Form 10-K Cell Source, Inc. For: Dec 31

Tweet

Tweet Share

Share|

☒

☐

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the years ended December 31, 2018

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

|

|

Nevada

|

|

32-0379665

|

|

(State or other jurisdiction of incorporation or organization)

|

|

(I.R.S. Employer Identification No.)

|

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

|

Non-accelerated filer ☒

|

Smaller reporting company ☒

|

|

|

Emerging growth company ☐

|

|

Page

|

||

|

PART I

|

||

|

Item 1.

|

Business.

|

1 |

|

Item 1A.

|

Risk Factors.

|

29 |

|

Item 1B.

|

Unresolved Staff Comments.

|

41 |

|

Item 2.

|

Properties.

|

41 |

|

Item 3.

|

Legal Proceedings.

|

41 |

|

Item 4.

|

Mine Safety Disclosures.

|

41 |

|

PART II

|

||

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

42 |

|

Item 6.

|

Selected Financial Data.

|

43 |

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

43 |

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk.

|

46 |

|

Item 8.

|

Financial Statements and Supplementary Data.

|

46 |

|

Item 9.

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure.

|

46 |

|

Item 9A.

|

Controls and Procedures.

|

46 |

|

Item 9B.

|

Other Information.

|

47 |

| PART III | |

|

|

Item 10.

|

Directors, Executive Officers and Corporate Governance.

|

48 |

|

Item 11.

|

Executive Compensation.

|

50 |

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

|

52 |

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence.

|

52 |

|

Item 14.

|

Principal Accounting Fees and Services.

|

54 |

| PART IV | |

|

|

Item 15.

|

Exhibits, Financial Statement Schedules.

|

55 |

|

Signatures

|

57 |

|

·

|

Hematological malignancies (leukemias, lymphomas, etc.). One of the most effective treatments for these

conditions is SCT - stem cell transplantation (e.g. bone marrow transplantation). While the challenge finding donors for allogeneic (donor vs. patient derived) SCT can be addressed through haploidentical (partially mismatched donor)

transplants, is a risky and difficult procedure primarily because of potential conflicts between host and donor immune systems and also due to viral infections that often follow even successful SCT while the compromised new immune system

works to reconstitute itself by using the transplanted stem cells.

|

|

·

|

The broader set of cancers, including solid tumors, that can potentially be treated effectively using

genetically modified cells such as CAR-T cells, but also face efficacy and economic constraints due to limited persistence based on immune system issues (i.e., the need to be able to safely and efficiently deliver allogeneic CAR-T

therapy).

|

|

·

|

Organ failure and transplantation. A variety of conditions can be treated by the transplantation of vital

organs. However, transplantation is limited both by the insufficient supply of available donor organs and the need for lifelong, daily anti-reject treatments post-transplant.

|

|

·

|

Non-malignant hematological conditions (such as sickle cell anemia) which could, in many cases, also be

effectively treated by stem cell transplantation if the procedure could be made safer and more accessible by addressing conflicts between host and donor immune systems.

|

Cell Source, Inc. (the "Company") is a Nevada corporation formed on June 6, 2012 under the name Ticket to See, Inc. ("TTSI"). Cell Source Ltd. (“Cell Source Israel”) was founded in 2011 in order to commercialize a suite of inventions that were the result of over ten (10) years of research at the Weizmann Institute of Science in Rehovot, Israel (“Weizmann Institute”). Pursuant to a Research and License Agreement by and between Cell Source Israel and Yeda, dated October 3, 2011, as amended in April, 2014 November, 2016, and, most recently, in March, 2018 (the “Yeda License Agreement”), Yeda, the commercial arm of the Weizmann Institute, granted Cell Source Israel an exclusive license to certain patents, discoveries, inventions, and other intellectual property generated (together with others) by Yair Reisner, Ph.D. (“Dr. Reisner”), former head of the Immunology Department at the Weizmann Institute.

| · |

being permitted to present only two years of audited financial statements and only two years of related Management’s Discussion & Analysis of Financial

Condition and Results of Operations in this report on Form 10-K;

|

| · |

not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as amended, or the Sarbanes-Oxley

Act; and

|

| · |

reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements.

