Form 424B3 CCC Intelligent Solution

Tweet

Tweet Share

Share

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-259142

PROSPECTUS

CCC INTELLIGENT SOLUTIONS HOLDINGS INC.

540,999,737 Shares of Common Stock

17,800,000 Warrants to Purchase Common Stock

This prospectus relates to: (1) the issuance by us of up to 17,800,000 shares of common stock, par value $0.0001 (“Common Stock”), that may be issued upon exercise of the Private Placement Warrants (as defined below) to purchase Common Stock at an exercise price of $11.50 per share of Common Stock; and (2) the offer and sale, from time to time, by the selling holders identified in this prospectus (the “Selling Holders”), or their permitted transferees, of (i) up to 540,999,737 shares of Common Stock (including 17,800,000 shares of Common Stock that may be issued upon exercise of the Private Placement Warrants) and (ii) up to 17,800,000 Private Placement Warrants.

This prospectus provides you with a general description of such securities and the general manner in which we and the Selling Holders may offer or sell the securities. More specific terms of any securities that we and the Selling Holders may offer or sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the securities being offered and the terms of the offering. The prospectus supplement may also add, update or change information contained in this prospectus.

We will not receive any proceeds from the sale of shares of Common Stock or Warrants by the Selling Holders pursuant to this prospectus or of the shares of Common Stock by us pursuant to this prospectus, except with respect to amounts received by us upon exercise of the Warrants to the extent such Warrants are exercised for cash. However, we will pay the expenses, other than underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus.

Our registration of the securities covered by this prospectus does not mean that either we or the Selling Holders will issue, offer or sell, as applicable, any of the securities. The Selling Holders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information about how the Selling Holders may sell the shares in the section entitled “Plan of Distribution.” In addition, certain of the securities being registered hereby are subject to vesting and/or transfer restrictions that may prevent the Selling Holders from offering or selling such securities upon the effectiveness of the registration statement of which this prospectus is a part. See “Description of Securities” for more information.

The Common Stock is listed on the New York Stock Exchange (the “NYSE”) under the symbol “CCCS.” On June 8, 2022, the last reported sales price of the Common Stock was $9.94 per share. The Public Warrants (as defined below) ceased trading on the New York Stock Exchange and were delisted, with the trading halt announced after close of market on December 28, 2021. Accordingly, the Public Warrants and the Forward Purchase Warrants (as defined below) have been exercised or redeemed in full and are no longer outstanding. We are an “emerging growth company” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. We are an “emerging growth company” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings.

See “Risk Factors” beginning on page 16 to read about factors you should consider before investing in shares of our Common Stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is June 9, 2022

| ii | ||||

| 1 | ||||

| 13 | ||||

| 16 | ||||

| 51 | ||||

| 52 | ||||

| 54 | ||||

| 61 | ||||

| 65 | ||||

| 70 | ||||

| 71 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

85 | |||

| 115 | ||||

| 125 | ||||

| 133 | ||||

| MATERIAL UNITED STATES FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS |

134 | |||

| 137 | ||||

| 142 | ||||

| 142 | ||||

| 142 | ||||

| F-1 |

i

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, the Selling Holders may, from time to time, sell or otherwise distribute the securities offered by them as described in the section titled “Plan of Distribution” in this prospectus. We will not receive any proceeds from the sale by such Selling Holders of the securities offered by them described in this prospectus. This prospectus also relates to the issuance by us of the shares of Common Stock issuable upon the exercise of any warrants. We will receive proceeds from any exercise of the warrants for cash.

Neither we nor the Selling Holders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Holders take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Holders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a prospectus supplement or post-effective amendment to the registration statement to add information to, or update or change information contained in, this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the sections of this prospectus entitled “Where You Can Find Additional Information.”

On July 30, 2021 (the “Closing Date”), Dragoneer Growth Opportunities Corp., a Cayman Islands exempted company and our predecessor company (“Dragoneer”), consummated the business combination (the “Business Combination”) pursuant to the terms of the Business Combination Agreement, dated as of February 2, 2021 (as amended on April 22, 2021 by Amendment No. 1 to the Business Combination Agreement and on July 6, 2021 by Amendment No. 2 to the Business Combination Agreement, the “Business Combination Agreement”), by and among Dragoneer, Chariot Opportunity Merger Sub, Inc., a Delaware corporation (“Chariot Merger Sub”), and Cypress Holdings, Inc., a Delaware corporation, and the other transactions contemplated by the Business Combination Agreement (together with the Business Combination, the “Transactions”).

Pursuant to the Business Combination Agreement, on the Closing Date, (i) Dragoneer changed its jurisdiction of incorporation by deregistering as a Cayman Islands exempted company and continuing and domesticating as a corporation incorporated under the laws of the State of Delaware (the “Domestication”), upon which Dragoneer changed its name to “CCC Intelligent Solutions Holdings Inc.” (“CCC” or the “Company”) and (ii) Chariot Merger Sub merged with and into CCC (the “Merger”), with CCC as the surviving company in the Merger and, after giving effect to such Merger, Cypress Holdings, Inc. becoming a wholly-owned subsidiary of CCC.

Unless the context otherwise requires, all references in this prospectus to “we,” “us” or “our” refer to (i) Cypress Holdings, Inc. prior to the consummation of the Business Combination and to (ii) CCC following the consummation of the Business Combination.

MARKET AND INDUSTRY DATA

CCC’s internal market and industry data and estimates are based upon information obtained from trade and business organizations and other contacts in the markets in which CCC operates and CCC management’s understanding of industry conditions. Although CCC believes that such information is reliable, CCC has not had this information verified by any independent sources. The estimates and market and industry information provided in this prospectus are subject to change based on various factors, including those described in the section entitled “Risk Factors—Risks Relating to Business and Industry” and elsewhere in this prospectus.

ii

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this registration statement may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

SELECTED DEFINITIONS

Unless otherwise stated in this prospectus or the context otherwise requires, references to:

“Advent Investor” are to, collectively, Cypress Investor Holdings, L.P., GPE VIII CCC Co-Investment (Delaware) Limited Partnership and Advent International GPE VIII-C Limited Partnership;

“Board” are to the board of directors of CCC Intelligent Solutions Holdings Inc.;

“Business Combination” are to the Domestication, the Merger and other transactions contemplated by the Business Combination Agreement, collectively, including the PIPE Financing;

“Business Combination Agreement” are to that certain Business Combination Agreement, dated February 2, 2021, by and among Dragoneer, Chariot Merger Sub and CCC, as amended on April 22, 2021 by Amendment No. 1 to the Business Combination Agreement and on July 6, 2021 by Amendment No. 2 to Business Combination Agreement, and as may be further amended, supplemented or otherwise modified from time to time;

“Bylaws” are to the Bylaws of CCC, effective as of July 30, 2021;

“Chariot Merger Sub” are to Chariot Opportunity Merger Sub, Inc., a Delaware corporation and wholly owned subsidiary of Dragoneer prior to the consummation of the Business Combination;

“CCC” are to Cypress Holdings, Inc., a Delaware corporation, prior to the consummation of the Business Combination and “CCC,” “we,” “us” or “our” are to CCC Intelligent Solutions Holdings Inc., a Delaware corporation, following the consummation of the Business Combination;

