Form 6-K EMERA INC For: Apr 13

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of April, 2018

Commission File Number: 000-54516

Emera Incorporated

(Exact name of registrant as specified in its charter)

1223 Lower Water Street

Halifax NS B3J 3S8

Canada

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ☐ Form 40-F ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ☐

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| EMERA INCORPORATED | ||||||

| Date: April 13, 2017 | By: | /s/ Stephen D. Aftanas | ||||

| Name: Stephen D. Aftanas | ||||||

| Title: Corporate Secretary | ||||||

EXHIBIT INDEX

| Exhibit No. |

Description | |

| 99.1 |

Emera Form of Proxy relating to Emera’s May 24, 2018 shareholders meeting. | |

| 99.2 |

Voting Instruction Form (VIF) relating to Emera’s May 24, 2018 shareholder meeting. | |

| 99.3 |

Notice of Meeting relating to Emera’s May 24, 2018 shareholder meeting. | |

| 99.4 |

Emera 2017 Annual Report | |

Exhibit 99.1

|

|

|

Form of Proxy - Emera Inc.

Annual Shareholders Meeting of May 24, 2018

Appointment of Proxyholder

I/We, being holder(s) of Emera Inc. (the “Company”) common shares, hereby appoint: M. Jacqueline Sheppard, or failing her, Scott C. Balfour, or failing him, Stephen D. Aftanas, OR

|

|

[Print the name of the person you are appointing if this person is someone other than the individuals listed above]

as proxy of the undersigned, to attend, act and vote on behalf of the undersigned in accordance with the below direction (or if no directions have been given, as the proxy sees fit) on all of the following matters and any other matter that may properly come before the Annual Meeting of Shareholders of the Company to be held at 2:00 p.m. Eastern Time on Thursday, May 24, 2018, in the Glenn Gould Studio, CBC Building, 250 Front Street West, Toronto, Ontario, Canada (the “Meeting”), and at any and all adjournments or postponements thereof in the same manner, to the same extent and with the same powers as if the undersigned were personally present, with full power of substitution.

Management recommends voting FOR Resolutions 1, 2, 3, and 4. Please use a dark black pencil or pen.

| 1. |

Election of Directors | FOR | WITHHOLD | FOR | WITHHOLD | |||||||

| 01. Scott C. Balfour |

☐ | ☐ | 07. B. Lynn Loewen |

☐ | ☐ | |||||||

| 02. Sylvia D. Chrominska |

☐ | ☐ | 08. Donald A. Pether |

☐ | ☐ | |||||||

| 03. Henry E. Demone |

☐ | ☐ | 09. John B. Ramil |

☐ | ☐ | |||||||

| 04. Allan L. Edgeworth |

☐ | ☐ | 10. Andrea S. Rosen |

☐ | ☐ | |||||||

| 05. James D. Eisenhauer |

☐ | ☐ | 11. Richard P. Sergel |

☐ | ☐ | |||||||

| 06. Kent M. Harvey |

☐ | ☐ | 12. M. Jacqueline Sheppard |

☐ | ☐ | |||||||

| 2. | Appointment of Auditors | FOR | WITHHOLD | |||||||||

| Appointment of Ernst & Young LLP as auditors |

☐ | ☐ | ||||||||||

| 3. | Auditors Fee | FOR | AGAINST | |||||||||

| Authorize Directors to establish the auditors’ fee as required pursuant to the Nova Scotia Companies Act |

☐ | ☐ | ||||||||||

| 4. | Advisory Vote on Executive Compensation | FOR | AGAINST | |||||||||

| Consider and approve, on an advisory basis, a resolution on Emera’s approach to executive compensation as disclosed in the Management Information Circular |

☐ | ☐ | ||||||||||

I/We authorize you to act in accordance with my/our instructions set out above. I/We hereby revoke any proxy previously given with respect to the Meeting.

If no voting instructions are indicated above, this Proxy will be voted FOR a matter by Management’s appointees or, if you appoint another proxyholder, as that other proxyholder sees fit. On any amendments or variations proposed or any new business properly submitted before the Meeting, I/We authorize you to vote as you see fit.

|

|

| |||

| Signature(s) |

Date |

Please sign exactly as your name(s) appear on this proxy. Please see reverse for instructions. All proxies must be received by 5:00 p.m. Eastern Time, Wednesday, May 23, 2018.

--------------------------------------------------------------

Under Canadian Securities Law, you are entitled to receive certain investor documents.

Electronic financial statements and MD&A are available at www.Emera.com and at www.SEDAR.com. If you wish paper copies, please tick the box below or go to the website https://ca.astfinancial.com/financialstatements and input code 1705a.

| ❑ | I would like to receive quarterly financial statements and MD&A in paper format |

| ❑ | I would like to receive annual financial statements and MD&A in paper format |

| A. Shareholder 320 Bay St., 3rd Floor Toronto, ON M5T 2A4 Line 6 Line 7 |

|

Form of Proxy - Emera Inc.

Annual Shareholders Meeting of May 24, 2018

Notes to Proxy

| 1. | This proxy must be signed by a holder or his or her attorney duly authorized in writing. If you are an individual, please sign exactly as your name appears on this proxy. If the holder is a corporation, a duly authorized officer or attorney of the corporation must sign this proxy, and if the corporation has a corporate seal, its corporate seal should be affixed. |

| 2. | If the securities are registered in the name of an executor, administrator or trustee, please sign exactly as your name appears on this proxy. If the securities are registered in the name of a deceased or other holder, the proxy must be signed by the legal representative with his or her name printed below his or her signature, and evidence of authority to sign on behalf of the deceased or other holder must be attached to this proxy. |

| 3. | Some holders may own securities as both a registered and a beneficial holder and will need to vote separately as a registered holder and as a beneficial holder. Beneficial holders may be forwarded either a form of proxy already signed by the intermediary or a voting instruction form to allow them to direct the voting of securities they beneficially own. Beneficial holders should follow instructions for voting conveyed to them by their intermediaries. |

| 4. | If a security is held by two or more individuals, any one of them present or represented by proxy at the Meeting may, in the absence of the other or others, vote at the Meeting. However, if one or more of them are present or represented by proxy, they must vote together the number of securities indicated on the proxy. |

| 5. | If this proxy is not dated, it will be deemed to bear the date on which it was mailed on behalf of management of the Company to you. |

All holders should refer to the Management Information Circular for further information regarding completion and use of this proxy and other information pertaining to the Meeting.

This proxy is solicited by and on behalf of Management of the Company.

Emera offers a number of ways to cast your vote.

|

• Go to www.astvotemyproxy.com • Follow the instructions on the screen • You will be required to enter the 13-digit control number located on the reverse • No need to return this proxy |

• Use any touch-tone telephone, call toll free in Canada and United States 1-888-489-5760 • Follow the voice instructions • When prompted, enter the 13-digit control number located on the reverse • No need to return this proxy |

To vote using your smartphone, please scan this QR Code

• No need to return this proxy

| ||

|

• Complete the reverse of this form • Return your signed proxy in the envelope provided or send to:

AST Trust Company (Canada) P.O. Box 721 Agincourt, ON M1S 0A1

|

• Complete the reverse of this form • Fax your signed proxy to 1-416-368-2502, or toll free in Canada and United States to 1-866-781-3111 |

• Complete the reverse of this form • Scan your signed proxy and email it to [email protected]. | ||

INTERNET

INTERNET TELEPHONE

TELEPHONE SMARTPHONE

SMARTPHONE

MAIL

MAIL FAX

FAX EMAIL

EMAIL

All proxies must be received by 5:00 p.m. Eastern Time, Wednesday, May 23, 2018.

Exhibit 99.2

|

|

|

Voting Instruction Form (“VIF”) - Emera Inc.

Annual Shareholders Meeting of May 24, 2018

Appointee

I/We, being holder(s) of Emera Inc. (the “Company”) common shares, hereby appoint: M. Jacqueline Sheppard, or failing her, Scott C. Balfour, or failing him, Stephen D. Aftanas, OR

[To attend the meeting or to appoint someone to attend on your behalf, print that name here]

as proxy of the undersigned, to attend, act and vote on behalf of the undersigned in accordance with the below direction (or if no directions have been given, as the proxy sees fit) on all of the following matters and any other matter that may properly come before the Annual Meeting of Shareholders of the Company to be held at 2:00 p.m. Eastern Time on Thursday, May 24, 2018, in the Glenn Gould Studio, CBC Building, 250 Front Street West, Toronto, Ontario, Canada (the “Meeting”), and at any and all adjournments or postponements thereof in the same manner, to the same extent and with the same powers as if the undersigned were personally present, with full power of substitution.

