Form 8-K OMNICOM GROUP INC. For: Feb 09

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): February 9, 2016

OMNICOM GROUP INC.

(Exact Name of Registrant as Specified in its Charter)

|

New York (State or other jurisdiction |

1-10551 (Commission |

13-1514814 (IRS Employer |

|

437 Madison Avenue, New York, NY (Address of principal executive offices) |

10022 (Zip Code) |

Registrant’s telephone number, including area code: (212) 415-3600

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Item 2.02 Results of Operations and Financial Condition.

On February 9, 2016, Omnicom Group Inc. (“Omnicom” or the “Company”) published an earnings release reporting its financial results for the three and twelve months ended December 31, 2015. A copy of the earnings release is attached as Exhibit 99.1 hereto and is incorporated by reference herein. Following the publication of the earnings release, Omnicom hosted an earnings call in which its financial results were discussed. The investor presentation materials used for the call are attached as Exhibit 99.2 hereto and are incorporated by reference herein.

On February 9, 2016, Omnicom posted the materials attached as Exhibits 99.1 and 99.2 on its web site (www.omnicomgroup.com).

Certain statements in the exhibits to this Current Report on Form 8-K constitute forward-looking statements, including statements within the meaning of the Private Securities Litigation Reform Act of 1995. In addition, from time to time, the Company or its representatives have made, or may make, forward-looking statements, orally or in writing. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management as well as assumptions made by, and information currently available to, the Company’s management. Forward-looking statements may be accompanied by words such as “aim,” “anticipate,” “believe,” “plan,” “could,” “should,” “would,” “estimate,” “expect,” “forecast,” “future,” “guidance,” “intend,” “may,” “will,” “possible,” “potential,” “predict,” “project” or similar words, phrases or expressions. These forward-looking statements are subject to various risks and uncertainties, many of which are outside the Company’s control. Therefore, you should not place undue reliance on such statements. Factors that could cause actual results to differ materially from those in the forward-looking statements include: international, national or local economic conditions that could adversely affect the Company or its clients; losses on media purchases and production costs incurred on behalf of clients; reductions in client spending, a slowdown in client payments and a deterioration in the credit markets; ability to attract new clients and retain existing clients in the manner anticipated; changes in client advertising, marketing and corporate communications requirements; failure to manage potential conflicts of interest between or among clients; unanticipated changes relating to competitive factors in the advertising, marketing and corporate communications industries; ability to hire and retain key personnel; currency exchange rate fluctuations; reliance on information technology systems; changes in legislation or governmental regulations affecting the Company or its clients; risks associated with assumptions the Company makes in connection with its critical accounting estimates and legal proceedings; and the Company’s international operations, which are subject to the risks of currency repatriation restrictions, social or political conditions and regulatory environment. The foregoing list of factors is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties that may affect the Company’s business, including those described under “Risk Factors” in Omnicom's Annual Report on Form 10-K for the year ended December 31, 2014 and other documents filed from time to time with the SEC. Except as required under applicable law, the Company does not assume any obligation to update these forward-looking statements.

The foregoing information (including the exhibits hereto) is being furnished and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, except as expressly set forth by specific reference in such filing.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits.

|

Exhibit |

Description |

| 99.1 | Earnings release dated February 9, 2016. |

| 99.2 |

Investor presentation materials dated February 9, 2016.

|

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Omnicom Group Inc. | |||

| By: | /s/ Andrew L. Castellaneta | ||

| Name: | Andrew L. Castellaneta | ||

| Title: | Senior Vice President, | ||

| Chief Accounting Officer | |||

Date: February 9, 2016

2

EXHIBIT INDEX

|

Exhibit |

Description |

| 99.1 | Earnings release dated February 9, 2016. |

| 99.2 |

Investor presentation materials dated February 9, 2016. |

3

Exhibit 99.1

Omnicom Group Reports Full Year and Fourth Quarter 2015 Results

NEW YORK, February 9, 2016 - Omnicom Group Inc. (NYSE: OMC) today announced that its diluted net income per common share for the twelve months ended December 31, 2015 increased 17 cents, or 4.0%, to $4.41 per share compared to $4.24 per share for the same period in 2014. For the fourth quarter of 2015, diluted net income per common share increased five cents, or 3.8%, to $1.35 per share versus $1.30 per share for the fourth quarter of 2014.

Worldwide revenue for the twelve months ended December 31, 2015 decreased 1.2% to $15,134.4 million from $15,317.8 million in the same period in 2014. The components of the change in revenue included an increase in revenue from organic growth of 5.3%, an increase in revenue from acquisitions, net of dispositions of 0.1% and a decrease in revenue from the negative impact of foreign exchange rates of 6.6% when compared to 2014.

In the fourth quarter of 2015, worldwide revenue decreased 1.0% to $4,153.3 million from $4,195.1 million in the fourth quarter of 2014. The components of the change in revenue included an increase in revenue from organic growth of 4.8%, a decrease in revenue from acquisitions, net of dispositions of 0.2% and a decrease in revenue from the negative impact of foreign exchange rates of 5.6% when compared to the fourth quarter of 2014.

Across our regional markets, for the twelve months ended December 31, 2015, organic revenue increased 5.4% in North America, 7.1% in the United Kingdom, 3.7% in the Euro Markets and Other Europe, 7.9% in Asia Pacific and 6.8% in Africa/Middle East, while organic revenue decreased 3.3% in Latin America when compared to the same period in 2014.

