Form N-CSR ALLIANCEBERNSTEIN GLOBAL For: Mar 31

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07732

ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: March 31, 2018

Date of reporting period: March 31, 2018

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

MAR 03.31.18

| Investment Products Offered | • Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed | |

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AB’s website at www.abfunds.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227 4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov. The Fund’s Forms N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC 0330.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

| FROM THE PRESIDENT |

|

Dear Shareholder,

We are pleased to provide this report for AllianceBernstein Global High Income Fund (the “Fund”). Please review the discussion of Fund performance, the market conditions during the reporting period and the Fund’s investment strategy.

As always, AB strives to keep clients ahead of what’s next by:

| + | Transforming uncommon insights into uncommon knowledge with a global research scope |

| + | Navigating markets with seasoned investment experience and sophisticated solutions |

| + | Providing thoughtful investment insights and actionable ideas |

Whether you’re an individual investor or a multi-billion-dollar institution, we put knowledge and experience to work for you.

AB’s global research organization connects and collaborates across platforms and teams to deliver impactful insights and innovative products. Better insights lead to better opportunities—anywhere in the world.

For additional information about AB’s range of products and shareholder resources, please log on to www.abfunds.com.

Thank you for your investment in the AB Mutual Funds.

Sincerely,

Robert M. Keith

President and Chief Executive Officer, AB Mutual Funds

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 1 |

ANNUAL REPORT

May 10, 2018

This report provides management’s discussion of fund performance for AllianceBernstein Global High Income Fund for the annual reporting period ended March 31, 2018. The Fund is a closed-end fund and its shares of common stock trade on the New York Stock Exchange.

The Fund seeks high current income, and secondarily, capital appreciation.

RETURNS AS OF MARCH 31, 2018 (unaudited)

| 6 Months | 12 Months | |||||||

| ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND (NAV) | -0.27% | 4.42% | ||||||

| Primary Benchmark: Bloomberg Barclays Global High Yield Index (USD hedged) |

-0.02% | 4.51% | ||||||

| Blended Benchmark: 33% JPM GBI-EM / 33% JPM EMBI Global / 33% Bloomberg Barclays US Corporate HY 2% Issuer Capped Index |

0.98% | 6.66% | ||||||

The Fund’s market price per share on March 31, 2018 was $11.89. The Fund’s NAV per share on March 31, 2018 was $13.56. For additional financial highlights, please see pages 120-121.

INVESTMENT RESULTS

The table above shows the Fund’s performance compared with its primary benchmark, the Bloomberg Barclays Global High Yield Index (USD hedged), as well as its blended benchmark for the six- and 12-month periods ended March 31, 2018. The blended benchmark is composed of equal weightings of the JPMorgan Government Bond Index-Emerging Markets (“JPM GBI-EM”, local currency-denominated), the JPMorgan Emerging Markets Bond Index Global (“JPM EMBI Global”) and the Bloomberg Barclays US Corporate High Yield (“HY”) 2% Issuer Capped Index.

During the 12-month period, the Fund underperformed its primary benchmark. Yield-curve positioning detracted from performance relative to the benchmark, primarily because of positioning along the UK yield curve, where an overweight in 10-year maturities detracted. Sector allocation was positive, as gains from the Fund’s out-of-benchmark positions in US agency risk-sharing transactions and non-agency mortgages more than offset negative returns from exposures to treasuries and commercial mortgage-backed securities (“CMBS”). Security selection also contributed, benefiting most from US high-yield corporate selections in the US and—to a lesser extent—the eurozone. Selections in emerging-market corporate bonds detracted. A long position in the Polish zloty contributed, while a short position in the Singapore dollar was negative.

During the six-month period, the Fund underperformed its primary benchmark. Yield-curve positioning detracted from performance, mostly as a

| 2 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

result of positioning along the US curve; the Fund was overweight the intermediate portion of the curve (two-, five- and 10-year maturities) where yields rose the most. Currency investments were also negative, primarily because of long positions in the Turkish lira, Norwegian krone and Mexican peso. A long position in the Polish zloty was positive. Sector allocation contributed due to the Fund’s exposure to US agency risk-sharing transactions and non-agency mortgages. Security selection also added to performance, the result of selections within investment-grade corporates and CMBS, both in the US.

During both periods the Fund utilized currency forwards and currency options, both written and purchased, to hedge currency exposure as well as to manage active currency risk. Credit default swaps, both single name and index, were used to hedge investment-grade and high-yield credit risk through cash bonds, as well as to take active credit risk. Treasury futures and interest rate swaps were used to manage duration, country exposure and yield-curve positioning. Variance swaps and swaptions were used to take active risk in an effort to add alpha (a measure of how the Fund is performing on a risk-adjusted basis versus its benchmark) by capturing risk premiums that are similar to high-yield exposure elsewhere in the Fund, while swaptions were also used to manage Fund performance versus the benchmark. Total return swaps were used to create synthetic high-yield exposure in the Fund.

MARKET REVIEW AND INVESTMENT STRATEGY

Fixed-income markets performed well over the 12-month period. Emerging-market debt rallied over the period, helped by increasing oil prices and an improving global growth story. Global high yield also performed well, followed by emerging-market local-currency government bonds, developed-market treasuries and investment-grade corporates. Within high yield, sector performance was almost uniformly positive. Transportation had the strongest absolute returns, while communications fell furthest. Outside of the eurozone, developed-market treasury yields generally flattened, with shorter maturities rising as long ends fell. Eurozone treasury yields moved in different directions.

After some initial uncertainty regarding the US government’s ability to implement meaningful changes, markets reacted with enthusiasm when the Tax Cuts and Jobs Act was passed in December. In Europe, despite some formal progress on Brexit, investor anxiety increased around a bifurcated outlook for the negotiation process. The US Federal Reserve (the “Fed”) raised interest rates in June, December and March, and began to formally reduce its balance sheet, as universally anticipated by markets. The European Central Bank confirmed that its newly reduced pace of asset purchases would continue through September 2018 and further, if necessary.

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 3 |

At the end of the reporting period, a severe spike in volatility shook a broad swath of capital markets. US yields rose dramatically, with the 10-year Treasury yield reaching a four-year peak. In the US, higher-than-expected wage gains and inflation numbers fueled concerns regarding the risk of the Fed tightening monetary policy faster than anticipated and pushed bond yields higher. Additionally, President Trump’s early-March announcement of import tariffs on Chinese steel and aluminum weighed on capital markets worldwide, as investors feared the possible onset of a global trade war. Nervous sentiment from the US reverberated across markets around the globe. Elsewhere, the Bank of England said that it too could increase rates faster than previously expected, depending on the strength of its economy.

INVESTMENT POLICIES

The Fund invests without limit in securities denominated in non-US currencies as well as those denominated in the US dollar. The Fund may also invest, without limit, in sovereign debt securities issued by emerging and developed nations and in debt securities of US and non-US corporate issuers. For more information regarding the Fund’s risks, please see “Disclosures and Risks” on pages 5-7 and “Note E—Risks Involved in Investing in the Fund” of the Notes to Financial Statements on pages 115-118.

| 4 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

DISCLOSURES AND RISKS

AllianceBernstein Global High Income Fund Shareholder Information

Weekly comparative net asset value (“NAV”) and market price information about the Fund is published each Saturday in Barron’s and in other newspapers in a table called “Closed End Funds”. Daily NAV and market price information, and additional information regarding the Fund, is available at www.abfunds.com and www.nyse.com. For additional shareholder information regarding this Fund, please see pages 125-126.

Benchmark Disclosure

All indices are unmanaged and do not reflect fees and expenses associated with the active management of a fund portfolio. The Bloomberg Barclays Global High Yield Index (USD hedged) represents non-investment grade fixed-income securities of companies in the US, and developed and emerging markets. The JPM® GBI-EM represents the performance of local currency government bonds issued by emerging markets. The JPM® EMBI Global (market-capitalization weighted) represents the performance of US dollar-denominated Brady bonds, Eurobonds and trade loans issued by sovereign and quasi-sovereign entities. The Bloomberg Barclays US Corporate HY 2% Issuer Capped Index is the 2% Issuer Capped component of the US Corporate High Yield Index, which represents the performance of fixed-income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million and at least one year to maturity. An investor cannot invest directly in an index, and its results are not indicative of the performance of any specific investment, including the Fund.

A Word About Risk

Market Risk: The value of the Fund’s assets will fluctuate as the stock or bond market fluctuates. The value of its investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events that affect large portions of the market.

Interest Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest rate risk is generally greater for fixed-income securities with longer maturities or durations.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security. The degree of risk for a particular security

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 5 |

DISCLOSURES AND RISKS (continued)

may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security.

Below Investment Grade Securities: Investments in fixed-income securities with lower ratings (commonly known as “junk bonds”) tend to have a higher probability that an issuer will default or fail to meet its payment obligations. These securities may be subject to greater price volatility due to such factors as specific corporate developments, interest rate sensitivity, negative perceptions of the junk bond market generally and less secondary market liquidity.

Inflation Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the Fund’s distributions. This risk is significantly greater if the Fund invests a significant portion of its assets in fixed-income securities with longer maturities.

Foreign (Non-US) Risk: Investments in securities of non-US issuers may involve more risk than those of US issuers. These securities may fluctuate more widely in price and may be less liquid due to adverse market, economic, political, regulatory or other factors.

Emerging-Market Risk: Investments in emerging-market countries may have more risk because the markets are less developed and less liquid as well as being subject to increased economic, political, regulatory or other uncertainties.

Currency Risk: Fluctuations in currency exchange rates may negatively affect the value of the Fund’s investments or reduce its returns.

Leverage Risk: As a result of the Fund’s use of leveraging techniques, its NAV may be more volatile because leverage tends to exaggerate the effect of changes in interest rates and any increase or decrease in the value of the Fund’s investments.

