Form 424B5 Essential Properties, Filed by: ESSENTIAL PROPERTIES REALTY TRUST, INC.

Tweet

Tweet Share

ShareTable of Contents

Filed Pursuant to Rule 424(b)(5)

Registration Nos. 333-257202 and 333-257202-01

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title Of Each Class of Securities To Be Registered |

Amount To Be |

Maximum Offering Price Per Unit |

Maximum Offering Price |

Amount of Registration Fee(1) | ||||

| Essential Properties, L.P. 2.950% Senior Notes due 2031 |

$400,000,000 | 99.800% | $399,200,000.00 | $43,552.72 | ||||

| Essential Properties Realty Trust, Inc. Guarantee of 2.950% Senior Notes due 2031 |

(2) | (2) | (2) | (2) | ||||

|

| ||||||||

| (1) | The filing fee is calculated in accordance with Rules 457(o) and 457(r) of the Securities Act of 1933, as amended (the “Act”). In accordance with Rules 456(b) and 457(r) of the Act, the registrants initially deferred payment of all of the registration fees for Registration Statement Nos. 333-257202 and 333-257202-01 filed by the registrants on June 21, 2021. |

| (2) | No separate consideration will be received for the guarantees. Pursuant to Rule 457(n) under the Act, no separate fee is payable with respect to the guarantees being registered hereby. |

Table of Contents

PROSPECTUS SUPPLEMENT

(To Prospectus Dated June 21, 2021)

$400,000,000

Essential Properties, L.P.

2.950% Senior Notes due 2031

guaranteed by

Essential Properties Realty Trust, Inc.

Essential Properties, L.P., a Delaware limited partnership, is offering $400,000,000 aggregate principal amount of 2.950% Senior Notes due 2031 (the “ notes”). The notes will bear interest at the rate of 2.950% per year and will mature on July 15, 2031. Interest on the notes is payable on January 15 and July 15 of each year, commencing on January 15, 2022.

Essential Properties, L.P. may redeem some or all of the notes at any time at the prices and as described under the caption “Description of Notes—Optional Redemption.” If any notes are redeemed on or after April 15, 2031 (three months prior to the maturity date of the notes), the redemption price will equal 100% of the principal amount of the notes to be redeemed plus accrued and unpaid interest, if any, up to, but not including, the redemption date, without any make-whole premium.

The notes will be Essential Properties, L.P.’s senior unsecured obligations, will rank equally in right of payment with all of its other existing and future senior unsecured indebtedness and will be effectively subordinated in right of payment to all of its existing and future mortgage indebtedness and other secured indebtedness (to the extent of the value of the collateral securing such indebtedness), to all existing and future indebtedness and other liabilities, whether secured or unsecured, of its subsidiaries and of any entity it accounts for using the equity method of accounting and to all preferred equity not owned by it, if any, in any of its subsidiaries and in any entity it accounts for using the equity method of accounting.

The notes will be fully and unconditionally guaranteed by Essential Properties Realty Trust, Inc., a Maryland corporation. Essential Properties Realty Trust, Inc. does not have any significant operations or material assets other than its direct and indirect investments in Essential Properties, L.P.

The notes are a new issue of securities with no established trading market. We do not intend to apply for listing of the notes on any securities exchange or for quotation of the notes on any automated dealer quotation system.

Investing in the notes involves risks. You should read carefully and consider the “Risk Factors” beginning on page S-6 of this prospectus supplement and the risk factors described in our Annual Report on Form 10-K for the year ended December 31, 2020, which is incorporated by reference herein, for factors you should consider before investing in the notes.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Note | Total | |||||||

| Public offering price(1) |

99.800 | % | $ | 399,200,000 | ||||

| Underwriting discount(2) |

0.650 | % | $ | 2,600,000 | ||||

| Proceeds, before expenses, to Essential Properties, L.P. |

99.150 | % | $ | 396,600,000 | ||||

| (1) | Plus accrued interest from June 28, 2021, if settlement occurs after that date. |

| (2) | We refer you to “Underwriting” beginning on page S-38 of this prospectus supplement for additional information regarding underwriting compensation. |

The notes will be ready for delivery in book-entry form only through the facilities of The Depository Trust Company for the accounts of its participants, including Euroclear Bank S.A./N.V., as operator of the Euroclear System, and Clearstream Banking, société anonyme, against payment in New York, New York on or about June 28, 2021.

Joint Book-Running Managers

| BofA Securities | Citigroup | Barclays | Goldman Sachs & Co. LLC | |||

Co-Managers

| Capital One Securities | Mizuho Securities | Stifel | Truist Securities | |||

The date of this prospectus supplement is June 22, 2021.

Table of Contents

| Page | ||||

| Prospectus Supplement |

| |||

| S-ii | ||||

| S-1 | ||||

| S-3 | ||||

| S-6 | ||||

| S-14 | ||||

| S-16 | ||||

| S-17 | ||||

| S-36 | ||||

| S-38 | ||||

| S-43 | ||||

| S-44 | ||||

| S-45 | ||||

Prospectus

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 6 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 12 | ||||

| 14 | ||||

| 23 | ||||

| 24 | ||||

| 27 | ||||

| CERTAIN PROVISIONS OF MARYLAND LAW AND OF OUR CHARTER AND BYLAWS |

31 | |||

| 37 | ||||

| 62 | ||||

| 63 | ||||

| 63 |

Neither we nor the underwriters have authorized any person to give any information or to make any representations in connection with this prospectus supplement and the accompanying prospectus other than those contained or incorporated by reference in this prospectus supplement, the accompanying prospectus and in any applicable free writing prospectus, and, if given or made, such information or representations must not be relied upon as having been so authorized. Neither we nor the underwriters are making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus supplement, the accompanying prospectus, any free writing prospectus prepared by us and in the documents incorporated by reference into this prospectus supplement and the accompanying prospectus is accurate only as of the respective dates of such documents or on the date or dates which are specified therein. Our business, financial condition, liquidity, results of operations and prospects may have changed since those dates.

Essential Properties Realty Trust, Inc. and the Essential Properties Realty Trust REIT are not affiliated with or sponsored by Griffin Capital Essential Asset Operating Partnership, L.P. or the Griffin Capital Essential Asset REIT.

S-i

Table of Contents

ABOUT THIS PROSPECTUS SUPPLEMENT AND THE PROSPECTUS

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering and also adds to and updates information contained in the accompanying prospectus and the documents incorporated by reference. The second part, the accompanying prospectus, gives more general information, some of which does not apply to this offering.

To the extent there is a conflict between the information contained in this prospectus supplement, on the one hand, and the information contained in the accompanying prospectus or documents incorporated by reference prior to the date hereof, on the other hand, you should rely on the information in this prospectus supplement. In addition, information incorporated by reference after the date of this prospectus supplement may add, update or change information contained in this prospectus supplement or the accompanying prospectus. Any information in such subsequent filings that is inconsistent with this prospectus supplement or the accompanying prospectus will supersede the information in this prospectus supplement or the accompanying prospectus.

This prospectus supplement does not contain all of the information that is important to you. You should read this prospectus supplement together with the accompanying prospectus, all free writing prospectuses, if any, that we have authorized for use in connection with this offering and all documents incorporated by reference. References to information incorporated by reference in this prospectus supplement or the accompanying prospectus include information deemed to be incorporated by reference herein or therein. The documents incorporated by reference into this prospectus supplement are identified under the caption “Information Incorporated by Reference” in this prospectus supplement.

