Form 497 GOLDMAN SACHS TRUST

Tweet

Tweet Share

ShareAN INVESTMENT IN A FUND IS NOT A BANK DEPOSIT AND IS NOT INSURED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION OR ANY OTHER GOVERNMENT AGENCY. AN INVESTMENT IN A FUND INVOLVES INVESTMENT RISKS, AND YOU MAY LOSE MONEY IN A FUND. |

Class A |

Institutional |

Class R6 | |

| Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | |||

| Maximum Deferred Sales Charge (Load) (as a percentage of the lower of original purchase price or sale proceeds) |

Class A |

Institutional |

Class R6 | |

| Management Fees | |||

| Distribution and/or Service (12b-1) Fees | |||

| Other Expenses 1 |

|||

| Acquired (Underlying) Fund Fees and Expenses | |||

Total Annual Fund Operating Expenses 2 |

|||

| Fee Waiver and Expense Limitation 3 |

( |

( |

( |

Total Annual Fund Operating Expenses After Fee Waiver and Expense Limitation 2 |

1 |

|

2 |

|

3 |

The Investment Adviser has agreed to waive a portion of its management fee in order to achieve an effective rate of 0.08% as an annual percentage rate of average daily net assets of the Fund through at least December 29, 2021, and prior to such date, the Investment Adviser may not terminate the arrangement without the approval of the Board of Trustees. In addition, the Investment Adviser has agreed to reduce or limit “Other Expenses” (excluding acquired (underlying) fund fees and expenses, transfer agency fees and expenses, taxes, interest, brokerage fees, expenses of shareholder meetings, litigation and indemnification, and extraordinary expenses) to 0.014% of the Fund’s average daily net assets through at least and prior to such date, the Investment Adviser may not terminate the arrangement without the approval of the Board of Trustees. |

1 Year |

3 Years |

5 Years |

10 Years | |

| Class A Shares | $ |

$ |

$ |

$ |

| Institutional Shares | $ |

$ |

$ |

$ |

| Class R6 Shares | $ |

$ |

$ |

$ |

Principal Risks of the Underlying Funds |

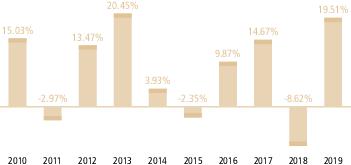

During the periods shown in the chart above: |

Returns |

Quarter ended |

| - |

| AVERAGE ANNUAL TOTAL RETURN |

1 Year |

5 Years |

10 Years | |

Class A Shares (Inception |

|||

| Returns Before Taxes | |||

| Returns After Taxes on Distributions | |||

| Returns After Taxes on Distributions and Sale of Fund Shares | |||

Institutional Shares (Inception |

|||

| Returns Before Taxes | |||

Class R6 Shares (Inception |

|||

| Returns Before Taxes | |||

| EDGE Composite Index (reflects no deduction for fees or expenses) | |||

| MSCI ACWI IMI (Net, USD, Unhedged; reflects no deduction for fees or expenses) | |||

| Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees or expenses) |

* |

Class R6 Shares commenced operations on December 29, 2017. Prior to that date, the performance of Class R6 Shares shown in the table above is that of Institutional Shares. Performance has not been adjusted to reflect the lower expenses of Class R6 Shares. Class R6 Shares would have had higher returns because: (i) Institutional Shares and Class R6 Shares represent interests in the same portfolio of securities; and (ii) Class R6 Shares have lower expenses. |

| Portfolio Management |

| Buying and Selling Fund Shares |

| Tax Information |

| Payments to Broker-Dealers and Other Financial Intermediaries |

Class A |

Institutional |

Class R6 | |

| Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) | |||

| Maximum Deferred Sales Charge (Load) (as a percentage of the lower of original purchase price or sale proceeds) |

Class A |

Institutional |

Class R6 | |

| Management Fees | |||

| Distribution and/or Service (12b-1) Fees | |||

| Other Expenses 1 |

|||

| Acquired (Underlying) Fund Fees and Expenses | |||

Total Annual Fund Operating Expenses 2 |

|||

| Fee Waiver and Expense Limitation 3 |

( |

( |

( |

Total Annual Fund Operating Expenses After Fee Waiver and Expense Limitation 2 |

1 |

|

2 |

|

3 |

The Investment Adviser has agreed to waive a portion of its management fee in order to achieve an effective rate of 0.08% as an annual percentage rate of average daily net assets of the Fund through at least |

1 Year |

3 Years |

5 Years |

10 Years | |

| Class A Shares | $ |

$ |

$ |

$ |

| Institutional Shares | $ |

$ |

$ |

$ |

| Class R6 Shares | $ |

$ |

$ |

$ |

| ■ | Investing in Underlying Tax-Managed Funds |

| ■ | Offsetting long-term and short-term capital gains with long-term and short-term capital losses and creating loss carry-forward positions |

| ■ | Limiting portfolio turnover that may result in taxable gains |

| Principal Risks of the Underlying Funds |

During the periods shown in the chart above: |

Returns |

Quarter ended |

| - |

AVERAGE ANNUAL TOTAL RETURN |

1 Year |

5 Years |

10 Years | |

Class A Shares (Inception |

|||

| Returns Before Taxes | |||

| Returns After Taxes on Distributions | |||

| Returns After Taxes on Distributions and Sale of Fund Shares | |||

Institutional Shares (Inception |

|||

| Returns Before Taxes | |||

Class R6 Shares (Inception |

|||

| Returns Before Taxes | |||

| TAG Composite Index (reflects no deduction for fees or expenses) | |||

| MSCI ACWI IMI (Net, USD, Unhedged; reflects no deduction for fees or expenses) | |||

| Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees or expenses) |

* |

Class R6 Shares commenced operations on December 29, 2017. Prior to that date, the performance of Class R6 Shares shown in the table above is that of Institutional Shares. Performance has not been adjusted to reflect the lower expenses of Class R6 Shares. Class R6 Shares would have had higher returns because: (i) Institutional Shares and Class R6 Shares represent interests in the same portfolio of securities; and (ii) Class R6 Shares have lower expenses. |

| Portfolio Management |

| Buying and Selling Fund Shares |

| Tax Information |

| Payments to Broker-Dealers and Other Financial Intermediaries |

Additional Summary Information

| Tax Information |

| Payments to Broker-Dealers and Other Financial Intermediaries |

| INVESTMENT OBJECTIVEs |

| PRINCIPAL INVESTMENT STRATEGIES |

| ■ | Investing in Underlying Tax-Managed Funds |

| ■ | Offsetting long-term and short-term capital gains with long-term and short-term capital losses and creating loss carry-forward positions |

| ■ | Limiting portfolio turnover that may result in taxable gains |

Fund |

Target |

Range |

Enhanced Dividend Global Equity |

||

| Equity | 90% | 80–100% |

| Fixed Income | 10% | 0–20% |

Tax-Advantaged Global Equity |

||

| Equity | 90% | 80–100% |

| Fixed Income | 10% | 0–20% |

| ADDITIONAL FEES AND EXPENSES INFORMATION |

| ADDITIONAL PERFORMANCE INFORMATION |

| OTHER INVESTMENT PRACTICES AND SECURITIES |

| ■ | Derivatives Risk— The Fund’s use of options, futures, forwards, swaps, options on swaps, structured securities and other derivative instruments may result in losses. These instruments, which may pose risks in addition to and greater than those associated with investing directly in securities, currencies or other instruments, may be illiquid or less liquid, volatile, difficult to price and leveraged so that small changes in the value of the underlying instruments may produce disproportionate losses to the Fund . Certain derivatives are also subject to counter-party risk, which is the risk that the other party in the transaction will not fulfill its contractual obligations, liquidity risk and risks arising from margin requirements, which include the risk that the Fund will be required to pay additional margin or set aside additional collateral to maintain open derivative positions. Derivatives may be used for both hedging and non-hedging purposes. |