“CCC Earnout Shares” are to 15,000,000 shares of Common Stock (as adjusted for share subdivisions, share capitalizations, reorganizations, recapitalizations and the like) that CCC will issue following a CCC Triggering Event to the CCC Shareholders existing as of immediately prior to the Closing and (subject to continued employment) holders of vested and unvested equity awards of CCC as of the date of the Business Combination Agreement;

“CCC Shareholders” are the Advent Investor, the OH Investor, the TCV Investor and current and former management and other services providers of CCC holding shares of CCC;

“CCC Triggering Event” are to the earlier to occur of (a) the first date on which the shares of CCC have traded for greater than or equal to $15.00 per share for any twenty (20) trading days within any thirty (30) consecutive trading day period commencing after the Closing or (b) a Change of Control (as defined in the Business Combination Agreement) of Dragoneer, in each case if such event occurs within ten (10) years after the Closing;

“Certificate of Incorporation” are to the Certificate of Incorporation of CCC effective as of July 30, 2021;

iii

“Class A ordinary shares” are to the Class A ordinary shares, par value $0.0001 per share, of Dragoneer, which automatically converted, on a one-for-one basis, into shares of Common Stock in connection with the Domestication;

“Class B ordinary shares” are to the 17,250,000 Class B ordinary shares, par value $0.0001 per share, of Dragoneer that were initially issued to Dragoneer’s Sponsor in a private placement prior to the initial public offering of which 375,000 were transferred to the Dragoneer independent directors (75,000 each) in July 2020 and of which the remainder were transferred to an affiliate of Sponsor and to Affiliates of Willett Advisors prior to the Domestication, and, in connection with the Domestication, automatically converted, on a one-for-one basis, into shares of Common Stock;

“Closing” are to the closing of the Business Combination;

“Closing Date” are to July 30, 2021;

“Continental” are to Continental Stock Transfer & Trust Company;

“Domestication” are to the transfer by way of continuation and deregistration of Dragoneer from the Cayman Islands and the continuation and domestication of Dragoneer as a corporation incorporated in the State of Delaware;

“Dragoneer,” “we,” “us” or “our” are to Dragoneer Growth Opportunities Corp., a Cayman Islands exempted company, prior to the consummation of the Business Combination;

“earnout shares” are to, collectively, the CCC Earnout Shares and the Sponsor Earnout Shares;

“Effective Time” are to the time at which the Merger became effective;

“Employee Stock Purchase Plan” are to the CCC 2021 Employee Stock Purchase Plan;

“Forward Purchase Agreements” are to the forward purchase agreement between Dragoneer and Dragoneer Funding LLC, dated August 12, 2020, and the forward purchase agreement between Dragoneer and certain affiliates of Willett Advisors LLC, dated July 24, 2020, whereby Dragoneer Funding LLC and certain affiliates of Willett Advisors LLC purchased 15,000,000 and 2,500,000 forward purchase units, respectively;

“forward purchase units” are to the 17,500,000 forward purchase units issued immediately prior to the closing of the Business Combination initially to Dragoneer Funding LLC and certain affiliates of Willett Advisors LLC, each such unit consisting of one Class A ordinary share and one-fifth of one warrant to purchase Class A ordinary share for $11.50 per share, for a purchase price of $10.00 per unit;

“forward purchase warrants” are to the 3,500,000 redeemable warrants to purchase Class A ordinary shares of Dragoneer issued as part of the forward purchase units immediately prior to the Closing of the Business Combination. The forward purchase warrants have been redeemed in their entirety;

“Governing Documents” are to the Certificate of Incorporation and the Bylaws;

“initial public offering” are to Dragoneer’s initial public offering that was consummated on August 18, 2020;

“Incentive Equity Plan” are to the CCC 2021 Equity Incentive Plan;

iv

“Merger” are to the merger of Chariot Merger Sub with and into CCC pursuant to the Business Combination Agreement, with CCC as the surviving company in the Merger and, after giving effect to such Merger, CCC becoming a wholly owned subsidiary of Dragoneer;

“Common Stock” or “Common Stock” are to the common stock, par value $0.0001 per share, of CCC;

“NYSE” are to the New York Stock Exchange;

“OH Investor” are to OH Cypress Aggregator, L.P.;

“ordinary shares” are to our Class A ordinary shares and our Class B ordinary shares, prior to the consummation of the Business Combination;

“Permitted Recapitalization Dividend” are to one or more CCC dividends in an aggregate amount not to exceed $300,000,000;

“PIPE Financing” are to the transactions contemplated by the Subscription Agreements, pursuant to which the PIPE Investors collectively subscribed for an aggregate of 15,000,000 shares of Common Stock for an aggregate purchase price of $150,000,000 consummated in connection with Closing;

“private placement warrants” are to the 15,800,000 private placement warrants that were issued initially to the Sponsor as part of the closing of Dragoneer’s initial public offering, which are substantially identical to the public warrants sold as part of the units in the initial public offering, subject to certain limited exceptions;

“Proxy Statement/Prospectus” are to the definitive proxy statement/prospectus filed by Dragoneer with the SEC on July 6, 2021;

“public warrants” are to the 13,800,0000 redeemable warrants to purchase Class A ordinary shares of Dragoneer that were issued by Dragoneer in its initial public offering. The public warrants have been redeemed in their entirety;

“SEC” are to the Securities and Exchange Commission;

“Securities Act” are to the Securities Act of 1933, as amended;

“Sponsor” are to Dragoneer Growth Opportunities Holdings, a Cayman Islands limited liability company;

“Sponsor Earnout Shares” are to the 8,625,000 Class A ordinary shares (as adjusted for share subdivisions, share capitalizations, reorganizations, recapitalizations and the like) initially held by the Sponsor that, following conversion into shares of Common Stock pursuant to the Domestication, became subject to forfeiture if a Sponsor Triggering Event does not occur within ten (10) years after the Closing;

“Sponsor Triggering Event” are to the earlier to occur of (a) the first date on which the shares of CCC have traded for greater than or equal to $13.00 per share for any twenty (20) trading days within any thirty (30) consecutive trading day period commencing after the Closing or (b) a Change of Control (as defined in the Business Combination Agreement) of Dragoneer, in each case if such event occurs within ten (10) years after the Closing;

“Subscription Agreements” are to the subscription agreements, entered into by Dragoneer and each of the PIPE Investors in connection with the PIPE Financing;

“TCV Investor” are to TCV IX, L.P., TCV IX (A), L.P., TCV IX (B), L.P. and TCV Member Fund, L.P.;

“transfer agent” are to Continental, our transfer agent;

v

“units” are to the units of Dragoneer, each unit representing one Class A ordinary share and one-fifth of one warrant to acquire one Class A ordinary share, that were offered and sold by Dragoneer in its initial public offering and in its concurrent private placement;

“warrants” are to the private placement warrants and the working capital warrants; and

“working capital warrants” are to the 2,000,000 warrants to purchase Class A ordinary shares that were issued to Sponsor upon conversion of the principal amount of a working capital loan provided to Dragoneer by Sponsor, which conversion occurred upon the consummation of the Business Combination.

vi

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this prospectus may constitute “forward-looking statements” for purposes of the federal securities laws. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, including those relating to the Business Combination. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, including those relating to the future financial performance and business strategies and expectations for our business. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “will,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements may include information concerning our possible or assumed future results of operations, client demand, business strategies, technology developments, financing and investment plans, competitive position, our industry and regulatory environment, potential growth opportunities and the effects of competition.

