Form 424B2 ROYAL BANK OF CANADA

Tweet

Tweet Share

Share

|

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-259205

|

||

|

Preliminary Pricing Supplement

Subject to Completion

Dated May 17, 2022 To the Product Prospectus Supplement FIN-1 Dated September 14, 2021, and the Prospectus and Prospectus Supplement, each dated September 14,

2021

|

$______

SOFR ICE Swap Rate Floating RateNotes, Due May 20, 2025

Royal Bank of Canada

|

||

Royal Bank of Canada is offering the SOFR ICE Swap Rate Floating Rate Notes (the “Notes”) described in this document.

The CUSIP number for the Notes is 78014REP1.

The Notes will pay interest quarterly on February 20, May 20, August 20 and November 20 of each year, commencing on August 20, 2022, and ending on the Maturity

Date.

The Notes will accrue interest at a per annum rate equal to the Reference Rate plus a Spread of 0.00% during the term of the Notes, subject to a Coupon Floor of

3.15% per annum. The “Reference Rate” is the 2 Year U.S. Dollar SOFR ICE Swap Rate.

The Notes will not be listed on any securities exchange.

Investing in the Notes involves a number of risks. See “Additional Risk Factors” on page P-6 of this pricing supplement, “Additional Risk Factors Specific to the

Notes” beginning on page PS-5 of the product prospectus supplement FIN-1 dated September 14, 2021 and “Risk Factors” on page S-2 of the prospectus supplement dated September 14, 2021.

The Notes will not constitute deposits insured by the Canada Deposit Insurance Corporation, the U.S. Federal Deposit Insurance Corporation or any other Canadian or

U.S. government agency or instrumentality. The Notes are not subject to conversion into our common shares under subsection 39.2(2.3) of the Canada Deposit Insurance Corporation Act.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or determined that

this pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The initial estimated value of the Notes as of the Pricing Date is expected to be between $985 and $1,000 per $1,000 in principal amount, and will be less than the

price to the public. The final pricing supplement relating to the Notes will set forth our estimate of the initial value of the Notes as of the Pricing Date. The actual value of the Notes at any time will reflect many factors, cannot be predicted

with accuracy, and may be less than this amount. We describe our determination of the initial estimated value in more detail below.

The Notes will initially be offered to investors at a price equal to 100% of their principal amount. RBC Capital Markets, LLC will purchase the Notes from us on

the issue date at purchase prices that are expected to be between 99.50% and 100% of the principal amount. See “Supplemental Plan of Distribution (Conflicts of Interest)” below.

We will deliver the Notes in book-entry only form through the facilities of The Depository Trust Company on or about May 20, 2022, against payment in immediately available funds.

RBC Capital Markets, LLC

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

SUMMARY

The information in this “Summary” section is qualified by the more detailed information set forth in this pricing supplement, the product prospectus supplement

FIN-1, the prospectus supplement, and the prospectus.

|

Issuer:

|

Royal Bank of Canada (“Royal Bank”)

|

|

Underwriter:

|

RBC Capital Markets, LLC

|

|

Currency:

|

U.S. Dollars

|

|

Minimum Investment:

|

$1,000 and minimum denominations of $1,000 in excess of $1,000

|

|

Pricing Date:

|

May 18, 2022

|

|

Issue Date:

|

May 20, 2022

|

|

Maturity Date:

|

May 20, 2025

|

|

Interest Rate:

|

The Notes will bear interest at a per annum rate equal to the Reference Rate plus the Spread, subject to the Coupon Floor.

|

|

Spread:

|

0.00%

|

|

Reference Rate:

|

The 2-Year U.S. Dollar SOFR ICE Swap Rate, which is the rate for U.S. dollar swaps with a designated maturity of two years, referencing the Secured Overnight Financing Rate

(“SOFR”), compounded in arrears for 12 months using standard market conventions.