|

|

a)

|

many blood cancer patients are not candidates for the primary treatment (HSCT) that represents a potential

cure;

|

|

b)

|

there is high mortality among those patients who are candidates for HSCT and do undergo the procedure;

|

|

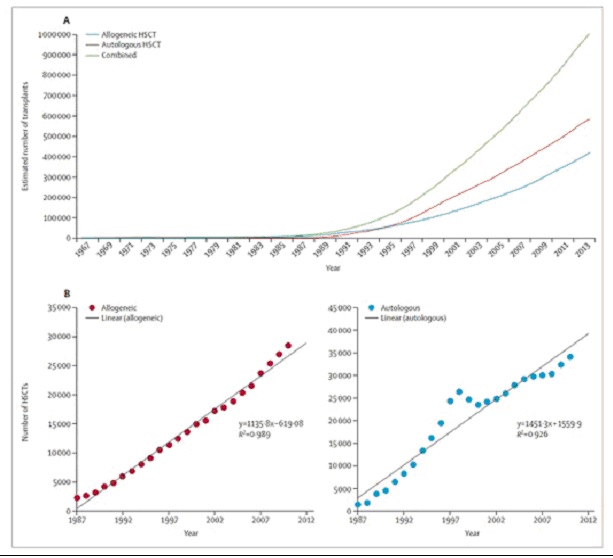

Initial Malignancy Indications

(note estimates for

North America and EU only)

|

Incidence

(Annual New Cases)

|

Annual Bone Marrow

Transplantations

|

||||||

|

Lymphoma

|

217,491

|

20,291

|

||||||

|

Multiple Myeloma

|

79,067

|

20,884

|

||||||

|

Leukemia

|

155,080

|

14,480

|

||||||

|

Total

|

451,638

|

55,655

|

||||||

|

1)

|

As noted above, increasing incidence of these disorders, largely driven by the aging population.

|

|

2)

|

Improvement and proliferation of HSCT treatments.

|

|

3)

|

A “virtuous circle” of lowered death rate due to better transplantations leading to more aggressive focus on

HSCT.

|

|

4)

|

The growing use of milder conditioning regimens, which makes the procedure more survivable for older patients

(see table below).

|

|

Name: VETO CELLS EFFECTIVE IN PREVENTING GRAFT REJECTION AND DEVOID OF GRAFT VERSUS HOST POTENTIAL

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA (Basic)

|

6,544,506

|

05-Jan-2000

|

05-Jan-2020

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

USA (National Phase)

|

7,270,810

|

28-Dec-2000

|

5-Dec-2021

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Israel

|

150440

|

28-Dec-2000

|

28-Dec-2020

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: ANTI THIRD PARTY CENTRAL MEMORY T CELLS, METHODS OF PRODUCING SAME AND USE OF SAME IN TRANSPLANTATION

AND DISEASE TREATMENT

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA

|

2011-0212071-A1

|

29-Oct-2009

|

29-Oct-2029

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

2365823

|

29-Oct-2009

|

29-Oct-2029

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Israel

|

212587

|

29-Oct-2009

|

29-Oct-2029

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

India

|

905/MUMNP/2011

|

29-Oct-2009

|

29-Oct-2029

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

China

|

ZL200980153053.4

|

29-Oct-2009

|

29-Oct-2029

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Russian Federation

|

2506311

|

29-Oct-2009

|

29-Oct-2029

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

| Name: USE OF ANTI THIRD PARTY CENTRAL MEMORY T CELLS FOR ANTI-LEUKEMIA/LYMPHOMA TREATMENT | ||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA

|

9,421,228

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

USA (Continuation)

|

2016-0354410-A1

|

08-Sep-2011

|

08-Sep-2031

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Japan

|

2013-527738

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Canada

|

2,810,632

|

08-Sep-2011

|

08-Sep-2031

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

China

|

CN 103282047 A 9

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

China (Divisional)

|

CN 105907713 A

|

08-Sep-2011

|

08-Sep-2031

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

| Israel | 225102 | 08-Sep-2011 | 08-Sep-2031 | Granted | Yeda Research and Development Co. Ltd. | |||||

|

Republic of Korea

|

2013-7008892

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Brazil

|

BR 11 2013 0057564

|

08-Sep-2011

|

08-Sep-2031

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Mexico

|

357746

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Singapore

|

188473

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

2613801

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Hong Kong

|

14100513.2

|

08-Sep-2011

|

08-Sep-2031

|

Granted

|

Yeda Research and Development Co. Ltd.

