Form 424B5 CANADIAN IMPERIAL BANK

Tweet

Tweet Share

Share

Product Supplement No. COMM MITTS-1 and Prospectus Supplement dated September 2, 2021) January 27, 2023 | Filed Pursuant to Rule 424(b)(5) Registration No. 333-257113 |

Market Index Target-Term Securities® “MITTS®” Linked to One or More Commodities, Related Futures Contracts or Commodity Indices

| · | MITTS are unsecured senior notes issued by Canadian Imperial Bank of Commerce. Any payments due on MITTS, including any repayment of principal, will be subject to the credit risk of Canadian Imperial Bank of Commerce. |

| · | MITTS may not guarantee the full return of principal at maturity, and we will not pay interest on MITTS. Instead, the return on MITTS will be based on the performance of an underlying “Market Measure,” which will be a commodity, a futures contract on a commodity, a commodity index, or a basket of the foregoing. |

| · | If the value of the Market Measure increases from its Starting Value to its Ending Value (each as defined below), you will receive at maturity a cash payment per unit (the “Redemption Amount”) that equals the principal amount plus a multiple (the “Participation Rate”) of that increase. The Participation Rate will generally be greater than or equal to 100%. The Redemption Amount may be subject to a specified cap (the “Capped Value”). |

| · | If the value of the Market Measure does not change or decreases from its Starting Value to its Ending Value, you will receive a Redemption Amount that is no less than the minimum redemption amount per unit (the “Minimum Redemption Amount”). The Minimum Redemption Amount may be less than or equal to the principal amount. If the Minimum Redemption Amount is less than the principal amount, you may lose a portion of your investment in MITTS. |

| · | This product supplement describes the general terms of MITTS, the risk factors to consider before investing, the general manner in which they may be offered and sold, and other relevant information. |

| · | For each offering of MITTS, we will provide you with a pricing supplement (which we refer to as a “term sheet”) that will describe the specific terms of that offering, including the specific Market Measure, the Participation Rate, the Minimum Redemption Amount and the Capped Value, if applicable, and certain related risk factors. The applicable term sheet will identify, if applicable, any additions or changes to the terms specified in this product supplement. |

| · | MITTS will be issued in denominations of whole units. Unless otherwise set forth in the applicable term sheet, each unit will have a principal amount of $10. The applicable term sheet may also set forth a minimum number of units that you must purchase. |

| · | Unless otherwise specified in the applicable term sheet, MITTS will not be listed on a securities exchange. |

| · | BofA Securities, Inc. (“BofAS”) and one or more of its affiliates may act as our agents to offer MITTS and will act in a principal capacity in such role. |

MITTS are unsecured and are not savings accounts or insured deposits of a bank. MITTS are not insured by the Canada Deposit Insurance Corporation, the U.S. Federal Deposit Insurance Corporation (the “FDIC”) or any other governmental agency of the United States, Canada, or any other jurisdiction. Potential purchasers of MITTS should consider the information in “Risk Factors” beginning on page PS-6 of this product supplement, page S-1 of the accompanying prospectus supplement, and page 1 of the accompanying prospectus.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or passed upon the adequacy or accuracy of this product supplement, the prospectus supplement, or the prospectus. Any representation to the contrary is a criminal offense.

BofA Securities

TABLE OF CONTENTS

| Page | |

| SUMMARY | PS-3 |

| RISK FACTORS | PS-6 |

| DESCRIPTION OF MITTS | PS-17 |

| SUPPLEMENTAL PLAN OF DISTRIBUTION | PS-27 |

| CANADIAN FEDERAL INCOME TAX SUMMARY | PS-28 |

| U.S. FEDERAL INCOME TAX SUMMARY | PS-28 |

MITTS® and “Market Index Target-Term Securities®” are registered service marks of Bank of America Corporation, the parent corporation of BofAS.

PS-2

SUMMARY

The information in this “Summary” section is qualified in its entirety by the more detailed explanation set forth elsewhere in this product supplement, the prospectus supplement, and the prospectus, as well as the applicable term sheet. Neither we nor BofAS have authorized any other person to provide you with any information different from the information set forth in these documents. If anyone provides you with different or inconsistent information about MITTS, you should not rely on it.

Key Terms:

| General: |

MITTS are senior unsecured debt securities issued by Canadian Imperial Bank of Commerce, and are not guaranteed or insured by the Canada Deposit Insurance Corporation, the FDIC or any other governmental agency of the United States, Canada or any other jurisdiction, and are not, either directly or indirectly, an obligation of any third party. They rank equally with all of our other unsecured senior debt from time to time outstanding. Any payments due on MITTS, including any repayment of principal, will be subject to our credit risk.

The return on MITTS will be based on the performance of a Market Measure. If the value of the applicable Market Measure decreases, you will receive at least the Minimum Redemption Amount specified in the applicable term sheet. If the Minimum Redemption Amount is less than the principal amount, you may lose a portion of your investment in MITTS.

Each issue of MITTS will mature on the date set forth in the applicable term sheet. We cannot redeem MITTS at any earlier date. We will not make any payments on MITTS until maturity, and you will not receive any interest payments. | |

| Market Measure: |

The Market Measure may consist of one or more of the following:

· commodities;

· futures contracts on a commodity;

· commodity indices; or

· any combination of the above.

The Market Measure may consist of a group, or “Basket,” of the foregoing. We refer to each component included in any Basket as a “Basket Component.” If the Market Measure to which your MITTS are linked is a Basket, the Basket Components will be set forth in the applicable term sheet. | |

| Market Measure Performance: |

The performance of the Market Measure will be measured according to the percentage change of the Market Measure from its Starting Value to its Ending Value.

Unless otherwise specified in the applicable term sheet:

The “Starting Value” will be the closing value of the Market Measure on the date when MITTS are priced for initial sale to the public (the “pricing date”).

If the Market Measure consists of a Basket, the Starting Value will be equal to 100. See “Description of MITTS—Basket Market Measures.”

If a Market Disruption Event (as defined below) occurs and is continuing on the scheduled pricing date, or if certain other events occur, the calculation agent will |

PS-3

determine the Starting Value as set forth in the section “Description of MITTS—Market Disruption Events— Starting Value” or “—Basket Market Measures— Determination of the Component Ratio for Each Basket Component.”

The “Ending Value” will equal the average of the closing values of the Market Measure on each calculation day during the Maturity Valuation Period (each as defined below).

If the Market Measure consists of a Basket, the Ending Value will be determined as described in “Description of MITTS—Basket Market Measures—Ending Value of the Basket.”

If a Market Disruption Event occurs and is continuing on a scheduled calculation day, or if certain other events occur, the calculation agent will determine the Ending Value as set forth in the section “Description of MITTS—Market Disruption Events—Ending Value” or “—Basket Market Measures—Ending Value of the Basket.” |

| Participation Rate: | The rate at which investors participate in any increase in the value of the Market Measure, as calculated below. The Participation Rate will generally be greater than or equal to 100%, and will be set forth in the applicable term sheet. If the Participation Rate is 100%, your participation in any upside performance of the Market Measure will not be leveraged. | |

| Capped Value: | The maximum Redemption Amount, if one is applicable to your MITTS. If a Capped Value is applicable to your MITTS, your investment return is limited to the return represented by the Capped Value specified in the applicable term sheet. We will determine the applicable Capped Value on the pricing date of each issue of MITTS. | |

| Redemption Amount at Maturity: |

At maturity, you will receive a Redemption Amount that is greater than the principal amount if the value of the Market Measure increases from the Starting Value to the Ending Value. However, in no event will the Redemption Amount exceed the Capped Value, if applicable. If the value of the Market Measure does not change or decreases from the Starting Value to the Ending Value, you will receive at least the Minimum Redemption Amount, and if the Minimum Redemption Amount is less than the principal amount, your investment may result in a loss.

