Form DFAN14A TICC Capital Corp. Filed by: TPG Specialty Lending, Inc.

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant ¨ Filed by a Party other than the Registrant x

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to §240.14a-12 | |

TICC CAPITAL CORP.

(Name of Registrant as Specified In Its Charter)

TPG Specialty Lending, Inc.

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | Fee not required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

TPG Specialty Lending, Inc., together with the other participants named herein (collectively, “TSLX”), has filed a definitive proxy statement and an accompanying GOLD proxy card with the Securities and Exchange Commission (the “SEC”) to be used to solicit votes from the stockholders of TICC Capital Corp. (“TICC”) to: (a) elect TSLX’s director nominee at TICC’s 2016 annual meeting of stockholders and (b) approve a proposal to terminate the Investment Advisory Agreement, dated as of July 1, 2011, by and between TICC and TICC Management, LLC, as contemplated by Section 15(a) of the Investment Company Act of 1940, as amended.

As part of the above-referenced solicitation, TSLX updated certain pages of its website, http://www.changeticcnow.com/, a website established by TSLX that contains information regarding the solicitation. This Schedule 14A filing consists of the following screenshots, which reflect the content of pages not previously filed with the SEC.

|

|

Toggle navigation TPG Specialty Lending

News & Filings

Presentations

Nominee

How to Vote

About TPG Specialty Lending

Contact

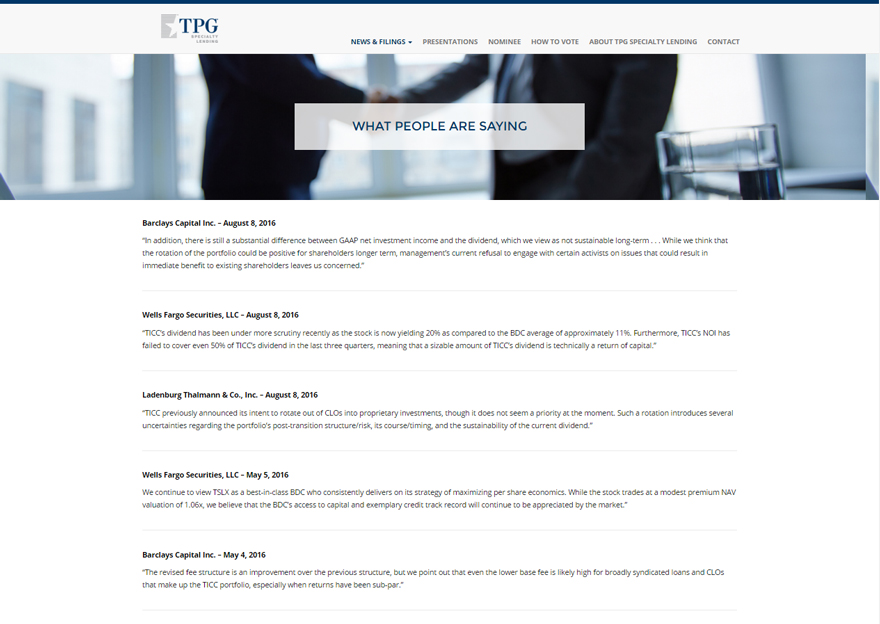

WHAT PEOPLE ARE SAYING

Barclays Capital Inc. – August 8, 2016

“In addition, there is still a substantial difference between GAAP net investment income and the dividend, which we view as not sustainable long-term . . . While we think that the rotation of the portfolio could be positive for shareholders longer term, management’s current refusal to engage with certain activists on issues that could result in immediate benefit to existing shareholders leaves us concerned.”

Wells Fargo Securities, LLC – August 8, 2016

“TICC’s dividend has been under more scrutiny recently as the stock is now yielding 20% as compared to the BDC average of approximately 11%. Furthermore, TICC’s NOI has failed to cover even 50% of TICC’s dividend in the last three quarters, meaning that a sizable amount of TICC’s dividend is technically a return of capital.”

Ladenburg Thalmann & Co., Inc. – August 8, 2016

“TICC previously announced its intent to rotate out of CLOs into proprietary investments, though it does not seem a priority at the moment. Such a rotation introduces several uncertainties regarding the portfolio’s post-transition structure/risk, its course/timing, and the sustainability of the current dividend.”