Unless the context otherwise requires, “we,” “our,” “us” and “our company” mean Essential Properties Realty Trust, Inc., a Maryland corporation, together with its consolidated subsidiaries, including our operating partnership, and “operating partnership” means Essential Properties, L.P., a Delaware limited partnership, through which we hold substantially all of our assets and conduct our operations. “CPI” means the consumer price index for all urban consumers (CPI-U): U.S. city average, all items, which is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

S-ii

Table of Contents

The following summary highlights information contained elsewhere or incorporated by reference in this prospectus supplement and the accompanying prospectus. This summary is not complete and does not contain all of the information that you should consider before investing in the notes. Before making an investment decision, you should carefully read this entire prospectus supplement, the accompanying prospectus and the documents incorporated by reference, including the information under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2020. You should also read the audited financial statements and related notes included in our Annual Report on Form 10-K for the year ended December 31, 2020 and our unaudited interim financial statements and related notes included in our Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2021. Such annual report and quarterly report are incorporated by reference in this prospectus supplement and the accompanying prospectus. See “Information Incorporated by Reference.”

Our Company

We are an internally managed real estate company that acquires, owns and manages primarily single-tenant properties that are net leased on a long-term basis to middle-market companies operating service-oriented or experience-based businesses. We generally invest in and lease freestanding, single-tenant commercial real estate facilities where a tenant services its customers and conducts activities that are essential to the generation of the tenant’s sales and profits. As of March 31, 2021, 95.3% of our $193.5 million of annualized base rent was attributable to properties operated by tenants in service-oriented and experience-based businesses. “Annualized base rent” or “ABR” means annualized contractually specified cash base rent in effect on March 31, 2021 or such other date as specified herein for all of our leases (including those accounted for as loans or direct financing leases) commenced as of that date and annualized cash interest on our mortgage loans receivable as of that date.

Substantially all of our assets are held by, and substantially all of our operations are conducted through, our operating partnership, either directly or through subsidiaries. Essential Properties OP G.P., LLC, one of our wholly-owned subsidiaries, is the sole general partner of our operating partnership. As of March 31, 2021, we held a 99.5% limited partnership interest in our operating partnership.

Recent Developments

April 2021 Equity Offering

In April 2021, we completed a follow-on offering of 8,222,500 shares of our common stock, including 1,072,500 shares of common stock purchased by the underwriters pursuant to an option to purchase additional shares, at a public offering price of $23.50 per share, raising gross proceeds of $193.2 million.

ATM Activity

In June 2020, we established our $250.0 million “at-the-market” equity distribution program (our “ATM Program”). From April 1, 2021 through June 18, 2021, we sold 102,608 shares of our common stock under our ATM Program, at a weighted average price per share of $23.45, raising gross proceeds of $2.4 million.

Recent ABR Collection Experience

We collected approximately 98% and 99% of our ABR for the months of April 2021 and May 2021, respectively. For the month of April 2021, we had recognized deferrals of approximately 1% of our ABR and for May 2021 we had recognized deferrals of less than 1% of our ABR. For purposes of this paragraph, ABR means annualized base rent in effect on April 1, 2021.

S-1

Table of Contents

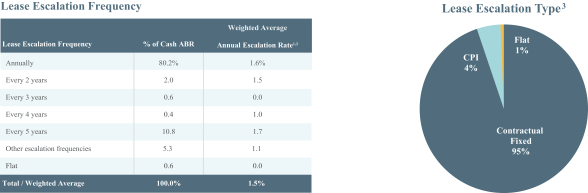

Lease Escalations

As of March 31, 2021, 99.4% of our leases (based on annualized base rent) provided for increases in future base rent at a weighted average rate of 1.5% per year and such increases generally range from 1.0% to 4.0% per year, in each case when assuming no growth in the CPI.

The charts below depict information about our lease escalation frequency and lease escalation type as of March 31, 2021:

| (1) | Based on annualized base rent as of March 31, 2021. |

| (2) | Represents the weighted average annual escalation rate of our entire portfolio as if all escalations occur annually. For leases in which rent escalates by the greater of a stated fixed percentage or the CPI, we have assumed an escalation equal to the stated fixed percentage in the lease. As any future increase in the CPI is uncertain, we have not included an increase in the rent pursuant to these leases in the calculation of the weighted average annual escalation rate. |

| (3) | Approximately 95% of our leases had contractually fixed rent escalation provisions, approximately 4% of our leases had rent escalation provisions linked to the CPI and approximately 1% of our leases had no rent (or flat) escalation provisions, in each case based on annualized base rent as of March 31, 2021. |

Our Tax Status

We elected to qualify to be taxed as a real estate investment trust (“REIT”) for federal income tax purposes commencing with our taxable year ended December 31, 2018. We believe that our organization and operations allowed us to qualify as a REIT for federal income tax purposes commencing with such taxable year, and we intend to continue operating in such a manner. To maintain REIT status, we must meet a number of organizational and operational requirements, including a requirement that we annually distribute to our stockholders at least 90% of our REIT taxable income, determined without regard to the dividends paid deduction and excluding any net capital gains. See “Federal Income Tax Considerations” in the accompanying prospectus.

Corporate Information

Our principal executive offices are located at 902 Carnegie Center Boulevard, Suite 520, Princeton, New Jersey 08540. Our main telephone number is (609) 436-0619. Our website is http://www.essentialproperties.com. The content of our website and any information that is linked to or accessible from our website (other than our filings with the SEC that are incorporated by reference, as set forth under “Information Incorporated By Reference”) is not incorporated by reference into this prospectus supplement, and you should not consider it a part of this prospectus supplement, the accompanying prospectus or the registration statement of which they are a part.

S-2

Table of Contents

The summary below describes the principal terms of the notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The section entitled “Description of Notes” of this prospectus supplement contains a more detailed description of the terms and conditions of the notes and the indenture governing the notes. For purposes of this section entitled “The Offering” and the section entitled “Description of Notes,” references to “we,” “us” and “our” refer only to Essential Properties, L.P. and not to its subsidiaries, and references to the “Guarantor” refer only to Essential Properties Realty Trust, Inc.

| Issuer of Notes |

Essential Properties, L.P. |

| Guarantor |

Essential Properties Realty Trust, Inc. |

| Securities Offered |

$400,000,000 aggregate principal amount of 2.950% Senior Notes due 2031 |

| Maturity Date |

July 15, 2031 |

| Interest Rate |

2.950% per year |

| Interest Payment Dates |

Interest on the notes will be payable semi-annually in arrears on January 15 and July 15 of each year, commencing on January 15, 2022. |

| Ranking of Notes |

The notes will be our senior unsecured obligations and will rank equally in right of payment with all of our other existing and future senior unsecured indebtedness. The notes will be effectively subordinated in right of payment to: |

| • | all of our existing and future mortgage indebtedness and other secured indebtedness (to the extent of the value of the collateral securing such indebtedness); |

| • | all existing and future indebtedness and other liabilities, whether secured or unsecured, of our subsidiaries and of any entity we account for using the equity method of accounting; and |

| • | all preferred equity not owned by us, if any, in any of our subsidiaries and in any entity we account for using the equity method of accounting. |

| Guarantee |

The notes will be fully and unconditionally guaranteed by the Guarantor. The guarantee of the notes will be a senior unsecured obligation of the Guarantor and will rank equally in right of payment with all other existing and future senior unsecured indebtedness and guarantees of the Guarantor. The Guarantor’s guarantee of the notes will be effectively subordinated in right of payment to: |

| • | all of the Guarantor’s existing and future secured indebtedness and secured guarantees (to the extent of the value of the collateral securing such indebtedness or guarantees); |

