Form 6-K SUNCOR ENERGY INC For: Feb 04

Tweet

Tweet Share

ShareQuickLinks -- Click here to rapidly navigate through this document

FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Report

of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of: February, 2016 |

Commission File Number: 1-12384 |

SUNCOR ENERGY INC.

(Name of registrant)

150 – 6th Avenue S.W.

P.O. Box 2844

Calgary, Alberta

Canada, T2P 3E3

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F |

o | Form 40-F | ý |

Indicate

by check mark if the registrant is submitting the Form 6-K in paper as permitted by

Regulation S-T Rule 101(b)(1): o

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by

Regulation S-T Rule 101(b)(7): o

The Registrant's Report to Shareholders for the quarter ended December 31, 2015, included as Exhibit 99.1 of this Form 6-K, is incorporated by reference into and as an exhibit to, as applicable, the following of Registrant's Registration Statements under the Securities Act of 1933: Form S-8 (File No. 333-87604), Form S-8 (File No. 333-112234), Form S-8 (File No. 333-118648), Form S-8 (File No. 333-124415), Form S-8 (File No. 333-149532), Form S-8 (File No. 333-161021), Form S-8 (File No. 333-161029), Form F-10 (File No. 333-196501), Form F-80 (File No. 333-207268) and Form F-80 (File No. 333-209087).

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

SUNCOR ENERGY INC. |

|||

Date: February 4, 2016 |

||||

|

||||

|

By: |

"Shawn Poirier" |

||

| Exhibit | Description of Exhibit | |

|---|---|---|

99.1 |

Report to Shareholders for the fourth quarter ended December 31, 2015 | |

99.2 |

News release dated February 3, 2016, Suncor Energy reports fourth quarter results |

SIGNATURES

EXHIBIT INDEX

QuickLinks -- Click here to rapidly navigate through this document

EXHIBIT 99.1

Report to Shareholders for the fourth quarter ended December 31, 2015

FOURTH QUARTER 2015

Report to shareholders for the period ended December 31, 2015

![]()

Suncor Energy reports fourth quarter results

All financial figures are unaudited and presented in Canadian dollars (Cdn$) unless noted otherwise. Production volumes are presented on a working-interest basis, before royalties, unless noted otherwise. Certain financial measures in this document are not prescribed by Canadian generally accepted accounting principles (GAAP). For a description of these non-GAAP financial measures, see the Non-GAAP Financial Measures Advisory section of this Report to Shareholders (this document). See also the Advisories section of this document. References to Oil Sands operations production and cash operating costs exclude Suncor's interest in Syncrude's operations.

"In 2015 we generated cash flow that exceeded our annual sustaining capital and dividend commitments," said Steve Williams, president and chief executive officer. "Our integrated business model, our ability to reduce costs, and our relentless focus on operational discipline made this possible. As a result, we are well positioned to weather the current low crude oil price environment."

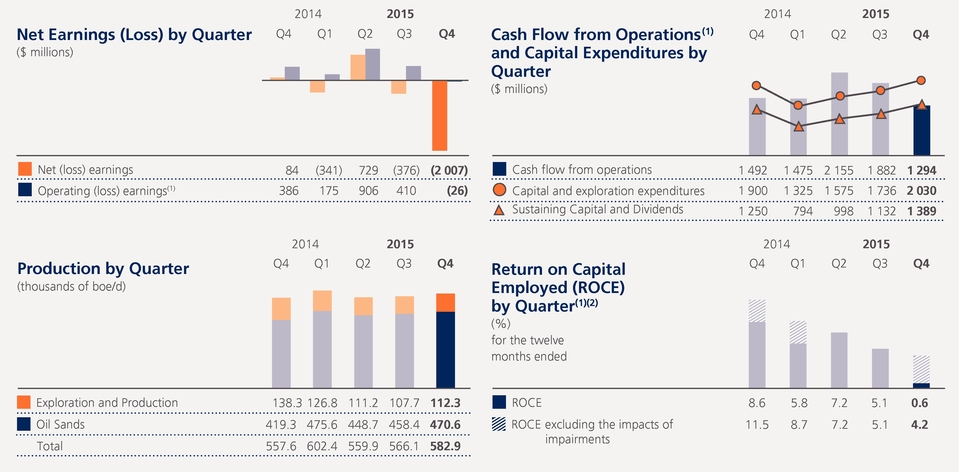

Highlights of the fourth quarter of 2015 include:

- •

- Cash

flow from operations(1) of $1.294 billion ($0.90 per common share), and an operating loss(1) of $26 million ($0.02 per common

share), driven by lower crude oil prices and a Refining and Marketing first-in, first-out (FIFO) loss of $77 million, partially offset by increased refining margins.

- •

- Net

loss of $2.007 billion ($1.38 per common share), due to non-cash asset writedowns, which were a result of the depressed commodity cycle, and a foreign exchange

loss on U.S. dollar denominated debt.

- •

- Oil

Sands operations cash operating costs per barrel(1) decreased to $28.00 for the fourth quarter of 2015, which was driven by strong production of

439,700 barrels per day (bbls/d), continued cost reduction initiatives, reduced unplanned maintenance activities and lower natural gas prices.

- •

- Effective

January 1, 2016, nameplate capacity of Firebag increased from 180,000 bbls/d to 203,000 bbls/d, as a result of completing cost-effective

debottleneck activities.

- •

- Subsequent to the end of the fourth quarter, Suncor and Canadian Oil Sands Limited (COS) reached an agreement for COS and its Board of Directors to support Suncor's offer to purchase all of the shares of COS for consideration of 0.28 of a Suncor share for each COS share. The transaction was valued at $6.6 billion at the time of the agreement.

- (1)

- Non-GAAP

financial measures. See page 4 for a reconciliation of net earnings to operating (loss) earnings. ROCE excludes capitalized costs related to major projects in

progress. See the Non-GAAP Financial Measures Advisory section of this document.

- (2)

- ROCE, excluding the impacts of impairments of $1.238 billion in the second quarter of 2014 and $1.599 billion in the fourth quarter of 2015, would have been 11.5%, 8.7%, and 4.2% for the fourth quarter of 2014, first quarter of 2015, and fourth quarter of 2015, respectively.

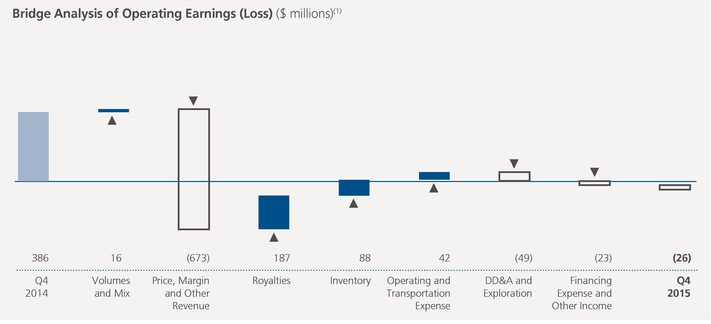

Suncor recorded a fourth quarter 2015 operating loss of $26 million ($0.02 per common share), including a FIFO loss of $77 million, and cash flow from operations of $1.294 billion ($0.90 per common share) reflecting the lower crude oil price environment, compared to operating earnings of $386 million ($0.27 per common share), including a FIFO loss of $372 million, and cash flow from operations of $1.492 billion ($1.03 per common share), in the prior year quarter. Highlights in the fourth quarter of 2015 included a favourable downstream pricing environment, increased production from Oil Sands operations, and lower operating costs.

For the twelve months ended December 31, 2015, free cash flow(1) was $139 million, compared to $2.097 billion for the twelve months ended December 31, 2014.

A net loss of $2.007 billion ($1.38 per common share) was recorded in the fourth quarter of 2015, compared with net earnings of $84 million ($0.06 per common share) in the prior year quarter. Net loss for the fourth quarter of 2015 was impacted by the same factors influencing the operating loss and included $1.599 billion of non-cash impairment charges and an unrealized after-tax foreign exchange loss of $382 million on the revaluation of U.S. dollar denominated debt. Net earnings in the prior year quarter included the impact of an unrealized after-tax foreign exchange loss of $302 million.

Operating Results

Suncor's total upstream production increased to 582,900 barrels of oil equivalent per day (boe/d) in the fourth quarter of 2015, compared with 557,600 boe/d in the prior year quarter, primarily due to strong reliability in Oil Sands operations.

Oil Sands operations production increased to 439,700 bbls/d in the fourth quarter of 2015, compared to 384,200 bbls/d in the prior year quarter, primarily due to record In Situ production and reliable operations across all assets following the completion of planned maintenance early in the quarter.

Cash operating costs per barrel for Oil Sands operations decreased in the fourth quarter of 2015 to $28.00/bbl, compared to $34.45/bbl in the prior year quarter, due to higher production combined with lower operating expenses as a result of cost reduction initiatives, lower unplanned maintenance and lower natural gas prices.

"We have surpassed the reliability and cost reduction targets we established in early 2015," said Williams. "Operating costs across the organization are down almost $1 billion from last year, while Oil Sands upgrading reliability exceeded 90%, more than a year ahead of our original plan."

