Form PREM14A TWITTER, INC. For: May 16

Tweet

Tweet Share

ShareTable of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☒ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☐ | Definitive Additional Materials |

| ☐ | Soliciting Material under §240.14a-12 |

TWITTER, INC.

(Name of Registrant as Specified In Its Charter)

Payment of Filing Fee (Check all boxes that apply):

| ☐ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☒ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. |

Table of Contents

PRELIMINARY PROXY STATEMENT—SUBJECT TO COMPLETION

TWITTER, INC.

1355 MARKET STREET, SUITE 900

SAN FRANCISCO, CALIFORNIA 94103

To the Stockholders of Twitter, Inc.:

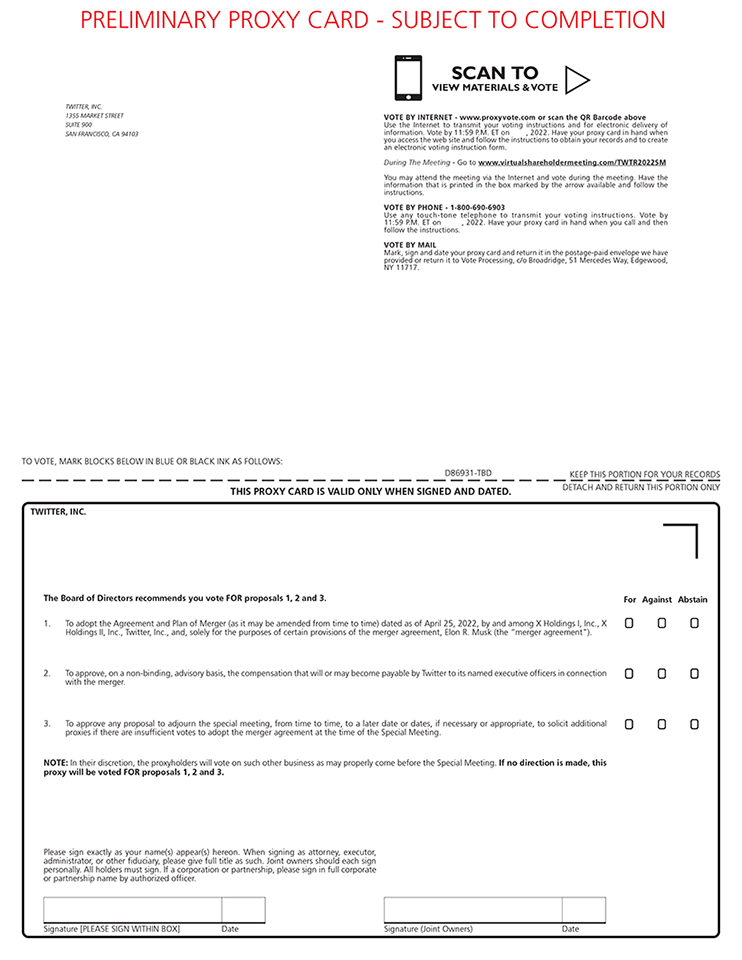

You are cordially invited to attend a special meeting of stockholders (which we refer to, together with any adjournment, postponement or other delay thereof, as the “special meeting”) of Twitter, Inc. (which we refer to as “Twitter”). The special meeting will be held on [•], 2022, at [•], Pacific time. You may attend the special meeting via a live interactive webcast at http://www.virtualshareholdermeeting.com/TWTR2022SM. You will be able to listen to the special meeting live and vote online. We believe that a virtual meeting provides expanded access, improved communication and cost savings for our stockholders and Twitter.

At the special meeting, you will be asked to consider and vote on a proposal to adopt the Agreement and Plan of Merger (as it may be amended from time to time), dated as of April 25, 2022 (which we refer to as the “merger agreement”), among X Holdings I, Inc. (which we refer to as “Parent”), X Holdings II, Inc., a wholly owned subsidiary of Parent (which we refer to as “Acquisition Sub”), Twitter, and, solely for the purposes of certain provisions of the merger agreement, Elon R. Musk. Parent is wholly owned by Mr. Musk. We refer to the merger of Acquisition Sub with and into Twitter as the “merger.”

At the special meeting, you will also be asked to consider and vote on a proposal to approve, on a non-binding, advisory basis, the compensation that will or may become payable by Twitter to its named executive officers in connection with the merger; and a proposal for the adjournment of the special meeting, from time to time, to a later date or dates, if necessary or appropriate, to solicit additional proxies if there are insufficient votes to adopt the merger agreement at the time of the special meeting.

If the merger is completed, you will be entitled to receive $54.20 in cash, without interest and subject to any applicable withholding taxes, for each share of our common stock that you own (unless you have properly exercised your appraisal rights). This amount constitutes a premium of approximately 38 percent to the closing price of our common stock on April 1, 2022, which was the last full trading day before Mr. Musk disclosed his approximately nine percent stake in Twitter.

Twitter’s Board of Directors, after considering the factors more fully described in the enclosed proxy statement, unanimously: (1) determined that the merger agreement is advisable and the merger and the other transactions contemplated by the merger agreement are fair to, advisable and in the best interests of Twitter and its stockholders; and (2) adopted and approved the merger agreement, the merger and the other transactions contemplated by the merger agreement.

Twitter’s Board of Directors unanimously recommends that you vote:

| (1) | “FOR” the adoption of the merger agreement; |

| (2) | “FOR” the compensation that will or may become payable by Twitter to its named executive officers in connection with the merger; and |

Table of Contents

| (3) | “FOR” the adjournment of the special meeting, from time to time, to a later date or dates, if necessary or appropriate, to solicit additional proxies if there are insufficient votes to adopt the merger agreement at the time of the special meeting. |

The accompanying proxy statement provides detailed information about the special meeting, the merger agreement and the merger, and the other proposals to be considered at the special meeting. A copy of the merger agreement is attached as Annex A to the proxy statement.

The accompanying proxy statement also describes the actions and determinations of Twitter’s Board of Directors in connection with its evaluation of the merger agreement and the merger. Please read the proxy statement and its annexes, including the merger agreement, carefully and in their entirety, as they contain important information.

Even if you plan to virtually attend the special meeting, please sign, date and return, as promptly as possible, the enclosed proxy card (a proxy card and a prepaid reply envelope are enclosed for your convenience) or grant your proxy electronically over the internet or by telephone (using the instructions found on the proxy card). If you virtually attend the special meeting and vote at the special meeting, your vote will revoke any proxy that you have previously submitted. If you fail to return your proxy or to attend the special meeting, your shares will not be counted for purposes of determining whether a quorum is present at the special meeting and will have the same effect as a vote against the adoption of the merger agreement.

If your shares are held through a bank, broker or other nominee, you are considered the “beneficial owner” of shares held in “street name.” If you hold your shares in “street name,” you will receive instructions from your bank, broker or other nominee that you must follow in order to submit your voting instructions and have your shares counted at the special meeting. Your bank, broker or other nominee cannot vote on any of the proposals to be considered at the special meeting without your instructions. Without your instructions, your shares will not be counted for purposes of a quorum or be voted at the special meeting, and that will have the same effect as voting against the adoption of the merger agreement.

Your vote is very important, regardless of the number of shares that you own.

If you have any questions or need assistance voting your shares, please contact our proxy solicitor:

Innisfree M&A Incorporated

501 Madison Avenue, 20th Floor

New York, New York 10022

Stockholders call: (877) 750-8338 (toll-free from the U.S. and Canada) or

+1 (412) 232-3651 (from other countries)

Banks and brokers call collect: (212) 750-5833

On behalf of Twitter’s Board of Directors, thank you for your support.

Very truly yours,

| Parag Agrawal | Bret Taylor | |

| Chief Executive Officer and Director |

Chairman of the Board of Directors |

The accompanying proxy statement is dated [•], 2022 and, together with the enclosed form of proxy card, is first being sent to stockholders on or about [•], 2022.