S-3

Table of Contents

| • | all existing and future indebtedness and other liabilities, whether secured or unsecured, of the Guarantor’s consolidated subsidiaries (including us) and of any entity the Guarantor accounts for using the equity method of accounting; and |

| • | all preferred equity not owned by the Guarantor, if any, in any of the Guarantor’s consolidated subsidiaries (including us) and in any entity the Guarantor accounts for using the equity method of accounting. |

| The Guarantor generally does not have any significant operations or material assets other than its direct and indirect investments in us. |

| Optional Redemption |

The notes will be redeemable in whole at any time or in part from time to time, at our option, at a redemption price calculated by us and equal to the sum of (1) 100% of the principal amount of the notes to be redeemed plus accrued and unpaid interest, if any, up to, but not including, the redemption date plus (2) a make-whole premium. |

| Notwithstanding the foregoing, if any notes are redeemed on or after April 15, 2031 (three months prior to the maturity date of the notes), the redemption price will equal 100% of the principal amount of the notes to be redeemed plus accrued and unpaid interest, if any, up to, but not including, the redemption date, without any make-whole premium. |

| Use of Proceeds |

We estimate that the net proceeds from this offering will be approximately $395.9 million, after deducting the underwriting discount and other estimated expenses. |

| We intend to use the net proceeds from this offering (i) to prepay all of the secured debt principal outstanding under our master trust funding program (plus a make whole amount); (ii) to repay amounts outstanding under our revolving credit facility; and (iii) for general corporate purposes, including funding future investment activity. See “Use of Proceeds.” |

| Affiliates of certain of the underwriters are lenders and, in certain cases, agents under our revolving credit facility and will receive pro rata portions of the net proceeds from this offering used to repay the balance outstanding thereunder. |

| Certain Covenants |

The indenture governing the notes will contain certain covenants that, among other things, limit: |

| • | our ability and the ability of the Guarantor to consummate a merger, consolidation or sale of all or substantially all of our assets; and |

| • | the ability of the Guarantor and its subsidiaries, including us, to incur secured and unsecured indebtedness. |

S-4

Table of Contents

| No Limitation on Incurrence of New Debt |

Subject to compliance with covenants relating to our aggregate debt, debt service, maintenance of total unencumbered assets and secured aggregate debt, the indenture will not limit the amount of debt we may issue under the indenture or otherwise. |

| Further Issuances |

We may in the future, without the consent of noteholders, issue additional notes on the same terms and conditions as the notes being offered hereby, except for any difference in the issue date, public offering price, interest accrued prior to the issue date of the additional notes, and, if applicable, the initial interest payment date. The notes and any additional notes of such series subsequently issued under the indenture would be treated as a single series for all purposes under the indenture, including, without limitation, waivers, amendments, redemptions and offers to purchase; provided, however, that if such additional notes will not be fungible with the previously issued notes for U.S. federal income tax purposes, such additional notes will have a separate CUSIP number. |

| No Public Market |

The notes offered hereby are a new issue of securities with no established trading market. |

| We do not intend to apply for listing of the notes on any securities exchange or for quotation of the notes on any automated dealer quotation system. Certain of the underwriters have advised us that they intend to make a market in the notes, but they are not obligated to do so and may discontinue any market-making at any time without notice. |

| Book-Entry Form |

The notes will be issued in book-entry only form and will be represented by one or more permanent global certificates deposited with a custodian for, and registered in the name of a nominee of, The Depository Trust Company (“DTC”), in New York, New York. Beneficial interests in the global certificates representing the notes will be shown on, and transfers will be effected only through, records maintained by DTC and its direct and indirect participants and such interests may not be exchanged for certificated notes, except in limited circumstances. |

| Governing Law |

The indenture, the notes and the guarantee will be governed by, and construed in accordance with, the laws of the State of New York. |

| Risk Factors |

Investing in the notes involves risks. You should carefully read and consider the information set forth under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2020, as well as the other information included and incorporated by reference in this prospectus supplement and the accompanying prospectus before investing in the notes. |

| Trustee |

U.S. Bank National Association |

S-5

Table of Contents

Investing in the notes involves risks. Before making an investment decision, you should carefully read this entire prospectus supplement, the accompanying prospectus and the documents incorporated by reference, including the information under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2020. The occurrence of any of these risks could materially and adversely affect our business, financial condition, liquidity, results of operations, adjusted funds from operations and prospects and might cause you to lose all or a part of your investment in the notes. Please also refer to the section entitled “Special Note Regarding Forward-Looking Statements” included elsewhere in this prospectus supplement.

Risks Related to this Offering and the Notes

Our indebtedness may expose us to the risk of default under our debt obligations and limit our ability to obtain additional financing and fulfill our obligations under the notes.

As of May 31, 2021, the outstanding principal amount of our consolidated indebtedness was approximately $848.5 million, all of which was incurred by our operating partnership or its subsidiaries. As of May 31, 2021, this debt is comprised of $171.5 million of secured debt principal outstanding under our master trust funding program (all of which will be prepaid with a portion of the net proceeds from this offering), $630.0 million of principal outstanding on our unsecured term loans and $47.0 million outstanding under our revolving credit facility (which will also be repaid with a portion of the net proceeds from this offering). As of May 31, 2021, we had approximately $353.0 million of borrowing capacity available (subject to customary conditions) under our revolving credit facility and $20.5 million of cash and cash equivalents. Any borrowings under our revolving credit facility that are repaid with any net proceeds from this offering may be reborrowed, subject to customary conditions.

The requirements imposed by our debt agreements with regard to servicing the debt through payments of principal and/or interest, as well as, the limitations associated with the applicable restrictive covenants, subject us to the potential for defaulting on those debt agreements through the failure to satisfy the debt service requirements or non-compliance with the covenants. An occurrence of default could cause the debt to become due and payable. Provisions of our other debt agreements may contain cross default provisions whereby the default on one of our debt agreements could cause other debt agreements to be in default, leading those debt agreements to also be due and payable.

