Form 485BPOS MERIDIAN FUND INC

Tweet

Tweet Share

ShareTable of Contents

File Nos. 811-04014 and 002-90949

As filed with the Securities and Exchange Commission on October 25, 2018

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-1A

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Post-Effective Amendment No. 58

and

REGISTRATION STATEMENT

UNDER

THE INVESTMENT COMPANY ACT OF 1940

Amendment No. 59

MERIDIAN FUND, INC.

(Exact name of Registrant as Specified in Charter)

100 Fillmore Street

Suite 325

Denver, CO 80206

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number: (303) 398-2929

David Corkins

100 Fillmore Street

Suite 325

Denver, CO 80206

(Name and Address of Agent for Service)

With copies to:

Peter H. Schwartz, Esq.

Davis Graham & Stubbs LLP

1550 17th Street, Suite 500

Denver, CO 80202

It is proposed that this filing will become effective: (check appropriate box)

| ☐ | immediately upon filing pursuant to paragraph (b) |

| ☒ | on November 1, 2018 pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | on (date) pursuant to paragraph (a)(1) |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) |

| ☐ | on (date) pursuant to paragraph (a)(2) of rule 485. |

If appropriate, check the following box:

| ☐ | this post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

Table of Contents

MERIDIAN FUND, INC.®

MERIDIAN GROWTH FUND®

CLASS A SHARES: MRAGX; CLASS C SHARES: MRCGX; INVESTOR CLASS SHARES: MRIGX

MERIDIAN CONTRARIAN FUND

CLASS A SHARES: MFCAX; CLASS C SHARES: MFCCX; INVESTOR CLASS SHARES: MFCIX

MERIDIAN ENHANCED EQUITY FUND® (FORMERLY KNOWN AS MERIDIAN EQUITY INCOME FUND)

CLASS A SHARES: MRAEX; CLASS C SHARES: MRCEX; INVESTOR CLASS SHARES: MRIEX

MERIDIAN SMALL CAP GROWTH FUND

CLASS A SHARES: MSGAX; CLASS C SHARES: MSGCX; INVESTOR CLASS SHARES: MISGX

PROSPECTUS

November 1, 2018

This Prospectus contains essential information for anyone considering an investment in the Funds. Please read this document carefully and retain it for future reference.

ArrowMark Colorado Holdings, LLC

(the “Investment Adviser”)

website: www.meridianfund.com

THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

As of the date of this prospectus, Class A Shares, Class C Shares and Investor Class Shares of the Meridian Growth Fund and the Meridian Small Cap Growth Fund are not offered to the public, except in limited circumstances.

Link to SAI

Table of Contents

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website (www.meridianfund.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by enrolling at www.meridianfund.com.

Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with a Fund, you can call 1-800-466-6662 to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held with the fund complex if you invest directly with a Fund.

Table of Contents

MERIDIAN FUND, INC.®

| 1 | ||||

| 1 | ||||

| 8 | ||||

| 15 | ||||

| 22 | ||||

| 29 | ||||

| FURTHER INFORMATION ABOUT THE FUNDS’ INVESTMENT OBJECTIVES AND PRINCIPAL INVESTMENT STRATEGIES |

29 | |||

| 29 | ||||

| 30 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 32 | ||||

| 33 | ||||

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 42 | ||||

| 42 | ||||

| Distribution and Networking, Sub-Accounting and Administrative Services |

48 | |||

| 50 | ||||

| 51 | ||||

| 54 | ||||

| 55 | ||||

| 56 | ||||

| 56 | ||||

| 59 | ||||

| 59 | ||||

| 59 | ||||

| 62 |

Table of Contents

Investment Objective

The MERIDIAN GROWTH FUND seeks long-term growth of capital.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

| Shareholder Fees (fees paid directly from your investment) |

|

Class A Shares |

1 |

|

Class C Shares |

1 |

|

Investor Class Shares |

1 | |||

| Maximum Sales Charge (Load) on Purchases |

5.75% | NONE | NONE | |||||||||

| Maximum Deferred Sales Charge (Load) |

NONE | 1.00% | NONE | |||||||||

| Redemption Fee (as a percentage of amount redeemed, if you sell or exchange your shares within 60 days of purchase) |

2.00% | NONE | 2.00% | |||||||||

| Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||||||||||||

| Management Fees |

0.76% | 0.76% | 0.76% | |||||||||

| Distribution (Rule 12b-1) Fees |

0.25% | 1.00% | 0.00% | |||||||||

| Other Expenses |

0.14% | 0.14% | 0.19% | |||||||||

| Total Annual Fund Operating Expenses |

1.15% | 1.90% | 0.95% | |||||||||

| Fee Waivers and/or Expense Reimbursements and Recoupment |

N/A | N/A | N/A | |||||||||

| Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment2,3 |

1.15% | 1.90% | 0.95% |

| 1 | As of June 15, 2017, Class A, Class C and Investor Class shares of the Meridian Growth Fund are no longer offered to the public, except in limited circumstances. |

| 2 | The Investment Adviser has agreed to waive a portion of the investment advisory and/or administration fees and/or reimburse other expenses of the Meridian Growth Fund so that the ratio of expenses to average net assets of the Meridian Growth Fund (excluding acquired fund fees and expenses, dividend expenses on securities sold short, and interest expenses on short sales) does not exceed 1.55% for Class A, 2.25% for Class C and 1.30% for Investor Class. These expense limitations may not be amended or withdrawn until one year after the date of this prospectus. To the extent acquired fund fees are excluded from the waiver and reimbursement calculation, “Total Annual Fund Operating Expenses after Fee Waivers and Expense Reimbursements” will be higher. The total annual fund operating expenses in this fee table may therefore differ from the expense ratios in the financial highlights in this prospectus because the financial highlights include only the Fund’s direct operating expenses and do not include fees or expenses incurred indirectly by the Fund through its investments in the underlying fund(s). |

| 1 | Meridian Growth Fund |

Table of Contents

| 3 | For a period not to exceed three (3) years on which a waiver of reimbursement in excess of the expense limitation is made by the Investment Adviser, the Fund will carry forward, and may repay the Investment Adviser such amounts; provided that the Fund is able to effect such reimbursement and maintain the expense limitation in effect at the time of the waiver. |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in Class A shares, Class C shares or Investor Class shares of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the Fund’s operating expenses remain the same and the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment shown above will only be in place for the length of the current commitment. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 685 | $ | 919 | $ | 1,172 | $ | 1,892 | ||||||||

| Class C Shares | $ | 293 | $ | 597 | $ | 1,026 | $ | 2,222 | ||||||||

| Investor Class Shares | $ | 97 | $ | 303 | $ | 525 | $ | 1,166 | ||||||||

You would pay the following expenses if you did not redeem your shares of the Fund:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 685 | $ | 919 | $ | 1,172 | $ | 1,892 | ||||||||

| Class C Shares | $ | 193 | $ | 597 | $ | 1,026 | $ | 2,222 | ||||||||

| Investor Class Shares | $ | 97 | $ | 303 | $ | 525 | $ | 1,166 | ||||||||

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when the Fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund’s performance. For the fiscal year ended June 30, 2018, the Fund’s portfolio turnover rate was 47% of the average value of its portfolio.