The Calculation Agent will determine the Reference Rate based on the rate that appears on the Bloomberg Screen USISSO02 Page, at approximately 11:00 a.m., New York City

time, on the applicable Interest Determination Date, provided that, if no such rate appears on the applicable Bloomberg Screen Page on that day at approximately 11:00 a.m., New York City time, then the Calculation Agent, after consulting

such sources as it deems comparable to the foregoing display page, or any such source it deems reasonable from which to estimate the relevant rate for U.S. dollar swaps referencing SOFR, will determine the applicable Reference Rate for that

day in its sole discretion.

“Bloomberg Screen USISSO02 Page” means the display designated as Bloomberg screen “USISSO02”, or such other page as may replace that Bloomberg screen on that service or

such other service or services as may be selected for the purpose of displaying rates for U.S. dollar swaps referencing SOFR by ICE Benchmark Administration Limited (“IBA”) or its successor or such other entity that assumes the

responsibility of IBA or its successor in calculating rates for U.S. dollar swaps referencing SOFR if IBA or its successor ceases to do so.

|

|

Coupon Floor:

|

3.15% per annum.

|

|

Day Count Fraction:

|

Interest will be calculated on an 30/360 basis.

|

|

Interest Payment

Dates:

|

Quarterly, on February 20, May 20, August 20 and November 20 of each year, commencing on August 20, 2022 and ending on the Maturity Date. If an Interest Payment Date falls

on a day that is not a business day in New York City, that Interest Payment Day will be postponed to the next day that is such a business day, with the same effect as if paid on the original due date.

|

|

Interest Period:

|

Each period from, and including, an Interest Payment Date (or, for the first period, the issue date) to, but excluding, the next following Interest Payment Date.

|

|

Interest Determination

|

Five U.S. Government Securities Business Days prior to the beginning of each interest

|

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

|

Dates:

|

period. A “U.S. Government Securities Business Day” is any day except for a Saturday, a Sunday, or a day on which the Securities Industry and Financial Markets Association (or any successor thereto) recommends that the fixed income departments of its members be closed for the entire day for purposes of trading in U.S. government securities. |

|

Unavailability of the

Reference Rate:

|

Notwithstanding the provisions set forth under "—Reference Rate" above:

(i) if the Calculation Agent determines in its sole discretion on or prior to the relevant Interest Determination Date that the relevant rate for U.S. dollar swaps

referencing SOFR has been discontinued or that rate has ceased to be published permanently or indefinitely, then the Calculation Agent will use as the applicable Reference Rate for that day a substitute or successor rate that it has

determined in its sole discretion to be a commercially reasonable replacement rate; and

(ii) if the Calculation Agent has determined a substitute or successor rate in accordance with the foregoing, the Calculation Agent may determine in its sole discretion, to

adjust the definitions of business day and Interest Determination Date and any other relevant methodology for calculating that substitute or successor rate, including any adjustment factor, spread and/or formula it determines is needed to

make that substitute or successor rate comparable to the relevant rate for U.S. dollar swaps referencing SOFR, in a manner that it determines to be consistent with industry-accepted practices for that substitute or successor rate.

|

|

Redemption:

|

Not Applicable.

|

|

Survivor’s Option:

|

Not Applicable.

|

|

Calculation Agent:

|

RBC Capital Markets, LLC

|

|

Listing:

|

The Notes will not be listed on any securities exchange.

|

|

Clearance and

Settlement:

|

DTC global (including through its indirect participants Euroclear and Clearstream, Luxembourg as described under “Ownership and Book-Entry Issuance” in the prospectus dated

September 14, 2021).

|

|

U.S. Tax Treatment:

|

In the opinion of our special U.S. tax counsel, Ashurst LLP, it would generally be reasonable to treat a Note with terms described herein, and we intend to take the

position that a Note will be treated, as a variable rate debt instrument for U.S. federal income tax purposes. The terms of the Notes require a holder (in the absence of a change in law or an administrative or judicial ruling to the

contrary) to treat the Notes for all tax purposes in accordance with such characterization. However, the U.S. federal income tax consequences of your investment in the Notes are uncertain and the IRS could assert that a Note with terms

described herein should be taxed in a manner that is different from that described in the preceding sentence, for example as a contingent payment debt instrument for U.S. federal income tax purposes.

