Form 424B4 MorphoSys AG

Tweet

Tweet Share

ShareTable of Contents

Filed pursuant to Rule 424(b)(4)

Registration Nos. 333-223843 and 333-130614

8,300,000 American Depositary Shares

| Representing | 2,075,000 | Ordinary Shares |

This is the initial public offering of American Depositary Shares, or the ADSs, representing ordinary shares of MorphoSys AG, a German stock corporation. We are offering 8,300,000 ADSs, at a public offering price of $25.04 per ADS.

Each ADS represents 0.25 of an ordinary share. Our ordinary shares are bearer shares with no par value.

The ADSs have been approved for listing on the Nasdaq Global Market, or the Nasdaq, under the symbol “MOR”. Our shares are listed on the Frankfurt Stock Exchange under the symbol “MOR”.

We are an “emerging growth company” as defined under Section 2(a) of the Securities Act of 1933, and, as such, we have elected to comply with certain reduced public company reporting requirements for this prospectus and may elect to comply with reduced public company reporting requirements for future filings.

Investing in our ADSs involves risks. See “Risk Factors” beginning on page 14.

| Per ADS | Total | |||||||

| Price to public |

$ | 25.0400 | $ | 207,832,000.00 | ||||

| Underwriting discounts and commissions(1) |

$ | 1.7528 | $ | 14,548,240.00 | ||||

| Proceeds, before estimated expenses, to us |

$ | 23.2872 | $ | 193,283,760.00 | ||||

| (1) | We have agreed to reimburse the underwriters for certain expenses in connection with this offering. See “Underwriting.” |

We have granted the underwriters the right to purchase up to an additional 1,245,000 ADSs. If the underwriters exercise their option in full, the total underwriting discounts and commissions payable by us will be $16,730,476, and the total proceeds to us, before expenses will be $222,276,324.

The underwriters expect to deliver the ADSs to purchasers on or about April 23, 2018.

Neither the U.S. Securities and Exchange Commission, or SEC, nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Goldman Sachs & Co. LLC | J.P. Morgan | Leerink Partners | ||

| Berenberg Capital Markets, LLC | JMP Securities | |||

Prospectus dated April 18, 2018

Table of Contents

| Page | ||||

| iii | ||||

| iv | ||||

| 1 | ||||

| 10 | ||||

| 12 | ||||

| 14 | ||||

| 66 | ||||

| 68 | ||||

| 69 | ||||

| 70 | ||||

| 72 | ||||

| 73 | ||||

| 74 | ||||

| 76 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

78 | |||

| 94 | ||||

| 169 | ||||

| 191 | ||||

| 192 | ||||

| 195 | ||||

| 218 | ||||

| 228 | ||||

| 230 | ||||

| 231 | ||||

| 246 | ||||

| 247 | ||||

| 259 | ||||

| 260 | ||||

| 261 | ||||

| 262 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus or contained in any free writing prospectus we file with the SEC. Neither we nor the underwriters have authorized anyone to provide you with additional information or information different from that contained in this prospectus or in any free writing prospectus filed with the SEC. We are offering to sell, and seeking offers to buy, our ADSs only in jurisdictions where offers and sales of these securities are legally permitted. The information contained in this prospectus or in any free writing prospectus we file is accurate only as of its date, regardless of the time of delivery of this prospectus or of any sale of our ADSs. Our business, financial condition, results of operation and prospects may have changed since that date.

i

Table of Contents

Through and including May 13, 2018 (the 25th day after the date of this prospectus), federal securities laws may require all dealers that buy, sell or trade the ADSs, whether or not participating in this offering, to deliver a prospectus. This requirement is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

ii

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

All references in this prospectus to “U.S. dollars” or “$” are to the legal currency of the United States, all references to “€” or “euro” are to the currency introduced at the start of the third stage of the European economic and monetary union pursuant to the treaty establishing the European Community, as amended.

Unless otherwise indicated, the consolidated financial statements and related notes included in this prospectus have been prepared in accordance with International Accounting Standards and also comply with International Financial Reporting Standards and interpretations issued by the International Accounting Standards Board, or IASB, which differ in certain significant respects from U.S. generally accepted accounting principles, or U.S. GAAP.

Financial information in thousands or millions, and percentage figures in this prospectus have been rounded. Rounded total and sub-total figures in tables in this prospectus may differ marginally from unrounded figures indicated elsewhere in this prospectus or in the consolidated financial statements. Moreover, rounded individual figures and percentages may not produce the exact arithmetic totals and sub-totals indicated elsewhere in this prospectus.

iii

Table of Contents

This prospectus contains estimates and other statistical data made by independent parties and by us relating to market size and growth and other data about our industry. We obtained the industry and market data in this prospectus from our own research as well as from industry and general publications, surveys and studies conducted by third parties some of which may not be publicly available. These data involve a number of assumptions and limitations and contain projections and estimates of the future performance of the industries in which we operate that are subject to a high degree of uncertainty. We caution you not to give undue weight to such projections, assumptions and estimates.

iv

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider in making your investment decision. Before investing in our ADSs, you should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and MorphoSys AG’s consolidated financial statements and related notes appearing elsewhere in this prospectus, for a more complete understanding of our business and this offering. Except as otherwise required by the context, references to “MorphoSys”, “Company”, “we”, “us” and “our” are to MorphoSys AG and its subsidiaries on a consolidated basis.

Overview

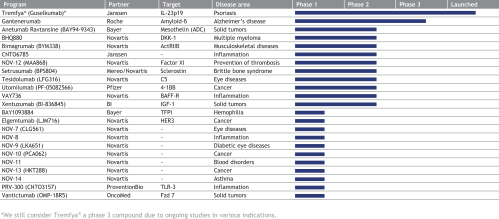

We are a late-stage biopharmaceutical company devoted to the development of innovative and differentiated therapies for patients suffering from serious diseases. Based on our proprietary technology platforms and leadership in the field of therapeutic antibody discovery, generation and engineering, we, together with our partners, have participated in the development of more than 100 therapeutic product candidates. Our broad pipeline spans two business segments: Proprietary Development, in which we invest in and develop product candidates, and Partnered Discovery, in which we generate product candidates for our partners in the pharmaceutical and biotechnology industries against targets identified by our partners. We currently have 28 product candidates in clinical development, including our most advanced proprietary product candidate, MOR208, for the treatment of relapsed or refractory diffuse large B cell lymphoma, or r/r DLBCL. We believe our pipeline of novel and differentiated product candidates has the potential to treat serious diseases and improve the lives of patients.

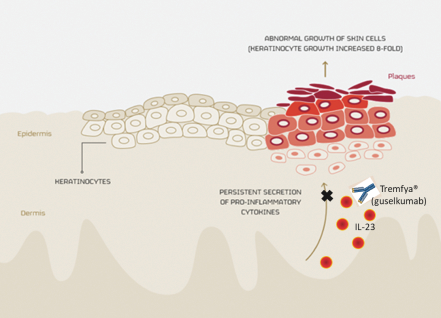

Our late-stage and most advanced proprietary product candidate, MOR208, received breakthrough therapy designation, or BTD, from the U.S. Food and Drug Administration, or the FDA, in 2017 in combination with lenalidomide for the treatment of patients with r/r DLBCL, who are not eligible for high-dose chemotherapy and autologous stem cell transplantation. We hold worldwide rights to develop and market MOR208. Also in 2017, Tremfya®, developed by our partner Janssen, became the first therapeutic antibody based on our proprietary technology to reach the market. Tremfya®, which is approved to treat moderate-to-severe plaque psoriasis, was launched in the United States in July 2017 and received approval for marketing in the European Union and Canada in November 2017.