Diversification Risk: The Fund may have more risk because it is “non-diversified”, meaning that it can invest more of its assets in a smaller number of issuers and that adverse changes in the value of one security could have a more significant effect on the Fund’s NAV.

Derivatives Risk: Investments in derivatives may be illiquid, difficult to price and leveraged so that small changes may produce disproportionate losses for the Fund, and may be subject to counterparty risk to a greater degree than more traditional investments.

| 6 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

DISCLOSURES AND RISKS (continued)

Management Risk: The Fund is subject to management risk because it is an actively managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is no guarantee that its techniques will produce the intended results. The Fund may invest in mortgage-backed and/or other asset-backed securities, including securities backed by mortgages and assets with an international or emerging-markets origination and securities backed by non-performing loans at the time of investment. Investments in mortgage-backed and other asset-backed securities are subject to certain additional risks. The value of these securities may be particularly sensitive to changes in interest rates. These risks include “extension risk”, which is the risk that, in periods of rising interest rates, issuers may delay the payment of principal, and “prepayment risk”, which is the risk that, in periods of falling interest rates, issuers may pay principal sooner than expected, exposing the Fund to a lower rate of return upon reinvestment of principal. Mortgage-backed securities offered by nongovernmental issuers and other asset-backed securities may be subject to other risks, such as higher rates of default in the mortgages or assets backing the securities or risks associated with the nature and servicing of mortgages or assets backing the securities.

These risks are fully discussed in the Fund’s prospectus. As with all investments, you may lose money by investing in the Fund.

An Important Note About Historical Performance

The performance shown in this report represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. All fees and expenses related to the operation of the Fund have been deducted. Performance assumes reinvestment of distributions and does not account for taxes.

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 7 |

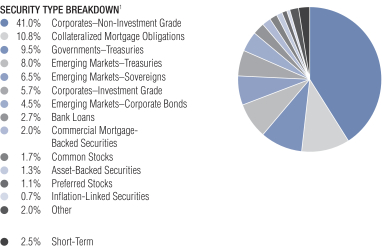

PORTFOLIO SUMMARY

March 31, 2018 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $1,169.2

| 1 | All data are as of March 31, 2018. The Fund’s security type breakdown is expressed as a percentage of total investments and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Portfolio of Investments” section of the report for additional details). “Other” security type weightings represent 0.5% or less in the following security types: Collateralized Loan Obligations, Governments–Sovereign Bonds, Local Governments–Regional Bonds, Local Governments–US Municipal Bonds, Options Purchased–Puts, Quasi-Sovereigns, Warrants and Whole Loan Trusts. |

| 8 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

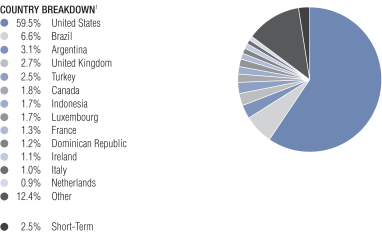

PORTFOLIO SUMMARY (continued)

March 31, 2018 (unaudited)

| 1 | All data are as of March 31, 2018. The Fund’s country breakdown is expressed as a percentage of total investments and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Portfolio of Investments” section of the report for additional details). “Other” country weightings represent 0.8% or less in the following countries: Angola, Australia, Bahrain, Belarus, Cameroon, Cayman Islands, Chile, China, Colombia, Costa Rica, Denmark, Ecuador, Egypt, El Salvador, Finland, Gabon, Germany, Guatemala, Honduras, Hong Kong, India, Iraq, Israel, Ivory Coast, Jamaica, Jersey (Channel Islands), Jordan, Kenya, Macau, Malaysia, Mexico, Mongolia, Nigeria, Norway, Pakistan, Peru, Russia, Senegal, Serbia, South Africa, Spain, Sri Lanka, Sweden, Switzerland, Trinidad & Tobago, Ukraine, United Arab Emirates, Uruguay, Venezuela and Zambia. |

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 9 |

PORTFOLIO OF INVESTMENTS

March 31, 2018

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| CORPORATES – NON-INVESTMENT GRADE – 43.8% |

||||||||||||

| Industrial – 34.5% |

||||||||||||

| Basic – 3.9% |

||||||||||||

| AK Steel Corp. |

U.S.$ | 1,164 | $ | 1,140,987 | ||||||||

| 7.625%, 10/01/21 |

278 | 285,476 | ||||||||||

| Aleris International, Inc. |

517 | 509,523 | ||||||||||

| ArcelorMittal |

734 | 847,060 | ||||||||||

| 7.25%, 10/15/39 |

1,938 | 2,291,759 | ||||||||||

| Ashland LLC |

501 | 508,573 | ||||||||||

| Axalta Coating Systems LLC |

516 | 517,788 | ||||||||||

| Berry Global, Inc. |

409 | 419,712 | ||||||||||

| CF Industries, Inc. |

595 | 519,687 | ||||||||||

| 5.375%, 3/15/44 |

545 | 495,593 | ||||||||||

| Cleveland-Cliffs, Inc. |

1,628 | 1,555,557 | ||||||||||

| Constellium NV |

400 | 393,740 | ||||||||||

| 5.875%, 2/15/26(a) |

1,310 | 1,299,948 | ||||||||||

| Crown Americas LLC/Crown Americas Capital Corp. VI |

815 | 786,687 | ||||||||||

| ERP Iron Ore, LLC |

382 | 381,853 | ||||||||||

| Freeport-McMoRan, Inc. |

3,414 | 3,157,977 | ||||||||||

| 6.75%, 2/01/22(b) |

1,197 | 1,237,399 | ||||||||||

| Grinding Media, Inc./Moly-Cop AltaSteel Ltd. |

1,296 | 1,363,734 | ||||||||||

| INEOS Finance PLC |

EUR | 790 | 993,267 | |||||||||

| Joseph T Ryerson & Son, Inc. |

U.S.$ | 3,215 | 3,545,267 | |||||||||

| Lecta SA |

EUR | 227 | 288,031 | |||||||||

| Lundin Mining Corp. |

U.S.$ | 837 | 884,902 | |||||||||

| Magnetation LLC/Mag Finance Corp. |

2,857 | 29 | ||||||||||

| 10 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Momentive Performance Materials, Inc. |

U.S.$ | 3,472 | $ | 3,629,830 | ||||||||

| 8.875%, 10/15/20(c)(d)(i)(j) |

3,472 | – 0 | – | |||||||||

| Multi-Color Corp. |

980 | 920,221 | ||||||||||

| NOVA Chemicals Corp. |

207 | 208,186 | ||||||||||

| Novelis Corp. |

1,573 | 1,547,124 | ||||||||||

| Pactiv LLC |

1,110 | 1,237,650 | ||||||||||

| Peabody Energy Corp. |

4,310 | – 0 | – | |||||||||

| 6.00%, 3/31/22(a) |

295 | 302,184 | ||||||||||

| 6.375%, 3/31/25(a) |

400 | 417,018 | ||||||||||

| Plastipak Holdings, Inc. |

774 | 772,866 | ||||||||||

| PQ Corp. |

277 | 274,920 | ||||||||||

| Reynolds Group Issuer, Inc./Reynolds Group Issuer LLC/Reynolds Group Issuer Lu |

781 | 788,384 | ||||||||||

| Sealed Air Corp. |

1,295 | 1,450,625 | ||||||||||

| SIG Combibloc Holdings SCA |

EUR | 682 | 872,059 | |||||||||

| Smurfit Kappa Acquisitions ULC |

U.S.$ | 2,064 | 2,067,164 | |||||||||

| Smurfit Kappa Treasury Funding Ltd. |

238 | 285,926 | ||||||||||

| SPCM SA |

975 | 947,136 | ||||||||||

| Teck Resources Ltd. |

2,374 | 2,222,235 | ||||||||||

| 5.40%, 2/01/43 |

1,454 | 1,393,829 | ||||||||||

| 6.00%, 8/15/40 |

470 | 486,690 | ||||||||||

| 6.25%, 7/15/41 |

238 | 252,806 | ||||||||||

| United States Steel Corp. |

295 | 295,290 | ||||||||||

| 6.875%, 8/15/25(b) |

775 | 797,217 | ||||||||||

| Valvoline, Inc. |

278 | 285,061 | ||||||||||

| W.R. Grace & Co.-Conn |

386 | 397,084 | ||||||||||

|

|

|

|||||||||||

| 45,276,054 | ||||||||||||

|

|

|

|||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 11 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Capital Goods – 1.7% |

||||||||||||

| ARD Finance SA |

EUR | 1,126 | $ | 1,462,110 | ||||||||

| ARD Securities Finance SARL |

U.S.$ | 279 | 293,888 | |||||||||

| Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc. |

EUR | 2,004 | 2,678,373 | |||||||||

| B456 Systems, Inc. |

U.S.$ | 955 | 74,013 | |||||||||

| Bombardier, Inc. |

975 | 965,163 | ||||||||||

| 6.00%, 10/15/22(a) |

261 | 258,357 | ||||||||||

| 6.125%, 1/15/23(a) |

738 | 736,037 | ||||||||||

| 7.50%, 3/15/25(a) |

1,124 | 1,154,326 | ||||||||||

| BWAY Holding Co. |

1,073 | 1,079,273 | ||||||||||

| Cleaver-Brooks, Inc. |

505 | 524,252 | ||||||||||

| Energizer Holdings, Inc. |

1,311 | 1,321,321 | ||||||||||

| EnPro Industries, Inc. |

970 | 1,003,137 | ||||||||||

| Gates Global LLC/Gates Global Co. |

352 | 357,741 | ||||||||||

| GFL Environmental, Inc. |

497 | 498,997 | ||||||||||

| 9.875%, 2/01/21(a) |

852 | 898,562 | ||||||||||

| Jeld-Wen, Inc. |

128 | 122,096 | ||||||||||

| 4.875%, 12/15/27(a) |

182 | 171,357 | ||||||||||

| KLX, Inc. |

877 | 903,769 | ||||||||||

| Liberty Tire Recycling LLC |

536 | 535,781 | ||||||||||

| Textron Financial Corp. |

575 | 525,011 | ||||||||||

| TransDigm, Inc. |

2,335 | 2,354,964 | ||||||||||

| 6.50%, 7/15/24 |

1,572 | 1,610,811 | ||||||||||

| Waste Pro USA, Inc. |

762 | 752,426 | ||||||||||

|

|

|

|||||||||||

| 20,281,765 | ||||||||||||

|

|

|

|||||||||||

| 12 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Communications - Media – 4.9% |