Any payments due on MITTS, including any repayment of principal, are subject to our credit risk as issuer of MITTS.

The Redemption Amount, denominated in U.S. dollars, will be calculated as follows:

The Redemption Amount will not be less than the Minimum Redemption Amount per unit. | |

| Minimum | The Minimum Redemption Amount may be less than or equal to the principal |

PS-4

| Redemption Amount: | amount, as specified in the applicable term sheet. | |

| Principal at Risk: | If the Minimum Redemption Amount for your MITTS is less than the principal amount, you may lose a portion of the principal amount of MITTS. Further, if you sell your MITTS prior to maturity in the secondary market (if any), you may find that the market value per MITTS is less than the price that you paid for MITTS, and could be less than the Minimum Redemption Amount. | |

| Calculation Agent: | The calculation agent will make all determinations associated with MITTS. Unless otherwise set forth in the applicable term sheet, we will appoint BofAS or one of its affiliates to act as the calculation agent for MITTS. See the section entitled “Description of MITTS—Role of the Calculation Agent.” | |

| Agents: | BofAS and one or more of its affiliates will act as our agents in connection with each offering of MITTS and will receive an underwriting discount based on the number of units of MITTS sold. None of the agents is your fiduciary or advisor solely as a result of the making of any offering of MITTS, and you should not rely upon this product supplement, the applicable term sheet, or the accompanying prospectus or prospectus supplement as investment advice or a recommendation to purchase MITTS. | |

| Listing: | Unless otherwise specified in the applicable term sheet, MITTS will not be listed on a securities exchange. | |

| U.S. Federal Income Tax Consequences: | MITTS will be subject to federal income tax, even though no payments on the MITTS will be made until the maturity date. You are urged to review the section entitled “U.S. Federal Income Tax Summary” and to consult your own tax advisor. | |

| ERISA Considerations: | See “Certain Considerations for U.S. Plan Investors” beginning on page 37 of the accompanying prospectus. |

This product supplement relates only to MITTS and does not relate to any commodity, futures contract or commodity index that comprises the Market Measure described in any term sheet. You should read carefully the entire prospectus, prospectus supplement, and this product supplement, together with the applicable term sheet, to understand fully the terms of your MITTS, as well as the tax and other considerations important to you in making a decision about whether to invest in any MITTS. In particular, you should review carefully the sections in this product supplement and the accompanying prospectus supplement and prospectus entitled “Risk Factors,” which highlight a number of risks of an investment in MITTS, to determine whether an investment in MITTS is appropriate for you. Additional risk factors may be set forth in the applicable term sheet. If information in this product supplement is inconsistent with information in the prospectus or prospectus supplement, this product supplement will supersede those documents. However, if information in any term sheet is inconsistent with information in this product supplement, that term sheet will supersede this product supplement. You should carefully review the applicable term sheet to understand the specific terms of your MITTS.

Neither we nor any agent is making an offer to sell MITTS in any jurisdiction where the offer or sale is not permitted.

Certain capitalized terms used and not defined in this product supplement have the meanings ascribed to them in the prospectus supplement and prospectus. Unless otherwise indicated or unless the context requires otherwise, all references in this product supplement to “we,” “us,” “our,” or similar references are to Canadian Imperial Bank of Commerce.

You are urged to consult with your own attorneys and business and tax advisors before making a decision to purchase any MITTS.

PS-5

RISK FACTORS

Your investment in MITTS is subject to investment risks, many of which differ from those of a conventional debt security. Your decision to purchase MITTS should be made only after carefully considering the risks, including those discussed below, in light of your particular circumstances. MITTS are not an appropriate investment for you if you are not knowledgeable about the material terms of MITTS or investments in commodities, futures contracts on commodities, or commodity-based indices in general.

Structure-related Risks

You may not receive a positive return on your investment and, if the Minimum Redemption Amount is less than the principal amount per unit, then your investment may result in a loss. The return on MITTS will be based on the performance of the Market Measure. If the value of the Market Measure decreases from the Starting Value to the Ending Value, you will not receive any positive return on your MITTS, and if the Minimum Redemption Amount is less than the principal amount, your investment will result in a loss.

Your investment return will be limited to the return represented by the Capped Value (if applicable), and may be less than a comparable investment directly in the Market Measure or any of its underlying assets. The appreciation potential of MITTS will be limited to the Capped Value, if applicable. In such a case, you will not receive a Redemption Amount greater than the Capped Value, regardless of the extent of the increase in the value of the Market Measure. In contrast, a direct investment in the Market Measure or any components included in the Market Measure would allow you to receive the full benefit of any appreciation in the value of the Market Measure or those components.

Additionally, the Market Measure may consist of one or more commodities, futures contracts or commodity indices that are or include components traded in a non-U.S. currency. If the value of that currency strengthens against the U.S. dollar during the term of your MITTS, you may not obtain the benefit of that increase, which you would have received if you had owned the commodities or futures contracts represented by the Market Measure.

The Redemption Amount will not reflect changes in the value of the Market Measure that occur other than during the Maturity Valuation Period. Changes in the value of the Market Measure during the term of MITTS other than during the Maturity Valuation Period will not be reflected in the calculation of the Redemption Amount. To calculate the Redemption Amount, the calculation agent will compare only the Ending Value to the Starting Value. No other values of the Market Measure will be taken into account. As a result, even if the value of the Market Measure has increased at certain times during the term of MITTS, you may receive a Redemption Amount that, depending on the Minimum Redemption Amount, is less than the principal amount if the Ending Value is less than the Starting Value. In addition, since the Ending Value will equal the average of the closing values of the Market Measure on each calculation day during the Maturity Valuation Period, the Ending Value may be less than the closing value of the Market Measure on any particular calculation day.

If your MITTS are linked to a Basket, changes in the value of one or more of the Basket Components may be offset by changes in the value of one or more of the other Basket Components. The Market Measure of your MITTS may be a Basket. In such a case, changes in the value of one or more of the Basket Components may not correlate with changes in the value of one or more of the other Basket Components. The value of one or more Basket Components may increase, while the value of one or more of the other Basket Components may decrease or not increase as much. Therefore, in calculating the value of the Market Measure at any time, increases in the value of one Basket Component may be moderated or wholly offset

PS-6

by decreases or lesser increases in the value of one or more of the other Basket Components. If the weightings of the applicable Basket Components are not equal, adverse changes in the values of the Basket Components that are more heavily weighted could have a greater impact upon the value of the Market Measure and, consequently, the return on your MITTS.

Your return on MITTS may be less than the yield on a conventional fixed or floating rate debt security of comparable maturity. There will be no periodic interest payments on MITTS as there would be on a conventional fixed-rate or floating-rate debt security having the same maturity. Any return that you receive on MITTS may be less than the return you would earn if you purchased a conventional debt security with the same maturity date. As a result, your investment in MITTS may not reflect the full opportunity cost to you when you consider factors, such as inflation, that affect the time value of money.