Management recommends voting FOR Resolutions 1, 2, 3, and 4. Please use a dark black pencil or pen.

| 1. |

Election of Directors |

FOR | WITHHOLD | FOR | WITHHOLD | |||||||

| 01. Scott C. Balfour |

☐ | ☐ | 07. B. Lynn Loewen |

☐ | ☐ | |||||||

| 02. Sylvia D. Chrominska |

☐ | ☐ | 08. Donald A. Pether |

☐ | ☐ | |||||||

| 03. Henry E. Demone |

☐ | ☐ | 09. John B. Ramil |

☐ | ☐ | |||||||

| 04. Allan L. Edgeworth |

☐ | ☐ | 10. Andrea S. Rosen |

☐ | ☐ | |||||||

| 05. James D. Eisenhauer |

☐ | ☐ | 11. Richard P. Sergel |

☐ | ☐ | |||||||

| 06. Kent M. Harvey |

☐ | ☐ | 12. M. Jacqueline Sheppard |

☐ | ☐ | |||||||

| 2. |

Appointment of Auditors |

FOR | WITHHOLD | |||||||||

| Appointment of Ernst & Young LLP as auditors |

☐ | ☐ | ||||||||||

| 3. |

Auditors Fee |

FOR | AGAINST | |||||||||

| Authorize Directors to establish the auditors’ fee as required pursuant to the Nova Scotia Companies Act |

☐ | ☐ | ||||||||||

| 4. |

Advisory Vote on Executive Compensation |

FOR | AGAINST | |||||||||

| Consider and approve, on an advisory basis, a resolution on Emera’s approach to executive compensation as disclosed in the Management Information Circular |

☐ | ☐ | ||||||||||

I/We authorize you to act in accordance with my/our instructions set out above. I/We hereby revoke any proxy previously given with respect to the Meeting.

If no voting instructions are indicated above, this VIF will be voted FOR a matter by Management’s appointees or, if you appoint another person, as such other person sees fit. On any amendments or variations proposed or any new business properly submitted before the Meeting, I/We authorize you to vote as you see fit.

|

|

|

|||||

| Signature(s) |

Date |

Please sign exactly as your name(s) appear on this VIF. Please see reverse for instructions. All VIFs must be received by 5:00 p.m. Eastern Time, Wednesday, May 23, 2018.

--------------------------------------------------------------

Under Canadian Securities Law, you are entitled to receive certain investor documents.

Electronic financial statements and MD&A are available at www.Emera.com and at www.SEDAR.com. If you wish paper copies, please tick the box below or go to the website https://ca.astfinancial.com/financialstatements and input code 1705a.

| ❑ |

I would like to receive quarterly financial statements and MD&A in paper format |

| ❑ |

I would like to receive annual financial statements and MD&A in paper format |

| A. Shareholder 320 Bay St., 3rd Floor Toronto, ON M5T 2A4 Line 6 Line 7 |

|

Voting Instruction Form (“VIF”) - Emera Inc.

Annual Shareholders Meeting of May 24, 2018

| 1. |

We are sending to you the enclosed proxy-related materials that relate to a meeting of holders of Emera Inc.’s common shares. Unless you attend the Meeting and vote in person, your securities can be voted only by management, as appointee of the registered holder, in accordance with your instructions. |

| 2. |

We are prohibited from voting these securities on any of the matters to be acted upon at the Meeting without your specific voting instructions. In order for these securities to be voted at the Meeting, it will be necessary for us to have your specific voting instructions. Please complete and return the information requested in this VIF to provide your voting instructions to us promptly. |

| 3. |

If you want to attend the Meeting and vote in person, please write your name in the place provided for that purpose in this form. You can also write the name of someone else whom you wish to attend the Meeting and vote on your behalf. Unless prohibited by law, the person whose name is written in the space provided will have full authority to present matters to the Meeting and vote on all matters that are presented at the Meeting, even if those matters are not set out in this form or the Management Information Circular. Consult a legal advisor if you wish to modify the authority of that person in any way. If you require help, please contact the Registered Representative who services your account. |

| 4. |

This VIF should be signed by you in the exact manner as your name appears on the VIF. If these voting instructions are given on behalf of a body corporate, set out the full legal name of the body corporate, the name and position of the person giving voting instructions on behalf of the body corporate, and the address for service of the body corporate. |

| 5. |

If this VIF is not dated it will be deemed to bear the date on which it is mailed by management to you. |

| 6. |

When properly signed and delivered, securities represented by this VIF will be voted as directed by you, however, if such a direction is not made in respect of any matter, the VIF will direct the voting of the securities to be made as recommended in the documentation provided by Management for the Meeting. |

| 7. |

This VIF confers discretionary authority on the appointee to vote as the appointee sees fit in respect of amendments or variations to matters identified in the notice of meeting or other matters as may properly come before the Meeting or any adjournment thereof. |

| 8. |

Your voting instructions will be recorded on receipt of the VIF. |

| 9. |

By providing voting instructions as requested, you are acknowledging that you are the beneficial owner of, and are entitled to instruct us with respect to the voting of, these securities. |

| 10. |

If you have any questions regarding the enclosed documents, please contact the Registered Representative who services your account. |

| 11. |

This VIF should be read in conjunction with the Management Information Circular and other proxy materials provided by Management. |

All holders should refer to the Management Information Circular for further information regarding completion and use of this VIF and other information pertaining to the Meeting.

Emera offers a number of ways to cast your vote.

|

• Go to www.astvotemyproxy.com • Follow the instructions on the screen • You will be required to enter the 13-digit control number located on the reverse • No need to return this VIF |

• Use any touch-tone telephone, call toll free in Canada and United States 1-888-489-5760 • Follow the voice instructions • When prompted, enter the 13-digit control number located on the reverse • No need to return this VIF |

To vote using your smartphone, please scan this QR Code

• No need to return this VIF

| ||

|

• Complete the reverse of this form • Return your signed VIF in the envelope provided or send to:

AST Trust Company (Canada) P.O. Box 721 Agincourt, ON M1S 0A1

|

• Complete the reverse of this form • Fax your signed VIF to 1-416-368-2502, or toll free in Canada and United States to 1-866-781-3111 |

• Complete the reverse of this form • Scan your signed VIF and email it to [email protected]. | ||

All VIFs must be received by 5:00 p.m. Eastern Time, Wednesday, May 23, 2018.

Exhibit 99.3

Notice of Annual Meeting

| Thursday, May 24, 2018 2:00 p.m. Eastern Time |

Glenn Gould Studio 250 Front Street West, Toronto, Ontario, Canada |

Record Date Close of business March 28, 2018 |

Items of Business

| 1. | Electing Directors to serve until the next annual meeting of Shareholders; |

| 2. | Appointing Auditors; |

| 3. | Authorizing the Directors to establish the Auditors’ fee; |

| 4. | Considering an advisory resolution on the Company’s approach to executive compensation; and |

| 5. | Transacting such other business as may properly come before the meeting. |

As a shareholder, it is important that you vote. Common shareholders are encouraged to return their proxy or voting instruction form as soon as possible. A postage-paid, pre-addressed envelope is provided. As an alternative, shareholders may choose to vote by telephone or on the internet as provided for on the proxy or voting instruction form. Proxies must be received prior to 5:00 p.m. Eastern Time on Wednesday, May 23, 2018, or if the meeting is adjourned, at least 48 hours (not including Saturdays, Sundays, or statutory holidays in Nova Scotia) prior to the reconvened meeting.

Should you have questions or comments, please contact Emera Incorporated by writing to the Corporate Secretary, Emera Incorporated, P.O. Box 910, Halifax, Nova Scotia B3J 2W5 or by calling 1-800-358-1995 from anywhere in North America or (902) 428-6060 within the Halifax-Dartmouth area.

Stephen D. Aftanas

Corporate Secretary

Table of Contents

Exhibit 99.4

Table of Contents

Table of Contents

Letter from the Chair

| Fellow Shareholder,

We continued to execute on our strategy in 2017, delivering strong results for the business and our shareholders. |

||

| The Board remained focused on corporate strategy, risk identification and management, the balance sheet, capital spending, our operations and our people, including leadership development and organizational capacity across Emera.

