Form 6-K BROOKFIELD ASSET MANAGEM For: Nov 13

FREE Breaking News Alerts from StreetInsider.com!

StreetInsider.com Top Tickers, 6/12/2026

- Wall Street ends higher as SpaceX's market debut dominates

- SpaceX prices historic IPO at $135/share in largest ever new listing

- 'Ocean of opportunity': Wolfe initiates SpaceX at Buy ahead of historic IPO

- UBS cuts gold price forecasts on delayed Fed easing outlook

- Brent falls to lowest since March on expected peace deal

- NASDAQ adds five companies to NASDAQ-100 index in quarterly rebalance

- Adobe CFO Dan Durn to depart company in June 2026

- Oppenheimer Starts SpaceX (SPCX) at Outperform, PT $190, 'space infrastructure appears structurally advantaged'

- Pentagon reportedly locked down, hazmat teams responding

- Super Micro Computer establishes $1.25 billion stock sale agreement

Tweet

Tweet Share

Share�

�

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

�

�

FORM 6-K

�

�

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of November, 2014

Commission File Number: 033-97038

�

�

BROOKFIELD ASSET MANAGEMENT INC.

(Translation of Registrant�s Name into English)

�

�

Suite�300, Brookfield Place, 181 Bay Street, P.O. Box 762, Toronto, Canada M5J 2T3

(Address of Principal Executive Offices)

�

�

Indicate by check mark whether the registrant files or will file annual reports

under cover of Form�20-F or Form�40-F.

Form�20-F�������������� �Form�40-F��x

Indicate by check mark if the registrant is submitting the Form 6-K in paper

as permitted by Regulation S-T Rule 101(b)(1): ������

Indicate by check mark if the registrant is submitting the Form 6-K in paper

as permitted by Regulation S-T Rule 101(b)(7): ������

Indicate by check mark whether the registrant by furnishing the information

contained in this form is also thereby furnishing the information to the

Commission pursuant to Rule�12g3-2(b) under the Securities Exchange Act of 1934.

Yes���������������No� �x

(If �Yes� is marked, indicate below the file number assigned to the registrant

in connection with Rule�12g3-2(b): 82- ������.

�

�

�

DOCUMENTS FILED AS PART OF THIS FORM 6-K

See the Exhibit Index to this Form 6-K.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

�

| � | � | BROOKFIELD ASSET MANAGEMENT INC. | ||||

| Date: November�13, 2014 | � | � | By: | � | /s/ A.J. Silber | |

| � | � | Name: | � | A.J. Silber | ||

| � | � | Title: | � | Corporate Secretary | ||

EXHIBIT INDEX

�

| Exhibit |

�� | Description |

| 1 | �� | Interim Report to Shareholders |

| �� | Interim Report to Shareholders of Brookfield Asset Management Inc. for the quarter ended September�30, 2014 | |

| 2 | �� | Certification of Chief Executive Officer pursuant to Canadian Law |

| 3 | �� | Certification of Chief Financial Officer pursuant to Canadian Law |

�

Exhibit 1

�

Interim Report Q3 2014

�

| � | �� | Three�Months�Ended�Sep.�30 | � | � | Nine�Months�Ended�Sep.�30 | � | ||||||||||

| FOR THE PERIODS ENDED (MILLIONS, EXCEPT PER SHARE AMOUNTS) |

�� | 2014� | � | �� | 2013� | � | � | 2014� | � | � | 2013� | � | ||||

| � |

� | |||||||||||||||

| Consolidated net income1 |

�� | $ | 1,109� | �� | �� | $ | 1,495� | �� | � | $ | 3,510� | �� | � | $ | 2,994� | �� |

| Funds from operations2,3 |

�� | � | 564� | �� | �� | � | 1,193� | �� | � | � | 1,625� | �� | � | � | 2,346� | �� |

| Per Brookfield share |

�� | �� | � | � | ||||||||||||

| Net income2 |

�� | $ | 1.09� | �� | �� | $ | 1.23� | �� | � | $ | 3.07� | �� | � | $ | 2.05� | �� |

| Funds from operations2,3 |

�� | � | 0.83� | �� | �� | � | 1.85� | �� | � | � | 2.39� | �� | � | � | 3.56� | �� |

| � 1.�������Consolidated basis � includes amounts attributable to non-controlling interests 2.�������Excludes amounts attributable to non-controlling interests 3.�������See basis of presentation on page 21 � |

���������� ���������� ���������� | |||||||||||||||

| � | �� | � | � | �� | � | � | � | As at | � | |||||||

| (MILLIONS, EXCEPT PER SHARE AMOUNTS) | � | �� | � | � | � | Sep.�30,�2014 | � | � | Dec.�31,�2013 | � | ||||||

| Assets under management |

�� |

�� | � | $ | �����192,863� | �� | � | $ | �����187,105� | �� | ||||||

| Consolidated balance sheet assets |

�� | �� | � | � | 118,232� | �� | � | � | 112,745� | �� | ||||||

| Fee bearing capital |

�� | �� | � | � | 84,369� | �� | � | � | 79,293� | �� | ||||||

| Diluted number of common shares outstanding |

�� | �� | � | � | 654.6� | �� | � | � | 651.1� | �� | ||||||

| Market trading price per share � NYSE |

�� | �� | � | $ | 44.96� | �� | � | $ | 38.83� | �� | ||||||

| � |

� | |||||||||||||||

�

| � | Q3 2014 INTERIM REPORT | � | 1 |

| � ��LETTER TO SHAREHOLDERS � |

Dear shareholders,

Overview

Financial results in the quarter were strong with net income of $1.1 billion or $1.09 per common share and FFO of $564 million or $0.83 per share. Both strong operations and value increases contributed to the results during the quarter.

Total assets under management were approximately $200 billion at quarter end, with $84 billion in fee bearing capital, up 14% over the same period last year. This capital is split $39 billion in our listed partnerships, $28 billion in private funds and $17 billion in our public markets business. Institutional investors continue to allocate increasing amounts of their portfolio to real assets.

Our flagship institutional funds for property and private equity are now virtually fully committed and we are in a position to launch a new generation of funds. We expect to raise approximately $20 billion for successor funds in the next few years, and each of these flagship funds should be substantially larger than its predecessor.

Our public markets group, which invests in real assets through portfolios of listed securities, grew assets under management by $4 billion compared to last year. The increase reflects both new mandates from clients and value increases.

Long-term Plans

Our long-term goal is to ensure Brookfield remains as one of the premier global brands for real asset investing. Today, we are among the largest in the world in our four real asset businesses � property, renewable energy, infrastructure and private equity. We continue to build out our franchise to keep it this way.

The environment has been particularly favourable to achieving growth over the past five years, as our clients� capital resources have been growing and they are allocating a greater percentage of their capital to real assets. In addition, virtually all real assets have increased in value over this period. This has enabled us to show excellent track records in our funds and therefore allowed us to attract increased allocations of capital from clients as our fund sizes grow.

Looking out 10 years, we believe that each of our strategies should be able to deploy on average $40 billion of capital, mixed between listed and unlisted strategies. As such, our objective is to increase fee bearing capital from the current level of approximately $85 billion to more than $200 billion in 10 years� time, representing a 10% annual growth rate. And if we are successful in achieving a 1.5% margin on this capital, which we consider to be attainable based on terms for funds currently in the market, we should be able to generate $3 billion of annual cash flow by the end of this period. Valued at 15x, consistent with valuations publicly ascribed to other alternative asset managers, this would represent $45 billion for a part of our business that was ascribed relatively minimal value five to 10 years ago. Furthermore, this value does not include the roughly $30 billion of capital on our balance sheet that we invest alongside clients. We believe we can continue to increase the value of this capital at attractive rates, which represents another source of potential growth in shareholder value. Finally, along the way there may be opportunities to repurchase shares back into treasury at attractive prices and therefore increase the per share compounding effect of the aforementioned increases in shareholder value. Of course, no plans are without risks but we believe we are firmly on this path and have a strong backdrop to work from.

We need three factors to be in our favour in order to achieve these results. The first is continued allocations by global institutional investors to real assets. To date, we see nothing stopping this. In fact, we see the opposite � allocations continue to increase.