Wells Fargo Securities, LLC – May 5, 2016

We continue to view TSLX as a best-in-class BDC who consistently delivers on its strategy of maximizing per share economics. While the stock trades at a modest premium NAV valuation of 1.06x, we believe that the BDC’s access to capital and exemplary credit track record will continue to be appreciated by the market.”

Barclays Capital Inc. – May 4, 2016

“The revised fee structure is an improvement over the previous structure, but we point out that even the lower base fee is likely high for broadly syndicated loans and CLOs that make up the TICC portfolio, especially when returns have been sub-par.”

|

|

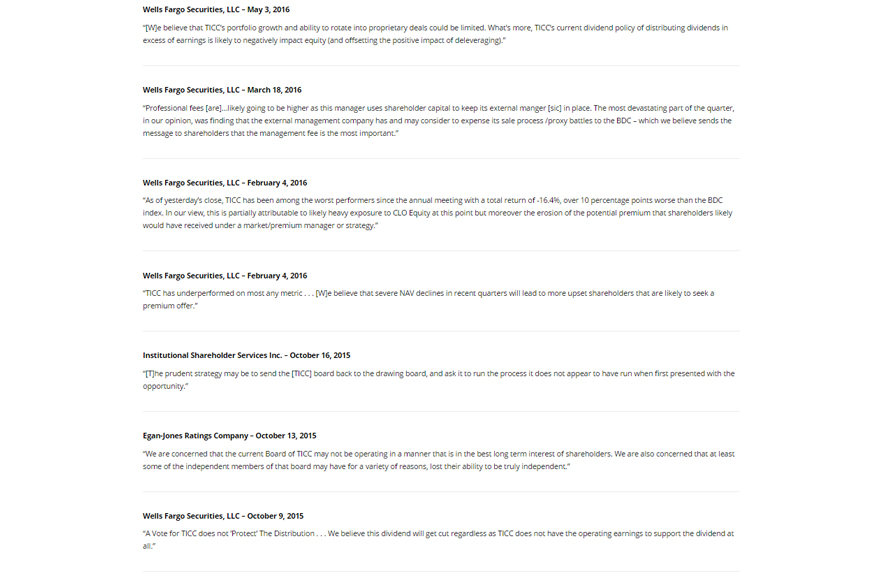

Wells Fargo Securities, LLC – May 3, 2016

“[W]e believe that TICC’s portfolio growth and ability to rotate into proprietary deals could be limited. What’s more, TICC’s current dividend policy of distributing dividends in excess of earnings is likely to negatively impact equity (and offsetting the positive impact of deleveraging).”

Wells Fargo Securities, LLC – March 18, 2016

“Professional fees [are]…likely going to be higher as this manager uses shareholder capital to keep its external manger [sic] in place. The most devastating part of the quarter, in our opinion, was finding that the external management company has and may consider to expense its sale process /proxy battles to the BDC – which we believe sends the message to shareholders that the management fee is the most important.”

Wells Fargo Securities, LLC – February 4, 2016

“As of yesterday’s close, TICC has been among the worst performers since the annual meeting with a total return of -16.4%, over 10 percentage points worse than the BDC index. In our view, this is partially attributable to likely heavy exposure to CLO Equity at this point but moreover the erosion of the potential premium that shareholders likely would have received under a market/premium manager or strategy.”

Wells Fargo Securities, LLC – February 4, 2016

“TICC has underperformed on most any metric . . . [W]e believe that severe NAV declines in recent quarters will lead to more upset shareholders that are likely to seek a premium offer.”

Institutional Shareholder Services Inc. – October 16, 2015

“[T]he prudent strategy may be to send the [TICC] board back to the drawing board, and ask it to run the process it does not appear to have run when first presented with the opportunity.”

Egan-Jones Ratings Company – October 13, 2015

“We are concerned that the current Board of TICC may not be operating in a manner that is in the best long term interest of shareholders. We are also concerned that at least some of the independent members of that board may have for a variety of reasons, lost their ability to be truly independent.”