Based on our heritage as an antibody discovery and development company, we have a large and diverse pipeline, composed of both proprietary and partnered programs, in multiple therapeutic areas and across all development phases. The combination of our technology platforms and antibody expertise has allowed us to generate promising product candidates and enter into multiple strategic collaborations with leading global pharmaceutical and biotechnology companies. These collaborations provide us with an additional funding source and allow us to leverage our collaborators’ expertise to advance the development of our proprietary product candidates.

1

Table of Contents

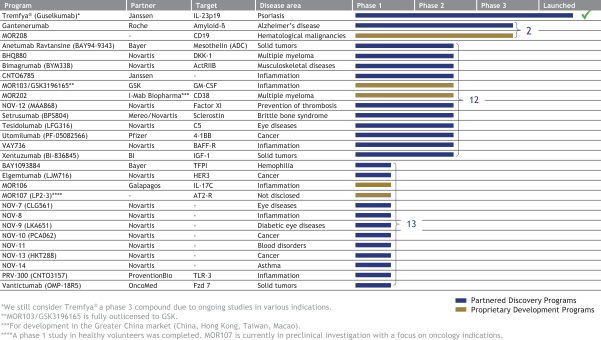

The following table summarizes our product candidates and programs:

Our most advanced Proprietary Development programs include:

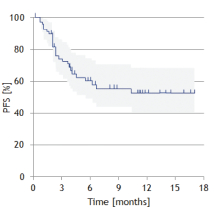

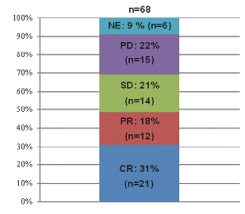

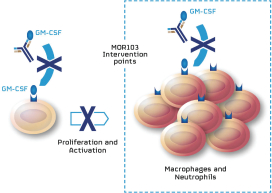

| · | MOR208—an investigational, humanized Fc-engineered monoclonal antibody directed against CD19. CD19 is a target for the treatment of B cell malignancies, including DLBCL, follicular lymphoma, or FL, chronic lymphocytic leukemia, or CLL, and others. On October 23, 2017, the FDA granted BTD for the use of MOR208 in combination with lenalidomide to treat patients with r/r DLBCL who are not eligible for high-dose chemotherapy and autologous stem cell transplantation. The granting of BTD was based on the interim results as of June 13, 2017 from our single arm Phase 2 L-MIND study, which showed a response in 23 out of 44 patients (Overall Response Rate, or ORR, 52%) and progression-free survival estimate based on a Kaplan Meier curve of 11.3 months based on investigator response assessment. Interim data from our most recent cut-off date, December 12, 2017, were consistent with our prior interim results, with a response in 33 out of 68 patients (ORR: 49%) and a progression-free survival, or PFS, rate at 12 months of 50.4% based on investigator response assessment, with the preliminary median progression-free survival, or mPFS, not yet reached. We are also investigating MOR208 in combination with bendamustine, in our pivotal Phase 2/3 B-MIND study targeting a comparable DLBCL patient population as the L-MIND study. B-MIND started as a randomized safety run-in with 10 patients in each treatment arm (the Phase 2 stage of the trial assessing safety of the combination with bendamustine) and continued then comparing MOR208 plus bendamustine with a standard of care rituximab plus bendamustine control arm (the Phase 3 stage of the trial comparing to standard of care). A third clinical trial, known as COSMOS, is an exploratory Phase 2 study in CLL patients who have progressed on or who do not tolerate treatment with Bruton tyrosine kinase inhibitors. Pursuant to our BTD, we are working closely with the FDA regarding further clinical development of MOR208. We |

2

Table of Contents

| hold worldwide rights to develop and market MOR208 and intend to commercialize it either alone or together with a partner. |

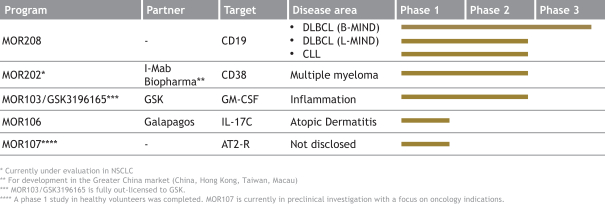

| · | MOR202—an investigational, human monoclonal HuCAL antibody directed against CD38. MOR202 is currently under clinical investigation in a Phase 1/2a trial in patients with relapsed or refractory multiple myeloma, or r/r MM. The study is evaluating the safety and preliminary efficacy of MOR202 alone and in combination with the immunomodulatory drugs pomalidomide or lenalidomide, plus dexamethasone, respectively. We believe MOR202 offers a potentially differentiated safety and administration profile relative to infusion site reaction and infusion time of other agents targeting CD38. Scientific research suggests that an anti-CD38 antibody such as MOR202 may have therapeutic activity in solid tumors including non-small cell lung cancer, or NSCLC. We plan to explore this potential activity in NSCLC in combination with nivolumab (an anti-PD-1 antibody) or more oncology indications either alone or together with a partner. |

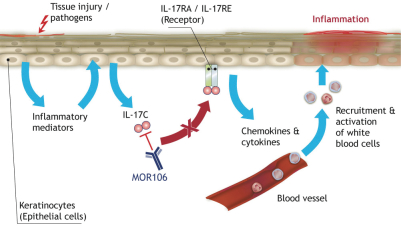

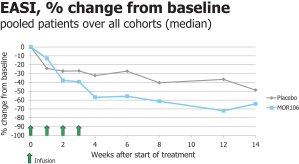

| · | MOR106—a human monoclonal antibody targeting IL-17C, currently under clinical development for the treatment of atopic dermatitis, or AD. We believe MOR106 is the first antibody directed against IL-17C in clinical development worldwide. MOR106 is also the first antibody from our Ylanthia platform to enter clinical development. Based on findings from pre-clinical models, we believe IL-17C plays an important role in inflammatory skin disorders. We are developing MOR106 in collaboration with our partner, Galapagos, and share equally the research and development costs as well as all future economics. In September 2017, we reported results from a randomized placebo-controlled Phase 1 study, testing MOR106 in single ascending doses in healthy volunteers and in multiple ascending doses in patients suffering from AD. In the trial, MOR106 was generally well-tolerated and showed first signs of clinical activity in five of six patients with moderate-to-severe AD. We plan to initiate a Phase 2 study with our partner Galapagos in the first half of 2018. |

Our most advanced Partnered Discovery products and product candidates include:

| · | Tremfya®—a HuCAL antibody directed against IL-23 marketed by our partner Janssen to treat moderate-to-severe plaque psoriasis was launched in the United States and received marketing approval in the EU and Canada in 2017. We are entitled to royalty payments on net sales of Tremfya®. Janssen is currently investigating Tremfya® in additional Phase 3 trials in psoriasis and in psoriatic arthritis and plans to develop the product in Crohn’s disease. |

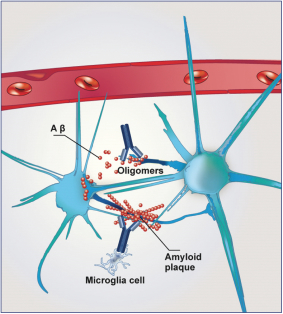

| · | Gantenerumab—a HuCAL antibody directed against amyloid beta that is being developed by Roche for the treatment of Alzheimer’s disease. In Phase 1 trials, gantenerumab has been shown to reduce brain amyloid in mild-to-moderate Alzheimer’s disease patients. Roche is currently planning to test a higher dose of gantenerumab in two Phase 3 trials, called GRADUATE 1 & 2, for patients with prodromal and mild Alzheimer’s disease. |