The second factor is our ability to find transactions and invest capital at returns which meet our targets. This always seems to be the most undeterminable factor, but so far we have grown our business to $200 billion of assets under management over the past 20 years. We have built a company with a strong investment culture that cares about all of the funds we invest. While never easy, we don�t see any reason we cannot scale the business further.

The third item that plays into our long-term success is global conditions that are positive for business. This is not entirely in our control, but we do attempt to invest on a contrarian basis in order to give us a competitive advantage. We attempt to invest where capital is scarce, and this allows us to avoid many of the risks that can come from growth investing. During just the past 20 years, we invested through the crises of 1993, 1998, 2003 and 2008 and we have compounded returns at approximately 19% for our shareholders despite pretty brutal conditions in some of those years. There surely will also be some tough years ahead but we invest so we can, at a minimum, endure and possibly even move forward during these challenging periods.

Global Markets

One of our major competitive advantages is that we have operations in over 25 countries. These teams of investment and operating professionals enable us to act on market inefficiencies as they arise. Today, developed markets are generally flush with cash but a number of emerging markets are lacking capital. As a result, our recent focus has been on the latter.

�

�

| 2 | � | BROOKFIELD ASSET MANAGEMENT | � |

�

The U.S. economy continues to improve and has set a base for acceptable GDP growth and a strong currency looking forward. Due to our sheer scale in the United States we always find lots of opportunities to invest there; however we increased our allocation of capital over the last 18 months to Brazil, China, India and Europe. We believe that this will continue for years to come.

India saw a greater reversal of foreign capital over the past three years than any other major market. This forced yields up and the lack of capital changed asset values significantly. Whereas in 2007 it seemed like every investor in the world was targeting India; today it is very different. We have been in India for seven years but had a hard time reconciling the valuations of assets until recently. This change led to a number of acquisitions in the past 18 months and should lead to more. Shortly after the quarter, we closed on the acquisition of a portfolio of 17�million square feet of properties in India. The recent change in government appears to be positive for the country, although we believe it will be years until the robustness of capital markets return.

Brazil is currently in technical recession and most investors who only arrived in Brazil in the last five years have experienced stress as the currency is down, interest rates are high and valuations are generally lower. Thankfully we have a long association with Brazil and are therefore experienced with these markets. We have made significant new investments over the past 12 months, and will continue to make more. We acquired a rail and port business, expanded our toll road business, are privatizing our residential development operations, and have invested follow-on capital in many of our operations. As a result of the economic situation, we believe that we will find many more transactions over the next few years. With the federal elections now complete, we are hopeful that the country will work towards being back on the path to reasonable GDP growth. While we are positive on Brazil in the longer term, we also recognize that this change will probably not happen overnight.

China has slower GDP growth than most expected but one must remember the law of large numbers. The amount of growth in China�s GDP today at a low 7% rate is the same as the amount generated by an 8% growth rate only a few years ago. In addition, many of the measures which people have historically reviewed to gauge the health of the Chinese economy appear to be less relevant today with the evolving consumer-led economy. When one travels in China, one can see the sheer scale of this bustling entrepreneurial country. This region is poised for strong longer term growth, even though in the short term China may have issues like every economy sometimes does as they consolidate. We continue to widen our real estate investing in China, and while we are in the early stages of our engagement, we believe that this is a good time to expand our presence.

In Europe, the story is about �value� and �deleveraging,� not growth. There is significant deleveraging to still occur among most of the governments, banks and selective corporates. While we do not believe that the Eurozone will see what would have been historically normalized growth for a long time, we do believe that there is still a significant opportunity to put capital to work. On the economic front, our underwriting assumes extremely low interest rates and a declining Euro currency for a while. The vast savings of the individuals in the European countries will, slowly over time, be eroded with negative real rates of return. This, combined with modest growth and some expense discipline, will eventually ensure that the fiscal situations of the Eurozone will improve, but this will take time.

Investment Process

Our competitive advantages are size of capital, global scale and operating platforms. These three together enable us to move capital to where it is scarce and access opportunities that many cannot. As a result, this should enable us to continue to invest at stronger returns on capital than would otherwise be the case.

Our new investments usually fit into two categories. The first is a purchase for value, often measured as a discount to tangible value, and the second is a purchase of an asset that we can drive more value out of because of our operating platform. Ideally we can combine both.

Many of our initial investments are made as value purchases. Sometimes this occurs by us buying debt at discounts and converting it through a reorganization into equity, sometimes we bid in bankruptcy auctions, sometimes we buy stakes in public companies under stress and privatize them, and other times we assist entities with assets seeking liquidity to find a home for their operations. Examples of these are our purchases of General Growth Properties, Babcock�& Brown Infrastructure, Reliant Energy Hydro, and UCP India real estate.

The second form of investing we participate in are repeatable investments in areas where we already have scale and knowledge. For example, in the last 20 years we have acquired over 200 renewable power plants, 200 office properties, 150 regional malls and 30 ports. As a consequence, the next one that comes along is relatively easy for us to understand and value. We therefore can offer quick decisions to sellers, and as we are known in the business, we often get the first call, sometimes avoiding auctions. In either event, sellers can be confident dealing with us, as we know the assets well, and have been through the same process numerous times before. As a result, within very short timeframes, we can close transactions.

A recent example of a repeatable investment strategy is our district energy infrastructure business. We identified this as a sector, as we believed scale could be built, barriers to entry were high, and there were few significant competitors. Furthermore, we had a competitive advantage due to our vast real estate operations and knowledge from this business. In 2011, we acquired our first system in Toronto. Since then, we have acquired the systems in Chicago, Houston, New Orleans, Seattle and Las Vegas. This repeatable process of acquisition has allowed us to build scale, and our people know the intricacies of acquiring the additional systems, integrating them with our business, and growing the operations organically afterward to enhance returns.

�

| � | Q3 2014 INTERIM REPORT | � | 3 |

Operations

We continued to increase both the quantity and quality of our fee bearing capital, with the result that annualized base management fees based on the contractual terms of in-place funds increased to $630 million at quarter end, up 19% from the same date last year. Fee bearing capital totalled $84 billion, up 14% from the end of the 2013 quarter.

Total fee revenues including incentive distributions, public market performance fees and transaction fees increased by 21% on a last twelve months (�LTM�) basis to $721 million, resulting in $346 million of LTM fee related earnings after direct costs, representing a 50% operating margin, consistent with our near term objectives.

Two of our three flagship funds (property, infrastructure and renewable energy, and private equity) are more than 90% invested, which enables us to launch successor funds prior to the expiry of their original investment periods. We raised $4 billion of fund capital over the past twelve months and currently have four funds in the market, including two flagship funds, seeking to raise more than $12 billion of capital; which if successful would allow us to continue to build on our track record of expanding fee bearing capital.

We continue to look for alternatives to grow our overall asset management business. These opportunities generally fit into three categories. The first is that we are continuously increasing the scale of our operations so that we can prudently put larger amounts of capital to work. This enables us to raise larger private funds for clients. In this regard, our flagship funds are growing significantly and our expectation is that each of our flagship funds will nearly double in size, which we believe gives us a competitive advantage versus many others.

Second, we have been adding complementary listed and unlisted funds for our clients. Originally we found that some of our smaller clients were not set up to invest in our private funds due to a greater need for liquidity. This led to the creation of listed long-only and long/short strategies in infrastructure and real estate; and we have attracted significant assets under management in these strategies. More recently we have added other complementary products which will ultimately be offered to our clients.

Lastly, we may add region-specific sleeves of capital for some of our funds, such as an Asian or European focused fund. We have generally chosen to keep our mandates as flexible as possible to maximize the opportunity set of investments. But some of our institutional clients are interested in greater capital deployment in some specific markets and this will allow us to scale the business further, and also be attentive to the needs of some of our investors who may wish to either have greater exposure or alternatively limit their exposure to some markets.

Brookfield Property Group

Our property group had strong results and is moving forward with growth initiatives in our office, retail and multifamily businesses. FFO was $136 million, up 12% from the same quarter last year. With the North American economic recovery picking up, we are seeing occupancy rates rise and we are signing new leases in our office buildings and retail malls at significant uplifts over expiring rents.