Payments on MITTS are subject to our credit risk, and any actual or perceived changes in our creditworthiness are expected to affect the value of MITTS. MITTS are our senior unsecured debt securities and are not, either directly or indirectly, an obligation of any third party. As a result, your receipt of the Redemption Amount at maturity is dependent upon our ability to repay our obligations on the maturity date, regardless of whether the Market Measure increases from the Starting Value to the Ending Value. No assurance can be given as to what our financial condition will be on the maturity date. If we become unable to meet our financial obligations as they become due, you may not receive the amounts payable under the terms of MITTS.

In addition, our credit ratings are an assessment by ratings agencies of our ability to pay our obligations. Consequently, our perceived creditworthiness and actual or anticipated decreases in our credit ratings or increases in the spread between the yield on our securities and the yield on U.S. Treasury securities (the “credit spread”) prior to the maturity date may adversely affect the market value of MITTS. However, because your return on MITTS depends upon factors in addition to our ability to pay our obligations, such as the value of the Market Measure, an improvement in our credit ratings will not reduce the other investment risks related to MITTS.

Valuation- and Market-related Risks

Our initial estimated value of MITTS will be lower than the public offering price of MITTS. The public offering price of MITTS will exceed our initial estimated value because costs associated with selling and structuring MITTS, as well as hedging MITTS, are included in the public offering price of MITTS.

Our initial estimated value does not represent future values of MITTS and may differ from others’ estimates. Our initial estimated value is only an estimate, which will be determined by reference to our internal pricing models when the terms of MITTS are set. This estimated value will be based on market conditions and other relevant factors existing at that time, our internal funding rate on the pricing date and our assumptions about market parameters, which can include volatility, dividend rates, interest rates and other factors. Different pricing models and assumptions could provide valuations for MITTS that are greater or less than our initial estimated value. In addition, market conditions and other relevant factors in the future may change, and any assumptions may prove to be incorrect. On future dates, the market value of MITTS could change significantly based on, among other things, changes in market conditions, including the value of the Market Measure, our creditworthiness, interest rate movements and other relevant factors, which may impact the price at which BofAS or any other party would be willing to buy MITTS from you in any secondary market transactions. Our estimated value does not represent a minimum price at which BofAS or any other party would be willing to buy your MITTS in any secondary market (if any exists) at any time.

PS-7

Our initial estimated value of MITTS will not be determined by reference to credit spreads for our conventional fixed-rate debt. The internal funding rate to be used in the determination of our initial estimated value of MITTS generally represents a discount from the credit spreads for our conventional fixed-rate debt. The discount is based on, among other things, our view of the funding value of MITTS as well as the higher issuance, operational and ongoing liability management costs of MITTS in comparison to those costs for our conventional fixed-rate debt. If we were to use the interest rate implied by our conventional fixed-rate debt, we would expect the economic terms of MITTS to be more favorable to you. Consequently, our use of an internal funding rate for market-linked notes would have an adverse effect on the economic terms of MITTS, the initial estimated value of MITTS on the pricing date and any secondary market prices of MITTS.

We cannot assure you that there will be a trading market for your MITTS. If a secondary market exists, we cannot predict how MITTS will trade, or whether that market will be liquid or illiquid. The development of a trading market for MITTS will depend on various factors, including our financial performance and changes in the value of the Market Measure. The number of potential buyers of your MITTS in any secondary market may be limited. There is no assurance that any party will be willing to purchase your MITTS at any price in any secondary market.

We anticipate that one or more of the agents or their affiliates will act as a market-maker for MITTS, but none of them is required to do so and may cease to do so at any time. Any price at which an agent or its affiliates may bid for, offer, purchase, or sell any MITTS may be higher or lower than the applicable public offering price, and that price may differ from the values determined by pricing models that it may use, whether as a result of dealer discounts, mark-ups, or other transaction costs. These bids, offers, or transactions may adversely affect the prices, if any, at which those MITTS might otherwise trade in the market. In addition, if at any time any entity were to cease acting as a market-maker for any issue of MITTS, it is likely that there would be significantly less liquidity in that secondary market. In such a case, the price at which those MITTS could be sold would likely be lower than if an active market existed.

Unless otherwise stated in the applicable term sheet, we will not list MITTS on any securities exchange. Even if an application were made to list your MITTS, we cannot assure you that the application will be approved or that your MITTS will be listed and, if listed, that they will remain listed for their entire term. The listing of MITTS on any securities exchange will not necessarily ensure that a trading market will develop, and if a trading market does develop, that there will be liquidity in the trading market.

If you attempt to sell MITTS prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount and the Minimum Redemption Amount. MITTS are not designed to be short-term trading instruments. The Minimum Redemption Amount will only apply if you hold MITTS to maturity. You have no right to have your MITTS redeemed prior to maturity. If you wish to liquidate your investment in MITTS prior to maturity, your only option would be to sell them. At that time, there may be an illiquid market for your MITTS or no market at all. Even if you were able to sell your MITTS, there are many factors outside of our control that may affect their market value, some of which, but not all, are stated below. These factors may interact with each other in complex and unpredictable ways, and the impact of any one factor may be offset or magnified by the effect of another factor. The following paragraphs describe a specific factor’s expected impact on the market value of MITTS, assuming all other conditions remain constant.

| · | Value of the Market Measure. We anticipate that the market value of MITTS prior to maturity generally will depend to a significant extent on the value of the Market Measure. In general, it is expected that the market value of MITTS will decrease as the value of the |

PS-8

Market Measure decreases, and increase as the value of the Market Measure increases. However, as the value of the Market Measure increases, the market value of MITTS may decrease or may not increase at the same rate. If you sell your MITTS when the value of the Market Measure is less than, or not sufficiently above, the applicable Starting Value, then you may receive less than the principal amount and the Minimum Redemption Amount of your MITTS.

In addition, if a Capped Value is specified in the applicable term sheet, because the Redemption Amount for MITTS will not exceed that Capped Value, we do not expect that MITTS will trade in any secondary market at a price that is greater than the Capped Value.

| · | Volatility of the Market Measure. Volatility is the term used to describe the size and frequency of market fluctuations. The volatility of the Market Measure during the term of the MITTS may vary. In addition, an unsettled international environment and related uncertainties may result in greater market volatility, which may continue over the term of the MITTS. Increases or decreases in the volatility of the Market Measure may have an adverse impact on the market value of MITTS. Even if the value of the Market Measure increases after the applicable pricing date, if you are able to sell your MITTS before their maturity date, you may receive substantially less than the amount that would be payable at maturity based on that value because of the anticipation that the value of the Market Measure will continue to fluctuate until the Ending Value is determined. |

| · | Economic and Other Conditions Generally. The general economic conditions of the capital markets in the United States, as well as geopolitical conditions and other financial, political, public health, regulatory and judicial events, natural disasters, acts of terrorism or war, and related uncertainties that affect commodity markets generally, may adversely affect the value of the Market Measure and the market value of MITTS. If the Market Measure includes one or more components traded in one or more non-U.S. markets (a “non-U.S. Market Measure”), the value of your MITTS may also be adversely affected by similar events in the markets of the relevant foreign countries. |

| · | Interest Rates. We expect that changes in interest rates will affect the market value of MITTS. In general, if U.S. interest rates increase, we expect that the market value of MITTS will decrease. In general, we expect that the longer the amount of time that remains until maturity, the more significant the impact of these changes will be on the value of MITTS. In the case of non-U.S. Market Measures, the level of interest rates in the relevant foreign countries may also affect their economies and in turn the value of the non-U.S. Market Measure, and, thus, the market value of MITTS may be adversely affected. |

| · | Exchange Rate Movements and Volatility. If the Market Measure of your MITTS includes any non-U.S. Market Measures, changes in, and the volatility of, the exchange rates between the U.S. dollar and the relevant non-U.S. currency or currencies could have an adverse impact on the value of your MITTS, and the Redemption Amount may depend in part on the relevant exchange rates. In addition, the correlation between the relevant exchange rate and any applicable non-U.S. Market Measure reflects the extent to which a percentage change in that exchange rate corresponds to a percentage change in the applicable non-U.S. Market Measure, and changes in these correlations may have an adverse impact on the value of your MITTS. |

| · | Our Financial Condition and Creditworthiness. Our perceived creditworthiness, including any increases in our credit spreads and any actual or anticipated decreases in our credit ratings, may adversely affect the market value of MITTS. In general, we expect the longer the amount of time that remains until maturity, the more significant the |

