Form 424B2 MORGAN STANLEY

Tweet

Tweet Share

Share

The information in this pricing supplement is not complete and may be changed. We may not deliver these securities until a final pricing supplement is delivered. This pricing supplement and the accompanying prospectus, prospectus supplement and index supplement do not constitute an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Preliminary Pricing Supplement dated June 30, 2016

| PROSPECTUS Dated February 16, 2016 | Pricing Supplement No. 981 to |

| PROSPECTUS SUPPLEMENT Dated February 16, 2016 | Registration Statement Nos. 333-200365; 333-200365-12 |

| INDEX SUPPLEMENT Dated February 29, 2016 | Dated June 30, 2016 |

| Rule 424(b)(2) |

$

Morgan Stanley Finance LLC

GLOBAL

MEDIUM-TERM NOTES, SERIES A

Senior Notes

Trigger Income Securities with Upside Participation Based on the Value of the S&P 500® Index due July 13, 2023

Fully and Unconditionally Guaranteed by Morgan Stanley

Principal at Risk Securities

The Trigger Income Securities with Upside Participation Based on the Value of the S&P 500® Index due July 13, 2023, which we refer to as the securities, are unsecured obligations of Morgan Stanley Finance LLC (“MSFL”) and are fully and unconditionally guaranteed by Morgan Stanley. Unlike ordinary debt securities, the securities do not guarantee the return of any principal at maturity. The securities will pay a fixed quarterly coupon at an annual rate of 1.50%. At maturity, in addition to the final quarterly coupon, you will receive for each security that you hold an amount in cash that will vary depending on the closing value of the S&P 500® Index, which we refer to as the index, on the valuation date. If the index has increased in value, you will receive a return on your investment equal to the index percent increase. If the index has remained unchanged or depreciated in value, but has not declined to below the trigger level of 50% of its initial index value, the securities will redeem for par. However, if the index has declined to below the trigger level, investors will lose 1% for every 1% decline in the index. There is no minimum payment at maturity on the securities. Accordingly, investors may lose their entire initial investment in the securities. These long-dated securities are for investors who are willing to forgo market interest rates and dividend payments, who seek an equity index-based return at maturity and who are willing to risk their principal in exchange for the limited protection against loss but only if the final index value is greater than or equal to the trigger level. The securities are notes issued as part of MSFL’s Series A Global Medium-Term Notes program.

All payments are subject to our credit risk. If we default on our obligations, you could lose some or all of your investment. These securities are not secured obligations and you will not have any security interest in, or otherwise have any access to, any underlying reference asset or assets.

| · | The stated principal amount and original issue price of each security is $10. |

| · | At maturity, in addition to the final quarterly coupon payment, you will receive an amount of cash per security based on the final index value, which is the closing value of the index on the valuation date, as follows: |

| º | If the final index value is greater than the initial index value, you will receive for each $10 stated principal amount of securities that you hold a payment at maturity equal to $10 plus the product of $10 and the index percent increase. |

| º | If the final index value is less than or equal to the initial index value but greater than or equal to the trigger level of 50% of the initial index value, meaning the value of the index has remained unchanged or has declined by no more than 50% from the initial index value, you will receive for each $10 stated principal amount of securities that you hold a payment at maturity equal to $10. |

| º | If the final index value is less than 50% of the initial index value, meaning the value of the index has declined by more than 50% from the initial index value, you will receive for each $10 stated principal amount of securities that you hold a payment at maturity equal to $10 × index performance factor. Under these circumstances, the payment at maturity will be less than the stated principal amount of $10 and will represent a loss of more than 50%, and possibly all, of your investment. |

Please see the graph illustrating the payment at maturity in “Hypothetical Payout on the Securities at Maturity” on PS-7.

| · | The index percent increase will be a fraction, the numerator of which will be the final index value minus the initial index value and the denominator of which will be the initial index value. |

| · | The index performance factor will be a fraction equal to the final index value divided by the initial index value. |

| · | The initial index value will equal the index closing value on July 8, 2016, which is the day we price the securities for initial sale to the public, which we refer to as the pricing date. |

| · | The final index value will equal the index closing value on the valuation date. |

| · | The valuation date will be July 10, 2023, subject to postponement for non-index business days and certain market disruption events. |

| · | Investing in the securities is not equivalent to investing in the index or its component stocks. |

| · | The securities will not be listed on any securities exchange. |

| · | The estimated value of the securities on the pricing date is approximately $9.340 per security, or within $0.30 of that estimate. See “Summary of Pricing Supplement” beginning on PS-3. |

| · | The CUSIP number for the securities is 61766B671. The ISIN for the securities is US61766B6719. |

You should read the more detailed description of the securities in this pricing supplement. In particular, you should review and understand the descriptions in “Summary of Pricing Supplement” and “Description of the Securities.”

The securities are riskier than ordinary debt securities. See “Risk Factors” beginning on PS-8.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

PRICE $10 PER SECURITY

Price to public |

Agent’s commissions and fees |

Proceeds to us(3) | ||

| Per security | $10.00 | $0.30(1) | ||

| $0.05(2) | $9.65 | |||

| Total | $ | $ | $ | |

| (1) | Selected dealers, including Morgan Stanley Wealth Management (an affiliate of the agent), and their financial advisors will collectively receive from the agent, MS & Co., a fixed sales commission of $0.30 for each security they sell. See “Supplemental information regarding plan of distribution; conflicts of interest.” For additional information, see “Plan of Distribution (Conflicts of Interest)” in the accompanying prospectus supplement. |

| (2) | Reflects a structuring fee payable to Morgan Stanley Wealth Management by the agent or its affiliates of $0.05 for each security. |

| (3) | See “Description of the Securities—Use of Proceeds and Hedging” beginning on PS-13. |

The Agent for this offering, Morgan Stanley & Co. LLC, is our affiliate. See “Description of the Securities––Supplemental Information Concerning Plan of Distribution; Conflicts of Interest.”

The securities are not deposits or savings accounts and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency or instrumentality, nor are they obligations of, or guaranteed by, a bank.

As used in this document, “we,” “us” and “our” refer to Morgan Stanley or MSFL, or Morgan Stanley and MSFL collectively, as the context requires.

MORGAN STANLEY

For a description of certain restrictions on offers, sales and deliveries of the securities and on the distribution of this pricing supplement and the accompanying prospectus supplement, index supplement and prospectus relating to the securities, see the section of this pricing supplement called “Description of the Securities—Supplemental Information Concerning Plan of Distribution; Conflicts of Interest.”

No action has been or will be taken by us, the Agent or any dealer that would permit a public offering of the securities or possession or distribution of this pricing supplement or the accompanying prospectus supplement, index supplement or prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Neither this pricing supplement nor the accompanying prospectus supplement, index supplement and prospectus may be used for the purpose of an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation.

In addition to the selling restrictions set forth in “Plan of Distribution (Conflicts of Interest)” in the accompanying prospectus supplement, the following selling restrictions also apply to the securities:

The securities have not been and will not be registered with the Comissão de Valores Mobiliários (The Brazilian Securities Commission). The securities may not be offered or sold in the Federative Republic of Brazil except in circumstances which do not constitute a public offering or distribution under Brazilian laws and regulations.

The securities have not been registered with the Superintendencia de Valores y Seguros in Chile and may not be offered or sold publicly in Chile. No offer, sales or deliveries of the securities or distribution of this pricing supplement or the accompanying prospectus supplement, index supplement or prospectus, may be made in or from Chile except in circumstances which will result in compliance with any applicable Chilean laws and regulations.