Strategy Oversight

With Emera’s new scale and scope in 2017, the company and the Board renewed their focus on strategy at both the corporate and subsidiary level. We worked to strengthen the strategic focus areas and ready the organization for the disruptive forces and changing technology facing the industry.

The company continued to deliver on its strategy of delivering clean affordable energy to customers in 2017, making significant advances in integrating renewables and embracing innovation. Emera recently completed the largest acquisition ever made by the company (TECO Energy, Inc.) and successfully completed the Maritime Link Project on time and under budget. Emera cut the ribbon on a 23 MW solar facility at Big Bend in Florida and announced plans to build 600MW of solar generation – installing six million photovoltaic panels and resulting in what will be the highest penetration of solar in the generation mix of any utility in Florida. The team also introduced innovative new pilot projects in Nova Scotia and Barbados that will focus on the capture, use and storage of renewable energy. These initiatives and others will drive Emera’s continued growth in 2018 and beyond. |

Jackie Sheppard Chair, Board of Directors Emera Inc. | |

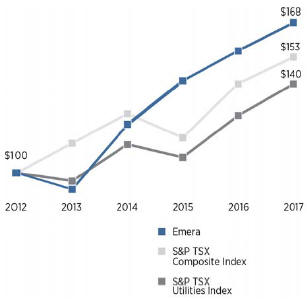

| Our strategic focus continues to emphasize the greening of our generation fleet in support of creating the grid of the future. These changes require a long-term commitment by the Board and management. Over the long term, Emera has consistently provided value to shareholders, delivering a total shareholder return (TSR) that exceeded the industry average. Over the past five years, Emera continued to be a leader in TSR, delivering annualized TSR of 11.0 per cent compared to 7.0 per cent delivered by the S&P/TSX Capped Utilities Index and 8.8 per cent delivered by the S&P/TSX Composite Index over the same period.

As the graph on the right indicates, $100 invested in Emera on December 31, 2012 was worth $168 on December 31, 2017, compared to $140 in the S&P/TSX Capped Utilities Index and $152 in the S&P/ TSX Composite Index.

Improving economic indicators and rising interest rates made the second half of 2017 and the beginning of 2018 challenging. US tax reform also impacted our business and the team continues to work through plans to mitigate impacts moving forward. We remain confident in our ability to deliver consistent value to our shareholders over the longer term. |

Cumulative Total Return on $100 Investment

December 31, 2012 to December 31, 2017

|

Emera Inc. — Annual Report 2017 1

Table of Contents

Our regulated asset base continues to be strong, offering more earnings diversity, capacity and quality. Over 90 per cent of our earnings currently come from our regulated businesses, exceeding our minimum target of 75 per cent.

Consistently delivering returns in a dynamic business environment requires strategy, planning and disciplined execution. In 2017, the team delivered despite many challenges, including extreme weather.

Unseasonably warm or cold temperatures affect our financial performance, while extreme weather events, such as a windstorm in Maine and Hurricanes Irma and Maria, presented critical challenges in 2017. That’s why the team is continuing to improve our ability to model weather to better understand system impacts and restore energy faster for customers. These improvements were evident in Tampa Electric’s response after Hurricane Irma. The team restored power to more than 425,000 customers, more than half of its customer base, in only seven days after the storm. Emera Maine restored 90,000 customers, over half of its customer base, in just seven days after a major windstorm in October.

Commitment to strong governance

| Every year, the Board completes an extensive governance review that sets out priorities and a rigorous action plan that is tracked throughout the year.

In the first full year of TECO integration into the Emera group of companies, we applied Emera’s subsidiary governance principles through the recruitment of new independent directors in both Florida and New Mexico. These Boards, with a complement of independent Directors, are well positioned to provide oversight and strategic direction for the businesses in these regions.

At the corporate level, Emera constituted a new Health, Safety and Environment (HSE) Committee in 2017. In response to Emera’s expanded size and diversity of operations, the Committee will focus on oversight of the safety, health and wellness of employees and advanced environmental monitoring and reporting. We aspire to be world class in all of these areas. The Committee monitors and evaluates HSE matters and emerging issues, reviews compliance, and identifies and oversees the management of risks in these areas that could adversely impact operations, strategy or reputation.

|

Emera’s new Health, Safety & Environment Committee is overseeing how employees take care of each other and the places we work. |

Given the tragic incidents that occurred in Florida and in Newfoundland and Labrador, the Committee spent significant time reviewing the company’s plans and actions to strengthen safety culture and safety programs across the business.

2 Emera Inc. — Annual Report 2017

Table of Contents

Letter from the Chair

Sustainability

| In 2017, Emera produced its first annual Sustainability Report. The report illustrates how we continue to advance Emera’s cleaner, affordable energy strategy and are creating value for our customers, our communities, and our environment. It highlights how we continue to invest in initiatives that promote stronger communities and growth; how our team members volunteer thousands of hours in support of local causes; and how we are investing in partnerships that build a culture of entrepreneurship and innovation in the communities in which we operate.

It is the first time all of Emera’s commitments have been presented in this way, demonstrating how sustainability is at the core of our business. It also highlights how we’ve been successfully applying our strategy for over a decade. We are committed to building a strong sustainability function at Emera that represents our strategy in action and ensures that all of our stakeholders understand our strategy, our commitments and our results beyond financial performance. |

We published Emera’s first Sustainability Report in 2017, showing how sustainability is core to who we are and what we do at www.emera.com/sustainability. |

Renewal and succession planning

As Emera continues to grow, the Board is committed to ensuring we have the right directors in place to guide the company today and into the future. Given the tenure of the Board, we are engaging in longer term succession planning that balances board renewal and the need for continuity and smooth transitions. We are continually striving for diversity of experience, thought and gender, focusing on Board and Committee effectiveness and instituting best practices.

Consistent with the Board renewal principles adopted in 2016, the Board welcomed new director Kent Harvey in 2017. Mr. Harvey is an accomplished executive with more than 30 years of experience in the energy industry in the United States.

I also want to extend a special thanks to my colleague and predecessor Chair of the Board, John McLennan, who will be retiring from the Board in May 2018. John joined the Board in 2005 and served as our Chair from May 2009 to May 2014. With his vast corporate experience John could always be counted on as a voice of rich insight and wisdom. I’d be remiss if I didn’t mention how much we all enjoyed, and will miss, his Cape Breton spirit and wit! On behalf of my fellow Board members, we wish John the very best.

I would like to take the opportunity to thank all of my colleagues on the Board for their ongoing commitment to Emera and to the highest standards of corporate governance.

Emera Inc. — Annual Report 2017 3

Table of Contents

CEO succession

In March 2017, we announced our CEO succession plans, providing a 12-month transition process that allowed for a seamless leadership transition.

On behalf of the Board of Directors, I’d like to thank Chris Huskilson for his remarkable contribution to the business and congratulate him on an outstanding legacy of growth and transformation at Emera.

Under Chris’ leadership, Emera’s assets have grown from $4 billion to approximately $29 billion, we’ve provided annual total shareholder return that outpaces our industry and increased the value of our shares to over twice what it was when he became President and CEO.

A big part of Chris’ legacy is the team and culture that he built at Emera. He believed in developing people by providing all employees equal opportunity to learn diverse skills across the business. The team is strong and ready for the future.

I would also like to thank Chris for working so constructively with the Board as we all focused on successfully transitioning the company for new leadership.

Scott Balfour became Emera’s new President and CEO on March 29, 2018. Scott’s proven leadership ability, financial acumen and business experience make him the natural choice to be the next CEO for Emera. We are confident that we have the right leader and the right team in place for Emera’s future growth.

Finally, Emera was recognized as one of Canada’s Best Employers by Forbes Magazine in 2017. I would like to thank the team across all the Emera companies for consistently delivering for our customers and our shareholders. Emera thrives because of the incredible work and commitment of the team.

Sincerely,

..

..

Jackie Sheppard

Chair, Emera Inc.

Board of Directors

4 Emera Inc. — Annual Report 2017

Table of Contents

Letter from the CEO

Letter from the CEO

Fellow Shareholder:

| In many ways, 2017 was a milestone year for Emera in both stability and growth.

We experienced the first full year of operations with Tampa Electric, Peoples Gas and New Mexico Gas. Integration has strengthened our team and ensured all of our companies are aligned with Emera’s strategy and positioned for growth. Of particular note, we completed the construction of the $1.56 billion Maritime Link project – on time and under budget, we announced a major solar initiative in Florida and invested in innovation for our customers. And the teams in the Caribbean, Florida, Maine and Nova Scotia each responded with exceptional restoration efforts to significant storm events.