|

| Name: ANTI THIRD PARTY CENTRAL MEMORY T CELLS, METHODS OF PRODUCING SAME AND USE OF SAME IN TRANSPLANTATION AND DISEASE TREATMENT | ||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA

|

15/825,275

|

06-Sep-2012

|

06-Sep-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

2753351

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Hong Kong

|

1200099A

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Japan

|

2014-529143

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Canada

|

2,848,121

|

06-Sep-2012

|

06-Sep-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

China

|

CN 103930130 A

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Australia

|

2012305931

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Republic of Korea

|

10-2014-7009267

|

06-Sep-2012

|

06-Sep-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

New Zealand

|

622749

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

South Africa

|

2014/01993

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

India

|

577/MUMNP/2014

|

06-Sep-2012

|

06-Sep-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Israel

|

231397

|

06-Sep-2012

|

06-Sep-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Russian Federation

|

2014110897

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Brazil

|

BR 11 2014 005355 3

|

06-Sep-2012

|

06-Sep-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Mexico

|

351226

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Singapore

|

11201400513P

|

06-Sep-2012

|

06-Sep-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|

Name: GENETICALLY MODIFIED ANTI-THIRD PARTY CENTRAL MEMORY T CELLS AND USE OF SAME IN IMMUNOTHERAPY

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA

|

2018-0207272-A1

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

3322425

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

China

|

201680053580.8

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Japan

|

2018-501339

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Hong Kong

|

18114191.8

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Israel

|

256916

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Canada

|

2,991,690

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Australia

|

2016291825

|

14-July-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: USE OF ANTI THIRD PARTY CENTRAL MEMORY T CELLS

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

China

|

CN 108025026 A

|

14-Jul-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

3322424

|

14-Jul-2016

|

16-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: METHODS OF TRANSPLANTATION AND DISEASE TREATMENT

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA

|

2018-0207247-A1

|

14-Jul-2016

|

14-Jul-2036

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: VETO CELLS GENERATED FROM MEMORY CELLS

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA

|

16/313,486

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Japan

|

2018-567129

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Canada

|

3,029,001

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Australia

|

2017289879

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

India

|

201927002672

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Israel

|

263924

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Russian Federation

|

2019101826

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Mexico

|

MX/a/2019/000022

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Republic of Korea

|

10-2019-7002824

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Singapore

|

11201811563R

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

62/354,950

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

China

|

62/354,950

|

27-Jun-2017

|

27-Jun-2037

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: METHODS OF TRANSPLANTATION AND DISEASE TREATMENT USING ANTI-THIRD-PARTY CTL VETO CELLS

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

USA

|

2018-0200300-A1

|

18-Jan-2018

|

18-Jan-2038

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: GENETICALLY MODIFIED VETO CELLS AND USE OF SAME IN IMMUNOTHERAPY

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

PCT

|

WO2018/134824

|

18-Jan-2018

|

18-Jan-2038

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: A COMBINATION THERAPY FOR A STABLE AND LONG-TERM ENGRAFTMENT

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

Singapore

|

10201801905W

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Mexico

|

MX/a/2014/007647

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Russian Federation

|

2014128479

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Israel

|

233303

|

20-Dec-2012

|

20-Dec-2032

|

Allowed

|

Yeda Research and Development Co. Ltd.

|

|||||

|

India

|

1468/MUMNP/2014

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

South Africa

|

2014/05071

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

New Zealand

|

627272

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Republic of Korea

|

10-2014-7020449

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Australia

|

2012355990

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Canada

|

2,859,953

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

2793914

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

USA

|

2014-0363437-A1

|

20-Dec-2012

|

20-Dec-2032

|

Allowed |

Yeda Research and Development Co. Ltd.

|

|||||

|

Hong Kong

|

15103467.1

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Name: A COMBINATION THERAPY FOR A STABLE AND LONG TERM ENGRAFTMENT USING SPECIFIC PROTOCOLS FOR T/B

CELL DEPLETION

|

||||||||||

|

Country

|

Patent Number

|

Filed

|

Expires

|

Status

|

Assignee

|

|||||

|

Singapore

|

11201403456U

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Mexico

|

MX/a/2014/007648

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Brazil

|

BR 11 2014 015959 9

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Russian Federation

|

2014129632

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Israel

|

233302

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

India

|

1467/MUMNP/2014

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

South Africa

|

2014/05298

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

New Zealand

|

627549

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Australia

|

2012355989

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Australia (Divisional)

|

2016259415

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

China

|

CN 104093314 A 4

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Canada

|

2,859,952

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Japan

|

6,313,219

|

20-Dec-2012

|

20-Dec-2032

|

Granted

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Europe

|

EP2797421

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

USA

|

2014-0369974-A1

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

Hong Kong

|

15103468.0

|

20-Dec-2012

|

20-Dec-2032

|

Pending

|

Yeda Research and Development Co. Ltd.