Principal Investment Strategies

The Fund seeks long-term growth of capital by investing primarily in a diversified portfolio of publicly traded common stocks of U.S. companies. Under normal circumstances, the Fund emphasizes small- and mid-capitalization growth companies that the Investment Adviser believes may have prospects for above-average growth in revenues and earnings because of many factors, including high sales growth, high unit growth, industry growth, high or improving returns on assets and equity and a strong balance sheet. The Fund may invest in securities of companies with any capitalization across a broad range of industries, though it typically

| Meridian Growth Fund | 2 |

Table of Contents

emphasizes small- and mid-capitalization companies. These may include companies that are relatively small in terms of total assets, revenues and earnings. The mix of the Fund’s investments at any time will depend on the industries and types of securities the Investment Adviser believes hold the most potential for achieving the Fund’s investment objective. The Fund may invest up to 25% of its total assets, calculated at the time of purchase, in securities of foreign companies, including emerging market companies. The Fund generally sells investments when the Investment Adviser concludes that better investment opportunities exist in other securities, the security is fully valued, or the issuer’s circumstances or the political or economic outlook have changed.

Principal Investment Risks

There are risks involved with any investment. The principal risks associated with an investment in the Fund, which could adversely affect its net asset value, yield and return, are set forth below. Please see the section “Further Information About Principal Risks” in this Prospectus for a more detailed discussion of these risks and other factors you should carefully consider before deciding to invest in the Fund.

An investment in the Fund may lose money and is not a deposit of a bank or insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

Investment Strategy Risk — The Investment Adviser uses the Fund’s principal investment strategies and other investment strategies to seek to achieve the Fund’s investment objective of long-term growth of capital. There is no assurance that the Investment Adviser’s investment strategies or securities selection method will achieve that investment objective.

Equity Securities Risk — Equity securities fluctuate in price and value in response to many factors including historical and prospective earnings of the issuer and its financial condition, the value of its assets, general economic conditions, interest rates, investors’ perceptions and market liquidity.

Market Risk — The value of the Fund’s investments will fluctuate in response to the activities of individual companies and general stock market and economic conditions. As a result, the value of your investment in the Fund may be more or less than your purchase price.

Growth Securities Risk — Because growth securities typically trade at a higher multiple of earnings than other types of securities, the market values of growth securities may be more sensitive to changes in current or expected earnings than the market values of other types of securities. In addition, growth securities, at times, may not perform as well as value securities or the stock market in general, and may be out of favor with investors for varying periods of time.

Small and Medium Company Risk — Generally, the smaller the capitalization of a company, the greater the risk associated with an investment in the company. The stock prices of small- and mid-capitalization and newer companies tend to fluctuate more than those of larger capitalized and/or more established companies and generally have a smaller market for their shares than do large capitalization companies.

Foreign Securities Risk — Investments in foreign securities may be subject to more risks than those associated with U.S. investments, including currency fluctuations, political and economic instability and differences in accounting, auditing and financial reporting standards. Foreign securities may be less liquid than domestic securities so that the Fund may, at times, be unable to sell foreign securities at desirable times or prices. In

| 3 | Meridian Growth Fund |

Table of Contents

addition, emerging market securities involve greater risk and more volatility than those of companies in more developed markets. Significant levels of foreign taxes are also a risk related to foreign investments.

Sector Concentration Risk — The Fund may concentrate its investments in companies that are in a single sector or related sector. Concentrating investments in a single sector may make the Fund more susceptible to adverse economic, business, regulatory or other developments affecting that sector. If an economic downturn occurs in a sector in which the Fund’s investments are concentrated, the Fund may perform poorly during that period. The Fund anticipates it will typically invest a significant portion of its assets in the information technology (IT) sector, the industrials sector and the consumer discretionary sector and, therefore, the Fund’s performance could be negatively impacted by events affecting these sectors.

The information technology sector includes, for example, internet, semiconductor, software, hardware, and technology equipment companies. The IT sector may be adversely affected by, among other things, the supply and demand for specific products and services, the pace of technological development, and government regulation. The industrials sector may be adversely affected by, among other things, changes in the supply of and demand for products and services, product obsolescence, claims for environmental damage or product liability and general economic conditions. The consumer discretionary sector depends heavily on disposable household income and consumer spending and may be adversly affected by, among other things, social trends and marketing campaigns.

Securities Lending Risk — The Fund may engage in securities lending. Securities lending involves the risk that the Fund may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for the Fund.

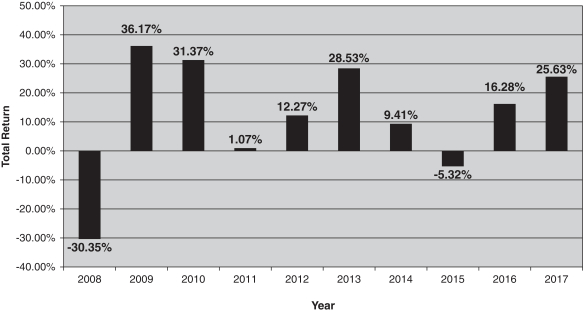

Performance

The bar chart and table below show the Fund’s historical performance and provide an indication of the risks of investing in the Fund. The bar chart shows changes in the performance of the Fund’s Investor Class shares from year-to-year. The performance of the Fund’s other share classes would have differed from the Investor Class shares only to the extent that such classes have higher expenses than the Investor Class shares, which would have resulted in lower performance.

The table shows how the Fund’s average annual returns compare with those of the Russell 2500® Growth Index. The Fund’s past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Updated performance information for the Fund may be obtained by visiting www.meridianfund.com or by calling 1-800-446-6662.

| Meridian Growth Fund | 4 |

Table of Contents

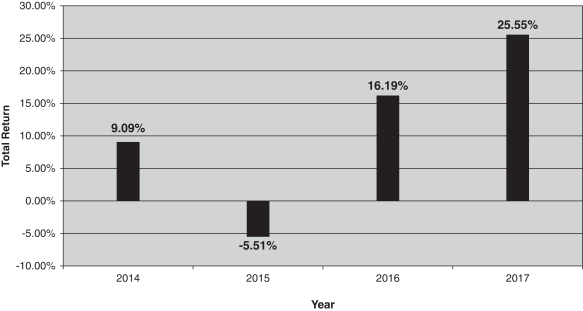

Year-by-Year Total Returns as of 12/31

During the period covered by this bar chart, the Fund’s Investor Class shares highest quarterly return was 10.10% (for the quarter ended December 31, 2014); and the lowest quarterly return was –11.62% (for the quarter ended September 30, 2015).

For the period January 1, 2018 through September 30, 2018, the total return of the Fund’s Investor Class shares was 14.29%.

Average Annual Total Returns

(For the year ended December 31, 2017)

| MERIDIAN GROWTH FUND Investor Class Shares (11/15/13) |

1 Year |

Life of Class | ||||||

| Return Before Taxes |

25.55% | 11.54% | ||||||

| Return After Taxes on Distributions |

23.19% | 9.29% | ||||||

| Return After Taxes on Distributions and Sale of Fund Shares1 |

15.73% | 8.40% | ||||||

| Russell 2500® Growth Index (reflects no deductions for fees, expenses or taxes) |

24.46% | 9.99% | ||||||

| 1 | The Fund’s returns after taxes on distributions and sale of Fund shares may be higher than its returns after taxes on distributions because it includes the effect of a tax benefit an investor may receive resulting from the capital losses that would have been incurred on the sale of the shares. |

| 5 | Meridian Growth Fund |

Table of Contents

After-tax returns are calculated using the historical highest individual federal marginal income tax rates for the character of income in question (as ordinary income or long-term gain) and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts.

Management

ArrowMark Colorado Holdings, LLC

Portfolio Managers

Chad Meade serves as a Co-Portfolio Manager of the Fund. Mr. Meade, who joined the Investment Adviser in 2013, has served as a Co-Portfolio Manager of the Fund since September 5, 2013.