Important factors that could cause actual results to differ materially from our expectations include:

| • | our revenues, the concentration of our customers and the ability to retain our current customers; |

| • | our ability to negotiate with our customers on favorable terms; |

| • | our ability to maintain and grow our brand and reputation cost-effectively; |

| • | the execution of our growth strategy; |

| • | our projected financial information, growth rate and market opportunity; |

| • | the health of our industry, claim volumes, and market conditions; |

| • | changes in the insurance and automotive collision industries, including the adoption of new technologies; |

| • | global economic conditions and geopolitical events; |

| • | competition in our market and our ability to retain and grow market share; |

| • | our ability to develop, introduce and market new enhanced versions of our solutions and products; |

| • | our sales and implementation cycles; |

| • | the ability of our research and development efforts to create significant new revenue streams; |

| • | changes in applicable laws or regulations; |

| • | changes in international economic, political, social and governmental conditions and policies, including corruption risks in China and other countries; |

| • | currency fluctuations; |

| • | our reliance on third-party data, technology and intellectual property; |

| • | our ability to protect our intellectual property; |

| • | our ability to keep our data and information systems secure from data security breaches; |

| • | our ability to acquire or invest in companies or pursue business partnerships, which may divert our management’s attention or result in dilution to our stockholders, and we may be unable to integrate acquired businesses and technologies successfully or achieve the expected benefits of such acquisitions, investments or partnership; |

vii

| • | our ability to raise financing in the future and improve our capital structure; |

| • | our success in retaining or recruiting, or changes required in, our officers, key employees or directors; |

| • | our officers and directors allocating their time to other businesses and potentially having conflicts of interest with our business; |

| • | our estimates regarding expenses, future revenue, capital requirements and needs for additional financing; |

| • | our financial performance; |

| • | our ability to expand or maintain its existing customer base; and |

| • | our ability to service our indebtedness. |

The forward-looking statements contained in this prospectus are based on current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described above and under the heading “Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. It is not possible to predict or identify all such risks. We do not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

viii

Non-GAAP Financial Measures

The presentation of non-GAAP financial measures is used to enhance our investors’ and lenders’ understanding of certain aspects of our financial performance. This discussion is not meant to be considered in isolation, superior to, or as a substitute for the directly comparable financial measures prepared in accordance with U.S. GAAP. Management also uses supplemental non-GAAP financial measures to manage and evaluate the business, make planning decisions, allocate resources and as performance measures for Company-wide bonus plans and executive compensation plans. These key financial measures provide an additional view of our operational performance over the long-term and provide useful information that we use in order to maintain and grow our business.

In addition to our results determined in accordance with U.S. GAAP, we believe that Adjusted Gross Margin, and EBITDA and Adjusted EBITDA, which are each non-GAAP measures, are useful in evaluating our operational performance. We use this non-GAAP financial information to evaluate our ongoing operations and for internal planning, budgeting and forecasting purposes and, starting in 2021, for setting management bonus programs. We believe that non-GAAP financial information, when taken collectively, may be helpful to investors in assessing our operating performance and comparing our performance with competitors and other comparable companies, which may present similar non-GAAP financial measures to investors. Our computation of these non-GAAP measures may not be comparable to other similarly titled measures computed by other companies, because all companies may not calculate these measures in the same fashion. We endeavor to compensate for the limitation of the non-GAAP measure presented by also providing the most directly comparable GAAP measure and a description of the reconciling items and adjustments to derive the non-GAAP measure. These non-GAAP measures should be considered in addition to results prepared in accordance with GAAP, but should not be considered in isolation or as a substitute for performance measures calculated in accordance with GAAP. We compensate for these limitations by relying primarily on our GAAP results and using non-GAAP measures on a supplemental basis.

Adjusted Gross Margin

We believe that Adjusted Gross Margin, as defined below, provides meaningful supplemental information regarding our performance by excluding certain items that may not be indicative of our recurring core business operating results. Adjusted Gross Margin is defined as gross margin, adjusted for gross margin associated with First Party Clinical Services, which was divested as of December 31, 2020, amortization and impairment of acquired technologies, and stock-based compensation, which are not indicative of our recurring core business operating results. The Adjusted Gross Margin percentage is defined as Adjusted Gross Margin divided by Revenue, less First Party Clinical Services divested revenue. Gross margin is the most directly comparable GAAP measure to Adjusted Gross Margin, and you should review the reconciliation of Gross Margin to Adjusted Gross Margin below and not rely on any single financial measure to evaluate our business.

EBITDA and Adjusted EBITDA

We believe that EBITDA and Adjusted EBITDA, as defined below, are useful in evaluating our operational performance distinct and apart from financing costs, certain expenses and non-operational expenses. EBITDA is defined as net income (loss) adjusted for interest, taxes, depreciation and amortization. Adjusted EBITDA is EBITDA adjusted for asset impairment charges, gain/loss on change in fair value of interest rate swaps, stock-based compensation expense, loss on early extinguishment of debt, business combination transaction costs, lease abandonment charges, lease overlap costs for the incremental expenses associated with the Company’s new corporate headquarters prior to termination of its existing headquarters’ lease, net costs related to divestiture and less revenue and related cost of revenue associated with First Party Clinical Services, which was divested as of December 31, 2020. Net loss is the most directly comparable GAAP measure to Adjusted EBITDA, and you should review the reconciliation of net loss to adjusted EBITDA below and not rely on any single financial measure to evaluate our business.

EBITDA and Adjusted EBITDA are intended as supplemental measures of our performance that are neither required by, nor presented in accordance with, GAAP. You should be aware that when evaluating EBITDA and Adjusted EBITDA, we may incur future expenses similar to those excluded when calculating these measures. In addition, our presentation of these measures should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items.

1

This summary highlights selected information contained elsewhere in this prospectus. It does not contain all of the information that may be important to you and your investment decision. Before investing in the Common Stock, you should carefully read this entire prospectus, including the matters set forth under the sections of this prospectus captioned “Cautionary Note Regarding Forward Looking Statements,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” “and our consolidated financial statements and our condensed consolidated interim financial statements and related notes included elsewhere in this prospectus. The definition of some of the terms used in this prospectus are set forth under “Selected Definitions.”

Founded in 1980, CCC is a leading provider of innovative cloud, mobile, AI, telematics, hyperscale technologies and applications for the property and casualty (“P&C”) insurance economy. Our SaaS platform connects trading partners, facilitates commerce, and supports mission-critical, AI-enabled digital workflows. Leveraging decades of deep domain experience, our industry-leading platform processes more than $100 billion in annual transaction value across this ecosystem, digitizing workflows and connecting more than 30,000 companies across the P&C insurance economy, including insurance carriers, collision repairers, parts suppliers, automotive manufacturers, financial institutions and others.

