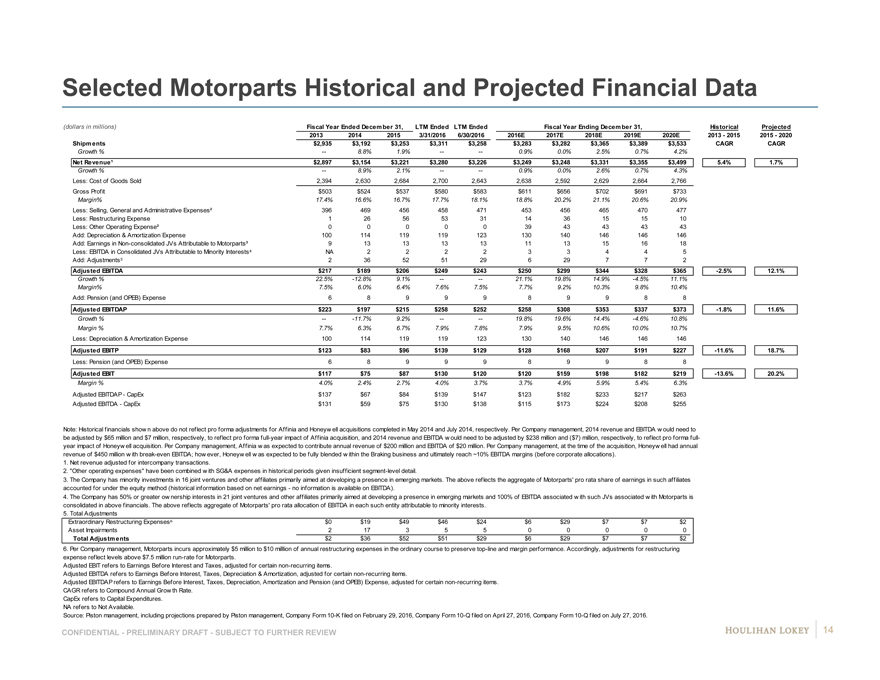

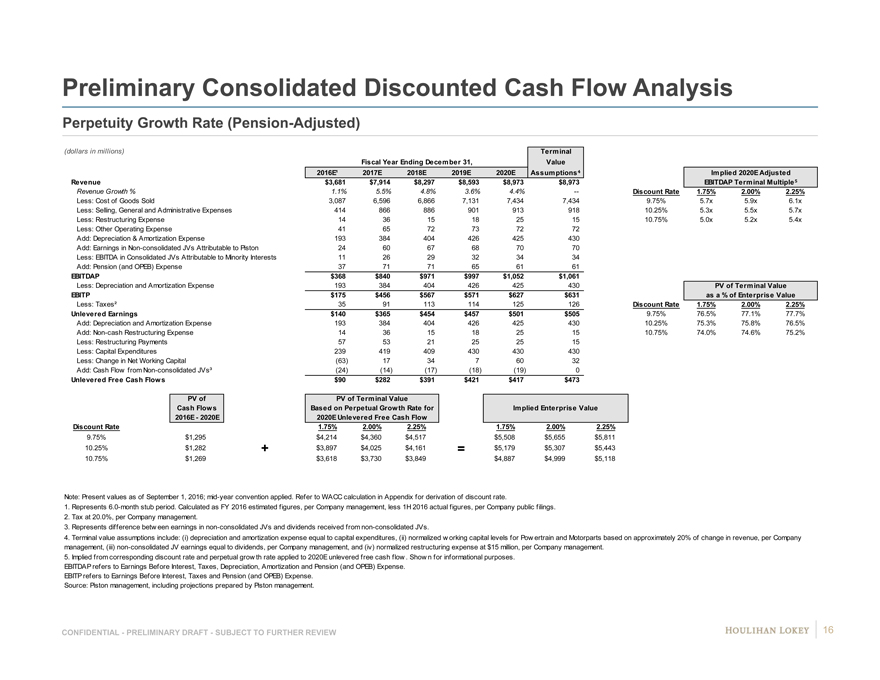

Form SC 13E3 Federal-Mogul Holdings Filed by: ICAHN CARL C

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 13E-3

(§240.13(e)-100)

Rule 13e-3 Transaction Statement under Section 13(e)

of the Securities Exchange Act of 1934

FEDERAL-MOGUL HOLDINGS CORPORATION

(Name of the Issuer)

IEH FM HOLDINGS LLC

AMERICAN ENTERTAINMENT PROPERTIES CORP.

ICAHN BUILDING LLC

ICAHN ENTERPRISES HOLDINGS L.P.

ICAHN ENTERPRISES G.P. INC.

BECKTON CORP.

CARL C. ICAHN

FEDERAL-MOGUL HOLDINGS CORPORATION

(Name of Person Filing Statement)

Common Stock, par value $0.01 per share

(Title of Class of Securities)

313549404

(CUSIP Number of Class of Securities)

| Michelle Epstein Taigman Senior Vice President, General Counsel and Secretary Federal-Mogul Holdings Corporation 27300 West 11 Mile Road Southfield, Michigan 48034 (248) 354-7063 |

Keith Cozza President and Chief Executive Officer Icahn Enterprises L.P. 767 Fifth Avenue, 47th Floor New York, New York 10153 (212) 702-4300 |

(Name, address and telephone number of person authorized to receive notices and communications on behalf of the persons filing statement)

With copies to:

| Bruce A. Toth Winston & Strawn LLP 35 West Wacker Drive Chicago, Illinois 60601 |

Jesse Lynn, Esq. General Counsel Icahn Enterprises L.P. 767 Fifth Avenue, 47th Floor New York, NY 10153 (212) 702-4300 |

Julie Allen, Esq. Proskauer Rose LLP 11 Times Square New York, NY 10036 (212) 969-3155 |

This statement is filed in connection with (check the appropriate box):

| a. |

¨ | The filing of solicitation materials or an information statement subject to Regulation 14A, Regulation 14C or Rule 13e-3(c) under the Securities Exchange Act of 1934. | ||

| b. |

¨ | The filing of a registration statement under the Securities Act of 1933. | ||

| c. |

x | A tender offer. | ||

| d. |

¨ | None of the above. | ||

Check the following box if the soliciting materials or information statement referred to in checking box (a) are preliminary copies: ¨

Check the following box if the filing is a final amendment reporting the results of the transaction: ¨

Calculation of Filing Fee

| Transaction valuation* | Amount of filing fee** | |

|

$281,667,218 |

$28,363.89 |

| * | The transaction valuation is estimated solely for purposes of calculating the filing fee. The calculation assumes the purchase of all outstanding shares of common stock, par value $0.01 per share (the “Shares”) of Federal-Mogul Holdings Corporation (the “Company”) not beneficially owned by IEH FM Holdings LLC, a Delaware limited liability company (the “Offeror”), at a purchase price of $9.25 per Share, net to the seller in cash. According to the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2016, filed with the SEC on July 27, 2016, 169,040,651 Shares were outstanding as of July 25, 2016, of which 138,590,141 are held by the Offeror. Accordingly, this calculation assumes the purchase of 30,450,510 Shares. |

| ** | The amount of the filing fee is calculated in accordance with Rule 0-11 of the Securities Exchange Act of 1934, as amended, and Fee Rate Advisory # 1 for Fiscal Year 2016 issued by the Securities and Exchange Commission, by multiplying the transaction valuation by 0.0001007. |

| x | Check the box if any part of the fee is offset as provided by Rule 0-11(a)(2) and identify the filing with which the offsetting fee was previously paid. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| Amount Previously Paid: | $28,363.89 | |

| Form or Registration No.: | Schedule TO (File No. 005-83475) | |

| Filing Party: | IEH FM Holdings LLC, American Entertainment Properties Corp., Icahn Buildings LLC, Icahn Enterprises Holdings L.P., Icahn Enterprises G.P. Inc., Beckton Corp. and Carl C. Icahn | |

| Date Filed: | September 26, 2016 | |

Neither the Securities and Exchange Commission nor any state securities commission has: approved or disapproved of the transaction contemplated herein; passed upon the merits or fairness of such transaction; or passed upon the adequacy or accuracy of the disclosure in this document. Any representation to the contrary is a criminal offense.

INTRODUCTION

This Transaction Statement on Schedule 13E-3 (this “Schedule 13E-3”) filed by IEH FM Holdings LLC, a Delaware limited liability company (the “Offeror”) and an indirect wholly owned subsidiary of American Entertainment Properties Corp., a Delaware corporation (“Parent”), Parent, Icahn Building LLC, a Delaware limited liability company, Icahn Enterprises Holdings L.P., a Delaware limited partnership, Icahn Enterprises G.P. Inc., a Delaware corporation, Beckton Corp., a Delaware corporation, Carl Icahn, an individual, and Federal-Mogul Holdings Corporation, a Delaware corporation (the “Company”) relates to the offer by Offeror to purchase all outstanding shares of common stock, par value $0.01 per share (the “Shares”), of the Company that are not already owned by the Offeror at $9.25 per Share, net to the seller in cash, without interest and less any required withholding taxes, and on the other terms and subject to the other conditions specified in the Offer to Purchase, dated September 26, 2016 (the “Offer to Purchase”), and in the related Letter of Transmittal, each as originally filed with the Tender Offer Statement by Purchaser with the Securities and Exchange Commission (the “SEC”) on September 26, 2016 (the “Schedule TO”). Unless otherwise defined herein, capitalized terms used in this Schedule 13E-3 shall have the meaning given to them in the Offer to Purchase.

In response to the Offer, on the date hereof, the Company is filing a Solicitation/Recommendation Statement on Schedule 14D-9 (the “Schedule 14D-9”). The information contained in the Schedule 14D-9 and the Offer to Purchase, including all schedules, annexes and exhibits thereto, copies of which are attached as exhibits hereto, is expressly incorporated by reference to the extent such information is required in response to the items of this Schedule 13E-3, and is supplemented by the information specifically provided herein.

The responses to each item in this Schedule 13E-3 are qualified in their entirety by the information contained in the Schedule 14D-9 and the Offer to Purchase. All information contained in this Schedule 13E-3 concerning the Company, Offeror and Parent has been provided by such person and not by any other person.

The cross references below are being supplied pursuant to General Instruction G to Schedule 13E-3 and show the location in the Schedule TO and Schedule 14D-9 of the information required to be included in response to the items of Schedule 13E-3. The information contained in the Schedule TO and Schedule 14D-9, including all annexes thereto, is incorporated by reference herein, and the responses to each Item in this Schedule 13E-3 are qualified in their entirety by the information contained in the Schedule TO and Schedule 14D-9 and the annexes thereto.

| Item 1. | Summary Term Sheet |

Item 1001 of Regulation M-A

The information set forth in the Offer to Purchase under “Summary Term Sheet” is incorporated herein by reference.

| Item 2. | Subject Company Information |

Item 1002 of Regulation M-A

(a) Name and Address. The information set forth in the Schedule 14D-9 under “Item 1. Subject Company Information—Name and Address” and the information set forth in the Offer to Purchase under the “The Offer—Section 8—Certain Information Concerning the Company” is incorporated herein by reference.

(b) Securities. The information set forth in the Schedule 14D-9 under “Item 1. Subject Company Information—Securities” and the information set forth in the Offer to Purchase under “Introduction” is incorporated herein by reference.

(c) Trading Marking and Price. The information set forth in the Offer to Purchase under “Summary Term Sheet” and “The Offer—Section 6—Price Range of Shares; Dividends” is incorporated herein by reference.

(d) Dividends. The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors— Section 7—Summary of the Merger Agreement”, “The Offer—Section 6—Price Range of Shares; Dividends” and “The Offer—Section 11—Dividends and Distributions” is incorporated herein by reference.

(e) Prior Public Offerings. Not applicable.

(f) Prior Stock Purchases. The information set forth in the Offer to Purchase under “Special Factors—Section 9—Transactions and Arrangements Concerning the Shares” and “The Offer—Section 9—Certain Information Concerning the Offeror and Parent” is incorporated herein by reference.

| Item 3. | Identity and Background of the Filing Person |

Item 1003(a)-(c) of Regulation M-A

(a) Name and Address. The information set forth in the Schedule 14D-9 under “Item 1. Subject Company Information” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “The Offer—Section 8—Certain Information Concerning the Company”, The Offer—Section 9—Certain Information Concerning the Offeror and Parent” and “Schedule A—Executive Officer(s) and Director(s) of IEH FM Holdings LLC, American Entertainment Properties Corp., Icahn Building LLC, Icahn Enterprises Holdings L.P., Icahn Enterprises L.P., Icahn Enterprises G.P. Inc. and Beckton Corp.” is incorporated herein by reference.

(b) Business and Background of Entities. The information set forth in the Schedule 14D-9 under “Item 1. Subject Company Information” and “The Offer—Section 8—Certain Information Concerning the Company” and the information set forth in the Offer to Purchase under “The Offer—Section 9—Certain Information Concerning the Offeror and Parent” is incorporated herein by reference.

(c) Business and Background of Natural Persons. The information set forth in the Offer to Purchase under “The Offer—Section 9—Certain Information Concerning the Offeror and Parent” and “Schedule A—Executive Officer(s) and Director(s) of IEH FM Holdings LLC, American Entertainment Properties Corp., Icahn Building LLC, Icahn Enterprises Holdings L.P., Icahn Enterprises L.P., Icahn Enterprises G.P. Inc. and Beckton Corp.” is incorporated herein by reference.

| Item 4. | Terms of the Transaction |

Item 1004(a), (c)-(f) of Regulation M-A

(a) Material Terms; Tender Offers

(a)(1)(i) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction” and “Special Factors—Section 7—Summary of the Merger Agreement” is incorporated herein by reference.

(a)(1)(ii) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction” and “The Offer—Section 10—Source and Amounts of Funds” is incorporated herein by reference.

(a)(1)(iii) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction” and “The Offer—Section 1—Terms of the Offer” is incorporated herein by reference.

(a)(1)(iv) The information set forth in the Offer to Purchase under “Summary Term Sheet” is incorporated herein by reference.

(a)(1)(v) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “The Offer—Section 1—Terms of the Offer” and “Special Factors—Section 7—Summary of the Merger Agreement” is incorporated herein by reference.

(a)(1)(vi) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction” and “The Offer—Section 4—Withdrawal Rights” is incorporated herein by reference.

(a)(1)(vii) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “The Offer—Section 3—Procedure for Tendering Shares” and “The Offer—Section 4—Withdrawal Rights” are incorporated herein by reference.

(a)(1)(viii) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “The Offer—Section 1—Terms of the Offer”, “The Offer—Section 2—Acceptance for Payment and Payment for Shares” and “The Offer—Section 12—Conditions of the Offer” is incorporated herein by reference.

(a)(1)(ix) Not applicable.

(a)(1)(x) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 5—Effects of the Offer and the Merger”, “Special Factors—Section 11—Interests of Certain Persons in the Offer” and “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” is incorporated herein by reference.

(a)(1)(xi) Not applicable.

(a)(1)(xii) The information set forth in the Offer to Purchase under “Summary Term Sheet” and “The Offer—Section 5—Certain U.S. Federal Income Tax Considerations” is incorporated herein by reference.

(a)(2)(i) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction” and “Special Factors—Section 7—Summary of the Merger Agreement” is incorporated herein by reference.

(a)(2)(ii) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 7—Summary of the Merger Agreement” and “The Offer—Section 2—Acceptance for Payment and Payment of Shares” is incorporated herein by reference.

(a)(2)(iii) The information set forth in the Offer to Purchase under “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company” and in the Schedule 14D-9 under “Item 4—The Solicitation or Recommendation—Reasons for the Special Committee’s Recommendation” and “Item 4—The Solicitation or Recommendation—Reasons for the Board’s Recommendation” is incorporated herein by reference.

(a)(2)(iv) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 1—Background”, “Special Factors—Section 3—The Recommendation by the Special Committee and the Company Board of Directors”, “Special Factors—Section 5—Effects of the Offer and the Merger” and “Special Factors—Section 7—Summary of the Merger Agreement” is incorporated herein by reference.

(a)(2)(v) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 5—Effects of the Offer and the Merger”, “Special Factors—Section 8—Dissenters’ Appraisal Rights; Rule 13e-3”, “Special Factors—Section 11—Interests of Certain Persons in the Offer” and “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” is incorporated herein by reference.

(a)(2)(vi) Not applicable.

(a)(2)(vii) The information set forth in the Offer to Purchase under “Summary Term Sheet” and “The Offer—Section 5—Certain U.S. Federal Income Tax Considerations” is incorporated herein by reference.

(c) Different Terms. The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction”, “Special Factors— Section 5—Effects of the Offer and the Merger”, “Special Factors—Section 8—Dissenters’ Appraisal Rights; Rule 13e-3”, “The Offer—Section 13—Certain Legal Matters; Regulatory Approvals” and “Schedule C—General Corporation Law of Delaware Section 262 Appraisal Rights” and the Schedule 14D-9 under “Item 3. Past Contacts, Transactions, Negotiations and Agreements—Arrangements with Current Executive Officers and Directors of the Company” is incorporated herein by reference.

(d) Appraisal Rights. The information set forth in the Schedule 14D-9 under the captions “Item 8 – Additional Information – Notice of Appraisal Rights” and “Annex B – Delaware Appraisal Statute (DGCL Section 262) and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors—Section 8—Dissenters’ Appraisal Rights; Rule 13e-3”, “The Offer—Section 13—Certain Legal Matters; Regulatory Approvals” and “Schedule C—General Corporation Law of Delaware Section 262 Appraisal Rights” is incorporated herein by reference.

(e) Provisions for Unaffiliated Security Holders. The information set forth in the Offer to Purchase under “Special Factors—Section 8—Dissenters’ Appraisal Rights; Rule 13e-3” and “The Offer—Section 9—Certain Information Concerning the Offeror and Parent” is incorporated herein by reference.

(f) Eligibility for Listing or Trading. Not applicable.

| Item 5. | Past Contacts, Transactions, Negotiations and Agreements |

Item 1005(a)-(c) and (e) of Regulation M-A

(a) Transactions. The information set forth in the Schedule 14D-9 under “Item 3. Past Contacts, Transactions, Negotiations and Agreements” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background”, “Special Factors—Section 9—Transactions and Arrangements Concerning the Shares”, “Special Factors—Section 10—Related Party Transactions” and “Special Factors—Section 11—Interests of Certain Persons in the Offer” is incorporated herein by reference.

(b) Significant Corporate Events. The information set forth in the Schedule 14D-9 under “Item 3. Past Contacts, Transactions, Negotiations and Agreements” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background”, “Special Factors—Section 7—Summary of the Merger Agreement”, “Special Factors—Section 9—Transactions and Arrangements Concerning the Shares” and “Special Factors—Section 10—Related Party Transactions” is incorporated herein by reference.

(c) Negotiations or Contracts. The information set forth in the Schedule 14D-9 under “Item 3. Past Contacts, Transactions, Negotiations and Agreements” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background” and “Special Factors—Section 10—Related Party Transactions” is incorporated herein by reference.

(e) Agreements Involving the Subject Company’s Securities. The information set forth in the Schedule 14D-9 under “Item 3. Past Contacts, Transactions, Negotiations and Agreements” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background” and “Special Factors—Section 10—Related Party Transactions” is incorporated herein by reference.

| Item 6. | Purposes of the Transaction and Plans or Proposals |

Item 1006(b) and (c)(1)-(8)

(b) Use of Securities Acquired. The information set forth in the Schedule 14D-9 under “Item 2. Identity and Background of Filing Person – Offer” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 5—Effects of the Offer and the Merger” and “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” is incorporated herein by reference.

(c) Plans.

(c)(1) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 1—Background”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company” and “Special Factors—Section 7—Summary of the Merger Agreement” is incorporated herein by reference.

(c)(2) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction” and “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company” is incorporated herein by reference.

(c)(3) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction”, “Special Factors—Section 7—Summary of the Merger Agreement”, “The Offer—Section 6—Price Range of Shares; Dividends” and “The Offer—Section 11—Dividends and Distributions” is incorporated herein by reference.

(c)(4) The information set forth in the Offer to Purchase under “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company” and “Special Factors—Section 7—Summary of the Merger Agreement” is incorporated herein by reference.

(c)(5) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 5—Effects of the Offer and the Merger” and “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” is incorporated herein by reference.

(c)(6) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 5—Effects of the Offer and the Merger” and “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” is incorporated herein by reference.

(c)(7) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 5—Effects of the Offer and the Merger” and “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” is incorporated herein by reference.

(c)(8) The information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 5—Effects of the Offer and the Merger” and “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” is incorporated herein by reference.

| Item 7. | Purposes, Alternatives, Reasons and Effects |

Item 1013 of Regulation M-A

(a) Purposes. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation—Reasons for the Special Committee’s Recommendation” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 1—Background” and “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company” is incorporated herein by reference.

(b) Alternatives. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation—Reasons for the Special Committee’s Recommendation” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background” and “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company” is incorporated herein by reference.

(c) Reasons. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation—Reasons for the Special Committee’s Recommendation” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company” and “Special Factors—Section 5—Effects of the Offer and the Merger” is incorporated herein by reference.

(d) Effects. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation—Reasons for the Special Committee’s Recommendation” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction”, “Special Factors—Section 5—Effects of the Offer and the Merger”, “Special Factors—Section 7—Summary of the Merger Agreement”, “Special Factors—Section 8—Dissenters’ Appraisal Rights; Rule 13e-3”, “The Offer—Section 5—Certain U.S. Federal Income Tax Considerations”, “The Offer—Section 7—Possible Effects of the Offer and the Merger on the Market for the Shares; NASDAQ Listing; Registration under the Exchange Act; Margin Regulations” “The Offer—Section 13—Certain Legal Matters; Regulatory Approvals” and “Schedule C—General Corporation Law of Delaware Section 262 Appraisal Rights” is incorporated herein by reference.

| Item 8. | Fairness of the Going-Private Transaction |

Item 1014 of Regulation M-A

(a) Fairness. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors—Section 3—The Recommendation by the Special Committee and the Company Board of Directors” and “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction” is incorporated herein by reference.

(b) Factors Considered in Determining Fairness. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Special Factors—Section 3—The Recommendation by the Special Committee and the Company Board of Directors” and “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction” is incorporated herein by reference.

(c) Approval of Security Holders. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 1—Background”, “Special Factors—Section 2—Purpose of and Reasons for the Offer; Plans for the Company”, “Special Factors—Section 3—The Recommendation by the Special Committee and the Company Board of Directors”, “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction”, “The Offer—Section 1—Terms of the Offer” and “The Offer—Section 12—Conditions of the Offer” is incorporated herein by reference.

(d) Unaffiliated Representative. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background”, “Special Factors—Section 3—The Recommendation by the Special Committee and the Company Board of Directors” and “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction” is incorporated herein by reference.

(e) Approval of Directors. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Summary Term Sheet”, “Introduction”, “Special Factors—Section 1—Background”, “Special Factors—Section 3—The Recommendation by the Special Committee and the Company Board of Directors” and “Special Factors—Section 4— Our Position Regarding Fairness of the Transaction” is incorporated herein by reference.

(f) Other Offers. Not applicable.

| Item 9. | Reports, Opinions, Appraisals and Negotiations |

Item 1015 of Regulation M-A

(a) Report, Opinion or Appraisal. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background” and “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction” is incorporated herein by reference.

(b) Preparer and Summary of the Report, Opinion or Appraisal. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Special Factors—Section 1—Background” and “Special Factors—Section 4—Our Position Regarding Fairness of the Transaction” is incorporated herein by reference.

(c) Availability of Documents. The reports, opinions or appraisals referenced in this Item 9 will be made available for inspection and copying at the principal executive offices of the Company during its regular business hours by any interested holder of Shares or any representative thereof who has been so designated in writing.

| Item 10. | Source and Amounts of Funds or Other Consideration |

Item 1007 of Regulation M-A

(a) Source of Funds. The information set forth in the Offer to Purchase under “Summary Term Sheet” and “The Offer—Section 10—Source and Amount of Funds” is incorporated herein by reference.

(b) Conditions. Not applicable.

(c) Expenses. The information set forth in the Offer to Purchase under “The Offer—Section 14—Fees and Expenses” is incorporated herein by reference.

(d) Borrowed Funds. Not applicable.

| Item 11. | Interest in Securities of the Subject Company |

Item 1008 of Regulation M-A

(a) Securities Ownership. The information set forth in the Offer to Purchase under “Introduction”, “Special Factors—Section 9—Transactions and Arrangements Concerning the Shares” and “Schedule B—Security Ownership of Certain Beneficial Owners” is incorporated herein by reference.

(b) Securities Transactions. The information set forth in the Schedule 14D-9 under “Item 6. Interest in Securities of the Subject Company” and the information set forth in the Offer to Purchase under “Introduction”, “Special Factors—Section 9—Transactions and Arrangements Concerning the Shares”, “Special Factors—Section 10—Related Party Transactions” and “Schedule B—Security Ownership of Certain Beneficial Owners” is incorporated herein by reference.

| Item 12. | The Solicitation or Recommendation |

Item 1012(d) and (e) of Regulation M-A

(d) Intent to Tender or Vote in a Going-Private Transaction. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation—Intent to Tender” and the information set forth in the Offer to Purchase under “Introduction”, “Special Factors—Section 9—Transactions and Arrangements Concerning the Shares” and “The Offer—Section 9—Certain Information Concerning the Offeror and Parent” is incorporated herein by reference.

