Form 485BPOS CYBER HORNET TRUST

Tweet

Tweet Share

Share

As filed with the Securities and Exchange Commission

on

Securities Act Registration No. 333-129930

Investment Company Act Reg. No. 811-21836

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | ☒ | |

| Pre-Effective Amendment No. | ☐ | |

| Post-Effective Amendment No. 78 | ☒ | |

| and/or | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | ☒ | |

| Amendment No. 82 | ☐ | |

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

200 Central Avenue, Suite 800

St. Petersburg, FL 33701

(Address of Principal Executive Offices) (Zip Code)

Registrant's Telephone Number, including Area Code: (727) 502-0808

| Michael G. Willis |

| 200 Central Avenue, Suite 800 |

| St. Petersburg, FL 33701 |

(Name and Address of Agent for Service)

With Copies To:

| Bo J. Howell |

| FinTech Law, LLC |

| 6224 Turpin Hills Drive |

| Cincinnati, Ohio 45244 |

Approximate Date of Proposed Public Offering: Immediately following effectiveness of this post-effective amendment.

It is proposed that this filing will become effective (check appropriate box)

| ☐ | immediately upon filing pursuant to paragraph (b) |

| ☒ | On January 29, 2026 pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | on (date) pursuant to paragraph (a)(1) |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) |

| ☐ | on (date) pursuant to paragraph (a)(2) of rule 485. |

If appropriate, check the following box:

| ☐ | This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

| CYBER HORNET S&P 500® and Bitcoin 75/25 Strategy ETF | BBB |

| CYBER HORNET S&P 500® and Ethereum 75/25 Strategy ETF | EEE |

| CYBER HORNET S&P 500® and Solana 75/25 Strategy ETF | SSS |

| CYBER HORNET S&P 500® and XRP 75/25 Strategy ETF | XXX |

Prospectus

The shares of each Fund are not individually redeemable by the Fund but are traded on the NASDAQ in individual share lots.

THE SEC HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

An investment in the Fund is not a bank deposit and is not insured by the Federal Deposit Insurance Corporation or any other government agency. An investment in the Fund involves investment risks, and you may lose money in the Fund.

CYBER HORNET S&P 500® and Bitcoin 75/25 Strategy ETF

CYBER HORNET S&P 500® and Ethereum 75/25 Strategy ETF

CYBER HORNET S&P 500® and Solana 75/25 Strategy ETF

CYBER HORNET S&P 500® and XRP 75/25 Strategy ETF

each, a series of CYBER HORNET TRUST

TABLE OF CONTENTS

About this Prospectus

This prospectus has been arranged into different sections so that you can easily review this important information. For detailed information about the Fund, please see:

CYBER HORNET S&P 500® AND BITCOIN 75/25 STRATEGY ETF SUMMARY

The Fund seeks to replicate, before fees and expenses, the total return of the S&P 500® and S&P Bitcoin 75/25 Blend Index (the “Index”), an index by Standard & Poor’s.

The following table describes the expenses and fees that you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Shareholder Fees | |

| (fees paid directly from your investment) | None |

| Annual Fund Operating Expenses | |

| (expenses that you pay each year as a percentage of the value of your investment) |

| Management Fees1 | |

| Distribution (12b-1) Fees | |

| Other Expenses | |

| Total Annual Fund Operating Expenses |

| 1 |

This Example is intended to help you compare the costs of investing in the Fund with the costs of investing in other funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. Expenses assuming no redemption are also shown. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses (excluding any sales loads on reinvested dividends, fee waivers and/or expense reimbursements) shown in the table above remain the same. The expenses used to calculate the Fund’s Example do not include fee waivers or expense reimbursements. Although your actual costs and returns may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years |

| $ |

$ |

$ |

$ |

The

Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio).

A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held

in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s

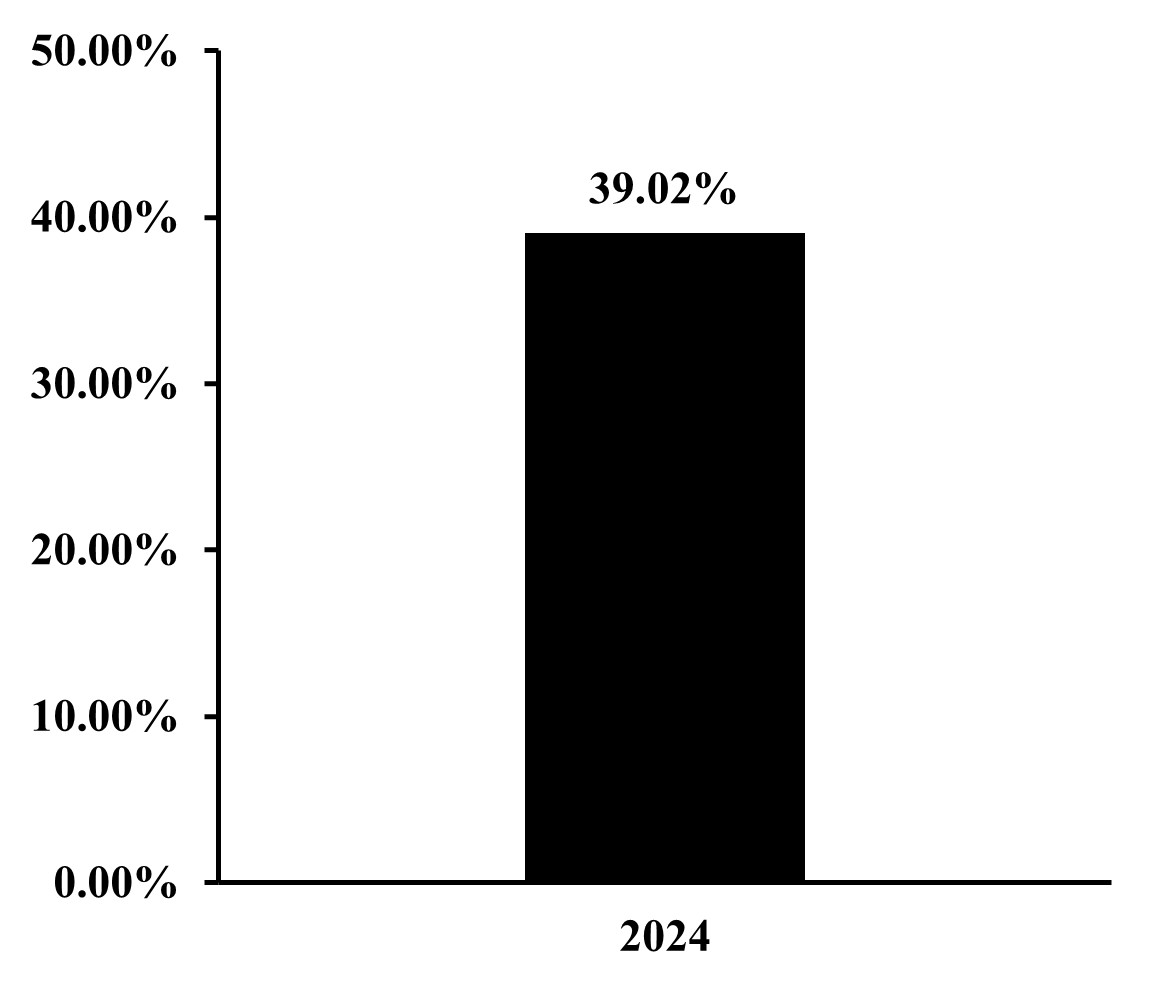

performance. During the Fund’s most recent fiscal period ended March 31, 2025, the Fund’s portfolio turnover was

3

The Fund seeks to replicate, before fees and expenses, the total return of the S&P 500® and S&P Bitcoin 75/25 Blend Index (the “Index”). The Index measures the weighted return performance of a multi-asset strategy comprising a 75% weight in the S&P 500® Index and a 25% weight in the S&P Bitcoin Index. Accordingly, in seeking to track the Index, the Fund will invest approximately 75% of its assets in a portfolio of common stocks that are included in the S&P 500® Index and will invest directly in Bitcoin so that the total value of the Bitcoin to which the Fund has economic exposure is approximately 25% of the assets of the Fund. S&P Dow Jones Indices LLC (“S&P DJI” or the “Index Provider”) compiles, maintains, and calculates the Index and each of the S&P 500® Index and the S&P Bitcoin Futures Index. The Index is rebalanced monthly and accordingly the Fund seeks to maintain the 75%/25% allocations by also rebalancing these allocations monthly. However, price fluctuations in the underlying assets and other factors, such as the Fund’s cash position, may cause these allocations to vary at any time. The Adviser reserves the right to rebalance the Fund’s allocations more frequently than monthly in periods of significant price volatility or less frequently than monthly to save on trading costs or during periods of low volatility. The Adviser may rebalance the Fund’s allocations on any day of the month. Such rebalancing decisions are made solely to reduce tracking error and enhance after-fee performance relative to the Index.

