Form 10-K Jaguar Health, Inc. For: Dec 31

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

COMMISSION FILE NO.

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification No.) |

(Address of principal executive offices)

Registrant’s telephone number, including area code:

(

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ◻

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ◻

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ⌧

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ◻ | Accelerated filer ◻ | Smaller reporting company | |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

As of June 30, 2021, the aggregate market value of the registrant’s common stock held by non-affiliates was approximately $

The number of shares of the registrant’s common stock outstanding as of March 10, 2022 was

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement for the registrant’s 2022 Annual Meeting of Stockholders, or Proxy Statement, to be filed within 120 days of the end of the fiscal year ended December 31, 2021 are incorporated by reference in Part III hereof. Except with respect to information specifically incorporated by reference in this Form 10-K, the Proxy Statement is not deemed to be filed as a part hereof.

TABLE OF CONTENTS

i

PART I

Forward-looking statements

This Form 10-K contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements other than statements of historical facts contained in this Form 10-K, including statements regarding our future results of operations and financial position, business strategy, prospective products, product approvals, research and development costs, timing of receipt of clinical trial, field study and other study data, and likelihood of success, commercialization plans and timing, other plans and objectives of management for future operations, and future results of current and anticipated products are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “aim,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Form 10-K are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Form 10-K and are subject to a number of risks, uncertainties and assumptions described under the sections in this Form 10-K titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Form 10-K. Forward-looking statements are subject to inherent risks and uncertainties, some of which cannot be predicted or quantified and some of which are beyond our control. The events and circumstances reflected in our forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. Moreover, we operate in a dynamic industry and economy. New risk factors and uncertainties may emerge from time to time, and it is not possible for management to predict all risk factors and uncertainties that we may face. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

Jaguar Health, our logo, Napo Pharmaceuticals, Napo Therapeutics, Mytesi, Equilevia, Canalevia, Canalevia-CA1, Canalevia-CA2, and Neonorm are our trademarks that are used in this Form 10 K. This Form 10 K also includes trademarks, tradenames and service marks that are the property of other organizations. Solely for convenience, trademarks and tradenames referred to in this Form 10 K appear without the ©, ® or ™ symbols, but those references are not intended to indicate that we will not assert, to the fullest extent under applicable law, our rights or that the applicable owner will not assert its rights, to these trademarks and tradenames.

ITEM 1. BUSINESS

BUSINESS

Jaguar Health, Inc. (“Jaguar” or the “Company”) is a commercial stage pharmaceuticals company focused on developing novel, plant-based, non-opioid, and sustainably derived prescription medicines for people and animals with GI distress, including chronic, debilitating diarrhea. Jaguar Animal Health is a tradename of Jaguar Health. Our wholly owned subsidiary, Napo Pharmaceuticals, Inc. (“Napo”), focuses on developing and commercializing proprietary plant-based human pharmaceuticals for the global marketplace from plants or plant products used traditionally in rainforest areas. Napo’s marketed drug Mytesi (crofelemer 125 mg delayed-release tablets) is a first-in-class oral botanical drug product approved by the U.S. Food and Drug Administration (“FDA”) for the symptomatic relief of noninfectious diarrhea in adults with HIV/AIDS on antiretroviral therapy. To date, this is the only oral plant-based botanical prescription medicine approved under the FDA’s Botanical Guidance. Jaguar Animal Health’s Canalevia-CA1 (crofelemer delayed-release tablets) drug is the first and only oral plant-based prescription product that is FDA conditionally approved to treat chemotherapy-induced diarrhea (“CID”) in dogs. Canalevia-CA1

1

is a canine-specific formulation of crofelemer. Napo Therapeutics S.p.A., Napo’s majority owned Italian subsidiary, focuses on expanding crofelemer access in Europe.

Jaguar, formerly known as Jaguar Animal Health, Inc., was founded in San Francisco, California as a Delaware corporation on June 6, 2013 (inception). The Company was a majority-owned subsidiary of Napo until the close of the Company's initial public offering on May 18, 2015. The Company was formed to develop and commercialize first-in-class prescription and non-prescription products for companion and production animals and horses. The Company's first non-prescription commercial products, Neonorm Calf and Neonorm Foal, were launched in 2014 and 2016, respectively.

On July 31, 2017, Jaguar completed a merger with Napo pursuant to the Agreement and Plan of Merger dated March 31, 2017, by and among Jaguar, Napo, Napo Acquisition Corporation (“Merger Sub”), and Napo's representative (the “Merger Agreement”). In accordance with the terms of the Merger Agreement, upon the completion of the merger, Merger Sub merged with and into Napo, with Napo surviving as the wholly-owned subsidiary (the “Merger” or “Napo Merger”). Immediately following the Merger, Jaguar changed its name from “Jaguar Animal Health, Inc.” to “Jaguar Health, Inc.” Napo now operates as a wholly-owned subsidiary of Jaguar focused on human health including the ongoing development of crofelemer and commercialization of Mytesi.

On March 15, 2021, Jaguar established Napo EU S.p.A (which changed its name in January 2022 to Napo Therapeutics S.p.A. “Napo Therapeutics”) based in Milan, Italy as a subsidiary of Napo. Napo Therapeutics’ mission is to provide access to crofelemer in Europe to address significant rare/orphan disease indications, including, initially, two key orphan target indications: Short bowel syndrome with intestinal failure (“SBS-IF”), and congenital diarrheal disorders (“CDD”). On November 3, 2021, Napo Therapeutics merged with Dragon SPAC S.p.A. (“Dragon SPAC”).

On December 13, 2021, the European Medicines Agency (“EMA”) granted orphan-drug designation (“ODD”) for crofelemer for short bowel syndrome (“SBS”) indication in the European Union following review of the ODD application Napo submitted to the EMA in September 2021. Following this decision from the EMA, Napo Therapeutics is initiating efforts to commence clinical development of crofelemer in both adult and pediatric SBS patients in support of the company’s key focus on leveraging the EMA’s accelerated conditional marketing authorization pathway in Europe for these rare diseases. Napo Therapeutics has also agreed to support an investigator-initiated trial (“IIT”) which will provide proof of concept (“POC”) support for potential expanded access programs for crofelemer for patients with CDD and/or SBS patients with intestinal failure (“IF”). The expanded access program will be initiated following completion of this study and upon publication of POC results, potentially in 2023. Crofelemer previously received ODD in the U.S. from the FDA for SBS. SBS affects approximately 10,000 to 20,000 people in the U.S., according to the Crohn's & Colitis Foundation, and it is estimated that the population of SBS patients in Europe is approximately the same size. Despite limited treatment options, the global SBS market exceeded $568 million in 2019 and is expected to reach $4.6 billion by 2027, according to a report by Vision Research Reports.

On December 21, 2021, we received conditional approval from the FDA to market Canalevia-CA1 (crofelemer delayed-release tablets), our oral plant-based prescription drug and the only drug for the treatment of CID in dogs. We expect Canalevia-CA1 to be available to multiple leading veterinary distributors in the U.S. in the second quarter of 2022 after we complete a post-approval update to the chemistry, manufacturing and controls (“CMC”) related to crofelemer. This update will align with the CMC requirements related to crofelemer used as the active ingredient in Mytesi.

On January 4, 2022, we announced the launch of Canalevia-CA1 (crofelemer delayed-released tablets), which is being commercialized as a prescription drug product under the Company’s Jaguar Animal Health tradename. Canalevia-CA1 is a tablet that is given orally and can be prescribed for home treatment of CID. Canalevia-CA1 is a canine-specific formulation of crofelemer that is conditionally approved by the FDA under application number 141-552. Conditional approval allows for commercialization of the product while Jaguar Animal Health continues to collect the substantial evidence of effectiveness required for a full approval. We have received Minor Use in a Major Species (“MUMS”) designation from the FDA for Canalevia-CA1 to treat CID in dogs. FDA has established a "small number" threshold for minor use in each of the seven major species covered by the MUMS act. The small number threshold is currently 70,000 for dogs, representing the largest number of dogs that can be affected by a disease or

2

condition over the course of a year and still have the use qualify as a minor use. We expect Canalevia-CA1 to be available to multiple leading veterinary distributors in the U.S. in the second quarter of 2022 after we complete a post-conditional-approval update to the CMC related to crofelemer. In the field of animal health, we are continuing limited activities related to developing and commercializing first in class gastrointestinal products for dogs, dairy calves, foals, and high value horses.

