| 1933 Act File No. |

33-54445 |

| 1940 Act File No. |

811-7193 |

Form N-1A

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

|

| |

|

|

|

| |

Pre-Effective Amendment No. |

|

|

| |

|

|

|

| |

Post-Effective Amendment No. |

|

102 |

| |

| and/or |

| |

|

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

|

| |

|

|

|

| |

Amendment No. |

|

103 |

| |

|

|

|

|

FEDERATED INSTITUTIONAL TRUST

(Exact Name of Registrant as Specified in Charter)

Federated Investors Funds

4000 Ericsson Drive

Warrendale, PA 15086-7561

(Address of Principal Executive Offices)

(412) 288-1900

(Registrant’s Telephone Number, including

Area Code)

Peter J. Germain, Esquire

Federated Investors Tower

Pittsburgh, Pennsylvania 15222-3779

(Name and Address of Agent for Service)

| It is proposed that this filing will become effective (check appropriate box): |

| |

|

| X |

immediately upon filing pursuant to paragraph (b) |

| |

on pursuant to paragraph (b) |

| |

60 days after filing pursuant to paragraph (a)(1) |

| |

on |

|

pursuant to paragraph (a)(1) |

| |

75 days after filing pursuant to paragraph (a)(2) |

| |

on |

|

pursuant to paragraph (a)(2) of Rule 485 |

| |

| If appropriate, check the following box: |

| |

|

| |

This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

Prospectus

December 31, 2019

| Share Class | Ticker

| Institutional | FIHBX

| R6 | FIHLX

|

|

|

Federated Institutional

High Yield Bond Fund

A Portfolio of Federated

Institutional Trust

A mutual fund seeking

high current income by investing primarily in lower-rated corporate fixed-income securities, including debt securities issued by U.S. or foreign businesses.

As with all mutual funds,

the Securities and Exchange Commission (SEC) has not approved or disapproved these securities or passed upon the adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

IMPORTANT

NOTICE TO SHAREHOLDERS

Beginning on January 1,

2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund's shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the

reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and

provided with a website link to access the report.

If you already elected to

receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund or your

financial intermediary electronically by contacting your financial intermediary (such as a broker-dealer or bank); other shareholders may call the Fund at 1-800-341-7400, Option 4.

You may elect to receive

all future reports in paper free of charge. You can inform the Fund or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by contacting your financial intermediary

(such as a broker-dealer or bank); other shareholders may call the Fund at 1-800-341-7400, Option 4. Your election to receive reports in paper will apply to all funds held with the Fund complex or your financial

intermediary.

Not FDIC Insured ■ May

Lose Value ■ No Bank Guarantee

CONTENTS

| 1

|

| 5

|

| 5

|

| 10

|

| 13

|

| 15

|

| 16

|

| 17

|

| 19

|

| 22

|

| 23

|

| 25

|

| 26

|

| 29

|

Fund Summary

Information

Federated Institutional High Yield

Bond Fund (the “Fund”)

RISK/RETURN SUMMARY: INVESTMENT

OBJECTIVE

The

Fund's investment objective is to seek high current income.

RISK/RETURN SUMMARY: FEES AND

EXPENSES

This

table describes the fees and expenses that you may pay if you buy and hold the Fund's Institutional Shares (IS) and Class R6 Shares (R6). If you purchase the Fund's Shares through a broker acting as an agent on behalf

of its customers, you may be required to pay a commission to such broker; such commissions, if any, are not reflected in the Example below.

| Shareholder Fees (fees paid directly from your investment)

| IS

| R6

|

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price)

| None

| None

|

Maximum Deferred Sales Charge (Load) (as a percentage of original purchase price or redemption proceeds, as applicable)

| None

| None

|

Maximum Sales Charge (Load) Imposed on Reinvested Dividends (and other Distributions) (as a percentage of offering price)

| None

| None

|

Redemption Fee (as a percentage of amount redeemed, if applicable)

| None

| None

|

Exchange Fee

| None

| None

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|

|

Management Fee

| 0.40%

| 0.40%

|

Distribution (12b-1) Fee

| None

| None

|

Other Expenses

| 0.15%

| 0.11%

|

Total Annual Fund Operating Expenses

| 0.55%

| 0.51%

|

Fee Waivers and/or Expense Reimbursements1

| (0.05)%

| (0.02)%

|

Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements

| 0.50%

| 0.49%

|

| 1

| The Adviser and certain of its affiliates on their own initiative have agreed to waive certain amounts of their respective fees and/or reimburse expenses. Total annual fund operating expenses (excluding

acquired fund fees and expenses, interest expense, extraordinary expenses and proxy-related expenses paid by the Fund, if any) paid by the Fund's IS class and R6 shares (after the voluntary waivers and/or

reimbursements) will not exceed 0.49% and 0.48% (the “Fee Limit”), respectively, up to but not including the later of (the “Termination Date”): (a) January 1, 2021; or (b) the date of the

Fund's next effective Prospectus. While the Adviser and its affiliates currently do not anticipate terminating or increasing these arrangements prior to the Termination Date, these arrangements may only be terminated

or the Fee Limit increased prior to the Termination Date with the agreement of the Fund's Board of Trustees.

|

Example

This

Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

The

Example assumes that you invest $10,000 for the time periods indicated and then redeem all of your Shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that

operating expenses are as shown in the table above and remain the same. Although your actual costs and returns may be higher or lower, based on these assumptions your costs would be:

| Share Class

| 1 Year

| 3 Years

| 5 Years

| 10 Years

|

| IS

| $56

| $176

| $307

| $689

|

| R6

| $52

| $164

| $285

| $640

|

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher

transaction costs and may result in higher taxes when Fund Shares are held in a taxable account. These costs, which are not reflected in Annual Fund Operating Expenses or in the Example, affect the Fund's performance.

During the most recent fiscal year, the Fund's portfolio turnover rate was 26% of the average value of its portfolio.

RISK/RETURN SUMMARY: INVESTMENTS,

RISKS and PERFORMANCE

What are the Fund's Main

Investment Strategies?

The

Fund pursues its investment objective by investing primarily in a diversified portfolio of high yield corporate bonds (also known as “junk bonds”), which include debt securities issued by U.S. or foreign

businesses (including emerging market debt securities). The Fund's investment adviser (the “Adviser”) selects securities that it believes have attractive risk-return characteristics. The Adviser's

securities selection process includes an analysis of the issuer's financial condition, business and product strength, competitive position and management expertise. The Adviser does not limit the Fund's investments to

securities of a particular maturity range.

The

Fund may invest in derivative contracts (for example, futures contracts, option contracts and swap contracts) to implement its investment strategies as more fully described in the Fund's Prospectus. There can be no

assurance that the Fund's use of derivative contracts or hybrid instruments will work as intended. Derivative investments made by the Fund are included within the Fund's 80% policy (as described below) and are

calculated at market value.

The

Fund will invest its assets so that at least 80% of its net assets (plus any borrowings for investment purposes) are invested in investments rated below investment-grade. The Fund will notify shareholders in advance

of any change in its investment policy that would enable the Fund to invest, under normal circumstances, less than 80% of its net assets in investments rated below investment-grade.

What are the Main Risks of

Investing in the Fund?