PS-9

| impact will be on the value of MITTS. However, a decrease in our credit spreads or an improvement in our credit ratings will not necessarily increase the market value of MITTS. | ||

| · | Time to Maturity. There may be a disparity between the market value of MITTS prior to maturity and their value at maturity. This disparity is often called a time “value,” “premium,” or “discount,” and reflects expectations concerning the value of the Market Measure prior to the maturity date. As the time to maturity decreases, this disparity will likely decrease, such that the market value of MITTS will approach the expected Redemption Amount to be paid at maturity. |

Conflict-related Risks

Trading and hedging activities by us, the agents, and our respective affiliates may affect your return on MITTS and their market value. We, the agents, and our respective affiliates may buy or sell the commodities represented by or included in the Market Measure, futures or options contracts or exchange-traded instruments on the Market Measure or its components, or other listed or over-the counter derivative instruments whose value is derived from the Market Measure or its components. We, the agents, or our respective affiliates may execute such purchases or sales for our own or their own accounts, for business reasons, or in connection with hedging our obligations under MITTS. These transactions could adversely affect the value of these components and, in turn, the value of a Market Measure in a manner that could be adverse to your investment in MITTS. On or before the applicable pricing date, any purchases or sales by us, the agents and our respective affiliates, or others on our or their behalf (including those for the purpose of hedging some or all of our anticipated exposure in connection with MITTS), may increase the value of the Market Measure or its components. Consequently, the value of that Market Measure or the components included in that Market Measure may decrease subsequent to the pricing date of an issue of MITTS, which may adversely affect the market value of MITTS.

We, the agents, or one or more of our respective affiliates expect to also engage in hedging activities that could increase the value of the Market Measure on the applicable pricing date. In addition, these activities, including the unwinding of a hedge, may decrease the market value of your MITTS prior to maturity, including during the Maturity Valuation Period, and may reduce the Redemption Amount. We, the agents, or one or more of our respective affiliates may purchase or otherwise acquire a long or short position in MITTS, and may hold or resell MITTS. For example, the agents may enter into these transactions in connection with any market making activities in which they engage. We cannot assure you that these activities will not adversely affect the value of the Market Measure, the market value of your MITTS prior to maturity or the Redemption Amount.

Our trading, hedging and other business activities, and those of the agents or one or more of our respective affiliates, may create conflicts of interest with you. We, the agents, or one or more of our respective affiliates may engage in trading activities related to the Market Measure and to components included in the Market Measure (and related futures and options contracts on the Market Measure or its components) that are not for your account or on your behalf. We, the agents, or one or more of our respective affiliates also may issue or underwrite other financial instruments with returns based upon the applicable Market Measure or its components. In addition, in the ordinary course of their business activities, the agents or their affiliates may hold and trade our or our affiliates’ debt and equity securities (or related derivative securities) and financial instruments (including bank loans) for their own account and for the accounts of their customers. Certain of the agents or their affiliates may also have a lending or other financial relationship with us. In order to hedge such exposure, the agents or their affiliates may enter into transactions such as the purchase of credit default swaps or the creation of short positions in our or our affiliates’ securities, including potentially

PS-10

MITTS. Any such short positions could adversely affect future trading prices of MITTS. These trading and other business activities may present a conflict of interest between your interest in MITTS and the interests we, the agents and our respective affiliates may have in our proprietary accounts, in facilitating transactions, including block trades, for our or their customers, and in accounts under our or their management. These trading and other business activities, if they influence the value of the Market Measure or secondary trading in your MITTS, could be adverse to your interests as a beneficial owner of MITTS.

We, the agents, and our respective affiliates expect to enter into arrangements or adjust or close out existing transactions to hedge our obligations under MITTS. We, the agents, or our respective affiliates also may enter into hedging transactions relating to other securities or instruments that we or they issue, some of which may have returns calculated in a manner related to that of a particular issue of MITTS. We may enter into such hedging arrangements with one or more of our subsidiaries or affiliates, or with one or more of the agents or their affiliates. Such a party may enter into additional hedging transactions with other parties relating to MITTS and the applicable Market Measure. This hedging activity is expected to result in a profit to those engaging in the hedging activity, which could be more or less than initially expected, but could also result in a loss. We, the agents, and our respective affiliates will price these hedging transactions with the intent to realize a profit, regardless of whether the value of MITTS increases or decreases or whether the Redemption Amount on MITTS is more or less than the principal amount of MITTS. Any profit in connection with such hedging activities will be in addition to any other compensation that we, the agents, and our respective affiliates receive for the sale of MITTS, which creates an additional incentive to sell MITTS to you.

There may be potential conflicts of interest involving the calculation agent. We have the right to appoint and remove the calculation agent. We expect to appoint BofAS or one of its affiliates as the calculation agent for MITTS and, as such, it will determine the Starting Value, the Ending Value, and the Redemption Amount. As the calculation agent, BofAS or one of its affiliates will have discretion in making various determinations that affect your MITTS. The exercise of this discretion by the calculation agent could adversely affect the value of your MITTS and may present the calculation agent with a conflict of interest of the kind described under “—Trading and hedging activities by us, the agents, and our respective affiliates may affect your return on MITTS and their market value” and “—Our trading, hedging and other business activities, and those of the agents or one or more of our respective affiliates, may create conflicts of interest with you” above.

Market Measure-related Risks

You must rely on your own evaluation of the merits of an investment linked to the applicable Market Measure. In the ordinary course of business, we, the agents, and our respective affiliates may have expressed views on expected movements in a Market Measure or the components included in the Market Measure, and may do so in the future. These views or reports may be communicated to our clients and clients of these entities. However, these views are subject to change from time to time. Moreover, other professionals who deal in markets relating to a Market Measure may at any time have significantly different views from our views and the views of these entities. For these reasons, you are encouraged to derive information concerning a Market Measure and its components from multiple sources, and you should not rely on our views or the views expressed by these entities.

Ownership of MITTS will not entitle you to any rights with respect to any commodities or futures contracts represented by or included in the Market Measure. You will not own or have any beneficial or other legal interest in any of the commodities or futures contracts represented by or included in the Market Measure. We will not invest in any of the

PS-11

commodities or futures contracts represented by or included in that Market Measure for your benefit.