Please see the discussion in the accompanying prospectus dated September 14, 2021 under the section entitled “Tax Consequences—United States Taxation” and specifically the discussion under

“Tax Consequences—United States Taxation—Original Issue Discount—Variable Rate Debt Securities,” and in the product prospectus supplement FIN-1 dated September 14, 2021 (including the opinion of our special U.S. tax counsel, Ashurst LLP)

under “Supplemental Discussion of U.S. Federal Income Tax Consequences” and specifically the discussion under “Supplemental Discussion of U.S. Federal Income Tax Consequences—Supplemental U.S. Tax Considerations—Where the term of your notes

will exceed one year—Fixed Rate Notes, Floating Rate Notes, Inverse Floating Rate Notes, Step Up Notes, Leveraged Notes, Range Accrual Notes, Dual Range Accrual Notes and Non-Inversion Range Accrual Notes,” and “Supplemental Discussion of

U.S. Federal Income Tax

|

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

| Consequences—Supplemental U.S. Tax Considerations—Where the term of your notes will exceed one year—Sale, Redemption or Maturity of Notes that Are Not Treated as Contingent Payment Debt Instruments,” which apply to your Notes. | |

|

Terms Incorporated in

the Master Note:

|

All of the terms appearing above the item captioned “Listing” on pages P-2 to P-4 of this pricing supplement and the applicable terms appearing under the caption “General Terms of the Notes”

in the product prospectus supplement FIN-1, as modified by this pricing supplement.

|

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

ADDITIONAL TERMS OF YOUR NOTES

You should read this pricing supplement together with the prospectus dated September 14, 2021, as supplemented by the prospectus supplement dated September 14, 2021 and the

product prospectus supplement FIN-1 dated September 14, 2021, relating to our Senior Global Medium-Term Notes, Series I, of which these Notes are a part. Capitalized terms used but not defined in this pricing supplement will have the meanings given

to them in the product prospectus supplement FIN-1. In the event of any conflict, this pricing supplement will control. The Notes vary from the terms described in the product prospectus

supplement FIN-1 in several important ways. You should read this pricing supplement carefully.

This pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other

written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things,

the matters set forth in “Risk Factors” in the prospectus supplement dated September 14, 2021, “Additional Risk Factors Specific to the Notes” in the product prospectus supplement FIN-1 dated September 14, 2021 and “Additional Risk Factors” in this

pricing supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. You may access these documents on the

SEC website at www.sec.gov as follows (or if that address has changed, by reviewing our filings for the relevant date on the SEC website):

Prospectus dated September 14, 2021:

Prospectus Supplement dated September 14, 2021:

Product Prospectus Supplement FIN-1 dated September 14, 2021:

Royal Bank of Canada has filed a registration statement (including a product prospectus supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which

this pricing supplement relates. Before you invest, you should read those documents and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may obtain these

documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Royal Bank of Canada, any agent or any dealer participating in this offering will arrange to send you the product prospectus supplement, the prospectus

supplement and the prospectus if you so request by calling toll-free at 1-877-688-2301.

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

ADDITIONAL RISK FACTORS

The Notes involve risks not associated with an investment in ordinary floating rate notes. This section describes the most significant risks relating to the terms of the Notes.

For additional information as to the risks related to an investment in the Notes, please see the accompanying product prospectus supplement FIN-1 and the prospectus supplement and prospectus, each dated September 14, 2021. You should carefully

consider whether the Notes are suited to your particular circumstances before you decide to purchase them. Accordingly, prospective investors should consult their financial and legal advisors as to the risks entailed by an investment in the Notes

and the suitability of the Notes in light of their particular circumstances.