All

mutual funds take investment risks. Therefore, it is possible to lose money by investing in the Fund. The primary factors that may reduce the Fund's returns include:

| ■

| Risk Associated with Noninvestment-Grade Securities. Securities rated below investment-grade may be subject to greater interest rate, credit and liquidity risks than investment-grade securities. These securities are considered speculative

with respect to the issuer's ability to pay interest and repay principal.

|

| ■

| Issuer Credit Risk. It is possible that interest or principal on securities will not be paid when due. Noninvestment-grade securities generally have a higher default risk than investment-grade securities. Such

non-payment or default may reduce the value of the Fund's portfolio holdings, its share price and its performance.

|

| ■

| Counterparty Credit Risk. Credit risk includes the possibility that a party to a transaction involving the Fund will fail to meet its obligations. This could cause the Fund to lose money or to lose the benefit of

the transaction or prevent the Fund from selling or buying other securities to implement its investment strategy.

|

| ■

| Risk Related to the Economy. The value of the Fund's portfolio may decline in tandem with a drop in the overall value of the markets in which the Fund invests and/or other markets. Economic, political and financial

conditions, or industry or economic trends and developments, may, from time to time, and for varying periods of time, cause the Fund to experience volatility, illiquidity, shareholder redemptions, or other potentially

adverse effects. Among other investments, lower-grade bonds and loans may be particularly sensitive to changes in the economy.

|

| ■

| Liquidity Risk. Liquidity of individual corporate bonds varies considerably. Low-grade corporate bonds have less liquidity than investment-grade securities, which means that it may be more difficult to

sell or buy a security at a favorable price or time.

|

| ■

| Interest Rate Risk. Prices of fixed-income securities generally fall when interest rates rise. The longer the duration of a fixed-income security, the more susceptible it is to interest-rate risk. Recent and

potential future changes in monetary policy made by central banks and/or their governments are likely to affect the level of interest rates.

|

| ■

| Risk of Foreign Investing. Because the Fund invests in securities issued by foreign companies and national governments, the Fund's Share price may be more affected by foreign economic and political conditions,

taxation policies and accounting and auditing standards than could otherwise be the case.

|

| ■

| Currency Risk. Exchange rates for currencies fluctuate daily. The value of the Fund's foreign investments and the value of the shares may be affected favorably or unfavorably by changes in currency

exchange rates relative to the U.S. dollar.

|

| ■

| Eurozone Related Risk. A number of countries in the European Union (EU) have experienced, and may continue to experience, severe economic and financial difficulties. Additional EU member countries may also fall

subject to such difficulties. These events could negatively affect the value and liquidity of the Fund's investments in euro-denominated securities and derivatives contracts, securities of issuers located in the EU or

with significant exposure to EU issuers or countries.

|

| ■

| Leverage Risk. Leverage risk is created when an investment exposes the Fund to a level of risk that exceeds the amount invested.

|

| ■

| Risk of Investing in Emerging Market Countries. Securities issued or traded in emerging markets generally entail greater risks than securities issued or traded in developed markets.

|

| ■

| Risk of Investing in Derivative Contracts and Hybrid Instruments. Derivative contracts and hybrid instruments involve risks different from, or possibly greater than, risks associated with investing directly in securities and other traditional

investments. Specific risk issues related to the use of such contracts and instruments include valuation and tax issues, increased potential for losses and/or costs to the Fund, and a potential reduction in gains to

the Fund. Each of these issues is described in greater detail in this prospectus.

|

| ■

| Risk of Loss after Redemption. The Fund may also invest in trade finance loan instruments primarily by investing in other investment companies (which are not available for general investment by the public) that own those

instruments, is advised by an affiliate of the Adviser and is structured as an extended payment fund.

|

| ■

| Technology Risk. The Adviser uses various technologies in managing the Fund, consistent with its investment objective and strategy described in this Prospectus. For example, proprietary and third party data

and systems are utilized to support decision making for the Fund. Data imprecision, software or other technology malfunctions, programming inaccuracies and similar circumstances may impair the performance of these

systems, which may negatively affect Fund performance.

|

The

Shares offered by this Prospectus are not deposits or obligations of any bank, are not endorsed or guaranteed by any bank and are not insured or guaranteed by the U.S. government, the Federal Deposit Insurance

Corporation, the Federal Reserve Board or any other government agency.

Performance: Bar Chart and

Table

Risk/Return Bar Chart

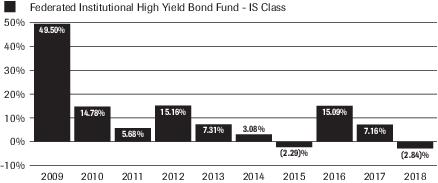

The bar

chart and performance table below reflects historical performance data for the Fund and are intended to help you analyze the Fund's investment risks in light of its historical returns. The bar chart shows the

variability of the Fund's IS class total returns on a calendar year-by-year basis. The Average Annual Total Return Table shows returns averaged over the stated periods, and includes comparative performance information. The Fund's performance will fluctuate, and past performance (before and after taxes) is not necessarily an indication of future results. Updated performance information for the Fund

is available under the “Products” section at FederatedInvestors.com or by calling 1-800-341-7400.

The Fund's IS

class total return for the nine-month period from January 1, 2019 to September 30, 2019, was 11.86%.

Within the periods shown in the

bar chart, the Fund's IS class highest quarterly return was 18.11% (quarter ended June 30, 2009). Its lowest quarterly return was (4.97)% (quarter ended September 30, 2011).

Average Annual Total Return

Table

The

Fund's R6 class commenced operations on June 29, 2016. For the periods prior to the commencement of operations of the Fund's R6 class, the performance information shown below is for the Fund's IS class. The

performance of the IS class has not been adjusted to reflect the expenses applicable to the R6 class since the R6 class has a lower expense ratio than the expense ratio of the IS class. The performance of the IS class

has been adjusted to remove any voluntary waiver of Fund expenses related to the IS class that may have occurred during the periods prior to the commencement of operations of the R6 class, which would have caused the

IS class expenses to be lower than the gross expenses of the R6 class. The Fund's R6 class would have annual returns substantially similar to those of the IS class because the shares are invested in the same portfolio

of securities and the annual returns would differ only to the extent that the classes do not have the same expenses. In addition to Return Before Taxes, Return After Taxes is shown for the Fund's IS class to

illustrate the effect of federal taxes on Fund returns. After-tax returns are shown only for the IS class, and after-tax returns for the R6 class will differ from those shown for the IS class. Actual after-tax returns depend on each investor's personal tax situation, and are likely to differ from those shown. After-tax returns are calculated using a standard set of

assumptions. The stated returns assume the highest historical federal income and capital gains tax rates. These after-tax returns do not reflect the effect of any applicable state and local taxes. After-tax returns are not relevant to investors holding Shares through a 401(k) plan, an Individual Retirement Account or other tax-advantaged investment plan.