The prices of commodities or futures contracts represented by or included in the Market Measure may change unpredictably, affecting the value of your MITTS in unforeseeable ways. Trading in commodities and futures contracts is speculative and can be extremely volatile. Their market prices may fluctuate rapidly based on numerous factors, including: changes in supply and demand relationships; liquidity; weather conditions and natural disasters; trends in agriculture; trade; fiscal, monetary, and exchange control programs; national and international political, military, public health and economic events and policies; disease or pestilence; technological developments; changes in interest rates, whether through governmental action or market movements; currency exchange rates; volatility from speculative activities; the development, availability and/or decrease in price of substitutes; monetary and other governmental policies, action and inaction; macroeconomic or geopolitical and military events, including political instability in some oil-producing countries or other countries in which the production of particular commodities may be concentrated; and natural or nuclear disasters. These factors may adversely affect the value of a Market Measure or its components in varying ways, and different factors may cause the levels and volatilities of commodity prices to move in inconsistent directions at inconsistent rates. A physical commodity futures contract (which may be a component of a commodity index) may decrease to zero or a negative price, which would adversely affect the value of your MITTS. The prices of physical commodities, including the commodities underlying the Market Measure or a Basket Component, can fluctuate widely due to supply and demand disruptions in major producing or consuming regions. Additionally, certain Market Measures may be concentrated in only a few, or even a single industry (e.g., energy). These Market Measures are likely to be more volatile than those that represent a broad base of commodities.

If the liquidity of the components of a Market Measure is limited, the value of MITTS may be adversely affected. Commodities and derivatives contracts on commodities may be difficult to buy or sell, particularly during adverse market conditions. Reduced liquidity would likely have an adverse effect on the value of the Market Measure and, therefore, on the return, if any, on your MITTS. Limited liquidity relating to the components of a Market Measure may also result in its publisher being unable to determine its value using its normal means. The resulting discretion by the publisher of a Market Measure in determining the value could adversely affect the value of MITTS.

Suspension or disruptions of market trading in the applicable commodities and related futures contracts may adversely affect the value of MITTS. The commodity markets are subject to disruptions due to various factors, including the lack of liquidity in the markets, the participation of speculators and government regulation and intervention. In addition, U.S. futures exchanges and some foreign exchanges have regulations that limit the amount of fluctuation in futures contract prices that may occur during a single business day. These limits are generally referred to as “daily price fluctuation limits,” and the maximum or minimum price of a contract on any given day as a result of these limits is referred to as a “limit price.” Once the limit price has been reached in a particular contract, no trades may be made at a different price. Limit prices have the effect of precluding trading in a particular contract or forcing the liquidation of contracts at disadvantageous times or prices. Any such disruption, or any other force majeure (such as an act of God, fire, flood, severe weather conditions, act of governmental authority, labor difficulty, etc.), could have an adverse effect on the value of or trading in the Market Measure, or the manner in which it is calculated, and therefore, the value of MITTS.

Changes in exchange methodology may adversely affect the value of MITTS prior to maturity. The value of a Market Measure will be determined by reference to fixing prices, spot prices, or related futures contracts of the commodities represented by or included in a

PS-12

Market Measure or Basket Component, as determined by the applicable exchange or as otherwise set forth in the applicable term sheet. An exchange may from time to time change its rules or take extraordinary actions under its rules, which could adversely affect the prices of the applicable commodities or futures contracts, which could reduce the value of the Market Measure and the value of MITTS.

In addition, some fixing prices or spot prices are derived from a principals’ market, which operates as an over the counter (“OTC”) physical commodity market. Although market-making members of principals’ markets are typically supervised by regulating entities, the principals’ markets themselves are not regulated. If any tax or other form of regulation should affect the members of the relevant principals’ market, the role of the principals’ market as a benchmark for the applicable commodity may be affected.

Legal and regulatory changes could adversely affect the return on and value of your MITTS. The value of the underlying commodities or futures contracts could be adversely affected by new laws or regulations or by the reinterpretation of existing laws or regulations (including, without limitation, those related to taxes and duties on commodities and futures contracts) by one or more governments, courts, or other official bodies.

In the U.S., the regulation of commodity transactions is subject to ongoing modification by governmental and judicial action. For example, the U.S. Commodity Futures Trading Commission (“CFTC”) has interpreted the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”), which was enacted in July 2010, to require the CFTC to impose limits on the size of positions that can be held by market participants in futures contracts and OTC derivatives on certain physical commodities. The CFTC adopted final position limits rules in October 2020; the final rules became effective in March 2021 and are in the process of being phased in. While the ultimate effect of the final position limit rules are not yet known, these limits will likely restrict the ability of many market participants to trade in the commodities markets to the same extent as they have in the past, including affecting their ability to enter into or maintain hedge positions in the applicable commodity or futures contracts. These rules and various other legislative and regulatory requirements may, among other things, reduce liquidity, increase market volatility, and increase costs in these markets. These consequences could adversely affect the applicable Market Measure and the value of your MITTS.

In addition, other governmental or regulatory bodies (such as the European Commission) have proposed or may propose in the future legislation or regulations containing restrictions similar to those contemplated by Dodd-Frank, or other legislation or regulations containing other restrictions that could adversely impact the liquidity of and increase costs of participating in the commodities markets. If such legislation or regulations are adopted or other legislation or regulations are adopted in the future, they could have an adverse effect on the value of the applicable Market Measure and your MITTS.

MITTS will not be regulated by the CFTC. Unlike an investment in MITTS, an investment in a collective investment vehicle that invests in futures contracts on behalf of its participants may be regulated as a commodity pool and its operator may be required to be registered with and regulated by the CFTC as a “commodity pool operator” (a “CPO”). Because MITTS will not be interests in a commodity pool, MITTS will not be regulated by the CFTC as a commodity pool, we will not be registered with the CFTC as a CPO, and you will not benefit from the CFTC’s or any non-U.S. regulatory authority’s regulatory protections afforded to persons who trade in futures contracts or who invest in regulated commodity pools. MITTS will not constitute investments by you or by us on your behalf in futures contracts traded on regulated futures exchanges, which may only be transacted through a person registered with the CFTC as a “futures commission merchant” (“FCM”). We are not registered with the CFTC as an FCM, and you will not benefit from the CFTC’s or any other non-U.S. regulatory authority’s

PS-13

regulatory protections afforded to persons who trade in futures contracts on a regulated futures exchange through a registered FCM.

A Market Measure may include commodities or futures contracts traded on foreign exchanges that are less regulated than U.S. markets and may involve different and greater risks than trading on U.S. exchanges. A Market Measure or Basket Component may include commodities or futures contracts that trade on exchanges located outside the U.S. The regulations of the CFTC do not apply to trading on foreign exchanges, and trading on foreign exchanges may involve different and greater risks than trading on U.S. exchanges. Certain foreign markets may be more susceptible to disruption than U.S. exchanges due to the lack of a government-regulated clearinghouse system. Trading on foreign exchanges also involves certain other risks that are not applicable to trading on U.S. exchanges. Those risks include: (a) exchange rate risk relative to the U.S. dollar; (b) exchange controls; (c) expropriation; (d) burdensome or confiscatory taxation; and (e) moratoriums, and political or diplomatic events. It may also be more costly and difficult for participants in those markets to enforce the laws or regulations of a foreign country or exchange, and it is possible that the foreign country or exchange may not have laws or regulations which adequately protect the rights and interests of investors in the relevant commodities or contracts. These factors could reduce the value of the applicable Market Measure and the value of MITTS.