Risks Relating to the Terms and Structure of the Notes

Investors Are Subject to Our Credit Risk, and Our Credit Ratings and Credit Spreads May Adversely Affect the Market Value of the Notes. Investors

are dependent on our ability to pay all amounts due on the Notes on the Interest Payment Dates and at maturity, and, therefore, investors are subject to our credit risk and to changes in the market’s view of our creditworthiness. Any decrease in

our credit ratings or increase in the credit spreads charged by the market for taking our credit risk is likely to adversely affect the market value of the Notes.

Risks Relating to the Initial Estimated Value of the Notes

The Initial Estimated Value of the Notes Will Be Less than the Price to the Public. The initial estimated value set forth on the cover page and that will be

set forth in the final pricing supplement for the Notes does not represent a minimum price at which we, RBCCM or any of our affiliates would be willing to purchase the Notes in any secondary market (if any exists) at any time. If you attempt to

sell the Notes prior to maturity, their market value may be lower than the price you paid for them and the initial estimated value. This is due to, among other things, changes in the levels of the Reference Rate, the borrowing rate we pay to issue

securities of this kind, and the inclusion in the price to the public of the underwriting discount and the estimated costs relating to our hedging of the Notes. These factors, together with various credit, market and economic factors over the term

of the Notes, are expected to reduce the price at which you may be able to sell the Notes in any secondary market and will affect the value of the Notes in complex and unpredictable ways. Assuming no change in market conditions or any other

relevant factors, the price, if any, at which you may be able to sell your Notes prior to maturity may be less than your original purchase price, as any such sale price would not be expected to include the underwriting discount and the hedging

costs relating to the Notes. In addition to bid-ask spreads, the value of the Notes determined for any secondary market price is expected to be based on the secondary rate rather than the internal funding rate used to price the Notes and determine

the initial estimated value. As a result, the secondary price will be less than if the internal funding rate was used. The Notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold the Notes

to maturity.

The Initial Estimated Value of the Notes that We Will Provide in the Final Pricing Supplement Is an Estimate Only, Calculated as of the Time the Terms

of the Notes Are Set. The initial estimated value of the Notes will be based on the value of our obligation to make the payments on the Notes, together with the mid-market value of the derivative embedded in the terms of the Notes. See

“Structuring the Notes” below. Our estimate will be based on a variety of assumptions, including our credit spreads, expectations as to interest rates and volatility, and the expected term of the Notes. These assumptions are based on certain

forecasts about future events, which may prove to be incorrect. Other entities may value the Notes or similar securities at a price that is significantly different than we do.

The value of the Notes at any time after the Pricing Date will vary based on many factors, including changes in market conditions, and cannot be predicted with accuracy. As a

result, the actual value you would receive if you sold the Notes in any secondary market, if any, should be expected to differ materially from the initial estimated value of the Notes.

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

Risks Relating to the Reference Rate

The Reference Rate and SOFR Have Limited Historical Information, and Future Performance Cannot Be Predicted Based on

Historical Performance. The publication of the U.S. Dollar SOFR ICE Swap Rate began in November 2021, and, therefore, has a limited history. IBA launched the U.S. Dollar SOFR ICE Swap Rate for use as a reference rate for financial

instruments in order to aid the market’s transition to SOFR and away from LIBOR. However, the composition and characteristics of SOFR differ from those of LIBOR in material respects, and the historical performance of LIBOR and the U.S. Dollar

LIBOR ICE Swap Rate will have no bearing on the performance of SOFR or the Reference Rate.

In addition, the publication of SOFR began in April 2018, and, therefore, it has a limited history. The future performance of the Reference Rate and SOFR

cannot be predicted based on the limited historical performance. The levels of the Reference Rate and SOFR during the term of the Notes may have little or no relation to the historical data.

