B (a) | 3,088,124 | ||||||

| 67,374 | Central Pacific Financial Corp. | 1,930,265 | ||||||

| Shares | Security Description | Value | ||||||

| Financials - 21.8% (continued) | ||||||||

| 25,975 | Citigroup, Inc. | $ | 1,738,247 | |||||

| 5,616 | Colliers International Group, Inc. | 425,131 | ||||||

| 132,268 | Credit Suisse Group AG, ADR | 1,968,148 | ||||||

| 5,616 | FirstService Corp. | 427,041 | ||||||

| 66,668 | Franklin Resources, Inc. | 2,136,709 | ||||||

| 9,500 | Legg Mason, Inc. | 329,935 | ||||||

| 3,025 | Marsh & McLennan Cos., Inc. | 247,959 | ||||||

| 48,550 | Mastercard, Inc., Class A | 9,541,046 | ||||||

| 1,100 | PayPal Holdings, Inc. (a) | 91,597 | ||||||

| 179,700 | The Bank of New York Mellon Corp. | 9,691,221 | ||||||

| 27,418 | The Travelers Cos., Inc. | 3,354,318 | ||||||

| 7,350 | U.S. Bancorp | 367,647 | ||||||

| 15,249 | Unum Group | 564,061 | ||||||

| 31,600 | Visa, Inc., Class A | 4,185,420 | ||||||

| 14,350 | Waddell & Reed Financial, Inc., Class A | 257,870 | ||||||

| 2,950 | Wells Fargo & Co. | 163,548 | ||||||

| 51,458,127 | ||||||||

| Health Care - 25.4% | ||||||||

| 46,051 | Abbott Laboratories | 2,808,650 | ||||||

| 2,900 | Alkermes PLC (a) | 119,364 | ||||||

| 5,230 | Allergan PLC | 871,946 | ||||||

| 740 | Amgen, Inc. | 136,597 | ||||||

| 18,981 | Anthem, Inc. | 4,518,047 | ||||||

| 15,200 | Becton Dickinson and Co. | 3,641,312 | ||||||

| 13,940 | Biogen, Inc. (a) | 4,045,946 | ||||||

| 55,424 | Express Scripts Holding Co. (a) | 4,279,287 | ||||||

| 1,780 | Gilead Sciences, Inc. | 126,095 | ||||||

| 3,700 | GlaxoSmithKline PLC, ADR | 149,147 | ||||||

| 56,240 | Johnson & Johnson | 6,824,162 | ||||||

| 93,818 | Medtronic PLC | 8,031,759 | ||||||

| 96,059 | Merck & Co., Inc. | 5,830,781 | ||||||

| 7,282 | Pfizer, Inc. | 264,191 | ||||||

| 23,337 | Quest Diagnostics, Inc. | 2,565,670 | ||||||

| 41,631 | UnitedHealth Group, Inc. | 10,213,749 | ||||||

| 47,400 | Zimmer Biomet Holdings, Inc. | 5,282,256 | ||||||

| 59,708,959 | ||||||||

| Industrials - 4.6% | ||||||||

| 173,141 | Corning, Inc. | 4,763,109 | ||||||

| 2,725 | FedEx Corp. | 618,738 | ||||||

| 88,671 | Manitex International, Inc. (a) | 1,106,614 | ||||||

| 11,500 | Raytheon Co. | 2,221,570 | ||||||

| 7,375 | Textainer Group Holdings, Ltd. (a) | 117,263 | ||||||

| 2,350 | The Boeing Co. | 788,448 | ||||||

| 11,595 | United Parcel Service, Inc., Class B | 1,231,737 | ||||||

| 10,847,479 | ||||||||

| Information Technology - 7.5% | ||||||||

| 1,430 | Alphabet, Inc., Class A (a) | 1,614,742 | ||||||

| 41,910 | Cerner Corp. (a) | 2,505,799 | ||||||

| 16,675 | Cognizant Technology Solutions Corp., Class A | 1,317,158 | ||||||

| 300 | Facebook, Inc., Class A (a) | 58,296 | ||||||

| 87,337 | Microsoft Corp. | 8,612,302 | ||||||

| 82,320 | Oracle Corp. | 3,627,019 | ||||||

| 17,735,316 | ||||||||

| Materials - 4.7% | ||||||||

| 14,225 | Celanese Corp., Class A | 1,579,829 | ||||||

| 85,376 | DowDuPont, Inc. | 5,627,986 | ||||||

| 26,505 | LyondellBasell Industries NV, Class A | 2,911,574 | ||||||

| 32,055 | The Mosaic Co. | 899,143 | ||||||

| 11,018,532 | ||||||||

| Telecommunications - 0.2% | ||||||||

| 23,775 | CenturyLink, Inc. | 443,166 | ||||||

See Notes to Financial Statements.