Suncor's share of Syncrude production was 30,900 bbls/d in the fourth quarter of 2015, compared to 35,100 bbls/d in the prior year quarter. The decrease was primarily due to unplanned maintenance activities during the fourth quarter of 2015.

Production volumes in Exploration and Production (E&P) decreased to 112,300 boe/d in the fourth quarter of 2015, compared to 138,300 boe/d in the prior year quarter, primarily due to shut-in production in Libya, natural declines at Terra Nova and temporary export pipeline constraints that impacted Buzzard, partially offset by higher production at Golden Eagle. Production in Libya temporarily resumed at the start of the quarter, but was shut in again in November. Libya continues to be impacted by political unrest, with the timing of a return to normal operations remaining uncertain.

During the fourth quarter of 2015, Refining and Marketing completed planned maintenance at the Montreal refinery. Average refinery utilization decreased to 93% in the fourth quarter, compared to 95% in the prior year quarter, primarily driven by unplanned maintenance at the Edmonton refinery and lower distillate demand in Western Canada.

Strategy Update

Subsequent to the end of the fourth quarter, Suncor and COS reached an agreement to support Suncor's offer to purchase all of the shares of COS for 0.28 of a Suncor share for each COS share. The offer has the support of the Boards of Directors of both companies, and expires on February 5, 2016. The transaction value at the time of the agreement of approximately $6.6 billion includes COS' estimated debt of $2.4 billion.

- (1)

- Non-GAAP financial measure. See the Non-GAAP Financial Measures Advisory section of this document.

2 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

"We are pleased that the Board of COS is supporting our offer," said Williams. "We believe that, working with the operator, we can drive real improvements in Syncrude's performance with a larger ownership interest, creating value for our shareholders."

Suncor continues to deliver on its commitment to add shareholder value and invest in long-term profitable growth in its core asset areas, while maintaining a strong financial position. In addition to extending the offer to COS shareholders, the company also completed its acquisition of an additional 10% working interest in the Fort Hills oil sands project from Total E&P Canada Ltd. for $360 million. Suncor's share in the project is now 50.8%.

To maintain our strong financial position and flexibility, Suncor has reduced its capital guidance for 2016 to a range of $6.0 to $6.5 billion from $6.7 to $7.3 billion issued in November of 2015. The capital spending reduction is not anticipated to impact the company's near term production targets.

Enbridge's Line 9 reversal was commissioned during the fourth quarter of 2015. The reversal will provide Suncor the flexibility of supplying its Montreal refinery with a full slate of inland-priced crude.

During the quarter, the Government of Alberta announced a new climate plan which includes a carbon pricing regime coupled with an overall emissions limit for the oil sands. The climate plan places some certainty on the future greenhouse gas (GHG) costs for Suncor, while the limit on oil sands emissions will force companies to ensure only the most profitable and efficient projects are developed.

The Government of Alberta conducted a review of the province's oil and gas royalties. Subsequent to year end, the new royalty system was announced and included no changes to the existing oil sand royalty rates, and improved transparency concerning disclosure of royalty information.

Oil Sands Operations

In the fourth quarter of 2015, Suncor safely completed planned maintenance at Upgrader 2 on a coker set, vacuum tower and hydrogen plant.

In Situ continued to focus on well pad construction to sustain existing production at Firebag and MacKay River, and successfully completed cost-effective debottlenecking activities at Firebag, which increased nameplate capacity from 180,000 bbls/d to 203,000 bbls/d.

Oil Sands Ventures

The Fort Hills project remains on schedule with construction more than 50% complete at the end of the fourth quarter. Spending during the quarter included engineering, procurement, module fabrication and site construction. The project is expected to deliver approximately 91,000 bbls/d of bitumen to Suncor, following the completion of the acquisition of an additional 10% working interest in the project during the fourth quarter. First oil is expected in the fourth quarter of 2017, and is expected to ramp up to 90% of capacity within twelve months thereafter.

Exploration and Production

Construction of the Hebron project continued in the fourth quarter of 2015, with first oil expected in late 2017. Effective January 1, 2016, working interests in the Hebron project have been reset. As a result, Suncor's working interest in the project decreased from 22.7% to 21.0%, with Suncor to be reimbursed for costs incurred to December 31, 2015.

Development drilling at Golden Eagle continued through the fourth quarter. Exploration drilling at the deepwater Shelburne Basin offshore Nova Scotia commenced in the fourth quarter, and will continue during 2016.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 3

Operating (Loss) Earnings Reconciliation(1)

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | |||||||

|

|

|||||||||||

| Net (loss) earnings | (2 007 | ) | 84 | (1 995 | ) | 2 699 | |||||

|

|

|||||||||||

| Unrealized foreign exchange loss on U.S. dollar denominated debt | 382 | 302 | 1 930 | 722 | |||||||

|

|

|||||||||||

| Impairments(2) | 1 599 | — | 1 599 | 1 238 | |||||||

|

|

|||||||||||

| Impact of income tax rate adjustments on deferred taxes(3) | — | — | 17 | — | |||||||

|

|

|||||||||||

| Gain on significant disposal(4) | — | — | (68 | ) | (61 | ) | |||||

|

|

|||||||||||

| Restructuring charges(5) | — | — | 57 | — | |||||||

|

|

|||||||||||

| Insurance proceeds(6) | — | — | (75 | ) | — | ||||||

|

|

|||||||||||

| Reserves redetermination(7) | — | — | — | (32 | ) | ||||||

|

|

|||||||||||

| Income tax charge(8) | — | — | — | 54 | |||||||

|

|

|||||||||||

| Operating (loss) earnings(1) | (26 | ) | 386 | 1 465 | 4 620 | ||||||

|

|

|||||||||||

- (1)

- Operating

(loss) earnings is a non-GAAP financial measure. All reconciling items are presented on an after-tax basis. See the Non-GAAP Financial Measures Advisory section of

this document.

- (2)

- After-tax

impairment charges of $798 million on certain offshore E&P assets as a result of declining crude oil pricing, $415 million (Q2

2014 – $297 million) against the company's Libyan assets, $290 million (Q2 2014 – $718 million) on the

company's interest in the Joslyn mining project, and $96 million (Q2 2014 – $223 million) related to certain assets in the Oil Sands segment

following a review of repurpose options due to previously revised growth strategies in the fourth quarter of 2015.

- (3)

- Adjustments

to the company's deferred income taxes from a 12% decrease in the U.K. tax rate on oil and gas profits from the North Sea in the first quarter of 2015 of

$406 million, and a 2% increase in the Alberta corporate income tax rate in the second quarter of 2015 of $423 million.

- (4)

- After-tax

gain related to the sale of the company's Wilson Creek natural gas assets in the E&P segment in the third quarter of 2014 and the after-tax gain related to the sale

of the company's share of certain assets and liabilities of Pioneer Energy in the Refining and Marketing segment in the second quarter of 2015.

- (5)

- Restructuring

charges related to cost reduction initiatives in the Corporate segment recorded in the first quarter of 2015.

- (6)

- Business

interruption insurance proceeds recorded in the first quarter of 2015 for the Terra Nova asset in the E&P segment.

- (7)

- Reserves

redetermination of 1.2 million barrels of oil receivable recorded in the second quarter of 2014 related to an interest in a Norwegian asset that Suncor previously

owned.

- (8)

- Represents a current income tax and associated interest charge recorded in the third quarter of 2014 related to the timing of tax depreciation deductions taken on certain capital expenditures incurred in a prior period in the Oil Sands segment.

Corporate Guidance

Suncor has reduced its capital guidance for 2016 to a range of $6.0 to $6.5 billion from $6.7 to $7.3 billion issued on November 17, 2015, in part due to the deferral of Firebag planned maintenance to 2017.

The following 2016 full year outlook assumptions have also been adjusted: Brent at Sullom Voe to US$40/bbl from US$55/bbl, WTI at Cushing to US$39/bbl from US$50/bbl, WCS at Hardisty to US$26/bbl from US$35/bbl, and Cdn/US exchange rate from $0.75 to $0.70. For further details and advisories regarding Suncor's 2016 corporate guidance, see www.suncor.com/guidance.

Measurement Conversions

Certain natural gas volumes in this report to shareholders have been converted to boe on the basis of one bbl to six mcf. See the Advisories section of this document.

4 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

FOURTH QUARTER DISCUSSION

February 3, 2016

Additional information about Suncor filed with Canadian securities regulatory authorities and the United States Securities and Exchange Commission (SEC), including quarterly and annual reports and Suncor's Annual Information Form dated February 26, 2015 (the 2014 AIF), which is also filed with the SEC under cover of Form 40-F, is available online at www.sedar.com, www.sec.gov and our website www.suncor.com. Information contained in or otherwise accessible through our website does not form part of this document, and is not incorporated into this document by reference.

References to "we", "our", "Suncor", or "the company" mean Suncor Energy Inc. and the company's subsidiaries and interests in associates and jointly controlled entities, unless the context otherwise requires.