Our default on our debt agreements could have significant adverse consequences to holders of the notes, including the following:

| • | our cash flow may be insufficient to meet our required principal and interest payments with respect to the notes and our other indebtedness; |

| • | we may be unable to borrow additional funds as needed or on favorable terms, which could, among other things, adversely affect our ability to capitalize upon investment opportunities or meet ongoing operational needs; |

| • | we may be unable to refinance our indebtedness at maturity or the refinancing terms may be less favorable than the terms of the maturing indebtedness; |

| • | because a portion of our debt bears interest at variable rates, increases in interest rates could increase our interest expense, thereby adversely impacting our cash flows; |

| • | should we seek to hedge any of our floating rate indebtedness, we may be unable to hedge floating rate debt, counterparties may fail to honor their obligations under any hedge agreements we enter into, such agreements may not effectively hedge interest rate fluctuation risk, and, upon the expiration of any hedge agreements we enter into, we would be exposed to then-existing market rates of interest and future interest rate volatility; |

S-6

Table of Contents

| • | we may be forced to dispose of properties, possibly on unfavorable terms or in violation of certain covenants to which we may be subject; |

| • | we may default on any secured debt obligations we may have and the lenders or mortgagees may foreclose on our properties subject to such indebtedness or our interests in the entities that own the properties that secure their loans and receive an assignment of rents and leases; |

| • | we may be restricted from accessing some of our excess cash flow after debt service; |

| • | we may violate restrictive covenants in our loan documents, which would entitle the lenders to accelerate our debt obligations; and |

| • | our default under any loan with cross-default provisions could result in a default on other indebtedness. |

If any one of these events were to occur, our financial condition, results of operations, cash flows and cash available for distribution, including our ability to satisfy our debt service obligations with respect to the notes, could be materially adversely affected. Furthermore, foreclosures could create taxable income without accompanying cash proceeds, which could hinder our ability to meet the REIT distribution requirements imposed by the Internal Revenue Code of 1986, as amended.

Additionally, payments of principal and interest on borrowings may leave us with insufficient cash resources to meet our other cash needs or to make distributions to our common stockholders that are necessary to maintain our REIT qualification.

The effective subordination of the notes may limit our ability to satisfy our obligations under the notes.

The notes will be our operating partnership’s senior unsecured obligations and will rank equally in right of payment with all of its other existing and future senior unsecured indebtedness. The notes will be effectively subordinated in right of payment to:

| • | all of our operating partnership’s existing and future mortgage indebtedness and other secured indebtedness (to the extent of the value of the collateral securing such indebtedness); |

| • | all existing and future indebtedness and other liabilities, whether secured or unsecured, of our operating partnership’s subsidiaries and of any entity our operating partnership accounts for using the equity method of accounting; and |

| • | all preferred equity not owned by our operating partnership, if any, in any of our operating partnership’s subsidiaries and in any entity our operating partnership accounts for using the equity method of accounting. |

Similarly, our guarantee of the notes will be our senior unsecured obligation and will rank equally in right of payment with all of our other existing and future senior unsecured indebtedness and guarantees. Our guarantee of the notes will be effectively subordinated in right of payment to:

| • | all of our existing and future secured indebtedness and secured guarantees (to the extent of the value of the collateral securing such indebtedness or guarantees); |

| • | all existing and future indebtedness and other liabilities, whether secured or unsecured, of our consolidated subsidiaries (including our operating partnership) and of any entity we account for using the equity method of accounting; and |

| • | all preferred equity not owned by us, if any, in any of our consolidated subsidiaries (including our operating partnership) and in any entity we account for using the equity method of accounting. |

Although the indenture that will govern the notes will contain covenants that will limit the ability of our company and its subsidiaries (including our operating partnership) to incur secured and unsecured indebtedness,

S-7

Table of Contents

those covenants are subject to significant exceptions. Moreover, our company and its subsidiaries (including our operating partnership) may be able to incur substantial amounts of additional secured and unsecured indebtedness without violating those covenants.

In the event of the bankruptcy, liquidation, reorganization or other winding up of our operating partnership or our company, assets that secure any of our respective secured indebtedness, secured guarantees and other secured obligations will be available to pay our respective obligations under the notes or the guarantee of the notes, as applicable, and our other respective unsecured indebtedness, unsecured guarantees and other unsecured obligations only after all of our respective indebtedness, guarantees and other obligations secured by those assets have been repaid in full, and we caution you that there may not be sufficient assets remaining to pay amounts due on any or all the notes or the guarantee of the notes, as the case may be, then outstanding. In the event of the bankruptcy, liquidation, reorganization or other winding up of any of the subsidiaries of our operating partnership or our company, the rights of holders of indebtedness and other obligations of our operating partnership (including the notes) or our company (including our guarantee of the notes), as the case may be, will be effectively subordinated to the prior claims of that subsidiary’s creditors and of the holders of any indebtedness or other obligations guaranteed by that subsidiary, except to the extent that our operating partnership or our company, is itself a creditor with recognized claims against that subsidiary, in which case those claims would still be effectively subordinated to all debt secured by mortgages or other liens on the assets of that subsidiary (to the extent of the value of those assets) and would be subordinate to all indebtedness of that subsidiary senior to that held by our operating partnership or our company, as the case may be. Moreover, in the event of the bankruptcy, liquidation, reorganization or other winding up of any subsidiary of our operating partnership or our company, the rights of holders of indebtedness and other obligations of our operating partnership (including the notes) or our company (including our guarantee of the notes), as the case may be, will be effectively subordinated to any equity interests in that subsidiary held by persons other than our operating partnership or our company, as the case may be. In addition, in the event of the bankruptcy, liquidation, reorganization or other winding up of any subsidiary or other entity that our operating partnership or our company accounts for using the equity method of accounting, the rights of holders of indebtedness and other obligations of our operating partnership (including the notes) or our company (including our guarantee of the notes) will be subject to the prior claims of that entity’s creditors and the holders of any indebtedness or other obligations of that entity, except to the extent that our operating partnership or our company, as the case may be, is itself a creditor with recognized claims against that entity, in which case those claims would still be effectively subordinated to all debt secured by mortgages or other liens on the assets of that entity (to the extent of the value of those assets) and would be subordinate to all indebtedness of that entity senior to that held by our operating partnership or our company, as the case may be.

We may not be able to generate sufficient cash flow to meet our debt service obligations.

Our ability to make payments on and to refinance our indebtedness, including the notes, and to fund our operations, working capital and capital expenditures, depends on our ability to generate cash flows from our operations in the future. Our operating cash flow is subject to, among other factors, general economic, industry, financial, competitive, operating, legislative, regulatory and other factors, many of which are beyond our control. The instruments and agreements governing some of our outstanding indebtedness (including borrowings under our revolving credit facility) contain provisions that require us to repay that indebtedness under specified circumstances or upon the occurrence of specified events (including certain changes of control of our company) and our future debt agreements and debt securities may contain similar provisions or may require that we repurchase or offer to repurchase the applicable indebtedness for cash under specified circumstances or upon the occurrence of specified changes of control of our company or our operating partnership or other events. We may not have sufficient funds to pay our indebtedness when due (including upon any such required repurchase, repayment or offer to repurchase), and we may not be able to arrange for the financing necessary to make those payments, on favorable terms or at all. In addition, our ability to make required payments on our indebtedness when due (including upon any such required repurchase, repayment or offer to repurchase) may be limited by the terms of other debt instruments or agreements. Any of these events could materially adversely affect our ability

S-8

Table of Contents

to make payments of principal and interest on the notes when due and could prevent us from making those payments altogether.

We cannot assure you that our business will generate sufficient cash flow from operations or that future sources of cash will be available to us in an amount sufficient to enable us to pay amounts due on our indebtedness, including the notes, or to fund our other liquidity needs, including cash distributions necessary to maintain our REIT status. Additionally, if we incur additional indebtedness, including for the purpose of funding future investment activities or for any other purpose, our debt service obligations would increase.