AUXIER FOCUS FUND

SCHEDULE OF INVESTMENTS

JUNE 30, 2018

| Shares | Security Description | Value | ||||||

| Transportation - 0.2% | ||||||||

| 2,550 | Delta Air Lines, Inc. | $ | 126,327 | |||||

| 3,160 | Union Pacific Corp. | 447,709 | ||||||

| 574,036 | ||||||||

| Total Common Stock (Cost $124,789,141) | 227,885,210 | |||||||

| Total Equity Securities (Cost $124,789,141) | 227,885,210 | |||||||

| Principal | Security Description | Rate | Maturity | Value | |||||||||||

| Fixed Income Securities - 0.9% | |||||||||||||||

| Corporate Non-Convertible Bonds - 0.8% | |||||||||||||||

| Financials - 0.6% | |||||||||||||||

| $ | 500,000 | Fifth Third Bancorp (callable at 100) (b)(c) | 5.10 | % | 06/30/23 | 493,485 | |||||||||

| 400,000 | SunTrust Banks, Inc. (callable at 100) (b)(c) | 5.13 | 12/15/27 | 380,750 | |||||||||||

| 500,000 | The Goldman Sachs Group, Inc. (callable at 100) (b)(c) | 5.00 | 11/10/22 | 470,300 | |||||||||||

| 1,344,535 | |||||||||||||||

| Industrials - 0.2% | |||||||||||||||

| 450,000 | General Electric Co. (callable at 100) (b)(c) | 5.00 | 01/21/21 | 444,487 | |||||||||||

| Total Corporate Non-Convertible Bonds | |||||||||||||||

| (Cost $1,839,182) | 1,789,022 | ||||||||||||||

| U.S. Government & Agency Obligations - 0.1% | |||||||||||||||

| U.S. Treasury Securities - 0.1% | |||||||||||||||

| 275,000 | U.S. Treasury Bill (d) (Cost $272,875) | 2.05 | 11/15/18 | 272,927 | |||||||||||

| Total Fixed Income Securities | |||||||||||||||

| (Cost $2,112,057) | 2,061,949 | ||||||||||||||

| Investments, at value - 97.7% (Cost $126,901,198) | $ | 229,947,159 | |||||||||||||

| Other Assets & Liabilities, Net - 2.3% | 5,510,696 | ||||||||||||||

| Net Assets - 100.0% | $ | 235,457,855 | |||||||||||||

| ADR | American Depositary Receipt |

| PLC | Public Limited Company |

| (a) | Non-income producing security. |

| (b) | Variable rate security, the interest rate of which adjusts periodically based on changes in current interest rates. Rate represented is as of June 30, 2018. |

| (c) | Perpetual maturity security. Maturity date presented is call date as of June 30, 2018. |

| (d) | Zero coupon bond. Interest rate presented is yield to maturity. |

The following is a summary of the inputs used to value the Fund's investments as of June 30, 2018.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in Note 2 of the accompanying Notes to Financial Statements.

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Investments at Value | ||||||||||||||||

| Common Stock | ||||||||||||||||

| Communications | $ | 6,356,608 | $ | – | $ | – | $ | 6,356,608 | ||||||||

| Consumer Discretionary | 14,492,343 | – | – | 14,492,343 | ||||||||||||

| Consumer Staples | 43,116,825 | – | – | 43,116,825 | ||||||||||||

| Consumer, Cyclical | 839,475 | – | – | 839,475 | ||||||||||||

| Energy | 11,294,344 | – | – | 11,294,344 | ||||||||||||

| Financials | 51,458,127 | – | – | 51,458,127 | ||||||||||||

| Health Care | 59,708,959 | – | – | 59,708,959 | ||||||||||||

| Industrials | 10,847,479 | – | – | 10,847,479 | ||||||||||||

| Information Technology | 17,735,316 | – | – | 17,735,316 | ||||||||||||

| Materials | 11,018,532 | – | – | 11,018,532 | ||||||||||||

| Telecommunications | 443,166 | – | – | 443,166 | ||||||||||||

| Transportation | 574,036 | – | – | 574,036 | ||||||||||||

| Corporate Non-Convertible Bonds | – | 1,789,022 | – | 1,789,022 | ||||||||||||

| U.S. Government & Agency Obligations | – | 272,927 | – | 272,927 | ||||||||||||

| Investments at Value | $ | 227,885,210 | $ | 2,061,949 | $ | – | $ | 229,947,159 | ||||||||

The Fund utilizes the end of period methodology when determining transfers. There were no transfers among Level 1, Level 2 and Level 3 for the year ended June 30, 2018.