Wells Fargo Securities, LLC – October 9, 2015

“A Vote for TICC does not ’Protect’ The Distribution . . . We believe this dividend will get cut regardless as TICC does not have the operating earnings to support the dividend at all.”

|

|

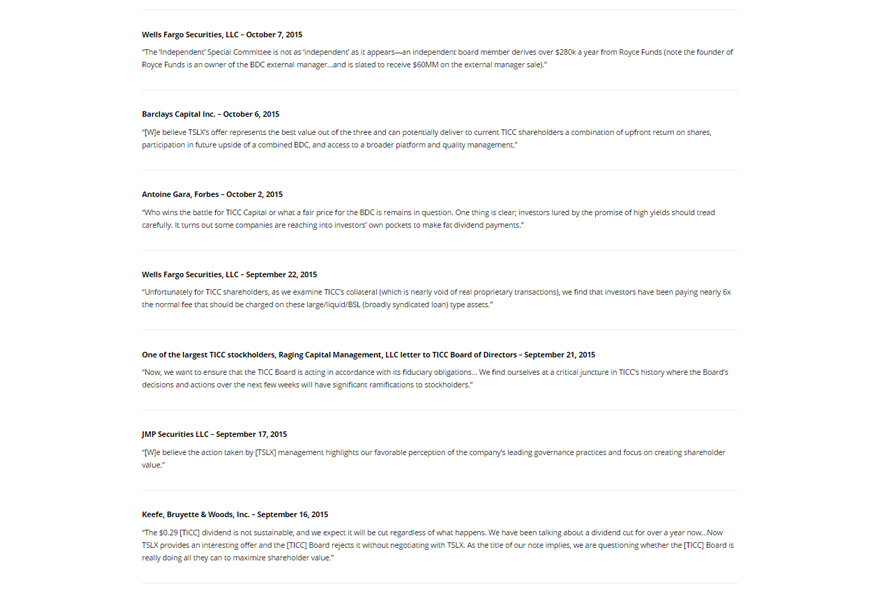

Wells Fargo Securities, LLC – October 7, 2015

“The ’Independent’ Special Committee is not as ‘independent’ as it appears—an independent board member derives over $280k a year from Royce Funds (note the founder of Royce Funds is an owner of the BDC external manager…and is slated to receive $60MM on the external manager sale).”

Barclays Capital Inc. – October 6, 2015

“[W]e believe TSLX’s offer represents the best value out of the three and can potentially deliver to current TICC shareholders a combination of upfront return on shares, participation in future upside of a combined BDC, and access to a broader platform and quality management.”

Antoine Gara, Forbes – October 2, 2015

“Who wins the battle for TICC Capital or what a fair price for the BDC is remains in question. One thing is clear; investors lured by the promise of high yields should tread carefully. It turns out some companies are reaching into investors’ own pockets to make fat dividend payments.”

Wells Fargo Securities, LLC – September 22, 2015

“Unfortunately for TICC shareholders, as we examine TICC’s collateral (which is nearly void of real proprietary transactions), we find that investors have been paying nearly 6x the normal fee that should be charged on these large/liquid/BSL (broadly syndicated loan) type assets.”

One of the largest TICC stockholders, Raging Capital Management, LLC letter to TICC Board of Directors – September 21, 2015

“Now, we want to ensure that the TICC Board is acting in accordance with its fiduciary obligations… We find ourselves at a critical juncture in TICC’s history where the Board’s decisions and actions over the next few weeks will have significant ramifications to stockholders.”

JMP Securities LLC – September 17, 2015

“[W]e believe the action taken by [TSLX] management highlights our favorable perception of the company’s leading governance practices and focus on creating shareholder value.”

Keefe, Bruyette & Woods, Inc. – September 16, 2015

“The $0.29 [TICC] dividend is not sustainable, and we expect it will be cut regardless of what happens. We have been talking about a dividend cut for over a year now…Now TSLX provides an interesting offer and the [TICC] Board rejects it without negotiating with TSLX. As the title of our note implies, we are questioning whether the [TICC] Board is really doing all they can to maximize shareholder value.”