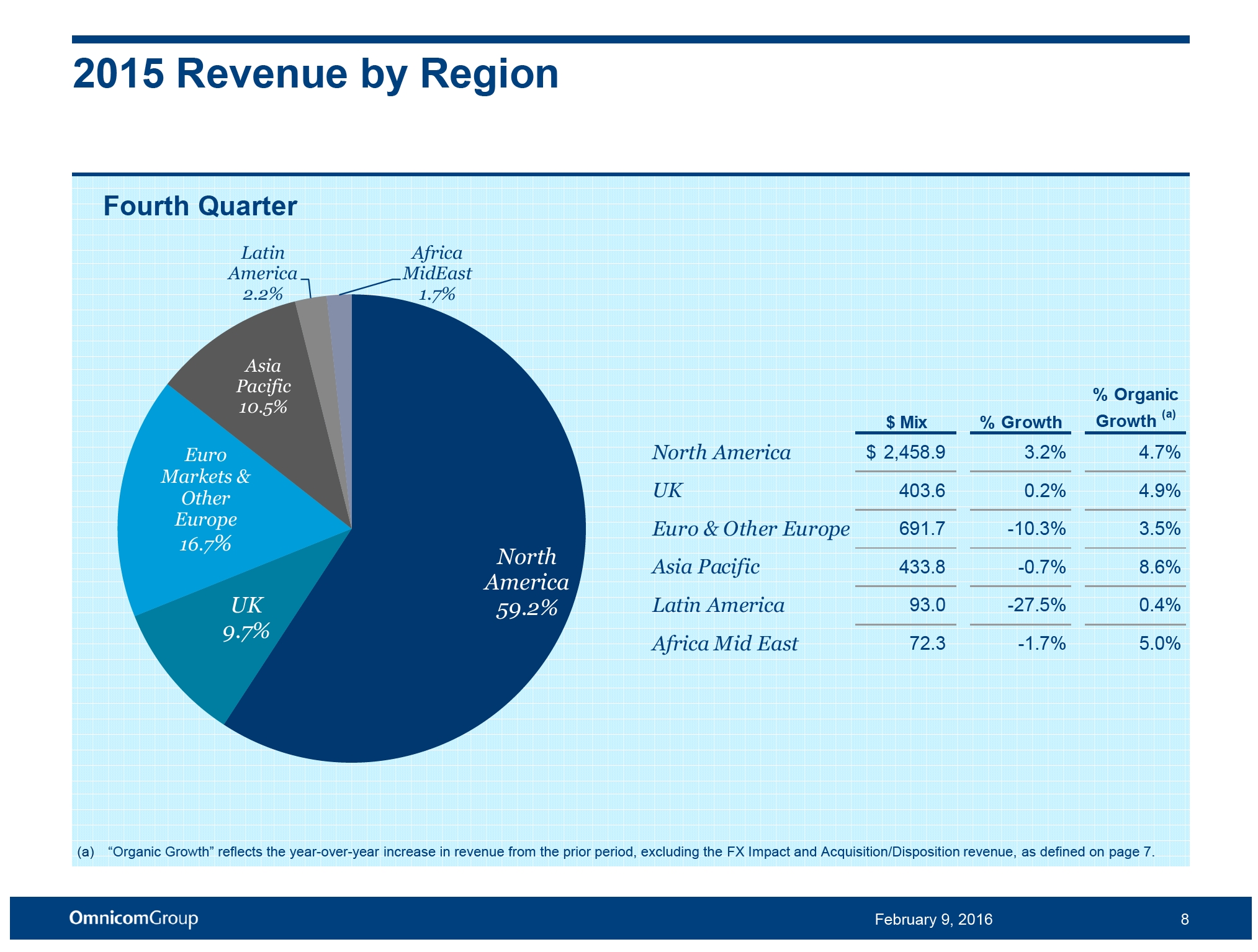

In the fourth quarter of 2015, organic revenue increased 4.7% in North America, 4.9% in the United Kingdom, 3.5% in the Euro Markets and Other Europe, 8.6% in Asia Pacific, 0.4% in Latin America and 5.0% in Africa/Middle East when compared to the same quarter of 2014.

437 Madison Avenue, New York, NY 10022 (212) 415-3600 Fax (212) 415-3530

1

Omnicom Group Inc.

The change in organic revenue in the twelve months ended December 31, 2015 compared to the same period in 2014 in our four fundamental disciplines was as follows: advertising increased 9.3%, CRM increased 1.9% and specialty communications increased 2.2%, while public relations decreased 1.4%.

In the fourth quarter of 2015, the change in organic revenue as compared to the fourth quarter of 2014 in our four fundamental disciplines was as follows: advertising increased 12.6% while CRM decreased 1.5%, public relations decreased 6.9% and specialty communications decreased 5.9%.

Omnicom’s earnings before interest, taxes and amortization of intangibles (“EBITA”), a non-GAAP financial measure, for the twelve months ended December 31, 2015 decreased 1.1%, or $21.8 million, to $2,029.4 million from $2,051.2 million for the same period in 2014. Our EBITA margin for the twelve months ended December 31, 2015 of 13.4% was unchanged when compared to the same period in 2014.

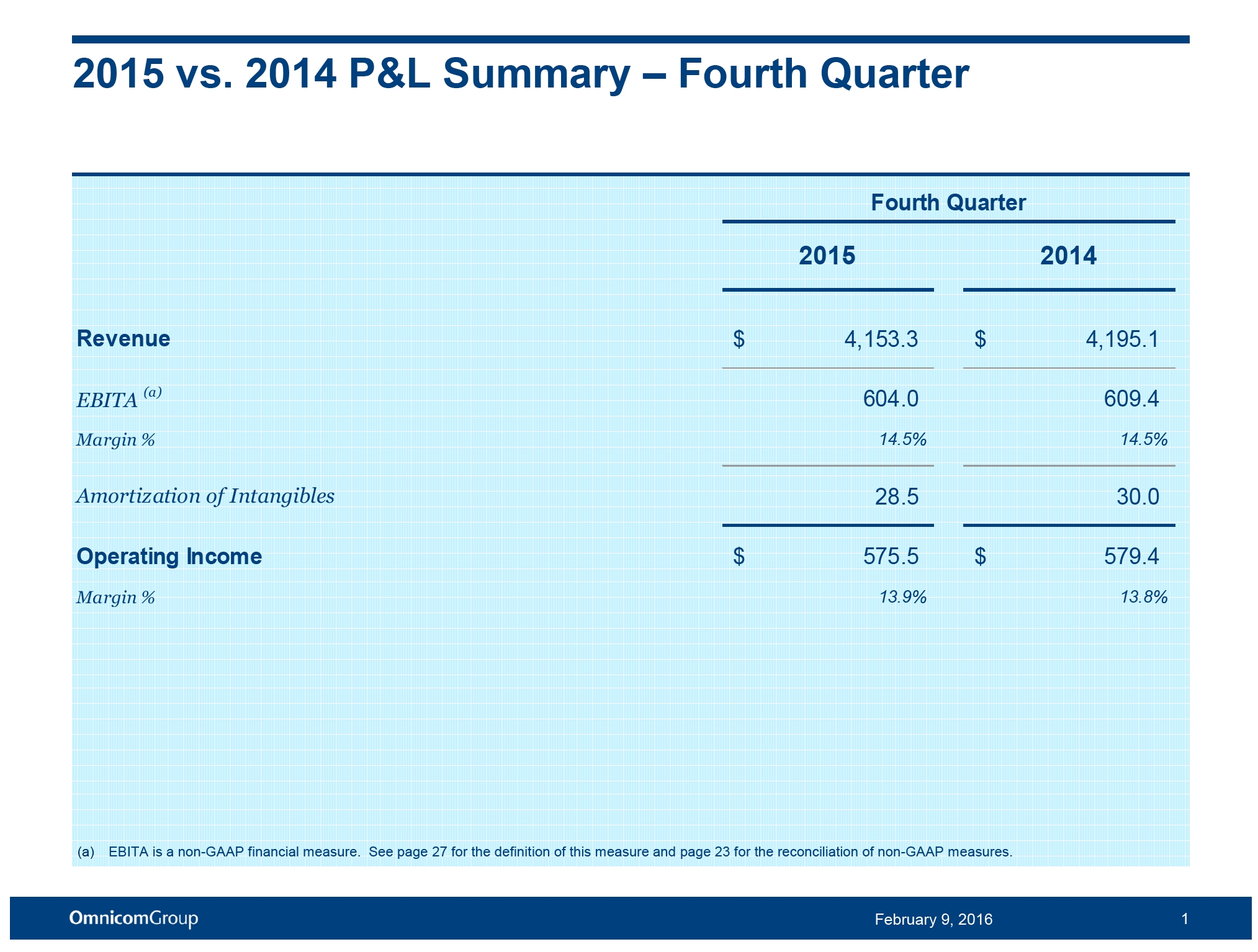

For the fourth quarter of 2015, Omnicom’s EBITA decreased $5.4 million, or 0.9%, to $604.0 million from $609.4 million in the fourth quarter of 2014. Our EBITA margin of 14.5% for the fourth quarter of 2015 was unchanged when compared to the fourth quarter of 2014.