| PORTFOLIO HOLDINGS (Unaudited) | |||

| % of Total Net Assets | |||

| Communications | 2.7% | ||

| Consumer Discretionary | 6.2% | ||

| Consumer Staples | 18.3% | ||

| Consumer, Cyclical | 0.4% | ||

| Energy | 4.8% | ||

| Financials | 21.8% | ||

| Health Care | 25.4% | ||

| Industrials | 4.6% | ||

| Information Technology | 7.5% | ||

| Materials | 4.7% | ||

| Telecommunications | 0.2% | ||

| Transportation | 0.2% | ||

| Corporate Non-Convertible Bonds | 0.8% | ||

| U.S. Government & Agency Obligations | 0.1% | ||

| Other Assets & Liabilities, Net | 2.3% | ||

| 100.0% |

AUXIER FOCUS FUND

STATEMENT OF ASSETS AND LIABILITIES

JUNE 30, 2018

| ASSETS | ||||

| Investments, at value (Cost $126,901,198) | $ | 229,947,159 | ||

| Cash | 5,302,232 | |||

| Receivables: | ||||

| Fund shares sold | 99,709 | |||

| Investment securities sold | 236,776 | |||

| Dividends and interest | 306,663 | |||

| Prepaid expenses | 23,813 | |||

| Total Assets | 235,916,352 | |||

| LIABILITIES | ||||

| Payables: | ||||

| Investment securities purchased | 142,936 | |||

| Fund shares redeemed | 112,221 | |||

| Accrued Liabilities: | ||||

| Investment Adviser fees | 131,733 | |||

| Trustees’ fees and expenses | 510 | |||

| Fund services fees | 25,166 | |||

| Other expenses | 45,931 | |||

| Total Liabilities | 458,497 | |||

| NET ASSETS | $ | 235,457,855 | ||

| COMPONENTS OF NET ASSETS | ||||

| Paid-in capital | $ | 122,406,550 | ||

| Undistributed net investment income | 1,556,427 | |||

| Accumulated net realized gain | 8,448,917 | |||

| Net unrealized appreciation | 103,045,961 | |||

| NET ASSETS | $ | 235,457,855 | ||

| SHARES OF BENEFICIAL INTEREST AT NO PAR VALUE (UNLIMITED SHARES AUTHORIZED) | ||||

| Investor Shares | 7,236,757 | |||

| A Shares | 123,287 | |||

| Institutional Shares | 3,161,837 | |||

| NET ASSET VALUE, OFFERING AND REDEMPTION PRICE PER SHARE* | ||||

| Investor Shares (based on net assets of $161,032,326) | $ | 22.25 | ||

| A Shares (based on net assets of $2,781,856) | $ | 22.56 | ||

| A Shares Maximum Public Offering Price Per Share (net asset value per share/(100%-5.75%)) | $ | 23.94 | ||

| Institutional Shares (based on net assets of $71,643,673) | $ | 22.66 | ||

| * | Shares redeemed or exchanged within 180 days of purchase are charged a 2.00% redemption fee. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

STATEMENT OF OPERATIONS

YEAR ENDED JUNE 30, 2018

| INVESTMENT INCOME | ||||

| Dividend income (Net of foreign withholding taxes of $46,551) | $ | 5,175,169 | ||

| Interest income | 157,896 | |||

| Total Investment Income | 5,333,065 | |||

| EXPENSES | ||||

| Investment Adviser fees | 2,005,321 | |||

| Fund services fees | 328,563 | |||

| Transfer agent fees: | ||||

| Investor Shares | 58,990 | |||

| A Shares | 1,080 | |||

| Institutional Shares | 4,953 | |||

| Distribution fees: | ||||

| A Shares | 7,118 | |||

| Custodian fees | 26,090 | |||

| Registration fees: | ||||

| Investor Shares | 19,764 | |||

| A Shares | 3,436 | |||

| Institutional Shares | 15,292 | |||

| Professional fees | 55,056 | |||

| Trustees' fees and expenses | 17,522 | |||

| Other expenses | 217,636 | |||

| Total Expenses | 2,760,821 | |||

| Fees waived | (416,724 | ) | ||

| Net Expenses | 2,344,097 | |||

| NET INVESTMENT INCOME | 2,988,968 | |||

| NET REALIZED AND UNREALIZED GAIN (LOSS) | ||||

| Net realized gain (loss) on: | ||||

| Investments | 9,308,900 | |||

| Foreign currency transactions | (5 | ) | ||

| Net realized gain | 9,308,895 | |||

| Net change in unrealized appreciation (depreciation) on investments | 4,800,356 | |||

| NET REALIZED AND UNREALIZED GAIN | 14,109,251 | |||

| INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 17,098,219 | ||

See Notes to Financial Statements.

AUXIER FOCUS FUND

STATEMENTS OF CHANGES IN NET ASSETS

| For the Year Ended June 30, 2018 |

For the Year Ended June 30, 2017 |

|||||||||||||||

| OPERATIONS | Shares | Shares | ||||||||||||||

| Net investment income | $ | 2,988,968 | $ | 2,873,195 | ||||||||||||

| Net realized gain | 9,308,895 | 10,382,605 | ||||||||||||||

| Net change in unrealized appreciation | 4,800,356 | 20,893,874 | ||||||||||||||

| Increase in Net Assets Resulting from Operations | 17,098,219 | 34,149,674 | ||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||