The majority of our Proprietary Development product candidates and all product candidates in our Partnered Discovery programs have been discovered and engineered using our advanced antibody technology platforms. Our core platforms include:

| · | HuCAL (Human Combinatorial Antibody Library)—HuCAL is our original technology platform, which constitutes a collection or “library” of several billion distinct fully human antibodies. |

3

Table of Contents

| This platform enables rapid selection of antibodies having high affinity and specificity as well as systematic optimization of antibodies to precisely-defined specifications to increase the probability of successful clinical development. |

| · | Ylanthia—Ylanthia is our newest antibody library, which comprises over 100 billion fully human antibodies. Ylanthia enables the generation of fully human antibody candidates with optimized biophysical properties, which we believe offer a number of important advantages over competing platforms. This platform builds on our experience in generating more than 100 therapeutic product candidates using our original HuCAL platform. We believe Ylanthia will be the source of the next generation of therapeutic antibody candidates in our and our partners’ future pipelines. |

| · | Lanthipeptides—Our lanthipeptide platform opens up new possibilities for discovering product candidates based on highly specific and stable peptides, which are intended to bind and activate only one target receptor subtype. |

We are committed to investing in our platforms, generating new therapeutics and developing them into products that address significant unmet medical needs.

We have an internationally-trained, multi-cultural team of more than 300 employees and consultants, including a research and development team of approximately 260 scientists, clinicians and support staff. Our management team and senior experts have deep experience and capabilities in biology, chemistry, product discovery and clinical development.

Our Strengths

We believe our core strengths include:

| · | Our lead product candidate MOR208, which has been granted BTD in r/r DLBCL by the FDA and has further potential in additional hematological malignancies. |

| · | Additional differentiated proprietary product candidates, such as MOR202 and MOR106, in clinical trials for the treatment of cancer and inflammatory diseases. |

| · | Tremfya®, the first approved product based on our technology which offers a royalty opportunity. |

| · | Our antibody pipeline, which we believe is one of the broadest and deepest in the biotech industry and which provides us with multiple opportunities for value creation. |

| · | Our long-term technology leadership in antibody discovery, generation and engineering, as demonstrated by multiple collaborations with leading pharmaceutical and biotechnology companies as well as by the breadth and depth of our technology platforms. |

| · | Our diversified business model with both proprietary and partnered development programs, which provides us with a strong financial base and strategic flexibility. |

| · | A broad intellectual property portfolio protecting product candidates as well as our technology platforms. |

| · | Our experienced management team, comprising industry leaders in antibody discovery and development. |

4

Table of Contents

Our Strategy

Our goal is to make differentiated, innovative biopharmaceuticals to improve the lives of patients suffering from serious diseases. Our strategy to achieve this goal is:

| · | Continue to advance the development of our lead product candidate MOR208 towards regulatory approval—The MOR208 program is currently in an advanced clinical development stage following receipt of BTD by the FDA in October 2017 based on interim data from our L-MIND study. We believe that with BTD, we can establish a path to approval of MOR208 in r/r DLBCL. In addition, we are evaluating opportunities to develop MOR208 in other treatment lines and hematological malignancies. |

| · | Build our commercial capabilities in connection with the potential future approval of MOR208—We are finalizing different commercialization strategies for MOR208. If we receive marketing approval for MOR208, our preferred option at this stage is to retain either sole or co-promotion rights in the United States and seek partners for commercialization elsewhere. We are currently commencing our commercialization preparation efforts with the goal of being ready to promote MOR208 as early as the first half of 2020. |

| · | Continue the development of MOR202—In order to maximize the value of MOR202, we are exploring opportunities for its further development, either alone or together with a partner, in one or more oncology indications, including in solid tumors, with an initial focus on NSCLC. |

| · | Advance our earlier stage product candidates—We continue to advance the development of our early-stage product candidates, in particular MOR106, for which we and our partner Galapagos intend to initiate a Phase 2 program in AD in 2018. |

| · | Realize the value of our technology platforms by using them to discover and develop additional early-stage proprietary programs—We continue to capitalize on the advantages of our antibody technologies and our internal expertise and know-how to discover and develop novel product candidates. |

Corporate Information

MorphoSys AG was founded in 1992 as a German limited liability company (Gesellschaft mit beschränkter Haftung). In June 1998, MorphoSys became a German stock corporation (Aktiengesellschaft) and is registered in the commercial register (Handelsregister) of the local court (Amtsgericht) of Munich under number HRB 121023. In March 1999, we listed on the Frankfurt Stock Exchange, and our shares currently trade under the symbol “MOR”.

Our registered address is Semmelweisstrasse 7, 82152 Planegg, Germany. Our telephone number is +49 89-89927-0. Our principal website is www.morphosys.com. The information contained on our website is not a part of this prospectus.

Our agent for service of process in the United States is CT Corporation System, 111 Eighth Avenue, New York, NY 10011.

5

Table of Contents

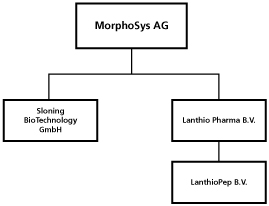

Organizational Chart

The following chart shows our organizational structure. All of the subsidiaries listed below are, directly or indirectly, wholly-owned by MorphoSys AG.

Our Risks and Challenges

Our business is subject to numerous risks, as more fully described in the section entitled “Risk Factors”. You should read these risks before you invest in the ADSs. We may be unable, for many reasons, including those that are beyond our control, to implement our business strategy. In particular, risks associated with our business include, but are not limited to, the following:

| · | we cannot assure you of the adequacy of our capital resources, including the proceeds from this offering, to successfully complete the development and commercialization of our product candidates, and a failure to obtain additional capital, if needed, could force us to delay, limit, reduce or terminate one or more of our product development programs or commercialization efforts; |

| · | we have incurred significant losses since inception and anticipate that we will continue to incur losses in the future; |

| · | all of our proprietary product candidates are still in pre-clinical or clinical development, and only one of our partnered products has been approved for marketing and sale. We cannot give any assurance that any of our product candidates will receive regulatory approval, and if we are unable to obtain regulatory approval and ultimately commercialize our product candidates or experience significant delays in doing so, our business will be materially harmed; |

| · | clinical trials are very expensive, time consuming and difficult to design and implement and involve uncertain outcomes. If clinical trials of our product candidates are prolonged, delayed or terminated, we may be unable to obtain required regulatory approvals, and therefore be unable to commercialize our product candidates on a timely basis or at all, which may materially adversely affect our business, financial condition, results of operations and prospects; |

| · | the FDA may rescind the breakthrough designation for MOR208 in combination with lenalidomide for the treatment of patients with r/r DLBCL who are not eligible for high-dose |

6

Table of Contents

| chemotherapy and autologous stem cell transplantation and we may be unable to obtain breakthrough therapy designation for other indications. In addition, breakthrough therapy designation by the FDA may not lead to a faster development, regulatory review or approval process, and it may not increase the likelihood that MOR208 will receive marketing approval in the United States; |

| · | we currently do not have a sales and marketing organization and we have no history of commercializing our proprietary products; |

| · | we face significant competition in seeking new partnerships, including for MOR202; |

| · | if we are unable to obtain and maintain sufficient intellectual property protection for our products or product candidates, or if the scope of our intellectual property protection is not sufficiently broad, our ability to commercialize our products or product candidates successfully and to compete effectively may be materially adversely affected; |

| · | we currently rely on third-party suppliers and single source third-party CMOs for the manufacturing of our product candidates and our dependence on these third parties may impair the development of our product candidates; |

| · | we are currently, and may in the future, be involved in lawsuits to protect or enforce our patents, which could be expensive, time-consuming and unsuccessful; |

| · | we face substantial competition from companies with considerably more resources and experience than we have, which may result in others discovering, developing, receiving approval for or commercializing products before or more successfully than us; |

| · | we do not currently intend to pay dividends on our securities, and, consequently, your ability to achieve a return on your investment will depend on appreciation in the price of the ADSs; and |

| · | the dual listing of our shares and the ADSs following this offering may adversely affect the liquidity and value of the ADSs. |

