Form 8-K FAMILY DOLLAR STORES For: Dec 08

Tweet

Tweet Share

Share�

�

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

�

�

FORM 8-K

�

�

CURRENT REPORT

Pursuant to Section�13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): December�8, 2014

�

�

Family Dollar Stores, Inc.

(Exact name of registrant as specified in charter)

�

�

�

| Delaware | � | 1-6807 | � | 56-0942963 |

| (State or Other Jurisdiction of Incorporation) |

� | (Commission File Number) |

� | (I.R.S. Employer Identification No.) |

�

| P.O. Box 1017, 10401 Monroe Road Charlotte, North Carolina |

� | 28201-1017 |

| (Address of Principal Executive Offices) | � | (Zip Code) |

Registrant�s telephone number, including area code: (704)�847-6961

�

�

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2 below):

�

| x | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

�

| � | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

�

| � | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

�

| � | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

�

�

�

| Item�8.01 | Other Events. |

On December�8, 2014, Family Dollar Stores, Inc. (�Family Dollar�) made a presentation to Institutional Shareholder Services Inc. A copy of the presentation is attached hereto as Exhibit 99.1 and is incorporated herein by reference.

Additional Information About the Dollar General Tender Offer

Family Dollar has filed a solicitation/recommendation statement with respect to the tender offer with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE SOLICITATION/RECOMMENDATION STATEMENT WITH RESPECT TO THE TENDER OFFER AND OTHER RELEVANT DOCUMENTS THAT ARE FILED WITH THE SEC BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT THE TENDER OFFER. You may obtain free copies of the solicitation/recommendation statement with respect to the tender offer and other documents filed with the SEC by Family Dollar through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Family Dollar are available free of charge on Family Dollar�s internet website at www.FamilyDollar.com under the heading �Investor Relations� and then under the heading �SEC Filings� or by contacting Family Dollar�s Investor Relations Department at 704-708-2858.

Important Information for Investors and Stockholders

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section�10 of the Securities Act of 1933, as amended. In connection with the proposed merger between Dollar Tree and Family Dollar, on October�28, 2014, the Securities and Exchange Commission (SEC) declared effective Dollar Tree�s registration statement on Form S-4 that included a definitive proxy statement of Family Dollar that also constitutes a prospectus of Dollar Tree. On October�28, 2014, Family Dollar commenced mailing the definitive proxy statement/prospectus to stockholders of Family Dollar. INVESTORS AND SECURITY HOLDERS OF FAMILY DOLLAR ARE URGED TO READ THE DEFINITIVE PROXY STATEMENT/PROSPECTUS (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER DOCUMENTS RELATING TO THE MERGER THAT ARE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. Investors and security holders are able to obtain free copies of the registration statement and the definitive proxy statement/prospectus (when available) and other documents filed with the SEC by Dollar Tree and Family Dollar through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Dollar Tree are available free of charge on Dollar Tree�s internet website at www.DollarTree.com under the heading �Investor Relations� and then under the heading �Download Library� or by contacting Dollar Tree�s Investor Relations Department at 757-321-5284. Copies of the documents filed with the SEC by Family Dollar are available free of charge on Family Dollar�s internet website at www.FamilyDollar.com under the heading �Investor Relations� and then under the heading �SEC Filings� or by contacting Family Dollar�s Investor Relations Department at 704-708-2858.

Participants in the Solicitation For the Proposed Dollar Tree/Family Dollar Merger

Dollar Tree, Family Dollar, and their respective directors, executive officers and certain other members of management and employees may be deemed to be participants in the solicitation of proxies from the holders of Family Dollar common stock in respect of the proposed merger between Dollar Tree and Family Dollar. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of proxies in favor of the proposed merger are set forth in the proxy statement/prospectus filed with the SEC. You can also find information about Dollar Tree�s and Family Dollar�s directors and executive officers in Dollar Tree�s definitive proxy statement filed with the SEC on May�12, 2014 and in Family Dollar�s Annual Report on Form 10-K for the fiscal year ended August�30, 2014, respectively. You can obtain free copies of these documents from Dollar Tree or Family Dollar using the contact information above.

Forward Looking Statements

Certain statements contained herein are �forward-looking statements� that are subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements and information about our current and future prospects and our operations and financial results are based on currently available information. Various risks, uncertainties and other factors could cause actual future results and financial performance to vary significantly from those anticipated in such statements. The forward looking statements contained herein include assumptions about our operations, such as cost controls and market conditions, and certain plans, activities or events which we expect will or may occur in the future and relate to, among other things, the business combination transaction involving Dollar Tree and Family Dollar, the unsolicited tender offer and proposals from Dollar General and any other alternative business combination transactions, the financing of the proposed transactions, the benefits, results, effects, timing and certainty of the proposed transactions, future financial and operating results, expectations concerning the antitrust review process for the proposed transactions and the combined company�s plans, objectives, expectations (financial or otherwise) and intentions.

Risks and uncertainties related to the proposed mergers include, among others: the risk that Family Dollar�s stockholders do not approve either merger; the risk that the merger agreement is terminated as a result of a competing proposal; the risk that regulatory approvals required for either merger are not obtained on the proposed terms and schedule or are obtained subject to conditions that are not anticipated; the risk that the other conditions to the closing of either merger are not satisfied; the risk that the financing required to fund either transaction is not obtained; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of either merger; uncertainties as to the timing of either merger; competitive responses to either proposed merger; response by activist stockholders to either merger; costs and difficulties related to the integration of Family Dollar�s business and operations with Dollar Tree�s or other potential business combination transaction counterparties� business and operations; the inability to obtain, or delays in obtaining, the cost savings and synergies contemplated by either merger; uncertainty of the expected financial performance of the combined company following completion of either proposed transaction; the calculations of, and factors that may impact the calculations of, the acquisition price in connection with either proposed transaction and the allocation of such acquisition price to the net assets acquired in accordance with applicable accounting rules and methodologies; unexpected costs, charges or expenses resulting from either merger; litigation relating to either merger; the outcome of pending or potential litigation or governmental investigations; the inability to retain key personnel; and any changes in general economic and/or industry specific conditions. Consequently, all of the forward-looking statements made by Family Dollar, in this and in other documents or statements are qualified by factors, risks and uncertainties, including, but not limited to, those set forth under the headings titled �Cautionary Statement Regarding Forward-Looking Statements� and �Risk Factors� in Family Dollar�s Annual Report on Form 10-K for the fiscal year ended August�30, 2014 and other reports filed by Family Dollar with the SEC, which are available at the SEC�s website http://www.sec.gov.

Please read our �Risk Factors� and other cautionary statements contained in these filings. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Family Dollar undertakes no obligation to update or revise any forward-looking statements, even if experience or future changes make it clear that projected results expressed or implied in such statements will not be realized, except as may be required by law. As a result of these risks and others, actual results could vary significantly from those anticipated herein, and our financial condition and results of operations could be materially adversely affected.

�

| Item�9.01. | Financial Statements and Exhibits. |

(d)�Exhibits

�

| Exhibit�99.1 | �� | Presentation to Institutional Shareholder Services Inc., dated December�8, 2014 |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

�

| � | � | FAMILY DOLLAR STORES, INC. | ||||

| � | � | (Registrant) | ||||

| Date: December 8, 2014 | � | � | By: | � | /s/ James C. Snyder, Jr. | |

| � | � | � | James C. Snyder, Jr. | |||

| � | � | � | Senior Vice President, General Counsel and Secretary | |||

Exhibit 99.1

�

�

Proposed Acquisition of

Family Dollar by Dollar Tree

December 8, 2014

1. DOLLAR TREE | FAMILY DOLLAR.

�

Additional Information About the Dollar General Tender Offer

Family Dollar has filed a solicitation/recommendation statement with respect to the tender offer with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE SOLICITATION/RECOMMENDATION STATEMENT WITH RESPECT TO THE TENDER OFFER AND OTHER RELEVANT DOCUMENTS THAT ARE FILED WITH THE SEC BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT THE TENDER OFFER. You may obtain free copies of the solicitation/recommendation statement with respect to the tender offer and other documents filed with the SEC by Family Dollar through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Family Dollar are available free of charge on Family Dollar�s internet website at www.FamilyDollar.com under the heading �Investor Relations� and then under the heading �SEC Filings� or by contacting Family Dollar�s Investor Relations Department at 704-708-2858.