Operating income for the twelve months ended December 31, 2015 decreased $24.0 million, or 1.2%, to $1,920.1 million compared to $1,944.1 million for the same period in 2014. Our operating margin for the twelve months ended December 31, 2015 of 12.7% was unchanged when compared to the same period in 2014.

In the fourth quarter of 2015, operating income decreased $3.9 million, or 0.7%, to $575.5 million from $579.4 million in the fourth quarter of 2014. Our operating margin increased to 13.9% for the fourth quarter of 2015 compared to 13.8% for the fourth quarter of 2014.

Our full year income tax rate for 2015 was 32.8%, which was unchanged versus the rate for 2014. For the fourth quarter of 2015, our income tax rate was 32.8% compared to 33.2% in the fourth quarter of 2014.

Page 2

Omnicom Group Inc.

Net income for the twelve months ended December 31, 2015 decreased $10.1 million, or 0.9%, to $1,093.9 million from $1,104.0 million in 2014. For the fourth quarter of 2015, net income increased $2.1 million, or 0.6%, to $331.6 million from $329.5 million in the fourth quarter of 2014.

Omnicom Group Inc. (NYSE: OMC) (www.omnicomgroup.com) is a leading global marketing and corporate communications company. Omnicom’s branded networks and numerous specialty firms provide advertising, strategic media planning and buying, digital and interactive marketing, direct and promotional marketing, public relations and other specialty communications services to over 5,000 clients in more than 100 countries. Follow us on Twitter for the latest news.

For a live webcast or a replay of our fourth quarter earnings conference call, go to http://investor.omnicomgroup.com/investor-relations/news-events-and-filings.

Contacts

| Investor Relations: | Media: |

| Shub Mukherjee, 212-415-3011 | Joanne Trout, 212-415-3669 |

| [email protected] | [email protected] |

Page 3

Omnicom Group Inc.

Consolidated Statements of Income

Twelve Months Ended December 31

(Unaudited)

(Dollars in Millions, Except Per Share Data)

| 2015 | 2014 | |||||||

| Revenue | $ | 15,134.4 | $ | 15,317.8 | ||||

| Operating Expenses, excluding amortization of intangibles | 13,105.0 | 13,266.6 | ||||||

| EBITA(a) | 2,029.4 | 2,051.2 | ||||||

| Less: Amortization of Intangibles | 109.3 | 107.1 | ||||||

| Operating Income | 1,920.1 | 1,944.1 | ||||||

| Net Interest Expense | 141.5 | 134.1 | ||||||

| Income before income taxes | 1,778.6 | 1,810.0 | ||||||

| Income tax expense | 583.6 | 593.1 | ||||||

| Income from equity method investments | 8.4 | 16.2 | ||||||

| Net income | 1,203.4 | 1,233.1 | ||||||

| Less: Net income allocated to noncontrolling interests | 109.5 | 129.1 | ||||||

| Net income - Omnicom Group Inc. | 1,093.9 | 1,104.0 | ||||||

| Less: Net income allocated to participating securities | 12.4 | 20.4 | ||||||

| Net income available for common shares | $ | 1,081.5 | $ | 1,083.6 | ||||

| Net income per common share - Omnicom Group Inc. | ||||||||

| Basic | $ | 4.43 | $ | 4.27 | ||||

| Diluted | $ | 4.41 | $ | 4.24 | ||||

| Weighted average shares (in millions) | ||||||||

| Basic | 244.2 | 253.9 | ||||||

| Diluted | 245.2 | 255.3 | ||||||

| Dividend declared per common share | $ | 2.00 | $ | 1.90 |

| (a) | EBITA (defined as Earnings before interest, taxes and amortization of intangibles) is a non-GAAP measure. We use EBITA as an additional operating performance measure, which excludes the non-cash amortization expense of acquired intangible assets. We believe that EBITA is a useful measure to evaluate the performance of our businesses. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with U.S. GAAP. Non-GAAP financial measures reported by us may not be comparable to similarly titled amounts reported by other companies. |

Page 4

Omnicom Group Inc.

Consolidated Statements of Income

Three Months Ended December 31

(Unaudited)

(Dollars in Millions, Except Per Share Data)

| 2015 | 2014 | |||||||

| Revenue | $ | 4,153.3 | $ | 4,195.1 | ||||

| Operating Expenses, excluding amortization of intangibles | 3,549.3 | 3,585.7 | ||||||

| EBITA (a) | 604.0 | 609.4 | ||||||

| Less: Amortization of Intangibles | 28.5 | 30.0 | ||||||

| Operating Income | 575.5 | 579.4 | ||||||

| Net Interest Expense | 36.8 | 30.0 | ||||||

| Income before income taxes | 538.7 | 549.4 | ||||||

| Income tax expense | 176.7 | 182.2 | ||||||

| Income from equity method investments | 2.2 | 5.7 | ||||||

| Net income | 364.2 | 372.9 | ||||||

| Less: Net income allocated to noncontrolling interests | 32.6 | 43.4 | ||||||

| Net income - Omnicom Group Inc. | 331.6 | 329.5 | ||||||

| Less: Net income allocated to participating securities | 3.3 | 5.6 | ||||||

| Net income available for common shares | $ | 328.3 | $ | 323.9 | ||||

| Net income per common share - Omnicom Group Inc. | ||||||||

| Basic | $ | 1.35 | $ | 1.30 | ||||

| Diluted | $ | 1.35 | $ | 1.30 | ||||

| Weighted average shares (in millions) | ||||||||

| Basic | 242.6 | 249.0 | ||||||

| Diluted | 243.8 | 249.9 | ||||||

| Dividend declared per common share | $ | 0.50 | $ | 0.50 |

| (a) | EBITA (defined as Earnings before interest, taxes and amortization of intangibles) is a non-GAAP measure. We use EBITA as an additional operating performance measure, which excludes the non-cash amortization expense of acquired intangible assets. We believe that EBITA is a useful measure to evaluate the performance of our businesses. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with U.S. GAAP. Non-GAAP financial measures reported by us may not be comparable to similarly titled amounts reported by other companies. |

Page 5

Exhibit 99.2

Fourth Quarter 2015 Results

February 9, 2016

Investor Presentation

2015 vs. 2014 P&L Summary – Fourth Quarter

Fourth Quarter

2015 2014

Revenue $ 4,153.3 $ 4,195.1

EBITA (a) 604.0 609.4

Margin % 14.5% 14.5%

Amortization of Intangibles 28.5 30.0

Operating Income $ 575.5 $ 579.4

Margin % 13.9% 13.8%

(a) EBITA is a non-GAAP financial measure. See page 28 for the definition of this measure and page 23 for the reconciliation of non-GAAP measures.