Most of the activities of the Company are focused on the commercialization of Mytesi and Canalevia-CA1 and the ongoing clinical development of crofelemer for the prophylaxis of diarrhea in adult patients receiving targeted cancer therapy. In June 2021, Napo Pharmaceuticals recruited Dr. Darlene Horton, as the Chief Medical Officer (“CMO”) of Napo Pharmaceuticals to support the ongoing clinical development activities for prescription products for human health. Dr. Horton is a 25-year veteran of the biotech and pharmaceutical industry. Prior to joining Napo, she led clinical development and regulatory strategy as CMO at Coherus Biosciences, Itero Biopharmaceuticals, and SMC Biotechnology. As Head of Clinical and Medical Affairs at Scios, she led the clinical development program that led to the approval of Natrecor® and was on the senior executive team when Scios was acquired by JNJ for $2.4B. At JNJ, she co-led (with strategic marketing) the cardiovascular therapeutic area when JNJ in-licensed and began developing the blockbuster drug Xarelto®. She also served as CEO at Nile Therapeutics and TulangCo Inc. Dr. Horton completed her Pediatric Cardiology fellowship and Pediatrics Residency at UCSF. She holds M.D. and B.S. in Microbiology degrees from the University of Florida.

We believe Jaguar is poised to realize a number of synergistic, value adding benefits—an expanded pipeline of potential blockbuster human follow on indications of crofelemer, and a second generation anti secretory agent—upon which to build global partnerships. Jaguar, through Napo, holds global unencumbered rights for crofelemer, Mytesi, and Canalevia-CA1. Additionally, several of the drug product opportunities in Jaguar’s crofelemer pipeline are backed by Phase 2 and proof of concept evidence from human clinical trials.

Crofelemer is a novel, first in class anti secretory agent which has a normalizing effect on electrolyte and fluid balance while acting locally in the gut, and this mechanism of action has the potential to benefit multiple disorders that cause gastrointestinal distress, including diarrhea and abdominal discomfort. Crofelemer is also in development for possible follow on indications, including prophylaxis for cancer therapy related diarrhea (“CTD”); for rare disease indications for symptomatic treatment of infants and children with CDD and for adult and pediatric patients with SBS-IF. As mentioned above, crofelemer has received ODD for SBS in the US and in the European Union (“EU”). Furthermore, the drug is being evaluated for management of diarrhea and abdominal discomfort in inflammatory bowel disease (“IBD”); diarrhea-predominant irritable bowel syndrome (“IBS-D”); and for idiopathic/functional diarrhea. A second generation proprietary anti secretory agent, NP-300 (lechlemer), is undergoing preclinical development for symptomatic relief and treatment of diarrhea in patients with acute infection from cholera.

Napo has a direct sales force of 8 sales representatives and a national sales director covering U.S. geographies with the highest commercial potential. In 2019, we hired Ian Wendt, an industry veteran with a broad range of experience that includes commercializing supportive care and HIV treatments, as Vice President of Commercial Strategy. He was promoted to Chief Commercial Officer in 2020. With support provided by concomitant marketing, promotional activities, patient education programs and peer education initiatives described below, we expect continued growth in the number of patients treated with Mytesi. Mr. Wendt will lead disease state educational initiatives that will pave the way for crofelemer’s final development for the CTD market and our commercial role for this next important, potential indication for Mytesi. Additionally, he is leading commercialization activities for Canalevia-CA1 in the U.S. veterinary market.

A key component of our marketing strategies for Mytesi in 2021 was focused on the transition of Mytesi distribution to a closed network of specialty pharmacies rather than to wholesalers that resell the product to retail pharmacies. This transition was intended to help remove access barriers for patients receiving Mytesi and includes services such as a higher level of support for prior authorizations, appeals, adherence counseling, and home delivery options. While patients often visit retail pharmacies for short-term or uncomplicated medical needs, specialty pharmacies focus on serving patients with complex and chronic medical conditions like HIV. The transition to a closed network of specialty pharmacies is expected to result in a meaningful reduction in Mytesi distribution costs and

3

prepare our U.S. commercial distribution network for future indication expansion of crofelemer to other populations of patients with complex medical needs. However, when we made the full transition on September 3, 2021, to selling to specialty pharmacies, it resulted in an underrepresentation of actual Mytesi utilization, as wholesalers depleted their inventory during the transition process.

The goal of Napo’s sales team is to deliver a frequent and consistent selling message to targeted, high volume prescribers of HIV antiretroviral therapies (“ART”) and to gastroenterologists who see large numbers of HIV patients. In 2017 we released the results of a survey of 350 people living with HIV and AIDS regarding the topic of “Talking to Your Doctor About Symptoms.” The survey results show that diarrhea remains prevalent in those living with HIV/AIDS, with 27% of respondents reporting that they currently have diarrhea, and 56% reporting that they have had diarrhea in the past. Additionally, the results of a 2017 Napo sponsored survey of 271 U.S. board certified gastroenterologists indicate that the number one GI complaint for people living with HIV/AIDS is diarrhea, and 93% of U.S. gastroenterologists see patients with HIV/AIDS in their practice.

Key to the success of our sales representatives in growing Mytesi sales is segmenting and targeting the right health care providers—those HIV treaters who are high prescribers of ART and those gastrointestinal doctors who see large populations of people living with HIV/AIDS. The target list of prescribers for our sales reps includes a pool of approximately 1,300 high volume ART prescribing HIV specialists, and gastroenterologists who see the largest number of people living with HIV/AIDs, and we’ve strategically focused our sales force in the US geographies with the highest potential, including San Francisco, Sacramento, Seattle, southern California, Arizona, Nevada, Florida, New York City/Long Island, Connecticut, New Jersey, Pennsylvania, Maryland, Kansas, Texas, Missouri, Chicago, Michigan, Atlanta, Louisiana, DC, Virginia, North Carolina, South Carolina, Indianapolis, and Ohio.

Medical education presentations led by health care providers (“HCPs”) participating in the Napo Speakers Bureau—a group that includes HIV/AIDS treaters, infectious disease specialists, gastroenterologists, colorectal surgeons, nurse practitioners, doctors of pharmacology, and physician assistants—focus on the prevalence and pathophysiology of gastrointestinal consequences of HIV infection and on the latest treatment options for HIV related diarrhea. Presentations given by patient advocate members provide information to HIV/AIDS patients about the prevalence of diarrhea in people living with HIV/AIDS (“PLWHA”) and offer guidance about talking to HCPs regarding diarrhea related concerns.

With the introduction of newer antiretroviral (“ARV”) drug therapies, there has been a reduction in the severity of ARV induced diarrhea. However, a significant portion of this patient population still suffers from diarrhea caused by HIV enteropathy, which is due to the direct and indirect effects of HIV on the intestinal mucosa. Chronic diarrhea remains a significant complaint of PLWHA, particularly those who are older and have lived with the virus in their gut for 10+ years. According to data from the U.S. Centers for Disease Control and Prevention, currently more than 70% of people living with HIV are over age 50 and have lived with HIV for more than 10 years.

Napo is on many AIDS Drug Assistance Program (“ADAP”) formularies. ADAPs provide lifesaving HIV treatments to low income, uninsured, and underinsured individuals living with HIV/AIDS in all 50 states and the territories. The ADAP program provides Mytesi free of charge to patients who qualify and copay support for some patients who have insurance coverage. Based on data from healthcare research firm Decision Resource Group, approximately 86% of ADAP eligible US lives now have access to Mytesi, which is now on the ADAP formularies for 30 states, including the four programs with the largest enrollment.

