Form 424B2 BARCLAYS BANK PLC

Tweet

Tweet Share

Share

| Pricing Supplement No. 2820 (To the Prospectus dated August 1, 2019, the Prospectus Supplement dated August 1, 2019 and the Product Supplement EQUITY LIRN-1 dated August 26, 2019) |

Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-232144 |

2,446,910 Units |

Pricing Date Settlement Date Maturity Date |

January 30, 2020 February 6, 2020 January 28, 2022 |

|

Leveraged Index Return Notes® Linked to an International Equity Index Basket § Maturity of approximately two years § 131% leveraged upside exposure to increases in the Basket § 1-to-1 downside exposure to decreases in the Basket beyond a 10.00% decline, with up to 90.00% of your principal at risk § The Basket is comprised of the EURO STOXX 50® Index, the FTSE® 100 Index, the Nikkei 225 Index, the Swiss Market Index, the S&P/ASX 200 Index, and the Hang Seng® Index. The EURO STOXX 50® Index was given an initial weight of 40%, each of the FTSE® 100 Index and the Nikkei 225 Index was given an initial weight of 20%, each of the Swiss Market Index and the S&P/ASX 200 Index was given an initial weight of 7.5%, and the Hang Seng® Index was given an initial weight of 5% § All payments occur at maturity and are subject to the credit risk of Barclays Bank PLC § No periodic interest payments § In addition to the underwriting discount set forth below, the notes include a hedging-related charge of $0.075 per unit. See “Structuring the Notes” § Limited secondary market liquidity, with no exchange listing § The notes are our unsecured and unsubordinated obligations and are not deposit liabilities of Barclays Bank PLC. The notes are not covered by the U.K. Financial Services Compensation Scheme or insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency or deposit insurance agency of the United States, the United Kingdom, or any other jurisdiction. |

The notes are being issued by Barclays Bank PLC (“Barclays”). There are important differences between the notes and a conventional debt security, including different investment risks. See “Risk Factors” beginning on page TS-7 of this term sheet, beginning on page PS-7 of product supplement EQUITY LIRN-1 and beginning on page S-7 of the prospectus supplement.

Our initial estimated value of the notes, based on our internal pricing models, is $9.71 per unit on the pricing date, which is less than the public offering price listed below. See “Summary” on the following page, “Risk Factors” beginning on page TS-7 of this term sheet and “Structuring the Notes” on page TS-33 of this term sheet.

Notwithstanding any other agreements, arrangements or understandings between Barclays and any holder or beneficial owner of the notes, by acquiring the notes, each holder and beneficial owner of the notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority. All payments are subject to the risk of exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. See “Consent to U.K. Bail-in Power” on page TS-3 and “Risk Factors” beginning on page TS-7 of this term sheet.

_________________________

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or determined if this Note Prospectus (as defined below) is truthful or complete. Any representation to the contrary is a criminal offense.

_________________________

| Per Unit | Total | |

| Public offering price | $ 10.00 | $ 24,469,100.00 |

| Underwriting discount | $ 0.20 | $ 489,382.00 |

| Proceeds, before expenses, to Barclays | $ 9.80 | $ 23,979,718.00 |

The notes:

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

BofA Securities

January 30, 2020

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

Summary

The Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 (the “notes”) are our unsecured and unsubordinated obligations and are not deposit liabilities of Barclays. The notes are not covered by the U.K. Financial Services Compensation Scheme or insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency or deposit insurance agency of the United States, the United Kingdom or any other jurisdiction. The notes will rank equally with all of our other unsecured and unsubordinated debt. Any payments due on the notes, including any repayment of principal, will be subject to the credit risk of Barclays and to the risk of exercise of any U.K. Bail-in Power (as described herein) or any other resolution measure by any relevant U.K. resolution authority. The notes provide you a leveraged return if the Ending Value of the Market Measure, which is the international equity index basket described below (the “Basket”), is greater than the Starting Value. If the Ending Value is equal to or less than the Starting Value but greater than or equal to the Threshold Value, you will receive the principal amount of your notes. If the Ending Value is less than the Threshold Value, you will lose a portion, which could be significant, of the principal amount of your notes. Any payments on the notes will be calculated based on the $10 principal amount per unit and will depend on the performance of the Basket, subject to our credit risk. See “Terms of the Notes” below.

The Basket is comprised of the EURO STOXX 50® Index, the FTSE® 100 Index, the Nikkei 225 Index, the Swiss Market Index, the S&P/ASX 200 Index, and the Hang Seng® Index (each a “Basket Component”). On the pricing date, the EURO STOXX 50® Index was given an initial weight of 40%, each of the FTSE® 100 Index and the Nikkei 225 Index was given an initial weight of 20%, each of the Swiss Market Index and the S&P/ASX 200 Index was given an initial weight of 7.5%, and the Hang Seng® Index was given an initial weight of 5%.

On the cover page of this term sheet, we have provided the estimated value for the notes. This estimated value was determined based on our internal pricing models, which take into account a number of variables, including volatility, interest rates and our internal funding rates, which are our internally published borrowing rates, and the economic terms of certain related hedging arrangements. This estimated value is less than the public offering price.

The economic terms of the notes (including the Participation Rate) are based on our internal funding rates, which may vary from the levels at which our benchmark debt securities trade in the secondary market, and the economic terms of certain related hedging arrangements. The difference between these rates, as well as the underwriting discount, the hedging-related charge and other amounts described below, reduced the economic terms of the notes. For more information about the estimated value and the structuring of the notes, see “Structuring the Notes” on page TS-33.

| Terms of the Notes | Redemption Amount Determination | |

| Issuer: | Barclays Bank PLC (“Barclays ”) | On the maturity date, you will receive a cash payment per unit determined as follows: |

| Principal Amount: | $10.00 per unit |  |

| Term: | Approximately two years | |

| Market Measure: | An international equity index basket comprised of the EURO STOXX 50® Index (Bloomberg symbol: “SX5E”), the FTSE® 100 Index (Bloomberg symbol: “UKX”), the Nikkei 225 Index (Bloomberg symbol: “NKY”), the Swiss Market Index (Bloomberg symbol: “SMI”), the S&P/ASX 200 Index (Bloomberg symbol: “AS51”) and the Hang Seng® Index (Bloomberg symbol: “HSI”). Each Basket Component is a price return index. | |

| Starting Value: | 100 | |

| Ending Value: | The average of the values of the Market Measure on each calculation day occurring during the Maturity Valuation Period. The scheduled calculation days are subject to postponement in the event of Market Disruption Events, as described beginning on page PS-25 of product supplement EQUITY LIRN-1. | |

| Threshold Value: | 90.00 (90.00% of the Starting Value) | |

| Participation Rate: | 131% | |

| Maturity Valuation Period: | January 18, 2022, January 19, 2022, January 20, 2022, January 21, 2022 and January 24, 2022 | |

| Fees Charged: | The public offering price of the notes includes the underwriting discount of $0.20 per unit as listed on the cover page and a hedging-related charge of $0.075 per unit described in “Structuring the Notes” on page TS-33. | |

| Calculation Agents: | Barclays and BofA Securities, Inc. (“BofAS”). | |

| Leveraged Index Return Notes® | TS-2 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The terms and risks of the notes are contained in this term sheet and the documents listed below (together, the “Note Prospectus”). The documents have been filed as part of a registration statement with the SEC, which may, without cost, be accessed on the SEC website as indicated below or obtained from Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”) or BofAS by calling 1-800-294-1322:

| § | Product supplement EQUITY LIRN-1 dated August 26, 2019: http://www.sec.gov/Archives/edgar/data/312070/000095010319011129/dp111576_424b2-equitylirn1.htm |

| § | Series A MTN prospectus supplement dated August 1, 2019: http://www.sec.gov/Archives/edgar/data/312070/000095010319010190/dp110493_424b2-prosupp.htm |

| § | Prospectus dated August 1, 2019: http://www.sec.gov/Archives/edgar/data/312070/000119312519210880/d756086d424b3.htm |

Before you invest, you should read the Note Prospectus, including this term sheet, for information about us and this offering. Any prior or contemporaneous oral statements and any other written materials you may have received are superseded by the Note Prospectus. Capitalized terms used but not defined in this term sheet have the meanings set forth in product supplement EQUITY LIRN-1. Unless otherwise indicated or unless the context requires otherwise, all references in this document to “we,” “us,” “our” or similar references are to Barclays.