|

|||||

|

1)

|

Significantly improve outcomes of transplantations by reducing the host (transplant recipient) rejection rate

of T-cell depleted stem cells (e.g. from bone marrow) – thus supporting successful engraftment of the transplanted cells, which is the treatment for the blood cancer itself. In order to improve the safety of this cancer treatment, Veto

Cell technology has shown in preclinical studies that it can markedly reduce both the risk of GVHD and the need for using aggressive amounts of immunosuppression medications, as well as preventing viral infections that typically threaten

patients post transplantation. This safer means of deliver stem cell transplants would significantly reduce the HSCT mortality rate and therefore lead to broader use of this treatment.

|

|

2)

|

Substantively increase the number of transplantations by enabling successful engraftment under lower levels of

immune suppression and therefore making the therapy accessible to older and sicker patients (who today may not survive ablation).

|

|

3)

|

Further increase the number of transplantations by making transplantation appropriate for other indications

(for which today transplantation would be considered an inappropriately risky treatment).

|

| – |

Gene modified cell therapy is considered to be one of the most promising cancer treatment approaches in decades, with companies like Kite Pharma and JUNO

Therapeutics having recently been acquired at multi-billion dollar valuations after having successfully treated relatively small numbers of patients in clinical trials.

|

| – |

While gene modified treatments such as CAR-T have shown remarkable results in cancer treatment trials, their published successes to date have been mostly

limited to “autologous” blood cell cancer treatments using the patient’s own cells. There are concerns that this type of “personalized” treatment may not have favorable economics on a large-scale basis.

|

| – |

The ideal, more lucrative commercial path for CAR-T and similar genetically engineered cell therapies is to become “allogeneic” or off-the-shelf product

with drug-like distribution economics and to treat a broad spectrum of cancers including solid tumors.

|

| – |

Cell Source licenses Yeda’s patent applications for combining Veto Cells with genetically modified T cells and is currently exploring active collaboration

with CAR-T cell providers to move Veto and CAR-T combined cell therapy towards the clinic.

|

| – |

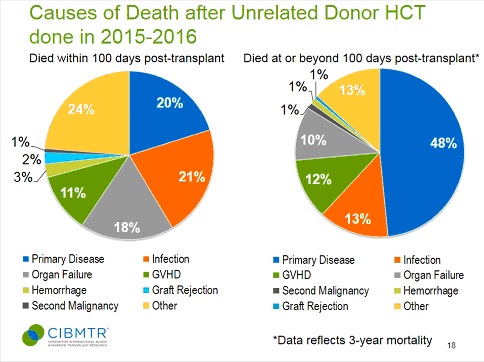

Other than primary disease (typically blood cell cancer) the leading causes of death in unrelated donor bone marrow transplants are rejection, GVHD (Graft

vs. Host Disease), where the donor bone marrow rejects the host or recipient), and infections, which collectively are responsible for 30% of deaths after unrelated donor transplants within the first 100 days post-transplant.

|

| – |

It is well established that GVHD can be prevented by T cell depletion of the bone marrow transplant. However, this procedure is also is associated with an

increased rate of graft rejection. Preclinical studies clearly suggest that this problem can be overcome by adding Veto Cells to the bone marrow transplant. However, viruses such as CMV and EBV remain a major threat to patients

post-transplant.

|

| – |

Cell Source has developed a next generation Veto Cell that not only facilitates mismatched transplants but also protects the transplant recipient against

these common viruses. During the initial period after a stem cell transplantation the patient’s body undergoes an immune system reconstitution period. While the “new” immune system is building up, the patient is particularly

vulnerable to viral infections such as CMV, an infection that is typically development in about half of bone marrow transplant recipients during the first 100 days post transplantation. Veto cells can fend off CMV until such time as

the patient’s own immune system reconstitutes to the point that it can fight off the infection on its own.

|

| – |

Combining GVHD prevention by using T cell depleted transplants with anti-rejection action as well as virus prevention, Veto Cell could potentially

significantly increase survival rates post-transplant.