Important Information for Investors and Stockholders

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended. In connection with the proposed merger between Dollar Tree and Family Dollar, on October 28, 2014, the Securities and Exchange Commission (SEC) declared effective Dollar Tree�s registration statement on Form S-4 that included a definitive proxy statement of Family Dollar that also constitutes a prospectus of Dollar Tree. On October 28, 2014, Family Dollar commenced mailing the definitive proxy statement/prospectus to stockholders of Family Dollar. INVESTORS AND SECURITY HOLDERS OF FAMILY DOLLAR ARE URGED TO READ THE DEFINITIVE PROXY STATEMENT/PROSPECTUS (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER DOCUMENTS RELATING TO THE MERGER THAT ARE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. Investors and security holders are able to obtain free copies of the registration statement and the definitive proxy statement/prospectus (when available) and other documents filed with the SEC by Dollar Tree and Family Dollar through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Dollar Tree are available free of charge on Dollar Tree�s internet website at www.DollarTree.com under the heading �Investor Relations� and then under the heading �Download Library� or by contacting Dollar Tree�s Investor Relations Department at 757-321-5284. Copies of the documents filed with the SEC by Family Dollar are available free of charge on Family Dollar�s internet website at www.FamilyDollar.com under the heading �Investor Relations� and then under the heading �SEC Filings� or by contacting Family Dollar�s Investor Relations Department at 704-708-2858.

Participants in the Solicitation For the Proposed Dollar Tree/Family Dollar Merger

Dollar Tree, Family Dollar, and their respective directors, executive officers and certain other members of management and employees may be deemed to be participants in the solicitation of proxies from the holders of Family Dollar common stock in respect of the proposed merger between Dollar Tree and Family Dollar. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of proxies in favor of the proposed merger are set forth in the proxy statement/prospectus filed with the SEC. You can also find information about Dollar Tree�s and Family Dollar�s directors and executive officers in Dollar Tree�s definitive proxy statement filed with the SEC on May 12, 2014 and in Family Dollar�s Annual Report on Form 10-K for the fiscal year ended August 30, 2014, respectively. You can obtain free copies of these documents from Dollar Tree or Family Dollar using the contact information above.

Forward Looking Statements

Certain statements contained herein are �forward-looking statements� that are subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements and information about our current and future prospects and our operations and financial results are based on currently available information. Various risks, uncertainties and other factors could cause actual future results and financial performance to vary significantly from those anticipated in such statements. The forward looking statements contained herein include assumptions about our operations, such as cost controls and market conditions, and certain plans, activities or events which we expect will or may occur in the future and relate to, among other things, the business combination transaction involving Dollar Tree and Family Dollar, the unsolicited tender offer and proposals from Dollar General and any other alternative business combination transactions, the financing of the proposed transactions, the benefits, results, effects, timing and certainty of the proposed transactions, future financial and operating results, expectations concerning the antitrust review process for the proposed transactions and the combined company�s plans, objectives, expectations (financial or otherwise) and intentions.

Risks and uncertainties related to the proposed mergers include, among others: the risk that Family Dollar�s stockholders do not approve either merger; the risk that the merger agreement is terminated as a result of a competing proposal; the risk that regulatory approvals required for either merger are not obtained on the proposed terms and schedule or are obtained subject to conditions that are not anticipated; the risk that the other conditions to the closing of either merger are not satisfied; the risk that the financing required to fund either transaction is not obtained; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of either merger; uncertainties as to the timing of either merger; competitive responses to either proposed merger; response by activist stockholders to either merger; costs and difficulties related to the integration of Family Dollar�s business and operations with Dollar Tree�s or other potential business combination transaction counterparties� business and operations; the inability to obtain, or delays in obtaining, the cost savings and synergies contemplated by either merger; uncertainty of the expected financial performance of the combined company following completion of either proposed transaction; the calculations of, and factors that may impact the calculations of, the acquisition price in connection with either proposed transaction and the allocation of such acquisition price to the net assets acquired in accordance with applicable accounting rules and methodologies; unexpected costs, charges or expenses resulting from either merger; litigation relating to either merger; the outcome of pending or potential litigation or governmental investigations; the inability to retain key personnel; and any changes in general economic and/or industry specific conditions. Consequently, all of the forward-looking statements made by Family Dollar, in this and in other documents or statements are qualified by factors, risks and uncertainties, including, but not limited to, those set forth under the headings titled �Cautionary Statement Regarding Forward-Looking Statements� and �Risk Factors� in Family Dollar�s Annual Report on Form 10-K for the fiscal year ended August 30, 2014 and other reports filed by Family Dollar with the SEC, which are available at the SEC�s website http://www.sec.gov.

Please read our �Risk Factors� and other cautionary statements contained in these filings. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Family Dollar undertakes no obligation to update or revise any forward-looking statements, even if experience or future changes make it clear that projected results expressed or implied in such statements will not be realized, except as may be required by law. As a result of these risks and others, actual results could vary significantly from those anticipated herein, and our financial condition and results of operations could be materially adversely affected.

FAMILY DOLLAR.

2

�

Roadmap for Presentation

Summary of Transaction Consideration and Key Terms

Antitrust and Execution Risks Favor Approval of the Dollar Tree Merger

Family Dollar Board�s Interests are Aligned with Stockholders

Timeline Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

Conclusion

FAMILY DOLLAR.

3

�

Summary of Transaction

Consideration and Key Terms

(HRL)

�

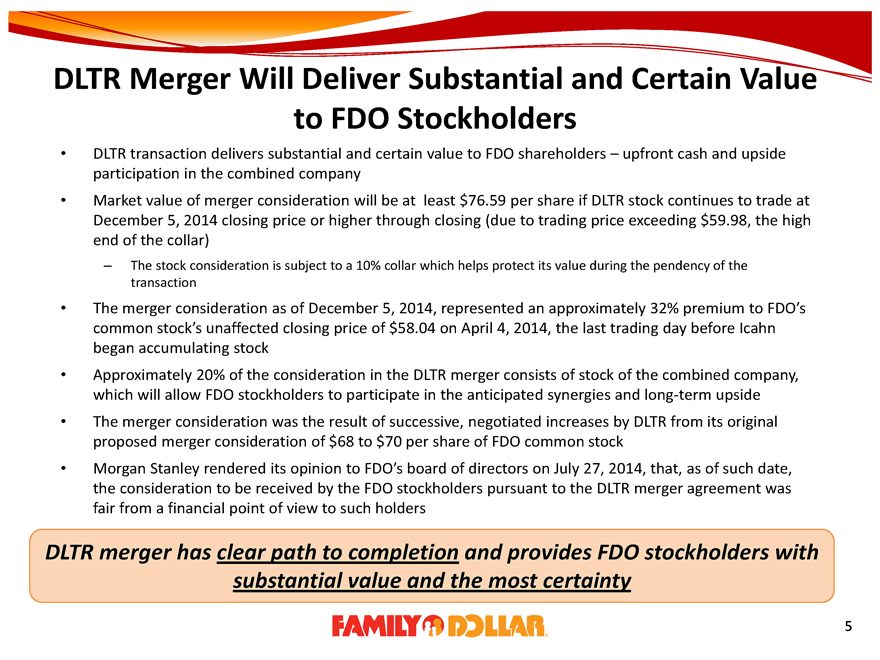

DLTR Merger Will Deliver Substantial and Certain Value

to FDO Stockholders

DLTR transaction delivers substantial and certain value to FDO shareholders � upfront cash and upside participation in the combined company

Market value of merger consideration will be at least $76.59 per share if DLTR stock continues to trade at December 5, 2014 closing price or higher through closing (due to trading price exceeding $59.98, the high end of the collar)

� The stock consideration is subject to a 10% collar which helps protect its value during the pendency of the transaction

The merger consideration as of December 5, 2014, represented an approximately 32% premium to FDO�s common stock�s unaffected closing price of $58.04 on April 4, 2014, the last trading day before Icahn began accumulating stock

Approximately 20% of the consideration in the DLTR merger consists of stock of the combined company, which will allow FDO stockholders to participate in the anticipated synergies and long-term upside

The merger consideration was the result of successive, negotiated increases by DLTR from its original proposed merger consideration of $68 to $70 per share of FDO common stock

Morgan Stanley rendered its opinion to FDO�s board of directors on July 27, 2014, that, as of such date, the consideration to be received by the FDO stockholders pursuant to the DLTR merger agreement was fair from a financial point of view to such holders

DLTR merger has clear path to completion and provides FDO stockholders with

substantial value and the most certainty

FAMILY DOLLAR.

