Form 424B1 Kalera Public Ltd Co

Tweet

Tweet Share

Share

Filed Pursuant to Rule 424(b)(1)

Registration No. 333-267797

PROSPECTUS

KALERA PUBLIC LIMITED COMPANY

UP TO 68,000,000 UNITS

consisting of

Ordinary Shares or Pre-Funded Warrants to Purchase Ordinary Shares and Class A Warrants to Purchase Ordinary Shares

We are offering on a best efforts basis up to 68,000,000 Units, each consisting of one ordinary share of Kalera Public Limited Company, a public limited company incorporated under the laws of the Republic of Ireland with registered number 606356 (the “Registrant”), with a nominal value of $0.0001 (the “Kalera Ordinary Shares”), at a public offering price of $0.13 per Kalera Ordinary Share, along with two Class A Warrants to subscribe for one Kalera Ordinary Share each for no additional consideration.

Each Class A Warrant will be immediately exercisable for one Kalera Ordinary Share at an exercise price of $0.13 per share and expire five years after the issuance date. We are also registering the Kalera Ordinary Shares issuable from time to time upon exercise of the Class A Warrants.

We are also offering to each purchaser of Units that would otherwise result in the purchaser’s beneficial ownership exceeding 4.99% of outstanding Kalera Ordinary Shares immediately following the consummation of this offering the opportunity to acquire one pre-funded warrant (in lieu of one Kalera Ordinary Share) and two Class A Warrants. A holder of pre-funded warrants will not have the right to exercise any portion of its pre-funded warrants if the holder, together with its affiliates, would beneficially own in excess of 4.99% (or, at the election of the holder, such limit may be increased to up to 9.99%) of the number of Kalera Ordinary Shares outstanding immediately after giving effect to such exercise. Each pre-funded warrant will be exercisable for one Kalera Ordinary Share. The pre-funded exercise price for each pre-funded warrant included in each Unit will be equal to the price per Unit including one Kalera Ordinary Share, minus $0.0001, and the remaining non pre-funded exercise price of each pre-funded warrant will equal $0.0001 per Kalera Ordinary Share. The pre-funded warrants will be immediately exercisable (subject to the beneficial ownership cap) and may be exercised at any time until all of the pre-funded warrants are exercised in full. For each Unit including a pre-funded warrant that is issued (without regard to any limitation on exercise set forth therein), the number of Units including a Kalera Ordinary Share we are offering will be decreased on a one-for-one basis. The Kalera Ordinary Shares and pre-funded warrants, if any, can each be subscribed for and/ or acquired (as applicable) in this offering only with the accompanying Class A Warrant as part of a Unit, but the components of the Units will immediately separate upon issuance. See “Description of Securities” in this prospectus for more information.

Kalera Ordinary Shares are listed on Nasdaq and began trading on Nasdaq on June 29, 2022 under the symbol KAL. On October 26, 2022, the closing sale price of the Kalera Ordinary Shares was $0.21 per share.

There is no established trading market for the pre-funded warrants or the Class A Warrants, and we do not expect an active trading market to develop. We do not intend to list the pre-funded warrants or the Class A Warrants on any securities exchange or other trading market. Without an active trading market, the liquidity of these securities will be limited.

We are an “emerging growth company,” as defined under the federal securities laws, and, as such, may elect to comply with certain reduced public company reporting requirements for future filings.

Investing in our securities involves a high degree of risk. Before buying any securities, you should carefully read the discussion of the risks of investing in our securities in “Risk Factors” beginning on page 7 of this prospectus.

You should rely only on the information contained in this prospectus or any prospectus supplement or amendment hereto. We have not authorized anyone to provide you with different information.

| Per Unit(1) | Total | |||||||

| Public Offering Price | $ | 0.13 | $ | 8,840,000 | ||||

| Placement Agent fees(2)(3) | $ | 0.0091 | $ | 618,800 | ||||

| Proceeds, before expenses, to us | $ | 0.1209 | $ | 8,221,200 | ||||

| (1) | Units consist of one Kalera Ordinary Share and two Class A Warrants. |

| (2) | The Placement Agent fee shall equal 7% of the public offering price of the securities sold by us in this offering. |

| (3) | The Placement Agent will receive compensation in addition to the placement agent fees described above. See “Plan of Distribution” for a description of compensation payable to the Placement Agent. |

We have engaged Maxim Group LLC (“Maxim”) (the “Placement Agent”) as our exclusive Placement Agent to use its reasonable best efforts to solicit offers to purchase our securities in this offering. The Placement Agent has no obligation to purchase any of the securities from us or to arrange for the purchase or sale of any specific number or dollar amount of the securities.

We expect that the offering will end two trading days after we first enter into a securities purchase agreement relating to the offering, the Kalera Ordinary Shares will settle delivery versus payment (“DVP”)/receipt versus payment (“RVP”) and the Class A Warrants and pre-funded warrants will be issued in certificated form. Accordingly, we and the Placement Agent have not made any arrangements to place investor funds in an escrow account or trust account since the Placement Agent will not receive investor funds in connection with the sale and/or issuance (as applicable) of the securities offered hereunder.

We have agreed to pay the Placement Agent the placement agent fee set forth in the table above and to provide certain other compensation to the Placement Agent. See “Plan of Distribution” beginning on page 128 of this prospectus for more information regarding these arrangements.

We expect to deliver the Kalera Ordinary Shares and Class A Warrants, or pre-funded warrants and Class A Warrants, constituting the Units, against payment in New York, New York on or about October 31, 2022 subject to the satisfaction of customary closing conditions.

Neither the Securities Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Maxim Group LLC

The date of this prospectus is October 26, 2022.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or in any free writing prospectus prepared by us or on our behalf. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

| i |

FREQUENTLY USED TERMS

Unless otherwise stated or unless the context otherwise requires, the term “Kalera”, the “Company”, “Registrant”, “we”, “us” and “our” refer to Kalera Public Limited Company, a public limited company incorporated in Ireland with registered number 606356, and where appropriate, our wholly owned subsidiaries.

In this document:

“$” means the currency in dollars of the United States of America.

“2022 Plan” means the 2022 Long-Term Stock Incentive Plan of Kalera.

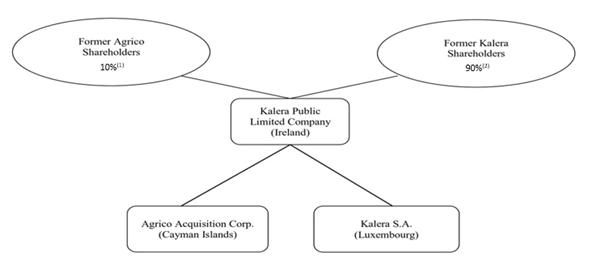

“Agrico” means Agrico Acquisition Corp., a Cayman Islands exempted company.

“Agrico Articles” means the Amended and Restated Memorandum and Articles of Association of Agrico adopted on July 7, 2021.

“Agrico Class A ordinary shares” means the class A ordinary shares of Agrico, par value $0.0001 per share.

“Agrico Class B ordinary shares” means the class B ordinary shares of Agrico, par value $0.0001 per share.

“Agrico Initial Shareholders” means holders of Founder Shares prior to the Agrico IPO, including the Sponsor.

“Agrico IPO” means the initial public offering of Agrico Units consummated on July 12, 2021.

“Agrico Ordinary Shares” means Agrico Class A ordinary shares and Agrico Class B ordinary shares.

“Agrico Public Warrant” means each whole warrant (other than the Private Placement Warrants), entitling the holder thereof to purchase one Agrico ordinary share at a price of $11.50 per share.

“Agrico Share Issuance” means the issuance by Agrico of Agrico Ordinary Shares to Kalera.