Table of Contents

| 1. | Advisories | 5 | ||

| 2. | Fourth Quarter Highlights | 6 | ||

| 3. | Consolidated Financial Information | 7 | ||

| 4. | Segment Results and Analysis | 12 | ||

| 5. | Capital Investment Update | 21 | ||

| 6. | Financial Condition and Liquidity | 23 | ||

| 7. | Quarterly Financial Data | 26 | ||

| 8. | Other Items | 27 | ||

| 9. | Non-GAAP Financial Measures Advisory | 28 | ||

| 10. | Common Abbreviations | 32 | ||

| 11. | Forward-Looking Information | 33 |

1. ADVISORIES

Basis of Presentation

Unless otherwise noted, all financial information has been prepared in accordance with Canadian generally accepted accounting principles (GAAP), specifically International Accounting Standard (IAS) 34 Interim Financial Reporting as issued by the International Accounting Standards Board, which is within the framework of International Financial Reporting Standards (IFRS).

All financial information is reported in Canadian dollars, unless otherwise noted. Production volumes are presented on a working-interest basis, before royalties, unless otherwise noted. Certain prior year amounts in the Consolidated Statements of Comprehensive (Loss) Income have been reclassified to conform to the current year's presentation.

Non-GAAP Financial Measures

Certain financial measures in this document – namely operating (loss) earnings, cash flow from operations, return on capital employed (ROCE), Oil Sands cash operating costs, free cash flow, and last-in, first-out (LIFO) – are not prescribed by GAAP. Operating (loss) earnings, Oil Sands cash operating costs and LIFO are defined in the Non-GAAP Financial Measures Advisory section of this document and reconciled to GAAP measures in the Consolidated Financial Information and Segment Results and Analysis sections of this document. Cash flow from operations, ROCE and free cash flow are defined and reconciled to GAAP measures in the Non-GAAP Financial Measures Advisory section of this document.

Risk Factors and Forward-Looking Information

The company's financial and operational performance is potentially affected by a number of factors, including, but not limited to, the factors described within the Forward-Looking Information section of this document. This document contains forward-looking information based on Suncor's current expectations, estimates, projections and assumptions. This information is provided to assist readers in understanding the company's future plans and expectations and may not be appropriate for other purposes. Refer to the Forward-Looking Information section of this document for information on the material risk factors and assumptions underlying our forward-looking information.

Measurement Conversions

Certain crude oil and natural gas liquids volumes have been converted to mcfe on the basis of one bbl to six mcf. Also, certain natural gas volumes have been converted to boe or mboe on the same basis. Any figure presented in mcfe, boe or mboe may be misleading, particularly if used in isolation. A conversion ratio of one bbl of crude oil or natural gas liquids to six mcf of natural gas is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, conversion on a 6:1 basis may be misleading as an indication of value.

Common Abbreviations

For a list of abbreviations that may be used in this document, refer to the Common Abbreviations section of this document.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 5

- •

- Fourth quarter financial results.

- •

- Net

loss for the fourth quarter of 2015 was $2.007 billion, compared to net earnings of $84 million in the prior year quarter. Net loss for the fourth quarter

of 2015 included impairment charges of $1.599 billion and an unrealized after-tax foreign exchange loss on the revaluation of U.S. dollar denominated debt of $382 million. Net

earnings in the prior year quarter included the impact of an unrealized after-tax foreign exchange loss of $302 million.

- •

- Operating

loss(1) for the fourth quarter of 2015 was $26 million, including a first-in, first-out (FIFO) loss of $77 million, compared to

operating earnings of $386 million, including a FIFO loss of $372 million, for the prior year quarter. The decrease was driven by lower crude oil price realizations, partially offset by

a favourable downstream pricing environment, increased Oil Sands operations production, lower royalties and lower operating costs compared to the prior year quarter.

- •

- Cash

flow from operations(1) was $1.294 billion for the fourth quarter of 2015, compared to $1.492 billion for the fourth quarter of 2014. The

decrease was largely due to the same factors that impacted operating earnings. Free cash flow(1) was $139 million for the twelve months ended December 31, 2015, compared to

$2.097 billion for the twelve months ended December 31, 2014.

- •

- ROCE(1)

(excluding major projects in progress) decreased to 0.6% for the twelve months ended December 31, 2015, compared to 8.6% for the twelve months

ended December 31, 2014, and has trended unfavourably throughout 2015 as a result of the depressed crude oil price environment, offset by lower operating costs and strong downstream

performance. ROCE for the twelve months ended December 31, 2015 was 4.2% when the impacts of the impairment charges from the fourth quarter of 2015 are excluded.

- •

- Higher downstream refining margins on strong location differentials helped drive operating earnings of $498 million for the Refining and

Marketing segment in the quarter. The reversal of Enbridge's Line 9 will provide Suncor with the flexibility to supply its Montreal refinery with a full

slate of inland-priced crude.

- •

- Oil Sands operations cash operating costs(1) averaged $28.00/bbl for the quarter, compared to $34.45/bbl in the prior year

quarter. Increased production, a continued focus on cost reductions, lower unplanned maintenance and lower natural gas prices resulted in a 19% decrease quarter

over quarter.

- •

- Strong Oil Sands production demonstrates Suncor's ongoing commitment to operational discipline and delivering reliable

operations. Oil Sands operations production was 439,700 bbls/d, an increase of 14% from the prior year quarter, with record In Situ production of

233,300 bbls/d achieved in the quarter.

- •

- Firebag nameplate capacity increased from 180,000 bbls/d to 203,000 bbls/d. Cost-effective

debottlenecking activities have been completed at Firebag, with sustained production levels in excess of 180,000 bbls/d in 2015.

- •

- Suncor Energy and Canadian Oil Sands Limited (COS) reach agreement to support the offer by Suncor to purchase all of the shares of

COS. Subsequent to the fourth quarter of 2015, Suncor reached an agreement with COS to support Suncor's offer to purchase all of the shares of COS for

consideration of 0.28 of a Suncor share per COS share. The transaction was valued at $6.6 billion at the time of the agreement.

- •

- Substantial completion of detailed engineering work at Fort Hills. Construction was more

than 50% complete by

the end of the fourth quarter, with first oil expected in the fourth quarter of 2017. In addition, the company completed its acquisition of an additional 10% of the project.

- •

- Suncor continued to return cash to shareholders. Suncor has maintained a strong financial

position, returning

$419 million to shareholders through dividends during the fourth quarter of 2015.

- (1)

- Operating (loss) earnings, cash flow from operations, free cash flow, ROCE and Oil Sands cash operating costs are non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this document.

6 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

3. CONSOLIDATED FINANCIAL INFORMATION

Financial Highlights

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | |||||||

|

|

|||||||||||

| Net (loss) earnings | |||||||||||

|

|

|||||||||||

| Oil Sands | (616 | ) | 180 | (856 | ) | 1 776 | |||||

|

|

|||||||||||

| Exploration and Production | (1 263 | ) | 198 | (758 | ) | 653 | |||||

|

|

|||||||||||

| Refining and Marketing | 498 | 173 | 2 266 | 1 692 | |||||||

|

|

|||||||||||

| Corporate, Energy Trading and Eliminations | (626 | ) | (467 | ) | (2 647 | ) | (1 422 | ) | |||

|

|

|||||||||||

| Total | (2 007 | ) | 84 | (1 995 | ) | 2 699 | |||||

|

|

|||||||||||

| Operating (loss) earnings(1) | |||||||||||

|

|

|||||||||||

| Oil Sands | (230 | ) | 180 | (111 | ) | 2 771 | |||||

|

|

|||||||||||

| Exploration and Production | (50 | ) | 198 | 7 | 857 | ||||||

|

|

|||||||||||

| Refining and Marketing | 498 | 173 | 2 234 | 1 692 | |||||||

|

|

|||||||||||

| Corporate, Energy Trading and Eliminations | (244 | ) | (165 | ) | (665 | ) | (700 | ) | |||

|

|

|||||||||||

| Total | (26 | ) | 386 | 1 465 | 4 620 | ||||||

|

|

|||||||||||

| Cash flow from (used in) operations(1) | |||||||||||

|

|

|||||||||||

| Oil Sands | 467 | 875 | 2 835 | 5 400 | |||||||

|

|

|||||||||||

| Exploration and Production | 257 | 401 | 1 386 | 1 909 | |||||||

|

|

|||||||||||

| Refining and Marketing | 596 | 240 | 2 872 | 2 178 | |||||||

|

|

|||||||||||

| Corporate, Energy Trading and Eliminations | (26 | ) | (24 | ) | (287 | ) | (429 | ) | |||

|

|

|||||||||||

| Total | 1 294 | 1 492 | 6 806 | 9 058 | |||||||

|

|

|||||||||||

| Capital and Exploration Expenditures(2) | |||||||||||

|

|

|||||||||||

| Sustaining | 952 | 823 | 2 602 | 3 014 | |||||||

|

|

|||||||||||

| Growth | 949 | 970 | 3 618 | 3 516 | |||||||

|

|

|||||||||||

| Total | 1 901 | 1 793 | 6 220 | 6 530 | |||||||

|

|

|||||||||||

|

Twelve months ended December 31 |

|||||

| ($ millions) | 2015 | 2014 | |||

|

|

|||||

| Free Cash Flow(1) | 139 | 2 097 | |||

|

|

|||||

- (1)

- Non-GAAP

financial measures. Operating (loss) earnings are reconciled to net earnings below. See the Non-GAAP Financial Measures Advisory section of this document.