5

�

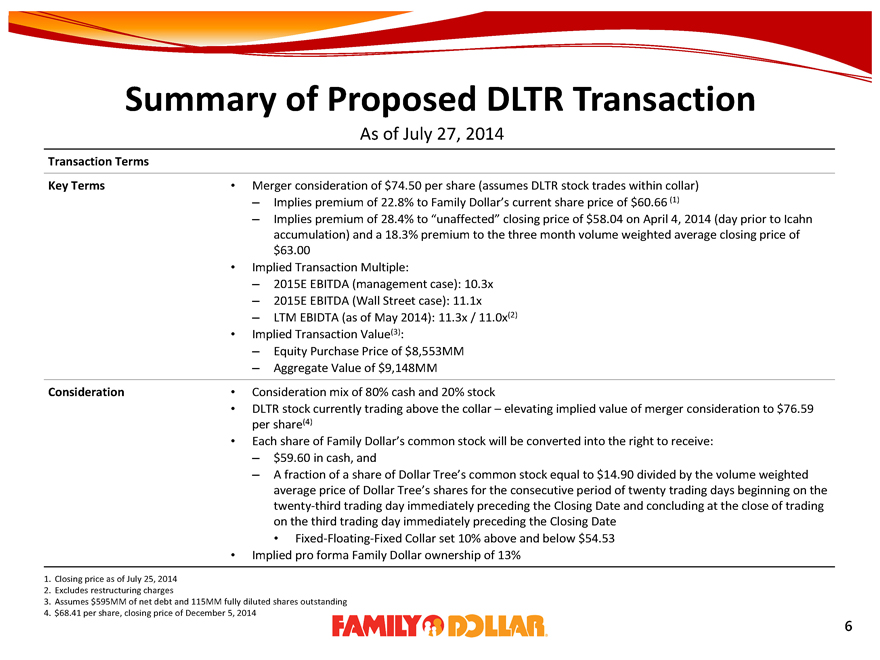

Summary of Proposed DLTR Transaction

As of July 27, 2014

Transaction Terms

Key Terms

Merger consideration of $74.50 per share (assumes DLTR stock trades within collar)

� Implies premium of 22.8% to Family Dollar�s current share price of $60.66 (1)

� Implies premium of 28.4% to �unaffected� closing price of $58.04 on April 4, 2014 (day prior to Icahn accumulation) and a 18.3% premium to the three month volume weighted average closing price of

$63.00

Implied Transaction Multiple:

� 2015E EBITDA (management case): 10.3x

� 2015E EBITDA (Wall Street case): 11.1x

� LTM EBIDTA (as of May 2014): 11.3x / 11.0x(2)

Implied Transaction Value(3):

� Equity Purchase Price of $8,553MM

� Aggregate Value of $9,148MM

Consideration

Consideration mix of 80% cash and 20% stock

DLTR stock currently trading above the collar � elevating implied value of merger consideration to $76.59 per share(4)

Each share of Family Dollar�s common stock will be converted into the right to receive:

� $59.60 in cash, and

� A fraction of a share of Dollar Tree�s common stock equal to $14.90 divided by the volume weighted average price of Dollar Tree�s shares for the consecutive period of twenty trading days beginning on the twenty-third trading day immediately preceding the Closing Date and concluding at the close of trading on the third trading day immediately preceding the Closing Date

Fixed-Floating-Fixed Collar set 10% above and below $54.53

Implied pro forma Family Dollar ownership of 13%

1. Closing price as of July 25, 2014

2. Excludes restructuring charges

3. Assumes $595MM of net debt and 115MM fully diluted shares outstanding

4. $68.41 per share, closing price of December 5, 2014

FAMILY DOLLAR.

6

�

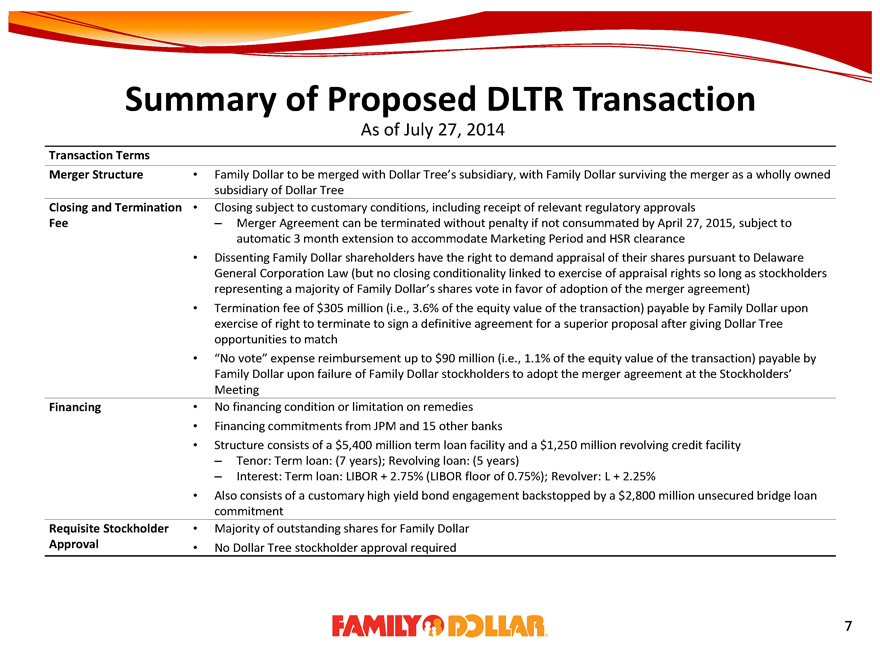

Summary of Proposed DLTR Transaction

As of July 27, 2014

Transaction Terms

Merger Structure

Family Dollar to be merged with Dollar Tree�s subsidiary, with Family Dollar surviving the merger as a wholly owned subsidiary of Dollar Tree

Closing and Termination Fee

Closing subject to customary conditions, including receipt of relevant regulatory approvals

� Merger Agreement can be terminated without penalty if not consummated by April 27, 2015, subject to automatic 3 month extension to accommodate Marketing Period and HSR clearance

Dissenting Family Dollar shareholders have the right to demand appraisal of their shares pursuant to Delaware General Corporation Law (but no closing conditionality linked to exercise of appraisal rights so long as stockholders representing a majority of Family Dollar�s shares vote in favor of adoption of the merger agreement)

Termination fee of $305 million (i.e., 3.6% of the equity value of the transaction) payable by Family Dollar upon exercise of right to terminate to sign a definitive agreement for a superior proposal after giving Dollar Tree opportunities to match

�No vote� expense reimbursement up to $90 million (i.e., 1.1% of the equity value of the transaction) payable by Family Dollar upon failure of Family Dollar stockholders to adopt the merger agreement at the Stockholders� Meeting

Financing

No financing condition or limitation on remedies

Financing commitments from JPM and 15 other banks

Structure consists of a $5,400 million term loan facility and a $1,250 million revolving credit facility

� Tenor: Term loan: (7 years); Revolving loan: (5 years)

� Interest: Term loan: LIBOR + 2.75% (LIBOR floor of 0.75%); Revolver: L + 2.25%

Also consists of a customary high yield bond engagement backstopped by a $2,800 million unsecured bridge loan

commitment

Requisite Stockholder

Approval

Majority of outstanding shares for Family Dollar

No Dollar Tree stockholder approval required

FAMILY DOLLAR.

7

�

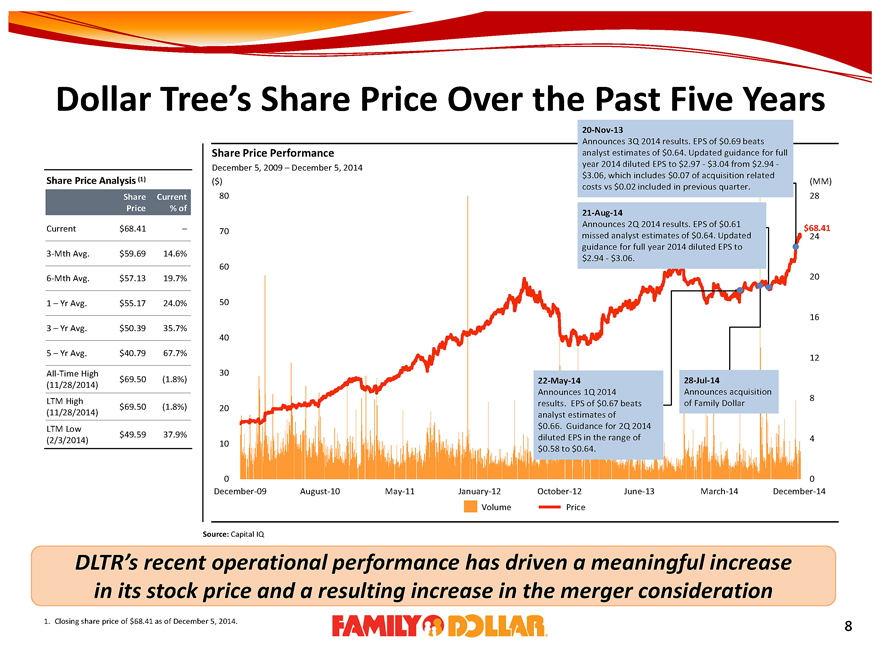

Dollar Tree�s Share Price Over the Past Five Years

Share Price Analysis (1)

Current

3-Mth Avg. 6-Mth Avg. 1 � Yr Avg. 3 � Yr Avg. 5 � Yr Avg.