“Agrico Shareholders” means the holders of Agrico Shares prior to the Business Combination, including the Agrico Initial Shareholders and members of the Agrico management team, provided that each Agrico Initial Shareholder’s and member of Agrico’s management team’s status as an “Agrico Shareholder” shall only exist with respect to such Agrico Shares.

“Agrico Shares” means Class A ordinary shares of Agrico issued as part of the Agrico Units sold in the Agrico IPO.

“Agrico Units” means the Agrico units issued in the Agrico IPO, each consisting of one ordinary share and one-half of one Agrico Public Warrant.

“Agrico Warrants” means Private Placement Warrants and Agrico Public Warrants, collectively.

“Armistice” means Armistice Capital Master Fund Ltd.

“Armistice Warrants” means the Series A Warrants and the Series B Warrants.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of January 30, 2022, as amended from time to time, by and among Agrico, Kalera SA, Kalera, Cayman Merger Sub and Lux Merger Sub.

| ii |

“Cayman Merger Sub” means Kalera Cayman Merger Sub, a Cayman Islands exempted company.

“Closing” means the consummation of the transactions contemplated under the Business Combination Agreement.

“Code” means the Internal Revenue Code of 1986, as amended.

“CVR” means one contractual contingent value right per Kalera Share which shall represent the right to receive up to two contingent payments of Kalera Ordinary Shares

“CVR Agreement” means the Contingent Value Rights Agreement entered into by Kalera and the Rights Agent party thereto.

“CVR Shares” means the Kalera Ordinary Shares issuable pursuant to the CVRs upon the satisfaction of certain conditions.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“First Closing” means the consummation of the First Merger and the related transactions thereby.

“First Closing Date” means the date on which all conditions of the First Closing are satisfied.

“First Merger” means the first merger pursuant to which Cayman Merger Sub merged with and into Agrico, with Agrico continuing as the surviving entity of the First Merger and as a wholly owned subsidiary of Kalera.

“First Merger Effective Time” has the meaning assigned to it in the Business Combination Agreement.

“Founder Shares” means Agrico Class B ordinary shares initially purchased by the Sponsor in a private placement prior to the Agrico IPO, of which 1,796,875 are currently outstanding.

“IRS” means the Internal Revenue Service of the United States.

“Kalera” means Kalera Public Limited Company, a public limited company incorporated under the laws of the Republic of Ireland.

“Kalera Articles” means the consolidated articles of association of Kalera, as amended from time to time.

“Kalera Capital Reduction” means certain of the Kalera SA Shares and all the Kalera SA Options being cancelled and ceasing to exist or being assumed (as applicable) upon completion of the Second Merger by way of a capital reduction pursuant to the Luxembourg Companies Act.

“Kalera Options” has the meaning assigned to the term “Pubco Options” in the Business Combination Agreement.

“Kalera Ordinary Shares” means the ordinary shares of Kalera.

“Kalera SA” means Kalera S.A., a public limited company incorporated in Luxembourg.

“Kalera SA Options” has the meaning assigned to the term “Kalera Options” in the Business Combination Agreement.

“Kalera SA Shareholders” means the holders of Kalera SA Shares.

“Kalera SA Shares” the ordinary shares of Kalera SA.

| iii |

“Kalera Warrant” means each one whole warrant entitling the holder thereof to subscribe for one Kalera Ordinary Share at a purchase price of $11.50 per share.

“Lux Holdco” means Kalera S.A.

“Lux Merger Sub” means Kalera Luxembourg Merger Sub SARL, a Luxembourg limited liability company (société à responsabilité limitée).

“Luxembourg Company Law” means the Luxembourg law dated August 10, 1915 on commercial companies, as amended.

“Maxim” means Maxim Group, LLC, acting as placement agent.

“Merger Subs” means collectively, Cayman Merger Sub and the Lux Merger Sub.

“Nasdaq” means the The Nasdaq Capital Market.

“New Kalera Options” means the 904,505 stock options outstanding under the 2022 Plan.

“New Restricted Stock Units” means the 607,446 restricted stock units outstanding under the 2022 Plan.

“Placement Agent” means Maxim.

“Private Placement Warrants” means the Agrico Warrants purchased by the Sponsor and Maxim in a private placement at the time of the Agrico IPO for a purchase price of $1.00 per warrant, each of which is exercisable for one ordinary share.

“Redemption” means the right of the holders of Agrico Shares to have their shares redeemed in accordance with the procedures set forth in the Prospectus.

“Redemption Price” means an amount equal to a pro rata portion of the aggregate amount on deposit in the Trust Account two (2) days prior to the completion of the Business Combination calculated in accordance with the Agrico Articles (as equitably adjusted for shares splits, shares dividends, combinations, recapitalizations and the like after the Closing).

“SEC” means the U.S. Securities and Exchange Commission.

“Second Closing” means the consummation of the Business Combination (other than those transactions which occur on the First Closing).

“Second Closing Date” means the date on which all conditions of the Second Closing were satisfied.

“Second Merger” means the second merger pursuant to which Lux Merger Sub merged with and into Kalera SA with Kalera SA as the surviving entity of such merger.

“Second Merger Effective Time” has the meaning assigned to it in the Business Combination Agreement.

“Securities” means the Kalera Ordinary Shares and Kalera Warrants offered and sold under this registration statement.

“Securities Act” means the U.S. Securities Act of 1933, as amended.

“Securities Purchase Agreement” means the securities purchase agreement entered into on July 7, 2022 between Kalera and Armistice.

“Series A Warrants” means the 2,500,000 series A warrants issued to Armistice on July 11, 2022, exercisable six months from their date of issuance at an exercise price of $4.41 per share and expiring two years from their date of issuance.

“Series B Warrants” means the 2,500,000 series B warrants issued to Armistice on July 11, 2022, exercisable six months from their date of issuance at an exercise price of $4.41 per share and expiring five and a half years from their date of issuance.

“Sponsor” means DJCAAC LLC, a Delaware limited liability company and each of the persons set forth on Schedule I to the Sponsor Support Agreement.

“Sponsor Support Agreement” means the agreement among the Sponsor, Agrico and Kalera SA entered into on January 30, 2022.

“Trust Account” means the trust account that held a portion of the proceeds of the Agrico IPO and the concurrent sale of warrants to the Sponsor in a private placement.

“U.S. GAAP” means United States generally accepted accounting principles.

| iv |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the information in this prospectus constitutes forward-looking statements for the purposes of federal securities laws. You can identify these statements by forward-looking words such as “may,” “might,” “could,” “will,” “would,” “should,” “expect,” “possible,” “potential,” “anticipate,” “contemplate,” “believe,” “estimate,” “plan,” “predict,” “project,” “intends,” and “continue” or similar words. You should read statements that contain these words carefully because they:

| ● | discuss future expectations; or | |

| ● | state other “forward-looking” information. |

Forward-looking statements in this prospectus may include, for example, statements about:

| ● | the expected benefits and costs of the Business Combination; | |

| ● | changes in Kalera’s strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects and plans; | |

| ● | the implementation, market acceptance and success of Kalera’s business models; | |

| ● | the impact of health epidemics, including the coronavirus SARS-CoV-2 (“COVID-19”), pandemic, on Kalera’s business and the actions Kalera may take in response thereto; | |

| ● | Kalera’s expectations regarding its ability to obtain and maintain intellectual property protection and not infringe on the rights of others; | |

| ● | expectations regarding the time during which Kalera will be an emerging growth company under the JOBS Act; | |

| ● | Kalera’s future capital requirements and sources and uses of cash; | |

| ● | Kalera’s ability to obtain funding for its operations; | |

| ● | Kalera’s business, expansion plans and opportunities; | |

| ● | the outcome of any known and unknown litigation and regulatory proceedings; and |