||||||||||||

| Altice Financing SA |

U.S.$ | 2,892 | $ | 2,861,724 | ||||||||

| 7.50%, 5/15/26(a) |

1,782 | 1,748,812 | ||||||||||

| Altice France SA |

EUR | 264 | 330,930 | |||||||||

| 5.625%, 5/15/24(a) |

386 | 482,078 | ||||||||||

| 6.00%, 5/15/22(a) |

U.S.$ | 707 | 689,553 | |||||||||

| 6.25%, 5/15/24(a) |

200 | 188,137 | ||||||||||

| Altice France SA/France |

2,923 | 2,782,468 | ||||||||||

| Altice Luxembourg SA |

EUR | 1,332 | 1,593,888 | |||||||||

| 7.75%, 5/15/22(a)(b) |

U.S.$ | 1,770 | 1,646,100 | |||||||||

| CCO Holdings LLC/CCO Holdings Capital Corp. |

160 | 151,663 | ||||||||||

| 5.375%, 5/01/25(a) |

128 | 126,148 | ||||||||||

| 5.75%, 1/15/24 |

166 | 168,802 | ||||||||||

| 5.75%, 2/15/26(a) |

400 | 397,931 | ||||||||||

| 5.875%, 5/01/27(a) |

499 | 498,075 | ||||||||||

| Cequel Communications Holdings I LLC/Cequel Capital Corp. |

298 | 303,286 | ||||||||||

| 7.50%, 4/01/28(a) |

1,192 | 1,222,030 | ||||||||||

| 7.75%, 7/15/25(a) |

861 | 912,371 | ||||||||||

| Clear Channel Worldwide Holdings, Inc. |

555 | 565,441 | ||||||||||

| Series B |

2,654 | 2,705,737 | ||||||||||

| CSC Holdings LLC |

1,302 | 1,230,390 | ||||||||||

| 6.625%, 10/15/25(a) |

274 | 282,562 | ||||||||||

| 10.125%, 1/15/23(a) |

765 | 849,150 | ||||||||||

| DISH DBS Corp. |

100 | 90,061 | ||||||||||

| 5.875%, 11/15/24(b) |

2,345 | 2,093,761 | ||||||||||

| 6.75%, 6/01/21 |

820 | 826,553 | ||||||||||

| 7.75%, 7/01/26 |

160 | 150,012 | ||||||||||

| Gray Television, Inc. |

1,037 | 1,006,567 | ||||||||||

| iHeartCommunications, Inc. |

2,016 | 373,908 | ||||||||||

| 9.00%, 12/15/19(g)(i) |

927 | 731,474 | ||||||||||

| 10.625%, 3/15/23(g)(i) |

142 | 112,042 | ||||||||||

| 11.25%, 3/01/21(a)(g)(i) |

254 | 199,159 | ||||||||||

| 11.25%, 3/01/21(g)(i) |

535 | 421,103 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 13 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Liberty Interactive LLC |

U.S.$ | 880 | $ | 602,966 | ||||||

| McClatchy Co. (The) |

958 | 997,261 | ||||||||

| McGraw-Hill Global Education Holdings LLC/McGraw-Hill Global Education Finance |

1,216 | 1,161,162 | ||||||||

| Mediacom Broadband LLC/Mediacom Broadband Corp. |

2,168 | 2,237,116 | ||||||||

| Meredith Corp. |

1,627 | 1,669,318 | ||||||||

| Netflix, Inc. |

1,552 | 1,466,938 | ||||||||

| 4.875%, 4/15/28(a) |

1,221 | 1,172,664 | ||||||||

| Outfront Media Capital LLC/Outfront Media Capital Corp. |

648 | 659,802 | ||||||||

| Radiate Holdco LLC/Radiate Finance, Inc. |

1,057 | 977,952 | ||||||||

| 6.875%, 2/15/23(a) |

451 | 435,232 | ||||||||

| Sinclair Television Group, Inc. |

1,487 | 1,526,034 | ||||||||

| TEGNA, Inc. |

284 | 286,882 | ||||||||

| 5.50%, 9/15/24(a) |

162 | 165,377 | ||||||||

| 6.375%, 10/15/23 |

718 | 746,091 | ||||||||

| Townsquare Media, Inc. |

1,781 | 1,678,826 | ||||||||

| Unitymedia Hessen GmbH & Co. KG/Unitymedia NRW GmbH |

1,078 | 1,098,428 | ||||||||

| 6.25%, 1/15/29(a) |

EUR | 496 | 687,002 | |||||||

| Univision Communications, Inc. |

U.S.$ | 1,064 | 991,299 | |||||||

| UPC Holding BV |

2,223 | 2,054,763 | ||||||||

| Urban One, Inc. |

1,400 | 1,386,000 | ||||||||

| 9.25%, 2/15/20(a)(b) |

1,451 | 1,407,470 | ||||||||

| Virgin Media Finance PLC |

1,347 | 1,337,377 | ||||||||

| 5.25%, 2/15/22 |

900 | 889,738 | ||||||||

| Virgin Media Receivables Financing Notes I DAC |

GBP | 128 | 176,042 | |||||||

| 14 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Virgin Media Secured Finance PLC |

GBP | 423 | $ | 607,494 | ||||||||

| Ziggo Bond Co. BV |

EUR | 968 | 1,287,599 | |||||||||

| Ziggo Bond Finance BV |

U.S.$ | 1,034 | 977,181 | |||||||||

| 6.00%, 1/15/27(a) |

150 | 139,987 | ||||||||||

| Ziggo Secured Finance BV |

1,163 | 1,091,710 | ||||||||||

|

|

|

|||||||||||

| 57,657,627 | ||||||||||||

|

|

|

|||||||||||

| Communications - Telecommunications – 2.6% |

||||||||||||

| Arqiva Broadcast Finance PLC |

GBP | 1,086 | 1,604,365 | |||||||||

| C&W Senior Financing DAC |

U.S.$ | 847 | 848,920 | |||||||||

| CenturyLink, Inc. |

314 | 305,455 | ||||||||||

| Cincinnati Bell, Inc. |

1,151 | 1,035,945 | ||||||||||

| Clear Channel Communications, Inc. |

607 | 1,092 | ||||||||||

| Embarq Corp. |

928 | 874,515 | ||||||||||

| Frontier Communications Corp. |

45 | 26,648 | ||||||||||

| 7.125%, 1/15/23 |

662 | 447,531 | ||||||||||

| 7.625%, 4/15/24 |

1,118 | 698,408 | ||||||||||

| 7.875%, 1/15/27 |

834 | 442,052 | ||||||||||

| Hughes Satellite Systems Corp. |

1,437 | 1,541,678 | ||||||||||

| Intelsat Jackson Holdings SA |

||||||||||||

| 5.50%, 8/01/23 |

1,675 | 1,348,375 | ||||||||||

| 7.25%, 10/15/20 |

443 | 409,740 | ||||||||||

| 7.50%, 4/01/21 |

980 | 880,760 | ||||||||||

| 8.00%, 2/15/24(a) |

216 | 226,560 | ||||||||||

| 9.50%, 9/30/22(a) |

516 | 588,541 | ||||||||||

| 9.75%, 7/15/25(a) |

1,262 | 1,176,950 | ||||||||||

| Iridium Communications, Inc. |

484 | 498,784 | ||||||||||

| Level 3 Financing, Inc. |

86 | 81,135 | ||||||||||

| 5.375%, 8/15/22-1/15/24 |

1,278 | 1,256,060 | ||||||||||

| 6.125%, 1/15/21 |

596 | 603,681 | ||||||||||

| Level 3 Parent LLC |

160 | 159,873 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 15 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Qwest Corp. |

U.S.$ | 1,335 | $ | 1,269,154 | ||||||||

| Sable International Finance Ltd. |

454 | 479,673 | ||||||||||

| Sprint Capital Corp. |

||||||||||||

| 6.875%, 11/15/28 |

1,210 | 1,130,547 | ||||||||||

| 8.75%, 3/15/32 |

215 | 224,922 | ||||||||||

| Sprint Corp. |

707 | 721,589 | ||||||||||

| T-Mobile USA, Inc. |

743 | 772,649 | ||||||||||

| 6.375%, 3/01/25 |

655 | 687,183 | ||||||||||

| 6.836%, 4/28/23 |

543 | 562,684 | ||||||||||

| Telecom Italia Capital SA |

483 | 570,264 | ||||||||||

| 7.721%, 6/04/38 |

1,759 | 2,159,714 | ||||||||||

| Telecom Italia SpA/Milano |

1,002 | 1,025,875 | ||||||||||

| Uniti Group LP/Uniti Group Finance, Inc./CSL Capital LLC |

1,113 | 1,070,713 | ||||||||||

| Wind Tre SpA |

1,600 | 1,357,056 | ||||||||||

| Windstream Services LLC/Windstream Finance Corp. |

232 | 133,349 | ||||||||||

| 8.75%, 12/15/24(a) |

1,526 | 905,049 | ||||||||||

| Zayo Group LLC/Zayo Capital, Inc. |

300 | 293,245 | ||||||||||

| 6.00%, 4/01/23 |

488 | 501,491 | ||||||||||

| 6.375%, 5/15/25 |

1,187 | 1,228,571 | ||||||||||

|

|

|

|||||||||||

| 30,150,796 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - |

||||||||||||

| Adient Global Holdings Ltd. |

1,323 | 1,249,994 | ||||||||||

| BCD Acquisition, Inc. |

2,264 | 2,445,657 | ||||||||||

| Cooper-Standard Automotive, Inc. |

1,101 | 1,098,319 | ||||||||||

| Dana Financing Luxembourg SARL |

215 | 218,257 | ||||||||||

| 6.50%, 6/01/26(a) |

602 | 626,080 | ||||||||||

| Exide Technologies |

162 | 102,264 | ||||||||||

| 11.00% (11.00% Cash or 4.125% PIK), 4/30/22(a)(c)(f)(j) |

4,154 | 3,717,857 | ||||||||||

| 16 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Series AI |

U.S.$ | 4,406 | $ | 2,775,896 | ||||||||

| Goodyear Tire & Rubber Co. (The) |

400 | 434,106 | ||||||||||

| IHO Verwaltungs GmbH |

889 | 874,093 | ||||||||||

| Meritor, Inc. |

305 | 316,094 | ||||||||||

| Navistar International Corp. |

1,190 | 1,190,714 | ||||||||||

| Titan International, Inc. |

1,093 | 1,124,495 | ||||||||||

|

|

|

|||||||||||

| 16,173,826 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Entertainment – 0.4% |