- (2)

- Excludes capitalized interest.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 7

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||

|

|

||||||||||

| Production volumes by segment | ||||||||||

|

|

||||||||||

| Oil Sands (mbbls/d) | 470.6 | 419.3 | 463.4 | 421.9 | ||||||

|

|

||||||||||

| Exploration and Production (mboe/d) | 112.3 | 138.3 | 114.4 | 113.0 | ||||||

|

|

||||||||||

| Total | 582.9 | 557.6 | 577.8 | 534.9 | ||||||

|

|

||||||||||

| Production mix | ||||||||||

|

|

||||||||||

| Crude oil and liquids / natural gas (%) | 99/1 | 99/1 | 99/1 | 99/1 | ||||||

|

|

||||||||||

| Refinery utilization (%) | 93 | 95 | 94 | 93 | ||||||

|

|

||||||||||

| Refinery crude oil processed (mbbls/d) | 430.2 | 440.8 | 432.1 | 427.5 | ||||||

|

|

||||||||||

Net Earnings

Suncor's consolidated net loss for the fourth quarter of 2015 was $2.007 billion, compared with net earnings of $84 million for the prior year quarter. Net loss for the year was $1.995 billion, compared to net earnings of $2.699 billion in the prior year. Net earnings were impacted by the same factors that influenced operating earnings described subsequently in this section of this document. Other items affecting net earnings over these periods included:

- •

- In

the fourth quarter of 2015, the company recorded after-tax impairment charges against property, plant and equipment and exploration and evaluation assets of

$359 million on White Rose, $331 million on Golden Eagle, $54 million on Terra Nova, and $54 million on Ballicatters, as a result of declining crude oil pricing, and

$290 million on the company's interest in the Joslyn mining project, due to uncertainty in the timing of development plans. In addition, $96 million of de-recognition charges were

recorded in Oil Sands following a review of certain assets that no longer fit with Suncor's growth strategies, and which could not be repurposed or otherwise deployed.

- •

- In

the fourth quarter of 2015, as a result of shut-in production due to the continued closure of certain Libyan export terminals, escalating political unrest, and increased

uncertainty with respect to the company's return to normal operations in the country, the company recorded an after-tax impairment charge of $415 million against property, plant and equipment

and exploration and evaluation assets.

- •

- The

after-tax unrealized foreign exchange loss on the revaluation of U.S. dollar denominated debt was $382 million for the fourth quarter of 2015 and

$1.930 billion for the twelve months of 2015, compared to $302 million for the fourth quarter of 2014 and $722 million for the twelve months of 2014.

- •

- In

the second quarter of 2015, the company recorded an after-tax gain of $68 million on the disposal of the company's share of certain assets and liabilities of

Pioneer Energy in the Refining and Marketing segment.

- •

- In

the second quarter of 2015, the company recorded a $423 million deferred income tax charge related to a 2% increase in the Alberta corporate income

tax rate.

- •

- In

the first quarter of 2015, the U.K. government enacted a decrease in the supplementary charge rate on oil and gas profits in the North Sea that reduced the

statutory tax rate on Suncor's earnings in the U.K. from 62% to 50%. The company revalued its deferred income tax balances, resulting in a one-time decrease to deferred income taxes of

$406 million.

- •

- In

the first quarter of 2015, the company recorded after-tax insurance proceeds of $75 million related to a claim on the Terra Nova asset in the Exploration and

Production (E&P) segment.

- •

- In

the first quarter of 2015, the company recorded after-tax restructuring charges of $57 million related to cost reduction initiatives in the Corporate segment.

- •

- In

the third quarter of 2014, the company recorded an after-tax gain of $61 million relating to the sale of its Wilson Creek natural gas assets in the

E&P segment.

- •

- In

the third quarter of 2014, the company recorded a current income tax expense adjustment and associated interest expense of $54 million related to the timing of tax

depreciation deductions taken on certain capital expenditures incurred in a prior period in the Oil Sands segment.

- •

- In the second quarter of 2014, Total E&P Canada Ltd. (Total E&P), the operator of the Joslyn mining project, together with Suncor and the other co-owners of the project agreed to scale back certain development activities in order to focus on engineering studies to further optimize the Joslyn project development plan. As a result of Suncor's assessment of expected future net cash flows and the uncertainty of the project, including the timing of the

8 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

development plans, Suncor recorded an after-tax charge to net earnings of $718 million against property, plant and equipment and exploration and evaluation assets.

- •

- In

the second quarter of 2014, as a result of the continued closure of certain Libyan export terminals and the company's view on production plans during the remaining term

of the production sharing agreements, the company recorded an after-tax impairment charge of $297 million against property, plant and equipment and exploration and evaluation assets.

- •

- In

the second quarter of 2014, the company recorded after-tax impairment charges of $223 million in Oil Sands following a review of certain assets that no longer fit

with Suncor's previously revised growth strategies and which could not be repurposed or otherwise deployed. Such assets included a pipeline and related compressor, as well as steam generator

components.

- •

- In the second quarter of 2014, the company recorded after-tax earnings of $32 million related to an agreement reached for Suncor to receive a reserves redetermination of 1.2 million barrels of oil related to an interest in a Norwegian asset that Suncor previously owned.

Operating (Loss) Earnings Reconciliation(1)(2)

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | ||||||

|

|

||||||||||

| Net (loss) earnings | (2 007 | ) | 84 | (1 995 | ) | 2 699 | ||||

|

|

||||||||||

| Unrealized foreign exchange loss on U.S. dollar denominated debt | 382 | 302 | 1 930 | 722 | ||||||

|

|

||||||||||

| Impact of income tax rate adjustments on deferred taxes | — | — | 17 | — | ||||||

|

|

||||||||||

| Gain on significant disposal | — | — | (68 | ) | (61 | ) | ||||

|

|

||||||||||

| Restructuring charges | — | — | 57 | — | ||||||

|

|

||||||||||

| Insurance proceeds | — | — | (75 | ) | — | |||||

|

|

||||||||||

| Impairments | 1 599 | — | 1 599 | 1 238 | ||||||

|

|

||||||||||

| Reserves redetermination | — | — | — | (32 | ) | |||||

|

|

||||||||||

| Income tax charge | — | — | — | 54 | ||||||

|

|

||||||||||

| Operating (loss) earnings(1) | (26 | ) | 386 | 1 465 | 4 620 | |||||

|

|

||||||||||

- (1)

- Operating

(loss) earnings is a non-GAAP financial measure. All reconciling items are presented on an after-tax basis. See the Non-GAAP Financial Measures Advisory section of

this document.

- (2)

- Refer to net earnings discussion above for descriptions of the adjustments.

- (1)

- For an explanation of this bridge analysis, see the Non-GAAP Financial Measures Advisory section of this document.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 9

Suncor's consolidated operating loss for the fourth quarter of 2015 was $26 million, compared to $386 million of operating earnings for the prior year quarter, primarily due to significantly lower upstream price realizations consistent with the decline in benchmark crude oil prices. The decrease was partially offset by a favourable downstream pricing environment, increased Oil Sands operations production, lower royalties resulting from the decrease in crude oil prices, and lower operating costs, compared to the prior year quarter.

Suncor's consolidated operating earnings were $1.465 billion for the twelve months of 2015, compared to $4.620 billion for the prior year period. The decrease was primarily due to the significantly lower upstream price realizations consistent with the decline in benchmark crude prices, partially offset by strong Oil Sands operations production due to improved reliability, lower operating costs, and a strong downstream pricing environment.

After-Tax Share-Based Compensation Expense (Recovery) by Segment

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | |||||

|

|

|||||||||

| Oil Sands | 17 | (3 | ) | 67 | 64 | ||||

|

|

|||||||||

| Exploration and Production | 2 | — | 8 | 11 | |||||

|

|

|||||||||

| Refining and Marketing | 9 | — | 39 | 37 | |||||

|

|

|||||||||

| Corporate, Energy Trading and Eliminations | 31 | (4 | ) | 120 | 139 | ||||

|

|

|||||||||

| Total share-based compensation expense (recovery) | 59 | (7 | ) | 234 | 251 | ||||

|

|

|||||||||

The after-tax share-based compensation expense increased to $59 million during the fourth quarter of 2015, compared to a recovery of $7 million during the prior year quarter, as a result of an increase in the company's share price in the fourth quarter of 2015 as compared to a decrease in the prior year quarter.