Consent to U.K. Bail-in Power

Notwithstanding any other agreements, arrangements or understandings between us and any holder or beneficial owner of the notes, by acquiring the notes, each holder and beneficial owner of the notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority.

Under the U.K. Banking Act 2009, as amended, the relevant U.K. resolution authority may exercise a U.K. Bail-in Power in circumstances in which the relevant U.K. resolution authority is satisfied that the resolution conditions are met. These conditions include that a U.K. bank or investment firm is failing or is likely to fail to satisfy the Financial Services and Markets Act 2000 (the “FSMA”) threshold conditions for authorization to carry on certain regulated activities (within the meaning of section 55B FSMA) or, in the case of a U.K. banking group company that is a European Economic Area (“EEA”) or third country institution or investment firm, that the relevant EEA or third country relevant authority is satisfied that the resolution conditions are met in respect of that entity.

The U.K. Bail-in Power includes any write-down, conversion, transfer, modification and/or suspension power, which allows for (i) the reduction or cancellation of all, or a portion, of the principal amount of, any interest on, or any other amounts payable on, the notes; (ii) the conversion of all, or a portion, of the principal amount of, any interest on, or any other amounts payable on, the notes into shares or other securities or other obligations of Barclays or another person (and the issue to, or conferral on, the holder or beneficial owner of the notes such shares, securities or obligations); and/or (iii) the amendment or alteration of the maturity of the notes, or amendment of the amount of any interest or any other amounts due on the notes, or the dates on which any interest or any other amounts become payable, including by suspending payment for a temporary period; which U.K. Bail-in Power may be exercised by means of a variation of the terms of the notes solely to give effect to the exercise by the relevant U.K. resolution authority of such U.K. Bail-in Power. Each holder and beneficial owner of the notes further acknowledges and agrees that the rights of the holders or beneficial owners of the notes are subject to, and will be varied, if necessary, solely to give effect to, the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. For the avoidance of doubt, this consent and acknowledgment is not a waiver of any rights holders or beneficial owners of the notes may have at law if and to the extent that any U.K. Bail-in Power is exercised by the relevant U.K. resolution authority in breach of laws applicable in England.

For more information, please see “Risk Factors” below as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement.

| Leveraged Index Return Notes® | TS-3 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

Investor Considerations

| You may wish to consider an investment in the notes if: | The notes may not be an appropriate investment for you if: |

|

§ You anticipate that the value of the Basket will increase from the Starting Value to the Ending Value.

§ You are willing to risk a loss of principal and return if the value of the Basket decreases from the Starting Value to an Ending Value that is below the Threshold Value.

§ You are willing to forgo the interest payments that are paid on traditional interest bearing debt securities.

§ You are willing to forgo dividends or other benefits of owning the stocks included in the Basket Components.

§ You are willing to accept a limited or no market for sales prior to maturity, and understand that the market prices for the notes, if any, will be affected by various factors, including our actual and perceived creditworthiness, the inclusion in the public offering price of the underwriting discount, the hedging-related charge and other amounts, as described on page TS-2.

§ You are willing to assume our credit risk, as issuer of the notes, for all payments under the notes, including the Redemption Amount.

§ You are willing to consent to the exercise of any U.K. Bail-in Power by U.K. resolution authorities.

|

§ You believe that the value of the Basket will decrease from the Starting Value to the Ending Value or that it will not increase sufficiently over the term of the notes to provide you with your desired return.

§ You seek 100% principal repayment or preservation of capital.

§ You seek interest payments or other current income on your investment.

§ You want to receive dividends or other distributions paid on the stocks included in the Basket Components.

§ You seek an investment for which there will be a liquid secondary market.

§ You are unwilling or are unable to take market risk on the notes or to take our credit risk as issuer of the notes.

§ You are unwilling to consent to the exercise of any U.K. Bail-in Power by U.K. resolution authorities.

|

We urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| Leveraged Index Return Notes® | TS-4 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

Hypothetical Payout Profile

Leveraged Index Return Notes®

|

This graph reflects the returns on the notes, based on the Participation Rate of 131% and the Threshold Value of 90% of the Starting Value. The green line reflects the returns on the notes, while the dotted gray line reflects the returns of a direct investment in the stocks included in the Basket Components, excluding dividends.

This graph has been prepared for purposes of illustration only.

|

Hypothetical Payments at Maturity

The following table and examples are for purposes of illustration only. They are based on hypothetical values and show hypothetical returns on the notes. The following table is based on the Starting Value of 100, the Threshold Value of 90 and the Participation Rate of 131%. It illustrates the effect of a range of hypothetical Ending Values on the Redemption Amount per unit of the notes and the total rate of return to holders of the notes. The actual amount you receive and the resulting total rate of return will depend on the actual Ending Value and term of your investment. The following examples do not take into account any tax consequences from investing in the notes.

For hypothetical historical values of the Basket, see “The Basket” section below. For recent actual levels of the Basket Components, see “The Basket Components” section below. Each Basket Component is a price return index and as such the Ending Value will not include any income generated by dividends paid on the stocks included in any of the Basket Components, which you would otherwise be entitled to receive if you invested in those stocks directly. In addition, all payments on the notes are subject to issuer credit risk.

|

Ending Value |

Percentage Change from the Starting Value to the Ending Value |

Redemption Amount per Unit |

Total Rate of Return on the Notes |

| 0.00 | -100.00% | $1.000 | -90.00% |

| 50.00 | -50.00% | $6.000 | -40.00% |

| 60.00 | -40.00% | $7.000 | -30.00% |

| 70.00 | -30.00% | $8.000 | -20.00% |

| 80.00 | -20.00% | $9.000 | -10.00% |

| 90.00(1) | -10.00% | $10.000 | 0.00% |

| 95.00 | -5.00% | $10.000 | 0.00% |

| 97.00 | -3.00% | $10.000 | 0.00% |

| 100.00(2) | 0.00% | $10.000 | 0.00% |

| 102.00 | 2.00% | $10.262 | 2.62% |

| 105.00 | 5.00% | $10.655 | 6.55% |

| 110.00 | 10.00% | $11.310 | 13.10% |

| 120.00 | 20.00% | $12.620 | 26.20% |

| 130.00 | 30.00% | $13.930 | 39.30% |

| 140.00 | 40.00% | $15.240 | 52.40% |

| 150.00 | 50.00% | $16.550 | 65.50% |

| 160.00 | 60.00% | $17.860 | 78.60% |

| (1) | This is the Threshold Value. |

| (2) | The Starting Value was set to 100.00 on the pricing date. |

| Leveraged Index Return Notes® | TS-5 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