| Net investment income: | ||||||||||||||||

| Investor Shares | (1,989,916 | ) | (2,228,585 | ) | ||||||||||||

| A Shares | (22,503 | ) | (18,288 | ) | ||||||||||||

| Institutional Shares | (741,116 | ) | (573,352 | ) | ||||||||||||

| Net realized gain: | ||||||||||||||||

| Investor Shares | (7,701,459 | ) | (3,141,650 | ) | ||||||||||||

| A Shares | (122,901 | ) | (41,172 | ) | ||||||||||||

| Institutional Shares | (2,835,592 | ) | (803,916 | ) | ||||||||||||

| Total Distributions to Shareholders | (13,413,487 | ) | (6,806,963 | ) | ||||||||||||

| CAPITAL SHARE TRANSACTIONS | ||||||||||||||||

| Sale of shares: | ||||||||||||||||

| Investor Shares | 12,207,193 | 545,032 | 13,833,788 | 675,235 | ||||||||||||

| A Shares | 76,206 | 3,206 | 25,047 | 1,169 | ||||||||||||

| Institutional Shares | 11,795,228 | 510,411 | 11,678,690 | 564,828 | ||||||||||||

| Reinvestment of distributions: | ||||||||||||||||

| Investor Shares | 9,332,848 | 415,331 | 5,165,360 | 255,391 | ||||||||||||

| A Shares | 140,941 | 6,189 | 59,012 | 2,879 | ||||||||||||

| Institutional Shares | 3,423,369 | 149,776 | 1,306,095 | 63,637 | ||||||||||||

| Redemption of shares: | ||||||||||||||||

| Investor Shares | (48,745,464 | ) | (2,169,226 | ) | (58,720,531 | ) | (2,840,659 | ) | ||||||||

| A Shares | (283,039 | ) | (11,944 | ) | (283,606 | ) | (13,793 | ) | ||||||||

| Institutional Shares | (3,857,324 | ) | (168,252 | ) | (2,325,115 | ) | (111,073 | ) | ||||||||

| Redemption fees: | ||||||||||||||||

| Investor Shares | 3,662 | – | 6,978 | – | ||||||||||||

| A Shares | 55 | – | 91 | – | ||||||||||||

| Institutional Shares | 1,208 | – | 1,835 | – | ||||||||||||

| Decrease in Net Assets from Capital Share Transactions | (15,905,117 | ) | (719,477 | ) | (29,252,356 | ) | (1,402,386 | ) | ||||||||

| Decrease in Net Assets | (12,220,385 | ) | (1,909,645 | ) | ||||||||||||

| NET ASSETS | ||||||||||||||||

| Beginning of Year | 247,678,240 | 249,587,885 | ||||||||||||||

| End of Year (Including line (a)) | $ | 235,457,855 | $ | 247,678,240 | ||||||||||||

| (a) Undistributed net investment income | $ | 1,556,427 | $ | 1,455,058 | ||||||||||||

See Notes to Financial Statements.

AUXIER FOCUS FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year.

| For the Years Ended June 30, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| INVESTOR SHARES | ||||||||||||||||||||

| NET ASSET VALUE, Beginning of Year | $ | 21.95 | $ | 19.69 | $ | 20.50 | $ | 20.75 | $ | 18.59 | ||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (a) | 0.26 | 0.23 | 0.21 | 0.17 | 0.20 | |||||||||||||||

| Net realized and unrealized gain | 1.28 | 2.59 | 0.08 | 0.38 | 2.63 | |||||||||||||||

| Total from Investment Operations | 1.54 | 2.82 | 0.29 | 0.55 | 2.83 | |||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||

| Net investment income | (0.25 | ) | (0.23 | ) | (0.20 | ) | (0.20 | ) | (0.22 | ) | ||||||||||

| Net realized gain | (0.99 | ) | (0.33 | ) | (0.90 | ) | (0.60 | ) | (0.45 | ) | ||||||||||

| Total Distributions to Shareholders | (1.24 | ) | (0.56 | ) | (1.10 | ) | (0.80 | ) | (0.67 | ) | ||||||||||

| REDEMPTION FEES(a) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | ||||||||||

| NET ASSET VALUE, End of Year | $ | 22.25 | $ | 21.95 | $ | 19.69 | $ | 20.50 | $ | 20.75 | ||||||||||

| TOTAL RETURN | 6.97 | % | 14.55 | % | 1.58 | % | 2.69 | % | 15.43 | % | ||||||||||

| RATIOS/SUPPLEMENTARY DATA | ||||||||||||||||||||

| Net Assets at End of Year (000s omitted) | $ | 161,032 | $ | 185,363 | $ | 203,921 | $ | 231,911 | $ | 285,094 | ||||||||||

| Ratios to Average Net Assets: | ||||||||||||||||||||

| Net investment income | 1.14 | % | 1.11 | % | 1.10 | % | 0.83 | % | 1.00 | % | ||||||||||

| Net expenses | 0.98 | % | 1.03 | % | 1.14 | % | 1.24 | % | 1.24 | % | ||||||||||

| Gross expenses (c) | 1.10 | % | 1.16 | % | 1.30 | % | 1.27 | % | 1.26 | % | ||||||||||

| PORTFOLIO TURNOVER RATE | 3 | % | 5 | % | 6 | % | 4 | % | 9 | % | ||||||||||

| (a) | Calculated based on average shares outstanding during each year. |

| (b) | Less than $0.01 per share. |

| (c) | Reflects the expense ratio excluding any waivers and/or reimbursements. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year.