U.S. Large-Cap

The Fund attempts to replicate this portion of its portfolio by investing in a portfolio of the common stocks included in the S&P 500® Index, holding each stock in proportion similar to its weighting in the S&P 500® Index. The Fund may hold more or fewer stocks than the index at any given time. The Fund may sell investments represented in the S&P 500® Index in anticipation of their removal from the S&P 500® Index or buy investments not yet represented in the Index in anticipation of their addition to it. The Fund may also invest in securities of other investment companies, such as certain ETFs,to implement its investment strategy.

Bitcoin

Under normal conditions, the Fund will invest in Bitcoin so that the total value of Bitcoin to which the Fund has economic exposure is approximately 25% of the assets of the Fund. The Fund will invest directly in Bitcoin through a subsidiary company organized under the laws of the Cayman Islands (the “Subsidiary”). The Fund may also gain exposure to Bitcoin by investing in Bitcoin futures contracts, and in shares of other exchange-traded funds (“ETFs”) and exchange-traded products (“ETPs”) which provide exposure to Bitcoin (collectively, the “Bitcoin ETPs”), although the Fund expects that its futures and ETP exposure will generally be less than 10% of its assets, Such exposure seeks to track, before fees and expenses, the performance of the S&P Bitcoin Futures Index. The S&P Bitcoin Index is designed to track the performance the digital asset Bitcoin. However, changes in the relative value of the Fund’s assets between the monthly rebalance could cause the Fund’s investments in Bitcoin, Bitcoin futures positions, and Bitcoin ETPs to represent greater than 25% of the Fund’s assets.

The Fund will generally purchase and sell Bitcoin on exchanges such as BitGo or Coinbase, neither of which is registered as a national securities exchange with the SEC. The price of Bitcoin on these exchanges and over-the-counter markets has a limited history, is volatile, and is subject to the influence of many factors, including operational interruptions.

Bitcoin held directly by the Fund is maintained at a qualified custodian. The custodian uses “cold storage” security measures for storing the private keys necessary to access the Fund’s Bitcoin offline in a manner that is not connected to the internet. This is designed to protect cryptocurrencies from hacking or other cybersecurity threats.

The ownership of Bitcoin is determined by participants in a decentralized, peer-to-peer network that connects computers that run publicly accessible, or “open source,” software, commonly referred to as the “Bitcoin Protocol.” The value of Bitcoin is determined, in part, by the supply of, and demand for, Bitcoin in the markets created to facilitate the trading of Bitcoin. Ownership and the ability to transfer or take other actions with respect to Bitcoin is protected through public-key cryptography. The supply of Bitcoin is determined by the Bitcoin Protocol which limits both the total amount of Bitcoin that will be produced to 21 million and the rate at which it is released into the network.

4

When the Fund invests in Bitcoin futures contracts, the Fund must sell its futures contracts as they near expiration and replace them with new futures contracts with a later expiration date. The Adviser anticipates that this “roll” of the futures contracts will normally occur shortly before the expiration of the current month contract in the last week of the month. However, such timing may change due to market conditions. Futures contracts with a longer term to expiration may be priced higher than futures contracts with a shorter term to expiration (e.g. trading at “contango”). Bitcoin futures have historically experienced extended periods of contango. Contango in the Bitcoin futures market may have a significant adverse impact on the performance of the Fund and may cause it to significantly deviate from the performance of the Index. The Fund will only invest in Bitcoin futures contracts that are traded on a futures exchange regulated by the Commodity Futures Trading Commission (“CFTC”). The Fund (or the Subsidiary, as applicable) also invests in short-term U.S. government securities intended to serve as margin or collateral for futures positions.

The Fund may invest in Bitcoin ETPs that invest directly in, provide exposure to, replicate the performance of, or have trading and/or price performance characteristics similar to Bitcoin.

PRINCIPAL RISKS

The following describes the principal risks of investing in the Fund, which could affect the Fund’s net asset value and total return. Other circumstances (including additional risks not described here) could prevent the Fund from achieving its investment objective. These risks are presented in an order that reflects the Adviser’s assessment of relative importance, but this assessment could change over time as the Fund’s portfolio changes or in light of changes in the market or the economic environment, among other things. The Fund is not required to and will not update this Prospectus solely because the Adviser’s assessment of the relative importance of the principal risks of investing in the Fund changes.

Bitcoin, Bitcoin futures contracts, and Bitcoin ETPs are relatively new investments. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. The value of an investment in the Fund could decline significantly and without warning. You should be prepared to lose the entirety of the Bitcoin component of your investment in the Fund. The performance of Bitcoin futures contracts and Bitcoin ETPs, and therefore the performance of the Fund may differ significantly from the performance of Bitcoin.

Equity Risk – The values of equity securities may decline due to general market conditions which are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment generally. The prices of equity securities fluctuate, and sometimes widely, in response to activities specific to the security issuer. Equity securities generally have greater price volatility than fixed-income securities. Returns from large-capitalization stocks may trail returns from the overall stock market. Large-cap stocks tend to go through cycles of performing better or worse than other segments of the stock market or the stock market in general. These periods have, in the past, lasted several years.

Bitcoin Risk – The Bitcoin network has a limited history relative to traditional commodities and currencies. There is no assurance that use or acceptance of Bitcoin will continue to grow. A contraction in use or adoption of Bitcoin may result in increased volatility or a reduction in the price of Bitcoin, which would likely have an adverse impact on the value of the Shares. Sales of newly created or “mined” Bitcoin may cause the price of Bitcoin to decline, which could negatively affect an investment in the Shares. Bitcoin trading prices experience high levels of volatility, and in some cases such volatility has been sudden and extreme. Because of such volatility, Shareholders could lose all or substantially all of the Bitcoin component of their investment in the Fund in a very short time, even in the course of one day. Shareholders who invest in the Fund should actively monitor their investments. The Bitcoin network could cease to be a focal point for developer activity, and there is no assurance that the most active developers who participate in monitoring and upgrading the software protocols on which the Bitcoin network is based will continue to do so in the future, which could damage the network or reduce Bitcoin’s competitiveness with competing digital assets or blockchain protocols. Disruptions at Bitcoin spot markets and in the Bitcoin futures markets could adversely affect the availability or price of Bitcoin.

From time to time, developers may suggest changes to the bitcoin software. If a sufficient number of users and miners elect not to adopt the changes, a new digital asset, operating on the earlier version of the bitcoin software, may be created. This is often referred to as a “fork.” Bitcoin has been forked numerous times to launch new digital assets. Additional hard forks of the Bitcoin blockchain could impact demand for bitcoin or other digital assets and could adversely impact the Fund’s Bitcoin futures. A fork in the Bitcoin network could adversely affect the market for Bitcoin futures in which the Fund invests and, therefore, an investment in the Fund.