Over the next five years, we believe we can increase FFO at Brookfield Property Partners (BPY) on average by 8% to 11% annually, due to increased rents on expiring leases, occupancy gains, new leases and new developments coming online. Based on this, we recently increased the distribution growth target for BPY to 5%-8% annually.

During the quarter, we expanded our portfolio with a number of acquisitions. We acquired 16�million square feet of U.S. net leased commercial properties for $4.3 billion, six apartment buildings in New York for $1.1 billion, shopping malls in Florida, Washington state and New York, a 270,000 square foot office building in S�o Paulo, and a hotel in Florida.

In London, we signed a 430,000 sq. ft. lease with online retailer Amazon for their European headquarters, and launched construction of both their office tower and an adjacent residential tower. At Brookfield Place New York, we signed a number of leases to increase occupancy to 95%.

Brookfield Infrastructure Group

During the quarter, FFO from our infrastructure group was $55 million, in line with expectations. We invested approximately $1 billion by completing acquisitions of a Brazilian railway network, three district energy businesses and a California natural gas storage facility. Our backlog of internal investment projects is approximately $1.2 billion, up from $700 million a year ago, with most of this capital earmarked for expansion of our toll roads, railways and ports in South America.

We continue to acquire assets from businesses in Europe, as many companies and financial institutions are selling infrastructure assets to recapitalize and focus their operations. Our investments in Europe to date have been focused on utilities and toll roads, although subsequent to quarter end, we committed to acquire a 50% interest in a portfolio of 6,700 telecommunications towers in France for $2.2 billion. These towers are essential infrastructure for broadcasters and telecom companies.

Brookfield Renewable Energy Group

Results for the year in our renewable energy group look to be on plan. During the quarter, FFO was $28 million, which was lower than the same quarter last year, reflecting lower-than-average water levels and wind generation in Canada. Generation is slightly below long-term averages on a LTM basis, however market pricing has been favourable.

�

�

| 4 | � | BROOKFIELD ASSET MANAGEMENT | � |

�

Growth in our renewable energy business will come from a combination of the inflation-linked escalations in electricity prices, long-term increases in energy prices, and development projects. Taken together, these three factors are expected to add up to $300 million to annual FFO over the next five years, without taking into account growth through acquisitions. Based on this growth, we increased the distribution growth target of Brookfield Renewable to 5%-9% annually.

During the quarter, we completed the acquisition of a Pennsylvania hydroelectric facility for $613 million and moved forward with developments in North America, Brazil and Ireland.

Brookfield Private Equity Group

FFO for our private equity business on a normalized basis was $110 million in the quarter. Our private equity group is harvesting capital from investments made in housing-related businesses, while investing in businesses that should benefit from a recovery of natural gas prices.

We added to our natural gas reserves in western Canada, acquiring assets for $540 million from a major energy company that wanted to exit their coal-bed methane business. This, combined with five acquisitions over the past four years, has enabled us to build one of North America�s largest coal-bed methane producers.

We hope to close on the acquisition of the balance of the shares of our Brazilian land development and homebuilding business shortly. During the quarter, we also announced an $846 million bid to acquire the other 30% of the shares in our similar North American entity, which should be completed in the first quarter of 2015. We are also working to close on the purchase of the Revel Casino in Atlantic City, which is being done jointly with the property group.

Summary

We remain committed to being a world-class alternative asset manager, and investing capital for you and our investment partners in high-quality, simple-to-understand assets which earn a solid cash return on equity, while emphasizing downside protection for the capital employed.

The primary objective of the company continues to be generating increased cash flows on a per share basis, and as a result, higher intrinsic value per share over the longer term.

And, while I personally sign this letter, I respectfully do on behalf of all of the members of the Brookfield team, who collectively generate the results for you. Please do not hesitate to contact any of us, should you have suggestions, questions, comments, or ideas you wish to share with us.

�

�

�

����

J. Bruce Flatt

Chief Executive Officer

November�7, 2014

�

| � | Q3 2014 INTERIM REPORT | � | 5 |

MANAGEMENT�S DISCUSSION AND ANALYSIS OF FINANCIAL RESULTS

Our Management�s Discussion and Analysis (�MD&A�) is provided to enable a reader to assess our results of operations and financial condition for the interim period ended September�30, 2014. This MD&A should be read in conjunction with our 2013 Annual Report. Unless the context indicates otherwise, references in this Report to the �Corporation� refer to Brookfield Asset Management Inc., and references to �Brookfield,� �us,� �we,� �our� or �the company� refer to the Corporation and its direct and indirect subsidiaries and consolidated entities. All amounts are in U.S. dollars, and are based on financial statements prepared in accordance with International Financial Reporting Standards (�IFRS�), as issued by the International Accounting Standards Board unless otherwise noted.

Additional information about the company, including our 2013 Annual Information Form, is available free of charge on our website at www.brookfield.com, on the Canadian Securities Administrators� website at www.sedar.com and on the EDGAR section of the U.S. Securities and Exchange Commission�s (�SEC�) website at www.sec.gov.

�

| Organization of the MD&A � | ||||||||||

| PART�1���Overview and Outlook |

� | � | PART 3 � Operating Segment Results |

� | PART 4 � Capitalization and Liquidity | |||||

| Our Business |

� | 7�� | � | Basis of Presentation |

� | 21�� | � | Capitalization |

� | 34�� |

| Economic and Market Review |

� | 8�� | � | Summary�of�Results�by�Operating |

� | � | Liquidity |

� | 38�� | |

| � | � | � | 22�� | � | Review�of�Consolidated�Statements |

� | ||||

| PART�2���Financial Performance Review |

� | � | Asset Management |

� | 24�� | � | � | 39�� | ||

| � | � | Property |

� | 26�� | � | � | ||||

| Selected Financial Information |

� | 10�� | � | Renewable Energy |

� | 28�� | � | PART 5 � Additional Information | ||

| Financial Performance |

� | 10�� | � | Infrastructure |

� | 30�� | � | Accounting Policies and Internal |

� | |

| Financial Profile |

� | 15�� | � | Private Equity |

� | 31�� | � | � | 40�� | |

| Summary of Quarterly Results |

� | 19�� | � | Residential Development |

� | 31�� | � | Management Representations |

� | |

| Corporate Dividends |

� | 20�� | � | Service Activities |

� | 32�� | � | � | 41�� | |

| � | � | Corporate Activities |

� | 33�� | � | � | ||||

We provide additional information on our basis of presentation of financial information contained in the MD&A and key financial measures on pages 34 and 35 of our December�31, 2013 Annual Report.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS AND USE OF NON-IFRS MEASURES

This Report to Shareholders contains �forward-looking information� within the meaning of Canadian provincial securities laws and �forward-looking statements� within the meaning of Section�27A of the U.S. Securities Act of 1933, as amended, Section�21E of the U.S. Securities Exchange Act of 1934, as amended, �safe harbor� provisions of the United States Private Securities Litigation Reform Act of 1995 and in any applicable Canadian securities regulations. We may provide such information and make such statements in the Report, in other filings with Canadian regulators or the U.S. Securities and Exchange Commission or in other communications. See �Cautionary Statement Regarding Forward-Looking Statements and Information� on page 42.

We disclose a number of financial measures in this Report that are calculated and presented using methodologies other than in accordance with IFRS. We utilize these measures in managing the business, including performance measurement, capital allocation and valuation purposes and believe that providing these performance measures on a supplemental basis to our IFRS results is helpful to investors in assessing the overall performance of our businesses. These financial measures should not be considered as a substitute for similar financial measures calculated in accordance with IFRS. We caution readers that these non-IFRS financial measures may differ from the calculations disclosed by other businesses, and as a result, may not be comparable to similar measures presented by others. Reconciliations of these non-IFRS financial measures to the most directly comparable financial measures calculated and presented in accordance with IFRS, where applicable, are included within this MD&A.

�

�

�

Information contained in or otherwise accessible through the websites mentioned does not form part of this Report. All references in this Report to websites are inactive textual references and are not incorporated by reference.

�

�

| 6 | � | BROOKFIELD ASSET MANAGEMENT | � |

�

PART 1 � OVERVIEW AND OUTLOOK

OUR BUSINESS

Brookfield is a global alternative asset manager with approximately $200 billion in assets under management. For more than 100 years we have owned and operated assets on behalf of shareholders and clients with a focus on property, renewable energy, infrastructure and private equity.