(e) Recommendation of Others. The information set forth in the Schedule 14D-9 under “Item 4. The Solicitation or Recommendation—Solicitation or Recommendation” and the information set forth in the Offer to Purchase under “Special Factors—Section 3—The Recommendation by the Special Committee and the Company Board of Directors” and “The Offer—Section 9—Certain Information Concerning the Offeror and Parent” is incorporated herein by reference.

| Item 13. | Financial Statements Consideration |

Item 1010(a) and (b) of Regulation M-A

(a) Financial Information. The information set forth in the Offer to Purchase under “The Offer—Section 8—Certain Information Concerning the Company” is incorporated herein by reference. The financial statements of the Company are also incorporated herein by reference to its Form 10-K and Form 10-K/A for the year ended December 31, 2015, including to the section in the Form 10-K titled “Part II—Item 8—Financial Statements and Supplementary Data”. The unaudited consolidated financial statements of the Company on its Form 10-Q for the quarter ended June 30, 2016 are incorporated herein by reference to the section titled “Item 1. Financial Information”.

(b) Pro Forma Information. Not applicable.

| Item 14. | Persons/Assets Retained, Employed, Compensated or Used |

Item 1009 of Regulation M-A

(a) Solicitations or Recommendations. The information set forth in the Schedule 14D-9 under “Item 5. Persons/Assets Retained, Employed, Compensated or Used” and in the Offer to Purchase under “The Offer—Section 14—Fees and Expenses” is incorporated herein by reference.

(b) Employees and Corporate Assets. No officer, class of employee or corporate assets of the Company has been or will be employed or used by Parent or the Offeror in connection with the Offer and the Merger.

| Item 15. | Additional Information |

Item 1011(b) and (c) of Regulation M-A

(b) The information set forth in the schedule 14D-9 under “Item 3—Arrangements with Current Executive Officers and Directors of the Company—Golden Parachute Compensation” is incorporated herein by reference.

(c) Other Material Information. The information set forth in the Schedule 14D-9 under “Item 8—Additional Information” is incorporated herein by reference.

| Item 16. | Exhibits |

The following Exhibits are filed herewith or incorporated herein by reference:

| Exhibit No. |

Description | |

| (a)(1)(i) | Offer to Purchase, dated September 26, 2016 (incorporated by reference to Exhibit (a)(1)(i) to the Schedule TO of American Entertainment Properties Corp. and IEH FM Holdings, LLC, filed with the SEC on September 26, 2016). | |

| (a)(1)(ii) | Form of Letter of Transmittal (incorporated by reference to Exhibit (a)(1)(ii) to the Schedule TO of American Entertainment Properties Corp. and IEH FM Holdings, LLC, filed with the SEC on September 26, 2016). | |

| (a)(1)(iii) | Form of Notice of Guaranteed Delivery (incorporated by reference to Exhibit (a)(1)(iii) to the Schedule TO of American Entertainment Properties Corp. and IEH FM Holdings, LLC, filed with the SEC on September 26, 2016). | |

| (a)(1)(iv) | Form of Letter to Brokers, Dealers, Commercial Banks, Trust Companies and Other Nominees (incorporated by reference to Exhibit (a)(1)(iv) to the Schedule TO of American Entertainment Properties Corp. and IEH FM Holdings, LLC, filed with the SEC on September 26, 2016). | |

| (a)(1)(v) | Form of Letter to Clients for Use by Brokers, Dealers, Commercial Banks, Trust Companies and Other Nominees (incorporated by reference to Exhibit (a)(1)(v) to the Schedule TO of American Entertainment Properties Corp. and IEH FM Holdings, LLC, filed with the SEC on September 26, 2016). | |

| (a)(1)(vi) | Form of summary advertisement, published September 26, 2016 in The New York Times (incorporated by reference to Exhibit (a)(1)(vi) to the Schedule TO of American Entertainment Properties Corp. and IEH FM Holdings, LLC, filed with the SEC on September 26, 2016). | |

| (a)(5)(i) | Letter dated February 28, 2016 to the Board of Directors of Federal-Mogul Holdings Corporation (incorporated by reference to Exhibit 1 to the Schedule 13D amendment filed by Icahn Enterprises L.P. with the SEC Commission on February 29, 2016). | |

| (a)(5)(ii) | Letter dated June 17, 2016 to the Board of Directors of Federal-Mogul Holdings Corporation (incorporated by reference to Schedule 13D amendment filed by Icahn Enterprises L.P with the SEC on June 20, 2016). | |

| (a)(5)(iii) | Joint Press Release issued by Federal-Mogul Holdings Corporation and Icahn Enterprises L.P. on September 6, 2016 (incorporated by reference to the Schedule 14D9-C filed by Federal-Mogul Holdings Corporation with the SEC on September 6, 2016). | |

| (b) | None. | |

| (c)(1) | Opinion of Houlihan Lokey Capital, Inc., dated September 6, 2016 (incorporated by reference to Annex A to the Schedule 14D-9 filed by Federal-Mogul Holdings Corporation with the SEC on September 26, 2016). | |

| (c)(2) | Discussion materials for discussion with Icahn Enterprises, L.P., dated May 17, 2016.* | |

| (c)(3) | Preliminary discussion materials of Houlihan Lokey Capital, Inc. for the Special Committee of the Board of Directors of Federal-Mogul Holdings Corporation, dated June 14, 2016.* | |

| (c)(4) | Preliminary discussion materials of Houlihan Lokey Capital, Inc. for the Special Committee of the Board of Directors of Federal-Mogul Holdings Corporation, dated August 15, 2016.* | |

| (c)(5) | Preliminary discussion materials of Houlihan Lokey Capital, Inc. for the Special Committee of the Board of Directors of Federal-Mogul Holdings Corporation, dated September 5, 2016.* | |

| (c)(6) | Presentation of Houlihan Lokey Capital, Inc. to the Special Committee of the Board of Directors of Federal-Mogul Holdings Corporation, dated September 6, 2016.* | |

| (d)(1) | Agreement and Plan of Merger, dated as of September 6, 2016, by and among Federal-Mogul Holdings Corporation, American Entertainment Properties Corp. and IEH FM Holdings LLC (incorporated by reference to Exhibit 2.1 to the Current Report on Form 8-K filed by Federal-Mogul Holdings Corporation with the SEC on September 7, 2016). | |

| (d)(2) | Amendment and Joinder to Federal-Mogul Corporation Registration Rights Agreement among Federal-Mogul Corporation and IEH FM Holdings LLC (incorporated by reference to Exhibit 4.1 to the Current Report on Form 8-K filed by Federal-Mogul Holdings Corporation with the SEC on July 11, 2013). | |

| (d)(3) | Tax Allocation Agreement by and among American Entertainment Properties Corp. and Federal Mogul Corporation dated as of July 11, 2013 (incorporated by reference to Exhibit 10. to the Current Report on Form 8-K filed by Federal-Mogul Holdings Corporation with the SEC on July 11, 2013). | |

| (f) | The information set forth in the Schedule 14D-9 under “Item 8. Additional Information—Appraisal Rights” and “Annex B—Section 262 of the Delaware General Corporation Law” is incorporated herein by reference. | |

| (g) | None. | |

| * | Filed herewith |

SIGNATURE

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this Statement is true, complete and correct.

Date: September 26, 2016

| FEDERAL-MOGUL HOLDINGS CORPORATION | ||

| By: | /s/ Michelle Epstein Taigman | |

| Name: | Michelle Epstein Taigman | |

| Title: | Senior Vice President, General Counsel and Secretary | |

| IEH FM HOLDINGS LLC | ||

| By: | Icahn Enterprises Holdings L.P., its sole member | |

| By: | Icahn Enterprises G.P. Inc., its general partner | |

| By: | /s/ SungHwan Cho | |

| Name: | SungHwan Cho | |

| Title: | Chief Financial Officer | |

| AMERICAN ENTERTAINMENT PROPERTIES CORP. | ||

| By: | /s/ SungHwan Cho | |

| Name: | SungHwan Cho | |

| Title: | Chief Financial Officer | |

| ICAHN BUILDING LLC | ||

| By: | Icahn Enterprises Holdings L.P., its sole member | |

| By: | Icahn Enterprises G.P. Inc., its general partner | |

| By: | /s/ SungHwan Cho | |

| Name: | SungHwan Cho | |

| Title: | Chief Financial Officer | |

| ICAHN ENTERPRISES HOLDINGS L.P. | ||

| By: | Icahn Enterprises G.P. Inc., its general partner | |

| By: | /s/ SungHwan Cho | |

| Name: | SungHwan Cho | |

| Title: | Chief Financial Officer | |

| ICAHN ENTERPRISES G.P. INC. | ||

| By: | /s/ SungHwan Cho | |

| Name: | SungHwan Cho | |

| Title: | Chief Financial Officer | |

| BECKTON CORP. | ||

| By: | /s/ Edward E. Mattner | |

| Name: | Edward E. Mattner | |

| Title: | Authorized Signatory | |

| CARL C. ICAHN | ||

| /s/ Carl C. Icahn | ||

| Exhibit C2

|

Project Piston

MATERIALS PREPARED FOR DISCUSSION WITH IC AHN ENTERPRISES, L . P.

MAY 17, 2016 | CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW AND REVISION

1

|

|

Table of Contents

Page

1. Selected Illustrative Financial Analyses 3

2. Certain Non-Financial Observations 9

3. Appendices 12

Selected Companies and Transactions Information 13

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 2

2

|

|

Page

1. Selected Illustrative Financial Analyses 3

2. Certain Non-Financial Observations 9

3. Appendices 12

3

|

|

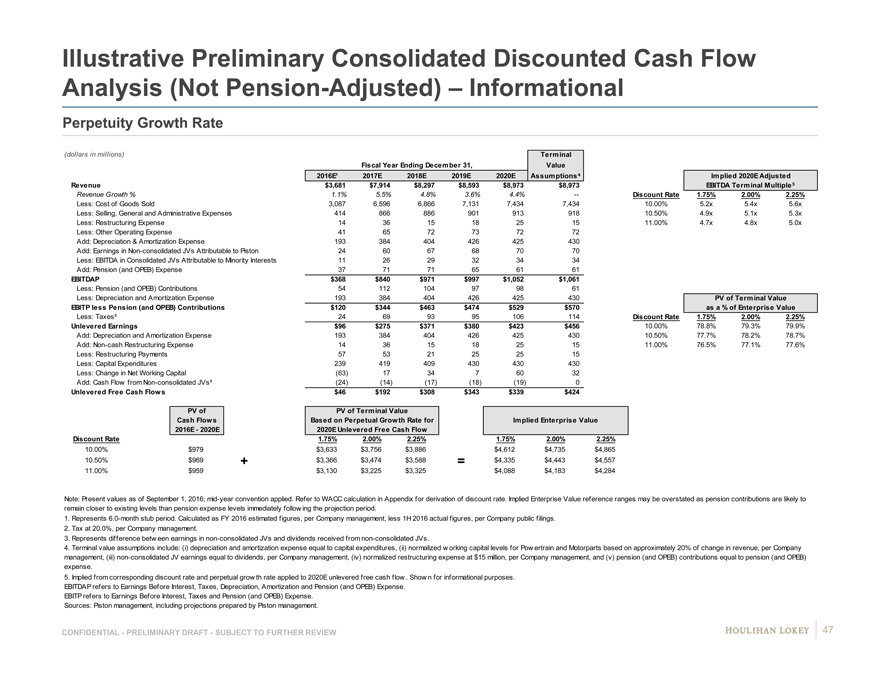

Piston Consolidated Summary Historical and Projected

Financial Data

The preliminary perspectives reflected are based on financial information provided by Company management.

(dollars in millions) LTM

3/31/2016 2016E 2017E 2018E 2019E 2020E

Revenue $7,481 $7,502 $7,914 $8,297 $8,593 $8,973

%Growth — 1.1% 5.5% 4.8% 3.6% 4.4%

Gross Profit $1,111 $1,186 $1,318 $1,431 $1,462 $1,539

%Margin 14.9% 15.8% 16.7% 17.2% 17.0% 17.2%

Less: Selling, General and Administrative Expenses 789 827 866 886 901 913

Less: Other Expenses / (Income)(28) 10 5 5 5 2

EBIT $350 $349 $446 $539 $556 $624

%Margin 4.7% 4.7% 5.6% 6.5% 6.5% 7.0%

Add: Depreciation, Amortization and Other Expenses 345 386 396 413 432 428

EBITDA¹ $695 $735 $842 $952 $988 $1,052

%Margin 9.3% 9.8% 10.6% 11.5% 11.5% 11.7%

Less: Adjustment for Pension Expense Included in D&A and Other Expenses² 2 13 12 9 6 3

Less: EBITDA of Interests in Consolidated JVs Not Attributable to Company² 20 23 26 29 32 34

Adjusted EBITDA² $673 $699 $804 $914 $950 $1,015

%Margin 9.0% 9.3% 10.2% 11.0% 11.1% 11.3%

Add: Pension (and OPEB) Expense 61 68 71 71 65 61

Adjusted EBITDAP $734 $767 $875 $985 $1,015 $1,076

Capital Expenditures $426 $434 $419 $409 $430 $430

Segment Information

Pow ertrain Adjusted EBITDA $416 $442 $497 $563 $614 $643

Pow ertrain Adjusted EBITDAP $468 $502 $560 $625 $671 $696

Motorparts Adjusted EBITDA $257 $257 $307 $351 $336 $372

Motorparts Adjusted EBITDAP $266 $265 $316 $360 $344 $380

Source: Company management

1. Per Company management, EBITDA reflects addbacks for projected restructuring expenses.

2. Reflects adjustments per direction of Company management, as discussed with the Special Committee.

Note: Illustrative discounted cash flow analyses also reflect additional cash flow items not shown above, including changes in net working capital,

restructuring expenses/payments, cash flows related to non-consolidated JVs, and pension (and OPEB) contributions.

Note: Certain figures may differ slightly due to rounding.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 4

4

|

|

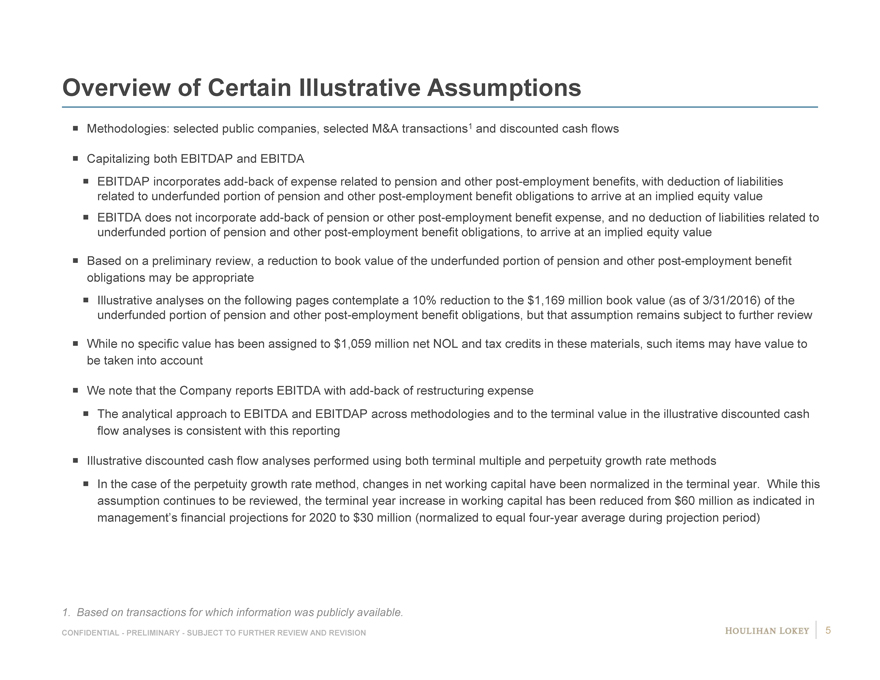

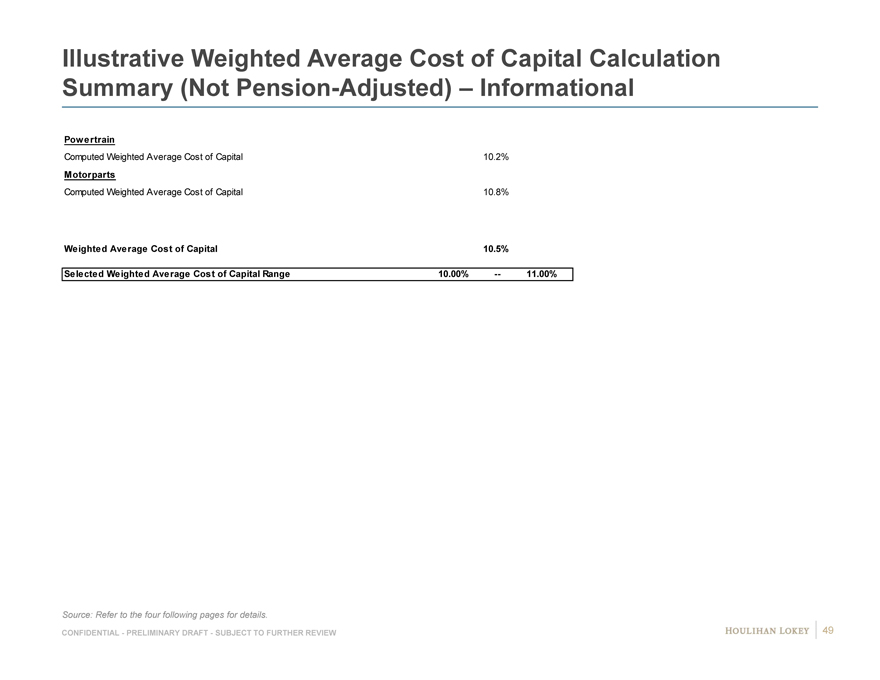

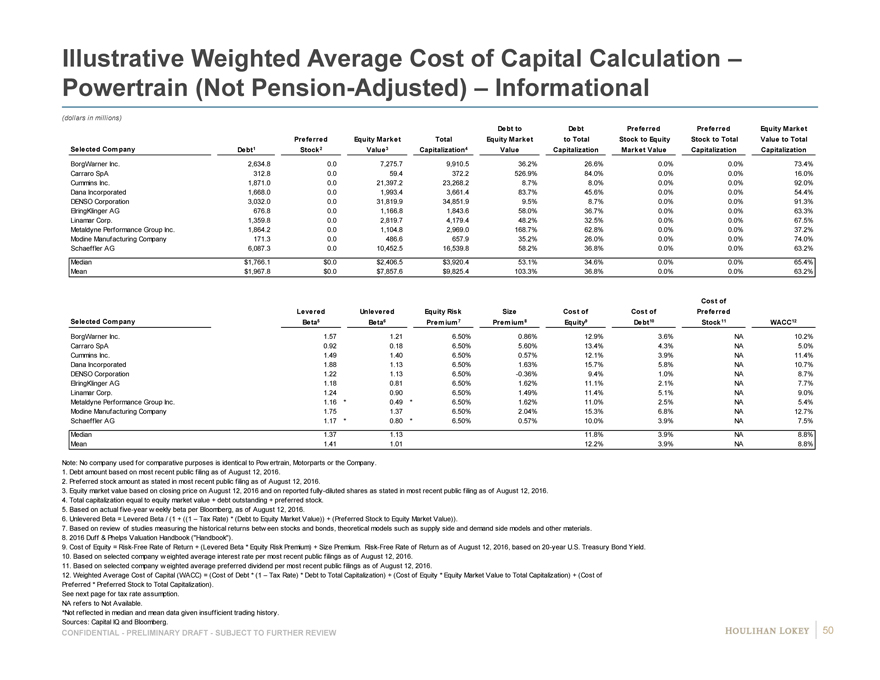

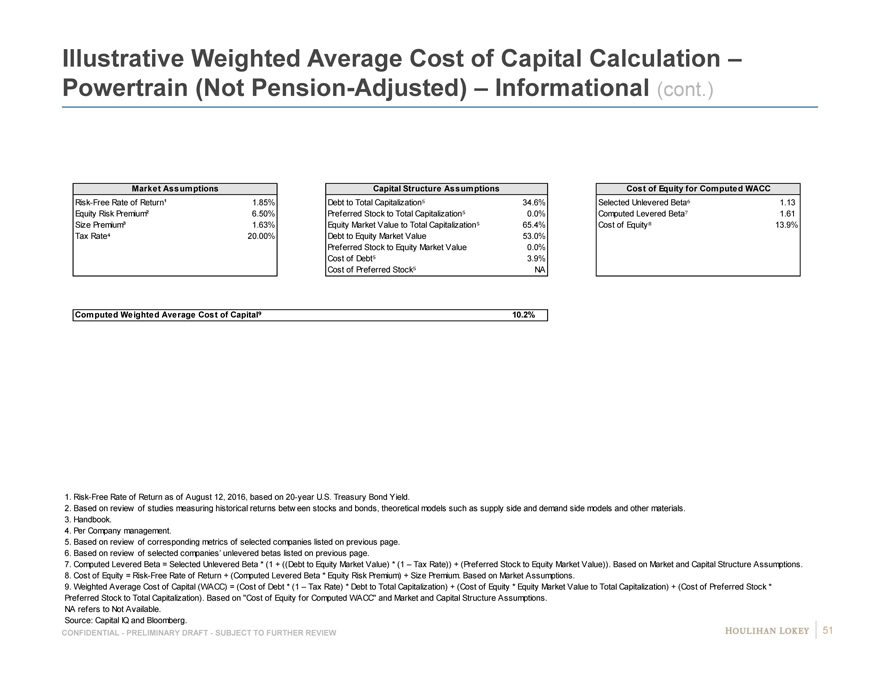

Overview of Certain Illustrative Assumptions

Methodologies: selected public companies, selected M&A transactions1 and discounted cash flows

Capitalizing both EBITDAP and EBITDA

EBITDAP incorporates add-back of expense related to pension and other post-employment benefits, with deduction of liabilities related to underfunded portion of pension and other post-employment benefit obligations to arrive at an implied equity value EBITDA does not incorporate add-back of pension or other post-employment benefit expense, and no deduction of liabilities related to underfunded portion of pension and other post-employment benefit obligations, to arrive at an implied equity value

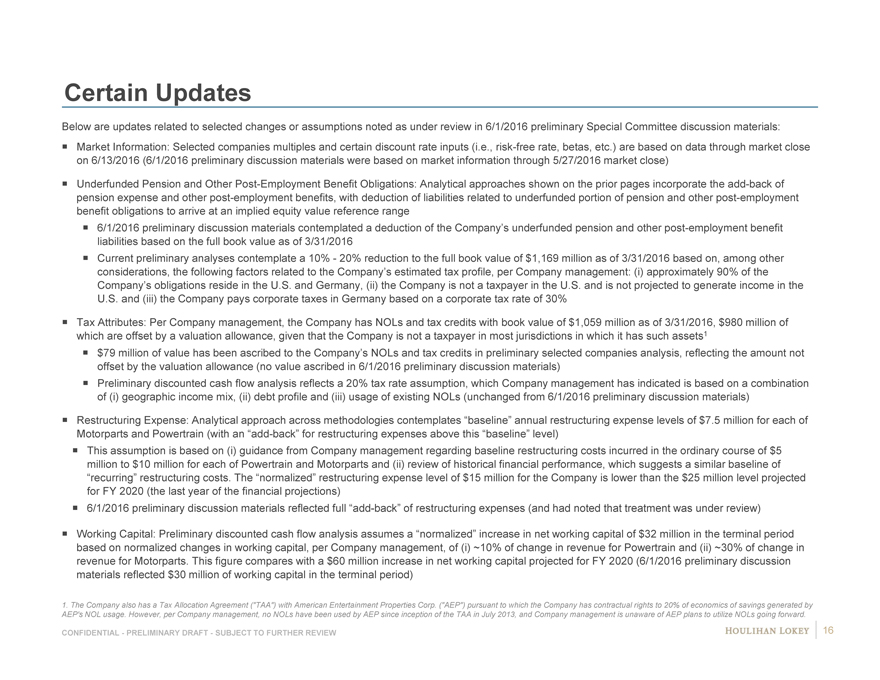

Based on a preliminary review, a reduction to book value of the underfunded portion of pension and other post-employment benefit obligations may be appropriate Illustrative analyses on the following pages contemplate a 10% reduction to the $1,169 million book value (as of 3/31/2016) of the underfunded portion of pension and other post-employment benefit obligations, but that assumption remains subject to further review

While no specific value has been assigned to $1,059 million net NOL and tax credits in these materials, such items may have value to be taken into account

We note that the Company reports EBITDA with add-back of restructuring expense

The analytical approach to EBITDA and EBITDAP across methodologies and to the terminal value in the illustrative discounted cash flow analyses is consistent with this reporting

Illustrative discounted cash flow analyses performed using both terminal multiple and perpetuity growth rate methods