Financial Highlights

In 2017, adjusted net income and earnings per share were $524 million and $2.46. When compared to 2016, and excluding the one-time impacts from that year, we saw a 28 per cent increase in our year-over-year adjusted earnings due to a full-year of contribution from Emera Florida and New Mexico in 2017. Adjusted earnings per share, excluding one-time impacts, increased by three per cent.

We experienced significant growth in our Florida utilities, a continuation of material and consistent earnings from our legacy utilities, increased our dividend eight per cent and completed a $700 million equity issuance to finance Emera’s continuing growth in 2018.

While maintaining some of the lowest customer rates for electricity and natural gas in the state, Tampa Electric and Peoples Gas had the largest net earnings in their companies’ history, an increase of over 10 per cent from 2016. The increase has been driven by customer and load growth and through increased rate base investments, including renewables.

Our legacy utilities, Nova Scotia Power, Emera Maine and the Caribbean all performed in line with expectations in 2017, providing stable earnings and cash generation. |

Scott Balfour President & CEO, Emera Inc. | |

| We continue to see the strength and potential in our regulated companies, which in 2017 made up more than 90 per cent of our business. To underline the confidence that we have in our regulated business and its growth potential, we’ve highlighted a minimum target of 75 per cent for regulated earnings, which also provides the foundational support in earnings and cash flow to support our dividend. |

||

| At present, our regulated operations contribute in excess of 95 per cent to our overall earnings and we believe these businesses also provide a stable platform for our future growth. The completion of the Maritime Link and the start of the 600MW Tampa solar project are notable examples of how we are growing our consolidated rate base, and Emera’s earnings and cash flow, both today and for the next several years.

In an effort to streamline Emera’s ownership structure in the Caribbean and in support of a more efficient capital structure for Emera’s investment in this region, Emera announced a transaction in 2017 for Emera Utilities Holdings Ltd. (“EUHL”), a wholly owned indirect subsidiary of Emera, to indirectly acquire all of the common

shares of ICDU that it did not already own. The transaction closed in January 2018. |

Maritime Link project team members celebrate achieving first energy exchange. |

Emera Inc. — Annual Report 2017 5

Table of Contents

Emera Energy’s results were in line with 2016 but below our expectations as a result of weak market conditions largely because of mild weather conditions. We expect strong results in 2018 as capacity prices in New England continue to increase.

| As a result of our 2017 financial performance and our outlook for 2018, in September we increased our annual common share dividend to $2.26, consistent with our targeted annual growth rate through to 2020.

In December, we successfully completed a bought deal offering of 14,614,000 common shares at $47.90 per common share for aggregate gross proceeds of approximately $700 million. These proceeds are being used to support Emera’s recently announced growth initiatives and for general corporate purposes, including to reduce indebtedness outstanding under the business’s credit facility and to fund other ordinary course capital expenses.

On December 22, 2017, the US Tax Cuts and Jobs Act of 2017, commonly referred to as US tax reform, was signed into legislation. There are a number of specific details that have yet to be clarified, but a number of provisions will impact our US business operations. This included a one-time non-cash valuation allowance on Emera’s |

Tampa Electric is significantly expanding its solar generation portfolio, which includes its 23 MW facility at Big Bend. |

consolidated US tax loss pool taken in 2017. We’ve also disclosed a conservative estimate of the possible near-term impacts on earnings and cash flow for 2018 and we’ve been working diligently to mitigate these impacts. Over the longer term, we see the impacts of US tax reform as being neutral to positive for our business.

The Journey to World Class Safety

While the team delivered in many ways and remained committed to our unwavering belief that safety is more important than any other business interest and our efforts to improve safety performance, we had two separate incidents resulting in six fatalities and one life altering injury in 2017.

These incidents deeply impacted all of us at Emera. As a result, we initiated numerous reviews, made significant enhancements to procedures, and improved processes to drive a positive shift in the safety culture across Emera to ensure these kinds of incidents never happen again. We are more focused than ever on safety and we are committed to an Emera where no one gets hurt.

Strategy in Action

| In 2017, we continued to lead the way on delivering our cleaner, affordable energy strategy with new developments in renewable generation, electricity transmission, and natural gas infrastructure expansion. After four years of construction, the Maritime Link was completed on time and under budget in late 2017 and began commercial operation on January, 2018. Connecting Newfoundland to the North American energy grid for the first time in history.

Tampa Electric received approval from its regulator for the construction and the recovery of revenue requirements for four phases of solar capacity totaling 600 MW between 2018 and 2021. Once complete, nearly seven per cent of Tampa Electric’s energy generation will come from the sun – a higher percentage of solar than any other Florida utility. |

Nova Scotia Power works with customers to test home-based energy storage. |

6 Emera Inc. — Annual Report 2017

Table of Contents

Letter from the ceo

Nova Scotia Power plans to spend approximately $1.8 billion in capital between 2018 and 2022. With these investments, Nova Scotia Power will optimize its existing clean generation assets and create greater efficiencies that will ultimately benefit customers.

Investing in Innovation

| Innovation is a part of how we do business, continually evolving to serve our customers better. Innovation inspires change, drives solutions, encourages collaboration and grows economies. We continue to work to understand rapidly changing technology so that we can create and shape opportunities that can be used to benefit customers.

In August, Nova Scotia Power received approval from the Nova Scotia Utilities and Review Board (NSUARB) on a pilot project to test battery storage technology from industry leaders Tesla and OpusOne Solutions. The $3.4 million project included the installation of 10 Tesla Powerwalls in customer’s homes and a grid-size Tesla Powerpack at a substation tied in with a local six MW capacity wind farm. The team is excited to test a number of use cases and assess the peak performance of the stored energy. Ultimately, by integrating new technologies and more renewable energy into the grid, we aim to provide better service and value for customers. |

Emera companies like Grand Bahama Power are advancing plans to use electric cars as part of the energy storage solution. |

We remain committed to investing in innovative, dependable storage and smarter, more reliable grids. Our operating companies in Maine and Barbados are partnering with Tesla to test the use of battery storage.

In October, Nova Scotia Power applied to the NSUARB for approval to launch the Advanced Metering Initiative (AMI), a $133 million project which would see the first smart meters rolled out in 2019 throughout the province. Over the next 20 years smart meters will result in $38 million in reduced costs to the electricity system. This cost reduction will help the company continue to provide rate stability for customers.

| We’re also investing in smart meters in Barbados, where we have installed 30,000 smart meters to date, and in Florida, where Tampa Electric has announced plans to roll out over 20,000 units in its own AMI pilot project.

By collaborating and cooperating on AMI and using the combined purchasing power of Nova Scotia Power, Tampa Electric and Emera Maine, we are able to find greater efficiency and negotiate with vendors to find the best technology, terms and pricing solutions that will ultimately benefit customers in each region where we operate.

In late 2017, we established Emera Technologies LLC., a small, dedicated and nimble organization that will focus on innovation, capitalize on business opportunities and develop new technologies to position Emera as a dominant player in an evolving energy landscape. |

Team members in Florida help the engineers of tomorrow learn about energy. |

At Emera, we embrace innovation as a key driver of how we continue to improve and grow as a business. It plays a critical role in getting us to a sustainable energy future that’s reliable and available to meet the needs of our customers anywhere, anytime. Emera believes in strategic investments that make our economy stronger and our communities smarter.

Emera Inc. — Annual Report 2017 7

Table of Contents

We invested in the IdeaHub at Dalhousie University in Nova Scotia. This will provide students and start- ups with mentorship and support to bring ideas for their technology-based products to the market.

In New Mexico, we invested in InnovateABQ, an entrepreneurial district in Albuquerque, where multi-purpose companies are working to create technological innovations and opportunities for expanded business growth throughout the state.

In September, we announced that Emera is a core investor in the Ocean Supercluster initiative. This industry-led network brings together industry, technology providers and researchers to accelerate the safe, financially and environmentally sustainable development of Canada’s ocean resources.

| We also invested in the Research Centre for Smart Grid Technologies at the University of New Brunswick, a state-of-the-art research facility that enables research and development, as well as industry partnerships for smart grid research.

Extreme Weather Events

As mentioned earlier, extreme weather was a significant factor in many of our operating regions in 2017. Weather always impacts our business and we are continuously improving how we model the system impacts of hurricanes and storms. This is essential for our customers, as it also means we are better prepared for these events and can improve power restoration times.