||||||||||||

| AMC Entertainment Holdings, Inc. |

1,580 | 1,555,820 | ||||||||||

| Silversea Cruise Finance Ltd. |

1,409 | 1,494,457 | ||||||||||

| VOC Escrow Ltd. |

1,076 | 1,022,039 | ||||||||||

|

|

|

|||||||||||

| 4,072,316 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Other – 2.2% |

||||||||||||

| Beazer Homes USA, Inc. |

682 | 631,495 | ||||||||||

| 6.75%, 3/15/25(b) |

1,400 | 1,392,990 | ||||||||||

| 8.75%, 3/15/22 |

99 | 106,619 | ||||||||||

| Caesars Entertainment Corp. |

121 | 207,191 | ||||||||||

| Cirsa Funding Luxembourg SA |

EUR | 396 | 502,002 | |||||||||

| Cooperativa Muratori & Cementisti-CMC di Ravenna SC |

276 | 323,616 | ||||||||||

| Diamond Resorts International, Inc. |

U.S.$ | 1,139 | 1,238,745 | |||||||||

| Five Point Operating Co. LP/Five Point Capital Corp. |

1,304 | 1,304,987 | ||||||||||

| GLP Capital LP/GLP Financing II, Inc. |

674 | 686,453 | ||||||||||

| International Game Technology PLC |

977 | 1,023,537 | ||||||||||

| James Hardie International Finance DAC |

285 | 279,619 | ||||||||||

| 5.00%, 1/15/28(a) |

273 | 265,334 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 17 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| K. Hovnanian Enterprises, Inc. |

U.S.$ | 2,257 | $ | 2,040,646 | ||||||||

| 10.00%, 7/15/22(a) |

389 | 413,343 | ||||||||||

| 10.50%, 7/15/24(a) |

389 | 403,297 | ||||||||||

| KB Home |

536 | 575,888 | ||||||||||

| 7.50%, 9/15/22 |

494 | 542,337 | ||||||||||

| Lennar Corp. |

1,332 | 1,403,556 | ||||||||||

| MDC Holdings, Inc. |

150 | 152,395 | ||||||||||

| 6.00%, 1/15/43 |

2,908 | 2,713,481 | ||||||||||

| Pinnacle Entertainment, Inc. |

829 | 868,641 | ||||||||||

| PulteGroup, Inc. |

115 | 112,178 | ||||||||||

| 6.00%, 2/15/35 |

500 | 505,194 | ||||||||||

| 7.875%, 6/15/32 |

1,400 | 1,655,655 | ||||||||||

| Shea Homes LP/Shea Homes Funding Corp. |

420 | 423,458 | ||||||||||

| 6.125%, 4/01/25(a) |

830 | 836,541 | ||||||||||

| Standard Industries, Inc./NJ |

977 | 1,003,868 | ||||||||||

| Sugarhouse HSP Gaming Prop Mezz LP/Sugarhouse HSP Gaming Finance Corp. |

1,785 | 1,704,652 | ||||||||||

| Taylor Morrison Communities, Inc./Taylor Morrison Holdings II, Inc. |

875 | 894,688 | ||||||||||

| Toll Brothers Finance Corp. |

1,124 | 1,099,717 | ||||||||||

| Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp. |

785 | 785,739 | ||||||||||

|

|

|

|||||||||||

| 26,097,862 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Restaurants – 0.1% |

||||||||||||

| Golden Nugget, Inc. |

933 | 937,779 | ||||||||||

| IRB Holding Corp. |

453 | 444,420 | ||||||||||

|

|

|

|||||||||||

| 1,382,199 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical - Retailers – 1.0% |

||||||||||||

| Dufry Finance SCA |

EUR | 1,208 | 1,548,470 | |||||||||

| 18 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| FirstCash, Inc. |

U.S.$ | 1,312 | $ | 1,333,655 | ||||||||

| JC Penney Corp., Inc. |

421 | 265,410 | ||||||||||

| 7.40%, 4/01/37 |

600 | 405,008 | ||||||||||

| L Brands, Inc. |

917 | 860,897 | ||||||||||

| 6.875%, 11/01/35 |

230 | 222,697 | ||||||||||

| 6.95%, 3/01/33 |

500 | 483,786 | ||||||||||

| 7.60%, 7/15/37 |

1,000 | 997,159 | ||||||||||

| Levi Strauss & Co. |

1,150 | 1,162,613 | ||||||||||

| Neiman Marcus Group Ltd. LLC |

2,115 | 1,338,309 | ||||||||||

| 8.75% (8.75% Cash or 9.50% PIK), 10/15/21(a)(f) |

404 | 257,735 | ||||||||||

| Penske Automotive Group, Inc. |

1,037 | 1,018,935 | ||||||||||

| PetSmart, Inc. |

1,140 | 647,749 | ||||||||||

| Sonic Automotive, Inc. |

534 | 510,937 | ||||||||||

| 6.125%, 3/15/27 |

817 | 790,100 | ||||||||||

|

|

|

|||||||||||

| 11,843,460 | ||||||||||||

|

|

|

|||||||||||

| Consumer Non-Cyclical – 3.9% |

||||||||||||

| Acadia Healthcare Co., Inc. |

684 | 712,784 | ||||||||||

| Air Medical Group Holdings, Inc. |

820 | 779,225 | ||||||||||

| Albertsons Cos. LLC/Safeway, Inc./New Albertson’s, Inc./Albertson’s LLC |

274 | 233,770 | ||||||||||

| 6.625%, 6/15/24(b) |

1,712 | 1,535,287 | ||||||||||

| Aveta, Inc. |

13,116 | – 0 | – | |||||||||

| BI-LO LLC/BI-LO Finance Corp. |

1,983 | 1,128,360 | ||||||||||

| 9.25%, 2/15/19(a)(c)(g)(i) |

1,553 | 1,556,268 | ||||||||||

| Catalent Pharma Solutions, Inc. |

EUR | 400 | 514,637 | |||||||||

| 4.875%, 1/15/26(a) |

U.S.$ | 416 | 405,378 | |||||||||

| Charles River Laboratories International, Inc. |

242 | 245,792 | ||||||||||

| CHS/Community Health Systems, Inc. |

2,543 | 1,471,761 | ||||||||||

| 7.125%, 7/15/20(b) |

828 | 675,624 | ||||||||||

| 8.00%, 11/15/19(b) |

408 | 367,390 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 19 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| DaVita, Inc. |

U.S.$ | 1,314 | $ | 1,270,512 | ||||||

| Diamond BC BV |

EUR | 362 | 426,830 | |||||||

| Eagle Holding Co. II LLC |

U.S.$ | 179 | 180,593 | |||||||

| Endo Dac/Endo Finance LLC/Endo Finco, Inc. |

4,260 | 3,150,500 | ||||||||

| Endo Finance LLC |

1,228 | 1,011,434 | ||||||||

| Endo Finance LLC/Endo Finco, Inc. |

200 | 151,109 | ||||||||

| Envision Healthcare Corp. |

1,009 | 1,013,998 | ||||||||

| 6.25%, 12/01/24(a) |

694 | 716,555 | ||||||||

| First Quality Finance Co., Inc. |

3,247 | 3,230,765 | ||||||||

| HCA, Inc. |

1,475 | 1,490,712 | ||||||||

| 4.50%, 2/15/27 |

135 | 130,373 | ||||||||

| 5.00%, 3/15/24 |

400 | 404,320 | ||||||||

| 5.25%, 6/15/26 |

235 | 237,932 | ||||||||

| 5.875%, 2/15/26 |

180 | 183,234 | ||||||||

| Kinetic Concepts, Inc./KCI USA, Inc. |

506 | 521,516 | ||||||||

| Lamb Weston Holdings, Inc. |

439 | 435,615 | ||||||||

| LifePoint Health, Inc. |

1,518 | 1,483,845 | ||||||||

| 5.875%, 12/01/23(b) |

1,448 | 1,460,544 | ||||||||

| Mallinckrodt International Finance SA |

2,770 | 2,141,362 | ||||||||

| Mallinckrodt International Finance SA/Mallinckrodt CB LLC |

772 | 597,848 | ||||||||

| 5.625%, 10/15/23(a) |

394 | 319,832 | ||||||||

| 5.75%, 8/01/22(a) |

1,281 | 1,111,296 | ||||||||

| MEDNAX, Inc. |

422 | 424,983 | ||||||||

| MPH Acquisition Holdings LLC |

1,563 | 1,615,509 | ||||||||

| Post Holdings, Inc. |

442 | 417,446 | ||||||||

| 5.50%, 3/01/25(a) |

642 | 638,355 | ||||||||

| 5.625%, 1/15/28(a) |

830 | 793,684 | ||||||||

| 5.75%, 3/01/27(a) |

90 | 89,344 | ||||||||

| 20 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Spectrum Brands, Inc. |