Redemption Amount Calculation Examples

| Example 1 | ||

| The Ending Value is 50.00, or 50.00% of the Starting Value: | ||

| Starting Value: 100.00 | ||

| Threshold Value: 90.00 | ||

| Ending Value: 50.00 | ||

|

Redemption Amount per unit

|

|

| Example 2 |

| The Ending Value is 95.00, or 95.00% of the Starting Value: |

| Starting Value: 100.00 |

| Threshold Value: 90.00 |

| Ending Value: 95.00 |

| Redemption Amount (per unit) = $10.000, the principal amount, since the Ending Value is less than the Starting Value but equal to or greater than the Threshold Value. |

| Example 3 | ||

| The Ending Value is 130.00, or 130.00% of the Starting Value: | ||

| Starting Value: 100.00 | ||

| Ending Value: 130.00 | ||

|

= $13.930 Redemption Amount per unit | |

| Leveraged Index Return Notes® | TS-6 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

Risk Factors

There are important differences between the notes and a conventional debt security. An investment in the notes involves significant risks, including those listed below. You should carefully review the more detailed explanation of risks relating to the notes in the “Risk Factors” sections beginning on page PS-7 of product supplement EQUITY LIRN-1 and page S-7 of the Series A MTN prospectus supplement identified above. We also urge you to consult your investment, legal, tax, accounting, and other advisors before you invest in the notes.

| § | Depending on the performance of the Basket as measured shortly before the maturity date, your investment may result in a loss; there is no guaranteed return of principal. |

| § | Your return on the notes may be less than the yield you could earn by owning a conventional fixed or floating rate debt security of comparable maturity. |

| § | Payments on the notes are subject to our credit risk, and any actual or perceived changes in our creditworthiness are expected to affect the value of the notes. If we become insolvent or are unable to pay our obligations, you may lose your entire investment. |

| § | Payments on the notes are subject to the exercise of U.K. Bail-in Power by the relevant U.K. resolution authority. As described above under “Consent to U.K. Bail-in Power,” the relevant U.K. resolution authority may exercise any U.K. Bail-in Power under the conditions described in such section of this term sheet. If any U.K. Bail-in Power is exercised, you may lose all or a part of the value of your investment in the notes or receive a different security, which may be worth significantly less than the notes and which may have significantly fewer protections than those typically afforded to debt securities. Moreover, the relevant U.K. resolution authority may exercise its authority to implement the U.K. Bail-in Power without providing any advance notice to the holders and beneficial owners of the notes. By your acquisition of the notes, you acknowledge, accept, agree to be bound by, and consent to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority. The exercise of any U.K. Bail-in Power with respect to the notes will not be a default or an Event of Default (as each term is defined in the senior debt securities indenture relating to the notes). The trustee will not be liable for any action that the trustee takes, or abstains from taking, in either case, in accordance with the exercise of the U.K. Bail-in Power with respect to the notes. See “Consent to U.K. Bail-in Power” above as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement for more information. |

| § | Your investment return may be less than a comparable investment directly in the stocks included in the Basket Components. |

| § | The estimated value of your notes is based on our internal pricing models. Our internal pricing models take into account a number of variables and are based on a number of subjective assumptions, which may or may not materialize, typically including volatility, interest rates, and our internal funding rates. These variables and assumptions are not evaluated or verified on an independent basis and may prove to be inaccurate. Different pricing models and assumptions of different financial institutions could provide valuations for the notes that are different from our estimated value. |

| § | The estimated value is based on a number of variables, including volatility, interest rates and our internal funding rates. Our internal funding rates may vary from the levels at which our benchmark debt securities trade in the secondary market. As a result of this difference, the estimated value referenced in this term sheet may be lower if such estimated value was based on the levels at which our benchmark debt securities trade in the secondary market. |

| § | The estimated value of your notes is lower than the public offering price of your notes. This difference is a result of certain factors, such as the inclusion in the public offering price of the underwriting discount, the hedging-related charge, the estimated profit, if any, that we or any of our affiliates expect to earn in connection with structuring the notes, and the estimated cost which we may incur in hedging our obligations under the notes, as further described in “Structuring the Notes” on page TS-33. If you attempt to sell the notes prior to maturity, their market value may be lower than the price you paid for the notes and lower than the estimated value because the secondary market prices take into consideration the levels at which our debt securities trade in the secondary market but do not take into account such fees, charges and other amounts. |

| § | The estimated value of the notes is not a prediction of the prices at which MLPF&S, BofAS or its affiliates, or any of our affiliates or any other third parties may be willing to purchase the notes from you in secondary market transactions. The price at which you may be able to sell your notes in the secondary market at any time will be influenced by many factors that cannot be predicted, such as market conditions, and any bid and ask spread for similar size trades, and may be substantially less than our estimated value of the notes. Any sale prior to the maturity date could result in a substantial loss to you. |

| § | A trading market is not expected to develop for the notes. We, MLPF&S, BofAS and our respective affiliates are not obligated to make a market for, or to repurchase, the notes. There is no assurance that any party will be willing to purchase your notes at any price in any secondary market. |

| § | Our business, hedging and trading activities, and those of MLPF&S, BofAS and our respective affiliates (including trading in securities of companies included in the Basket Components), and any hedging and trading activities we, MLPF&S, BofAS or our respective affiliates engage in for our clients’ accounts, may affect the market value and return of the notes and may create conflicts of interest with you. |

| Leveraged Index Return Notes® | TS-7 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

| § | Changes in the level of one of the Basket Components may be offset by changes in the levels of the other Basket Components. Due to the different Initial Component Weights, changes in the levels of some Basket Components will have a more substantial impact on the value of the Basket than similar changes in the levels of the other Basket Components. |

| § | An index sponsor may adjust the relevant Basket Component in a way that affects its level, and has no obligation to consider your interests. |

| § | You will have no rights of a holder of the securities included in the Basket Components, and you will not be entitled to receive securities or dividends or other distributions by the issuers of those securities. |

| § | While we, MLPF&S, BofAS or our respective affiliates may from time to time own securities of companies included in the Basket Components, except to the extent that the common stock of Barclays PLC is included in the FTSE® 100 Index, we, MLPF&S, BofAS and our respective affiliates do not control any company included in any Basket Component, and have not verified any disclosure made by any other company. |

| § | Your return on the notes may be affected by factors affecting the international securities markets. In addition, you will not obtain the benefit of any increase in the value of any currency in which the securities included in the Basket Components are traded against the U.S. dollar, which you would receive if you had owned the securities included in the Basket Components during the term of your notes, although the value of the notes may be adversely affected by general exchange rate movements in the market. |

| § | There may be potential conflicts of interest involving the calculation agents, one of which is us and one of which is BofAS. We have the right to appoint and remove the calculation agents. |

| § | The U.S. federal income tax consequences of the notes are uncertain, and may be adverse to a U.S. investor of the notes. See “Tax Consequences” below. |

Other Terms of the Notes

Market Measure Business Day

The following definition shall supersede and replace the definition of “Market Measure Business Day” set forth in product supplement EQUITY LIRN-1.

A “Market Measure Business Day” means a day on which:

| (A) | each of the Eurex (as to the EURO STOXX 50® Index), the London Stock Exchange (as to the FTSE® 100 Index), the Tokyo Stock Exchange (as to the Nikkei 225 Index), the SIX Swiss Exchange (as to the Swiss Market Index), the Australian Stock Exchange (as to the S&P/ASX 200 Index), and the Hong Kong Stock Exchange (as to the Hang Seng® Index) (or any successor to the foregoing exchanges) are open for trading; and |

| (B) | the Basket Components or any successors thereto are calculated and published. |

| Leveraged Index Return Notes® | TS-8 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The Basket

The Basket is designed to allow investors to participate in the percentage changes in the levels of the Basket Components from the Starting Value to the Ending Value of the Basket. The Basket Components are described in the section “The Basket Components” below. Each Basket Component was assigned an initial weight on the pricing date, as set forth in the table below.

For more information on the calculation of the value of the Basket, please see the section entitled “Description of LIRNs—Basket Market Measures” beginning on page PS-32 of product supplement EQUITY LIRN-1.