5

Bitcoin exchanges and other trading venues on which bitcoin trades are relatively new and, in most cases, largely unregulated and may therefore be more exposed to fraud and failure than established, regulated exchanges for securities and derivatives. Bitcoin exchanges have in the past, and may in the future, stop operating or permanently shut down due to fraud, cybersecurity issues, manipulation, technical glitches, hackers or malware, which may also affect the price of bitcoin and thus the Fund’s indirect investment in bitcoin. All networked systems are vulnerable to various kinds of attacks. As with any computer network, the Bitcoin network contains certain flaws. For example, the Bitcoin network is currently vulnerable to a “51% attack” where, if a mining pool were to gain control of more than 50% of the “hash” rate, or the amount of computing and process power being contributed to the network through mining, a malicious actor would be able to gain full control of the network and the ability to manipulate the blockchain. A significant portion of bitcoin may be held by a small number of holders sometimes referred to as “whales.” These holders have the ability to manipulate the price of bitcoin. As a digital asset, bitcoin is subject to cybersecurity risks, including the risk that malicious actors will exploit flaws in its code or structure that will allow them to, among other things, steal bitcoin held by others, control the blockchain, steal personally identifying information, or issue significant amounts of bitcoin in contravention of the Bitcoin protocols.

The occurrence of any of these events is likely to have a significant adverse impact on the price and liquidity of bitcoin and Bitcoin Futures and therefore the value of an investment in the Fund. Additionally, the Bitcoin network’s functionality relies on the Internet. A significant disruption of Internet connectivity affecting large numbers of users or geographic areas could impede the functionality of the Bitcoin network. Any technical disruptions or regulatory limitations that affect Internet access may have an adverse effect on the Bitcoin network, the price of bitcoin and Bitcoin Futures, and the value of an investment in the Fund.

Rebalancing Costs and Tax Risk. The Fund is subject to the risk of rebalancing to track the Index that may result in significant transaction costs and tax consequences for shareholders. The Fund seeks to maintain a 75% allocation to the S&P 500 Index and a 25% allocation to the S&P Cryptocurrency Top 10 Index. The Fund rebalances these allocations monthly and may rebalance more frequently during periods of significant market volatility. When cryptocurrency prices rise or fall relative to equity prices between rebalancing dates, the Fund must sell appreciated assets and purchase depreciated assets to restore the target allocation of 75% to 25% in equity and cryptocurrency, respectively. These transactions generate transaction costs and may result in the realization of capital gains that will be distributed to shareholders.

Risks Related to the Regulation of Cryptocurrency. Any final determination by a court that a cryptocurrency is a “security” or “commodity” may adversely affect the value of the cryptocurrency and the value of the Fund’s shares, and, if the cryptocurrency is not, or cannot, be registered as a security, result in a potential termination of the Fund.

Depending on its characteristics, a cryptocurrency may be considered a “security” under the federal securities laws. The test for determining whether a particular cryptocurrency is a “security” is complex and challenging to apply, and the outcome is difficult to predict. If an appropriate court determines that the relevant cryptocurrency is a security, the Adviser would not intend to permit the Fund to continue holding its investments in a way that would violate the federal securities laws (and therefore, if necessary, would either dissolve the Fund or potentially seek to operate the Fund in a manner that complies with the federal securities laws).

Cryptocurrency Market Volatility Risk. The prices of cryptocurrencies have historically been highly volatile. The value of the Fund’s exposure to a cryptocurrency – and therefore the value of an investment in the Fund – could decline significantly and without warning, including to zero. If you are not prepared to accept significant and unexpected changes in the value of the Fund and the possibility that you could lose your entire investment in the cryptocurrency component of the Fund, you should not invest in it.

Cryptocurrency Futures Contracts Risk – The market for cryptocurrency futures contracts may be less developed, potentially less liquid, and more volatile than more established futures markets. While the cryptocurrency futures contracts market has grown substantially since cryptocurrency futures contracts commenced trading, there can be no assurance that this growth will continue. The price for cryptocurrency futures contracts is based on many factors, including the supply and demand for cryptocurrency futures contracts. Market conditions and expectations, position limits, collateral requirements, and other factors can each impact the supply and demand for cryptocurrency futures contracts. At times, increased demand paired with supply constraints and other factors have caused cryptocurrency futures contracts to trade at a significant discount or premium to the “spot” price of the relevant cryptocurrency. Additional demand, including demand resulting from the purchase, or anticipated purchase, of cryptocurrency futures contracts by the Fund or other entities, may increase that premium, perhaps significantly. It is impossible to predict whether or how long such conditions will continue. To the extent the Fund purchases futures contracts at a premium and the premium declines, the value of an investment in the Fund also should be expected to decline.

6

Market conditions and expectations, position limits, collateral requirements, and other factors may also limit the Fund’s ability to achieve its desired exposure to cryptocurrency futures contracts. If the Fund cannot achieve such exposure, it may not meet its investment objective, and its returns may be different from the index or lower than expected. Additionally, collateral requirements may require the Fund to liquidate its position, potentially incurring losses and expenses, when it otherwise would not do so. Investing in derivatives like cryptocurrency futures contracts may be considered aggressive and expose the Fund to significant risks. These risks include counterparty risk and liquidity risk. The performance of cryptocurrency futures contracts and the relevant cryptocurrency may differ and may not be correlated with each other, over short or long periods, and may cause cryptocurrency futures to underperform the spot price of the relevant cryptocurrency.

Cryptocurrency Futures Capacity Risk – If the Fund’s ability to obtain exposure to cryptocurrency futures contracts consistent with its investment objective is disrupted for any reason including, for example, limited liquidity in the cryptocurrency futures market, a disruption to the cryptocurrency futures market, or as a result of margin requirements or position limits imposed by the Fund’s futures commission merchants (“FCMs”), the CME, or the CFTC, the Fund may not be able to achieve its investment objective and may experience significant losses. Margin levels for cryptocurrency futures contracts are substantially higher than the margin requirements for more established futures contracts. Margin requirements are subject to change and may be raised in the future by the exchanges on which they trade and the FCMs. High margin requirements could prevent the Fund from obtaining its desired exposure to cryptocurrency futures and may adversely affect the Fund’s ability to achieve its investment objective. Any disruption in the Fund’s ability to get exposure to cryptocurrency futures contracts will cause the Fund’s performance to deviate from the performance of the relevant cryptocurrency, cryptocurrency futures, or the Index.

Cost of Futures Investment Risk – When a cryptocurrency futures contract is nearing expiration, the Fund will typically “roll” the futures contract, which means it will generally sell such a contract and use the proceeds to buy a cryptocurrency futures contract with a later expiration date. The price difference between the expiring contract and longer-dated contract associated with rolling cryptocurrency futures may be substantially higher than the price difference associated with rolling other futures contracts. Additionally, the returns of cryptocurrency futures may differ from those of the relevant cryptocurrency. These differences in returns can arise due to several factors, including the costs associated with futures investments, such as “rolling,” supply and demand dynamics, interest rates, and market expectations.

Cryptocurrency ETP Investing Risk. Issuer-specific attributes related to ETPs in which the Fund may invest may cause an investment held by the Fund to be more volatile than the market generally. The value of an individual security or asset, or a particular type of security or asset, may be more volatile than the market as a whole and perform differently from the value of the market as a whole. When the Fund invests in ETPs, it will incur costs related to such funds, including management fees and expenses borne by shareholders of such ETPs. The value of shares in an ETP may not replicate the performance of the relevant cryptocurrency, and, therefore, the Fund’s investments in the ETPs will not perform the same as the Fund’s direct investments in the relevant cryptocurrency.

Leverage Risk. Leverage risk is created when an investment, which includes, for example, an investment in a derivative contract, exposes the Fund to a level of risk that exceeds the amount invested. Changes in the value of such an investment magnify the Fund’s risk of loss and potential for gain. Investments can have these same results if their returns are based on a multiple of a specified index, security, or other benchmark.