| The use of derivatives is a highly specialized activity that involves investment techniques and risks different from those associated with investments in more traditional securities and instruments, and there is no guarantee that the use of derivatives will achieve their intended result. If the Investment Adviser is incorrect in its expectation of the timing or level of fluctuation in securities prices, interest rates, currency prices or other variables, the use of derivatives could result in losses, which in some cases may be significant. A lack of correlation between changes in the value of derivatives and the value of the portfolio assets (if any) being hedged could also result in losses. In addition, there is a risk that the performance of the derivatives or other instruments used by the Investment Adviser to replicate the performance of a particular asset class may not accurately track the performance of that asset class. Derivatives are also subject to risks arising from margin requirements. There is also risk of loss if the Investment Adviser is incorrect in its expectation of the timing or level of fluctuation in securities prices, interest rates, currency prices or other variables. | |

| The Fund may use derivatives, including futures and swaps, to implement short positions. Taking short positions involves leverage of the Fund’s assets and presents various risks. If the value of the instrument or market in which the Fund has taken a short position increases, then the Fund will incur a loss equal to the increase in value from the time that the short position was entered into plus any premiums and interest paid to a counterparty. Therefore, taking short positions involves the risk that losses may be exaggerated, potentially losing more money than the actual cost of the investment. | |

| As an investment company registered with the SEC, the Fund must identify on their books (often referred to as “asset segregation”) liquid assets, or engage in other SEC- or SEC staff-approved or other appropriate measures, to “cover” open positions with respect to certain kinds of derivative instruments. For more information about these practices, see Appendix A. As discussed in more detail in Appendix A and the SAI, the SEC adopted a final rule related to the use of derivatives, short sales, reverse repurchase agreements and certain other transactions by registered investment companies. In connection with the final rule, the SEC and its staff will rescind and withdraw applicable guidance and relief regarding asset segregation and coverage transactions reflected in the Fund’s asset segregation and cover practices discussed therein. | |

| ■ | Dividend-Paying Investments Risk —The Fund’s investments in dividend-paying securities could cause the Fund to underperform other funds that invest in similar asset classes but employ a different investment style. Securities that pay dividends, as a group, can fall out of favor with the market, causing such securities to underperform securities that do not pay dividends. Depending upon market conditions and political and legislative responses to such conditions, dividend-paying securities that meet the Fund’s investment criteria may not be widely available and/or may be highly concentrated in only a few market sectors. For example, in response to the outbreak of a novel strain of coronavirus (known as COVID-19), the U.S. Government passed the Coronavirus Aid, Relief and Economic Security Act in March 2020, which established loan programs for certain issuers impacted by COVID-19. Among other conditions, borrowers under these loan programs are generally restricted from paying dividends. The adoption of new legislation could further limit or restrict the ability of issuers to pay dividends. To the extent that dividend-paying securities are concentrated in only a few market sectors, the Fund may be subject to the risks of volatile economic cycles and/or conditions or developments that may be particular to a sector to a greater extent than if its investments were diversified across different sectors. In addition, issuers that have paid regular dividends or distributions to shareholders may not continue to do so at the same level or at all in the future. A sharp rise in interest rates or an economic downturn could cause an issuer to abruptly reduce or eliminate its dividend. This may limit the ability of the Fund to produce current income. |

| ■ | Expenses Risk —Because the Fund and the Underlying Funds may invest in in pooled investment vehicles (including investment companies and ETFs), partnerships and real estate investment trusts (“REITs”), the investor will incur not only a proportionate share of the expenses of the other pooled investment vehicles, partnerships and REITs held by the Underlying Fund (including operating costs and investment management fees), but also expenses of the Underlying Fund. |

| ■ | Interest Rate Risk— When interest rates increase, fixed income securities or instruments held by the Fund (which may include inflation protected securities) will generally decline in value. Long-term fixed income securities or instruments will normally have more price volatility because of this risk than short-term fixed income securities or instruments. A wide variety of market factors can cause interest rates to rise, including central bank monetary policy, rising inflation and changes in general economic conditions. The risks associated with changing interest rates may have unpredictable effects on the markets and the Fund’s investments. Fluctuations in interest rates may also affect the liquidity of fixed income securities and instruments held by the Fund. |

| Interest rates in the United States are currently at historically low levels. Certain countries have experienced negative interest rates on certain fixed-income instruments. Very low or negative interest rates may magnify interest rate risk. Changing interest rates, including rates that fall below zero, may have unpredictable effects on markets, may result in heightened market volatility and may detract from Fund performance to the extent the Fund is exposed to such interest rates and/or volatility. | |

| ■ | Investing in the Underlying Funds —The Fund’s investments are concentrated in one or more of the Underlying Funds (including ETFs and other registered investment companies) subject to statutory limitations prescribed by the Investment Company Act, or exemptive relief or regulations thereunder. The Fund’s investment performance is directly related to the investment performance of the Underlying Funds it holds. The ability of the Fund to meet its investment objective is directly related to the ability of the Underlying Funds to meet their objectives as well as the allocation among those Underlying Funds by the Investment Adviser. The value of the Underlying Funds’ investments, and the net asset values (“NAV”) of the shares of both the Fund and the Underlying Funds, will fluctuate in response to various market and economic factors related to the equity and fixed income markets, as well as the financial condition and prospects of issuers in which the Underlying Funds invest. There can be no assurance that the investment objective of the Fund or any Underlying Fund will be achieved. The risks presented by the investment practices of the Underlying Funds are discussed in the "Risks of the Underlying Funds" section, Appendix A to the Prospectus and in the SAI. |

| ■ | Investments in Affiliated Underlying Funds— In managing the Fund, the Investment Adviser will have the authority to select and substitute Underlying Funds. The Investment Adviser is subject to conflicts of interest in allocating Fund assets among the various Underlying Funds both because the fees payable to it and/or its affiliates by some Underlying Funds are higher than the fees payable by other Underlying Funds and because the Investment Adviser and its affiliates are also responsible for managing the Underlying Funds. The Investment Adviser and/or its affiliates are compensated by the Fund and by the Underlying Funds for advisory, transfer agency and/or principal underwriting services provided. The portfolio managers may also be subject to conflicts of interest in allocating Fund assets among the various Underlying Funds because the Fund’s portfolio management team may also manage some of the Underlying Funds. The Board of Trustees (the “Trustees”) and officers of the Goldman Sachs Trust (the “Trust”) may also have conflicting interests in fulfilling their fiduciary duties to both the Fund and the Underlying Funds for which GSAM or its affiliates now or in the future serve as investment adviser or principal underwriter. Other funds with similar investment strategies may perform better or worse than the Underlying Funds. |

| ■ | Investments in ETFs Risk— The Fund may also invest directly in affiliated and/or unaffiliated ETFs. The ETFs in which the Fund may invest are subject to the same risks and may invest directly in the same securities as those of the Underlying Funds, as described below under “Investments of the Underlying Funds.” In addition, the Fund’s investments in these ETFs will be subject to the restrictions applicable to investments by an investment company in other investment companies, unless relief is otherwise provided under the terms of an SEC exemptive order or SEC exemptive rule. |