Table of Contents

PRELIMINARY PROXY STATEMENT—SUBJECT TO COMPLETION

TWITTER, INC.

1355 MARKET STREET, SUITE 900

SAN FRANCISCO, CALIFORNIA 94103

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON [•], 2022

Notice is given that a special meeting of stockholders (which we refer to, together with any adjournment, postponement or other delay thereof, as the “special meeting”) of Twitter, Inc., a Delaware corporation (which we refer to as “Twitter”), will be held on [•], 2022, at [•], Pacific time, for the following purposes:

| 1. | To consider and vote on the proposal to adopt the Agreement and Plan of Merger (as it may be amended from time to time) dated as of April 25, 2022, among X Holdings I, Inc., X Holdings II, Inc., Twitter, and, solely for the purposes of certain provisions of the merger agreement, Elon R. Musk (which we refer to as the “merger agreement”); |

| 2. | To consider and vote on the proposal to approve, on a non-binding, advisory basis, the compensation that will or may become payable by Twitter to its named executive officers in connection with the merger of X Holdings II, Inc., a wholly owned subsidiary of X Holdings I, Inc., with and into Twitter (which we refer to as the “merger”); |

| 3. | To consider and vote on any proposal to adjourn the special meeting, from time to time, to a later date or dates, if necessary or appropriate, to solicit additional proxies if there are insufficient votes to adopt the merger agreement at the time of the special meeting; and |

| 4. | To transact any other business that may properly come before the special meeting. |

The special meeting will be held by means of a live interactive webcast on the internet at http://www.virtualshareholdermeeting.com/TWTR2022SM. You will be able to listen to the special meeting live and vote online. The special meeting will begin promptly at [•], Pacific time. Online check-in will begin a few minutes prior to the special meeting. You will need the control number found on your proxy card or voting instruction form in order to participate in the special meeting (including voting your shares).

Only Twitter stockholders as of the close of business on [•], 2022 are entitled to notice of, and to vote at, the special meeting.

Twitter’s Board of Directors unanimously recommends that you vote: (1) “FOR” the adoption of the merger agreement; (2) “FOR” the compensation that will or may become payable by Twitter to its named executive officers in connection with the merger; and (3) “FOR” the adjournment of the special meeting, from time to time, to a later date or dates, if necessary or appropriate, to solicit additional proxies if there are insufficient votes to adopt the merger agreement at the time of the special meeting.

Twitter stockholders who do not vote in favor of the proposal to adopt the merger agreement will have the right to seek appraisal of the “fair value” of their shares of our common stock (exclusive of any

Table of Contents

elements of value arising from the accomplishment or expectation of the merger and together with interest (as described in the accompanying proxy statement) to be paid on the amount determined to be “fair value”) in lieu of receiving $54.20 per share in cash if the merger is completed, as determined in accordance with Section 262 of the Delaware General Corporation Law (which is referred to as the “DGCL”). To do so, a Twitter stockholder must properly demand appraisal before the vote is taken on the merger agreement and comply with all other requirements of the DGCL, including Section 262 thereof, which are summarized in the accompanying proxy statement, and must meet certain other conditions. Section 262 of the DGCL is reproduced in its entirety in Annex B to the accompanying proxy statement and is incorporated in this notice by reference.

Even if you plan to attend the special meeting, please sign, date and return, as promptly as possible, the enclosed proxy card (a proxy card and a prepaid reply envelope are enclosed for your convenience) or grant your proxy electronically over the internet or by telephone (using the instructions found on the proxy card). If you attend the special meeting and vote at the special meeting, your vote will revoke any proxy that you have previously submitted. If you fail to return your proxy or to attend the special meeting, your shares will not be counted for purposes of determining whether a quorum is present at the special meeting and will have the same effect as a vote against the adoption of the merger agreement.

If your shares are held through a bank, broker or other nominee, you are considered the “beneficial owner” of shares held in “street name.” If you hold your shares in “street name,” you will receive instructions from your bank, broker or other nominee that you must follow in order to submit your voting instructions and have your shares counted at the special meeting. Your bank, broker or other nominee cannot vote on any of the proposals to be considered at the special meeting without your instructions. Without your instructions, your shares will not be counted for purposes of a quorum or voted at the special meeting, and that will have the same effect as voting against the adoption of the merger agreement.

By Order of the Board of Directors,

Parag Agrawal

Chief Executive Officer and Director

Dated: [•], 2022

San Francisco, California

Table of Contents

IMPORTANT INFORMATION

Even if you plan to attend the special meeting, we encourage you to submit your proxy as promptly as possible: (1) over the internet; (2) by telephone; or (3) by signing, dating and returning the enclosed proxy card (a proxy card and a prepaid reply envelope are enclosed for your convenience). You may revoke your proxy or change your vote at any time before your proxy is voted at the special meeting.

If your shares are held through a bank, broker or other nominee, you are considered the “beneficial owner” of shares held in “street name.” If you hold your shares in “street name,” you will receive instructions from your bank, broker or other nominee that you must follow in order to submit your voting instructions and have your shares counted at the special meeting. Your bank, broker or other nominee cannot vote on any of the proposals to be considered at the special meeting without your instructions. Without your instructions, your shares will not be counted for purposes of a quorum or voted at the special meeting, and that will have the same effect as voting against the adoption of the merger agreement.

If you are a stockholder of record, voting at the special meeting will revoke any proxy that you previously submitted. If you hold your shares through a bank, broker or other nominee, you must provide a “legal proxy” from the bank, broker or other nominee that holds your shares in order to vote at the special meeting.

We encourage you to read the accompanying proxy statement and its annexes, including all documents incorporated by reference into the accompanying proxy statement, carefully and in their entirety. If you have any questions concerning the merger, the special meeting or the accompanying proxy statement, would like additional copies of the accompanying proxy statement, or need help voting your shares, please contact our proxy solicitor:

Innisfree M&A Incorporated

501 Madison Avenue, 20th Floor

New York, New York 10022

Stockholders call: (877) 750-8338 (toll-free from the U.S. and Canada) or

+1 (412) 232-3651 (from other countries)

Banks and brokers call collect: (212) 750-5833

Table of Contents

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 2 | ||||

| 3 | ||||

| Recommendation of the Twitter Board and Reasons for the Merger |

5 | |||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 8 | ||||

| Interests of Twitter’s Directors and Executive Officers in the Merger |

9 | |||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 31 | ||||

| 33 | ||||

| 33 | ||||

| 33 | ||||

| 33 | ||||

| 33 | ||||

| 34 | ||||

| 34 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

-i-

Table of Contents

| 36 | ||||

| 36 | ||||

| 37 | ||||

| 37 | ||||

| 38 | ||||

| Important Notice Regarding the Availability of Proxy Materials |

38 | |||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 39 | ||||

| 40 | ||||

| 40 | ||||

| 41 | ||||

| 41 | ||||

| Recommendation of the Twitter Board and Reasons for the Merger |

55 | |||

| 60 | ||||

| 71 | ||||

| 78 | ||||

| Interests of Twitter’s Directors and Executive Officers in the Merger |

81 | |||

| 89 | ||||

| 89 | ||||

| 95 | ||||

| 95 | ||||

| 98 | ||||

| 102 | ||||

| 102 | ||||

| 105 | ||||

| 105 | ||||

| 106 | ||||

| 107 | ||||

| 108 | ||||

| 109 | ||||

| 109 | ||||

| Effects of the Merger; Certificate of Incorporation; Bylaws; Directors and Officers |

110 | |||

| 110 | ||||

| Payment Agent, Exchange Fund and Exchange and Payment Procedures |

112 | |||

| 113 | ||||

| 116 | ||||

-ii-

Table of Contents

| 119 | ||||

| The Twitter Board’s Recommendation; Board Recommendation Change |

121 | |||

| 122 | ||||

| 122 | ||||

| 123 | ||||

| 126 | ||||

| 128 | ||||

| 128 | ||||

| 130 | ||||

| 131 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

133 | |||

| 136 | ||||

| 137 | ||||

| 139 | ||||

|

|

|

| ||

| ANNEX B – Section 262 of the Delaware General Corporation Law |

|

|

| |

|

|

|

| ||

|

|

|

| ||

-iii-

Table of Contents

Except as otherwise specifically noted in this proxy statement, “Twitter,” “we,” “our,” “us” and similar words refer to Twitter, Inc., including, in certain cases, our subsidiaries. Throughout this proxy statement, the “Twitter Board” refers to Twitter’s Board of Directors. Throughout this proxy statement, we refer to X Holdings I, Inc. as “Parent” and X Holdings II, Inc. as “Acquisition Sub.” In addition, throughout this proxy statement we refer to the Agreement and Plan of Merger (as it may be amended from time to time), dated April 25, 2022, between Twitter, Parent, Acquisition Sub and, solely for the purposes described therein, Elon Musk as the “merger agreement.”