Kalera believes it is important to communicate its expectations to its security holders. However, there may be events in the future that Kalera is not able to predict accurately or over which it has no control. The risk factors and cautionary language discussed in this prospectus, including in the section titled “Risk Factors,” provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described by Kalera in such forward-looking statements, including among other things:

| ● | changes adversely affecting the vertical farming industry and the development of existing or new technologies; | |

| ● | the effect of the COVID-19 pandemic on Kalera’s business; | |

| ● | the ability of Kalera to obtain financing to address its liquidity, operating or capital expenditure needs or other financing objectives on favorable terms, if at all; |

| v |

| ● | the potential restrictive terms, dilutive impact or other material adverse effects of the terms of any financing arrangements entered into by Kalera; | |

| ● | the outcome of any legal proceedings that may be instituted against Kalera; | |

| ● | lack of useful financial information for an accurate estimate of future capital expenditures; | |

| ● | possibility of continuing to incur losses for the foreseeable future; | |

| ● | potential delay in the completion of new facilities; | |

| ● | the competitiveness of the agriculture industry; | |

| ● | the difficulty of controlling customer perception of Kalera’s brand; | |

| ● | the limits that are imposed on Kalera by the amount of facilities in operation at a given time; | |

| ● | distribution agreements with third parties; | |

| ● | consolidation of customers or suppliers; | |

| ● | consumer preferences and spending habits; | |

| ● | the volatility of energy costs. | |

| ● | changes in applicable laws or regulations, including environmental and export control laws; | |

| ● | the ability to retain key employees; | |

| ● | Kalera’s business strategy and plans; | |

| ● | Kalera’s ability to target and retain customers and suppliers; | |

| ● | the failure to build Kalera’s finance infrastructure and improve its accounting systems and controls; | |

| ● | whether and when Kalera might pay dividends; and | |

| ● | the ability of Kalera to source its materials from an ethically and sustainably sourced supply chain. |

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this prospectus.

All forward-looking statements included herein attributable to Kalera or any person acting on Kalera’s behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable laws and regulations, Kalera undertakes no obligations to update these forward-looking statements to reflect events or circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events.

| vi |

PROSPECTUS SUMMARY

This summary highlights information contained in greater detail elsewhere in this prospectus. This summary is not complete and does not contain all the information that may be important to you. You should read the entire prospectus carefully before making your investment decision with respect to our Units. You should carefully consider, among other things, the financial statements included elsewhere in this prospectus and the related notes, and the sections titled “Risk Factors,” “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus. Unless expressly indicated or the context requires otherwise, the terms the “Company,” “Kalera,” the “Registrant,” “we,” “us” and “our” in this prospectus refer to Kalera Public Limited Company, and where appropriate, our wholly-owned subsidiaries.

Kalera is a leading vertical farming company. We utilize proprietary technology and plant and seed science to sustainably grow local, delicious, nutrient-rich, pesticide-free, non-GMO leafy greens year-round. In contrast to produce that requires costly and extended long-haul supply chains, our leafy greens are delivered within hours of harvesting, always fresh, and maintain a longer shelf life. Our high-yield, automated, data-driven hydroponic production facilities have been designed for rapid roll-out with attractive unit economics to grow leafy greens faster, cleaner and in a manner that is better for the environment than traditional farming. Given our cost-efficient production process from seed to harvest and capital discipline, we are able to sell our “better than organic” produce at competitive prices. With our mission to serve humanity, wherever we are, fresh, safe, sustainable and affordable nourishment, we aim to become a global leader in controlled-environment agriculture (“CEA”) for leafy greens addressing an expanding $50 billion addressable market opportunity for vertical farming products.

Kalera was incorporated under the laws of the Republic of Ireland as a private limited company, for purposes of a business combination. Kalera was re-registered as an Irish public limited company on March 29, 2022 and changed its name to “Kalera Public Limited Company” on April 4, 2022. Kalera owns no material assets and does not operate any businesses.

The mailing address of Kalera’s principal executive offices are 7455 Emerald Dunes Dr., Suite 2100, Orlando Florida 32822, and its phone number is. +1 (407) 574-8204. Kalera’s corporate website address is https://www.kalera.com. Kalera’s website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference in, and is not considered part of, this prospectus.

Kalera announces material information to the public through a variety of means, including filings with the Securities and Exchange Commission, press releases, public conference calls, Kalera’s website (https://www.kalera.com/), and its investor relations website (https://investors.kalera.com/). Kalera uses these channels, as well as social media, including its LinkedIn account (https://www.linkedin.com/company/kalera) to communicate with investors and the public news and developments about Kalera and other matters. Therefore, Kalera encourages investors, the media, and others interested in the Company to review the information it makes public in these locations, as such information could be deemed to be material information.

Stock Exchange Listing

Kalera Ordinary Shares and Kalera Warrants are currently listed on Nasdaq under the symbols KAL and KALWW, respectively.

| 1 |

Summary of Risk Factors

Our business is subject to numerous risks and uncertainties, including those highlighted in the section title “Risk Factors.” Such risks include, but are not limited to:

| ● | Substantial doubt regarding Kalera’s ability to continue as a going concern or maintain adequate liquidity to fund its operations; | |

| ● | Kalera is in an early commercial phase, and is highly dependent on a successful roll-out and commercialization of its products; | |

| ● | Kalera lacks useful financial information for the accurate estimation of its future capital expenditures and unit economics; | |

| ● | Kalera is an early stage company with a history of losses and expects to continue to incur losses going forward; | |

| ● | Kalera may be unable to successfully integrate &ever in order to realize the anticipated benefits; | |

| ● | Kalera’s growth plans depend on deploying new production facilities, which will require significant expenditures; | |

| ● | Inflation and increases in operating costs could materially and adversely impact Kalera; | |

| ● | Kalera’s success, competitive position and future revenues will depend in part on its ability to further develop and protect its intellectual property and know-how; | |

| ● | Kalera’s commercial success is dependent on its ability to enter into produce distribution agreements and other agreements with third parties; | |

| ● | Kalera uses a limited number of distributors for the substantial majority of its sales; | |

| ● | Consolidation of customers or the loss of a significant customer could negatively impact Kalera’s sales and profitability; | |

| ● | Kalera may face difficulties as it expands its operations into geographical locations in which it has no prior operating experience; | |

| ● | Kalera may not be able to identify suitable acquisition candidates or consummate acquisitions on acceptable terms; | |

| ● | The failure of suppliers to perform their obligations, Kalera’s inability to replace or renew supply agreements, or disruptions in the supply chain; | |

| ● | Estimates of market opportunity and forecasts of market growth may prove to be inaccurate or not materialize; | |

| ● | Failure to retain and motivate Kalera’s senior management may adversely affect its operations and growth prospects; | |

| ● | Kalera is reliant on key personnel and the ability to attract new, qualified personnel; | |

| ● | Ingredient, packaging and energy costs are volatile and may rise significantly; |

| 2 |

| ● | Kalera relies on information technology systems and any inadequacy, failure, interruption or security breaches of those systems, including a cybersecurity incident or other technology disruptions, may harm its ability to effectively operate its business; | |

| ● | The recent development of the coronavirus (COVID-19) pandemic and its multiple variants; | |

| ● | Conducting business internationally, and international geopolitical events and economic factors, create operational, financial and tax risks for Kalera’s business; | |

| ● | Kalera’s management has limited experience in operating a U.S. public company; | |

| ● | Potential dilutive impact, restrictions or other terms in Kalera’s financing arrangements; | |

