Form N-Q T. Rowe Price Dividend For: Mar 31

Tweet

Tweet Share

Share| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-Q |

| QUARTERLY SCHEDULE OF PORTFOLIO HOLDINGS OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act File Number: 811-07055 |

| T. Rowe Price Dividend Growth Fund, Inc. |

| (Exact name of registrant as specified in charter) |

| 100 East Pratt Street, Baltimore, MD 21202 |

| (Address of principal executive offices) |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

| (Name and address of agent for service) |

| Registrant’s telephone number, including area code: (410) 345-2000 |

| Date of fiscal year end: December 31 |

| Date of reporting period: March 31, 2016 |

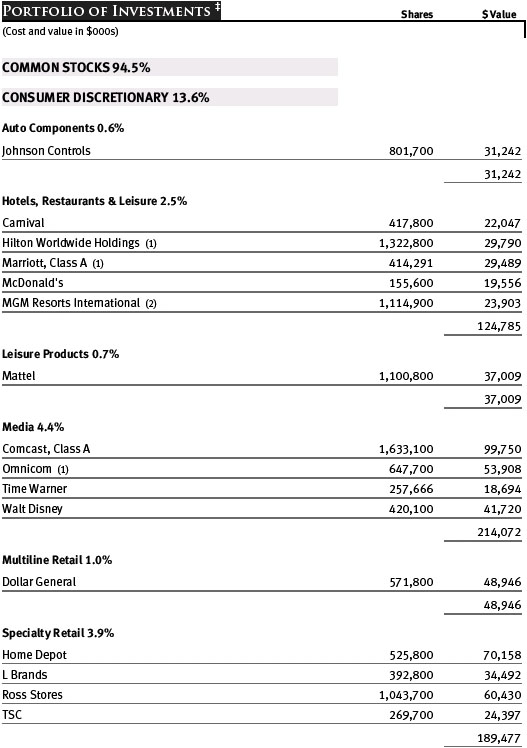

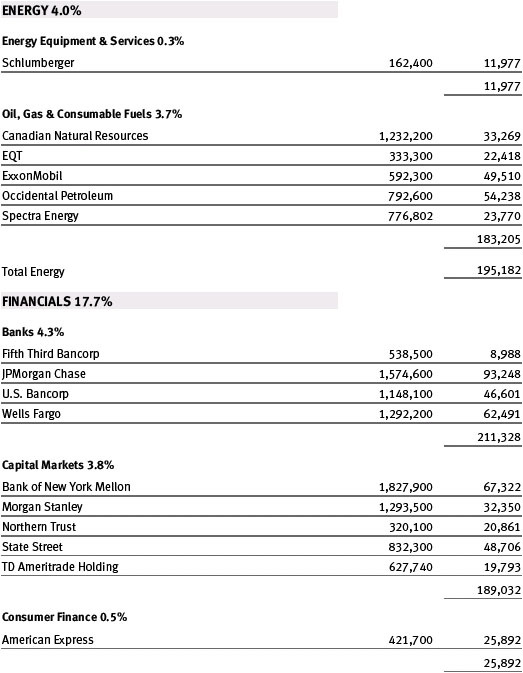

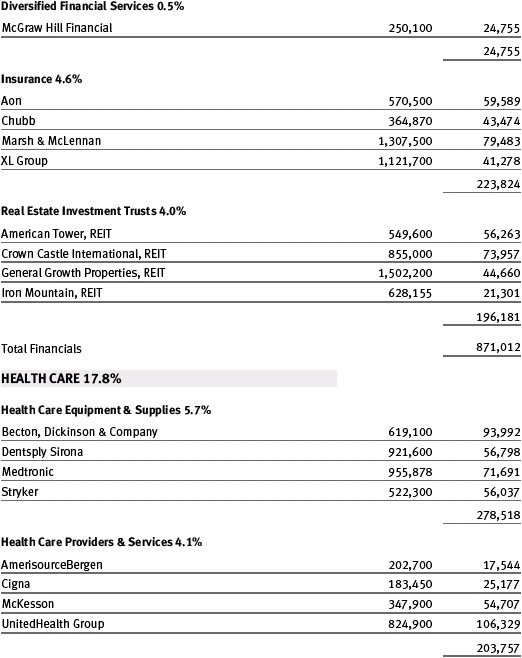

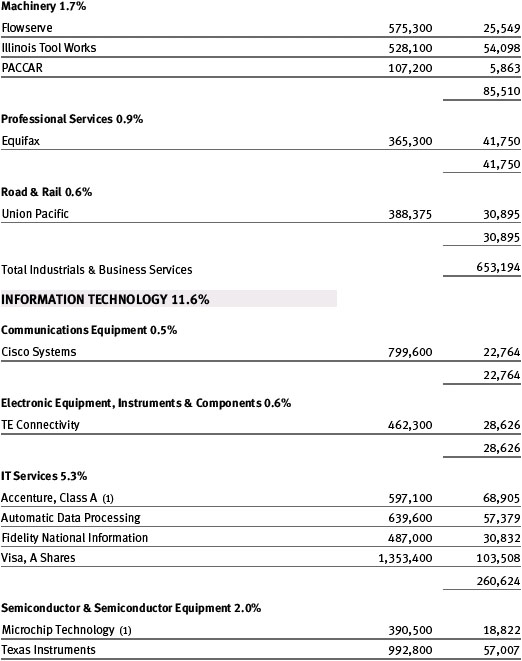

Item 1. Schedule of Investments

|

|

Dividend Growth Fund |

March 31, 2016 |

| T. Rowe Price Dividend Growth Fund |

|

|

Unaudited

The accompanying notes are an integral part of this Portfolio of Investments.

T. Rowe Price Dividend Growth

Fund

Unaudited

Notes To Portfolio of Investments

T. Rowe Price Dividend Growth Fund, Inc. (the fund), is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund commenced operations on December 30, 1992. The fund seeks dividend income and long-term capital growth primarily through investments in stocks.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of

Preparation

The fund is an investment

company and follows accounting and reporting guidance in the Financial

Accounting Standards Board (FASB) Accounting

Standards Codification Topic 946 (ASC 946).

The accompanying Portfolio of Investments was prepared in accordance with

accounting principles generally accepted in the United States of America (GAAP),

including, but not limited to, ASC 946. GAAP requires the use of estimates made

by management. Management believes that estimates and valuations are

appropriate; however, actual results may differ from those estimates, and the

valuations reflected in the Portfolio of Investments may differ from the values

ultimately realized upon sale or maturity.

Investment

Transactions

Investment transactions are

accounted for on the trade date.

Currency

Translation

Investments denominated in

foreign currencies are translated into U.S. dollar values each day at the

prevailing exchange rate, using the mean of the bid and asked prices of such

currencies against U.S. dollars as quoted by a major bank. Purchases and sales

of securities are translated into U.S. dollars at the prevailing exchange rate

on the date of the transaction.

New Accounting Guidance

In May 2015, FASB issued

ASU No. 2015-07, Fair Value Measurement (Topic

820), Disclosures for Investments in Certain Entities That Calculate Net Asset

Value per Share (or Its Equivalent). The ASU

removes the requirement to categorize within the fair value hierarchy all