Business Environment

Commodity prices, refining crack spreads and foreign exchange rates are important factors that affect the results of Suncor's operations.

|

Average for three months ended December 31 |

Average for twelve months ended December 31 |

||||||||||

| 2015 | 2014 | 2015 | 2014 | ||||||||

|

|

|||||||||||

| WTI crude oil at Cushing | US$/bbl | 42.15 | 73.15 | 48.75 | 93.00 | ||||||

|

|

|||||||||||

| ICE Brent crude oil at Sullom Voe | US$/bbl | 44.70 | 77.00 | 53.60 | 99.50 | ||||||

|

|

|||||||||||

| Dated Brent/Maya crude oil FOB price differential | US$/bbl | 10.35 | 10.05 | 9.50 | 13.70 | ||||||

|

|

|||||||||||

| MSW at Edmonton | Cdn$/bbl | 53.55 | 75.95 | 57.60 | 94.85 | ||||||

|

|

|||||||||||

| WCS at Hardisty | US$/bbl | 27.70 | 58.90 | 35.25 | 73.60 | ||||||

|

|

|||||||||||

| Light/heavy differential for WTI at Cushing less WCS at Hardisty | US$/bbl | 14.50 | 14.25 | 13.50 | 19.40 | ||||||

|

|

|||||||||||

| Condensate at Edmonton | US$/bbl | 41.65 | 70.55 | 47.35 | 92.95 | ||||||

|

|

|||||||||||

| Natural gas (Alberta spot) at AECO | Cdn$/mcf | 2.45 | 3.60 | 2.65 | 4.50 | ||||||

|

|

|||||||||||

| Alberta Power Pool Price | Cdn$/MWh | 21.20 | 30.55 | 33.40 | 49.65 | ||||||

|

|

|||||||||||

| New York Harbor 3-2-1 crack(1) | US$/bbl | 13.60 | 16.15 | 19.70 | 19.65 | ||||||

|

|

|||||||||||

| Chicago 3-2-1 crack(1) | US$/bbl | 13.90 | 14.40 | 18.50 | 17.40 | ||||||

|

|

|||||||||||

| Portland 3-2-1 crack(1) | US$/bbl | 17.90 | 12.45 | 25.15 | 20.15 | ||||||

|

|

|||||||||||

| Gulf Coast 3-2-1 crack(1) | US$/bbl | 11.05 | 10.15 | 18.35 | 16.50 | ||||||

|

|

|||||||||||

| Exchange rate | US$/Cdn$ | 0.75 | 0.88 | 0.78 | 0.91 | ||||||

|

|

|||||||||||

| Exchange rate (end of period) | US$/Cdn$ | 0.72 | 0.86 | 0.72 | 0.86 | ||||||

|

|

|||||||||||

- (1)

- 3-2-1 crack spreads are indicators of the refining margin generated by converting three barrels of WTI into two barrels of gasoline and one barrel of diesel. The crack spreads presented here generally approximate the regions into which the company sells refined products through retail and wholesale channels.

10 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

Suncor's sweet SCO price realizations are influenced primarily by the price of WTI at Cushing and by the supply and demand for sweet SCO from Western Canada. Price realizations in the fourth quarter of 2015 for sweet SCO were negatively affected by a lower WTI price of US$42.15/bbl, compared to US$73.15/bbl in the prior year quarter, partially offset by a lower differential for SCO relative to WTI. Suncor produces sour SCO, the price of which is influenced by various crude benchmarks, including, but not limited to, MSW at Edmonton and WCS at Hardisty, and which can also be affected by prices negotiated for spot sales. Prices for MSW at Edmonton and WCS at Hardisty decreased in the fourth quarter of 2015 to $53.55/bbl and US$27.70 /bbl, respectively, compared to $75.95/bbl and US$58.90/bbl, respectively, in the prior year quarter, resulting in lower price realizations for sour SCO.

Bitumen production that Suncor does not upgrade is blended with diluent or SCO to facilitate delivery on pipeline systems. Net bitumen price realizations are therefore influenced by both prices for Canadian heavy crude oil (WCS at Hardisty is a common reference), prices for diluent (Condensate at Edmonton) and SCO. Bitumen price realizations can also be affected by bitumen quality and spot sales.

Suncor's price realizations for production from East Coast Canada and International assets are influenced primarily by the price for Brent crude. Brent crude pricing decreased to an average of US$44.70/bbl in the fourth quarter of 2015, compared to US$77.00/bbl in the prior year quarter.

Natural gas used in Suncor's Oil Sands and Refining operations is primarily referenced to Alberta spot prices at AECO. The average AECO benchmark decreased to $2.45/mcf in the fourth quarter of 2015, from $3.60/mcf in the prior year quarter.

Suncor's refining margins are influenced primarily by 3-2-1 crack spreads, which are industry indicators approximating the gross margin on a barrel of crude oil that is refined to produce gasoline and distillates, and by light/heavy and light/sour crude differentials. More complex refineries can earn greater refining margins by processing less expensive, heavier crudes. Crack spreads do not necessarily reflect the margins of a specific refinery. Crack spreads are based on current crude feedstock prices whereas actual refining margins are based on FIFO inventory accounting, where a delay exists between the time that feedstock is purchased, processed and sold to a third party. FIFO losses normally reflect a declining price environment for crude oil and finished products, whereas FIFO gains reflect an increasing price environment for crude oil and finished products. Specific refinery margins are further impacted by actual crude purchase costs, refinery configuration and refined products sales markets unique to that refinery.

Excess electricity produced in Suncor's Oil Sands business is sold to the Alberta Electric System Operator (AESO), with the proceeds netted against the cash operating cost per barrel metric. The Alberta power pool price decreased to an average of $21.20/MWh in the fourth quarter of 2015 from $30.55/MWh in the prior year quarter.

The majority of Suncor's revenue from the sale of oil and natural gas commodities is based on prices that are determined by or referenced to U.S. dollar benchmark prices. The majority of Suncor's expenditures are realized in Canadian dollars. In the fourth quarter of 2015, the Canadian dollar weakened in relation to the U.S. dollar as the average exchange rate decreased to US$0.75 per one Canadian dollar from US$0.88 per one Canadian dollar in the prior year quarter. This rate decrease had a positive impact on price realizations for the company during the fourth quarter.

Suncor also has assets and liabilities, notably most of the company's debt, which are denominated in U.S. dollars and translated to Suncor's reporting currency (Canadian dollars) at each balance sheet date. A decrease in the value of the Canadian dollar relative to the U.S. dollar from the previous balance sheet date increases the amount of Canadian dollars required to settle U.S. dollar denominated obligations.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 11

4. SEGMENT RESULTS AND ANALYSIS

OIL SANDS

Financial Highlights

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | |||||||

|

|

|||||||||||

| Gross revenues | 2 017 | 2 838 | 9 332 | 14 561 | |||||||

|

|

|||||||||||

| Less: Royalties | (10 | ) | (107 | ) | (114 | ) | (982 | ) | |||

|

|

|||||||||||

| Operating revenues, net of royalties | 2 007 | 2 731 | 9 218 | 13 579 | |||||||

|

|

|||||||||||

| Net (loss) earnings | (616 | ) | 180 | (856 | ) | 1 776 | |||||

|

|

|||||||||||

| Adjusted for: | |||||||||||

|

|

|||||||||||

| Impact of income tax rate adjustments on deferred taxes(1) | — | — | 359 | — | |||||||

|

|

|||||||||||

| Income tax charge | — | — | — | 54 | |||||||

|

|

|||||||||||

| Impairment of Joslyn mining project and other assets(2) | 386 | — | 386 | 941 | |||||||

|

|

|||||||||||

| Operating (loss) earnings(3) | (230 | ) | 180 | (111 | ) | 2 771 | |||||

|

|

|||||||||||

| Oil Sands operations | (231 | ) | 182 | (33 | ) | 2 696 | |||||

|

|

|||||||||||

| Oil Sands ventures | 1 | (2 | ) | (78 | ) | 75 | |||||

|

|

|||||||||||

| Cash flow from operations(3) | 467 | 875 | 2 835 | 5 400 | |||||||

|

|

|||||||||||

- (1)

- Adjustment

to the company's deferred income taxes resulting from a 2% increase in the Alberta corporate income tax rate in Q2 2015.

- (2)

- After-tax

impairment charges of $290 million on the company's interest in the Joslyn mining project and $96 million related to certain assets in Oil Sands

operations.

- (3)

- Non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this document.

- (1)

- For an explanation of this bridge analysis, see the Non-GAAP Financial Measures Advisory section of this document.

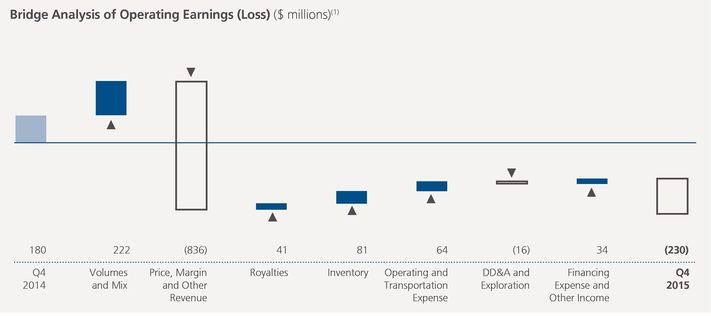

Operating loss for Oil Sands operations was $231 million, compared to operating earnings of $182 million in the prior year quarter. The decrease was primarily due to lower price realizations as a result of lower crude oil benchmark prices, partially offset by increased production, lower operating and transportation expenses as a result of the impact of cost reduction initiatives, lower unplanned maintenance activities, lower natural gas prices, and lower royalties.

Operating earnings for Oil Sands ventures were $1 million, compared to an operating loss of $2 million in the prior year quarter, primarily due to lower operating costs and lower royalties, partially offset by lower price realizations and decreased production.