Investment in the Subsidiary Risk – The Fund is exposed to the risks of the Subsidiary’s investments, which are exposed to the risks of investing in Bitcoin futures contracts. The Fund will also incur the expenses of the Subsidiary. Although the Subsidiary is not registered under the 1940 Act, it will provide investors with the same protections the Fund provides.

Tracking Error Risk – Various factors may impede the Fund's ability to track the Index or achieve a high degree of correlation with the Index. Factors contributing to tracking error include:

| ● | Fees and Expenses: The Fund has operating and other expenses, while the Index does not. The Fund's expense ratio reduces net asset value, while the Index reflects gross performance without deductions for fees or expenses. |

7

| ● | Transaction Costs: Buying and selling cryptocurrencies and Cryptocurrency-Related Products involve bid-ask spreads, market impact costs, trading fees, and blockchain network transaction fees that reduce the Fund's returns but are not reflected in Index performance. |

| ● | Cash Drag: The Fund may not be fully invested at times, generally due to cash flows into or out of the Fund, rebalancing activities, or excess cash held for various reasons. Cash positions create performance drag when cryptocurrency prices appreciate and may provide relative benefit when prices depreciate. |

Rebalancing and Reallocation Timing: The Fund cannot instantaneously adjust holdings when rebalancing or reallocation events occur. Settlement of cryptocurrency transactions requires blockchain confirmations, custody transfers, and operational processes that create timing lags. During these lags, the Fund's composition may differ from the target portfolio.

Investment in Investment Companies Risk – Investing in other investment companies, including money market funds, ETFs, and ETPs, subjects the Fund to the fees and expenses of, as well as risks affecting, the investment company, including the possibility that the value of the underlying securities held by the investment company could decrease.

Trading Halt Risk – An exchange or market may issue trading halts on specific securities, contracts, or instruments, or may close early or late, which will affect the Fund’s ability to buy or sell certain securities. In such circumstances, the Fund may be unable to rebalance its portfolio, may be unable to accurately price its investments or may incur substantial trading losses.

Exchange-Traded Fund (ETF) Risks –

Absence of an Active Market: Although the Fund’s shares are approved for listing on the NASDAQ (the “Exchange”), there can be no assurance that an active trading market will develop and be maintained for Fund shares. There can also be no assurance that the Fund will grow to or maintain an economically viable size, in this case it may experience greater tracking error to its Index than it otherwise would at higher asset levels or may ultimately liquidate.

Authorized Participants (“APs”), Market Makers, and Liquidity Providers Concentration: The Fund has a limited number of financial institutions that may act as APs. In addition, there may be a limited number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events occur, Shares may trade at a material discount to net asset value (“NAV”) and possibly face delisting: (i) APs exit the business or otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business activities and no other entities step forward to perform their functions.

Cash Transaction Risk. The Fund intends to affect some portion of redemptions for cash, rather than in-kind, because of the nature of the Fund’s investments. The Fund may be required to sell portfolio securities to obtain the cash needed to distribute redemption proceeds, which involves transaction costs that the Fund may not have incurred had it effected redemptions entirely in kind. These costs may include brokerage costs and/or taxable gains or losses, which may be imposed on the Fund and decrease the Fund’s NAV. If the Fund recognizes gain on these sales, this generally will cause the Fund to recognize gain it might not otherwise have recognized if it were to distribute all of its portfolio securities in-kind, or to recognize such gain sooner than would otherwise be required. This may decrease the tax efficiency of the Fund compared to ETFs that utilize a complete in-kind redemption process.

8

Trading Issues: Trading in Fund shares may be halted due to market conditions or for reasons that make trading in shares inadvisable in the view of the Exchange. There can be no assurance that the requirements of the Exchange necessary to maintain the listing of any Fund will continue to be met or will remain unchanged, or that the shares will trade with any volume. Further, secondary markets may be subject to erratic trading activity, wide bid/ask spreads, and extended trade settlement periods in times of market stress because market makers and APs may step away from making a market in Fund shares and in executing creation and redemption orders, which could cause a material deviation in the Fund’s market price from its NAV.

Passive Investment Risk. The Fund is not actively managed and therefore would not sell an equity security, futures contract or other investment due to current or projected underperformance of a security, industry, sector, or asset class. Unlike with an actively managed fund, the Adviser does not use techniques or defensive strategies designed to lessen the effects of market volatility or to reduce the impact of periods of market decline. This means that, based on market and economic conditions, the Fund’s performance could be lower than other types of funds that may actively shift their portfolio assets to take advantage of market opportunities or to lessen the impact of a market decline.

All

investments carry some degree of risk that will affect the value of the Fund, its investment performance and the price of its

shares.

9

During

the period shown in the bar chart, the

| 1 Year | Since Inception ( | |

| CYBER HORNET S&P 500® AND BITCOIN 75/25 STRATEGY ETF | ||

| Return Before Taxes | ||

| Return After Taxes on Distributions | ||

| Return After Taxes on Distributions and Sale of Fund Shares | ||

S&P 500 TR |

||

S&P 500 and S&P Bitcoin Futures 75/25 Blend Index (reflects no deduction for fees, expenses or taxes) |

||

FUND MANAGEMENT

INVESTMENT ADVISER

CYBER HORNET ETFs, LLC (formerly known as “ONEFUND, LLC”) serves as the investment adviser to the Fund.

PORTFOLIO MANAGER

Michael G. Willis, portfolio manager of the Adviser, has managed the Fund since its inception in December 2023.

PURCHASE AND SALE OF FUND SHARES

Individual shares may only be purchased and sold through a broker-dealer on a national securities exchange. You can buy and sell individual shares of the Fund any day the Nasdaq Stock Market (“NASDAQ”) is open for business, like any publicly traded security. The Fund’s shares are listed on the Nasdaq Stock Market exchange. The price of the Fund’s shares is based on market price, and because exchange-traded fund shares trade at market prices rather than NAV, shares may trade at a price greater than NAV (premium) or less than NAV (discount). The Fund issues and redeems shares continuously, at NAV, only in blocks of 25,000 shares (“Creation Units”), which may be partially in-kind for securities included in the Index and partially in cash, and only Authorized Participants (typically, broker-dealers) may purchase or redeem Creation Units. Except when aggregated in Creation Units, the Fund’s shares are not redeemable securities.

TAX INFORMATION

For U.S. federal income tax purposes, the Fund’s distributions are taxable. They will be taxed as ordinary income or capital gains, unless you invest through a tax-advantaged arrangement, such as a 401(k) plan or an individual retirement account. Such tax-advantaged arrangements are subject to special tax rules upon withdrawal of monies from those arrangements.

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Adviser or its affiliates may pay the intermediary to sell Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

10

CYBER HORNET S&P 500® AND ETHEREUM 75/25 STRATEGY ETF SUMMARY

The CYBER HORNET S&P 500® and Ethereum 75/25 Strategy ETF (the “Fund”) seeks to replicate, before fees and expenses, the total return of the S&P 500® and S&P Ethereum 75/25 Blend Index (the “Index”), an index by Standard & Poor’s.

The following table describes the expenses and fees that you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Shareholder Fees | |

| (fees paid directly from your investment) | None |

| Annual Fund Operating Expenses | |

| (expenses that you pay each year as a percentage of the value of your investment) |

| Management Fees1 | |

| Distribution (12b-1) Fees | |

| Other Expenses | |

| Total Annual Fund Operating Expenses |

| 1 |

This Example is intended to help you compare the costs of investing in the Fund with the costs of investing in other funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. Expenses assuming no redemption are also shown. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses (excluding any sales loads on reinvested dividends, fee waivers, and/or expense reimbursements) shown in the table above remain the same. The expenses used to calculate the Fund’s Example do not include fee waivers or expense reimbursements. Although your actual costs and returns may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years |

| $ |

$ |

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or the example, affect the Fund’s performance. Because the Fund is newly organized, portfolio turnover information is unavailable.