| ■ | Large Shareholder Transactions Risk —The Fund may experience adverse effects when certain large shareholders, such as other funds, institutional investors (including those trading by use of non-discretionary mathematical formulas), financial intermediaries (who may make investment decisions on behalf of underlying clients and/or include the Fund in their investment model), individuals, accounts and Goldman Sachs affiliates, purchase or redeem large amounts of shares of the Fund. Such large shareholder redemptions, which may occur rapidly or unexpectedly, may cause the Fund to sell portfolio securities at times when it would not otherwise do so, which may negatively impact the Fund’s NAV and liquidity. Similarly, large Fund share purchases may adversely affect the Fund’s performance to the extent that the Fund is delayed in investing new cash or otherwise maintains a larger cash position than it ordinarily would. These transactions may also accelerate the realization of taxable income to shareholders if such sales of investments resulted in gains, and may also increase transaction costs. In addition, a large redemption could result in the Fund’s current expenses being allocated over a smaller asset base, leading to an increase in the Fund’s expense ratio. |

| ■ | Management Risk —A strategy used by the Investment Adviser may fail to produce the intended results. |

| ■ | Market Risk— The value of the securities in which the Fund and/or an Underlying Fund invests may go up or down in response to the prospects of individual companies, particular sectors or governments and/or general economic conditions throughout the world. |

| Price changes may be temporary or last for extended periods. The Fund's and/or an Underlying Fund's investments may be overweighted from time to time in one or more sectors or countries, which will increase the Fund's and/or an Underlying Fund's exposure to risk of loss from adverse developments affecting those sectors or countries. | |

| Global economies and financial markets are becoming increasingly interconnected, and conditions and events in one country, region or financial market may adversely impact issuers in a different country, region or financial market. Furthermore, local, regional and global events such as war, acts of terrorism, social unrest, natural disasters, the spread of infectious illness or other public health threats could also adversely impact issuers, markets and economies, including in ways that cannot necessarily be foreseen. The Fund could be negatively impacted if the value of a portfolio holding were harmed by such political or economic conditions or events. In addition, governmental and quasi-governmental organizations have taken a number of unprecedented actions designed to support the markets. Such conditions, events and actions may result in greater market risk. | |

| ■ | NAV Risk— The NAV of the Fund and the value of your investment will fluctuate. |

| ■ | Short Position Risk —The Fund may use derivatives, including futures and swaps, to implement short positions and may also engage in direct short selling. If the Fund uses a derivative to implement a short position and the value of the underlying instrument or market in which the Fund has taken a short position increases, then the Fund will incur a loss equal to the increase in value from the time that the short position was entered into plus any interest payments or other fees. Short positions also may involve leverage of the Fund’s assets and presents various risks (see “Risks of the Underlying Funds—Risks That Are Particularly Important For Specific Underlying Funds—Leverage Risk” for a description of the related risks to which the Fund may also be subject). |

| In order to directly establish a short position in a security, the Fund must first borrow the security from a lender, such as a broker or other institution. The Fund may not always be able to borrow the security at a particular time or at an acceptable price. Thus, there is risk that the Fund may be unable to implement its investment strategy due to the lack of available stocks or for other reasons. | |

| After selling the borrowed security, the Fund is then obligated to “cover” the short sale by purchasing and returning the security to the lender on a later date. The Fund cannot guarantee that the security necessary to cover a short position will be available for purchase at the time the Fund wishes to close a short position or, if available, that the security will be available at an acceptable price. If the borrowed security has appreciated in value, the Fund will be required to pay more for the replacement security than the amount it received for selling the security short. Moreover, purchasing a security to cover a short position can itself cause the price of the security to rise further, thereby exacerbating the loss. The potential loss on a short sale is unlimited because the loss increases as the price of the security sold short increases and the price may rise indefinitely. If the price of a borrowed security declines before the short position is covered, the Fund may realize a gain. The Fund’s gain on a short sale, before transaction and other costs, is generally limited to the difference between the price at which it sold the borrowed security and the price it paid to purchase the security to return to the lender. | |

| While the Fund has an open short position, it is subject to the risk that the security’s lender will terminate the loan at a time when the Fund is unable to borrow the same security from another lender. If this happens, the Fund may be required to buy the replacement shares immediately at the security’s then current market price or “buy in” by paying the lender an amount equal to the cost of purchasing the security to close out the short position. | |

| Short sales also involve other costs. The Fund must normally repay to the lender an amount equal to any dividends or interest that accrues while the loan is outstanding. In addition, to borrow the security, the Fund may be required to pay a premium. The Fund also will incur transaction costs in effecting short sales. The amount of any ultimate gain for the Fund resulting from a short sale will be decreased, and the amount of any ultimate loss will be increased, by the amount of premiums, dividends, interest or expenses the Fund may be required to pay in connection with the short sale. | |

| Until the Fund replaces a borrowed instrument, the Fund may be required to maintain short sale proceeds with the lending broker as collateral. Moreover, the Fund will be required to make margin payments to the lender during the term of the borrowing if the value of the security it borrowed (and short sold) increases. Thus, short sales involve credit exposure to the broker that executes the short sales. In the event of the bankruptcy or other similar insolvency with respect to a broker with whom the Fund has an open short position, the Fund may be unable to recover, or delayed in recovering, any margin or other collateral held with or for the lending broker. In addition, the Fund is required to identify on its books liquid assets (less any additional collateral held by the broker, not including the short sale proceeds) to cover the short sale obligation, marked-to-market daily. The requirement to identify liquid assets limits the Fund’s leveraging of its investments and the related risk of losses from leveraging. However, such identification may also limit the Fund’s investment flexibility, as well as its ability to meet redemption requests or other current obligations. | |

| ■ | Tax-Managed Investment Risk —Because the Investment Adviser balances investment considerations and tax considerations, the pre-tax performance of the Goldman Sachs Tax-Advantaged Global Equity Portfolio may be lower than the performance of similar |

| funds that are not tax-managed. This is because the Investment Adviser may choose not to make certain investments that may result in taxable distributions to the Goldman Sachs Tax-Advantaged Global Equity Portfolio. Even though tax managed strategies are being used, they may not reduce the amount of taxable income and capital gains distributed by the Goldman Sachs Tax-Advantaged Global Equity Portfolio to shareholders. | |

| ■ | Temporary Investments— Although the Fund normally seeks to invest approximately 80% of their Total Assets in the Underlying Funds, the Fund may invest its assets in high-quality, short-term debt obligations (including commercial paper, certificates of deposit, bankers’ acceptances, repurchase agreements, debt obligations backed by the full faith and credit of the U.S. government and demand and time deposits of domestic and foreign banks and savings and loan associations) to maintain liquidity, to meet shareholder redemptions and for other short-term cash needs. Also, there may be times when, in the opinion of the Investment Adviser, abnormal market or economic conditions warrant that, for temporary defensive purposes, the Fund may invest without limitation in short-term obligations. When the Fund’s assets are invested in such investments, the Fund may not be achieving its investment objective. |

| ■ | U.S. Government Securities Risk— The U.S. government may not provide financial support to U.S. government agencies, instrumentalities or sponsored enterprises if it is not obligated to do so by law. U.S. Government Securities issued by those agencies, instrumentalities and sponsored enterprises, including those issued by Fannie Mae, Freddie Mac and Federal Home Loan Banks, are neither issued nor guaranteed by the U.S. Treasury and, therefore, are not backed by the full faith and credit of the United States. The maximum potential liability of the issuers of some U.S. Government Securities held by an Underlying Fund may greatly exceed their current resources, including any legal right to support from the U.S. Treasury. It is possible that issuers of U.S. Government Securities will not have the funds to meet their payment obligations in the future. Fannie Mae and Freddie Mac have been operating under conservatorship, with the Federal Housing Finance Agency (“FHFA”) acting as their conservator, since September 2008. The entities are dependent upon the continued support of the U.S. Department of the Treasury and FHFA in order to continue their business operations. These factors, among others, could affect the future status and role of Fannie Mae and Freddie Mac and the value of their securities and the securities which they guarantee. Additionally, the U.S. government and its agencies and instrumentalities do not guarantee the market values of their securities, which may fluctuate. |

| DESCRIPTION OF THE UNDERLYING FUNDS |

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

Large Cap Value Insights |

Long-term growth of capital and dividend income. | At least 80% of its Net Assets in a diversified portfolio of equity investments in large-cap U.S. issuers, including foreign issuers that are traded in the United States. The Fund’s investments are selected using fundamental research and a variety of quantitative techniques based on certain investment themes, including, among others, Fundamental Mispricings, High Quality Business Models, Sentiment Analysis and Market Themes & Trends. The Fund maintains risk, style, and capitalization characteristics similar to the Russell 1000 ® Value Index. |