12 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

Production Volumes(1)

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| (mbbls/d) | 2015 | 2014 | 2015 | 2014 | ||||||

|

|

||||||||||

| Upgraded product (SCO and diesel) | 292.2 | 276.3 | 320.1 | 289.1 | ||||||

|

|

||||||||||

| Non-upgraded bitumen | 147.5 | 107.9 | 113.5 | 101.8 | ||||||

|

|

||||||||||

| Oil Sands operations | 439.7 | 384.2 | 433.6 | 390.9 | ||||||

|

|

||||||||||

| Oil Sands ventures | 30.9 | 35.1 | 29.8 | 31.0 | ||||||

|

|

||||||||||

| Total | 470.6 | 419.3 | 463.4 | 421.9 | ||||||

|

|

||||||||||

- (1)

- Bitumen production from Oil Sands Base operations is upgraded, while bitumen production from In Situ operations is either upgraded or sold directly to customers, including Suncor's own refineries. Yields of SCO and diesel from Suncor's upgrading process are approximately 79% of bitumen feedstock input.

Sales Volumes

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| (mbbls/d) | 2015 | 2014 | 2015 | 2014 | ||||||

|

|

||||||||||

| Oil Sands operations sales volumes | ||||||||||

|

|

||||||||||

| Sweet SCO | 100.2 | 75.5 | 107.0 | 99.7 | ||||||

|

|

||||||||||

| Diesel | 29.4 | 31.2 | 31.3 | 30.7 | ||||||

|

|

||||||||||

| Sour SCO | 154.2 | 152.7 | 182.5 | 158.9 | ||||||

|

|

||||||||||

| Upgraded product | 283.8 | 259.4 | 320.8 | 289.3 | ||||||

|

|

||||||||||

| Non-upgraded bitumen | 136.3 | 110.2 | 107.7 | 101.4 | ||||||

|

|

||||||||||

| Oil Sands operations | 420.1 | 369.6 | 428.5 | 390.7 | ||||||

|

|

||||||||||

| Oil Sands ventures | 30.9 | 35.1 | 29.8 | 31.0 | ||||||

|

|

||||||||||

| Total | 451.0 | 404.7 | 458.3 | 421.7 | ||||||

|

|

||||||||||

Production volumes for Oil Sands operations increased to 439,700 bbls/d in the fourth quarter of 2015, compared to 384,200 bbls/d in the prior year quarter. The increase was primarily due to reliable operations across all assets, compared to the prior year quarter, which was impacted by unplanned maintenance at Upgrader 2 and on certain utility assets supporting upgrading and extraction. Planned upgrader maintenance was completed in the fourth quarter of 2015.

Sales volumes for Oil Sands operations increased to an average of 420,100 bbls/d in the fourth quarter of 2015, up from 369,600 bbls/d in the prior year quarter, due to higher production volumes. The SCO mix reflected higher sweet production due to less planned maintenance completed in the quarter. The prior year quarter included the impacts of planned and unplanned maintenance.

Inventory builds occurred in both quarters; however, the volumes built in the fourth quarter of 2015 had a relatively smaller impact on earnings due to the lower price environment.

Suncor's share of Syncrude production decreased to 30,900 bbls/d in the fourth quarter of 2015, compared to 35,100 bbls/d in the prior year quarter. The decrease was primarily due to unplanned maintenance activities associated with sulphur removal and water treatment assets, and an unplanned coker maintenance event that began late in the quarter.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 13

Bitumen Production

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||

|

|

||||||||||

| Oil Sands Base | ||||||||||

|

|

||||||||||

| Bitumen production (mbbls/d) | 292.4 | 254.1 | 307.3 | 274.4 | ||||||

|

|

||||||||||

| Bitumen ore mined (thousands of tonnes per day) | 433.7 | 384.6 | 461.3 | 408.5 | ||||||

|

|

||||||||||

| Bitumen ore grade quality (bbls/tonne) | 0.67 | 0.66 | 0.67 | 0.67 | ||||||

|

|

||||||||||

| In Situ | ||||||||||

|

|

||||||||||

| Bitumen production – Firebag (mbbls/d) | 198.8 | 182.2 | 186.9 | 172.0 | ||||||

|

|

||||||||||

| Bitumen production – MacKay River (mbbls/d) | 34.5 | 28.7 | 30.7 | 27.0 | ||||||

|

|

||||||||||

| Total In Situ bitumen production | 233.3 | 210.9 | 217.6 | 199.0 | ||||||

|

|

||||||||||

| Steam-to-oil ratio – Firebag | 2.7 | 2.6 | 2.6 | 2.8 | ||||||

|

|

||||||||||

| Steam-to-oil ratio – MacKay River | 3.0 | 2.9 | 2.9 | 2.9 | ||||||

|

|

||||||||||

Oil Sands Base bitumen production from mining and extraction activities increased to an average of 292,400 bbls/d in the fourth quarter of 2015 from 254,100 bbls/d in the prior year quarter. The increase was mainly a result of stronger reliability in the fourth quarter of 2015.

In Situ achieved record bitumen production in the fourth quarter of 2015, increasing to 233,300 bbls/d from 210,900 bbls/d in the prior year quarter. The increase was primarily driven by cost-effective debottlenecking activities at Firebag and strong infill well performance. Effective January 1, 2016, nameplate capacity for Firebag has been increased to 203,000 bbls/d from 180,000 bbls/d with sustained production levels in excess of 180,000 bbls/d in 2015. Production at MacKay River increased to 34,500 bbls/d in the fourth quarter of 2015 from 28,700 bbls/d in the prior year quarter. The increase was primarily due to additional production associated with the debottlenecking project.

Steam-to-oil ratios for the fourth quarter of 2015 increased compared to the prior year quarter to 2.7 from 2.6 for Firebag and 3.0 from 2.9 for MacKay River, due to additional steam requirements for the commissioning of new wells.

Price Realizations

| Net of transportation costs, but before royalties |

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| ($/bbl) | 2015 | 2014 | 2015 | 2014 | |||||||

|

|

|||||||||||

| Oil Sands operations | |||||||||||

|

|

|||||||||||

| Sweet SCO and diesel | 60.86 | 88.78 | 66.00 | 109.02 | |||||||

|

|

|||||||||||

| Sour SCO and bitumen | 32.93 | 61.68 | 41.58 | 76.66 | |||||||

|

|

|||||||||||

| Crude sales basket (all products) | 41.55 | 69.51 | 49.46 | 87.46 | |||||||

|

|

|||||||||||

| Crude sales basket, relative to WTI | (14.77 | ) | (13.57 | ) | (12.91 | ) | (15.28 | ) | |||

|

|

|||||||||||

| Oil Sands ventures | |||||||||||

|

|

|||||||||||

| Syncrude – sweet SCO | 57.37 | 81.85 | 61.55 | 99.32 | |||||||

|

|

|||||||||||

| Syncrude, relative to WTI | 1.06 | (1.23 | ) | (0.83 | ) | (3.42 | ) | ||||

|

|

|||||||||||

Average price realizations from Oil Sands operations decreased to $41.55/bbl in the fourth quarter of 2015 from $69.51/bbl in the prior year quarter, primarily due to lower benchmark prices, partially offset by favourable foreign exchange rates.

Royalties

Royalties for the Oil Sands segment were lower in the fourth quarter of 2015 compared to the prior year quarter, primarily due to lower bitumen prices, partially offset by higher production.

14 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

Expenses and Other Factors

Operating and transportation expenses for the fourth quarter of 2015 decreased from the prior year quarter, primarily due to the impact of cost reduction initiatives, lower unplanned maintenance activities and lower natural gas prices. See the Cash Operating Costs Reconciliation section below for further details regarding cash operating costs and non-production costs for Oil Sands operations. Transportation expense for the fourth quarter of 2015 was higher than the prior year quarter, primarily due to the costs related to increased sales volumes.

DD&A expense for the fourth quarter of 2015 was higher in comparison to the same period in 2014, mainly due to assets commissioned in 2015, including well pads and infill wells, and increased In Situ production.

Cash Operating Costs Reconciliation(1)

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | |||||||

|

|

|||||||||||

| Operating, selling and general expense (OS&G) | 1 317 | 1 451 | 5 220 | 5 940 | |||||||

|

|

|||||||||||

| Syncrude OS&G | (118 | ) | (153 | ) | (471 | ) | (593 | ) | |||

|

|

|||||||||||

| Non-production costs(2) | (68 | ) | (49 | ) | (279 | ) | (340 | ) | |||

|

|

|||||||||||

| Other(3) | 1 | (31 | ) | (63 | ) | (187 | ) | ||||

|

|

|||||||||||

| Oil Sands cash operating costs | 1 132 | 1 218 | 4 407 | 4 820 | |||||||

|

|

|||||||||||

| Oil Sands cash operating costs ($/bbl) | 28.00 | 34.45 | 27.85 | 33.80 | |||||||

|

|

|||||||||||

- (1)

- Cash

operating costs and cash operating costs per barrel are non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this document.

- (2)

- Significant

non-production costs include, but are not limited to, share-based compensation adjustments, research, and the expense recorded as part of a non-monetary arrangement

involving a third-party processor.