| For the Years Ended June 30, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| A SHARES | ||||||||||||||||||||

| NET ASSET VALUE, Beginning of Year | $ | 22.23 | $ | 19.90 | $ | 20.64 | $ | 20.85 | $ | 18.63 | ||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (a) | 0.20 | 0.19 | 0.19 | 0.18 | 0.20 | |||||||||||||||

| Net realized and unrealized gain | 1.29 | 2.61 | 0.09 | 0.36 | 2.64 | |||||||||||||||

| Total from Investment Operations | 1.49 | 2.80 | 0.28 | 0.54 | 2.84 | |||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||

| Net investment income | (0.17 | ) | (0.14 | ) | (0.12 | ) | (0.15 | ) | (0.17 | ) | ||||||||||

| Net realized gain | (0.99 | ) | (0.33 | ) | (0.90 | ) | (0.60 | ) | (0.45 | ) | ||||||||||

| Total Distributions to Shareholders | (1.16 | ) | (0.47 | ) | (1.02 | ) | (0.75 | ) | (0.62 | ) | ||||||||||

| REDEMPTION FEES(a) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | ||||||||||

| NET ASSET VALUE, End of Year | $ | 22.56 | $ | 22.23 | $ | 19.90 | $ | 20.64 | $ | 20.85 | ||||||||||

| TOTAL RETURN(c) | 6.68 | % | 14.28 | % | 1.49 | % | 2.63 | % | 15.45 | % | ||||||||||

| RATIOS/SUPPLEMENTARY DATA | ||||||||||||||||||||

| Net Assets at End of Year (000s omitted) | $ | 2,782 | $ | 2,797 | $ | 2,698 | $ | 5,541 | $ | 5,108 | ||||||||||

| Ratios to Average Net Assets: | ||||||||||||||||||||

| Net investment income | 0.87 | % | 0.91 | % | 0.94 | % | 0.84 | % | 1.02 | % | ||||||||||

| Net expenses | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | ||||||||||

| Gross expenses (d) | 1.44 | % | 1.54 | % | 1.61 | % | 1.56 | % | 1.62 | % | ||||||||||

| PORTFOLIO TURNOVER RATE | 3 | % | 5 | % | 6 | % | 4 | % | 9 | % | ||||||||||

| (a) | Calculated based on average shares outstanding during each year. |

| (b) | Less than $0.01 per share. |

| (c) | Total Return does not include the effect of front end sales charge or contingent deferred sales charge. |

| (d) | Reflects the expense ratio excluding any waivers and/or reimbursements. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each year.

| For the Years Ended June 30, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| INSTITUTIONAL SHARES | ||||||||||||||||||||

| NET ASSET VALUE, Beginning of Year | $ | 22.29 | $ | 19.96 | $ | 20.74 | $ | 20.91 | $ | 18.66 | ||||||||||

| INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (a) | 0.31 | 0.28 | 0.25 | 0.24 | 0.25 | |||||||||||||||

| Net realized and unrealized gain | 1.30 | 2.61 | 0.08 | 0.36 | 2.64 | |||||||||||||||

| Total from Investment Operations | 1.61 | 2.89 | 0.33 | 0.60 | 2.89 | |||||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | ||||||||||||||||||||

| Net investment income | (0.25 | ) | (0.23 | ) | (0.21 | ) | (0.17 | ) | (0.19 | ) | ||||||||||

| Net realized gain | (0.99 | ) | (0.33 | ) | (0.90 | ) | (0.60 | ) | (0.45 | ) | ||||||||||

| Total Distributions to Shareholders | (1.24 | ) | (0.56 | ) | (1.11 | ) | (0.77 | ) | (0.64 | ) | ||||||||||

| REDEMPTION FEES(a) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | ||||||||||

| NET ASSET VALUE, End of Year | $ | 22.66 | $ | 22.29 | $ | 19.96 | $ | 20.74 | $ | 20.91 | ||||||||||

| TOTAL RETURN | 7.20 | % | 14.72 | % | 1.74 | % | 2.93 | % | 15.73 | % | ||||||||||

| RATIOS/SUPPLEMENTARY DATA | ||||||||||||||||||||

| Net Assets at End of Year (000s omitted) | $ | 71,644 | $ | 59,518 | $ | 42,969 | $ | 29,366 | $ | 8,001 | ||||||||||

| Ratios to Average Net Assets: | ||||||||||||||||||||

| Net investment income | 1.34 | % | 1.32 | % | 1.27 | % | 1.13 | % | 1.25 | % | ||||||||||

| Net expenses | 0.80 | % | 0.86 | % | 1.00 | % | 1.00 | % | 1.00 | % | ||||||||||

| Gross expenses (c) | 1.10 | % | 1.16 | % | 1.31 | % | 1.36 | % | 1.47 | % | ||||||||||

| PORTFOLIO TURNOVER RATE | 3 | % | 5 | % | 6 | % | 4 | % | 9 | % | ||||||||||

| (a) | Calculated based on average shares outstanding during each year. |

| (b) | Less than $0.01 per share. |

| (c) | Reflects the expense ratio excluding any waivers and/or reimbursements. |

See Notes to Financial Statements.