(For the

Period Ended December 31, 2018)

|

| 1 Year

| 5 Years

| 10 Years

|

| IS:

|

|

|

|

| Return Before Taxes

| (2.84)%

| 3.83%

| 10.46%

|

| Return After Taxes on Distributions

| (5.14)%

| 1.24%

| 7.41%

|

| Return After Taxes on Distributions and Sale of Fund Shares

| (1.64)%

| 1.76%

| 7.08%

|

| R6:

|

|

|

|

| Return Before Taxes

| (2.82)%

| 3.83%

| 10.41%

|

Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index1

(reflects no deduction for fees, expenses or taxes)

| (2.08)%

| 3.84%

| 11.14%

|

| Lipper High Yield Funds Average2

| (2.99)%

| 2.73%

| 9.19%

|

| 1

| The Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index is an issuer-constrained version of the Bloomberg Barclays U.S. Corporate High-Yield Index that measures the

market of USD-denominated, noninvestment-grade, fixed-rate, taxable corporate bonds. The index follows the same rules as the uncapped index but limits the exposure of each issuer to 2% of the total market value and

redistributes any excess market value index-wide on a pro-rata basis.

|

| 2

| Lipper figures represent the average of the total returns reported by all mutual funds designated by Lipper, Inc., as falling into the respective category and is

not adjusted to reflect any sales charges.

|

FUND MANAGEMENT

The

Fund's Investment Adviser is Federated Investment Management Company.

Mark E.

Durbiano, CFA, Senior Portfolio Manager, has been the Fund's portfolio manager since its inception November of 2002.

Steven

J. Wagner, Senior Portfolio Manager, has been the Fund's portfolio manager since December of 2017.

purchase and sale of fund

shares

You may

purchase, redeem or exchange Shares of the Fund on any day the New York Stock Exchange is open. Shares may be purchased through a financial intermediary firm that has entered into a Fund selling and/or servicing

agreement with the Distributor or an affiliate (“Financial Intermediary”) or directly from the Fund, by wire or by check. Please note that certain purchase restrictions may apply. Redeem or exchange Shares

through a financial intermediary or directly from the Fund by telephone at 1-800-341-7400 or by mail.

IS Class

The

minimum initial investment amount for the Fund's Institutional Shares is generally $1,000,000 and there is no minimum subsequent investment amount. Certain types of accounts are eligible for lower minimum investments.

The minimum investment amount for Systematic Investment Programs is $50.

R6 Class

There

are no minimum initial or subsequent investment amounts required. The minimum investment amount for Systematic Investment Programs is $50.

Tax Information

IS Class

The

Fund's distributions are taxable as ordinary income or capital gains except when your investment is through a 401(k) plan, an Individual Retirement Account or other tax-advantaged investment plan.

R6 Class

The

Fund's distributions are taxable as ordinary income or capital gains except when your investment is through a tax-advantaged investment plan.

Payments to Broker-Dealers and

Other Financial Intermediaries

IS Class

If you

purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and/or its related companies may pay the intermediary for the sale of Fund Shares and related services. These

payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial

intermediary's website for more information.

Payments to Broker-Dealers and

Other Financial Intermediaries

R6 Class

Class

R6 Shares do not make any payments to financial intermediaries, either from Fund assets or from the investment adviser and its affiliates.

What are the Fund's

Investment Strategies?

The

Fund's investment objective is to seek high current income. While there is no assurance that the Fund will achieve its investment objective, it endeavors to do so by following the strategies and policies described in

this Prospectus.

The

Fund provides exposure to the high-yield corporate bond market. The Fund's investment adviser (the “Adviser”) actively manages the Fund's portfolio seeking to realize the potentially higher returns of

high-yield bonds (also known as “junk bonds”), compared to returns of high-grade securities by seeking to minimize default risk and other risks through careful security selection and diversification. The

Fund primarily invests in domestic high-yield bonds but may invest a portion of its portfolio in securities of issuers based outside of the United States (including emerging markets). A description of the various

types of securities in which the Fund invests, and their risks, immediately follows the strategy discussion.

The Adviser selects securities that it believes have attractive risk-return characteristics. The securities in which the Fund invests have high yields primarily because of the market's greater

uncertainty about the issuer's ability to make all required interest and principal payments, and therefore about the returns that will in fact be realized by the Fund.

The

Adviser attempts to select bonds for investment by the Fund which offer high potential returns for the default risks being assumed. The Adviser's securities selection process consists of a credit-intensive,

fundamental analysis of the issuing firm. The Adviser's analysis focuses on the financial condition of the issuing firm together with the issuer's business and product strength, competitive position and management

expertise. Further, the Adviser considers current economic, financial market and industry factors, which may affect the issuer.

The

Adviser attempts to minimize the Fund's portfolio credit risk through diversification. The Adviser selects securities to maintain broad portfolio diversification both by company and industry. The Adviser does not

target an average maturity for the Fund's portfolio.

The

Fund may use derivative contracts and/or hybrid instruments to implement elements of its investment strategy. For example, the Fund may use derivative contracts or hybrid instruments to increase or decrease the

portfolio's exposure to the investment(s) underlying the derivative or hybrid instrument in an attempt to benefit from changes in the value of the underlying investment(s). Additionally, by way of example, the Fund

may use derivative contracts in an attempt to:

| ■

| increase or decrease the effective duration of the Fund portfolio;

|

| ■

| obtain premiums from the sale of derivative contracts;

|

| ■

| realize gains from trading a derivative contract; or

|

| ■

| hedge against potential losses.

|

There

can be no assurance that the Fund's use of derivative contracts or hybrid instruments will work as intended. Derivative investments made by the Fund are included within the Fund's 80% policy (as described below) and

are calculated at market value.

The

Fund will invest its assets so that at least 80% of its net assets (plus any borrowings for investment purposes) are invested in investments rated below investment-grade. The Fund will notify shareholders in advance

of any change in its investment policy that would enable the Fund to invest, under normal circumstances, less than 80% of its net assets in investments rated below investment-grade.

TEMPORARY INVESTMENTS

The

Fund may temporarily depart from its principal investment strategies by investing its assets in shorter-term debt securities and similar obligations or holding cash. It may do this in response to unusual

circumstances, such as: adverse market, economic or other conditions (for example, to help avoid potential losses, or during periods when there is a shortage of appropriate securities); to maintain liquidity to meet

shareholder redemptions; or to accommodate cash inflows. It is possible that such investments could affect the Fund's investment returns and/or the ability to achieve the Fund's investment objectives.

What are the Fund's

Principal Investments?

The

following provides general information on the Fund's principal investments. The Fund's Statement of Additional Information (SAI) provides information about the Fund's non-principal investments and may provide

additional information about the Fund's principal investments.

Fixed-Income Securities

Fixed-income securities pay interest, dividends or distributions at a specified rate. The rate may be a fixed percentage of the principal or may be adjusted periodically. In addition, the issuer of a fixed-income

security must repay the principal amount of the security, normally within a specified time. Fixed-income securities provide more regular income than equity securities. However, the returns on fixed-income securities

are limited and normally do not increase with the issuer's earnings. This limits the potential appreciation of fixed-income securities as compared to equity securities.

A

security's yield measures the annual income earned on a security as a percentage of its price. A security's yield will increase or decrease depending upon whether it costs less (a “discount”) or more (a

“premium”) than the principal amount. If the issuer may redeem the security before its scheduled maturity, the price and yield on a discount or premium security may change based upon the probability of an

early redemption. Securities with higher risks generally have higher yields.