This summary highlights selected information from this proxy statement related to the proposed merger of Acquisition Sub (a wholly owned subsidiary of Parent) with and into Twitter, with Twitter surviving and continuing as a wholly owned subsidiary of Parent. We refer to that transaction as the “merger.”

This proxy statement may not contain all of the information that is important to you. To understand the merger more fully and for a complete description of its legal terms, you should carefully read this proxy statement, including the annexes to this proxy statement and the other documents to which we refer in this proxy statement. You may obtain the information incorporated by reference in this proxy statement without charge by following the instructions in the section of this proxy statement captioned “Where You Can Find More Information.” A copy of the merger agreement is attached as Annex A to this proxy statement. We encourage you to read the merger agreement, which is the legal document that governs the merger, carefully and in its entirety.

On April 25, 2022, Twitter agreed to be acquired by an affiliate of Elon Musk. If the merger is completed, each outstanding share of our common stock (which we refer to as our “common stock”) (subject to certain exceptions) will be converted into the right to receive $54.20 per share in cash.

Parties Involved in the Merger

Twitter, Inc.

Twitter is what’s happening in the world and what people are talking about right now. Our primary product, Twitter, is a global platform for public self-expression and conversation in real time. We have democratized content creation and distribution so people can consume, create, distribute and discover content about the topics and events they care about most. Through Topics, Interests, and Trends, we help people discover what’s happening through text, images, on demand and live video, and audio from people, content partners, media organizations, advertisers and others. Media outlets, websites, and other partners extend the reach of Twitter content by distributing Tweets beyond our app and website.

Our common stock is listed on the New York Stock Exchange (which we refer to as the “NYSE”) under the symbol “TWTR.” Twitter’s corporate offices are located at 1355 Market Street, Suite 900, San Francisco, California 94103, and its telephone number is (415) 222-9670.

X Holdings I, Inc.

Parent was formed on April 19, 2022, solely for the purpose of engaging in the transactions contemplated by the merger agreement and has not engaged in any business activities other than as

-1-

Table of Contents

incidental to its formation and in connection with the transactions contemplated by the merger agreement and arranging of the equity financing and the debt financing in connection with the merger.

Parent’s address is c/o Elon Musk, 2110 Ranch Road 620 S. #341886, Austin, TX 78734.

X Holdings II, Inc.

Acquisition Sub is a wholly owned subsidiary of Parent and was formed on April 19, 2022, solely for the purpose of engaging in the transactions contemplated by the merger agreement. Acquisition Sub has not engaged in any business activities other than as incidental to its formation and in connection with the transactions contemplated by the merger agreement and arranging of the equity financing and the debt financing in connection with the merger. Upon completion of the merger, Acquisition Sub will cease to exist and Twitter will continue as the surviving corporation.

Acquisition Sub’s address is c/o Elon Musk, 2110 Ranch Road 620 S. #341886, Austin, TX 78734.

Elon Musk

Elon Musk leads SpaceX, Tesla, Inc., Neuralink Corp. and The Boring Company. Mr. Musk has served as the Chief Executive Officer of Tesla, Inc. since October 2008, as a member of the Board of Directors of Tesla, Inc. since April 2004, as the Chief Executive Officer, Chief Technology Officer and Chairman of the Board of SpaceX since May 2002, and served as Chairman of the Board of SolarCity Corporation, a solar installation company, from July 2006 until its acquisition by Tesla in November 2016. Mr. Musk is also the founder of The Boring Company and of Neuralink Corp. Mr. Musk also co-founded Zip2 Corporation, an early internet company, and PayPal. Mr. Musk has served on the board of directors of Endeavor Group Holdings, Inc. since April 2021. Mr. Musk holds a B.A. in physics from the University of Pennsylvania and a B.S. in business from the Wharton School of the University of Pennsylvania.

Mr. Musk’s address is 2110 Ranch Road 620 S. #341886, Austin, TX 78734.

Upon the terms and subject to the conditions of the merger agreement, and in accordance with the Delaware General Corporation Law (which we refer to as the “DGCL”), at the effective time of the merger: (1) Acquisition Sub will merge with and into Twitter; (2) the separate existence of Acquisition Sub will cease; and (3) Twitter will continue as the surviving corporation in the merger and as a wholly owned subsidiary of Parent. Throughout this proxy statement, we use the term “surviving corporation” to refer to Twitter as the surviving corporation following the merger.

As a result of the merger, Twitter will cease to be a publicly traded company. If the merger is completed, you will not own any shares of capital stock of the surviving corporation.

The time at which the merger becomes effective (which we refer to as the “effective time of the merger”) will occur upon the filing of a certificate of merger with, and acceptance of that certificate by, the Secretary of State of the State of Delaware (or at a later time as Twitter, Parent and Acquisition Sub may agree and specify in the certificate of merger).

At the effective time of the merger, each outstanding share of our common stock (subject to certain exceptions) will be automatically canceled and will cease to exist and will be converted into the right to

-2-

Table of Contents

receive $54.20 in cash, without interest. We refer to this amount as the “per share price.” For more information, see the section of this proxy statement captioned “The Merger Agreement—Conversion of Shares.”

Prior to the closing of the merger, Parent will designate an appropriate paying agent to make payments of the merger consideration to our stockholders. At or prior to the effective time of the merger, Parent will deposit (or cause to be deposited) with the paying agent cash constituting an amount equal to the aggregate merger consideration in accordance with the merger agreement. Once a stockholder (subject to certain exceptions) has provided the paying agent with any documentation required by the paying agent, the paying agent will pay such stockholder the appropriate portion of the aggregate merger consideration (subject to any applicable withholding taxes) in exchange for the shares of our common stock held by that stockholder. For more information, see the section of this proxy statement captioned “The Merger Agreement—Paying Agent, Exchange Fund and Exchange and Payment Procedures.”

After the merger is completed, you will have the right to receive the per share price for each share of our common stock that you own, but you will no longer have any rights as a stockholder of Twitter (except that our stockholders who properly and validly exercise and perfect, and do not validly withdraw or otherwise lose, their demand for appraisal or dissenters’ rights under the DGCL or other applicable law will have the right to receive a payment for the “fair value” of their shares as determined pursuant to an appraisal proceeding as contemplated by the DGCL, as described in the section of this proxy statement captioned “The Merger—Appraisal Rights”).

Date, Time and Place

A special meeting of our stockholders will be held on [•], 2022, at [•], Pacific time. You may attend the special meeting via a live interactive webcast at http://www.virtualshareholdermeeting.com/TWTR2022SM. We refer to the special meeting, and any adjournment, postponement or other delay of the special meeting, as the “special meeting.” You will need the control number found on your proxy card or voting instruction form in order to participate in the special meeting (including voting your shares). We believe that a virtual meeting provides expanded access, improved communication and cost savings for our stockholders and Twitter.

Purpose

At the special meeting, we will ask stockholders to vote on proposals to: (1) adopt the merger agreement; (2) approve, on a non-binding, advisory basis, the compensation that will or may become payable by Twitter to our named executive officers in connection with the merger; and (3) adjourn the special meeting, from time to time, to a later date or dates, if necessary or appropriate, to solicit additional proxies if there are insufficient votes to adopt the merger agreement at the time of the special meeting.