In the case of the perpetuity growth rate method, changes in net working capital have been normalized in the terminal year. While this assumption continues to be reviewed, the terminal year increase in working capital has been reduced from $60 million as indicated in management’s financial projections for 2020 to $30 million (normalized to equal four-year average during projection period)

1. Based on transactions for which information was publicly available.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 5

|

|

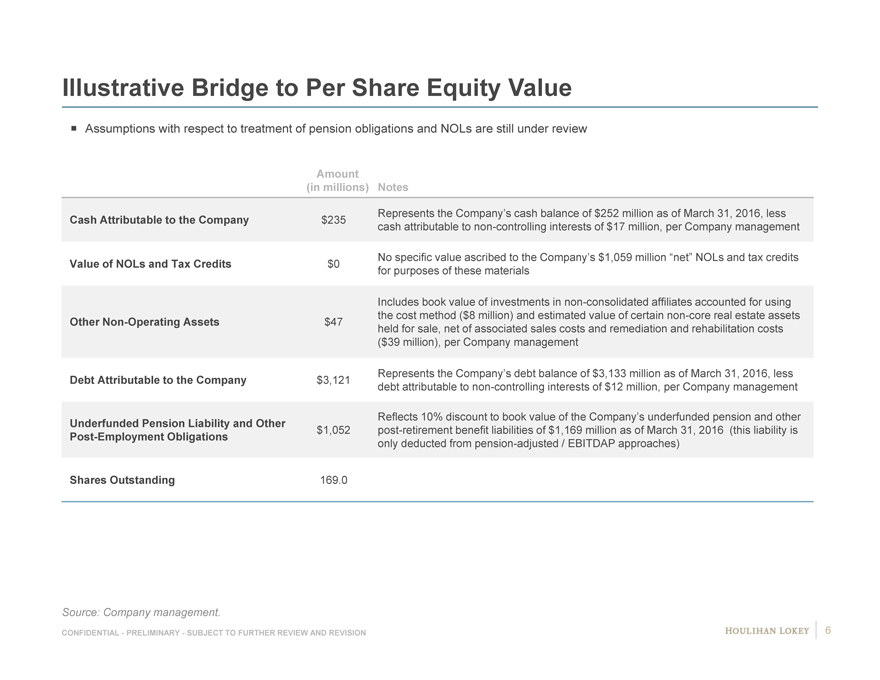

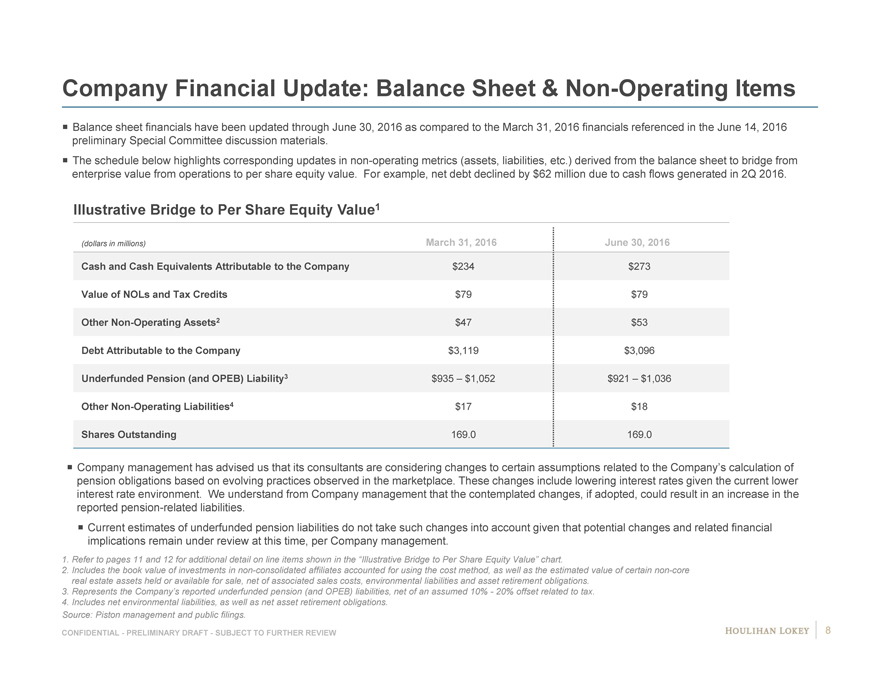

Illustrative Bridge to Per Share Equity Value

Assumptions with respect to treatment of pension obligations and NOLs are still under review

Amount

(in millions) Notes

Represents the Company’s cash balance of $252 million as of March 31, 2016, less

Cash Attributable to the Company $235 cash attributable to non-controlling interests of $17 million, per Company management

No specific value ascribed to the Company’s $1,059 million “net” NOLs and tax credits

Value of NOLs and Tax Credits $0 for purposes of these materials

Includes book value of investments in non-consolidated affiliates accounted for using the cost method ($8 million) and estimated value of certain non-core real estate assets

Other Non-Operating Assets $47 held for sale, net of associated sales costs and remediation and rehabilitation costs

($39 million), per Company management

Represents the Company’s debt balance of $3,133 million as of March 31, 2016, less

Debt Attributable to the Company $3,121 debt attributable to non-controlling interests of $12 million, per Company management

Reflects 10% discount to book value of the Company’s underfunded pension and other

Underfunded Pension Liability and Other $1,052 post-retirement benefit liabilities of $1,169 million as of March 31, 2016 (this liability is

Post-Employment Obligations only deducted from pension-adjusted / EBITDAP approaches)

Shares Outstanding 169.0

Source: Company management.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 6

|

|

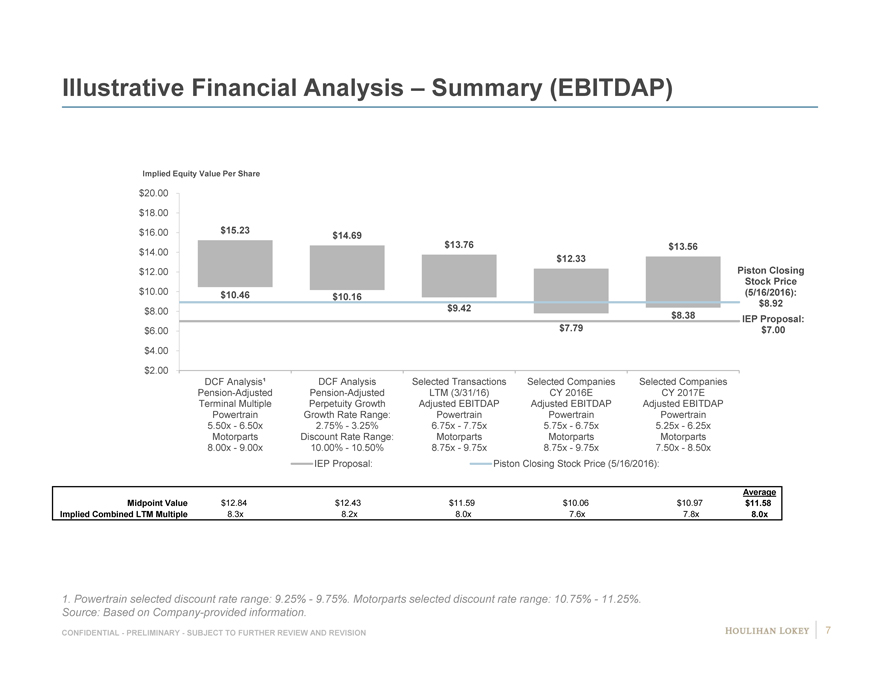

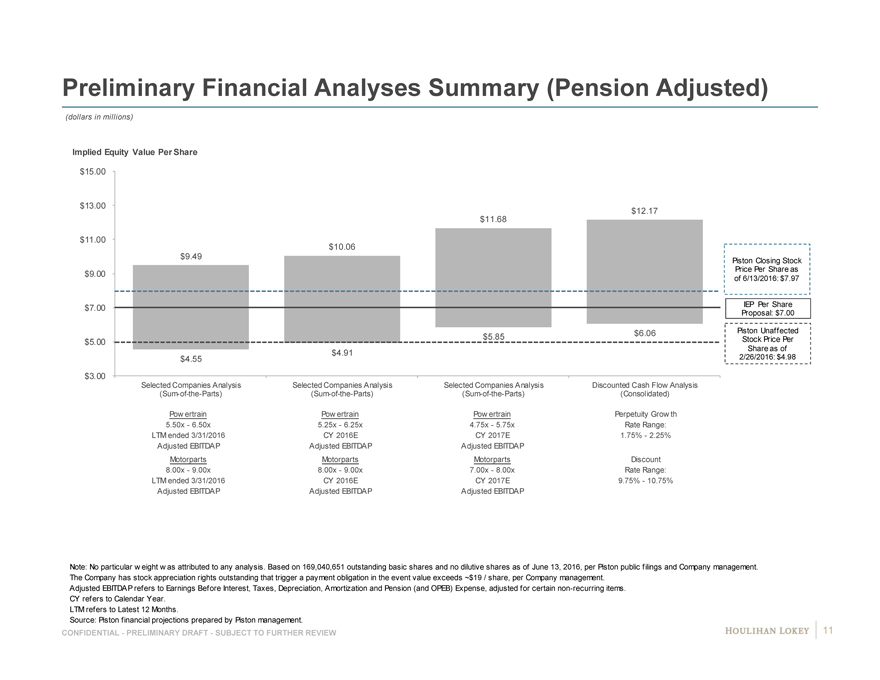

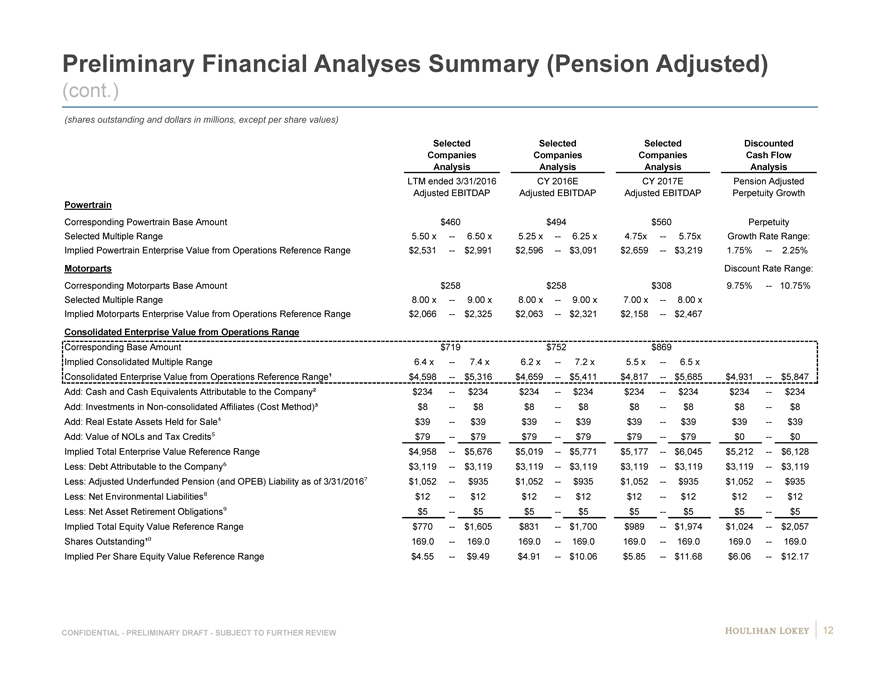

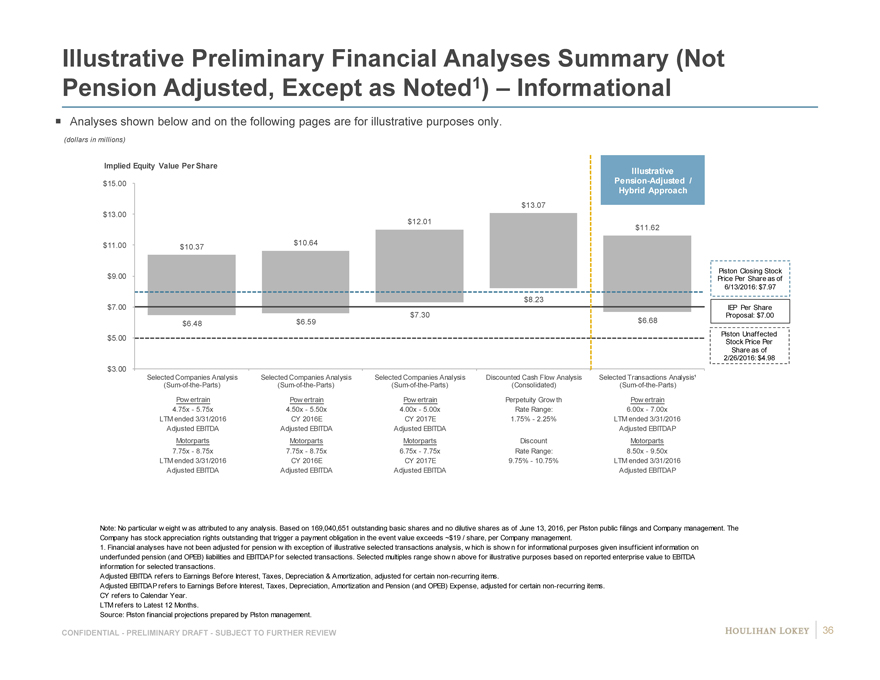

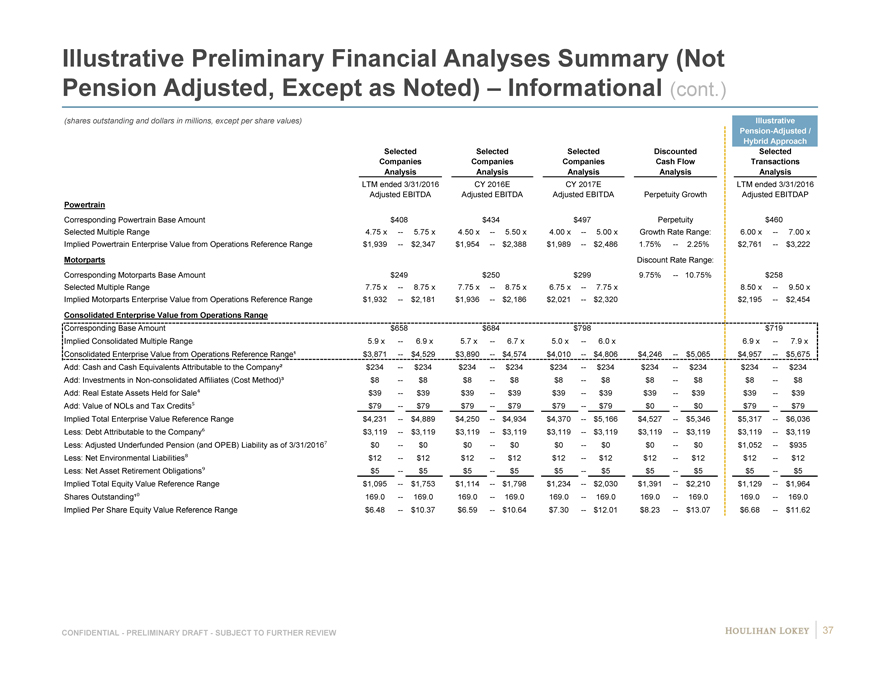

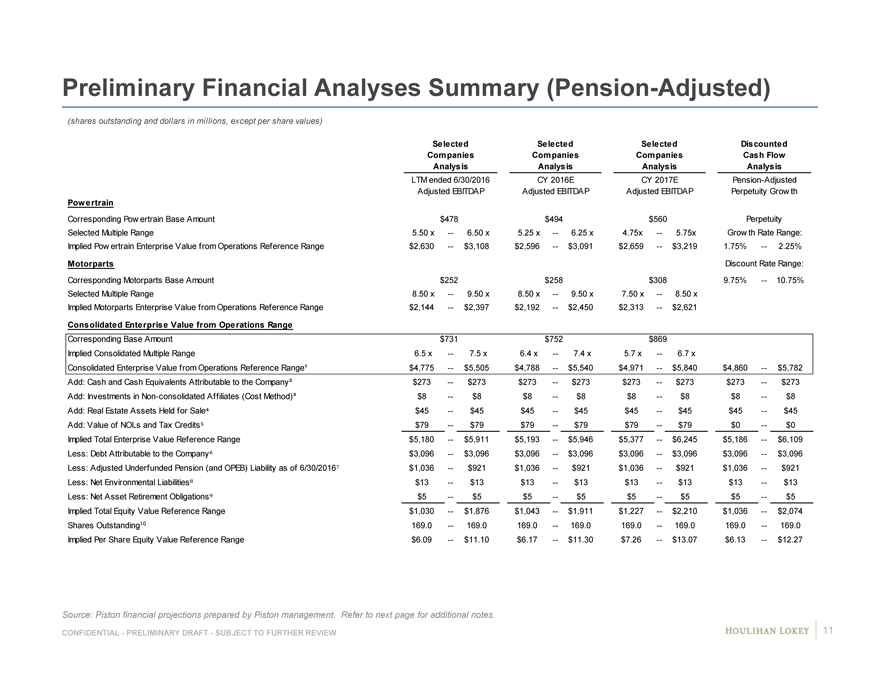

Illustrative Financial Analysis – Summary (EBITDAP)

Implied Equity Value Per Share

$20.00

$18.00

$16.00 $ 15.23 $ 14.69

$14.00 $13.76 $13.56

$12.33

$12.00 Piston Closing

Stock Price

$10.00 $ 10.46 $ 10.16(5/16/2016):

$8.92

$8.00 $9.42

$8.38 IEP Proposal:

$6.00 $7.79 $7.00

$4.00

$2.00

DCF Analysis¹ DCF Analysis Selected Transactions Selected Companies Selected Companies

Pension-Adjusted Pension-Adjusted LTM (3/31/16) CY 2016E CY 2017E

Terminal Multiple Perpetuity Growth Adjusted EBITDAP Adjusted EBITDAP Adjusted EBITDAP

Powertrain Growth Rate Range: Powertrain Powertrain Powertrain

5.50x—6.50x 2.75%—3.25% 6.75x—7.75x 5.75x—6.75x 5.25x—6.25x

Motorparts Discount Rate Range: Motorparts Motorparts Motorparts

8.00x—9.00x 10.00%—10.50% 8.75x—9.75x 8.75x—9.75x 7.50x—8.50x

IEP Proposal: Piston Closing Stock Price (5/16/2016):

Average

Midpoint Value $12.84 $12.43 $11.59 $10.06 $10.97 $11.58

Implied Combined LTM Multiple 8.3x 8.2x 8.0x 7.6x 7.8x 8.0x

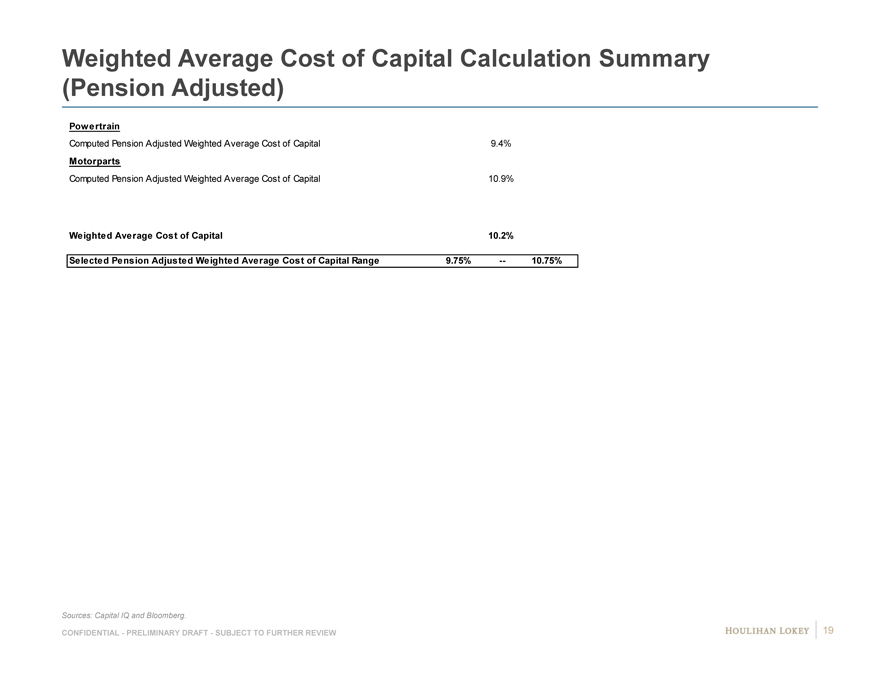

1. Powertrain selected discount rate range: 9.25%—9.75%. Motorparts selected discount rate range: 10.75%—11.25%.

Source: Based on Company-provided information.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 7

|

|

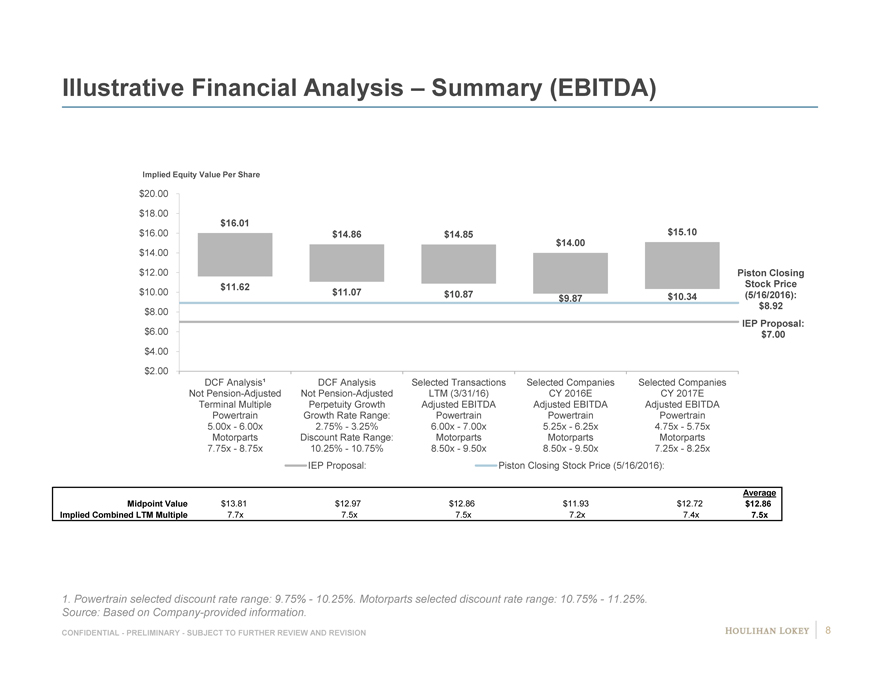

Illustrative Financial Analysis – Summary (EBITDA)

Implied Equity Value Per Share

$20.00

$18.00

$16.01

$16.00 $14.86 $14.85 $15.10

$14.00

$14.00

$12.00 Piston Closing

$11.62 Stock Price

$10.00 $11.07 $10.87 $9.87 $10.34(5/16/2016):

$8.00 $8.92

IEP Proposal:

$6.00 $7.00

$4.00

$2.00

DCF Analysis¹ DCF Analysis Selected Transactions Selected Companies Selected Companies

Not Pension-Adjusted Not Pension-Adjusted LTM (3/31/16) CY 2016E CY 2017E

Terminal Multiple Perpetuity Growth Adjusted EBITDA Adjusted EBITDA Adjusted EBITDA

Powertrain Growth Rate Range: Powertrain Powertrain Powertrain

5.00x—6.00x 2.75%—3.25% 6.00x—7.00x 5.25x—6.25x 4.75x—5.75x

Motorparts Discount Rate Range: Motorparts Motorparts Motorparts

7.75x—8.75x 10.25%—10.75% 8.50x—9.50x 8.50x—9.50x 7.25x—8.25x

IEP Proposal: Piston Closing Stock Price (5/16/2016):