We manage a wide range of investment funds and other entities that enable institutional and retail clients to invest alongside us in these assets and earn fees, carried interests and other forms of performance income for doing so. As at September�30, 2014, our managed funds and listed partnerships represented $84 billion of invested and committed fee bearing capital. These products include publicly listed partnerships that are listed on major stock exchanges as well as private institutional partnerships that are available to accredited investors, typically pension funds, endowments and other institutional investors. We also manage portfolios of listed securities through a series of segregated accounts and mutual funds.

In addition, we have $26 billion of capital invested in our operations, based on IFRS carrying values, most of which is invested in our listed partnerships.

Our business model is simple: (i)�raise pools of capital from ourselves and clients that target attractive investment strategies (ii)�utilize our global reach to identify and acquire high quality assets at favourable valuations, (iii)�finance them on a long-term basis, (iv)�enhance the cash flows and values of these assets through our operating platforms to earn reliable, attractive long-term total returns, and (v)�realize capital from asset sales or refinancings when opportunities arise.

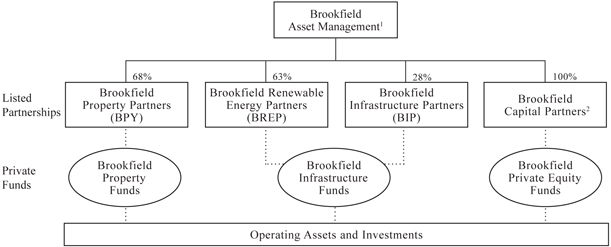

Organization Structure

Our operations are organized into four principal groups (�operating platforms�): property, renewable energy, infrastructure and private equity. These platforms are responsible for operating the assets owned by our various funds and investee companies. The equity capital invested in these assets is provided by a series of listed partnerships and private funds which are managed by us and are funded with capital from ourselves and our clients. A fifth group operates our public markets business.

We have formed a large capitalization listed partnership in each of our property, renewable energy and infrastructure groups, which serves as the primary vehicle through which we will invest in each respective segment. As well as owning assets directly, these partnerships serve as the cornerstone investors in our private funds, alongside capital committed by institutional investors. This approach enables us to attract a broad range of public and private investment capital and the ability to match our various investment strategies with the most appropriate form of capital.

Our private equity business is conducted primarily through private funds with capital provided by institutions and ourselves. We do not currently envisage the formation of a listed partnership within these operations as we do not believe these investments would be properly valued in the capital markets on a standalone basis.

Our balance sheet capital is invested primarily in our three flagship listed partnerships, Brookfield Property Partners L.P. (�BPY� or �Brookfield Property Partners�); Brookfield Renewable Energy Partners L.P. (�BREP� or �Brookfield Renewable Energy�); and Brookfield Infrastructure Partners L.P. (�BIP� or �Brookfield Infrastructure Partners�), our private equity funds, and in several directly held investments and businesses.

The following chart is a condensed version of our organizational structure:

�

�

| 1. | Includes asset management and corporate activities |

� |

| 2. | Privately held, includes private equity, residential development and service activities |

� |

�

| � | Q3 2014 INTERIM REPORT | � | 7 |

ECONOMIC AND MARKET REVIEW

(As at October�30th, 2014)

Overview and Outlook

Real GDP growth in the U.S. is approaching the 3.0% run-rate that we have been expecting, despite the somewhat sluggish recovery in the housing sector. This bodes well for our positive outlook on the U.S., as we continue to believe that residential construction should return to more normal levels, suggesting a meaningful level of potential support for current growth momentum. Real GDP growth of 2.5% for the Canadian economy in the third quarter was consistent with our expectation, although the strength in the housing market has persisted longer and the increase in net exports has arrived a bit sooner than we anticipated. Nevertheless, we continue to believe Canada will underperform the U.S. slightly, which along with weaker commodity prices, should put additional downward pressure on the Canadian dollar. The recovery in the UK continues to be strong, with growth of 3.0% in the third quarter, as private consumption and business investment remained robust. However, the growing current account deficit raises concerns about the stability of the UK funding model moving forward. Eurozone real GDP growth was subdued again this quarter at 0.7%. As expected, weak growth and low inflation, together with the contraction of total credit, has prompted the European Central Bank to implement its own quantitative easing program. This will keep interest rates near historical lows in the Eurozone even as other central banks start to normalize policy rates next year. We expect the Eurozone will continue on a fairly modest growth path over the next few years but low interest rates and a weaker Euro should provide support as the deleveraging cycle plays out. Real GDP growth in Brazil stalled in the third quarter as dry conditions have pushed power prices to record highs, which has weighed on industrial production. While consumer and business confidence have both declined substantially in Brazil, the depreciation of the Real over the past few years and a return to normal hydrological conditions should provide a lift to industrial activity and help push Brazil�s economic growth closer to 3 � 4% over the medium term. In China, real GDP growth slowed to 7.3% as property markets remain under pressure. Longer term, rebalancing of the Chinese economy away from investment towards consumption will lead to slower growth rates, but this should be expected given the sheer size of this economy following 30+ years of rapid growth. Australian GDP growth slowed modestly to 3.0% in the third quarter as declining commodity prices has led to declines in mining investment, reducing the momentum in underlying growth.

United States

The U.S. economy grew 3.5% in the third quarter, as fiscal headwinds have abated and robust consumption growth and an increase in private business investment all contributed to strong real GDP growth. The pace of expansion is expected to moderate to about 3.0% for the rest of 2014 and into 2015. The labour market also continued to improve over the quarter with job creation averaging 224,000�per month and the unemployment rate falling to 5.9% in September. Despite slow wage growth, rising employment and gains in household wealth have led to increased consumption. Going forward, lower oil prices will be an additional source of support for U.S. consumers, with global oil benchmarks down 20�25% since early July. The decline in oil prices is due, in part, to stronger U.S. oil production, which continues to grow at a 1�million barrel per day pace. Housing starts remained slightly below 1�million units in the third quarter as first-time home buyers continue to experience difficulty in accessing credit. Encouragingly, we are starting to see a pickup in household formation and we expect that further economic recovery will see this pent-up demand return to the market. While demand-side weakness likely explains most of the sluggishness in residential construction so far, we would also note that some markets are seeing skilled labour shortages and experiencing difficulties in bringing lots to market. Commercial and industrial loans outstanding rose 12% on a year-over-year basis in the third quarter and non-residential business investment was up 6.8% last quarter. We have been expecting business investment to play a more important role in the growth story this year and are encouraged by these recent data-points. The U.S. dollar strengthened significantly against major currencies this quarter, gaining approximately 8% versus the Yen, Euro and Australian dollar and approximately 5% versus the Pound and Canadian dollar.

Canada

Economic activity in Canada grew by approximately 2.5% in the third quarter as export growth surprised to the upside. Exports were up 5.1% on a year-over-year basis last quarter and appear to be on pace for another strong result this quarter, which should continue to benefit from an improving U.S. economy. The housing sector remained stable, with housing starts at an annualized rate of 200,000 and house prices rising approximately 5% on a year-over-year basis. However, we expect to see the housing sector eventually slow as housing starts are running above demographic demand and households in Canada have significantly increased their debt levels over the past few years. The Bank of Canada is expected to remain cautious as the economy adjusts to lower commodity prices and weaker domestic demand, suggesting that increases in short-term interest rates in Canada will likely lag U.S. rate increases, despite starting from a higher base. This should put additional downward pressure on the Canadian dollar, which fell below US$0.90 this quarter.