In May 2020, Napo launched a program to educate insurance companies about the benefits of Mytesi and negotiate better access to Mytesi for commercially insured patients. We believed that our enhanced Mytesi market access strategy engaged select payors in contracting discussions with the objective of removing barriers for patients in order to allow them to more easily start on – and stay on – Mytesi. This initiative represented a commercial opportunity to employ a strategic mechanism that was well-established in the U.S. pharmaceutical industry to help patients access Mytesi.

4

Napo expanded the NapoCares Patient Support Program for Mytesi in April 2020 as part of the Company's enhanced market access strategy. The expansion meaningfully increased co-pay support for commercially insured patients, which also includes allowing the co-pay amount to remain the same whether a patient fills a 30-day or a 90-day prescription of Mytesi. The expansion also increased the income ceiling from two times the Federal poverty limit to five times the Federal poverty limit for our patient assistance program, which will allow more low-income patients to receive Mytesi at no cost. The co-pay program and patient assistance program are components of a comprehensive suite of patient support services Napo rolled out in the second quarter of 2020 with the support of AssistRx, a specialty therapy initiation and patient support company.

On August 2021, Napo signed a license agreement with Napo EU S.p.A. to study, develop, manufacture, and commercialize Napo’s plant-based crofelemer and lechlemer drug product candidates in the European Union (excluding Russia) and in specified non-EU countries in Europe for specific indications, which rights and obligations were assumed by the combined company formed by the merger of Napo Therapeutics with Dragon SPAC (the combined company uses the Napo Therapeutics name). Per the terms of the license agreement, Napo will receive payment of up to $10 million as the initial license fee (to be paid in two installments, the first of which has already been received) as the initial license fee and is eligible to receive additional payments related to milestones, royalties, and product transfers.

In November 2021, Napo Therapeutics appointed Mr. Massimo Mineo, a veteran of the European pharmaceutical industry for 20+ years, as general manager (the equivalent in Europe of chief executive). He has significant experience in the field of orphan-drug development and commercialization activities and his leadership is expected to be instrumental in the ongoing development and commercialization activities for crofelemer for the planned SBS-IF indication in the EU. Mr. Mineo is responsible for the strategy, planning, direction, and implementation of all Napo Therapeutics’ commercial, operational, and product development activities within Europe, with success defined by bringing crofelemer to market for key initial target indications, beginning with SBS-IF and CDD.

In November 2021, Napo Therapeutics announced the appointment of Annabella Amatulli as chief regulatory officer. A recognized expert in global regulatory affairs, Ms. Amatulli is responsible for both high-level strategic planning and hands-on support for Napo Therapeutics’ development programs and licensed products from a regulatory perspective and serves as the primary liaison between Napo Therapeutics and European health authorities.

In January 2022, Napo Therapeutics announced the appointment of Martire Particco, MD, a physician with 30+ years of experience in Europe’s pharmaceutical industry and in clinical practice, as its CMO for the EU-related development activities of Napo Therapeutics. Dr. Particco possesses in-depth experience in the field of orphan and rare diseases, having been involved in the clinical development and launch of Pfizer’s pulmonary hypertension indication for sildenafil and the clinical development of Kerdion Biopharma’s ligneous conjunctivitis indication for plasminogen, with direct experience with patients and experts treating these rare pathologies.

In February 2022, Napo announced the completion of a third-party, investigator-initiated preclinical enterocyte (intestinal cell) in vitro study to evaluate the effects of crofelemer on cells with certain genetic defects that result in specific forms of CDD. Jaguar believes that these study results will support certain requests received from the Office of Orphan Products Development at the U.S. FDA in response to the ODD application Napo filed with the FDA for crofelemer for CDD in infants and children. The data from this study will support the rare disease business model that Napo Therapeutics is pursuing in Europe under its exclusive license for crofelemer from Jaguar and Napo. CDD patients have intestinal failure and morbidity resulting in a failure to thrive due to malabsorption of nutrients and need parenteral nutrition. We believe the novel mechanism of action of crofelemer may have considerable potential to manage the severe secretory loss of electrolytes and fluid resulting in dehydration. There are currently no therapies for CDD except parenteral nutrition. Thus, crofelemer may reduce the associated morbidity and mortality of CDD and lessen the need for total parenteral nutrition (“TPN”).

5

Napo has actively ensured that its intellectual property (“IP”) filings in support of the development of crofelemer for various proposed indications are protected appropriately. The IP portfolio for crofelemer includes the relief and treatment of HIV-associated diarrhea and chemotherapy-induced diarrhea as well as planned indications for inflammatory diarrhea, IBS-D, CID and SBS, with all indications, Napo prioritizes IP protection. Napo currently holds approximately 143 patents, the majority of which do not expire until 2027 - 2031, and approximately 43 patents pending.

In October 2020, Napo initiated its pivotal Phase 3 clinical trial of crofelemer (Mytesi) for prophylaxis of diarrhea in adult cancer patients receiving targeted therapy (OnTarget study). The Phase 3 OnTarget clinical trial is a 24-week (two 12-week stages), randomized, placebo-controlled, double-blind study to evaluate the safety and efficacy of crofelemer in the prophylaxis of diarrhea in adult cancer patients with solid tumors receiving targeted cancer therapy-containing treatment regimens. Patients will be randomized to receive either crofelemer or matching placebo treatment that will start concurrently with the initiation of targeted cancer therapy regimen. The primary endpoint will be assessed at the end of the initial (Stage I) 12-week double-blind placebo-controlled primary treatment phase after the last patient has completed 12 weeks of treatment. After completing the Stage I treatment phase, the subjects will have the option to remain on their assigned treatment arm and reconsent to enter into the Stage II 12-week extension phase. The safety and efficacy of orally administered crofelemer will be evaluated for the prophylaxis of diarrhea in adult cancer patients receiving targeted cancer therapies with or without standard chemotherapy regimens. The assessment of the frequency of diarrhea will be measured by the average number of weekly loose and/or watery stools for the active (crofelemer) or placebo arms over 12-week Stage I treatment period.

A significant proportion of patients undergoing cancer therapy experience diarrhea. Novel “targeted cancer therapy” agents, such as epidermal growth factor receptor (“EGFR”) antibodies and tyrosine kinase inhibitors (“TKIs”), with or without cycle chemotherapy agents, may activate intestinal chloride ion channel-mediated secretory pathways leading to increased electrolyte and fluid content in the gut lumen, which results in passage of loose/watery stools, i.e., secretory diarrhea. With increased approval of several novel targeted therapies, it is estimated that 13.6% of cancer patients in 2020 were eligible for targeted therapies with or without standard chemotherapy regimens, according to a paper published in April 2021 in the journal Annals of Oncology1. According to the National Cancer Institute, in 2020, 1,806,590 new cases of cancer were diagnosed and nearly 250,000 of these newly diagnosed patients could be eligible for available targeted therapies.

Due to the chronic dosing and toxicity associated with targeted therapies, many cancer patients on targeted therapy require drug holidays or dose reductions in their therapy, including those due to diarrhea. By improving stool consistency and reducing the frequency of watery stools, crofelemer is expected to provide improved adherence to the therapeutic dosing of any targeted therapies, potentially leading to better clinical outcomes. We have learned from business development discussions with cancer drug manufacturers that the adoption and continued use of targeted cancer therapies is directly related to the ability of patients to tolerate these therapies—highlighting the importance of supportive care drugs like crofelemer to help manage cancer treatment-related diarrhea in this patient population.

As previously announced, an abstract regarding patient outcomes associated with cancer-related diarrhea (“CRD”) by Napo and Napo's collaborators was accepted for poster presentation at the American Society of Clinical Oncology (ASCO®) Annual Meeting, which was held virtually from June 4-8, 2021. This study found that patients with CRD were 40% more likely to discontinue the chemotherapy or targeted therapy than patients without CRD. The persistence of index cancer therapy and time to switch were also lower for patients with CRD. Strategies to control CRD and continue cancer therapy are urgently needed2.