Our business has been built upon two foundational pillars: automotive insurance claims and automotive collision repair. For decades we have delivered leading software solutions to both the insurance and repair industries, including pioneering Direct Repair Programs (“DRP”) in the United States (“U.S.”) beginning in 1992. Direct Repair Programs connect auto insurers and collision repair shops to create business value for both parties, and require digital tools to facilitate interactions and manage partner programs. Insurer-to-shop DRP connections have created a strong network effect for CCC’s platform, as insurers and repairers both benefit by joining the largest network to maximize opportunities. This has led to a virtuous cycle in which more insurers on the platform drives more value for the collision shops on the platform, and vice versa.

We believe we have become a leading insurance and repair SaaS provider in the U.S. by increasing the depth and breadth of our SaaS offerings over many years. Our insurance solutions help insurance carriers manage mission-critical workflows across the claims lifecycle, while building smart, dynamic experiences for their own customers. Our software integrates seamlessly with both legacy and modern systems alike and enables insurers to rapidly innovate on our platform. Our repair solutions help collision repair facilities achieve better performance throughout the collision repair cycle by digitizing processes to drive business growth, streamline operations, and improve repair quality. We have more than 300 insurers on our network, connecting with over 27,000 repair facilities through our multi-tenant cloud platform. We believe our software is the architectural backbone of insurance DRP programs and is the primary driver of material revenue for our collision shop customers and a source of material efficiencies for our insurance carrier customers.

Our platform is designed to solve the “many-to-many” problem faced by the insurance economy. There are numerous internally and externally developed insurance software solutions in the market today, with the vast majority of applications focused on insurance-only use cases and not on serving the broader insurance ecosystem. We have prioritized building a leading network around our automotive insurance and collision repair pillars to further digitize interactions and maximize value for our customers. We have tens of thousands of companies on our platform that participate in the insurance economy, including insurers, repairers, parts suppliers, automotive manufacturers, and financial institutions. Our solutions create value for each of these parties by enabling them to connect to our vast network to collaborate with other companies, streamline operations, and reduce processing costs and dollars lost through claims management inefficiencies, or claims leakage. Expanding our platform has added new layers of network effects, further accelerating the adoption of our software solutions.

1

We have processed more than $1 trillion of historical data across our network, allowing us to build proprietary data assets that leverage insurance claims, vehicle repair, automotive parts and other vehicle-specific information. We believe we are uniquely positioned to provide data-driven insights, analytics, and AI-enhanced workflows that strengthen our solutions and improve business outcomes for our customers. Our Smart Suite of AI solutions increases automation across existing insurance and repair processes including vehicle damage detection, claim triage, repair estimating, and intelligent claims review. We deliver real-world AI with more than 95 U.S. auto insurers actively using AI-powered solutions in production environments. We have processed more than 9 million unique claims using CCC deep learning AI as of December 31, 2021, an increase of more than 80 percent over December 31, 2020.

One of the primary obstacles facing the P&C insurance economy is increasing complexity. Complexity in the P&C insurance economy is driven by technological advancements, Internet of Things (“IoT”) data, new business models, and changing customer expectations. We believe digitization plays a critical role in managing this growing complexity while meeting customer expectations. Our technology investments are focused on digitizing complex processes and interactions across our ecosystem, and we believe we are well positioned to power the P&C insurance economy of the future with our data, network, and platform.

While our position in the P&C insurance economy is grounded in the automotive insurance sector, the largest insurance sector in the U.S. representing nearly half of Direct Written Premiums (“DWP”), we believe our integrations and cloud platform are capable of driving innovation across the entire P&C insurance economy. Our customers are increasingly looking for CCC to expand its solutions to other parts of their business where they can benefit from our technology, service, and partnership. In response, we are investing in new solutions that we believe will enable us to digitize the entire automotive claims lifecycle, and over time expand into adjacencies including other insurance lines.

We have strong customer relationships in the end-markets we serve, and these relationships are a key component of our success given the long-term nature of our contracts and the interconnectedness of our network. We have customer agreements with more than 300 insurers (including carriers, self-insurers and other entities processing insurance claims), including 18 of the top 20 automotive insurance carriers in the U.S., based on DWP, and hundreds of regional carriers. We have more than 30,000 total customers, including over 27,000 automotive collision repair facilities (including repairers and other entities that estimate damaged vehicles), thousands of automotive dealers, 13 of the top 15 automotive manufacturers, based on new vehicle sales, and numerous other companies that participate in the P&C insurance economy.

We generate revenue through the sale of software subscriptions and other revenue, primarily from professional services. We generated $688.3 million of revenue for the year ended December 31, 2021, an increase of 9% from the prior year which included $34.7 million attributable to the portion of our casualty solution (specifically, the First Party Clinical Services) divested in fiscal year 2020. The divestiture of First Party Clinical Services had a (6%) impact on total revenue growth. Net loss for the year ended December 31, 2021 was $248.9 million, compared to a net loss for the year ended December 31, 2020 of $16.9 million, mainly due to $209.9 million of stock based compensation expense recognized in conjunction with the Business Combination. Adjusted EBITDA increased 28.9% year over year to $261.4 million.

P&C Insurance Economy

P&C insurance is one of the largest global industries. The U.S. P&C insurance industry alone serviced approximately $650 billion in DWP in 2020. Insurance is a necessity for the majority of businesses and consumers, and, as a result, the P&C insurance industry has seen steady long-term growth.

2

P&C insurers face a number of challenging market dynamics in today’s environment, including increasing customer expectations, competition from new entrants and business models, emerging technologies, retaining and attracting talent, and cost pressures. Insurers are often reliant on legacy on-premise systems to assist with policy and claims adjustments and processing, which can be inflexible and costly to maintain, challenging their ability to innovate and respond to market dynamics.

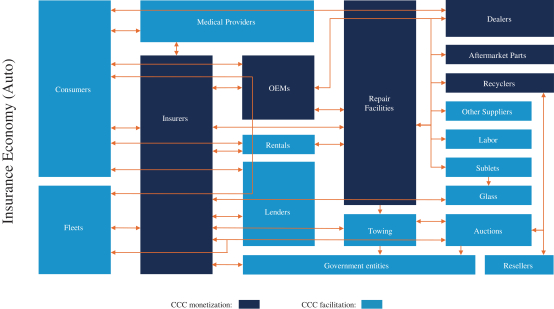

Further complicating matters, the P&C insurance industry is dependent on the P&C insurance economy, an interconnected economy of industries that interact to service, underwrite, finance, and repair insured assets. Insurance carriers invest in data, systems, services and partnerships to manage the many required collaboration points across these industries. To deliver end-to-end digital workflows and customer experiences, technology needs to extend beyond insurance organizations and include its supporting economy, in order to enable the many interactions and handoffs required to process insurance events.

In the automotive insurance sector, which represents nearly half of the U.S. P&C insurance industry, processing a single event, such as a claim, can require hundreds of micro-transactions across its supporting economy, involving consumers, lenders, collision repair facilities, automotive manufacturers, dealers, parts suppliers, medical providers, vehicle auctions, and others. These transactions depend on extensive hyper-local decisions and data, creating a level of complexity that can increase processing costs as well as the potential for fraud and other forms of claims leakage. For automotive claims, the end result is more than one billion days of cumulative claims cycle time (loss date to claim completion date) in the U.S. each year. For our insurance partners, cycle time is costly, which is one reason why, as of 2021, CCC’s platform is relied upon by 18 of the top 20 auto insurers based on DWP in the U.S. to digitize complexity and improve business outcomes.