Unfortunately, some storms are catastrophic, as was the case when Hurricane Maria devastated the island of Dominica. As a result, all 36,000 of Domlec’s customers lost power. This impacted everyone, including our own team - many of whom lost their homes. Following the hurricane, our team immediately got to work to restore power to vital services like hospitals and airports and we continue to restore power to customers on the island.

Our People

Our successes would not have been possible without the team at Emera. I would like to take this opportunity to thank every Emera employee for their hard work and dedication. You have all been instrumental in growing Emera into what it is today. I am honoured and excited to lead such a talented and committed team. |

Grand Bahama Power team members work to restore customers following Hurricane Irma.

Team members in Florida support community members in need over the holiday season. |

In closing, I’d like to thank Chris for his leadership and vision. He has been a driving force behind the growth and success of Emera. Over his more than 13 years as President and CEO, Chris has shaped this organization and we certainly would not be in the position we are today without him. Along the way, he assembled and developed a strong team that has been inspired by his vision.

We are ready and excited to build on his legacy – delivering even more value for our customers and our shareholders.

Sincerely,

Scott Balfour

President and CEO

Emera Inc.

8 Emera Inc. — Annual Report 2017

Table of Contents

Management’s Discussion & Analysis

As at February 9, 2018

Management’s Discussion & Analysis (“MD&A”) provides a review of the results of operations of Emera Incorporated and its subsidiaries and investments (“Emera”) during the fourth quarter of 2017 relative to the same quarter in 2016; the full year of 2017 relative to 2016 and selected financial information for 2015; and its financial position as at December 31, 2017 relative to December 31, 2016. To enhance shareholders’ understanding, certain multi-year historical financial and statistical information is presented. Throughout this discussion, “Emera Incorporated”, “Emera” and “Company” refer to Emera Incorporated and all of its consolidated subsidiaries and investments. The Company’s activities are carried out through six business segments: Emera Florida and New Mexico, Nova Scotia Power Inc., Emera Maine, Emera Caribbean, Emera Energy and Corporate and Other.

This discussion and analysis should be read in conjunction with the Emera Incorporated annual audited consolidated financial statements and supporting notes as at and for the year ended December 31, 2017. Emera follows United States Generally Accepted Accounting Principles (“USGAAP” or “GAAP”).

The accounting policies used by Emera’s rate-regulated entities may differ from those used by Emera’s non-rate-regulated businesses with respect to the timing of recognition of certain assets, liabilities, revenues and expenses. Emera’s rate-regulated subsidiaries include:

| Emera Rate-Regulated Subsidiary or Equity Investment | Accounting Policies Approved/Examined By | |

| Subsidiary | ||

| Tampa Electric – Electric Division of Tampa Electric Company (“TEC”) | Florida Public Service Commission (“FPSC”) and the Federal Energy Regulatory Commission (“FERC”) | |

| Peoples Gas System (“PGS”) – Gas Division of TEC | FPSC | |

| New Mexico Gas Company, Inc. (“NMGC”) | New Mexico Public Regulation Commission (“NMPRC”) | |

| Nova Scotia Power Inc. (“NSPI”) | Nova Scotia Utility and Review Board (“UARB”) | |

| Emera Maine | Maine Public Utilities Commission (“MPUC”) and FERC | |

| Barbados Light & Power Company Limited (“BLPC”) | Fair Trading Commission, Barbados | |

| Grand Bahama Power Company Limited (“GBPC”) | The Grand Bahama Port Authority (“GBPA”) | |

| Dominica Electricity Services Ltd. (“Domlec”) | Independent Regulatory Commission, Dominica | |

| (“IRC”) Emera Brunswick Pipeline Company Limited (“Brunswick Pipeline”) | National Energy Board (“NEB”) | |

| Equity Investments | ||

| NSP Maritime Link Inc. (“NSPML”) | UARB | |

| Maritimes & Northeast Pipeline Limited Partnership and Maritimes & Northeast Pipeline LLC (“M&NP”) | NEB and FERC | |

| Labrador Island Link Limited Partnership (“LIL”) | Newfoundland and Labrador Board of Commissioners of Public Utilities (“NLPUB”) | |

| St. Lucia Electricity Services Limited (“Lucelec”) | National Utility Regulatory Commission (“NURC”) | |

All amounts are in Canadian dollars (“CAD”), except for the Emera Florida and New Mexico, Emera Maine and Emera Caribbean sections of the MD&A, which are reported in US dollars (“USD”), unless otherwise stated.

Additional information related to Emera, including the Company’s Annual Information Form, can be found on SEDAR at www.sedar.com.

Emera Inc. — Annual Report 2017 9

Table of Contents

This MD&A contains “forward-looking information” and statements which reflect the current view with respect to the Company’s expectations regarding future growth, results of operations, performance, business prospects and opportunities and may not be appropriate for other purposes within the meaning of applicable Canadian securities laws. All such information and statements are made pursuant to safe harbour provisions contained in applicable securities legislation. The words “anticipates”, “believes”, “could”, “estimates”, “expects”, “intends”, “may”, “plans”, “projects”, “schedule”, “should”, “budget”, “forecast”, “might”, “will”, “would”, “targets” and similar expressions are often intended to identify forward-looking information, although not all forward-looking information contains these identifying words. The forward-looking information reflects management’s current beliefs and is based on information currently available to Emera’s management and should not be read as guarantees of future events, performance or results, and will not necessarily be accurate indications of whether, or the time at which, such events, performance or results will be achieved.

The forward-looking information is based on reasonable assumptions and is subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or results anticipated by the forward-looking information. Factors that could cause results or events to differ from current expectations are discussed in the Business Overview and Outlook section of the MD&A and may also include: regulatory risk; operating and maintenance risks; changes in economic conditions; commodity price and availability risk; capital market and liquidity risk; future dividend growth; timing and costs associated with certain capital projects; the expected impacts on Emera of challenges in the global economy; estimated energy consumption rates; maintenance of adequate insurance coverage; changes in customer energy usage patterns; developments in technology that could reduce demand for electricity; weather; commodity price risk; unanticipated maintenance and other expenditures; system operating and maintenance risk; derivative financial instruments and hedging; interest rate risk; credit risk; commercial relationship risk; disruption of fuel supply; country risks; environmental risks; foreign exchange; regulatory and government decisions, including changes to environmental, financial reporting and tax legislation; risks associated with pension plan performance and funding requirements; loss of service area; risk of failure of information technology infrastructure and cybersecurity risks; market energy sales prices; labour relations; and availability of labour and management resources.

Readers are cautioned not to place undue reliance on forward-looking information as actual results could differ materially from the plans, expectations, estimates or intentions and statements expressed in the forward-looking information. All forward-looking information in this MD&A is qualified in its entirety by the above cautionary statements and, except as required by law, Emera undertakes no obligation to revise or update any forward-looking information as a result of new information, future events or otherwise.

10 Emera Inc. — Annual Report 2017

Table of Contents

Management’s Discussion & Analysis

INTRODUCTION AND STRATEGIC OVERVIEW

Emera is a geographically diverse energy and services company. The Company has investments in electricity generation, transmission and distribution and gas transmission and distribution, predominantly within rate-regulated utilities which support strong, consistent earnings and cash flow. Emera seeks to provide its customers with reliable, cost-effective and sustainable energy products and services, and provides regional energy solutions by connecting its assets, markets and partners in Canada, the United States and the Caribbean.