The securities have not been registered with the National Registry of Securities maintained by the Mexican National Banking and Securities Commission and may not be offered or sold publicly in Mexico. This pricing supplement and the accompanying prospectus supplement, index supplement and prospectus may not be publicly distributed in Mexico.

PS-2

SUMMARY OF PRICING SUPPLEMENT

The following summary describes the securities in general terms only. You should read the summary together with the more detailed information that is contained in the rest of this pricing supplement and in the accompanying prospectus supplement, index supplement and prospectus. You should carefully consider, among other things, the matters set forth in “Risk Factors.”

The securities are medium-term debt securities of MSFL and are fully and unconditionally guaranteed by Morgan Stanley. The securities do not guarantee the return of any principal at maturity. The securities will pay a fixed quarterly coupon at an annual rate of 1.50%. The securities have been designed for investors who are willing to forgo market interest rates and dividend payments and seek a return at maturity based on the performance of the of the S&P 500® Index, which we refer to as the index, as measured on the valuation date, as follows: If, as of the valuation date, the index has appreciated at all as compared to the initial index value, you will realize a positive return on your investment in the securities equal to the index percent increase. If the index has remained unchanged or depreciated in value, but has not declined to below the trigger level of 50% of its initial index value, the securities will redeem for the stated principal amount. However, if the index has declined as of the valuation date to below the trigger level, the payment at maturity will be less than the stated principal amount of $10 and will represent a loss of more than 50%, and possibly all, of your investment. There is no minimum payment at maturity on the securities. Accordingly, you could lose your entire initial investment in the securities. All payments on the securities are subject to the credit risk of Morgan Stanley.

“Standard & Poor’s®,” “S&P®,” “S&P 500®,” “Standard & Poor’s 500” and “500” are trademarks of Standard & Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc., and have been licensed for use by S&P Dow Jones Indices LLC and Morgan Stanley.

| Each security costs $10 | We are offering the Trigger Income Securities with Upside Participation Based on the Value of the S&P 500® Index due July 13, 2023, which we refer to as the securities. The stated principal amount and original issue price of each security is $10. |

The original issue price includes costs associated with issuing, selling, structuring and hedging the securities, which are borne by you, and, consequently, the estimated value of the securities on the pricing date will be less than $10. We estimate that the value of each security on the pricing date will be approximately $9.340, or within $0.30 of that estimate. Our estimate of the value of the securities as determined on the pricing date will be set forth in the final pricing supplement.

What goes into the estimated value on the pricing date?

In valuing the securities on the pricing date, we take into account that the securities comprise both a debt component and a performance-based component linked to the index. The estimated value of the securities is determined using our own pricing and valuation models, market inputs and assumptions relating to the index, instruments based on the index, volatility and other factors including current and expected interest rates, as well as an interest rate related to our secondary market credit spread, which is the implied interest rate at which our conventional fixed rate debt trades in the secondary market.

What determines the economic terms of the securities?

In determining the economic terms of the securities, including the quarterly coupon rate and the trigger level, we use an internal funding rate, which is likely to be lower than our secondary market credit spreads and therefore advantageous to us. If the issuing, selling, structuring and hedging costs borne by you were lower or if the internal funding rate were higher, one or more of the economic terms of the securities would be more favorable to you. |

PS-3

What is the relationship between the estimated value on the pricing date and the secondary market price of the securities?

The price at which Morgan Stanley & Co. LLC, which we refer to as MS & Co., purchases the securities in the secondary market, absent changes in market conditions, including those related to the index, may vary from, and be lower than, the estimated value on the pricing date, because the secondary market price takes into account our secondary market credit spread as well as the bid-offer spread that MS & Co. would charge in a secondary market transaction of this type and other factors. However, because the costs associated with issuing, selling, structuring and hedging the securities are not fully deducted upon issuance, for a period of up to 6 months following the issue date, to the extent that MS & Co. may buy or sell the securities in the secondary market, absent changes in market conditions, including those related to the index, and to our secondary market credit spreads, it would do so based on values higher than the estimated value. We expect that those higher values will also be reflected in your brokerage account statements.

MS & Co. may, but is not obligated to, make a market in the securities, and, if it once chooses to make a market, may cease doing so at any time. |

||||

| The securities do not guarantee the return of any principal at maturity | Unlike ordinary debt securities, the securities do not guarantee the return of any principal at maturity. The securities will pay a fixed quarterly coupon at an annual rate of 1.50%. At maturity, you will receive, in addition to the final quarterly coupon, for each $10 stated principal amount of securities that you hold an amount in cash that will vary depending on the closing value of the index on the valuation date, and this amount may be significantly less than the stated principal amount of the securities and could be zero. If the index declines as of the valuation date to below the trigger level of 50% of the initial index value, for every 1% decline in the index, you will lose an amount equal to 1% of the principal amount of your securities. There is no minimum payment at maturity on the securities. Accordingly, you could lose your entire initial investment in the securities. | |||

| Payment at maturity depends on the final index value | At maturity, in addition to the final quarterly coupon payment, you will receive for each $10 stated principal amount of securities that you hold an amount in cash that will vary depending upon the closing value of the index on the valuation date, determined as follows: | |||

| If the final index value is greater than the initial index value, you will receive for each $10 stated principal amount of securities that you hold a payment at maturity equal to: | ||||

$10 + $10 × the index percent increase

where,

|

||||

| index percent increase = | final index value – initial index value | |||

| initial index value | ||||

| final index value = | The closing value of the index on July 10, 2023, which we refer to as the valuation date, subject to postponement for non-index business days and certain market disruption events | |||

| initial index value = | The closing value of the index on July 8, 2016, which we refer to as the pricing date | |||

PS-4

| · If the final index value is less than or equal to the initial index value but greater than or equal to the trigger level of 50% of the initial index value, meaning the value of the index has remained unchanged or has declined by no more than 50% from the initial index value, you will receive for each $10 stated principal amount of securities that you hold a payment at maturity equal to: | ||||

| $10 | ||||

| · If the final index value is less than 50% of the initial index value, meaning the value of the index has declined by more than 50% from the initial index value, you will receive for each $10 stated principal amount of securities that you hold a payment at maturity equal to: | ||||

| $10 × (index performance factor) | ||||

| where, | ||||

| index performance factor | = | final index value |

||

| initial index value | ||||

| Under these circumstances, the payment at maturity will be less than the stated principal amount of $10 and will represent a loss of more than 50%, and possibly all, of your investment. There is no minimum payment at maturity on the securities. Accordingly, you could lose your entire initial investment in the securities. | ||||

| All payments on the securities are subject to our credit risk. | ||||

| Beginning on PS-7, in the section titled “Hypothetical Payout on the Securities at Maturity,” we have provided a graph illustrating the payout on the securities at maturity over a range of hypothetical closing values of the index on the valuation date. The examples do not show every situation that can occur. | ||||

| You can review the historical values of the index in the section of this pricing supplement called “Description of the Securities—Historical Information” starting on PS-21. You cannot predict the future performance of the index based on its historical performance. | ||||

| Investing in the securities is not equivalent to investing in the index or its component stocks. | ||||

| Morgan Stanley & Co. LLC will be the calculation agent | We have appointed our affiliate, Morgan Stanley & Co. LLC, which we refer to as MS & Co., to act as calculation agent for The Bank of New York Mellon, a New York banking corporation, the trustee for our senior notes. As calculation agent, MS & Co. will determine the initial index value, the trigger level, the final index value, the index percent increase or the index performance factor, as applicable, whether a market disruption event has occurred and the payment that you will receive at maturity, if any. | |||

| Morgan Stanley & Co. LLC will be the Agent; conflicts of interest | The Agent for the offering of the securities, MS & Co., a wholly owned subsidiary of Morgan Stanley and an affiliate of MSFL, will conduct this offering in compliance with the requirements of FINRA Rule 5121 of the Financial Industry Regulatory Authority, Inc., which is commonly referred to as FINRA, regarding a FINRA member firm’s distribution of the securities of an affiliate and related | |||