February 9, 2016 1

2015 vs. 2014 P&L Summary – Fourth Quarter

Fourth Quarter

2015 2014

Operating Income $ 575.5 $ 579.4

Net Interest Expense 36.8 30.0 Income Taxes 176.7 182.2

Tax Rate % 32.8% 33.2%

Income from Equity Method Investments 2.2 5.7 Noncontrolling Interests 32.6 43.4

Net Income - Omnicom Group 331.6 329.5

February 9, 2016 2

2015 vs. 2014 Earnings Per Share – Fourth Quarter

Fourth Quarter

2015 2014

Net Income - Omnicom Group $ 331.6 $ 329.5

Net Income allocated to Participating Securities (3.3) (5.6) Net Income available for common shares $ 328.3 $ 323.9

Diluted Shares (millions) 243.8 249.9

EPS - Diluted $ 1.35 $ 1.30

Dividend Declared per Share $ 0.50 $ 0.50

February 9, 2016 3

2015 vs. 2014 P&L Summary – Full Year

Full Year

2015 Reported 2014 Reported

Revenue $ 15,134.4 $ 15,317.8

EBITA (a) 2,029.4 2,051.2

Margin % 13.4% 13.4%

Amortization of Intangibles 109.3 107.1

Operating Income $ 1,920.1 $ 1,944.1

Margin % 12.7% 12.7%

(a) EBITA is a non-GAAP financial measure. See page 28 for the definition of this measure and page 23 for the reconciliation of non-GAAP measures.

February 9, 2016 4

2015 vs. 2014 P&L Summary – Full Year

Full Year 2015 2014 Reported Reported

Operating Income $ 1,920.1 $ 1,944.1

Net Interest Expense 141.5 134.1 Income Taxes 583.6 593.1

Tax Rate % 32.8% 32.8%

Income from Equity Method Investments 8.4 16.2 Noncontrolling Interests 109.5 129.1

Net Income - Omnicom Group 1,093.9 1,104.0

February 9, 2016 5

2015 vs. 2014 Earnings Per Share – Full Year

Full Year 2015 2014 Reported Reported Net Income - Omnicom Group $ 1,093.9 $ 1,104.0

Net Income allocated to Participating Securities (12.4) (20.4) Net Income available for common shares $ 1,081.5 $ 1,083.6

Diluted Shares (millions) 245.2 255.3

EPS - Diluted $ 4.41 $ 4.24

Dividend Declared per Share $ 2.00 $ 1.90

February 9, 2016 6

2015 Total Revenue Change

Fourth Quarter Full Year

$ % $ %

Prior Period Revenue $ 4,195.1 $ 15,317.8

Foreign Exchange (FX) Impact (a) (236.3) -5.6% (1,008.8) -6.6%

Acquisition/Disposition Revenue (b) (5.7) -0.2% 14.6 0.1%

Organic Revenue (c) 200.2 4.8% 810.8 5.3%

Current Period Revenue $ 4,153.3 -1.0% $ 15,134.4 -1.2%

(a) The FX Impact is calculated by translating the current period’s local currency revenue using the prior period average exchange rates to derive current period constant currency revenue. The FX impact is the difference between the current period revenue in U.S. Dollars and the current period constant currency revenue.

(b) Acquisition/Disposition revenue is calculated by aggregating the prior period revenue of the acquired businesses, less the prior period revenue of any business that was disposed of in the current period.

(c) Organic revenue is calculated by subtracting both the Acquisition/Disposition revenue and the FX impact from total revenue growth.

February 9, 2016 7

2015 Revenue by Region

Fourth Quarter

Latin Africa America MidEast 2.2% 1.7%

Asia Pacific

% Organic

10.5% $ Mix % Growth Growth (a)

Euro North America $ 2,458.9 3.2% 4.7%

Markets &

Other UK 403.6 0.2% 4.9%

Europe

Euro & Other Europe 691.7 -10.3% 3.5% 16.7% North

Asia Pacific 433.8 -0.7% 8.6%

America

UK 59.2% Latin America 93.0 -27.5% 0.4%

9.7%

Africa Mid East 72.3 -1.7% 5.0%

(a) “Organic Growth” reflects the year-over-year increase in revenue from the prior period, excluding the FX Impact and Acquisition/Disposition revenue, as defined on page 7.

February 9, 2016 8

2015 Revenue by Region

Full Year

Latin Africa America MidEast 2.2% 1.7%

Asia Pacific

% Organic

10.4% $ Mix % Growth Growth(a)

Euro North America $ 9,029.2 4.1% 5.4%

Markets &

Other UK 1,510.3 0.2% 7.1%

Europe

Euro & Other Europe 2,432.6 -14.3% 3.7%

16.1%

North Asia Pacific 1,571.9 -2.0% 7.9%

UK America

59.6% Latin America 329.8 -25.0% -3.3%

10.0%

Africa Mid East 260.6 1.7% 6.8%

(a) “Organic Growth” reflects the year-over-year increase or decrease in revenue from the prior period, excluding the FX Impact and Acquisition/Disposition revenue, as defined on page 7.

February 9, 2016 9

2015 Revenue by Discipline

Fourth Quarter Full Year

Specialty Specialty 6.8% 7.2% PR PR

8.2% 9.0%

Advertising Advertising 53.4% 51.1% CRM

31.6% CRM 32.7%

% Organic % Organic $ Mix % Growth Growth (a) $ Mix % Growth Growth (a)

Advertising $ 2,216.8 5.5% 12.6% Advertising $ 7,730.2 1.8% 9.3% CRM 1,314.1 -7.4% -1.5% CRM 4,958.2 -5.6% 1.9% PR 339.9 -7.7% -6.9% PR 1,361.0 -2.3% -1.4% Specialty 282.5 -7.8% -5.9% Specialty 1,085.0 0.8% 2.2%

(a) “Organic Growth” reflects the year-over-year increase or decrease in revenue from the prior period, excluding the FX Impact and Acquisition/Disposition revenue, as defined on page 7.