The complexity seen in one auto claim grows exponentially more difficult to manage at scale, and complexity is continuing to increase across the P&C insurance economy. In the automotive sector, this is due to several converging factors including, without limitation:

| • | Vehicle parts proliferation: Repairable parts per auto claim have increased 48% since 2010 |

| • | Internal technology systems: An average new vehicle uses more than 100 million lines of code |

3

| • | Growing connected car capabilities: 86% of new vehicles to be sold in 2022 are forecasted to have embedded cellular connectivity |

| • | Transportation as a Service (“TaaS”) and other new business models: More than 40 million rides are shared per month in the U.S. |

| • | Advanced Driver Assistance Systems (“ADAS”) and diagnostics systems: The number of vehicles receiving a diagnostic scan as part of a collision repair has increased 1,000% since 2017 |

| • | Vehicle Electrification and related infrastructure: Recent OEM announcements translate to estimated cumulative electric light-duty-vehicle sales of 55-72 million by 2025 |

We believe the only way to effectively manage increasing complexity is through digitization. Since our inception over forty years ago, we have focused our technology on what we believe to be our customers’ most complex problems. We have digitized total loss valuations, repair estimates, DRP programs, shop management functions, repair workflows, medical claims, parts ordering, and much more. In the process, we have built integrations and facilitated partnerships that enable information sharing across our vast network of customer companies. Our solutions are well-suited for the next wave of complexity, and we believe these trends will continue to accelerate adoption of CCC’s platform and applications.

Our Approach

Serving as the platform for the P&C insurance economy is a significant challenge that CCC is uniquely positioned to address. We believe our proprietary data and network assets, combined with our track record of innovation on our cloud platform, differentiates us from other potential P&C platform companies. Our approach is to continue to innovate and expand our solutions to create value for the P&C insurance economy.

CCC’s foundation for innovation is built upon decades of data and extensive network assets. We have deep proprietary data assets and more than $1 trillion of historical data, enabling us to provide insights, analytics, and AI-driven workflows. Our leading network was built company by company, and spans the P&C insurance economy, giving us the ability to deploy cross-market solutions and create seamless customer experiences. We believe our data and network assets are highly differentiated and very difficult to replicate.

Our innovative cloud-based applications provide the P&C insurance economy with the capabilities required to manage their businesses, optimize decision making, and digitize intricate workflows. We have a proven Research & Development (R&D) engine with a strong track record of software innovation and deployment on our cloud platform. CCC’s innovations are helping to deliver on the industry’s vision of achieving Straight-Through Processing (STP)—processing claims digitally with limited to no human intervention. In the third quarter of 2021, CCC launched CCC Estimate—STP, the industry’s first estimating experience capable of delivering touchless line level estimate detail in minutes. By combining artificial intelligence, insurer driven rules and a connected ecosystem, Estimate—STP is designed to revolutionize the estimating experience for insurers and policyholders. CCC Estimate—STP has already been deployed in-market with eight insurance carriers.

We believe our ability to rapidly innovate and deploy new software solutions via our cloud technology platform, along with our depth of data and leading network, sets us apart from the competition. The key benefits we deliver for our customers include:

| • | Multi-tenant cloud platform enabling flexibility and innovation: CCC’s platform operates in a secure multi-tenant cloud environment, with over 520,000 registered users and 3.5 billion database transactions processed per day. Our platform enables us to innovate in response to new market trends and customer needs and rapidly deploy new solutions to our more than 30,000 customers. We |

4

| continuously enhance existing solutions and bring new solutions to market, deploying more than 1,700 software releases in 2021. |

| • | Deep domain expertise: With decades of experience serving the insurance economy, we have developed a deep understanding of the industries and ecosystem we serve. Our domain expertise enables us to offer tailored solutions to help our customers achieve their business objectives. We understand the importance of the role we play as the independent party facilitating interactions across various ecosystem participants, and as a result, we have developed deep and trusting relationships with our customers. We are well positioned to enable cross-market programs and partnerships and have a decades-long history playing this role. Our business is led by a deep and experienced management team with a customer-centric mindset. |

| • | Long-term customer relationships: Over several decades we have developed strong relationships with leading insurers, collisions repair groups, and automotive manufacturers, among others. Our company-wide Net Promoter Score is 80, which underscores the customer-centric focus that defines our organization including our sales, marketing, product, technology, and operations teams. We are a trusted partner to our clients, which allows us to collaborate and adapt our business based on customer feedback and changing expectations to stay ahead of our competition. |

| • | Network access: CCC’s cloud platform is used by more than 30,000 companies, including insurers, repairers, automotive manufacturers, parts suppliers, financial institutions, and others. Integrating to CCC’s platform unlocks real-time cloud connections across our ecosystem, enabling customers to digitize workflows that are otherwise cumbersome and costly. Our network processes more than 400 million interface transactions each year where information is passed from one network participant to another; for example, from an insurer to a repair facility. |

| • | Proven R&D engine: We invest heavily in R&D efforts and are committed to delivering market-leading technology for the P&C insurance economy. In recent years, our innovation efforts have focused on Mobile and AI technology, and we have released several new solutions incorporating Mobile and AI that have experienced rapid industry adoption as our customers look to improve customer experience and enable automation. We deploy real-world AI solutions at enterprise scale. Our AI solutions combine our data assets with proprietary machine learning and analytics frameworks to automate processes so as to reduce processing costs and leakage for our customer base. Today, CCC has developed more than 300 AI models, some of which are in use across more than 95 insurers, including 18 of the top 20 U.S. automotive insurers in 2021 based on DWP. |

| • | Proprietary data assets: CCC’s platform has processed more than $1 trillion of historical data, enabling us to deliver unique analytics and insights for our customers leveraging our deep proprietary data assets. Our platform allows customers to make optimal decisions by incorporating event-specific factors, local geographic factors, and historical data. Database solutions and corresponding rules engines can be configured and adjusted in real-time based on business needs and market trends. |

| • | Enterprise scale and support: We process more than $100 billion of transactions annually for our more than 30,000 customers, delivering mission-critical SaaS solutions that our customers can count on. Since January 2018, CCC’s systems have achieved 99.94% uptime on average, giving our customers the confidence to depend on CCC’s performance. We have dedicated implementation and training teams, and have proven success in implementing solutions for leading insurance carriers and thousands of small businesses. |