United Kingdom

Growth and employment in the UK have been stronger than expected thus far in 2014, a trend which continued in the third quarter with GDP growth of 3.0% year-over-year, supported by both consumption and business investment. Retail sales growth remained strong at 2.6% in September while the 11.0% increase in business investment observed last quarter is expected to

�

�

| 8 | � | BROOKFIELD ASSET MANAGEMENT | � |

�

continue. The unemployment rate has fallen to 6.0%, down 1.7 percentage points since last year and is now at its lowest level since late 2008. The tightening labour market, however, has not yet translated into faster wage growth and the Bank of England has indicated that this will be one of the key indicators they will use to determine the timing of the first interest rate hike. The Purchasing Managers Index (PMI) for the construction and services sectors are still pointing to strong expansion while the PMI for the manufacturing sector has weakened over the quarter owing to concerns that the stronger Pound will reduce UK manufacturers� relative competitiveness. Over the past year the Pound has appreciated by 6.5% versus the Euro and while it had appreciated against the U.S. dollar earlier in the year, recent U.S. dollar strength has since erased those gains. The current account deficit in the UK is at record levels, and while it is difficult to foresee a scenario where London financial markets lose their attractiveness as a haven for global capital flows, this imbalance raises the risk of an external adjustment via a weaker Pound if this source of funding were to disappear.

Eurozone

Eurozone GDP growth remained subdued at 0.7% on a year-over-year basis in the third quarter with a modest improvement in peripheral countries offset by a deceleration in Germany. Over the period, France and Germany grew by 0.3% and 1.3%, respectively on a year-over-year basis while Portugal, Spain and Ireland each grew between 1.0% and 1.5%. German industrial production contracted by 4.0% month-over-month in August and the PMI suggests that activity has stalled. This has raised concerns that Germany may slip into a mild recession this quarter. Inflation continued to slow, with core inflation in nearly all Eurozone countries trending lower. For the Eurozone as a whole, the core inflation rate was only 0.8% year-over-year in September while domestic credit to the private sector has contracted 8.2% since 2009 and shows no signs of improving. In response to weak growth and low inflation, the European Central Bank has reduced its main lending rate to 0.05% and its deposit rate below 0.0%, and is implementing two quantitative easing programs that will target lending to firms and households as well as the direct purchase of asset backed securities. The key question for the Eurozone over the next several years is whether these programs will help ease the impact of deleveraging and help return growth and inflation to more sustainable levels.

Brazil

Brazil real GDP stalled in the third quarter following a contraction of 0.9% on a year-over-year basis in the previous quarter. Manufacturing and construction were the largest sources of weakness in GDP, with energy-intensive sectors such as metallurgy and the production of vehicles seeing outright declines. We believe that much of the weakness in energy-intensive industries is related to the fact that poor hydrological conditions and low reservoir levels have led to record high power prices. This has caused several energy-intensive industrial producers to curtail production as high power prices have made them uncompetitive with imports and, in some cases, they are taking advantage of high prices to sell contracted power back to the grid. In addition, reduced hydro generation has increased demand for thermal generation, which has led to an increase in fuel imports (oil and LNG). This has partly masked a positive trend in net exports due to a weaker Brazilian Real, which has depreciated significantly over the past few years. Real GDP growth will remain weak through the remainder of 2014 as short-term challenges persist. However, despite the near term challenges, we are less pessimistic than many commentators have become recently and see current growth rates as being far below Brazil�s long-term growth potential. We believe this potential will be underpinned by labour force growth of at least approximately 1.0% and productivity growth of 2.0% or higher if the newly-elected government pursues a more growth oriented agenda.

China

Chinese GDP growth slowed to 7.3% in the third quarter, as year-over-year retail sales growth of 10.3% and an unexpected lift from export volumes, which grew 9.0% year-over-year in August, were not enough to fully offset a further contraction in property sales and the moderation of oil, steel and electricity demand growth to between 2.0% and 4.0%. Residential property markets remain under pressure with housing sales declining 10.9% over the first eight months of the year. The government has responded to this weakness by relaxing home purchase restrictions on second buyers and increasing social housing construction but the extent to which the government will intervene remains unclear. Authorities have acknowledged, in part, that structural reforms are necessary and are likely associated with a lower growth target going forward. Somewhat slower growth should be expected given the size of the Chinese economy, second only to the United States and almost twice the size of Japan.

Australia

Australian GDP growth remains around 3.0% as declines in private investment are being offset by stronger residential construction, public investment and a positive contribution from exports as volumes continue to rise. Capital expenditures decreased in all three mining sectors last quarter and we expect an overall slowing trend due to declines in commodity prices and the completion of currently committed projects over the next few years. Iron ore, metallurgical coal and thermal coal prices are down 40%, 25% and 20%, respectively, year-over-year and by the end of next year, four of the six onshore mega gas projects will reach completion. Combined, these projects account for 51% of the $229 billion worth of resource projects currently committed. Overall growth, however, has been supported by a pickup in residential construction, which is on pace for 180,000 units to be built this year, a 11% increase over last year and a 20 year high. The Australian dollar was down to US$0.87 in this quarter, buffeted by U.S. dollar strength and weakness in commodity prices.

�

| � | Q3 2014 INTERIM REPORT | � | 9 |

PART 2 � FINANCIAL PERFORMANCE REVIEW

SELECTED FINANCIAL INFORMATION

�

| � | � | Three Months Ended | � | � | Nine Months Ended | � | ||||||||||||||||||

| CONDENSED ��STATEMENTS OF ��OPERATIONS |

� | 2014� | � | � | 2013� | � | � | Change� | � | � | 2014� | � | � | 2013� | � | � | Change� | � | ||||||

| FOR THE PERIODS ENDED SEP. 30 (MILLIONS, EXCEPT PER SHARE AMOUNTS) |

� | � | � | � | � | � | � | � | � | � | � | � | � | � | � | � | � | � | ||||||

| Revenues |

� | $ | ��������4,659� | �� | � | $ | ��������4,501� | �� | � | $ | ��������158� | �� | � | $ | ��������13,670� | �� | � | $ | ��������14,600� | �� | � | $ | ��������(930) | �� |

| Direct costs |

� | � | (3,467) | �� | � | � | (3,230) | �� | � | � | (237) | �� | � | � | (9,686) | �� | � | � | (10,256) | �� | � | � | 570� | �� |

| Other income and gains |

� | � | (7) | �� | � | � | 1,200� | �� | � | � | (1,207) | �� | � | � | 190� | �� | � | � | 1,218� | �� | � | � | (1,028) | �� |

| Equity accounted income |

� | � | 350� | �� | � | � | 194� | �� | � | � | 156� | �� | � | � | 969� | �� | � | � | 684� | �� | � | � | 285� | �� |

| Expenses |

� | � | � | � | � | � | ||||||||||||||||||

| Interest |

� | � | (645) | �� | � | � | (617) | �� | � | � | (28) | �� | � | � | (1,910) | �� | � | � | (1,940) | �� | � | � | 30� | �� |

| Corporate costs |

� | � | (27) | �� | � | � | (36) | �� | � | � | 9 | �� | � | � | (93) | �� | � | � | (116) | �� | � | � | 23� | �� |

| Fair value changes |

� | � | 637 | �� | � | � | 104 | �� | � | � | 533 | �� | � | � | 2,348 | �� | � | � | 630� | �� | � | � | 1,718� | �� |

| Depreciation and amortization |

� | � | (353) | �� | � | � | (357) | �� | � | � | 4 | �� | � | � | (1,100) | �� | � | � | (1,095) | �� | � | � | (5) | �� |

| Income taxes |

� | � | (38) | �� | � | � | (264) | �� | � | � | 226 | �� | � | � | (878) | �� | � | � | (731) | �� | � | � | (147) | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| Net income |

� | � | 1,109 | �� | � | � | 1,495 | �� | � | � | (386) | �� | � | � | 3,510 | �� | � | � | 2,994� | �� | � | � | 516� | �� |

| Non-controlling interests |

� | � | (375) | �� | � | � | (682) | �� | � | � | 307 | �� | � | � | (1,450) | �� | � | � | (1,591) | �� | � | � | 141� | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| Net income attributable to shareholders | � | $ | 734� | �� | � | $ | 813� | �� | � | $ | (79) | �� | � | $ | 2,060� | �� | � | $ | 1,403� | �� | � | $ | 657� | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| Net income per share |

� | $ | 1.09� | �� | � | $ | 1.23� | �� | � | $ | (0.14) | �� | � | $ | 3.07� | �� | � | $ | 2.05� | �� | � | $ | ��������1.02� | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| � BALANCE SHEET INFORMATION � |