February 9, 2016 10

Revenue by Industry

Full Year – 2015 Full Year – 2014

T&E Auto T&E Auto

6% 8% 6% 8% Telcom Telcom

5% 5%

Consumer Consumer Products Products

9% Tech 9% Tech 9% 10%

Financial Financial Services Services

7% 7% Retail Retail

6% 7%

Food & Food & Beverage Pharma & Beverage Pharma & 13% Health 13% Health 11% 10%

Other Other 25% 26%

February 9, 2016 11

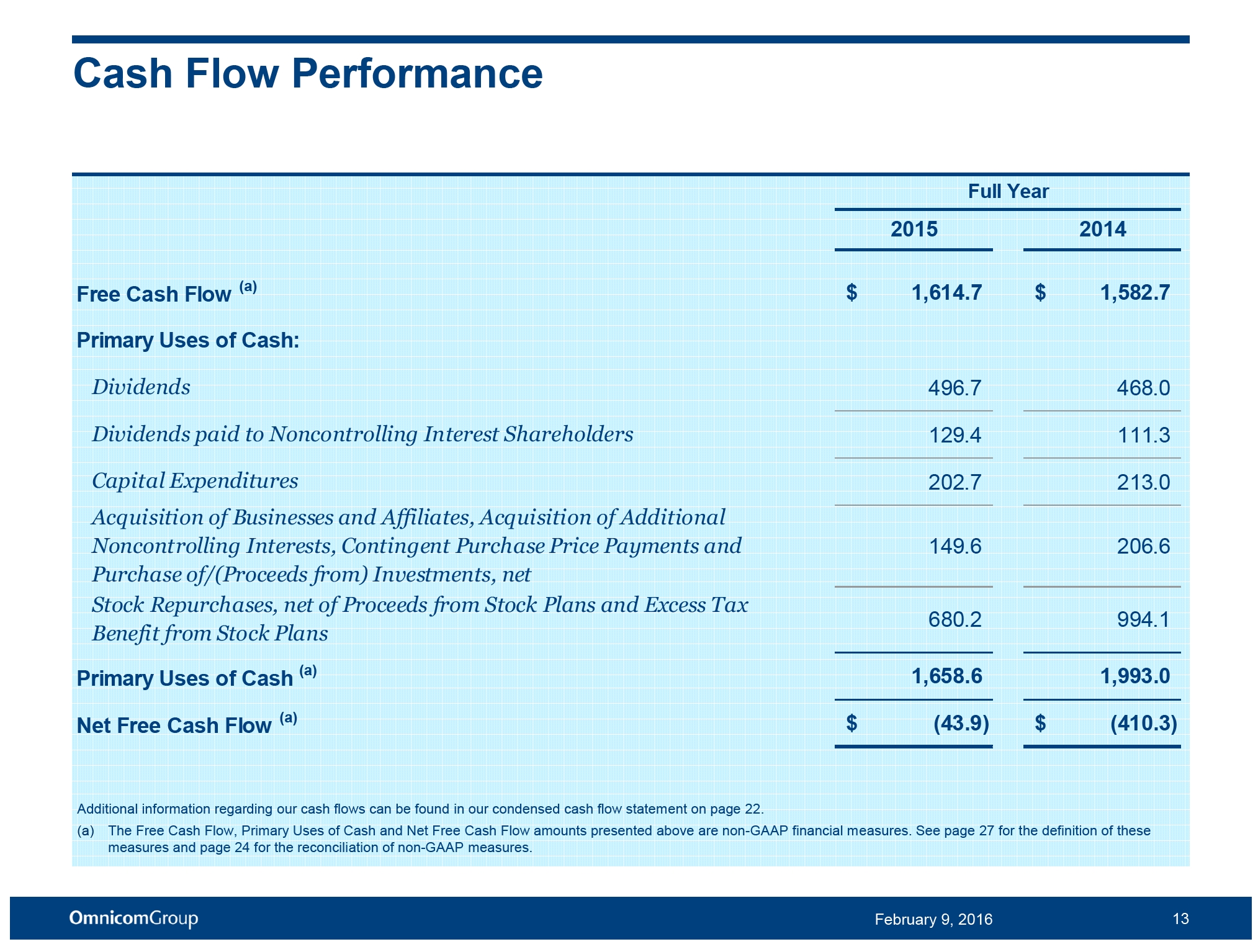

Cash Flow Performance

Full Year 2015 2014

Net Income $ 1,203.4 $ 1,233.1

Depreciation and Amortization Expense 291.1 294.4

Share-Based Compensation Expense 99.4 93.5

Other Items to Reconcile to Net Cash Provided by Operating Activities,

20.8 (38.3) net

Free Cash Flow (a) $ 1,614.7 $ 1,582.7

Additional information regarding our cash flows can be found in our condensed cash flow statement on page 22.

(a) The Free Cash Flow amounts presented above are non-GAAP financial measures. See page 28 for the definition of these measures and page 25 for the reconciliation of the non-GAAP measures.

February 9, 2016 12

Cash Flow Performance

Full Year 2015 2014

Free Cash Flow (a) $ 1,614.7 $ 1,582.7 Primary Uses of Cash:

Dividends 496.7 468.0

Dividends paid to Noncontrolling Interest Shareholders 129.4 111.3 Capital Expenditures 202.7 213.0 Acquisition of Businesses and Affiliates, Acquisition of Additional Noncontrolling Interests, Contingent Purchase Price Payments and 149.6 206.6 Purchase of/(Proceeds from) Investments, net Stock Repurchases, net of Proceeds from Stock Plans and Excess Tax

680.2 994.1

Benefit from Stock Plans

Primary Uses of Cash (a) 1,658.6 1,993.0 Net Free Cash Flow (a) $ (43.9) $ (410.3)

Additional information regarding our cash flows can be found in our condensed cash flow statement on page 22.

(a) The Free Cash Flow, Primary Uses of Cash and Net Free Cash Flow amounts presented above are non-GAAP financial measures. See page 28 for the definition of these measures and page 25 for the reconciliation of non-GAAP measures.

February 9, 2016 13

Current Credit Picture

Full Year 2015 2014

EBITDA (a) $ 2,211.2 $ 2,238.5

Gross Interest Expense 181.1 177.2 EBITDA / Gross Interest Expense 12.2 x 12.6 x Total Debt / EBITDA 2.1 x 2.0 x Net Debt (b) / EBITDA 0.9 x 1.0 x

Debt

Bank Loans (Due Less Than 1 Year) $ 6 $ 8 CP & Borrowings Issued Under Revolver - -Convertible Notes - -Senior Notes (c) 4,500 4,500 Adjustment to carrying value of Debt for Interest Rate Swaps and

65 42

Other Debt

Total Debt $ 4,571 $ 4,550

Cash and Short Term Investments 2,620 2,390

Net Debt (b) $ 1,951 $ 2,160

(a) EBITDA is a non-GAAP financial measure. See page 28 for the definition of this measure and page 23 for the reconciliation of non-GAAP measures. (b) Net Debt is a non-GAAP financial measure. See page 28 for the definition of this measure.

(c) See pages 18 and 19 for additional information on our Senior Notes.