All-Time High (11/28/2014)

LTM High (11/28/2014)

LTM Low (2/3/2014)

Share Price

$68.41 $59.69 $57.13 $55.17 $50.39 $40.79 $69.50 $69.50 $49.59

Current % of

� 14.6% 19.7% 24.0% 35.7% 67.7% (1.8%) (1.8%) 37.9%

Share Price Performance

December 5, 2009 � December 5, 2014

($) 80 70 60 50 40 30 20 10 0

December-09 August-10 May-11 January-12 October-12 June-13 March-14 December-14 Volume Price

20-Nov-13

Announces 3Q 2014 results. EPS of $0.69 beats analyst estimates of $0.64. Updated guidance for full year 2014 diluted EPS to $2.97 - $3.04 from $2.94 - $3.06, which includes $0.07 of acquisition related costs vs $0.02 included in previous quarter.

21-Aug-14

Announces 2Q 2014 results. EPS of $0.61 missed analyst estimates of $0.64. Updated guidance for full year 2014 diluted EPS to $2.94 - $3.06.

22-May-14

Announces 1Q 2014 results. EPS of $0.67 beats analyst estimates of $0.66. Guidance for 2Q 2014 diluted EPS in the range of $0.58 to $0.64.

28-Jul-14

Announces acquisition of Family Dollar

(MM) 28

$68.41 24 20 16 12 8 4 0

Source: Capital IQ

DLTR�s recent operational performance has driven a meaningful increase in its stock price and a resulting increase in the merger consideration

1. Closing share price of $68.41 as of December 5, 2014.

FAMILY DOLLAR.

8

�

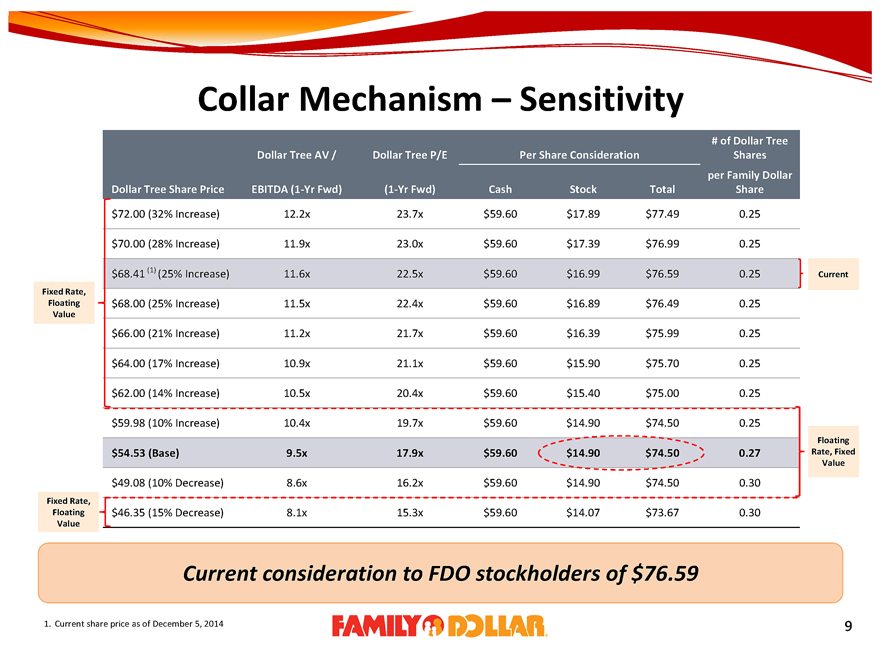

Collar Mechanism � Sensitivity

Fixed Rate, Floating Value

Fixed Rate, Floating Value

Dollar Tree Share Price

$72.00 (32% Increase)

$70.00 (28% Increase)

$68.41 (1) (25% Increase)

$68.00 (25% Increase)

$66.00 (21% Increase)

$64.00 (17% Increase)

$62.00 (14% Increase)

$59.98 (10% Increase)

$54.53 (Base)

$49.08 (10% Decrease)

$46.35 (15% Decrease)

Dollar Tree AV / EBITDA (1-Yr Fwd)

12.2x 11.9x 11.6x 11.5x 11.2x 10.9x 10.5x 10.4x 9.5x 8.6x 8.1x

Dollar Tree P/E (1-Yr Fwd)

23.7x 23.0x 22.5x 22.4x 21.7x 21.1x 20.4x 19.7x 17.9x 16.2x 15.3x

Per Share Consideration

Cash

$59.60 $59.60 $59.60 $59.60 $59.60 $59.60 $59.60 $59.60 $59.60 $59.60 $59.60

Stock

$17.89 $17.39 $16.99 $16.89 $16.39 $15.90 $15.40 $14.90 $14.90 $14.90 $14.07

Total

$77.49 $76.99 $76.59 $76.49 $75.99 $75.70 $75.00 $74.50 $74.50 $74.50 $73.67

# of Dollar Tree Shares per Family Dollar Share

0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.27 0.30 0.30

Current

Floating Rate, Fixed Value

Current consideration to FDO stockholders of $76.59

1. Current share price as of December 5, 2014

FAMILY DOLLAR.

9

�

Antitrust and Execution Risks

Favor Approval of the Dollar Tree

Merger

(HRL/ EG)

�

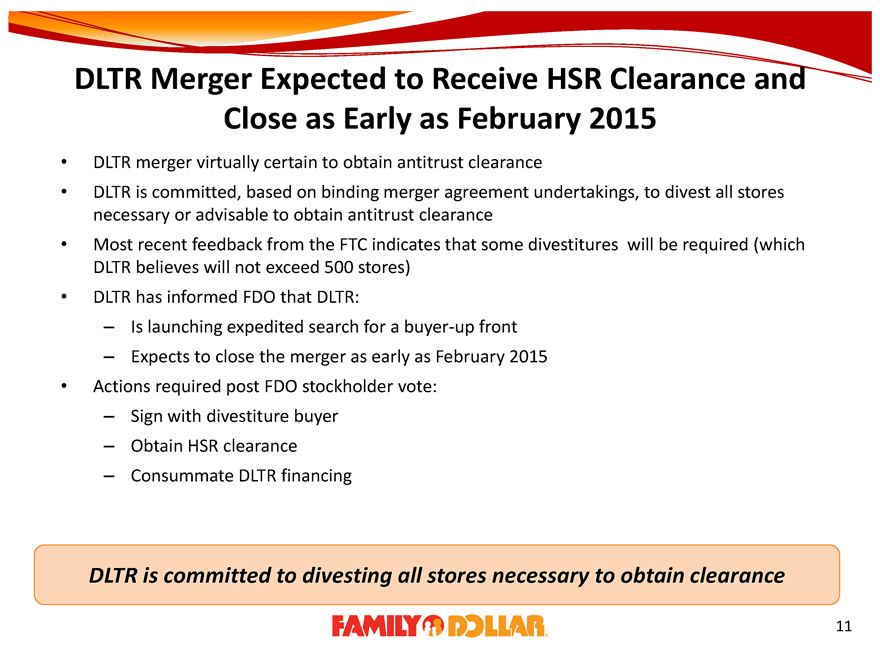

DLTR Merger Expected to Receive HSR Clearance and Close as Early as February 2015

DLTR merger virtually certain to obtain antitrust clearance

DLTR is committed, based on binding merger agreement undertakings, to divest all stores necessary or advisable to obtain antitrust clearance

Most recent feedback from the FTC indicates that some divestitures will be required (which DLTR believes will not exceed 500 stores)

DLTR has informed FDO that DLTR:

� Is launching expedited search for a buyer-up front

� Expects to close the merger as early as February 2015

Actions required post FDO stockholder vote:

� Sign with divestiture buyer

� Obtain HSR clearance

� Consummate DLTR financing

DLTR is committed to divesting all stores necessary to obtain clearance

FAMILY DOLLAR.