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2018

Note 1. Organization

The Auxier Focus Fund (the “Fund”) is a diversified portfolio of Forum Funds (the “Trust”). The Trust is a Delaware statutory trust that is registered as an open-end, management investment company under the Investment Company Act of 1940, as amended (the “Act”). Under its Trust Instrument, the Trust is authorized to issue an unlimited number of the Fund’s shares of beneficial interest without par value.

The Fund currently offers three classes of shares: Investor Shares, A Shares and Institutional Shares. A Shares are offered at net asset value plus a maximum sales charge of 5.75%. A Shares are also subject to contingent deferred sales charge (“CDSC”) of 1.00% on purchases without an initial sales charge and redeemed less than one year after they are purchased. Investor Shares and Institutional Shares are not subject to a sales charge. Investor Shares, A Shares and Institutional Shares commenced operations on July 9, 1999, July 8, 2005 and May 9, 2012, respectively. The Fund’s investment objective is to provide long-term capital appreciation.

Note 2. Summary of Significant Accounting Policies

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. These financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”), which require management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities at the date of the financial statements, and the reported amounts of increases and decreases in net assets from operations during the fiscal year. Actual amounts could differ from those estimates. The following summarizes the significant accounting policies of the Fund:

Security Valuation – Securities are valued at market prices using the last quoted trade or official closing price from the principal exchange where the security is traded, as provided by independent pricing services on each Fund business day. In the absence of a last trade, securities are valued at the mean of the last bid and ask price provided by the pricing service. Debt securities may be valued at prices supplied by a fund’s pricing agent based on broker or dealer supplied valuations or matrix pricing, a method of valuing securities by reference to the value of other securities with similar characteristics such as rating, interest rate and maturity. Shares of non-exchange traded open-end mutual funds are valued at net asset value (“NAV”). Short-term investments that mature in sixty days or less may be valued at amortized cost.

The Fund values its investments at fair value pursuant to procedures adopted by the Trust’s Board of Trustees (the “Board”) if (1) market quotations are not readily available or (2) the Adviser, as defined in Note 4, believes that the values available are unreliable. The Trust’s Valuation Committee, as defined in the Fund’s registration statement, performs certain functions as they relate to the administration and oversight of the Fund’s valuation procedures. Under these procedures, the Valuation Committee convenes on a regular and ad hoc basis to review such investments and considers a number of factors, including valuation methodologies and significant unobservable inputs, when arriving at fair value.

The Valuation Committee may work with the Adviser to provide valuation inputs. In determining fair valuations, inputs may include market-based analytics that may consider related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant investment information. Adviser inputs may include an income-based approach in which the anticipated future cash flows of the investment are discounted in determining fair value. Discounts may also be applied based on the nature or duration of any restrictions on the disposition of the investments. The Valuation Committee performs regular reviews of valuation methodologies, key inputs and assumptions, disposition analysis and market activity.

Fair valuation is based on subjective factors and, as a result, the fair value price of an investment may differ from the security’s market price and may not be the price at which the asset may be sold. Fair valuation could result in a different NAV than a NAV determined by using market quotes.

GAAP has a three-tier fair value hierarchy. The basis of the tiers is dependent upon the various “inputs” used to determine the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

Level 1 - Quoted prices in active markets for identical assets and liabilities.

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2018

Level 2 - Prices determined using significant other observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Short-term securities with maturities of sixty days or less are valued at amortized cost, which approximates market value, and are categorized as Level 2 in the hierarchy. Municipal securities, long-term U.S. government obligations and corporate debt securities are valued in accordance with the evaluated price supplied by the pricing service and generally categorized as Level 2 in the hierarchy. Other securities that are categorized as Level 2 in the hierarchy include, but are not limited to, warrants that do not trade on an exchange, securities valued at the mean between the last reported bid and ask quotation and international equity securities valued by an independent third party with adjustments for changes in value between the time of the securities respective local market closes and the close of the U.S. market.

Level 3 - Significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments).

The aggregate value by input level, as of June 30, 2018, for the Fund’s investments is included at the end of the Fund’s Schedule of Investments.

Security Transactions, Investment Income and Realized Gain and Loss – Investment transactions are accounted for on the trade date. Dividend income is recorded on the ex-dividend date. Foreign dividend income is recorded on the ex-dividend date or as soon as possible after determining the existence of a dividend declaration after exercising reasonable due diligence. Income and capital gains on some foreign securities may be subject to foreign withholding taxes, which are accrued as applicable. Interest income is recorded on an accrual basis. Premium is amortized and discount is accreted using the effective interest method. Identified cost of investments sold is used to determine the gain and loss for both financial statement and federal income tax purposes.