The

following describes the fixed-income securities in which the Fund principally invests:

Preferred Stocks

Preferred stocks have the right to receive specified dividends or distributions before the issuer makes payments on its common stock. Some preferred stocks also participate in dividends and distributions paid on

common stock. Preferred stocks may also permit the issuer to redeem the stock. The Fund may also treat such redeemable preferred stock as a fixed-income security.

Corporate Debt Securities (A Type

of Fixed-Income Security)

Corporate debt securities are fixed-income securities issued by businesses. Notes, bonds, debentures and commercial paper are the most prevalent types of corporate debt securities. The Fund may also purchase

interests in bank loans to companies. The credit risks of corporate debt securities vary widely among issuers.

In

addition, the credit risk of an issuer's debt security may vary based on its priority for repayment. For example, higher ranking (“senior”) debt securities have a higher priority than lower ranking

(“subordinated”) securities. This means that the issuer might not make payments on subordinated securities while continuing to make payments on senior securities. In addition, in the event of bankruptcy,

holders of senior securities may receive amounts otherwise payable to the holders of subordinated securities. Some subordinated securities, such as trust-preferred and capital-securities notes, also permit the issuer

to defer payments under certain circumstances. For example, insurance companies issue securities known as surplus notes that permit the insurance company to defer any payment that would reduce its capital below

regulatory requirements.

Lower-Rated, Fixed-Income

Securities

Lower-rated, fixed-income securities are securities rated below investment grade (i.e., BB or lower) by a nationally recognized statistical rating organization (NRSRO). There is no minimal acceptable rating for a

security to be purchased or held by the Fund and the Fund may purchase or hold unrated securities and securities whose issuers are in default.

Zero-Coupon Securities (A Type of

Fixed-Income Security)

Zero-coupon securities do not pay interest or principal until final maturity unlike debt securities that provide periodic payments of interest (referred to as a coupon payment). Investors buy zero-coupon securities

at a price below the amount payable at maturity. The difference between the purchase price and the amount paid at maturity represents interest on the zero-coupon security. Investors must wait until maturity to receive

interest and principal, which increases the interest rate and credit risks of a zero-coupon security.

There

are many forms of zero-coupon securities. Some are issued at a discount and are referred to as zero coupon or capital appreciation bonds. Others are created from interest-bearing bonds by separating the right to

receive the bond's coupon payments from the right to receive the bond's principal due at maturity, a process known as coupon stripping. In addition, some securities give the issuer the option to deliver additional

securities in place of cash interest payments, thereby increasing the amount payable at maturity. These are referred to as pay-in-kind, PIK securities or toggle securities.

Demand Instruments (A Type of

Corporate Debt Security)

Demand

instruments are corporate debt securities that require the issuer or a third party, such as a dealer or bank (the “Demand Provider”), to repurchase the security for its face value upon demand. Some demand

instruments are “conditional,” so that the occurrence of certain conditions relieves the Demand Provider of its obligation to repurchase the security. Other demand instruments are

“unconditional,” so that there are no conditions under which the Demand Provider's obligation to repurchase the security can terminate. The Fund treats demand instruments as short-term securities, even

though their stated maturity may extend beyond one year.

Convertible Securities (A

Fixed-Income Security)

Convertible securities are fixed-income securities that the Fund has the option to exchange for equity securities at a specified conversion price. The option allows the Fund to realize additional returns if the

market price of the equity securities exceeds the conversion price. For example, the Fund may hold fixed-income securities that are convertible into shares of common stock at a conversion price of $10 per share. If

the market value of the shares of common stock reached $12, the Fund could realize an additional $2 per share by converting its fixed-income securities.

Convertible securities have lower yields than comparable fixed-income securities. In addition, at the time a convertible security is issued, the conversion price exceeds the market value of the underlying equity

securities. Thus, convertible securities may provide lower returns than non-convertible, fixed-income securities or equity securities depending upon changes in the price of the underlying equity securities. However,

convertible securities permit the Fund to realize some of the potential appreciation of the underlying equity securities with less risk of losing its initial investment.

To the

extent the Fund invests in convertible securities, it typically invests in securities that can be exchanged for instruments that are publically traded or listed on a centralized market or stock exchange. The Fund may

receive securities not publically traded or listed on a centralized market or stock exchange in connection with bankruptcies, restructurings, or other unusual circumstances.

The

Fund treats convertible securities as fixed-income securities for purposes of its investment policies and limitations, because of their unique characteristics.

FOREIGN SECURITIES

Foreign

securities are securities of issuers based outside the United States. To the extent a Fund invests in securities included in its applicable broad-based securities market index, the Fund may consider an issuer to be

based outside the United States if the applicable index classifies the issuer as based outside the United States. Accordingly, the Fund may consider an issuer to be based outside the United States if the issuer

satisfies at least one, but not necessarily all, of the following:

| ■

| it is organized under the laws of, or has its principal office located in, another country;

|

| ■

| the principal trading market for its securities is in another country;

|

| ■

| it (directly or through its consolidated subsidiaries) derived in its most current fiscal year at least 50% of its total assets, capitalization, gross revenue or profit from goods produced, services

performed or sales made in another country; or

|

| ■

| it is classified by an applicable index as based outside the United States.

|

While

the Fund typically invests in U.S. dollar denominated foreign securities, the Fund may also invest in foreign securities that are denominated in foreign currencies Along with the risks normally associated with

domestic securities of the same type, foreign securities are subject to currency risks and risks of foreign investing. Trading in certain foreign markets is also subject to liquidity risks.

Foreign Exchange Contracts

In

order to convert U.S. dollars into the currency needed to buy a foreign security, or to convert foreign currency received from the sale of a foreign security into U.S. dollars, or to decrease or eliminate the Fund's

exposure to foreign currencies in which a portfolio security is denominated, the Fund may enter into spot currency trades. In a spot trade, the Fund agrees to exchange one currency for another at the current

exchange rate. The Fund may also enter into derivative contracts in which a foreign currency is an underlying asset. The exchange rate for currency derivative contracts may be higher or lower than the spot exchange

rate. Use of these derivative contracts may increase or decrease the Fund's exposure to currency risks.

Derivative Contracts

Derivative contracts are financial instruments that require payments based upon changes in the values of designated securities, commodities, currencies, indices, or other assets or instruments including other

derivative contracts, (each a “Reference Instrument” and collectively, “Reference Instruments”). Each party to a derivative contract may sometimes be referred to as a counterparty. Some

derivative contracts require payments relating to an actual, future trade involving the Reference Instrument. These types of derivatives are frequently referred to as “physically settled” derivatives.

Other derivative contracts require payments relating to the income or returns from, or changes in the market value of, a Reference Instrument. These types of derivatives are known as “cash-settled”

derivatives, since they require cash payments in lieu of delivery of the Reference Instrument.

Many

derivative contracts are traded on securities or commodities exchanges. In this case, the exchange sets all the terms of the contract except for the price. Investors make payments due under their contracts through the

exchange. Most exchanges require investors to maintain margin accounts through their brokers to cover their potential obligations to the exchange. Parties to the contract make (or collect) daily payments to the margin

accounts to reflect losses (or gains) in the value of their contracts. This protects investors against potential defaults by the other party to the contract. Trading contracts on an exchange also allows investors to

close out their contracts by entering into offsetting contracts.