On the pricing date, for each Basket Component, the Initial Component Weight, the closing level, the Component Ratio and the initial contribution to the Basket value were as follows:

| Basket Component | Bloomberg Symbol | Initial Component Weight | Closing Level(1) | Component Ratio(2) | Initial Basket Value Contribution | |||||

| EURO STOXX 50® Index | SX5E | 40.00% | 3,690.78 | 0.01083782 | 40.00 | |||||

| FTSE® 100 Index | UKX | 20.00% | 7,381.96 | 0.00270931 | 20.00 | |||||

| Nikkei 225 Index | NKY | 20.00% | 22,977.75 | 0.00087041 | 20.00 | |||||

| Swiss Market Index | SMI | 7.50% | 10,748.92 | 0.00069774 | 7.50 | |||||

| S&P/ASX 200 Index | AS51 | 7.50% | 7,008.429 | 0.00107014 | 7.50 | |||||

| Hang Seng® Index | HSI | 5.00% | 26,449.13 | 0.00018904 | 5.00 | |||||

| Starting Value | 100.00 |

| (1) | These were the closing levels of the Basket Components on the pricing date. |

| (2) | Each Component Ratio equals the Initial Component Weight of the relevant Basket Component (as a percentage) multiplied by 100, and then divided by the closing level of that Basket Component on the pricing date and rounded to eight decimal places. |

The calculation agents will calculate the value of the Basket by summing the products of the closing level for each Basket Component on each calculation day during the Maturity Valuation Period and the Component Ratio applicable to such Basket Component. If a Market Disruption Event occurs as to any Basket Component on any scheduled calculation day, the closing level of that Basket Component will be determined as more fully described in the section entitled “Description of LIRNs—Basket Market Measures—Ending Value of the Basket” beginning on page PS-35 of product supplement EQUITY LIRN-1.

| Leveraged Index Return Notes® | TS-9 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

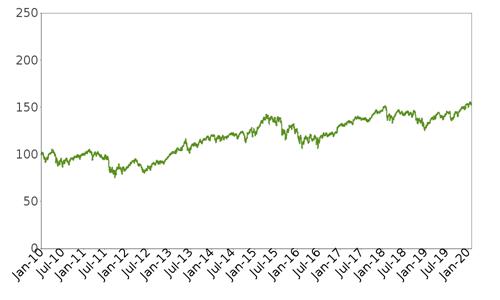

While actual historical information on the Basket did not exist before the pricing date, the following graph sets forth the hypothetical historical performance of the Basket from January 1, 2010 through January 30, 2020. The graph is based upon actual daily historical levels of the Basket Components, hypothetical Component Ratios based on the closing levels of the Basket Components as of December 31, 2009, and a Basket value of 100.00 as of that date. This hypothetical historical data on the Basket is not necessarily indicative of the future performance of the Basket or what the value of the notes may be. Any hypothetical historical upward or downward trend in the value of the Basket during any period set forth below is not an indication that the value of the Basket is more or less likely to increase or decrease at any time over the term of the notes.

Hypothetical Historical Performance of the Basket

| Leveraged Index Return Notes® | TS-10 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The Basket Components

All disclosures contained in this term sheet regarding the Basket Components, including, without limitation, their make-up, method of calculation, and changes in their components, have been derived from publicly available sources without independent verification. The information reflects the policies of, and is subject to change by each of STOXX Limited with respect to the EURO STOXX 50® Index, FTSE Russell (“FTSE”) with respect to the FTSE® 100 Index, Nikkei Inc. with respect to the Nikkei 225 Index, SIX Swiss Exchange Ltd (“SSE”) with respect to the Swiss Market Index, S&P Dow Jones Indices LLC (“S&P Dow Jones”) with respect to the S&P/ASX 200 Index and Hang Seng Indexes Company Limited (“HSI Company Limited”) with respect to the Hang Seng® Index (STOXX Limited, FTSE, Nikkei Inc., SSE, S&P Dow Jones and HSI Company Limited together, the “Index sponsors”). The Index sponsors have no obligation to continue to publish, and may discontinue or suspend the publication of any Basket Component at any time. The consequences of any Index sponsor discontinuing publication of a Basket Component are discussed in the section entitled “Description of LIRNs—Discontinuance of an Index” beginning on page PS-27 of product supplement EQUITY LIRN-1. None of us, the calculation agents, MLPF&S or BofAS accepts any responsibility for the calculation, maintenance or publication of any Basket Component or any successor index.

The EURO STOXX 50® Index

The EURO STOXX 50® Index (the “SX5E”) was created and is calculated, maintained and published by STOXX Limited, a wholly owned subsidiary of Deutsche Börse AG. The euro price return version of the SX5E is reported by Bloomberg L.P. under the ticker symbol “SX5E.”

EURO STOXX 50® Index Composition

The SX5E is a free-float market-capitalization weighted index composed of 50 of the largest stocks in terms of free-float market capitalization traded on the major exchanges of 11 Eurozone countries: Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain. At any given time, some eligible countries may not be represented in the SX5E.

The selection list for the SX5E includes the top 60% of the free-float market capitalization of each of the 19 EURO STOXX® Supersector indices and all current SX5E component stocks. All the stocks on the selection list are ranked in terms of free-float market capitalization. The largest 40 stocks on the selection list are selected for inclusion in the SX5E; the remaining 10 stocks are selected from the largest remaining current stocks ranked between 41 and 60. If the number of stocks selected is still below 50, then the largest remaining stocks are selected until there are 50 stocks.

The composition of the SX5E is reviewed annually in September. The review cut-off date is the last trading day of August. The composition of the SX5E is also reviewed monthly and components that rank 75 or below are replaced and non-component stocks that rank 25 or above are added. In addition, changes to country classification and listing are effective as of the next quarterly review. At that time, the SX5E is adjusted accordingly to remain consistent with its country membership rules by deleting the company where necessary.

EURO STOXX 50® Index Maintenance

The SX5E is also reviewed on an ongoing basis. Corporate actions (including initial public offerings, mergers and takeovers, spin-offs, delistings, bankruptcy, and price and share adjustments) that affect the composition of the SX5E are immediately reviewed. Any changes are announced, implemented and effective in line with the type of corporate action and the magnitude of the effect.

To maintain the number of components constant, a removed company is replaced by the highest-ranked non-component on the selection list. The selection list is updated on a monthly basis according to the review component selection process.

The free-float factors for each component stock used to calculate the SX5E are reviewed, calculated and implemented on a quarterly basis and are fixed until the next quarterly review.

EURO STOXX 50® Index Calculation

The SX5E is calculated with the “Laspeyres formula,” which measures the aggregate price changes in the component stocks against a fixed base quantity weight. The formula for calculating the value of the SX5E can be expressed as follows:

| Index = |

free-float market capitalization of the SX5E | |

| divisor | ||

The “free-float market capitalization of the SX5E” is equal to the sum of the products, for each component stock, of the price, number of shares, free-float factor, weighting cap factor and, if applicable, the exchange rate from the local currency into the index currency of the

| Leveraged Index Return Notes® | TS-11 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

SX5E as of the time that the SX5E is being calculated. The weighting cap factor limits the weight of each component stock within the SX5E to a maximum of 10% at the time of each review.

The free-float factor of each component stock is intended to reduce the number of shares to the actual amount available on the market. All fractions of the total number of shares that are larger than 5% and whose holding is of a long-term nature are excluded from the calculation of the SX5E, including: cross-ownership (stock owned either by the company itself, in the form of treasury shares, or owned by other companies); government ownership (stock owned by either governments or their agencies); private ownership (stock owned by either individuals or families); and restricted shares that cannot be traded during a certain period or have a foreign ownership restriction. Block ownership is not applied for holdings of custodian nominees, trustee companies, mutual funds, investment companies with short-term investment strategies, pension funds and similar entities.