|

|

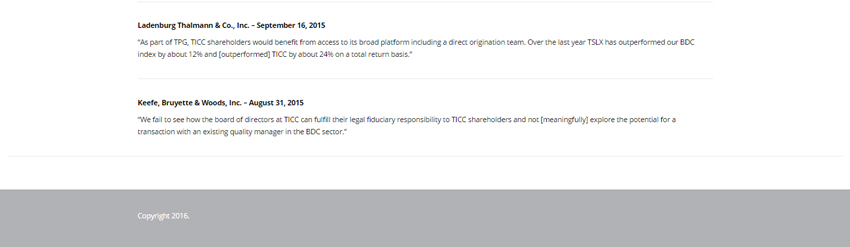

Ladenburg Thalmann & Co., Inc. – September 16, 2015

“As part of TPG, TICC shareholders would benefit from access to its broad platform including a direct origination team. Over the last year TSLX has outperformed our BDC index by about 12% and [outperformed] TICC by about 24% on a total return basis.”

Keefe, Bruyette & Woods, Inc. – August 31, 2015

“We fail to see how the board of directors at TICC can fulfill their legal fiduciary responsibility to TICC shareholders and not [meaningfully] explore the potential for a transaction with an existing quality manager in the BDC sector.”

Copyright 2016.

About TPG Specialty Lending

TPG Specialty Lending, Inc. (“TSLX” or the “Company”) is a specialty finance company focused on lending to middle-market companies. The Company seeks to generate current income primarily in U.S.-domiciled middle-market companies through direct originations of senior secured loans and, to a lesser extent, originations of mezzanine loans and investments in corporate bonds and equity securities. The Company has elected to be regulated as a business development company, or BDC, under the Investment Company Act of 1940 and the rules and regulations promulgated thereunder. TSLX is externally managed by TSL Advisers, LLC, a Securities and Exchange Commission registered investment adviser. TSLX leverages the deep investment, sector, and operating resources of TPG Special Situations Partners, the dedicated special situations and credit platform of TPG, with over $16 billion of assets under management as of March 31, 2016, and the broader TPG platform, a global private investment firm with over $74 billion of assets under management as of March 31, 2016. For more information, visit the Company’s website at www.tpgspecialtylending.com.

Forward-Looking Statements

Information set forth herein may contain forward-looking statements, including, but not limited to, statements with regard to the expected future financial position, results of operations, cash flows, dividends, portfolio, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management of TICC Capital Corp. (“TICC”), statements with regard to the expected future financial position, results of operations, cash flows, dividends, portfolio, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management of TPG Specialty Lending, Inc. (“TSLX”), and statements with regard to TSLX’s proposed business combination transaction with TICC (including any financing required in connection with a possible transaction and the benefits, results, effects and timing of a possible transaction). Statements set forth herein concerning the business outlook or future economic performance, anticipated profitability, revenues, expenses, dividends or other financial items, and product or services line growth of TSLX, TICC and/or the combined businesses of TSLX and TICC, including, but not limited to, statements containing words such as “anticipate,” “approximate,” “believe,” “plan,” “estimate,” “expect,” “project,” “could,” “would,” “should,” “will,” “intend,” “may,” “potential,” “upside” and other similar expressions, together with other statements that are not historical facts, are forward-looking statements that are estimates reflecting the best judgment of TSLX based upon currently available information.

Such forward-looking statements are inherently uncertain, and stockholders and other potential investors must recognize that actual results may differ materially from TSLX’s expectations as a result of a variety of factors including, without limitation, those discussed below. Such forward-looking statements are based upon TSLX’s current expectations and include known and unknown risks, uncertainties and other factors, many of which TSLX is unable to predict or control, that may cause TSLX’s plans with respect to TICC or the actual results or performance of TICC, TSLX or TICC and TSLX on a combined basis to differ materially from any plans, future results or performance expressed or implied by such forward-looking statements. These statements involve risks, uncertainties and other factors discussed below and detailed from time to time in TSLX’s filings with the Securities and Exchange Commission (“SEC”).