The

Fund may also trade derivative contracts over-the-counter (OTC) in transactions negotiated directly between the Fund and a financial institution. OTC contracts do not necessarily have standard terms, so they may be

less liquid and more difficult to close out than exchange-traded contracts. In addition, OTC contracts with more specialized terms may be more difficult to value than exchange-traded contracts, especially in times of

financial stress.

The

market for swaps and other OTC derivatives was largely unregulated prior to the enactment of federal legislation known as the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank

Act”). Regulations enacted by the Commodity Futures Trading Commission (the CFTC) under the Dodd-Frank Act require the Fund to clear certain swap contracts through a clearing house or central counterparty (a

CCP).

To

clear a swap through the CCP, the Fund will submit the contract to, and post margin with, a futures commission merchant (FCM) that is a clearing house member. The Fund may enter into the swap with a financial

institution other than the FCM and arrange for the contract to be transferred to the FCM for clearing, or enter into the contract with the FCM itself. If the Fund must centrally clear a transaction, the CFTC's

regulations also generally require that the swap be executed on a registered exchange or through a market facility that is known as a swap execution facility or SEF. Central clearing is presently required only for

certain swaps; the CFTC is expected to impose a mandatory central clearing requirement for additional derivative instruments over time.

The

CCP, SEF and FCM are all subject to regulatory oversight by the CFTC. In addition, most derivative market participants are now regulated as swap dealers or major swap participants and are subject to certain minimum

capital and margin requirements and business conduct standards. Similar regulatory requirements are expected to apply to derivative contracts that are subject to the jurisdiction of the SEC, although the SEC has not

yet finalized its regulations. In addition, uncleared OTC swaps will be subject to regulatory collateral requirements that could adversely affect the Fund's ability to enter into swaps in the OTC market. These

developments could cause the Fund to terminate new or existing swap agreements or to realize amounts to be received under such instruments at an inopportune time.

Until

the mandated rulemaking and regulations are implemented completely, it will not be possible to determine the complete impact of the Dodd-Frank Act and related regulations on the Fund.

Depending on how the Fund uses derivative contracts and the relationships between the market value of a derivative contract and the Reference Instrument, derivative contracts may increase or decrease the Fund's

exposure to the risks of the Reference Instrument, and may also expose the Fund to liquidity and leverage risks. OTC contracts also expose the Fund to credit risks in the event that a counterparty defaults on the

contract, although this risk may be mitigated by submitting the contract for clearing through a CCP.

Payment

obligations arising in connection with derivative contracts are frequently required to be secured with margin (which is commonly called “collateral”). To the extent necessary to meet such requirements, the

Fund may purchase U.S. Treasury and/or government agency securities.

The

Fund may invest in a derivative contract if it is permitted to own, invest in, or otherwise have economic exposure to the Reference Instrument. The Fund is not required to own a Reference Instrument in order to buy or

sell a derivative contract relating to that Reference Instrument. The Fund may trade in the following specific types and/or combinations of derivative contracts:

Futures Contracts (A Type of

Derivative)

Futures

contracts provide for the future sale by one party and purchase by another party of a specified amount of a Reference Instrument at a specified price, date and time. Entering into a contract to buy a Reference

Instrument is commonly referred to as buying a contract or holding a long position in the asset. Entering into a contract to sell a Reference Instrument is commonly referred to as selling a contract or holding a short

position in the Reference Instrument. Futures contracts are considered to be commodity contracts. The Adviser has claimed an exclusion from the definition of the term “commodity pool operator” under the

Commodity Exchange Act with respect to the Fund and, therefore, is not subject to registration or regulation with respect to the Fund. Futures contracts traded OTC are frequently referred to as forward contracts. The

Fund can buy or sell financial futures (such as interest rate futures, index futures and security futures), as well as, currency futures and currency forward contracts.

Option Contracts (A Type of

Derivative)

Option

contracts (also called “options”) are rights to buy or sell a Reference Instrument for a specified price (the “exercise price”) during, or at the end of, a specified period. The seller (or

“writer”) of the option receives a payment, or premium, from the buyer, which the writer keeps regardless of whether the buyer uses (or exercises) the option. A call option gives the holder (buyer) the

right to buy the Reference Instrument from the seller (writer) of the option. A put option gives the holder the right to sell the Reference Instrument to the writer of the option. Options may be bought or sold on a

wide variety of Reference Instruments. Options that are written on futures contracts will be subject to margin requirements similar to those applied to futures contracts.

Swap Contracts (A Type of

Derivative)

A swap

contract (also known as a “swap”) is a type of derivative contract in which two parties agree to pay each other (swap) the returns derived from Reference Instruments. Swaps do not always involve the

delivery of the Reference Instruments by either party, and the parties might not own the Reference Instruments underlying the swap. The payments are usually made on a net basis so that, on any given day, the Fund

would receive (or pay) only the amount by which its payment under the contract is less than (or exceeds) the amount of the other party's payment. Swap agreements are sophisticated instruments that can take many

different forms and are known by a variety of names. Common types of swaps in which the Fund may invest include interest rate swaps, caps and floors, total return swaps, credit default swaps and currency swaps.

OTHER INVESTMENTS, TRANSACTIONS,

TECHNIQUES

Hybrid Instruments

Hybrid

instruments combine elements of two different kinds of securities or financial instruments (such as a derivative contract). Frequently, the value of a hybrid instrument is determined by reference to changes in the

value of a Reference Instrument (that is a designated security, commodity, currency, index or other asset or instrument including a derivative contract). The Fund may use hybrid instruments only in connection with

permissible investment activities. Hybrid instruments can take on many forms including, but not limited to, the following forms. First, a common form of a hybrid instrument combines elements of a derivative contract

with those of another security (typically a fixed-income security). In this case all or a portion of the interest or principal payable on a hybrid security is determined by reference to changes in the price of a

Reference Instrument. Second, hybrid instruments may include convertible securities with conversion terms related to a Reference Instrument.

Depending on the type and terms of the hybrid instrument, its risks may reflect a combination of the risks of investing in the Reference Instrument with the risks of investing in other securities, currencies and

derivative contracts. Thus, an investment in a hybrid instrument may entail significant risks in addition to those associated with traditional securities or the Reference Instrument. Hybrid instruments are also

potentially more volatile than traditional securities or the Reference Instrument. Moreover, depending on the structure of the particular hybrid, it may expose the Fund to leverage risks or carry liquidity risks.

Asset Segregation

In order to cover its obligations in connection with derivative contracts or special transactions, the Fund will either own the underlying assets, enter into offsetting transactions or set aside

cash or readily marketable securities in each case, as provided by the SEC or SEC staff guidance. This requirement may cause the Fund to miss favorable trading opportunities, due to a lack of sufficient cash or

readily marketable securities. This requirement may also cause the Fund to realize losses on offsetting or terminated derivative contracts or special transactions.