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company”, as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and is exempt from other burdens that are otherwise applicable generally to public companies. These provisions include:

| · | the ability to include only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations disclosure; |

| · | an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002, as amended, or the Sarbanes-Oxley Act; |

| · | to the extent that we no longer qualify as a foreign private issuer (1) reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, |

7

Table of Contents

| and (2) exemptions from the requirements of holding a non-binding advisory vote on executive compensation, including golden parachute compensation; and |

| · | an exemption from compliance with the requirement that the Public Company Accounting Oversight Board, or the PCAOB, has adopted regarding a supplement to the auditor’s report providing additional information about the audit and the financial statements. |

We may take advantage of these provisions for up to five years following the completion of this offering or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1.07 billion in annual revenue, have more than $700 million in market value of our shares held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced burdens. For example, Section 107 of the JOBS Act provides that an emerging growth company that uses U.S. GAAP for financial reporting can use the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended, or the Securities Act, for complying with new or revised accounting standards. Given that we currently report and expect to continue to report under International Financial Reporting Standards as issued by the IASB, or IFRS, we have irrevocably elected not to avail ourselves of this extended transition period and, as a result, we will adopt new or revised accounting standards on the relevant dates on which adoption of such standards is required by the IASB. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold equity securities.

Implications of Being a Foreign Private Issuer

Upon consummation of this offering, we will report under the Securities Exchange Act of 1934, as amended, or the Exchange Act, as a non-U.S. company with foreign private issuer status. Even after we no longer qualify as an emerging growth company, as long as we qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| · | the rules under the Exchange Act requiring domestic filers to issue financial statements prepared under U.S. GAAP; |

| · | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

| · | the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

| · | the rules under the Exchange Act requiring the filing with the SEC of quarterly reports on Form 10-Q, containing unaudited financial and other specified information, and current reports on Form 8-K, upon the occurrence of specified significant events. |

Notwithstanding these exemptions, we will file with the SEC, within four months after the end of each fiscal year, or such applicable time as required by the SEC, an annual report on Form 20-F containing financial statements audited by an independent registered public accounting firm.

8

Table of Contents

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held by U.S. residents and any of the following three circumstances applies: the majority of our executive officers or directors are U.S. citizens or residents, more than 50% of our assets are located in the United States or our business is administered principally in the United States.

Both foreign private issuers and emerging growth companies are also exempt from certain more stringent executive compensation disclosure rules. Thus, even if we no longer qualify as an emerging growth company but remain a foreign private issuer, we will continue to be exempt from the more stringent compensation disclosure requirements for companies that are not emerging growth companies and will continue to be permitted to follow our home country practice on such matters.

9

Table of Contents

| ADSs offered by us |

8,300,000 ADSs |

| Option to purchase additional ADSs |

We granted the underwriters an option to purchase up to an additional 1,245,000 ADSs from us. |

| The ADSs |

Each ADS represents 0.25 of an ordinary share. |

| The depositary, the custodian or any of their respective nominees will hold the ordinary shares and any other rights or property underlying your ADSs. As an ADS holder, we will not treat you as one of our shareholders. The depositary, The Bank of New York Mellon, will be the holder of the ordinary shares underlying your ADSs. You will have rights as provided in the deposit agreement. You may surrender your ADSs and withdraw the underlying ordinary shares as provided, and pursuant to, the limitations set forth in, the deposit agreement. The depositary will charge you fees for, among other acts, any such surrender for the purpose of withdrawal. In certain limited instances described in the deposit agreement, we may amend or terminate the deposit agreement without your consent. If you continue to hold your ADSs, you agree to be bound by the terms of the deposit agreement then in effect. |

| To better understand the terms of the ADSs, you should carefully read the “Description of American Depositary Shares” section of this prospectus. You should also read the deposit agreement, which is an exhibit to the Registration Statement of which this prospectus forms a part. |

| Depositary |

The Bank of New York Mellon |

| Custodian |

The Bank of New York Mellon SA/NV |

| Use of proceeds |

We estimate that we will receive total net proceeds of approximately $189.9 million, after deducting the underwriting discounts and commissions and estimated offering expenses payable by us. If the underwriters exercise in full their option to purchase additional ADSs, we estimate that the net proceeds of the offering will be approximately $218.9 million, after deducting the underwriting discounts and commissions and estimated offering expenses payable by us. |

| We intend to use the net proceeds from this offering, together with a portion of our cash and cash equivalents, available-for-sale financial assets, bonds available-for-sale, and financial assets classified as loans and receivables to continue the development of our proprietary clinical pipeline, initiate pre-commercial and |

10

Table of Contents

| commercial activities and to advance earlier stage product candidates in particular as follows: (i) further development of MOR208, our wholly-owned anti-CD19 antibody currently being evaluated in r/r DLBCL (a) in combination with lenalidomide for patients ineligible for high-dose chemotherapy, or HDCT, and autologous stem cell transplantation, or ASCT, (b) in combination with bendamustine for patients ineligible for HDCT and ASCT, and (c) in additional treatment lines and additional indications; (ii) build our commercial capabilities in connection with the potential future approval of MOR208; (iii) to fund clinical development of MOR202 in MM and NSCLC and MOR106 in atopic dermatitis; and (iv) for general corporate purposes, including the addition of further compounds to our pipeline via own research, in-licensing or acquisition, if promising compounds are available, and potential addition of technologies to expand our existing technology base. See the “Use of Proceeds” section of this prospectus beginning on page 70 for a more complete description of the intended use of proceeds from this offering. |

| Dividend policy |

We have not paid any dividends on our ordinary shares since our inception, and we currently intend to retain any future earnings to finance the growth and development of our business. Therefore, we do not anticipate that we will declare or pay any cash dividends in the foreseeable future. Except as required by law, any future determination to pay cash dividends will be at the discretion of our management board and supervisory board and will be dependent upon our financial condition, results of operations, capital requirements, and other factors our management board and supervisory board deem relevant. See “Dividend Policy”. |

| Lock-up agreements |

We have agreed with the underwriters, subject to certain exceptions, not to offer, sell, or dispose of any of our share capital or securities convertible into or exchangeable or exercisable for any of our share capital during the 90-day period following the date of this prospectus. Members of our management board have agreed to substantially similar 90-day lock-up provisions, subject to certain exceptions. |

| Risk factors |

You should carefully read the information set forth in the “Risk Factors” section of this prospectus beginning on page 14 and the other information set forth in this prospectus before deciding to invest in the ADSs. |

| Nasdaq Global Market Symbol |

“MOR” |

11

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

We present below summary historical consolidated financial data of MorphoSys AG. The financial data as of and for the years ended December 31, 2016 and 2017, have been derived from our audited consolidated financial statements and the related notes, which are included elsewhere in this prospectus and which have been prepared in accordance with IFRS.