investments for which fair value is measured using the net asset value per share

practical expedient and amends certain disclosure requirements for such

investments. The ASU is effective for interim and annual reporting periods

beginning after December 15, 2015. Adoption will have no effect on the fund’s

net assets or results of operations.

NOTE 2 – VALUATION

The fund’s financial instruments are valued and each class’s net asset value (NAV) per share is computed at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day the NYSE is open for business.

Fair Value

The fund’s financial instruments are reported at fair value,

which GAAP defines as the price that would be received to sell an asset or paid

to transfer a liability in an orderly transaction between market participants at

the measurement date. The T. Rowe Price Valuation Committee (the Valuation

Committee) has been established by the fund’s Board of Directors (the Board) to

ensure that financial instruments are appropriately priced at fair value in

accordance with GAAP and the 1940 Act. Subject to oversight by the Board, the

Valuation Committee develops and oversees pricing-related policies and

procedures and approves all fair value determinations. Specifically, the

Valuation Committee establishes procedures to value securities; determines

pricing techniques, sources, and persons eligible to effect fair value pricing

actions; oversees the selection, services, and performance of pricing vendors;

oversees valuation-related business continuity practices; and provides guidance

on internal controls and valuation-related matters. The Valuation Committee

reports to the Board and has representation from legal, portfolio management and

trading, operations, risk management and the fund’s treasurer.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions that market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. When multiple inputs are used to derive fair value, the financial instrument is assigned to the level within the fair value hierarchy based on the lowest-level input that is significant to the fair value of the financial instrument. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values.

Valuation Techniques

Equity securities listed or regularly

traded on a securities exchange or in the over-the-counter (OTC) market are

valued at the last quoted sale price or, for certain markets, the official

closing price at the time the valuations are made. OTC Bulletin Board securities

are valued at the mean of the closing bid and asked prices. A security that is

listed or traded on more than one exchange is valued at the quotation on the

exchange determined to be the primary market for such security. Listed

securities not traded on a particular day are valued at the mean of the closing

bid and asked prices for domestic securities and the last quoted sale or closing

price for international securities.