An investment linked to commodity futures contracts is not equivalent to an investment linked to the spot prices of physical commodities. The price of a futures contract reflects the expected value of the commodity upon delivery in the future, whereas the price of a physical commodity reflects the value of such commodity upon immediate delivery, which is referred to as the spot price. Several factors can result in differences between the price of a commodity futures contract and the spot price of a commodity, including the cost of storing such commodity for the length of the futures contract, interest costs related to financing the purchase of such commodity, and expectations of supply and demand for such commodity. While the changes in the price of a futures contract are usually correlated with the changes in the spot price, such correlation is not exact. In some cases, the performance of a commodity futures contract can deviate significantly from the spot price performance of the related underlying commodity, especially over longer periods of time. Accordingly, investments linked to the return of commodities futures contracts may underperform similar investments that reflect the spot price return on physical commodities.

If a Market Measure includes a commodity index, future prices of the commodities included in that index that are different from their current prices may have a negative effect on the level of that index, and therefore the value of MITTS. A Market Measure may include a commodity index. Commodity indices generally reflect movements in commodity prices by measuring the value of futures contracts for the applicable commodities, not the change in the spot price of the actual physical commodity to which such futures contracts relate. To maintain the index, as futures contracts approach expiration, they are replaced by similar contracts that have a later expiration. For example, a futures contract purchased and held in August may specify an October expiration date. As time passes, the contract expiring in October may be replaced by a contract for delivery in December. This process is referred to as “rolling.” The level of the index is calculated as if the expiring futures contracts are sold and the proceeds from those sales are used to purchase longer-dated futures contracts. The difference in the price between the contracts that are sold and the new contracts for more distant delivery that are purchased is called “roll yield,” and the change in price that contracts experience while they are components of the index is sometimes referred to as “spot return.”

PS-14

If the expiring futures contract included in the index is “rolled” into a less expensive futures contract with a more distant delivery date, the market for that futures contract is (putting aside other considerations) trading in “backwardation.” In the example above, the purchase of the December contract would take place at a price that is lower than the sale price of the October contract. In this case, the effect of the roll yield on the level of the applicable index will be positive because it costs less to replace the expiring futures contract. However, if the expiring futures contract included in the index is “rolled” into a more expensive futures contract with a more distant delivery date, the market for that futures contract is trading in “contango.” This would occur, for example, if the purchase of the December contract took place at a price that is higher than the sale price of the October contract. In this case, the effect of the roll yield on the level of the index will be negative because it will cost more to replace the expiring futures contract.

There is no indication that the markets for any specific commodity will consistently be in backwardation or that there will be a positive roll yield that increases the level of any applicable index. It is possible, when near-term or spot prices of the constituent commodities are decreasing, for the level of that index to decrease significantly over time even when some or all of the constituent commodities are experiencing backwardation. If all other factors remain constant, the presence of contango in the market for a commodity included in an index could generally result in negative roll yield, even when the near-term or spot prices of the constituent commodities are stable or increasing, which could decrease the level of that index and the market value of MITTS.

The publisher of an index may adjust that index in a way that affects its level, and the publisher has no obligation to consider your interests. If the Market Measure consists of a commodity index, unless otherwise specified in the term sheet, we have no affiliation with the publisher of that index (the “Index Publisher”). The composition of a commodity index may change over time as additional commodities satisfy the eligibility criteria or commodities or futures contracts currently included in that index fail to satisfy such criteria. The weighting factors applied to each commodity included in an index may change over time, based on changes in commodity prices, commodity forward curves, production statistics, or other factors. An Index Publisher can add, delete, or substitute the components included in that index or make other methodological changes that could change its level. A new component included in an index may perform significantly better or worse than the replaced component, and the performance will impact the level of the applicable index. Additionally, an Index Publisher may alter, discontinue, or suspend calculation or dissemination of an index. Any of these actions could adversely affect the value of the Market Measure and, consequently, the market value of your MITTS. No Index Publisher will have any obligation to consider your interests in calculating or revising any index. See “Description of MITTS —Adjustments to a Market Measure” and “—Discontinuance of a Market Measure.”

We are not responsible for the actions or public disclosure of information of any principals’ market or exchange on which a Market Measure trades. None of us, the selling agents or any of our respective affiliates is responsible for the adequacy or accuracy of the prices determined by these entities relating to the Market Measure. You should make your own investigation into the applicable Market Measure and how it is traded. None of the principals’ markets or any exchange on which a Market Measure or component trades will be involved in any offering of MITTS in any way and none of them has any obligation to consider your interests in taking any actions that might affect the value of MITTS.

Exchange rate movements may adversely impact the value of MITTS. If any component included in an index is traded in a currency other than U.S. dollars and, for purposes of calculating the level of that index, is converted into U.S. dollars, then the level of that index may depend in part on the relevant exchange rates. If the value of the U.S. dollar strengthens against the currencies of that index, the level of the applicable index may be

PS-15

adversely affected and the Redemption Amount may be reduced. Exchange rate movements may be particularly impacted by existing and expected rates of inflation and interest rate levels; political, civil, or military unrest; the balance of payments between countries; and the extent of governmental surpluses or deficits in the relevant countries and the United States. All of these factors are in turn sensitive to the monetary, fiscal, and trade policies pursued by the governments of those countries and the United States and other countries important to international trade and finance.

Other Risk Factors Relating to the Applicable Market Measure

The applicable term sheet may set forth additional risk factors as to the Market Measure that you should review prior to purchasing MITTS.

Tax-related Risks

You may be required to include income on MITTS over their term for tax purposes, even though you will not receive any payments until maturity. MITTS are considered to be issued with original issue discount. You will be required to include income on MITTS over their term based upon a comparable yield, even though you will not receive any payments until maturity. You are urged to review the section entitled “U.S. Federal Income Tax Summary” and consult your own tax advisor.

The U.S. federal income tax consequences of an investment in MITTS are uncertain, and may be adverse to a holder of MITTS. No statutory, judicial, or administrative authority directly addresses the characterization of MITTS or securities similar to MITTS for U.S. federal income tax purposes. As a result, significant aspects of the U.S. federal income tax consequences of an investment in MITTS are not certain. We intend to treat MITTS as debt instruments for U.S. federal income tax purposes. Accordingly, you should consider the tax consequences of investing in MITTS, aspects of which are uncertain. See the section entitled “U.S. Federal Income Tax Summary.”

You are urged to consult with your own tax advisor regarding all aspects of the U.S. federal income tax consequences of investing in MITTS.

PS-16

DESCRIPTION OF MITTS

General

Each issue of MITTS will be part of a series of medium-term notes entitled “Senior Global Medium-Term Notes” that will be issued under the indenture, as amended and supplemented from time to time. The indenture is described more fully in the prospectus and prospectus supplement. The following description of MITTS supplements and, to the extent it is inconsistent with, supersedes the description of the general terms and provisions of the notes and debt securities set forth under the headings “Description of the Notes We May Offer” in the prospectus supplement and “Description of Senior Debt Securities” in the prospectus. These documents should be read in connection with the applicable term sheet.

The maturity date of MITTS and the aggregate principal amount of each issue of MITTS will be stated in the applicable term sheet. If the scheduled maturity date is not a business day, we will make the required payment on the next business day, and no interest will accrue as a result of such delay. A “business day” means a Monday, Tuesday, Wednesday, Thursday or Friday that is neither a legal holiday nor a day on which banking institutions are authorized or required by law or executive order to close in New York City.

We will not pay interest on MITTS. Depending on the terms of MITTS, they may not provide for the full return of principal at maturity. MITTS will be payable only in U.S. dollars.

Prior to the maturity date, MITTS are not redeemable at our option or repayable at the option of any holder. MITTS are not subject to any sinking fund. MITTS are not subject to the defeasance provisions described in the section “Description of Senior Debt Securities—Defeasance” beginning on page 8 of the accompanying prospectus.