5

Our Growth Strategy

We intend to extend our position as the leading provider of SaaS solutions for the P&C insurance economy. The key components of our strategy are:

| • | Growing our customer base: Our customers span the P&C insurance economy, and we believe we have significant opportunity to continue to grow our customer base by targeting key new accounts and expanding our sales and marketing capabilities. We believe there is ample opportunity to add new customers within the U.S., where our business is most established. |

| • | Deepening relationships with existing customers: We seek to grow our revenue base with existing customers primarily by selling additional software subscriptions. We regularly launch new solutions and have a proven track record of cross-selling software across our customer segments, as well as up-selling customers based on package and feature upgrades. We intend to build upon strong customer relationships and access to key customer decision makers to increase software adoption and usage. |

| • | Expanding the breadth of our solutions: Our long-term focus is to digitize all P&C insurance economy workflows, targeting processing costs and leakage. In 2021, our R&D spend was 24% of revenue; however, including the impact of capitalized time related to internal use software, our total spend was 27% of revenue on R&D with a primary focus on technology leadership and continuous innovation. In 2021 we launched offerings that expanded the breadth and depth of our solutions across a number of areas, including Estimate – STP for insurance, Estimating-IQ for repair, Enterprise Payments, and more. |

| • | Broadening our network ecosystem: We have a large network of companies on our platform that are dependent on the P&C insurance economy and derive value from connecting to others across the ecosystem through CCC. The breadth and depth of our platform creates network effects that accelerate the demand for our software solutions. We intend to extend our network of companies to enhance our value proposition and create new market growth opportunities. |

| • | Growing our geographic footprint: We believe there is significant opportunity for our solutions outside of the U.S. For example, in China we have built an early leadership position with four of the top five insurance carriers and are positioning ourselves to establish an ecosystem that is similar to ours in the U.S. We believe similar opportunities exist in other markets across the world which we intend to pursue over time. |

| • | Pursuing acquisitions: We have acquired and integrated numerous businesses throughout CCC’s history. We intend to continue to pursue targeted acquisition opportunities to accelerate our business strategy and growth through solution, market, or geographic expansion. |

6

Our Solutions

We provide an integrated suite of software applications built on our cloud platform to serve the P&C insurance economy, including insurance, repair, and other end-markets. Our SaaS solutions are sold individually, bundled, or in packages, depending on the specific solution and end-market.

CCC Insurance Solutions

CCC’s solutions help insurers digitize processes, from customer intake to claims, while building smart, dynamic experiences for their customers. Many of our solutions leverage the power of the CCC network by facilitating ecosystem interactions required to complete insurer processes. All of our insurance solutions are cloud-based SaaS solutions that power critical carrier workflows. Our insurance solutions represent approximately 52% of our 2021 total revenues, with 94% of that representing software revenue and 6% representing other revenue. Our key insurance solutions include:

| • | CCC Workflow: Our suite of workflow tools supports end-to-end digital insurance workflows, from customer intake to claim resolution. Our solutions enable mobile experiences, modern communications, configurable workflows, and network integrations, all while empowering insurers to seamlessly customize and configure solutions to meet unique business needs. Mobile modules provide a digital channel for communicating with the modern consumer, starting with vehicle documentation when a new insurance policy is created. Our solutions support critical claims processes, including claims documentation, photo capture, repair scheduling, and two-way text communications. Our workflow solutions leverage a sophisticated rules engine to customize routing for escalations, review, and approval processes. Our network management capability powers insurance DRPs, enabling |

7

| insurers to seamlessly connect and collaborate with repair facilities and other companies to provide accurate and timely information about a claim flow from the right party at the right time. |

| • | CCC Estimating: Our insurance automotive repair estimating solution is built on CCC’s proprietary estimating database that has been cultivated for decades to deliver best-in-class repair estimating data and decisioning. CCC estimating innovations have enabled virtual inspections using consumer photos, integrated to CCC’s portal. Estimates are further automated by AI that combines machine learning and estimating logic to predict repair requirements, suggest estimate lines, and generate fast baseline estimates. Our Estimate – STP solution takes estimate automation to the next level by combining AI, digital workflows, data, and partner connections to automatically initiate and populate detailed estimates within seconds. The outcome is actionable estimates with line-level detail, including parts, labor operations and hours, and taxes. Our estimating solutions accelerate auto physical damage estimation to reduce costs and cycle time for our customers. |

| • | CCC Total Loss: Total loss solutions enable our insurance customers to identify, value, and resolve total loss automotive claims digitally. We deliver valuations representing a vehicle’s fair market value based on CCC’s market-driven valuation methodology and provide insurers with information to make total loss determinations. Once a total loss has been identified, we support our carrier customers in managing lender payoff requests, letters of guarantee, lien and title resolution, and signature collection. Throughout the process, our mobile solutions deliver a seamless customer experience integrated into CCC’s holistic workflow suite. |

| • | CCC AI and Analytics: We inject AI and Analytics throughout CCC’s software offerings to accelerate decision-making and improve outcomes. We have numerous AI solutions in production with leading insurers and are continuing to invest to improve our AI and launch new AI-enabled solutions. All of our core software offerings are supported by Analytics solutions that allow our customers to benchmark and manage their business performance across key performance indicators. |

| • | CCC Casualty: Personal injuries resulting from automotive accidents lead to casualty claims, which require insurers to process medical bills and demand packages for first and third-party claims, respectively. Our casualty solutions automate and expedite casualty claims processing by applying intelligent rules engines based on insurer-specific parameters to process casualty claims data quickly and segment payment-ready bills from those that the insurer wants to review. Our tools and services modernize a manual, paper-burdened system with a comprehensive, configurable experience to help insurers make timely, consistent payments across bill types, and provide analytics dashboards to visualize trends and industry benchmarks. |

CCC Repair Solutions

CCC’s solutions help automotive collision repairers achieve better shop performance, from lead generation through repair completion and payment. Our platform improves every stage and level of the collision repair cycle, combining key business operations into one solution to drive more business, improve repair quality, simplify operations, and exceed customer expectations for our collision facility customers. Collision repairers use our platform to connect with the industry’s leading network of partners and suppliers across the insurance and repair ecosystem. Our repair solutions represented approximately 42% of our 2021 total revenues, with 99% of that representing software revenue and 1% representing other revenue. Our key repair solutions include:

| • | CCC Estimating: Our collision repair estimating solution is built on CCC’s proprietary database that enables repair estimate creation while connecting repairers to real-time parts pricing and availability, Original Equipment Manufacturer (“OEM”) repair procedures, and insurer guidelines. Repairers can capture photos and repair information at the vehicle with CCC’s Estimating mobile application and collaborate on repair estimates digitally with insurance partners. Users have access to our network of |

8

| insurers and their corresponding requirements, which can accelerate estimate reviews and supplemental requests. Our Estimating-IQ upgrade incorporates AI into the repair estimating application to provide repairers with a jump start on estimating by applying machine learning to prepopulate estimates with parts and labor operations based on photos of vehicle damage and individual repair facility configurations. Our estimating solutions help reduce errors and improve cycle time for collision repairers and their partners. |

| • | CCC Network Management: We provide software solutions that power collaboration between repairers and insurers. Our technology facilitates the majority of the automotive insurance DRP in the U.S. Participating repairers benefit from our connected technology platform that allows them to receive repair assignments and collaborate with partner insurers throughout the repair process, delivering on program metrics that drive their business. We also provide tools that allow repair Multi Store Owners (“MSOs”) to manage performance, metrics, and compliance across their repair shop network. |

| • | CCC Repair Workflow: Repair workflow is the industry’s leading repair management tool that accelerates productivity and simplifies operations for thousands of repair facilities. Repairers can schedule and track vehicle repair status, assign tasks, and manage productivity across their operation. Configurable dashboards provide visibility into performance. Repairers can also streamline repair management leveraging CCC’s real-time parts ordering platform, selecting parts from multiple vendors through a single cart and invoice. Customer-to-shop payments are integrated as well, automatically storing payment records and simplifying reconciliation. |

| • | CCC Repair Quality: We provide advanced solutions to help repairers deliver quality repairs. Our repair procedures provide technicians with a single source for data-driven insights to assist them in conducting thorough, consistent repairs, reducing the need for multiple subscriptions and enabling access to current OEM guidelines and processes. Our checklist solutions enable documentation of standard operating procedures and tracking of performance which allows shop managers to identify areas for improvement. CCC’s diagnostics solutions simplify scan initiation and reporting with integrated functionality for all scan types (OEM Direct, Technician Assisted, or Aftermarket), which saves repairers time on pre, post, and calibration scans. |