Brian Schaub, CFA, serves as a Co-Portfolio Manager of the Fund. Mr. Schaub, who joined the Investment Adviser in 2013, has served as a Co-Portfolio Manager of the Fund since September 5, 2013.

Purchase and Sale of Fund Shares

Effective as of June 15, 2017, the Meridian Growth Fund no longer accepts offers to purchase Investor Class, Class A and Class C shares of the Fund, unless the purchase is made pursuant to or by:

| • | Current Investor Class, Class A, and Class C shareholders; |

| • | Financial intermediaries and advisors investing on behalf of clients currently invested in the Fund; |

| • | Sponsors of wrap programs or model portfolios who include the Fund as part of a discretionary fee-based program or model portfolio on behalf of current and new clients with pre-approval by the Adviser; |

| • | Existing and new participants in employer-sponsored retirement plans that currently offer the Fund as an investment option; or |

| • | Investment consultants with clients currently invested in the Fund or an exception request for a new client opportunity has been pre-approved by the Adviser. |

The Board of Directors (the “Board”) reserves the right to re-open the Investor Class, Class A and Class C shares of the Fund to new investors at any time or to modify the extent to which future sales of shares are limited. The Fund reserves the right to permit the establishment of new accounts under circumstances not identified above, and to reject any purchase order or rescind any exception listed above that the Board determines does not benefit the Fund and its shareholders.

| Meridian Growth Fund | 6 |

Table of Contents

The following table shows the minimum investment amounts for purchasing share classes of the Meridian Growth Fund.

| Class | Minimum Initial Investment | Minimum Subsequent Investment | Distribution Fee | |||

| Class A Shares | $2,5001 | $50 | 0.25% | |||

| Class C Shares | $2,5001 | $50 | 1.00% | |||

| Investor Class Shares | $99,999 | NONE | NONE |

| 1 | Certain tax-deferred retirement accounts or UGMA/UTMA accounts are subject to a $500 minimum. |

The Funds reserve the right to change the amount of these minimums from time to time or to waive them in whole or in part if, in the Investment Adviser’s or the Fund’s opinion, the investor has adequate intent and availability of assets to reach a future level of investment in the Fund that is equal to or greater than the minimum.

You may purchase, redeem or exchange shares of the Funds on any business day, which is any day the New York Stock Exchange is open for business. Generally, you may purchase, redeem or exchange shares only through institutional channels, such as financial intermediaries and retirement platforms. The minimum investment for Class A shares and Class C shares is $2,500 per Fund account for non-retirement accounts. The minimum investment for the Investor Class shares is $99,999 per Fund account for non-retirement accounts. Certain tax-deferred retirement accounts or UGMA/UTMA accounts are subject to a $500 minimum. Investors in a defined contribution plan through a third-party administrator should refer to their plan document or contact their plan administrator for additional information. Accounts that are a part of certain wrap programs may not be subject to these minimums. Investors should refer to their intermediary for additional information.

Tax Information

Any distributions you receive from a Fund will be taxable as ordinary income, capital gains or qualified dividend income, except when your investment is in an IRA, 401(k) or other tax advantaged investment plan. Subsequent withdrawals from such a tax-advantaged investment plan will be subject to special tax rules. You should consult your tax adviser about your specific tax situation.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of a Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related entities may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your advisor to recommend the Fund or one share class over another investment or share class, as applicable. Ask your advisor or financial intermediary for more information.

| 7 | Meridian Growth Fund |

Table of Contents

FUND SUMMARY

Investment Objective

The MERIDIAN CONTRARIAN FUND seeks long-term growth of capital.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

| Shareholder Fees (fees paid directly from your investment) |

|

Class A Shares |

|

|

Class C Shares |

|

|

Investor Class Shares |

| |||

| Maximum Sales Charge (Load) on Purchases |

5.75% | NONE | NONE | |||||||||

| Maximum Deferred Sales Charge (Load) |

NONE | 1.00% | NONE | |||||||||

| Redemption Fee (as a percentage of amount redeemed, if you sell or exchange your shares within 60 days of purchase) |

2.00% | NONE | 2.00% | |||||||||

| Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||||||||||||

| Management Fees |

1.00% | 1.00% | 1.00% | |||||||||

| Distribution (Rule 12b-1) Fees |

0.25% | 1.00% | 0.00% | |||||||||

| Other Expenses |

0.16% | 0.14% | 0.18% | |||||||||

| Total Annual Fund Operating Expenses |

1.41% | 2.14% | 1.18% | |||||||||

| Fee Waivers and/or Expense Reimbursements and Recoupment |

0.19% | 2 | N/A | 0.17% | 2 | |||||||

| Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment1,3 |

1.60% | 2.14% | 1.35% |

| 1 | The Investment Adviser has agreed to waive a portion of the investment advisory and/or administration fees and/or reimburse other expenses of the Meridian Contrarian Fund so that the ratio of expenses to average net assets of the Meridian Contrarian Fund (excluding acquired fund fees and expenses, dividend expenses on securities sold short, and interest expenses on short sales) does not exceed 1.60% for Class A, 2.20% for Class C and 1.35% for Investor Class. These expense limitations may not be amended or withdrawn until one year after the date of this prospectus. To the extent acquired fund fees are excluded from the waiver and reimbursement calculation, “Total Annual Fund Operating Expenses after Fee Waivers and Expense Reimbursements” will be higher. The total annual fund operating expenses in this fee table may therefore differ from the expense ratios in the financial highlights in this prospectus because the financial highlights include only the Fund’s direct operating expenses and do not include fees or expenses incurred indirectly by the Fund through its investments in the underlying fund(s). |

| Meridian Contrarian Fund | 8 |

Table of Contents

| 2 | Positive waiver reflects recoupment by the Adviser. |

| 3 | For a period not to exceed three (3) years on which a waiver of reimbursement in excess of the expense limitation is made by the Investment Adviser, the Fund will carry forward, and may repay the Investment Adviser such amounts; provided that the Fund is able to effect such reimbursement and maintain the expense limitation in effect at the time of the waiver. |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in Class A shares, Class C shares or Investor Class shares of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the Fund’s operating expenses remain the same and the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment shown above will only be in place for the length of the current commitment. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 728 | $ | 1,013 | $ | 1,319 | $ | 2,184 | ||||||||

| Class C Shares | $ | 317 | $ | 670 | $ | 1,149 | $ | 2,472 | ||||||||

| Investor Class Shares | $ | 137 | $ | 392 | $ | 665 | $ | 1,447 | ||||||||

You would pay the following expenses if you did not redeem your shares of the Fund:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 728 | $ | 1,013 | $ | 1,319 | $ | 2,184 | ||||||||

| Class C Shares | $ | 217 | $ | 670 | $ | 1,149 | $ | 2,472 | ||||||||

| Investor Class Shares | $ | 137 | $ | 392 | $ | 665 | $ | 1,447 | ||||||||

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when the Fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund’s performance. For the fiscal year ended June 30, 2018, the Fund’s portfolio turnover rate was 49% of the average value of its portfolio.