EUR | 530 | $ | 681,772 | ||||||||

| 6.125%, 12/15/24 |

U.S.$ | 361 | 374,541 | |||||||||

| 6.625%, 11/15/22 |

560 | 579,808 | ||||||||||

| Synlab Unsecured Bondco PLC |

EUR | 700 | 921,142 | |||||||||

| Tenet Healthcare Corp. |

U.S.$ | 95 | 98,285 | |||||||||

| 6.75%, 6/15/23(b) |

1,308 | 1,282,958 | ||||||||||

| 6.875%, 11/15/31 |

239 | 217,490 | ||||||||||

| 8.125%, 4/01/22 |

752 | 784,109 | ||||||||||

| Valeant Pharmaceuticals International |

34 | 34,077 | ||||||||||

| 7.25%, 7/15/22(a) |

635 | 636,967 | ||||||||||

| Valeant Pharmaceuticals International, Inc. |

230 | 201,700 | ||||||||||

| 5.625%, 12/01/21(a) |

26 | 24,855 | ||||||||||

| 5.875%, 5/15/23(a) |

1,146 | 1,014,210 | ||||||||||

| 6.50%, 3/15/22(a) |

287 | 296,598 | ||||||||||

| 7.50%, 7/15/21(a) |

1,146 | 1,153,408 | ||||||||||

| Vizient, Inc. |

774 | 857,635 | ||||||||||

| Voyage Care BondCo PLC |

GBP | 891 | 1,255,511 | |||||||||

|

|

|

|||||||||||

| 45,691,388 | ||||||||||||

|

|

|

|||||||||||

| Energy – 7.3% |

||||||||||||

| Alta Mesa Holdings LP/Alta Mesa Finance Services Corp. |

U.S.$ | 897 | 937,085 | |||||||||

| Antero Resources Corp. |

789 | 796,224 | ||||||||||

| Berry Petroleum Co. LLC |

2,383 | – 0 | – | |||||||||

| 7.00%, 2/15/26(a) |

580 | 584,654 | ||||||||||

| Bill Barrett Corp. |

534 | 539,854 | ||||||||||

| 8.75%, 6/15/25 |

637 | 688,249 | ||||||||||

| Bristow Group, Inc. |

1,000 | 1,010,159 | ||||||||||

| California Resources Corp. |

299 | 230,471 | ||||||||||

| 6.00%, 11/15/24 |

232 | 141,748 | ||||||||||

| 8.00%, 12/15/22(a) |

3,539 | 2,774,410 | ||||||||||

| Carrizo Oil & Gas, Inc. |

642 | 643,943 | ||||||||||

| 7.50%, 9/15/20 |

54 | 54,894 | ||||||||||

| 8.25%, 7/15/25 |

301 | 316,161 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 21 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Cheniere Corpus Christi Holdings LLC |

U.S.$ | 783 | $ | 865,776 | ||||||

| Cheniere Energy Partners LP |

1,055 | 1,040,477 | ||||||||

| Cheniere Energy, Inc. |

1,064 | 1,054,520 | ||||||||

| Chesapeake Energy Corp. |

1,528 | 1,425,830 | ||||||||

| 5.75%, 3/15/23 |

610 | 550,061 | ||||||||

| 6.125%, 2/15/21 |

335 | 336,827 | ||||||||

| 8.00%, 1/15/25-6/15/27(a) |

851 | 815,560 | ||||||||

| Continental Resources, Inc./OK |

96 | 92,564 | ||||||||

| 4.90%, 6/01/44 |

212 | 202,912 | ||||||||

| 5.00%, 9/15/22 |

1,119 | 1,137,312 | ||||||||

| Denbury Resources, Inc. |

134 | 168,148 | ||||||||

| 9.25%, 3/31/22(a) |

604 | 616,609 | ||||||||

| Diamond Offshore Drilling, Inc. |

2,575 | 2,586,459 | ||||||||

| Energy Transfer Equity LP |

2,203 | 2,135,284 | ||||||||

| 7.50%, 10/15/20 |

309 | 332,287 | ||||||||

| Ensco PLC |

290 | 231,251 | ||||||||

| 5.20%, 3/15/25 |

1,066 | 860,788 | ||||||||

| 7.75%, 2/01/26 |

970 | 888,250 | ||||||||

| EP Energy LLC/Everest Acquisition Finance, Inc. |

467 | 246,572 | ||||||||

| 7.75%, 9/01/22 |

1,366 | 902,243 | ||||||||

| 8.00%, 2/15/25(a) |

1,792 | 1,196,466 | ||||||||

| 9.375%, 5/01/20 |

538 | 501,667 | ||||||||

| 9.375%, 5/01/24(a) |

1,076 | 764,324 | ||||||||

| Genesis Energy LP/Genesis Energy Finance Corp. |

412 | 391,777 | ||||||||

| 6.25%, 5/15/26 |

1,327 | 1,266,421 | ||||||||

| 6.50%, 10/01/25(c) |

481 | 473,132 | ||||||||

| 6.75%, 8/01/22 |

173 | 178,150 | ||||||||

| Gulfport Energy Corp. |

515 | 489,168 | ||||||||

| 6.375%, 5/15/25(b) |

1,054 | 1,013,679 | ||||||||

| 6.375%, 1/15/26 |

1,718 | 1,653,635 | ||||||||

| Hess Infrastructure Partners LP/Hess Infrastructure Partners Finance Corp. |

1,587 | 1,563,625 | ||||||||

| 22 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Hilcorp Energy I LP/Hilcorp Finance Co. |

U.S.$ | 593 | $ | 584,091 | ||||||

| 5.75%, 10/01/25(a) |

1,610 | 1,592,841 | ||||||||

| Indigo Natural Resources LLC |

1,095 | 1,040,309 | ||||||||

| Laredo Petroleum, Inc. |

787 | 789,224 | ||||||||

| Murphy Oil Corp. |

852 | 891,408 | ||||||||

| Murphy Oil USA, Inc. |

69 | 69,517 | ||||||||

| 6.00%, 8/15/23 |

716 | 737,842 | ||||||||

| Nabors Industries, Inc. |

996 | 961,090 | ||||||||

| 5.50%, 1/15/23 |

1,784 | 1,740,123 | ||||||||

| 5.75%, 2/01/25(a) |

470 | 442,314 | ||||||||

| Noble Holding International Ltd. |

191 | 119,112 | ||||||||

| 6.20%, 8/01/40 |

276 | 182,840 | ||||||||

| 7.75%, 1/15/24 |

2,261 | 2,097,077 | ||||||||

| 7.95%, 4/01/25 |

375 | 329,533 | ||||||||

| Oasis Petroleum, Inc. |

226 | 229,563 | ||||||||

| 6.875%, 3/15/22 |

376 | 381,709 | ||||||||

| Parkland Fuel Corp. |

1,147 | 1,151,158 | ||||||||

| PDC Energy, Inc. |

1,447 | 1,425,298 | ||||||||

| 6.125%, 9/15/24 |

490 | 500,577 | ||||||||

| PHI, Inc. |

1,567 | 1,531,742 | ||||||||

| Precision Drilling Corp. |

787 | 784,182 | ||||||||

| QEP Resources, Inc. |

1,248 | 1,202,479 | ||||||||

| 5.625%, 3/01/26 |

31 | 29,298 | ||||||||

| 6.875%, 3/01/21(b) |

1,225 | 1,290,226 | ||||||||

| Range Resources Corp. |

948 | 878,494 | ||||||||

| 5.00%, 8/15/22 |

396 | 383,438 | ||||||||

| 5.00%, 3/15/23(b) |

995 | 954,236 | ||||||||

| 5.875%, 7/01/22 |

97 | 97,399 | ||||||||

| Rowan Cos., Inc. |

536 | 377,580 | ||||||||

| 7.375%, 6/15/25(b) |

1,285 | 1,203,636 | ||||||||

| Sanchez Energy Corp. |

3,602 | 2,628,037 | ||||||||

| 7.25%, 2/15/23(a) |

790 | 798,184 | ||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 23 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| SandRidge Energy, Inc. |