CCC Other Ecosystem Solutions

CCC’s solutions support other segments of the insurance ecosystem, including parts suppliers, automotive manufacturers, and financial institutions. These solutions extend the CCC network and create value for companies connecting to our platform to improve business outcomes. Other ecosystem solutions represent approximately 5% of our 2021 total revenue, with 91% of that representing software revenue and 9% representing other revenue. Some of CCC’s other ecosystem solutions include:

| • | CCC Parts Solutions: Our parts platform allows automotive parts wholesale dealers, aftermarket parts suppliers, and parts recyclers to make their inventory available to our collision repair and insurance networks in real-time. Using this platform, participating customers are able to use our platform to give their parts maximum visibility at the moment when repairers are using CCC software to write their repair estimates. This enables parts providers to display their parts inventory and promotional pricing, while automating order processing, invoicing, and settlement. |

| • | CCC Automotive Manufacturer Solutions: We offer a range of automotive manufacturer solutions that give access to our network, enable repair quality, and leverage telematics vehicle data to create valuable efficiencies across insurance and repair workflows. We provide network management tools to automotive manufacturers including network dashboards, that deliver detailed metrics on certified repair shop network performance and inform data-driven decisions. We enable the integration of up-to-date OEM repair methods and diagnostics trouble codes into our platform to give our network of |

9

| repair facilities and technicians the tools to execute a proper repair. Our automotive telematics solutions enable new use cases across CCC’s integrated ecosystem, including connected safety and vehicle diagnostics solutions. Our telematics solutions integrate vehicle telemetry data, such as driving data, accident data, and diagnostics trouble codes, into existing insurance and repair workflows, expediting decisions and reducing cycle time across our ecosystem. Auto manufacturers also benefit from CCC Parts and Lender solutions, across their parts and financing businesses, respectively. |

| • | CCC Lender Solutions: Our lender portal integrates into CCC’s insurance solutions, enabling financial institutions with automotive loans to optimize vehicle total loss processes. Auto lenders connect with participating insurers to receive earlier notice of loss, digitally exchange documents, and quickly settle existing loans while minimizing the likelihood of missed customer payments. This improves customer experience, boosts productivity, and reduces cycle time. |

| • | CCC Payments: Our enterprise payments platform, launched in the third quarter of 2021, enables electronic payment flows via a third-party payment processing partner for companies across the P&C insurance economy. CCC payments functionality is designed to integrate into existing CCC applications, presenting payment information within existing workflows. The solution is initially focused on insurer outbound B2B payments, where it enables payments across P&C lines. Recipients of payments only need to enter their payment information once to have it seamlessly deployed across the CCC network, making it easy to activate electronic payments at scale. Our payments platform reduces administrative costs and cycle time while improving customer satisfaction. |

CCC International Solutions

CCC provides insurance claims software in China, with four of the top five automotive insurers in China using our platform. Our software solutions are tailored for the Chinese market, and include workflow, estimating, audit and analytics solutions. We are expanding our software solutions in China to the automotive repair market, where we are building momentum with repair facilities and automotive dealers. We are assessing other international market expansion opportunities by evaluating partnerships and acquisitions of strategic assets. Our international solutions represent approximately 1% of our 2021 total revenue, with 100% of that representing software revenue.

Our Technology

CCC has been a technology leader in the P&C insurance economy for several decades and has a strong track record of innovation. We were one of the leaders in the transition to cloud services, launching our initial CCC cloud capabilities beginning in 2003. Today, our solutions are powered by our secure multi-tenant cloud. Our cloud architecture creates several benefits for our customers and partners across the P&C insurance economy, including:

| • | Ease of implementation: We are able to implement solutions rapidly and cost-effectively, with average customer implementations taking less than three months. Implementations are performed by CCC’s service operations and training teams, and rarely require the support of external consultants. We utilize an Application Programming Interface (“API”) framework to integrate to our customers’ existing systems, enabling CCC’s solutions to perform high-value workflows without disrupting existing business processes. |

| • | Flexibility: Our solutions are highly flexible, enabling customers to deploy our software in various ways to meet their needs. For example, our insurer mobile services can be integrated into customer applications via Software Development Kits (“SDK”), deployed via HTML5, or enabled by API calls. In addition, customers can configure and adjust rules based on business outcomes, which can be deployed in real-time via the CCC cloud. For example, our configurable carrier workflow allows |

10

| insurers to design custom workflows that create differentiated experiences and adjust parameters to deliver targeted results. |

| • | Innovation: We invest heavily in R&D and continuously bring new innovative solutions to market. For existing customers with integrations to CCC’s platform, new solutions can be deployed into production environments as soon as configuration and training is complete, enabling our customers to keep up with rapidly changing industry trends and customer expectations. We continuously update and enhance our software, deploying more than 1,700 releases in 2021, with a software release quality success rate averaging more than 96% since 2018. |

| • | Security and Quality: CCC’s software suite is provided as SaaS hosted in multiple geographically diverse hosting locations, with data replication between primary hosting locations and secondary locations in near real-time. CCC protects its services through a series of complex security controls and services, including but not limited to privileged access controls, malware detection and prevention controls, secure application development controls, controls for data at rest, and in transmission, external threat and prevention testing, benchmarking and 24x7 Security Operations Center (“SOC”) monitoring. |

| • | Availability and Uptime: CCC’s application environment is designed for high availability utilizing redundant databases, servers, network components, and storage, which maximizes availability through a network architecture designed to compartmentalize web, application, and database layers. Since 2018, CCC system availability has been 99.94% while meeting CCC’s customer service performance and processing commitments. |

Our technology infrastructure offers proven performance at enterprise scale and is designed to support the future needs of our industry as data continues to proliferate. As of year-end 2021, we process more than 90 terabytes of network traffic and execute nearly 3.5 billion database transactions each day. We have invested in hyperscale infrastructure, enabling us to effectively process and store extremely large amounts of information, photos, videos, and driving data. For example, we receive, process, and store more than 500 million photos each year.

Our application layer delivers solutions to a base of more than 520,000 registered users. CCC applications power end-to-end customer experiences, digital workflows, AI, network management, and telematics capabilities across the markets we serve. Our AI approach is based on automated deep learning and parallel processing of mathematical models. This comprehensive approach to data science allows us to continuously improve the accuracy of existing models and release new models that automate time consuming workloads.

Network integrations across more than 300 insurers, 27,000 repair facilities, and thousands of other ecosystem participants unlock the power of the CCC platform. Our network creates tremendous value for our customers, is not easily replicated, and sets us apart from other vertical software companies. We believe that integrating to the insurance economy is the only way to deliver full end-to-end digital workflows across insurance processes. Today we enable more than 400 million interface transactions each year.