Principal Investment Strategies

The Fund seeks long-term growth of capital by investing primarily in a diversified portfolio of publicly traded common stocks of U.S. companies. Under normal circumstances, the Fund invests in the stocks of businesses that are out of consensus favor and likely to have recently underperformed their peers, or the market due to what the Investment Adviser deems to be temporary operational issues. The Fund then emphasizes

| 9 | Meridian Contrarian Fund |

Table of Contents

stocks which the Investment Adviser believes are undervalued in relation to the business’ (or issuer’s) long-term earnings power or asset value, or the stock market in general. Securities in which the Fund invests may be undervalued because of many factors, including market decline, poor economic conditions, tax-loss selling or actual or anticipated unfavorable developments affecting the issuer of the security. The Fund may invest in securities of companies with any capitalization across a broad range of industries. The Fund intends to invest at least 65% of its total assets in common stocks and equity-related securities (such as convertible debt securities and warrants). The Fund may invest up to 35% of its total assets in debt or fixed income securities, including higher yield, higher risk, lower rated or unrated corporate bonds commonly referred to as “junk bonds.” These are bonds that are rated Ba or below by Moody’s or BB or below by S&P. The Fund may invest up to 10% of its total assets in securities rated Ca or below by Moody’s or C or below by S&P, or unrated but considered by the Investment Adviser to be of comparable quality. The Fund may also invest up to 25% of its total assets, calculated at the time of purchase, in securities of foreign companies, including emerging market companies. The Fund generally sells investments when (i) the Investment Adviser concludes that the company’s fundamentals are not meeting expectations; (ii) better investment opportunities exist; and/or (iii) the company’s business has improved and this, in the Investment Adviser’s opinion, is reflected in the share price.

Principal Investment Risks

There are risks involved with any investment. The principal risks associated with an investment in the Fund, which could adversely affect its net asset value, yield and return, are set forth below. Please see the section “Further Information About Principal Risks” in this Prospectus for a more detailed discussion of these risks and other factors you should carefully consider before deciding to invest in the Fund.

An investment in the Fund may lose money and is not a deposit of a bank or insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

Investment Strategy Risk — The Investment Adviser uses the Fund’s principal investment strategies and other investment strategies to seek to achieve the Fund’s investment objective of long-term growth of capital. There is no assurance that the Investment Adviser’s investment strategies or securities selection method will achieve that investment objective.

Equity Securities Risk — Equity securities fluctuate in price and value in response to many factors including historical and prospective earnings of the issuer and its financial condition, the value of its assets, general economic conditions, interest rates, investors’ perceptions and market liquidity.

Market Risk — The value of the Fund’s investments will fluctuate in response to the activities of individual companies and general stock market and economic conditions. As a result, the value of your investment in the Fund may be more or less than your purchase price.

Value Securities Risk — The market value of a value security may take longer than anticipated to rise, may decline or may fail to meet the Investment Adviser’s assessment of its potential value. In addition, value securities, at times, may not perform as well as growth securities or the stock market in general, and may be out of favor with investors for varying periods of time.

| Meridian Contrarian Fund | 10 |

Table of Contents

Small and Medium Company Risk — Generally, the smaller the capitalization of a company, the greater the risk associated with an investment in the company. The stock prices of small- and mid-capitalization and newer companies tend to fluctuate more than those of larger capitalized and/or more established companies and generally have a smaller market for their shares than do large capitalization companies.

Foreign Securities Risk — Investments in foreign securities may be subject to more risks than those associated with U.S. investments, including currency fluctuations, political and economic instability and differences in accounting, auditing and financial reporting standards. Foreign securities may be less liquid than domestic securities so that the Fund may, at times, be unable to sell foreign securities at desirable times or prices. In addition, emerging market securities involve greater risk and more volatility than those of companies in more developed markets. Significant levels of foreign taxes are also a risk related to foreign investments.

High Yield Bond Risk — Debt securities that are rated below investment grade (commonly referred to as “junk bonds”) involve a greater risk of default or price declines than investment grade securities. The market for high-yield, lower rated securities may be smaller and less active, causing market price volatility and limited liquidity in the secondary market. This may limit the ability of a Fund to sell these securities at their fair market values either to meet redemption requests, or in response to changes in the economy or the financial markets.

Debt Securities Risk — Debt securities are subject to credit risk, interest rate risk and liquidity risk. Credit risk is the risk that the entity that issued a debt security may become unable to make payments of principal and interest when due and includes the risk of default. Interest rate risk is the risk of losses due to changes in interest rates. Liquidity risk is the risk that the Fund may not be able to sell portfolio securities because there are too few buyers for them.

Sector Concentration Risk — The Fund may concentrate its investments in companies that are in a single sector or related sector. Concentrating investments in a single sector may make the Fund more susceptible to adverse economic, business, regulatory or other developments affecting that sector. If an economic downturn occurs in a sector in which the Fund’s investments are concentrated, the Fund may perform poorly during that period. The Fund anticipates it will typically invest a significant portion of its assets in the information technology (IT) sector and, therefore, the Fund’s performance could be negatively impacted by events affecting this sector. The information technology sector includes, for example, internet, semiconductor, software, hardware, and technology equipment companies. The IT sector may be adversely affected by, among other things, the supply and demand for specific products and services, the pace of technological development, and government regulation.

Securities Lending Risk — The Fund may engage in securities lending. Securities lending involves the risk that the Fund may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for the Fund.

| 11 | Meridian Contrarian Fund |

Table of Contents

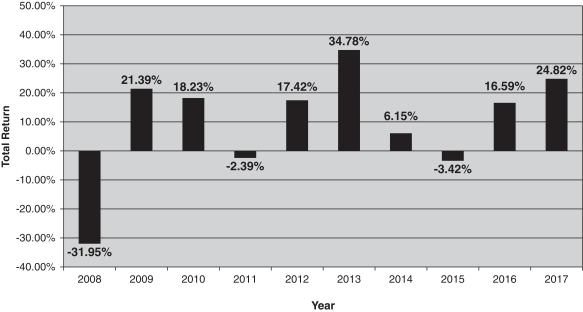

Performance

The bar chart and table below show the Fund’s historical performance and provide an indication of the risks of investing in the Fund. The bar chart shows changes in the performance of the Fund’s Investor Class shares from year-to-year. The performance of the Fund’s other share classes would have differed from the Investor Class shares only to the extent that such classes have higher expenses than the Investor Class shares, which would have resulted in lower performance.

The table shows how the Fund’s average annual returns compare with those of the Russell 2500® Index. The Fund’s past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Updated performance information for the Fund may be obtained by visiting www.meridianfund.com or by calling 1-800-446-6662.

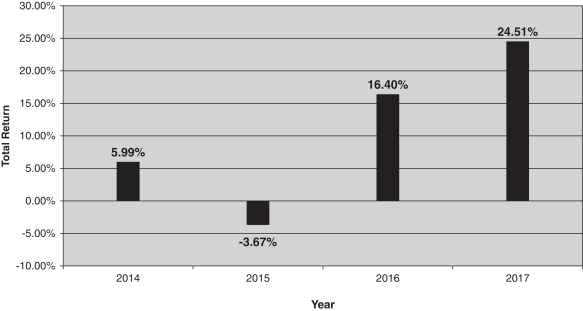

Year-by-Year Total Returns as of 12/31

During the period covered by this bar chart, the Fund’s Investor Class shares highest quarterly return was 9.92% (for the quarter ended September 30, 2016); and the lowest quarterly return was –11.51% (for the quarter ended September 30, 2015).

For the period January 1, 2018 through September 30, 2018, the total return of the Fund’s Investor Class shares was 13.89%.

| Meridian Contrarian Fund | 12 |

Table of Contents

Average Annual Total Returns

(For the year ended December 31, 2017)

| MERIDIAN CONTRARIAN FUND Investor Class Shares (11/15/13) |

1 Year |

Life of Class | ||||||

| Return Before Taxes |

24.51% | 10.88% | ||||||

| Return After Taxes on Distributions |

21.65% | 8.21% | ||||||

| Return After Taxes on Distributions and Sale of Fund Shares1 |

16.19% | 8.08% | ||||||

| Russell 2500® Index (reflects no deductions for fees, expenses or taxes) |

16.81% | 10.71% | ||||||

| 1 | The Fund’s returns after taxes on distributions and sale of Fund shares may be higher than its returns after taxes on distributions because it includes the effect of a tax benefit an investor may receive resulting from the capital losses that would have been incurred on the sale of the shares. |

After-tax returns are calculated using the historical highest individual federal marginal income tax rates for the character of income in question (as ordinary income or long-term gain) and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts.