11

The Fund seeks to replicate, before fees and expenses, the total return of the S&P 500® and S&P Ethereum 75/25 Blend Index (the “Index”). The Index measures the weighted return performance of a multi-asset strategy comprising two underlying indexes, a 75% weight in the S&P 500® Index and a 25% weight in the S&P Ethereum Index. Accordingly, in seeking to track the Index, the Fund will invest approximately 75% of its assets in a portfolio of common stocks that are included in the S&P 500® Index and will invest directly in Ether, so that the total value of the Ether to which the Fund has economic exposure is approximately 25% of the assets of the Fund. S&P Dow Jones Indices LLC (“S&P DJI” or the “Index Provider”) compiles, maintains, and calculates the Index and each of the S&P 500® Index and the S&P Ethereum Index. The Index is rebalanced monthly, and accordingly, the Fund seeks to maintain the 75%/25% allocations by also rebalancing these allocations monthly. However, price fluctuations in the underlying assets and other factors, such as the Fund’s cash position, may cause these allocations to vary at any time. The Adviser reserves the right to rebalance the Fund’s allocations more frequently than monthly in periods of significant price volatility or less frequently than monthly to save on trading costs or during periods of low volatility. The Adviser may rebalance the Fund’s allocations on any day of the month. Such rebalancing decisions are made solely to reduce tracking error and enhance after-fee performance relative to the Index.

U.S. Large-Cap

The Fund attempts to replicate this portion of its portfolio by investing in a portfolio of the common stocks included in the S&P 500 Index, holding each stock in proportion similar to its weighting in the S&P 500 Index. The Fund may hold more or fewer stocks than the index at any given time. The Fund may sell investments represented in the S&P 500 Index in anticipation of their removal from the S&P 500 Index or buy investments not yet represented in the index in anticipation of their addition to it. The Fund may also invest in securities of other investment companies, such as certain ETFs, to implement its investment strategy.

Ether

Under normal conditions, the Fund will invest in Ether so that the total value of the Ether to which the Fund has economic exposure is approximately 25% of the Fund’s assets. The Fund will invest directly in Ether through a wholly-owned subsidiary company, Cyber Hornet EEE, organized under the laws of the Cayman Islands (the “Subsidiary”). The Fund may also gain exposure to Ether by investing in Ether futures contracts, and in shares of other exchange-traded funds (“ETFs”) and exchange-traded products (“ETPs”) which provide exposure to Ether (collectively, “Ethereum ETPs” and, together with the Ether futures contracts, “Cryptocurrency-Related Products”), although the Fund expects that its futures and ETP exposure will generally be less than 10% of its assets. Such exposure seeks to track, before fees and expenses, the performance of the S&P Ethereum Index. The S&P Ethereum Index is designed to track the performance of the digital asset Ethereum. However, changes in the relative value of the Fund’s assets between the monthly rebalance could cause the Fund’s investment in Ether, Ether futures positions, and Ethereum ETPs to represent greater than 25% of the Fund’s assets.

The Fund will generally purchase and sell Ether on exchanges such as BitGo or Coinbase, neither of which is registered as a national securities exchange with the SEC. The price of Ether on these exchanges and over-the-counter markets has a limited history, is volatile, and is subject to the influence of many factors, including operational interruptions.

Ether held directly by the Fund is maintained at a qualified custodian. The custodian uses "cold storage" security measures for storing the private keys necessary to access the Fund's Ether offline in a manner that is not connected to the internet. This is designed to protect cryptocurrencies from hacking or other cybersecurity threats.

The value of Ether is not backed by any government, corporation, or other identified body. Instead, its value is determined in part by the supply and demand in markets created to facilitate the trading of Ether. Ownership and transaction records for Ether are protected through public-key cryptography. The Ethereum Protocol determines the supply of Ether. No single entity owns or operates the Ethereum Network.

12

When the Fund invests in Ether futures contracts, the Fund must sell its futures contracts as they near expiration and replace them with new futures contracts with a later expiration date. The Adviser anticipates that this “roll” of the futures contracts will normally occur shortly before the expiration of the current month contract in the last week of the month. However, such timing may change due to market conditions. Futures contracts with a longer term to expiration may be priced higher than futures contracts with a shorter term to expiration (e.g., trading at “contango”). Ether futures have historically experienced extended periods of contango. Contango in the Ether futures market may have a significant adverse impact on the performance of the Fund and may cause it to significantly deviate from the performance of the Index. The Fund will only invest in Ether futures contracts that are traded on a futures exchange regulated by the Commodity Futures Trading Commission (“CFTC”). The Fund (or the Subsidiary, as applicable) also invests in short-term U.S. government securities intended to serve as margin or collateral for futures positions.

The Fund may invest in Ethereum ETPs that invest directly in, provide exposure to, replicate the performance of, or have trading and/or price performance characteristics similar to Ether.

PRINCIPAL RISKS

The following describes the principal risks of investing in the Fund, which could affect the Fund’s net asset value and total return. Other circumstances (including additional risks not described here) could prevent the Fund from achieving its investment objective. These risks are presented in an order that reflects the Adviser’s assessment of relative importance, but this assessment could change over time as the Fund’s portfolio changes or in light of changes in the market or the economic environment, among other things. The Fund is not required to and will not update this Prospectus solely because the Adviser’s assessment of the relative importance of the principal risks of investing in the Fund changes.

Ether, Ether futures contracts, and Ethereum ETPs are relatively new investments. They are subject to unique and substantial risks and have historically been subject to significant price volatility. The value of an investment in the Fund could decline significantly and without warning. You should be prepared to lose the entirety of the Ether component of your investment in the Fund. The performance of Ether futures contracts and Ethereum ETPs, and therefore the performance of the Fund, may differ significantly from the performance of Ether.

Equity Risk – The values of equity securities may decline due to general market conditions not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment. The prices of equity securities fluctuate, sometimes widely, in response to activities specific to the security issuer. Equity securities generally have greater price volatility than fixed-income securities. Returns from large-capitalization stocks may trail returns from the overall stock market. Large-cap stocks tend to go through cycles of performing better or worse than other segments of the stock market or the stock market in general. These periods have, in the past, lasted several years.

Ether Risk: Ether is a relatively new innovation with unique and substantial risks. The market for Ether is subject to rapid price swings, changes, and uncertainty. A significant portion of the demand for Ether may result from speculation. Such speculation regarding the potential future appreciation of the price of Ether may artificially inflate or deflate the price of Ether and increase volatility. The further development of the Ethereum Network and the acceptance and use of Ether are subject to various factors that are difficult to evaluate. The slowing, stopping, or reversing of the development of the Ethereum Network or the acceptance of Ether may adversely affect Ether's price and liquidity. Ether is subject to the risk of fraud, theft, manipulation, security failures, and operational or other problems that impact Ether trading platforms.

Ether generally trades on trading platforms that support trading in various crypto assets, and such platforms may be unregulated or operating out of compliance with applicable regulations. Ether and Ether trading venues are mainly unregulated, unlike the exchanges for more traditional assets such as equity securities and futures contracts. Crypto asset trading platforms where Ether is traded may become subject to regulatory authorities' enforcement actions. Realizing any of these risks could result in a decline in the acceptance of Ether and, consequently, a reduction in the value of Ether, Ether futures, and the Fund.

Rebalancing Costs and Tax Risk. The Fund is subject to the risk of rebalancing to track the Index that may result in significant transaction costs and tax consequences for shareholders. The Fund seeks to track the Index, which allocates 75% to the S&P 500 Index and 25% to the S&P Ethereum Index. The Fund rebalances these allocations monthly and may rebalance more frequently during periods of significant market volatility. When cryptocurrency prices rise or fall relative to equity prices between rebalancing dates, the Fund must sell appreciated assets and purchase depreciated assets to restore the target allocation of 75% to 25% in equity and cryptocurrency, respectively. These transactions generate transaction costs and may result in the realization of capital gains that will be distributed to shareholders.