Corporate Information

CCC is a Delaware corporation. Our principal executive offices are located at 167 N. Green Street, 9th Floor, Chicago, Illinois 60607, and our telephone number is (312) 222-4636. Our principal website address is https://cccis.com/. Information contained in, or accessible through, our website is not a part of, and is not incorporated into, this prospectus.

11

Advent International Corporation

Advent Investor is an affiliate of Advent International Corporation. Advent International Corporation is one of the largest and most experienced global private equity investors. Since its founding in 1984, Advent has invested over $54 billion of equity in more than 370 private equity transactions across 41 countries and has maintained consistent industry leading investment performance across its funds. Advent has established a globally integrated team of over 200 investment professionals across North America, Europe, Latin America and Asia. The firm focuses on investments in five core sectors, including business & financial services, healthcare, industrial, retail, consumer & leisure, and technology, media & telecom. After more than 35 years dedicated to international investing, Advent remains committed to partnering with management teams to deliver sustained revenue and earnings growth for its portfolio companies.

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of relief from certain reporting requirements and other burdens that are otherwise applicable generally to public companies. These provisions include:

| • | presenting only two years of audited financial statements and only two years of selected financial data; |

| • | an exemption from compliance with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act; |

| • | reduced disclosure about our executive compensation arrangements in our periodic reports, proxy statements, and registration statements; and |

| • | exemptions from the requirements of holding nonbinding advisory votes on executive compensation or golden parachute arrangements. |

In addition, under the JOBS Act, emerging growth companies can delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have elected to avail ourselves of this exemption from new or revised accounting standards, and therefore, we will not be subject to the same new or revised accounting standards at the same time as other public companies that are not emerging growth companies or those that have opted out of using such extended transition period, which may make comparison of our financial statements with such other public companies more difficult. We may take advantage of these reporting exemptions until we no longer qualify as an emerging growth company or, with respect to adoption of certain new or revised accounting standards, until we irrevocably elect to opt out of using the extended transition period.

We will remain an emerging growth company until the earliest of (i) the last day of the fiscal year in which we have total annual gross revenues of $1.07 billion or more; (ii) the last day of our fiscal year following the fifth anniversary of the date of the completion of this offering; (iii) the date on which we have issued more than $1 billion in nonconvertible debt during the previous three years; and (iv) the date on which we are deemed to be a large accelerated filer under the rules of the SEC. We may choose to take advantage of some but not all of these reduced reporting burdens.

12

We are registering the issuance by us of up to 17,800,000 shares of Common Stock that may be issued upon exercise of the Warrants. We are also registering the resale by the Selling Holders or their permitted transferees of (i) up to 540,999,737 shares of Common Stock (including 17,800,000 shares of Common Stock that may be issued upon exercise of the Warrants) and (ii) up to 17,800,000 Warrants to purchase Common Stock.

Any investment in the securities offered hereby is speculative and involves a high degree of risk. You should carefully consider the information set forth under “Risk Factors” in this prospectus.

Issuance of Common Stock

The following information is as of May 27, 2022 and does not give effect to issuances of Common Stock, warrants or options to purchase shares of Common Stock after such date, or the exercise of warrants or options after such date.

| Shares of Common Stock to be issued upon exercise of all Warrants |

17,800,000 shares. |

| Shares of Common Stock outstanding prior to the exercise of all Warrants |

614,720,075 shares. |

| Use of proceeds |

We will receive up to an aggregate of approximately $204.7 million from the exercise of all Warrants assuming the exercise in full of all such Warrants for cash. Unless we inform you otherwise in a prospectus supplement or free writing prospectus, we intend to use the net proceeds from the exercise of such Warrants for general corporate purposes, which may include acquisitions, strategic investments, or repayment of outstanding indebtedness. |

Resale of Common Stock and Warrants

| Shares of Common Stock offered by the Selling Holders, consisting of (i) 17,800,000 shares of Common Stock underlying the Warrants and (ii) 523,199,737 shares of Common Stock |

540,999,737 shares. |

| Warrants offered by the Selling Holders |

17,800,000 warrants. |

| Exercise price |

$11.50 per share, subject to adjustment as described herein. |

| Redemption |

The Warrants are redeemable in certain circumstances. See “Description of Securities—Private Placement Warrants” for further discussion. |

13

| Use of proceeds |

We will not receive any proceeds from the sale of the Common Stock and Warrants to be offered by the Selling Holders. With respect to shares of Common Stock underlying the Warrants, we will not receive any proceeds from such shares except with respect to amounts received by us upon exercise of such Warrants to the extent such Warrants are exercised for cash. |

| NYSE Ticker Symbol |

Common Stock: “CCCS” |

Risk Factor Summary

Our business is subject to numerous risks and uncertainties, including those highlighted in the section titled “Risk Factors,” that represent challenges that we face in connection with the successful implementation of our strategy and growth of our business. The occurrence of one or more of the events or circumstances described in the section titled “Risk Factors,” alone or in combination with other events or circumstances, may materially adversely affect our business, financial condition and operating results. Such risks include, but are not limited to:

| • | A substantial portion of our revenue is derived from a relatively small number of customers in the P&C insurance and automotive collision industries, and the loss of any of these customers, or a significant revenue reduction from any of these customers, could materially harm our business, results of operations and financial condition; |

| • | Our business depends on our brand, and if we fail to develop, maintain, and enhance our brand and reputation cost-effectively, our business and financial condition may be adversely affected; |

| • | Our revenue growth rate depends on existing customers renewing and upgrading their SaaS software subscriptions for our solutions. A decline in our customer renewals and expansions could adversely impact our future results of operations; |

| • | Our growth strategy depends on continued investment in and delivery of innovative SaaS solutions. If we are unsuccessful in delivering innovative SaaS solutions, it could adversely impact our results of operations and financial condition; |

| • | Public health outbreaks, epidemics or pandemics, including the global COVID-19 pandemic, could harm our business and results of operations; |

| • | Macroeconomic factors impacting the principal industries we serve could adversely affect our product adoption, usage, or average selling prices; |

| • | If we are unable to develop, introduce and market new and enhanced versions of our solutions and products, we may be put at a competitive disadvantage and our operating results could be adversely affected; |

| • | Our sales and implementation cycles can be lengthy and variable, depend upon factors outside our control, and could cause us to expend significant time and resources prior to generating revenue; |

| • | If we are unable to develop new markets or sell our solutions into these new and existing markets, our revenue will not grow as expected; |

| • | Sales to customers or operations outside the United States may expose us to risks inherent in international sales; |

| • | Changes in China’s economic, political or social conditions or government policies, as well as the corruption risks presented by operating in China, could have an adverse effect on our efforts to expand our business in China. |

14

| • | We rely on data, technology and intellectual property of third parties and our solutions rely on information generated by third parties and any interruption of our access to such information, technology, and intellectual property could materially harm our operating results; |

| • | Failure to protect our intellectual property could adversely impact our business and results of operations; |

| • | Our solutions or products or our third-party cloud providers have experienced in the past, and could experience in the future, data security breaches, which could adversely impact our reputation, business, and ongoing operations; |

| • | Some of our services and technologies use “open source” software, which may restrict how we use or distribute our services or require that we release the source code of certain products subject to those licenses; and |