Management

ArrowMark Colorado Holdings, LLC

Portfolio Managers

Larry Cordisco serves as a Co-Portfolio Manager of the Fund. Mr. Cordisco, who joined the Investment Adviser in 2013 when it acquired the asset management business of the previous investment adviser to the Fund, where he worked as an investment professional since 2012, has served as a Co-Portfolio Manager of the Fund since September 5, 2013.

James England, CFA, serves as a Co-Portfolio Manager of the Fund. Mr. England, who joined the Investment Adviser in 2013 when it acquired the asset management business of the previous investment adviser to the Fund, where he worked as an investment professional since 2001, has assisted with managing the Fund since 2001.

Purchase and Sale of Fund Shares

The following table shows the minimum investment amounts for purchasing share classes of the Meridian Contrarian Fund.

| Class | Minimum Initial Investment | Minimum Subsequent Investment | Distribution Fee | |||

| Class A Shares | $2,5001 | $50 | 0.25% | |||

| Class C Shares | $2,5001 | $50 | 1.00% | |||

| Investor Class Shares | $99,999 | NONE | NONE |

| 1 | Certain tax-deferred retirement accounts or UGMA/UTMA accounts are subject to a $500 minimum. |

| 13 | Meridian Contrarian Fund |

Table of Contents

The Funds reserve the right to change the amount of these minimums from time to time or to waive them in whole or in part if, in the Investment Adviser’s or the Fund’s opinion, the investor has adequate intent and availability of assets to reach a future level of investment in the Fund that is equal to or greater than the minimum.

You may purchase, redeem or exchange shares of the Funds on any business day, which is any day the New York Stock Exchange is open for business. Generally, you may purchase, redeem or exchange shares only through institutional channels, such as financial intermediaries and retirement platforms. The minimum investment for Class A shares and Class C shares is $2,500 per Fund account for non-retirement accounts. The minimum investment for the Investor Class shares is $99,999 per Fund account for non-retirement accounts. Certain tax-deferred retirement accounts or UGMA/UTMA accounts are subject to a $500 minimum. Investors in a defined contribution plan through a third-party administrator should refer to their plan document or contact their plan administrator for additional information. Accounts that are a part of certain wrap programs may not be subject to these minimums. Investors should refer to their intermediary for additional information.

Tax Information

Any distributions you receive from a Fund will be taxable as ordinary income, capital gains or qualified dividend income, except when your investment is in an IRA, 401(k) or other tax advantaged investment plan. Subsequent withdrawals from such a tax-advantaged investment plan will be subject to special tax rules. You should consult your tax adviser about your specific tax situation.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of a Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related entities may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your advisor to recommend the Fund or one share class over another investment or share class, as applicable. Ask your advisor or financial intermediary for more information.

| Meridian Contrarian Fund | 14 |

Table of Contents

FUND SUMMARY

Investment Objective

The MERIDIAN ENHANCED EQUITY FUND (formerly known as Meridian Equity Income Fund) seeks long-term growth of capital.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

| Shareholder Fees (fees paid directly from your investment) |

|

Class A Shares |

|

|

Class C Shares |

|

|

Investor Class Shares |

| |||

| Maximum Sales Charge (Load) on Purchases |

5.75% | NONE | NONE | |||||||||

| Maximum Deferred Sales Charge (Load) |

NONE | 1.00% | NONE | |||||||||

| Redemption Fee (as a percentage of amount redeemed, if you sell or exchange your shares within 60 days of purchase) |

2.00% | NONE | 2.00% | |||||||||

| Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||||||||||||

| Management Fees |

0.86% | 0.86% | 0.86% | |||||||||

| Distribution (Rule 12b-1) Fees |

0.25% | 1.00% | 0.00% | |||||||||

| Dividend and Interest Expense on Securities Sold Short |

0.23% | 0.24% | 0.23% | |||||||||

| Other Expenses |

0.44% | 0.15% | 0.38% | |||||||||

| Total Annual Fund Operating Expenses |

1.78% | 2.25% | 1.47% | |||||||||

| Fee Waivers and/or Expense Reimbursements and Recoupment |

0.06% | 3 | (0.01)% | 0.12% | 3 | |||||||

| Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment1,2 |

1.84% | 2.24% | 1.59% |

| 1 | The Investment Adviser has agreed to waive a portion of the investment advisory and/or administration fees and/or reimburse other expenses of the Meridian Enhanced Equity Fund so that the ratio of expenses to average net assets of the Meridian Enhanced Equity Fund (excluding acquired fund fees and expenses, dividend expenses on securities sold short, and interest expenses on short sales) does not exceed 1.60% for Class A, 2.00% for Class C and 1.35% for Investor Class. These expense limitations may not be amended or withdrawn until one year after the date of this prospectus. To the extent acquired fund fees are excluded from the waiver and reimbursement calculation, “Total Annual Fund Operating Expenses after Fee Waivers and Expense Reimbursements” will be higher. The total annual fund operating expenses in this fee table |

| 15 | Meridian Enhanced Equity Fund |

Table of Contents

| may therefore differ from the expense ratios in the financial highlights in this prospectus because the financial highlights include only the Fund’s direct operating expenses and do not include fees or expenses incurred indirectly by the Fund through its investments in the underlying fund(s). |

| 2 | For a period not to exceed three (3) years on which a waiver of reimbursement in excess of the expense limitation is made by the Investment Adviser, the Fund will carry forward, and may repay the Investment Adviser such amounts; provided that the Fund is able to effect such reimbursement and maintain the expense limitation in effect at the time of the waiver. |

| 3 | Positive waiver reflects recoupment by the Adviser. |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in Class A shares, Class C shares or Investor Class shares of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the Fund’s operating expenses remain the same and the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment shown above will only be in place for the length of the current commitment. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 751 | $ | 1,109 | $ | 1,489 | $ | 2,554 | ||||||||

| Class C Shares | $ | 327 | $ | 702 | $ | 1,204 | $ | 2,584 | ||||||||

| Investor Class Shares | $ | 162 | $ | 477 | $ | 814 | $ | 1,768 | ||||||||

You would pay the following expenses if you did not redeem your shares of the Fund:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 751 | $ | 1,109 | $ | 1,489 | $ | 2,554 | ||||||||

| Class C Shares | $ | 227 | $ | 702 | $ | 1,204 | $ | 2,584 | ||||||||

| Investor Class Shares | $ | 162 | $ | 477 | $ | 814 | $ | 1,768 | ||||||||

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when the Fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund’s performance. For the fiscal year ended June 30, 2018, the Fund’s portfolio turnover rate was 49% of the average value of its portfolio.