11

�

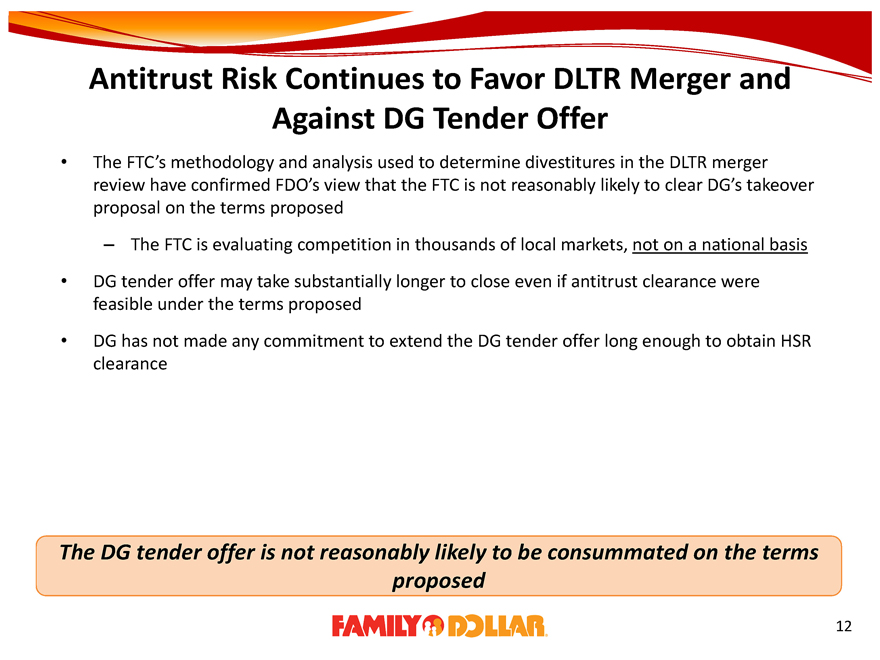

Antitrust Risk Continues to Favor DLTR Merger and Against DG Tender Offer

The FTC�s methodology and analysis used to determine divestitures in the DLTR merger review have confirmed FDO�s view that the FTC is not reasonably likely to clear DG�s takeover proposal on the terms proposed

� The FTC is evaluating competition in thousands of local markets, not on a national basis

DG tender offer may take substantially longer to close even if antitrust clearance were feasible under the terms proposed

DG has not made any commitment to extend the DG tender offer long enough to obtain HSR clearance

The DG tender offer is not reasonably likely to be consummated on the terms proposed

FAMILY DOLLAR.

12

�

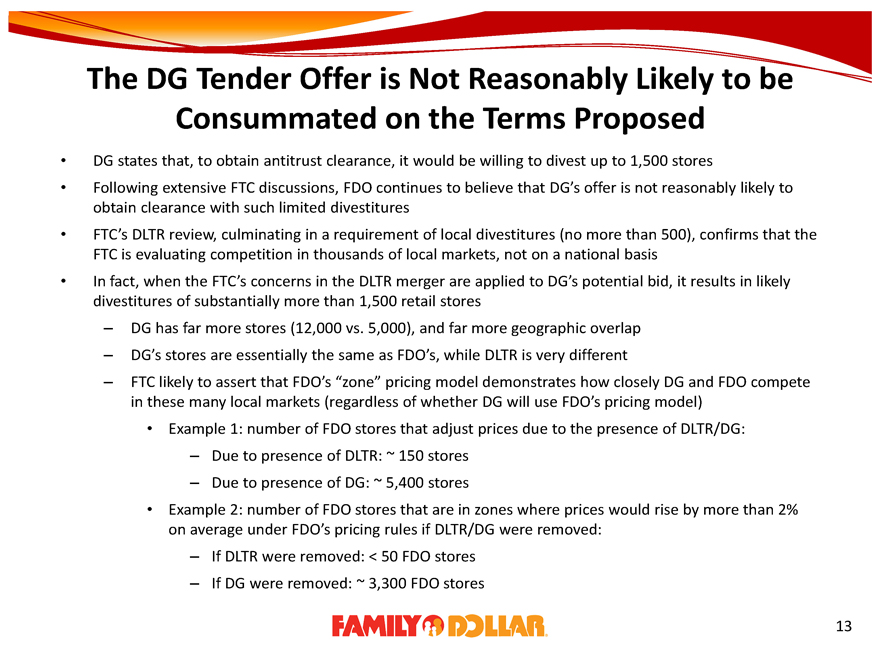

The DG Tender Offer is Not Reasonably Likely to be Consummated on the Terms Proposed

DG states that, to obtain antitrust clearance, it would be willing to divest up to 1,500 stores

Following extensive FTC discussions, FDO continues to believe that DG�s offer is not reasonably likely to

obtain clearance with such limited divestitures

FTC�s DLTR review, culminating in a requirement of local divestitures (no more than 500), confirms that the

FTC is evaluating competition in thousands of local markets, not on a national basis

In fact, when the FTC�s concerns in the DLTR merger are applied to DG�s potential bid, it results in likely

divestitures of substantially more than 1,500 retail stores

� DG has far more stores (12,000 vs. 5,000), and far more geographic overlap

� DG�s stores are essentially the same as FDO�s, while DLTR is very different

� FTC likely to assert that FDO�s �zone� pricing model demonstrates how closely DG and FDO compete

in these many local markets (regardless of whether DG will use FDO�s pricing model)

Example 1: number of FDO stores that adjust prices due to the presence of DLTR/DG:

� Due to presence of DLTR: ~ 150 stores

� Due to presence of DG: ~ 5,400 stores

Example 2: number of FDO stores that are in zones where prices would rise by more than 2%

on average under FDO�s pricing rules if DLTR/DG were removed:

� If DLTR were removed: < 50 FDO stores

� If DG were removed: ~ 3,300 FDO stores

FAMILY DOLLAR.

13

�

DG Tender Offer May Take Substantially Longer to Close Even If Antitrust Clearance were Feasible

On October 10, 2014, FTC issued �second request� in connection with its review of DG�s

tender offer

Even after DG complies with second request, there could be a further six-month period

during which DG would:

� Advocate before FTC

� Negotiate agreement as to the assets, properties and rights to divest

� Find buyer for divested assets and execute agreements with respect to all divestiture

transactions

All of these actions would most likely need to occur before HSR clearance of the DG tender

offer

Litigation between DG and the FTC would make the timeline to HSR clearance of the DG

tender offer considerably longer

FAMILY DOLLAR.

14

�

DG Has Not Made Any Commitment to Extend the DG Tender Offer Long Enough to Obtain HSR Clearance

Once the DG tender offer expires on December 31, 2014 without HSR clearance, DG is free to walk away

Even though DG is likely aware that it will take several months, at best, to obtain HSR clearance, there is no commitment by DG to extend and keep open the DG tender offer until DG has obtained HSR clearance

Even if DG continuously extends the DG tender offer over the many months until HSR clearance occurs, DG may adversely modify the terms of its tender offer, including the price, in connection with any extension

DLTR is bound by the DLTR merger agreement and cannot walk away except under narrowly specified circumstances

� DG may elect to walk away from its tender offer after any scheduled expiration date for the DG tender offer and has not made any commitment to the contrary

DG is free to walk away when its tender offer expires on 12/31/14

FAMILY DOLLAR.

15

�

DG Tender Offer May Be Designed to Harm FDO

On June 19, 2014, DG indicated to FDO that it was not interested in a strategic transaction at that time

The announcement of Mr. Dreiling�s retirement on June 27, 2014, reinforced the June 19 message

There are potential commercial advantages to DG arising from prevention of the DLTR merger

Despite DG�s statements that it has taken �this issue [of antitrust risk] completely off the table�, FDO stockholders continue to bear significant antitrust risk under the DG tender offer

DG�s antitrust approval process has been delayed because DG failed to file with the FTC until DG commenced its tender offer and DG elected a longer 30-day waiting period

No shares tendered in the DG tender offer will be permitted to be purchased by DG on the scheduled expiration date of December 31, 2014, because, inter alia, HSR clearance will not have been obtained yet

DG tender offer may be intended to cause FDO stockholders to refrain from approving DLTR merger and harm FDO�s business, rather than to result in successful acquisition of FDO

FAMILY DOLLAR.

16

�

DLTR Merger Agreement � Customary Limitations Coupled with Security and Flexibility

DLTR merger agreement expressly prohibits FDO from engaging in discussions with or providing information to DG � an entirely customary provision

� DLTR merger agreement permits discussions only if, among other criteria, DG makes a proposal that is reasonably expected to lead to a superior proposal that is reasonably likely to be consummated on the terms proposed

� Due to antitrust regulatory considerations, the DG tender offer is not a such a proposal

DLTR merger agreement provides FDO with security of binding agreement with DLTR and, in the event an unsolicited superior proposal (that is reasonably likely to be consummated on the terms proposed) were made by a competing bidder, would allow the FDO board to comply with its fiduciary duties by accepting the competing bidder�s proposal after complying with match rights and paying a termination fee to DLTR

The absence of a requirement for an approval by DLTR�s stockholders eliminates the risk for FDO that third parties, such as DG, could impede the consummation of the merger between FDO and DLTR by making a bid for DLTR conditioned on DLTR�s abandonment of the merger with FDO

DLTR merger agreement prohibits discussions with DG due to absence of likelihood that DG Offer will be consummated on terms proposed

FAMILY DOLLAR.