For investors, Emera seeks to deliver consistent earnings, cash flow and long-term growth, and accordingly, the primary measures of performance are annual dividend growth, earnings per common share growth, adjusted earnings per common share growth (a non-GAAP measure described in the Non-GAAP Financial Measures section below) and total shareholder return. The Company targets eight per cent annual dividend growth through 2020. Emera targets achieving a minimum of 75 per cent of its adjusted net income from its rate-regulated utilities and an average dividend payout ratio of 70 to 75 per cent of adjusted net income.

| For the | Year ended December 31, 2017 | |||||||||||

| 1 year | 3 year | 5 year | ||||||||||

| Dividend per share compound annual growth rate |

6.5% | 12.9% | 9.4% | |||||||||

| Earnings per share compound annual growth rate |

(6.0%) | (23.9%) | (6.7%) | |||||||||

| Adjusted earnings per share compound annual growth rate (see Non-GAAP Financial Measures below) |

(11.2%) | 3.3% | 5.9% | |||||||||

| Emera annualized total shareholder return (1) |

8.3% | 11.2% | 11.0% | |||||||||

| S&P/TSX Capped Utilities Index annualized total shareholder return (2) |

10.7% | 7.6% | 7.0% | |||||||||

| (1) | Total shareholder return combines share price appreciation and dividends per common share paid during the fiscal year to show the total return to the shareholder expressed as an annualized percentage, assuming dividends are reinvested each time they are paid. |

| (2) | The S&P/TSX Capped Sector Indices provide liquid and tradable benchmarks for related derivative products of Canadian economic sectors. Constituents are selected from a stock pool of S&P/TSX Composite Index Stocks, and the relative weight of any single index constituent is capped at 25 per cent. The indices are based upon the Global Industry Classification Standards (GICS®). The S&P/TSX Capped Utilities Index imposes capped weights on the index constituents included in the S&P/TSX Composite that are classified in the GICS® utilities sector. |

Energy markets worldwide, in particular across North America, are undergoing foundational changes that have created significant investment opportunities for companies with Emera’s experience and capabilities. Key trends contributing to these investment opportunities include: aging infrastructure, lower-cost natural gas, growing demand for new electric heating and cooling solutions, the requirement for large-scale transmission projects to deliver new energy sources to customers, technological developments, and environmental concerns. These environmental concerns include a desire to reduce emissions of carbon dioxide and other greenhouse gases and the potential system impacts of climate change, including changes in global and regional weather patterns, changes in the frequency and intensity of extreme weather events, and rising sea levels. At the core of Emera’s utilities strategy is identifying opportunities to invest in the transition from higher-carbon methods of electricity generation to lower-carbon alternatives, and the related transmission and distribution infrastructure to deliver that energy to market.

The energy sector continues to be impacted by mandated and incented carbon reductions throughout eastern North America and in the Caribbean. It is unclear whether economic volatility, government policy and lower fossil fuel prices will slow the pace of this change in the industry. Investment in wind, solar, and hydro generation, natural gas and new transmission infrastructure is likely to continue across the sector despite any cost differential with more carbon-intensive generating options. The capital spending requirements related to these investments will need to be managed within the context of overall energy pricing.

In Florida, the Company is evaluating and investing in a number of initiatives, including solar generation, that would reduce carbon emissions. In Nova Scotia, the Company has invested in wind energy, biomass and hydroelectricity and is on track to meet a minimum 40 per cent renewable standard by 2020. In the Caribbean, Emera is similarly focused on introducing cleaner generation alternatives, with an emphasis on affordability and fuel cost stability for its customers.

Emera is investing in electricity transmission to deliver new renewable energy to market. Emera’s ownership in the Maritime Link and Labrador Island Link projects will contribute to the transformation of the electricity market in the Atlantic provinces, enabling growth in the availability of clean, renewable energy for the region. In addition, the Atlantic provinces will benefit from enhanced connection to the northeastern United States, providing potential for excess renewable energy to be delivered throughout that region.

Emera Energy is a physical energy marketing and trading business, complemented by a portfolio of competitive electricity generation facilities. A substantial portion of Emera Energy’s activities are in northeastern North America, and its market knowledge, focus on customer service and robust risk management are key success factors. Unlike the vast majority of Emera’s businesses, Emera Energy is not rate-regulated.

Emera’s ability to achieve its strategy is a result of its ability to apply a collaborative approach to strategic partnerships, ability to find creative solutions within and across multiple jurisdictions and its experience dealing with complex projects and investment structures. The Company will continue to make investments in its regulated utilities to benefit customers and focus on providing rate stability. From time to time, Emera will make acquisitions, both regulated and unregulated, where the business or asset acquired aligns with Emera’s strategic initiatives and delivers shareholder value.

Emera Inc. — Annual Report 2017 11

Table of Contents

To ensure stability in the utilities’ net income and cash flows, Emera employs operating and governance models that focus on safety and operational excellence, a customer focus through service reliability and rate stability, constructive regulatory approaches, and proactive stakeholder engagement.

Emera has grown its asset base to deliver on its strategic objectives. Over the last 10 years, Emera’s ability to raise the capital necessary to fund investments has been a strong enabler of the Company’s growth. In addition to access to debt and equity capital markets, cash flow from operations will continue to play a role in financing the Company’s future growth. Maintaining strong, investment grade credit ratings is an important component of Emera’s financing strategy.

The energy industry is seasonal in nature. Seasonal patterns and other weather events, including the number and severity of storms, can affect demand for energy and cost of service. Similarly, mark-to-market adjustments and foreign currency exchange can have a material impact on the financial results for a specific period. Results in any one quarter are not necessarily indicative of results in any other quarter, or for the year as a whole.

The effect of foreign currency exchange on Emera’s net income is noteworthy, as it is expected that approximately 70 per cent of Emera’s adjusted net income will be derived from subsidiaries with a US functional currency. Emera’s consolidated net income and cash flows will be impacted by movements in the US dollar relative to the Canadian dollar. In general, Emera benefits from a weakening Canadian dollar and is adversely impacted by a strengthening Canadian dollar.

12 Emera Inc. — Annual Report 2017

Table of Contents

Management’s Discussion & Analysis

Emera uses financial measures that do not have standardized meaning under USGAAP and may not be comparable to similar measures presented by other entities. Emera calculates the non-GAAP measures by adjusting certain GAAP measures for specific items the Company believes are significant, but not reflective of underlying operations in the period. These measures are discussed and reconciled below.

Adjusted Net Income

Emera calculates an adjusted net income measure by excluding the effect of MTM adjustments and the impact in 2017 of US tax reform, signed into legislation on December 22, 2017 in the US Tax Cuts and Jobs Act of 2017 (“the Act”) (refer to the “Developments” section for further details).

The MTM adjustments are a result of the following:

| • | the mark-to-market adjustments related to Emera’s held-for-trading (“HFT”) commodity derivative instruments, including adjustments related to the price differential between the point where natural gas is sourced and where it is delivered; |

| • | the mark-to-market adjustments included in Emera’s equity income related to the business activities of Bear Swamp Power Company LLC (“Bear Swamp”); |

| • | the amortization of transportation capacity recognized as a result of certain Emera Energy marketing and trading transactions; |

| • | the mark-to-market adjustments related to an interest rate swap in Brunswick Pipeline; and |

| • | the mark-to-market adjustments included in Emera’s other income in 2016 related to the effect of USD-denominated currency and forward contracts for the TECO Energy, Inc. (“TECO Energy”) acquisition. These contracts were put in place to economically hedge the anticipated proceeds from the 2015 sale of $2.185 billion four-per-cent convertible unsecured subordinated debentures represented by instalment receipts (“the Debenture Offering” or “Debentures” or “Convertible Debentures”). |

The US tax reform adjustment is a result of the estimated revaluation of US non-regulated net deferred income tax assets as a result of the US federal corporate income tax rate reduction from 35 per cent to 21 per cent that was enacted in December 2017.

For the mark-to-market valuation adjustments, management believes excluding from net income the effect of these valuations and changes thereto, until settlement, better aligns the intent and financial effect of these contracts with the underlying cash flows and the ongoing operations of the business, and allows investors to better understand and evaluate the business. Management and the Board of Directors exclude these mark-to-market adjustments for evaluation of performance and incentive compensation.

Mark-to-market adjustments are further discussed in the Consolidated Financial Review section, Emera Energy and Corporate and Other.

Due to the enactment of the US Tax Cuts and Jobs Act of 2017, the Company recorded a non-cash income tax expense resulting from the provisional revaluation of the existing US non-regulated net deferred income tax assets. This provisional revaluation of an existing asset is not the result of any operational or market driven event. Management therefore believes excluding from net income the effect of this provisional revaluation better distinguishes the ongoing operations of the business, and allows investors to better understand and evaluate the Company. The impact of US tax reform is further discussed in the “Developments” section.