The Russell 1000 ® Value Index is an unmanaged index of common stock prices that measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. |

Large Cap Growth Insights |

Long-term growth of capital. Dividend income is a secondary consideration. | At least 80% of its Net Assets in a broadly diversified portfolio of equity investments in large-cap U.S. issuers, including foreign issuers that are traded in the United States. The Fund’s investments are selected using fundamental research and a variety of quantitative techniques based on certain investment themes, including, among others, Fundamental Mispricings, High Quality Business Models, Sentiment Analysis and Market Themes & Trends. The Fund maintains risk, style, and capitalization characteristics similar to the Russell 1000 ® Growth Index. |

The Russell 1000 ® Growth Index is an unmanaged index of common stock prices that measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. |

Small Cap Equity Insights |

Long-term growth of capital. | At least 80% of its Net Assets in a broadly diversified portfolio of equity investments in small-cap U.S. issuers, including foreign issuers that are traded in the United States. The Fund’s investments are selected using fundamental research and a variety of quantitative techniques based on certain investment themes, including, among others, Fundamental Mispricings, High Quality Business Models, Sentiment Analysis and Market Themes & Trends. The Fund maintains risk, style, and capitalization characteristics similar to the Russell 2000 ® Index. |

The Russell 2000 ® Index is an index designed to represent an investable universe of small cap companies. |

International Tax-Managed Equity |

Long-term after-tax growth of capital through tax-sensitive participation in a broadly diversified portfolio of international equity securities. | At least 80% of its Net Assets in equity investments in non-U.S. issuers. The Fund uses a variety of quantitative techniques, in combination with a qualitative overlay, when selecting investments. The Fund expects to maintain risk, style, capitalization and industry characteristics similar to the MSCI ® EAFE® Index. The Investment Adviser balances investment considerations and tax considerations. The Fund may seek tax-efficiency by offsetting gains and losses, managing portfolio turnover that may result in taxable gains, or selling securities with a higher tax basis. |

The MSCI ® EAFE® Index (Net, USD, Unhedged) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the United States and Canada. |

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

U.S. Tax-Managed Equity |

Long-term after-tax growth of capital through tax-sensitive participation in a broadly diversified portfolio of U.S. equity securities. | At least 80% of its Net Assets in equity investments in U.S. issuers. The Fund uses a variety of quantitative techniques, in combination with a qualitative overlay, when selecting investments. The Fund will seek to maintain risk, style, capitalization and industry characteristics similar to the Russell 3000 ® Index. The Investment Adviser balances investment considerations and tax considerations. The Fund may seek tax-efficiency by offsetting gains and losses, managing portfolio turnover that may result in taxable gains, or selling securities with a higher tax basis. |

The Russell 3000 ® Index is an unmanaged index that measures the performance of the 3,000 largest U.S. companies based on total market capitalization. |

Emerging Markets Equity Insights |

Long-term growth of capital. | At least 80% of its Net Assets in a diversified portfolio of equity investments in emerging country issuers. The Fund uses a quantitative style of management, in combination with a qualitative overlay, that emphasizes fundamentally-based stock and country/ currency selection, careful portfolio construction and efficient implementation. The Fund seeks to maintain risk, style, and capitalization characteristics similar to the MSCI ® Emerging Markets Standard Index (adjusted for the Investment Adviser’s country views). |

The MSCI ® Emerging Markets Standard Index (Net, USD, Unhedged) is a free float-adjusted market capitalization index that is designed to measure equity market performance of the large and mid-market capitalization segments of emerging markets. |

International Small Cap Insights |

Long-term growth of capital. | At least 80% of its Net Assets in a broadly diversified portfolio of equity investments in small cap non-U.S. issuers. The Fund uses a quantitative style of management, in combination with a qualitative overlay, that emphasizes fundamentally-based stock selection, careful portfolio construction and efficient implementation. The Fund seeks to maintain risk, style, and capitalization characteristics similar to the MSCI ® EAFE® Small Cap Index. |

The MSCI ® EAFE® Small Cap Index (Net, USD, Unhedged) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of the small market capitalization segment of developed markets, excluding the United States and Canada. |

U.S. Equity Dividend and Premium |

Maximize income and total return. | At least 80% of its Net Assets in dividend-paying equity investments in large-cap U.S. issuers with public stock market capitalizations within the range of the market capitalization of the S&P 500 ® Index at the time of investment. The Fund uses a variety of quantitative techniques, in combination with a qualitative overlay, when selecting investments. The Fund will seek to maintain risk, style, capitalization and industry characteristics similar to the S&P 500® Index. Under normal circumstances, the Fund expects to sell call options in an amount that is between 20% and 75% of the value of the Fund’s portfolio. |

The primary benchmark is the S&P 500 ® Index, which is the Standard & Poor’s 500 Composite Stock Price Index of 500 stocks, an unmanaged index of common stock prices. |

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

International Equity Dividend and Premium |

Maximize total return with an emphasis on income. | At least 80% of its Net Assets in dividend-paying equity investments in non-U.S. issuers with public stock market capitalizations within the range of capitalization of the MSCI ® EAFE® Index at the time of investment. The Fund uses a variety of quantitative techniques, in combination with a qualitative overlay, when selecting investments. The Fund will seek to maintain risk, style, capitalization and industry characteristics similar to the MSCI® EAFE® Index. The Fund expects that, under normal circumstances, it will sell call options in an amount that is between 20% and 75% of the value of the Fund’s portfolio. |

The primary benchmark is the MSCI ® EAFE® Index (Net, USD, Unhedged), which is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the United States and Canada. |

Small Cap Growth Insights |

Long-term growth of capital. | At least 80% of its Net Assets in a broadly diversified portfolio of equity investments in small-cap U.S. issuers, including foreign issuers that are traded in the United States. The Fund uses a quantitative style of management, in combination with a qualitative overlay, that emphasizes fundamentally-based stock selection, careful portfolio construction and efficient implementation. The Fund maintains risk, style, and capitalization characteristics similar to the Russell 2000 Growth Index. | The Russell 2000 ® Growth Index is an unmanaged index of common stock prices that measures the performance of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. |

Small Cap Value Insights |

Long-term growth of capital. | At least 80% of its Net Assets in a broadly diversified portfolio of equity investments in small-cap U.S. issuers, including foreign issuers that are traded in the United States. The Fund uses a quantitative style of management, in combination with a qualitative overlay, that emphasizes fundamentally-based stock selection, careful portfolio construction and efficient implementation. The Fund maintains risk, style, and capitalization characteristics similar to the Russell 2000 Value Index. | The Russell 2000 ® Value Index is an unmanaged index of common stock prices that measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. |

U.S. Equity Insights |

Long-term growth of capital and dividend income. | At least 80% of its Net Assets in a diversified portfolio of equity investments in U.S. issuers. The Fund uses a quantitative style of management, in combination with a qualitative overlay, that emphasizes fundamentally-based stock selection, careful portfolio construction and efficient implementation. The Fund maintains risk, style, and capitalization characteristics similar to the S&P 500 Index. | The S&P 500 ® Index is the Standard & Poor’s 500 Composite Stock Price Index of 500 stocks, an unmanaged index of common stock prices. |