Record Date; Shares Entitled to Vote

You are entitled to vote at the special meeting if you owned shares of our common stock as of the close of business on [•], 2022 (which we refer to as the “record date”). For each share of our common stock that you owned as of the close of business on the record date, you will have one vote on each matter submitted for a vote at the special meeting.

-3-

Table of Contents

Quorum

As of the record date, there were [•] shares of our common stock outstanding and entitled to vote at the special meeting. The holders of a majority of the voting power of our stock issued and outstanding and entitled to vote, present in person or represented by proxy, shall constitute a quorum.

Required Vote

The proposals to be voted on at the special meeting require the following votes:

| • | Proposal 1: Approval of the proposal to adopt the merger agreement requires the affirmative vote of the holders of a majority of the shares of our common stock outstanding as of the record date. |

| • | Proposal 2: Approval of the proposal to approve the compensation that will or may become payable by Twitter to our named executive officers in connection with the merger requires the affirmative vote of a majority of the voting power of the shares of our common stock present in person or represented by proxy at the special meeting and entitled to vote on the proposal. This vote will be on a non-binding, advisory basis. |

| • | Proposal 3: Approval of the proposal to adjourn the special meeting, from time to time, to a later date or dates, if necessary or appropriate, to solicit additional proxies if there are insufficient votes to adopt the merger agreement at the time of the special meeting requires the affirmative vote of a majority of the voting power of the shares of our common stock present in person or represented by proxy at the special meeting and entitled to vote on the proposal. |

Voting and Proxies

Any stockholder of record entitled to vote at the special meeting may vote in any of the following ways:

| • | by proxy, by returning a signed and dated proxy card (a proxy card and a prepaid reply envelope are enclosed for your convenience); |

| • | by proxy, by granting a proxy electronically over the internet or by telephone (using the instructions found on the proxy card); or |

| • | by attending the special meeting and voting at the special meeting using the control number on the enclosed proxy card. |

If you are a stockholder of record, you may change your vote or revoke your proxy at any time before it is voted at the special meeting by (1) signing another proxy card with a later date and returning it prior to the special meeting; (2) submitting a new proxy electronically over the internet or by telephone after the date of the earlier submitted proxy; (3) delivering a written notice of revocation to our Corporate Secretary; or (4) attending the special meeting and voting at the special meeting.

If you are a beneficial owner and hold your shares of our common stock in “street name” through a bank, broker or other nominee, you should instruct your bank, broker or other nominee on how you wish to vote your shares of our common stock using the instructions provided by your bank, broker or other nominee. Under applicable stock exchange rules, banks, brokers or other nominees have the discretion to vote on routine matters, but not on non-routine matters. The proposals to be considered

-4-

Table of Contents

at the special meeting are all non-routine matters, and banks, brokers and other nominees cannot vote on these proposals without your instructions. Therefore, it is important that you cast your vote or instruct your bank, broker or nominee on how you wish to vote your shares.

If you hold your shares of our common stock in “street name,” you should contact your bank, broker or other nominee for instructions regarding how to change your vote. You may also vote at the special meeting if you provide a “legal proxy” from your bank, broker or other nominee giving you the right to vote your shares at the special meeting.

Recommendation of the Twitter Board and Reasons for the Merger

The Twitter Board, after considering various factors described in the section of this proxy statement captioned “The Merger—Recommendation of the Twitter Board and Reasons for the Merger,” unanimously: (1) determined that the merger agreement is advisable and the merger and the other transactions contemplated by the merger agreement are fair to, advisable and in the best interests of Twitter and its stockholders; and (2) adopted and approved the merger agreement, the merger and the other transactions contemplated by the merger agreement.

The Twitter Board unanimously recommends that you vote: (1) “FOR” the adoption of the merger agreement; (2) “FOR” the compensation that will or may become payable by Twitter to our named executive officers in connection with the merger; and (3) “FOR” the adjournment of the special meeting, from time to time, to a later date or dates, if necessary or appropriate, to solicit additional proxies if there are insufficient votes to adopt the merger agreement at the time of the special meeting.

Opinion of Goldman Sachs & Co. LLC

At a meeting of the Twitter Board held on April 25, 2022, Goldman Sachs & Co. LLC (which we refer to as “Goldman Sachs”) rendered its oral opinion, subsequently confirmed by delivery of its written opinion, dated April 25, 2022, to the Twitter Board that, as of the date of the written opinion and based upon and subject to limitations, qualifications and assumptions set forth therein, the $54.20 in cash per share of Twitter common stock to be paid to the holders (other than Parent, Mr. Musk and their respective affiliates) of such shares pursuant to the merger agreement was fair from a financial point of view to such holders, as more fully described in the section of this proxy statement captioned “The Merger—Opinion of Goldman Sachs & Co. LLC.”

The full text of the written opinion of Goldman Sachs, dated April 25, 2022, which sets forth assumptions made, procedures followed, matters considered and limitations on the review undertaken in connection with the opinion, is attached as Annex C to this proxy statement. Goldman Sachs provided advisory services and its opinion for the information and assistance of the Twitter Board in connection with its consideration of the merger. The Goldman Sachs opinion is not a recommendation as to how any holder of our common stock should vote with respect to the merger or any other matter.

Opinion of J.P. Morgan Securities LLC

At the meeting of the Twitter Board on April 25, 2022, J.P. Morgan Securities LLC (which we refer to as “J.P. Morgan”) rendered its oral opinion to the Twitter Board that, as of such date and based upon and subject to the factors and assumptions set forth in its opinion, the consideration to be paid to our common stockholders in the proposed transaction was fair, from a financial point of view, to such stockholders. J.P. Morgan has confirmed its April 25, 2022 oral opinion by delivering its written opinion to the Twitter Board, dated April 25, 2022, that, as of such date, the consideration to be paid to

-5-

Table of Contents

Twitter’s common stockholders in the proposed merger was fair, from a financial point of view, to such stockholders, as more fully described in the section of this proxy statement captioned “The Merger—Opinion of J.P. Morgan Securities LLC.”

The full text of the written opinion of J.P. Morgan dated April 25, 2022, which sets forth, among other things, the assumptions made, matters considered and limits on the review undertaken, is attached as Annex D to this proxy statement. The summary of the opinion of J.P. Morgan set forth in this proxy statement is qualified in its entirety by reference to the full text of such opinion. Twitter’s stockholders are urged to read the opinion in its entirety. J.P. Morgan’s written opinion was addressed to the Twitter Board (in its capacity as such) in connection with and for the purposes of its evaluation of the proposed merger, was directed only to the $54.20 per share in cash to be paid to holders of our common stock pursuant to the merger agreement and did not address any other aspect of the merger. J.P. Morgan expressed no opinion as to the fairness of the consideration to the holders of any class of securities, creditors or other constituencies of Twitter or as to the underlying decision by Twitter to engage in the proposed merger. The issuance of J.P. Morgan’s opinion was approved by a fairness committee of J.P. Morgan. The summary of the opinion of J.P. Morgan set forth in this proxy statement is qualified in its entirety by reference to the full text of such opinion. The opinion does not constitute a recommendation to any stockholder of Twitter as to how such stockholder should vote with respect to the proposed merger or any other matter.

Treatment of Equity Awards in the Merger

The merger agreement provides that Twitter’s equity awards that are outstanding immediately prior to the effective time of the merger will be treated in the following manner in connection with the merger. For more information, see the section of this proxy statement captioned “The Merger Agreement—Conversion of Shares—Equity Awards; ESPP.” We refer to awards of restricted stock units as “Twitter RSUs” (including performance-based restricted stock units, or “Twitter PSUs”) and restricted stock as “Twitter equity-based awards.” We refer to awards of stock options to purchase shares of our common stock as “Twitter options.”