Average

Midpoint Value $13.81 $12.97 $12.86 $11.93 $12.72 $12.86

Implied Combined LTM Multiple 7.7x 7.5x 7.5x 7.2x 7.4x 7.5x

1. Powertrain selected discount rate range: 9.75%—10.25%. Motorparts selected discount rate range: 10.75%—11.25%.

Source: Based on Company-provided information.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 8

|

|

Page

1. Selected Illustrative Financial Analyses 3

2. Certain Non-Financial Observations 9

3. Appendices 12

|

|

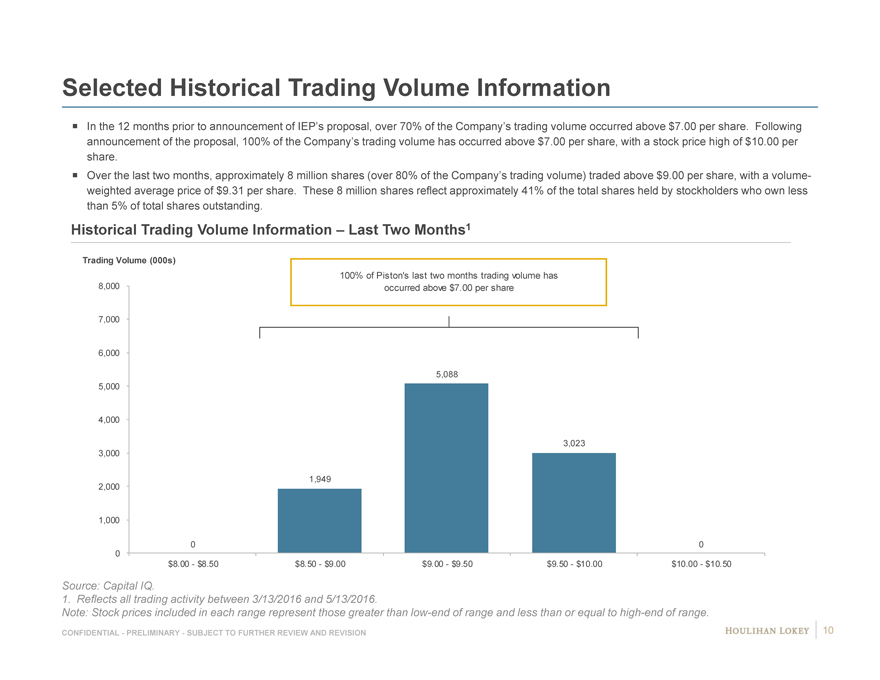

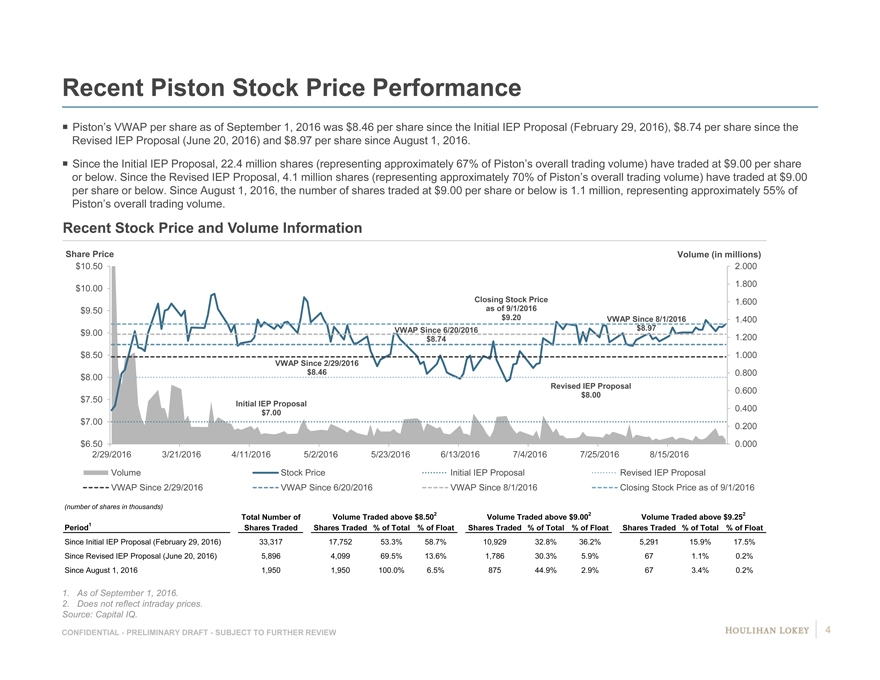

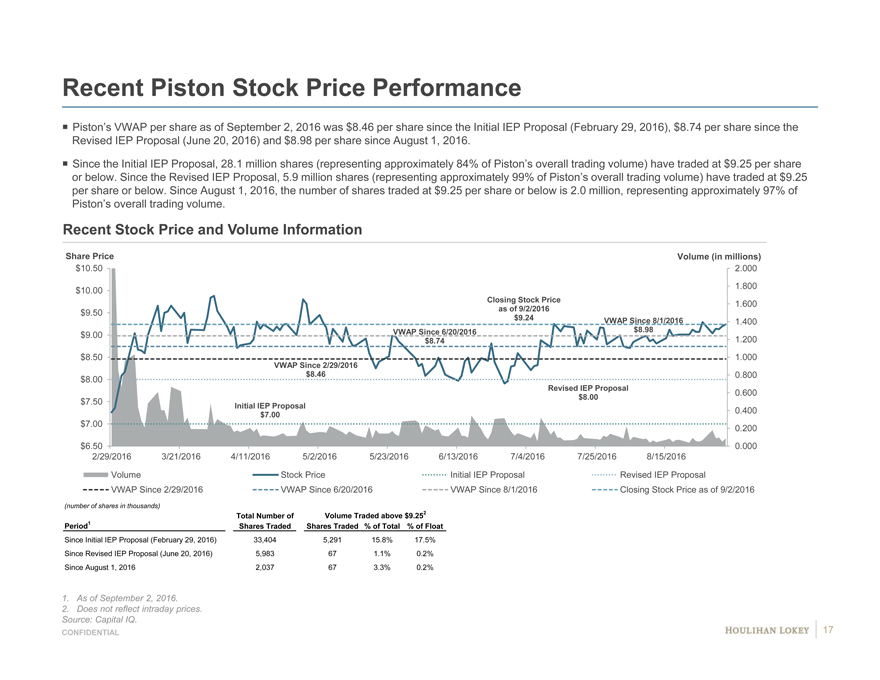

Selected Historical Trading Volume Information

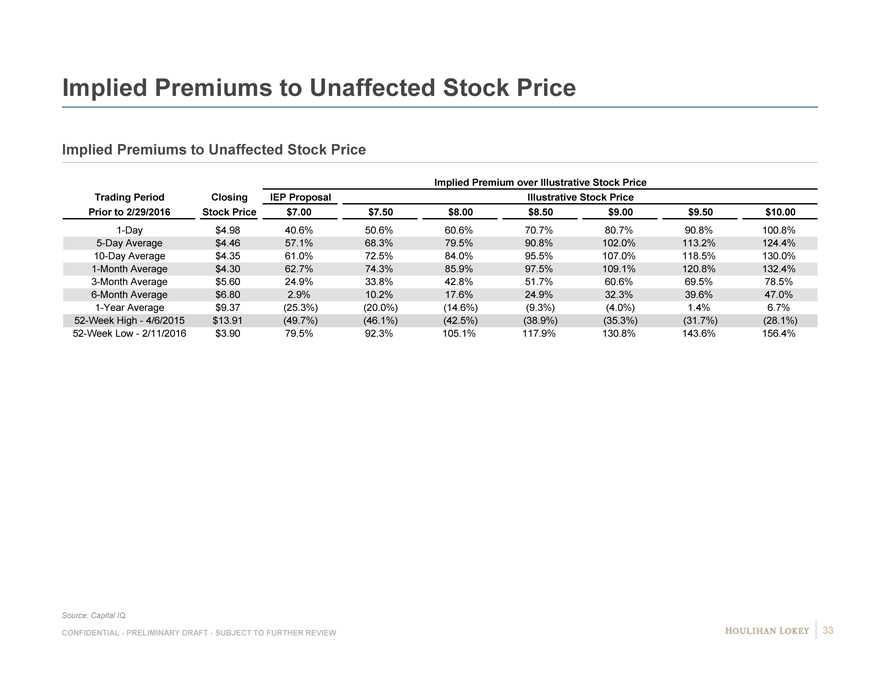

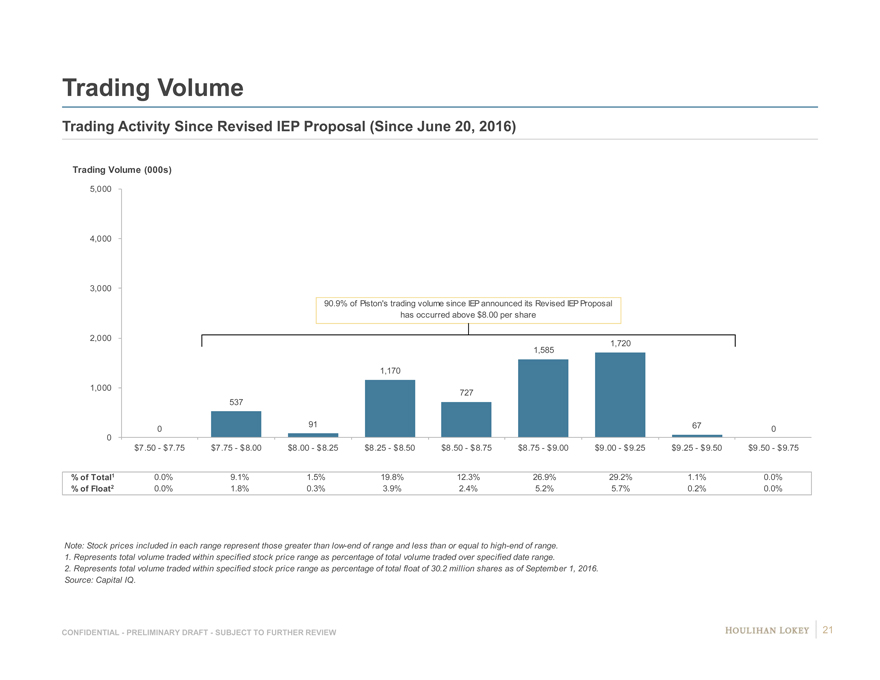

In the 12 months prior to announcement of IEP’s proposal, over 70% of the Company’s trading volume occurred above $7.00 per share. Following announcement of the proposal, 100% of the Company’s trading volume has occurred above $7.00 per share, with a stock price high of $10.00 per share.

Over the last two months, approximately 8 million shares (over 80% of the Company’s trading volume) traded above $9.00 per share, with a volume-weighted average price of $9.31 per share. These 8 million shares reflect approximately 41% of the total shares held by stockholders who own less than 5% of total shares outstanding.

Historical Trading Volume Information – Last Two Months1

Trading Volume (000s)

100% of Piston’s last two months trading volume has

8,000 occurred above $7.00 per share

7,000

6,000

5,088

5,000

4,000

3,023

3,000

1,949

2,000

1,000

0 0

0

$8.00—$8.50 $8.50—$9.00 $9.00—$9.50 $9.50—$10.00 $10.00—$10.50

Source: Capital IQ.

1. Reflects all trading activity between 3/13/2016 and 5/13/2016.

Note: Stock prices included in each range represent those greater than low-end of range and less than or equal to high-end of range.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 10

|

|

Selected Wall Street Analyst Commentary

Broker Selected Commentary

BB&T Capital “Piston’s aftermarket division continues to move in the right direction. For the third consecutive quarter, Piston has shown Markets steady operational improvement, with increased revenue in 1Q the result of more efficient distribution in NA (+26%) along with growth in Asia, where the company is well positioned to benefit from a car parc that soon will require more and more replacement parts…We were encouraged by a steady quarter from Powertrain. While FX and global commercial and off-highway vehicle markets were headwinds in the quarter, benefits of restructuring along with growth global light vehicle production and the company’s valvetrain acquisition helped provide stronger profitability.” “While Piston’s Board of Directors considers this offer, the shares appear to be signaling a $10 per share offer price to get a deal done. Management thinks the Board will have an answer to the proposal within the next few weeks. We see this as his final step in terms of vertically integrating IEP’s aftermarket conglomerate, although we continue to think this strategy will be challenging to fully implement and likely lead to share loss at a minimum in the early stages.”

Gabelli & “In our 3/1 note on Piston, we explained that IEP’s $7/sh bid for the company did not reflect the full underlying value given the Company transformation required to transform Motorparts. This quarter only bolstered our thesis that significant value creation remains as Piston modernizes its distribution system and positions Motorparts for two decades of upcoming growth in the Asian automotive aftermarket. Our 2017 Private Market Value for Piston is $17 per share ($15 per share prior), which assigns a 7.0x multiple to Powertrain and 8.5x for Motorparts. As we highlighted then, IEP clearly sees the value in Piston shares at current prices. We believe it to be a matter of time before the rest of the market does as well.”

Source: Wall Street research; the above reflect those broker reports that Houlihan Lokey has been able to access.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 11

|

|

Page

1. Selected Illustrative Financial Analyses 3

2. Certain Non-Financial Observations 9

3. Appendices 12 Selected Companies and Transactions Information 13

|

|

Page

1. Selected Illustrative Financial Analyses 3

2. Certain Non-Financial Observations 9

3. Appendices 12 Selected Companies and Transactions Information 13

|

|

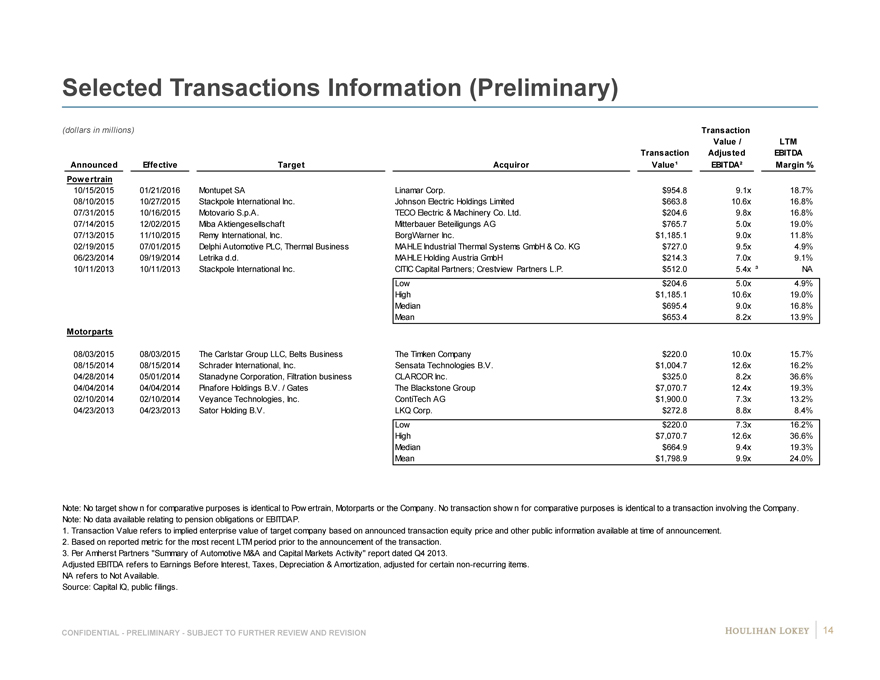

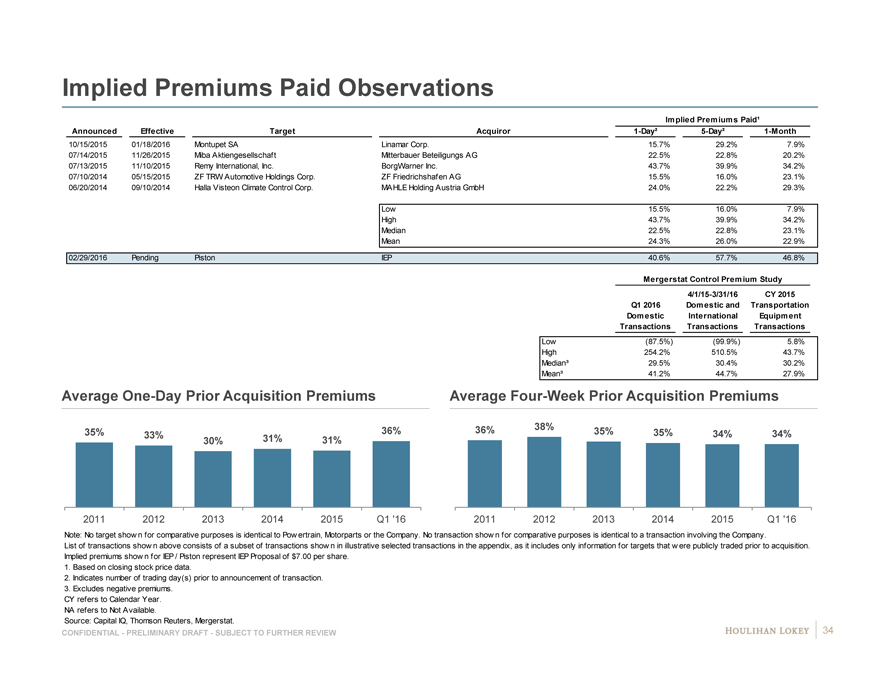

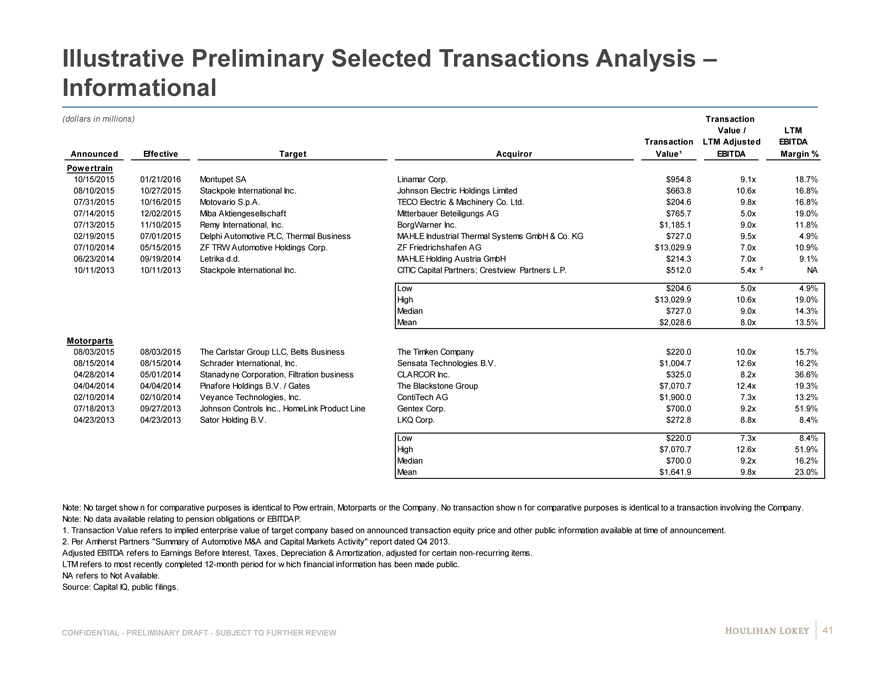

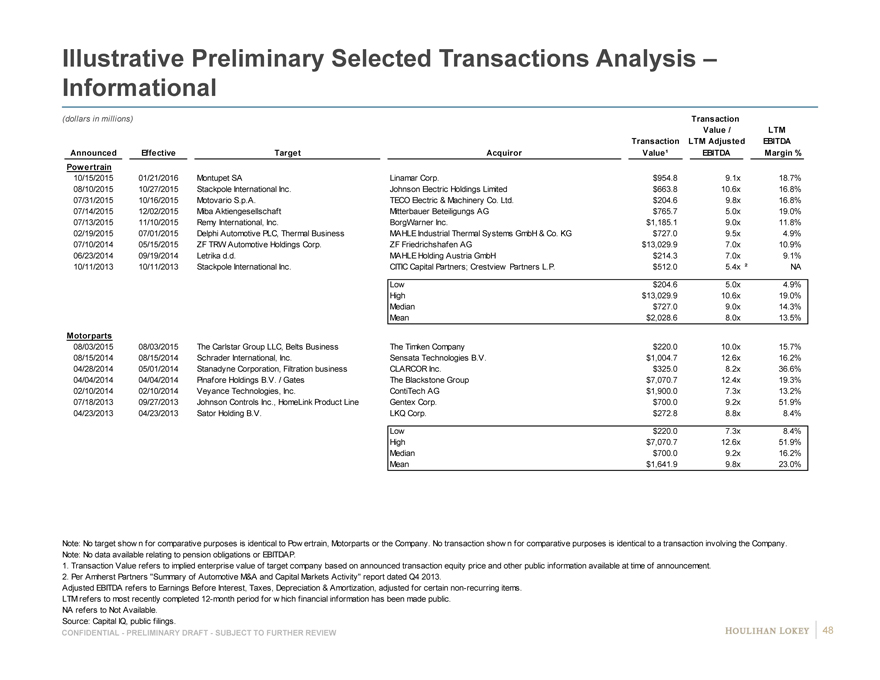

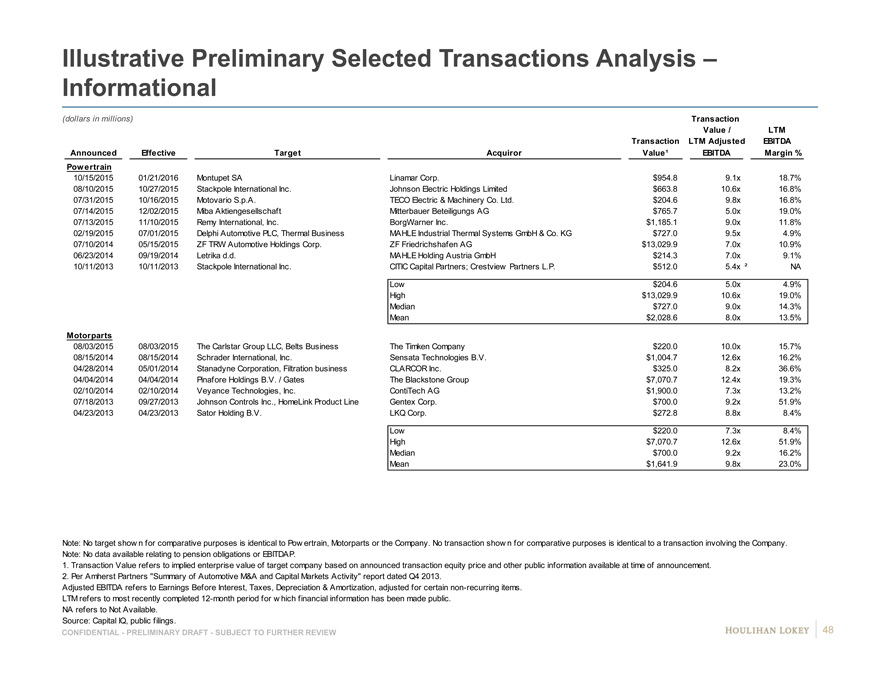

Selected Transactions Information (Preliminary)

(dollars in millions) Transaction

Value / LTM

Transaction Adjusted EBITDA

Announced Effective Target Acquiror Value¹ EBITDA² Margin %

Powertrain

10/15/2015 01/21/2016 Montupet SA Linamar Corp. $954.8 9.1x 18.7%

08/10/2015 10/27/2015 Stackpole International Inc. Johnson Electric Holdings Limited $663.8 10.6x 16.8%

07/31/2015 10/16/2015 Motovario S.p.A. TECO Electric & Machinery Co. Ltd. $204.6 9.8x 16.8%

07/14/2015 12/02/2015 Miba Aktiengesellschaft Mitterbauer Beteiligungs AG $765.7 5.0x 19.0%

07/13/2015 11/10/2015 Remy International, Inc. BorgWarner Inc. $1,185.1 9.0x 11.8%

02/19/2015 07/01/2015 Delphi Automotive PLC, Thermal Business MAHLE Industrial Thermal Systems GmbH & Co. KG $727.0 9.5x 4.9%

06/23/2014 09/19/2014 Letrika d.d. MAHLE Holding Austria GmbH $214.3 7.0x 9.1%

10/11/2013 10/11/2013 Stackpole International Inc. CITIC Capital Partners; Crestview Partners L.P. $512.0 5.4x ³ NA N

Low $204.6 5.0x 4.9%

High $1,185.1 10.6x 19.0%

Median $695.4 9.0x 16.8%

Mean $653.4 8.2x 13.9%

Motorparts

08/03/2015 08/03/2015 The Carlstar Group LLC, Belts Business The Timken Company $220.0 10.0x 15.7%

08/15/2014 08/15/2014 Schrader International, Inc. Sensata Technologies B.V. $1,004.7 12.6x 16.2%

04/28/2014 05/01/2014 Stanadyne Corporation, Filtration business CLARCOR Inc. $325.0 8.2x 36.6%

04/04/2014 04/04/2014 Pinafore Holdings B.V. / Gates The Blackstone Group $7,070.7 12.4x 19.3%

02/10/2014 02/10/2014 Veyance Technologies, Inc. ContiTech AG $1,900.0 7.3x 13.2%

04/23/2013 04/23/2013 Sator Holding B.V. LKQ Corp. $272.8 8.8x 8.4%

Low $220.0 7.3x 16.2%

High $7,070.7 12.6x 36.6%

Median $664.9 9.4x 19.3%

Mean $1,798.9 9.9x 24.0%

Note: No target show n for comparative purposes is identical to Pow ertrain, Motorparts or the Company. No transaction show n for comparative purposes is identical to a transaction involving the Company.

Note: No data available relating to pension obligations or EBITDAP.

1. Transaction Value refers to implied enterprise value of target company based on announced transaction equity price and other public information available at time of announcement.

2. Based on reported metric for the most recent LTM period prior to the announcement of the transaction.

3. Per Amherst Partners “Summary of Automotive M&A and Capital Markets Activity” report dated Q4 2013.

Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation & Amortization, adjusted for certain non-recurring items.

NA refers to Not Available.