Principal Investment Strategies

The Fund seeks to maximize total return by investing primarily in a diversified portfolio of equity securities of large capitalization U.S. companies that have the potential for capital appreciation. Under normal

| Meridian Enhanced Equity Fund | 16 |

Table of Contents

circumstances, the Fund will invest at least 80% of its net assets in long or short positions in equity securities. Equity securities include, but are not limited to, common and preferred stocks as well as convertible securities, such as options, in domestic and foreign companies. The Fund may invest in securities of companies with any capitalization across a broad range of industries. These may include companies that are relatively small in terms of assets, revenues and earnings. The mix of the Fund’s investments at any time will depend on the industries and types of securities the Investment Adviser believes hold the most potential for achieving the Fund’s investment objective. The Fund may invest up to 25% of its total assets, calculated at the time of purchase, in securities of foreign companies, including emerging market companies. The Fund may also invest its assets in debt or fixed income securities including higher yield, higher risk, lower rated or unrated corporate bonds commonly referred to as “junk bonds.” These are bonds that are rated Ba or below by Moody’s Investors Service, Inc. (“Moody’s”) or BB or below by Standard and Poor’s Ratings Services (“S&P”) or are in default or unrated but of comparable quality as determined by the Investment Adviser. The Fund generally sells investments when the Investment Adviser concludes that the long-term growth or dividend prospects of the company have deteriorated, or the issuer’s circumstances or the political or economic outlook relative to the security have changed, and better investment opportunities exist in other securities.

Principal Investment Risks

There are risks involved with any investment. The principal risks associated with an investment in the Fund, which could adversely affect its net asset value, yield and return, are set forth below. Please see the section “Further Information About Principal Risks” in this Prospectus for a more detailed discussion of these risks and other factors you should carefully consider before deciding to invest in the Fund.

An investment in the Fund may lose money and is not a deposit of a bank or insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

Investment Strategy Risk — The Investment Adviser uses the Fund’s principal investment strategies and other investment strategies to seek to achieve the Fund’s investment objective of long-term growth of capital along with income as a component of total return. There is no assurance that the Investment Adviser’s investment strategies or securities selection method will achieve that investment objective.

Equity Securities Risk — Equity securities fluctuate in price and value in response to many factors including historical and prospective earnings of the issuer and its financial condition, the value of its assets, general economic conditions, interest rates, investors’ perceptions and market liquidity.

Market Risk — The value of the Fund’s investments will fluctuate in response to the activities of individual companies and general stock market and economic conditions. As a result, the value of your investment in the Fund may be more or less than your purchase price.

Income Risk — The Fund may not be able to pay distributions or may have to reduce its distribution level if the amount of dividends and/or interest received by the Fund on the securities it holds declines or is insufficient to pay such distributions.

Small Company Risk — Generally, the smaller the capitalization of a company, the greater the risk associated with an investment in the company. The stock prices of small capitalization and newer companies tend to fluctuate more than those of larger capitalized and/or more established companies and generally have a smaller market for their shares than do large capitalization companies.

| 17 | Meridian Enhanced Equity Fund |

Table of Contents

Foreign Securities Risk — Investments in foreign securities may be subject to more risks than those associated with U.S. investments, including currency fluctuations, political and economic instability and differences in accounting, auditing and financial reporting standards. Foreign securities may be less liquid than domestic securities so that the Fund may, at times, be unable to sell foreign securities at desirable times or prices. In addition, emerging market securities involve greater risk and more volatility than those of companies in more developed markets. Significant levels of foreign taxes are also a risk related to foreign investments.

High Yield Bond Risk — Debt securities that are rated below investment grade (commonly referred to as “junk bonds”) involve a greater risk of default or price declines than investment grade securities. The market for high-yield, lower rated securities may be smaller and less active, causing market price volatility and limited liquidity in the secondary market. This may limit the ability of a Fund to sell these securities at their fair market values either to meet redemption requests, or in response to changes in the economy or the financial markets.

Debt Securities Risk — Debt securities are subject to credit risk, interest rate risk and liquidity risk. Credit risk is the risk that the entity that issued a debt security may become unable to make payments of principal and interest when due and includes the risk of default. Interest rate risk is the risk of losses due to changes in interest rates. Liquidity risk is the risk that the Fund may not be able to sell portfolio securities because there are too few buyers for them.

Options Risk — The success of the Fund’s investment in options depends upon many factors, such as the price of the options, which is a function of interest rates, volatility, dividends, the exercise price, stock price and other market factors. These factors may change rapidly over time.

The principal risk associated with writing put options, is that the Fund assumes the risk that it will have to purchase the underlying security at an exercise price that may be higher than the market price of the security. If the market price of the underlying security declines, the Fund would expect to suffer a loss. However, the premium the Fund received for writing the put should offset a portion of the decline.

The principal risk associated with purchasing options is that price valuations or market movements may not justify purchasing the options, or, if purchased, the options may expire unexercised, causing the Fund to lose the premium paid (i.e., incur the cost of the options but not the attendant benefits).

The principal risk associated with writing covered call options is that the Fund will be required to sell the underlying security (i.e., have the security “called”) and, therefore, will not participate in gains if the stock price exceeds the exercise price generally at the expiration date of the option.

The Fund’s investment in options may also result in reduced flexibility in purchases and sales of portfolio securities. Because the Fund may hold the securities underlying the options held or sold by the Fund, the Fund may be less likely to sell such securities in its portfolio to take advantage of new investment opportunities.

Sector Concentration Risk — The Fund may concentrate its investments in companies that are in a single sector or related sector. Concentrating investments in a single sector may make the Fund more susceptible to adverse economic, business, regulatory or other developments affecting that sector. If an economic downturn occurs in a sector in which the Fund’s investments are concentrated, the Fund may perform poorly during that period. The Fund anticipates it will typically invest a significant portion of its assets in the information technology (IT) sector and, therefore, the Fund’s performance could be negatively impacted by events affecting this sector. The information technology sector includes, for example, internet, semiconductor,

| Meridian Enhanced Equity Fund | 18 |

Table of Contents

software, hardware, and technology equipment companies. The IT sector may be adversely affected by, among other things, the supply and demand for specific products and services, the pace of technological development, and government regulation.

Securities Lending Risk — The Fund may engage in securities lending. Securities lending involves the risk that the Fund may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for the Fund.

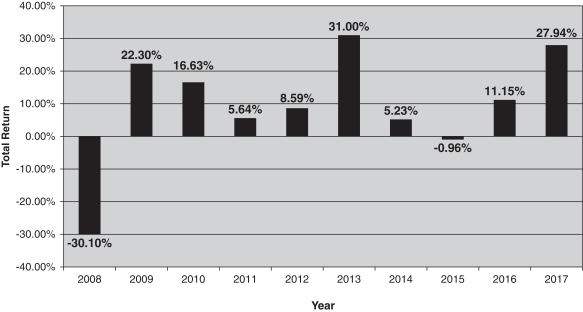

Performance

The bar chart and table below show the Fund’s historical performance and provides an indication of the risks of investing in the Fund. The bar chart shows changes in the performance of the Fund’s Investor Class shares from year-to-year. The performance of the Fund’s other share classes would have differed from the Investor Class shares only to the extent that such classes’ shares have higher expenses than the Investor Class shares, which would have resulted in lower performance.

The table shows how the Fund’s average annual returns compare with those of the Fund’s benchmark, the S&P 500® Index. The Fund’s past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Updated performance information for the Fund may be obtained by visiting www.meridianfund.com or by calling 1-800-446-6662.

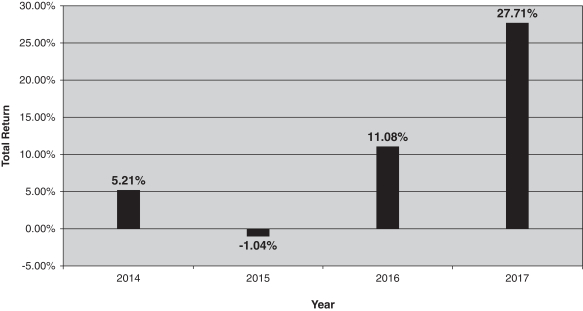

Year-by-Year Total Returns as of 12/31

| 19 | Meridian Enhanced Equity Fund |

Table of Contents

During the period covered by this bar chart, the Fund’s Investor Class shares highest quarterly return was 10.05% (for the quarter ended December 31, 2017); and the lowest quarterly return was –8.06% (for the quarter ended September 30, 2015).