Investing in Securities of Other

Investment Companies

The

Fund may invest its assets in securities of other investment companies, including the securities of affiliated money market funds, as an efficient means of implementing its investment strategies and/or managing its

uninvested cash. The Fund may also invest in high yield and loan instruments, including trade finance loan instruments, primarily by investing in another investment company (which is not available for general

investment by the public) that owns those securities and that is advised by an affiliate of the Adviser. The Fund's investment in the trade finance instruments through these other investment vehicles may expose the

Fund to risks of loss after redemption. The Fund may also invest in such securities directly. These other investment companies are managed independently of the Fund and incur additional fees and/or expenses which

would, therefore, be borne indirectly by the Fund in connection with any such investment. However, the Adviser believes that the benefits and efficiencies of this approach should outweigh the potential additional fees

and/or expenses.

What are the Specific

Risks of Investing in the Fund?

The

following provides general information on the risks associated with the Fund's principal investments. Any additional risks associated with the Fund's non-principal investments are described in the Fund's SAI. The

Fund's SAI also may provide additional information about the risks associated with the Fund's principal investments.

Risk Associated with

Noninvestment-Grade Securities

Securities rated below investment grade, also known as junk bonds, generally entail greater economic, credit and liquidity risks than investment-grade securities. For example, their prices are more volatile,

economic downturns and financial setbacks may affect their prices more negatively, and their trading market may be more limited. These securities are considered speculative with respect to the issuer's ability to pay

interest and repay principal.

ISSUER Credit Risk

It is

possible that interest or principal on securities will not be paid when due. Noninvestment-grade securities generally have a higher default risk than investment-grade securities. Such non-payment or default may reduce

the value of the Fund's portfolio holdings, its share price and its performance.

Many

fixed-income securities receive credit ratings from nationally recognized statistical rating organizations (NRSROs) such as Fitch Rating Service, Moody's Investor Services, Inc. and Standard & Poor's that assign

ratings to securities by assessing the likelihood of an issuer and/or guarantor default. Higher credit ratings correspond to lower perceived credit risk and lower credit ratings correspond to higher perceived credit

risk. Credit ratings may be upgraded or downgraded from time to time as an NRSRO's assessment of the financial condition of a party obligated to make payments with respect to such securities and credit risk changes.

The impact of any credit rating downgrade can be uncertain. Credit rating downgrades may lead to increased interest rates and volatility in financial markets, which in turn could negatively affect the value of the

Fund's portfolio holdings, its share price and its investment performance. Credit ratings are not a guarantee of quality. Credit ratings may lag behind the current financial conditions of the issuer and/or guarantor

and do not provide assurance against default or other loss of money. Credit ratings do not protect against a decline in the value of a security. If a security has not received a rating, the Fund must rely entirely

upon the Adviser's credit assessment.

Fixed-income securities generally compensate for greater credit risk by paying interest at a higher rate. The difference between the yield of a security and the yield of a U.S. Treasury security or other appropriate

benchmark with a comparable maturity (the “spread”) measures the additional interest paid for risk. Spreads may increase generally in response to adverse economic or market conditions. A security's spread

may also increase if the security's rating is lowered, or the security is perceived to have an increased credit risk. An increase in the spread will cause the price of the security to decline if interest rates remain

unchanged.

Counterparty Credit Risk

Credit

risk includes the possibility that a party to a transaction involving the Fund will fail to meet its obligations. This could cause the Fund to lose money or to lose the benefit of the transaction or prevent the Fund

from selling or buying other securities to implement its investment strategy.

RISK RELATED TO THE ECONOMY

The

value of the Fund's portfolio may decline in tandem with a drop in the overall value of the markets in which the Fund invests and/or other markets based on negative developments in the U.S. and global economies.

Economic, political and financial conditions, or industry or economic trends and developments, may, from time to time, and for varying periods of time, cause volatility, illiquidity or other potentially adverse

effects in the financial markets, including the fixed-income market. The commencement, continuation or ending of government policies and economic stimulus programs, changes in monetary policy, increases or decreases

in interest rates, or other factors or events that affect the financial markets, including the fixed-income markets, may contribute to the development of or increase in volatility, illiquidity, shareholder redemptions

and other adverse effects, which could negatively impact the Fund's performance. For example, the value of certain portfolio securities may rise or fall in response to changes in interest rates, which could result

from a change in government policies, and has the potential to cause investors to move out of certain portfolio securities, including fixed-income securities, on a large scale. This may increase redemptions from funds

that hold large amounts of certain securities and may result in decreased liquidity and increased volatility in the financial markets. Market factors, such as the demand for particular portfolio securities, may cause

the price of certain portfolio securities to fall while the prices of other securities rise or remain unchanged. Among other investments, lower-grade bonds and loans may be particularly sensitive to changes in the

economy.

LIQUIDITY RISK

Trading

opportunities are more limited for fixed-income securities that have not received any credit ratings, have received any credit ratings below investment grade or are not widely held. These features may make it more

difficult to sell or buy a security at a favorable price or time. Consequently, the Fund may have to accept a lower price to sell a security, sell other securities to raise cash or give up an investment opportunity,

any of which could have a negative effect on the Fund's performance. Infrequent trading of securities may also lead to an increase in their price volatility.

Liquidity risk also refers to the possibility that the Fund may not be able to sell a security or close out a derivative contract when it wants to. If this happens, the Fund will be required to continue to hold the

security or keep the position open, and the Fund could incur losses.

OTC

derivative contracts generally carry greater liquidity risk than exchange-traded contracts. This risk may be increased in times of financial stress, if the trading market for OTC derivative contracts becomes

restricted.

Interest Rate Risk

Prices

of fixed-income securities rise and fall in response to changes in interest rates. Generally, when interest rates rise, prices of fixed-income securities fall. However, market factors, such as the demand for

particular fixed-income securities, may cause the price of certain fixed-income securities to fall while the prices of other securities rise or remain unchanged.

The

longer the duration of a fixed-income security, the more susceptible it is to interest rate risk. The duration of a fixed-income security may be equal to or shorter than the stated maturity of a fixed-income security.

Recent and potential futures changes in monetary policy made by central banks and/or their governments are likely to affect the level of interest rates. Duration measures the price sensitivity of a fixed-income

security given a change in interest rates. For example, if a fixed-income security has an effective duration of three years, a 1% increase in general interest rates would be expected to cause the security's value to

decline about 3% while a 1% decrease in general interest rates would be expected to cause the security's value to increase about 3%.

Risk of Foreign Investing

Foreign

securities pose additional risks because foreign economic or political conditions may be less favorable than those of the United States. Securities in foreign markets may also be subject to taxation policies that

reduce returns for U.S. investors.

Foreign

companies may not provide information (including financial statements) as frequently or to as great an extent as companies in the United States. Foreign companies may also receive less coverage than U.S. companies by

market analysts and the financial press. In addition, foreign countries may lack uniform accounting, auditing and financial reporting standards or regulatory requirements comparable to those applicable to U.S.

companies. These factors may prevent the Fund and its Adviser from obtaining information concerning foreign companies that is as frequent, extensive and reliable as the information available concerning companies in

the United States.

Foreign

countries may have restrictions on foreign ownership of securities or may impose exchange controls, capital flow restrictions or repatriation restrictions which could adversely affect the liquidity of the Fund's

investments.

Since

many loan instruments involve parties (for example, lenders, borrowers and agent banks) located in multiple jurisdictions outside of the United States, there is a risk that a security interest in any related

collateral may be unenforceable and obligations under the related loan agreements may not be binding.