We may need to or seek to refinance all or a portion of our indebtedness, including the notes, on or before maturity. Our ability to refinance our indebtedness or obtain additional financing will depend on, among other things:

| • | our financial condition, results of operations and market conditions at the time; and |

| • | restrictions in the agreements governing our indebtedness. |

As a result, we may not be able to refinance any of our indebtedness, including the notes, on commercially reasonable terms, or at all. If we do not generate sufficient cash flow from operations, and additional borrowings or refinancings or proceeds of asset sales or other sources of cash are not available to us, we may not have sufficient cash to enable us to meet all of our obligations, including payments on the notes. Accordingly, if we cannot service our indebtedness, we may have to take actions such as seeking additional equity financing, delaying additional investments in income producing properties, postponing capital expenditures, or discontinuing the pursuit of strategic acquisitions or alliances, any of which could have a material adverse effect on our financial condition, results of operations, cash flows, the trading price of our securities (including the notes) and our ability to satisfy our debt service obligations and to pay dividends and distributions to our security holders.

The agreements governing our indebtedness contain, and the indenture governing the notes will contain, restrictions and covenants which may limit our ability to enter into or obtain funding for certain transactions and operate our business.

The agreements governing our indebtedness contain and the indenture governing the notes will contain restrictions and covenants that limit or will limit our ability to operate our business. The agreements governing our indebtedness contain covenants and other restrictions that will affect, among other things, our ability to:

| • | incur indebtedness; |

| • | create liens on assets; |

| • | sell or substitute assets; |

| • | modify certain terms of our leases; |

| • | manage our cash flows; and |

| • | make distributions to equity holders. |

The indenture governing the notes will also contain covenants and other restrictions that will affect, among other things, our ability to:

| • | consummate a merger, consolidation or sale of all or substantially all of our assets; and |

| • | incur secured and unsecured indebtedness. |

In addition, the indenture governing the notes will require us to maintain at all times a specified ratio of unencumbered assets to unsecured debt. These covenants, as well as any additional covenants to which we may

S-9

Table of Contents

be subject in the future because of additional indebtedness, could cause us to forgo investment opportunities or obtain financing that is more expensive than financing we could obtain if we were not subject to such covenants.

If the financial performance of the collateral for our indebtedness under our master trust funding program fails to achieve certain criteria, cash from such collateral may be unavailable to us until the terms are cured or the debt refinanced. The occurrence of these events limits the amount of cash available to us for use in our business.

Despite our current level of indebtedness, we may incur significantly more debt, which could exacerbate any or all of the risks described above, and adversely impact our ability to pay the principal of or interest on the notes.

We may be able to incur substantial additional indebtedness in the future. Although the agreements governing our revolving credit facility and certain other indebtedness (including the indenture governing the notes) limit, and the indenture governing the notes will limit, our ability to incur additional indebtedness, these restrictions are subject to a number of qualifications and exceptions and, under certain circumstances, we may, in compliance with these restrictions, incur additional indebtedness, which could be substantial. To the extent that we incur additional indebtedness or such other obligations, the risks associated with our leverage as described above, including our possible inability to service our debt, would increase. In addition, the agreements governing our revolving credit facility and certain other indebtedness, and the indenture governing the notes, will not prevent us from incurring obligations that do not constitute indebtedness.

Our company does not have any significant operations or material assets other than its direct and indirect investments in our operating partnership.

The notes will be fully and unconditionally guaranteed by our company. Our company does not have any significant operations or material assets other than its direct and indirect investments in our operating partnership. Accordingly, if our operating partnership fails to make a payment on the notes when due, there can be no assurance that we would have the necessary funds to pay that amount due pursuant to our guarantee.

Furthermore, as described above under “—The effective subordination of the notes may limit our ability to satisfy our obligations under the notes,” our guarantee will be effectively subordinated in right of payment to:

| • | all of our existing and future secured indebtedness and secured guarantees (to the extent of the value of the collateral securing such indebtedness or guarantees); |

| • | all existing and future indebtedness and other liabilities, whether secured or unsecured, of our consolidated subsidiaries (including our operating partnership) and of any entity we account for using the equity method of accounting; and |

| • | all preferred equity not owned by us, if any, in any of our consolidated subsidiaries (including our operating partnership) and in any entity we account for using the equity method of accounting. |

Federal and state statutes allow courts, under specific circumstances, to void guarantees and require holders of guaranteed debt to return payments received from guarantors.

Under the federal bankruptcy law and comparable provisions of state fraudulent transfer laws, a guarantee, such as the guarantee provided by our company, could be voided, or claims in respect of a guarantee could be subordinated to all other debts of that guarantor if, among other things, the guarantor, at the time it incurred or entered into its guarantee:

| • | received less than reasonably equivalent value or fair consideration for the incurrence of the guarantee; |

| • | was insolvent or rendered insolvent by reason of the incurrence of the guarantee; |

| • | was engaged in a business or transaction for which the guarantor’s remaining assets constituted unreasonably small capital; or |

S-10

Table of Contents

| • | intended to incur, or believed that it would incur, debts beyond its ability to pay those debts as they mature. |

In addition, any payment by that guarantor pursuant to its guarantee could be voided and required to be returned to the guarantor, or to a fund for the benefit of the creditors of the guarantor.

The measures of insolvency for purposes of these fraudulent transfer laws will vary depending upon the law applied in any proceeding to determine whether a fraudulent transfer has occurred. Generally, however, a guarantor would be considered insolvent if:

| • | the sum of its debts, including contingent liabilities, was greater than the fair saleable value of all of its assets; |

| • | the present fair saleable value of its assets was less than the amount that would be required to pay its probable liability on its existing debts, including contingent liabilities, as they became absolute and mature; or |

| • | it could not pay its debts as they become due. |

The court might also void such guarantee, without regard to the above factors, if it found that a guarantor entered into its guarantee with actual or deemed intent to hinder, delay, or defraud its creditors.

We cannot be certain as to the standards a court would use to determine whether reasonably equivalent value or fair consideration was received by our company for its guarantee of the notes. If a court voided such guarantee, holders of the notes would no longer have a claim against such guarantor. In addition, the court might direct holders of the notes to repay any amounts already received from a guarantor. If the court were to void our company’s guarantee, require the return of monies paid by such guarantor or subordinate the guarantee to other obligations of such guarantor, we could not assure you that funds would be available to pay the notes from any of our subsidiaries or from any other source.

There is no prior public market for the notes, and if an active trading market does not develop for the notes, you may not be able to resell them.

We do not intend to apply for the listing of the notes on any national securities exchange or any automated dealer quotation system. As a result, an active trading market for the notes may not develop or be sustained. We have been informed by certain of the underwriters that they currently intend to make a market in the notes after this offering is completed. However, the underwriters are not obligated to make a market in the notes, and one or more of the underwriters may cease market-making at any time. We cannot assure you that any market for the notes will develop, or if one does develop, that it will be liquid. If the notes are traded, they may trade at a discount from their initial offering price, depending on prevailing interest rates, the market for similar securities, our credit rating, our operating performance and financial condition and other factors. If an active trading market does not develop, the market price and liquidity of the notes may be adversely affected. As a result, we cannot ensure you that you will be able to sell any of the notes at a particular time, at attractive prices, or at all. Thus, you may be required to bear the financial risk of your investment in the notes indefinitely.