Source: Capital IQ, public filings.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 14

|

|

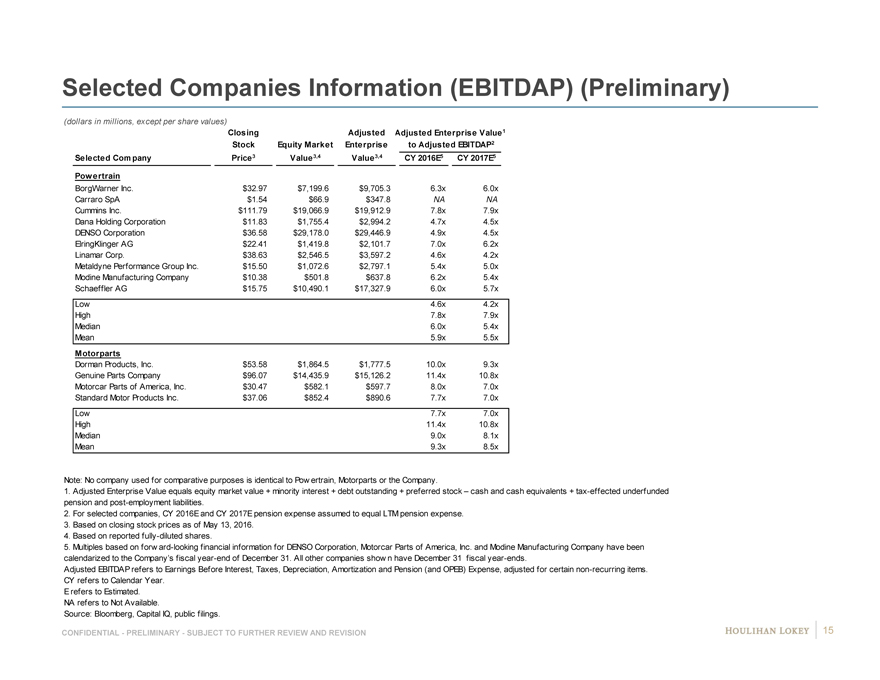

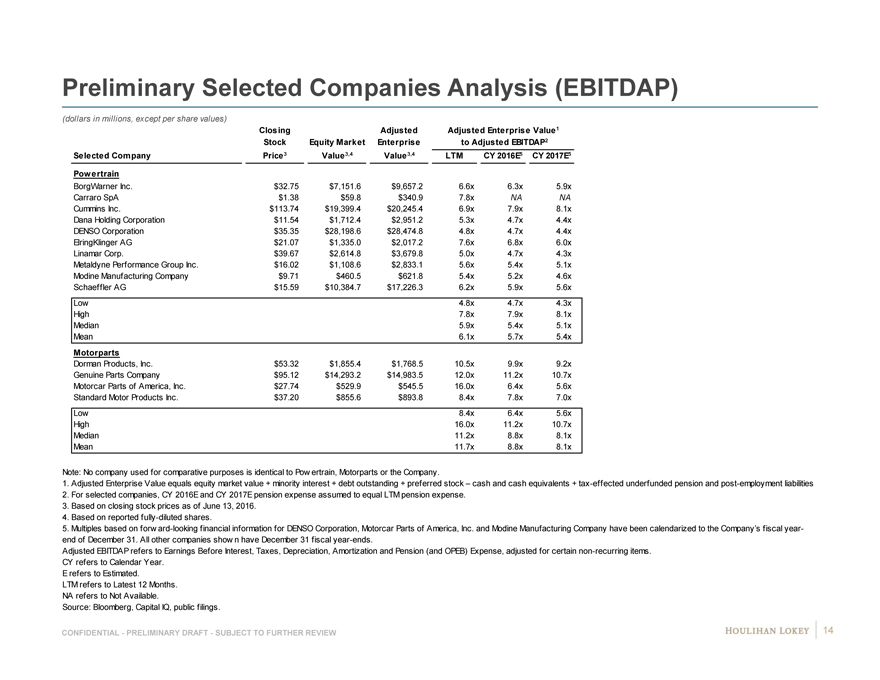

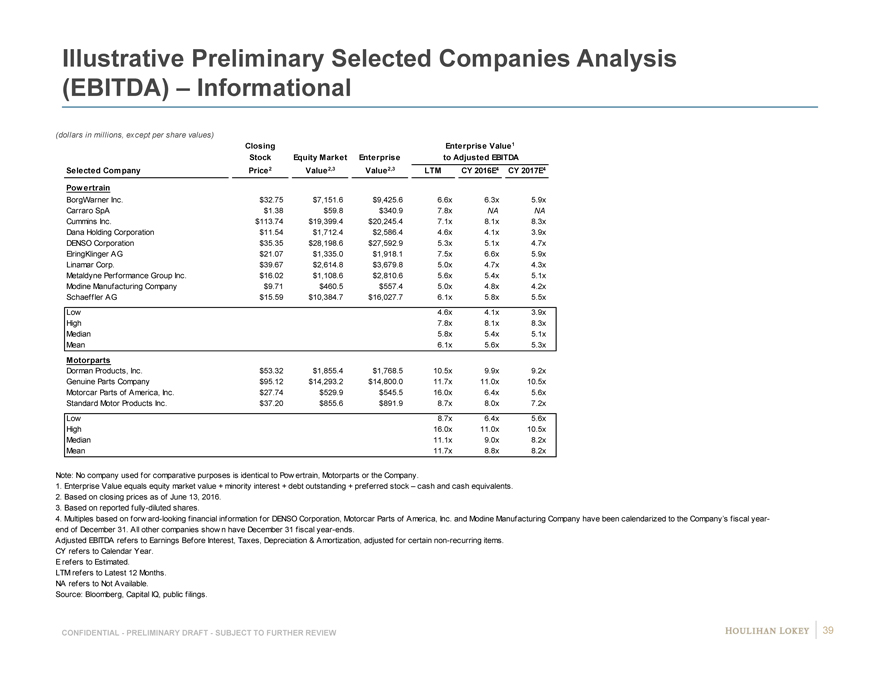

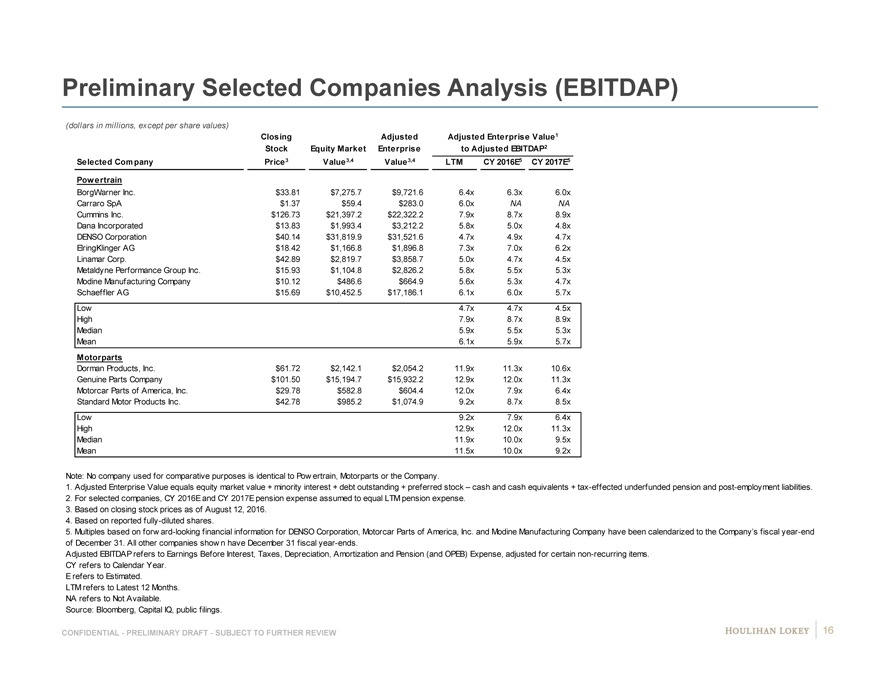

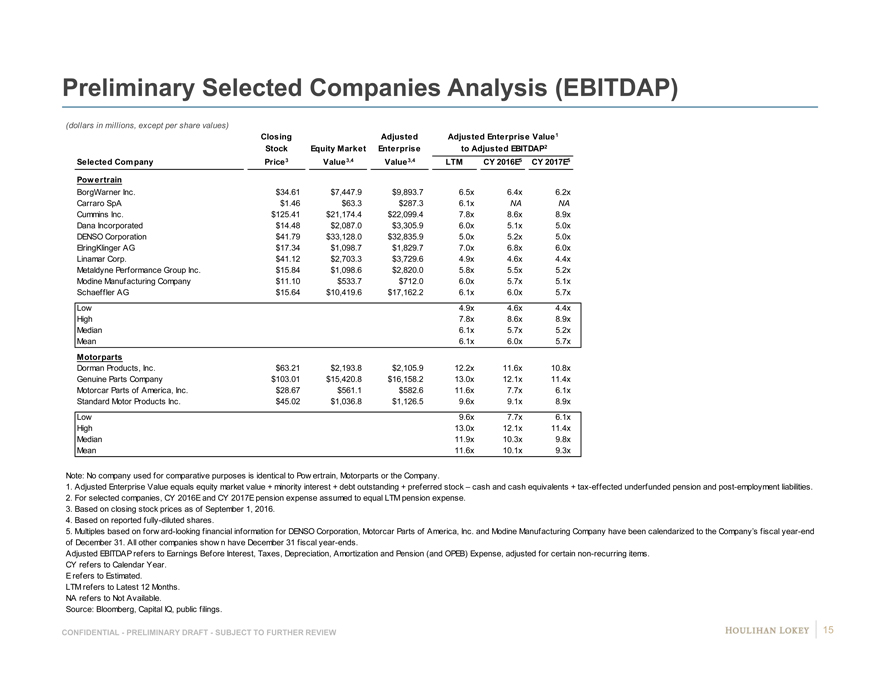

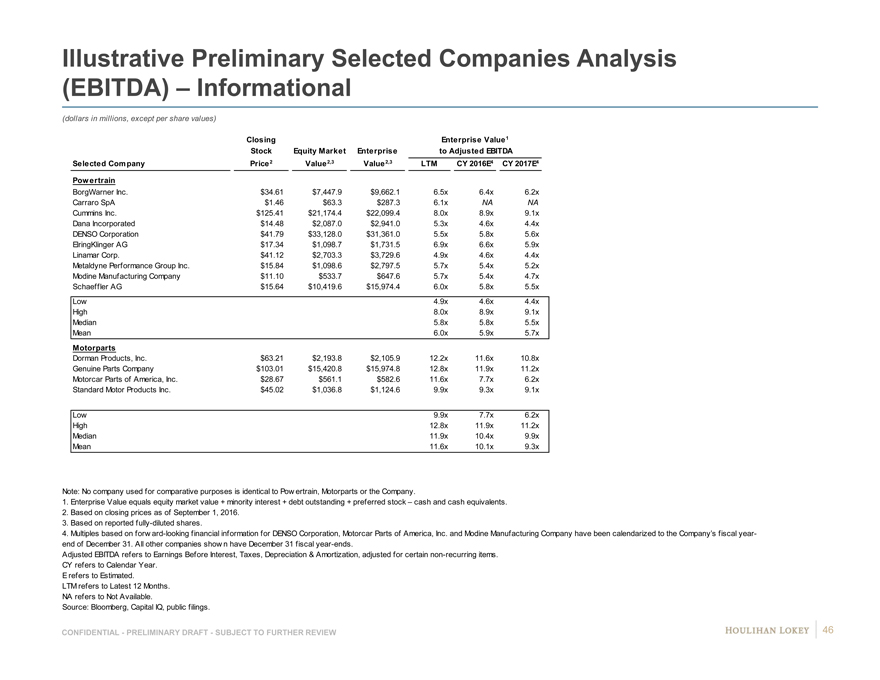

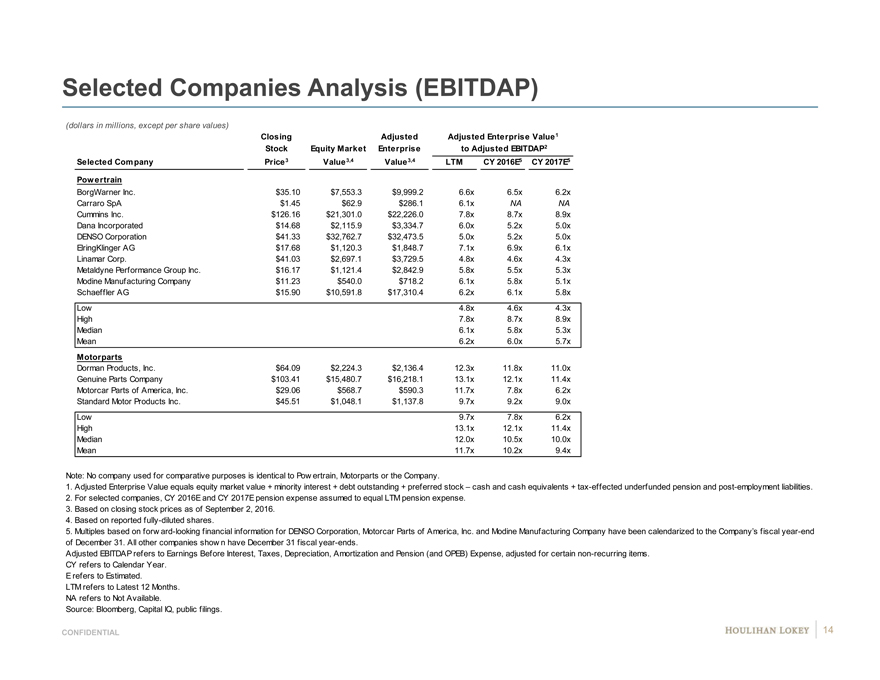

Selected Companies Information (EBITDAP) (Preliminary)

(dollars in millions, except per share values)

Closing Adjusted Adjusted Enterprise Value1

Stock Equity Market Enterprise to Adjusted EBITDAP2

Selected Company Price3 Value 3,4 Value 3,4 CY 2016E5 CY 2017E5

Powertrain

BorgWarner Inc. $32.97 $7,199.6 $9,705.3 6.3x 6.0x 6 9

Carraro SpA $1.54 $66.9 $347.8 NA NA N NA

Cummins Inc. $111.79 $19,066.9 $19,912.9 7.8x 7.9x 8 #

Dana Holding Corporation $11.83 $1,755.4 $2,994.2 4.7x 4.5x 4 8

DENSO Corporation $36.58 $29,178.0 $29,446.9 4.9x 4.5x 5 8

ElringKlinger AG $22.41 $1,419.8 $2,101.7 7.0x 6.2x 6 #

Linamar Corp. $38.63 $2,546.5 $3,597.2 4.6x 4.2x 4 9

Metaldyne Performance Group Inc. $15.50 $1,072.6 $2,797.1 5.4x 5.0x 5 8

Modine Manufacturing Company $10.38 $501.8 $637.8 6.2x 5.4x 5 #

Schaeffler AG $15.75 $10,490.1 $17,327.9 6.0x 5.7x 6 9

Low 4.6x 4.2x

High 7.8x 7.9x

Median 6.0x 5.4x

Mean 5.9x 5.5x

Motorparts

Dorman Products, Inc. $53.58 $1,864.5 $1,777.5 10.0x 9.3x 9 #

Genuine Parts Company $96.07 $14,435.9 $15,126.2 11.4x 10.8x # #

Motorcar Parts of America, Inc. $30.47 $582.1 $597.7 8.0x 7.0x 7 7

Standard Motor Products Inc. $37.06 $852.4 $890.6 7.7x 7.0x 7 NA

Low 7.7x 7.0x

High 11.4x 10.8x

Median 9.0x 8.1x

Mean 9.3x 8.5x

Note: No company used for comparative purposes is identical to Pow ertrain, Motorparts or the Company.

1. Adjusted Enterprise Value equals equity market value + minority interest + debt outstanding + preferred stock – cash and cash equivalents + tax-effected underfunded

pension and post-employment liabilities.

2. For selected companies, CY 2016E and CY 2017E pension expense assumed to equal LTM pension expense.

3. Based on closing stock prices as of May 13, 2016.

4. Based on reported fully-diluted shares.

5. Multiples based on forw ard-looking financial information for DENSO Corporation, Motorcar Parts of America, Inc. and Modine Manufacturing Company have been

calendarized to the Company’s fiscal year-end of December 31. All other companies show n have December 31 fiscal year-ends.

Adjusted EBITDAP refers to Earnings Before Interest, Taxes, Depreciation, Amortization and Pension (and OPEB) Expense, adjusted for certain non-recurring items.

CY refers to Calendar Year.

E refers to Estimated.

NA refers to Not Available.

Source: Bloomberg, Capital IQ, public filings.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 15

|

|

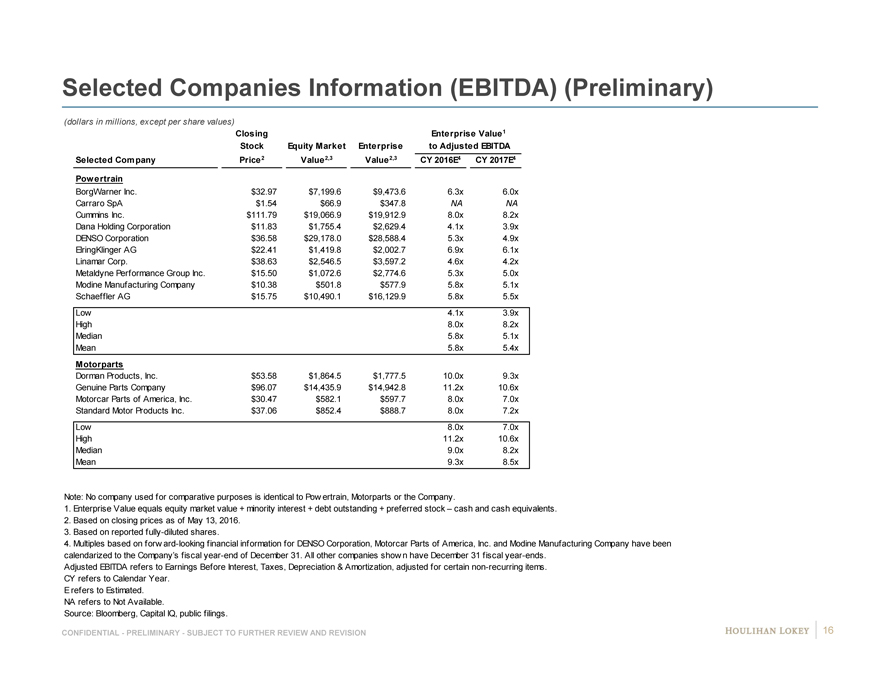

Selected Companies Information (EBITDA) (Preliminary)

(dollars in millions, except per share values)

Closing Enterprise Value 1

Stock Equity Market Enterprise to Adjusted EBITDA

Selected Company Price 2 Value 2,3 Value2,3 CY 2016E4 CY 2017E4

Powertrain

BorgWarner Inc. $32.97 $7,199.6 $9,473.6 6.3x 6.0x 6 9

Carraro SpA $1.54 $66.9 $347.8 NA NA N NA

Cummins Inc. $111.79 $19,066.9 $19,912.9 8.0x 8.2x 8 #

Dana Holding Corporation $11.83 $1,755.4 $2,629.4 4.1x 3.9x 4 7

DENSO Corporation $36.58 $29,178.0 $28,588.4 5.3x 4.9x 5 #

ElringKlinger AG $22.41 $1,419.8 $2,002.7 6.9x 6.1x 6 #

Linamar Corp. $38.63 $2,546.5 $3,597.2 4.6x 4.2x 4 9

Metaldyne Performance Group Inc. $15.50 $1,072.6 $2,774.6 5.3x 5.0x 5 8

Modine Manufacturing Company $10.38 $501.8 $577.9 5.8x 5.1x 5 #

Schaeffler AG $15.75 $10,490.1 $16,129.9 5.8x 5.5x 6 9

Low 4.1x 3.9x

High 8.0x 8.2x

Median 5.8x 5.1x

Mean 5.8x 5.4x

Motorparts

Dorman Products, Inc. $53.58 $1,864.5 $1,777.5 10.0x 9.3x 9 #

Genuine Parts Company $96.07 $14,435.9 $14,942.8 11.2x 10.6x # #

Motorcar Parts of America, Inc. $30.47 $582.1 $597.7 8.0x 7.0x 7 7

Standard Motor Products Inc. $37.06 $852.4 $888.7 8.0x 7.2x 7 NA

Low 8.0x 7.0x

High 11.2x 10.6x

Median 9.0x 8.2x

Mean 9.3x 8.5x

Note: No company used for comparative purposes is identical to Pow ertrain, Motorparts or the Company.

1. Enterprise Value equals equity market value + minority interest + debt outstanding + preferred stock – cash and cash equivalents.

2. Based on closing prices as of May 13, 2016.

3. Based on reported fully-diluted shares.

4. Multiples based on forw ard-looking financial information for DENSO Corporation, Motorcar Parts of America, Inc. and Modine Manufacturing Company have been

calendarized to the Company’s fiscal year-end of December 31. All other companies show n have December 31 fiscal year-ends.

Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation & Amortization, adjusted for certain non-recurring items.

CY refers to Calendar Year.

E refers to Estimated.

NA refers to Not Available.

Source: Bloomberg, Capital IQ, public filings.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 16

|

|

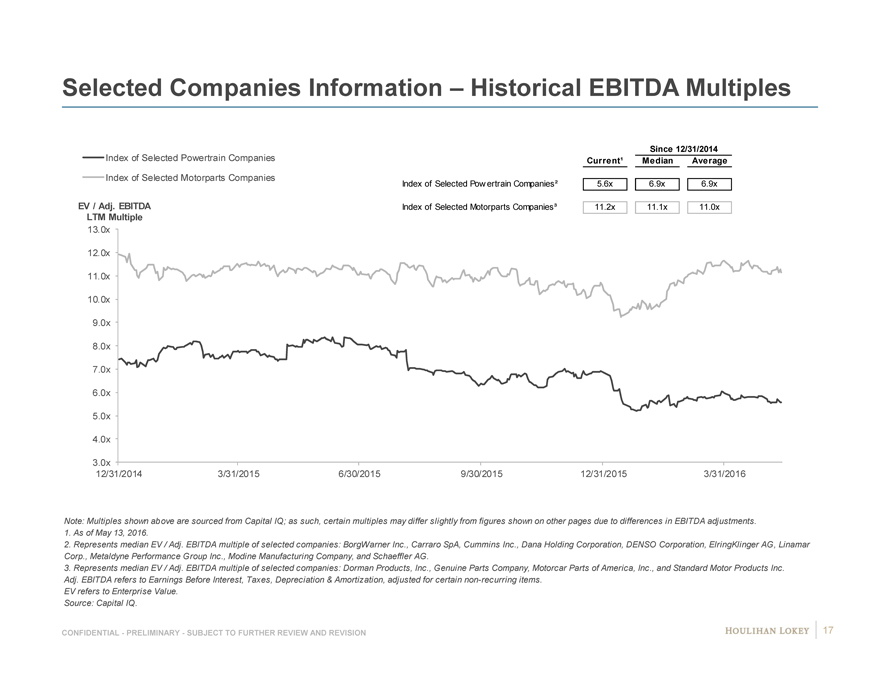

Selected Companies Information – Historical EBITDA Multiples

Since 12/31/2014

Index of Selected Powertrain Companies Current¹ Median Average

Index of Selected Motorparts Companies Index of Selected Pow ertrain Companies² 5.6x 6.9x 6.9x

EV / Adj. EBITDA Index of Selected Motorparts Companies³ 11.2x 11.1x 11.0x

LTM Multiple

13.0x

12.0x

11.0x

10.0x

9.0x

8.0x

7.0x

6.0x

5.0x

4.0x

3.0x

12/31/2014 3/31/2015 6/30/2015 9/30/2015 12/31/2015 3/31/2016

Note: Multiples shown above are sourced from Capital IQ; as such, certain multiples may differ slightly from figures shown on other pages due to differences in EBITDA adjustments.

1. As of May 13, 2016.

2. Represents median EV / Adj. EBITDA multiple of selected companies: BorgWarner Inc., Carraro SpA, Cummins Inc., Dana Holding Corporation, DENSO Corporation, ElringKlinger AG, Linamar

Corp., Metaldyne Performance Group Inc., Modine Manufacturing Company, and Schaeffler AG.

3. Represents median EV / Adj. EBITDA multiple of selected companies: Dorman Products, Inc., Genuine Parts Company, Motorcar Parts of America, Inc., and Standard Motor Products Inc.

Adj. EBITDA refers to Earnings Before Interest, Taxes, Depreciation & Amortization, adjusted for certain non-recurring items.

EV refers to Enterprise Value.

Source: Capital IQ.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 17

|

|

Disclaimer

Houlihan Lokey Capital, Inc. (“Houlihan Lokey”) has been retained by the Special Committee of the Board of Directors of Piston (“Piston” or the “Company”) to serve as its financial advisor in connection with the evaluation of a potential transaction involving the Company (a “Transaction”).