The SX5E is also subject to a divisor, which is adjusted to maintain the continuity of the values of the SX5E despite changes due to corporate actions. The following is a summary of the adjustments to any component stock of the SX5E made for corporate actions and the effect of such adjustment on the divisor of the SX5E, where shareholders of the component stock will receive “B” number of shares for every “A” share held (where applicable).

|

(1) Special cash dividend:

Cash distributions that are outside the scope of the regular dividend policy or that the company defines as an extraordinary distribution

Adjusted price = closing price – dividend announced by the company × (1 – withholding tax if applicable)

Divisor: decreases | |

|

(2) Split and reverse split:

Adjusted price = closing price × A / B

New number of shares = old number of shares × B / A

Divisor: unchanged

| |

|

(3) Rights offering:

If the subscription price is not available or if the subscription price is equal to or greater than the closing price on the day before the effective date, then no adjustment is made.

In case the share increase is greater than or equal to 100% (B / A ≥ 1), the adjustment of the shares and weight factors are delayed until the new shares are listed.

Adjusted price = (closing price × A + subscription price × B) / (A + B)

New number of shares = old number of shares × (A + B) / A

Divisor: increases

| |

|

(4) Stock dividend:

Adjusted price = closing price × A / (A + B)

New number of shares = old number of shares × (A + B) / A

Divisor: unchanged

|

(5) Stock dividend (from treasury stock):

Adjusted only if treated as extraordinary dividend.

Adjusted close = close – close × B / (A + B)

Divisor: decreases

|

|

(6) Stock dividend of another company:

Adjusted price = (closing price × A – price of other company × B) / A

Divisor: decreases

|

(7) Return of capital and share consolidation:

Adjusted price = (closing price – capital return announced by company × (1-withholding tax)) × A / B

New number of shares = old number of shares × B / A

Divisor: decreases

|

|

(8) Repurchase of shares / self-tender:

Adjusted price = ((price before tender × old number of shares) – (tender price × number of tendered shares)) / (old number of shares – number of tendered shares)

New number of shares = old number of shares – number of tendered shares

|

(9) Spin-off:

Adjusted price = (closing price × A – price of spun-off shares × B) / A

Divisor: decreases

|

| Leveraged Index Return Notes® | TS-12 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

| Divisor: decreases | ||

|

(10) Combination stock distribution (dividend or split) and rights offering:

For this corporate action, the following additional assumptions apply:

Shareholders receive B new shares from the distribution and C new shares from the rights offering for every A share held.

If A is not equal to one share, all the following “new number of shares” formulae need to be divided by A:

| ||

|

- If rights are applicable after stock distribution (one action applicable to other):

Adjusted price = (closing price × A + subscription price × C × (1 + B / A)) / ((A + B) × ( 1 + C / A))

New number of shares = old number of shares × ((A + B) × (1 + C / A)) / A

Divisor: increases

|

- If stock distribution is applicable after rights (one action applicable to other):

Adjusted price = (closing price × A + subscription price × C) /((A + C) × (1 + B / A))

New number of shares = old number of shares × ((A + C) × (1 + B / A))

Divisor: increases

| |

|

- Stock distribution and rights (neither action is applicable to the other):

Adjusted price = (closing price × A + subscription price × C) / (A + B + C)

New number of shares = old number of shares × (A + B + C) / A

Divisor: increases

| ||

|

(11) Addition / deletion of a company:

No price adjustments are made. The net change in market capitalization determines the divisor adjustment. |

(12) Free-float and shares changes:

No price adjustments are made. The net change in market capitalization determines the divisor adjustment. | |

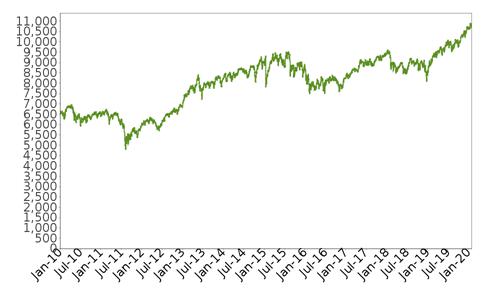

The following graph shows the daily historical performance of the SX5E in the period from January 1, 2010 through January 30, 2020. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On the pricing date, the closing level of the SX5E was 3,690.78.

Historical Performance of the EURO STOXX 50® Index

This historical data on the SX5E is not necessarily indicative of the future performance of the SX5E or what the value of the notes may be. Any historical upward or downward trend in the level of the SX5E during any period set forth above is not an indication that the level of the SX5E is more or less likely to increase or decrease at any time over the term of the notes.

Before investing in the notes, you should consult publicly available sources for the levels of the SX5E.

| Leveraged Index Return Notes® | TS-13 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

License Agreement

We have entered into a non-exclusive license agreement with STOXX Limited whereby we, in exchange for a fee, are permitted to use the SX5E in connection with the notes. STOXX Limited and its licensors (the “Licensors”) have no relationship to Barclays Bank PLC, other than the licensing of indices and the related trademarks for use in connection with the notes.

STOXX Limited and its Licensors do not:

| · | sponsor, endorse, sell or promote the notes; |

| · | recommend that any person invest in the notes or any other securities; |

| · | have any responsibility or liability for or make any decisions about the timing, amount or pricing of the notes. |

| · | have any responsibility or liability for the administration, management or marketing of the notes; or |

| · | consider the needs of the notes or the owners of the notes in determining, composing or calculating the SX5E or have any obligation to do so. |

STOXX Limited and its Licensors will not have any liability in connection with the notes. Specifically,

| · | STOXX Limited and its Licensors do not make any warranty, express or implied and disclaim any and all warranty about: |

| · | the results to be obtained by the notes, the owner of the notes or any other person in connection with the use of the SX5E and the data included in the SX5E; |

| · | the accuracy or completeness of the SX5E and its data; or |

| · | the merchantability and the fitness for a particular purpose or use of the SX5E and its data; |

STOXX Limited and its Licensors will have no liability for any errors, omissions or interruptions in the SX5E or its data; and

Under no circumstances will STOXX Limited or its Licensors be liable for any lost profits or indirect, punitive, special or consequential damages or losses, even if STOXX Limited or its Licensors knows that they might occur.

The licensing agreement between Barclays Bank PLC and STOXX Limited is solely for their benefit and not for the benefit of the owners of the notes or any other third parties.

| Leveraged Index Return Notes® | TS-14 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The FTSE® 100 Index

The FTSE® 100 Index (the “UKX”) is an index calculated, published and disseminated by FTSE, a wholly owned subsidiary of London Stock Exchange Group plc (the “LSEG”). The UKX measures the composite price performance of the 100 largest companies (determined on the basis of market capitalization) traded on the London Stock Exchange (the “LSE”). Publication of the UKX began in January 1984. The UKX is reported by Bloomberg L.P. under the ticker symbol “UKX.”

Composition of the FTSE® 100 Index

The 100 stocks included in the UKX (the “UKX Underlying Stocks”) were selected from a reference group of stocks trading on the LSE that were selected by excluding certain stocks that have low liquidity, public float accuracy, and reliability of prices, or size or have limited voting right by unrestricted shareholders or foreign ownership restrictions. The UKX Underlying Stocks were selected from this reference group by selecting 100 stocks with the largest market value. Where there are multiple lines of listed equity capital in a company, all are included and priced separately, provided that the secondary line’s full market capitalization (i.e. before the application of any investability weightings) is greater than 25% of the full market capitalization of the company’s principal line and the secondary line satisfies the eligibility rules and screens in its own right in all respects. A list of the issuers of the UKX Underlying Stocks is available from FTSE.