In addition, two CRD-related abstracts from Napo and its collaborators were accepted for online publication at ASCO. One of these studies found that patients with CRD used significantly more resources, including outpatient services, ED visits, and hospitalizations. Effective prevention of CRD remains an unmet strategy to reduce the overall

1A. Haslam, M.S. Kim, V. Prasad, Updated estimates of eligibility for and response to genome-targeted oncology drugs among US cancer patients, 2006-2020

2Pablo C. Okhuysen, M.D., Lee Schwartzberg, M.D., FACP, Eric Roeland, M.D., FAAHPM, The impact of cancer-related diarrhea on changes in cancer therapy patterns: Real world evidence

6

cost of cancer care3. Findings from the other study indicated that patients with CRD had nearly 2.9 times higher all-cause total cost than patients without CRD after adjusting for covariates. Prevention of CRD may result in a significant reduction in cancer-treatment cost4.

As previously announced in June 2020, the effects of crofelemer (Mytesi) were evaluated in reducing diarrhea associated with the irreversible pan-HER TKI neratinib in female dogs. The data were presented at the American Association for Cancer Research (“AACR”) Annual Meeting II in 2020. The results from the dog study provide further scientific support for the evaluation of crofelemer in providing symptomatic relief of watery diarrhea in patients receiving a targeted cancer therapy drug like neratinib with or without cycle chemotherapy, without the use of antimotility drugs like loperamide, in future clinical studies.

The dog study was conducted without the prophylaxis or concomitant use of loperamide and demonstrated that crofelemer caused an approximate 30% reduction in the incidence and severity of diarrhea associated with daily oral administration of neratinib, which was statistically significant, within the 28-day period. Crofelemer also demonstrated significant improvement in the proportion of responder dogs, and there was a trend for fewer neratinib dose reductions in both crofelemer treatment groups when compared to the control group.

The results and finding from a clinical, third-party investigator-initiated Phase 2 study (called HALT-D) evaluated the effectiveness of crofelemer for reduction of diarrhea in HER2 positive breast cancer patients receiving trastuzumab, pertuzumab, and chemotherapy agents such as docetaxel or pacilitaxel with or without carboplatin. The investigators of the HALT-D study, sponsored by Georgetown University and funded by Genentech, a member of the Roche Group, were presented at the San Antonio Breast Cancer Symposium on December 10, 2021. It has been reported that these pertuzumab-containing regimens cause diarrhea in up to 80% of breast cancer patients and approximately 8 to 12% of patients reach grade 3, which often requires hospitalization. No antidiarrheal medications are currently approved that specifically target the underlying mechanism of CID associated with pertuzumab-containing regimens. Recent studies have shown that EGFR inhibitors cause increased chloride secretion into the lumen of the gut and Crofelemer through its unique and novel mechanism of reducing the chloride-secretory actions of the cystic fibrosis transmembrane conductance regulator (“CFTR”) and calcium-activated chloride channels (CaCC), was considered to be mechanistically- and physiologically-appropriate for reducing the loss of electrolyte and fluid in breast cancer patients receiving this regimen.

The Principal Investigator (“PI”), Paula Pohlmann, MD, PhD, Associated Professor at the University of Texas MD Anderson Cancer Center and formerly from Georgetown University, reported the results of the HALT-D study. This clinical study evaluated 51 breast cancer patients that were eligible to receive at least three cycles of pertuzumab-containing regimen with chemotherapy that were randomly assigned to either crofelemer in cycles 1 and 2 or the control group, in which patients received standard of care. Breakthrough anti-diarrheal medicines (“BAM”) were permitted but not given prophylactically. Findings showed that the primary endpoint, the incidence of diarrhea for at least two consecutive days, was not statistically different for the two groups. However, crofelemer patients demonstrated significantly better outcomes compared to control group patients across a number of key secondary endpoints including reductions in the incidence and severity of diarrhea in cycle 2 based on Investigator and Patient Reported Outcomes (“PRO”) (see Jaguar Health's November 19, 2021 press release). In the presentation, additional findings were reported that showed that CID occurred significantly lesser (by 23%) in the crofelemer group during cycle 1 and crofelemer patients were 1.8 times more likely than control patients to have their diarrhea resolved. These data provide concordance to the planned primary endpoint in Napo’s ongoing phase 3 OnTarget study.

Dr. Pohlmann commented that the HALT-D study showed benefits of crofelemer across a range of important diarrhea-related measures, including its incidence, severity and probability of resolving and that the lack of difference in the primary endpoint was because about 70% of the patients in both groups would have at least two consecutive days of diarrhea regardless of cycle or CID treatment group. The incidence of two consecutive days of diarrhea is

3Lee Schwartzberg, M.D., FACP, Eric Roeland, M.D., FAAHPM, Pablo C. Okhuysen, M.D., Characterizing unplanned resource utilization associated with cancer-related diarrhea

4Eric Roeland, M.D., FAAHPM, Pablo C. Okhuysen, M.D., Lee Schwartzberg, M.D., FACP, Healthcare utilization and costs associated with cancer-related diarrhea

7

typical in cancer patient experiences from receiving chemotherapy regimens and is thus not clinically relevant as it does not differentiate the severity nor duration of CID among treatment groups. Dr. Pohlmann also commented that the secondary endpoints provided a more relevant assessment of CID, which may guide future studies that address this significant comorbidity in cancer patients receiving such regimens.

Napo is also continuing to conduct preclinical and formulation activities to support the evaluation of its second generation, plant-based oral prescription drug product, NP-300 (lechlemer), for its planned evaluation in the symptomatic treatment of diarrhea associated with acute infections including that from Vibrio cholerae. Cholera produces a devastating loss of electrolytes and fluid in patients and without appropriate reduction in loss of fluid and electrolytes, patients experience significant hospitalization and mortality. Lechlemer provides the opportunity to treat cholera patients in combination with oral rehydration salts (“ORS”) and the recommended guidelines from the World Health Organization (“WHO”) for the use of appropriate antibiotics to reduce the burden of the pathogen. Appropriate preclinical toxicity studies and formulation development activities are ongoing to support the conduct of clinical studies with lechlemer.

As previously mentioned, Napo completed 7-day and 28-day preclinical toxicology and safety studies in rats and dogs with lechlemer (NP-300) following repeated daily oral dosing. Napo received partial support for preclinical services from the National Institute of Allergy and Infectious Diseases (“NIAID”) of the National Institutes of Health, and Napo is grateful for their partial support of lechlemer’s development.

Napo is currently conducting additional, prerequisite IND-enabling toxicity studies and also developing appropriate oral solid dosage forms to allow the clinical evaluation of lechlemer. The Company plans to provide appropriate regulatory documents by end of the second quarter of 2022 to support the initiation of first-in-human (“FIH”) evaluation in the third quarter of 2022.

Cholera is an acute diarrheal illness caused by infection of the intestine with the bacterium Vibrio cholerae. According to the Centers for Disease Control and Prevention of the U.S. Department of Health & Human Services, an estimated 3 5 million cholera cases and more than 100,000 cholera-related deaths occur each year around the world. The infection is often mild or without symptoms but can sometimes be severe. Approximately one in 10 of infected persons will have severe disease characterized by profuse watery diarrhea, vomiting, and leg cramps. In these people, rapid loss of body fluids leads to dehydration and shock. Without treatment, death can occur within hours. The largest cholera outbreak in recorded history recently occurred in Yemen. According to Oxfam, the number of cholera cases in Yemen in 2019 was the second largest ever recorded in a country in a single year, surpassed only by the numbers in Yemen in 2017. According to the Brookings Institution, cholera continues to spread in Yemen, with 180,000 new cases reported in the first eight months of 2020.

We expect that lechlemer will be significantly less expensive and would support development efforts to receive a tropical disease priority review voucher from the FDA for an indication for the symptomatic treatment of diarrhea from acute infections such as cholera. Priority review vouchers are granted by the FDA as an incentive to develop treatments for neglected diseases and rare pediatric diseases. Priority review vouchers are transferable and, in past transactions by other companies, have sold for prices ranging from $60 million to $350 million. Additionally, we believe lechlemer may provide a long-term pipeline opportunity as a second-generation anti-secretory agent for multiple gastrointestinal diseases—especially in resource-constrained countries.