For valuation purposes, the last quoted prices of non-U.S. equity securities may be adjusted to reflect the fair value of such securities at the close of the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will, in its judgment, materially affect the value of some or all of its portfolio securities, the fund will adjust the previous quoted prices to reflect what it believes to be the fair value of the securities as of the close of the NYSE. In deciding whether it is necessary to adjust quoted prices to reflect fair value, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. The fund uses outside pricing services to provide it with quoted prices and information to evaluate or adjust those prices. The fund cannot predict how often it will use quoted prices and how often it will determine it necessary to adjust those prices to reflect fair value. As a means of evaluating its security valuation process, the fund routinely compares quoted prices, the next day’s opening prices in the same markets, and adjusted prices.

Actively traded equity securities listed on a domestic exchange generally are categorized in Level 1 of the fair value hierarchy. Non-U.S. equity securities generally are categorized in Level 2 of the fair value hierarchy despite the availability of quoted prices because, as described above, the fund evaluates and determines whether those quoted prices reflect fair value at the close of the NYSE or require adjustment. OTC Bulletin Board securities, certain preferred securities, and equity securities traded in inactive markets generally are categorized in Level 2 of the fair value hierarchy.

Investments in mutual funds are valued at the mutual fund’s closing NAV per share on the day of valuation and are categorized in Level 1 of the fair value hierarchy.

Thinly traded financial instruments and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the Valuation Committee. The objective of any fair value pricing determination is to arrive at a price that could reasonably be expected from a current sale. Financial instruments fair valued by the Valuation Committee are primarily private placements, restricted securities, warrants, rights, and other securities that are not publicly traded.

Subject to oversight by the Board, the Valuation Committee regularly makes good faith judgments to establish and adjust the fair valuations of certain securities as events occur and circumstances warrant. For instance, in determining the fair value of an equity investment with limited market activity, such as a private placement or a thinly traded public company stock, the Valuation Committee considers a variety of factors, which may include, but are not limited to, the issuer’s business prospects, its financial standing and performance, recent investment transactions in the issuer, new rounds of financing, negotiated transactions of significant size between other investors in the company, relevant market valuations of peer companies, strategic events affecting the company, market liquidity for the issuer, and general economic conditions and events. In consultation with the investment and pricing teams, the Valuation Committee will determine an appropriate valuation technique based on available information, which may include both observable and unobservable inputs. The Valuation Committee typically will afford greatest weight to actual prices in arm’s length transactions, to the extent they represent orderly transactions between market participants; transaction information can be reliably obtained; and prices are deemed representative of fair value. However, the Valuation Committee may also consider other valuation methods such as market-based valuation multiples; a discount or premium from market value of a similar, freely traded security of the same issuer; or some combination. Fair value determinations are reviewed on a regular basis and updated as information becomes available, including actual purchase and sale transactions of the issue. Because any fair value determination involves a significant amount of judgment, there is a degree of subjectivity inherent in such pricing decisions, and fair value prices determined by the Valuation Committee could differ from those of other market participants. Depending on the relative significance of unobservable inputs, including the valuation technique(s) used, fair valued securities may be categorized in Level 2 or 3 of the fair value hierarchy.

Valuation Inputs

The following table summarizes the fund’s financial

instruments, based on the inputs used to determine their fair values on March

31, 2016:

There were no material transfers between Levels 1 and 2 during the period ended March 31, 2016.

NOTE 3 – OTHER INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Securities Lending

The fund may lend its securities to approved brokers to earn

additional income. Its securities lending activities are administered by a

lending agent in accordance with a securities lending agreement. Security loans

generally do not have stated maturity dates, and the fund may recall a security

at any time. The fund receives collateral in the form of cash or U.S. government

securities, valued at 102% to 105% of the value of the securities on loan.

Collateral is maintained over the life of the loan in an amount not less than

the value of loaned securities; any additional collateral required due to

changes in security values is delivered the next business day. Cash collateral

is invested by the lending agent(s) in accordance with investment guidelines

approved by fund management. Additionally, the lending agent indemnifies the

fund against losses resulting from borrower default. Although risk is mitigated

by the collateral and indemnification, the fund could experience a delay in

recovering its securities and a possible loss of income or value if the borrower

fails to return the securities, collateral investments decline in value, and the

lending agent fails to perform. In accordance with GAAP, investments made with

cash collateral are reflected in the accompanying Portfolio of Investments, but

collateral received in the form of securities is not. At March 31, 2016, the

value of loaned securities was $21,688,000, including securities sold but not

yet settled, which are not reflected in the accompanying Portfolio of

Investments; the value of cash collateral and related investments was

$22,760,000.