PS-5

| conflicts of interest. MS & Co. or any of our other affiliates may not make sales in this offering to any discretionary account. See “Description of the Securities—Supplemental Information Concerning Plan of Distribution; Conflicts of Interest” starting on PS-23. | |

| You may revoke your offer to purchase the securities prior to our acceptance | We are using this pricing supplement to solicit from you an offer to purchase the securities. You may revoke your offer to purchase the securities at any time prior to the time at which we accept such offer by notifying the relevant agent. We reserve the right to change the terms of, or reject any offer to purchase, the securities prior to their issuance. In the event of any material changes to the terms of the securities, we will notify you. |

| Where you can find more information on the securities | The securities are unsecured debt securities issued as part of our Series A medium-term note program. You can find a general description of our Series A medium-term note program in the accompanying prospectus supplement dated February 16, 2016, the index supplement dated February 29, 2016 and the prospectus dated February 16, 2016. We describe the basic features of this type of debt security in the sections of the prospectus supplement called “Description of Notes—Notes Linked to Commodity Prices, Single Securities, Baskets of Securities or Indices” and in the section of the prospectus called “Description of Debt Securities—Fixed Rate Debt Securities.” |

| Because this is a summary, it does not contain all of the information that may be important to you. For a detailed description of the terms of the securities, you should read the “Description of the Securities” section in this pricing supplement. You should also read about some of the risks involved in investing in the securities in the section called “Risk Factors.” The tax and accounting treatment of investments in equity-linked securities such as these may differ from that of investments in ordinary debt securities or common stock. See the section of this pricing supplement called “Description of the Securities—United States Federal Taxation.” We urge you to consult with your investment, legal, tax, accounting and other advisers with regard to any proposed or actual investment in the securities. | |

| How to reach us | You may contact your local Morgan Stanley branch office or Morgan Stanley’s principal executive offices at 1585 Broadway, New York, New York 10036 (telephone number (212) 761-4000). |

PS-6

HYPOTHETICAL PAYOUT ON THE SECURITIES AT MATURITY

The following graph illustrates the payment at maturity on the securities for a range of hypothetical percentage changes in the index. The graph is based on the following terms:

| Stated principal amount: | $10 per security |

| Trigger level: | 50% |

| · | Upside Scenario. If the final index value is greater than the initial index value, investors will receive at maturity the $10 stated principal amount plus 100% of the appreciation of the index over the term of the securities. |

| · | Par Scenario. If the final index value is less than or equal to the initial index value but is greater than or equal to the trigger level, investors will receive the stated principal amount of $10 per security. |

| · | Downside Scenario. If the final index value is less than the trigger level, investors will receive an amount that is less than the stated principal amount by an amount that is proportionate to the full percentage decrease of the index from the initial index value to the final index value. There is no minimum payment at maturity on the securities. Accordingly, you could lose your entire initial investment in the securities. |

| o | For example, if the index depreciates 60%, investors would lose 60% of their principal and receive only $4 per security at maturity, or 40% of the stated principal amount. |

PS-7

RISK FACTORS

The securities are not secured debt and, unlike ordinary debt securities, do not guarantee the return of any principal at maturity. Investing in the securities is not equivalent to investing in the index or its component stocks. This section describes the most significant risks relating to the securities. For a further discussion of risk factors, please see the accompanying prospectus supplement, index supplement and prospectus. You should carefully consider whether the securities are suited to your particular circumstances before you decide to purchase them.

| The securities guarantee any return of principal | The terms of the securities differ from those of ordinary debt securities in that the securities do not guarantee to pay you any of the principal amount of the securities at maturity. At maturity, you will receive, in addition to the final quarterly coupon, for each $10 stated principal amount of securities that you hold an amount in cash based upon the closing value of the index on the valuation date. If the final index value decreases to below the trigger level of 50% of the initial index value, you will receive an amount in cash that is at least 50% less than the stated principal amount of each security, and this decrease will be by an amount that is proportionate to the full percentage decrease of the index from the initial index value to the final index value. There is no minimum payment at maturity. Accordingly, you could lose your entire initial investment in the securities. See “Hypothetical Payout on the Securities at Maturity” on PS-7. |

| The market price of the securities will be influenced by many unpredictable factors | Several factors, many of which are beyond our control, will influence the value of the securities in the secondary market and the price at which MS & Co. may be willing to purchase or sell the securities in the secondary market, including: | |

| · the value of the index at any time, including in relation to the trigger level, | ||

| · the volatility (frequency and magnitude of changes in value) of the index, | ||

| · dividend rates on the securities underlying the index, | ||

| · interest and yield rates in the market, | ||

| · geopolitical conditions and economic, financial, political, regulatory or judicial events that affect the securities markets generally or the component stocks of the index and which may affect the value of the index, | ||

| · the time remaining until the maturity of the securities, | ||

| · the composition of the index and changes in the constituent stocks of the index, and | ||

· any actual or anticipated changes in our credit ratings or credit spreads. | ||

| Generally, the longer the time remaining to maturity, the more the market price of the securities will be affected by the other factors described above. Some or all of these factors will influence the price you will receive if you sell your securities prior to maturity. For example, you may have to sell your securities at a substantial discount from the stated principal amount if at the time of sale the value of the index is near or below the initial index value, and especially if it is near or below the trigger level. | ||

| You cannot predict the future performance of the index based on its historical performance. There can be no assurance that you will not suffer a loss on your initial investment in the securities. |

| The securities are subject to our credit risk, and any actual or anticipated changes to our credit | You are dependent on our ability to pay all amounts due on the securities on the coupon payment dates and at maturity and therefore you are subject to our credit risk. If we default on our obligations under the securities, your investment would be at risk and you could lose some or all of your investment. As a result, the market |

PS-8

| ratings or credit spreads may adversely affect the market value of the securities | value of the securities prior to maturity will be affected by changes in the market's view of our creditworthiness. Any actual or anticipated decline in our credit ratings or increase in the credit spreads charged by the market for taking our credit risk is likely to adversely affect the market value of the securities. |

| As a finance subsidiary, MSFL has no independent operations and will have no independent assets | As a finance subsidiary, MSFL has no independent operations beyond the issuance and administration of its securities and will have no independent assets available for distributions to holders of MSFL securities if they make claims in respect of such securities in a bankruptcy, resolution or similar proceeding. Accordingly, any recoveries by such holders will be limited to those available under the related guarantee by Morgan Stanley and that guarantee will rank pari passu with all other unsecured, unsubordinated obligations of Morgan Stanley. Holders will have recourse only to a single claim against Morgan Stanley and its assets under the guarantee. Holders of securities issued by MSFL should accordingly assume that in any such proceedings they would not have any priority over and should be treated pari passu with the claims of other unsecured, unsubordinated creditors of Morgan Stanley, including holders of Morgan Stanley-issued securities. |

| The amount payable at maturity is not linked to the value of the index at any time other than the valuation date | The final index value will be the index closing value on the valuation date, subject to adjustment for non-index business days and certain market disruption events. Even if the value of the index appreciates prior to the valuation date but then drops by the valuation date by more than 50% of the initial index value, the payment at maturity will be significantly less than it would have been had the payment at maturity been linked to the value of the index prior to such drop. Although the actual value of the index on the stated maturity date or at other times during the term of the securities may be higher than the final index value, the payment at maturity will be based solely on the index closing value on the valuation date. |

| The securities will not be listed on any securities exchange and secondary trading may be limited | The securities will not be listed on any securities exchange. Therefore, there may be little or no secondary market for the securities. MS & Co. may, but is not obligated to, make a market in the securities and, if it once chooses to make a market, may cease doing so at any time. When it does make a market, it will generally do so for transactions of routine secondary market size at prices based on its estimate of the current value of the securities, taking into account its bid/offer spread, our credit spreads, market volatility, the notional size of the proposed sale, the cost of unwinding any related hedging positions, the time remaining to maturity and the likelihood that it will be able to resell the securities. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities easily. Since other broker-dealers may not participate significantly in the secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which MS & Co. is willing to transact. If, at any time, MS & Co. were to cease making a market in the securities, it is likely that there would be no secondary market for the securities. Accordingly, you should be willing to hold your securities to maturity. |