� | � | � | � | � | � | � | � | � | � | ||||||||||||||

| (MILLIONS) | � | � | Sep.�30,�2014� | � | � | Dec.�31,�2013� | � | � | ������������Change� | � | ||||||||||||||

| Consolidated assets |

�� |

� | $ | 118,232� | �� | � | $ | 112,745� | �� | � | $ | 5,487� | �� | |||||||||||

| Borrowings and other non-current financial liabilities |

�� |

� | � | 56,220� | �� | � | � | 53,061� | �� | � | � | 3,159� | �� | |||||||||||

| Equity |

�� |

� | � | 48,933� | �� | � | � | 47,526� | �� | � | � | 1,407� | �� | |||||||||||

| � | � | � | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | ||||||||||

The relevant exchange rates that impact our business are shown in the following table:

�

| � | � | � | � | � | � | � | � | � | � | � | Average Rate | � | ||||||||||||||||||||||||

| AS AT SEP. 30, 2014 AND DEC. 31, 2013 AND FOR THE PERIODS ENDED SEP. 30 |

� | � | � | � | � | � | � | � | � | � | � | � | � | � | � | � | � | � | � | |||||||||||||||||

| � | � | Period-end Spot Rate | � | � | Three Months Ended | � | � | Nine Months Ended | � | |||||||||||||||||||||||||||

| � | � | ����2014� | � | � | ����2013� | � | � | �Change� | � | � | ����2014� | � | � | ����2013� | � | � | �Change� | � | � | ����2014� | � | � | ����2013� | � | � | �Change� | � | |||||||||

| Australian dollar |

� | � | 0.8746� | �� | � | � | 0.8918� | �� | � | � | (2)% | �� | � | � | 0.9250� | �� | � | � | 0.9161� | �� | � | � | 1% | �� | � | � | 0.9184� | �� | � | � | 0.9817� | �� | � | � | (6)% | �� |

| Brazilian real |

� | � | 2.4450� | �� | � | � | 2.3635� | �� | � | � | (3)% | �� | � | � | 2.2732� | �� | � | � | 2.2852� | �� | � | � | 1% | �� | � | � | 2.2862� | �� | � | � | 2.1124� | �� | � | � | (8)% | �� |

| Canadian dollar |

� | � | 0.8932� | �� | � | � | 0.9414� | �� | � | � | (5)% | �� | � | � | 0.9187� | �� | � | � | 0.9628� | �� | � | � | (5)% | �� | � | � | 0.9143� | �� | � | � | 0.9774� | �� | � | � | (6)% | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

FINANCIAL PERFORMANCE

Overview

Three Months Ended September�30

Net income in the third quarter was $1,109 million, compared to $1,495 million recorded in the same period in the prior year. The largest variance related to �other income and gains� which totalled $1,200 million in the 2013 quarter whereas the current quarter included a small loss. The prior year gains included a $525 million gain on the settlement of a long-dated interest rate swap contract and a $664�million gain on the disposition of a private equity investment. These gains were partially offset by $206 million of associated deferred income tax expenses, resulting in an aggregate net variance in net income of $983 million after taxes. The year-over-year variance was partially offset by a $533 million increase in fair value changes over the 2013 quarter, primarily due to a large amount of appraisal gains in our property operations.

�

�

| 10 | � | BROOKFIELD ASSET MANAGEMENT | � |

�

Net income attributable to shareholders after deducting non-controlling interests decreased by $79 million to $734 million in the third quarter. The decline in net income attributable to shareholders was significantly less than the decline in net income because a large portion of private equity disposition gain accrued largely to non-controlling interests and, conversely, a larger portion of the fair value gains was attributable to shareholders due to our higher ownership interest in our office property portfolio.

Nine Months Ended September�30

Net income for the first nine months of 2014 was $3.5 billion, of which $2.1 billion was attributable to shareholders. On a per share basis net income for the nine months increased by $1.02 to $3.07 in the current year.

In addition to the variances discussed above for the three months, the first quarter of 2014 included a $230 million gain on the partial disposition of a forest products investment in our private equity operations, which is included within fair value changes, along with an additional $1,336 million of positive appraisal gains on consolidated investment properties. We also recorded a $320 million income tax expense in the first quarter of 2014 due to a change in tax legislation that increased the tax rate utilized in a key market for our property operations.

Net income attributable to shareholders increased by $657 million to $2,060 million for the nine months, due to the above mentioned positive variances.

Statements of Operations

Revenues and Direct Costs

The following tables present consolidated revenues and direct costs, which we have disaggregated into our operating segments in order to facilitate a review of year-over-year variances. Segmented revenue and direct costs are presented and reconciled to consolidated revenues and direct costs in the following tables.

�

| ��������������� | ��������������� | ��������������� | ��������������� | ��������������� | ��������������� | |||||||||||||||||||

| � | � | Revenues | � | � | Direct Costs | � | ||||||||||||||||||

| FOR THE THREE MONTHS ENDED SEP. 30 (MILLIONS) |

� | 2014� | � | � | 2013� | � | � | Change� | � | � | 2014� | � | � | 2013� | � | � | Change | � | ||||||

| Revenues |

� | � | � | � | � | � | ||||||||||||||||||

| Asset management |

� | $ | 194� | �� | � | $ | 175� | �� | � | $ | 19� | �� | � | $ | 90� | �� | � | $ | 79� | �� | � | $ | 11� | �� |

| Property |

� | � | 1,225� | �� | � | � | 1,133� | �� | � | � | 92�� | �� | � | � | 625� | �� | � | � | 563� | �� | � | � | 62� | �� |

| Renewable energy |

� | � | 345� | �� | � | � | 384� | �� | � | � | (39) | �� | � | � | 135� | �� | � | � | 144� | �� | � | � | (9) | �� |

| Infrastructure |

� | � | 553� | �� | � | � | 498� | �� | � | � | 55� | �� | � | � | 246� | �� | � | � | 227� | �� | � | � | 19� | �� |

| Private equity |

� | � | 622� | �� | � | � | 896� | �� | � | � | (274) | �� | � | � | 580� | �� | � | � | 753� | �� | � | � | (173) | �� |

| Residential development |

� | � | 920� | �� | � | � | 598� | �� | � | � | 322� | �� | � | � | 815� | �� | � | � | 540� | �� | � | � | 275� | �� |

| Service activities |

� | � | 942� | �� | � | � | 905� | �� | � | � | 37� | �� | � | � | 891� | �� | � | � | 866� | �� | � | � | 25� | �� |

| Corporate activities |

� | � | 9� | �� | � | � | 35� | �� | � | � | (26) | �� | � | � | 6� | �� | � | � | 16� | �� | � | � | (10) | �� |

| Eliminations and adjustments1 |

� | � | (151) | �� | � | � | (123) | �� | � | � | (28) | �� | � | � | 79� | �� | � | � | 42� | �� | � | � | 37� | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| Total consolidated revenues |

� | $ | ������4,659� | �� | � | $ | ������4,501� | �� | � | $ | ������158� | �� | � | $ | ������3,467� | �� | � | $ | ������3,230� | �� | � | $ | ������237� | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

�

| 1. | Adjustment to eliminate base management fees and interest income earned from entities that we consolidate. See Note 3 to our Consolidated Financial Statements |