13

Risks Related to the Regulation of Cryptocurrency. Any final determination by a court that a cryptocurrency is a “security” or “commodity” may adversely affect the value of the cryptocurrency and the value of the Fund’s shares, and, if the cryptocurrency is not, or cannot, be registered as a security, result in a potential termination of the Fund.

Depending on its characteristics, a cryptocurrency may be considered a “security” under the federal securities laws. The test for determining whether a particular cryptocurrency is a “security” is complex and challenging to apply, and the outcome is difficult to predict. If an appropriate court determines that the relevant cryptocurrency is a security, the Adviser would not intend to permit the Fund to continue holding its investments in a way that would violate the federal securities laws (and therefore, if necessary, would either dissolve the Fund or potentially seek to operate the Fund in a manner that complies with the federal securities laws).

Cryptocurrency Market Volatility Risk. The prices of cryptocurrencies have historically been highly volatile. The value of the Fund’s exposure to a cryptocurrency – and therefore the value of an investment in the Fund – could decline significantly and without warning, including to zero. If you are not prepared to accept significant and unexpected changes in the value of the Fund and the possibility that you could lose your entire investment in the cryptocurrency component of the Fund, you should not invest in it.

Cryptocurrency Futures Contracts Risk – The market for cryptocurrency futures contracts may be less developed, potentially less liquid, and more volatile than more established futures markets. While the cryptocurrency futures contracts market has grown substantially since cryptocurrency futures contracts commenced trading, there can be no assurance that this growth will continue. The price for cryptocurrency futures contracts is based on many factors, including the supply and demand for cryptocurrency futures contracts. Market conditions and expectations, position limits, collateral requirements, and other factors can each impact the supply and demand for cryptocurrency futures contracts. At times, increased demand paired with supply constraints and other factors have caused cryptocurrency futures contracts to trade at a significant discount or premium to the “spot” price of the relevant cryptocurrency. Additional demand, including demand resulting from the purchase, or anticipated purchase, of cryptocurrency futures contracts by the Fund or other entities, may increase that premium, perhaps significantly. It is impossible to predict whether or how long such conditions will continue. To the extent the Fund purchases futures contracts at a premium and the premium declines, the value of an investment in the Fund also should be expected to decline.

Market conditions and expectations, position limits, collateral requirements, and other factors may also limit the Fund’s ability to achieve its desired exposure to cryptocurrency futures contracts. If the Fund cannot achieve such exposure, it may not meet its investment objective, and its returns may be different from the index or lower than expected. Additionally, collateral requirements may require the Fund to liquidate its position, potentially incurring losses and expenses, when it otherwise would not do so. Investing in derivatives like cryptocurrency futures contracts may be considered aggressive and expose the Fund to significant risks. These risks include counterparty risk and liquidity risk. The performance of cryptocurrency futures contracts and the relevant cryptocurrency may differ and may not be correlated with each other, over short or long periods, and may cause cryptocurrency futures to underperform the spot price of the relevant cryptocurrency.

Cryptocurrency Futures Capacity Risk – If the Fund’s ability to obtain exposure to cryptocurrency futures contracts consistent with its investment objective is disrupted for any reason including, for example, limited liquidity in the cryptocurrency futures market, a disruption to the cryptocurrency futures market, or as a result of margin requirements or position limits imposed by the Fund’s futures commission merchants (“FCMs”), the CME, or the CFTC, the Fund may not be able to achieve its investment objective and may experience significant losses. Margin levels for cryptocurrency futures contracts are substantially higher than the margin requirements for more established futures contracts. Margin requirements are subject to change and may be raised in the future by the exchanges on which they trade and the FCMs. High margin requirements could prevent the Fund from obtaining its desired exposure to cryptocurrency futures and may adversely affect the Fund’s ability to achieve its investment objective. Any disruption in the Fund’s ability to get exposure to cryptocurrency futures contracts will cause the Fund’s performance to deviate from the performance of the relevant cryptocurrency, cryptocurrency futures, or the Index.

14

Cost of Futures Investment Risk – When a cryptocurrency futures contract is nearing expiration, the Fund will typically “roll” the futures contract, which means it will generally sell such a contract and use the proceeds to buy a cryptocurrency futures contract with a later expiration date. The price difference between the expiring contract and longer-dated contract associated with rolling cryptocurrency futures may be substantially higher than the price difference associated with rolling other futures contracts. Additionally, the returns of cryptocurrency futures may differ from those of the relevant cryptocurrency. These differences in returns can arise due to several factors, including the costs associated with futures investments, such as “rolling,” supply and demand dynamics, interest rates, and market expectations.

Cryptocurrency ETP Investing Risk. Issuer-specific attributes related to ETPs in which the Fund may invest may cause an investment held by the Fund to be more volatile than the market generally. The value of an individual security or asset, or a particular type of security or asset, may be more volatile than the market as a whole and perform differently from the value of the market as a whole. When the Fund invests in ETPs, it will incur costs related to such funds, including management fees and expenses borne by shareholders of such ETPs. The value of shares in an ETP may not replicate the performance of the relevant cryptocurrency, and, therefore, the Fund’s investments in the ETPs will not perform the same as the Fund’s direct investments in the relevant cryptocurrency.

Leverage Risk. Leverage risk is created when an investment, which includes, for example, an investment in a derivative contract, exposes the Fund to a level of risk that exceeds the amount invested. Changes in the value of such an investment magnify the Fund’s risk of loss and potential for gain. Investments can have these same results if their returns are based on a multiple of a specified index, security, or other benchmark.

Investment in the Subsidiary Risk – The Fund is exposed to the risks of the Subsidiary’s investments, which are exposed to the risks of investing in Ether and Ether futures contracts. The Fund will also incur the expenses of the Subsidiary. Although the Subsidiary is not registered under the 1940 Act, it will provide investors with the same protections the Fund provides.

Tracking Error Risk – Various factors may impede the Fund's ability to track the Index or achieve a high degree of correlation with the Index. Factors contributing to tracking error include:

| ● | Fees and Expenses: The Fund has operating and other expenses, while the Index does not. The Fund's expense ratio reduces net asset value, while the Index reflects gross performance without deductions for fees or expenses. |

| ● | Transaction Costs: Buying and selling cryptocurrencies and Cryptocurrency-Related Products involve bid-ask spreads, market impact costs, trading fees, and blockchain network transaction fees that reduce the Fund's returns but are not reflected in Index performance. |

| ● | Cash Drag: The Fund may not be fully invested at times, generally due to cash flows into or out of the Fund, rebalancing activities, or excess cash held for various reasons. Cash positions create performance drag when cryptocurrency prices appreciate and may provide relative benefit when prices depreciate. |

| ● | Rebalancing and Reallocation Timing: The Fund cannot instantaneously adjust holdings when rebalancing or reallocation events occur. Settlement of cryptocurrency transactions requires blockchain confirmations, custody transfers, and operational processes that create timing lags. During these lags, the Fund's composition may differ from the target portfolio. |

Investment in Investment Companies Risk—Investing in other investment companies, including money market funds, ETFs, and ETPs, subjects the Fund to the fees and expenses of, as well as risks affecting, the investment company, including the possibility that the value of the underlying securities held by the investment company could decrease.

Trading Halt Risk—An exchange or market may issue trading halts on specific securities, contracts, or instruments or may close early or late, which will affect the Fund's ability to buy or sell certain securities. In such circumstances, the Fund may be unable to rebalance its portfolio, may be unable to accurately price its investments, or may incur substantial trading losses.

15

ETF Risks

Absence of an Active Market: Although the Fund’s shares are approved for listing on the NASDAQ (the “Exchange”), there can be no assurance that an active trading market will develop and be maintained for Fund shares. There can also be no assurance that the Fund will grow to or maintain an economically viable size; in this case, it may experience greater tracking error to its Index than it otherwise would at higher asset levels or may ultimately liquidate.