The summary historical consolidated financial data presented below are not necessarily indicative of the financial results expected for any future periods. The summary historical consolidated financial data below do not contain all the information included in our financial statements. You should read this information in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, “Selected Consolidated Financial Data” and our consolidated financial statements and related notes, each included elsewhere in this prospectus.

The following tables also contain translations of euro amounts into U.S. dollars for amounts presented as of and for the year ended December 31, 2017. These translations are solely for convenience of the reader and were calculated at the rate of €1.00 per $1.2022, which equals the noon buying rate of the Federal Reserve Bank of New York on December 29, 2017. You should not assume that, on that or any other date, one could have converted these amounts of euro into U.S. dollars at this exchange rate.

Consolidated Statement of Income Data:

| Year ended December 31, | ||||||||||||

| 2016 | 2017 | |||||||||||

| (in €) | (in €) | (in $) | ||||||||||

| (in thousands except per share data) | ||||||||||||

| Revenues |

49,744 | 66,791 | 80,296 | |||||||||

| Operating Expenses |

||||||||||||

| Research and Development |

(95,723 | ) | (116,809 | ) | (140,428 | ) | ||||||

| General and Administrative |

(14,116 | ) | (17,039 | ) | (20,484 | ) | ||||||

| Total Operating Expenses |

(109,839 | ) | (133,848 | ) | (160,912 | ) | ||||||

| Other Income |

709 | 1,120 | 1,346 | |||||||||

| Other Expenses |

(554 | ) | (1,671 | ) | (2,009 | ) | ||||||

| Earnings before Interest and Taxes (EBIT) |

(59,941 | ) | (67,608 | ) | (81,278 | ) | ||||||

| Finance Income |

1,385 | 712 | 856 | |||||||||

| Finance Expenses |

(1,308 | ) | (1,895 | ) | (2,278 | ) | ||||||

| Income Tax Expenses |

(519 | ) | (1,036 | ) | (1,245 | ) | ||||||

| Consolidated Net Profit/(Loss) |

(60,383 | ) | (69,827 | ) | (83,946 | ) | ||||||

| Earnings per Share, basic and diluted(1) |

(2.28 | ) | (2.41 | ) | (2.90 | ) | ||||||

| Shares Used In Computing Earnings per Share (in units), basic and diluted(1) |

26,443,415 | 28,947,566 | n/a | |||||||||

| Dividends Declared per Share |

— | — | — | |||||||||

| (1) | Basic and diluted Earnings per Share are the same in each of the years ended December 31, 2016 and 2017, because the assumed exercise of outstanding stock options and convertible bonds would be anti-dilutive due to our consolidated net loss in the respective period. |

12

Table of Contents

Consolidated Balance Sheet Data:

| As of December 31, | ||||||||||||

| 2016 | 2017 | |||||||||||

| (in €) | (in €) | (in $) | ||||||||||

| (in thousands) | ||||||||||||

| Cash and Cash Equivalents |

73,929 | 76,589 | 92,075 | |||||||||

| Available-for-sale Financial Assets |

63,362 | 86,538 | 104,036 | |||||||||

| Bonds, Available-for-sale |

6,532 | — | — | |||||||||

| Financial Assets classified as Loans and Receivables (current and non-current) |

215,630 | 149,059 | 179,199 | |||||||||

| Total Current Assets |

308,056 | 340,681 | 409,567 | |||||||||

| Total Assets |

463,600 | 415,398 | 499,391 | |||||||||

| Total Liabilities |

48,140 | 56,727 | 68,197 | |||||||||

| Total Stockholders’ Equity |

415,460 | 358,671 | 431,194 | |||||||||

13

Table of Contents

Investing in our ADSs involves a high degree of risk. You should carefully consider the risks and uncertainties described below, which we believe are the material risks of our business, our industry, our intellectual property, the ADSs and this offering, before making an investment decision. If any of the following risks actually occurs, our business, financial condition and operating results could be harmed. In that case, the trading price of the ADSs could decline and you might lose all or part of your investment. In assessing these risks, you should also refer to the other information contained in this prospectus, including MorphoSys AG’s consolidated financial statements and the related notes thereto appearing elsewhere in this prospectus.

Risks Related to Our Financial Condition

We cannot assure you of the adequacy of our capital resources, including the proceeds from this offering, to successfully complete the development and commercialization of our product candidates, and a failure to obtain additional capital, if needed, could force us to delay, limit, reduce or terminate one or more of our product development programs or commercialization efforts.

As of December 31, 2017, we had cash and cash equivalents, available-for-sale financial assets and current financial assets classified as loans and receivables amounting to €312.2 million. We believe that we will continue to expend substantial resources for the foreseeable future developing our proprietary product candidates and in particular MOR208. These expenditures will include costs associated with research and development, conducting pre-clinical studies and clinical trials, seeking regulatory approvals, as well as launching and commercializing products approved for sale, if any, and potentially acquiring new products. In addition, other unanticipated costs may arise. Because the outcome of our anticipated clinical trials is highly uncertain, we cannot reasonably estimate the actual amounts necessary to successfully complete the development and commercialization of our proprietary product candidates.

Our future funding requirements will depend on many factors, including but not limited to:

| · | the numerous risks and uncertainties associated with developing therapeutic product candidates; |

| · | the number and characteristics of product candidates that we pursue; |

| · | the rate of enrollment, progress, cost and outcomes of our clinical trials, which may or may not meet their primary end-points; |

| · | the timing of, and cost involved in, conducting non-clinical studies that are regulatory prerequisites to conducting clinical trials of sufficient duration for successful product registration; |

| · | the cost of manufacturing clinical supply and establishing commercial supply of our product candidates; |

| · | the timing of, and the costs involved in, obtaining regulatory approvals for our product candidates if clinical trials are successful; |

| · | the timing of, and costs involved in, conducting post-approval studies that may be required by regulatory authorities; |

14

Table of Contents

| · | the cost of commercialization activities for our product candidates, if any of our product candidates are approved for sale; |

| · | the terms and timing of any collaborative, licensing, and other arrangements that we may establish, including any required milestone and royalty payments thereunder and any non-dilutive funding that we may receive; |

| · | the costs involved in preparing, filing, prosecuting, maintaining, defending and enforcing patent claims, including litigation costs, if any, and the outcome of any such litigation; |

| · | the timing, receipt, and amount of sales of, or royalties or milestones on, our future products, if any; and |

| · | the costs to recruit and build the organization including key executives needed to transform to a commercial organization. |

In addition, our operating plan may change as a result of many factors currently unknown to us. As a result of these factors, we may need additional funds sooner than planned. We expect to finance future cash needs primarily through a combination of public or private equity offerings, strategic collaborations and non-dilutive funding. If sufficient funds on acceptable terms are not available when needed, or at all, we could be forced to significantly reduce operating expenses and delay, limit, reduce or terminate one or more of our product development programs or commercialization efforts.

We have incurred significant losses since inception and anticipate that we will continue to incur losses in the future.

We are a late-stage biopharmaceutical company. We have incurred significant losses since our inception. Our consolidated net loss for the year ended December 31, 2017 was €69.8 million. As of December 31, 2017, our accumulated deficit was approximately €97.4 million. We expect to continue to incur losses in the future as we continue our research and development of, and seek regulatory approvals for, our product candidates, prepare for and begin to commercialize any approved product candidates and add infrastructure and personnel to support our product development efforts and operations as a public company in the United States. The net losses and negative cash flows incurred to date, together with expected future losses, have had, and likely will continue to have, an adverse effect on our shareholders’ deficit and working capital. The amount of future net losses will depend, in part, on the rate of future growth of our expenses and our ability to generate revenue.