PS-9

| The rate we are willing to pay for securities of this type, maturity and issuance size is likely to be lower than the rate implied by our secondary market credit spreads and advantageous to us. Both the lower rate and the inclusion of costs associated with issuing, selling, structuring and hedging the securities in the original issue price reduce the economic terms of the securities, cause the estimated value of the securities to be less than the original issue price and will adversely affect secondary market prices | Assuming no change in market conditions or any other relevant factors, the prices, if any, at which dealers, including MS & Co., may be willing to purchase the securities in secondary market transactions will likely be significantly lower than the original issue price, because secondary market prices will exclude the issuing, selling, structuring and hedging-related costs that are included in the original issue price and borne by you and because the secondary market prices will reflect our secondary market credit spreads and the bid-offer spread that any dealer would charge in a secondary market transaction of this type as well as other factors.

The inclusion of the costs of issuing, selling, structuring and hedging the securities in the original issue price and the lower rate we are willing to pay as issuer make the economic terms of the securities less favorable to you than they otherwise would be.

However, because the costs associated with issuing, selling, structuring and hedging the securities are not fully deducted upon issuance, for a period of up to 6 months following the issue date, to the extent that MS & Co. may buy or sell the securities in the secondary market, absent changes in market conditions, including those related to the index, and to our secondary market credit spreads, it would do so based on values higher than the estimated value, and we expect that those higher values will also be reflected in your brokerage account statements. | |

| The estimated value of the securities is determined by reference to our pricing and valuation models, which may differ from those of other dealers and is not a maximum or minimum secondary market price | These pricing and valuation models are proprietary and rely in part on subjective views of certain market inputs and certain assumptions about future events, which may prove to be incorrect. As a result, because there is no market-standard way to value these types of securities, our models may yield a higher estimated value of the securities than those generated by others, including other dealers in the market, if they attempted to value the securities. In addition, the estimated value on the pricing date does not represent a minimum or maximum price at which dealers, including MS & Co., would be willing to purchase your notes in the secondary market (if any exists) at any time. The value of your securities at any time after the date of this document will vary based on many factors that cannot be predicted with accuracy, including our creditworthiness and changes in market conditions. See also “The market price of the securities will be influenced by many unpredictable factors” above. | |

| Investing in the securities is not equivalent to investing in the index | Investing in the securities is not equivalent to investing in the index or its component stocks. Investors in the securities will not have voting rights or rights to receive dividends or other distributions or any other rights with respect to stocks that constitute the index. | |

| Adjustments to the index could adversely affect the value of the securities | The index publisher may add, delete or substitute the stocks constituting the index or make other methodological changes that could change the value of the index. The index publisher may discontinue or suspend calculation or publication of the index at any time. In these circumstances, the calculation agent will have the sole discretion to substitute a successor index that is comparable to the discontinued index and is not precluded from considering indices that are calculated and published by the calculation agent or any of its affiliates. If the calculation agent determines that there is no appropriate successor index, the payment at maturity on the securities will be an amount based on the closing prices at maturity of the securities composing the index at the time of such discontinuance, without rebalancing or substitution, computed by the calculation agent in accordance with the formula for calculating the index last in effect prior to discontinuance of the index. | |

| The calculation agent, | As calculation agent, MS & Co. will determine the initial index value, the trigger |

PS-10

| which is a subsidiary of Morgan Stanley and an affiliate of MSFL, will make determinations with respect to the securities | level, the final index value, the index percent increase or the index performance factor, as applicable, and the amount of cash, if any, you will receive at maturity. Moreover, certain determinations made by MS & Co., in its capacity as calculation agent, may require it to exercise discretion and make subjective judgments, such as with respect to the occurrence or non-occurrence of market disruption events and the selection of a successor index or calculation of the final index value in the event of a market disruption event or discontinuance of the index. These potentially subjective determinations may adversely affect the payout to you at maturity, if any. For further information regarding these types of determinations, see “Description of the Securities—Postponement of Valuation Date(s),” “—Calculation Agent and Calculations,” “—Alternate Exchange Calculation in Case of an Event of Default,” “—Discontinuance of the Index; Alteration of Method of Calculation” and related definitions. In addition, MS & Co. has determined the estimated value of the securities on the pricing date. | |

| Hedging and trading activity by our affiliates could potentially adversely affect the value of the securities | One or more of our affiliates and/or third-party dealers expect to carry out hedging activities related to the securities (and to other instruments linked to the index or its component stocks), including trading in the stocks that constitute the index as well as in other instruments related to the index. As a result, these entities may be unwinding or adjusting hedge positions during the term of the securities, and the hedging strategy may involve greater and more frequent dynamic adjustments to the hedge as the valuation date approaches. Some of our affiliates also trade the stocks that constitute the index and other financial instruments related to the index on a regular basis as part of their general broker-dealer and other businesses. Any of these hedging or trading activities on or prior to the pricing date could potentially increase the initial index value, and, therefore, the value at or above which the index must close on the valuation date so that you do not suffer a significant loss on your initial investment in the securities. Additionally, such hedging or trading activities during the term of the securities, including on the valuation date, could adversely affect the value of the index on the valuation date, and, accordingly, the amount of cash an investor will receive at maturity, if any. | |

The U.S. federal income tax consequences of an investment in the securities are uncertain

|

There is no direct legal authority as to the proper treatment of the securities for U.S. federal income tax purposes, and, therefore, significant aspects of the tax treatment of the securities are uncertain.

Please read the discussion under “United

States Federal Taxation” in this pricing supplement concerning the U.S. federal income tax consequences of an investment

in the securities. We intend to treat a security for U.S. federal income tax purposes as a single financial contract that provides

for a coupon that will be treated as gross income to you at the time received or accrued, in accordance with your regular method

of tax accounting. Under this treatment, the ordinary income treatment of the coupon payments, in conjunction with the capital

loss treatment of any loss recognized upon the sale, exchange or settlement of the securities, could result in adverse tax consequences

to holders of the securities because the deductibility of capital losses is subject to limitations. We do not plan to request

a ruling from the Internal Revenue Service (the “IRS”) regarding the tax treatment of the securities, and the IRS

or a court may not agree with the tax treatment described herein. If the IRS were successful in asserting an alternative treatment

for the securities, the timing and character of income or loss on the securities might differ significantly from the tax treatment

described herein. For example, under one possible treatment, the IRS could seek to recharacterize the securities as debt instruments.