Any Failure of SOFR to Gain Market Acceptance Could Adversely Affect the Notes. SOFR was developed for use in certain

U.S. dollar derivatives and other financial contracts as an alternative to USD LIBOR in part because it is considered a good representation of general funding conditions in the overnight U.S. Treasury repurchase agreement market. However, as a rate

based on transactions secured by U.S. Treasury securities, it does not measure bank-specific credit risk and, as a result, is less likely to correlate with the unsecured short-term funding costs of banks. This may mean that market participants

would not consider SOFR a suitable replacement or successor for all of the purposes for which USD LIBOR historically has been used (including, without limitation, as a representation of the unsecured short-term funding costs of banks), which may,

in turn, lessen market acceptance of SOFR. Any failure of SOFR to gain market acceptance could adversely affect the return on and value of the Notes and the price at which investors can sell the Notes in any secondary market.

In addition, if SOFR does not prove to be widely used as a benchmark in securities that are similar or comparable to the Notes, the

trading price of the Notes may be lower than those of securities that are linked to rates that are more widely used. Similarly, market terms for floating-rate debt securities linked to SOFR, such as the spread over the base rate reflected in

interest rate provisions or the manner of compounding the base rate, may evolve over time, and trading prices of the Notes may be lower than those of later-issued SOFR-based debt securities as a result. Investors in the Notes may not be able to

sell the Notes at all or may not be able to sell the Notes at prices that will provide them with a yield comparable to similar investments that have a developed secondary market, and may consequently suffer from increased pricing volatility and

market risk.

The Administrator of SOFR May Make Changes That Could Adversely Affect the Level of SOFR or Discontinue SOFR, and Has No

Obligation to Consider Your Interest in Doing So. SOFR is a relatively new rate, and Federal Reserve Bank of New York (“FRBNY”) (or a successor), as administrator of SOFR, may make methodological or other changes that could change the

level of SOFR, including changes related to the method by which SOFR is calculated, eligibility criteria applicable to the transactions used to calculate SOFR, or timing related to the publication of SOFR. If the manner in which SOFR is calculated

is changed, that change may result in a reduction in the Reference Rate, and may reduce the payments on the Notes. The administrator of SOFR may withdraw, modify, amend, suspend or discontinue the calculation or dissemination of SOFR in its sole

discretion and without notice, and has no obligation to consider the interests of holders of the Notes in calculating, withdrawing, modifying, amending, suspending or discontinuing SOFR. In that case, the method by which the Reference Rate is

calculated will change, which could reduce the Reference Rate.

The Reference Rate and the Manner in Which It Is Calculated May Change in the Future. There can be no assurance that

the method by which the Reference Rate is calculated will continue in its current form. Any changes in the method of calculation could reduce the amount of interest payable on the Notes.

The Reference Rate May Be Determined by the Calculation Agent in Its Sole Discretion or, if It Is Discontinued or Ceased to Be

Published Permanently or Indefinitely, Replaced by a Successor or Substitute Rate — If no relevant

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

rate appears on the applicable Bloomberg Screen Page on a relevant day at approximately 11:00 a.m., New York City time, then the Calculation Agent will have

the discretion to determine the Reference Rate for that day.

Notwithstanding the foregoing, if the Calculation Agent determines in its sole discretion on or prior to the relevant day that the relevant rate for U.S.

dollar swaps referencing SOFR has been discontinued or that rate has ceased to be published permanently or indefinitely, then the Calculation Agent will use as the applicable Reference Rate for that day a substitute or successor rate that it has

determined to be a commercially reasonable replacement rate. If the Calculation Agent has determined a substitute or successor rate in accordance with the foregoing, the Calculation Agent may determine in its sole discretion to make adjustments to

the definitions of business day and Interest Determination Date and any other relevant methodology for calculating that substitute or successor rate, including any adjustment factor, spread and/or formula it determines is needed to make that

substitute or successor rate comparable to the relevant rate for U.S. dollar swaps referencing SOFR.