NOTE 4 - FEDERAL INCOME TAXES

At March 31, 2016, the cost of investments for federal income tax purposes was $3,421,897,000. Net unrealized gain aggregated $1,516,973,000 at period-end, of which $1,568,065,000 related to appreciated investments and $51,092,000 related to depreciated investments.

NOTE 5 - RELATED PARTY TRANSACTIONS

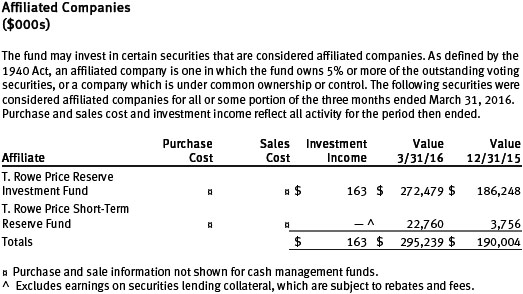

The fund may invest in the T. Rowe Price Reserve Investment Fund, the T. Rowe Price Government Reserve Investment Fund, or the T. Rowe Price Short-Term Reserve Fund (collectively, the Price Reserve Investment Funds), open-end management investment companies managed by T. Rowe Price Associates, Inc. (Price Associates) and considered affiliates of the fund. The Price Reserve Investment Funds are offered as short-term investment options to mutual funds, trusts, and other accounts managed by Price Associates or its affiliates and are not available for direct purchase by members of the public. The Price Reserve Investment Funds pay no investment management fees.

Item 2. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-Q was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 3. Exhibits.

Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

T. Rowe Price Dividend Growth Fund, Inc.

| By | /s/ Edward C. Bernard | |

| Edward C. Bernard | ||

| Principal Executive Officer | ||

| Date May 25, 2016 | ||

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By | /s/ Edward C. Bernard | |

| Edward C. Bernard | ||

| Principal Executive Officer | ||

| Date May 25, 2016 | ||

| By | /s/ Catherine D. Mathews | |

| Catherine D. Mathews | ||

| Principal Financial Officer | ||

| Date May 25, 2016 | ||

| Item 3. |

| CERTIFICATIONS |

| I, Edward C. Bernard, certify that: |

| 1. | I have reviewed this report on Form N-Q of T. Rowe Price Dividend Growth Fund, Inc.; | |||

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; | |||

| 3. | Based on my knowledge, the schedules of investments included in this report fairly present in all material respects the investments of the registrant as of the end of the fiscal quarter for which the report is filed; | |||

| 4. | The registrant's other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in rule 30a-3(c) under the Investment Company Act of 1940) and internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) for the registrant and have: | |||

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; | |||

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; | |||

| (c) | Evaluated the effectiveness of the registrant's disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of a date within 90 days prior to the filing date of this report, based on such evaluation; and | |||

| (d) | Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and | |||

| 5. | The registrant's other certifying officer(s) and I have disclosed to the registrant's auditors and the audit committee of the registrant's board of directors (or persons performing the equivalent functions): | |||

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant's ability to record, process, summarize, and report financial information; and | |||

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant's internal control over financial reporting. | |||

| Date: | May 25, 2016 | /s/ Edward C. Bernard |

| Edward C. Bernard | ||

| Principal Executive Officer |

CERTIFICATIONS

I, Catherine D. Mathews, certify that:

| 1. | I have reviewed this report on Form N-Q of T. Rowe Price Dividend Growth Fund, Inc.; | |||

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; | |||

| 3. | Based on my knowledge, the schedules of investments included in this report fairly present in all material respects the investments of the registrant as of the end of the fiscal quarter for which the report is filed; | |||

| 4. | The registrant's other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in rule 30a-3(c) under the Investment Company Act of 1940) and internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) for the registrant and have: | |||

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; | |||

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; | |||

| (c) | Evaluated the effectiveness of the registrant's disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of a date within 90 days prior to the filing date of this report, based on such evaluation; and | |||

| (d) | Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and | |||

| 5. | The registrant's other certifying officer(s) and I have disclosed to the registrant's auditors and the audit committee of the registrant's board of directors (or persons performing the equivalent functions): | |||

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant's ability to record, process, summarize, and report financial information; and | |||

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant's internal control over financial reporting. | |||

| Date: | May 25, 2016 | /s/ Catherine D. Mathews |

| Catherine D. Mathews | ||

| Principal Financial Officer |

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- USCB Financial Holdings (USCB) Reports Q1, Announces 500K Share Buyback

- S&T Bancorp (STBA) Declares $0.33 Quarterly Dividend; 4.2% Yield

- Bank of Princeton (BPRN) Declares $0.30 Quarterly Dividend; 4% Yield

Create E-mail Alert Related Categories

SEC FilingsRelated Entities

DividendSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!