Because of the numerous risks and uncertainties associated with biopharmaceutical product development, we are unable to accurately predict the timing or amount of increased expenses or when, or if, we will be able to achieve profitability. For example, our expenses could increase if we are required by the FDA or EMA to perform trials in addition to those that we currently expect to perform, or if there are any delays in completing our currently planned clinical trials, the partnering process for our proprietary product candidates or in the development of any of our proprietary product candidates.

Our revenue to date has been primarily revenue from the license of our proprietary technology platforms and from milestone payments for the development of product candidates against targets provided by our collaborators. Our ability to generate revenue and achieve profitability in the future depends in large part on our ability, alone or with our collaborators, to achieve milestones and to successfully complete the development of, obtain the necessary regulatory

15

Table of Contents

approvals for, and commercialize, product candidates. This will require us to be successful in a range of challenging activities, including developing product candidates, obtaining regulatory approval for such product candidates, and manufacturing, marketing and selling those product candidates for which we may obtain regulatory approval. We may never succeed in these activities and may never generate revenue from product sales that is significant enough to achieve profitability. Even if we achieve profitability in the future, we may not be able to sustain profitability in subsequent periods. Our failure to become or remain profitable would depress our market value and could impair our ability to raise capital, expand our business, develop other product candidates, or continue our operations. A decline in the value of our company could also cause you to lose all or part of your investment.

Our operating results may fluctuate significantly in the future.

Our results of operations may fluctuate significantly in the future due to a variety of factors, many of which are outside of our control. The revenues we generate, if any, and our operating results will be affected by numerous factors, including, but not limited to:

| · | the development status of our product candidates and, particularly, the timing of any milestone payments to be paid or received by us under our collaboration agreements; |

| · | the incurrence of clinical expenses that could fluctuate significantly from period to period; |

| · | the commercial success of the products marketed by our partners, in particular Tremfya®, and the amount of royalties to us associated therewith; |

| · | the unpredictable effects of collaborations during these periods; |

| · | the timing of our satisfaction of applicable regulatory requirements; |

| · | the rate of expansion of our clinical development and other development efforts; |

| · | the effect of competing technologies and products and market developments; and |

| · | general and industry-specific economic conditions. |

For example, we expect our revenues in 2018 to be significantly less than we generated in 2017 as a result of the conclusion of our collaboration with Novartis and the corresponding reduction in revenues from funded research and license fee payments. If our operating results fall below the expectations of investors or securities analysts, the price of our ordinary shares could decline substantially. Furthermore, any fluctuations in our operating results and cash flows may, in turn, cause the price of our ADSs to fluctuate substantially.

Raising additional capital may cause dilution to our shareholders, restrict our operations or require us to relinquish rights to our technologies or product candidates.

Identifying and acquiring rights to develop potential product candidates and conducting pre-clinical testing and clinical trials is a time-consuming, expensive and uncertain process that may take years to complete. We may never generate the necessary data or results required to obtain regulatory approval and achieve product sales, and even if one or more of our product candidates is approved, they may not achieve commercial success. Accordingly, we will need to continue to rely on additional financing to achieve our business objectives. Adequate additional financing may not be available to us on acceptable terms, or at all.

We may seek additional funding through a combination of equity offerings, debt financings, including convertible bond offerings, collaborations, licensing arrangements, strategic alliances

16

Table of Contents

and marketing or distribution arrangements. To the extent that we raise additional capital through the sale of equity or convertible debt securities, your ownership interest will be diluted, and the terms may include liquidation or other preferences that adversely affect your rights as a holder of our ADSs. The incurrence of indebtedness or the issuance of certain equity securities could result in increased fixed payment obligations and could also result in certain additional restrictive covenants, such as limitations on our ability to incur additional debt or issue additional equity, limitations on our ability to acquire or license intellectual property rights and other operating restrictions that could adversely impact our ability to conduct our business. In addition, issuance of additional equity securities, or the possibility of such issuance, may cause the market price of our ADSs to decline. In the event that we enter into collaborations or licensing arrangements to raise capital, we may be required to accept unfavorable terms, including relinquishing or licensing to a third party on unfavorable terms our rights to technologies or product candidates that we otherwise would seek to develop or commercialize ourselves or potentially reserve for future potential arrangements when we might be able to achieve more favorable terms.

A substantial portion of our historical revenues are from a limited number of strategic collaborations and partnerships, and the termination of these collaborations could have a material adverse effect on our business, financial condition and results of operations.

Historically, we derived a substantial portion of our revenues from a limited number of collaborations, under which we generated revenues through licensing arrangements such as research and development payments, up-front payments, milestone payments, and, once a product is commercialized, royalty payments based on a portion of the revenue of product sold. For the year ended December 31, 2017, 90.4% of our revenues were derived from our collaboration partners Novartis, I-Mab Biopharma and Janssen. We do not have further research and development collaborations with Janssen and Novartis at this time and, as a result, we expect our revenues from funded research and license fee payments to be significantly lower in 2018. We expect royalties from Janssen on sales of Tremfya® to account for a substantial portion of our revenues for the next several years. The loss of any significant collaborator or any significant reduction in payments by a collaborator may have a material adverse effect on our business, financial condition and results of operations.

Risks Related to the Development, Clinical Testing and Commercialization of Our Product Candidates

All of our proprietary product candidates are still in pre-clinical or clinical development, and only one of our partnered products has been approved for marketing and sale. We cannot give any assurance that any of our product candidates will receive regulatory approval, and if we are unable to obtain regulatory approval and ultimately commercialize our product candidates or experience significant delays in doing so, our business will be materially harmed.

All of our proprietary product candidates are still in pre-clinical or clinical development, and only one of our partnered products, Tremfya®, has received regulatory approval. Although we may receive certain payments from our collaboration partners, including upfront payments, payments for achieving certain development, regulatory or commercial milestones and royalties, our ability to generate revenue from our product candidates’ sales is dependent on receipt of regulatory approval for, and successful commercialization of, such product candidates, which

17

Table of Contents

may never occur. Our business and future success is in particular dependent on our ability to develop, either alone or in partnership, successfully, receive regulatory approval for, and then successfully commercialize our proprietary product candidates, in particular MOR208. Each of our product candidates will require additional pre-clinical and/or clinical development, regulatory approval in multiple jurisdictions, manufacturing supply, substantial investment and significant marketing efforts before we generate any revenue from product sales or royalties. We are not permitted to market or promote any of our product candidates before we receive regulatory approval from applicable regulatory authorities. The success of our product candidates will depend on several factors, including the following:

| · | successful completion of pre-clinical and/or clinical studies; |

| · | successful enrollment of patients in, and completion of, clinical trials; |

| · | strategic commitment to particular product candidates and indications by us and our collaborators; |

| · | receipt of regulatory authorizations from applicable regulatory authorities for future clinical trials; |

| · | receipt of product approvals, including marketing approvals, from applicable regulatory authorities; |

| · | successful completion of all safety studies required to obtain regulatory approval in the United States, the European Union and other jurisdictions for our product candidates; |

| · | obtaining and maintaining patent and trade secret protection or regulatory exclusivity for our product candidates; |

| · | launching commercial sales of our product candidates, if and when approved, whether alone or in collaboration with others; |

| · | acceptance of the product candidates, if and when approved, by patients, the medical community and third-party payors; |

| · | effectively competing with other therapies; |

| · | obtaining and maintaining coverage and adequate reimbursement from third-party payors; |

| · | enforcing and defending intellectual property rights and claims; |

| · | maintaining a continued acceptable safety and quality profile of the product candidates following approval; and |

| · | maintaining a continued, sufficient supply of drug substance in acceptable quality. |

If we do not achieve one or more of these factors in a complete and timely manner or at all, we could experience significant delays or an inability to successfully commercialize our product candidates, which would materially adversely affect our business, financial condition, results of operations and prospects and, in case of product candidates, technologies and licenses we have acquired, may result in a significant impairment of assets.