� |

�

| ��������������� | ��������������� | ��������������� | ��������������� | ��������������� | ��������������� | |||||||||||||||||||

| � | � | Revenues | � | � | Direct Costs | � | ||||||||||||||||||

| FOR THE NINE MONTHS ENDED SEP. 30 (MILLIONS) |

� | 2014� | � | � | 2013� | � | � | Change� | � | � | 2014� | � | � | 2013� | � | � | Change� | � | ||||||

| Revenues |

� | � | � | � | � | � | ||||||||||||||||||

| Asset management |

� | $ | 565� | �� | � | $ | 456� | �� | � | $ | ������109� | �� | � | $ | 283� | �� | � | $ | 225� | �� | � | $ | 58� | �� |

| Property |

� | � | 3,731� | �� | � | � | 3,418� | �� | � | � | 313� | �� | � | � | ������1,949� | �� | � | � | ������1,722� | �� | � | � | ������227� | �� |

| Renewable energy |

� | � | 1,310� | �� | � | � | 1,243� | �� | � | � | 67� | �� | � | � | 388� | �� | � | � | 413� | �� | � | � | (25) | �� |

| Infrastructure |

� | � | 1,676� | �� | � | � | 1,806� | �� | � | � | (130) | �� | � | � | 752� | �� | � | � | 879� | �� | � | � | (127) | �� |

| Private equity |

� | � | 1,919� | �� | � | � | 3,293� | �� | � | � | (1,374) | �� | � | � | 1,679� | �� | � | � | 2,639� | �� | � | � | (960) | �� |

| Residential development |

� | � | 2,041� | �� | � | � | 1,675� | �� | � | � | 366� | �� | � | � | 1,780� | �� | � | � | 1,542� | �� | � | � | 238� | �� |

| Service activities |

� | � | ������2,693� | �� | � | � | ������2,780� | �� | � | � | (87) | �� | � | � | 2,590� | �� | � | � | 2,688� | �� | � | � | (98) | �� |

| Corporate activities |

� | � | 139� | �� | � | � | 236� | �� | � | � | (97) | �� | � | � | 73� | �� | � | � | 46� | �� | � | � | 27� | �� |

| Eliminations and adjustments1 |

� | � | (404) | �� | � | � | (307) | �� | � | � | (97) | �� | � | � | 192� | �� | � | � | 102� | �� | � | � | 90� | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| Total consolidated revenues |

� | $ | 13,670� | �� | � | $ | 14,600� | �� | � | $ | (930) | �� | � | $ | 9,686� | �� | � | $ | 10,256� | �� | � | $ | (570) | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

�

| 1. | Adjustment to eliminate base management fees and interest income earned from entities that we consolidate. See Note 3 to our Consolidated Financial Statements |

� |

�

| � | Q3 2014 INTERIM REPORT | � | 11 |

Revenues and direct costs increased by $158 million and $237 million in the quarter. On a nine-month basis, revenues and direct costs decreased by $930 million and $570 million, respectively. We sold and deconsolidated two forest products businesses within our private equity operations and non-core timberlands within our infrastructure segment over the past twelve months, which collectively reduced revenues and direct costs on a three-month basis by $299 million and $257 million and on a nine-month basis by $1,614 million and $1,284 million, respectively. After adjusting for these sales, revenues and direct costs increased on a three-month basis by $455 million and $494 million and on a nine-month basis by $684 million and $714 million, respectively. Notable variances in revenues and direct costs on a segmented basis for the three and nine months are described in the following paragraphs.

Asset management: Revenues increased by $19 million to $194 million for the third quarter of 2014. We recorded $160 million of base management fees, representing a 24% increase over the $129 million recognized in 2013, primarily due to $15 million of additional fees generated on BPY�s increased capitalization as well as fees earned from additional commitments to our real estate and infrastructure flagship private funds. These positive variances were partially offset, as the prior year included $18 million of catch-up fees as a result of capital called on the final close of our flagship property fund. Direct costs increased by $11 million, reflecting the expansion of our operations. Revenues for the first nine months of 2014 increased by $109 million to $565 million, due primarily to increased base management fees from a higher level of fee bearing capital under management. The formation of and subsequent unit issuances by Brookfield Property Partners contributed $47 million of the change with the remainder of the increase being primarily due to additional capital committed to our infrastructure and property private funds. Direct costs increased by $58 million to $283 million on a nine-month basis, due to the expansion of our asset management operations and $10 million being reallocated to this segment following the formation of Brookfield Property Partners in April 2013.

Property: Revenues and direct costs increased by $92 million and $62 million, respectively. The increase in revenue and costs were a result of assets acquired over the past year, including our industrial and logistics operations, which were acquired in the latter half of 2013. Lower occupancy levels in our U.S. office portfolio reduced revenues by $40 million in the quarter ($120 million for the nine months) following the expected expiry of a large lease in the fourth quarter of 2013, which was partially offset by the impact of higher rents on new leases entered into over the past year. On a year-to-date basis, revenues and direct costs increased $313 million and $227 million, respectively, and reflects a full period of contribution from the aforementioned industrial operations, as well as recently acquired multifamily, hotel and office properties.

Renewable energy: Revenues decreased by $39 million in the third quarter compared to the prior year. Generation of 4,383 GWh decreased by 15% over the prior year of 5,154 GWh, which resulted in a $69 million reduction in revenue. Newly acquired or commissioned assets generated $30 million of revenue. U.S. hydroelectric generation was in line with the long-term average but below the prior year which experienced stronger inflows. The Canadian hydroelectric portfolio was impacted by below average inflows resulting from the dry conditions. Direct costs are largely fixed and declined by $9 million over the prior year, due primarily to foreign exchange. On a year-to-date basis revenues were $67 million higher than the same period in the prior year, primarily due from $83 million of additional revenues in the first quarter on higher realized energy prices, particularly in New York and New England, and generation levels that were higher than the comparable period due to improved water levels and the contribution from net new assets.

Infrastructure: Revenues increased by $55 million compared to the 2013 quarter as a reduction in revenues of $23 million from the sale of our Pacific Northwest timberlands in July 2013 was more than offset by increased revenues of $78 million from recent capital expansions, acquisitions completed in the last twelve months and higher volumes across our transport businesses. Direct operating costs were higher by $19 million compared to prior year as a $32 million increase in costs due to acquisitions and capital expansion programs completed in the past year was partially offset by a decline in operating costs of $13�million from the sale of our Pacific Northwest timberlands. On a nine-month basis, revenues decreased by $130 million compared to the prior year due to a reduction in revenues of $304 million from the sale of our Pacific Northwest timberlands in July 2013 and a $30 million decrease from a 6% decline in the Australian dollar were partially offset by increased revenues generated from recently completed development projects and acquisitions.

Private equity: Revenues decreased by $274 million and direct costs decreased by $173 million in the quarter, primarily as a result of the sale of two forest products investments which contributed $276 million in revenues and $244 million in direct costs in the prior year. In addition, a 14% decline in our panelboard operations compared to the prior year, decreased revenues by a further $35 million. These decreases were partially offset by higher sales at our energy-related investments due to higher natural gas production compared to the prior year. On a nine-month basis revenues decreased by $1.37 billion and direct costs decreased by $960 million, primarily reflecting asset sales including the above-mentioned forest products investments, which collectively decreased revenues and direct costs by $1,326 million and $1,138 million, respectively. In addition, lower oriented panelboard pricing decreased revenues by $220 million on a nine-month basis.

Residential development: Revenues and direct costs increased by $322 million and $275 million, respectively, reflecting the completion and delivery of a large number of projects in our Brazilian operations which resulted in increases in both revenues and the associated cost of goods sold. Our North American operations revenues increased by $23 million due to increased U.S.�housing sales. Nine-month results reflect the higher level of deliveries in our Brazilian operations noted above, as well as an increase in volumes in North America primarily due to higher levels on our U.S. housing sales. We also sold two commercial properties within our North American operations in the first quarter of 2014, which generated revenues of $83 million.

�

�

| 12 | � | BROOKFIELD ASSET MANAGEMENT | � |

�

Service activities: Revenues increased by $37 million in the third quarter, as an increase in revenues within our construction operations offset lower activity levels in our relocation services. Year-to-date revenues and costs declined by $87 million and $98 million, respectively, as lower level of construction activity in the first quarter of 2014 more than offset the increase in the third quarter.

Corporate activities: Revenues in our investment portfolios decreased compared to 2013 by $26 million on a three-month basis and by $97 million year-to-date due to tempered capital market performance.

Other Income and Gains

Other income and gains were a loss of $7 million in the quarter compared to $1,200 million in the prior year. The prior period included a $525 million gain on the termination of a long-dated interest rate swap contract in August 2013 as well as a $664 million gain on the sale of a pulp and paper investment. On a year-to-date basis, other income and gains totalled $190 million and includes a $143 million gain on the repayment of a distressed debt investment in a European office portfolio.