Companies are required to have greater than 5% of the company’s voting rights (aggregated across all of its equity securities, including, where identifiable, those that are not listed or trading) in the hands of unrestricted shareholders in order to be eligible for index inclusion. Companies already included in the UKX have a five-year grandfathering period to comply or they will be removed from the UKX in September 2022.

The UKX is overseen and reviewed quarterly by the FTSE Russell Europe, Middle East & Africa Regional Equity Advisory Committee (the “Index Steering Committee”) in order to maintain continuity in the level. The Index Steering Committee undertakes the reviews of the UKX and ensures that constituent changes and index calculations are made in accordance with the ground rules of the UKX. The UKX is reviewed on a quarterly basis in March, June, September and December. Each review is based on data from the close of business on the Tuesday before the first Friday of the review month. Any constituent changes are implemented after the close of business on the third Friday of the review month (i.e. effective Monday), following the expiry of the ICE Futures Europe futures and options contracts.

The UKX Underlying Stocks may be replaced, if necessary, in accordance with deletion/addition rules that provide generally for the removal and replacement of a stock from the UKX if such stock is delisted or its issuer is subject to a takeover offer that has been declared unconditional or it has ceased, in the opinion of the Index Steering Committee, to be a viable component of the UKX. To maintain continuity, a stock will be added at the quarterly review if it has risen to 90th place or above and a stock will be deleted if at the quarterly review it has fallen to 111th place or below, in each case ranked on the basis of market capitalization. A constant number of constituents will be maintained for the UKX. Where a greater number of companies qualify to be inserted in the UKX than those qualifying to be deleted, the lowest ranking constituents presently included in the UKX will be deleted to ensure that an equal number of companies are inserted and deleted at the periodic review. Likewise, where a greater number of companies qualify to be deleted than those qualifying to be inserted, the securities of the highest ranking companies which are presently not included in the UKX will be inserted to match the number of companies being deleted at the periodic review.

Companies that are large enough to be constituents of the UKX but do not pass the liquidity test are excluded. They will remain ineligible until the next annual review in June when they will be re-tested against all eligibility screens.

Calculation of the FTSE® 100 Index

The UKX is an arithmetic weighted index where the weights are the market capitalization of each company. The UKX is calculated by summing the free float adjusted market values (or capitalizations) of all companies within the UKX divided by the divisor. On the base date, the divisor is calculated as the sum of the market capitalizations of the UKX constituents divided by the initial index value of 1,000. The divisor is subsequently adjusted for any capital changes in the UKX constituents. In order to prevent discontinuities in the UKX in the event of a corporate action or change in constituents, it is necessary to make an adjustment to the prices used to calculate the UKX to ensure that the change in index between two consecutive dates reflects only market movements rather than including change due to the impact of corporate actions or constituent changes. This ensures that the UKX values remain comparable over time and that changes in the UKX level properly reflect the change in value of a portfolio of index constituents with weights the same as in the UKX.

| Leveraged Index Return Notes® | TS-15 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The following graph shows the daily historical performance of the UKX in the period from January 1, 2010 through January 30, 2020. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On the pricing date, the closing level of the UKX was 7,381.96.

Historical Performance of the FTSE® 100 Index

This historical data on the UKX is not necessarily indicative of the future performance of the UKX or what the value of the notes may be. Any historical upward or downward trend in the level of the UKX during any period set forth above is not an indication that the level of the UKX is more or less likely to increase or decrease at any time over the term of the notes.

Before investing in the notes, you should consult publicly available sources for the levels of the UKX.

License Agreement

We have entered into a non-exclusive license agreement with FTSE whereby we, in exchange for a fee, are permitted to use the UKX in connection with certain securities, including the notes. We are not affiliated with FTSE; the only relationship between FTSE and us is any licensing of the use of FTSE’s indices and trademarks relating to them.

The notes are not in any way sponsored, endorsed, sold or promoted by FTSE or by the London Stock Exchange Group companies (“LSEG”) (together the “Licensor Parties”) and none of the Licensor Parties make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as (i) to the results to be obtained from the use of the UKX, (ii) the figure at which the UKX stands at any particular time on the particular day or otherwise, or (iii) the suitability of the UKX for the purpose to which it is being put in connection with the notes. None of the Licensor Parties have provided or will provide any financial or investment advice or recommendation in relation to the UKX to Barclays Bank PLC or to its clients. The UKX is calculated by FTSE or its agent. None of the Licensor Parties shall be (a) liable (whether in negligence or otherwise) to any person for any error in the UKX or (b) be under any obligation to advise any person of any error therein.

“FTSE®,” “FT-SE®” and “Footsie®” are trademarks of LSEG and are used by FTSE under license. “All-World,” “All-Share” and “All-Small” are trademarks of FTSE.

| Leveraged Index Return Notes® | TS-16 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The Nikkei 225 Index

The Nikkei 225 Index (the “NKY”) is a stock index that measures the composite price performance of selected Japanese stocks. The NKY is currently based on 225 underlying stocks (the “Nikkei Underlying Stocks”) trading on the Tokyo Stock Exchange (“TSE”) representing a broad cross-section of Japanese industries. Non-ordinary shares, such as shares of exchange-traded funds, real estate investment trusts, preferred stock or other preferred securities or tracking stocks, are excluded from the NKY. The NKY is reported by Bloomberg L.P. under the ticker symbol “NKY.”

All 225 Nikkei Underlying Stocks are stocks listed in the First Section of the TSE. Stocks listed in the First Section of the TSE are among the most actively traded stocks on the TSE. Nikkei Inc. rules require that the 75 most liquid issues (one-third of the component count of the NKY) be included in the NKY. Nikkei Inc. first calculated and published the NKY in 1970.

Rules of the Periodic Review

Nikkei Underlying Stocks are reviewed annually (the “periodic review”) in accordance with the following rules, and results of the review are applied on the first trading day in October. Results of the review become effective on the first trading day of October, and there is no limit to the number of Nikkei Underlying Stocks that can be affected. Stocks selected by the procedures outlined below are presented as candidates to a committee composed of academics and market professionals for comment; based on comments from the committee, Nikkei Inc. determines and announces any changes to the Nikkei Underlying Stocks.

High Liquidity Group

The top 450 most liquid stocks are chosen from the TSE First Section. For purposes of this selection, liquidity is measured by (i) trading volume in the preceding 5-year period and (ii) the magnitude of price fluctuation by volume in the preceding 5-year period. These 450 stocks constitute the “High Liquidity Group” for the review. Those Nikkei Underlying Stocks that are not in the High Liquidity Group are removed. Those stocks that are not currently Nikkei Underlying Stocks but that are in the top 75 of the High Liquidity Group are added.

Sector Balance

The High Liquidity Group is then categorized into the following six sectors: Technology, Financials, Consumer Goods, Materials, Capital Goods/Others, and Transportation and Utilities. These six sector categories are further divided into 36 industrial classifications as follows:

| · | Technology — Pharmaceuticals, Electrical Machinery, Automobiles & Auto Parts, Precision Instruments and Telecommunications; |

| · | Financials — Banks, Other Financial Services, Securities and Insurance; |

| · | Consumer Goods — Fishery, Food, Retail and Services; |

| · | Materials — Mining, Textiles & Apparel, Paper & Pulp, Chemicals, Petroleum, Rubber, Ceramics, Steel, Nonferrous Metals and Trading Companies; |

| · | Capital Goods/Others — Construction, Machinery, Shipbuilding, Transportation Equipment, Other Manufacturing and Real Estate; and |

| · | Transportation/Utilities — Railway & Transport, Marine Transport, Air Transport, Warehousing, Electric Power and Gas. |

The “appropriate number” of constituents for each sector is defined to be half the number of stocks in that sector. After the liquidity-based adjustments, discussed above, a rebalancing is conducted if any of the sectors are over- or under-represented. The degree of representation is evaluated by comparing the actual number of constituents in the sector against the appropriate number for that sector.