For the period January 1, 2018 through September 30, 2018, the total return of the Fund’s Investor Class shares was 21.53%.

Average Annual Total Returns

(For the year ended December 31, 2017)

| MERIDIAN ENHANCED EQUITY FUND Investor Class Shares (11/15/13) |

1 Year |

Life of Class | ||||||

| Return Before Taxes |

27.71% | 10.49% | ||||||

| Return After Taxes on Distributions |

27.37% | 8.86% | ||||||

| Return After Taxes on Distributions and Sale of Fund Shares1 |

15.94% | 7.92% | ||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

21.82% | 12.51% | ||||||

| 1 | The Fund’s returns after taxes on distributions and sale of Fund shares may be higher than its returns after taxes on distributions because it includes the effect of a tax benefit an investor may receive resulting from the capital losses that would have been incurred on the sale of the shares. |

After-tax returns are calculated using the historical highest individual federal marginal income tax rates for the character of income in question (as ordinary income or long-term gain) and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts.

Management

ArrowMark Colorado Holdings, LLC

Portfolio Manager

Minyoung Sohn, CFA, serves as Portfolio Manager of the Fund. Mr. Sohn, who joined the Investment Adviser in 2008, has served as Portfolio Manager of the Fund since October 31, 2014.

Purchase and Sale of Fund Shares

The following table shows the minimum investment amounts for purchasing share classes of the Meridian Enhanced Equity Fund.

| Class | Minimum Initial Investment | Minimum Subsequent Investment | Distribution Fee | |||

| Class A Shares | $2,5001 | $50 | 0.25% | |||

| Class C Shares | $2,5001 | $50 | 1.00% | |||

| Investor Class Shares | $99,999 | NONE | NONE |

| 1 | Certain tax-deferred retirement accounts or UGMA/UTMA accounts are subject to a $500 minimum. |

| Meridian Enhanced Equity Fund | 20 |

Table of Contents

The Funds reserve the right to change the amount of these minimums from time to time or to waive them in whole or in part if, in the Investment Adviser’s or the Fund’s opinion, the investor has adequate intent and availability of assets to reach a future level of investment in the Fund that is equal to or greater than the minimum.

You may purchase, redeem or exchange shares of the Funds on any business day, which is any day the New York Stock Exchange is open for business. Generally, you may purchase, redeem or exchange shares only through institutional channels, such as financial intermediaries and retirement platforms. The minimum investment for Class A shares and Class C shares is $2,500 per Fund account for non-retirement accounts. The minimum investment for the Investor Class shares is $99,999 per Fund account for non-retirement accounts. Certain tax-deferred retirement accounts or UGMA/UTMA accounts are subject to a $500 minimum. Investors in a defined contribution plan through a third-party administrator should refer to their plan document or contact their plan administrator for additional information. Accounts that are a part of certain wrap programs may not be subject to these minimums. Investors should refer to their intermediary for additional information.

Tax Information

Any distributions you receive from a Fund will be taxable as ordinary income, capital gains or qualified dividend income, except when your investment is in an IRA, 401(k) or other tax advantaged investment plan. Subsequent withdrawals from such a tax-advantaged investment plan will be subject to special tax rules. You should consult your tax adviser about your specific tax situation.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of a Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related entities may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your advisor to recommend the Fund or one share class over another investment or share class, as applicable. Ask your advisor or financial intermediary for more information.

| 21 | Meridian Enhanced Equity Fund |

Table of Contents

FUND SUMMARY

MERIDIAN SMALL CAP GROWTH FUND

Investment Objective

The MERIDIAN SMALL CAP GROWTH FUND seeks long-term growth of capital by investing primarily in equity securities of small capitalization companies.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

| Shareholder Fees (fees paid directly from your investment) |

|

Class A Shares |

|

|

Class C Shares |

|

|

Investor Class Shares |

| |||

| Maximum Sales Charge (Load) on Purchases |

5.75% | NONE | NONE | |||||||||

| Maximum Deferred Sales Charge (Load) |

NONE | 1.00% | NONE | |||||||||

| Redemption Fee (as a percentage of amount redeemed, if you sell or exchange your shares within 60 days of purchase) |

2.00% | NONE | 2.00% | |||||||||

| Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||||||||||||

| Management Fees |

1.00% | 1.00% | 1.00% | |||||||||

| Distribution (Rule 12b-1) Fees |

0.25% | 1.00% | 0.00% | |||||||||

| Acquired Fund Fees and Expenses |

0.05% | 0.05% | 0.05% | |||||||||

| Other Expenses |

0.16% | 0.15% | 0.16% | |||||||||

| Total Annual Fund Operating Expenses1 |

1.46% | 2.20% | 1.21% | |||||||||

| Fee Waivers and/or Expense Reimbursements and Recoupment |

N/A | N/A | N/A | |||||||||

| Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment2,3 |

1.46% | 2.20% | 1.21% |

| 1 | Please note that Total Annual Fund Operating Expenses in the table above does not correlate to the ratio of Operating Expenses Before Waivers/Reimbursements/Reductions to Average Net Assets found in the “Financial Highlights” section of this prospectus since the latter reflects the operating expenses of the Fund and does not include Acquired Fund Fees and Expenses. |

| 2 | The Investment Adviser has agreed to waive a portion of the investment advisory and/or administration fees and/or reimburse other expenses of the Meridian Small Cap Growth Fund so that the ratio of expenses to average net assets of the Meridian Small Cap Growth Fund (excluding acquired fund fees and expenses, dividend expenses on securities sold short, and interest expenses on short sales) does not exceed 1.60% for |

| Meridian Small Cap Growth Fund | 22 |

Table of Contents

| Class A, 2.25% for Class C and 1.35% for Investor Class. These expense limitations may not be amended or withdrawn until one year after the date of this prospectus. To the extent acquired fund fees are excluded from the waiver and reimbursement calculation, “Total Annual Fund Operating Expenses after Fee Waivers and Expense Reimbursements” will be higher. The total annual fund operating expenses in this fee table may therefore differ from the expense ratios in the financial highlights in this prospectus because the financial highlights include only the Fund’s direct operating expenses and do not include fees or expenses incurred indirectly by the Fund through its investments in the underlying fund(s). |

| 3 | For a period not to exceed three (3) years on which a waiver of reimbursement in excess of the expense limitation is made by the Investment Adviser, the Fund will carry forward, and may repay the Investment Adviser such amounts; provided that the Fund is able to effect such reimbursement and maintain the expense limitation in effect at the time of the waiver. |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in Class A shares, Class C shares or Investor Class shares of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the Fund’s operating expenses remain the same and the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement and Recoupment shown above will only be in place for the length of the current commitment. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 715 | $ | 1,010 | $ | 1,327 | $ | 2,221 | ||||||||

| Class C Shares | $ | 323 | $ | 688 | $ | 1,180 | $ | 2,534 | ||||||||

| Investor Class Shares | $ | 123 | $ | 384 | $ | 665 | $ | 1,466 | ||||||||

You would pay the following expenses if you did not redeem your shares of the Fund:

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class A Shares | $ | 715 | $ | 1,010 | $ | 1,327 | $ | 2,221 | ||||||||

| Class C Shares | $ | 223 | $ | 688 | $ | 1,180 | $ | 2,534 | ||||||||

| Investor Class Shares | $ | 123 | $ | 384 | $ | 665 | $ | 1,466 | ||||||||

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when the Fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund’s performance. For the fiscal year ended June 30, 2018, the Fund’s portfolio turnover rate was 44% of the average value of its portfolio.

| 23 | Meridian Small Cap Growth Fund |

Table of Contents

Principal Investment Strategies

The Fund seeks long-term growth of capital by investing, under normal circumstances, at least 80% of its net assets, including the amount of any borrowings for investment purposes, in equity securities (including common stocks, preferred stocks and securities convertible into common and preferred stocks) of U.S. small capitalization companies. In the view of the Investment Adviser, small capitalization companies are defined as companies whose total market capitalization falls within the range of companies included in the Russell 2000® Growth Index or the S&P SmallCap 600® Index at the time of purchase. Both indices are broad indices of small capitalization stocks. As of September 30, 2018, the market capitalization of the companies in these indices ranged from approximately $11 million to $7.7 billion. The Fund may also invest up to 20% of its net assets in securities of companies of any market capitalization.