International Equity Insights |

Long-term growth of capital. | At least 80% of its Net Assets in a broadly diversified portfolio of equity investments in non-U.S. issuers. The Fund uses a quantitative style of management, in combination with a qualitative overlay, that emphasizes fundamentally-based stock and country/ currency selection, careful portfolio construction and efficient implementation. The Fund seeks to maintain style, risk and capitalization characteristics similar to the MSCI EAFE Standard Index (adjusted for the Investment Adviser’s country views). | The MSCI ® EAFE® Standard Index (Net, USD, Unhedged) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of large and mid-capitalization segments of developed markets, excluding the United States and Canada. |

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

Global Infrastructure Fund |

Long-term growth of capital and income. | At least 80% of its Net Assets in a portfolio of investments in issuers that are engaged in or related to the infrastructure group of industries. The Fund will invest primarily in the common stock of infrastructure companies. The Fund may invest in REITs. The Fund may also invest up to 20% of its total assets (measured at time of purchase) in MLPs that are taxed as partnerships and up to 20% of its Net Assets (measured at time of purchase) in issuers that are not infrastructure companies. The Fund’s investment strategy combines bottom-up company analysis with fundamental real asset research. |

The Dow Jones Brookfield Global Infrastructure Index intends to measure the stock performance of “pure-play” infrastructure companies domiciled globally. The index covers all sectors of the infrastructure market. Components are required to have more than 70% of cash flows derived from infrastructure lines of business. |

Global Real Estate Securities Fund |

Total return comprised of long-term growth of capital and dividend income. | At least 80% of its Net Assets in a portfolio of equity investments in issuers that are primarily engaged in or related to the real estate industry within and outside the United States. Real estate industry companies may include REITs, REIT-like structures, or real estate operating companies whose businesses and services are related to the real estate industry. The Fund’s investment strategy is based on the premise that property market fundamentals are the primary determinant of growth, underlying the success of companies in the real estate industry. The Fund may also invest up to 20% of its Net Assets (measured at the time of purchase) in issuers that are not real estate industry companies, or fixed income investments, such as government, corporate and bank debt obligations. | The FTSE EPRA Nareit Developed Index (Net, USD, Unhedged) is designed to track the performance of listed real estate companies and REITs worldwide. |

Underlying Fund |

Investment Objectives |

Duration or Maturity |

Investment Sector |

Credit Quality |

Other Investments |

Core Fixed Income |

Total return consisting of capital appreciation and income that exceeds the total return of the Bloomberg Barclays U.S. Aggregate Bond Index. | Target Duration* = Bloomberg Barclays U.S. Aggregate Bond Index plus or minus one year | At least 80% of its Net Assets in fixed income securities, including U.S. Government Securities and Agency Mortgage-Backed Securities, corporate debt securities, privately issued adjustable rate and fixed rate mortgage-backed securities or other mortgage-related securities and asset-backed securities. | Minimum = BBB–/Baa3 (at time of purchase) | Foreign fixed income securities, custodial receipts, municipal and convertible securities, forward foreign currencies and repurchase agreements collateralized by U.S. Government Securities. Also invests in futures, swaps, other derivatives and ETFs. |

High Yield |

A high level of current income, and may also consider the potential for capital appreciation. | Target Duration* = Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index plus or minus 2.5 years | At least 80% of its Net Assets in high-yield, fixed income securities that, at the time of purchase, are non-investment grade securities. | At least 80% of Net Assets rated BB+/Ba1 or below (at time of purchase) | Foreign fixed income securities, senior and subordinated corporate debt obligations, convertible and non-convertible corporate debt obligations, loan participations, custodial receipts, municipal securities, and preferred stock. Also invests in credit default swap indices, other derivatives and ETFs. |

Underlying Fund |

Investment Objectives |

Duration or Maturity |

Investment Sector |

Credit Quality |

Other Investments |

Local Emerging Markets Debt |

A high level of total return consisting of income and capital appreciation. | Target Duration* = J.P. Morgan Government Bond Index – Emerging Markets Global Diversified Index, plus or minus 2 years. | At least 80% of its Net Assets in sovereign and corporate debt securities of issuers in emerging market countries, denominated in the local currency, and other instruments, including credit linked notes and other investments, with similar economic exposures. | The Fund may invest in securities of any credit rating. | All types of foreign and emerging country fixed income securities, including Brady bonds and other government-issued debt, interests issued by entities organized and operated for the purpose of restructuring the investment characteristics of instruments issued by emerging country issuers, fixed and floating rate, senior and subordinated corporate debt obligations (such as bonds, debentures, notes, and commercial paper), loan participations, and repurchase agreements with respect to these types of securities. Also invests in swaps, forwards, futures and ETFs. |

High Yield Floating Rate |

A high level of current income. | Average Duration* = Credit Suisse Leveraged Loan Index, plus or minus one year. | At least 80% of Net Assets in domestic or foreign floating rate loans and other floating or variable rate obligations rated below investment grade. | At least 80% of Net Assets rated BB+/Ba1 or below (at time of purchase) | Fixed income instruments, regardless of rating, including fixed rate corporate bonds, government bonds, convertible debt obligations, and mezzanine fixed income instruments. Also invests in floating or variable rate instruments that are rated investment grade and in preferred stock, repurchase agreements, cash securities and ETFs. |

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

MLP Energy Infrastructure |

Total return through current income and capital appreciation. | At least 80% of its Net Assets in U.S. and non-U.S. equity or fixed income securities issued by energy infrastructure companies, including master limited partnerships (“MLPs”) and “C” corporations (“C-Corps”). | The Alerian MLP Index (Total Return, Unhedged, USD) is the leading gauge of energy infrastructure MLPs and is a capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities. |

| The Fund’s investments in MLPs will consist of at least 25% of the Fund’s total assets as measured at the time of purchase. The Fund intends to concentrate its investments in the energy sector. For purposes of the Fund’s 80% policy discussed above, the Fund’s investments in energy infrastructure companies include U.S. and non-U.S. issuers that: (i) are classified by a third party as operating within the oil and gas storage and transportation sub-industries; (ii) are part of the Fund’s stated benchmark; or (iii) have at least 50% of their assets, income, sales or profits committed to, or derived from, traditional or alternative midstream (energy infrastructure) businesses, which include businesses that are engaged in the treatment, gathering, compression, processing, transportation, transmission, fractionation, storage, terminalling, wholesale marketing, liquefaction/regasification of natural gas, natural gas liquids, crude oil, refined products or other energy sources as well as businesses engaged in owning, storing and transporting alternative energy sources, such as renewables (wind, solar, hydrogen, geothermal, biomass) and alternative fuels (ethanol, hydrogen, biodiesel). | |||

| The Fund’s MLP investments may include MLPs structured as limited partnerships (“LPs”) or limited liability companies (“LLCs”); MLPs that are taxed as C-Corps; institutional units (“I-Units”) issued by MLP affiliates; private investments in public equities (“PIPEs”) issued by MLPs; and other U.S. and non-U.S. equity and fixed income securities and derivative instruments, including pooled investment vehicles and exchange-traded notes (“ETNs”), that provide exposure to MLPs. |