- (3)

- Other includes the impacts of changes in inventory valuation and operating revenues associated with excess capacity, primarily associated with excess power from cogeneration units.

Cash operating costs per barrel for Oil Sands operations in the fourth quarter of 2015 decreased to $28.00, compared to $34.45 in the prior year quarter, primarily due to higher production volumes combined with the impact of cost reduction initiatives, lower unplanned maintenance activities and lower natural gas input costs. Total cash operating costs decreased to $1.132 billion, from $1.218 billion in the prior year quarter despite the increase in production.

In the fourth quarter of 2015, non-production costs, which are excluded from cash operating costs, were higher than the prior year quarter. The increase was primarily due to higher share-based compensation expense during the fourth quarter of 2015, partially offset by cost reduction initiatives, including reductions to discretionary spending, lower expenses related to a gas swap arrangement with a third-party processor, and a decrease in costs associated with future growth activities.

Other items, which are also excluded from cash operating costs, decreased in the fourth quarter of 2015 compared to the prior year quarter, primarily due to the impacts of changes in inventory and a decrease in operating revenues associated with excess power from cogeneration units as a result of the decrease in power prices.

Planned Maintenance

The company plans to complete a turnaround at Upgrader 2, commencing at the end of the first quarter of 2016. The impact of this maintenance has been reflected in the company's 2016 guidance.

Fort Hills Acquisition

During the fourth quarter of 2015, the company completed its purchase of an additional 10% working interest in the Fort Hills oil sands project from Total E&P for $360 million. Suncor's working interest in the project is now 50.8%.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 15

EXPLORATION AND PRODUCTION

Financial Highlights

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | |||||||

|

|

|||||||||||

| Gross revenues | 505 | 1 078 | 2 612 | 4 715 | |||||||

|

|

|||||||||||

| Less: Royalties | (33 | ) | (203 | ) | (267 | ) | (672 | ) | |||

|

|

|||||||||||

| Operating revenues, net of royalties | 472 | 875 | 2 345 | 4 043 | |||||||

|

|

|||||||||||

| Net (loss) earnings | (1 263 | ) | 198 | (758 | ) | 653 | |||||

|

|

|||||||||||

| Adjusted for: | |||||||||||

|

|

|||||||||||

| Impairments(1) | 1 213 | — | 1 213 | 297 | |||||||

|

|

|||||||||||

| Impact of income tax rate adjustments on deferred taxes(2) | — | — | (373 | ) | — | ||||||

|

|

|||||||||||

| Insurance proceeds(3) | — | — | (75 | ) | — | ||||||

|

|

|||||||||||

| Gain on significant disposals | — | — | — | (61 | ) | ||||||

|

|

|||||||||||

| Reserves redetermination | — | — | — | (32 | ) | ||||||

|

|

|||||||||||

| Operating (loss) earnings(4) | (50 | ) | 198 | 7 | 857 | ||||||

|

|

|||||||||||

| E&P Canada | (9 | ) | 85 | (14 | ) | 502 | |||||

|

|

|||||||||||

| E&P International | (41 | ) | 113 | 21 | 355 | ||||||

|

|

|||||||||||

| Cash flow from operations(4) | 257 | 401 | 1 386 | 1 909 | |||||||

|

|

|||||||||||

- (1)

- After-tax

impairment charges of $798 million on certain offshore E&P assets as a result of declining crude oil pricing and $415 million (Q2

2014 – $297 million) against the company's Libyan assets.

- (2)

- Adjustments

to the company's deferred income taxes from a 12% decrease in the U.K. tax rate on oil and gas profits from the North Sea in the first quarter of 2015 and a 2%

increase in the Alberta corporate income tax rate in the second quarter of 2015.

- (3)

- Business

interruption insurance proceeds recorded in the first quarter of 2015 for the Terra Nova asset.

- (4)

- Non-GAAP financial measures. See also the Non-GAAP Financial Measures Advisory section of this document.

- (1)

- For an explanation of this bridge analysis, see the Non-GAAP Financial Measures Advisory section of this document.

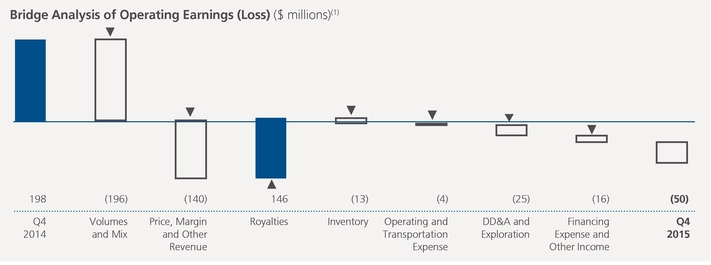

E&P operating loss was $50 million in the fourth quarter of 2015, compared to operating earnings of $198 million in the prior year quarter.

Operating loss of $9 million in E&P Canada compared with operating earnings of $85 million in the prior year quarter, primarily due to lower price realizations and a decrease in production.

Operating loss of $41 million in E&P International compared with operating earnings of $113 million in the prior year quarter, primarily due to lower price realizations and lower Buzzard production, partially offset by additional production from Golden Eagle.

16 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||

|

|

||||||||||

| E&P Canada | ||||||||||

|

|

||||||||||

| Terra Nova (mbbls/d) | 13.1 | 24.0 | 13.5 | 17.3 | ||||||

|

|

||||||||||

| Hibernia (mbbls/d) | 15.6 | 20.8 | 18.1 | 23.1 | ||||||

|

|

||||||||||

| White Rose (mbbls/d) | 14.8 | 13.3 | 12.2 | 14.6 | ||||||

|

|

||||||||||

| North America Onshore (mboe/d) | 3.1 | 2.4 | 3.2 | 3.6 | ||||||

|

|

||||||||||

| 46.6 | 60.5 | 47.0 | 58.6 | |||||||

|

|

||||||||||

| E&P International | ||||||||||

|

|

||||||||||

| Buzzard (mboe/d) | 45.5 | 54.0 | 49.8 | 47.1 | ||||||

|

|

||||||||||

| Golden Eagle (mboe/d) | 17.7 | 2.2 | 14.8 | 0.6 | ||||||

|

|

||||||||||

| United Kingdom (mboe/d) | 63.2 | 56.2 | 64.6 | 47.7 | ||||||

|

|

||||||||||

| Libya (mbbls/d) | 2.5 | 21.6 | 2.8 | 6.7 | ||||||

|

|

||||||||||

| 65.7 | 77.8 | 67.4 | 54.4 | |||||||

|

|

||||||||||

| Total Production (mboe/d) | 112.3 | 138.3 | 114.4 | 113.0 | ||||||

|

|

||||||||||

| Production mix (liquids/gas) (%) | 96/4 | 97/3 | 96/4 | 97/3 | ||||||

|

|

||||||||||

E&P Canada production averaged 46,600 boe/d in the fourth quarter of 2015, compared to 60,500 boe/d in the prior year quarter. The decrease was primarily due to expected natural declines at Terra Nova and Hibernia, in addition to a planned turnaround at Hibernia and unplanned maintenance at Terra Nova.

E&P International production averaged 65,700 boe/d in the fourth quarter of 2015, compared to 77,800 boe/d in the prior year quarter. The decrease was primarily due to Libyan production being substantially shut in, as well as decreased production at Buzzard as a result of constraints on the export pipeline system due to unplanned maintenance at one of the terminals, partially offset by increased production at Golden Eagle, which operated at peak production rates in the fourth quarter of 2015. Production in Libya temporarily resumed at the start of the quarter, but was once again shut in during November. Production in Libya remains impacted by political unrest, with the timing of a return to normal operations remaining uncertain.

Price Realizations

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| Net of transportation costs, but before royalties | 2015 | 2014 | 2015 | 2014 | ||||||

|

|

||||||||||

| Exploration and Production | ||||||||||

|

|

||||||||||

| E&P Canada – Crude oil and natural gas liquids ($/bbl) | 49.48 | 78.51 | 61.78 | 105.98 | ||||||

|

|

||||||||||

| E&P Canada – Natural gas ($/mcfe) | 1.03 | 3.42 | 1.78 | 4.49 | ||||||

|

|

||||||||||

| E&P International ($/boe) | 52.68 | 82.27 | 61.44 | 104.12 | ||||||

|

|

||||||||||

In the fourth quarter of 2015, price realizations for crude oil from E&P Canada and E&P International were lower than the prior year quarter, consistent with the decrease in benchmark prices for Brent crude oil, partially offset by favourable foreign exchange rates.

Royalties

Royalties were lower in the fourth quarter of 2015, compared with the prior year quarter, primarily due to lower production and lower price realizations.

Inventory

The inventory build during the fourth quarter of 2015 was slightly higher than the inventory build in the prior year quarter, due to timing of shuttle tankers in East Coast Canada.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 17

Expenses and Other Factors

DD&A and exploration expenses increased in the fourth quarter of 2015, compared to the prior year quarter, due to increased production associated with Golden Eagle.

Planned Maintenance

A planned four-week maintenance event at Terra Nova has been scheduled to commence in the second quarter of 2016. The impact of this maintenance has been reflected in the company's 2016 guidance.