Foreign Currency Translations – Foreign currency amounts are translated into U.S. dollars as follows: (1) assets and liabilities at the rate of exchange at the end of the respective period; and (2) purchases and sales of securities and income and expenses at the rate of exchange prevailing on the dates of such transactions. The portion of the results of operations arising from changes in the exchange rates and the portion due to fluctuations arising from changes in the market prices of securities are not isolated. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

Distributions to Shareholders – The Fund declares any dividends from net investment income and pays them annually. Any net capital gains realized by the Fund are distributed at least annually. Distributions to shareholders are recorded on the ex-dividend date. Distributions are based on amounts calculated in accordance with applicable federal income tax regulations, which may differ from GAAP. These differences are due primarily to differing treatments of income and gain on various investment securities held by the Fund, timing differences and differing characterizations of distributions made by the Fund.

Federal Taxes – The Fund intends to continue to qualify each year as a regulated investment company under Subchapter M of Chapter 1, Subtitle A, of the Internal Revenue Code of 1986, as amended (“Code”), and to distribute all of its taxable income to shareholders. In addition, by distributing in each calendar year substantially all of its net investment income and capital gains, if any, the Fund will not be subject to a federal excise tax. Therefore, no federal income or excise tax provision is required. The Fund files a U.S. federal income and excise tax return as required. The Fund’s federal income tax returns are subject to examination by the Internal Revenue Service for a period of three fiscal years after they are filed. As of June 30, 2018, there are no uncertain tax positions that would require financial statement recognition, de-recognition or disclosure.

Income and Expense Allocation – The Trust accounts separately for the assets, liabilities and operations of each of its investment portfolios. Expenses that are directly attributable to more than one investment portfolio are allocated among the respective investment portfolios in an equitable manner.

The Fund's class-specific expenses are charged to the operations of that class of shares. Income and expenses (other than expenses attributable to a specific class) and realized and unrealized gains or losses on investments are allocated to each class of shares based on the class’ respective net assets to the total net assets of the Fund.

Redemption Fees – A shareholder who redeems or exchanges shares within 180 days of purchase will incur a redemption fee of 2.00% of the current NAV of shares redeemed or exchanged, subject to certain limitations. The fee is charged for the benefit of the remaining shareholders and will be paid to the Fund to help offset transaction costs. The fee is accounted for as an addition to paid-in capital. The Fund reserves the right to modify the terms of or terminate the fee at any time. There are limited exceptions to

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2018

the imposition of the redemption fee. Redemption fees incurred for the Fund, if any, are reflected on the Statements of Changes in Net Assets.

Commitments and Contingencies – In the normal course of business, the Fund enters into contracts that provide general indemnifications by the Fund to the counterparty to the contract. The Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote. The Fund has determined that none of these arrangements requires disclosure on the Fund’s balance sheet.

Note 3. Cash – Concentration in Uninsured Account

For cash management purposes, the Fund may concentrate cash with the Fund’s custodian. This typically results in cash balances exceeding the Federal Deposit Insurance Corporation (“FDIC”) insurance limits. As of June 30, 2018, the Fund had $5,052,232 at MUFG Union Bank, N.A. that exceeded the FDIC insurance limit.

Note 4. Fees and Expenses

Investment Adviser – Auxier Asset Management LLC (the “Adviser”) is the investment Adviser to the Fund. Pursuant to an investment advisory agreement, the Adviser receives an advisory fee, payable monthly, from the Fund at an annual rate of 0.80% of the Fund’s average daily net assets.

Distribution – Foreside Fund Services, LLC serves as the Fund’s distributor (the “Distributor”). The Distributor is not affiliated with the Adviser or Atlantic Fund Administration, LLC (d/b/a Atlantic Fund Services) (“Atlantic”) or their affiliates. The Fund has adopted a Distribution Plan (the “Plan”) for A Shares of the Fund in accordance with Rule 12b-1 of the Act. Under the Plan, the Fund pays the Distributor and/or any other entity as authorized by the Board a fee of up to 0.25% of the average daily net assets of A Shares. The Distributor has no role in determining the investment policies or which securities are to be purchased or sold by the Trust or its Funds.

For the year ended June 30, 2018, there were $1,400 in front-end sales charges assessed on the sale of A Shares and no contingent deferred sales charges were assessed on the sale of A Shares. The Distributor received $294 of the total front-end sales charges. Such amounts are set aside by the Distributor and used solely for distribution-related expenses.

Other Service Providers – Atlantic provides fund accounting, fund administration, compliance and transfer agency services to the Fund. The fees related to these services are included in Fund services fees within the Statement of Operations. Atlantic also provides certain shareholder report production and EDGAR conversion and filing services. Atlantic provides a Principal Executive Officer, a Principal Financial Officer, a Chief Compliance Officer and an Anti-Money Laundering Officer to the Fund, as well as certain additional compliance support functions.