17

�

Family Dollar Board�s Interests

Are Aligned with Stockholders

(EG/GE)

�

Board Independence

10 of 11 directors are independent

� Howard Levine is the only director who serves as an employee of FDO

Director Edward P. Garden�s Trian Partners owns over 7.3% of FDO; at the closing of a sale to DG at $80 per share, Trian would receive roughly $46 million more in financial value than it would in a sale at $74.50 to DLTR

Since January 2014, a committee of four independent directors (Glenn A. Eisenberg, Ed Garden, George R. Mahoney, Jr., and Harvey Morgan) has been overseeing the development of FDO�s stand-alone strategic plan and consideration and exploration of strategic alternatives

� All negotiations with DLTR

� Consideration of the proposals by DG

� Antitrust analysis by Cleary Gottlieb and an economic consultant of combinations with DLTR, DG and others

FDO�s Board is completely aligned with FDO shareholders and committed to acting in their best interests

FAMILY DOLLAR.

19

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

(ALL)

�

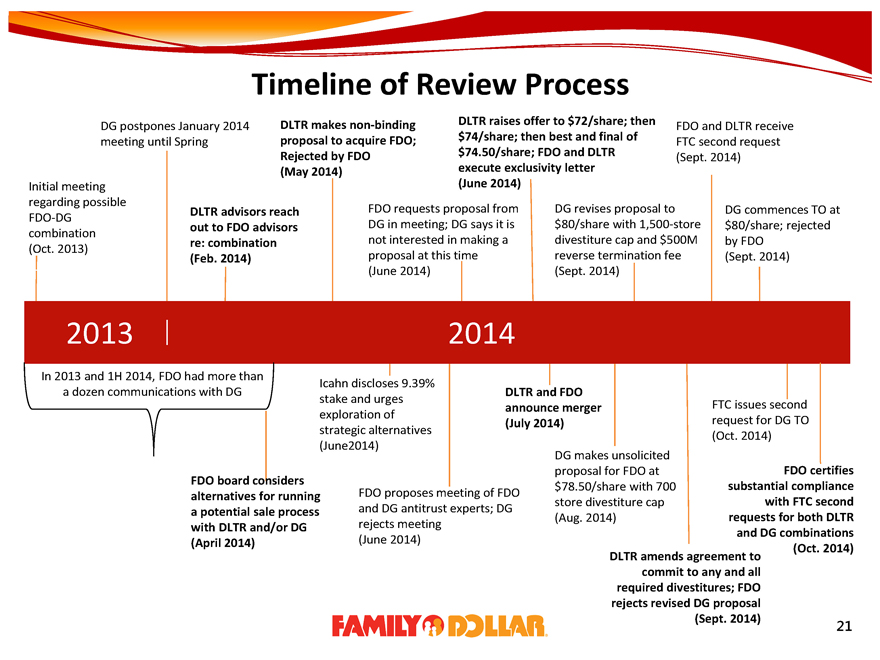

Timeline of Review Process

DG postpones January 2014 meeting until Spring

DLTR makes non-binding proposal to acquire FDO; Rejected by FDO (May 2014) DLTR raises offer to $72/share; then $74/share; then best and final of $74.50/share; FDO and DLTR execute exclusivity letter (June 2014)

FDO and DLTR receive FTC second request (Sept. 2014)

Initial meeting regarding possible FDO-DG combination (Oct. 2013)

DLTR advisors reach out to FDO advisors re: combination (Feb. 2014)

FDO requests proposal from DG in meeting; DG says it is not interested in making a proposal at this time (June 2014)

DG revises proposal to $80/share with 1,500-store divestiture cap and $500M reverse termination fee (Sept. 2014)

DG commences TO at $80/share; rejected by FDO

(Sept. 2014)

2013 |

2014

In 2013 and 1H 2014, FDO had more than a dozen communications with DG

Icahn discloses 9.39% stake and urges exploration of strategic alternatives (June 2014)

DLTR and FDO announce merger (July 2014)

FTC issues second request for DG TO (Oct. 2014)

FDO board considers alternatives for running a potential sale process with DLTR and/or DG (April 2014)

FDO proposes meeting of FDO and DG antitrust experts; DG rejects meeting (June 2014)

DG makes unsolicited proposal for FDO at $78.50/share with 700 store divestiture cap (Aug. 2014)

FDO certifies substantial compliance with FTC second requests for both DLTR and DG combinations

(Oct. 2014)

DLTR amends agreement to commit to any and all required divestitures; FDO rejects revised DG proposal (Sept. 2014)

FAMILY DOLLAR.

21

�

Conclusion

�

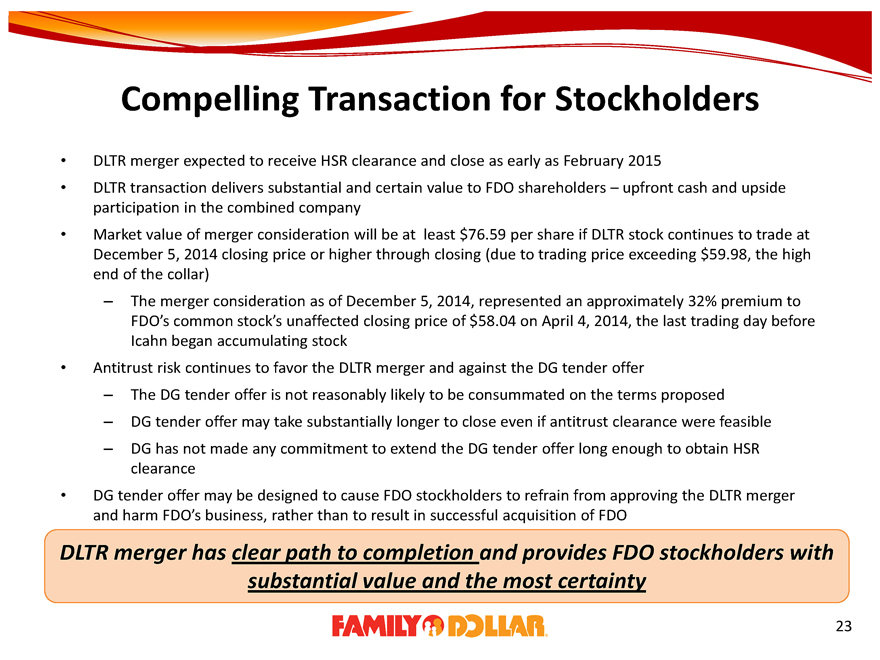

Compelling Transaction for Stockholders

DLTR merger expected to receive HSR clearance and close as early as February 2015

DLTR transaction delivers substantial and certain value to FDO shareholders � upfront cash and upside participation in the combined company

Market value of merger consideration will be at least $76.59 per share if DLTR stock continues to trade at December 5, 2014 closing price or higher through closing (due to trading price exceeding $59.98, the high end of the collar)

� The merger consideration as of December 5, 2014, represented an approximately 32% premium to FDO�s common stock�s unaffected closing price of $58.04 on April 4, 2014, the last trading day before Icahn began accumulating stock

Antitrust risk continues to favor the DLTR merger and against the DG tender offer

� The DG tender offer is not reasonably likely to be consummated on the terms proposed

� DG tender offer may take substantially longer to close even if antitrust clearance were feasible

� DG has not made any commitment to extend the DG tender offer long enough to obtain HSR clearance

DG tender offer may be designed to cause FDO stockholders to refrain from approving the DLTR merger and harm FDO�s business, rather than to result in successful acquisition of FDO

DLTR merger has clear path to completion and provides FDO stockholders with substantial value and the most certainty

FAMILY DOLLAR.

23

�

Appendix

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

On October 15, 2013, Mr. Levine and an independent director met with Mr. Dreiling and one of his directors to explore the possibility of a combination of FDO and DG

- Prior to the meeting, Mr. Levine, Mr. Garden and FDO�s advisors discussed tactics to employ at the meeting to ensure that any discussions of combining the companies led to proposals from DG that would maximize value for FDO stockholders. These consultations led to the view that it would be optimal to create the impression that a meaningful premium would be required to win over FDO by explaining that, at this point in time, FDO was not for sale and envisioned that, if there were ever to be a strategic combination, FDO management would continue to run the combined company out of its headquarters in Charlotte, North Carolina

- During the course of the meeting, Mr. Levine mentioned the possibility of maintaining FDO�s existing headquarters and management for the combined company

- Mr. Dreiling explained that DG had dedicated resources to analyzing a possible combination with FDO and would, if at all, be interested only if DG were actually acquiring FDO with the combined company having DG�s existing headquarters and management

- Mr. Levine indicated that he was one of the largest stockholders of FDO, would have no problem with such an approach and that, subject to the views of the FDO board, Mr. Dreiling�s approach could be acceptable if DG paid FDO stockholders an appropriate premium

Another meeting was scheduled for December 2013 to discuss a business combination transaction, but DG subsequently delayed the meeting until January 2014 and then canceled, requesting a delay until Spring 2014

FAMILY DOLLAR.