In that event, U.S. Holders would be required to accrue into income original issue discount on the securities every year at a

“comparable yield” determined at the time of issuance (as adjusted based on the difference, if any, between the actual

and the projected amount |

PS-11

|

of any contingent payments on the securities) and recognize all income and gain in respect of the securities as ordinary income. The risk that financial instruments providing for buffers, triggers or similar downside protection features, such as the securities, would be recharacterized as debt is greater than the risk of recharacterization for comparable financial instruments that do not have such features. Non-U.S. Holders should note that we currently intend to withhold on any coupon paid to Non-U.S. Holders generally at a rate of 30%, or at a reduced rate specified by an applicable income tax treaty under an “other income” or similar provision, and will not be required to pay any additional amounts with respect to amounts withheld.

In 2007, the U.S. Treasury Department and the IRS released a notice requesting comments on the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. While it is not clear whether the securities would be viewed as similar to the prepaid forward contracts described in the notice, it is possible that any Treasury regulations or other guidance issued after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, possibly with retroactive effect. The notice focuses on a number of issues, the most relevant of which for holders of the securities are the character and timing of income or loss and the degree, if any, to which income realized by non-U.S. investors should be subject to withholding tax. Both U.S. and Non-U.S. Holders (as defined below) should consult their tax advisers regarding the U.S. federal income tax consequences of an investment in the securities, including possible alternative treatments, the issues presented by this notice and any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

PS-12

DESCRIPTION OF THE SECURITIES

Terms not defined herein have the meanings given to such terms in the accompanying prospectus supplement. The term “Security” refers to each $10 Stated Principal Amount of our Trigger Income Securities with Upside Participation Based on the Value of the S&P 500® Index due July 13, 2023.

| Aggregate Principal Amount | $ | |

| Pricing Date | July 8, 2016 | |

| Original Issue Date (Settlement Date) | July 13, 2016 (3 Business Days after the Pricing Date) | |

| Maturity Date | July 13, 2023, subject to extension as described in the following paragraph. | |

| If the Valuation Date is postponed in accordance with the definition thereof so that it falls less than two Business Days prior to the scheduled Maturity Date, the Maturity Date will be postponed to the second Business Day following the Valuation Date as postponed. See “––Valuation Date” below. | ||

| Issue Price | 100% ($10 per Security) | |

| Stated Principal Amount | $10 per Security | |

| Denominations | $10 and integral multiples thereof | |

| CUSIP Number | 61766B671 | |

| ISIN | US61766B6719 | |

| Specified Currency | U.S. dollars | |

| Payment at Maturity | At maturity, upon delivery of the Securities to the Trustee, we will pay, in addition to the final Quarterly Coupon, with respect to the $10 Stated Principal Amount of each Security an amount in cash, as determined by the Calculation Agent, equal to: | |

| (i) if the Final Index Value is greater than the Initial Index Value, $10 plus the product of $10 and the Index Percent Increase, | ||

| (ii) if the Final Index Value is less than or equal to the Initial Index Value but greater than or equal to the Trigger Level, meaning the value of the Index has remained unchanged or has declined by no more than 50% from the Initial Index Value, the Stated Principal Amount of $10, or | ||

| (iii) if the Final Index Value is less than the Trigger Level, meaning the value of the Index has declined by more than 50% from the Initial Index Value, | ||

| $10 x Index Performance Factor | ||

| We shall, or shall cause the Calculation Agent to, (i) provide written notice to the Trustee and to The Depository Trust Company, which we refer to as DTC, of the amount of cash to be delivered with respect to the $10 Stated Principal Amount of each Security, on or prior to 10:30 a.m. (New York City time) on the |

PS-13

| Business Day preceding the Maturity Date, and (ii) deliver the aggregate cash amount due with respect to the Securities to the Trustee for delivery to DTC, as holder of the Securities, on or prior to the Maturity Date. We expect such amount of cash will be distributed to investors on the Maturity Date in accordance with the standard rules and procedures of DTC and its direct and indirect participants. See “—Book Entry Security or Certificated Security” below, and see “Forms of Securities—The Depositary” in the accompanying prospectus. | ||

| Quarterly Coupon | The Quarterly Coupon payable on this Security on each Coupon Payment Date for the related Interest Period will be payable at an annual rate of 1.50% for the related Interest Period (computed on the basis of a year of 360 days and twelve 30-day months). | |

We shall, or shall cause the Calculation Agent to, (i) provide written notice to the Trustee, on which notice the Trustee may conclusively rely, and to the Depositary of the amount of cash to be delivered as Quarterly Coupon pursuant to the preceding paragraph with respect to each Stated Principal Amount of each Security on or prior to 10:30 a.m. (New York City time) on the Business Day preceding each Coupon Payment Date, and (ii) deliver the aggregate cash amount due with respect to the applicable Quarterly Coupon to the Trustee for delivery to the Depositary, as holder of the Securities, on the applicable Coupon Payment Date. | ||

| Interest Period | The quarterly period from and including the Original Issue Date (in the case of the first Interest Period) or the previous scheduled Coupon Payment Date, as applicable, to but excluding the following scheduled Coupon Payment Date, with no adjustment for any postponement thereof. | |

| Trigger Level | , which is 50% of the Initial Index Value. See “Discontinuance of the Index; Alteration of Method of Calculation” below. | |

| Index Percent Increase | A fraction, as determined by the Calculation Agent, the numerator of which is the Final Index Value minus the Initial Index Value and the denominator of which is the Initial Index Value, as described by the following formula: |

| Index Percent Increase | = | Final Index Value – Initial Index Value |

| Initial Index Value |

| Index Performance Factor | A fraction, as determined by the Calculation Agent, the numerator of which is the Final Index Value and the denominator of which is the Initial Index Value, as described by the following formula: |

| Index Performance Factor | = | Final Index Value |

|

| Initial Index Value |

PS-14

| Initial Index Value | , which is the Index Closing Value on the Pricing Date. See “Discontinuance of the Index; Alteration of Method of Calculation” below. | |

| Final Index Value | The Index Closing Value on the Valuation Date, as determined by the Calculation Agent. | |

| Index Closing Value | The Index Closing Value on any Index Business Day will be determined by the Calculation Agent and will equal the official closing value of the Index, or any Successor Index (as defined under “—Discontinuance of the Index; Alteration of Method of Calculation” below), published at the regular official weekday close of trading on that Index Business Day by the Index Publisher. In certain circumstances, the Index Closing Value will be based on the alternate calculation of the Index described under “—Discontinuance of the Index; Alteration of Method of Calculation.” | |

| Index Publisher | S&P Dow Jones Indices LLC or any successor thereto | |

| Coupon Payment Dates | Quarterly, on the 13th day of each January, April, July and October, beginning October 13, 2016; provided that if any scheduled Coupon Payment Date is not a Business Day, that Quarterly Coupon, if any, shall be paid on the next succeeding Business Day and no adjustment shall be made to any coupon payment made on that succeeding Business Day; provided further that the final Quarterly Coupon shall be paid on the Maturity Date. | |

| Valuation Date | July 10, 2023, subject to postponement for non-Index Business Days or Market Disruption Events as described in the following paragraph. | |

| If the scheduled Valuation Date is not an Index Business Day or if there is a Market Disruption Event on such day, the Valuation Date shall be the next succeeding Index Business Day on which there is no Market Disruption Event; provided that the Index Closing Value for the Valuation Date will not be determined on a date later than the fifth scheduled Index Business Day after the scheduled Valuation Date, and if such date is not an Index Business Day or if there is a Market Disruption Event on such date, the Calculation Agent will determine the Index Closing Value on such date in accordance with the formula for and method of calculating the Index last in effect prior to the commencement of the Market Disruption Event (or prior to the non-Index Business Day), without rebalancing or substitution, using the closing price (or, if trading in the relevant securities has been materially suspended or materially limited, its good faith estimate of the closing price that would have prevailed but for such suspension, limitation or non-Index Business Day) on such date of each security most recently constituting the Index. | ||

| Record Date | One Business Day prior to the related scheduled Coupon Payment Date; provided that the Quarterly Coupon payable at maturity |