Currency Risk

Exchange rates for currencies fluctuate daily. The combination of currency risk and market risks tends to make securities traded in foreign markets more volatile than securities traded exclusively in the United

States. The Adviser attempts to manage currency risk by limiting the amount the Fund invests in securities denominated in a particular currency. However, diversification will not protect the Fund against a general

increase in the value of the U.S. dollar relative to other currencies.

Investing in currencies or securities denominated in a foreign currency, entails risk of being exposed to a currency that may not fully reflect the strengths and weaknesses of the economy of the country or region

utilizing the currency. Currency risk includes both the risk that currencies in which the Fund's investments are traded, or currencies in which the Fund has taken an active investment position, will decline in value

relative to the U.S. dollar and, in the case of hedging positions, that the U.S. dollar will decline in value relative to the currency being hedged. In addition, it is possible that a currency (such as, for example,

the euro) could be abandoned in the future by countries that have already adopted its use, and the effects of such an abandonment on the applicable country and the rest of the countries utilizing the currency are

uncertain but could negatively affect the Fund's investments denominated in the currency. If a currency used by a country or countries is replaced by another currency, the Fund's Adviser would evaluate whether to

continue to hold any investments denominated in such currency, or whether to purchase investments denominated in the currency that replaces such currency, at the time. Such investments may continue to be held, or

purchased, to the extent consistent with the Fund's investment objective(s) and permitted under applicable law.

Many countries rely heavily upon export-dependent businesses and any strength in the exchange rate between a currency and the U.S. dollar or other currencies can have either a positive or a

negative effect upon corporate profits and the performance of investments in the country or region utilizing the currency. Adverse economic events within such country or region may increase the volatility of exchange

rates against other currencies, subjecting the Fund's investments denominated in such country's or region's currency to additional risks. In addition, certain countries, particularly emerging market countries, may

impose foreign currency exchange controls or other restrictions on the transferability, repatriation or convertibility of currency.

eurozone Related risk

A

number of countries in the European Union (EU) have experienced, and may continue to experience, severe economic and financial difficulties. Additional EU member countries may also fall subject to such difficulties.

These events could negatively affect the value and liquidity of the Fund's investments in euro-denominated securities and derivatives contracts, securities of issuers located in the EU or with significant exposure to

EU issuers or countries. If the euro is dissolved entirely, the legal and contractual consequences for holders of euro-denominated obligations and derivative contracts would be determined by laws in effect at such

time. Such investments may continue to be held, or purchased, to the extent consistent with the Fund's investment objective(s) and permitted under applicable law. These potential developments, or market perceptions

concerning these and related issues, could adversely affect the value of the Shares.

Certain

countries in the EU have had to accept assistance from supra-governmental agencies such as the International Monetary Fund, the European Stability Mechanism (the ESM) or other supra-governmental agencies. The European

Central Bank has also been intervening to purchase Eurozone debt in an attempt to stabilize markets and reduce borrowing costs. There can be no assurance that these agencies will continue to intervene or provide

further assistance and markets may react adversely to any expected reduction in the financial support provided by these agencies. Responses to the financial problems by European governments, central banks and others

including austerity measures and reforms, may not work, may result in social unrest and may limit future growth and economic recovery or have other unintended consequences.

In

addition, one or more countries may abandon the euro and/or withdraw from the EU. The impact of these actions, especially if they occur in a disorderly fashion, could be significant and far-reaching. In June 2016, the

United Kingdom (U.K.) approved a referendum to leave the EU, commonly referred to as “Brexit,” which sparked depreciation in the value of the British pound, short-term declines in global stock markets and

heightened risk of continued worldwide economic volatility. As a result of Brexit, there is considerable uncertainty as to the arrangements that will apply to the U.K.'s relationship with the EU and other countries

leading up to, and following, its withdrawal. This long-term uncertainty may affect other countries in the EU and elsewhere. Further, the U.K.'s departure from the EU may cause volatility within the EU, triggering

prolonged economic downturns in certain European countries or sparking additional member states to contemplate departing the EU. In addition, Brexit can create actual or perceived additional economic stresses for the

U.K., including potential for decreased trade, capital outflows, devaluation of the British pound, wider corporate bond spreads due to uncertainty and possible declines in business and consumer spending as well as

foreign direct investment.

Leverage Risk

Leverage risk is created when an investment, which includes, for example, an investment in a derivative contract, exposes the Fund to a level of risk that exceeds the amount invested. Changes in the value of such an

investment magnify the Fund's risk of loss and potential for gain. Investments can have these same results if their returns are based on a multiple of a specified index, security or other benchmark.

Risk of Investing in Emerging

Market Countries

Securities issued or traded in emerging markets generally entail greater risks than securities issued or traded in developed countries. For example, their prices may be significantly more volatile than prices in

developed countries. Emerging market economies may also experience more severe down-turns (with corresponding currency devaluations) than developed economies.

Emerging market countries may have relatively unstable governments and may present the risk of nationalization of businesses, expropriation, confiscatory taxation or, in certain instances, reversion to closed

market, centrally planned economies.

Risk of Investing in Derivative

Contracts and Hybrid Instruments

The

Fund's exposure to derivative contracts and hybrid instruments (either directly or through its investment in another investment company) involves risks different from, or possibly greater than, the risks associated

with investing directly in securities and other traditional investments. First, changes in the value of the derivative contracts and hybrid instruments in which the Fund invests may not be correlated with changes in

the value of the underlying Reference Instruments or, if they are correlated, may move in the opposite direction than originally anticipated. Second, while some strategies involving

derivatives may reduce the risk of loss,

they may also reduce potential gains or, in some cases, result in losses by offsetting favorable price movements in portfolio holdings. Third, there is a risk that derivative contracts and hybrid instruments may be

erroneously priced or improperly valued and, as a result, the Fund may need to make increased cash payments to the counterparty. Fourth, exposure to derivative contracts and hybrid instruments may have tax

consequences to the Fund and its shareholders. For example, derivative contracts and hybrid instruments may cause the Fund to realize increased ordinary income or short-term capital gains (which are treated as

ordinary income for Federal income tax purposes) and, as a result, may increase taxable distributions to shareholders. In addition, under certain circumstances certain derivative contracts and hybrid instruments may

cause the Fund to: (a) incur an excise tax on a portion of the income related to those contracts and instruments; and/or (b) reclassify, as a return of capital, some or all of the distributions previously made to

shareholders during the fiscal year as dividend income. Fifth, a common provision in OTC derivative contracts permits the counterparty to terminate any such contract between it and the Fund, if the value of the Fund's

total net assets declines below a specified level over a given time period. Factors that may contribute to such a decline (which usually must be substantial) include significant shareholder redemptions and/or a marked

decrease in the market value of the Fund's investments. Any such termination of the Fund's OTC derivative contracts may adversely affect the Fund (for example, by increasing losses and/or costs, and/or preventing the

Fund from fully implementing its investment strategies). Sixth, the Fund may use a derivative contract to benefit from a decline in the value of a Reference Instrument. If the value of the Reference Instrument

declines during the term of the contract, the Fund makes a profit on the difference (less any payments the Fund is required to pay under the terms of the contract). Any such strategy involves risk. There is no

assurance that the Reference Instrument will decline in value during the term of the contract and make a profit for the Fund. The Reference Instrument may instead appreciate in value creating a loss for the Fund.