For over-represented sectors, current constituents in the sector are deleted in the order of liquidity (lowest liquidity first) to correct the overage. For under-represented sectors, non-constituent stocks are added from the High Liquidity Group in the order of liquidity (highest liquidity first) to correct the shortage.

Extraordinary Replacement Rules

Nikkei Underlying Stocks removed from the TSE First Section are deleted from the NKY. Reasons for removal from the TSE First Section include: designation to “securities to be delisted” (i.e., “Seiri Meigara”) or delisting due to bankruptcy (including filing under the Corporate Reorganization Act, Civil Rehabilitation Act or liquidation), delisting due to corporate restructuring such as merger, share exchange or share transfer, designation to “securities to be delisted” or actual delisting due to excess debt or transfer to the TSE Second Section. In addition, constituents designated to “securities under supervision” (i.e., “Kanri Meigara”) become deletion candidates. However, the decision to delete such candidates will be made by examining the sustainability and the probability of delisting for each individual case.

| Leveraged Index Return Notes® | TS-17 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

When a Nikkei Underlying Stock is deleted from the NKY as outlined in the preceding paragraph, a new Nikkei Underlying Stock will be selected and added, in principle, from the same sector of the High Liquidity Group in order of liquidity. Notwithstanding the foregoing, the following rules may apply depending on the timing and circumstances of the deletion: (i) when such deletion is scheduled close to the periodic review, additional stocks may be selected as part of the periodic review process and (ii) when multiple deletions are scheduled in a season other than the periodic review, additions may be selected using the liquidity and sector balancing rules outlined above.

Procedures to Implement Constituent Changes

As a general rule, for both the periodic review and the extraordinary replacement rules, additions and deletions are made effective on the same day in order to keep the number of Nikkei Underlying Stocks 225. However, under the circumstances outlined below, when an addition cannot be made on the same day as a deletion, the NKY may be calculated with fewer than 225 Nikkei Underlying Stocks. In this case, the divisor is adjusted to ensure continuity.

The first instance when the NKY may be calculated with fewer than 225 Nikkei Underlying Stocks is when a Nikkei Underlying Stock is delisted by reason of share exchange or transfer and the succeeding company becomes listed a short period of time later. The second instance is when a Nikkei Underlying Stock is deleted due to a sudden announcement of bankruptcy or is designated as a “security to be delisted.” The addition will be made after a short period (approximately 2 days). The exact schedule is announced on a case by case basis.

Calculation of the Nikkei 225 Index

The NKY is a modified, price-weighted index (i.e., a Nikkei Underlying Stock’s weight in the index is based on its price per share rather than the total market capitalization of the issuer) that is calculated by (i) multiplying the per share price of each Nikkei Underlying Stock by the corresponding weighting factor for such Nikkei Underlying Stock (a “Weight Factor”), (ii) calculating the sum of all these products and (iii) dividing such sum by a divisor (the “Divisor”). The Divisor is subject to periodic adjustments as set forth below. Each Weight Factor is computed by dividing ¥50 by the par value of the relevant Nikkei Underlying Stock, so that the share price of each Nikkei Underlying Stock when multiplied by its Weight Factor corresponds to a share price based on a uniform par value of ¥50. The stock prices used in the calculation of the NKY are those reported by a primary market for the Nikkei Underlying Stocks (currently the TSE). The level of the NKY is calculated every 5 seconds.

In order to maintain continuity in the NKY in the event of certain changes due to non-market factors affecting the Nikkei Underlying Stocks, such as the addition or deletion of stocks, substitution of stocks, stock splits or distributions of assets to stockholders, the Divisor used in calculating the NKY is adjusted in a manner designed to prevent any instantaneous change or discontinuity in the level of the NKY. Thereafter, the Divisor remains at the new value until a further adjustment is necessary as the result of another change. As a result of such change affecting any Nikkei Underlying Stock, the Divisor is adjusted in such a way that the sum of all share prices immediately after such change multiplied by the applicable Weight Factor and divided by the new Divisor (i.e., the level of the NKY immediately after such change) will equal the level of the NKY immediately prior to the change.

| Leveraged Index Return Notes® | TS-18 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The following graph shows the daily historical performance of the NKY in the period from January 1, 2010 through January 30, 2020. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On the pricing date, the closing level of the NKY was 22,977.75.

Historical Performance of the Nikkei 225 Index

This historical data on the NKY is not necessarily indicative of the future performance of the NKY or what the value of the notes may be. Any historical upward or downward trend in the level of the NKY during any period set forth above is not an indication that the level of the NKY is more or less likely to increase or decrease at any time over the term of the notes.

Before investing in the notes, you should consult publicly available sources for the levels of the NKY.

License Agreement

For any specific issuance of securities, we will enter into a non-exclusive license agreement with Nikkei Inc., whereby we, in exchange for a fee, will be permitted to use the NKY in connection with such securities. We are not affiliated with Nikkei Inc.; the only relationship between Nikkei Inc. and us is any licensing of the use of Nikkei Inc.’s indices and trademarks relating to them.

The copyright relating to the NKY and intellectual property rights as to the indications for “Nikkei,” “Nikkei Stock Average” and “Nikkei 225” and any other rights shall belong to Nikkei Inc. Nikkei Inc. will be entitled to change the details of the NKY and to suspend the announcement thereof. All the businesses and implementation relating to our license agreement with Nikkei Inc. will be conducted exclusively at our risk, and Nikkei Inc. assumes no obligation or responsibility therefor.

The notes are not sponsored, endorsed, sold, or promoted by Nikkei Inc., and Nikkei Inc. makes no representation whatsoever, whether express or implied, either as to the results to be obtained from the use of the NKY and/or the levels at which the NKY stands at any particular time on any particular date or otherwise. Nikkei Inc. will not be liable (whether in negligence or otherwise) to any person for any error in the NKY, and Nikkei Inc. is under no obligation to advise any person of any error therein. Nikkei Inc. is making no representation whatsoever, whether express or implied, as to the advisability of purchasing or assuming any risk in connection with the notes.

| Leveraged Index Return Notes® | TS-19 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The Swiss Market Index

The SMI® (the “SMI®”) is a free-float adjusted market capitalization-weighted price return index of the Swiss equity market. The SMI® was standardized on June 30, 1988 with an initial baseline value of 1,500 points. The SMI® is reported by Bloomberg L.P. under the ticker symbol “SMI.”

Composition of the SMI®

The SMI® is composed of the most highly capitalized and liquid stocks of the Swiss Performance Index® (“SPI®”). The SMI® represents more than 75% of the free-float market capitalization of the Swiss equity market.

The SMI® is composed of the 20 highest ranked securities of the SPI®, where the ranking of each security is determined by a combination of the following criteria:

| · | average free-float market capitalization over the last 12 months (compared to the capitalization of the entire SPI®); and |

| · | cumulated on order book turnover over the last 12 months (compared to the total turnover of the SPI®). |

The average market capitalization in percent and the turnover in percent are each given a weighting of 50% and yield the weighted market share. A security is excluded from the SMI® if it ranked 23 or lower in the selection list. To reduce fluctuations in the SMI®, a buffer is applied for securities ranked 19 to 22. Out of the candidates from ranks 19 to 22, current components are selected with priority over the other candidates. New components out of the buffer are selected until 20 components have been reached. Instruments that are primary listed on more than one stock exchange and generate less than 50% of their total turnover at SIX Swiss Exchange, need to fulfill additional liquidity criteria in order to be selectable for the SMI®. For this purpose, all components of the SPI® are ranked based on their cumulated order book turnover over the past 12 months relative to the total turnover of the index universe. For this list, only turnovers of stock exchanges are considered where the instrument is primary listed. Such an instrument with several primary listings must rank among the first 18 components on the order book turnover list in order to be selectable for the SMI®. Such an instrument is excluded from the SMI® once it reaches 23 or lower.