The portfolio managers apply a “bottom up” fundamental research process in selecting investments. In other words, the portfolio managers analyze individual companies to determine if a company presents an attractive investment opportunity and if it is consistent with the Fund’s investment strategies and policies.

Principal Investment Risks

There are risks involved with any investment. The principal risks associated with an investment in the Fund, which could adversely affect its net asset value, yield and return, are set forth below. Please see the section “Further Information About Principal Risks” in this Prospectus for a more detailed discussion of these risks and other factors you should carefully consider before deciding to invest in the Fund.

An investment in the Fund may lose money and is not a deposit of a bank or insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

Investment Strategy Risk — The Investment Adviser uses the Fund’s principal investment strategies and other investment strategies to seek to achieve the Fund’s investment objective of long-term growth of capital by investing primarily in equity securities of small capitalization companies. There is no assurance that the Investment Adviser’s investment strategies or securities selection method will achieve that investment objective.

Equity Securities Risk — Equity securities fluctuate in price and value in response to many factors including historical and prospective earnings of the issuer and its financial condition, the value of its assets, general economic conditions, interest rates, investors’ perceptions and market liquidity.

Market Risk — The value of the Fund’s investments will fluctuate in response to the activities of individual companies and general stock market and economic conditions. As a result, the value of your investment in the Fund may be more or less than your purchase price.

Growth Securities Risk — Because growth securities typically trade at a higher multiple of earnings than other types of securities, the market values of growth securities may be more sensitive to changes in current or expected earnings than the market values of other types of securities. In addition, growth securities, at times, may not perform as well as value securities or the stock market in general, and may be out of favor with investors for varying periods of time.

| Meridian Small Cap Growth Fund | 24 |

Table of Contents

Small Company Risk — Generally, the smaller the capitalization of a company, the greater the risk associated with an investment in the company. The stock prices of small capitalization and newer companies tend to fluctuate more than those of larger capitalized and/or more established companies and generally have a smaller market for their shares than do large capitalization companies.

Sector Concentration Risk — The Fund may concentrate its investments in companies that are in a single sector or related sector. Concentrating investments in a single sector may make the Fund more susceptible to adverse economic, business, regulatory or other developments affecting that sector. If an economic downturn occurs in a sector in which the Fund’s investments are concentrated, the Fund may perform poorly during that period. The Fund anticipates it will typically invest a significant portion of its assets in the information technology (IT) sector, the industrials sector and the health care sector and, therefore, the Fund’s performance could be negatively impacted by events affecting these sectors.

The information technology sector includes, for example, internet, semiconductor, software, hardware, and technology equipment companies. The IT sector may be adversely affected by, among other things, the supply and demand for specific products and services, the pace of technological development, and government regulation. The industrials sector may be adversely affected by, among other things, changes in the supply of and demand for products and services, product obsolescence, claims for environmental damage or product liability and general economic conditions. The health care sector is subject to extensive government regulation and its profitability can be adversly affected by, among other things, restrictions on government reimbursement for medical expenses, rising costs of medical products and services, and increased emphasis on the delivery of healthcare through outpatient services.

Securities Lending Risk — The Fund may engage in securities lending. Securities lending involves the risk that the Fund may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for the Fund.

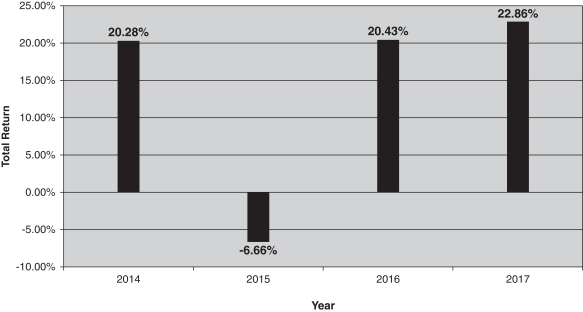

Performance

The bar chart and table below show the Fund’s historical performance and provide an indication of the risks of investing in the Fund. The bar chart shows changes in the performance of the Fund’s Investor Class shares from year-to-year. The performance of the Fund’s other share classes would have differed from the Investor Class shares only to the extent that such classes have higher expenses than the Investor Class shares, which would have resulted in lower performance.

The Fund’s Benchmark is the Russell 2000® Growth Index. Updated performance information for the Fund may be obtained by visiting www.meridianfund.com or by calling 1-800-446-6662.

| 25 | Meridian Small Cap Growth Fund |

Table of Contents

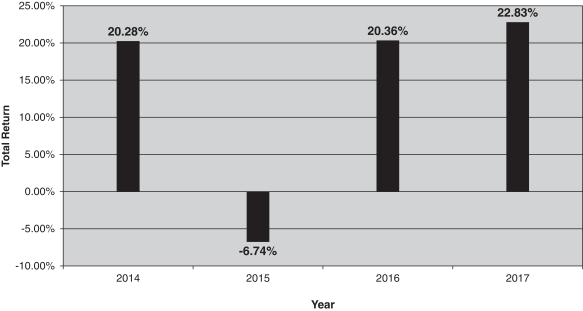

Year-by-Year Total Returns as of 12/31

During the period covered by this bar chart, the Fund’s Investor Class shares highest quarterly return was 13.03% (for the quarter ended December 31, 2014); and the lowest quarterly return was –12.41% (for the quarter ended September 30, 2015).

For the period January 1, 2018 through September 30, 2018, the total return of the Fund’s Investor Class shares was 20.87%.

Average Annual Total Returns

(For the year ended December 31, 2017)

| MERIDIAN SMALL CAP GROWTH FUND Investor Class Shares (12/16/13) |

1 Year |

Life of Class | ||||||

| Return Before Taxes |

22.83% | 14.57% | ||||||

| Return After Taxes on Distributions |

21.12% | 13.70% | ||||||

| Return After Taxes on Distributions and Sale of Fund Shares1 |

13.35% | 11.20% | ||||||

| Russell 2000® Growth Index (reflects no deductions for fees, expenses or taxes) |

22.17% | 10.47% | ||||||

| 1 | The Fund’s returns after taxes on distributions and sale of Fund shares may be higher than its returns after taxes on distributions because it includes the effect of a tax benefit an investor may receive resulting from the capital losses that would have been incurred on the sale of the shares. |

| Meridian Small Cap Growth Fund | 26 |

Table of Contents

After-tax returns are calculated using the historical highest individual federal marginal income tax rates for the character of income in question (as ordinary income or long-term gain) and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts.

Management

ArrowMark Colorado Holdings, LLC

Portfolio Managers

Chad Meade serves as a Co-Portfolio Manager of the Fund. Mr. Meade, who joined the Investment Adviser in 2013, has served as a Co-Portfolio Manager of the Fund since inception.