| ● | Each of Kalera and Agrico has identified a material weakness in its internal control over financial reporting and Kalera may be unable to establish and maintain effective internal control over financial reporting; | |

| ● | Nasdaq may delist Kalera’s securities on its exchange; | |

| ● | The market price of Kalera’s securities may be volatile and fluctuate substantially, which could result in substantial losses for investors and may subject Kalera to securities litigation suits; | |

| ● | Kalera’s ability to utilize its federal net operating loss and tax credit carryforwards may be limited under applicable laws; | |

| ● | The grant and future exercise of registration rights; | |

| ● | Sales or perceived sales of a substantial number of Kalera’s securities could adversely affect the market price of such securities and impact Kalera’s ability to raise additional capital in the future; | |

| ● | The issuance of the CVR Shares could materially dilute Kalera Shareholders; | |

| ● | Kalera may be a passive foreign investment company, which could result in adverse U.S. federal income tax consequences to U.S. investors; | |

| ● | Kalera may be considered a U.S. corporation for U.S. federal income tax purposes, which could result in adverse U.S. federal tax consequences to Kalera and its investors; and | |

| ● | Kalera’s operations are subject to FDA, USDA, EPA and OSHA governmental regulation and state regulation and Kalera is exposed to risks related to regulatory processes and changes in regulatory environment. |

| 3 |

THE OFFERING

| Securities offered by us hereunder | Up to 68,000,000 Units on a best efforts basis, at a public offering price of $0.13 per Kalera Ordinary Shares with no additional consideration payable for the Class A Warrant. Each Unit consists of one Kalera Ordinary Share and two Class A Warrants. We are also registering the Kalera Ordinary Shares issuable from time to time upon exercise of the Class A Warrants.

We are also offering to each purchaser, with respect to the purchase of Units that would otherwise result in the purchaser’s beneficial ownership exceeding 4.99% of our outstanding Ordinary Shares immediately following the consummation of this offering, the opportunity to acquire one pre-funded warrant in lieu of one Kalera Ordinary Share. A holder of pre-funded warrants will not have the right to exercise any portion of its pre-funded warrant if the holder, together with its affiliates, would beneficially own in excess of 4.99% (or, at the election of the holder, such limit may be increased to up to 9.99%) of the number of Kalera Ordinary Shares outstanding immediately after giving effect to such exercise. Each pre-funded warrant will be exercisable for one Kalera Ordinary Share. The pre-funded exercise price payable per pre-funded warrant will be equal to the price per Kalera Ordinary Share, minus $0.0001, and the non pre-funded exercise price of each pre-funded warrant will equal $0.0001 per share. The pre-funded warrants will be immediately exercisable (subject to the beneficial ownership cap) and may be exercised at any time in perpetuity until all of the pre-funded warrants are exercised in full.

The Units will not be certificated or issued in stand-alone form. The Kalera Ordinary Shares and/or pre-funded warrants and the Class A Warrants comprising the Units are immediately separable upon issuance and will be issued separately in this offering. |

| 4 |

| Description of the Class A Warrants | Each Class A Warrant will have an exercise price of $0.13 per share, will be exercisable upon issuance and will expire five years from issuance. Each Class A Warrant is exercisable for one Kalera Ordinary Share, subject to adjustment in the event of stock dividends and distributions, stock splits, adjustments, stock combinations, reclassifications, dilutive issuances or similar events affecting the Kalera Ordinary Shares as described herein. Subject to certain exemptions outlined in the Class A Warrant, if the Company shall sell, enter into an agreement to sell, or grant any option to purchase, or sell, enter into an agreement to sell, or grant any right to reprice, or otherwise dispose of or issue (or announce any offer, sale, grant or any option to purchase or other disposition) any Kalera Ordinary Shares or Ordinary Share Equivalents (as defined in the Class A Warrant), at an effective price per share less than the exercise price of the Class A Warrant then in effect, the exercise price of the Class A Warrant shall be reduced to equal the effective price per share in such dilutive issuance. The Class A Warrants contain a one-time reset of the exercise price to a price equal to the lesser of (i) the then exercise price and (ii) 100% of the five-day volume weighted average prices for the five (5) trading days immediately preceding the date that is sixty days after issuance of such Class A Warrants. This prospectus also relates to the offering of the Kalera Ordinary Shares issuable upon exercise of the Class A Warrants. For more information regarding the Class A Warrants, you should carefully read the section titled “Description of Securities” in this prospectus. | |

| Public Offering Price | $0.13 per Unit. | |

| Kalera Ordinary Shares outstanding prior to this offering | 23,877,828 Kalera Ordinary Shares. | |

| Kalera Ordinary Shares to be outstanding after this offering | Up to 91,877,828 shares at a public offering price of $0.13 per Kalera Ordinary Share, or pre-funded exercise price of $0.1299 per pre-funded warrant. |

| 5 |

| Use of Proceeds | Our net proceeds from the offering amount of the sale of Units in this offering will be approximately $7,765,135 million, after deducting placement agent fees and estimated offering expenses payable by us, based on an offering price of $0.13 per Kalera Ordinary Share, or pre-funded exercise price of $0.1299 per pre-funded warrant. We intend to use the net proceeds of this offering for general corporate purposes. Ultimately, our management will have discretion and flexibility in applying the net proceeds of this offering. We may use the proceeds of this offering for purposes with which you do not agree. See “Risk Factors-Risks Relating to the Offering-Since we have broad discretion in how we use the proceeds from this offering, we may use the proceeds in ways with which you disagree.” See the section titled “Use of Proceeds” appearing elsewhere in this prospectus for more information.

| |

| Listing | Kalera Ordinary Shares are listed on Nasdaq and began trading on Nasdaq on June 29, 2022 under the symbol KAL. We do not intend to list the Class A Warrants or pre-funded warrants offered hereunder on any stock exchange. There are no established public trading markets for the Class A Warrants or the pre-funded warrants, and we do not expect such markets to develop. Without an active trading market, the liquidity of the Class A Warrants and the pre-funded warrants will be limited. | |

| Risk Factors | See the section titled “Risk Factors” and other information included in this prospectus for a discussion of factors that you should consider carefully before deciding to invest in our securities. | |

| Lock-Up Restrictions | We and each of our directors and officers are subject to certain lock-up restrictions as identified in the section titled “Plan of Distribution-Lock-Up Agreements.” |

The number of Kalera Ordinary Shares shown above to be outstanding after this offering is based on the Kalera Ordinary Shares outstanding as of October 26, 2022 and excludes:

| ● | 904,505 Kalera Ordinary Shares issuable under our 2022 Plan; | |

| ● | 364,000 Kalera Ordinary Shares issuable in relation to the Kalera Options; | |

| ● | 607,446 Kalera Ordinary Shares issuable in relation to the New Restricted Stock Units; | |

| ● | 14,437,500 Kalera Ordinary Shares issuable upon exercise of the Kalera Warrants; | |

| ● | 5,000,000 Kalera Ordinary Shares issuable upon exercise of the Armistice Warrants; | |

| ● | 136,000,000 Kalera Ordinary Shares issuable upon exercise of the Class A Warrants; | |

| ● | 4,000,000 Kalera Ordinary Shares issuable upon the conversion of the Second Amended and Restated Secured Convertible Bridge Promissory Note; and | |

| ● | Kalera Ordinary Shares issuable pursuant to the CVRs upon the satisfaction of certain conditions under the CVR Agreement. |

Except as otherwise noted, all information in this prospectus reflects and assumes (i) no sale of pre-funded warrants in this offering, which, if sold, would reduce the number of Kalera Ordinary Shares that we are offering on a one-for-one basis and (ii) no exercise of Class A Warrants issued in this offering.