PS-15

| shall be payable to the person to whom the payment at maturity shall be payable. | ||

| Business Day | Any day, other than a Saturday or Sunday, that is neither a legal holiday nor a day on which banking institutions are authorized or required by law or regulation to close in The City of New York. | |

| Index Business Day | A day, as determined by the Calculation Agent, on which trading is generally conducted on each of the Relevant Exchange(s) for the Index, other than a day on which trading on such exchange(s) is scheduled to close prior to the time of the posting of its regular final weekday closing price. | |

| Relevant Exchange | The primary exchange(s) or market(s) of trading for (i) any security then included in the Index, or any Successor Index, and (ii) any futures or options contracts related to the Index or to any security then included in the Index. | |

| Book Entry Security or | ||

| Certificated Security | Book Entry. The Securities will be issued in the form of one or more fully registered global securities which will be deposited with, or on behalf of, DTC and will be registered in the name of a nominee of DTC. DTC’s nominee will be the only registered holder of the Securities. Your beneficial interest in the Securities will be evidenced solely by entries on the books of the Securities intermediary acting on your behalf as a direct or indirect participant in DTC. In this pricing supplement, all references to actions taken by “you” or to be taken by “you” refer to actions taken or to be taken by DTC and its participants acting on your behalf, and all references to payments or notices to you will mean payments or notices to DTC, as the registered holder of the Securities, for distribution to participants in accordance with DTC’s procedures. For more information regarding DTC and book-entry securities, please read “Forms of Securities—The Depositary” and “Forms of Securities—Global Securities—Registered Global Securities” in the accompanying prospectus. | |

| Senior Security or Subordinated Security | Senior | |

| Trustee | The Bank of New York Mellon, a New York banking corporation | |

| Agent | Morgan Stanley & Co. LLC (“MS & Co.”) | |

| Calculation Agent | MS & Co. and its successors | |

| All determinations made by the Calculation Agent will be at the sole discretion of the Calculation Agent and will, in the absence of manifest error, be conclusive for all purposes and binding on you, the Trustee and us. | ||

| All calculations with respect to the Payment at Maturity, if any, will be made by the Calculation Agent and will be rounded to the nearest one hundred-thousandth, with five one-millionths rounded upward (e.g., .876545 would be rounded to .87655); all dollar amounts related to determination of the amount of cash payable per Security will be rounded to the nearest ten-thousandth, with |

PS-16

five one hundred-thousandths rounded upward (e.g., .76545 would be rounded up to .7655); and all dollar amounts paid on the aggregate number of Securities will be rounded to the nearest cent, with one-half cent rounded upward. | ||

| Because the Calculation Agent is our affiliate, the economic interests of the Calculation Agent and its affiliates may be adverse to your interests as an investor in the Securities, including with respect to certain determinations and judgments that the Calculation Agent must make in determining the Initial Index Value, the Final Index Value or whether a Market Disruption Event has occurred. See “—Discontinuance of the Index; Alteration of Method of Calculation” and “—Market Disruption Event” below. MS & Co. is obligated to carry out its duties and functions as Calculation Agent in good faith and using its reasonable judgment. | ||

| Market Disruption Event | Market Disruption Event means, with respect to the Index: | |

| (i) the occurrence or existence of: | ||

| (a) a suspension, absence or material limitation of trading of stocks then constituting 20 percent or more of the value of the Index (or the Successor Index) on the Relevant Exchange for such securities for more than two hours of trading or during the one-half hour period preceding the close of the principal trading session on such Relevant Exchange, or | ||

| (b) a breakdown or failure in the price and trade reporting systems of any Relevant Exchange as a result of which the reported trading prices for stocks then constituting 20 percent or more of the value of the Index (or the Successor Index) during the last one-half hour preceding the close of the principal trading session on such Relevant Exchange are materially inaccurate, or | ||

| (c) the suspension, material limitation or absence of trading on any major U.S. securities market for trading in futures or options contracts or exchange-traded funds related to the Index (or the Successor Index) for more than two hours of trading or during the one-half hour period preceding the close of the principal trading session on such market, | ||

| in each case, as determined by the Calculation Agent in its sole discretion; and | ||

| (ii) a determination by the Calculation Agent in its sole discretion that any event described in clause (i) above materially interfered with our ability or the ability of any of our affiliates to unwind or adjust all or a material portion of the hedge position with respect to these Securities. | ||

| For the purpose of determining whether a Market Disruption Event exists at any time, if trading in a security included in the Index is materially suspended or materially limited at that time, then the relevant percentage contribution of that security to the level of the Index shall be based on a comparison of (x) the |

PS-17

| portion of the value of the Index attributable to that security relative to (y) the overall value of the Index, in each case immediately before that suspension or limitation. | ||

| For the purpose of determining whether a Market Disruption Event has occurred: (1) a limitation on the hours or number of days of trading will not constitute a Market Disruption Event if it results from an announced change in the regular business hours of the Relevant Exchange or market, (2) a decision to permanently discontinue trading in the relevant futures or options contract or exchange-traded fund will not constitute a Market Disruption Event, (3) a suspension of trading in futures or options contracts or exchange-traded funds on the Index by the primary securities market trading in such contracts or funds by reason of (a) a price change exceeding limits set by such securities exchange or market, (b) an imbalance of orders relating to such contracts or funds or (c) a disparity in bid and ask quotes relating to such contracts or funds will constitute a suspension, absence or material limitation of trading in futures or options contracts or exchange-traded funds related to the Index and (4) a “suspension, absence or material limitation of trading” on any Relevant Exchange or on the primary market on which futures or options contracts or exchange-traded funds related to the Index are traded will not include any time when such securities market is itself closed for trading under ordinary circumstances. | ||

| Alternate Exchange Calculation | ||

| in Case of an Event of Default | If an Event of Default with respect to the Securities shall have occurred and be continuing, the amount declared due and payable upon any acceleration of the Securities (the “Acceleration Amount”) will be an amount, determined by the Calculation Agent in its sole discretion, that is equal to the cost of having a Qualified Financial Institution, of the kind and selected as described below, expressly assume all our payment and other obligations with respect to the Securities as of that day and as if no default or acceleration had occurred, or to undertake other obligations providing substantially equivalent economic value to you with respect to the Securities. That cost will equal: | |

• the lowest amount that a Qualified Financial Institution would charge to effect this assumption or undertaking, plus | ||

• the reasonable expenses, including reasonable attorneys’ fees, incurred by the holders of the Securities in preparing any documentation necessary for this assumption or undertaking. | ||

|

During the Default Quotation Period for the Securities, which we describe below, the holders of the Securities and/or we may request a Qualified Financial Institution to provide a quotation of the amount it would charge to effect this assumption or undertaking. If either party obtains a quotation, it must notify the other party in writing of the quotation. The amount referred to in the first bullet point above will equal the lowest—or, if there is only one, the only—quotation obtained, and as to which notice is |