Any of the foregoing determinations or actions by the Calculation Agent could result in adverse consequences to the value of the Reference Rate used on the applicable Interest

Determination Date, which could adversely affect the return on and the market value of the Notes.

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

THE REFERENCE RATE

A U.S. dollar SOFR ICE swap rate of a given maturity on any date of determination is the swap rate for a fixed-for-floating U.S. dollar SOFR-linked interest rate swap transaction

with that maturity as published by the administrator of the USD SOFR ICE swap rate as of 11:00 a.m. (New York City time) on that date of determination. In a fixed-for-floating U.S. Dollar SOFR-linked interest rate swap transaction, one party pays a

fixed rate (the “swap rate”) and the other pays a floating rate based on SOFR, compounded in arrears for 12 months using standard market conventions.

SOFR is intended to be a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities.

According to information provided by the IBA, each published USD SOFR ICE swap rate is calculated using eligible prices and volumes for specified interest rate derivative products, provided by trading

venues in accordance with a “Waterfall” methodology. The first level of the Waterfall (“Level 1”) uses eligible, executable prices and volumes provided by regulated, electronic, trading venues. If these trading venues do not provide sufficient

eligible input data to calculate a rate in accordance with Level 1 of the methodology, then the second level of the Waterfall (“Level 2”) uses eligible dealer to client prices and volumes displayed electronically by trading venues. If there is

insufficient eligible input data to calculate a rate in accordance with Level 2 of the methodology, then the third level of the Waterfall (“Level 3”) uses movement interpolation, where possible for applicable tenors, to calculate the rate. Where it

is not possible to calculate a rate at Level 1, Level 2 or Level 3 of the Waterfall, then the "insufficient data policy" applies for that rate, and the applicable U.S. dollar SOFR ICE swap rate may not be published for that date.

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

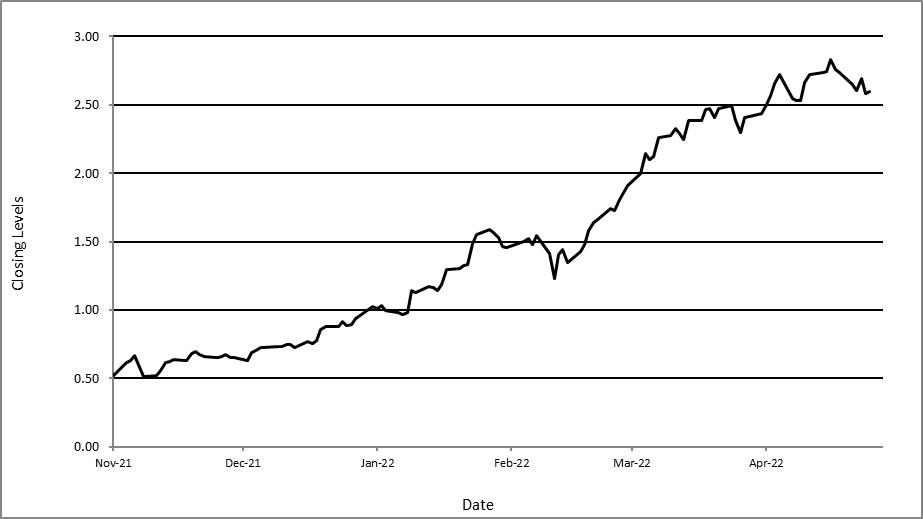

Historical Information

Historically, the Reference Rate has experienced significant fluctuations. Any historical upward or downward trend in the levels of the Reference Rate during any period shown

below is not an indication that the interest payable on the Notes is more or less likely to increase or decrease at any time during the term of the Notes.

The graph below sets forth the historical performance of the Reference Rate from November 19, 2021 to May 16, 2022.