For additional information concerning the offering, see the section titled “Plan of Distribution” beginning on page 128 of this prospectus.

| 6 |

RISK FACTORS

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. The value of your investment in Kalera will be subject to significant risks affecting Kalera and inherent in the industry in which Kalera operates. If any of the events described below occur, the business and financial results could be adversely affected in a material way. This could cause the trading price of Kalera Ordinary Shares to decline, perhaps significantly, and you therefore may lose all or part of your investment. Please see the section titled “Where You Can Find Additional Information” in this prospectus. The risks set out below are not exhaustive and do not comprise all of the risks associated with an investment in Kalera. Additional risks and uncertainties not currently known to Kalera or which Kalera currently deems immaterial may also have a material adverse effect on Kalera’s business, financial condition, results of operations, prospects and/or its share price.

Risks Relating to Kalera’s Business and the Industry in Which it Operates

There is substantial doubt about Kalera’s ability to continue as a going concern, and Kalera will need to raise additional capital in the future in order to execute its roll-out and commercialization strategy or for other purposes, which may not be available on favorable terms, or at all.

Kalera’s operating losses and accumulated deficits raise substantial doubt about its ability to continue as a going concern. Kalera will need to raise additional capital in order to execute and complete its roll-out and commercialization strategy, and to fund its operations. While the exact timing and amount of our future funding plans depend on many factors, we are exploring various funding and liquidity opportunities, including further issuances of equity and/or equity-linked securities, the incurrence of additional debt, the restructuring of our existing debt, the potential for strategic investments by private investors and asset sales.

There is a risk that adequate sources of funds may not be available at all, or not available at acceptable terms and conditions, when needed. Kalera may need to seek additional funds through public or private equity or debt financings or other sources, such as strategic collaborations. If Kalera raises additional funds by issuing additional equity securities, or through instruments convertible into equity securities, the existing shareholders may be significantly diluted. Further, equity or debt financings may result in issuance of securities with priority as to liquidation and dividend and other rights more favorable than shares, imposition of debt covenants and repayment obligations, or other restrictions that may adversely affect Kalera’s business. If funding is insufficient at any time in the future, Kalera may be unable to fund its current and ongoing roll-out and commercialization strategy and lose business opportunities and thereby risk failing to respond to competitive pressures. Failure to obtain the necessary capital when needed could force Kalera to delay, limit, reduce or terminate its product development or commercialization efforts.

In addition, Kalera may seek additional capital due to favorable market conditions or strategic considerations even if Kalera believes that it has sufficient funds for current or future operating plans. There can be no assurance that financing will be available to Kalera on favorable terms, or at all. If Kalera for any reason does not obtain additional funding as needed in the future, this could have a material adverse effect on its revenues, profitability, liquidity, cash flow, financial position and/or prospects.

| 7 |

Kalera is in an early commercial phase, and is highly dependent on a successful roll-out and commercialization of its products.

Kalera is in an early commercial phase, and is highly dependent on succeeding with its roll-out and commercialization strategy in order to deliver future operating profits. In 2020, Kalera started to execute a strategy for rapid capacity expansion based on installing and operating large-scale production facilities allowing it to target and expand its customer base to large US regional and national accounts such as grocery chains, distributors and contract food service companies. Kalera has until recently solely been present in the US produce market, with a roll-out and commercialization plan for establishing its business throughout the US, by building new large-scale production facilities in US cities and areas that it currently is not present in and that provide attractive markets. Through the acquisition (the “&ever Acquisition”) of the vertical farming company &ever GmbH (“&ever”) in October 2021, and the purchase of NOX Culinary General Trading Company LLC’s 50% remaining interest in &ever Middle East Holding Ltd. (“&ever ME”) to own 100% of &ever ME, Kalera has also added operations in Germany, Kuwait and Singapore. Going forward, Kalera is seeking to further expand its US operations.

Kalera’s failure to execute its roll-out and commercialization strategy or to manage its growth effectively could adversely affect its business, financial condition, results of operations, cash flow and/or prospects. In addition, there can be no guarantee that even if Kalera successfully implements its strategy, it would result in Kalera achieving its business and financial objectives, taking advantage of market opportunities, satisfying customer requirements or securing additional customer commitments, any of which could adversely affect Kalera’s business, financial condition and results of operations. Indeed, as vertical farming itself is a relatively new concept, the industry and Kalera’s markets may fail to grow or grow more slowly than expected. Kalera’s management team will review and evaluate the business strategy with the board of directors on a regular basis, and Kalera may decide to alter or discontinue elements of its business strategy and may adopt alternative or additional strategies in response to the operating environment or competitive situation or other factors or events beyond its control.

Kalera lacks useful financial information for the accurate estimation of its future capital expenditures and unit economics.

As a result of Kalera being in an early commercial phase, there is a lack of useful financial information for the accurate estimation of future capital expenditures and unit economics. This applies in particular to Kalera’s Orlando, Atlanta, Houston, Denver, and Kuwait facilities, which commenced operations in February 2020, September 2021 (post electrical component upgrades), October 2021, April 2022 and March 2020 respectively, and on which its estimates of capital expenditure and unit economics for new facilities are based. Any failure by Kalera to estimate its capital expenditure and unit economics accurately could limit its ability to implement its roll-out and commercial strategy and to accurately forecast future cash flow needs. In addition, the economics for new facilities can also be subject to adverse changes or developments affecting any new facilities and that could impair Kalera’s ability to produce the business results and prospects as expected. Such adverse changes and developments include, but are not limited to, natural disasters, fire, power interruptions, disease outbreaks or pandemics (such as COVID-19), or changes in customer demand.

Kalera is an early stage company with a history of losses and expects to continue to incur losses going forward.

Kalera is an early stage company and has incurred significant operating losses since its incorporation. Historically, Kalera has financed its operations mainly through the sale of equity securities and in part through diverse financing arrangements. Going forward, Kalera expects to continue to incur operating losses for the foreseeable future and no assurances can be given on when, or if at all, Kalera will achieve profitability from its operations. The extent of Kalera’s losses going forward will depend, in part, on its future expenses and its ability to generate revenue. Achieving profitability is dependent on a number of factors, amongst others, Kalera succeeding with its roll-out and commercialization strategy, but also the operating environment, the competitive environment and other factors or events beyond its control.

| 8 |

Kalera expects the rate at which it will incur losses to be significantly higher in future periods as it:

| ● | expands its commercial production capabilities and incurs construction costs associated with building its facilities; | |

| ● | completes the buildout of its facilities in Honolulu, Columbus, Seattle, St Paul, and Singapore; | |

| ● | identifies and invests in future growth opportunities, including new or expanded facilities and new product lines and potentially undertaking future acquisitions such as the &ever acquisition; | |

| ● | integrates the business of &ever; | |

| ● | increases its spending on research, innovation and development; | |

| ● | increases its expenditures associated with its supply chain; | |

| ● | increases its sales and marketing activities to increase brand awareness and the sales of its products and develops its distribution infrastructure; and | |

| ● | incurs additional general and administrative expenses, including increased finance, legal and accounting expenses, to support its growing operations and infrastructure. |

The abovementioned efforts may be more expensive than Kalera currently estimates or such investments may not result in additional or commensurately higher revenue, which would further increase its losses. In addition, its revenue growth may slow or decline for a number of other reasons, including reduced demand for its products, increased competition, a decrease in the growth or reduction in size of its overall market, the impacts to its business from the COVID-19 pandemic, or if Kalera cannot capitalize on growth opportunities. Kalera may never succeed in becoming profitable and, even if it does, it may never generate revenue or sustainable income that is significant enough to maintain profitability. Should any of these risks materialize, it could have a material and adverse effect on its business, financial condition, results of operations, cash flows, time to market and prospects.