PS-18

| so given, during the Default Quotation Period. With respect to any quotation, however, the party not obtaining the quotation may object, on reasonable and significant grounds, to the assumption or undertaking by the Qualified Financial Institution providing the quotation and notify the other party in writing of those grounds within two Business Days after the last day of the Default Quotation Period, in which case that quotation will be disregarded in determining the Acceleration Amount. | ||

| Notwithstanding the foregoing, if a voluntary or involuntary liquidation, bankruptcy or insolvency of, or any analogous proceeding is filed with respect to Morgan Stanley, then depending on applicable bankruptcy law, your claim may be limited to an amount that could be less than the Acceleration Amount. | ||

| If the maturity of the Securities is accelerated because of an Event of Default as described above, we shall, or shall cause the Calculation Agent to, provide written notice to the Trustee at its New York office, on which notice the Trustee may conclusively rely, and to DTC of the Acceleration Amount and the aggregate cash amount due, if any, with respect to the Securities as promptly as possible and in no event later than two Business Days after the date of such acceleration. | ||

| Default Quotation Period | ||

| The Default Quotation Period is the period beginning on the day the Acceleration Amount first becomes due and ending on the third Business Day after that day, unless: | ||

| • no quotation of the kind referred to above is obtained, or | ||

| • every quotation of that kind obtained is objected to within five Business Days after the due date as described above. | ||

| If either of these two events occurs, the Default Quotation Period will continue until the third Business Day after the first Business Day on which prompt notice of a quotation is given as described above. If that quotation is objected to as described above within five Business Days after that first Business Day, however, the Default Quotation Period will continue as described in the prior sentence and this sentence. | ||

| In any event, if the Default Quotation Period and the subsequent two Business Day objection period have not ended before the Valuation Date, then the Acceleration Amount will equal the principal amount of the Securities. | ||

| Qualified Financial Institutions | ||

| For the purpose of determining the Acceleration Amount at any time, a Qualified Financial Institution must be a financial institution organized under the laws of any jurisdiction in the United States or Europe, which at that time has outstanding debt obligations with a stated maturity of one year or less from the date of issue and rated either: |

PS-19

| • A-2 or higher by Standard & Poor’s Ratings Services or any successor, or any other comparable rating then used by that rating agency, or | ||

| • P-2 or higher by Moody’s Investors Service or any successor, or any other comparable rating then used by that rating agency. | ||

| Discontinuance of the Index; | ||

| Alteration of Method of Calculation | If the Index Publisher discontinues publication of the Index and the Index Publisher or another entity (including MS & Co.) publishes a successor or substitute index that MS & Co., as the Calculation Agent, determines, in its sole discretion, to be comparable to the discontinued Index (such index being referred to herein as a “Successor Index”), then any subsequent Index Closing Value will be determined by reference to the published value of such Successor Index at the regular weekday close of trading on any Index Business Day that the Index Closing Value is to be determined, and to the extent the Index Closing Value of the Successor Index differs from the Index Closing Value of the Index at the time of such substitution, proportionate adjustments will be made by the Calculation Agent to the Initial Index Value and Trigger Level. | |

| Upon any selection by the Calculation Agent of a Successor Index, the Calculation Agent will cause written notice thereof to be furnished to the Trustee, to Morgan Stanley and to DTC, as holder of the Securities, within three Business Days of such selection. We expect that such notice will be made available to you, as a beneficial owner of the Securities, in accordance with the standard rules and procedures of DTC and its direct and indirect participants. | ||

| If the Index Publisher discontinues the publication of the Index prior to, and such discontinuance is continuing on, the Valuation Date and the Calculation Agent determines, in its sole discretion, that no Successor Index is available at such time, then the Calculation Agent will determine the Index Closing Value for such date. The Index Closing Value will be computed by the Calculation Agent in accordance with the formula for calculating the Index last in effect prior to such discontinuance, using the closing price (or, if trading in the relevant securities has been materially suspended or materially limited, its good faith estimate of the closing price that would have prevailed but for such suspension or limitation) at the close of the principal trading session of the Relevant Exchange on such date of each security most recently constituting the Index without any rebalancing or substitution of such securities following such discontinuance. Notwithstanding these alternative arrangements, discontinuance of the publication of the Index may adversely affect the value of the Securities. | ||

| If at any time the method of calculating the Index or a Successor Index, or the value thereof, is changed in a material respect, or if the Index or a Successor Index is in any other way modified so that such index does not, in the sole opinion of MS & Co., as the |

PS-20

| Calculation Agent, fairly represent the value of the Index or such Successor Index had such changes or modifications not been made, then, from and after such time, the Calculation Agent will, at the close of business in New York City on each date on which the Index Closing Value is to be determined, make such calculations and adjustments as, in the good faith judgment of the Calculation Agent, may be necessary in order to arrive at a value of a stock index comparable to the Index or such Successor Index, as the case may be, as if such changes or modifications had not been made, and the Calculation Agent will calculate the Final Index Value with reference to the Index or such Successor Index, as adjusted. Accordingly, if the method of calculating the Index or such Successor Index is modified so that the value of such index is a fraction of what it would have been if it had not been modified (e.g., due to a split in the index), then the Calculation Agent will adjust such index in order to arrive at a value of the Index or such Successor Index as if it had not been modified (e.g., as if such split had not occurred). | ||

| The Index | The S&P 500® Index, which is calculated, maintained and published by S&P Dow Jones Indices LLC (“S&P”), consists of stocks of 500 component companies selected to provide a performance benchmark for the U.S. equity markets. The calculation of the S&P 500® Index is based on the relative value of the float adjusted aggregate market capitalization of the 500 component companies as of a particular time as compared to the aggregate average market capitalization of 500 similar companies during the base period of the years 1941 through 1943. For additional information about the S&P 500® Index, see the information set forth under “S&P 500® Index” in the accompanying index supplement. | |

| License Agreement between S&P and | ||

| Morgan Stanley | “Standard & Poor’s®,” “S&P®,” “S&P 500®,” “Standard & Poor’s 500” and “500” are trademarks of S&P and have been licensed for use by Morgan Stanley. For more information, see “S&P 500® Index—License Agreement Between S&P and Morgan Stanley” in the accompanying index supplement. | |

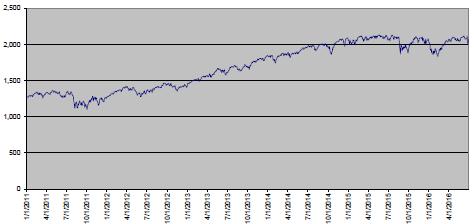

| Historical Information | The following table sets forth the published high and low Index Closing Values, as well as end-of-quarter Index Closing Values, of the Index for each quarter in the period from January 1, 2011 through June 29, 2016. The Index Closing Value on June 29, 2016 was 2,070.77. The graph following the table sets forth the historical performance of the Index for the period from January 1, 2011 through June 29, 2016. We obtained the information in the table below from Bloomberg Financial Markets, without independent verification. | |

| The historical values of the Index should not be taken as an indication of future performance, and no assurance can be given as to the Index Closing Value on the Valuation Date. The Final Index Value may decline below the Trigger Level so that the Payment at Maturity will be less than the Stated Principal Amount |