Standards for Admission and Exclusion

To ensure that the composition of the SMI® maintains a high level of continuity, the stocks contained within it are subject to a special admission and exclusion procedure. This is based on the criteria of free-float market capitalization and liquidity. The index-basket adjustments which arise from this procedure are, as a rule, made once per year.

The securities included in the SMI® are weighted according to their free-float. The free-float is calculated only for shares with voting rights. This means that large positions in a security that reach or exceed the threshold of 5% and are held in firm hands are subtracted from the total market capitalization. The following positions in a security are deemed to be held in firm hands:

| · | Shareholding that has been acquired by one person or a group of persons who are subject to a shareholder or lockup agreement. |

| · | Shareholding that has been acquired by one person or a group of persons who according to publicly known facts, have a long-term interest in a company. |

The free-float is calculated on the basis of outstanding shares. Issued and outstanding equity capital is, as a rule, the total amount of equity capital that has been fully subscribed, wholly or partially paid in and documented in the Commercial Registry. Neither conditional nor approved capital is counted as issued and outstanding equity capital. The free-float is calculated on the basis of listed shares only. Where a company has different categories of listed participation rights, these are considered separately for the free-float calculation.

Exceptions

The positions in a security held by institutions of the following kind are deemed free-floating:

| · | custodian nominees |

| · | trustee companies |

| · | investment funds |

| · | pension funds |

| · | investment companies |

The SIX Swiss Exchange classifies at its own discretion persons and groups of persons who, because of their area of activity or the absence of important information, cannot be clearly assigned.

Ordinary Index Review

Each year on the third Friday of September, the composition of the SMI® is updated in the ordinary index review based on the selection list of June. With the cut-off dates on March 31, September 30 and December 31, a provisional selection list is created, which serves as

| Leveraged Index Return Notes® | TS-20 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

the basis for the adjustment of extraordinary corporate actions. The number of securities and free-float shares are adjusted on four ordinary adjustment dates a year: the third Friday in March, June, September and December.

Extraordinary Corporate Actions

An extraordinary corporate action is an initial public offering (“IPO”), merger and acquisition activity, spin-off, insolvency or any other event that leads to a listing or delisting. An extraordinary corporate action has an ex-date, but its effect can usually not be calculated by a generic predefined formula. In most cases, an extraordinary corporate action leads to a new listing or delisting and subsequently there is a change in the composition of the SMI® and in the component weights of the composition of the SMI®.

Newly listed instruments that fulfill the selection rules of the SMI®, are extraordinarily included in the SMI® on their second trading day and the SMI® is adjusted with the free-float market capitalization at the close of the first trading day. The extraordinary inclusion of a newly listed instrument in the SMI® can lead to an extraordinary replacement of an existing index component. Extraordinary inclusions are implemented after a notification period of 5 trading days. The adjusted cap factors are implemented after a notification period of generally 5 trading days, but no less than one trading day.

If an IPO of a real estate instrument leads to an extraordinary inclusion, it is included in the SMI® in three equal stages. This is achieved by the gradual increase of the number of shares or the free-float factor over three trading days starting on the second trading day.

In case of a delisting, the exclusion of an index component is made, if possible, on the next ordinary index review date on the third Friday of March, June, September or December. However, if the delisting would be effective before the ordinary index review, the component is excluded from the SMI® on the effective date of the delisting. If a component is excluded from the SMI® outside of the ordinary index review, it is replaced by the best-ranked candidate on the selection list that is not yet part composition of the SMI® in order to maintain a stable number of components within the SMI®. Extraordinary exclusions are implemented after a notification period of 5 trading days. Adjusted cap factors are implemented after a notification period of generally 5 trading days, but no less than one trading day.

Extraordinary inclusions in the SMI® take place if the selection rules for the SMI® are fulfilled after a three-month period. This occurs on a quarterly basis after the close of trading on the third Friday of March, June, September and December as follows:

|

Latest Listing Date |

Earliest Extraordinary Acceptance Date |

| 5 trading days prior to the end of November | March |

| 5 trading days prior to the end of February | June |

| 5 trading days prior to the end of May | September |

| 5 trading days prior to the end of August | December |

In the case of major market changes as a result of a corporate action, an instrument may be admitted to the SMI® outside of the accepted admission period as long as it clearly fulfills the index selection rules. For the same reasons, a component can be excluded if the requirements for admission to the SMI® are no longer fulfilled.

Calculation of the SMI®

The SMI® is calculated using the Laspeyres method with the weighted arithmetic mean of a defined number of securities issues. The index level is calculated by dividing the market capitalizations of all securities included in the SMI® by a divisor:

where t is current day; s is current time on day t; Is is the current index level at time s; Dt is the divisor on day t; M is the number of issues in the SMI®; pi,s is the last-paid price of security i; xi,t is the number of shares of security i on day t; fi,t is the free-float for security i on day t; Ki,t is the capping factor for security i on day t and rs is the current CHF exchange rate at time s.

The divisor is a technical number used to calculate the SMI®. If the market capitalization changes due to a corporate event, the divisor changes while the index value remains the same. The new divisor is calculated on the evening of the day before the corporate event takes effect.

In calculating the SMI®, the last-paid price is taken into account. If no price has been paid on the day of calculation, the previous day’s price is used. Only the prices achieved via the electronic order book of the SIX Swiss Exchange are used.

| Leveraged Index Return Notes® | TS-21 |

Leveraged Index Return Notes® Linked to an International Equity Index Basket, due January 28, 2022 |

The trading hours for Swiss equities, participation certificates and bonus certificates are determined by the SIX Swiss Exchange. Since the opening phase usually causes strong price fluctuations, the SMI® is first calculated two minutes after the start of on order book trading. This index level is called the “open.” A closing auction takes place ten minutes before close of trading. At the close of trading, the final closing prices used in calculating the closing level of the SMI® are established.

Component Weighting

The SMI® is weighted by the free-float market capitalization of its components. The number of shares and the free-float factor are reviewed on a quarterly basis. In the same context, each component of the SMI® with a free-float market capitalization larger than 18% of the total market capitalization of the index is capped to that weight of 18%.

Additionally, the components of the index are capped to 18% between two ordinary index reviews as soon as two components exceed a weight of 20% each. If such an intra quarter breach is observed after the close of markets, the new cap factors are calculated so that any component has a maximum weight of 18%. This cap factor is set to be effective after the close of the following trading day.

If an issuer has issued more than one equity instrument (e.g., registered shares, bearer shares, participation certificates, bonus certificates), it is possible that one issuer is represented in the SMI® with more than one instrument. In this case, the free-float market capitalization of those instruments is cumulated for the calculation of the cap factors. If the cumulated index weight exceeds the 18% threshold, the weight is capped accordingly. The cumulated, capped index weight is distributed proportionally based on the free-float market capitalization of those instruments.

The following graph shows the daily historical performance of the SMI in the period from January 1, 2010 through January 30, 2020. We obtained this historical data from Bloomberg L.P. We have not independently verified the accuracy or completeness of the information obtained from Bloomberg L.P. On the pricing date, the closing level of the SMI was 10,748.92.

Historical Performance of the Swiss Market Index

This historical data on the SMI is not necessarily indicative of the future performance of the SMI or what the value of the notes may be. Any historical upward or downward trend in the level of the SMI during any period set forth above is not an indication that the level of the SMI is more or less likely to increase or decrease at any time over the term of the notes.

Before investing in the notes, you should consult publicly available sources for the levels of the SMI®.

| Leveraged Index Return Notes® | TS-22 |