U.S.$ | 865 | $ | – 0 | – | |||||

| 8.125%, 10/15/22(c)(d)(e)(i) |

2,076 | – 0 | – | |||||||

| Seitel, Inc. |

597 | 597,000 | ||||||||

| SemGroup Corp. |

594 | 567,323 | ||||||||

| 7.25%, 3/15/26 |

540 | 539,071 | ||||||||

| SemGroup Corp./Rose Rock Finance Corp. |

438 | 414,080 | ||||||||

| SM Energy Co. |

1,341 | 1,246,442 | ||||||||

| 5.625%, 6/01/25(b) |

1,150 | 1,089,480 | ||||||||

| 6.50%, 1/01/23 |

1,000 | 995,811 | ||||||||

| Southern Star Central Corp. |

1,200 | 1,223,498 | ||||||||

| SRC Energy, Inc. |

800 | 805,913 | ||||||||

| Sunoco LP/Sunoco Finance Corp. |

1,355 | 1,307,465 | ||||||||

| 5.875%, 3/15/28(a) |

1,026 | 997,897 | ||||||||

| Targa Resources Partners LP/Targa Resources Partners Finance Corp. |

215 | 213,656 | ||||||||

| Transocean Phoenix 2 Ltd. |

1,094 | 1,170,207 | ||||||||

| Transocean, Inc. |

1,252 | 1,205,119 | ||||||||

| 6.80%, 3/15/38 |

2,543 | 1,992,207 | ||||||||

| 7.50%, 1/15/26(a) |

791 | 778,700 | ||||||||

| 9.00%, 7/15/23(a) |

712 | 756,961 | ||||||||

| Vantage Drilling International |

1,283 | – 0 | – | |||||||

| 7.50%, 11/01/19(c)(d)(e)(i) |

2,176 | – 0 | – | |||||||

| 10.00%, 12/31/20(c)(e) |

105 | 102,900 | ||||||||

| 10.00%, 12/31/20(c)(h) |

87 | 85,260 | ||||||||

| Vine Oil & Gas LP/Vine Oil & Gas Finance Corp. |

1,741 | 1,633,147 | ||||||||

| Weatherford International LLC |

614 | 552,279 | ||||||||

| Weatherford International Ltd. |

154 | 137,640 | ||||||||

| 6.50%, 8/01/36 |

752 | 538,585 | ||||||||

| 6.75%, 9/15/40 |

849 | 618,532 | ||||||||

| 7.00%, 3/15/38 |

409 | 299,316 | ||||||||

| 24 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| 7.75%, 6/15/21 |

U.S.$ | 297 | $ | 280,114 | ||||||||

| 9.875%, 2/15/24(b) |

901 | 821,121 | ||||||||||

| Whiting Petroleum Corp. |

542 | 510,150 | ||||||||||

| 5.75%, 3/15/21 |

211 | 213,197 | ||||||||||

| 6.25%, 4/01/23 |

483 | 487,889 | ||||||||||

| 6.625%, 1/15/26(a) |

771 | 776,994 | ||||||||||

| WPX Energy, Inc. |

187 | 209,988 | ||||||||||

|

|

|

|||||||||||

| 85,292,125 | ||||||||||||

|

|

|

|||||||||||

| Other Industrial – 0.7% |

||||||||||||

| Algeco Global Finance PLC |

956 | 958,385 | ||||||||||

| American Tire Distributors, Inc. |

1,793 | 1,825,536 | ||||||||||

| Global Partners LP/GLP Finance Corp. |

2,976 | 2,963,328 | ||||||||||

| H&E Equipment Services, Inc. |

437 | 441,370 | ||||||||||

| KAR Auction Services, Inc. |

458 | 455,891 | ||||||||||

| Laureate Education, Inc. |

1,085 | 1,163,526 | ||||||||||

|

|

|

|||||||||||

| 7,808,036 | ||||||||||||

|

|

|

|||||||||||

| Services – 1.5% |

||||||||||||

| APTIM Corp. |

1,311 | 1,139,150 | ||||||||||

| APX Group, Inc. |

1,746 | 1,816,767 | ||||||||||

| 8.75%, 12/01/20 |

1,328 | 1,334,785 | ||||||||||

| Aramark Services, Inc. |

686 | 670,780 | ||||||||||

| 5.125%, 1/15/24 |

274 | 279,480 | ||||||||||

| Carlson Travel, Inc. |

1,128 | 1,125,185 | ||||||||||

| eDreams ODIGEO SA |

EUR | 1,560 | 2,033,204 | |||||||||

| Gartner, Inc. |

U.S.$ | 482 | 481,570 | |||||||||

| GEO Group, Inc. (The) |

162 | 160,258 | ||||||||||

| 5.875%, 1/15/22-10/15/24 |

670 | 683,744 | ||||||||||

| 6.00%, 4/15/26 |

677 | 663,467 | ||||||||||

| Monitronics International, Inc. |

807 | 618,946 | ||||||||||

| Nielsen Finance LLC/Nielsen Finance Co. |

599 | 598,902 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 25 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Prime Security Services Borrower LLC/Prime Finance, Inc. |

U.S.$ | 2,327 | $ | 2,520,774 | ||||||||

| Ritchie Bros Auctioneers, Inc. |

366 | 366,281 | ||||||||||

| Sabre GLBL, Inc. |

607 | 613,798 | ||||||||||

| 5.375%, 4/15/23(a) |

720 | 726,287 | ||||||||||

| Service Corp. International/US |

1,209 | 1,389,922 | ||||||||||

| Team Health Holdings, Inc. |

861 | 738,924 | ||||||||||

|

|

|

|||||||||||

| 17,962,224 | ||||||||||||

|

|

|

|||||||||||

| Technology – 1.6% |

||||||||||||

| Amkor Technology, Inc. |

2,681 | 2,741,784 | ||||||||||

| Ascend Learning LLC |

302 | 310,305 | ||||||||||

| BMC Software Finance, Inc. |

1,649 | 1,644,284 | ||||||||||

| Boxer Parent Co., Inc. |

411 | 410,444 | ||||||||||

| Conduent Finance, Inc./Conduent Business Services LLC |

1,610 | 1,895,123 | ||||||||||

| CURO Financial Technologies Corp. |

819 | 906,356 | ||||||||||

| Dell International LLC/EMC Corp. |

251 | 268,160 | ||||||||||

| Dell, Inc. |

1,671 | 1,664,102 | ||||||||||

| Goodman Networks, Inc. |

664 | 425,154 | ||||||||||

| Infor Software Parent LLC/Infor Software Parent, Inc. |

160 | 161,610 | ||||||||||

| Infor US, Inc. |

1,286 | 1,307,561 | ||||||||||

| Micron Technology, Inc. |

686 | 712,455 | ||||||||||

| Nokia Oyj |

527 | 561,884 | ||||||||||

| Quintiles IMS, Inc. |

EUR | 782 | 965,454 | |||||||||

| 26 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Solera LLC/Solera Finance, Inc. |

U.S.$ | 2,005 | $ | 2,230,430 | ||||||||

| Veritas US, Inc./Veritas Bermuda Ltd. |

1,462 | 1,369,632 | ||||||||||

| Western Digital Corp. |

1,087 | 1,085,800 | ||||||||||

|

|

|

|||||||||||

| 18,660,538 | ||||||||||||

|

|

|

|||||||||||

| Transportation - Airlines – 0.1% |

||||||||||||

| UAL Pass-Through Trust |

1,017 | 1,067,422 | ||||||||||

|

|

|

|||||||||||

| Transportation - Services – 1.2% |

||||||||||||

| Avis Budget Car Rental LLC/Avis Budget Finance, Inc. |

264 | 252,400 | ||||||||||

| 5.50%, 4/01/23 |

524 | 521,650 | ||||||||||

| CEVA Group PLC |

1,836 | 1,808,460 | ||||||||||

| Europcar Groupe SA |

EUR | 670 | 853,928 | |||||||||

| Herc Rentals, Inc. |

U.S.$ | 1,521 | 1,647,094 | |||||||||

| Hertz Corp. (The) |

2,807 | 2,384,067 | ||||||||||

| 5.875%, 10/15/20 |

1,419 | 1,408,166 | ||||||||||

| Hertz Holdings Netherlands BV |

EUR | 1,117 | 1,373,703 | |||||||||

| Loxam SAS |

186 | 237,051 | ||||||||||

| 4.25%, 4/15/24(a) |

138 | 178,938 | ||||||||||

| United Rentals North America, Inc. |

U.S.$ | 477 | 482,707 | |||||||||

| 5.75%, 11/15/24 |

1,005 | 1,045,823 | ||||||||||

| XPO CNW, Inc. |

1,371 | 1,427,395 | ||||||||||

| XPO Logistics, Inc. |

522 | 538,159 | ||||||||||

|

|

|

|||||||||||

| 14,159,541 | ||||||||||||

|

|

|

|||||||||||

| 403,577,179 | ||||||||||||

|

|

|

|||||||||||

| Financial Institutions – 7.8% |

||||||||||||

| Banking – 5.2% |

||||||||||||

| Allied Irish Banks PLC |

EUR | 871 | 1,198,777 | |||||||||

| Ally Financial, Inc. |

U.S.$ | 2,251 | 2,750,074 | |||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 27 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Banco Bilbao Vizcaya Argentaria SA |