|

| – |

Based on preclinical data, veto cells can also be used to facilitate organ transplants (e.g. kidney transplant combined with a bone marrow transplant) with

partially mismatched donors and either reduce or eliminate the need for lifelong daily anti-rejection treatment currently given to even fully matched donor organ recipients.

|

| – |

Cell Source is currently in the process of attaining regulatory validation for the production of its Anti-Viral Veto Cells in Europe and plans to commence

human clinical trials in the US in 2019.

|

|

1)

|

It has an outer surface coating that triggers attack by specific host T-cells (and only those specific

T-cells).

|

|

2)

|

It can annihilate an attacking T-cell without itself being damaged (specifically, it exposes or releases a

death-signaling molecule when an attacking T-cell binds to it).

|

|

3)

|

It has been oriented to attack cells of a simulated third party (i.e., neither host nor donor) and thus

exhibits markedly reduced risk of GVHD or graft rejection.

|

|

4)

|

It is long-lived and endures in the body for extended periods.

|

|

5)

|

It migrates to the thymus and lymph nodes.

|

|

1)

|

It destroys the host T-cells so they will not attack (reject) the donor bone marrow cells.

|

|

2)

|

It makes space in the host bone marrow for the new donor cells.

|

|

3)

|

It destroys diseased host blood cells so that they do not proliferate and cause relapse following the

procedure.

|

|

·

|

Host rejection - the myeloablative conditioning does not destroy all of the host T-cells. Those that remain

may aggressively attack the donor bone marrow cells before they can engraft.

|

|

·

|

“Graft versus Host Disease” (GVHD) - the transplanted cells include donor T-cells which recognize the host's

body as foreign and attack it.

|

|

·

|

Viral infections are a common complication from HSCT and result in 20% of early patients deaths in

unrelated-donor transplants in the US

|

|

1.

|

Inducing chimerism: |

|

Offering

|

Objective

|

Major Activities

|

Estimated Start Date

|

|||

|

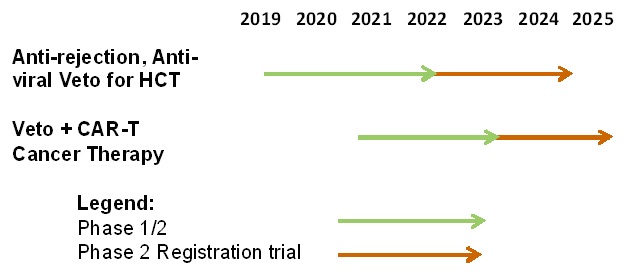

Anti-Rejection,

Anti-Viral Veto Cell

|

Validate and introduce new commercial treatment to increase engraftment of allogeneic bone marrow transplantations

|

1. Regulatory approval and treatment protocols

2. Conduct human clinical trials

3. Develop plan for commercial exploitation

|

· Initiate a human clinical trial in the US by 2019

· Commence human trials in Europe in 2020

|

|||

|

Veto – CAR-T Cell Therapy

|

Validate the possibility of combining Veto Cell treatment with CAR-T cell treatment for both blood cell cancer and solid tumor

cancer treatment

|

4. Collaboration with Zelig Eshhar, inventor of Car-T cells

5. Validate combined treatment model in clinical trials

|

· Proof of concept in completion in 2019

· Commence human trials in 2021 or 2022

|

|

1.

|

“Anti-rejection,

Anti-Viral” Veto Cell tolerance therapy for donor mismatched allogeneic bone marrow transplantations.

|

|

2.

|

“Anti-cancer”

Veto + CAR-T cell therapy for blood cell and, eventually, solid tumor cancers.

|

|

3.

|

“Anti-rejection”

Veto Cell tolerance therapy for donor mismatched organ transplantation.

|

| 4. |

Veto Cell tolerance therapy for non-malignant disorders.