These materials have been prepared at the direction of the Special Committee for discussion purposes only and are delivered on a confidential basis in accordance with procedures established by the Special Committee. These materials do not purport to contain all of the information that may be required or relevant to an evaluation of the Company or any Transaction and you are solely responsible for conducting your own investigations and analysis and arriving at your own independent conclusions.

These materials may not be distributed, reproduced or used without the express consent of Special Committee or for any purpose other than the evaluation of a possible Transaction. In addition, if you do not wish to pursue a Transaction, you must promptly return these materials to Houlihan Lokey as soon as practicable, together with any other materials relating to the Company which you have received from or on behalf of the Special Committee or its representatives.

Houlihan Lokey has not independently verified any of the information contained herein. Neither the Special Committee nor Houlihan Lokey or any other representatives of the Special Committee makes any representation, warranty or guaranty of any kind, express or implied, as to the accuracy, completeness or reasonableness of the information contained herein or any other written or oral communication transmitted or made available to you. The Special Committee, Houlihan Lokey and other representatives of the Special Committee expressly disclaim any and all liability based on or arising from, in whole or in part, such information, errors therein or omissions therefrom. In addition, these materials include certain projections and forward-looking statements provided by the Company with respect to the anticipated future performance of the Company. Such projections and forward-looking statements, including the assumptions on which they are based, are subject to adjustment based on discussions with Company management and the Special Committee. Financial analyses performed by Houlihan Lokey for purposes of advising the Special Committee may differ from those set forth herein. In addition, the projections and forward-looking statements contained herein are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control of the Special Committee and the Company. Accordingly, there can be no assurance that such projections or forward-looking statements will be realized. Actual results may vary from anticipated results and such variations may be material. No representations or warranties are made as to the accuracy or reasonableness of such projections or forward-looking statements or the assumptions based thereon. Only those representations and warranties that are made in a definitive written agreement relating to a Transaction, when and if executed, and subject to any limitations and restrictions as may be specified in such definitive agreement, shall have any legal effect. You should make an independent assessment of the merits of pursuing a Transaction and should consult your own professional advisors.

CONFIDENTIAL—PRELIMINARY—SUBJECT TO FURTHER REVIEW AND REVISION 18

| Exhibit C3

|

Project Piston

DISCUSSION MATERIALS FOR THESPECIAL COMMITTEE

JUNE 14, 2016 | PRELIMINARY DRAFT – SUBJECT TO REVIEW – CONFIDENTIAL

|

|

Table of Contents

Page

1. Selected Public Market Observations 3

2. Preliminary Financial Analyses 7

3. Appendix 17

Cost of Capital Considerations 18

Benchmarking 24

Company Financial Performance Observations 28

Premiums Paid Observations 32

Illustrative Preliminary Financial Analyses (EBITDA) 35

Selected Excerpt from June 1, 2016 Preliminary Discussion Materials:

47

Items Subject to Further Review

Selected Excerpts from May 11, 2016 / June 1, 2016 Preliminary

49

Discussion Materials: Illustrative Sensitivities

4. Disclaimer 53

CONFIDENTIAL—PRELIMINARY DRAFT—SUBJECT TO FURTHER REVIEW 2

Page

|

|

1. Selected Public Market Observations 3

2. Preliminary Financial Analyses 7

3. Appendix 17

4. Disclaimer 53

|

|

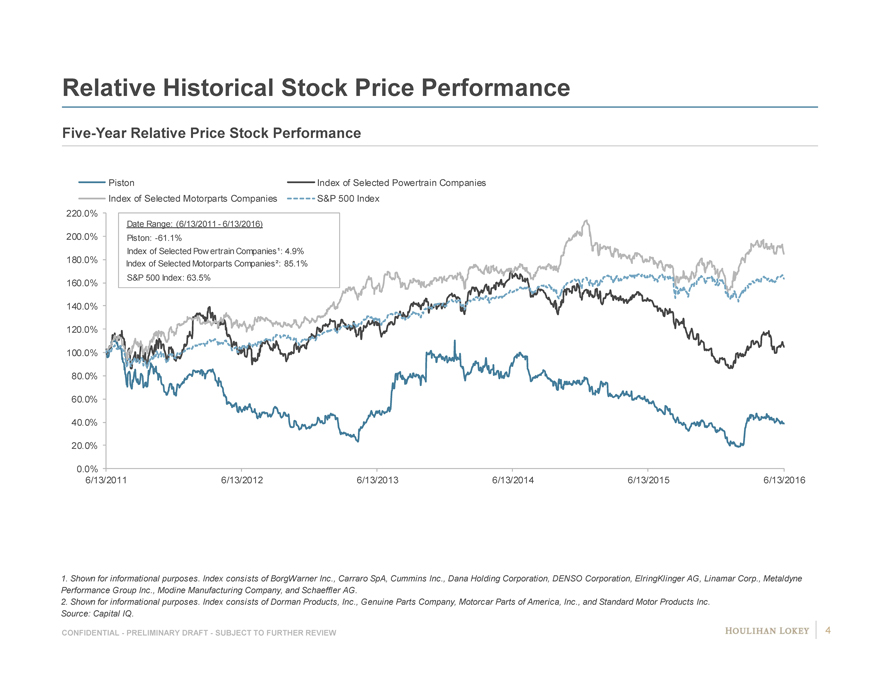

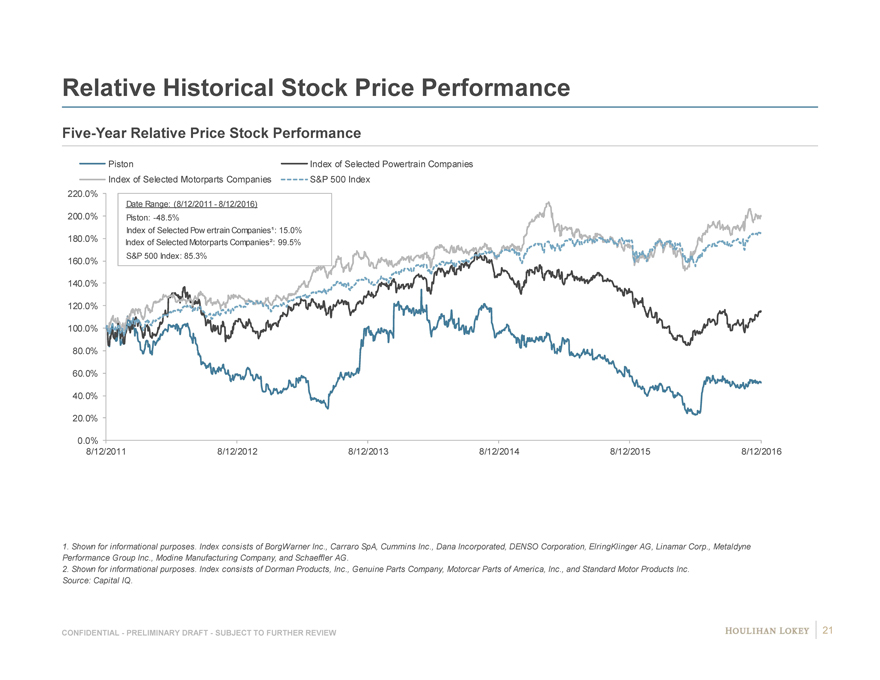

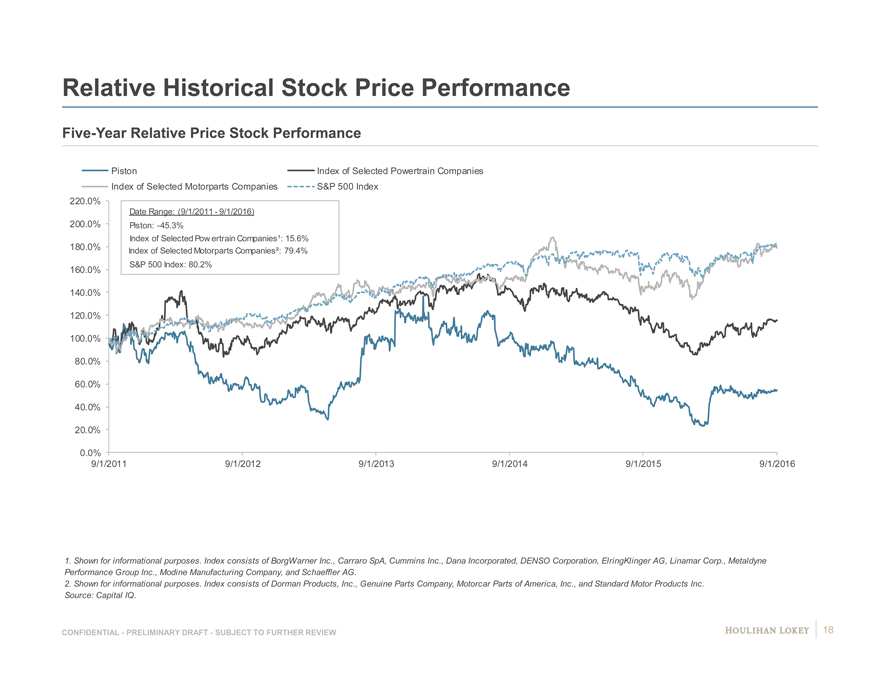

Relative Historical Stock Price Performance

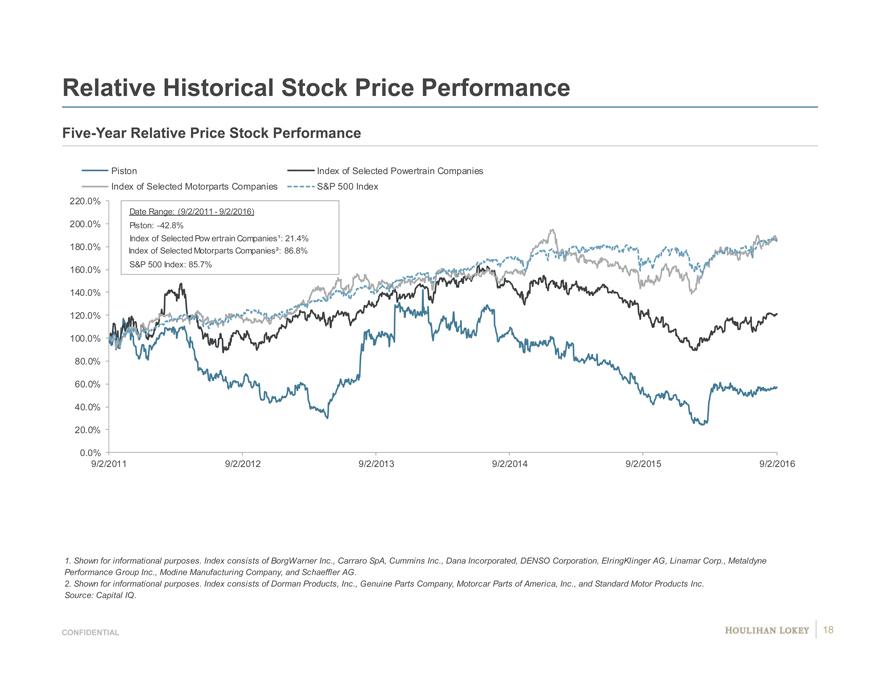

Five-Year Relative Price Stock Performance

Piston Index of Selected Powertrain Companies

Index of Selected Motorparts Companies S&P 500 Index

220.0%

Date Range: (6/13/2011—6/13/2016)

200.0% Piston: -61.1%

Index of Selected Pow ertrain Companies¹: 4.9%

180.0% Index of Selected Motorparts Companies²: 85.1%

160.0% S&P 500 Index: 63.5%

140.0%

120.0%

100.0%

80.0%

60.0%

40.0%

20.0%

0.0%

6/13/2011 6/13/2012 6/13/2013 6/13/2014 6/13/2015 6/13/2016

1. Shown for informational purposes. Index consists of BorgWarner Inc., Carraro SpA, Cummins Inc., Dana Holding Corporation, DENSO Corporation, ElringKlinger AG, Linamar Corp., Metaldyne Performance Group Inc., Modine Manufacturing Company, and Schaeffler AG.

2. Shown for informational purposes. Index consists of Dorman Products, Inc., Genuine Parts Company, Motorcar Parts of America, Inc., and Standard Motor Products Inc.

Source: Capital IQ.

CONFIDENTIAL—PRELIMINARY DRAFT—SUBJECT TO FURTHER REVIEW 4

|

|

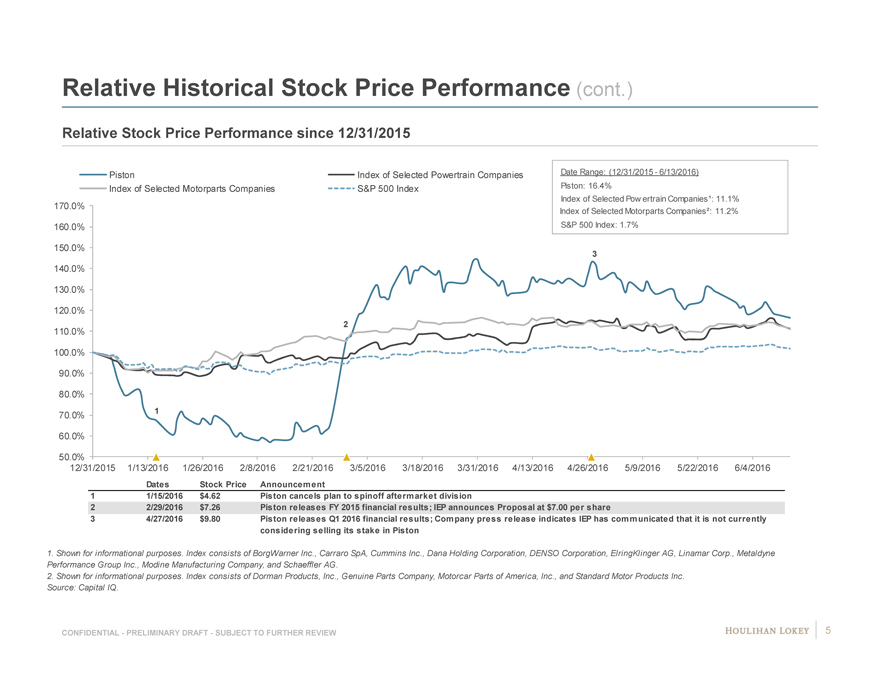

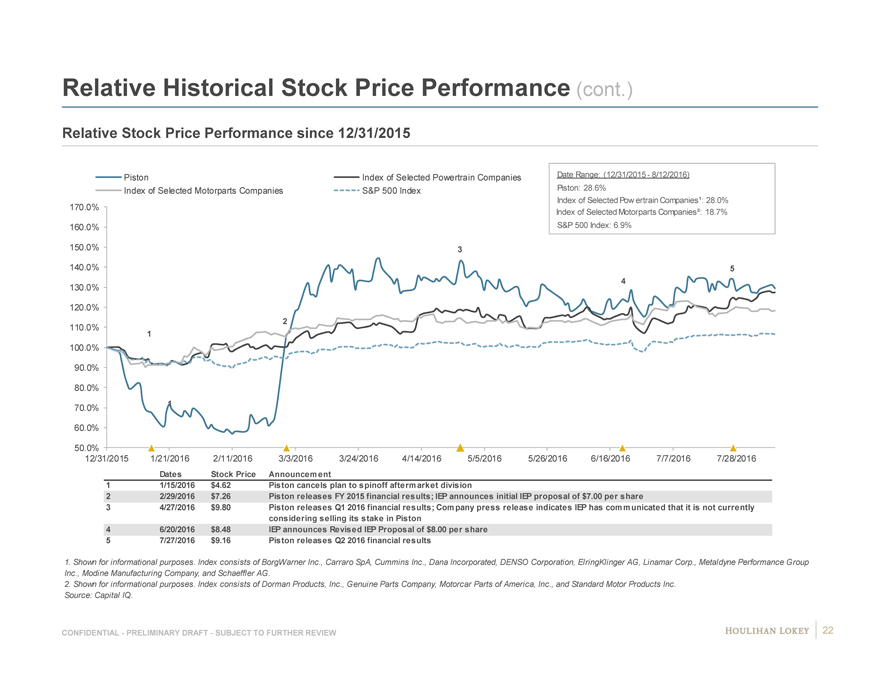

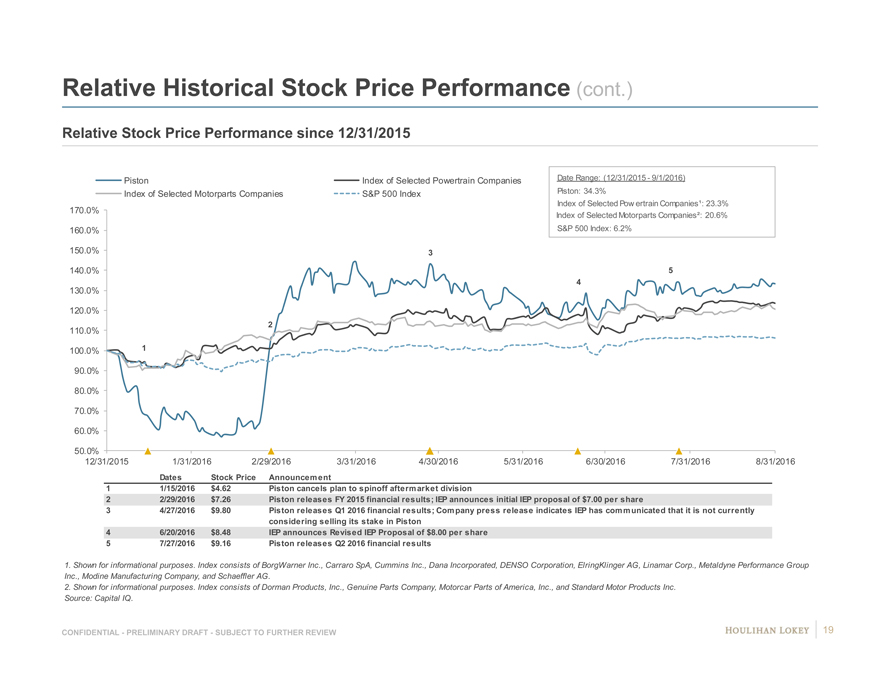

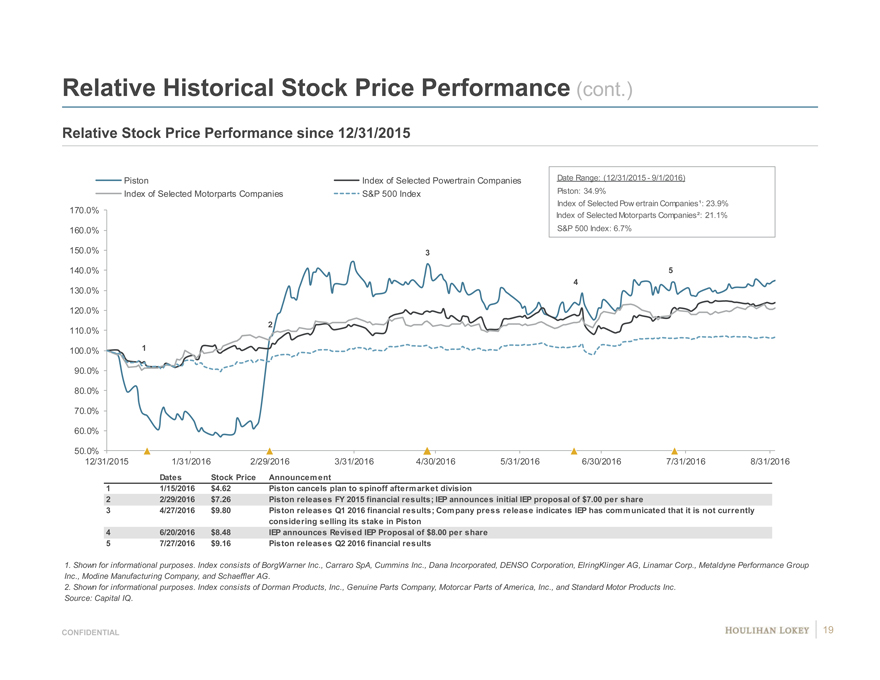

Relative Historical Stock Price Performance (cont.)

Relative Stock Price Performance since 12/31/2015

Piston Index of Selected Powertrain Companies Date Range: (12/31/2015—6/13/2016)

Index of Selected Motorparts Companies S&P 500 Index Piston: 16.4%

Index of Selected Pow ertrain Companies¹: 11.1%

170.0% Index of Selected Motorparts Companies²: 11.2%

160.0% S&P 500 Index: 1.7%

150.0%

3

140.0%

130.0%

120.0%

2

110.0%

100.0%

90.0%

80.0%

70.0% 1

60.0%

50.0%

12/31/2015 1/13/2016 1/26/2016 2/8/2016 2/21/2016 3/5/2016 3/18/2016 3/31/2016 4/13/2016 4/26/2016 5/9/2016 5/22/2016 6/4/2016

Dates Stock Price Announcement

1 1/15/2016 $4.62 Piston cancels plan to spinoff aftermarket division

2 2/29/2016 $7.26 Piston releases FY 2015 financial results; IEP announces Proposal at $7.00 per share

3 4/27/2016 $9.80 Piston releases Q1 2016 financial results; Company press release indicates IEP has communicated that it is not currently

considering selling its stake in Piston

1. Shown for informational purposes. Index consists of BorgWarner Inc., Carraro SpA, Cummins Inc., Dana Holding Corporation, DENSO Corporation, ElringKlinger AG, Linamar Corp., Metaldyne

Performance Group Inc., Modine Manufacturing Company, and Schaeffler AG.

2. Shown for informational purposes. Index consists of Dorman Products, Inc., Genuine Parts Company, Motorcar Parts of America, Inc., and Standard Motor Products Inc.

Source: Capital IQ.