Trustees and Officers – Through December 31, 2017, the Trust paid each Independent Trustee an annual retainer fee of $50,000 for service to the Trust ($66,000 for the Chairman), and the Audit Committee Chairman and Vice Chairman receive an additional $6,000 annually. Effective January 1, 2018, each Independent Trustee’s annual retainer is $31,000 ($41,000 for the Chairman), and the Audit Committee Chairman receives an additional $2,000 annually. The Trustees and Chairman may receive additional fees for special Board meetings. Each Trustee is also reimbursed for all reasonable out-of-pocket expenses incurred in connection with his or her duties as a Trustee, including travel and related expenses incurred in attending Board meetings. The amount of Trustees’ fees attributable to the Fund is disclosed in the Statement of Operations. Certain officers of the Trust are also officers or employees of the above named service providers, and during their terms of office received no compensation from the Fund.

Note 5. Expense Reimbursement and Fees Waived

The Adviser has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, dividend expenses on short sales, and extraordinary expenses) to 0.98%, 1.25% and 0.80% of the Investor Shares, A Shares and Institutional Shares, respectively, through at least October 31, 2018. These contractual waivers may only be raised or eliminated with consent

AUXIER FOCUS FUND

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2018

of the Board. Other fund service providers have voluntarily agreed to waive a portion of their fees. These voluntary reductions may be reduced or eliminated at any time. For the year ended June 30, 2018, the fees waived and expenses reimbursed were as follows:

| Investment Adviser Fees Waived |

Other Waivers | Total Fees Waived and Expenses Reimbursed |

||||||||

| $ | 327,675 | $ | 89,049 | $ | 416,724 | |||||

The Adviser may be reimbursed by the Fund for fees waived and expenses reimbursed by the Adviser pursuant to the Expense Cap if such payment is made within three years of the fee waiver or expense reimbursement, and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current expense cap, or (ii) the expense cap in place at the time the fees/expenses were waived/reimbursed. As of June 30, 2018, $1,079,484 is subject to recapture by the Adviser. Other Waivers are not eligible for recoupment.

Note 6. Security Transactions

The cost of purchases and proceeds from sales of investment securities (including maturities), other than short-term investments, during the year ended June 30, 2018, totaled $6,652,829 and $27,038,479.

Note 7. Federal Income Tax

As of June 30, 2018, cost for federal income tax purposes is $126,819,789 and net unrealized appreciation consists of:

| Gross Unrealized Appreciation | $ | 110,506,904 | ||

| Gross Unrealized Depreciation | (7,379,534 | ) | ||

| Net Unrealized Appreciation | $ | 103,127,370 |

Distributions paid during the fiscal years ended as noted were characterized for tax purposes as follows:

| 2018 | 2017 | |||||||

| Ordinary Income | $ | 2,986,907 | $ | 3,396,865 | ||||

| Long-Term Capital Gain | 10,426,580 | 3,410,098 | ||||||

| $ | 13,413,487 | $ | 6,806,963 | |||||

As of June 30, 2018, distributable earnings (accumulated loss) on a tax basis were as follows:

| Undistributed Ordinary Income | $ | 1,556,427 | ||

| Undistributed Long-Term Gain | 8,367,508 | |||

| Unrealized Appreciation | 103,127,370 | |||

| Total | $ | 113,051,305 |

The difference between components of distributable earnings on a tax basis and the amounts reflected in the Statement of Assets and Liabilities are primarily due to wash sales and equity return of capital.

On the Statement of Assets and Liabilities, as a result of permanent book to tax differences, certain amounts have been reclassified for the year ended June 30, 2018. The following reclassification was the result of equity return of capital distributions and foreign currency transactions and has no impact on the net assets of the Fund.

| Undistributed net investment income | $ | (134,064 | ) | |

| Accumulated net realized gain | 134,064 |

Note 8. Subsequent Events

Subsequent events occurring after the date of this report through the date these financial statements were issued have been evaluated for potential impact, and the Fund has had no such events.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Forum Funds

and the Shareholders of Auxier Focus Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Auxier Focus Fund, a series of shares of beneficial interest in Forum Funds (the “Fund”), including the schedule of investments, as of June 30, 2018, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of June 30, 2018, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund's management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of those financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of June 30, 2018 by correspondence with the custodian and brokers, or by other appropriate auditing procedures where replies from brokers were not received. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

Philadelphia, Pennsylvania

August 23, 2018

AUXIER FOCUS FUND

ADDITIONAL INFORMATION (Unaudited)

JUNE 30, 2018

Proxy Voting Information

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to securities held in the Fund’s portfolio is available, without charge and upon request, by calling (877) 328-9437 and on the SEC’s website at www.sec.gov. The Fund’s proxy voting record for the most recent twelve-month period ended June 30 is available, without charge and upon request, by calling (877) 328-9437 and on the SEC’s website at www.sec.gov.

Availability of Quarterly Portfolio Schedules

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. These filings are available, without charge and upon request on the SEC’s website at www.sec.gov or may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments on certain classes, redemption fees, exchange fees and CDSC fees, and (2) ongoing costs, including management fees, 12b-1 fees, and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund, and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2018 through June 30, 2018.

Actual Expenses – The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes – The second line under each share class of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.