Kalera’s business may suffer if it does not achieve the anticipated benefits of the &ever Acquisition.

Kalera expects to achieve certain benefits as a result of the &ever Acquisition. There can be no assurances that Kalera will realize the expected benefits currently anticipated from the &ever Acquisition or that &ever will perform according to Kalera’s projections following the &ever Acquisition. A failure to achieve any of the anticipated benefits of the &ever Acquisition or a failure of &ever to perform according to Kalera’s projections could adversely affect Kalera’s business, financial condition and results of operations.

Kalera may be unable to successfully integrate &ever in order to realize the anticipated benefits of the &ever Acquisition or do so within the intended time frame.

Kalera has and will be required to devote significant management attention and resources to integrating the business practices and operations of &ever with Kalera. This integration may prove to be more difficult, costly and time-consuming than expected, which could cause us not to realize some or all of the anticipated benefits from the &ever Acquisition. Potential difficulties we may encounter as part of the integration process include the following:

| 9 |

| ● | any delay in the integration of management teams, strategies, operations, products and services; | |

| ● | diversion of the attention of management of Kalera or &ever as a result of the &ever Acquisition; | |

| ● | differences in business backgrounds, corporate cultures and management philosophies that may delay successful integration; | |

| ● | the ability to retain key employees; | |

| ● | potential unknown liabilities and unforeseen increased expenses or delays associated with the &ever Acquisition, including costs to integrate &ever beyond current estimates; and | |

| ● | the disruption of, or the loss of momentum in, either Kalera’s or &ever’s ongoing operations or inconsistencies in standards, controls, procedures and policies. |

Any of these factors could adversely affect &ever’s ability to maintain relationships with customers, suppliers, employees and other constituencies or Kalera’s ability to achieve the anticipated benefits of the &ever Acquisition or could reduce earnings or otherwise adversely affect Kalera’s business, financial condition and results of operations after the &ever Acquisition.

Kalera’s growth plans depend on deploying new production facilities, which will require significant expenditures and may be subject to delays in construction and unexpected costs due to governmental approvals and permitting requirements, reliance on third parties for construction, delays relating to material delivery and supply chains, and fluctuating material prices.

Kalera’s build-out of new production facilities will be dependent on a number of key inputs and their related costs including materials such as steel, aluminum, plastic materials, electronic components, horticultural lights, and other supplies, as well as access to electricity, internet, and other local utilities. Any significant interruption or negative change in the availability or economics of the supply chain for key inputs for new facility build-out could materially impact Kalera’s business, financial condition and operating results. Kalera plans to rely on local contractors for the building of its production facilities. If Kalera or its contractors encounter unexpected costs, delays or other problems in building any production facility, Kalera’s financial position and ability to execute on its growth strategy could be negatively affected. Any inability to secure required materials and services to build out such facility, or to do so on appropriate terms, could have a materially adverse impact on Kalera’s business, financial condition and operating results. Kalera may also face unexpected delays in obtaining the required governmental permits and approvals in connection with the build-out of its planned facilities which could require significant time and financial resources and delay its ability to operate these facilities.

The costs to procure such materials and services to build new facilities may fluctuate widely based on the impact of numerous factors beyond Kalera’s control including, international, economic and political trends, foreign currency fluctuations, inflation, global or regional consumptive patterns, speculative activities and increased or improved production and distribution methods.

COVID-19 continues to impact worldwide economic activity, and the governments of many countries, states, cities and other geographic regions have taken preventative or protective actions, which are creating disruption in global supply chains such as closures or other restrictions on the conduct of business operations of manufacturers, suppliers and vendors. The recovery from COVID-19 also may have risks in that increased economic activity globally or regionally may result in high demand for, and constrained access to, materials and services required for Kalera to construct and commission new facilities, which may lead to increased costs or delays that could materially and adversely affect Kalera’s business.

| 10 |

Global demand on shipping and transport services may cause delays in key input supply, which could impact Kalera’s ability to obtain materials or build its production facilities in a timely manner. These factors could otherwise disrupt the Group’s operations and could negatively impact its business, financial condition and results of operations. Logistical problems, unexpected costs, and delays in production facility construction, whether or not caused by the COVID-19 pandemic, which cannot be directly controlled by Kalera, may cause prolonged disruption to or increased costs of third-party transportation services used to ship materials, which could negatively affect Kalera’s facility building schedule, and more generally its business, financial condition, results of operations and prospects. If Kalera experiences significant unexpected delays in construction, it may have to delay or limit its growth depending on the timing and extent of the delays, which could harm Kalera’s business, financial condition and results of operation.

Inflation and increases in operating costs could materially and adversely impact Kalera’s business, financial position, results of operations, and cash flows.

The cost of producing and supplying Kalera’s products is affected by many factors, some of which can be volatile and some of which may be challenging. The cost of producing and supplying Kalera’s products could be impacted by significant inflation in labor, raw materials, energy and other items necessary to produce and supply our products. Kalera may not be able to increase prices to pass through all cost inflation or to improve its productivity sufficiently to nullify such impact of cost inflation, which could have a material adverse impact on Kalera’s business, financial condition, results of operations, and cash flows.

A delay in the completion of, or cost overruns in relation to, the construction of new facilities may affect Kalera’s ability to achieve its operational plan and full schedule of production, thereby adversely impacting Kalera’s business and results of operations.

As of the date of this prospectus, Kalera has three large-scale facilities under construction, which are expected to be completed during 2022 and 2023. For the large-scale facilities, Kalera leases buildings but bears the cost associated with customizing the buildings for its vertical farming operations. For customizing the buildings, Kalera relies on third party constructors and other service providers. Any delay by such third parties in the completion of construction may result in a decrease in revenues expected to be received by Kalera from operations as a result of the commencement of full-scale operations on a date later than originally expected, thereby adversely impacting Kalera’s business and results of operations, especially if completion of construction is delayed on several large-scale production facilities at the same time. The construction of new facilities is also subject to other risks that may cause delays or cost overruns, including issues tied to material delivery, supply chains, fluctuating material prices, transportation services, electricity and other local utilities. These risks may in turn cause disruptions to operations and the need to implement changes in production to adapt to such delays, including the commissioning of systems before final completion, all of which could have a material adverse effect on production and Kalera’s business, results of operations, cash flows, financial condition and/or prospects.

Production ramp-up time is dependent on a number of factors, all of which may affect full schedule of production and yields achieved

Kalera currently has five large-scale facilities in operation, all in production ramp-up phase. The estimated time it takes to ramp-up the production and the production yields achieved are subject to several factors, some of which are beyond Kalera’s control. For example, COVID-19, which significantly impacted the foodservice industry in Central Florida and beyond, resulted in lower production needs. As a consequence, Kalera may have to slow down the ramp-up of its production from a large-scale facility and Kalera may also need to alter the proportion or production that is planned for either the retail market or the food service industry.

| 11 |

Obtaining good production yields, is dependent on a number of factors, where the most important is achieving good environmental conditions at the facilities, hereunder temperature, humidity and sufficient airflow. Additional factors include supplying adequate light to the crops, water, and fertilizers. Climate control, air flow, lighting, water treatment, irrigation, and nutrient dosage equipment may break down due to several possible causes, some of which are beyond Kalera’s control. Returning down equipment back to operation after a breakdown event may be delayed due to slow response time by manufacturers, suppliers, dealers, or repair service providers and/or by delayed availability of replacement parts.

Ramping up and maintaining strong production yields is also dependent on availability and development of a trained work force. Lack of a trained work force may negatively affect production ramp-up plans and yields achieved.