We will issue MITTS in denominations of whole units. Unless otherwise set forth in the applicable term sheet, each unit will have a principal amount of $10. The CUSIP number for each issue of MITTS will be set forth in the applicable term sheet. You may transfer MITTS only in whole units.

Payment at Maturity

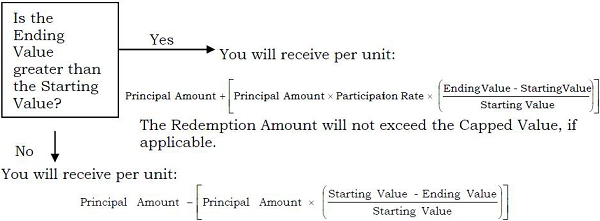

At maturity, subject to our credit risk as issuer of MITTS, you will receive a Redemption Amount, denominated in U.S. dollars. Unless otherwise specified in the applicable term sheet, the “Redemption Amount” will be calculated as follows:

| · | If the Ending Value is greater than the Starting Value, then the Redemption Amount will equal: |

If so specified in the applicable term sheet, the Redemption Amount will not exceed the “Capped Value” set forth in the applicable term sheet.

| · | If the Ending Value is equal to or less than the Starting Value, then the Redemption Amount will equal: |

PS-17

The Redemption Amount will not be less than the Minimum Redemption Amount per unit.

The “Participation Rate” will generally be greater than or equal to 100%, unless otherwise set forth in the applicable term sheet. If the applicable term sheet specifies that the Participation Rate is 100%, your participation in any upside performance of the Market Measure will not be leveraged.

The “Minimum Redemption Amount” may be less than or equal to the principal amount, as specified in the applicable term sheet. If the Minimum Redemption Amount is less than the principal amount and the Ending Value is less than the Starting Value, you will lose a portion of your investment in MITTS.

Each term sheet will provide examples of Redemption Amounts based on a range of hypothetical Ending Values.

The applicable term sheet will set forth information as to the specific Market Measure, including information as to the historical values of the Market Measure. However, historical values of the Market Measure are not indicative of its future performance or the performance of your MITTS.

An investment in MITTS does not entitle you to any ownership interest in any commodities or futures contracts that are represented by or included in a Market Measure.

The Starting Value and the Ending Value

Starting Value

Unless otherwise specified in the applicable term sheet, the “Starting Value” will be the closing value of the Market Measure on the pricing date.

If the Market Measure consists of a Basket, the Starting Value will be equal to 100. See “—Basket Market Measures.”

Ending Value

Unless otherwise specified in the applicable term sheet, the “Ending Value” will equal the average of the closing value of the Market Measure on each calculation day during the Maturity Valuation Period.

The “Maturity Valuation Period” means the period consisting of one or more calculation days shortly before the maturity date. The timing and length of the period will be set forth in the applicable term sheet.

A “calculation day” means any scheduled Market Measure Business Day during the Maturity Valuation Period.

Unless otherwise specified in the applicable term sheet, a “Market Measure Business Day” means a day on which the index level, spot price or official settlement price (as applicable) for the applicable Market Measure is determined and published by the applicable index sponsor, commodities exchange, or other price source (or any successor thereto) described in the applicable term sheet.

If the Market Measure consists of a Basket, the Ending Value of the Basket will be determined as described in “—Basket Market Measures.”

PS-18

Market Disruption Events

Unless otherwise set forth in the applicable term sheet, a “Market Disruption Event” for a Market Measure, a Basket Component or an index component means any of the following events, as determined by the calculation agent in its sole discretion:

| (1) | a material limitation, suspension, or disruption of trading in a Market Measure, a Basket Component or in one or more index components which results in a failure by the exchange on which the Market Measure, each applicable Basket Component or index component is traded to report an exchange published settlement price for such contract on the day on which such event occurs or any succeeding day on which it continues; | |

| (2) | the exchange published settlement price for the Market Measure, Basket Component or any index component is a “limit price,” which means that the exchange published settlement price for such contract for a day has increased or decreased from the previous day’s exchange published settlement price by the maximum amount permitted under applicable exchange rules; | |

| (3) | failure by the applicable exchange to announce or publish the exchange published settlement price for the Market Measure, Basket Component or any index component; | |

| (4) | a suspension of trading in the Market Measure, Basket Component or one or more index components, for which the trading does not resume at least 10 minutes prior to the scheduled or rescheduled closing time; or | |

| (5) | any other event, if the calculation agent determines in its sole discretion that the event materially interferes with our ability or the ability of any of our affiliates to unwind all or a material portion of a hedge that we, the agents or any of our respective affiliates has effected or may effect as to the applicable MITTS. |

Starting Value

Market Measure That Is a Commodity or Futures Contract

For a Market Measure that is a commodity or futures contract, if the scheduled pricing date is determined by the calculation agent not to be a Market Measure Business Day by reason of an extraordinary event, occurrence, declaration, or otherwise (a “non-Market Measure Business Day”), or if there is a Market Disruption Event on that day, the pricing date will be the immediately succeeding Market Measure Business Day during which no Market Disruption Event occurs or is continuing; provided that the Starting Value will be determined (or, if not determinable, estimated) by the calculation agent in a manner which the calculation agent considers commercially reasonable under the circumstances on a date no later than the second scheduled Market Measure Business Day following the scheduled pricing date, regardless of the occurrence of a Market Disruption Event or non-Market Measure Business Day on that day.

Market Measure That Is a Commodity Index

For a Market Measure that is a commodity index, if a Market Disruption Event occurs on the scheduled pricing date with respect to any component of the index or the scheduled pricing date is determined by the calculation agent to be a non-Market Measure Business Day (each such component of the index, an “Affected Component” on the pricing date), the calculation agent will determine the Starting Value as follows:

PS-19

| (1) | With respect to each commodity or futures contract included in the index that is not an Affected Component on the scheduled pricing date, the Starting Value of the Market Measure will be based on the exchange published settlement price or other applicable price of that commodity or futures contract on the scheduled pricing date. |

| (2) | With respect to each Affected Component on the scheduled pricing date: |

| a. | The Starting Value of the Market Measure will be based on the exchange published settlement price or other applicable price of that Affected Component on the first Market Measure Business Day following the scheduled pricing date on which no Market Disruption Event occurs or is continuing with respect to that Affected Component, provided that the Starting Value will not be determined on a date later than the second scheduled Market Measure Business Day following the scheduled pricing date. If a Market Disruption Event or non-Market Measure Business Day continues to occur on the second scheduled Market Measure Business Day following the scheduled pricing date, the calculation agent will estimate on such date the price of that Affected Component to be used to determine the value of the Market Measure in a manner that it considers commercially reasonable under the circumstances. |

| b. | The final term sheet will set forth a brief statement of the facts relating to the establishment of the Starting Value (including a description of the relevant Market Disruption Event(s) or non-Market Measure Business Day). |

The calculation agent will determine the value of the Market Measure by reference to the exchange published settlement prices or other prices determined in clauses (1) and (2) above using the then current method for calculating the index. The exchange or other price source on which an applicable commodity or futures contract is traded or valued for purposes of the above definition means the exchange or other price source used to value that commodity or futures contract for the calculation of the index.