Our management has significant flexibility in applying the net proceeds we expect to receive in this offering. We intend to use the net proceeds from this offering as described in “Use of Proceeds,” but because a portion of the net proceeds is not required to be allocated to any specific purpose, investment or transaction, you cannot determine at this time the value or propriety of our application of that portion of the net proceeds, and you may not agree with our decisions. In addition, our use of the net proceeds from this offering may not yield a significant return or any return at all. The failure by our management to apply these funds effectively could have a material adverse effect on our financial condition, results of operations, business or prospects. See “Use of Proceeds.”

S-11

Table of Contents

The market price of the notes may fluctuate significantly.

The market price of the notes may fluctuate significantly in response to many factors, including:

| • | actual or anticipated variations in our operating results, adjusted funds from operations, cash flows, liquidity or distributions; |

| • | our ability to successfully execute on our investment strategy; |

| • | our ability to successfully complete investments and lease acquired properties; |

| • | changes in our earnings estimates or those of research analysts; |

| • | publication of research reports about us, the real estate industry generally or the sectors in which we invest; |

| • | the failure to maintain our current credit ratings or comply with our debt covenants; |

| • | increases in market interest rates; |

| • | changes in market valuations of similar companies; |

| • | adverse market reaction to any debt or equity securities we may issue or additional debt we may incur in the future; |

| • | additions or departures of key management personnel; |

| • | actions by institutional investors invested in our company; |

| • | speculation in the press or investment community; |

| • | high levels of volatility in the credit markets; |

| • | adverse market reactions as a result of epidemics, pandemics or other outbreaks of illness, disease or virus (such as the strain of coronavirus known as COVID-19); |

| • | general market and economic conditions; and |

| • | the realization of any of the other risk factors included in or incorporated by reference in this prospectus supplement and the accompanying prospectus. |

Many of the factors listed above are beyond our control. These factors may cause the market price of the notes to decline, regardless of our financial condition, results of operations, business or prospects. We cannot assure you that the market price of the notes will not fall in the future, and as a result it may be difficult for investors to resell the notes at prices they find attractive, or at all.

An increase in interest rates could result in a decrease in the market value of the notes.

In general, as market interest rates rise, notes bearing interest at a fixed rate generally decline in value. Consequently, if you purchase these notes and market interest rates increase, the market value of your notes may decline. We are not able to predict the future level of market interest rates.

A downgrade in our credit ratings could materially adversely affect our business and financial condition and the market value of the notes.

The credit ratings assigned to the notes and other debt securities of our operating partnership could change based upon, among other things, our results of operations and financial condition. These ratings are subject to ongoing evaluation by credit rating agencies, and we cannot assure you that any rating will not be changed or withdrawn by a rating agency in the future if, in its judgment, circumstances warrant. Moreover, these credit ratings are not recommendations to buy, sell or hold the notes or any other securities. If any of the credit rating agencies that have rated the notes or other debt securities of our operating partnership downgrades or lowers its

S-12

Table of Contents

credit rating, or if any credit rating agency indicates that it has placed any such rating on a so-called “watch list” for a possible downgrading or lowering or otherwise indicates that its outlook for that rating is negative, it could have a material adverse effect on the market value of the notes and our costs and availability of capital, which could in turn have a material adverse effect on our financial condition, results of operations, cash flows and our ability to satisfy our debt service obligations (including payments on the notes) and to make dividends and distributions to our security holders and could also have a material adverse effect on the market value of the notes.

S-13

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus supplement and the accompanying prospectus contain or incorporate by reference forward- looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). In particular, statements pertaining to our business and growth strategies, investment, financing and leasing activities and trends in our business, including trends in the market for long-term, net leases of freestanding, single-tenant properties, contain forward-looking statements. When used in this prospectus supplement, the accompanying prospectus or the documents incorporated by reference in this prospectus supplement and the accompanying prospectus, the words “estimate,” “anticipate,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “seek,” “approximately,” “plan,” and variations of such words, and similar words or phrases, that are predictions of future events or trends and that do not relate solely to historical matters, are intended to identify forward-looking statements. You can also identify forward-looking statements by discussions of strategy, plans or intentions of management.

Forward-looking statements involve known and unknown risks and uncertainties that may cause our actual results, performance or achievements to be materially different from the results of operations or plans expressed or implied by such forward-looking statements; accordingly, you should not rely on forward-looking statements as predictions of future events. Forward-looking statements depend on assumptions, data or methods that may be incorrect or imprecise, and may not be realized. We do not guarantee that the transactions and events described will happen as described (or that they will happen at all). The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements:

| • | the ongoing adverse impact of the COVID-19 pandemic on us and our tenants; |

| • | general business and economic conditions; |

| • | risks inherent in the real estate business, including tenant defaults or bankruptcies, illiquidity of real estate investments, fluctuations in real estate values and the general economic climate in local markets, competition for tenants in such markets, potential liability relating to environmental matters and potential damages from natural disasters; |

| • | the performance and financial condition of our tenants; |

| • | the availability of suitable properties to invest in and our ability to acquire and lease those properties on favorable terms; |

| • | our ability to renew leases, lease vacant space or re-lease space as existing leases expire or are terminated; |

| • | volatility and uncertainty in the credit markets and broader financial markets, including potential fluctuations in the CPI; |

| • | the degree and nature of our competition; |

| • | our failure to generate sufficient cash flows to service our outstanding indebtedness; |

| • | our ability to access debt and equity capital on attractive terms; |

| • | fluctuating interest rates; |

| • | availability of qualified personnel and our ability to retain our key management personnel; |

| • | changes in, or the failure or inability to comply with, applicable law or regulation; |

| • | our failure to continue to qualify for taxation as a REIT; |

| • | changes in the U.S. tax law and other U.S. laws, whether or not specific to REITs; and |

S-14

Table of Contents

| • | additional factors, including, but not limited to, those referred to under the caption “Risk Factors” in this prospectus supplement and in our Annual Report on Form 10-K for the year ended December 31, 2020. |

You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of the document in which they are contained. While forward-looking statements reflect our good faith beliefs, they are not guarantees of future events or of our performance. We disclaim any obligation to publicly update or revise any forward-looking statements to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes, except as required by law.

Because we operate in a highly competitive and rapidly changing environment, new risks emerge from time to time, and it is not possible for management to predict all such risks, nor can management assess the impact of all such risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, investors should not place undue reliance on forward-looking statements as a prediction of actual events or results.

S-15

Table of Contents

We estimate that the net proceeds from this offering will be approximately $395.9 million, after deducting the underwriting discount and other estimated expenses.

We intend to use the net proceeds from this offering (i) to prepay all of the secured debt principal outstanding under our master trust funding program (plus a make whole amount); (ii) to repay amounts outstanding under our revolving credit facility; and (iii) for general corporate purposes, including funding future investment activity.

As of May 31, 2021, $171.5 million of secured debt principal was outstanding under our master trust funding program. This secured debt bears interest at a weighted average annual rate of 4.2%. In connection with the prepayment of this indebtedness, we expect to pay a make whole amount of approximately $2.6 million and incur a loss on debt extinguishment of approximately $4.6 million (approximately $1.9 million of which will be a non-cash charge associated with the write off of unamortized deferred financing costs). Such loss on debt extinguishment is not expected to impact our adjusted funds from operations. As of May 31, 2021, we had pledged 261 properties, with a net investment amount of $366.9 million, as collateral under our master trust funding program, and these properties will be released from such pledge and become unencumbered in connection with our prepayment of the secured debt.