Authorized Participants (“APs”), Market Makers, and Liquidity Providers Concentration: The Fund has a limited number of financial institutions that may act as APs. In addition, there may be a limited number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events occur, Shares may trade at a material discount to net asset value (“NAV”) and possibly face delisting: (i) APs exit the business or otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business activities and no other entities step forward to perform their functions.

Cash Transaction Risk. The Fund intends to affect some portion of redemptions for cash, rather than in-kind, because of the nature of the Fund’s investments. The Fund may be required to sell portfolio securities to obtain the cash needed to distribute redemption proceeds, which involves transaction costs that the Fund may not have incurred had it effected redemptions entirely in kind. These costs may include brokerage costs and/or taxable gains or losses, which may be imposed on the Fund and decrease the Fund’s NAV. If the Fund recognizes gain on these sales, this generally will cause the Fund to recognize gain it might not otherwise have recognized if it were to distribute all of its portfolio securities in-kind, or to recognize such gain sooner than would otherwise be required. This may decrease the Fund's tax efficiency compared to ETFs that utilize a complete in-kind redemption process.

Trading Issues: Trading in Fund shares may be halted due to market conditions or for reasons that make trading in shares inadvisable in the view of the Exchange. There can be no assurance that the requirements of the Exchange necessary to maintain the listing of any Fund will continue to be met or will remain unchanged, or that the shares will trade with any volume. Further, secondary markets may be subject to erratic trading activity, wide bid/ask spreads, and extended trade settlement periods in times of market stress because market makers and APs may step away from making a market in Fund shares and in executing creation and redemption orders, which could cause a material deviation in the Fund’s market price from its NAV.

New Fund Risk. The Fund was recently organized with limited operating history. As a result, prospective investors have a limited track record or history on which to base their investment decisions. There can be no assurance that the Fund will grow to or maintain an economically viable size.

Passive Investment Risk. The Fund is not actively managed and therefore would not sell an equity security, futures contract, or other investment due to current or projected underperformance of a security, industry, sector, or asset class. Unlike an actively managed fund, the Adviser does not use techniques or defensive strategies designed to lessen the effects of market volatility or reduce the impact of periods of market decline. This means that, based on market and economic conditions, the Fund’s performance could be lower than other types of funds that may actively shift their portfolio assets to take advantage of market opportunities or to lessen the impact of a market decline.

All

investments carry some risk that will affect the value of the Fund, its investment performance, and the price of its shares.

16

FUND MANAGEMENT INVESTMENT ADVISER

CYBER HORNET ETFs, LLC serves as the investment adviser to the Fund.

PORTFOLIO MANAGER

Michael G. Willis, portfolio manager of the Adviser, has managed the Fund since its inception.

PURCHASE AND SALE OF FUND SHARES

Individual shares may only be purchased and sold through a broker-dealer on a national securities exchange. You can buy and sell individual shares of the Fund any day the Nasdaq Stock Market (“NASDAQ”) is open for business, like any publicly traded security. The Fund’s shares are listed on the Nasdaq Stock Market exchange. The price of the Fund’s shares is based on market price, and because exchange-traded fund shares trade at market prices rather than NAV, shares may trade at a price greater than NAV (premium) or less than NAV (discount). The Fund issues and redeems shares continuously, at NAV, only in blocks of 25,000 shares (“Creation Units”), which may be partially in-kind for securities included in the Index and partially in cash, and only Authorized Participants (typically, broker-dealers) may purchase or redeem Creation Units. Except when aggregated in Creation Units, the Fund’s shares are not redeemable securities.

TAX INFORMATION

For U.S. federal income tax purposes, the Fund’s distributions are taxable. They will be taxed as ordinary income or capital gains, unless you invest through a tax-advantaged arrangement, such as a 401(k) plan or an individual retirement account. Such tax-advantaged arrangements are subject to special tax rules upon withdrawal of monies from those arrangements.

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

If you purchase the Fund through a broker-dealer or other financial intermediary (such as a bank), the Adviser or its affiliates may pay the intermediary to sell Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

17

CYBER HORNET S&P 500® AND SOLANA 75/25 STRATEGY ETF SUMMARY

The CYBER HORNET S&P 500® and Solana 75/25 Strategy ETF (the “Fund”) seeks to replicate, before fees and expenses, the total return of the S&P 500® and S&P Solana Reference Price 75/25 Blend Index (the “Index”), an index by Standard & Poor’s.

The following table describes the expenses and fees that you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Shareholder Fees | |

| (fees paid directly from your investment) | None |

| Annual Fund Operating Expenses | |

| (expenses that you pay each year as a percentage of the value of your investment) |

| Management Fees1 | |

| Distribution (12b-1) Fees | |

| Other Expenses | |

| Total Annual Fund Operating Expenses |

| 1 |

This Example is intended to help you compare the costs of investing in the Fund with the costs of investing in other funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. Expenses assuming no redemption are also shown. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses (excluding any sales loads on reinvested dividends, fee waivers, and/or expense reimbursements) shown in the table above remain the same. The expenses used to calculate the Fund’s Example do not include fee waivers or expense reimbursements. Although your actual costs and returns may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years |

| $ |

$ |

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or the example, affect the Fund’s performance. Because the Fund is newly organized, portfolio turnover information is unavailable.

18

The Fund seeks to replicate, before fees and expenses, the total return of the S&P 500® and S&P Solana Reference Price 75/25 Blend Index (the “Index”). The Index measures the weighted return performance of a multi-asset strategy comprising a 75% weight in the S&P 500® Index and a 25% weight in the S&P Solana Reference Price Index. Accordingly, in seeking to track the Index, the Fund will invest approximately 75% of its assets in a portfolio of common stocks that are included in the S&P 500® Index and will invest directly in Solana (SOL) so that the total value of the Solana (SOL) to which the Fund has economic exposure is approximately 25% of the assets of the Fund. S&P Dow Jones Indices LLC (“S&P DJI” or the “Index Provider”) compiles, maintains, and calculates the Index and each of the S&P 500® Index and the S&P Solana Reference Price Index. The Index is rebalanced monthly, and accordingly, the Fund seeks to maintain the 75%/25% allocations by also rebalancing these allocations monthly. However, price fluctuations in the underlying assets and other factors, such as the Fund’s cash position, may cause these allocations to vary at any time. The Adviser reserves the right to rebalance the Fund’s allocations more frequently than monthly in periods of significant price volatility or less frequently than monthly to save on trading costs or during periods of low volatility. The Adviser may rebalance the Fund’s allocations on any day of the month. Such rebalancing decisions are made solely to reduce tracking error and enhance after-fee performance relative to the Index.

U.S. Large-Cap

The Fund attempts to replicate this portion of its portfolio by investing in a portfolio of the common stocks included in the S&P 500 Index, holding each stock in a similar proportion as its weighting in the S&P 500 Index. The Fund may hold more or fewer stocks than the index at any given time. The Fund may sell investments represented in the S&P 500 Index in anticipation of their removal from the S&P 500 Index or buy investments not yet represented in the index in anticipation of their addition to it. The Fund may also invest in securities of other investment companies, such as certain ETFs, to implement its investment strategy.

Solana

Under normal conditions, the Fund will invest in Solana (SOL) so that the total value of the Solana (SOL) to which the Fund has economic exposure is approximately 25% of the Fund’s assets. The Fund will invest directly in Solana (SOL) and Solana futures contracts through a wholly-owned subsidiary company, Cyber Hornet SSS, organized under the laws of the Cayman Islands (the “Subsidiary”). The Fund may also gain exposure to Solana by investing in Solana futures contracts, and in shares of other exchange-traded funds (“ETFs”) and exchange-traded products (“ETPs”) which provide exposure to Solana (SOL) (collectively “Solana ETPs” and together with the Solana futures contracts, “Cryptocurrency-Related Products”), although the Fund expects that its futures and ETP exposure will generally be less than 10% of its assets. Such exposure seeks to track, before fees and expenses, the performance of the S&P Solana Reference Price Index. The S&P Solana Reference Price Index tracks the performance of the digital asset Solana. However, changes in the relative value of the Fund’s assets between the monthly rebalance could cause the Fund’s investment in Solana (SOL), Solana futures, and Solana ETPs to represent greater than 25% of the Fund’s assets.