|

|

1)

|

Complete development of human treatment protocol (2-5 years)

|

|

2)

|

Apply for and receive approval to commence human trials (9-18 months)

|

|

3)

|

Recruit patients (1-6 months)

|

|

4)

|

Conduct Phase I trials showing safety of product (1-2 years)

|

|

5)

|

Apply for and receive approval to conduct trials showing product efficacy (6-12 months)

|

|

6)

|

Data collecting and analysis (6-12 months)

|

|

7)

|

Conduct Phase II efficacy trials (2-3 years)

|

|

8)

|

Data collecting and analysis (6-12 months)

|

|

9)

|

Apply for and receive approval to conduct trials showing efficacy in larger numbers of patients (6-12 months)

|

|

10)

|

Conduct Phase III efficacy trials with larger numbers of patients (2-4 years)

|

|

11)

|

Data collecting and analysis (6-12 months)

|

|

12)

|

Apply for and receive approval for production scale manufacturing facilities (6-12 months)

|

|

13)

|

Contract third party or establish own production facilities (6-30 months)

|

|

14)

|

Contract third party or establish own distribution platform (6-18 months)

|

|

15)

|

Commence manufacturing and distribution (6-12 months)

|

|

·

|

successfully complete adequate and well-controlled clinical trials that demonstrate statistically significant

safety and efficacy and to obtain all requisite regulatory approvals in a timely and cost-effective manner;

|

|

·

|

effectively use patents and possibly exclusive partnership agreements with important third-party treatment

providers and collaboration partners to maintain a stable competitive stance for our Technology;

|

|

·

|

attract and retain appropriate clinical and commercial personnel and service providers; and

|

|

·

|

establish adequate distribution relationships for our products.

|

|

Strategy

Element

|

Introductory period

(years 1 -3 post FDA approval)

|

Years 4+

|

||

|

Market Segments

|

· Lymphoma and Leukemia

· Multiple Myeloma

|

· Same as before plus broader set of solid tumor cancer targets, kidney

and liver failure, sickle cell anemia beta

thalassemia and other

non-malignant hematological disorders;

|

||

|

Product Rollout

|

· Veto Cell therapy for B-cell malignancies

· Veto+CAR-T Veto Cell therapy for both blood cell cancers

cancers

|

· Veto Cell tolerizing treatment for HSCT and organ transplantation

· Veto Cell therapy for both liquid and solid tumor cancers as well

as non-malignant disorders;

|

|

Customer/ Geographic Focus

|

· North America

· Western Europe

· China

|

· North America, Western & Eastern Europe, Australia/New Zealand,

Russia, Brazil, selected Asian markets

|

||

|

Channels/Go to Market

|

· Direct relationships with leading transplantation centers

· International production and distribution through partners

|

· Partnership with global market leaders

|

||

|

Pricing

|

· Consistent with other cell therapy offerings currently associated with

transplantations and immuno-oncology

|

· Potentially higher volume, lower cost for “off the shelf” offerings

|

||

|

Operations

|

· Three production centers:

- US

- Western Europe

- Far East

· Initial capacity leased from or situated adjacent to major transplantation

center.

|

· Regional production centers owned or JV with partners

|

|

1)

|

Severity of unmet medical need: degree of severity of the indication and the effectiveness of existing

treatments. These criteria help determine the proper regulatory pathway.

|

|

2)

|

Technology relevance: relative value of the ability to manage immune response to the treatment of a given

indication.

|

|

1)

|

Treating patients after the end of Phase 2 (based on US Fast Track approvals and/or European Marketing

Authorization Approvals) with either partial or full insurance reimbursement available); and

|

|

2)

|

Potential upfront and milestone driven licensing revenues from collaborations with third parties.

|

|

a.

|

by January 1, 2022, to have commenced Phase II clinical trials in a respect of a Product;

|

|

b.

|

by January 1, 2025, to have either commenced Phase III clinical trials or to have received FDA or EMA

marketing approval in a respect of a Product (“Marketing Approval”);

|

|

c.

|

within 12 (twelve) months from the date of Marketing Approval, to have made a First Commercial Sale of a

Product; or

|

|

d.

|

in case commercial sale of any Product having commenced, there shall be a period of 12 (twelve) months or more

during which no sales of any Product shall take place by the Company or its Sublicensees (except as a result of force majeure or other factors beyond the control of the Company)."

|

|

·

|

Title.

All right, title and interest in and to the Licensed Information and the Patents (as those terms are defined in the Yeda License Agreement) and all right, title and interest in and to any drawings, plans, diagrams, specifications, other

documents, models, or any other physical matter in any way containing, representing or embodying any of the foregoing, vest and shall vest in Yeda and subject to the license granted in the Yeda License Agreement.

|

|

·

|

Patents.

Both Yeda and the Company shall consult with one another on the filing of patent applications for any portion of Licensed Information and/or corresponding to patent application existing at the time the Yeda License Agreement was executed.