As of May 31, 2021, our operating partnership had $47.0 million of indebtedness outstanding under its revolving credit facility. Our revolving credit facility bears interest at applicable LIBOR, plus an applicable margin, which is initially set according to a leverage-based pricing grid; however, at our operating partnership’s election, at and after receipt of an investment grade corporate credit rating from Standard & Poor’s Ratings Services or Moody’s Investors Service, Inc., the applicable margin will be a spread set according to the credit ratings. As of May 31, 2021, our revolving credit facility bore interest at LIBOR plus 1.30% per annum and incurred an unused facility fee of 0.25% per annum, based on our leverage ratio and our usage of our revolving credit facility, respectively. Our revolving credit facility has a maturity date of April 12, 2023 (extendable at our operating partnership’s option to up to April 12, 2024, subject to certain conditions). Any borrowings under our revolving credit facility that are repaid with any such net proceeds may be reborrowed, subject to customary conditions.

Affiliates of certain of the underwriters are lenders and, in certain cases, agents under our revolving credit facility and will receive pro rata portions of the net proceeds from this offering used to repay the balance outstanding thereunder. See “Underwriting.”

Pending the permanent use of the net proceeds from this offering, we intend to invest the net proceeds in interest-bearing, short-term investment-grade securities, money-market accounts or other investments that are consistent with our qualification for taxation as a REIT for federal income tax purposes.

S-16

Table of Contents

The following description of the terms of the notes (referred to in the accompanying prospectus as the “debt securities”) supplements, and to the extent inconsistent, replaces the description of the general terms and provisions of the debt securities set forth in the accompanying prospectus. The following description of the notes does not purport to be complete and is subject to, and qualified in its entirety by reference to, the actual terms and provisions of the notes and the indenture, which are incorporated herein by reference. Capitalized terms used but not otherwise defined herein shall have the meanings given to them in the notes or the indenture, as applicable. Unless the context otherwise requires, as used in this section, the terms “we,” “us” and “our” refer only to Essential Properties, L.P. and not to its subsidiaries or Essential Properties Realty Trust, Inc., and the term “Guarantor” refers only to Essential Properties Realty Trust, Inc. and not to its subsidiaries.

General

We will issue the notes under an indenture and a supplemental indenture, each to be dated as of June 28, 2021, among us, the Guarantor, as guarantor, and U.S. Bank National Association, as trustee (together, the “indenture”). The terms of the notes will include those made part of the indenture by reference to the Trust Indenture Act of 1939, as amended (the “Trust Indenture Act”). The notes are subject to all of these terms, and holders of notes are referred to the indenture and the Trust Indenture Act for a statement of those terms.

The notes will be limited initially to $400.0 million aggregate principal amount. We may in the future, without the consent of holders, issue additional notes on the same terms and conditions as the notes being offered hereby, except for any difference in the issue date, public offering price, interest accrued prior to the issue date of the additional notes, and, if applicable, the initial interest payment date. The notes and any additional notes of such series subsequently issued under the indenture would be treated as a single series for all purposes under the indenture, including, without limitation, waivers, amendments, redemptions and offers to purchase; provided, however, that if such additional notes will not be fungible with the previously issued notes for U.S. federal income tax purposes, such additional notes will have a separate CUSIP number.

The following description is a summary of the material provisions of the indenture. It does not restate the terms of the indenture in their entirety. We urge you to read the indenture because it, and not this description, defines your rights as holders of the notes. Copies of the indenture are available as set forth below under “—Additional Information.” Certain defined terms used in this description but not defined below have the meanings assigned to them in the indenture. Except as set forth in this prospectus supplement under the caption “—Covenants,” the indenture does not contain any provisions applicable to the notes that would limit our, our subsidiaries’ or the Guarantor’s ability to incur indebtedness or that would afford holders of the notes protection in the event of a highly leveraged or similar transaction involving us or in the event of a change of control.

The notes will be issued only in fully registered form, in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof.

Principal and Interest

The notes will bear interest at the rate of 2.950% per year and will mature on July 15, 2031. Interest on the notes will accrue from June 28, 2021.

Interest on the notes will be payable semi-annually in arrears on January 15 and July 15 of each year, commencing on January 15, 2022 (each such date being an “interest payment date”), to the persons in whose names the notes are registered in the security register on the preceding January 1 or July 1, whether or not a business day, as the case may be (each such date being a “regular record date”). Interest on the notes will be computed on the basis of a 360-day year consisting of twelve 30-day months.

S-17

Table of Contents

If any interest payment date, maturity date or earlier date of redemption falls on a day that is not a business day, the required payment shall be made on the next business day as if it were made on the date the payment was due and no interest shall accrue on the amount so payable for the period from and after that interest payment date, that maturity date or that date of redemption, as the case may be, until the next business day. For purposes of the notes, a business day means any day, other than a Saturday or Sunday, or legal holidays on which banks in The City of New York are not required or authorized by law or executive order to be closed.

The principal of, and premium, if any, and interest, if any, on, the notes will be payable at the corporate trust office of the trustee, initially located at 111 Fillmore Avenue E, St. Paul, Minnesota 55107; except that, at our option, payment of interest, if any, may be made by check mailed to the address of the person entitled to the payment as it appears in the security register or by wire transfer of funds to the person to an account maintained within the United States. Notes may be surrendered for registration of transfer or exchange, and notices or demands to or upon us in respect of the notes and the indenture may be served, at such corporate trust office as well.

If we redeem the notes, we will pay accrued and unpaid interest, if any, to holders of the notes who surrender such notes for redemption. However, if a redemption date falls after a regular record date and on or prior to the corresponding interest payment date, we will pay the full amount of accrued and unpaid interest, if any, due on such interest payment date to the holder of record at the close of business on the corresponding regular record date (instead of the holder surrendering its notes for redemption) and the redemption price shall not include accrued and unpaid interest, if any, up to, but not including, the redemption date.

Ranking

The notes will be our senior unsecured obligations and will rank equally in right of payment with all of our other existing and future senior unsecured indebtedness. The notes will be effectively subordinated in right of payment to:

| • | all of our existing and future mortgage indebtedness and other secured indebtedness (to the extent of the value of the collateral securing such indebtedness); |

| • | all existing and future indebtedness and other liabilities, whether secured or unsecured, of our subsidiaries and of any entity we account for using the equity method of accounting; and |

| • | all preferred equity not owned by us, if any, in any of our subsidiaries and in any entity we account for using the equity method of accounting. |

The indenture that will govern the notes will not prohibit us or the Guarantor or any of our respective subsidiaries from incurring secured or unsecured indebtedness in the future. Although the indenture will contain covenants that will limit the Guarantor’s ability and the ability of its subsidiaries (including us) to incur secured and unsecured indebtedness, those covenants are subject to significant exceptions. Moreover, the Guarantor and its subsidiaries may be able to incur substantial amounts of additional secured and unsecured indebtedness without violating those covenants.

Assuming we had completed this offering of the notes on May 31, 2021, the notes would have been effectively subordinated to approximately $171.5 million principal amount of total consolidated mortgage debt outstanding; however, all of such mortgage debt will be prepaid with a portion of the net proceeds from this offering. At such date, we and our subsidiaries had no unsecured indebtedness or preferred equity outstanding other than $630.0 million of principal outstanding on our unsecured term loans and $47.0 million outstanding under our revolving credit facility (which will also be repaid with a portion of the net proceeds from this offering).