February 9, 2016 14

Historical Returns

Return on Invested Capital (ROIC) (a) :

Twelve Months Ended December 31, 2015 21.5% Twelve Months Ended December 31, 2014 20.7%

Return on Equity (b):

Twelve Months Ended December 31, 2015 41.3% Twelve Months Ended December 31, 2014 34.3%

(a) Return on Invested Capital is After Tax Reported Operating Income (a non-GAAP measure – see page 28 for the definition of this measure and page 25 for the reconciliation of non-GAAP measures) divided by the average of Invested Capital at the beginning and the end of the period (book value of all long-term liabilities and short-term interest bearing debt plus shareholders’ equity less cash, cash equivalents and short term investments). On December 31, 2015 we retrospectively adopted ASU 2015-03 and ASU

2015-17. The ROIC ratio presented for 2014 has been calculated as if we had adopted the two ASUs for the periods impacting the calculation.

(b) Return on Equity is Reported Net Income for the given period divided by the average of shareholders’ equity at the beginning and end of the period.

February 9, 2016 15

Net Cash Returned to Shareholders through Dividends and Share Repurchases

Over the period 2004 through 2015, Omnicom distributed over 100% of Net Income to shareholders through Dividends and Share Repurchases.

108% 108% $11.1 $12.0

104% $10.0

107% $10.0 $8.9

Billions

103% $7.9 103% $8.0

92% $6.9 8.7

In 105% $5.9 8.0 $ $6.0 $5.1

108% 7.0 110% $4.3 6.5 $3.3 5.6 $4.0 92% 4.8

76% $2.4

3.7 3.6 $1.5 2.9 $2.0 $0.7 2.1 3.3 2.3 2.8 1.6 2.0 0.9 1.1 1.3 0.5 0.7 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Cumulative Cost of Net Shares Repurchased - Payments for repurchases of common stock less proceeds from stock plans.

Cumulative Dividends Paid

Cumulative Net Income - Omnicom Group Inc.

% of Cumulative Net Income Returned to Shareholders - Cumulative Dividends Paid plus Cumulative Cost of Net Shares Repurchased divided by Cumulative Net Income.

February 9, 2016 16

Supplemental Financial Information

February 9, 2016 17

Omnicom Debt Structure

Bank Loans $6

2024 Senior Notes $750 2016 Senior Notes $1,000

2019 Senior Notes

2022 Senior Notes $500 $1,250

2020 Senior Notes $1,000

The above chart sets forth Omnicom’s debt outstanding at December 31, 2015. The amounts reflected above for the 2016, 2019, 2020, 2022 and 2024 Senior Notes represent the principal amount of these notes at maturity on April 15, 2016, July 15, 2019, August 15, 2020, May 1, 2022 and November 1, 2024, respectively.

February 9, 2016 18

Omnicom Debt Maturity Profile

2022 Senior Notes

$1,250

2016 2020 Senior Senior Notes Notes

$1,000

2024 Senior Notes

$750

2019 Senior Notes

$500

$250

Other Borrowings

$0

Other borrowings at December 31, 2015 include short-term borrowings of $6 million which are due in less than one year. For purposes of this presentation we have included these borrowings as outstanding through July 31, 2020, the date of expiration of our five-year credit facility.

February 9, 2016 19

Historical Return Trends

Return on Equity Average through December 31, 2015 – 26.1% ROE(a) Return on Invested Capital Average through December 31, 2015 – 20.7%

45.0% ROIC(b)

40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0%

0.0%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

(a) Return on Equity (“ROE”) is Reported Net Income for the given period divided by the average shareholders’ equity at the beginning and end of the period.

(b) Return on Invested Capital (“ROIC”) is After Tax Reported Operating Income (a non-GAAP measure – see page 28 for the definition of this measure and page 25 for the reconciliation of non-GAAP measure for FY 2015) divided by the average of Invested Capital at the beginning and end of the period (book value of all long-term liabilities and short-term interest bearing debt plus shareholders’ equity less cash, cash equivalents and short term investments). On December 31, 2015 we retrospectively adopted ASU 2015-03 and ASU 2015-17. The ROIC ratio presented for 2014, 2013 , 2012 and 2011 have been calculated as if we had adopted the two ASUs for the periods impacting the calculation.

February 9, 2016 20

2015 Acquisition Related Expenditures

Full Year

Acquisition of Businesses and Affiliates (a) $ 60.3 Acquisition of Additional Noncontrolling Interests (b) 33.5 Contingent Purchase Price Payments (c) 58.6

Total Acquisition Expenditures (d) $ 152.4

(a) Includes acquisitions of a majority interest in agencies resulting in their consolidation, including additional interest in existing affiliate agencies resulting in majority ownership. (b) Includes the acquisition of additional equity interests in already consolidated subsidiary agencies which are recorded to Equity – Noncontrolling Interest.

(c) Includes additional consideration paid for acquisitions completed in prior periods. (d) Total Acquisition Expenditures is net of cash acquired.

February 9, 2016 21

Condensed Cash Flow

Full Year 2015 2014 Net Income $ 1,203.4 $ 1,233.1

Share-Based Compensation Expense 99.4 93.5 Depreciation and Amortization 291.1 294.4 Other Items to Reconcile to Net Cash Provided by Operating Activities, net 20.8 (38.3) Changes in Operating Capital 557.6 (106.2)

Net Cash Provided by Operating Activities 2,172.3 1,476.5

Capital Expenditures (202.7) (213.0) Acquisition of Businesses and Affiliates and Proceeds from Sales of Investments, net (60.8) (53.9)

Net Cash Used in Investing Activities (263.5) (266.9)

Dividends (496.7) (468.0)

Dividends paid to Noncontrolling Interest Shareholders (129.4) (111.3) Repayment of Convertible Debt - (252.7) (Repayments of)/Proceeds from Short-term & Long-term Debt, net (1.1) 749.7 Stock Repurchases, net of Proceeds from Stock Plans and Excess Tax Benefit from Stock Plans (680.2) (994.1) Acquisition of Additional Noncontrolling Interests (33.5) (69.5) Contingent Purchase Price Payments (55.3) (83.2) Other Financing Activities, net (32.9) (29.0)

Net Cash Used in Financing Activities (1,429.1) (1,258.1) Effect of exchange rate changes on cash and cash equivalents (262.6) (273.9) Net Increase/(Decrease) in Cash and Cash Equivalents $ 217.1 $ (322.4)