25

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

In February 2014, DLTR�s financial advisor contacted Morgan Stanley to express DLTR�s interest in a potential business combination transaction with FDO, and during March and April 2014 representatives of DLTR and FDO subsequently negotiated the signing of a customary NDA, so that some initial confidential information, including internal forecasts, could be exchanged to permit DLTR to make an indication of the consideration it would be willing to pay

- Prior to meeting with DLTR, Mr. Levine confirmed to the FDO board that he would comply with his commitment not to negotiate any arrangements for himself and to keep the board updated on any discussions with DLTR

- At Mr. Levine and Mr. Sasser�s first meeting in March 2014, Mr. Sasser also noted that if an agreement between the companies were to be reached, Mr. Levine would have to have a management role at the combined company to facilitate the transition and integration following closing.

Mr. Levine indicated that it would be inappropriate at this time to enter into any negotiations of such an agreement

- As is customary, the NDA included a reciprocal provision that restricted each party from making disclosures to the third parties about the existence or status of any discussions or negotiations

FAMILY DOLLAR.

26

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

In April 2014, shortly after signing the NDA with DLTR, the FDO board considered alternatives for running a potential sale process with DLTR and/or DG, including the following considerations:

- The risk that, if the board were to invite DG at that time into a more formal process to compete with DLTR for the right to participate in a business combination transaction with FDO, DG might decide it was not interested in competing with DLTR for FDO, and instead pursue a business combination transaction with DLTR, leaving FDO without a merger partner and otherwise in a disadvantageous position

- How a potential merger agreement with DLTR could be structured to provide:

FDO with the security of a binding agreement with DLTR and

In the event an unsolicited superior proposal were to be made by a competing bidder after execution of the DLTR merger agreement, for the FDO board to comply with its fiduciary duties by accepting the competing bidder�s proposal after complying with match rights and paying a termination fee to DLTR

- The risk that a publicly disclosed sale process could either (i) adversely affect DLTR�s interest in a transaction with FDO, in view of DLTR�s stated interest in a confidential and exclusive process or (ii) induce DG to publicly confirm its lack of interest in a transaction with FDO, which would adversely affect FDO�s negotiating leverage with DLTR

FAMILY DOLLAR.

27

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

In May 2014, DLTR made a non-binding proposal to acquire FDO for between $68 and $70 per share, with 75% of the consideration in cash

- DLTR would not expect to require approval of the merger by DLTR�s stockholders

- The proposal was conditioned on, among other things, Mr. Levine entering into a commitment to remain employed by FDO following the closing of the transaction

- Mr. Levine explained that he would be unwilling and unable to negotiate the terms of his post-closing contractual arrangements while material terms for a business combination transaction remained open and before he had instructions from his board to proceed with such negotiations

The FDO board rejected this proposal, but considered the absence of a DLTR stockholder vote to be favorable to FDO, as third parties, in particular DG, could not impede the consummation of an executed merger agreement between DLTR and FDO by making a bid for DLTR conditioned on DLTR�s abandonment of the merger with FDO.

- The FDO board also reiterated its instructions to Mr. Levine to refrain from engaging in any negotiations with DLTR about his post-closing contractual arrangements.

The FDO board directed senior management to communicate to DLTR that DLTR�s proposal was inadequate, that FDO remained not-for-sale but that FDO would at least consider a more competitive offer

FAMILY DOLLAR.

28

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

On June 6, 2014, Carl Icahn announced that he and certain of his affiliates (�Icahn�) beneficially owned 9.39% of FDO stock, and that they wished to explore strategies to enhance stockholder value, including exploring strategic alternatives with FDO.

- Shortly thereafter, Icahn announced that FDO should sell itself

- In subsequent discussions with Icahn, Icahn repeatedly pushed for a sale of FDO to DG and stated that he might call DG directly to ask them to consider a transaction

FDO proposed to DG, most recently on June 9, 2014, that the parties� respective antitrust experts meet to discuss a combination of the two companies; DG rejected these proposed meetings

FDO no longer has the flexibility to engage freely in meetings with DG

- The merger agreement with DLTR contains a customary provision that permits FDO to enter into discussions and share information with DG or any other third party only if the FDO board determines that, among other conclusions, the third party has made a bona fide, unsolicited proposal that would be reasonably expected to lead to a superior proposal that is �reasonably likely to be completed on the terms proposed�

FAMILY DOLLAR.

29

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

On June 13, 2014, DLTR increased the price specified in its previous proposal to $72, which the FDO board subsequently rejected

The most recent meeting between FDO and DG occurred on June 19, 2014, against a backdrop where FDO was widely considered to be a takeover target

- Carl Icahn, Bill Ackman, John Paulson, as well as Trian Fund, had all advocated for FDO to sell itself in recent years, including a series of bold pronouncements to this effect by Icahn in the first half of June 2014

- Over the past year, analysts from a number of prominent investment banks had published reports indicating that FDO is, should be or is about to be in play to be sold, including two such reports in the first 10 days of June 2014

FAMILY DOLLAR.

30

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

On June 19, 2014, Mr. Levine and an independent director from FDO met with Mr. Dreiling and a director from DG:

� Mr. Levine noted to the representatives of DG that Mr. Icahn had highlighted the possibility of a sale to DLTR. Mr. Levine could not say anything more directly about FDO�s then-ongoing talks with DLTR due to customary restrictions under FDO�s confidentiality agreement with DLTR

� Mr. Levine expressly asked the representatives of DG to make a proposal to acquire FDO; Representatives of DG responded:

Stockholders of DG had been pressuring DG to make a proposal to FDO, but DG was not interested in making a proposal at this time

FDO�s stock price was inflated due to speculation about a business combination with DG

DG was considering taking actions in the near future to quell market expectations that a DG-FDO business combination was a current priority for DG, including the issuance of a press release or communications to one or more DG shareholders that DG was not interested or the announcement of a new share repurchase program

DG indicated it was important for DG to signal to the market that DG had no current intention to pursue a transaction with FDO

FAMILY DOLLAR.

31

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

On June 20, 2014, a day after the June 19 meeting with DG where DG declined to make a bid for FDO, representatives of DLTR met with FDO and increased the price of its proposal to $74 per share. Mr. Levine indicated that this price proposal remained too low of a price. Mr. Sasser subsequently increased the proposed price to $74.50 per share as DLTR�s best and final price and conditioned this price on FDO�s agreeing to a six week period of exclusivity to permit DLTR to conduct due diligence and negotiate the transaction

On June 24, 2014, the FDO board met to consider the DLTR proposal. The board considered:

� The absence of interest from DG at that time and absence of any inbound inquiries about a possible transaction despite statements by prominent stockholders and analysts about how the company should be or was in play for a sale

� The remoteness of the likelihood that any other bidder could offer comparable value or would be interested in offering comparable value

� The proposed exclusivity agreement with DLTR that would expire, subject to certain exceptions, on July 28, 2014

On June 25, 2014, FDO and DLTR executed an exclusivity letter which, subject to certain exceptions, provided for an exclusivity period expiring on July 28, 2014

FAMILY DOLLAR.

32

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

On June 27, 2014, DG issued a press release announcing that Mr. Dreiling intended to retire as chief executive officer of DG

� The media and Icahn publicly observed that this development indicated that DG would not be or would be unlikely to be pursuing an acquisition of FDO

� Similarly, FDO viewed this announcement as reinforcing the message of June 19, 2014 that DG was not interested in a business combination transaction with FDO at that time

During late June and July 2014, representatives of DLTR and FDO negotiated a merger agreement and conducted due diligence of each other, during which FDO management kept the FDO board and board committee apprised of developments:

� In the evening of July 25, 2014, DLTR and FDO reached agreement on all material terms of the merger agreement

� Subsequent to July 25, as noted above, Mr. Levine began negotiations on the terms of his continued employment following the closing of the transaction

� On July 27, 2014, the FDO board met to consider and approve the terms of the merger agreement with DLTR

FAMILY DOLLAR.