Treatment of Twitter Equity-based Awards

| • | At the effective time of the merger, each vested Twitter equity-based award (other than a vested Twitter option) outstanding as of immediately prior to the effective time of the merger will be canceled and converted into the right to receive an amount in cash, without interest and less any required withholding taxes, equal to the product of (1) the per share price and (2) the total number of shares of our common stock subject to such vested Twitter equity-based award (and with respect to any vested equity-based awards subject to performance vesting conditions, calculated based on the achievement of the applicable performance metrics at the level of performance at which such equity-based award vested in accordance with its terms). |

| • | At the effective time of the merger, each unvested Twitter equity-based award (other than an unvested Twitter option) outstanding as of immediately prior to the effective time of the merger will be canceled and converted into the right to receive an amount in cash, without interest and less any required withholding taxes, equal to the product of (1) the per share price and (2) the total number of shares of our common stock subject to such unvested Twitter equity-based award (and with respect to any unvested equity-based awards subject to performance vesting conditions, calculated based on the achievement of the applicable performance metrics at the target level of performance), which amount will, subject to the holder’s continued service with Parent and its affiliates (including the surviving corporation and its subsidiaries) through the |

-6-

Table of Contents

| applicable vesting dates, vest and be payable at the same time as the unvested Twitter equity-based award for which such cash amount was exchanged would have vested pursuant to its terms and will otherwise remain subject to the same terms and conditions as were applicable to the unvested Twitter equity-based award immediately prior to the effective time of the merger (other than performance-based vesting conditions, which will not apply following the effective time of the merger). |

Treatment of Twitter Options

| • | At the effective time of the merger, each vested Twitter option outstanding as of immediately prior to the effective time of the merger will be canceled and converted into the right to receive an amount in cash, without interest and less any required withholding taxes, equal to the product of (1) the excess, if any, of the per share price less the exercise price per share of our common stock underlying such Twitter option, and (2) the total number of shares of our common stock subject to such Twitter option. |

| • | At the effective time of the merger, each unvested Twitter option outstanding as of immediately prior to the effective time of the merger will be canceled and converted into the right to receive an amount in cash, without interest and less any required withholding taxes, equal to the product of (1) the excess, if any, of the per share price less the exercise price per share of our common stock underlying such Twitter option, and (2) the total number of shares of our common stock subject to such Twitter option, which cash amount will, subject to the holder’s continued service with Parent and its affiliates (including the surviving corporation and its subsidiaries) through the applicable vesting dates, vest and be payable at the same time as the unvested Twitter option for which such cash amount was exchanged would have vested pursuant to its terms and will otherwise remain subject to the same terms and conditions as were applicable to the unvested Twitter option immediately prior to the effective time of the merger. |

| • | At the effective time of the merger, any Twitter option outstanding as of immediately prior to the effective time of the merger and for which the exercise price per share of our common stock underlying such Twitter options is equal to or greater than the per share price will be canceled without any cash payment or other consideration being made in respect of such Twitter option. |

Treatment of the ESPP

| • | As provided in the merger agreement, the Twitter Board has adopted resolutions that provide that (1) the current offering period under our 2013 Employee Stock Purchase Plan (which we refer to as the “ESPP”) will be the final offering period and no further offering period will commence pursuant to the ESPP after the date of the merger agreement, and (2) except as may be required by law, each individual participating in the final offering period as of the date of the merger agreement will not be permitted to (a) increase his or her payroll contribution rate pursuant to the ESPP from the rate in effect when the final offering period commenced or (b) make separate non-payroll contributions to the ESPP on or following the date of the merger agreement. |

| • | Prior to the effective time of the merger, Twitter will take all actions that may be necessary to give effect to the treatment described above and to (1) cause the final offering period, to the extent that it would otherwise be outstanding at the effective time, to be terminated no later |

-7-

Table of Contents

| than 10 business days prior to the date on which the effective time of the merger occurs; (2) make any pro rata adjustments that may be necessary to reflect the final offering period, but otherwise treat the final offering period as a fully effective and completed offering period for all purposes pursuant to the ESPP; and (3) cause the exercise (as of no later than 10 business days prior to the date on which the effective time of the merger occurs) of each outstanding purchase right pursuant to the ESPP. |

| • | On such exercise date, Twitter will apply the funds credited as of such date pursuant to the ESPP within each participant’s payroll withholding account to the purchase of whole shares of our common stock in accordance with the terms of the ESPP, and such shares of our common stock will be entitled to the per share price. Immediately prior to and effective as of the effective time of the merger (but subject to the consummation of the merger), Twitter will terminate the ESPP. |

| • | For a period of one year following the effective time of the merger, Parent will, or will cause the surviving corporation or any of their affiliates to, provide for each continuing employee (1) at least the same base salary and wage rate, (2) short- and long-term target incentive compensation opportunities that are no less favorable in the aggregate than those provided to each such continuing employee immediately prior to the effective time of the merger (provided that Parent will not be obligated to provide such incentives in the form of equity or equity-based awards) and (3) employee benefits (excluding equity and equity-based awards) which are substantially comparable in the aggregate (including with respect to the proportion of employee cost) to those provided to such continuing employee immediately prior to the effective time of the merger. During the one-year period following the effective time of the merger, Parent will, or will cause the surviving corporation or any of their affiliates to, provide severance payments and benefits to each continuing employee that are no less favorable than those applicable to the continuing employee immediately prior to the effective time of the merger under the existing arrangements providing for compensation or employee benefits (which we refer to as “Twitter benefit plans”). |

| • | Parent agrees that the surviving corporation will cause the surviving corporation’s employee benefit plans established following the closing of the merger (if any) and any other employee benefit plans covering the continuing employees following the effective time of the merger (which we refer to, collectively, as the “post-closing benefit plans”), to recognize the service of each continuing employee (to the extent such service was recognized by Twitter) for purposes of eligibility, vesting and determination of the level of benefits (but not for the benefit accrual purposes under a defined benefit pension plan) under the post-closing benefit plans, to the extent such recognition does not result in the duplication of any benefits. |

| • | For the calendar year including the effective time of the merger, the continuing employees will not be required to satisfy any deductible, co-payment, out-of-pocket maximum or similar requirements under the post-closing benefit plans that provide medical, dental and other welfare benefits (which we refer to, collectively, as the “post-closing welfare plans”) to the extent amounts were previously credited for such purposes under comparable Twitter benefit plans that provide medical, dental and other welfare benefits. |

| • | As of the effective time of the merger, any waiting periods, pre-existing condition exclusions and requirements to show evidence of good health contained in such post-closing welfare |

-8-

Table of Contents

| plans will be waived with respect to the continuing employees (except to the extent any such waiting period, pre-existing condition exclusion or requirement to show evidence of good health was already in effect with respect to such employees and has not been satisfied under the applicable Twitter benefit plan in which the participant then participates or is otherwise eligible to participate as of immediately prior to the effective time of the merger). |

For more information, see the section of this proxy statement captioned “The Merger Agreement—Employee Benefits.”