Seventh, a default or failure by a CCP or an FCM (also sometimes called a “futures broker”), or the failure of a contract to be transferred from an Executing Dealer to the FCM for clearing, may expose the

Fund to losses, increase its costs, or prevent the Fund from entering or exiting derivative positions, accessing margin, or fully implementing its investment strategies. The central clearing of a derivative and

trading of a contract over a SEF could reduce the liquidity in, or increase costs of entering into or holding, any contracts. Finally, derivative contracts and hybrid instruments may also involve other risks described

in this Prospectus, such as interest rate, credit, currency, liquidity and leverage risks.

RISK OF LOSS AFTER REDEMPTION

The

Fund may also invest in trade finance loan instruments primarily by investing in other investment companies (which are not available for general investment by the public) that owns those instruments, and that are

advised by an affiliate of the Adviser and is structured as an extended payment fund (EPF). In the EPF, the Fund, as shareholder, will bear the risk of investment loss during the period between when shares of such EPF

are presented to the transfer agent of the EPF for redemption and when the net asset value of the EPF is determined for payment of the redeemed EPF shares (the “Redemption Pricing Date”). The time between

when EPF shares are presented for redemption and the Redemption Pricing Date will be at least twenty-four (24) calendar days. EPF shares tendered for redemption will participate proportionately in the EPF's gains and

losses during between when EPF shares are presented for redemption and the Redemption Pricing Date. During this time the value of the EPF shares will likely fluctuate and EPF shares presented for redemption could be

worth less on the Redemption Pricing Date than on the day the EPF shares were presented to the transfer agent of the EPF for redemption. The EPF has adopted a fundamental policy that may only be changed by shareholder

vote, that the Redemption Pricing Date will fall no more than twenty-four (24) days after the date the Fund, as shareholder, presents EPF shares for redemption in good order. If such date is a weekend or holiday, the

Redemption Pricing Date will be on the preceding business day.

technology Risk

The

Adviser uses various technologies in managing the Fund, consistent with its investment objective(s) and strategy described in this Prospectus. For example, proprietary and third-party data and systems are utilized to

support decision-making for the Fund. Data imprecision, software or other technology malfunctions, programming inaccuracies and similar circumstances may impair the performance of these systems, which may negatively

affect Fund performance.

What Do Shares Cost?

CALCULATION OF NET ASSET

VALUE

When

the Fund receives your transaction request in proper form (as described in this Prospectus under the sections entitled “How to Purchase Shares” and “How to Redeem and Exchange Shares”), it is

processed at the next calculated net asset value of a Share (NAV). A Share's NAV is determined as of the end of regular trading on the New York Stock Exchange (NYSE) (normally 4:00 p.m. Eastern time) each day the NYSE

is open. The Fund calculates the NAV of each class by valuing the assets allocated to each class and dividing the balance by the number of Shares of the class outstanding.

The NAV for each class of Shares may

differ due to the level of expenses allocated to each class as well as a result of the variance between the amount of accrued investment income and capital gains or losses allocated to each class and the amount

actually distributed to shareholders of each class. The Fund's current NAV and/or public offering price may be found at FederatedInvestors.com, via online news sources and in certain newspapers.

You

can purchase, redeem or exchange Shares any day the NYSE is open.

When

the Fund holds securities that trade principally in foreign markets on days the NYSE is closed, the value of the Fund's assets may change on days you cannot purchase or redeem Shares. This may also occur when the U.S.

markets for fixed-income securities are open on a day the NYSE is closed.

In

calculating its NAV, the Fund generally values investments as follows:

| ■

| Fixed-income securities are fair valued using price evaluations provided by a pricing service approved by the Board of Trustees (“Board”).

|

| ■

| Derivative contracts listed on exchanges are valued at their reported settlement or closing price, except that options are valued at the mean of closing bid and asked quotations.

|

| ■

| Over-the-counter (OTC) derivative contracts are fair valued using price evaluations provided by a pricing service approved by the Board.

|

If any

price, quotation, price evaluation or other pricing source is not readily available when the NAV is calculated, if the Fund cannot obtain price evaluations from a pricing service or from more than one dealer for an

investment within a reasonable period of time as set forth in the Fund's valuation policies and procedures, or if information furnished by a pricing service, in the opinion of the Valuation Committee, is deemed not

representative of the fair value of such security, the Fund uses the fair value of the investment determined in accordance with the procedures generally described below. There can be no assurance that the Fund could

obtain the fair value assigned to an investment if it sold the investment at approximately the time at which the Fund determines its NAV per share.

Shares

of other mutual funds are valued based upon their reported NAVs. The prospectuses for these mutual funds explain the circumstances under which they will use fair value pricing and the effects of using fair value

pricing.

Fair Valuation and Significant

Events Procedures

The

Board has ultimate responsibility for determining the fair value of investments for which market quotations are not readily available. The Board has appointed a Valuation Committee comprised of officers of the Fund,

the Adviser and certain of the Adviser's affiliated companies to assist in determining fair value and in overseeing the calculation of the NAV. The Board has also authorized the use of pricing services recommended by

the Valuation Committee to provide fair value evaluations of the current value of certain investments for purposes of calculating the NAV. In the event that market quotations and price evaluations are not available

for an investment, the Valuation Committee determines the fair value of the investment in accordance with procedures adopted by the Board. The Board periodically reviews and approves the fair valuations made by the

Valuation Committee and any changes made to the procedures. The Fund's SAI discusses the methods used by pricing services and the Valuation Committee to assist the Board in valuing investments.

Using

fair value to price investments may result in a value that is different from an investment's most recent closing price and from the prices used by other mutual funds to calculate their NAVs. The application of the

fair value procedures to an investment represent a good faith determination of such investment's fair value. There can be no assurance that the Fund could obtain the fair value assigned to an investment if it sold the

investment at approximately the time at which the Fund determines its NAV per share.

The

Board also has adopted procedures requiring an investment to be priced at its fair value whenever the Adviser determines that a significant event affecting the value of the investment has occurred between the time as

of which the price of the investment would otherwise be determined and the time as of which the NAV is computed. An event is considered significant if there is both an affirmative expectation that the investment's

value will change in response to the event and a reasonable basis for quantifying the resulting change in value.

Examples of significant events that may occur after the close of the principal market on which a security is traded, or after the time of a price evaluation provided by a pricing service or a dealer, include:

| ■

| With respect to securities traded principally in foreign markets, significant trends in U.S. equity markets or in the trading of foreign securities index futures contracts;

|

| ■

| Political or other developments affecting the economy or markets in which an issuer conducts its operations or its securities are traded; and

|

| ■

| Announcements concerning matters such as acquisitions, recapitalizations or litigation developments or a natural disaster affecting the issuer's operations or regulatory changes or

market developments affecting the issuer's industry.

|

The Board has adopted procedures whereby the Valuation Committee uses a pricing service to provide factors to update the fair value of equity securities traded principally in foreign markets from

the time of the close of their respective foreign stock exchanges to the pricing time of the Fund. For other significant events, the Fund may seek to obtain more current quotations or price evaluations from

alternative pricing sources. If a reliable alternative pricing source is not available, the Valuation Committee will determine the fair value of the investment using another method approved by the Board. The Board has