Source: Bloomberg L.P. We have not independent verified the information provided by Bloomberg L.P.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

|

|

|

|

SOFR ICE Swap Rate Floating Rate Notes

Royal Bank of Canada

|

SUPPLEMENTAL PLAN OF DISTRIBUTION (CONFLICTS OF INTEREST)

Delivery of the Notes will be made against payment for the Notes on May 20, 2022, which is the second business day following the Pricing Date (this settlement cycle being referred

to as “T+2”). See “Plan of Distribution” in the prospectus supplement dated September 14, 2021. For additional information as to the relationship between us and RBC Capital Markets, LLC, please see the section “Plan of Distribution—Conflicts of

Interest” in the prospectus dated September 14, 2021.

After the initial offering of the Notes, the price to the public may change.

The value of the Notes shown on your account statement may be based on RBCCM’s estimate of the value of the Notes if RBCCM or another of our affiliates were to make a market in

the Notes (which it is not obligated to do). That estimate will be based upon the price that RBCCM may pay for the Notes in light of then prevailing market conditions, our creditworthiness and transaction costs. For a period of up to

approximately six months after the issue date of the Notes, the value of the Notes that may be shown on your account statement is expected to be higher than RBCCM’s estimated value of the Notes at that time. This is because the estimated value of

the Notes will not include the underwriting discount and our hedging costs and profits; however, the value of the Notes shown on your account statement during that period may initially be a higher amount, reflecting the addition of RBCCM’s

underwriting discount and our estimated costs and profits from hedging the Notes. This excess is expected to decrease over time until the end of this period. After this period, if RBCCM repurchases your Notes, it expects to do so at prices that

reflect their estimated value.

We may use this pricing supplement in the initial sale of the Notes. In addition, RBCCM or another of our affiliates may use this pricing supplement in a market-making transaction

in the Notes after their initial sale. Unless we or our agent informs the purchaser otherwise in the confirmation of sale, this pricing supplement is being used in a market-making transaction.

STRUCTURING THE NOTES

The Notes are our debt securities, the return on which is linked to the Reference Rate. As is the case for all of our debt securities, including our structured notes, the economic

terms of the Notes reflect our actual or perceived creditworthiness at the time of pricing. In addition, because structured notes result in increased operational, funding and liability management costs to us, we typically borrow the funds under

these Notes at a rate that is more favorable to us than the rate that we might pay for a conventional fixed or floating rate debt security of comparable maturity. Using this relatively lower implied borrowing rate rather than the secondary market

rate, is a factor that is likely to reduce the initial estimated value of the Notes at the time their terms are set. Unlike the estimated value included in this terms supplement or in the final pricing supplement, any value of the Notes determined

for purposes of a secondary market transaction may be based on a different funding rate, which may result in a lower value for the Notes than if our initial internal funding rate were used.

In order to satisfy our payment obligations under the Notes, we may choose to enter into certain hedging arrangements (which may include call options, put options or other

derivatives) on the issue date with RBCCM or one of our other subsidiaries. The terms of these hedging arrangements take into account a number of factors, including our creditworthiness, interest rate movements, the volatility of the Reference

Rates, and the tenor of the Notes. The economic terms of the Notes and their initial estimated value depend in part on the terms of these hedging arrangements.

The lower implied borrowing rate is a factor that reduces the economic terms of the Notes to you. The initial offering price of the Notes also reflects the underwriting commission and our estimated

hedging costs. These factors result in the initial estimated value for the Notes on the Pricing Date being less than their public offering price. See “Additional Risk Factors—The Initial Estimated Value of the Notes Will Be Less than the Price to

the Public” above.

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Introducing Altcat: Your AI Girlfriend Experience with Your Favorite Influencer

- Board Committee Changes

- Amendment of the terms concerning Convertible Bonds 2021/1, 2021/2, 2021/3, 2021/4 and 2022/1 issued by Digitalist Group Plc

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!