REFINING AND MARKETING

Financial Highlights

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | ||||||

|

|

||||||||||

| Operating revenues | 4 442 | 6 056 | 19 826 | 26 627 | ||||||

|

|

||||||||||

| Net earnings | 498 | 173 | 2 266 | 1 692 | ||||||

|

|

||||||||||

| Adjusted for: | ||||||||||

|

|

||||||||||

| Impact of income tax rate adjustments on deferred taxes(1) | — | — | 36 | — | ||||||

|

|

||||||||||

| Gain on significant disposal(2) | — | — | (68 | ) | — | |||||

|

|

||||||||||

| Operating earnings(3) | 498 | 173 | 2 234 | 1 692 | ||||||

|

|

||||||||||

| Refining and Supply | 424 | 78 | 1 864 | 1 385 | ||||||

|

|

||||||||||

| Marketing | 74 | 95 | 370 | 307 | ||||||

|

|

||||||||||

| Cash flow from operations(3) | 596 | 240 | 2 872 | 2 178 | ||||||

|

|

||||||||||

- (1)

- Adjustment

to the company's deferred income taxes resulting from a 2% increase in the Alberta corporate income tax rate in Q2 2015.

- (2)

- After-tax

gain related to the sale of the company's share of certain assets and liabilities of Pioneer Energy in the Refining and Marketing segment in the second quarter

of 2015.

- (3)

- Non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this document.

- (1)

- For an explanation of this bridge analysis, see the Non-GAAP Financial Measures Advisory section of this document.

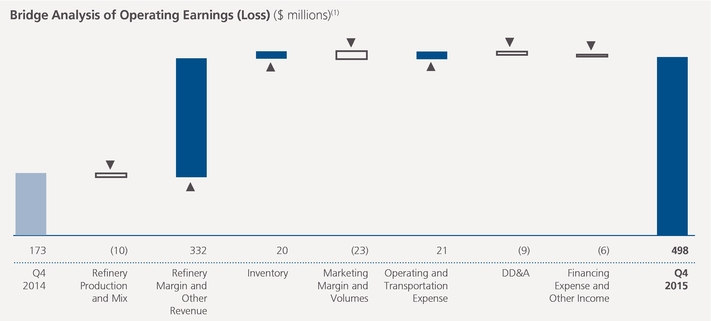

Refining and Supply operating earnings were $424 million in the fourth quarter of 2015, compared to $78 million in the prior year quarter. The increase in the fourth quarter of 2015 was primarily due to higher gasoline benchmark cracking margins, higher location differentials supported by the positive impact of the weaker Canadian dollar, partially offset by

18 SUNCOR ENERGY INC. 2015 FOURTH QUARTER

lower distillate cracking margins, lower throughput, and the impact of narrower inland crude differentials. In addition, the fourth quarter of 2015 included lower operating expenses driven by lower maintenance costs, lower environmental expenses, and the impact of cost reduction initiatives, partially offset by higher share-based compensation expense.

Marketing activities contributed $74 million to operating earnings in the fourth quarter of 2015, compared to $95 million in the prior year quarter, primarily due to lower wholesale volumes impacted by softer demand.

Volumes

|

Three months ended December 31 |

Twelve months ended December 31 |

|||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||

|

|

||||||||||

| Crude oil processed (mbbls/d) | ||||||||||

|

|

||||||||||

| Eastern North America | 208.0 | 201.0 | 208.1 | 199.2 | ||||||

|

|

||||||||||

| Western North America | 222.2 | 239.8 | 224.0 | 228.3 | ||||||

|

|

||||||||||

| Total | 430.2 | 440.8 | 432.1 | 427.5 | ||||||

|

|

||||||||||

| Refinery utilization(1) (%) | ||||||||||

|

|

||||||||||

| Eastern North America | 94 | 91 | 94 | 90 | ||||||

|

|

||||||||||

| Western North America | 93 | 100 | 93 | 95 | ||||||

|

|

||||||||||

| Total | 93 | 95 | 94 | 93 | ||||||

|

|

||||||||||

| Refined product sales (mbbls/d) | ||||||||||

|

|

||||||||||

| Gasoline | 243.8 | 247.4 | 246.2 | 243.4 | ||||||

|

|

||||||||||

| Distillate | 187.0 | 211.6 | 198.0 | 199.7 | ||||||

|

|

||||||||||

| Other | 70.4 | 89.2 | 79.1 | 88.6 | ||||||

|

|

||||||||||

| Total | 501.2 | 548.2 | 523.3 | 531.7 | ||||||

|

|

||||||||||

- (1)

- Refinery utilization is the amount of crude oil and natural gas plant liquids run through crude distillation units, expressed as a percentage of the capacity of these units.

Refinery crude throughput decreased in the fourth quarter of 2015, resulting in an average refinery utilization of 93%, compared to 95% in the prior year quarter. In Eastern North America, the average volume of crude oil processed increased to 208,000 bbls/d in the fourth quarter of 2015 from 201,000 bbls/d in the prior year quarter. The increase was primarily due to an eight-week planned maintenance event at the Sarnia refinery in the prior year quarter, partially offset by a four-week planned maintenance event at the Montreal refinery that was completed at the beginning of the fourth quarter of 2015. The average volumes of crude oil processed in Western North America decreased to 222,200 bbls/d in the fourth quarter of 2015 from 239,800 bbls/d in the prior year quarter, primarily due to planned and unplanned maintenance work at the Edmonton refinery.

Total sales of 501,200 bbls/d in the fourth quarter of 2015 were lower than 548,200 bbls/d in the prior year quarter reflecting softer distillate demand.

Prices and Margins

Refined product margins in Refining and Supply were higher in the fourth quarter of 2015 than in the prior year quarter, and were impacted by the following factors:

- •

- In

the fourth quarter of 2015, the impact of the FIFO inventory valuation used by Suncor, as compared to an estimated LIFO(1) valuation, had a negative impact

to operating earnings of approximately $77 million after-tax. This compares to a negative impact to operating earnings of approximately $372 million after-tax in the prior year quarter,

for a total quarter over quarter positive impact to operating earnings of $295 million.

- •

- Refining

margins were also higher due to strong location differentials and the positive impact of the weaker Canadian dollar, partially offset by the impacts of narrower

inland crude differentials relative to WTI.

- •

- Benchmark

crack spreads were lower in the fourth quarter of 2015 relative to the prior year quarter due to lower distillate cracking margins, offset by higher gasoline

cracking margins.

- •

- Marketing margins in the fourth quarter of 2015 were lower than margins in the prior year quarter, primarily due to softer demand in Western North America, partially offset by higher lubricant margins.

SUNCOR ENERGY INC. 2015 FOURTH QUARTER 19

Expenses and Other Factors

Operating expenses were lower in the fourth quarter of 2015 compared to the prior year quarter, primarily due to lower environmental remediation expense, lower maintenance costs, and the impact of cost reduction initiatives, partially offset by higher share-based compensation expense. DD&A expense increased due to a larger asset base, while transportation expense was relatively unchanged between quarters.

CORPORATE, ENERGY TRADING AND ELIMINATIONS

Financial Highlights

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||||

| ($ millions) | 2015 | 2014 | 2015 | 2014 | |||||||

|

|

|||||||||||

| Net loss | (626 | ) | (467 | ) | (2 647 | ) | (1 422 | ) | |||

|

|

|||||||||||

| Adjusted for: | |||||||||||

|

|

|||||||||||

| Unrealized foreign exchange loss on U.S. dollar denominated debt | 382 | 302 | 1 930 | 722 | |||||||

|

|

|||||||||||

| Restructuring charges(1) | — | — | 57 | — | |||||||

|

|

|||||||||||

| Impact of income tax rate adjustments on deferred taxes(2) | — | — | (5 | ) | — | ||||||

|

|

|||||||||||

| Operating loss(3) | (244 | ) | (165 | ) | (665 | ) | (700 | ) | |||

|

|

|||||||||||

| Renewable Energy | 13 | 15 | 56 | 78 | |||||||

|

|

|||||||||||

| Energy Trading | (13 | ) | (13 | ) | 36 | 66 | |||||

|

|

|||||||||||

| Corporate | (249 | ) | (222 | ) | (799 | ) | (850 | ) | |||

|

|

|||||||||||

| Eliminations | 5 | 55 | 42 | 6 | |||||||

|

|

|||||||||||

| Cash flow from (used in) operations(3) | (26 | ) | (24 | ) | (287 | ) | (429 | ) | |||

|

|

|||||||||||

- (1)

- Restructuring

charges related to cost reduction initiatives in the Corporate segment.

- (2)

- Adjustment

to the company's deferred income taxes resulting from a 2% increase in the Alberta corporate income tax rate in Q2 2015.

- (3)

- Non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this document.

Renewable Energy

|

Three months ended December 31 |

Twelve months ended December 31 |

||||||||

| 2015 | 2014 | 2015 | 2014 | ||||||

|

|

|||||||||

| Power generation marketed (gigawatt hours) | 124 | 122 | 407 | 411 | |||||

|

|

|||||||||

| Ethanol production (millions of litres) | 111 | 109 | 418 | 412 | |||||

|

|

|||||||||