We have not previously submitted a biologics license application, or BLA, to the FDA, or similar regulatory approval filings to comparable foreign authorities, for any product candidate, and we cannot be certain that any of our product candidates will be successful in clinical trials or receive regulatory approval. Further, our product candidates may not receive regulatory

18

Table of Contents

approval even if they are successful in clinical trials. If we do not receive regulatory approvals for our product candidates, we may not be able to continue our operations. Even if we successfully obtain regulatory approvals to market one or more of our product candidates, our revenues will be dependent, in part, upon the size of the markets in the territories for which we gain regulatory approval and have commercial rights. If the markets for patient subsets that we are targeting are not as significant as we estimate, we may not generate significant revenues from sales of such products, if approved.

We plan to seek regulatory approval to commercialize our product candidates both in the United States and the EU, and potentially in additional foreign countries. While the scope of regulatory approval is similar in other countries, to obtain separate regulatory approval in many other countries, we must comply with numerous and varying regulatory requirements of such countries regarding safety and efficacy and governing, among other things, clinical trials and commercial sales, pricing and distribution of our product candidates, and we cannot predict success in these jurisdictions.

Clinical trials are very expensive, time consuming and difficult to design and implement and involve uncertain outcomes. If clinical trials of our product candidates are prolonged, delayed or terminated, we may be unable to obtain required regulatory approvals, and therefore be unable to commercialize our product candidates on a timely basis or at all, which may materially adversely affect our business, financial condition, results of operations and prospects.

We are currently conducting clinical trials for MOR208, MOR202, and MOR106. Each of our clinical trials requires the investment of substantial expense and time and the timing of the commencement, continuation and completion of these clinical trials may be subject to significant delays or termination relating to various causes, including, among other things:

| · | scheduling conflicts with participating clinicians and clinical institutions; |

| · | difficulties in identifying and enrolling patients who meet trial eligibility criteria; |

| · | failure of patients to complete the clinical trials or return for post-treatment follow-up; |

| · | delays in accumulating the required number of clinical events for data analyses; |

| · | clinical investigators or sites deviating from trial protocol or failing to comply with regulatory requirements or meet their contractual obligations; |

| · | delay or failure to obtain required approvals; |

| · | delays in or failure to reach agreement on acceptable terms with prospective contract research organizations, or CROs, and clinical trial sites, the terms of which can be subject to extensive negotiation and may vary significantly among different CROs and trial sites; |

| · | delays in or failure to obtain institutional review board, or IRB, approval at each site; |

| · | failure of third-party contractors used in our clinical trials or contract manufacturing organizations, or CMOs, to comply with regulatory requirements or meet their contractual obligations in a timely manner, or not at all; |

| · | changes in regulatory requirements; |

| · | the development and approval of competitive products, in particular with respect to MOR202 for the treatment of MM; |

19

Table of Contents

| · | results from clinical trials of competing compounds, which may give rise to concerns about the target, the envisioned mode of action, the compound class or the commercial potential of the product candidate we are evaluating — in particular, in respect of MOR208, data being produced from other product candidates in CLL may make our ability to get an approval for MOR208 in this indication more difficult; |

| · | higher-than-expected costs of clinical trials of our product candidates; and |

| · | insufficient, inadequate or prohibitively expensive supply or quality of our product candidates or other materials necessary to conduct clinical trials of our product candidate. |

We do not know whether any of our clinical trials will begin as planned, will need to be redesigned or amended or will be completed on schedule, or at all. Clinical testing is expensive and can take many years to complete, and its outcome is inherently uncertain. Failure can occur at any time during the clinical trial process. We could encounter delays if a clinical trial is suspended or terminated by us, by the IRBs of the institutions in which such trials are being conducted, by a data review committee or data safety monitoring board for such trial or by the FDA or other regulatory authorities. Such authorities may impose such a suspension or termination due to a number of factors, including failure to conduct the clinical trial in accordance with regulatory requirements or our clinical protocols, inspection of the clinical trial operations or trial site by the FDA or other regulatory authorities resulting in the imposition of a clinical hold, safety issues or adverse side effects, failure to demonstrate a benefit from using a drug, changes in governmental regulations or administrative actions or lack of adequate funding to continue the clinical trial. If we experience delays in the completion of, or termination of, any clinical trial of our product candidates, the commercial prospects of our product candidates will be harmed, and our ability to generate product revenues from any of these product candidates will be delayed. In addition, any delays in completing our clinical trials will increase our costs, slow down our product candidate development and approval process and jeopardize our ability to commence product sales and generate revenues. Significant clinical trial delays could also allow our competitors to bring products to market before we do or shorten any periods during which we have the exclusive right to commercialize our product candidates and impair our ability to commercialize our product candidates, and may harm our business and results of operations. In addition, some of the factors that cause, or lead to, a delay in the commencement or completion of clinical trials may also ultimately lead to the denial of regulatory approval of our product candidates.

Clinical trials must be conducted with supplies of our product candidates produced under current good manufacturing practice, or cGMP, requirements and other regulations. Furthermore, we rely on CROs and clinical trial sites to ensure the proper and timely conduct of our clinical trials and while we have agreements governing their committed activities, we have limited influence over their actual performance. We depend on our collaborators and on medical institutions and CROs to conduct our clinical trials in compliance with Good Clinical Practice, or GCP, requirements. To the extent our collaborators or the CROs fail to enroll participants for our clinical trials, fail to conduct the study to GCP standards or are delayed for a significant time or fail in the execution of trials, including achieving full enrollment, we may be affected by increased costs, program delays or both, which may harm our business.

If we are unable to successfully complete clinical trials of our product candidates or other testing, if the results of these trials or tests are unfavorable or are only modestly favorable, if

20

Table of Contents

there are safety concerns associated with our product candidates we may decide to develop in the future, or if we are required to conduct additional clinical trials or other testing of our product candidates that we may develop in future beyond the trials and testing that we contemplate, we may:

| · | be delayed in obtaining marketing approval for our product candidates; |

| · | not obtain marketing approval at all; |

| · | obtain approval for indications or patient populations that are not as broad as intended or desired; |

| · | obtain approval with product labeling that includes significant use or distribution restrictions or significant safety warnings, including boxed warnings; |

| · | be subject to additional post-marketing testing or other requirements; or |

| · | remove the product from the market after obtaining marketing approval. |

The occurrence of any such events may materially adversely affect our business, financial condition, results of operations and prospects.

The incidence and prevalence for target patient populations of our product candidates are based on estimates and third-party sources. If the market opportunities for our product candidates are smaller than we estimate or if any approval that we obtain is based on a narrower definition of the patient population, our business, financial condition, results of operations and prospects may be materially adversely affected.

Periodically, we make estimates regarding the incidence and prevalence of target patient populations for particular diseases based on various third-party sources and internally generated analysis and use such estimates in making decisions regarding our product development strategy, including determining indications on which to focus in pre-clinical or clinical trials.

These estimates may be inaccurate or based on imprecise data. For example, the total addressable market opportunity will depend on, among other things, the acceptance of such data by the medical community and patient access, product pricing and reimbursement. The number of patients in the addressable markets may turn out to be lower than expected, patients may not be otherwise amenable to treatment with our products, or new patients may become increasingly difficult to identify or gain access to, all of which could materially adversely affect our business, financial condition, results of operations and prospects.