EUR | 1,200 | $ | 1,602,264 | ||||||

| 6.125%, 11/16/27(b)(m) |

U.S.$ | 800 | 777,036 | |||||||

| 6.75%, 2/18/20(a)(m) |

EUR | 800 | 1,065,463 | |||||||

| 8.875%, 4/14/21(a)(m) |

1,000 | 1,457,100 | ||||||||

| Banco Santander SA |

1,200 | 1,597,739 | ||||||||

| 6.75%, 4/25/22(a)(m) |

900 | 1,247,215 | ||||||||

| Bank of America Corp. |

U.S.$ | 3,194 | 3,215,071 | |||||||

| Bank of Ireland |

EUR | 1,455 | 1,982,836 | |||||||

| Barclays Bank PLC |

U.S.$ | 166 | 194,939 | |||||||

| 7.70%, 4/25/18(a)(m) |

1,815 | 1,819,886 | ||||||||

| Barclays PLC |

GBP | 219 | 328,322 | |||||||

| 8.00%, 12/15/20(m) |

EUR | 1,732 | 2,424,299 | |||||||

| CIT Group, Inc. |

U.S.$ | 588 | 612,812 | |||||||

| Citigroup, Inc. |

2,689 | 2,762,746 | ||||||||

| Credit Agricole SA |

GBP | 1,000 | 1,518,749 | |||||||

| 8.125%, 12/23/25(a)(m) |

U.S.$ | 1,909 | 2,174,544 | |||||||

| Credit Suisse Group AG |

1,404 | 1,437,283 | ||||||||

| 7.50%, 12/11/23(a)(m) |

3,043 | 3,290,244 | ||||||||

| Goldman Sachs Group, Inc. (The) |

1,599 | 1,551,598 | ||||||||

| Intesa Sanpaolo SpA |

EUR | 331 | 438,352 | |||||||

| 5.71%, 1/15/26(a) |

U.S.$ | 1,232 | 1,237,373 | |||||||

| 7.75%, 1/11/27(a)(m) |

EUR | 1,366 | 2,052,010 | |||||||

| Lloyds Banking Group PLC |

U.S.$ | 235 | 259,315 | |||||||

| 6.657%, 5/21/37(a)(m) |

98 | 109,118 | ||||||||

| 7.50%, 6/27/24(m) |

528 | 571,691 | ||||||||

| 7.625%, 6/27/23(a)(m) |

GBP | 1,760 | 2,757,413 | |||||||

| Macquarie Bank Ltd./London |

U.S.$ | 200 | 195,710 | |||||||

| Royal Bank of Scotland Group PLC |

EUR | 150 | 183,067 | |||||||

| 8.625%, 8/15/21(m) |

U.S.$ | 3,518 | 3,841,403 | |||||||

| 28 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Series U |

U.S.$ | 1,100 | $ | 1,112,816 | ||||||||

| SNS Bank NV |

EUR | 620 | 8,839 | |||||||||

| Societe Generale SA |

U.S.$ | 1,485 | 1,577,812 | |||||||||

| 7.875%, 12/18/23(a) |

778 | 843,157 | ||||||||||

| 8.00%, 9/29/25(a)(b)(m) |

1,124 | 1,254,665 | ||||||||||

| Standard Chartered PLC |

1,269 | 1,344,131 | ||||||||||

| 7.75%, 4/02/23(a)(m) |

440 | 470,458 | ||||||||||

| SunTrust Banks, Inc. |

853 | 848,052 | ||||||||||

| Series H |

1,016 | 971,346 | ||||||||||

| UBS Group AG |

200 | 209,788 | ||||||||||

| 7.00%, 2/19/25(a)(m) |

2,492 | 2,680,796 | ||||||||||

| UniCredit SpA |

EUR | 1,554 | 2,289,447 | |||||||||

| Zions Bancorporation |

U.S.$ | 508 | 515,304 | |||||||||

|

|

|

|||||||||||

| 60,781,060 | ||||||||||||

|

|

|

|||||||||||

| Brokerage – 0.1% |

||||||||||||

| Lehman Brothers Holdings, Inc. |

1,690 | 70,135 | ||||||||||

| LPL Holdings, Inc. |

1,517 | 1,498,144 | ||||||||||

|

|

|

|||||||||||

| 1,568,279 | ||||||||||||

|

|

|

|||||||||||

| Finance – 1.1% |

||||||||||||

| Enova International, Inc. |

770 | 812,350 | ||||||||||

| 9.75%, 6/01/21 |

960 | 1,012,091 | ||||||||||

| goeasy Ltd. |

466 | 499,249 | ||||||||||

| ILFC E-Capital Trust II |

2,000 | 1,953,754 | ||||||||||

| Lincoln Finance Ltd. |

EUR | 1,139 | 1,450,534 | |||||||||

| Navient Corp. |

U.S.$ | 2,496 | 2,528,318 | |||||||||

| 5.875%, 3/25/21 |

324 | 331,523 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 29 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| 6.50%, 6/15/22 |

U.S.$ | 406 | $ | 419,695 | ||||||||

| 6.625%, 7/26/21 |

231 | 240,002 | ||||||||||

| 7.25%, 1/25/22 |

377 | 399,167 | ||||||||||

| 8.00%, 3/25/20 |

233 | 247,736 | ||||||||||

| SLM Corp. |

605 | 606,473 | ||||||||||

| TMX Finance LLC/TitleMax Finance Corp. |

1,801 | 1,722,275 | ||||||||||

|

|

|

|||||||||||

| 12,223,167 | ||||||||||||

|

|

|

|||||||||||

| Insurance – 0.6% |

||||||||||||

| Ambac Assurance Corp. |

20 | 26,193 | ||||||||||

| Galaxy Bidco Ltd. |

GBP | 133 | 186,143 | |||||||||

| Genworth Holdings, Inc. |

U.S.$ | 240 | 110,256 | |||||||||

| 7.625%, 9/24/21 |

1,616 | 1,548,795 | ||||||||||

| Liberty Mutual Group, Inc. |

2,559 | 3,177,541 | ||||||||||

| Polaris Intermediate Corp. |

2,108 | 2,151,441 | ||||||||||

|

|

|

|||||||||||

| 7,200,369 | ||||||||||||

|

|

|

|||||||||||

| Other Finance – 0.6% |

||||||||||||

| Creditcorp |

1,300 | 1,215,500 | ||||||||||

| Intrum Justitia AB |

EUR | 977 | 1,175,425 | |||||||||

| 3.125%, 7/15/24(a)(b) |

489 | 582,135 | ||||||||||

| LHC3 PLC |

239 | 296,033 | ||||||||||

| NVA Holdings, Inc. |

U.S.$ | 599 | 603,667 | |||||||||

| Oxford Finance LLC/Oxford Finance Co-Issuer II, Inc. |

199 | 203,310 | ||||||||||

| Tempo Acquisition LLC/Tempo Acquisition Finance Corp. |

1,680 | 1,677,248 | ||||||||||

| Travelport Corporate Finance PLC |

595 | 597,348 | ||||||||||

|

|

|

|||||||||||

| 6,350,666 | ||||||||||||

|

|

|

|||||||||||

| REITS – 0.2% |

||||||||||||

| Iron Mountain, Inc. |

1,640 | 1,543,650 | ||||||||||

| 30 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| MPT Operating Partnership LP/MPT Finance Corp. |

U.S.$ | 218 | $ | 213,532 | ||||||||

| 5.25%, 8/01/26 |

155 | 154,404 | ||||||||||

| 5.50%, 5/01/24 |

264 | 269,020 | ||||||||||

|

|

|

|||||||||||

| 2,180,606 | ||||||||||||

|

|

|

|||||||||||

| 90,304,147 | ||||||||||||

|

|

|

|||||||||||

| Utility – 1.5% |

||||||||||||

| Electric – 1.4% |

||||||||||||

| AES Corp./VA |

1,013 | 1,028,502 | ||||||||||

| Calpine Corp. |

1,918 | 1,841,288 | ||||||||||

| 5.50%, 2/01/24 |

1,205 | 1,099,588 | ||||||||||

| 5.75%, 1/15/25 |

168 | 153,691 | ||||||||||

| ContourGlobal Power Holdings SA |

EUR | 1,501 | 1,901,574 | |||||||||

| DPL, Inc. |

U.S.$ | 343 | 356,658 | |||||||||

| Dynegy, Inc. |

1,604 | 1,689,676 | ||||||||||

| 7.625%, 11/01/24 |

981 | 1,060,423 | ||||||||||

| NRG Energy, Inc. |

740 | 726,053 | ||||||||||

| 7.25%, 5/15/26 |

1,791 | 1,897,373 | ||||||||||

| NRG Yield Operating LLC |

843 | 845,719 | ||||||||||

| Talen Energy Supply LLC |

1,945 | 1,682,279 | ||||||||||

| 6.50%, 6/01/25 |

794 | 559,437 | ||||||||||

| 10.50%, 1/15/26(a) |

1,489 | 1,280,721 | ||||||||||

| Texas Competitive/TCEH |

626 | – 0 | – | |||||||||

|

|

|

|||||||||||

| 16,122,982 | ||||||||||||

|

|

|

|||||||||||

| Natural Gas – 0.1% |

||||||||||||

| NGL Energy Partners LP/NGL Energy Finance Corp. |

1,691 | 1,694,122 | ||||||||||

|

|

|

|||||||||||

| 17,817,104 | ||||||||||||

|

|

|

|||||||||||

| Total Corporates – Non-Investment Grade |

511,698,430 | |||||||||||

|

|

|

|||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 31 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS – 11.5% |

||||||||||||

| Risk Share Floating Rate – 9.4% |

||||||||||||

| Bellemeade Re II Ltd. |

U.S.$ | 283 | $ | 300,461 | ||||||||

| Series 2016-1A, Class M2B |

1,986 | 2,022,526 | ||||||||||

| Bellemeade Re Ltd. |

586 | 594,127 | ||||||||||

| Federal Home Loan Mortgage Corp. Structured Agency Credit Risk Debt Notes |

2,350 | 2,859,424 | ||||||||||

| Series 2013-DN2, Class M2 |

1,911 | 2,126,525 | ||||||||||

| Series 2014-DN1, Class M3 |

1,939 | 2,252,782 | ||||||||||

| Series 2014-DN2, Class M3 |

514 | 575,397 | ||||||||||

| Series 2014-DN3, Class M3 |

712 | 777,379 | ||||||||||

| Series 2014-DN4, Class M3 |

422 | 470,802 | ||||||||||

| Series 2014-HQ1, Class M3 |

1,686 | 1,883,757 | ||||||||||

| Series 2014-HQ2, Class M3 |

3,710 | 4,286,366 | ||||||||||

| Series 2014-HQ3, Class M3 |

4,905 | 5,468,727 | ||||||||||

| Series 2015-DN1, Class B |

2,230 | 3,219,613 | ||||||||||

| 32 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Series 2015-DN1, Class M3 |

U.S.$ | 1,588 | $ | 1,713,568 | ||||||

| Series 2015-DNA1, Class B |

598 | 806,493 | ||||||||

| Series 2015-DNA1, Class M3 |

480 | 534,326 | ||||||||

| Series 2015-DNA2, Class B |

1,461 | 1,806,165 | ||||||||

| Series 2015-DNA3, Class B |

1,030 | 1,369,174 | ||||||||

| Series 2015-HQ1, Class B |

3,902 | 5,341,176 | ||||||||

| Series 2015-HQ1, Class M3 |

530 | 572,114 | ||||||||

| Series 2015-HQA1, Class B |

1,013 | 1,275,720 | ||||||||

| Series 2015-HQA1, Class M3 |

1,455 | 1,668,880 | ||||||||

| Series 2016-DNA2, Class B |

862 | 1,191,793 | ||||||||

| Series 2016-DNA2, Class M3 |

811 | 931,023 | ||||||||

| Series 2016-DNA3, Class B |

2,780 | 3,924,155 | ||||||||

| Series 2016-DNA3, Class M3 |

1,113 | 1,296,340 | ||||||||

| Series 2016-DNA4, Class B |

396 | 481,713 | ||||||||

| Series 2016-HQA2, Class B |

423 | 586,541 | ||||||||

| Series 2017-DNA2, Class B1 |

415 | 467,953 | ||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 33 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Series 2017-DNA2, Class M2 |