February 9, 2016 22

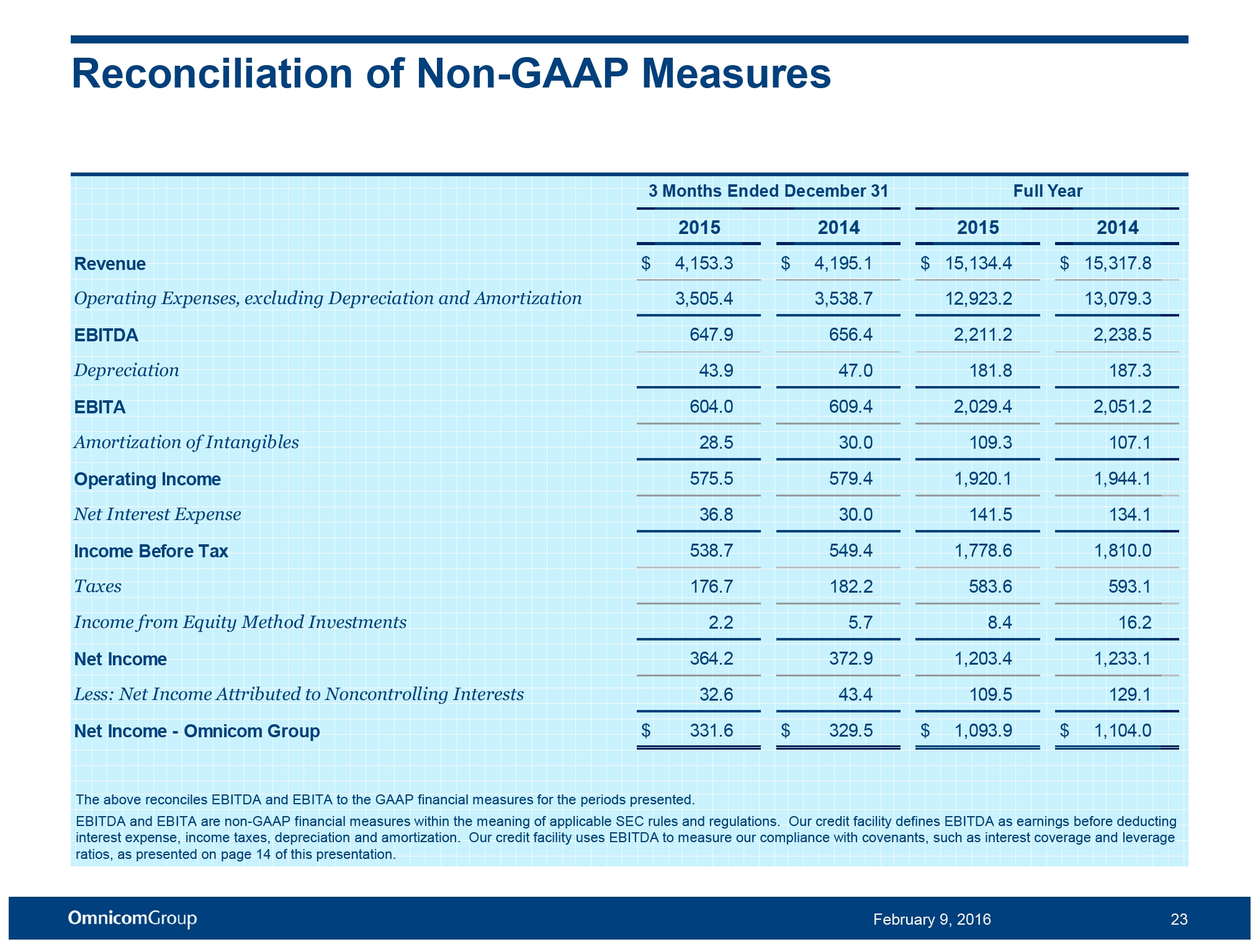

Reconciliation of Non-GAAP Measures

3 Months Ended December 31 Full Year

2015 2014 2015 2014 Revenue $ 4,153.3 $ 4,195.1 $ 15,134.4 $ 15,317.8

Operating Expenses, excluding Depreciation and Amortization 3,505.4 3,538.7 12,923.2 13,079.3

EBITDA 647.9 656.4 2,211.2 2,238.5 Depreciation 43.9 47.0 181.8 187.3 EBITA 604.0 609.4 2,029.4 2,051.2

Amortization of Intangibles 28.5 30.0 109.3 107.1

Operating Income 575.5 579.4 1,920.1 1,944.1

Net Interest Expense 36.8 30.0 141.5 134.1

Income Before Tax 538.7 549.4 1,778.6 1,810.0 Taxes 176.7 182.2 583.6 593.1

Income from Equity Method Investments 2.2 5.7 8.4 16.2

Net Income 364.2 372.9 1,203.4 1,233.1

Less: Net Income Attributed to Noncontrolling Interests 32.6 43.4 109.5 129.1

Net Income - Omnicom Group $ 331.6 $ 329.5 $ 1,093.9 $ 1,104.0

The above reconciles EBITDA and EBITA to the GAAP financial measures for the periods presented.

EBITDA and EBITA are non-GAAP financial measures within the meaning of applicable SEC rules and regulations. Our credit facility defines EBITDA as earnings before deducting interest expense, income taxes, depreciation and amortization. Our credit facility uses EBITDA to measure our compliance with covenants, such as interest coverage and leverage ratios, as presented on page 14 of this presentation.

February 9, 2016 23

Reconciliation of Non-GAAP Measures

Full Year

Merger-related 2014 Exclude 2014 Reported Tax Benefit Tax Benefit

EBITA $ 2,051.2 $ - $ 2,051.2

Operating Income 1,944.1 - 1,944.1 Income Tax Expense 593.1 11.2 604.3 Net Income - Omnicom Group Inc. 1,104.0 11.2 1,092.8 Net Income allocated to participating securities 20.4 0.2 20.2 Net Income available for common shares 1,083.6 11.0 1,072.6

EPS - Diluted $ 4.24 $ 0.04 $ 4.20

The above table reconciles our reported 2014 results to the "2014 Exclude Tax Benefit" amounts, which are non-GAAP financial measures. These measures exclude the recognition of an income tax benefit of $11.2 million related to expenses incurred in prior periods in connection with the proposed merger with Publicis which was terminated on May 8, 2014. Prior to the termination of the merger, the majority of the merger costs, which were incurred in 2013, were capitalized for income tax purposes and the related tax benefits were not recorded. Because the merger was terminated, the merger costs were no longer required to be capitalized for income tax purposes. We believe that investors should consider the “2014 Exclude Tax Benefit” measures as they are indicative of our ongoing performance and reflect how management evaluates our operational results. Non-GAAP financial measures should not be considered in isolation from or as a substitute for financial information presented in compliance with U.S. GAAP. Non-GAAP financial measures reported by us may not be comparable to similarly titled amounts reported by other companies.