CONFIDENTIAL—PRELIMINARY DRAFT—SUBJECT TO FURTHER REVIEW 5

|

|

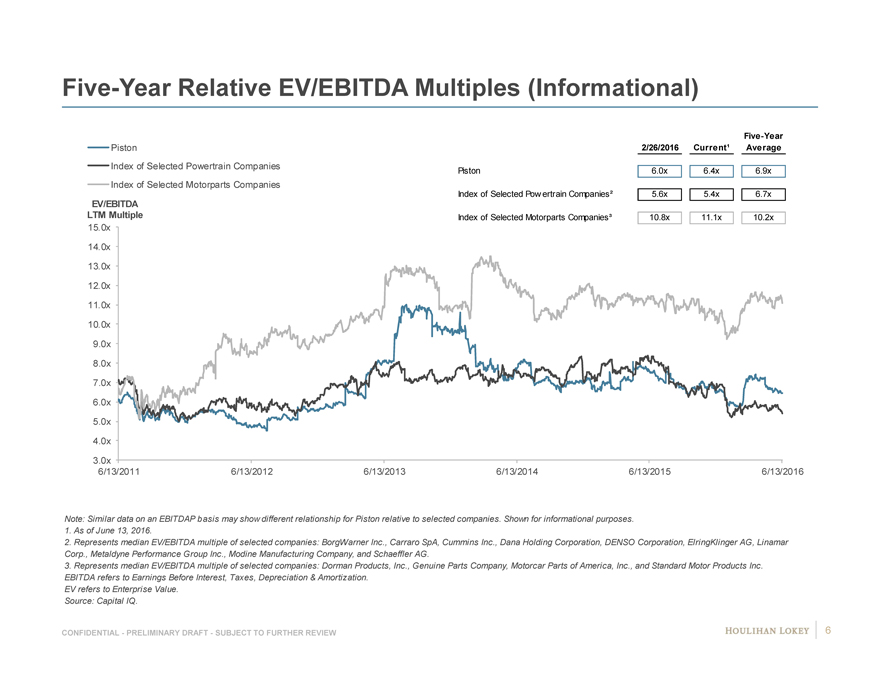

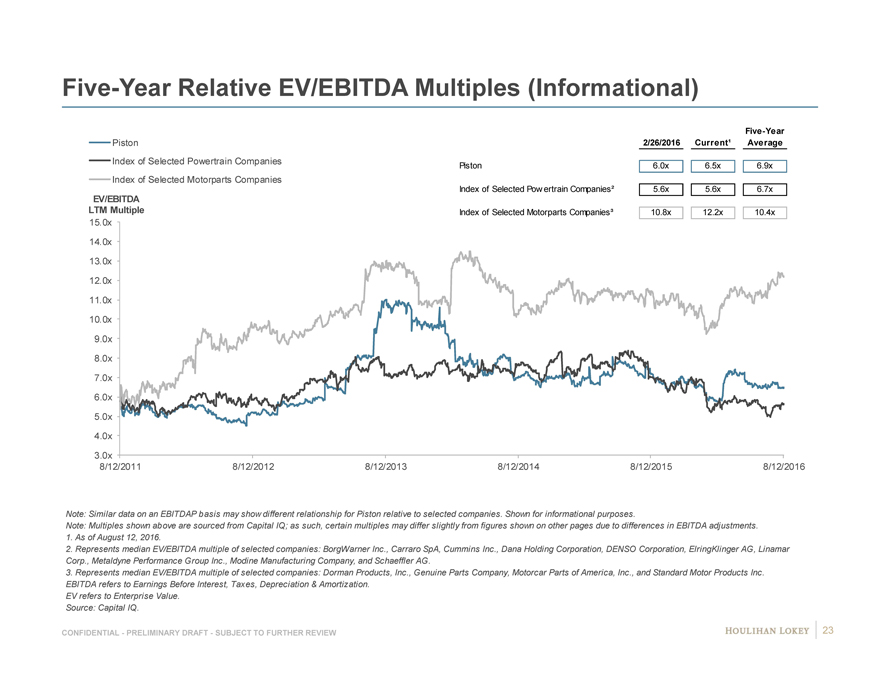

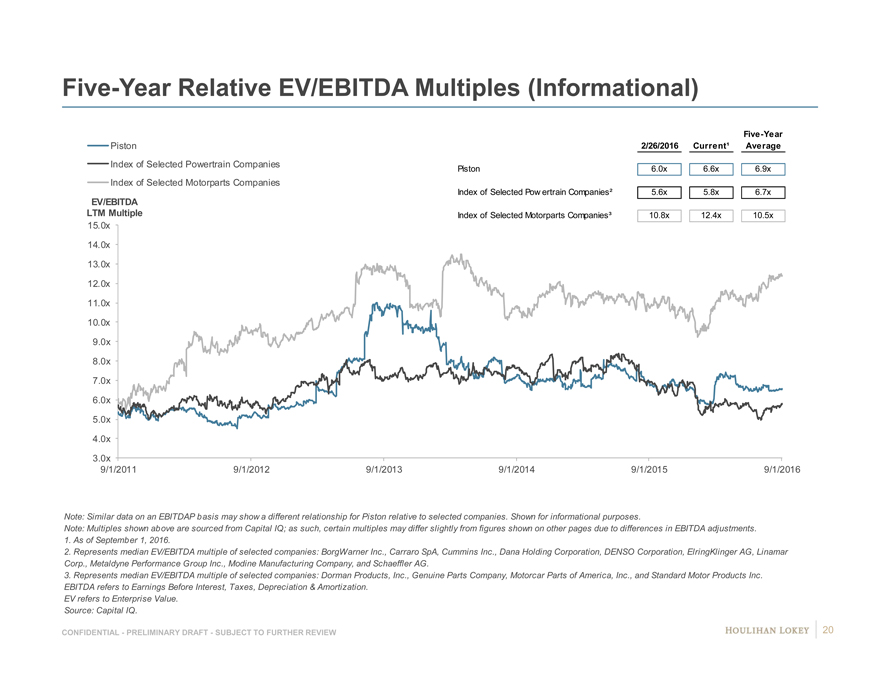

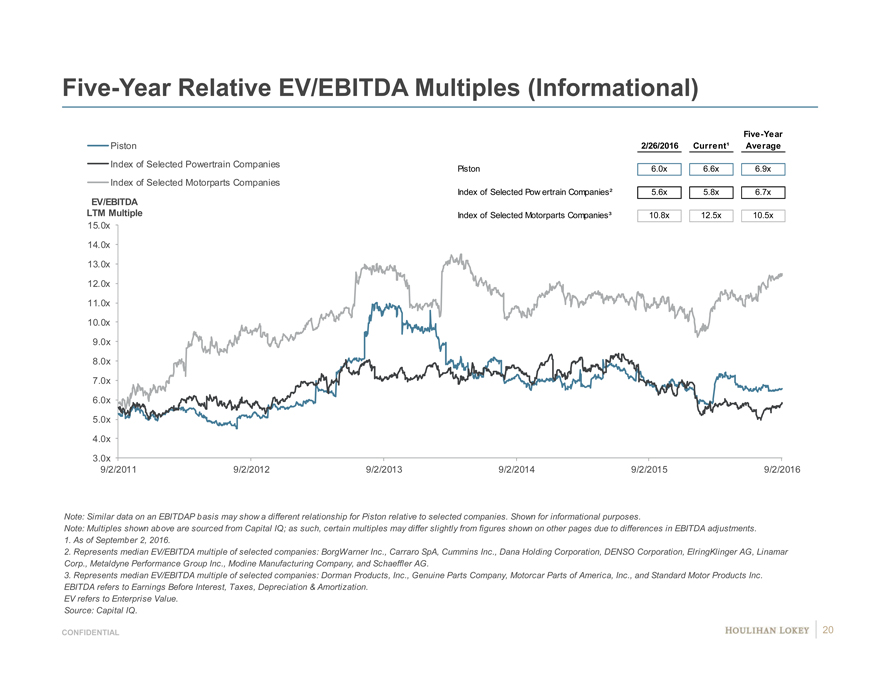

Five-Year Relative EV/EBITDA Multiples (Informational)

Five-Year

Piston 2/26/2016 Current¹ Average

Index of Selected Powertrain Companies Piston 6.0x 6.4x 6.9x

Index of Selected Motorparts Companies

Index of Selected Pow ertrain Companies² 5.6x 5.4x 6.7x

EV/EBITDA

LTM Multiple Index of Selected Motorparts Companies³ 10.8x 11.1x 10.2x

15.0x

14.0x

13.0x

12.0x

11.0x

10.0x

9.0x

8.0x

7.0x

6.0x

5.0x

4.0x

3.0x

6/13/2011 6/13/2012 6/13/2013 6/13/2014 6/13/2015 6/13/2016

Note: Similar data on an EBITDAP basis may show different relationship for Piston relative to selected companies. Shown for informational purposes.

1. As of June 13, 2016.

2. Represents median EV/EBITDA multiple of selected companies: BorgWarner Inc., Carraro SpA, Cummins Inc., Dana Holding Corporation, DENSO Corporation, ElringKlinger AG, Linamar

Corp., Metaldyne Performance Group Inc., Modine Manufacturing Company, and Schaeffler AG.

3. Represents median EV/EBITDA multiple of selected companies: Dorman Products, Inc., Genuine Parts Company, Motorcar Parts of America, Inc., and Standard Motor Products Inc.

EBITDA refers to Earnings Before Interest, Taxes, Depreciation & Amortization.

EV refers to Enterprise Value.

Source: Capital IQ.