For additional information, see “Risk Factors—Risks Related to this Offering and the Notes—The effective subordination of the notes may limit our ability to satisfy our obligations under the notes.”

S-18

Table of Contents

Guarantee

The Guarantor will guarantee our obligations under the notes on a full and unconditional basis, including the due and punctual payment of principal of, and premium, if any, and interest, if any, on, the notes, whether at stated maturity, upon acceleration, upon redemption or otherwise. Under the terms of the guarantee, holders of the notes will not be required to exercise their remedies against us before they proceed directly against the Guarantor. The Guarantor’s obligations under its guarantee of the notes will be limited to the maximum amount that will not, after giving effect to all other contingent and fixed liabilities of the Guarantor, result in the guarantee constituting a fraudulent transfer or conveyance. See “Risk Factors—Risks Related to this Offering and the Notes—Federal and state statutes allow courts, under specific circumstances, to void guarantees and require holders of guaranteed debt to return payments received from guarantors.”

The guarantee of the notes will be a senior unsecured obligation of the Guarantor and will rank equally in right of payment with all other existing and future senior unsecured indebtedness and guarantees of the Guarantor. The Guarantor’s guarantee of the notes will be effectively subordinated in right of payment to:

| • | all of the Guarantor’s existing and future secured indebtedness and secured guarantees (to the extent of the value of the collateral securing such indebtedness or guarantees); |

| • | all existing and future indebtedness and other liabilities, whether secured or unsecured, of the Guarantor’s consolidated subsidiaries (including us) and of any entity the Guarantor accounts for using the equity method of accounting; and |

| • | all preferred equity not owned by the Guarantor, if any, in any of the Guarantor’s consolidated subsidiaries (including us) and in any entity the Guarantor accounts for using the equity method of accounting. |

The Guarantor generally does not have any significant operations or material assets other than its direct and indirect investments in us. See “Risk Factors—Risks Related to this Offering and the Notes—Our company does not have any significant operations or material assets other than its direct and indirect investments in our operating partnership.”

For additional information, see “Risk Factors—Risks Related to this Offering and the Notes—The effective subordination of the notes may limit our ability to satisfy our obligations under the notes.”

Optional Redemption

The notes will be redeemable in whole at any time or in part from time to time, at our option, at a redemption price calculated by us and equal to the sum of (1) 100% of the principal amount of the notes to be redeemed plus accrued and unpaid interest, if any, up to, but not including, the redemption date plus (2) a make-whole premium.

Notwithstanding the foregoing, if any notes are redeemed on or after April 15, 2031 (three months prior to the maturity date of the notes (the “Par Call Date”)), the redemption price will equal 100% of the principal amount of the notes to be redeemed plus accrued and unpaid interest, if any, up to, but not including, the redemption date, without any make-whole premium.

We will calculate the make-whole premium with respect to any notes redeemed before the Par Call Date as the excess, if any, of:

| • | the sum of the present values of the remaining scheduled payments of principal and interest, if any, thereon (exclusive of interest, if any, accrued to the date of redemption) that would be due if the notes matured on the Par Call Date, determined by discounting to the redemption date, on a semiannual basis, each such scheduled payment of principal and interest, if any, at the Treasury Rate (as defined below) |

S-19

Table of Contents

| plus 25 basis points, determined on the third business day preceding the date the notice of redemption is given from the respective dates on which such principal and interest would have been payable if such redemption had not been made; over |

| • | the principal amount of such notes. |

“Comparable Treasury Issue” means the United States Treasury security selected by an Independent Investment Banker as having a maturity comparable to the remaining term of the notes to be redeemed (assuming, for this purpose, that the notes matured on the Par Call Date) that could be utilized, at the time of selection and in accordance with customary financial practice, in pricing new issues of corporate debt securities of comparable maturity to the remaining term of the notes to be redeemed (assuming, for this purpose, that the notes matured on the Par Call Date).

“Comparable Treasury Price” means, with respect to any redemption, (1) the average of the Reference Treasury Dealer Quotations for such redemption, after excluding the highest and lowest Reference Treasury Dealer Quotations, or (2) if we obtain fewer than four such Reference Treasury Dealer Quotations, the average of all such quotations.

“Independent Investment Banker” means one of the Reference Treasury Dealers that we appoint to act as the Independent Investment Banker from time to time.

“Reference Treasury Dealer” means, each of BofA Securities, Inc., Citigroup Global Markets Inc., Barclays Capital Inc. and Goldman Sachs & Co. LLC and their successors, and one other firm that is a primary U.S. Government securities dealer (each a “Primary Treasury Dealer”) which we specify from time to time; provided, however, that if any of them ceases to be a Primary Treasury Dealer, we will substitute another Primary Treasury Dealer.

“Reference Treasury Dealer Quotations” means, with respect to each Reference Treasury Dealer and any redemption, the average, as determined by us, of the bid and asked prices for the Comparable Treasury Issue (expressed in each case as a percentage of its principal amount) quoted in writing to us by such Reference Treasury Dealer at 5:00 p.m., New York City time, on the third business day preceding the date the notice of such redemption is given.

“Treasury Rate” means, with respect to any redemption, the rate per year equal to: (1) the yield, under the heading which represents the average for the week immediately preceding the third business day prior to the date the notice of such redemption is given, appearing in the most recently published statistical release designated “H.15” or any successor publication which is published weekly by the Board of Governors of the Federal Reserve System and which establishes yields on actively traded United States Treasury securities adjusted to constant maturity under the caption “Treasury Constant Maturities,” for the maturity corresponding to the Comparable Treasury Issue; provided that, if no maturity is within three months before or after the remaining term of the notes to be redeemed, yields for the two published maturities most closely corresponding to the Comparable Treasury Issue shall be determined and the Treasury Rate shall be interpolated or extrapolated from those yields on a straight line basis, rounding to the nearest month; or (2) if such release (or any successor release) is not published during the week preceding the calculation date or does not contain such yields, the rate per year equal to the semiannual equivalent yield to maturity of the Comparable Treasury Issue, calculated using a price for the Comparable Treasury Issue (expressed as a percentage of its principal amount) equal to the Comparable Treasury Price for such redemption. The Treasury Rate shall be calculated on the third business day preceding the date the notice of redemption is given. In the case of a satisfaction and discharge, such rates shall be determined as of the date of the deposit with the trustee.

Notice of redemption will be mailed or sent by electronic transmission at least 15 but not more than 60 calendar days before the redemption date to each holder of record of the notes to be redeemed at its last registered address and the trustee (if the notice is to be delivered by us). The notice of redemption for the notes

S-20

Table of Contents

will state, among other things, the aggregate principal amount of notes to be redeemed, the redemption date, the redemption price and the place or places that payment will be made upon presentation and surrender of notes to be redeemed. Unless we default in payment of the redemption price, interest, if any, will cease to accrue on any notes that have been called for redemption at the redemption date, on and after the redemption date (unless we default in the payment of the redemption price) such notes shall cease to be entitled to any benefit or security under the indenture, and the holders of such notes shall have no right in respect of such notes except the right to receive the redemption price thereof.

If less than all of the notes are to be redeemed at our option, the trustee will select the notes to be redeemed by lot, subject to the customary procedures of DTC (or relevant depositary), in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof.

In the event of any redemption of the notes in part, we will not be required to: