Form 497 Managed Account Series

Tweet

Tweet Share

ShareTable of Contents

|

Prospectus |

| • | BlackRock GA Disciplined Volatility Equity Fund |

| Institutional: BIDVX | |

| • | BlackRock GA Dynamic Equity Fund |

| Institutional: BIEEX |

Table of Contents

| Fund Overview | Key facts and details about the Funds listed in this prospectus, including investment objectives, principal investment strategies, principal risk factors, fee and expense information and historical performance information | |

|

|

3 | |

|

|

12 |

| Account Information | Information about account services, sales charges and waivers, shareholder transactions, and distributions and other payments | |

|

|

36 | |

|

|

38 | |

|

|

38 | |

|

|

43 | |

|

|

44 | |

|

|

44 | |

|

|

45 |

| Management of the Funds | Information about BlackRock and the Portfolio Managers | |

|

|

46 | |

|

|

48 | |

|

|

48 | |

|

|

50 | |

|

|

51 |

| Financial Highlights |

Financial Performance of the

Funds |

52 |

| General Information |

|

54 |

|

|

54 | |

|

|

55 |

| Glossary |

Glossary of Investment

Terms |

56 |

| For More Information |

|

Inside Back Cover |

|

|

Back Cover |

Table of Contents

| Annual

Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

Institutional

Shares | |

| Management Fee1 | 0.40% | |

| Distribution and/or Service (12b-1) Fees | None | |

| Other Expenses2,3 | 5.15% | |

| Other Expenses of the Fund | 5.10% | |

| Other Expenses of the Subsidiary | 0.05% | |

| Acquired Fund Fees and Expenses3 | 0.01% | |

| Total Annual Fund Operating Expenses3 | 5.56% | |

| Fee Waivers and/or Expense Reimbursements1,4 | (5.00)% | |

| Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements1,4 | 0.56% |

| 1 | As described in the “Management of the Funds” section of the Fund’s prospectus beginning on page 46, BlackRock Advisors, LLC (“BlackRock”) has contractually agreed to waive the management fee with respect to any portion of the Fund’s assets estimated to be attributable to investments in other equity and fixed-income mutual funds and exchange-traded funds managed by BlackRock or its affiliates that have a contractual management fee, through February 28, 2021. In addition, BlackRock has contractually agreed to waive its management fee by the amount of investment advisory fees the Fund pays to BlackRock indirectly through its investment in money market funds managed by BlackRock or its affiliates, through February 28, 2021. The contractual agreements may be terminated upon 90 days’ notice by a majority of the non-interested trustees of Managed Account Series (the “Trust”) or by a vote of a majority of the outstanding voting securities of the Fund. |

| 2 | Other Expenses have been restated to reflect current fees. |

| 3 | The Total Annual Fund Operating Expenses do not correlate to the ratio of expenses to average net assets given in the Fund’s most recent annual report, which does not include the restatement of Other Expenses to reflect current fees or Acquired Fund Fees and Expenses. |

| 4 | As described in the “Management of the Funds” section of the Fund’s prospectus beginning on page 46, BlackRock has contractually agreed to waive and/or reimburse fees or expenses in order to limit Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements (excluding Dividend Expense, Interest Expense, Acquired Fund Fees and Expenses and certain other Fund expenses) to 0.55% of average daily net assets through February 28, 2021. The Fund may have to repay some of these waivers and/or reimbursements to BlackRock in the two years following such waivers and/or reimbursements and such repayment arrangement will terminate on June 1, 2024. The contractual agreement may be terminated upon 90 days’ notice by a majority of the non-interested trustees of the Trust or by a vote of a majority of the outstanding voting securities of the Fund. |

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Institutional Shares | $57 | $1,212 | $2,354 | $5,154 |

Table of Contents

Table of Contents

| ■ | Commodities Related Investments Risk — Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, embargoes, tariffs and international economic, political and regulatory developments. |

| ■ | Convertible Securities Risk — The market value of a convertible security performs like that of a regular debt security; that is, if market interest rates rise, the value of a convertible security usually falls. In addition, convertible securities are subject to the risk that the issuer will not be able to pay interest or dividends when due, and their market value may change based on changes in the issuer’s credit rating or the market’s perception of the issuer’s creditworthiness. Since it derives a portion of its value from the common stock into which it may be converted, a convertible security is also subject to the same types of market and issuer risks that apply to the underlying common stock. |

| ■ | Corporate Loans Risk — Commercial banks and other financial institutions or institutional investors make corporate loans to companies that need capital to grow or restructure. Borrowers generally pay interest on corporate loans at rates that change in response to changes in market interest rates such as the London Interbank Offered Rate or the prime rates of U.S. banks. As a result, the value of corporate loan investments is generally less exposed to the adverse effects of shifts in market interest rates than investments that pay a fixed rate of interest. The market for corporate loans may be subject to irregular trading activity and wide bid/ask spreads. In addition, transactions in corporate loans may settle on a delayed basis. As a result, the proceeds from the sale of corporate loans may not be readily available to make additional investments or to meet the Fund’s redemption obligations. To the extent the extended settlement process gives rise to short-term liquidity needs, the Fund may hold additional cash, sell investments or temporarily borrow from banks and other lenders. |

| ■ | Debt Securities Risk — Debt securities, such as bonds, involve interest rate risk, credit risk, extension risk, and prepayment risk, among other things. |

| Interest Rate Risk — The market value of bonds and other fixed-income securities changes in response to interest rate changes and other factors. Interest rate risk is the risk that prices of bonds and other fixed-income securities will increase as interest rates fall and decrease as interest rates rise. | |

| The Fund may be subject to a greater risk of rising interest rates due to the current period of historically low rates. For example, if interest rates increase by 1%, assuming a current portfolio duration of ten years, and all other factors being equal, the value of the Fund’s investments would be expected to decrease by 10%. The magnitude of these fluctuations in the market price of bonds and other fixed-income securities is generally greater for those securities with longer maturities. Fluctuations in the market price of the Fund’s investments will not affect interest income derived from instruments already owned by the Fund, but will be reflected in the Fund’s net asset value. The Fund may lose money if short-term or long-term interest rates rise sharply in a manner not anticipated by Fund management. | |

| To the extent the Fund invests in debt securities that may be prepaid at the option of the obligor (such as mortgage-backed securities), the sensitivity of such securities to changes in interest rates may increase (to the detriment of the Fund) when interest rates rise. Moreover, because rates on certain floating rate debt securities typically reset only periodically, changes in prevailing interest rates (and particularly sudden and significant changes) can be expected to cause some fluctuations in the net asset value of the Fund to the extent that it invests in floating rate debt securities. | |

| These basic principles of bond prices also apply to U.S. Government securities. A security backed by the “full faith and credit” of the U.S. Government is guaranteed only as to its stated interest rate and face value at maturity, not its current market price. Just like other fixed-income securities, government-guaranteed securities will fluctuate in value when interest rates change. | |

| A general rise in interest rates has the potential to cause investors to move out of fixed-income securities on a large scale, which may increase redemptions from funds that hold large amounts of fixed-income securities. Heavy redemptions could cause the Fund to sell assets at inopportune times or at a loss or depressed value and could hurt the Fund’s performance. |

Table of Contents

| Credit Risk — Credit risk refers to the possibility that the issuer of a debt security (i.e., the borrower) will not be able to make payments of interest and principal when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. The degree of credit risk depends on both the financial condition of the issuer and the terms of the obligation. | |

| Extension Risk — When interest rates rise, certain obligations will be paid off by the obligor more slowly than anticipated, causing the value of these obligations to fall. | |

| Prepayment Risk — When interest rates fall, certain obligations will be paid off by the obligor more quickly than originally anticipated, and the Fund may have to invest the proceeds in securities with lower yields. | |

| ■ | Derivatives Risk — The Fund’s use of derivatives may increase its costs, reduce the Fund’s returns and/or increase volatility. Derivatives involve significant risks, including: |

| Volatility Risk — Volatility is defined as the characteristic of a security, an index or a market to fluctuate significantly in price within a short time period. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate with the overall securities markets. | |

| Counterparty Risk — Derivatives are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. | |

| Market and Illiquidity Risk — The possible lack of a liquid secondary market for derivatives and the resulting inability of the Fund to sell or otherwise close a derivatives position could expose the Fund to losses and could make derivatives more difficult for the Fund to value accurately. | |

| Valuation Risk — Valuation may be more difficult in times of market turmoil since many investors and market makers may be reluctant to purchase complex instruments or quote prices for them. | |

| Hedging Risk — Hedges are sometimes subject to imperfect matching between the derivative and the underlying security, and there can be no assurance that the Fund’s hedging transactions will be effective. The use of hedging may result in certain adverse tax consequences. | |

| Tax Risk — Certain aspects of the tax treatment of derivative instruments, including swap agreements and commodity-linked derivative instruments, are currently unclear and may be affected by changes in legislation,

regulations or other legally binding authority. Such treatment may be less favorable than that given to a direct investment in an underlying asset and may adversely affect the timing, character and amount of income the Fund realizes from its

investments. | |

| Regulatory Risk — Derivative contracts, including, without limitation, swaps, currency forwards and non-deliverable forwards, are subject to regulation under the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) in the United States and under comparable regimes in Europe, Asia and other non-U.S. jurisdictions. Under the Dodd-Frank Act, certain derivatives are subject to margin requirements and swap dealers are required to collect margin from the Fund with respect to such derivatives. Specifically, regulations are now in effect that require swap dealers to post and collect variation margin (comprised of specified liquid instruments and subject to a required haircut) in connection with trading of over-the-counter (“OTC”) swaps with the Fund. Shares of investment companies (other than certain money market funds) may not be posted as collateral under these regulations. Requirements for posting of initial margin in connection with OTC swaps will be phased-in through at least 2021. In addition, regulations adopted by global prudential regulators that are now in effect require certain bank-regulated counterparties and certain of their affiliates to include in certain financial contracts, including many derivatives contracts, terms that delay or restrict the rights of counterparties, such as the Fund, to terminate such contracts, foreclose upon collateral, exercise other default rights or restrict transfers of credit support in the event that the counterparty and/or its affiliates are subject to certain types of resolution or insolvency proceedings. The implementation of these requirements with respect to derivatives, as well as regulations under the Dodd-Frank Act regarding clearing, mandatory trading and margining of other derivatives, may increase the costs and risks to the Fund of trading in these instruments and, as a result, may affect returns to investors in the Fund. | |

| ■ | Distressed Securities Risk — Distressed securities are speculative and involve substantial risks in addition to the risks of investing in junk bonds. The Fund will generally not receive interest payments on the distressed securities and may incur costs to protect its investment. In addition, distressed securities involve the substantial risk that principal will not be repaid. These securities may present a substantial risk of default or may be in default at the time of investment. The Fund may incur additional expenses to the extent it is required to seek recovery upon a default in the payment of principal of or interest on its portfolio holdings. In any reorganization or liquidation proceeding relating to a portfolio company, the Fund may lose its entire investment or may be required to accept cash or securities with a value less than its original investment. Distressed securities and any securities received in an exchange for such securities may be subject to restrictions on resale. |

Table of Contents

| ■ | Emerging Markets Risk — Emerging markets are riskier than more developed markets because they tend to develop unevenly and may never fully develop. Investments in emerging markets may be considered speculative. Emerging markets are more likely to experience hyperinflation and currency devaluations, which adversely affect returns to U.S. investors. In addition, many emerging securities markets have far lower trading volumes and less liquidity than developed markets. |

| ■ | Equity Securities Risk — Stock markets are volatile. The price of equity securities fluctuates based on changes in a company’s financial condition and overall market and economic conditions. |

| ■ | Foreign Securities Risk — Foreign investments often involve special risks not present in U.S. investments that can increase the chances that the Fund will lose money. These risks include: |

| ■ | The Fund generally holds its foreign securities and cash in foreign banks and securities depositories, which may be recently organized or new to the foreign custody business and may be subject to only limited or no regulatory oversight. |

| ■ | Changes in foreign currency exchange rates can affect the value of the Fund’s portfolio. |

| ■ | The economies of certain foreign markets may not compare favorably with the economy of the United States with respect to such issues as growth of gross national product, reinvestment of capital, resources and balance of payments position. |

| ■ | The governments of certain countries may prohibit or impose substantial restrictions on foreign investments in their capital markets or in certain industries. |

| ■ | Many foreign governments do not supervise and regulate stock exchanges, brokers and the sale of securities to the same extent as does the United States and may not have laws to protect investors that are comparable to U.S. securities laws. |

| ■ | Settlement and clearance procedures in certain foreign markets may result in delays in payment for or delivery of securities not typically associated with settlement and clearance of U.S. investments. |

| ■ | The European financial markets have recently experienced volatility and adverse trends due to concerns about economic downturns in, or rising government debt levels of, several European countries. These events may spread to other countries in Europe. These events may affect the value and liquidity of certain of the Fund’s investments. |

| ■ | High Portfolio Turnover Risk — The Fund may engage in active and frequent trading of its portfolio securities. High portfolio turnover (more than 100%) may result in increased transaction costs to the Fund, including brokerage commissions, dealer mark-ups and other transaction costs on the sale of the securities and on reinvestment in other securities. The sale of Fund portfolio securities may result in the realization and/or distribution to shareholders of higher capital gains or losses as compared to a fund with less active trading policies. These effects of higher than normal portfolio turnover may adversely affect Fund performance. |

| ■ | Indexed and Inverse Securities Risk — Indexed and inverse securities provide a potential return based on a particular index of value or interest rates. The Fund’s return on these securities will be subject to risk with respect to the value of the particular index. These securities are subject to leverage risk and correlation risk.Certain indexed and inverse securities have greater sensitivity to changes in interest rates or index levels than other securities, and the Fund’s investment in such instruments may decline significantly in value if interest rates or index levels move in a way Fund management does not anticipate. |

| ■ | Inflation-Indexed Bonds Risk — The principal value of an investment is not protected or otherwise guaranteed by virtue of the Fund’s investments in inflation-indexed bonds. |

| Inflation-indexed bonds are fixed-income securities whose principal value is periodically adjusted according to the rate of inflation. If the index measuring inflation falls, the principal value of inflation-indexed bonds will be adjusted downward, and consequently the interest payable on these securities (calculated with respect to a smaller principal amount) will be reduced. | |

| Repayment of the original bond principal upon maturity (as adjusted for inflation) is guaranteed in the case of U.S. Treasury inflation-indexed bonds. For bonds that do not provide a similar guarantee, the adjusted principal value of the bond repaid at maturity may be less than the original principal value. | |

| The value of inflation-indexed bonds is expected to change in response to changes in real interest rates. Real interest rates are tied to the relationship between nominal interest rates and the rate of inflation. If nominal interest rates increase at a faster rate than inflation, real interest rates may rise, leading to a decrease in value of inflation-indexed bonds. Short-term increases in inflation may lead to a decline in value. Any increase in the principal amount of an inflation-indexed bond will be considered taxable ordinary income, even though investors do not receive their principal until maturity. |

Table of Contents

| Periodic adjustments for inflation to the principal amount of an inflation-indexed bond may give rise to original issue discount, which will be includable in the Fund’s gross income. Due to original issue discount, the Fund may be required to make annual distributions to shareholders that exceed the cash received, which may cause the Fund to liquidate certain investments when it is not advantageous to do so. Also, if the principal value of an inflation-indexed bond is adjusted downward due to deflation, amounts previously distributed in the taxable year may be characterized in some circumstances as a return of capital. | |

| ■ | Junk Bonds Risk — Although junk bonds generally pay higher rates of interest than investment grade bonds, junk bonds are high risk investments that are considered speculative and may cause income and principal losses for the Fund. |

| ■ | Leverage Risk — Some transactions may give rise to a form of economic leverage. These transactions may include, among others, derivatives, and may expose the Fund to greater risk and increase its costs. The use of leverage may cause the Fund to liquidate portfolio positions when it may not be advantageous to do so to satisfy its obligations or to meet any required asset segregation requirements. Increases and decreases in the value of the Fund’s portfolio will be magnified when the Fund uses leverage. |

| ■ | Market Risk and Selection Risk — Market risk is the risk that one or more markets in which the Fund invests will go down in value, including the possibility that the markets will go down sharply and unpredictably. Selection risk is the risk that the securities selected by Fund management will underperform the markets, the relevant indices or the securities selected by other funds with similar investment objectives and investment strategies. This means you may lose money. |

| ■ | Mid Cap Securities Risk — The securities of mid cap companies generally trade in lower volumes and are generally subject to greater and less predictable price changes than the securities of larger capitalization companies. |

| ■ | Mortgage- and Asset-Backed Securities Risks — Mortgage- and asset-backed securities represent interests in “pools” of mortgages or other assets, including consumer loans or receivables held in trust. Mortgage- and asset-backed securities are subject to credit, interest rate, prepayment and extension risks. These securities also are subject to risk of default on the underlying mortgage or asset, particularly during periods of economic downturn. Small movements in interest rates (both increases and decreases) may quickly and significantly reduce the value of certain mortgage-backed securities. |

| ■ | Precious Metal and Related Securities Risk — Prices of precious metals and of precious metal related securities historically have been very volatile. The high volatility of precious metal prices may adversely affect the financial condition of companies involved with precious metals. The production and sale of precious metals by governments or central banks or other larger holders can be affected by various economic, financial, social and political factors, which may be unpredictable and may have a significant impact on the prices of precious metals. Other factors that may affect the prices of precious metals and securities related to them include changes in inflation, the outlook for inflation and changes in industrial and commercial demand for precious metals. |

| ■ | Real Estate-Related Securities Risk — The main risk of real estate-related securities is that the value of the underlying real estate may go down. Many factors may affect real estate values. These factors include both the general and local economies, vacancy rates, tenant bankruptcies, the ability to re-lease space under expiring leases on attractive terms, the amount of new construction in a particular area, the laws and regulations (including zoning, environmental and tax laws) affecting real estate and the costs of owning, maintaining and improving real estate. The availability of mortgage financing and changes in interest rates may also affect real estate values. If the Fund’s real estate-related investments are concentrated in one geographic area or in one property type, the Fund will be particularly subject to the risks associated with that area or property type. Many issuers of real estate-related securities are highly leveraged, which increases the risk to holders of such securities. The value of the securities the Fund buys will not necessarily track the value of the underlying investments of the issuers of such securities. |

| ■ | Short Sales Risk — Because making short sales in securities that it does not own exposes the Fund to the risks associated with those securities, such short sales involve speculative exposure risk. The Fund will incur a loss as a result of a short sale if the price of the security increases between the date of the short sale and the date on which the Fund replaces the security sold short. |

| ■ | Small Cap and Emerging Growth Securities Risk — Small cap or emerging growth companies may have limited product lines or markets. They may be less financially secure than larger, more established companies. They may depend on a more limited management group than larger capitalized companies. |

| ■ | Sovereign Debt Risk — Sovereign debt instruments are subject to the risk that a governmental entity may delay or refuse to pay interest or repay principal on its sovereign debt, due, for example, to cash flow problems, insufficient foreign currency reserves, political considerations, the relative size of the governmental entity’s debt position in relation to the economy or the failure to put in place economic reforms required by the International Monetary Fund or other multilateral agencies. |

Table of Contents

| ■ | Structured Notes Risk — Structured notes and other related instruments purchased by the Fund are generally privately negotiated debt obligations where the principal and/or interest is determined by reference to the performance of a specific asset, benchmark asset, market or interest rate (“reference measure”). The purchase of structured notes exposes the Fund to the credit risk of the issuer of the structured product. Structured notes may be leveraged, increasing the volatility of each structured note’s value relative to the change in the reference measure. Structured notes may also be less liquid and more difficult to price accurately than less complex securities and instruments or more traditional debt securities. |

| ■ | Subsidiary Risk — By investing in the Subsidiary, the Fund is indirectly exposed to the risks associated with the Subsidiary’s investments. The commodity-related instruments held by the Subsidiary are generally similar to those that are permitted to be held by the Fund and are subject to the same risks that apply to similar investments if held directly by the Fund (see “Commodities Related Investments Risk” above). There can be no assurance that the investment objective of the Subsidiary will be achieved. The Subsidiary is not registered under the Investment Company Act of 1940, as amended (the “Investment Company Act”), and, unless otherwise noted in this prospectus, is not subject to all the investor protections of the Investment Company Act. However, the Fund wholly owns and controls the Subsidiary, and the Fund and the Subsidiary are both managed by BlackRock, making it unlikely that the Subsidiary will take action contrary to the interests of the Fund and its shareholders. The Board has oversight responsibility for the investment activities of the Fund, including its investment in the Subsidiary, and the Fund’s role as sole shareholder of the Subsidiary. The Subsidiary is subject to the same investment restrictions and limitations, and follows the same compliance policies and procedures, as the Fund, except that the Subsidiary may invest without limitation in commodity-related instruments. Changes in the laws of the United States and/or the Cayman Islands could result in the inability of the Fund and/or the Subsidiary to operate as described in this prospectus and the Statement of Additional Information and could adversely affect the Fund. |

As of 12/31

Table of Contents

| As

of 12/31/19 Average Annual Total Returns |

1 Year | Since

Inception (June 1, 2017) |

| BlackRock GA Disciplined Volatility Equity Fund — Institutional Shares | ||

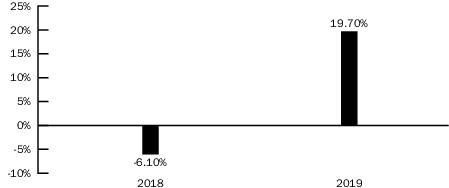

| Return Before Taxes | 19.54% | 6.77% |

| Return After Taxes on Distributions | 17.76% | 5.90% |

| Return After Taxes on Distributions and Sale of Fund Shares | 11.97% | 5.01% |

| MSCI ACWI Minimum Volatility (USD) Index (Reflects no deduction for fees, expenses or taxes) | 21.05% | 9.67% |

| Name | Portfolio

Manager of the Fund Since |

Title |

| Dan Chamby, CFA1 | 2017 | Managing Director of BlackRock, Inc. |

| Russ Koesterich, CFA, JD | 2017 | Managing Director of BlackRock, Inc. |

| David Clayton, CFA, JD | 2018 | Managing Director of BlackRock, Inc. |

| 1 | On or about March 2, 2020, Dan Chamby will retire from BlackRock, Inc., and will no longer serve as a portfolio manager of the Fund. |

Table of Contents

| Minimum

Initial Investment |

There

is no minimum initial investment for: • Employer-sponsored retirement plans (not including SEP IRAs, SIMPLE IRAs or SARSEPs), state sponsored 529 college savings plans, collective trust funds, investment companies or other pooled investment vehicles, unaffiliated thrifts and unaffiliated banks and trust companies, each of which may purchase shares of the Fund through a Financial Intermediary that has entered into an agreement with the Fund’s distributor to purchase such shares. • Clients of Financial Intermediaries that: (i) charge such clients a fee for advisory, investment consulting, or similar services or (ii) have entered into an agreement with the Fund’s distributor to offer Institutional Shares through a no-load program or investment platform.$2 million for individuals and “Institutional Investors,” which include, but are not limited to, endowments, foundations, family offices, local, city, and state governmental institutions, corporations and insurance company separate accounts who may purchase shares of the Fund through a Financial Intermediary that has entered into an agreement with the Fund’s distributor to purchase such shares.$1,000 for: • Clients investing through Financial Intermediaries that offer such shares on a platform that charges a transaction based sales commission outside of the Fund. • Tax-qualified accounts for insurance agents that are registered representatives of an insurance company’s broker-dealer that has entered into an agreement with the Fund’s distributor to offer Institutional Shares, and the family members of such persons. |

| Minimum

Additional Investment |

No subsequent minimum. |

Table of Contents

| Annual

Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

Institutional

Shares | |

| Management Fee1 | 0.40% | |

| Distribution and/or Service (12b-1) Fees | None | |

| Other Expenses2,3 | 5.81% | |

| Other Expenses of the Fund | 5.76% | |

| Other Expenses of the Subsidiary | 0.05% | |

| Acquired Fund Fees and Expenses3 | 0.01% | |

| Total Annual Fund Operating Expenses3 | 6.22% | |

| Fee Waivers and/or Expense Reimbursements1,4 | (5.66)% | |

| Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements1,4 | 0.56% |

| 1 | As described in the “Management of the Funds” section of the Fund’s prospectus beginning on page 46, BlackRock Advisors, LLC (“BlackRock”) has contractually agreed to waive the management fee with respect to any portion of the Fund’s assets estimated to be attributable to investments in other equity and fixed-income mutual funds and exchange-traded funds managed by BlackRock or its affiliates that have a contractual management fee, through February 28, 2021. In addition, BlackRock has contractually agreed to waive its management fee by the amount of investment advisory fees that Fund pays to BlackRock indirectly through its investment in money market funds managed by BlackRock or its affiliates, through February 28, 2021. The contractual agreements may be terminated upon 90 days’ notice by a majority of the non-interested trustees of Managed Account Series (the “Trust”) or by a vote of a majority of the outstanding voting securities of the Fund. |

| 2 | Other Expenses have been restated to reflect current fees. |

| 3 | The Total Annual Fund Operating Expenses do not correlate to the ratio of expenses to average nets assets given in the Fund’s most recent annual report, which does not include the restatement of Other Expenses to reflect current fees or Acquired Fund Fees and Expenses. |

| 4 | As described in the “Management of the Funds” section of the Fund’s prospectus beginning on page 46, BlackRock has contractually agreed to waive and/or reimburse fees or expenses in order to limit Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements (excluding Dividend Expense, Interest Expense, Acquired Fund Fees and Expenses and certain other Fund expenses) to 0.55% of average daily net assets through February 28, 2021. The Fund may have to repay some of these waivers and/or reimbursements to BlackRock in the two years following such waivers and/or reimbursements and such repayment arrangement will terminate on June 1, 2024. The contractual agreement may be terminated upon 90 days’ notice by a majority of the non-interested trustees of the Trust or by a vote of a majority of the outstanding voting securities of the Fund. |

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Institutional Shares | $57 | $1,341 | $2,593 | $5,592 |

Table of Contents

Table of Contents

| ■ | Commodities Related Investments Risk — Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, embargoes, tariffs and international economic, political and regulatory developments. |

| ■ | Convertible Securities Risk — The market value of a convertible security performs like that of a regular debt security; that is, if market interest rates rise, the value of a convertible security usually falls. In addition, convertible securities are subject to the risk that the issuer will not be able to pay interest or dividends when due, and their market value may change based on changes in the issuer’s credit rating or the market’s perception of the issuer’s creditworthiness. Since it derives a portion of its value from the common stock into which it may be converted, a convertible security is also subject to the same types of market and issuer risks that apply to the underlying common stock. |

| ■ | Corporate Loans Risk — Commercial banks and other financial institutions or institutional investors make corporate loans to companies that need capital to grow or restructure. Borrowers generally pay interest on corporate loans at rates that change in response to changes in market interest rates such as the London Interbank Offered Rate or the prime rates of U.S. banks. As a result, the value of corporate loan investments is generally less exposed to the adverse effects of shifts in market interest rates than investments that pay a fixed rate of interest. The market for corporate loans may be subject to irregular trading activity and wide bid/ask spreads. In addition, transactions in corporate loans may settle on a delayed basis. As a result, the proceeds from the sale of corporate loans may not be readily available to make additional investments or to meet the Fund’s redemption obligations. To the extent the extended settlement process gives rise to short-term liquidity needs, the Fund may hold additional cash, sell investments or temporarily borrow from banks and other lenders. |

| ■ | Debt Securities Risk — Debt securities, such as bonds, involve interest rate risk, credit risk, extension risk, and prepayment risk, among other things. |

| Interest Rate Risk — The market value of bonds and other fixed-income securities changes in response to interest rate changes and other factors. Interest rate risk is the risk that prices of bonds and other fixed-income securities will increase as interest rates fall and decrease as interest rates rise. | |

| The Fund may be subject to a greater risk of rising interest rates due to the current period of historically low rates. For example, if interest rates increase by 1%, assuming a current portfolio duration of ten years, and all other factors being equal, the value of the Fund’s investments would be expected to decrease by 10%. The magnitude of these fluctuations in the market price of bonds and other fixed-income securities is generally greater for those securities with longer maturities. Fluctuations in the market price of the Fund’s investments will not affect interest income derived from instruments already owned by the Fund, but will be reflected in the Fund’s net asset value. The Fund may lose money if short-term or long-term interest rates rise sharply in a manner not anticipated by Fund management. | |

| To the extent the Fund invests in debt securities that may be prepaid at the option of the obligor (such as mortgage-backed securities), the sensitivity of such securities to changes in interest rates may increase (to the detriment of the Fund) when interest rates rise. Moreover, because rates on certain floating rate debt securities typically reset only periodically, changes in prevailing interest rates (and particularly sudden and significant changes) can be expected to cause some fluctuations in the net asset value of the Fund to the extent that it invests in floating rate debt securities. | |

| These basic principles of bond prices also apply to U.S. Government securities. A security backed by the “full faith and credit” of the U.S. Government is guaranteed only as to its stated interest rate and face value at maturity, not its current market price. Just like other fixed-income securities, government-guaranteed securities will fluctuate in value when interest rates change. | |

| A general rise in interest rates has the potential to cause investors to move out of fixed-income securities on a large scale, which may increase redemptions from funds that hold large amounts of fixed-income securities. Heavy redemptions could cause the Fund to sell assets at inopportune times or at a loss or depressed value and could hurt the Fund’s performance. |

Table of Contents

| Credit Risk — Credit risk refers to the possibility that the issuer of a debt security (i.e., the borrower) will not be able to make payments of interest and principal when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. The degree of credit risk depends on both the financial condition of the issuer and the terms of the obligation. | |

| Extension Risk — When interest rates rise, certain obligations will be paid off by the obligor more slowly than anticipated, causing the value of these obligations to fall. | |

| Prepayment Risk — When interest rates fall, certain obligations will be paid off by the obligor more quickly than originally anticipated, and the Fund may have to invest the proceeds in securities with lower yields. | |

| ■ | Derivatives Risk — The Fund’s use of derivatives may increase its costs, reduce the Fund’s returns and/or increase volatility. Derivatives involve significant risks, including: |

| Volatility Risk — Volatility is defined as the characteristic of a security, an index or a market to fluctuate significantly in price within a short time period. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate with the overall securities markets. | |

| Counterparty Risk — Derivatives are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. | |

| Market and Illiquidity Risk — The possible lack of a liquid secondary market for derivatives and the resulting inability of the Fund to sell or otherwise close a derivatives position could expose the Fund to losses and could make derivatives more difficult for the Fund to value accurately. | |

| Valuation Risk — Valuation may be more difficult in times of market turmoil since many investors and market makers may be reluctant to purchase complex instruments or quote prices for them. | |

| Hedging Risk — Hedges are sometimes subject to imperfect matching between the derivative and the underlying security, and there can be no assurance that the Fund’s hedging transactions will be effective. The use of hedging may result in certain adverse tax consequences. | |

| Tax Risk — Certain aspects of the tax treatment of derivative instruments, including swap agreements and commodity-linked derivative instruments, are currently unclear and may be affected by changes in legislation,

regulations or other legally binding authority. Such treatment may be less favorable than that given to a direct investment in an underlying asset and may adversely affect the timing, character and amount of income the Fund realizes from its

investments. | |

| Regulatory Risk — Derivative contracts, including, without limitation, swaps, currency forwards and non-deliverable forwards, are subject to regulation under the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) in the United States and under comparable regimes in Europe, Asia and other non-U.S. jurisdictions. Under the Dodd-Frank Act, certain derivatives are subject to margin requirements and swap dealers are required to collect margin from the Fund with respect to such derivatives. Specifically, regulations are now in effect that require swap dealers to post and collect variation margin (comprised of specified liquid instruments and subject to a required haircut) in connection with trading of over-the-counter (“OTC”) swaps with the Fund. Shares of investment companies (other than certain money market funds) may not be posted as collateral under these regulations. Requirements for posting of initial margin in connection with OTC swaps will be phased-in through at least 2021. In addition, regulations adopted by global prudential regulators that are now in effect require certain bank-regulated counterparties and certain of their affiliates to include in certain financial contracts, including many derivatives contracts, terms that delay or restrict the rights of counterparties, such as the Fund, to terminate such contracts, foreclose upon collateral, exercise other default rights or restrict transfers of credit support in the event that the counterparty and/or its affiliates are subject to certain types of resolution or insolvency proceedings. The implementation of these requirements with respect to derivatives, as well as regulations under the Dodd-Frank Act regarding clearing, mandatory trading and margining of other derivatives, may increase the costs and risks to the Fund of trading in these instruments and, as a result, may affect returns to investors in the Fund. | |

| ■ | Distressed Securities Risk — Distressed securities are speculative and involve substantial risks in addition to the risks of investing in junk bonds. The Fund will generally not receive interest payments on the distressed securities and may incur costs to protect its investment. In addition, distressed securities involve the substantial risk that principal will not be repaid. These securities may present a substantial risk of default or may be in default at the time of investment. The Fund may incur additional expenses to the extent it is required to seek recovery upon a default in the payment of principal of or interest on its portfolio holdings. In any reorganization or liquidation proceeding relating to a portfolio company, the Fund may lose its entire investment or may be required to accept cash or securities with a value less than its original investment. Distressed securities and any securities received in an exchange for such securities may be subject to restrictions on resale. |

Table of Contents

| ■ | Emerging Markets Risk — Emerging markets are riskier than more developed markets because they tend to develop unevenly and may never fully develop. Investments in emerging markets may be considered speculative. Emerging markets are more likely to experience hyperinflation and currency devaluations, which adversely affect returns to U.S. investors. In addition, many emerging securities markets have far lower trading volumes and less liquidity than developed markets. |

| ■ | Equity Securities Risk — Stock markets are volatile. The price of equity securities fluctuates based on changes in a company’s financial condition and overall market and economic conditions. |

| ■ | Foreign Securities Risk — Foreign investments often involve special risks not present in U.S. investments that can increase the chances that the Fund will lose money. These risks include: |

| ■ | The Fund generally holds its foreign securities and cash in foreign banks and securities depositories, which may be recently organized or new to the foreign custody business and may be subject to only limited or no regulatory oversight. |

| ■ | Changes in foreign currency exchange rates can affect the value of the Fund’s portfolio. |

| ■ | The economies of certain foreign markets may not compare favorably with the economy of the United States with respect to such issues as growth of gross national product, reinvestment of capital, resources and balance of payments position. |

| ■ | The governments of certain countries may prohibit or impose substantial restrictions on foreign investments in their capital markets or in certain industries. |

| ■ | Many foreign governments do not supervise and regulate stock exchanges, brokers and the sale of securities to the same extent as does the United States and may not have laws to protect investors that are comparable to U.S. securities laws. |

| ■ | Settlement and clearance procedures in certain foreign markets may result in delays in payment for or delivery of securities not typically associated with settlement and clearance of U.S. investments. |

| ■ | The European financial markets have recently experienced volatility and adverse trends due to concerns about economic downturns in, or rising government debt levels of, several European countries. These events may spread to other countries in Europe. These events may affect the value and liquidity of certain of the Fund’s investments. |

| ■ | High Portfolio Turnover Risk — The Fund may engage in active and frequent trading of its portfolio securities. High portfolio turnover (more than 100%) may result in increased transaction costs to the Fund, including brokerage commissions, dealer mark-ups and other transaction costs on the sale of the securities and on reinvestment in other securities. The sale of Fund portfolio securities may result in the realization and/or distribution to shareholders of higher capital gains or losses as compared to a fund with less active trading policies. These effects of higher than normal portfolio turnover may adversely affect Fund performance. |

| ■ | Indexed and Inverse Securities Risk — Indexed and inverse securities provide a potential return based on a particular index of value or interest rates. The Fund’s return on these securities will be subject to risk with respect to the value of the particular index. These securities are subject to leverage risk and correlation risk.Certain indexed and inverse securities have greater sensitivity to changes in interest rates or index levels than other securities, and the Fund’s investment in such instruments may decline significantly in value if interest rates or index levels move in a way Fund management does not anticipate. |

| ■ | Junk Bonds Risk — Although junk bonds generally pay higher rates of interest than investment grade bonds, junk bonds are high risk investments that are considered speculative and may cause income and principal losses for the Fund. |

| ■ | Leverage Risk — Some transactions may give rise to a form of economic leverage. These transactions may include, among others, derivatives, and may expose the Fund to greater risk and increase its costs. The use of leverage may cause the Fund to liquidate portfolio positions when it may not be advantageous to do so to satisfy its obligations or to meet any required asset segregation requirements. Increases and decreases in the value of the Fund’s portfolio will be magnified when the Fund uses leverage. |

| ■ | Market Risk and Selection Risk — Market risk is the risk that one or more markets in which the Fund invests will go down in value, including the possibility that the markets will go down sharply and unpredictably. Selection risk is the risk that the securities selected by Fund management will underperform the markets, the relevant indices or the securities selected by other funds with similar investment objectives and investment strategies. This means you may lose money. |

| ■ | Mid Cap Securities Risk — The securities of mid cap companies generally trade in lower volumes and are generally subject to greater and less predictable price changes than the securities of larger capitalization companies. |

Table of Contents

| ■ | Mortgage- and Asset-Backed Securities Risks — Mortgage- and asset-backed securities represent interests in “pools” of mortgages or other assets, including consumer loans or receivables held in trust. Mortgage- and asset-backed securities are subject to credit, interest rate, prepayment and extension risks. These securities also are subject to risk of default on the underlying mortgage or asset, particularly during periods of economic downturn. Small movements in interest rates (both increases and decreases) may quickly and significantly reduce the value of certain mortgage-backed securities. |

| ■ | Precious Metal and Related Securities Risk — Prices of precious metals and of precious metal related securities historically have been very volatile. The high volatility of precious metal prices may adversely affect the financial condition of companies involved with precious metals. The production and sale of precious metals by governments or central banks or other larger holders can be affected by various economic, financial, social and political factors, which may be unpredictable and may have a significant impact on the prices of precious metals. Other factors that may affect the prices of precious metals and securities related to them include changes in inflation, the outlook for inflation and changes in industrial and commercial demand for precious metals. |

| ■ | Real Estate-Related Securities Risk — The main risk of real estate-related securities is that the value of the underlying real estate may go down. Many factors may affect real estate values. These factors include both the general and local economies, vacancy rates, tenant bankruptcies, the ability to re-lease space under expiring leases on attractive terms, the amount of new construction in a particular area, the laws and regulations (including zoning, environmental and tax laws) affecting real estate and the costs of owning, maintaining and improving real estate. The availability of mortgage financing and changes in interest rates may also affect real estate values. If the Fund’s real estate-related investments are concentrated in one geographic area or in one property type, the Fund will be particularly subject to the risks associated with that area or property type. Many issuers of real estate-related securities are highly leveraged, which increases the risk to holders of such securities. The value of the securities the Fund buys will not necessarily track the value of the underlying investments of the issuers of such securities. |

| ■ | Short Sales Risk — Because making short sales in securities that it does not own exposes the Fund to the risks associated with those securities, such short sales involve speculative exposure risk. The Fund will incur a loss as a result of a short sale if the price of the security increases between the date of the short sale and the date on which the Fund replaces the security sold short. |

| ■ | Small Cap and Emerging Growth Securities Risk — Small cap or emerging growth companies may have limited product lines or markets. They may be less financially secure than larger, more established companies. They may depend on a more limited management group than larger capitalized companies. |

| ■ | Sovereign Debt Risk — Sovereign debt instruments are subject to the risk that a governmental entity may delay or refuse to pay interest or repay principal on its sovereign debt, due, for example, to cash flow problems, insufficient foreign currency reserves, political considerations, the relative size of the governmental entity’s debt position in relation to the economy or the failure to put in place economic reforms required by the International Monetary Fund or other multilateral agencies. |

| ■ | Structured Notes Risk — Structured notes and other related instruments purchased by the Fund are generally privately negotiated debt obligations where the principal and/or interest is determined by reference to the performance of a specific asset, benchmark asset, market or interest rate (“reference measure”). The purchase of structured notes exposes the Fund to the credit risk of the issuer of the structured product. Structured notes may be leveraged, increasing the volatility of each structured note’s value relative to the change in the reference measure. Structured notes may also be less liquid and more difficult to price accurately than less complex securities and instruments or more traditional debt securities. |

| ■ | Subsidiary Risk — By investing in the Subsidiary, the Fund is indirectly exposed to the risks associated with the Subsidiary’s investments. The commodity-related instruments held by the Subsidiary are generally similar to those that are permitted to be held by the Fund and are subject to the same risks that apply to similar investments if held directly by the Fund (see “Commodities Related Investments Risk” above). There can be no assurance that the investment objective of the Subsidiary will be achieved. The Subsidiary is not registered under the Investment Company Act of 1940, as amended (the “Investment Company Act”), and, unless otherwise noted in this prospectus, is not subject to all the investor protections of the Investment Company Act. However, the Fund wholly owns and controls the Subsidiary, and the Fund and the Subsidiary are both managed by BlackRock, making it unlikely that the Subsidiary will take action contrary to the interests of the Fund and its shareholders. The Board has oversight responsibility for the investment activities of the Fund, including its investment in the Subsidiary, and the Fund’s role as sole shareholder of the Subsidiary. The Subsidiary is subject to the same investment restrictions and limitations, and follows the same compliance policies and procedures, as the Fund, except that the Subsidiary may invest without limitation in commodity-related instruments. Changes in the laws of the United States and/or the Cayman Islands could result in the inability of the Fund and/or the Subsidiary to operate as described in this prospectus and the Statement of Additional Information and could adversely affect the Fund. |

Table of Contents

As of 12/31

| As

of 12/31/19 Average Annual Total Returns |

1 Year | Since

Inception (June 1, 2017) |

| BlackRock GA Dynamic Equity Fund — Institutional Shares | ||

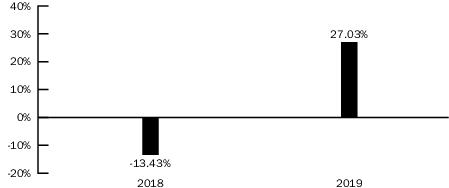

| Return Before Taxes | 27.03% | 8.68% |

| Return After Taxes on Distributions | 26.53% | 7.71% |

| Return After Taxes on Distributions and Sale of Fund Shares | 16.32% | 6.41% |

| MSCI World Index (Reflects no deduction for fees, expenses or taxes) | 27.67% | 10.25% |

| Name | Portfolio

Manager of the Fund Since |

Title |

| Dan Chamby, CFA1 | 2017 | Managing Director of BlackRock, Inc. |

| Russ Koesterich, CFA, JD | 2017 | Managing Director of BlackRock, Inc. |

| David Clayton, CFA, JD | 2018 | Managing Director of BlackRock, Inc. |

Table of Contents

| 1 | On or about March 2, 2020, Dan Chamby will retire from BlackRock, Inc., and will no longer serve as a portfolio manager of the Fund. |

| Minimum

Initial Investment |

There

is no minimum initial investment for: • Employer-sponsored retirement plans (not including SEP IRAs, SIMPLE IRAs or SARSEPs), state sponsored 529 college savings plans, collective trust funds, investment companies or other pooled investment vehicles, unaffiliated thrifts and unaffiliated banks and trust companies, each of which may purchase shares of the Fund through a Financial Intermediary that has entered into an agreement with the Fund’s distributor to purchase such shares. • Clients of Financial Intermediaries that: (i) charge such clients a fee for advisory, investment consulting, or similar services or (ii) have entered into an agreement with the Fund’s distributor to offer Institutional Shares through a no-load program or investment platform.$2 million for individuals and “Institutional Investors,” which include, but are not limited to, endowments, foundations, family offices, local, city, and state governmental institutions, corporations and insurance company separate accounts who may purchase shares of the Fund through a Financial Intermediary that has entered into an agreement with the Fund’s distributor to purchase such shares.$1,000 for: • Clients investing through Financial Intermediaries that offer such shares on a platform that charges a transaction based sales commission outside of the Fund. • Tax-qualified accounts for insurance agents that are registered representatives of an insurance company’s broker-dealer that has entered into an agreement with the Fund’s distributor to offer Institutional Shares, and the family members of such persons. |

| Minimum

Additional Investment |

No subsequent minimum. |

Table of Contents

Table of Contents

Table of Contents

| 1 | On or about March 2, 2020, Dan Chamby will retire from BlackRock, Inc., and will no longer serve as a portfolio manager of the Fund. |

Table of Contents

Table of Contents

| 1 | On or about March 2, 2020, Dan Chamby will retire from BlackRock, Inc., and will no longer serve as a portfolio manager of the Fund. |

| ■ | Borrowing — Each Fund may borrow up to the limits set forth under the Investment Company Act, the rules and regulations thereunder and any applicable exemptive relief. |

| ■ | Floating Rate Investments — The Fund may invest in floating rate investments and investments that are the economic equivalent of floating rate investments. These investments may include, but are not limited to, any combination of the following securities: (i) senior secured floating rate loans or debt; (ii) second lien or other subordinated or unsecured floating rate loans or debt; and (iii) fixed-rate loans or debt with respect to which the Fund has entered into derivative instruments to effectively convert the fixed-rate interest payments into floating rate interest payments. |

| ■ | Illiquid Investments — The Fund may invest up to an aggregate amount of 15% of its net assets in illiquid investments. An illiquid investment is any investment that the Fund reasonably expects cannot be sold or disposed of in current market conditions in seven calendar days or less without the sale or disposition significantly changing the market value of the investment. The Subsidiary will also limit its investment in illiquid investments to 15% of its net assets. In applying the illiquid investments restriction to the Fund, the Fund’s investment in the Subsidiary is considered to be liquid. |

| ■ | Temporary Defensive Strategies — For temporary defensive purposes, the Fund may restrict the markets in which it invests and may invest without limitation in cash, cash equivalents, money market securities, such as U.S. Treasury and agency obligations, other U.S. Government securities, short-term debt obligations of corporate issuers, certificates of deposit, bankers acceptances, commercial paper (short-term, unsecured, negotiable promissory notes of a domestic or foreign issuer) or other high quality fixed-income securities. Temporary defensive positions may affect the Fund’s ability to achieve its investment objective. |

| ■ | Warrants — A warrant gives the Fund the right to buy stock. The warrant specifies the amount of underlying stock, the purchase (or “exercise”) price and the date the warrant expires. The Fund has no obligation to exercise the warrant and buy the stock. A warrant has value only if the Fund is able to exercise it or sell it before it expires. |

| ■ | Inflation-Linked Bonds — The Fund may invest in inflation-linked bonds issued by U.S. and non-U.S. Governments, their agencies or instrumentalities, and corporations. Inflation linked bonds are structured to protect against inflation by linking the bond’s principal and interest payments to an inflation index, such as the Consumer Price Index for Urban Consumers, so that principal and interest adjust to reflect changes in the index. |

| ■ | Commodities Related Investments Risk — Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors |

Table of Contents

| affecting a particular industry or commodity, such as drought, floods, weather, embargoes, tariffs and international economic, political and regulatory developments. | |

| ■ | Convertible Securities Risk — The market value of a convertible security performs like that of a regular debt security; that is, if market interest rates rise, the value of a convertible security usually falls. In addition, convertible securities are subject to the risk that the issuer will not be able to pay interest or dividends when due, and their market value may change based on changes in the issuer’s credit rating or the market’s perception of the issuer’s creditworthiness. Since it derives a portion of its value from the common stock into which it may be converted, a convertible security is also subject to the same types of market and issuer risks that apply to the underlying common stock. |

| ■ | Corporate Loans Risk — Commercial banks and other financial institutions or institutional investors make corporate loans to companies that need capital to grow or restructure. Borrowers generally pay interest on corporate loans at rates that change in response to changes in market interest rates such as the London Interbank Offered Rate or the prime rates of U.S. banks. As a result, the value of corporate loan investments is generally less exposed to the adverse effects of shifts in market interest rates than investments that pay a fixed rate of interest. However, because the trading market for certain corporate loans may be less developed than the secondary market for bonds and notes, the Fund may experience difficulties in selling its corporate loans. Transactions in corporate loans may settle on a delayed basis. As a result, the proceeds from the sale of corporate loans may not be readily available to make additional investments or to meet the Fund’s redemption obligations. To the extent the extended settlement process gives rise to short-term liquidity needs, the Fund may hold additional cash, sell investments or temporarily borrow from banks and other lenders. Leading financial institutions often act as agent for a broader group of lenders, generally referred to as a syndicate. The syndicate’s agent arranges the corporate loans, holds collateral and accepts payments of principal and interest. If the agent develops financial problems, the Fund may not recover its investment or recovery may be delayed. By investing in a corporate loan, the Fund may become a member of the syndicate. |

| The market for corporate loans may be subject to irregular trading activity and wide bid/ask spreads. | |

| The corporate loans in which the Fund invests are subject to the risk of loss of principal and income. Although borrowers frequently provide collateral to secure repayment of these obligations they do not always do so. If they do provide collateral, the value of the collateral may not completely cover the borrower’s obligations at the time of a default. If a borrower files for protection from its creditors under the U.S. bankruptcy laws, these laws may limit the Fund’s rights to its collateral. In addition, the value of collateral may erode during a bankruptcy case. In the event of a bankruptcy, the holder of a corporate loan may not recover its principal, may experience a long delay in recovering its investment and may not receive interest during the delay. | |

| ■ | Debt Securities Risk — Debt securities, such as bonds, involve interest rate risk, credit risk, extension risk, and prepayment risk, among other things. |

| Interest Rate Risk — The market value of bonds and other fixed-income securities changes in response to interest rate changes and other factors. Interest rate risk is the risk that prices of bonds and other fixed-income securities will increase as interest rates fall and decrease as interest rates rise. | |

| The Fund may be subject to a greater risk of rising interest rates due to the current period of historically low rates. For example, if interest rates increase by 1%, assuming a current portfolio duration of ten years, and all other factors being equal, the value of the Fund’s investments would be expected to decrease by 10%. The magnitude of these fluctuations in the market price of bonds and other fixed-income securities is generally greater for those securities with longer maturities. Fluctuations in the market price of the Fund’s investments will not affect interest income derived from instruments already owned by the Fund, but will be reflected in the Fund’s net asset value. The Fund may lose money if short-term or long-term interest rates rise sharply in a manner not anticipated by Fund management. | |

| To the extent the Fund invests in debt securities that may be prepaid at the option of the obligor (such as mortgage-backed securities), the sensitivity of such securities to changes in interest rates may increase (to the detriment of the Fund) when interest rates rise. Moreover, because rates on certain floating rate debt securities typically reset only periodically, changes in prevailing interest rates (and particularly sudden and significant changes) can be expected to cause some fluctuations in the net asset value of the Fund to the extent that it invests in floating rate debt securities. | |

| These basic principles of bond prices also apply to U.S. Government securities. A security backed by the “full faith and credit” of the U.S. Government is guaranteed only as to its stated interest rate and face value at maturity, not its current market price. Just like other fixed-income securities, government-guaranteed securities will fluctuate in value when interest rates change. |

Table of Contents

| Following the financial

crisis that began in 2007, the Federal Reserve has attempted to stabilize the economy and support the economic recovery by keeping the federal funds rate (the interest rate at which depository institutions lend reserve balances to other depository

institutions overnight) at or near zero percent. In addition, as part of its monetary stimulus program known as quantitative easing, the Federal Reserve has purchased on the open market large quantities of securities issued or guaranteed by the U.S.

Government, its agencies or instrumentalities. As the Federal Reserve “tapers” or reduces the amount of securities it purchases pursuant to quantitative easing, and/or if the Federal Reserve raises the federal funds rate, there is a risk

that interest rates will rise. A general rise in interest rates has the potential to cause investors to move out of fixed-income securities on a large scale, which may increase redemptions from mutual funds that hold large amounts of fixed-income

securities. Heavy redemptions could cause the Fund to sell assets at inopportune times or at a loss or depressed value and could hurt the Fund’s performance. | |

| During periods of very low or negative interest rates, the Fund may be unable to maintain positive returns. Certain countries have recently experienced negative interest rates on certain fixed-income instruments. Very low or negative interest rates may magnify interest rate risk. Changing interest rates, including rates that fall below zero, may have unpredictable effects on markets, may result in heightened market volatility and may detract from Fund performance to the extent the Fund is exposed to such interest rates. | |

| Credit Risk — Credit risk refers to the possibility that the issuer of a debt security (i.e., the borrower) will not be able to make payments of interest and principal when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. The degree of credit risk depends on both the financial condition of the issuer and the terms of the obligation. | |

| Extension Risk — When interest rates rise, certain obligations will be paid off by the obligor more slowly than anticipated, causing the value of these obligations to fall. Rising interest rates tend to extend the duration of securities, making them more sensitive to changes in interest rates. The value of longer-term securities generally changes more in response to changes in interest rates than shorter-term securities. As a result, in a period of rising interest rates, securities may exhibit additional volatility and may lose value. | |

| Prepayment Risk — When interest rates fall, certain obligations will be paid off by the obligor more quickly than originally anticipated, and the Fund may have to invest the proceeds in securities with lower yields. In periods of falling interest rates, the rate of prepayments tends to increase (as does price fluctuation) as borrowers are motivated to pay off debt and refinance at new lower rates. During such periods, reinvestment of the prepayment proceeds by the management team will generally be at lower rates of return than the return on the assets that were prepaid. Prepayment reduces the yield to maturity and the average life of the security. | |

| ■ | Derivatives Risk — The Fund’s use of derivatives may increase its costs, reduce the Fund’s returns and/or increase volatility. Derivatives involve significant risks, including: |

| Volatility Risk — The Fund’s use of derivatives may reduce the Fund’s returns and/or increase volatility. Volatility is defined as the characteristic of a security, an index or a market to fluctuate significantly in price within a short time period. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate with the overall securities markets. | |

| Counterparty Risk — Derivatives are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. | |

| Market and Illiquidity Risk — Some derivatives are more sensitive to interest rate changes and market price fluctuations than other securities. The possible lack of a liquid secondary market for derivatives and the resulting inability of the Fund to sell or otherwise close a derivatives position could expose the Fund to losses and could make derivatives more difficult for the Fund to value accurately. The Fund could also suffer losses related to its derivatives positions as a result of unanticipated market movements, which losses are potentially unlimited. Finally, BlackRock may not be able to predict correctly the direction of securities prices, interest rates and other economic factors, which could cause the Fund’s derivatives positions to lose value. | |

| Valuation Risk — Valuation may be more difficult in times of market turmoil since many investors and market makers may be reluctant to purchase complex instruments or quote prices for them. Derivatives may also expose the Fund to greater risk and increase its costs. Certain transactions in derivatives involve substantial leverage risk and may expose the Fund to potential losses that exceed the amount originally invested by the Fund. | |

| Hedging Risk — When a derivative is used as a hedge against a position that the Fund holds, any loss generated by the derivative generally should be substantially offset by gains on the hedged investment, and vice versa. While hedging can reduce or eliminate losses, it can also reduce or eliminate gains. Hedges are sometimes subject to |

Table of Contents

| imperfect matching between the derivative and the underlying security, and there can be no assurance that the Fund’s hedging transactions will be effective. The use of hedging may result in certain adverse tax consequences noted below. | |

| Tax Risk — The federal income tax treatment of a derivative may not be as favorable as a direct investment in an underlying asset and may adversely affect the timing, character and amount of income the Fund realizes from its investments. As a result, a larger portion of the Fund’s distributions may be treated as ordinary income rather than capital gains. In addition, certain derivatives are subject to mark-to-market or straddle provisions of the Internal Revenue Code of 1986, as amended. If such provisions are applicable, there could be an increase (or decrease) in the amount of taxable dividends paid by the Fund. In addition, the tax treatment of certain derivatives, such as swaps, is unsettled and may be subject to future legislation, regulation or administrative pronouncements issued by the Internal Revenue Service (the “IRS”). | |

| Regulatory Risk — Derivative contracts, including, without limitation, swaps, currency forwards and non-deliverable forwards, are subject to regulation under the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) in the United States and under comparable regimes in Europe, Asia and other non-U.S. jurisdictions. Under the Dodd-Frank Act, certain derivatives are subject to margin requirements and swap dealers are required to collect margin from the Fund with respect to such derivatives. Specifically, regulations are now in effect that require swap dealers to post and collect variation margin (comprised of specified liquid instruments and subject to a required haircut) in connection with trading of over-the-counter (“OTC”) swaps with the Fund. Shares of investment companies (other than certain money market funds) may not be posted as collateral under these regulations. Requirements for posting of initial margin in connection with OTC swaps will be phased-in through at least 2021. In addition, regulations adopted by global prudential regulators that are now in effect require certain bank-regulated counterparties and certain of their affiliates to include in certain financial contracts, including many derivatives contracts, terms that delay or restrict the rights of counterparties, such as the Fund, to terminate such contracts, foreclose upon collateral, exercise other default rights or restrict transfers of credit support in the event that the counterparty and/or its affiliates are subject to certain types of resolution or insolvency proceedings. The implementation of these requirements with respect to derivatives, as well as regulations under the Dodd-Frank Act regarding clearing, mandatory trading and margining of other derivatives, may increase the costs and risks to the Fund of trading in these instruments and, as a result, may affect returns to investors in the Fund. | |

| Future regulatory developments may impact the Fund’s ability to invest or remain invested in certain derivatives. Legislation or regulation may also change the way in which the Fund itself is regulated. BlackRock cannot predict the effects of any new governmental regulation that may be implemented on the ability of the Fund to use swaps or any other financial derivative product, and there can be no assurance that any new governmental regulation will not adversely affect the Fund’s ability to achieve its investment objective. | |

| Risks Specific to Certain Derivatives Used by the Funds |

Table of Contents