Interests of Twitter’s Directors and Executive Officers in the Merger

When considering the recommendation of the Twitter Board that you vote to approve the proposal to adopt the merger agreement, you should be aware that our directors and executive officers may have interests in the merger that are different from, or in addition to, your interests as a stockholder. In (1) evaluating and negotiating the merger agreement, (2) approving the merger agreement and the merger and (3) recommending that the merger agreement be adopted by our stockholders, the Twitter Board was aware of and considered these interests to the extent that they existed at the time, among other matters. These interests include the following:

| • | For our executive officers, the treatment of their Twitter equity-based awards, as described in more detail in the section of this proxy statement captioned “The Merger—Interests of Twitter’s Directors and Executive Officers in the Merger—Treatment of Equity-Based Awards.” |

| • | For our non-employee directors, the treatment of their Twitter equity-based awards and Twitter options, as described in more detail in the section of this proxy statement captioned “The Merger—Interests of Twitter’s Directors and Executive Officers in the Merger—Treatment of Equity-Based Awards.” |

| • | The entitlement of each of our executive officers to receive payments and benefits pursuant to Twitter’s Change of Control and Involuntary Termination Policy (which we refer to as the “severance policy”) if, during the period beginning on our change of control (or, in the case of Mr. Agrawal, beginning three months before our change of control) and ending 12 months after our change of control (which we refer to as the “COC period”), Twitter terminates their employment with Twitter for a reason other than “cause,” death or “disability” or they resign for “good reason” (which we refer to as an “involuntary termination”), in each case as set forth in the severance policy. These payments and benefits include: |

| ○ | a lump sum payment equal to 100 percent of base salary; |

| ○ | payment of continuation of coverage premiums under the Consolidated Omnibus Budget Reconciliation Act of 1985 (which we refer to as “COBRA”) for up to 12 months, or taxable payments in lieu of such payment; and |

| ○ | 50 percent (or 100 percent in the case of Mr. Agrawal and Mr. Segal) acceleration of vesting of unvested equity awards (with performance-based vesting deemed achieved at target levels as to that percentage). |

| • | The continued indemnification and insurance coverage for our directors and executive officers from the surviving corporation and Parent under the terms of the merger agreement. |

-9-

Table of Contents

If the merger is consummated, our stockholders who (1) do not vote in favor of the adoption of the merger agreement; (2) continuously hold their applicable shares of our common stock through the effective time of the merger; (3) properly demand appraisal of their applicable shares; (4) meet certain statutory requirements described in this proxy statement; and (5) do not withdraw their demands or otherwise lose their rights to appraisal, will be entitled to seek appraisal of their shares in connection with the merger under Section 262 of the DGCL if certain conditions set forth in Section 262(g) of the DGCL are satisfied. This means that these stockholders will be entitled to have their shares appraised by the Delaware Court of Chancery and to receive payment in cash of the “fair value” of their shares of our common stock, exclusive of any elements of value arising from the accomplishment or expectation of the merger, together with (unless the Delaware Court of Chancery in its discretion determines otherwise for good cause shown) interest on the amount determined by the Delaware Court of Chancery to be fair value from the effective date of the merger through the date of payment of the judgment at a rate of five percent over the Federal Reserve discount rate (including any surcharge) as established from time to time during the period between the effective date of the merger and the date of payment of the judgment, compounded quarterly (except that, if at any time before the entry of judgment in the proceeding, the surviving corporation makes a voluntary cash payment to stockholders seeking appraisal, interest will accrue thereafter only upon the sum of (1) the difference, if any, between the amount so paid and the fair value of the shares as determined by the Delaware Court of Chancery; and (2) interest theretofore accrued, unless paid at that time). The surviving corporation is under no obligation to make such voluntary cash payment prior to such entry of judgment. Due to the complexity of the appraisal process, stockholders who wish to seek appraisal of their shares are encouraged to seek the advice of legal counsel with respect to the exercise of appraisal rights.

Stockholders considering seeking appraisal should be aware that the fair value of their shares as determined pursuant to Section 262 of the DGCL could be more than, the same as or less than the value of the consideration that they would receive pursuant to the merger agreement if they did not seek appraisal of their shares.

Only a stockholder of record may submit a demand for appraisal. To exercise appraisal rights, the stockholder of record must (1) submit a written demand for appraisal to Twitter before the vote is taken on the proposal to adopt the merger agreement; (2) not vote, in person or by proxy, in favor of the proposal to adopt the merger agreement; (3) continue to hold the subject shares of our common stock of record through the effective time of the merger; and (4) strictly comply with all other procedures for exercising appraisal rights under the DGCL. The failure to follow exactly the procedures specified under the DGCL may result in the loss of appraisal rights. In addition, the Delaware Court of Chancery will dismiss appraisal proceedings in respect of Twitter unless certain conditions are satisfied by the stockholders seeking appraisal, as described further below. The requirements under Section 262 of the DGCL for exercising appraisal rights are described in further detail in this proxy statement, which description is qualified in its entirety by Section 262 of the DGCL, the relevant section of the DGCL regarding appraisal rights, a copy of which is attached as Annex B to this proxy statement. If you hold your shares of our common stock through a bank, broker or other nominee and you wish to exercise appraisal rights, you should consult with your bank, broker or other nominee to determine the appropriate procedures for the making of a demand for appraisal on your behalf by your bank, broker or other nominee.

Material U.S. Federal Income Tax Consequences of the Merger

For U.S. federal income tax purposes, the receipt of cash by a U.S. Holder (as defined in the section of this proxy statement captioned “The Merger—Material U.S. Federal Income Tax Consequences of the

-10-

Table of Contents

Merger”) in exchange for such U.S. Holder’s shares of our common stock in the merger generally will result in the recognition of gain or loss in an amount measured by the difference, if any, between the amount of cash that such U.S. Holder receives in the merger and such U.S. Holder’s adjusted tax basis in the shares of our common stock surrendered in the merger.

A Non-U.S. Holder (as defined in the section of this proxy statement captioned “The Merger—Material U.S. Federal Income Tax Consequences of the Merger”) generally will not be subject to U.S. federal income tax with respect to the exchange of our common stock for cash in the merger unless such Non-U.S. Holder has certain connections to the United States, but may be subject to backup withholding tax unless the Non-U.S. Holder complies with certain certification procedures or otherwise establishes a valid exemption from backup withholding tax.

For more information, see the section of this proxy statement captioned “The Merger—Material U.S. Federal Income Tax Consequences of the Merger.” Stockholders should consult their own tax advisors concerning the U.S. federal income tax consequences relating to the merger in light of their particular circumstances and any consequences arising under U.S. federal non-income tax laws or the laws of any territory, state, local or non-U.S. taxing jurisdiction.

Regulatory Approvals Required for the Merger

The merger cannot be completed until the waiting periods (and any extensions thereof, if any) applicable to the merger under the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (which we refer to as the “HSR Act”) and the laws of certain other jurisdictions have expired or otherwise been terminated, or all requisite consents pursuant to those laws have been obtained. Under the merger agreement, each of Twitter, Parent and Acquisition Sub agreed to (1) promptly make its respective filings under the HSR Act, and (2) as promptly as reasonably practicable, make any other applications and filings as are mutually agreed by Parent and Twitter, under any antitrust laws or foreign investment laws with respect to the transactions contemplated by the merger agreement. Although we expect that all required regulatory clearances and approvals will be obtained, we cannot assure you that these regulatory clearances and approvals will be timely obtained or obtained at all, or that the granting of these regulatory clearances and approvals will not involve the imposition of additional conditions on the completion of the merger. For more information, please see the section of this proxy statement captioned “The Merger—Regulatory Approvals Required for the Merger.”

The total amount of funds necessary to consummate the merger and related transactions, including payment of related fees and expenses, will be approximately $46.5 billion. The transactions contemplated by the merger agreement, including (1) the payment of consideration due to our stockholders and the holders of our equity awards under the merger agreement, (2) the repayment of all or a portion of Twitter’s outstanding indebtedness, and (3) the aggregate of all other amounts, costs, fees and expenses required to be paid by Parent will be funded with the proceeds of committed equity and debt financing, as further described below.

Pursuant to an equity commitment letter, as amended and restated (which we refer to as the “equity commitment letter”), Mr. Musk initially committed to contribute or otherwise provide equity capital to Parent in an aggregate amount of up to approximately $21.0 billion in immediately available funds, as necessary to fully discharge, when taken together with the aggregate proceeds of the debt financing (or, if applicable, alternative financing) actually funded at the closing, the amounts required to be funded by Parent in connection with the merger agreement, including (1) the consideration due to our

-11-

Table of Contents

stockholders and the holders of our equity awards under the merger agreement and (2) the aggregate of all other amounts, costs, fees and expenses required to be paid by Parent in connection with the transactions pursuant to and in accordance with the merger agreement. On May 4, 2022, the equity commitment letter was amended to increase Mr. Musk’s financing commitment thereunder to $27.25 billion (which we refer to as the “equity financing”).