Risks and uncertainties related to a possible transaction include, among others, uncertainty as to whether TSLX will further pursue, enter into or consummate a transaction on the terms set forth in its proposal or on other terms, uncertainty as to whether TICC’s board of directors will engage in good faith, substantive discussions or negotiations with TSLX concerning its proposal or any other possible transaction, potential adverse reactions or changes to business relationships resulting from the announcement or completion of a transaction, uncertainties as to the timing of a transaction, adverse effects on TSLX’s stock price resulting from the announcement or consummation of a transaction or any failure to complete a transaction, competitive responses to the announcement or consummation of a transaction, the risk that regulatory or other approvals and any financing required in connection with the consummation of a transaction are not obtained or are obtained subject to terms and conditions that are not anticipated, costs and difficulties related to a potential integration of TICC’s businesses and operations with TSLX’s businesses and operations, the inability to obtain, or delays in obtaining, cost savings and synergies from a transaction, unexpected costs, liabilities, charges or expenses resulting from a transaction, litigation relating to a transaction, the inability to retain key personnel, and any changes in general economic and/or industry specific conditions.

In addition to these factors, other factors that may affect TSLX’s plans, results or stock price are set forth in TSLX’s Annual Report on Form 10-K and in its reports on Forms 10-Q and 8-K.

Many of these factors are beyond TSLX’s control. TSLX cautions investors that any forward-looking statements made by TSLX are not guarantees of future performance. TSLX disclaims any obligation to update any such factors or to announce publicly the results of any revisions to any of the forward-looking statements to reflect future events or developments.

Third Party-Sourced Statements and Information

Certain statements and information included herein have been sourced from third parties. TSLX does not make any representations regarding the accuracy, completeness or timeliness of such third party statements or information. Except as expressly set forth herein, permission to cite such statements or information has neither been sought nor obtained from such third parties. Any such statements or information should not be viewed as an indication of support from such third parties for the views expressed herein. All information in this communication regarding TICC, including its businesses, operations and financial results, was obtained from public sources. While TSLX has no knowledge that any such information is inaccurate or incomplete, TSLX has not verified any of that information. TSLX reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. TSLX disclaims any obligation to update the data, information or opinions contained herein.

Proxy Solicitation Information

In connection with TSLX’s solicitation of proxies for the 2016 annual meeting of TICC stockholders in favor of (a) the election of TSLX’s nominee to serve as a director of TICC and (b) TSLX’s proposal to terminate the Investment Advisory Agreement, dated as of July 1, 2011, by and between TICC and TICC Management, LLC, as contemplated by Section 15(a) of the Investment Company Act of 1940, as amended, TSLX filed an amended definitive proxy statement in connection therewith on Schedule 14A with the SEC on July 14, 2016 (the “TSLX Proxy Statement”). TSLX has mailed the TSLX Proxy Statement and accompanying GOLD proxy card to stockholders of TICC. This communication is not a substitute for the TSLX Proxy Statement.

TSLX STRONGLY ADVISES ALL STOCKHOLDERS OF TICC TO READ THE TSLX PROXY STATEMENT AND THE OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY CONTAIN IMPORTANT INFORMATION. SUCH TSLX PROXY MATERIALS ARE AND WILL BECOME AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV AND ON TSLX’S WEBSITE AT HTTP://WWW.TPGSPECIALTYLENDING.COM. IN ADDITION, TSLX WILL PROVIDE COPIES OF THE TSLX PROXY STATEMENT WITHOUT CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO TSLX’S PROXY SOLICITOR AT [email protected].

The participants in the solicitation are TSLX and T. Kelley Millet, and certain of TSLX’s directors and executive officers may also be deemed to be participants in the solicitation. As of the date hereof, TSLX beneficially owned 1,633,719 shares of common stock of TICC. As of the date hereof, Mr. Millet did not directly or indirectly beneficially own any shares of common stock of TICC.

Security holders may obtain information regarding the names, affiliations and interests of TSLX’s directors and executive officers in TSLX’s Annual Report on Form 10-K for the year ended December 31, 2015, which was filed with the SEC on February 24, 2016, its proxy statement for the 2016 annual meeting of TSLX stockholders, which was filed with the SEC on April 8, 2016, and certain of its Current Reports on Form 8-K. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the interests of these participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, is available in the TSLX Proxy Statement and other relevant materials to be filed with the SEC (if and when available).

This document shall not constitute an offer to sell, buy or exchange or the solicitation of an offer to sell, buy or exchange any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- HSBC Continental Europe: Post Stabilisation Notice

- CTT Systems AB (publ.) - Interim Report First Quarter 2024

- Riber: 2024 first quarter revenues: +20%

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!