PS-21

| of $10 and will represent a loss of at least 50%, and possibly all, of your investment. | ||

| We cannot give you any assurance that the value of the Index on the Valuation Date will increase from the Initial Index Value so that you will receive a Payment at Maturity that exceeds the Stated Principal Amount of the Securities. |

| S&P 500® Index | High |

Low |

Period End |

| 2011 | |||

| First Quarter | 1,343.01 | 1,256.88 | 1,325.83 |

| Second Quarter | 1,363.61 | 1,265.42 | 1,320.64 |

| Third Quarter | 1,353.22 | 1,119.46 | 1,131.42 |

| Fourth Quarter | 1,285.09 | 1,099.23 | 1,257.60 |

| 2012 | |||

| First Quarter | 1,416.51 | 1,277.06 | 1,408.47 |

| Second Quarter | 1,419.04 | 1,278.04 | 1,362.16 |

| Third Quarter | 1,465.77 | 1,334.76 | 1,440.67 |

| Fourth Quarter | 1,461.40 | 1,353.33 | 1,426.19 |

| 2013 | |||

| First Quarter | 1,569.19 | 1,457.15 | 1,569.19 |

| Second Quarter | 1,669.16 | 1,541.61 | 1,606.28 |

| Third Quarter | 1,725.52 | 1,614.08 | 1,681.55 |

| Fourth Quarter | 1,848.36 | 1,655.45 | 1,848.36 |

| 2014 | |||

| First Quarter | 1,878.04 | 1,741.89 | 1,872.34 |

| Second Quarter | 1,962.87 | 1,815.69 | 1,960.23 |

| Third Quarter | 2,011.36 | 1,909.57 | 1,972.29 |

| Fourth Quarter | 2,090.57 | 1,862.49 | 2,058.90 |

| 2015 | |||

| First Quarter | 2,117.39 | 1,992.67 | 2,067.89 |

| Second Quarter | 2,130.82 | 2,057.64 | 2,063.11 |

| Third Quarter | 2,128.28 | 1,867.61 | 1,920.03 |

| Fourth Quarter | 2,109.79 | 1,923.82 | 2,043.94 |

| 2016 | |||

| First Quarter | 2,063.95 | 1,829.08 | 2,059.74 |

| Second Quarter (through June 29, 2016) | 2,119.12 | 2,000.54 | 2,070.77 |

Historical Daily Index Closing Values of the S&P 500® Index

January 1, 2011 through June 29, 2016

|

| Use of Proceeds and Hedging | The proceeds from the sale of the Securities will be used by us for general corporate purposes. We will receive, in aggregate, $10 per Security issued, because, when we enter into hedging transactions in order to meet our obligations under the Securities, our hedging counterparty will reimburse the cost of the Agent’s |

PS-22

| commissions. The costs of the Securities borne by you and described beginning on PS-3 above comprise the Agent’s commissions and the cost of issuing, structuring and hedging the Securities. See also “Use of Proceeds” in the accompanying prospectus. | ||

| On or prior to the Pricing Date, we will hedge our anticipated exposure in connection with the Securities by entering into hedging transactions with our affiliates and/or third party dealers. We expect our hedging counterparties to take positions in the stocks constituting the Index, in futures and/or options contracts on the Index or its component stocks listed on major securities markets, or positions in any other available securities or instruments that they may wish to use in connection with such hedging. Such purchase activity could potentially increase the Initial Index Value, and therefore could increase the value at or above which the Index must close on the Valuation Date so that you do not suffer a significant loss on your initial investment in the Securities. In addition, through our subsidiaries, we are likely to modify our hedge position throughout the term of the Securities by purchasing and selling the stocks underlying the Index, futures and/or options contracts on the Index or its component stocks listed on major securities markets or positions in any other available securities or instruments that we may wish to use in connection with such hedging activities, including by selling any such securities or instruments on the Valuation Date. As a result, these entities may be unwinding or adjusting hedge positions during the term of the Securities, and the hedging strategy may involve greater and more frequent dynamic adjustments to the hedge as the Valuation Date approaches. We cannot give any assurance that our hedging activities will not affect the value of the Index, and, therefore, adversely affect the value of the Securities or the payment you will receive at maturity, if any. | ||

| Supplemental Information Concerning | ||

| Plan of Distribution; Conflicts of Interest | The Agent may distribute the Security through Morgan Stanley Smith Barney LLC (“Morgan Stanley Wealth Management”), as selected dealer, or other dealers, which may include Morgan Stanley & Co. International plc (“MSIP”) and Bank Morgan Stanley AG. Morgan Stanley Wealth Management, MSIP and Bank Morgan Stanley AG are affiliates of Morgan Stanley. Selected dealers, including Morgan Stanley Wealth Management, and their financial advisors will collectively receive from the Agent, Morgan Stanley & Co. LLC, a fixed sales commission of $0.30 for each Security they sell. In addition, Morgan Stanley Wealth Management will receive a structuring fee of $0.05 for each Security. | |

| MS & Co. is an affiliate of MSFL and a wholly owned subsidiary of Morgan Stanley, and it and other affiliates of ours expect to make a profit by selling, structuring and, when applicable, hedging the Securities. When MS & Co. prices this offering of Securities, it will determine the economic terms of the Securities such that for each Security the estimated value on the Pricing Date |

PS-23

| will be no lower than the minimum level described in “Summary of Pricing Supplement” beginning on PS-3. | ||

| MS & Co. will conduct this offering in compliance with the requirements of FINRA Rule 5121 of the Financial Industry Regulatory Authority, Inc., which is commonly referred to as FINRA, regarding a FINRA member firm’s distribution of the Securities of an affiliate and related conflicts of interest. MS & Co. or any of our other affiliates may not make sales in this offering to any discretionary account. | ||

| In order to facilitate the offering of the Securities, the Agent may engage in transactions that stabilize, maintain or otherwise affect the price of the Securities or the level of the Index. Specifically, the Agent may sell more securities than it is obligated to purchase in connection with the offering, creating a naked short position in the Securities for its own account. The Agent must close out any naked short position by purchasing the Securities in the open market after the offering. A naked short position in the Securities is more likely to be created if the Agent is concerned that there may be downward pressure on the price of the Securities in the open market after pricing that could adversely affect investors who purchase in the offering. As an additional means of facilitating the offering, the Agent may bid for, and purchase, the Securities in the open market to stabilize the price of the Securities. Any of these activities may raise or maintain the market price of the Securities above independent market prices or prevent or retard a decline in the market price of the Securities. The Agent is not required to engage in these activities, and may end any of these activities at any time. An affiliate of the Agent has entered into a hedging transaction in connection with this offering of the Securities. See “—Use of Proceeds and Hedging” above. | ||

| General | ||

| No action has been or will be taken by us, the Agent or any dealer that would permit a public offering of the Securities or possession or distribution of this pricing supplement or the accompanying prospectus supplement, index supplement or prospectus in any jurisdiction, other than the United States, where action for that purpose is required. No offers, sales or deliveries of the Securities, or distribution of this pricing supplement or the accompanying prospectus supplement, index supplement or prospectus or any other offering material relating to the Securities, may be made in or from any jurisdiction except in circumstances which will result in compliance with any applicable laws and regulations and will not impose any obligations on us, the Agent or any dealer. | ||

| The Agent has represented and agreed, and each dealer through which we may offer the Securities has represented and agreed, that it (i) will comply with all applicable laws and regulations in force in each non-U.S. jurisdiction in which it purchases, offers, sells or delivers the Securities or possesses or distributes this pricing supplement and the accompanying prospectus supplement, |

PS-24

| index supplement and prospectus and (ii) will obtain any consent, approval or permission required by it for the purchase, offer or sale by it of the Securities under the laws and regulations in force in each non-U.S. jurisdiction to which it is subject or in which it makes purchases, offers or sales of the Securities. We shall not have responsibility for the Agent’s or any dealer’s compliance with the applicable laws and regulations or obtaining any required consent, approval or permission. | ||

| In addition to the selling restrictions set forth in “Plan of Distribution (Conflicts of Interest)” in the accompanying prospectus supplement, the following selling restrictions also apply to the Securities: | ||

| Brazil | ||