CONFIDENTIAL—PRELIMINARY DRAFT—SUBJECT TO FURTHER REVIEW 6

|

|

Page

1. Selected Public Market Observations 3

2. Preliminary Financial Analyses 7

3. Appendix 17

4. Disclaimer 53

|

|

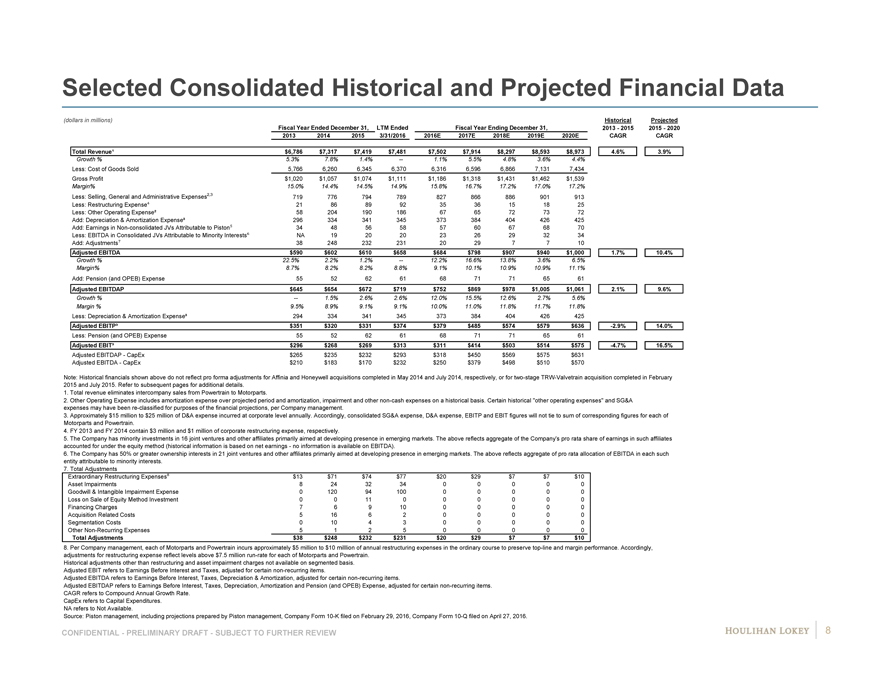

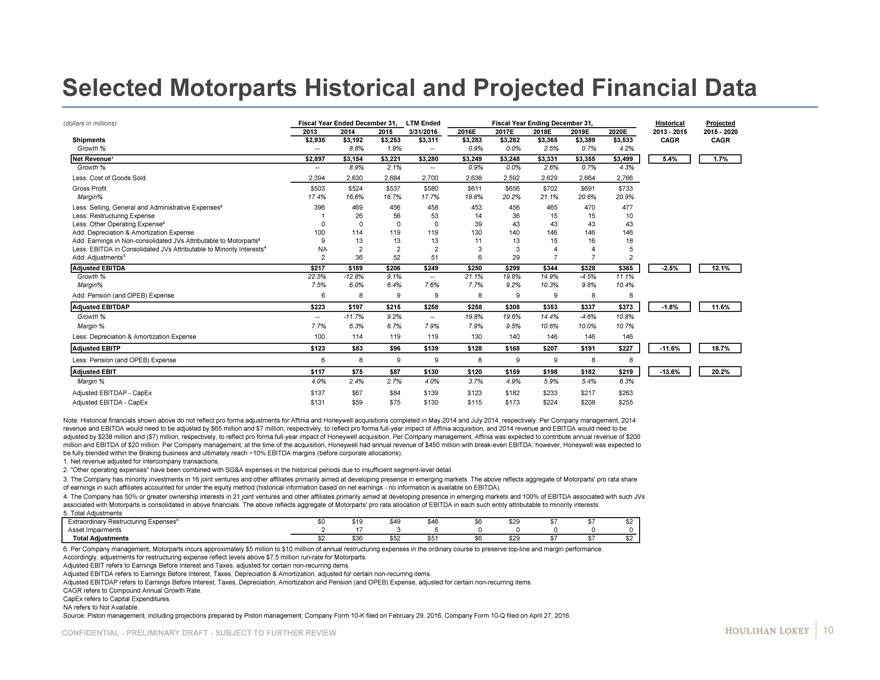

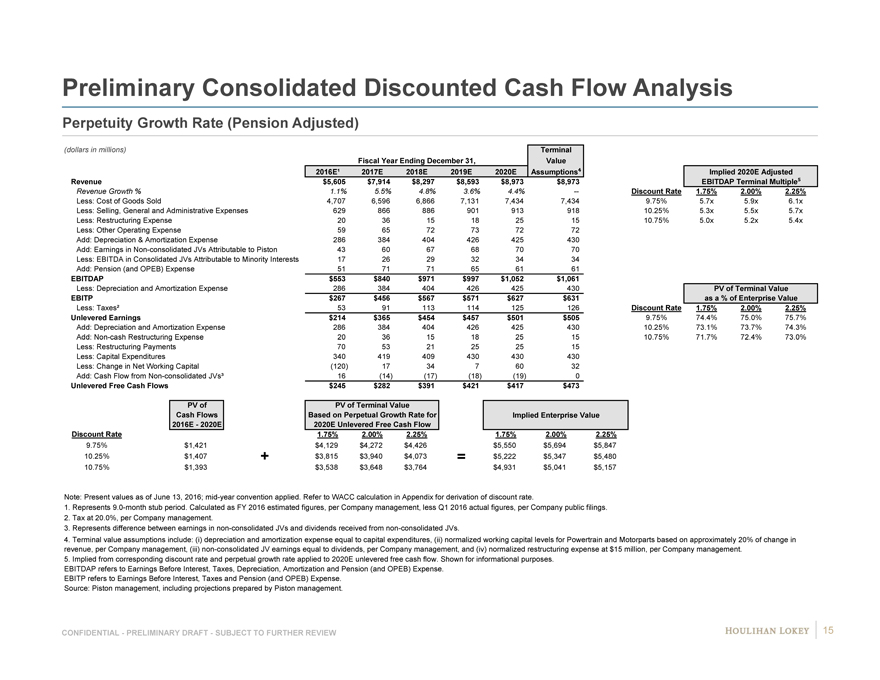

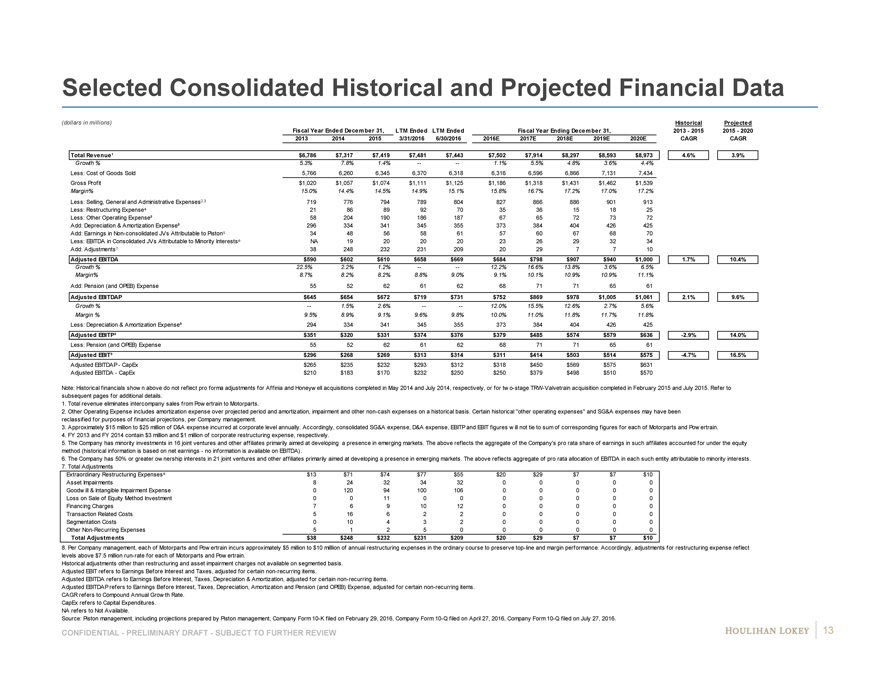

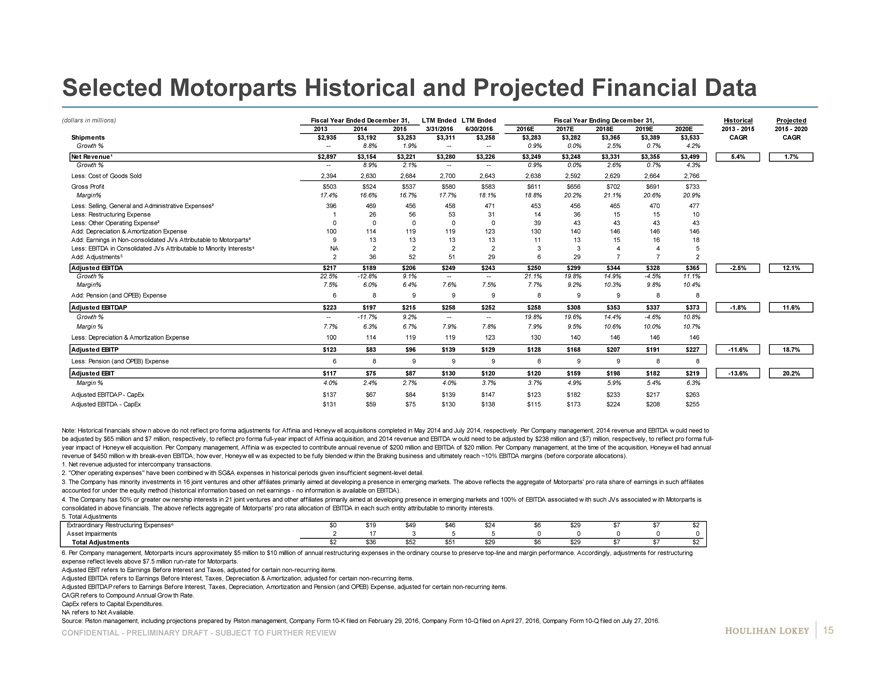

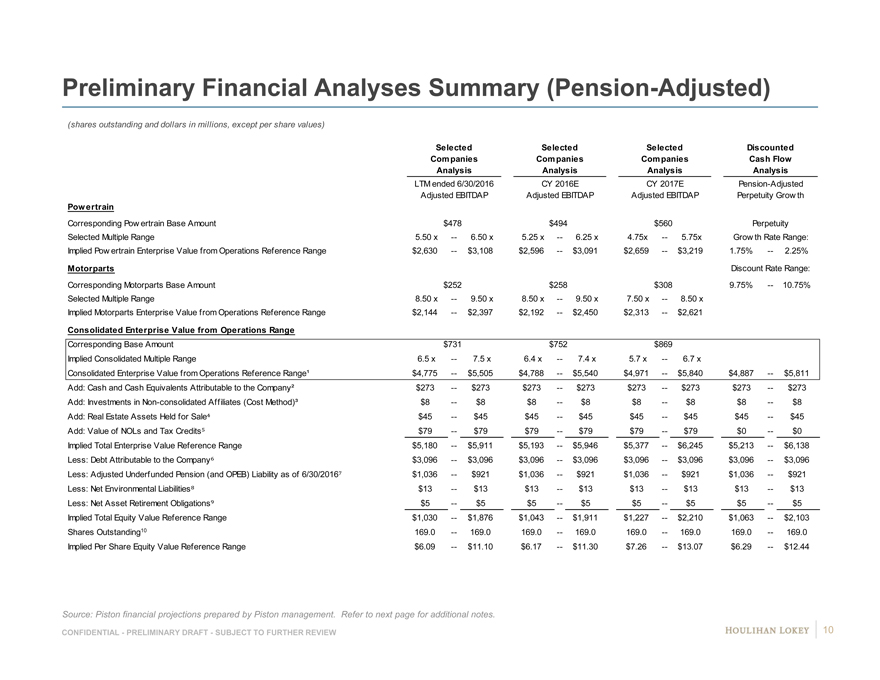

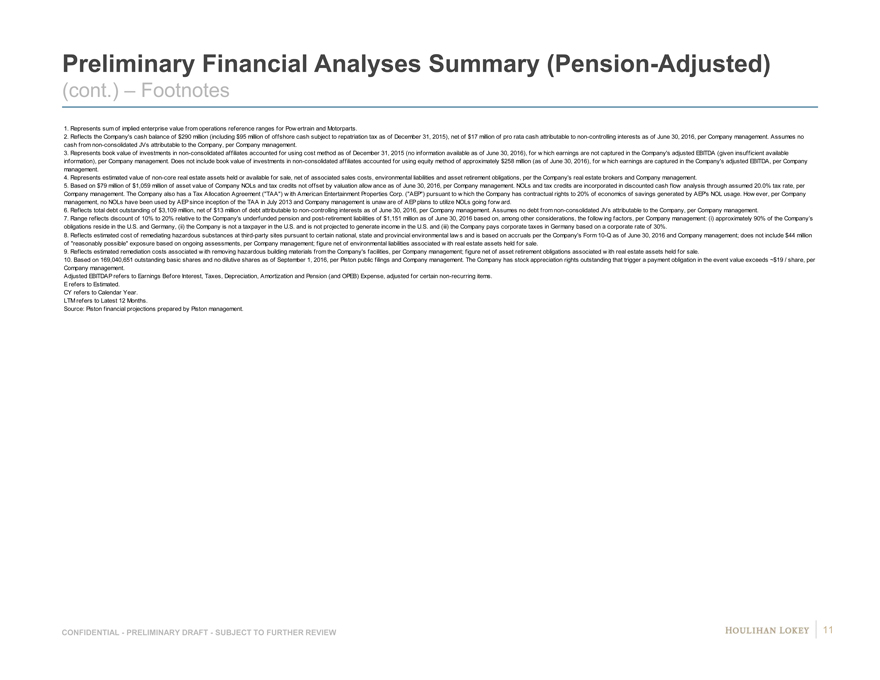

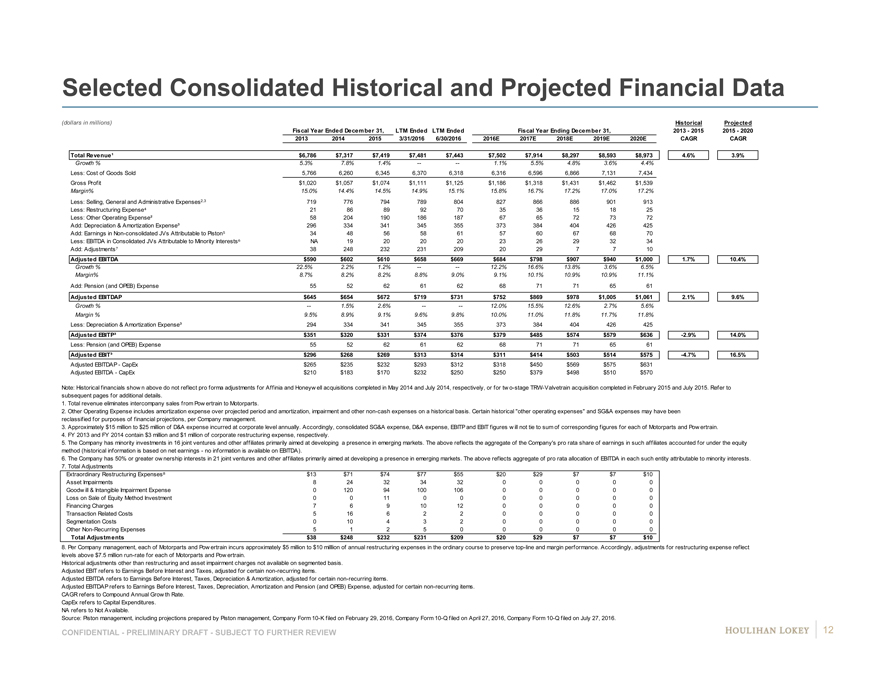

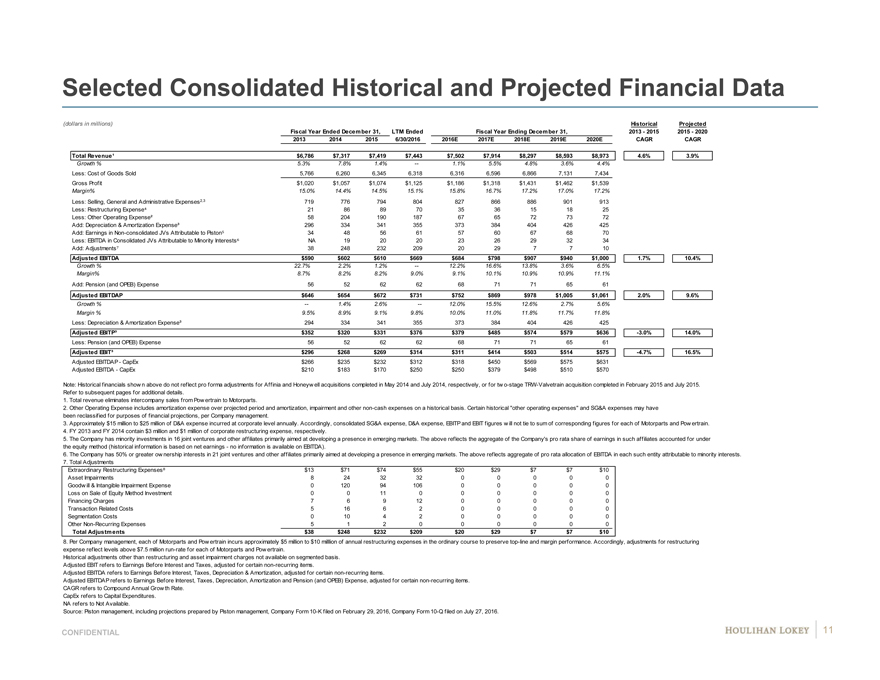

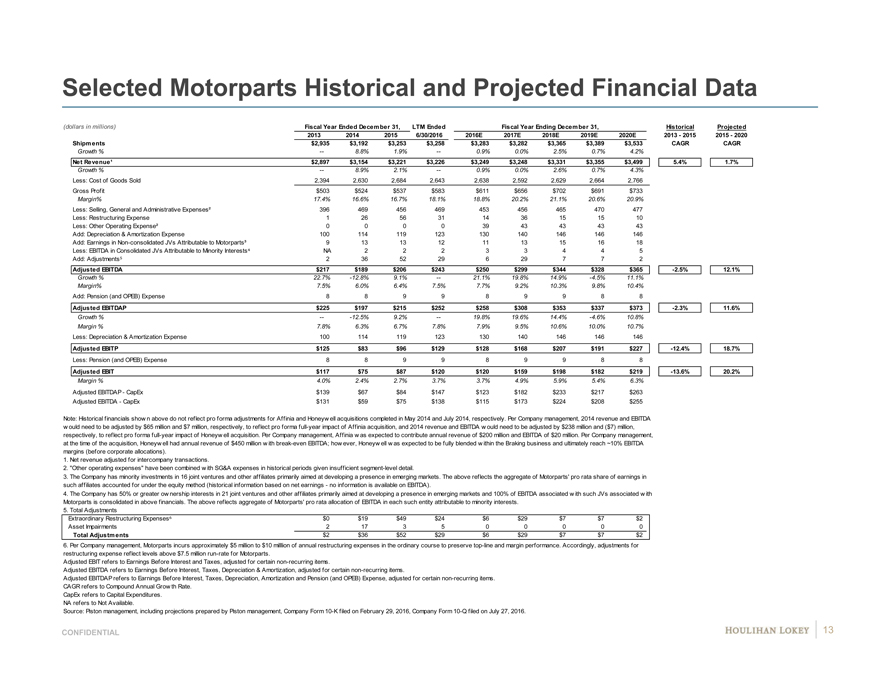

Selected Consolidated Historical and Projected Financial Data

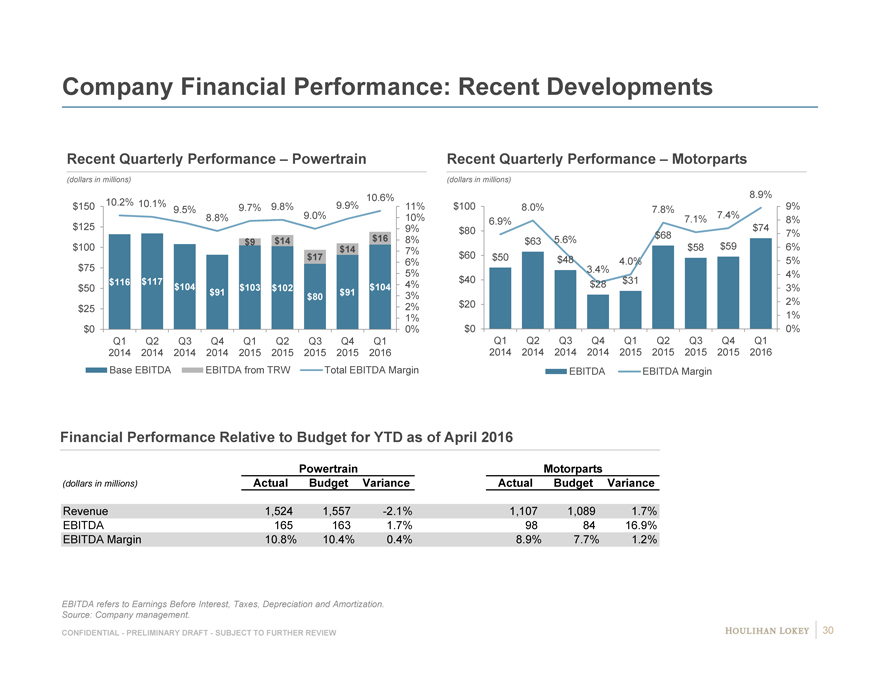

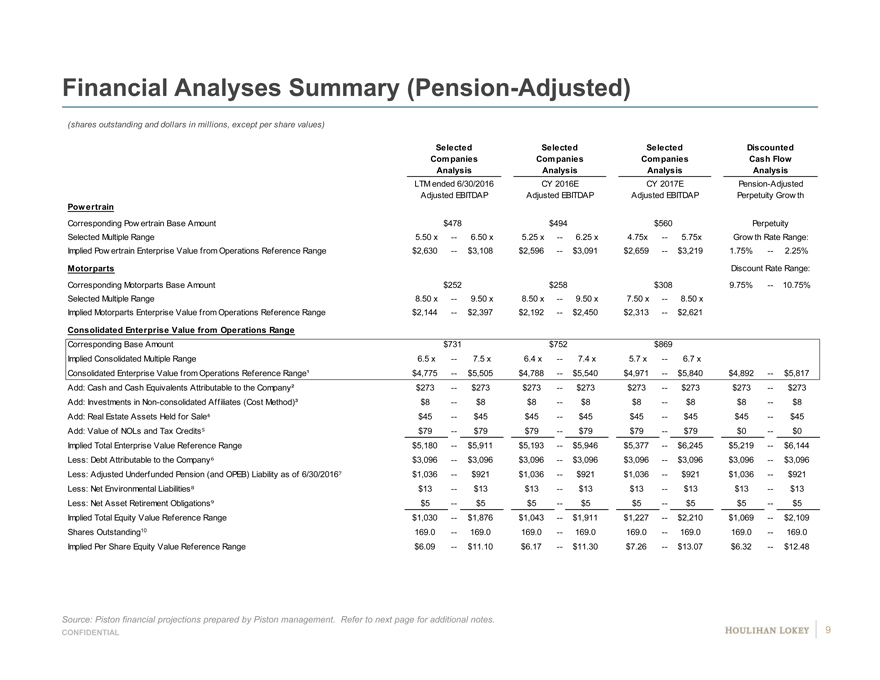

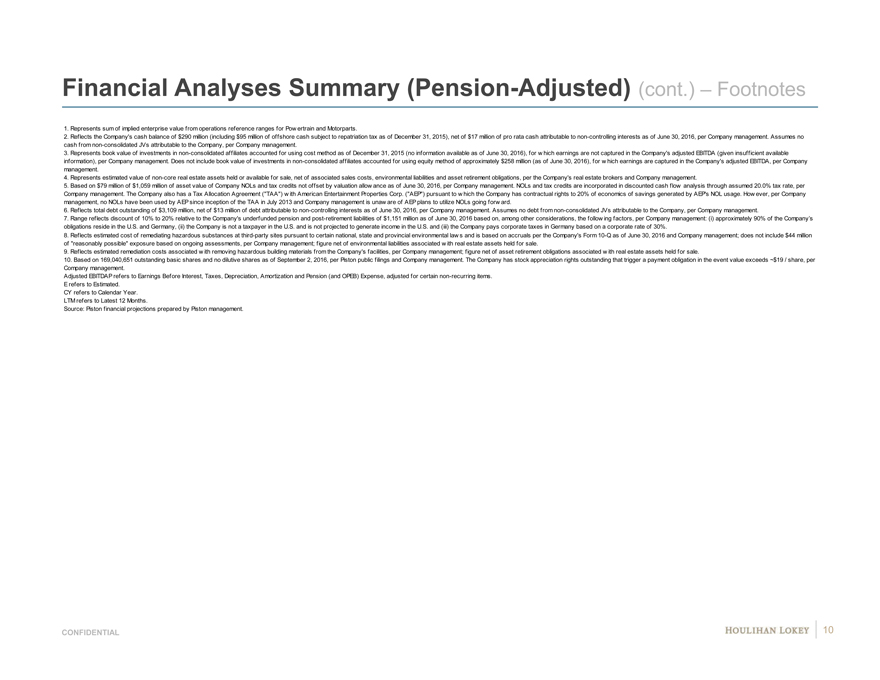

(dollars in millions) Historical Projected Fiscal Year Ended December 31, LTM Ended Fiscal Year Ending December 31, 2013—2015 2015—2020 2013 2014 2015 3/31/2016 2016E 2017E 2018E 2019E 2020E CAGR CAGR

Total Revenue¹ $6,786 $7,317 $7,419 $7,481 $7,502 $7,914 $8,297 $8,593 $8,973 4.6% 3.9%

Growth % 5.3% 7.8% 1.4% — 1.1% 5.5% 4.8% 3.6% 4.4%

Less: Cost of Goods Sold 5,766 6,260 6,345 6,370 6,316 6,596 6,866 7,131 7,434 Gross Profit $1,020 $1,057 $1,074 $1,111 $1,186 $1,318 $1,431 $1,462 $1,539

Margin% 15.0% 14.4% 14.5% 14.9% 15.8% 16.7% 17.2% 17.0% 17.2%

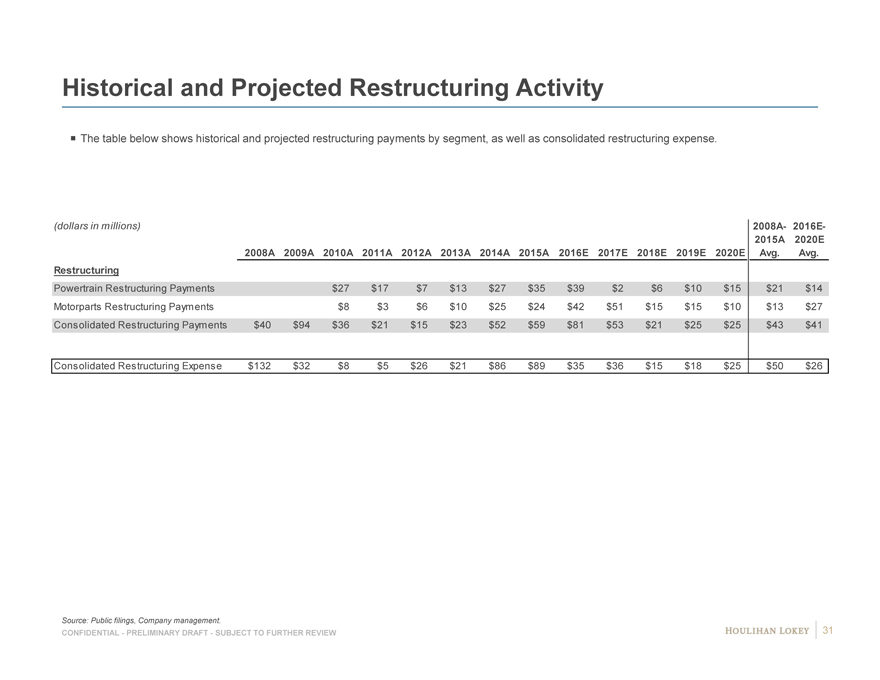

Less: Selling, General and Administrative Expenses2,3 719 776 794 789 827 866 886 901 913 Less: Restructuring Expense 21 86 89 92 35 36 15 18 25 Less: Other Operating Expense² 58 204 190 186 67 65 72 73 72 Add: Depreciation & Amortization Expense³ 296 334 341 345 373 384 404 426 425 Add: Earnings in Non-consolidated JVs Attributable to Piston 34 48 56 58 57 60 67 68 70 Less: EBITDA in Consolidated JVs Attributable to Minority Interests NA 19 20 20 23 26 29 32 34 Add: Adjustments 38 248 232 231 20 29 7 7 10

Adjusted EBITDA $590 $602 $610 $658 $684 $798 $907 $940 $1,000 1.7% 10.4%

Growth % 22.5% 2.2% 1.2% — 12.2% 16.6% 13.8% 3.6% 6.5% Margin% 8.7% 8.2% 8.2% 8.8% 9.1% 10.1% 10.9% 10.9% 11.1%

Add: Pension (and OPEB) Expense 55 52 62 61 68 71 71 65 61

Adjusted EBITDAP $645 $654 $672 $719 $752 $869 $978 $1,005 $1,061 2.1% 9.6%

Growth % — 1.5% 2.6% 2.6% 12.0% 15.5% 12.6% 2.7% 5.6% Margin % 9.5% 8.9% 9.1% 9.1% 10.0% 11.0% 11.8% 11.7% 11.8%

Less: Depreciation & Amortization Expense³ 294 334 341 345 373 384 404 426 425

Adjusted EBITP³ $351 $320 $331 $374 $379 $485 $574 $579 $636 -2.9% 14.0%

Less: Pension (and OPEB) Expense 55 52 62 61 68 71 71 65 61

Adjusted EBIT³ $296 $268 $269 $313 $311 $414 $503 $514 $575 -4.7% 16.5%

Adjusted EBITDAP—CapEx $265 $235 $232 $293 $318 $450 $569 $575 $631 Adjusted EBITDA—CapEx $210 $183 $170 $232 $250 $379 $498 $510 $570

Note: Historical financials shown above do not reflect pro forma adjustments for Affinia and Honeywell acquisitions completed in May 2014 and July 2014, respectively, or for two-stage TRW-Valvetrain acquisition completed in February 2015 and July 2015. Refer to subsequent pages for additional details.

1. Total revenue eliminates intercompany sales from Powertrain to Motorparts.

2. Other Operating Expense includes amortization expense over projected period and amortization, impairment and other non-cash expenses on a historical basis. Certain historical “other operating expenses” and SG&A expenses may have been re-classified for purposes of the financial projections, per Company management.

3. Approximately $15 million to $25 million of D&A expense incurred at corporate level annually. Accordingly, consolidated SG&A expense, D&A expense, EBITP and EBIT figures will not tie to sum of corresponding figures for each of Motorparts and Powertrain.

4. FY 2013 and FY 2014 contain $3 million and $1 million of corporate restructuring expense, respectively.

5. The Company has minority investments in 16 joint ventures and other affiliates primarily aimed at developing presence in emerging markets. The above reflects aggregate of the Company’s pro rata share of earnings in such affiliates accounted for under the equity method (historical information is based on net earnings—no information is available on EBITDA).

6. The Company has 50% or greater ownership interests in 21 joint ventures and other affiliates primarily aimed at developing presence in emerging markets. The above reflects aggregate of pro rata allocation of EBITDA in each such entity attributable to minority interests.

7. Total Adjustments

Extraordinary Restructuring Expenses $13 $71 $74 $77 $20 $29 $7 $7 $10 Asset Impairments 8 24 32 34 0 0 0 0 0 Goodwill & Intangible Impairment Expense 0 120 94 100 0 0 0 0 0 Loss on Sale of Equity Method Investment 0 0 11 0 0 0 0 0 0 Financing Charges 7 6 9 10 0 0 0 0 0 Acquisition Related Costs 5 16 6 2 0 0 0 0 0 Segmentation Costs 0 10 4 3 0 0 0 0 0 Other Non-Recurring Expenses 5 1 2 5 0 0 0 0 0

Total Adjustments $38 $248 $232 $231 $20 $29 $7 $7 $10

8. Per Company management, each of Motorparts and Powertrain incurs approximately $5 million to $10 milllion of annual restructuring expenses in the ordinary course to preserve top-line and margin performance. Accordingly, adjustments for restructuring expense reflect levels above $7.5 million run-rate for each of Motorparts and Powertrain.

Historical adjustments other than restructuring and asset impairment charges not available on segmented basis. Adjusted EBIT refers to Earnings Before Interest and Taxes, adjusted for certain non-recurring items.

Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation & Amortization, adjusted for certain non-recurring items.

Adjusted EBITDAP refers to Earnings Before Interest, Taxes, Depreciation, Amortization and Pension (and OPEB) Expense, adjusted for certain non-recurring items. CAGR refers to Compound Annual Growth Rate.

CapEx refers to Capital Expenditures. NA refers to Not Available.

Source: Piston management, including projections prepared by Piston management, Company Form 10-K filed on February 29, 2016, Company Form 10-Q filed on April 27, 2016.

CONFIDENTIAL—PRELIMINARY DRAFT—SUBJECT TO FURTHER REVIEW 8

|

|

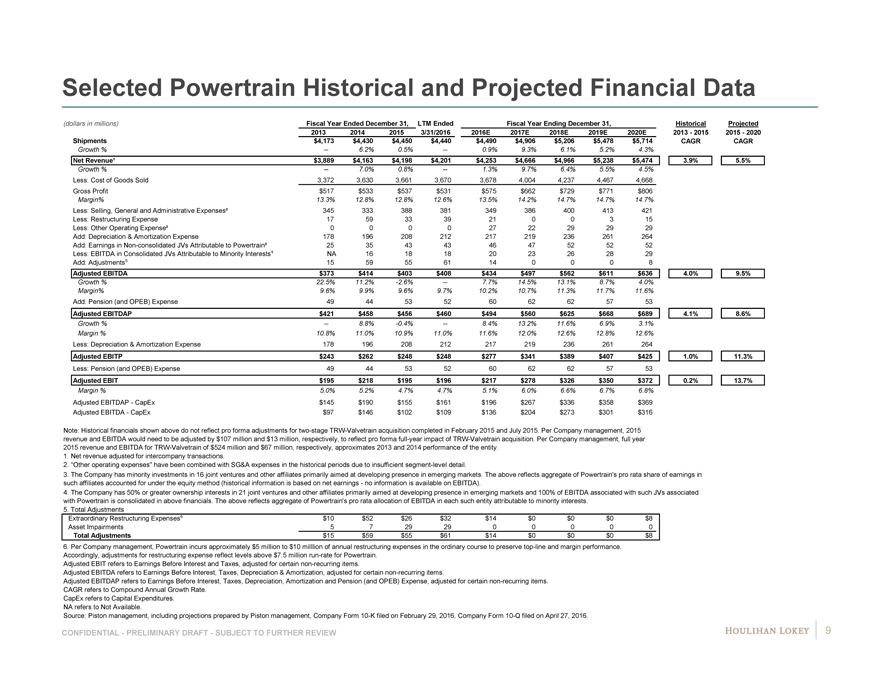

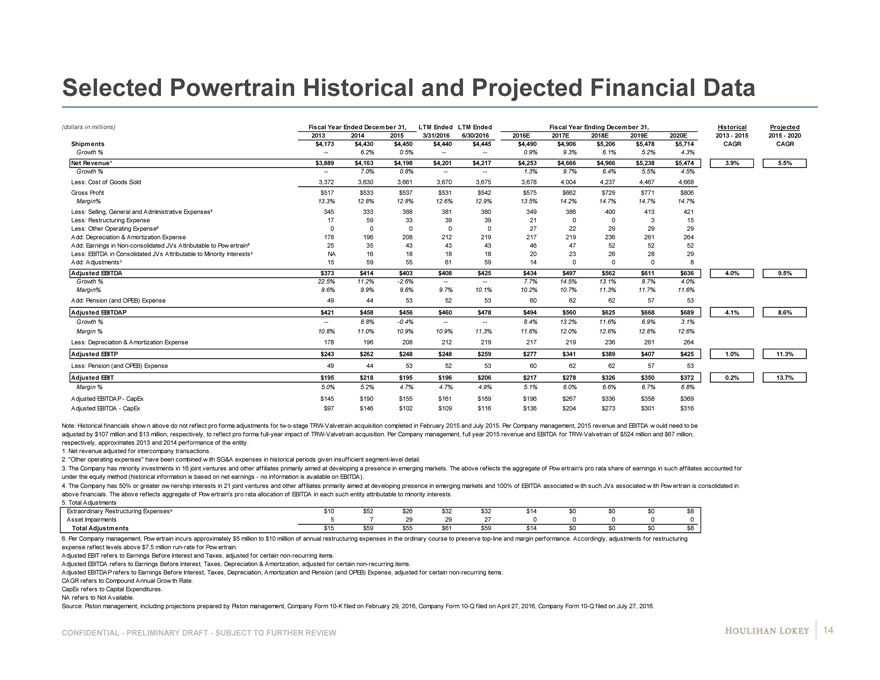

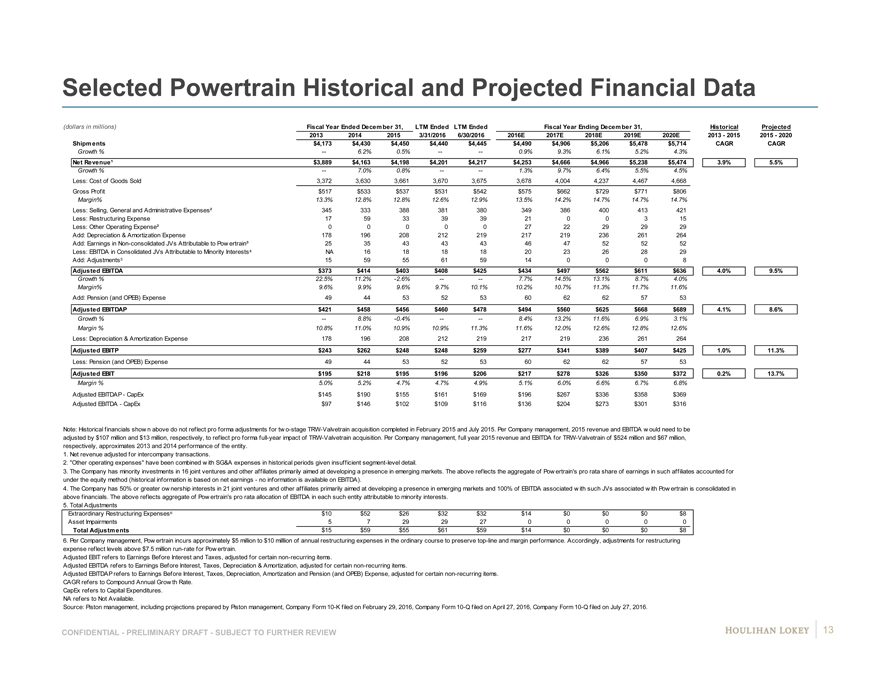

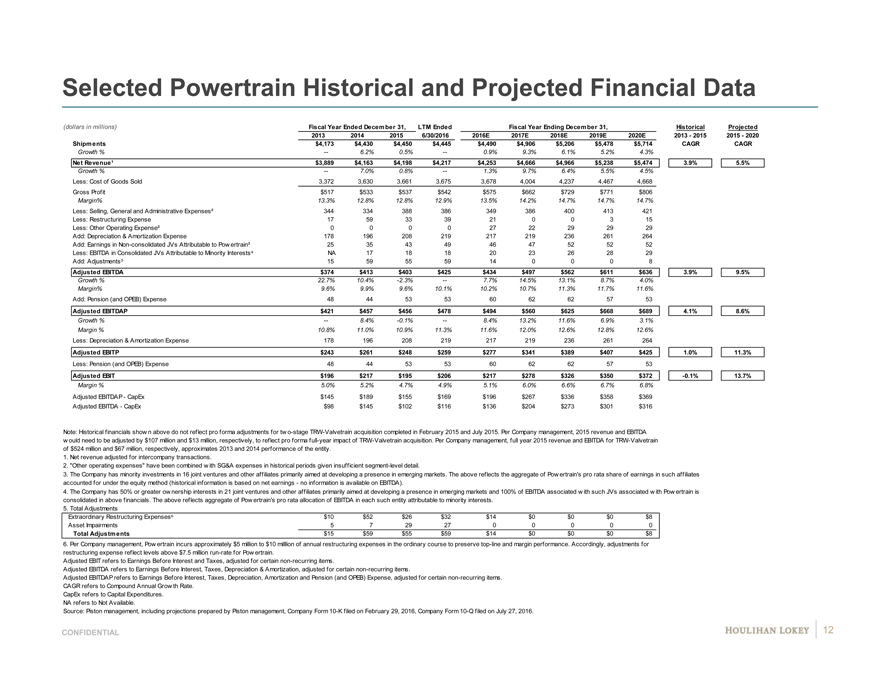

Selected Powertrain Historical and Projected Financial Data

(dollars in millions) Fiscal Year Ended December 31, LTM Ended Fiscal Year Ending December 31, Historical Projected

2013 2014 2015 3/31/2016 2016E 2017E 2018E 2019E 2020E 2013—2015 2015—2020

Shipments $4,173 $4,430 $4,450 $4,440 $4,490 $4,906 $5,206 $5,478 $5,714 CAGR CAGR

Growth % — 6.2% 0.5% — 0.9% 9.3% 6.1% 5.2% 4.3%

Net Revenue¹ $3,889 $4,163 $4,198 $4,201 $4,253 $4,666 $4,966 $5,238 $5,474 3.9% 5.5%

Growth % — 7.0% 0.8% — 1.3% 9.7% 6.4% 5.5% 4.5%

Less: Cost of Goods Sold 3,372 3,630 3,661 3,670 3,678 4,004 4,237 4,467 4,668

Gross Profit $517 $533 $537 $531 $575 $662 $729 $771 $806

Margin% 13.3% 12.8% 12.8% 12.6% 13.5% 14.2% 14.7% 14.7% 14.7%

Less: Selling, General and Administrative Expenses² 345 333 388 381 349 386 400 413 421

Less: Restructuring Expense 17 59 33 39 21 0 0 3 15

Less: Other Operating Expense² 0 0 0 0 27 22 29 29 29

Add: Depreciation & Amortization Expense 178 196 208 212 217 219 236 261 264

Add: Earnings in Non-consolidated JVs Attributable to Powertrain³ 25 35 43 43 46 47 52 52 52

Less: EBITDA in Consolidated JVs Attributable to Minority Interests NA 16 18 18 20 23 26 28 29

Add: Adjustments 15 59 55 61 14 0 0 0 8

Adjusted EBITDA $373 $414 $403 $408 $434 $497 $562 $611 $636 4.0% 9.5%

Growth % 22.5% 11.2% -2.6% — 7.7% 14.5% 13.1% 8.7% 4.0%

Margin% 9.6% 9.9% 9.6% 9.7% 10.2% 10.7% 11.3% 11.7% 11.6%

Add: Pension (and OPEB) Expense 49 44 53 52 60 62 62 57 53

Adjusted EBITDAP $421 $458 $456 $460 $494 $560 $625 $668 $689 4.1% 8.6%

Growth % — 8.8% -0.4% — 8.4% 13.2% 11.6% 6.9% 3.1%

Margin % 10.8% 11.0% 10.9% 11.0% 11.6% 12.0% 12.6% 12.8% 12.6%

Less: Depreciation & Amortization Expense 178 196 208 212 217 219 236 261 264

Adjusted EBITP $243 $262 $248 $248 $277 $341 $389 $407 $425 1.0% 11.3%