Pursuant to a debt commitment letter (which we refer to as the “debt commitment letter”), Morgan Stanley Senior Funding, Inc. and the other financial institutions party thereto committed to provide to Acquisition Sub (which we collectively refer to as the “bank debt financing”):

| • | a senior secured term loan facility in an aggregate principal amount of $6.5 billion; |

| • | a senior secured revolving facility in an aggregate committed amount of $500.0 million; |

| • | up to $3.0 billion in aggregate principal amount of senior secured bridge commitments (which commitments may be replaced by the proceeds of the issuance of one or more series of senior secured notes (in escrow or otherwise) pursuant to a Rule 144A offering or other private placement, as contemplated by the debt commitment letter); and |

| • | up to $3.0 billion in aggregate principal amount of senior unsecured bridge commitments (which commitments may be replaced by the proceeds of the issuance of one or more series of senior unsecured notes (in escrow or otherwise) pursuant to a Rule 144A offering or other private placement, as contemplated by the debt commitment letter). |

The proceeds of the bank debt financing would be used at the closing of the merger, together with the proceeds of the equity financing, for the purposes of (1) financing the consummation of the merger, paying fees and expenses incurred in connection with the merger, and (2) the repayment of all or a portion of Twitter’s outstanding indebtedness (we refer to clause (2) as the “refinancing”).

Pursuant to a margin loan commitment letter (which we refer to as the “margin loan commitment letter”), Morgan Stanley Senior Funding, Inc. and the other financial institutions party thereto committed to provide $12.5 billion (which we refer to as the “margin loan financing”) to X Holdings III, LLC, a Delaware limited liability company of which Mr. Musk is the sole member (which we refer to as “X Holdings III”). The margin loan financing is to be used, together with the proceeds of the equity financing and the bank debt financing, for the purpose of financing the consummation of the merger and paying fees and expenses incurred in connection with the merger. On May 4, 2022, the aggregate principal amount of the commitments available to X Holdings III under the margin loan commitment letter was reduced to an aggregate principal amount of $6.25 billion. For more information, please see the section of this proxy statement captioned “The Merger Agreement—Efforts to Close the Merger—Financing.”

Restrictions on Solicitation of Other Acquisition Offers

Under the merger agreement, during the period commencing on the date of the merger agreement and continuing until the earlier of the effective time of the merger or the date, if any, of termination of the merger agreement, Twitter has agreed that it will, and will cause each of its directors, executive officers and subsidiaries to, and will instruct its other representatives to, immediately cease and cause to be terminated any existing solicitation of, or discussions or negotiations with, any third party relating to any competing proposal.

-12-

Table of Contents

Until the earlier of the effective time of the merger or the date, if any, of termination of the merger agreement, except as otherwise provided in the relevant provisions of the merger agreement, Twitter has agreed that it will not, and will cause each of its directors, executive officers and subsidiaries not to, and it will instruct its other representatives not to:

| • | solicit, initiate, knowingly encourage or knowingly facilitate, whether publicly or otherwise, any substantive discussion, offer or request that constitutes, or would reasonably be expected to lead to, a competing proposal; or |

| • | engage in negotiations or substantive discussions with, or furnish any material non-public information to, any person relating to a competing proposal or any inquiry or proposal that would reasonably be expected to lead to a competing proposal. |

In addition, until the earlier of the effective time of the merger or the date, if any, of termination of the merger agreement, Twitter has agreed to:

| • | as promptly as reasonably practicable, and in any event within one business day of receipt by Twitter or any of its directors, executive officers or subsidiaries of any competing proposal or any request that would reasonably be expected to lead to the making of a competing proposal, deliver to Parent a written notice setting forth the identity of the person making such competing proposal or request and the material terms and conditions of any such competing proposal; and |

| • | keep Parent reasonably informed of any material amendment or other modification of any such competing proposal or request on a prompt basis, and in any event within two business days following Twitter’s receipt in writing of such an amendment or modification. |

However, at any time prior to obtaining the requisite stockholder approval, in the event that Twitter receives a competing proposal from any person or group of persons, (1) Twitter and its representatives may contact such person to clarify the terms and conditions thereof and (2) Twitter, the Twitter Board and their respective representatives may engage in negotiations or discussions with, or furnish any information and other access to, any person or group of persons making such competing proposal and any of its representatives or potential sources of financing if the Twitter Board determines in good faith (after consultation with its legal counsel and financial advisors) that such competing proposal either constitutes a superior proposal or would reasonably be expected to result in a superior proposal; provided that (a) prior to furnishing any material non-public information concerning Twitter or its subsidiaries, Twitter receives from such person or group, to the extent that such person or group is not already subject to a confidentiality agreement with Twitter, an executed confidentiality agreement containing customary confidentiality terms (it being understood that such confidentiality agreement need not contain a standstill provision or otherwise restrict the making, or amendment, of a competing proposal to Twitter or the Twitter Board) and (b) any such material non-public information so furnished in writing shall be promptly made available to Parent to the extent it was not previously made available to Parent or its representatives. For more information, see the section of this proxy statement captioned “The Merger Agreement—Restrictions on Solicitation of Other Acquisition Offers.”

Twitter is not entitled to terminate the merger agreement to enter into an agreement for a superior proposal unless it complies with certain procedures in the merger agreement, including engaging in good faith negotiations with Parent during a specified period. If Twitter terminates the merger agreement in order to accept a superior proposal from a third party it must pay a termination fee to Parent. For more information, see the section of this proxy statement captioned “The Merger Agreement—The Twitter Board’s Recommendation; Board Recommendation Change.”

-13-

Table of Contents

Change in the Twitter Board’s Recommendation

Under the merger agreement, the Twitter Board will not (1) publicly recommend that Twitter’s stockholders vote against the adoption of the merger agreement, (2) approve or recommend to Twitter’s stockholders any competing proposal (we refer to the actions described in (1) and (2), collectively, as a “Twitter Board recommendation change”), or (3) approve or recommend or allow Twitter to enter into an agreement with respect to a competing proposal, other than, under certain circumstances, if it determines in good faith, after consultation with its legal counsel and financial advisors, that (a) failure to take such action would reasonably be expected to be inconsistent with the Twitter Board’s fiduciary duties under applicable law or (b) a competing proposal constitutes a superior proposal, and, in each case, the Twitter Board complies with the terms of the merger agreement. If Twitter or Parent terminates the merger agreement under certain circumstances, including because of a Twitter Board recommendation change prior to the adoption of the merger agreement, then Twitter must pay to Parent a termination fee. For more information, see the section of this proxy statement captioned “The Merger Agreement—The Twitter Board’s Recommendation; Board Recommendation Change.”

Conditions to the Closing of the Merger

The obligations of Parent, Acquisition Sub and Twitter, as applicable, to consummate the merger are subject to the satisfaction or waiver of certain conditions, including the following:

| • | the adoption of the merger agreement by the requisite affirmative vote of our stockholders; |

| • | the expiration or termination of the waiting period applicable to the merger under the HSR Act, and, to the extent applicable, each consent or approval required under any antitrust laws or foreign investment laws in certain specified jurisdictions having been made, obtained or received (or, as applicable, the waiting periods, if any, with respect thereto will have expired or been terminated); and |

| • | the absence of any then-effective law or order enacted, issued, promulgated, enforced or entered into by any governmental authority in certain specified jurisdictions which has the effect of restraining, enjoining, rendering illegal or otherwise prohibiting consummation of the merger, or causing the merger to be rescinded following the consummation thereof. |

The obligations of Parent and Acquisition Sub to consummate the merger are subject to the satisfaction or waiver of each of the following additional conditions, any of which may be waived by Parent:

| • | Twitter having performed and complied in all material respects with the obligations required by the merger agreement to be performed or complied with by it on or prior to the closing of the merger; |

| • | the accuracy of the representations and warranties of Twitter in the merger agreement, subject to applicable materiality or other qualifiers, as of the effective time of the merger or the date in respect of which such representation or warranty was specifically made; and |

| • | the absence of any Company Material Adverse Effect (as defined in the section of this proxy statement captioned “The Merger Agreement—Representations and Warranties”) having occurred that is continuing. |