Equity Accounted Income

Equity accounted income represents our share of the net income recorded by investments over which we exercise significant influence and is reported as a single line item in our consolidated statement of operations. The following table disaggregates consolidated equity accounted income to facilitate analysis:

�

| � | � | Three Months Ended | � | � | Nine Months Ended | � | ||||||||||||||||||

| FOR THE PERIODS ENDED SEP.�30 (MILLIONS) |

� | 2014� | � | � | 2013 | � | � | Change | � | � | 2014� | � | � | 2013� | � | � | Change� | � | ||||||

| General Growth Properties |

� | $ | 168� | �� | � | $ | 92� | �� | � | $ | 76� | �� | � | $ | 481� | �� | � | $ | 317� | �� | � | $ | 164� | �� |

| Other property operations |

� | � | 96� | �� | � | � | 61� | �� | � | � | 35� | �� | � | � | 316� | �� | � | � | 268� | �� | � | � | 48� | �� |

| Infrastructure operations |

� | � | 40� | �� | � | � | 20� | �� | � | � | 20� | �� | � | � | 73� | �� | � | � | 51� | �� | � | � | 22� | �� |

| Forest products business |

� | � | 5� | �� | � | � | �� | �� | � | � | 5� | �� | � | � | 24� | �� | � | � | �� | �� | � | � | 24� | �� |

| Other |

� | � | 41� | �� | � | � | 21� | �� | � | � | 20� | �� | � | � | 75� | �� | � | � | 48� | �� | � | � | 27� | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| � | $ | ����������350� | �� | � | $ | ����������194� | �� | � | $ | ����������156� | �� | � | $ | ����������969� | �� | � | $ | ����������684� | �� | � | $ | ����������285� | �� | |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

Equity accounted income from our investment in General Growth Properties (�GGP�) increased by $76 million in the current quarter and $164 million on a year-to-date basis due to an increased consolidated ownership interest in GGP from 22% to 29%, a higher level of appraisal gains on GGP�s investment properties, 5.4% same-store net operating income growth due to higher rents on new leases and a 20 bps increase in occupancy. Our share of GGP�s valuation gains on a year-to-date basis totalled $198 million, compared to $92 million in the same period in 2013, representing an increase of $106 million.

Equity accounted income from other property operations increased by $35 million from the third quarter of 2013, and by $48 million from the first nine months of 2013, due to the commencement of equity accounting for a Denver office property following the sale of a 50% interest in the second quarter of 2014 and an increased level of fair value gains within other deconsolidated investment properties. The increase also reflects the contribution from an equity accounted hotel portfolio, which was acquired in May�2014.

Equity accounted income from infrastructure operations increased compared to the prior year by $20 million for the third quarter, and by $22 million for the first nine months of 2014. The improved results are primarily due to earnings from our Texas transmission investment which was commissioned into operations during the fourth quarter of 2013, and the contribution from acquisitions completed over the past twelve months including Brazil logistics operations. These positive variances were partially offset by the sale of our Australasian regulated distribution utility, which was equity accounted.

We commenced equity accounting for a Forest Products operation in the first quarter of 2014 and generated $24 million of equity accounted income on a year-to-date basis. We subsequently disposed of this operation in September�2014.

Other equity accounted income includes $35 million of profit from our Brazilian residential operations upon delivery of projects which were held through joint ventures.

Interest Expense

The following table presents interest expense organized by the balance sheet classification of the associated liability:

�

| � | � | Three Months Ended | � | � | Nine Months Ended | � | ||||||||||||||||||

| FOR THE PERIODS ENDED SEP.�30 (MILLIONS) |

� | 2014� | � | � | 2013� | � | � | Change� | � | � | 2014� | � | � | 2013� | � | � | Change� | � | ||||||

| Corporate borrowings |

� | $ | 58� | �� | � | $ | 48� | �� | � | $ | 10� | �� | � | $ | ����������172� | �� | � | $ | ����������146� | �� | � | $ | 26� | �� |

| Non-recourse borrowings |

� | � | � | � | � | � | ||||||||||||||||||

| Property-specific mortgages |

� | � | 515� | �� | � | � | 459� | �� | � | � | 56� | �� | � | � | 1,508� | �� | � | � | 1,414� | �� | � | � | 94� | �� |

| Subsidiary borrowings |

� | � | 66� | �� | � | � | 99� | �� | � | � | (33) | �� | � | � | 204� | �� | � | � | 343� | �� | � | � | (139) | �� |

| Subsidiary equity obligations |

� | � | 6� | �� | � | � | 11� | �� | � | � | (5) | �� | � | � | 26� | �� | � | � | 37� | �� | � | � | (11) | �� |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

| � | $ | ����������645� | �� | � | $ | ����������617� | �� | � | �$ | ����������28� | �� | � | $ | 1,910� | �� | � | $ | 1,940� | �� | � | $ | ���������(30) | �� | |

| � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | � | � |

� |

� | |

�

| � | Q3 2014 INTERIM REPORT | � | 13 |

The majority of our borrowings are fixed rate long-term financings. Accordingly, changes in interest rates are generally limited to the impact of refinancing activities or changes in the level of debt as a result of acquisitions and dispositions.

Interest expense from corporate borrowings increased on a three and nine-month basis compared to 2013 as a result of a higher level of borrowings. We refinanced high cost subsidiary borrowings in the third quarter of 2013 with lower coupon corporate debt, which decreased subsidiary borrowings interest expense by $21 million and $87 million on a three-month and year-to-date basis respectively.

Interest expense on property-specific borrowings increased by $56 million ($94 million year-to-date) over the prior year as the aggregate amount of borrowings from debt increased due to debt associated with acquisitions and refinancings. Interest expense on subsidiary borrowings decreased following the termination of a long-dated high coupon interest rate liability in the third quarter of 2013, the elimination of interest following the sale of previously consolidated private equity investments, and the repayment of subsidiary unsecured facilities.

Fair Value Changes

The following table disaggregate fair value changes into major components to facilitate analysis:

�

| � | �� | Three Months Ended | � | �� | Nine Months Ended | � | ||||||||||||||||||

| FOR THE PERIODS ENDED SEP. 30 (MILLIONS) |

�� | 2014� | � | �� | 2013� | � | �� | Change� | � | �� | 2014� | � | �� | 2013� | � | �� | Change� | � | ||||||

| Investment properties |

�� | $ | 661� | �� | �� | $ | 145� | �� | �� | $ | 516� | �� | �� | $ | 1,997� | �� | �� | $ | 754� | �� | �� | $ | 1,243� | �� |

| Investment in Canary Wharf |

�� | � | 178� | �� | �� | � | 57� | �� | �� | � | 121� | �� | �� | � | 319� | �� | �� | � | 103� | �� | �� | � | 216� | �� |

| Forest products investment |

�� | � | �� | �� | �� | � | �� | �� | �� | � | �� | �� | �� | � | 230� | �� | �� | � | �� | �� | �� | � | 230� | �� |

| Power contracts |

�� | � | (83) | �� | �� | � | 7� | �� | �� | � | (90) | �� | �� | � | (95) | �� | �� | � | (69) | �� | �� | � | (26) | �� |

| Other |

�� | � | (119) | �� | �� | � | (105) | �� | �� | � | (14)� | �� | �� | � | (103) | �� | �� | � | (158) | �� | �� | � | (55) | �� |

| �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | |

| �� | $ | ����������637� | �� | �� | $ | ����������104� | �� | �� | $ | ����������533� | �� | �� | $ | ��������2,348� | �� | �� | $ | ����������630� | �� | �� | $ | ��������1,718� | �� | |

| �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | �� | � |

� |

� | |

Investment Properties

Fair value gains from changes in investment property values totalled $661 million in the third quarter of 2014 and $2.0 billion year-to-date. Most of these gains occurred within our U.S. office investment properties as valuations benefitted from positive leasing activities in New York City, downtown Los Angeles and London. Valuations benefitted from declines in discount rates and terminal capitalization rates, and improvements in projected cash flows based on tenant profile and rental markets. The overall decline in discount rates during the quarter contributed approximately 75% of the gains, while improvements in projected cash flows contributed approximately 25% of the gains.

Forest Products Investment

During the first quarter of 2014 we disposed of a partial interest in a private equity investee company, resulting in us deconsolidating the business from our results and revaluing our retained interest based on its quoted market price at the time of our loss of control. This gave rise to a $230 million revaluation gain relating to the excess of fair value over our IFRS book value of our retained interest.

Investment in Canary Wharf