Napo received advice from the Division of Anti-Infectives at the U.S. FDA in September 2021 as part of the pre-investigational New Drug Application (“Pre-IND”) discussion. Napo plans to include the advice in its plans for the Phase 1 clinical trial in healthy volunteers, currently planned the second half of 2022. The NP-300 (lechlemer) program is paired with funding from a promissory note related to the potential future sale of a possible TDPRV.

As previously announced, the Company also launched the Entheogen Therapeutics (“ETI”) initiative to support the discovery and development of novel, natural medicines derived from psychoactive and psychedelic plant compounds for treatment of mood disorders, neuro-degenerative diseases, addiction, and other mental health disorders. The initiative is initially focused on plants with the potential to treat depression and leverages Napo’s proprietary library of approximately 2,300 plants with medicinal properties. According to statistics available from the

8

National Institute of Mental Health Disorders, part of the National Institutes of Health, approximately 9.5% of American adults ages 18 and over will suffer from a depressive illness (major depression, bipolar disorder, or dysthymia) each year.

Field research collaborations have been conducted in the past by members of the scientific strategy team (“SST”) of Jaguar’s predecessor company Shaman Pharmaceuticals, who are also members of the ETI SST, yielded possible applications for a compound called alstonine. Alstonine is derived from a plant used by traditional healers in Nigeria, and has demonstrated a potential novel mechanism of action for the treatment of difficult to manage conditions such as schizophrenia.

The ETI SST consists of leading and globally renowned ethnobotanists, physicians, and pharmacologists as well as experts in the fields of natural product chemistry and neuropharmacology. We believe the wealth of expertise, experience, and commitment of the ETI SST—comprised of multiple members of the original SST that contributed to development of Jaguar's proprietary library of approximately 2,300 plants—will play an instrumental role in advancing our shared initial goal of identifying plants in our library that may have the potential to treat mood disorders and neurodegenerative diseases, such as Alzheimer's disease, Parkinson's disease, and amyotrophic sclerosis. Mood disorders and neurodegenerative diseases affect hundreds of millions of people around the globe and represent classic unmet medical needs.

While Napo and Jaguar remain steadfastly focused on the commercial success of Mytesi and Canalevia-CA1, respectively, and on the development of potential crofelemer follow-on indications in the area of gastrointestinal treatments, the Company believes the same competencies and multi-disciplinary scientific strategy that led to the development of crofelemer will support collaborative efforts with potential partners to develop novel first-in-class prescription medicines derived from psychoactive plants.

Our management team has significant experience in gastrointestinal product development for both humans and animals. Napo was founded 32 years ago to perform drug discovery and development by leveraging the knowledge of traditional healers working in rainforest areas. Ten members of the Jaguar and Napo team have been together for more than 15 years. Dr. Steven King, our chief sustainable supply, ethnobotanical research and intellectual property officer, and Lisa Conte, our founder, president and CEO, have worked together for more than 30 years. We have buttressed the early founding team with the expertise and experiences of team members like Dr. Darlene Horton and Dr. Karen Brunke to support the continued development and commercialization activities of the Napo and Jaguar family. We have assembled an impressive group of scientific advisory board (SAB) members that work closely with the Chair of Jaguar’s Scientific Advisory Board, Dr. Pravin Chaturvedi, who also serves as the Chief Scientific Officer (“CSO”) of Jaguar. Together, these dedicated personnel successfully transformed crofelemer, which is extracted from trees growing in the rainforest, to Mytesi and Canalevia-CA1, which are natural, sustainably harvested, FDA-approved drugs.

As announced in February 2020, the American Botanical Council named Napo the recipient of the 2019 Varro E. Tyler Commercial Investment in Phytomedicinal Research Award in recognition of Napo’s ongoing commitment to the sustainable development and production of natural therapeutic preparations. Specifically, this award acknowledges the successful development and approval of crofelemer, which is derived from the medicinal Croton lechleri tree in the Amazon rainforest. Previous recipients of this award include Jaguar’s partner, Italy based Indena S.p.A., one of the world’s largest producers of clinically-tested botanical extracts for the food, dietary supplement, cosmetic, and pharmaceutical markets.

Pipeline within a product—crofelemer

Crofelemer is currently being evaluated for the prophylaxis of CTD in adult patients receiving targeted therapy. As announced in October 2020, Napo has initiated its pivotal Phase 3 clinical trial of crofelemer (Mytesi) for prophylaxis of diarrhea in adult cancer patients receiving targeted therapy (OnTarget study). A significant proportion of patients undergoing cancer therapy experience diarrhea. Novel targeted cancer therapy agents, such as epidermal growth factor receptor antibodies and tyrosine kinase inhibitors, with or without cycle chemotherapy agents, may

9

activate intestinal chloride secretory pathways leading to increased chloride secretion into the gut lumen, coupled with significant loss of water that would result in secretory diarrhea.

According to data appearing in “Treatment Guidelines for CID” (chemotherapy induced diarrhea) in the April 2004 issue of Gastroenterology and Endoscopy News, diarrhea is the most common adverse event reported in chemotherapy patients. Approved third-party supportive care products for chemotherapy induced nausea and vomiting (“CINV”) include Sustol, Aloxi, Akynzeo and Sancuso. According to a report published by Allied Market Research, the global CINV market was valued at $1.66 billion in 2015 and is estimated to reach $2.66 billion by 2022.

Diarrhea has been reported as the most common side effect of the recently approved CDK 4/6 inhibitor abemaciclib and the pan HER TKI neratinib, with occurrence ranging from 86% to >95% and grade 3 over 40%, in published studies. Diarrhea in this patient population has the potential to cause dehydration, potential infections, and non-adherence to treatment. A novel antidiarrheal like crofelemer may hold promise for treating secretory diarrhea—and therefore also support long term cancer treatment adherence—in this population.

Napo has previously received orphan drug designation from the FDA for adult and/or pediatric SBS. The Orphan Drug Act provides for granting special status to a drug or biological product to treat a rare disease or condition upon request of a sponsor. Orphan drug designation qualifies the sponsor of the drug for various development incentives, including extended exclusivity, tax credits for qualified clinical testing, and relief of filing fees. As mentioned above, Napo Therapeutics has licensed the rights for the orphan and rare diseases associated with SBS and CDD with IF.

Napo Therapeutics expects that an IIT in pediatric patients with CDD will study crofelemer in the second half of 2022. This study will be initiated in the Middle East/North Africa (“MENA”) region with sites that treat infants and children with CDD and SBS with IF.

CDD is a group of rare, chronic intestinal channel diseases, with onset in early infancy, that are characterized by severe, lifelong diarrhea and a lifelong need for nutritional intake either parenterally or with a feeding tube. CDD is related to specific genetic defects inherited as autosomal recessive traits. The incidence of CDD is prevalent in regions where consanguineous marriage (related by blood) is part of the culture. CDD is directly associated with serious secondary conditions including dehydration, metabolic acidosis, and failure to thrive, prompting the need for immediate therapy to prevent death and limit lifelong disability. A recent preclinical study shows that crofelemer reduces the chloride secretion in intestinal cells derived from patients with CDD and these preclinical results provide additional support and rationale for the use of crofelemer in treating patients with CDD and/or SBS with IF.