February 9, 2016 24

Reconciliation of Non-GAAP Measures

Full Year 2015 2014 Net Free Cash Flow $ (43.9) $ (410.3) Cash Flow items excluded from Net Free Cash Flow:

Changes in Operating Capital 557.6 (106.2) Repayment of Convertible Debt - (252.7) (Repayments of)/Proceeds from Short-term & Long-term Debt, net (1.1) 749.7 Other Financing Activities, net (32.9) (29.0) Effect of exchange rate changes on cash and cash equivalents (262.6) (273.9)

Net Increase/(Decrease) in Cash and Cash Equivalents $ 217.1 $ (322.4)

Full Year 2015 2014 Reported Operating Income $ 1,920.1 $ 1,944.1

Effective Tax Rate for the applicable period 32.8% 32.8% Income Taxes on Reported Operating Income 629.8 637.7

After Tax Reported Operating Income $ 1,290.3 $ 1,306.4

February 9, 2016 25

Supplemental Information

Fourth Quarter Full Year

2015 % of 2014 % of 2015 % of 2014 % of

Rev Rev Rev Rev

Revenue $ 4,153.3 $ 4,195.1 $ 15,134.4 $ 15,317.8

Operating expenses:

Salary and service costs $ 3,118.8 75.1% $ 3,119.2 74.4% $ 11,361.9 75.1% $ 11,350.0 74.1%

Office and general expenses:

Amortization of Intangibles 28.5 30.0 109.3 107.1

Depreciation 43.9 47.0 181.8 187.3

Other office and general expenses 386.6 419.5 1,561.3 1,729.3

Total office and general expenses 459.0 11.1% 496.5 11.8% 1,852.4 12.2% 2,023.7 13.2%

Total operating expenses $ 3,577.8 86.1% $ 3,615.7 86.2% $ 13,214.3 87.3% $ 13,373.7 87.3%

Net Interest expense:

Interest expense $ 47.2 $ 41.8 $ 181.1 $ 177.2 Interest income 10.4 11.8 39.6 43.1 Net Interest expense $ 36.8 $ 30.0 $ 141.5 $ 134.1

February 9, 2016 26

Fourth Quarter Acquisition

Established in 2003, Wednesday Agency Group is a leading integrated creative agency for the fashion, luxury and consumer lifestyles industry.

The agency’s main areas of focus include fully integrated campaigns, content strategy, digital design & branding and production.

With offices in New York and London, Wednesday will operate within the BBDO Worldwide network.

February 9, 2016 27

Disclosure

The preceding materials have been prepared for use in the February 9, 2016 conference call on Omnicom’s results of operations for the period ended December 31, 2015. The call will be archived on the Internet at http://investor.omnicomgroup.com/investor-relations/news-events-and-filings.

Forward-Looking Statements

Certain statements in this presentation constitute forward-looking statements, including statements within the meaning of the Private Securities Litigation Reform Act of 1995. In addition, from time to time, the Company or its representatives have made, or may make, forward-looking statements, orally or in writing. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management as well as assumptions made by, and information currently available to, the Company’s management. Forward-looking statements may be accompanied by words such as “aim,” “anticipate,” “believe,” “plan,” “could,” “should,” “would,” “estimate,” “expect,” “forecast,” “future,” “guidance,” “intend,” “may,” “will,” “possible,” “potential,” “predict,” “project” or similar words, phrases or expressions. These forward-looking statements are subject to various risks and uncertainties, many of which are outside the Company’s control. Therefore, you should not place undue reliance on such statements. Factors that could cause actual results to differ materially from those in the forward-looking statements include: international, national or local economic conditions that could adversely affect the Company or its clients; losses on media purchases and production costs incurred on behalf of clients; reductions in client spending, a slowdown in client payments and a deterioration in the credit markets; ability to attract new clients and retain existing clients in the manner anticipated; changes in client advertising, marketing and corporate communications requirements; failure to manage potential conflicts of interest between or among clients; unanticipated changes relating to competitive factors in the advertising, marketing and corporate communications industries; ability to hire and retain key personnel; currency exchange rate fluctuations; reliance on information technology systems; changes in legislation or governmental regulations affecting the Company or its clients; risks associated with assumptions the Company makes in connection with its critical accounting estimates and legal proceedings; and the Company’s international operations, which are subject to the risks of currency repatriation restrictions, social or political conditions and regulatory environment. The foregoing list of factors is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties that may affect the Company’s business, including those described in the “Risk Factors” in Omnicom’s Annual Report on Form 10-K for the year ended December 31, 2014. Except as required under applicable law, the Company does not assume any obligation to update these forward-looking statements.

Non-GAAP Financial Measures

We present financial measures determined in accordance with generally accepted accounting principles in the United States (“GAAP”) and adjustments to the GAAP presentation (“Non-GAAP”), which we believe are meaningful for understanding our performance. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP. Non-GAAP financial measures as reported by us may not be comparable to similarly titled amounts reported by other companies. We provide a reconciliation of non-GAAP measures to the comparable GAAP measures on pages 23, 24 and 25.

The Non-GAAP measures used in this presentation include the following:

2014 Exclude Tax Benefit, which excludes the impact of the tax benefit related to expenses incurred in 2013 related to the proposed merger with Publicis which was terminated in 2014. We believe that this presentation allows for a more meaningful understanding of our performance.

Net Free Cash Flow, defined as Free Cash Flow (defined below) less the Primary Uses of Cash (defined below). Net Free Cash Flow is one of the metrics used by us to assess our sources and uses of cash and was derived from our consolidated statements of cash flows. We believe that this presentation is meaningful for understanding our primary sources and primary uses of that cash flow. Free Cash Flow, defined as net income plus depreciation, amortization, share based compensation expense plus/(less) other non-cash items to reconcile to net cash provided by operating activities. Primary Uses of Cash, defined as dividends to common shareholders, dividends paid to non-controlling interest shareholders, capital expenditures, cash paid on acquisitions, payments for additional interest in controlled subsidiaries and stock repurchases, net of the proceeds and excess tax benefit from our stock plans, and excludes changes in operating capital and other investing and financing activities, including commercial paper issuances and redemptions used to fund working capital changes.

EBITDA, defined as operating income before interest, taxes, depreciation and amortization. We believe EBITDA is meaningful because the financial covenants in our credit facilities are based on EBITDA.

EBITA, defined as operating income before interest, taxes and amortization. We use EBITA as an additional operating performance measure, which excludes non-cash acquisition-related amortization expense, because we believe that EBITA is a useful measure to evaluate the performance of our businesses.

Net Debt, defined as total debt less cash, cash equivalents and short-term investments. We believe net debt, together with the comparable GAAP measures, reflects one of the metrics used by us to assess our cash management.

After Tax Reported Operating Income, defined as reported operating income less income taxes calculated using the effective tax rate for the applicable period.

Other Information

All dollar amounts are in millions except for per share amounts and figures shown on pages 3, 6 and 24 and the net cash returned to shareholders figures on page 16. The information contained in this document has not been audited, although some data has been derived from Omnicom’s historical financial statements, including its audited financial statements. In addition, industry, operational and other non-financial data contained in this document have been derived from sources that we believe to be reliable, but we have not independently verified such information, and we do not, nor does any other person, assume responsibility for the accuracy or completeness of that information. Certain amounts in prior periods have been reclassified to conform to our current presentation.

The inclusion of information in this presentation does not mean that such information is material or that disclosure of such information is required.

February 9, 2016 28

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Wells Fargo Upgrades Omnicom Group (OMC) to Overweight

- Robbins LLP Reminds IRobot Corporation Shareholders of the Pending May 7, 2024 Lead Plaintiff Deadline

- ROSEN, A LEADING NATIONAL FIRM, Encourages Sharecare, Inc. Investors to Secure Counsel Before Important Deadline in Securities Class Action First Filed by the Firm – SHCR

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!