-14-

Table of Contents

The obligation of Twitter to consummate the merger are subject to the satisfaction or waiver of each of the following additional conditions, any of which may be waived by Twitter:

| • | Parent and Acquisition Sub having performed and complied in all material respects with the obligations required by the merger agreement to be performed or complied with by Parent or Acquisition Sub on or prior to the closing of the merger; and |

| • | the accuracy of the representations and warranties of Parent and Acquisition Sub in the merger agreement, subject to applicable materiality or other qualifiers, as of the effective time of the merger or the date in respect of which such representation or warranty was specifically made. |

Termination of the Merger Agreement

The merger agreement may be terminated at any time prior to the effective time of the merger, whether before or after the adoption of the merger agreement by our stockholders (except as otherwise provided in the merger agreement), in the following ways:

| • | by mutual written agreement of Twitter and Parent; |

| • | by either Twitter or Parent if: |

| ○ | the merger has not been consummated by 5:00 p.m., Pacific time, on October 24, 2022 (as such date may be extended pursuant to the terms of this provision, which we refer to as the “termination date”), except that (1) a party may not terminate the merger agreement pursuant to this provision if such party’s failure to perform or comply with any of its obligations under the merger agreement has been the principal cause of, or resulted in, the failure to consummate the merger by the termination date, and (2) the termination date will be extended for an additional six months if, as of the termination date, the closing condition regarding (a) the expiration or termination of the waiting period under the HSR Act or the receipt of approvals under the other specified antitrust laws or foreign investment laws or (b) the absence of any applicable legal restraint prohibiting the consummation of the merger has not been satisfied; |

| ○ | prior to the effective time of the merger, any governmental authority of competent jurisdiction has enacted, issued, promulgated, enforced or entered any law or order or taken any other action permanently restraining, enjoining, rendering illegal or otherwise prohibiting the consummation of the transactions contemplated by the merger agreement, and such law or order or other action has become final and non-appealable, except, in each case, that the right to terminate will not be available to any party (1) that has failed to use the efforts required by the merger agreement to remove such law, order or other action, or (2) if the issuance of such law or order or taking of such action was primarily due to the failure of such party, and, in the case of Parent, the failure of Acquisition Sub or Mr. Musk, to perform any of its obligations under the merger agreement; or |

| ○ | our stockholders do not adopt the merger agreement at the special meeting (or at any adjournment or postponement thereof at which the merger agreement and the transactions contemplated thereby are voted on); |

-15-

Table of Contents

| • | by Twitter if: |

| ○ | subject to a 30-day cure period, Parent, Acquisition Sub or Mr. Musk has breached or failed to perform any of their respective representations, warranties, covenants or other agreements in the merger agreement, which breach or failure would give rise to the failure of relevant conditions to effect the closing of the merger, except that the right to terminate will not be available to Twitter if Twitter is then in material breach of any of its representations, warranties, covenants or agreements under the merger agreement; |

| ○ | the Twitter Board has authorized Twitter to enter into a definitive agreement with respect to a superior proposal, if, substantially concurrently with the termination of the merger agreement, Twitter enters into such definitive agreement and pays (or causes to be paid) the termination fee to and at the direction of Parent; or |

| ○ | (1) Parent and Acquisition Sub have been notified in writing that the conditions precedent to Parent’s and Acquisition Sub’s obligations to close the merger set forth in the merger agreement (other than those conditions that by their nature are to be satisfied at the closing, each of which is capable of being satisfied if the closing were to occur at such time) have been satisfied or waived in accordance with the merger agreement; (2) Parent and Acquisition Sub fail to consummate the merger within three business days following the date on which the closing should have occurred; and (3) during such three business day period, Twitter stood ready, willing and able to consummate the merger and the other transactions contemplated by the merger agreement; and |

| • | by Parent if: |

| ○ | subject to a 30-day cure period, Twitter has breached or failed to perform any of its representations, warranties, covenants or other agreements in the merger agreement, which breach or failure would give rise to the failure of relevant conditions to effect the closing of the merger, except that the right to terminate will not be available to Parent if Parent, Acquisition Sub or Mr. Musk is then in material breach of any of its representations, warranties, covenants or agreements under the merger agreement; or |

| ○ | prior to the adoption of the merger agreement by the requisite affirmative vote of our stockholders, the Twitter Board has made a Twitter Board recommendation change. |

The merger agreement contains certain termination rights for Twitter and Parent.

Upon valid termination of the merger agreement under specified circumstances, Twitter will be required to pay, at the direction of Parent, a termination fee of $1,000,000,000. Specifically, this termination fee will be payable by Twitter to Parent if:

| • | (1) a third party will have made a competing proposal after the date of the merger agreement, (2) the merger agreement is subsequently terminated by (a) Twitter or Parent because our stockholders have failed to approve the merger agreement at the special meeting or (b) Parent as a result of a breach or failure by Twitter to perform any of its representations, warranties, |

-16-

Table of Contents

| covenants or other agreements in the merger agreement (subject to a 30-day cure period), which breach or failure would give rise to the failure of any condition to effect the closing of the merger, and at the time of such special meeting or breach, as applicable, a competing proposal has been publicly announced and has not been withdrawn, and (3) within 12 months of such termination of the merger agreement, Twitter consummates a transaction involving a competing proposal or enters into a definitive agreement providing for the consummation of a competing proposal and such competing proposal is subsequently consummated (provided that, for purposes of this paragraph, all percentages in the definition of competing proposal are increased to 50 percent); |

| • | the merger agreement is terminated by Twitter to enter into a definitive agreement with respect to a superior proposal; or |

| • | the merger agreement is terminated by Parent if the Twitter Board made a Twitter Board recommendation change prior to the adoption of the merger agreement by the requisite affirmative vote of our stockholders. |

Upon valid termination of the merger agreement under certain specified circumstances, Parent will be required to pay, at the direction of Twitter, a termination fee of $1,000,000,000, the payment of which has been guaranteed pursuant and subject to the terms and conditions of the limited guaranty. Specifically, the termination fee will be payable by Parent to Twitter if the merger agreement is terminated by Twitter:

| • | as a result of a breach or failure by Parent, Acquisition Sub or Mr. Musk to perform any of its respective representations, warranties, covenants or other agreements in the merger agreement (subject to a 30-day cure period), which breach or failure would give rise to the failure of relevant conditions to effect the closing of the merger; or |

| • | because Parent and Acquisition Sub failed to consummate the merger as required pursuant to, and in the circumstances specified in, and subject to the terms of, the merger agreement while Twitter stood ready, willing and able to consummate the merger and the other transactions contemplated by the merger agreement. |

The merger agreement also provides that Twitter, on one hand, or Parent and Acquisition Sub, on the other hand, may specifically enforce the obligations under the merger agreement in accordance with its terms. In addition, Twitter is entitled to obtain specific performance or other equitable relief to enforce Parent’s and Acquisition Sub’s obligations to cause Mr. Musk to fund the equity financing, or to enforce Mr. Musk’s obligation to fund the equity financing directly, and to consummate the closing of the merger, if certain conditions are satisfied, including the funding or availability of the debt financing.

Neither Parent nor Twitter is required to pay to the other a termination fee on more than one occasion.

Pursuant to the limited guarantee delivered by Elon Musk in favor of Twitter, dated as of April 25, 2022 (which we refer to as the “limited guarantee”), Mr. Musk agreed to guarantee the due, complete and punctual payment, observance, performance and discharge of the payment obligations of Parent under the merger agreement, including the termination fee payable by Parent, plus amounts in respect of reimbursement, indemnification or other payment obligations of Parent for certain costs, expenses, monetary damages or losses incurred or sustained by Twitter, subject to the conditions set forth in the limited guarantee. For more information, please see the section of this proxy statement captioned “The Merger—Limited Guarantee.”

-17-

Table of Contents