As previously announced (in 2019), a clinical research study sponsored by The University of Texas Health Science Center at Houston (“UTHealth”) is being supported by Napo. This study evaluates the safety and effectiveness of crofelemer for treatment of chronic idiopathic diarrhea in patients. Chronic idiopathic diarrhea is a common complaint of patients presenting to family practitioners and internists and is one of the most common reasons for referral to gastroenterologists. It is estimated that the prevalence of chronic idiopathic diarrhea in developed countries (including the U.S.) is approximately 3-5%. It has a significant negative effect on health-related quality of life and causes a high economic burden on patients and society. The American Gastroenterological Association Burden of Illness study (2012) showed that the estimated annual direct and indirect costs associated with chronic idiopathic diarrhea is up to $524 million per year and $136 million per year, respectively. The principal investigator for this study is Dr. Brooks D. Cash, MD, AGAF, FACG, FACP, FASGE, Chief – Division of Gastroenterology, Hepatology and Nutrition, Sterling Professor of Medicine, McGovern Medical School at UTHealth, Co-Director, Ertan Digestive Disease Center at Memorial Hermann-Texas Medical Center. The Study is titled Yield of Diagnostic Tests and Management of Crofelemer for Chronic Idiopathic Diarrhea in Non-HIV Patients.

10

Crofelemer is also being evaluated in another investigator-initiated trial for the management of functional diarrhea in non-HIV patients. The principal investigator for this clinical study is Dr. Anthony Lembo, Professor, Gastroenterology, Beth Israel Deaconess Medical Center, Harvard Medical School, Boston, MA. This clinical study is a randomized double-blind, placebo-controlled study in adult subjects with functional diarrhea. Eligible patients will have functional diarrhea defined by Rome IV criteria as >25% loose watery stools and <25% hard/lumpy stools. The study plans to randomize 80 patients and the subjects will be randomized 1:1 for 4 weeks to either the placebo or crofelemer 125 mg delayed-release tablets (Mytesi) arm, administered twice daily for 4 weeks. Following the four-week placebo-controlled period, all subjects will receive Mytesi for an additional four weeks in an open label extension phase. The safety and tolerability of crofelemer and the clinical response during the placebo-controlled period will be evaluated in this study. Subjects will be allowed to use limited amounts of an antimotility drug (loperamide) during the placebo-controlled and open-label extension phase to manage uncontrolled diarrhea. However, no more than 11 doses of 2 mg loperamide will be permitted during any given week per subject.

Jaguar’s and Napo’s portfolio development strategy involves meeting with Key Opinion Leaders (“KOLs”) to identify indications that are potentially high value because they address important medical needs that are significantly or globally unmet, obtain input on protocol practicality and protocol generation, and then strategically sequencing indication development priorities, second generation product pipeline development, and partnering goals on a global basis.

Mytesi is the only antidiarrheal drug that has been approved by the US FDA for the treatment of chronic, noninfectious diarrhea in adult HIV/AIDS patients receiving ART. This approval was on the basis of the drug’s safety and efficacy in reducing the number of weekly and daily watery stools in patients and improvement of stool consistency, from unformed to formed stools, over a 24-week treatment period.

Unlike other available diarrhea treatments, crofelemer does not act by inhibiting intestinal motility. It has minimal oral absorption and does not have any clinically significant food or drug interactions, thereby allowing patients to maintain their appropriate dosing of treatment to suppress their viral load and maintain adequate CD4 levels in PLWHA. Crofelemer is also the only approved antidiarrheal drug that is approved for chronic use. Moreover, it is not an opioid, like other traditionally used treatments, thus avoiding both the acute side effect of constipation and the potential for abuse.

Napo’s Scientific Advisory Board has focused primarily on physician education, and community and global awareness regarding the importance and availability of solutions for neglected comorbidities, such as the first in class anti secretory mechanism of action of Mytesi for its currently approved indication.

There are significant barriers to entry for Mytesi (crofelemer). Through Napo, we hold an extensive global patent portfolio. At the present time, we hold approximately 143 issued worldwide patents, with coverage in many cases that extends until 2031. These issued patents cover multiple indications, including HIV AIDS diarrhea, irritable bowel syndrome (“IBS”), IBD, manufacturing, enteric protection from gastric juices, among others. We also have approximately 43 pending patent applications worldwide in the human health areas that are being prosecuted.

Mytesi is the first oral drug approved under the FDA’s Botanical Guidance, which provides another barrier to entry from potential generic competition. The FDA requires that the manufacturer of crofelemer use a validated proprietary bioassay to release the drug substance and drug product of Mytesi. While most generic products are fashioned to meet chemical release specifications that are in the public domain, the specifics of this assay are not publicly available. There is no pathway by which a generic product can be developed for a drug approved under botanical guidance. In addition, Mytesi is minimally absorbed systemically, so the classic approach of creating a generic drug by matching pharmacokinetic blood levels is not possible. A generic player would have to conduct costly and risky clinical trials.

While Jaguar’s commercial and development efforts have evolved to focus primarily on Mytesi and human pipeline indications since its merger with Napo, the Company has commenced launch initiatives related to Canalevia-CA1, our drug product which received conditional approval in December 2021 for treatment of CID in dogs. CID in dogs is typically caused by the same mechanism of action as in humans, and hence the work in dogs serves as a

11

preclinical proof of concept for the diarrhea in humans that is related to targeted cancer therapy. CID is an interesting model for human medical need and is being pursued as a prescription indication for animal health. We believe there is an important unmet medical need for the treatment of CID in dogs. Certain cancer treatment agents provided to dogs are human drugs or have the same mechanism of action as human cancer drugs, and these agents and mechanisms of action often have meaningful rates of diarrhea in humans as well.

As previously announced, Jaguar has received MUMS designation status from the FDA for Canalevia-CA1 for the indication of CID in dogs. MUMS designation is modeled on the orphan drug designation for human drug development and offers possible financial incentives to encourage MUMS drug development, such as the availability of grants to help with the cost of developing the MUMS drug.

For Jaguar Animal Health’s second proposed indication for Canalevia, exercise induced diarrhea (“EID”) in dogs, the Company is leveraging the use of many of the same major technical sections that have been submitted in support of the Company's application for Canalevia-CA1 for the indication of CID in dogs. Conditional approval of Canalevia for EID, under the name Canalevia-CA2, is expected in the fourth quarter of 2022.

Crofelemer is extracted and purified from the Croton lechleri tree, which we sustainably harvest and manage through programs that we have been developing over the past 30 years. This process has involved working with local and indigenous communities to plant trees, obtaining permits for export, and creating a supply network that is robust and reliable.

Our team continues to have relationships with partners that we began working with in the 1990s. Additionally, through the establishment of a nonprofit called the Healing Forest Conservancy, our team has created a long term mechanism for benefit sharing that recognizes the intellectual contribution of Indigenous populations. This program is intended to contribute to the continued strength and effectiveness of the valued and strategically important relationships we have carefully cultivated over the past 30+ years.

Product Pipeline

In addition to our Mytesi (crofelemer) product that is approved by the U.S. FDA for the symptomatic relief of noninfectious diarrhea in adults with HIV/AIDS on antiretroviral therapy, we are also developing a pipeline of prescription drug product candidates to address unmet needs in gastrointestinal health through Napo. Mytesi (crofelemer) is a novel, first in class anti secretory agent which has a basic normalizing effect locally in the gut and lumen, and this mechanism of action has the potential to benefit multiple disorders. Clinical trials demonstrated that nearly 80% of Mytesi users experienced an improvement in their diarrhea over a four week period. At week 20 of the pivotal trial, over half the patients had no watery stools, or a 100% decrease, and 83% had at least a 50% decrease in watery stools. Our Mytesi pipeline currently includes prescription drug product candidates for four follow on indications, several of which are backed by Phase 2 evidence from completed Phase 2 trials. In addition, a second generation proprietary anti secretory agent, lechlemer, is in development for cholera-related diarrhea.