33

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

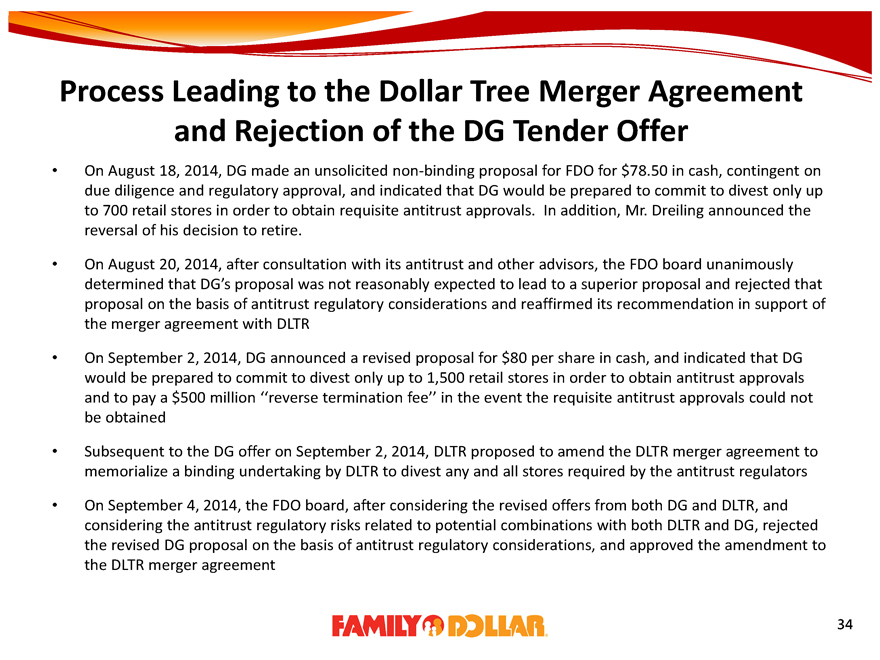

On August 18, 2014, DG made an unsolicited non-binding proposal for FDO for $78.50 in cash, contingent on due diligence and regulatory approval, and indicated that DG would be prepared to commit to divest only up to 700 retail stores in order to obtain requisite antitrust approvals. In addition, Mr. Dreiling announced the reversal of his decision to retire.

On August 20, 2014, after consultation with its antitrust and other advisors, the FDO board unanimously determined that DG�s proposal was not reasonably expected to lead to a superior proposal and rejected that proposal on the basis of antitrust regulatory considerations and reaffirmed its recommendation in support of the merger agreement with DLTR

On September 2, 2014, DG announced a revised proposal for $80 per share in cash, and indicated that DG would be prepared to commit to divest only up to 1,500 retail stores in order to obtain antitrust approvals and to pay a $500 million �reverse termination fee� in the event the requisite antitrust approvals could not be obtained

Subsequent to the DG offer on September 2, 2014, DLTR proposed to amend the DLTR merger agreement to memorialize a binding undertaking by DLTR to divest any and all stores required by the antitrust regulators

On September 4, 2014, the FDO board, after considering the revised offers from both DG and DLTR, and considering the antitrust regulatory risks related to potential combinations with both DLTR and DG, rejected the revised DG proposal on the basis of antitrust regulatory considerations, and approved the amendment to the DLTR merger agreement

FAMILY DOLLAR.

34

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

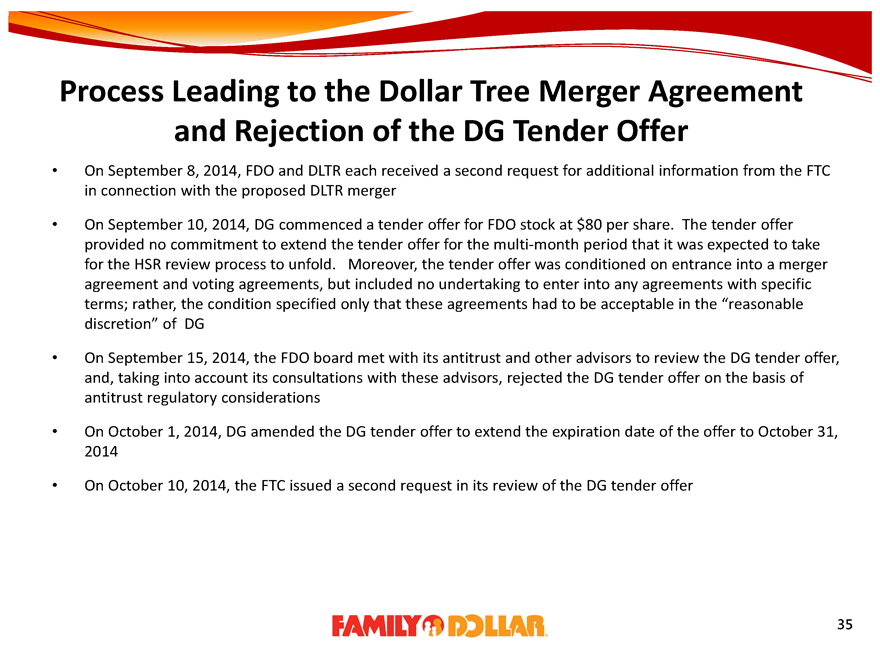

On September 8, 2014, FDO and DLTR each received a second request for additional information from the FTC in connection with the proposed DLTR merger

On September 10, 2014, DG commenced a tender offer for FDO stock at $80 per share. The tender offer provided no commitment to extend the tender offer for the multi-month period that it was expected to take for the HSR review process to unfold. Moreover, the tender offer was conditioned on entrance into a merger agreement and voting agreements, but included no undertaking to enter into any agreements with specific terms; rather, the condition specified only that these agreements had to be acceptable in the �reasonable discretion� of DG

On September 15, 2014, the FDO board met with its antitrust and other advisors to review the DG tender offer, and, taking into account its consultations with these advisors, rejected the DG tender offer on the basis of antitrust regulatory considerations

On October 1, 2014, DG amended the DG tender offer to extend the expiration date of the offer to October 31, 2014

On October 10, 2014, the FTC issued a second request in its review of the DG tender offer

FAMILY DOLLAR.

35

�

Process Leading to the Dollar Tree Merger Agreement and Rejection of the DG Tender Offer

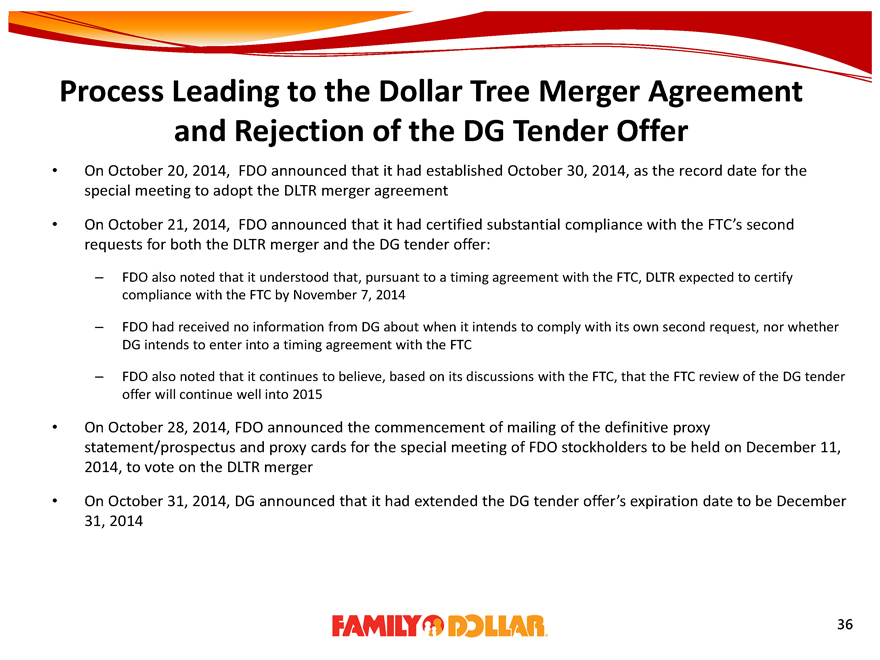

On October 20, 2014, FDO announced that it had established October 30, 2014, as the record date for the special meeting to adopt the DLTR merger agreement

On October 21, 2014, FDO announced that it had certified substantial compliance with the FTC�s second requests for both the DLTR merger and the DG tender offer:

� FDO also noted that it understood that, pursuant to a timing agreement with the FTC, DLTR expected to certify compliance with the FTC by November 7, 2014

� FDO had received no information from DG about when it intends to comply with its own second request, nor whether DG intends to enter into a timing agreement with the FTC

� FDO also noted that it continues to believe, based on its discussions with the FTC, that the FTC review of the DG tender offer will continue well into 2015

On October 28, 2014, FDO announced the commencement of mailing of the definitive proxy statement/prospectus and proxy cards for the special meeting of FDO stockholders to be held on December 11, 2014, to vote on the DLTR merger

On October 31, 2014, DG announced that it had extended the DG tender offer�s expiration date to be December 31, 2014

FAMILY DOLLAR.

36

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Stockholder Alert: Robbins LLP Informs Investors of the Class Action Filed Against Compass Minerals International, Inc. (CMP)

- Aterian Sets Date for First Quarter 2024 Earnings Announcement & Investor Conference Call

- ADSK INVESTOR ALERT: ROSEN, TOP RANKED INVESTOR COUNSEL, Encourages Autodesk, Inc. Investors to Secure Counsel Before Important Deadline in Securities Class Action First Filed by the Firm – ADSK

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!