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

Tactical Tilt Overlay |

Long-term total return | The Fund seeks to implement investment ideas that are generally derived from short-term or medium-term market views on a variety of asset classes and instruments (“Tactical Tilts”) generated by the Goldman Sachs Investment Strategy Group. Tactical Tilts are generally implemented by investing in any one or in any combination of the following securities and instruments: (i) U.S. and foreign equity securities, including common and preferred stocks; (ii) pooled investment vehicles including, but not limited to, (a) unaffiliated investment companies, ETFs and exchange-traded notes (“ETNs”) and (b) affiliated investment companies that currently exist or that may become available for investment in the future for which GSAM or an affiliate now or in the future acts as investment adviser or principal underwriter; (iii) fixed income instruments, which include, among others, debt issued by governments (including the U.S. and foreign governments), their agencies, instrumentalities, sponsored entities, and political subdivisions, notes, commercial paper, certificates of deposit, debt participations and non-investment grade securities (commonly known as “junk bonds”); (iv) derivatives; and (v) commodity investments, primarily through a wholly-owned subsidiary of the Fund organized as a company under the laws of the Cayman Islands. | The Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index tracks the performance of a synthetic asset paying the LIBOR to a stated maturity. |

| The Fund’s investments may be publicly traded or privately issued or negotiated. The Fund may invest without restriction as to issuer capitalization, country, currency, maturity or credit rating. The Fund may implement short positions for hedging purposes or to seek to enhance absolute return, and may do so by using swaps or futures, or through short sales of any instrument that the Fund may purchase for investment. |

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

Energy Infrastructure |

Total return through current income and capital appreciation | At least 80% of its Net Assets in U.S. and non-U.S. equity or fixed income securities issued by energy infrastructure companies, including master limited partnerships (“MLPs”) and “C” corporations (“C-Corps”). | The Alerian Midstream Energy Select Index (Total Return, Unhedged, USD) is a composite of North American energy infrastructure companies and is a capped, float-adjusted, capitalization-weighted index, whose constituents are engaged in midstream activities involving energy commodities. |

| For purposes of the Fund’s 80% policy discussed above, the Fund’s investments in energy infrastructure companies include U.S. and non-U.S. issuers that: (i) are classified by a third party as operating within the oil and gas storage and transportation sub-industries; (ii) are part of the Fund’s stated benchmark; or (iii) have at least 50% of their assets, income, sales or profits committed to, or derived from, traditional or alternative midstream (energy infrastructure) businesses, which include businesses that are engaged in the treatment, gathering, compression, processing, transportation, transmission, fractionation, storage, terminalling, wholesale marketing, liquefaction/regasification of natural gas, natural gas liquids, crude oil, refined products or ether energy sources as well as businesses engaged in owning, storing and transporting alternative energy sources, such as renewables (wind, solar, hydrogen, geothermal, biomass) and alternative fuels (ethanol, hydrogen, biodiesel). | |||

| The Fund’s MLP investments may include MLPs structured as limited partnerships (“LPs”) or limited liability companies (“LLCs”); MLPs that are taxed as C-Corps; institutional units (“I-Units”) issued by MLP affiliates; private investments in public equities (“PIPEs”) issued by MLPs; and other U.S. and non-U.S. equity and fixed income securities and derivative instruments, including pooled investment vehicles and exchange-traded notes (“ETNs”), that provide exposure to MLPs. | |||

Underlying Fund |

Investment Objectives |

Investment Criteria |

Benchmark Descriptions |

Clean Energy Income |

Total return through current income and capital appreciation | At least 80% of its Net Assets in U.S. and non-U.S. securities issued by clean energy companies. | The Fund has a blended benchmark comprised of three indices: Eagle North American Renewables Infrastructure Index (50%), Indxx Yieldco and Renewable Energy Income Index (35%), and Eagle Global Renewables Infrastructure Index (15%). |

| For purposes of the Fund’s 80% policy discussed above, the Fund’s investments in clean energy companies may include: U.S. and non-U.S. companies that (i) are constituents of one or more of the Fund’s stated benchmarks; (ii) are classified by the Global Industry Classification Standard (“GICS”) as part of the Renewable Electricity sub-industry; or (iii) have at least 50% of their assets, income, earnings, sales or profits committed to, or derived from, renewable energy electricity generation (wind, solar, hydrogen, geothermal, biomass, etc.), renewable storage and transmission, renewable energy equipment development manufacturing, electrified transport, biofuel production or energy efficiency solutions (including smart grid). Some of the clean energy companies in which the Fund invests, including companies that the Investment Adviser believes are involved in the transition to a more sustainable energy sector, may have operations that involve traditional energy facilities (including oil, gas or other hydrocarbons). | |||

| The Fund will concentrate its investments in companies in the clean energy group of industries. The Fund intends to focus its investmentson clean energy infrastructure companies. The Investment Adviser expects that the Fund’s investments will be weighted in favor of companies that pay dividends or other current distributions. |

* |

An Underlying Fund’s duration approximates its price sensitivity to changes in interest rates. |

| ■ | Credit/Default Risk —An issuer or guarantor of fixed income securities or instruments held by an Underlying Fund (which may have low credit ratings), may default on its obligation to pay interest and repay principal or default on any other obligation. The credit quality of an Underlying Fund’s portfolio securities or instruments may meet the Underlying Fund’s credit quality requirements at the time of purchase but then deteriorate thereafter, and such a deterioration can occur rapidly. In certain instances, the downgrading or default of a single holding or guarantor of the Underlying Fund’s holdings may impair the Underlying Fund’s liquidity and have the potential to cause significant NAV deterioration. These risks are more pronounced in connection with an Underlying Fund’s investments in non-investment grade fixed income securities. |

| ■ | Interest Rate Risk— When interest rates increase, fixed income securities or instruments held by an Underlying Fund (which may include inflation protected securities) will generally decline in value. Long-term fixed income securities or instruments will normally have more price volatility because of this risk than short-term fixed income securities or instruments. A wide variety of market factors can cause interest rates to rise, including central bank monetary policy, rising inflation and changes in general economic conditions. The risks associated with changing interest rates may have unpredictable effects on the markets and an Underlying Fund’s investments. Fluctuations in interest rates may also affect the liquidity of fixed income securities and instruments held by an Underlying Fund. |

| Interest rates in the United States are currently at historically low levels. Certain countries have experienced negative interest rates on certain fixed-income instruments. Very low or negative interest rates may magnify interest rate risk. Changing interest rates, including rates that fall below zero, may have unpredictable effects on markets, may result in heightened market volatility and may detract from Underlying Fund performance to the extent the Underlying Fund is exposed to such interest rates and/or volatility. | |

| ■ | Large Shareholder Transactions Risk — An Underlying Fund may experience adverse effects when certain large shareholders, such as other funds, institutional investors (including those trading by use of non-discretionary mathematical formulas), financial intermediaries (who may make investment decisions on behalf of underlying clients and/or include the Underlying Fund in their investment model), individuals, accounts and Goldman Sachs affiliates, purchase or redeem large amounts of shares of the Underlying Fund. Such large shareholder redemptions, which may occur rapidly or unexpectedly, may cause an Underlying Fund to sell portfolio securities at times when it would not otherwise do so, which may negatively impact the Underlying Fund’s NAV and liquidity. Similarly, large purchases of Underlying Fund shares may adversely affect the Underlying Fund’s performance to the extent that the Underlying Fund is delayed in investing new cash or otherwise maintains a larger cash position than it ordinarily would. These transactions may also accelerate the realization of taxable income to shareholders if such sales of investments resulted in gains, and may also increase transaction costs. In addition, a large redemption could result in an Underlying Fund’s current expenses being allocated over a smaller asset base, leading to an increase in the Underlying Fund’s expense ratio. |

| ■ | Liquidity Risk— An Underlying Fund may invest to a greater degree in securities or instruments that trade in lower volumes and may make investments that may be less liquid than other investments. An Underlying Fund may make investments that may become less liquid in response to market developments or adverse investor perceptions. Investments that are illiquid or that trade in lower volumes may be more difficult to value. When there is no willing buyer and investments cannot be readily sold at the desired time or price, an Underlying Fund may have to accept a lower price or may not be able to sell the security or instrument at all. An inability to sell one or more portfolio positions can adversely affect the Underlying Fund’s value or prevent the Underlying Fund from being able to take advantage of other investment opportunities. |