Should the production ramp-up phase take longer than projected at one or several facilities or if Kalera does not succeed in obtaining strong production yields, this could have a material adverse effect on production and Kalera’s business, results of operations, cash flows, financial condition and/or prospects.

The industry in which Kalera operates is highly competitive and Kalera may not be able to compete successfully in such industry.

Kalera competes in an industry still under establishment that is increasingly competitive. The competition is comprised of both traditional farming and companies in CEA. Kalera expects to continue to experience competition from both existing and new competitors, some of which are more established and who may have (i) greater capital and/or commercial, marketing and technical resources, (ii) longer operating histories and/or (iii) superior brand recognition. Kalera’s competitors may be able to adapt more quickly to new or emerging technologies, changes in customer requirements and changes in the regulatory environment. In addition, current and potential competitors have established or may establish financial or strategic relationships among themselves or with existing or potential customers or other third parties. Accordingly, new competitors or alliances among competitors could emerge and rapidly acquire significant market share. Kalera’s competitors may also improve their relative competitive position by successfully introducing new products or products that can be substituted for Kalera’s products, improving their production processes, or expanding their capacity or production capabilities. This could put pressure on Kalera to reduce its prices, resulting in lower profitability or, in the alternative, cause Kalera to lose market share if Kalera fails to reduce prices. If Kalera is unable to keep pace with its competitors’ product and manufacturing process innovations or cost position, it could harm Kalera’s results of operations, financial condition and cash flows.

Further, Kalera believes that competitive pressure will likely increase as early entrants into the market start to show revenue growth and profitability. If Kalera is unable to remain competitive, this could have a material adverse effect on its revenues, profitability, liquidity, cash flow, financial positions and/or prospects.

If Kalera fails to develop and maintain its brand, its business could suffer.

Kalera’s continuing mission is to build an iconic vertical farming brand that is focused on sustainable and technology driven agriculture. Kalera’s success depends on its ability to maintain and grow the value of the Kalera brand. Maintaining, promoting and positioning Kalera’s brand and reputation will depend on, among other factors, the success of Kalera’s product offerings, food safety, quality assurance, marketing and merchandising efforts, Kalera’s continued focus on the environment and sustainability and Kalera’s ability to provide a consistent, high-quality consumer and customer experience. If Kalera is unable to promote its brand successfully or if its competitors’ marketing efforts are more effective, Kalera could fail to capture market share. In addition, any negative publicity, regardless of its accuracy, could impair Kalera’s business.

| 12 |

There can be no assurance that Kalera’s products will always comply with the standards set for its products. In addition, Kalera has no control over its products once purchased by consumers. Accordingly, consumers may use Kalera’s products in a manner that is inconsistent with Kalera’s directions or store Kalera’s products for long periods of time, which may adversely affect the quality and safety of Kalera’s products. If consumers do not perceive Kalera’s products to be safe or of high quality, then the value of Kalera’s brand would be diminished, and its business, results of operations and financial condition would be adversely affected. Real or perceived quality or food safety concerns or failures to comply with applicable food regulations and requirements, whether or not ultimately based on fact and whether or not involving Kalera (such as incidents involving Kalera’s competitors) may have a substantial and adverse effect on Kalera’s brand, reputation and operating results.

Further, the growing use of social and digital media by Kalera, Kalera’s customers and third parties increases the speed and extent that information or misinformation and opinions can be shared. Negative publicity about Kalera, Kalera’s partners, any person associated with Kalera, including board members and key employees and/or Kalera’s products on social or digital media, or in general, could seriously damage Kalera’s brand and reputation. Brand value is based on perceptions of subjective qualities, and any incident that erodes the trust and loyalty of Kalera’s consumers, customers or distributors, including adverse publicity or a governmental investigation, litigation or regulatory enforcement action, could significantly reduce the value of Kalera’s brand and significantly damage its business. If Kalera does not achieve and maintain a favorable perception of its brand, its business, financial condition and results of operations could be adversely affected.

Kalera’s success, competitive position and future revenues will depend in part on its ability to further develop and protect its intellectual property and know-how.

Kalera’s intellectual property mainly relates to production processes and methods, plant nutrient mixture formulas, custom hardware, software code, and its trademarks. Our intellectual property forms the foundation of Kalera and drives the key elements of the business strategy. Any failure by Kalera in protecting its intellectual property rights adequately could result in its competitors offering similar products, potentially resulting in the loss of some of its competitive advantage and a decrease in its revenue which would adversely affect its business, prospects, financial condition, operating results and/or prospects. Kalera’s success depends, at least in part, on its ability to further develop and protect its intellectual property. Kalera relies on a combination of patents, trade secrets, including know-how, limiting access to key information, confidentiality provisions in agreements, confidentiality procedures and IT security to protect its intellectual property rights. Kalera cannot give any assurance that the measures implemented to protect intellectual property rights will give satisfactory protection, that its intellectual property rights can be successfully defended and asserted in the future or that third parties will not infringe upon or misappropriate any such rights. Adequate remedies may not be available in the event of an unauthorized use or disclosure of its production expertise or proprietary plant science. Intellectual property disputes and proceedings and infringement claims could be burdensome and may result in a significant distraction for management and significant expense. Whether or not measures to secure the intellectual property and other confidential information are successful, such information may still become known to existing or new competitors or be independently developed.

Kalera’s failure to process, obtain or maintain adequate protection of its intellectual property rights for any reason, may have a material adverse effect on Kalera’s business, results of operations, financial condition and/or prospects.

Where Kalera believes patent protection is not appropriate or obtainable, Kalera relies on trade secrets to protect some of its technology and proprietary information. However, trade secrets can be difficult to protect. The misappropriation or other activities that may compromise Kalera’s trade secrets may lead to a reduction or loss of its competitive advantages resulting from such trade secrets. Further, litigating a claim that a third party had misappropriated Kalera’s trade secrets would be expensive and time consuming, and the outcome may be unpredictable. Moreover, if Kalera’s competitors independently develop similar knowledge, methods and know-how, it will be difficult for Kalera to enforce its rights and its business could be harmed.

| 13 |

Further, Kalera may be required to make significant capital investments into the research and development of production methods, plant nutrient mixture formulas, custom hardware and software codes and other intellectual property as Kalera develops, improves and scales its processes, technologies and products, and failure to fund and make these investments, or underperformance of the technology funded by these investments, could severely impact Kalera’s business, financial condition, results of operations and prospects.

Kalera currently relies on a limited number of facilities for all of its operations.

As of the date of this prospectus, Kalera has five large-scale facilities in operation. Adverse changes or developments affecting any of these facilities could impair its ability to produce its products and fulfill its contractual obligations. Any shutdown or period of reduced production at a single facility, which may be caused by regulatory noncompliance or other issues, as well as other factors beyond its control, such as severe weather conditions, natural disaster, fire, power interruption, work stoppage, disease outbreaks or pandemics (such as COVID-19), equipment failure or delay in supply delivery, would significantly disrupt its ability to grow and deliver its produce in a timely manner, meet its contractual obligations and operate its business. As an example, Kalera’s Atlanta facility experienced intermittent faults on electrical components that drive the grow lights. The intermittent outages forced delays in shipments to new customers, which negatively impacted revenues in May, June, and July 2021.

The equipment in Kalera’s facilities is costly to replace or repair, and its equipment supply chains may be disrupted in connection with pandemics, such as COVID-19, trade wars or other factors. If any material amount of its machinery were damaged, it would be unable to predict when, if at all, Kalera could replace or repair such machinery or find suitable alternative machinery, which could adversely affect its business, financial condition, results of operations and prospects. Any insurance coverage that Kalera has acquired may not be sufficient to cover all of its potential losses and may not continue to be available to it on acceptable terms, or at all.