The speed at which we complete our pre-clinical studies and clinical trials depend on many factors, including, but not limited to, patient enrollment. If we are unable to enroll patients in our clinical trials, our research and development efforts and business, financial condition, results of operations and prospects could be materially adversely affected.

Patient enrollment, a significant factor in the timing and successful completion of clinical trials, is affected by many factors, including the size and nature of the patient population, the proximity of patients to clinical sites, the eligibility criteria for the trial, the design of the clinical trial, competing clinical trials and clinicians’ and patients’ perceptions as to the potential advantages of the product being studied in relation to other available therapies, including any new products that may be approved for the indications we are investigating. Because there is a relatively limited number of patients worldwide, patient enrollment may be challenging. Trials

21

Table of Contents

may be subject to delays as a result of patient enrollment taking longer than anticipated or patient withdrawal. Delays in the completion of any clinical trial of our product candidates will increase our costs, slow down our product candidate development and delay or potentially jeopardize our ability to receive regulatory approval, commence product sales and generate revenue. Any of these occurrences may harm our clinical trials, which could materially adversely affect our business, financial condition, results of operations and prospects.

Results of previous pre-clinical studies and clinical trials may not be predictive of future results, and the results of our current and planned clinical trials may not satisfy the requirements of the FDA, the EMA or comparable foreign regulatory authorities.

Positive or timely results from pre-clinical or early-stage trials do not ensure positive or timely results in late-stage clinical trials or product approval by the FDA, European Medicines Agency, or the EMA, or comparable foreign regulatory authorities. This includes the interim data presented from the L-MIND study as of June 13, 2017, which will evolve over time and may not be as positive as interim data that were the basis on which the FDA awarded breakthrough therapy designation. We will generally be required to demonstrate with substantial evidence through well-conducted, possibly controlled clinical trials that our product candidates are safe and effective for use in a well-defined patient population before we can seek regulatory approvals for their commercial sale. Our planned clinical trials may produce negative or inconclusive results, and we or any of our current and future collaborators may decide, or regulators may require us, to conduct additional clinical or pre-clinical testing. Success in pre-clinical studies or early-stage clinical trials does not mean that future clinical trials or registration clinical trials will be successful because product candidates in later-stage clinical trials may fail to demonstrate sufficient safety or efficacy to the satisfaction of the FDA, EMA and comparable foreign regulatory authorities, despite having progressed through pre-clinical studies and initial clinical trials. Product candidates that have shown promising results in early clinical trials may still suffer significant setbacks in subsequent clinical trials. For example, a number of companies in the pharmaceutical industry, including those with greater resources and experience than us, have suffered significant setbacks in advanced clinical trials, even after obtaining promising results in earlier clinical trials. Similarly, interim results of a clinical trial do not necessarily predict final results.

The regulatory approval processes of the FDA and comparable foreign authorities are lengthy, time consuming and inherently unpredictable and if we fail to obtain regulatory approval in any jurisdiction, we will not be able to commercialize our products in that jurisdiction and our business, results of operations, financial condition and prospects, may be materially adversely affected.

The time required to obtain approval by the FDA and comparable foreign authorities is unpredictable but typically takes many years following the commencement of clinical trials and depends upon numerous factors, including the substantial discretion of the regulatory authorities. In addition, approval laws, regulations, policies or the type and amount of clinical data or other information necessary to gain approval may change during the course of a product candidate’s clinical development and may vary among jurisdictions. We have not obtained regulatory approval for any product candidate, and it is possible that none of our existing product candidates or any product candidates we may seek to develop in the future will ever obtain regulatory approval.

22

Table of Contents

Our product candidates could fail to receive regulatory approval for many reasons, including the following:

| · | the FDA or comparable foreign regulatory authorities may disagree with the design or implementation of our clinical trials; |

| · | we may be unable to demonstrate to the satisfaction of the FDA or comparable foreign regulatory authorities that a product candidate is safe and effective for its proposed indication; |

| · | the designs of clinical trials might not be considered adequate, or the results of clinical trials may not meet the level of statistical significance required, by the FDA or comparable foreign regulatory authorities for approval; |

| · | we may be unable to demonstrate that a product candidate’s clinical and other benefits outweigh its safety risks; |

| · | the FDA or comparable foreign regulatory authorities may disagree with our interpretation of data from pre-clinical studies or clinical trials; |

| · | the data collected may not be sufficient to support the submission of a BLA or other submission, or to obtain regulatory approval in the United States, the EU or elsewhere; |

| · | the FDA or comparable foreign regulatory authorities may fail to approve the manufacturing processes or facilities of third-party manufacturers with which we contract for clinical and commercial supplies; and |

| · | the laws, regulations or policies of the FDA or comparable foreign regulatory authorities may significantly change in a manner rendering our clinical data or other regulatory submissions insufficient for approval. |

This lengthy approval process as well as the unpredictability of future clinical trial results may result in our failing to obtain regulatory approval to market any of our product candidates, which would significantly harm our business, results of operations and prospects. The FDA, the EMA and other regulatory authorities have substantial discretion in the approval process and determining when or whether regulatory approval will be obtained for any of our product candidates. Even if we believe the data collected from clinical trials of our product candidates are promising, such data may not be sufficient to support approval by the FDA, the EMA or any other regulatory authority.

In addition, even if we were to obtain approval, regulatory authorities may approve any of our product candidates for fewer or more limited indications than we request, may not approve the price we intend to charge for our products, may grant approval contingent on the performance of costly post-marketing clinical trials, or may approve a product candidate with a label that does not include the labeling claims necessary or desirable for the successful commercialization of that product candidate. Any of the foregoing scenarios could materially harm the commercial prospects for our product candidates.

In order to commercialize our products in more than one jurisdiction, we will require separate regulatory approval in each market and compliance with numerous and varying regulatory requirements. The approval procedures vary from country to country and may require additional testing or other steps. Satisfying these and other regulatory requirements is costly, time

23

Table of Contents

consuming, uncertain and subject to unanticipated delays. In addition, in many countries outside the United States and in particular in many of the Member States of the European Union, a product must undergo health economic assessments to agree on pricing and/or be approved for reimbursement before it can be approved for sale in that country, or before it becomes commercially viable. The FDA and the EMA may come to different conclusions regarding approval of a marketing application. Approval by the FDA or EMA does not ensure approval by regulatory authorities in other countries or jurisdictions, and approval by one foreign regulatory authority does not ensure approval by regulatory authorities in other foreign countries or by the FDA or EMA. In addition, our failure to obtain regulatory approval in any country may delay or have negative effects on the process for regulatory approval in other countries. Clinical trials conducted in one country may not be accepted by regulatory authorities in other countries. We may not obtain regulatory approvals on a timely basis, if at all. We may not be able to file for regulatory approvals and may not receive necessary approvals to commercialize our products in any market. We may be required to conduct additional pre-clinical studies or clinical trials, which would be costly and time consuming. If we or any future partner are unable to obtain regulatory approval for our product candidates in one or more significant jurisdictions, then the commercial opportunity for our product candidates, and our business, results of operations, financial condition and prospects, may be materially adversely affected.

The FDA may rescind the breakthrough designation for MOR208 in combination with lenalidomide for the treatment of patients with r/r DLBCL who are not eligible for high-dose chemotherapy and autologous stem cell transplantation and we may be unable to obtain breakthrough therapy designation for other indications. In addition, breakthrough therapy designation by the FDA may not lead to a faster development, regulatory review or approval process, and it may not increase the likelihood that MOR208 will receive marketing approval in the United States.