| To the extent that the traditional dealer counterparties that engage in fixed income trading do not maintain inventories of bonds (which provide an important indication of their ability to “make markets”) that keep pace with the growth of the bond markets over time, relatively low levels of dealer inventories could lead to decreased liquidity and increased volatility in the fixed income markets. Additionally, market participants other than an Underlying Fund may attempt to sell fixed income holdings at the same time as the Underlying Fund, which could cause downward pricing pressure and contribute to decreased liquidity. |

| Underlying Funds that invest in non-investment grade fixed income securities, small- and mid-capitalization stocks, REITs and/or emerging country issuers may be especially subject to the risk that, during certain periods, the liquidity of particular issuers or industries, or all securities within a particular investment category, may shrink or disappear suddenly and without warning as a result of adverse economic, market or political events, or adverse investor perceptions whether or not accurate. | |

| Liquidity risk may also refer to the risk that an Underlying Fund will not be able to pay redemption proceeds within the allowable time period stated in the Underlying Fund’s prospectus or without significant dilution to remaining investors’ interests because of unusual market conditions, an usually high volume of redemption requests, or other reasons. While an Underlying Fund reserves the right to meet redemption requests through in-kind distributions, the Underlying Fund may instead choose to raise cash to meet redemption requests through sales of portfolio securities or permissible borrowings. In connection with the Goldman Sachs Tax-Advantaged Global Equity Portfolio’s quarterly and other periodic rebalances of its investments in the Underlying Tax-Managed Funds, the Goldman Sachs Tax-Advantaged Global Equity Portfolio may, and in some cases is expected to, receive in-kind distributions of securities from the Underlying Tax-Managed Funds. The Goldman Sachs Tax-Advantaged Global Equity Portfolio will incur transaction costs upon the disposition of those securities. In addition, the Goldman Sachs Tax-Advantaged Global Equity Portfolio will be subject to market gains or losses, and may realize gains or losses, upon the disposition of those securities. If an Underlying Fund is forced to sell securities at an unfavorable time and/or under unfavorable conditions, such sales may adversely affect the Underlying Fund’s NAV and dilute remaining investors’ interests. | |

| Certain shareholders, including clients or affiliates of the Investment Adviser and/or other funds managed by the Investment Adviser, may from time to time own or control a significant percentage of an Underlying Fund’s shares. Redemptions by these shareholders of their shares of that Underlying Fund may further increase the Underlying Fund’s liquidity risk and may impact the Underlying Fund’s NAV. These shareholders may include, for example, institutional investors, funds of funds, discretionary advisory clients and other shareholders whose buy-sell decisions are controlled by a single decision-maker. | |

| ■ | Management Risk — A strategy used by an investment adviser to the Underlying Funds may fail to produce the intended results. With respect to certain Underlying Funds, the Underlying Fund’s investment adviser attempts to execute a complex investment strategy using proprietary quantitative models. Investments selected using these models may perform differently than expected as a result of the factors used in the models, the weight placed on each factor, changes from the factors’ historical trends, the speed that market conditions change, and technical issues in the construction and implementation of the models (including, for example, data problems and/or software issues). The use of proprietary quantitative models could be adversely impacted by unforeseeable software or hardware malfunction and other technological failures, power loss, software bugs, malicious code such as “worms,” viruses or system crashes or various other events or circumstances within or beyond the control of the Investment Adviser. Certain of these events or circumstances may be difficult to detect. |

| Models that have been formulated on the basis of past market data may not be predictive of future price movements. Models may not be reliable if unusual or disruptive events cause market movements, the nature or size of which are inconsistent with the historical performance of individual markets and their relationship to one another or to other macroeconomic events. Models also rely heavily on data that may be licensed from a variety of sources, and the functionality of the models depends, in part, on the accuracy of voluminous data inputs. There is no guarantee that an Underlying Fund’s investment adviser’s use of this quantitative methodology will result in effective investment decisions for the Underlying Fund. Additionally, commonality of holdings across quantitative money managers may amplify losses. | |

| ■ | Market Risk— The value of the securities in which the Fund and/or an Underlying Fund invests may go up or down in response to the prospects of individual companies, particular sectors or governments and/or general economic conditions throughout the world. Price changes may be temporary or last for extended periods. The Fund's and/or an Underlying Fund's investments may be overweighted from time to time in one or more sectors or countries, which will increase the Fund's and/or an Underlying Fund's exposure to risk of loss from adverse developments affecting those sectors or countries. |

| Global economies and financial markets are becoming increasingly interconnected, and conditions and events in one country, region or financial market may adversely impact issuers in a different country, region or financial market. Furthermore, local, regional and global events such as war, acts of terrorism, social unrest, natural disasters, the spread of infectious illness or other public health threats could also adversely impact issuers, markets and economies, including in ways that cannot necessarily be foreseen. could be negatively impacted if the value of a portfolio holding were harmed by such political or economic conditions or events. In addition, governmental and quasi-governmental organizations have taken a number of unprecedented actions designed to support the markets. Such conditions, events and actions may result in greater market risk. | |

| ■ | NAV Risk— The NAV of an Underlying Fund and the value of your investment will fluctuate. |

| ■ | Non-Diversification Risk— Certain Underlying Funds are non-diversified, meaning that the Underlying Fund is permitted to invest a larger percentage of their assets in fewer issuers than diversified mutual funds. Thus, the Underlying Funds may be more susceptible to adverse developments affecting any single issuer held in their portfolios , and may be more susceptible to greater losses because of these developments. |

| ■ | U.S. Government Securities Risk— The U.S. government may not provide financial support to U.S. government agencies, instrumentalities or sponsored enterprises if it is not obligated to do so by law. U.S. Government Securities issued by those agencies, instrumentalities and sponsored enterprises, including those issued by the Federal National Mortgage Association (“Fannie Mae”), Federal Home Loan Mortgage Corporation (“Freddie Mac”) and Federal Home Loan Banks, are neither issued nor guaranteed by the U.S. Treasury and, therefore, are not backed by the full faith and credit of the United States. The maximum potential liability of the issuers of some U.S. Government Securities held by an Underlying Fund may greatly exceed their current resources, including any legal right to support from the U.S. Treasury. It is possible that issuers of U.S. Government Securities will not have the funds to meet their payment obligations in the future. Fannie Mae and Freddie Mac have been operating under conservatorship, with the Federal Housing Finance Agency (“FHFA”) acting as their conservator, since September 2008. The entities are dependent upon the continued support of the U.S. Department of the Treasury and FHFA in order to continue their business operations. These factors, among others, could affect the future status and role of Fannie Mae and Freddie Mac and the value of their securities and the securities which they guarantee. Additionally, the U.S. government and its agencies and instrumentalities do not guarantee the market values of their securities, which may fluctuate. |

| ■ | Dividend-Paying Investments Risk —An Underlying Fund’s investments in dividend-paying securities could cause the Underlying Fund to underperform other funds that invest in similar asset classes but employ a different investment style. Securities that pay dividends, as a group, can fall out of favor with the market, causing such securities to underperform securities that do not pay dividends. Depending upon market conditions and political and legislative responses to such conditions, dividend-paying securities that meet an Underlying Fund’s investment criteria may not be widely available and/or may be highly concentrated in only a few market sectors. For example, in response to the outbreak of a novel strain of coronavirus (known as COVID-19), the U.S. Government passed the Coronavirus Aid, Relief and Economic Security Act in March 2020, which established loan programs for certain issuers impacted by COVID-19. Among other conditions, borrowers under these loan programs are generally restricted from paying dividends. The adoption of new legislation could further limit or restrict the ability of issuers to pay dividends. To the extent that dividend-paying securities are concentrated in only a few market sectors, an Underlying Fund may be subject to the risks of volatile economic cycles and/or conditions or developments that may be particular to a sector to a greater extent than if its investments were diversified across different sectors. In addition, issuers that have paid regular dividends or distributions to shareholders may not continue to do so at the same level or at all in the future. A sharp rise in interest rates or an economic downturn could cause an issuer to abruptly reduce or eliminate its dividend. This may limit the ability of an Underlying Fund to produce current income. |