U.S.$ | 599 | $ | 650,929 | ||||||

| Series 2017-DNA3, Class B1 |

615 | 656,918 | ||||||||

| Federal National Mortgage Association Connecticut Avenue Securities |

1,451 | 1,688,718 | ||||||||

| Series 2014-C01, Class M2 |

3,991 | 4,556,371 | ||||||||

| Series 2014-C03, Class 1M2 |

1,100 | 1,176,575 | ||||||||

| Series 2014-C04, Class 1M2 |

2,883 | 3,300,069 | ||||||||

| Series 2015-C01, Class 1M2 |

2,863 | 3,153,303 | ||||||||

| Series 2015-C01, Class 2M2 |

1,370 | 1,486,616 | ||||||||

| Series 2015-C02, Class 1M2 |

846 | 928,178 | ||||||||

| Series 2015-C02, Class 2M2 |

2,393 | 2,582,641 | ||||||||

| Series 2015-C03, Class 1M2 |

2,611 | 2,970,758 | ||||||||

| Series 2015-C03, Class 2M2 |

2,288 | 2,558,441 | ||||||||

| Series 2015-C04, Class 1M2 |

3,012 | 3,493,603 | ||||||||

| Series 2015-C04, Class 2M2 |

1,135 | 1,278,923 | ||||||||

| Series 2016-C01, Class 1B |

684 | 1,009,804 | ||||||||

| 34 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||

|

|

||||||||||

| Series 2016-C01, Class 1M2 |

U.S.$ | 2,077 | $ | 2,510,987 | ||||||

| Series 2016-C01, Class 2M2 |

761 | 915,485 | ||||||||

| Series 2016-C02, Class 1B |

450 | 673,491 | ||||||||

| Series 2016-C02, Class 1M2 |

2,375 | 2,842,996 | ||||||||

| Series 2016-C03, Class 1B |

374 | 546,664 | ||||||||

| Series 2016-C03, Class 2B |

634 | 945,070 | ||||||||

| Series 2016-C03, Class 2M2 |

3,707 | 4,353,999 | ||||||||

| Series 2016-C04, Class 1B |

1,493 | 2,034,704 | ||||||||

| Series 2016-C05, Class 2B |

1,823 | 2,449,830 | ||||||||

| Series 2016-C05, Class 2M2 |

1,486 | 1,661,397 | ||||||||

| Series 2016-C06, Class 1B |

1,288 | 1,645,510 | ||||||||

| Series 2016-C07, Class 2B |

1,561 | 2,035,416 | ||||||||

| Series 2016-C07, Class 2M2 |

918 | 1,019,435 | ||||||||

| Series 2017-C01, Class 1B1 |

148 | 172,834 | ||||||||

| Series 2017-C02, Class 2M2 |

1,152 | 1,250,396 | ||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 35 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| JP Morgan Madison Avenue Securities Trust |

U.S.$ | 1,431 | $ | 1,601,020 | ||||||||

| Wells Fargo Credit Risk Transfer Securities Trust |

616 | 721,761 | ||||||||||

|

|

|

|||||||||||

| 109,677,862 | ||||||||||||

|

|

|

|||||||||||

| Non-Agency Fixed Rate – 1.1% |

||||||||||||

| Alternative Loan Trust |

898 | 778,825 | ||||||||||

| Series 2006-42, Class 1A6 |

742 | 625,679 | ||||||||||

| Series 2006-HY12, Class A5 |

1,529 | 1,565,348 | ||||||||||

| Series 2006-J1, Class 1A10 |

1,310 | 1,195,760 | ||||||||||

| Series 2006-J5, Class 1A1 |

954 | 782,190 | ||||||||||

| Series 2007-13, Class A2 |

1,184 | 1,019,093 | ||||||||||

| Bear Stearns ARM Trust |

244 | 234,533 | ||||||||||

| Series 2007-4, Class 22A1 |

898 | 883,221 | ||||||||||

| BNPP Mortgage Securities LLC Trust |

809 | 652,601 | ||||||||||

| ChaseFlex Trust |

583 | 445,765 | ||||||||||

| Citigroup Mortgage Loan Trust |

189 | 183,218 | ||||||||||

| Series 2010-3, Class 2A2 |

391 | 334,218 | ||||||||||

| CitiMortgage Alternative Loan Trust |

1,045 | 981,904 | ||||||||||

| 36 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Countrywide Home Loan Mortgage Pass-Through Trust |

U.S.$ | 297 | $ | 277,796 | ||||||||

| Credit Suisse Mortgage Trust |

117 | 94,134 | ||||||||||

| CSMC Mortgage-Backed Trust |

378 | 312,586 | ||||||||||

| Residential Accredit Loans, Inc. Trust |

543 | 519,208 | ||||||||||

| Residential Asset Securitization Trust |

214 | 187,667 | ||||||||||

| Washington Mutual Mortgage Pass-Through Certificates Trust |

1,649 | 833,081 | ||||||||||

| Wells Fargo Mortgage Backed Securities Trust |

1,338 | 1,299,146 | ||||||||||

|

|

|

|||||||||||

| 13,205,973 | ||||||||||||

|

|

|

|||||||||||

| Non-Agency Floating Rate – 1.0% |

||||||||||||

| Alternative Loan Trust |

2,831 | 1,322,808 | ||||||||||

| Citigroup Mortgage Loan Trust |

483 | 20,927 | ||||||||||

| Countrywide Home Loan Mortgage Pass-Through Trust |

631 | 462,085 | ||||||||||

| First Horizon Alternative Mortgage Securities Trust |

126 | 16,530 | ||||||||||

| Series 2007-FA2, Class 1A10 |

372 | 208,058 | ||||||||||

| abfunds.com | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | 37 |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Lehman XS Trust |

U.S.$ | 403 | $ | 68,090 | ||||||||

| Residential Accredit Loans, Inc. Trust |

4,444 | 786,464 | ||||||||||

| Structured Asset Mortgage Investments II Trust |

1,685 | 1,583,370 | ||||||||||

| Wachovia Mortgage Loan Trust Series |

10,897 | 7,685,993 | ||||||||||

|

|

|

|||||||||||

| 12,154,325 | ||||||||||||

|

|

|

|||||||||||

| Total Collateralized Mortgage Obligations |

135,038,160 | |||||||||||

|

|

|

|||||||||||

| GOVERNMENTS – TREASURIES – 10.1% |

||||||||||||

| Colombia – 0.4% |

|

|||||||||||

| Colombian TES |

COP | 3,621,500 | 1,357,928 | |||||||||

| 10.00%, 7/24/24 |

8,000,000 | 3,436,342 | ||||||||||

|

|

|

|||||||||||

| 4,794,270 | ||||||||||||

|

|

|

|||||||||||

| Indonesia – 1.2% |

||||||||||||

| Indonesia Treasury Bond |

IDR | 15,727,000 | 1,214,009 | |||||||||

| Series FR56 |

58,563,000 | 4,717,368 | ||||||||||

| Series FR59 |

70,459,000 | 5,202,221 | ||||||||||

| Series FR73 |

37,753,000 | 3,107,622 | ||||||||||

|

|

|

|||||||||||

| 14,241,220 | ||||||||||||

|

|

|

|||||||||||

| Malaysia – 0.5% |

||||||||||||

| Malaysia Government Bond |

MYR | 23,700 | 6,136,983 | |||||||||

|

|

|

|||||||||||

| 6,136,983 | ||||||||||||

|

|

|

|||||||||||

| 38 | ALLIANCEBERNSTEIN GLOBAL HIGH INCOME FUND | abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

| Principal Amount (000) |

U.S. $ Value | |||||||||||

|

|

||||||||||||

| Russia – 0.9% |

||||||||||||

| Russian Federal Bond – OFZ |

RUB | 37,074 | $ | 675,991 | ||||||||

| Series 6212 |

185,020 | 3,253,526 | ||||||||||

| Series 6217 |

360,108 | 6,492,033 | ||||||||||

|

|

|

|||||||||||

| 10,421,550 | ||||||||||||

|

|

|

|||||||||||

| United States – 7.0% |

||||||||||||

| U.S. Treasury Bonds |

U.S.$ | 2,600 | 2,509,812 | |||||||||

| 4.50%, 2/15/36(o) |

2,400 | 2,965,500 | ||||||||||

| 5.00%, 5/15/37(o)(p) |

3,500 | 4,613,437 | ||||||||||

| 5.25%, 2/15/29(o) |

5,350 | 6,595,547 | ||||||||||

| 6.125%, 11/15/27(o) |

1,900 | 2,442,688 | ||||||||||

| 6.25%, 5/15/30(o) |

7,800 | 10,582,407 | ||||||||||

| 8.125%, 5/15/21(o) |

5,250 | 6,147,422 | ||||||||||

| U.S. Treasury Notes |

42,074 | 41,521,779 | ||||||||||

| 2.25%, 2/15/27(b)(o) |

3,873 | 3,722,921 | ||||||||||

|

|

|

|||||||||||

| 81,101,513 | ||||||||||||

|

|

|

|||||||||||

| Uruguay – 0.1% |

||||||||||||

| Uruguay Government International Bond |

UYU | 23,821 | 771,611 | |||||||||

| 9.875%, 6/20/22(a) |

18,660 | 665,340 | ||||||||||

|

|

|

|||||||||||

| 1,436,951 | ||||||||||||

|

|

|

|||||||||||

| Total Governments – Treasuries |

118,132,487 | |||||||||||

|

|

|

|||||||||||

| EMERGING MARKETS – TREASURIES – 8.6% |

||||||||||||

| Argentina – 1.2% |