The Fund will generally purchase and sell Solana (SOL) on exchanges such as BitGo and Coinbase, neither of which is registered as a national securities exchange with the SEC. The price of Solana (SOL) on these exchanges and over-the-counter markets has a limited history, is volatile, and is subject to the influence of many factors, including operational interruptions.

Solana held directly by the Fund are maintained at a qualified custodian. The custodian uses "cold storage" security measures for storing the private keys necessary to access the Fund's Solana offline in a manner that is not connected to the internet. This is designed to protect cryptocurrencies from hacking or other cybersecurity threats.

When the Fund invests in Solana futures contracts, the Fund must sell its futures contracts as they near expiration and replace them with new futures contracts with a later expiration date. The Adviser anticipates that this “roll” of the futures contracts will normally occur shortly before the expiration of the current month contract in the last week of the month. However, such timing may change due to market conditions. Futures contracts with a longer term to expiration may be priced higher than futures contracts with a shorter term to expiration (e.g. trading at “contango”). Solana futures have historically experienced extended periods of contango. Contango in the Solana futures market may have a significant adverse impact on the performance of the Fund and may cause it to significantly deviate from the performance of the Index. The Fund will only invest in Solana futures contracts that are traded on a futures exchange regulated by the Commodity Futures Trading Commission (“CFTC”). The Fund (or the Subsidiary, as applicable) also invests in short-term U.S. government securities intended to serve as margin or collateral for futures positions.

19

The Fund may invest in Solana ETPs that invest directly in, provide exposure to, replicate the performance of, or have trading and/or price performance characteristics similar to Solana (SOL).

PRINCIPAL RISKS

The following describes the principal risks of investing in the Fund, which could affect the Fund’s net asset value and total return. Other circumstances (including additional risks not described here) could prevent the Fund from achieving its investment objective. These risks are presented in an order that reflects the Adviser’s assessment of relative importance, but this assessment could change over time as the Fund’s portfolio changes or in light of changes in the market or the economic environment, among other things. The Fund is not required to and will not update this Prospectus solely because the Adviser’s assessment of the relative importance of the principal risks of investing in the Fund changes.

Solana (SOL), Solana futures contracts, and Solana ETPs are relatively new investments. They are subject to unique and substantial risks and have historically been subject to significant price volatility. The value of an investment in the Fund could decline significantly and without warning. You should be prepared to lose the entirety of the Solana component of your investment in the Fund. The performance of Solana futures contracts and Solana ETPs, and therefore the performance of the Fund, may differ significantly from that of Solana (SOL).

Equity Risk – The values of equity securities may decline due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment generally. The prices of equity securities fluctuate, and sometimes widely fluctuate, in response to activities specific to the issuer of the security. Equity securities generally have greater price volatility than fixed-income securities.

Solana (SOL) Risk. The Fund is subject to the risks of investing in Solana (SOL) directly and indirectly through its investments in the ETPs that obtain exposure to Solana (SOL) and other assets that provide exposure to Solana (SOL). The market price for Solana (SOL) is extremely volatile and will likely continue to be volatile. Solana (SOL) is the native token for the Solana Network and is used for transaction fees and governance on the Solana Network. Accordingly, Solana (SOL)'s value largely depends on the acceptability and usage levels of the Solana Network and its applications by users. Factors contributing to the volatility of the price of Solana (SOL) include, but are not limited to, the maintenance and development of the open-source software protocol of the Solana Network, forks in the Solana Network, speculation and consumer preferences and perceptions of Solana (SOL) specifically and digital assets generally, investment and trading activities of large investors that invest directly or indirectly in Solana (SOL), and the fees associated with processing a transaction on the Solana Network, the speed at which transactions are processed and settled on the Solana Network. The price of Solana (SOL) is also affected by interruptions in service from closures or failures of major digital asset trading platforms, cloud services, and network latency.

Rebalancing Costs and Tax Risk. The Fund is subject to the risk of rebalancing to track the Index that may result in significant transaction costs and tax consequences for shareholders. The Fund seeks to maintain a 75% allocation to the S&P 500 Index and a 25% allocation to the S&P Cryptocurrency Top 10 Index. The Fund rebalances these allocations monthly and may rebalance more frequently during periods of significant market volatility. When cryptocurrency prices rise or fall relative to equity prices between rebalancing dates, the Fund must sell appreciated assets and purchase depreciated assets to restore the target allocation of 75% to 25% in equity and cryptocurrency, respectively. These transactions generate transaction costs and may result in the realization of capital gains that will be distributed to shareholders.

Risks Related to the Regulation of Cryptocurrency. Any final determination by a court that a cryptocurrency is a “security” or “commodity” may adversely affect the value of the cryptocurrency and the value of the Fund’s shares, and, if the cryptocurrency is not, or cannot, be registered as a security, result in a potential termination of the Fund.

20

Depending on its characteristics, a cryptocurrency may be considered a “security” under the federal securities laws. The test for determining whether a particular cryptocurrency is a “security” is complex and difficult to apply, and the outcome is difficult to predict. If an appropriate court determines that the relevant cryptocurrency is a security, the Adviser would not intend to permit the Fund to continue holding its investments in a way that would violate the federal securities laws (and therefore, if necessary, would either dissolve the Fund or potentially seek to operate the Fund in a manner that complies with the federal securities laws).

Cryptocurrency Market Volatility Risk. The prices of cryptocurrencies have historically been highly volatile. The value of the Fund’s exposure to a cryptocurrency – and therefore the value of an investment in the Fund – could decline significantly and without warning, including to zero. If you are not prepared to accept significant and unexpected changes in the value of the Fund and the possibility that you could lose your entire investment in the cryptocurrency component of the Fund, you should not invest in it.

Cryptocurrency Futures Contracts Risk – The market for cryptocurrency futures contracts may be less developed, and potentially less liquid and more volatile, than more established futures markets. While the cryptocurrency futures contracts market has grown substantially since cryptocurrency futures contracts commenced trading, there can be no assurance that this growth will continue. The price for cryptocurrency futures contracts is based on many factors, including the supply of and the demand for cryptocurrency futures contracts. Market conditions and expectations, position limits, collateral requirements, and other factors can each impact the supply of and demand for cryptocurrency futures contracts. At times, increased demand paired with supply constraints and other factors have caused cryptocurrency futures contracts to trade at a significant discount or premium to the “spot” price of the relevant cryptocurrency. Additional demand, including demand resulting from the purchase, or anticipated purchase, of cryptocurrency futures contracts by the Fund or other entities, may increase that premium, perhaps significantly. It is impossible to predict whether or how long such conditions will continue. To the extent the Fund purchases futures contracts at a premium and the premium declines, the value of an investment in the Fund also should be expected to decline.

Market conditions and expectations, position limits, collateral requirements, and other factors may also limit the Fund’s ability to achieve its desired exposure to cryptocurrency futures contracts. If the Fund cannot achieve such exposure, it may not meet its investment objective, and its returns may be different from those of the index or lower than expected. Additionally, collateral requirements may require the Fund to liquidate its position, potentially incurring losses and expenses, when it otherwise would not do so. Investing in derivatives like cryptocurrency futures contracts may be considered aggressive and expose the Fund to significant risks. These risks include counterparty risk and liquidity risk. The performance of cryptocurrency futures contracts and the relevant cryptocurrency may differ and may not be correlated with each other, over short or long periods, and may cause cryptocurrency futures to underperform the spot price of the relevant cryptocurrency.