| ■ | Portfolio Turnover Rate Risk — A high rate of portfolio turnover (100% or more) involves correspondingly greater expenses which must be borne by an Underlying Fund and its shareholders (including the Funds), and is also likely to result in short-term capital gains taxable to shareholders of the Underlying Fund. |

| ■ | Stock Risk— Stock prices have historically risen and fallen in periodic cycles. U.S.and foreign stock markets have experienced periods of substantial price volatility in the past and may do so again in the future. Stock prices may fluctuate from time to time in response to the activities of individual companies and in response to general market and economic conditions. Individual companies may report poor results or be negatively affected by industry and/or economic trends and developments, and the stock prices of such companies may suffer a decline in response. |

| ■ | Call/Prepayment Risk —An issuer could exercise its right to pay principal on an obligation held by the Fund and/or an Underlying Fund the value of the obligation may decrease, and the Fund and/or an Underlying Fund(such as a mortgage-backed security) earlier than expected. This may happen when there is a decline in interest rates, when credit spreads change, or when an issuer’s credit quality improves. Under these circumstances, the Fund and/or an Underlying Fund the value of the obligation may decrease, and the Fund and/or an Underlying Fund may be unable to recoup all of its initial investment and will also suffer from having to reinvest in lower-yielding securities. |

| ■ | Distressed Debt Risk —When an Underlying Fund invests in obligations of financially troubled companies (sometimes known as “distressed” securities), there exists the risk that the transaction involving such debt obligations will be unsuccessful, take considerable time or will result in a distribution of cash or a new security or obligation in exchange for the stressed and distressed debt obligations, the value of which may be less than such Underlying Fund’s purchase price of such debt obligations. Furthermore, if an anticipated transaction does not occur, an Underlying Fund may be required to sell its investment at a loss or hold its investment pending bankruptcy proceedings in the event the issuer files for bankruptcy. |

| ■ | Extension Risk —An issuer could exercise its right to pay principal on an obligation held by an Underlying Fund (such as a mortgage-backed security) later than expected. This may happen when there is a rise in interest rates. Under these circumstances, the value of the obligation will decrease, and an Underlying Fund will also suffer from the inability to reinvest in higher yielding securities. |

| ■ | Floating and Variable Rate Obligations Risk— Floating rate and variable rate obligations are debt instruments issued by companies or other entities with interest rates that reset periodically (typically, daily, monthly, quarterly, or semi-annually) in response to changes in the market rate of interest on which the interest rate is based. For floating and variable rate obligations, there may be a lag between an actual change in the underlying interest rate benchmark and the reset time for an interest payment of such an obligation, which could harm or benefit the Underlying Fund, depending on the interest rate environment or other circumstances. In a rising interest rate environment, for example, a floating or variable rate obligation that does not reset immediately would prevent the Fund from taking full advantage of rising interest rates in a timely manner. However, in a declining interest rate environment, the Underlying Fund may benefit from a lag due to an obligation’s interest rate payment not being immediately impacted by a decline in interest rates. |

| Certain floating and variable rate obligations have an interest rate floor feature, which prevents the interest rate payable by the security from dropping below a specified level as compared to a reference interest rate (the “reference rate”), such as LIBOR. Such a floor protects the Underlying Fund from losses resulting from a decrease in the reference rate below the specified level. However, if the reference rate is below the floor, there will be a lag between a rise in the reference rate and a rise in the interest rate payable by the obligation, and the Underlying Fund may not benefit from increasing interest rates for a significant amount of time. | |

| In 2017, the United Kingdom’s Financial Conduct Authority (“FCA”) warned that LIBOR may cease to be available or appropriate for use by 2021. The unavailability or replacement of LIBOR may affect the value, liquidity or return on certain Underlying Fund investments and may result in costs incurred in connection with closing out positions and entering into new trades. Any pricing adjustments to the Underlying Fund’s investments resulting from a substitute reference rate may adversely affect the Underlying Fund’s performance and/or NAV. | |

| ■ | Loan-Related Investments Risk— In addition to risks generally associated with debt investments ( e.g. , interest rate risk and default risk), loan-related investments such as loan participations and assignments are subject to other risks. Although a loan obligation may be fully collateralized at the time of acquisition, the collateral may decline in value, be or become illiquid or less liquid, or lose all or substantially all of its value subsequent to investment. Many loan investments are subject to legal or contractual restrictions on resale and certain loan investments may be or become illiquid or less liquid and more difficult to value, particularly in the event of a downgrade of the loan or the borrower. There is less readily available, reliable information about most loan investments than is the case for many other types of securities and the Investment Adviser relies primarily on its own evaluation of a borrower’s credit quality rather than on any available independent sources. The ability of an Underlying Fund to realize full value in the event of the need to sell a loan investment may be impaired by the lack of an active trading market for certain loans or adverse market conditions limiting liquidity. Loan obligations are not traded on an exchange, and purchasers and sellers rely on certain market makers, such as the administrative agent for the particular loan obligation, to trade that loan obligation. The market for loan obligations may be subject to irregular trading activity, wide bid/ask spreads and extended trade settlement periods. Because transactions in many loans are subject to extended trade settlement periods, an Underlying Fund may not receive the proceeds from the sale of a loan for a period after the sale. As a result, sale proceeds related to the sale of loans may not be available to make additional investments or to meet an Underlying Fund's redemption obligations for a period after the sale of the loans, and, as a result, an Underlying Fund may have to sell other investments or engage in borrowing transactions, such as borrowing from a credit facility, if necessary to raise cash to meet its obligations. During periods of heightened redemption activity or distressed market conditions, an Underlying Fund may seek to obtain expedited trade settlement, which will generally incur additional costs (although expedited trade settlement will not always be available). An Underlying Fund may also hold a larger position in cash and cash items to limit the impact of extended trade settlement periods, which may adversely impact an Underlying Fund's performance. In addition, substantial increases in interest rates may cause an increase in loan obligation defaults. |

| Affiliates of the Investment Adviser may participate in the primary and secondary market for loans. Because of limitations imposed by applicable law, the presence of such affiliates in the loan markets may restrict an Underlying Fund's ability to acquire certain loans, affect the timing of such acquisition, or affect the price at which the loan is acquired. | |

| With respect to loan participations, an Underlying Fund may not always have direct recourse against a borrower if the borrower fails to pay scheduled principal and/or interest; may be subject to greater delays, expenses and risks than if an Underlying Fund had purchased a direct obligation of the borrower; and may be regarded as the creditor of the agent lender (rather than the borrower), subjecting an Underlying Fund to the creditworthiness of that lender as well and the ability of the lender to enforce appropriate credit remedies against the borrower. Investors in loans, such as an Underlying Fund, may not be entitled to rely on the anti-fraud protections of the federal securities laws, although they may be entitled to certain contractual remedies. | |

| Senior loans hold the most senior position in the capital structure of a business entity, and are typically secured with specific collateral and have a claim on the assets and/or stock of the borrower that is senior to that held by subordinated debt holders and stockholders of the borrower. Nevertheless, senior loans are usually rated below investment grade. Because second lien loans are subordinated or unsecured and thus lower in priority of payment to senior loans, they are subject to the additional risk that the cash flow of the borrower and property securing the loan or debt, if any, may be insufficient to meet scheduled payments after giving effect to the senior secured obligations of the borrower. This risk is generally higher for subordinated unsecured loans or debt, |