Kalera’s commercial success is dependent on its ability to enter into produce distribution agreements and other agreements with third parties.

Kalera’s large-scale production facilities generally serve customers within a 300-mile radius of the relevant facility. As Kalera continues its roll-out plan by building new facilities, Kalera may be dependent on entering into new produce distribution agreements with new customers located within the target radius or renegotiating existing produce distribution agreements to also cover such new areas. Should Kalera be unsuccessful in entering into new produce distribution agreements, this could in turn have a material adverse effect on its business, results of operations, financial condition and/or prospects.

Kalera uses a limited number of distributors and large retailers for the substantial majority of its sales, and if it experiences the loss of one or more of its distributors or large retailers and cannot replace them in a timely manner, Kalera’s results of operations may be adversely affected.

Many customers purchase Kalera’s products through food distributors which purchase, store, sell, and deliver its products to food service providers or retailers. Alternatively, some large retail customers may purchase products directly from Kalera. For the six months ended June 30, 2022, Kalera’s largest customers in terms of their respective percentage of sales included the following: Publix (26%), H-E-B Grocery (16%), Kroger (10%), Sysco (9%), Harvill’s Produce Co. (6%) and US Foods (5%). For the foreseeable future, Kalera expects that most of its sales will be made through a core number of distributors or directly to a core number of large retailers. Kalera does not have short-term or long-term commitments or minimum purchase volumes in its contracts with the distributors or large retailers that ensure future sales of its products. If Kalera loses one or more of its significant distributors or large retailers and cannot replace the distributor or large retailer or do so in a timely manner, its business, results of operation and financial condition may be materially adversely affected.

| 14 |

Consolidation of customers or the loss of a significant customer could negatively impact Kalera’s sales and profitability.

Supermarkets in North America continue to consolidate. This consolidation has produced larger, more sophisticated organizations with increased negotiating and buying power that are able to resist price increases, as well as operate with lower inventories, decrease the number of brands that they carry and increase their emphasis on private label products, all of which could negatively impact Kalera’s business. The consolidation of retail customers also increases the risk that a significant adverse impact on their business could have a corresponding material adverse impact on Kalera’s business.

The loss of any large customer, the reduction of purchasing levels or the cancellation of any business from a large customer for an extended length of time could negatively impact Kalera’s sales and profitability. Furthermore, as retailers consolidate, they may reduce the number of branded products they offer in order to accommodate private label products and generate more competitive terms from branded suppliers. Consequently, Kalera’s financial results may fluctuate significantly from period to period based on the actions of one or more significant retailers. A retailer may take actions that affect Kalera for reasons that it cannot always anticipate or control, such as their financial condition, changes in their business strategy or operations, the introduction of competing products or the perceived quality of its products. Despite operating in different channels, Kalera’s retailers sometimes compete for the same consumers. Because of actual or perceived conflicts resulting from this competition, retailers may take actions that negatively affect Kalera.

Kalera may face difficulties as it expands its operations into geographical locations in which it has no prior operating experience.

Kalera’s growth strategy includes developing new vertical farming facilities and the expansion of its product lines.

Kalera’s newest facilities include those in Atlanta, Georgia, which began operations in March 2021, Houston, Texas, which began operations in October 2021, and Denver, which began operations in April 2022. Internationally, Kalera’s newest facility is in Kuwait, acquired through the &ever Acquisition, which began operations in March 2020 and continued ramp-up in October 2021 after Kuwait’s COVID-19 related international travel ban had been lifted. Any substantial delay in bringing these facilities up to full production on our current schedule may hinder Kalera’s ability to produce all of the estimated produce and/or achieve its expected financial performance. Even if Kalera’s new facilities are brought up to full production according to our current schedule, they may not provide all of the operational and financial benefits Kalera expects to receive.

Identifying, planning, developing, constructing and finishing new large-scale vertical farming facilities has required and will continue to require substantial time, efforts and resources. Kalera may be unsuccessful in identifying available sites that are conducive to its planned projects, and even if identified, Kalera may ultimately be unable to lease or purchase the land for any number of reasons. Additionally, if Kalera overestimates market demand and expands into new locations too quickly, Kalera may have significantly underutilized assets and may experience reduced profitability. If Kalera does not accurately align capacity at its facilities with demand, its business, financial condition and results of operations could be adversely affected. Kalera intends to further expand its footprint in order to enter into new markets. It may be difficult for Kalera to understand and accurately predict taste preferences and purchasing habits of consumers in these new geographic markets. It is costly to establish, develop and maintain wide ranging operations and develop and promote its brand in multiple markets. As Kalera expands its business into new locations, Kalera may encounter regulatory, legal, personnel, technological and other difficulties that increase its expenses and/or delay its ability to become profitable in such locations, which may have a material adverse effect on its business and brand.

| 15 |

A continued rollout of Kalera’s in-store grow towers and grow boxes is dependent on Kalera being able to reach agreements with new supermarket chains. Further, Kalera may spend time and resources developing facilities at the expense of other appropriate facilities, which may ultimately have been a better selection or more profitable location, or the project start date for new facilities may have to be postponed due to existing facilities and/or other operations and projects requiring more resources than originally estimated.

A key element of Kalera’s growth strategy depends on Kalera’s ability to develop, produce and market new products and improvements to its existing products that meet its standards for quality and appeal to consumer preferences. The success of Kalera’s innovation and product development efforts is affected by its ability to anticipate changes in consumer preferences, the technical capability of its innovation staff in developing and testing product prototypes, including complying with applicable governmental regulations, and the success of its management and sales and marketing teams in introducing and marketing new products. Failure to develop, produce and market new products that appeal to consumers may lead to a decrease in Kalera’s growth, sales and profitability. The development and introduction of new products requires substantial research, development and marketing expenditures, which Kalera may be unable to recoup if the new products do not gain widespread market acceptance. Kalera may invest in product opportunities that are not ultimately successful or profitable. If Kalera is unsuccessful in meeting its objectives with respect to new or improved products, its business could be harmed.

Kalera’s sales and operating results will be adversely affected if it fails to implement our growth strategy successfully or if it invests resources in a growth strategy that ultimately proves unsuccessful as Kalera expands its operations into new geographical locations.

Kalera may not be able to identify suitable acquisition candidates or consummate acquisitions on acceptable terms, and as Kalera acquires companies or technologies in the future, they could prove difficult to integrate, disrupt Kalera’s core business, dilute stockholder value and adversely impact Kalera’s business and operating results and the value of your investment.

As part of Kalera’s business strategy, it regularly evaluates investments in, or acquisitions of, complementary businesses, joint ventures, services, products and technologies. Kalera acquired Vindara, Inc. (“Vindara”) and &ever in 2021. Kalera intends to continue to pursue complementary acquisitions in the future, expand its customer base and provide access to new markets and increase benefits of scale. Acquisitions involve certain known and unknown risks that could cause actual growth or operating results to differ from expectations. For example:

| ● | Kalera may not be able to identify suitable acquisition candidates or to consummate acquisitions on acceptable terms; | |

| ● | Kalera may pursue additional international acquisitions, which could pose more risks than domestic acquisitions; | |

| ● | Kalera competes with others to acquire complementary products, technologies and businesses, which may result in decreased availability of, or increased price for, suitable acquisition candidates; |

| 16 |

| ● | Kalera may not be able to obtain the necessary financing, on favorable terms or at all, to finance any or all of its potential acquisitions; | |

| ● | Kalera may ultimately fail to consummate an acquisition even if Kalera announces that it plans to acquire a technology, product or business; and | |