The following reconciles reported net income attributable to common shareholders, to adjusted net income attributable to common shareholders; and reported earnings per common share – basic, to adjusted earnings per common share – basic:

| Three months ended | Year ended | |||||||||||||||||||

| For the | December 31 | December 31 | ||||||||||||||||||

| millions of Canadian dollars (except per share amounts) | 2017 | 2016 | 2017 | 2016 | 2015 | |||||||||||||||

| Net income (loss) attributable to common shareholders |

$ | (228 | ) | $ | 70 | $ | 266 | $ | 227 | $ | 397 | |||||||||

| Revaluation of US non-regulated deferred income taxes |

$ | (317 | ) | $ | — | $ | (317 | ) | $ | — | $ | — | ||||||||

| After-tax mark-to-market gain (loss) |

$ | (48 | ) | $ | (34 | ) | $ | 59 | $ | (248 | ) | $ | 67 | |||||||

| Adjusted net income attributable to common shareholders |

$ | 137 | $ | 104 | $ | 524 | $ | 475 | $ | 330 | ||||||||||

| Earnings per common share – basic |

$ | (1.06 | ) | $ | 0.34 | $ | 1.25 | $ | 1.33 | $ | 2.72 | |||||||||

| Adjusted earnings per common share – basic |

$ | 0.64 | $ | 0.51 | $ | 2.46 | $ | 2.77 | $ | 2.26 | ||||||||||

Emera Inc. — Annual Report 2017 13

Table of Contents

EBITDA and Adjusted EBITDA

Earnings before interest, income taxes, depreciation and amortization (“EBITDA”) is a non-GAAP financial measure used by Emera. EBITDA is used by numerous investors and lenders to better understand cash flows and credit quality. EBITDA is useful to assess Emera’s operating performance and indicates the Company’s ability to service or incur debt, invest in capital and finance working capital requirements.

Adjusted EBITDA is a non-GAAP financial measure used by Emera. Similar to adjusted net income calculations described above, this measure represents EBITDA absent the income effect of Emera’s mark-to-market adjustments.

The Company’s EBITDA and Adjusted EBITDA may not be comparable to the EBITDA measures of other companies but in management’s view appropriately reflects Emera’s specific operating performance. These measures are not intended to replace “Net income attributable to common shareholders” which, as determined in accordance with GAAP, is an indicator of operating performance.

EBITDA and Adjusted EBITDA are discussed further in the Consolidated Financial Review, Emera Florida and New Mexico, NSPI, Emera Maine, Emera Caribbean, Emera Energy, and Corporate and Other sections.

The following is a reconciliation of reported net income to EBITDA and Adjusted EBITDA.

| Three months ended | Year ended | |||||||||||||||||||

| For the | December 31 | December 31 | ||||||||||||||||||

| millions of Canadian dollars | 2017 | 2016 | 2017 | 2016 | 2015 | |||||||||||||||

| Net income(loss) (1) |

$ | (232 | ) | $ | 71 | $ | 299 | $ | 266 | $ | 452 | |||||||||

| Interest expense, net |

175 | 169 | 698 | 585 | 212 | |||||||||||||||

| Income tax expense (recovery) |

329 | (6 | ) | 520 | (22 | ) | 93 | |||||||||||||

| Depreciation and amortization |

212 | 212 | 856 | 588 | 340 | |||||||||||||||

| EBITDA |

484 | 446 | 2,373 | 1,417 | 1,097 | |||||||||||||||

|

Mark-to-market gain (loss), excluding income tax and interest |

(75 | ) | (52 | ) | 78 | (327 | ) | 66 | ||||||||||||

| Adjusted EBITDA |

$ | 559 | $ | 498 | $ | 2,295 | $ | 1,744 | $ | 1,031 | ||||||||||

| (1) | Net income (loss) is income before Non-controlling interest in subsidiaries and Preferred stock dividends. |

14 Emera Inc. — Annual Report 2017

Table of Contents

Management’s Discussion & Analysis

Significant Items Affecting Earnings

2017

US Tax Reform

On December 22, 2017, the Tax Cuts and Jobs Act of 2017 (the “Act”) was signed into legislation. As a result of this legislation being enacted during 2017, the Company is required to revalue its US deferred income tax assets and liabilities based on the new 21 per cent tax rate. The Company has recognized an estimated $317 million income tax expense in 2017 as a result of the provisional revaluation of its US non- regulated net deferred income tax assets. There was no impact to earnings on the revaluation of the utilities net deferred tax liabilities as the Act allows for an offsetting regulatory liability. Refer to the “Developments” section for further details.

Earnings Impact of After-Tax Mark-to-Market Gains and Losses

After-tax mark-to-market losses increased $14 million to $48 million in Q4 2017 compared to $34 million in Q4 2016 mainly due to changes in existing positions on contracts at Emera Energy. Year-to-date, after-tax mark-to-market increased $307 million to a $59 million gain in 2017 compared to a $248 million loss for the same period in 2016. 2016 year-to-date included a $116 million loss resulting from the reversal of 2015 gains on USD-denominated currency and forward contracts related to the financing of the TECO Energy acquisition. Other factors contributing to the increase include changes in existing positions on long-term contracts at Emera Energy, and the reversal of 2016 mark-to-market losses at Emera Energy.

2016

Acquisition Related Costs

Emera incurred after-tax costs of $166 million ($0.97 per common share) in 2016 related to its acquisition of TECO Energy. All acquisition costs were recognized in the Corporate and Other segment.

Investment in Algonquin Power and Utilities Corp.

On December 8, 2016, Emera completed the sale of 12.9 million common shares of Algonquin Power and Utilities Corp. (“APUC”), representing approximately 4.7 per cent of APUC’s issued and outstanding common shares, for gross proceeds of $142 million. This sale resulted in a pre-tax loss of $12 million or $0.07 per common share (after-tax loss of $10 million or $0.06 per common share), which was recorded in “Other income (expenses), net” in Q4 2016. Emera no longer holds any interest in APUC.

On June 30, 2016, Emera exchanged 12.9 million APUC subscription receipts and dividend equivalents into 12.9 million APUC common shares. This conversion resulted in a pre-tax gain of $63 million or $0.42 per common share (after-tax gain of $53 million or $0.35 per common share), which was recorded in “Other income (expenses), net” in Q2 2016.

On May 24, 2016, Emera completed the sale of 50.1 million common shares of APUC, representing approximately 19.3 per cent of APUC’s issued and outstanding common shares, for gross proceeds of $544 million. This sale resulted in a pre-tax gain of $172 million or $1.15 per common share (after-tax gain of $146 million or $0.97 per common share), which was recorded in “Other income (expenses), net” in Q2 2016.

Gain on BLPC Self-Insurance Fund Regulatory Liability

BLPC maintains a Self-Insurance Fund (“SIF”) for the purpose of building an insurance fund to cover risk against damage and consequential loss to certain of BLPC’s generating, transmission and distribution systems. Third-party risk advisors were engaged to support a detailed risk analysis, which was completed to quantify the prudent assessment of the risk to BLPC’s transmission and distribution system from natural catastrophes.

In June 2016, BLPC secured support from the Government of Barbados and the Trustees of the SIF to reduce the contingency funding in the SIF to $29 million ($22 million USD). As a result, Emera recorded a pre-tax gain of $53 million ($41 million USD) or $0.35 per common share and an after-tax gain of $43 million ($34 million USD) or $0.29 per common share in “Other income (expenses), net”. In Q3 2016, Emera received a distribution of $65 million ($50 million USD) from the fund.

Emera Energy Recognition of State Fuel Taxes

In Q2 2016, Emera Energy recorded a $20 million pre-tax or $0.13 per common share ($12 million after-tax or $0.08 per common share) liability for state tax on natural gas sales made from November 2013 through March 2016, including $4 million pre-tax ($2 million after-tax) related to Q1 2016. The recognition of this liability resulted in an increase to “Non-regulated fuel for generation and purchased power”.