12

Napo Prescription Drug Product Candidates

Product Candidates | Indication | Completed Milestones | Current Phase of | Anticipated Near-Term | |

Mytesi | CTD | • Initiated pivotal Phase 3 clinical trial in October 2020 • Findings of Phase 2 HALT-D study presented in Q4 2021 | Phase 3 | • Enrollment in Phase 3 trial ongoing | |

Novel lyophilized crofelemer product | Rare disease indications (SBS & CDD) | • Orphan drug designation for SBS granted by FDA and EMA | Phase 2 | • Initiate Phase 2 proof of concept (POC) study in SBS and/or CDD in 2022 | |

Mytesi | IBS-D | • Two Phase 2 studies completed | Phase 2 | • Potential business development opportunities | |

Mytesi | Chronic idiopathic diarrhea | • Initiated clinical study at The University of Texas Health Science Center at Houston (“UTH”) | Phase 2 | • Top line results of UTH trial expected in 2022 | |

Mytesi | Functional diarrhea | • Initiated clinical study at Beth Israel Deaconess Medical Center, Harvard Medical School, Boston | Phase 2 | • Enrollment ongoing | |

Mytesi | IBD | • Safety evidence from other chronic diarrhea indications | Phase 2 | • KOL discussions ongoing | |

NP-300 (lechlemer) | Second-generation antidiarrheal drug for infectious diarrhea including from cholera | • Ongoing IND-enabling toxicology studies and formulation development | Pre IND | • Initiate Phase 1 trial in the second half of 2022 | |

*Clinical trials are funding dependent

Estimated Size of Mytesi Target Markets

We believe the medical need for Mytesi is significant, compelling, and unmet, and that doctors are looking for a drug product with a mechanism of action that is distinct from the options currently available to resolve diarrhea. A growing percentage of HIV patients have lived with the virus in their gut for 10+ years, often causing gut enteropathy and chronic or chronic episodic diarrhea. According to data from the U.S. Centers for Disease Control and Prevention, by 2020 more than 70% of Americans with HIV are expected to be 50 and older and have lived with HIV for more than 10 years (1).

13

Market | Competition | Market Size/Potential | |

HIV-related Diarrhea | None | We estimate the U.S. market revenue potential for Mytesi to be approximately $50 million in gross annual sales | |

CTD | None | An estimated 650,000 U.S. cancer patients receive chemotherapy in an outpatient oncology clinic(2). Comparable supportive care (i.e., CINV) product sales of ~$620 million in 2013(3). Global CINV market projected to reach a valuation of $2.7 billion by 2022(4) | |

SBS/CDD | 1 | Financial benefits of Orphan Drug Designation. The global SBS market exceeded $568 million in 2019 and is expected to reach $4.6 billion by 2027, according to a report by Vision Research Reports(5) | |

IBS-D | 3 | Most IBS products have an estimated revenue potential of greater than $1.0 billion(6) | |

IBD | None | Estimated 1,171,000 Americans have IBD(7) | |

Infectious Diarrhea from Cholera | None | In recent transactions by other companies, priority review vouchers have sold for $67 million to $350 million(8) | |

(1) | HIV Among People Aged 50 and Older (https://www.cdc.gov/hiv/group/age/olderamericans/index.html) |

(2) | Centers for Disease Control and Prevention. Preventing Infections in Cancer Patients: Information for Health Care Providers (cdc.gov/cancer/prevent infections/providers.htm) |

(3) | Heron Therapeutics, Inc. Form 10 K for the fiscal year ended December 31, 2016 |

(4) | Report published by Allied Market Research, titled, "Chemotherapy-induced Nausea and Vomiting (CINV) Market-Global Opportunity Analysis and Industry Forecast, 2014-2022” (https://www.prnewswire.com/news-releases/chemotherapy-induced-nausea-and-vomiting-cinv-market-expected-to-reach-2659-million-by-2022-611755395.html) |

(5) | Short Bowel Syndrome Market – Global Industry Analysis, Size, Share, Trends, Revenue, Forecast 2020 to 2027 (https://www.mynewsdesk.com/us/medical-technology-news/pressreleases/short-bowel-syndrome-market-global-industry-analysis-size-share-trends-revenue-forecast-2020-to-2027-3069433) |

(6) | Merrill Lynch forecasts peak US sales of roughly $1.5 bn for Ironwood’s Linzess (https://247wallst.com/healthcare-business/2015/04/27/key-analyst-sees-nearly-30-upside-in-ironwood/); Rodman & Renshaw estimate peak annual sales of Synergy Pharmaceuticals’ Trulance at $2.3 bn in 2021 (https://www.benzinga.com/analyst-ratings/analyst-color/17/04/9304883/what-synergys-new-patents-mean-for-its-commercial-prospe) |

(7) | Kappelman, M. et al. Recent Trends in the Prevalence of Crohn’s Disease and Ulcerative Colitis in a Commercially Insured US Population. Dig Dis Sci. 2013 Feb; 58(2): 519 525 |

(8) | In Aug. 2015, AbbVie Inc. bought a priority review voucher from United Therapeutics Corp for $350 million (https://www.wsj.com/articles/united-therapeutics-sells-priority-review-voucher-to-abbvie-for-350-million-1439981104 ). In July 2014, BioMarin announced that it had sold a priority review voucher to Sanofi and Regeneron for $67.5 million. (https://investors.biomarin.com/2014-07-30-BioMarin-Sells-Priority-Review-Voucher-for-67-5-Million). |

14

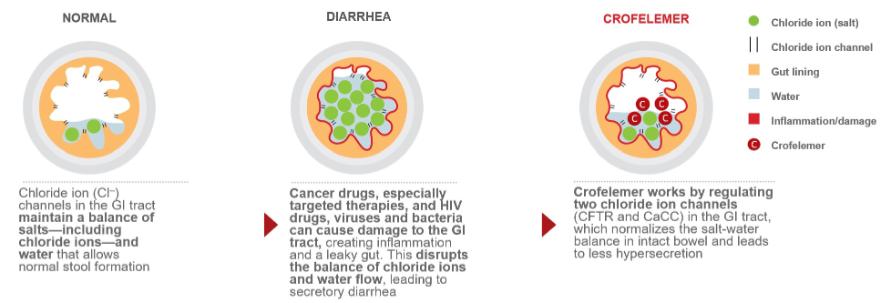

The following diagram illustrates the mechanism of action of our human and animal gastrointestinal drug products and drug product candidates, which normalize chloride and water flow and transit time of fluids within the intestinal lumen.

Business Strategy

Our goal is to become a leading pharmaceutical company with first in class, sustainably derived products that address significant unmet gastrointestinal medical needs globally. To accomplish this goal, we plan to:

Expand Mytesi by leveraging our significant gastrointestinal product knowledge, experience and intellectual property portfolio

Mytesi is a novel, first in class anti secretory antidiarrheal agent which has a basic normalizing effect locally on the gut, and this mechanism of action has the potential to benefit multiple gastrointestinal disorders. Our Mytesi (crofelemer) product is approved by the U.S. FDA for the symptomatic relief of noninfectious diarrhea in adults with HIV/AIDS on antiretroviral therapy. Jaguar, through Napo, holds global unencumbered rights for Mytesi. Mytesi is in development for multiple possible follow on indications, including diarrhea related to targeted cancer therapy; orphan drug indications for infants and children with congenital diarrheal disorders and short bowel syndrome; inflammatory bowel disease; irritable bowel syndrome; and for idiopathic/functional diarrhea. In addition, a second generation proprietary anti secretory agent is in development for cholera.

Our management team collectively has extensive experience in the development of prescription drugs. This experience covers all aspects of product development, including discovery, preclinical and clinical development, GMP manufacturing, regulatory affairs, and commercialization. Key members of this team successfully developed Mytesi.

Maintain commercial capabilities in Mytesi sales and marketing efforts

Napo’s direct sales organization is comprised of Mytesi field sales representatives strategically positioned to cover U.S. geographies with the highest potential. With support provided by concomitant marketing, promotional activities, patient empowerment programs, including an integrated social digital campaign, and medical education initiatives described below, we expect a proportional response in the number of patients treated with Mytesi.

Leverage our relationships with Scientific Advisory Board (SAB) members for crofelemer commercialization and development in follow on indications

The Company has retained 10 SAB members that have extensive clinical experience in HIV, CTD, IBD, SBS, and CDD. In addition, the Company engages key opinion leaders (KOLs) for specific turnkey needs.