Ending Value

Market Measure That Is a Commodity or Futures Contract

For a Market Measure that is a commodity or futures contract, if (i) a Market Disruption Event occurs on a scheduled calculation day during the Maturity Valuation Period; or (ii) any scheduled calculation day is determined by the calculation agent not to be a Market Measure Business Day by reason of an extraordinary event, occurrence, declaration, or otherwise (any such day in either (i) or (ii) being a “non-calculation day”), the closing value of the Market Measure for the applicable non-calculation day will be the closing value of the Market Measure on the next calculation day that occurs during the Maturity Valuation Period. For example, if the first and second scheduled calculation days during the Maturity Valuation Period are non-calculation days, then the closing value of the Market Measure on the next calculation day will also be deemed to be the closing value for the Market Measure on the first and second scheduled calculation days during the Maturity Valuation Period. If no further scheduled calculation days occur after a non-calculation day, or if every scheduled calculation day after that non-calculation day is also a non-calculation day, then the closing value of the Market Measure for that non-calculation day and for each following non-calculation day, if any, will be determined (or, if not determinable, estimated) by the calculation agent in a manner which the calculation agent considers commercially reasonable under the circumstances on the last scheduled calculation day during the Maturity Valuation Period, although that last scheduled calculation day is a non-calculation day.

PS-20

Market Measure That Is a Commodity Index

For a Market Measure that is a commodity index, if (i) a Market Disruption Event occurs on a scheduled calculation day during the Maturity Valuation Period with respect to any component of the index; or (ii) any scheduled calculation day is determined by the calculation agent to be a non-Market Measure Business Day with respect to any component of the index (each such component of the index in either (i) or (ii) being an “Affected Component” on such calculation day), the calculation agent will determine the closing value of the Market Measure for such calculation day as follows:

| (1) | With respect to each commodity or futures contract included in the index that is not an Affected Component on such calculation day, the closing value of the Market Measure will be based on the exchange published settlement price or other applicable price of that commodity or futures contract on the scheduled calculation day. |

| (2) | With respect to an Affected Component on such calculation day, the closing value of the Market Measure will be based on the exchange published settlement price or other applicable price of that Affected Component on the first Market Measure Business Day following the scheduled calculation day on which no Market Disruption Event occurs or is continuing with respect to that Affected Component, provided that the closing value of the Market Measure will not be determined on a date later than the last scheduled calculation day during the Maturity Valuation Period. If a Market Disruption Event or non-Market Measure Business Day continues to occur on the last scheduled calculation day, the calculation agent will estimate on such date the price of that Affected Component to be used to determine the closing value of the Market Measure in a manner that it considers commercially reasonable under the circumstances, regardless of the occurrence of a Market Disruption Event or non-Market Measure Business Day on that last scheduled calculation day. |

The calculation agent will determine the value of the Market Measure by reference to the exchange published settlement prices or other prices determined in clauses (1) and (2) above using the then current method for calculating the index. The exchange or other price source on which an applicable commodity or futures contract is traded or valued for purposes of the above definition means the exchange or other price source used to value that commodity or futures contract for the calculation of the index.

Adjustments to a Market Measure

After the applicable pricing date, the relevant index sponsor, exchange or other price source for a Market Measure or a Basket Component (a “Market Measure Publisher”) may make a material change in the method of determining the value of a Market Measure or Basket Component, or in any other way that changes the Market Measure or a Basket Component, such that it does not, in the opinion of the calculation agent, fairly represent the value of the Market Measure or a Basket Component had those changes or modifications not been made. In this case, the calculation agent will, at the close of business in New York, New York, on each date that the closing value of the Market Measure or a Basket Component is to be calculated, make adjustments to the Market Measure or a Basket Component. Those adjustments will be made in good faith as necessary to arrive at a calculation of a value of the applicable Market Measure or Basket Component as if those changes or modifications had not been made, and calculate the closing value of the Market Measure or a Basket Component, as so adjusted.

PS-21

Discontinuance of a Market Measure

After the pricing date, a Market Measure Publisher may discontinue publication or determination of the Market Measure, or one or more Basket Components. The Market Measure Publisher or another entity may then publish or calculate a successor or substitute market measure that the calculation agent determines, in its sole discretion, to be comparable to that Market Measure or Basket Component (a “successor market measure”). If this occurs, the calculation agent will substitute the successor market measure and calculate the Ending Value as described above under “—The Starting Value and the Ending Value” or below under “—Basket Market Measures,” as applicable. If the calculation agent selects a successor market measure, the calculation agent will give written notice of the selection to the trustee, to us and to the holders of MITTS.

If a Market Measure Publisher discontinues publication or determination of the Market Measure or a Basket Component before the end of the Maturity Valuation Period and the calculation agent does not select a successor market measure, then on each day that would have been a calculation day, until the earlier to occur of:

| · | the determination of the Ending Value; and |

| · | a determination by the calculation agent that a successor market measure is available, |

the calculation agent will compute a substitute value for the Market Measure or that Basket Component in accordance with the procedures last used to calculate the value of the Market Measure or that Basket Component before any discontinuance as if that day were a calculation day. The calculation agent will make available to holders of MITTS information regarding those values by means of Bloomberg L.P., Thomson Reuters, a website, or any other means selected by the calculation agent in its reasonable discretion.

If a successor market measure is selected or the calculation agent calculates a value as a substitute for a Market Measure or a Basket Component as described above, the successor market measure or value will be used as a substitute for that Market Measure or Basket Component for all purposes, including for the purpose of determining whether a Market Disruption Event exists.

Notwithstanding these alternative arrangements, any modification or discontinuance of the publication of the Market Measure or any Basket Component may adversely affect trading in MITTS.

Basket Market Measures

If the Market Measure to which your MITTS are linked is a Basket, the Basket Components will be set forth in the applicable term sheet. We will assign each Basket Component a weighting (the “Initial Component Weight”) so that each Basket Component represents a percentage of the Starting Value of the Basket on the pricing date. The Basket Components may or may not have equal Initial Component Weights, as set forth in the applicable term sheet.

Determination of the Component Ratio for Each Basket Component

The “Starting Value” of the Basket will be equal to 100. We will set a fixed factor (the “Component Ratio”) for each Basket Component on the applicable pricing date, based on the weighting of that Basket Component. The Component Ratio for each Basket Component will equal:

PS-22

| · | the Initial Component Weight (expressed as a percentage) for that Basket Component, multiplied by 100; divided by |

| · | the closing value of that Basket Component on the applicable pricing date. |

Each Component Ratio will be rounded to eight decimal places.

The Component Ratios will be calculated in this way so that the Starting Value of the Basket will equal 100 on the applicable pricing date. The Component Ratios will not be revised subsequent to their determination on the applicable pricing date, except that the calculation agent may in its good faith judgment adjust the Component Ratio of any Basket Component in the event that Basket Component is materially changed or modified in a manner that does not, in the opinion of the calculation agent, fairly represent the value of that Basket Component had those material changes or modifications not been made.

The following table is for illustration purposes only, and does not reflect the actual composition, Initial Component Weights, or Component Ratios, all of which will be set forth in the applicable term sheet.

Example: The hypothetical Basket Components are Commodity ABC, Commodity XYZ, and Commodity RST, with their Initial Component Weights being 50.00%, 25.00% and 25.00%, respectively, on a hypothetical pricing date:

|

Basket Component |

Initial |

Hypothetical |

Hypothetical |

Initial Basket |

| Commodity ABC | 50.00% | 500.00 | 0.10000000 | 50.00 |

| Commodity XYZ | 25.00% | 2,420.00 | 0.01033058 | 25.00 |