Emera Inc. — Annual Report 2017 15

Table of Contents

Consolidated Financial Highlights

| For the millions of Canadian dollars (except per share amounts) |

Three months ended December 31 |

Year ended December 31 |

||||||||||||||||||

| Adjusted Net Income | 2017 | 2016 | 2017 | 2016 | 2015 | |||||||||||||||

| Emera Florida and New Mexico |

$ | 80 | $ | 63 | $ | 382 | $ | 172 | $ | — | ||||||||||

| NSPI |

23 | 34 | 129 | 130 | 130 | |||||||||||||||

| Emera Maine |

8 | 11 | 46 | 47 | 45 | |||||||||||||||

| Emera Caribbean |

1 | 8 | 31 | 100 | 41 | |||||||||||||||

| Emera Energy |

26 | 5 | 24 | 24 | 130 | |||||||||||||||

| Corporate and Other |

(1 | ) | (17 | ) | (88 | ) | 2 | (16 | ) | |||||||||||

| Adjusted net income attributable to common shareholders |

$ | 137 | $ | 104 | $ | 524 | $ | 475 | $ | 330 | ||||||||||

| Revaluation of US non-regulated deferred income taxes |

(317 | ) | — | (317 | ) | — | — | |||||||||||||

| After-tax mark-to-market gain (loss) |

(48 | ) | (34 | ) | 59 | (248 | ) | 67 | ||||||||||||

| Net income (loss) attributable to common shareholders |

$ | (228 | ) | $ | 70 | $ | 266 | $ | 227 | $ | 397 | |||||||||

| For the millions of Canadian dollars (except per share amounts) |

Three months ended December 31 |

Year ended December 31 |

||||||||||||||||||

| 2017 | 2016 | 2017 | 2016 | 2015 | ||||||||||||||||

| Operating revenues |

$ | 1,473 | $ | 1,513 | $ | 6,226 | $ | 4,277 | $ | 2,789 | ||||||||||

| Income from operations |

236 | 208 | 1,391 | 555 | 508 | |||||||||||||||

| Net income (loss) attributable to common shareholders |

(228 | ) | 70 | 266 | 227 | 397 | ||||||||||||||

| Revaluation of US non-regulated deferred income taxes |

(317 | ) | — | (317 | ) | — | — | |||||||||||||

| After-tax mark-to-market gain (loss) |

(48 | ) | (34 | ) | 59 | (248 | ) | 67 | ||||||||||||

| Adjusted net income attributable to common shareholders |

$ | 137 | $ | 104 | $ | 524 | $ | 475 | $ | 330 | ||||||||||

| Earnings per common share – basic |

$ | (1.06 | ) | $ | 0.34 | $ | 1.25 | $ | 1.33 | $ | 2.72 | |||||||||

| Earnings per common share – diluted |

$ | (1.06 | ) | $ | 0.34 | $ | 1.24 | $ | 1.32 | $ | 2.71 | |||||||||

| Adjusted earnings per common share – basic |

$ | 0.64 | $ | 0.51 | $ | 2.46 | $ | 2.77 | $ | 2.26 | ||||||||||

| Dividends per common share declared |

$ | — | $ | — | $ | 2.1325 | $ | 1.9950 | $ | 1.6625 | ||||||||||

| Adjusted EBITDA |

$ | 559 | $ | 498 | $ | 2,295 | $ | 1,744 | $ | 1,031 | ||||||||||

16 Emera Inc. — Annual Report 2017

Table of Contents

Management’s Discussion & Analysis

The following table highlights the significant changes in adjusted net income from 2016 to 2017:

| For the | Three months ended | Year ended | ||||||||||||||

| millions of Canadian dollars | December 31 | December 31 | ||||||||||||||

| Adjusted net income – 2016 |

$ | 104 | $ | 475 | ||||||||||||

| Emera Florida and New Mexico |

17 | 210 | ||||||||||||||

| 2016 acquisition and financing costs related to the acquisition of TECO Energy |

(13 | ) | 166 | |||||||||||||

| NSPML and LIL AFUDC earnings |

6 | 28 | ||||||||||||||

| 2016 Emera Energy’s recognition of fuel taxes for 2013 to March 2016 |

— | 12 | ||||||||||||||

| NSPI |

(11 | ) | (1 | ) | ||||||||||||

| Emera Energy |

21 | (12 | ) | |||||||||||||

| APUC equity earnings – sold in 2016 |

— | (18 | ) | |||||||||||||

| Emera Caribbean |

(7 | ) | (26 | ) | ||||||||||||

| 2016 gain on BLPC SIF regulatory liability |

— | (43 | ) | |||||||||||||

| 2016 gain on conversion of APUC subscription receipts and dividend equivalents to common shares of APUC |

— | (53 | ) | |||||||||||||

| TECO Energy post-acquisition financing costs |

— | (83 | ) | |||||||||||||

| 2016 gain/loss on sale of APUC common shares |

10 | (136 | ) | |||||||||||||

| Other |

10 | 5 | ||||||||||||||

| Adjusted net income – 2017 |

$ | 137 | $ | 524 | ||||||||||||

| For the | Year ended December 31 |

|||||||||||||||

| millions of Canadian dollars | 2017 | 2016 | 2015 | |||||||||||||

| Operating cash flow before changes in working capital |

$ | 1,297 | $ | 919 | $ | 776 | ||||||||||

| Change in working capital |

(104 | ) | 134 | (102 | ) | |||||||||||

| Operating cash flow |

$ | 1,193 | $ | 1,053 | $ | 674 | ||||||||||

| Investing cash flow (1) |

$ | (1,761 | ) | $ | (9,037 | ) | $ | (124 | ) | |||||||

| Financing cash flow |

$ | 593 | $ | 7,448 | $ | 221 | ||||||||||

|

(1) These financial statements contain certain reclassifications of prior period amounts to be consistent with the current period presentation, with no effect on net income. |

|

|||||||||||||||

| As at | December 31 | |||||||||||||||

| millions of Canadian dollars | 2017 | 2016 | 2015 | |||||||||||||

| Total assets |

$ | 28,771 | $ | 29,221 | $ | 12,039 | ||||||||||

| Total long-term debt (including current portion) |

$ | 13,881 | $ | 14,744 | $ | 4,009 | ||||||||||

Emera Inc. — Annual Report 2017 17

Table of Contents

Q4 Consolidated Income Statement Highlights

Operational Results

Income from operations increased $28 million to $236 million in Q4 2017 compared to $208 million in the same quarter in 2016. Absent mark-to-market losses of $23 million, income from operations increased $51 million due to increased contributions from Emera Florida and New Mexico and Emera Energy.

Details of operating revenues and operating expenses line item variances are described below:

Total operating revenues decreased $40 million to $1,473 million in Q4 2017 compared to $1,513 million in Q4 2016. Absent mark-to-market losses of $13 million, operating revenues decreased $27 million due to:

| • | $17 million decrease from Emera Florida and New Mexico reflecting the impact of a stronger CAD. This decrease was partially offset by increased revenues at Tampa Electric reflecting customer growth and higher base rates offset by lower clause-related revenues; |

| • | $10 million decrease from Emera Utility Services (“EUS”) reflecting decreased project activity. |

Total operating expenses decreased $68 million to $1,237 million in Q4 2017 compared to $1,305 million in Q4 2016. This is primarily due to the impact of a stronger CAD, lower operating, maintenance and general (“OM&G”) expense at Emera Florida and New Mexico reflecting lower generation outage and maintenance costs, lower fuel expense at Tampa Electric and decreased natural gas purchases at Bayside Power reflecting the renegotiation of the Bayside Power PPA for the winter of 2017/2018.

Income tax expense (recovery)

Income tax expense increased $335 million to a $329 million expense in Q4 2017 compared to a $6 million recovery for the same period in 2016 primarily due to the estimated impact of the enacted US federal corporate income tax rate reduction from US tax reform (refer to the “Developments” section for further details) and increased income before provision for income taxes.

18 Emera Inc. — Annual Report 2017

Table of Contents

Management’s Discussion & Analysis

2017 Consolidated Income Statement and Operating Cash Flow Highlights

Operational Results

Income from operations increased $836 million to $1,391 million for the year ended December 31, 2017 compared to $555 million in 2016. Absent mark-to-market increases of $267 million, income from operations increased $569 million mainly due to the contribution of Emera Florida and New Mexico for the full year of 2017 and the 2016 costs related to the acquisition of TECO Energy.

Details of operating revenues and operating expenses line item variances are described below:

Total operating revenues increased $1,949 million to $6,226 million for the year ended December 31, 2017 compared to $4,277 million in the same period in 2016. Absent mark-to-market increases of $285 million, operating revenues increased $1,664 million due to:

| • | $1,784 million increase from Emera Florida and New Mexico as 2017 includes a full year of revenues; |

| • | $115 million decrease at Emera Energy Generation (“EEG”) reflecting lower hedged power prices in Q1 2017 compared to Q1 2016, decreased sales volumes driven by an unplanned outage at the Bridgeport Facility and less favourable market conditions in 2017. This decrease was partially offset by higher capacity revenue that came into effect for New England Gas Generating Facilities (“NEGG”) in June 2017. |

Total operating expenses increased $1,113 million to $4,835 million for the year ended December 31, 2017 compared to $3,722 million in 2016, primarily due to:

| • | $1,285 million increase from Emera Florida and New Mexico as 2017 includes a full year of expenses; |

| • | $116 million decrease in fuel expense at EEG due to decreased sales volumes reflecting an unplanned outage at the Bridgeport Facility, lower hedged natural gas prices in Q1 2017 compared to Q1 2016, the recognition of prior period state fuel taxes in Q2 2016 and less favourable market conditions in 2017; |