15

Establish partnerships to support moving pipeline indications to pivotal clinical trials

Jaguar is actively pursuing the development of a robust pipeline of potential follow on indications for crofelemer, and the Company’s goal is to establish partnerships to support moving pipeline indications to pivotal clinical trials.

Strategically sequence the development of follow on indications of Mytesi and seek geographically focused licensing opportunities

As announced September 24, 2018, Jaguar and Knight Therapeutics Inc. (“Knight”) entered into a Distribution, License and Supply Agreement that grants Knight the exclusive right to commercialize Mytesi and related products in Canada and Israel. The License Agreement has a term of 15 years (with automatic renewals) and provides Knight with an exclusive right to commercialize current and future Jaguar human health products (including crofelemer, Lechlemer, and any product containing a proanthocyanidin or with an anti-secretory mechanism) in Canada and Israel. Knight forfeited its right of first negotiation for expansion to Latin America. Under the License Agreement, Knight is responsible for applying for and obtaining necessary regulatory approvals in the territory of Canada and Israel, as well as marketing, sales and distribution of the licensed products. Knight will pay a transfer price for all licensed products, and upon achievement of certain regulatory and sales milestones, the Company may receive payments from Knight in an aggregate amount of up to approximately $18 million payable throughout the initial 15-year term of the agreement. The Company did not have any license revenues since the execution of this agreement.

Although it is possible that we may enter into additional corporate partnering relationships related to Mytesi, our intention would be to retain all or co commercialization and promotional rights in the U.S., so that we do not become primarily a royalty collecting organization, and we are opposed to entering into any Mytesi partnering relationship that would require splitting indications. We are seeking to put limited geographically focused partnerships in place in the near term, while also considering possibilities for a worldwide partnership with a leading global entity (excluding the U.S. exclusive commercial rights) in the field of gastrointestinal care and cancer in the long term.

Reduce risks relating to product development

Risk reduction is a key focus of our product development planning. Mytesi is approved for chronic indication, providing us the ability to leverage this corresponding safety data when seeking approval for planned follow on indications that are also chronic or chronic episodic indications. In an effort to reduce risk further, we have implemented the following approach: first, we meet with key opinion leaders, typically at medical conferences. Next, we confirm unmet medical needs with these key opinion leaders and discuss the practicality of patient enrollment and trial implementation. We then generate protocols to discuss with the FDA, seeking, when possible, special protocol assessments. Our goal is to have de risked the program as much as we believe we possibly can, by the time we start devoting significant funds to a clinical trial, in particular the regulatory pathway. We believe this approach will lead to better long-term outcomes for our products in development.

We will continue to seek partnerships outside the United States for the above indications while focusing on development and commercial access in the United States directly. We are also focused on investigating (lechlemer) for various gastrointestinal indications. Lechlemer is a proprietary Jaguar pharmaceutical product, a standardized botanical extract distinct from crofelemer, also sustainably derived from the Croton lechleri tree.

We believe lechlemer, which has a similar mechanism of action as crofelemer and is significantly less costly to produce, may support efforts to receive a priority review voucher from the U.S. FDA for symptomatic treatment of diarrhea from cholera infection. Priority review vouchers are granted by the FDA to drug developers for tropical disease indications (TDPRV) as an incentive to develop treatments for neglected diseases and rare pediatric diseases. Additionally, we believe lechlemer represents a long-term pipeline opportunity as a second generation anti secretory agent, on a global basis, for multiple gastrointestinal diseases—especially in resource constrained countries where the cost of goods is a factor, in part, because requirements often exist in such regions for drug prices to decrease annually.

16

The Company has previously presented Phase 2 data on crofelemer for the treatment of diarrhea in cholera patients from a study in Bangladesh. Napo plans to follow a similar clinical study design to support the development of lechlemer (NP-300) for a cholera related indication.

Napo is conducting IND-enabling preclinical toxicology studies and developing novel NP-300 formulations that will support the initiation of clinical studies in 2022.

Our portfolio development strategy is based on identifying indications that are potentially high value because they address important medical needs that are significantly or globally unmet, and then strategically sequencing indication development priorities, second generation product pipeline development, and partnering goals on a global basis.

Our technology for proprietary gastrointestinal disease products is central to the product pipelines of both human and veterinary indications. Crofelemer is also the API in Canalevia-CA1, our prescription drug product recently conditionally approved by the FDA and launched for CID in dogs, and also expected to be approved and launched, under the name Canalevia-CA2, for EID in dogs in the fourth quarter of 2022.

Napo Therapeutics Provides New Opportunities to Treat Orphan Indications Like Short Bowel Syndrome

Jaguar is strategically pursuing multiple important shots on goal for its drug development pipeline: Crofelemer for CTD, led by Napo, and crofelemer for SBS and CDD, led by Napo Therapeutics. Jaguar’s exclusive license agreement with Napo Therapeutics provides a perpetual, royalty-bearing license for Europe (excluding Russia), and includes traditional terms such as up-front fees, milestone payments, royalties on sales in Europe, and a supply agreement, and rights to utilized all data Napo Therapeutics generates for Jaguar development and approval activities globally.

Competition

There are several significantly larger pharmaceutical companies competing with us in the gastrointestinal segment.

Diarrhea in adult patients living with HIV/AIDs. We are not aware of any other FDA approved drugs for the symptomatic relief of diarrhea in HIV/AIDs patients. HIV/AIDs diarrhea patients may also use loperamide or Lomotil but these medications affect motility which can result in rebound diarrhea and are not indicated for chronic use. Other agents’ patients may use include over the counter anti diarrheal remedies such as Mylanta or Kaopectate.

Cancer therapy related diarrhea. We are not aware of any FDA approved drugs specifically indicated for cancer therapy related diarrhea, including chemotherapy related diarrhea. A recent Phase 2b trial of elsiglutide for the treatment of chemotherapy induced diarrhea in colorectal cancer patients did not meet statistical significance. Opioids and over the counter drugs are commonly used to treat chemotherapy induced diarrhea, but these drugs affect motility. Certain tyrosine kinase inhibitor chemotherapy agents have diarrhea as a significant side effect. For example, FDA guidance suggests diarrhea prophylaxis prior to initiating adjuvant therapy with neratinib.

Short Bowel Syndrome and Congenital Diarrheal Disorders. We are not aware of any FDA approved drugs specifically indicated for congenital diarrheal disorders. In the U.S., Takeda Pharmaceuticals’ GATTEX® (teduglutide) is indicated for the treatment of adults and pediatric patients 1 year of age and older with short bowel syndrome who are dependent on parenteral support, and Zorbtive® is a recombinant human growth hormone indicated for the treatment of short bowel syndrome in adult patients receiving specialized nutritional support.

Diarrhea predominant irritable bowel syndrome. Two drugs were approved in 2015 for the treatment of diarrhea predominant irritable bowel syndrome, Allergan plc’s Virbezi and Xifaxan, which is marketed by Valeant Pharmaceuticals International. Also, Lotronex was approved by the FDA in 2000 but was withdrawn from the market and later reintroduced in 2002 under a Risk Management Program. With the exception of Lotronex, the sponsors of

17

Verbezi and Xifaxan employ extensive media and print promotion for the commercialization of these products. We are seeking a partner to further the clinical development and commercialization of crofelemer for IBS-D. There are currently numerous trials ongoing for IBS-D.

Inflammatory Bowel Disorders. We are not aware of any FDA approved drugs specifically indicated as an anti-secretory agent for use to address IBD.

Infectious Diarrhea from Cholera. We are not aware of any FDA approved drugs specifically indicated as an anti-secretory agent for use to address the devastating dehydration in cholera patients.

Manufacturing

The plant material used to manufacture is crude plant latex (“CPL”) extracted and purified from Croton lechleri, a widespread and naturally regenerating tree in the rainforest that is managed as part of sustainable harvesting programs. The tree is found in several South American countries and has been the focus of long term sustainable harvesting research and development work. Napo’s collaborating suppliers obtain CPL and arrange for the shipment of CPL to Napo’s third party contract manufacturer.