Yeda shall retain outside patent counsel that will be approved by Cell Source, to prepare, file and prosecute patent applications. All applications will be filed in Yeda’s name.

|

|

·

|

Patents;

Patent Infringements. Where the Company determines that a third party is infringing one or more of the Patents or is sued, in prosecuting or defending such litigation, the Company must pay any expenses or costs or other

liabilities incurred in connection with such litigation (including attorney’s fees, costs and other sums awarded to the counterparty in such action). The Company agreed to indemnify Yeda against any such expenses or costs or other

liabilities.

|

|

·

|

License.

With regard to the expiration of Patents, a Product is deemed to be covered by a Patent so long as such Product is protected by “Orphan Drug” status (or the like). The Company has an exclusive worldwide license under the Licensed

Information and the Patents for the development, manufacture and sales of the Products. License remains in force in each country with respect to each Product until the later of (i) the expiration of the last Patent in such country

covering such Product or (ii) the expiration of a 15-year period commencing the day FDA New Drug Approval is received for a Product in such country.

|

|

i.

|

the proposed Sublicense is for monetary consideration only;

|

|

ii.

|

the proposed Sublicense is to be granted in a bona fide arm’s length commercial transaction;

|

|

iii.

|

a copy of the agreement granting the Sublicense and all amendments thereof shall be made available to Yeda, 14

days before their execution and Cell Source shall submit to Yeda copies of all such Sublicenses and all amendments thereof promptly upon execution thereof; and

|

|

iv.

|

the proposed Sublicense is made by written agreement, the provisions of which are consistent with the terms of

the License and contain, inter alia, the following terms and conditions, including: the Sublicense shall expire automatically on the termination of the License for any reason.

|

|

·

|

Termination.

The Yeda License Agreement terminates on the later of: (i) the expiration of the last of the Patents or (ii) the expiry of a continuous period of 20 years during which there shall not have been a First commercial sale of any product in

any country. Yeda may terminate by written notice, effective immediately, if the Company challenges the validity of any of the Patents. If a challenge is unsuccessful, then in addition to Yeda’s right to termination, the Company shall pay

to Yeda liquidated damages in the amount of $8,000,000. Either the Company or Yeda may terminate the Yeda License Agreement and the License by serving a written notice upon (i) occurrence of a material breach or (ii) the granting of a

winding-up order. Additionally, Yeda may terminate for failure to reimburse Yeda for patent application and/or prosecution expenses.

|

Our success may depend, in part, on the extent to which reimbursement for the costs of therapeutic products and related treatments will be available from third-party payers such as government health administration authorities, private health insurers, managed care programs, and other organizations. Over the past decade, the cost of health care has risen significantly, and there have been numerous proposals by legislators, regulators, and third-party health care payers to curb these costs. Some of these proposals have involved limitations on the amount of reimbursement for certain products. Similar federal or state health care legislation may be adopted in the future and any products that we or our collaborators seek to commercialize may not be considered cost-effective. Adequate third-party insurance coverage may not be available for us or our collaborative partners to establish and maintain price levels that are sufficient for realization of an appropriate return on investment in product development.

|

·

|

the degree and range of protection any patents will afford us against competitors, including whether third

parties will find ways to invalidate or otherwise circumvent the patents that we license;

|

|

·

|

whether or not others will obtain patents claiming aspects similar to those covered by the patents

that we license; or

|

|

·

|

whether we will need to initiate litigation or administrative proceedings, which may be costly whether we win

or lose.

|

|

·

|

the duration of the clinical trial;

|

|

·

|

the number of sites included in the trials;

|

|

·

|

the countries in which the trial is conducted;

|

|

·

|

the length of time required and ability to enroll eligible patients;

|

|

·

|

the number of patients that participate in the trials;

|

|

·

|

the number of doses that patients receive;

|

|

·

|

the drop-out or discontinuation rates of patients;

|

|

·

|

per patient trial costs;

|

|

·

|

third party contractors failing to comply with regulatory requirements or meet their contractual obligations

to us in a timely manner;

|

|

·

|

our final product candidates having different properties in humans than in laboratory testing;

|

|

·

|

the need to suspend or terminate our clinical trials;

|

|

·

|

insufficient or inadequate supply of quality of necessary materials to conduct our trials;

|

|

·

|

potential additional safety monitoring, or other conditions required by FDA or comparable foreign regulatory

authorities regarding the scope or design of our clinical trials, or other studies requested by regulatory agencies;

|

|

·

|

problems engaging institutional review boards (“IRB”) to oversee trials or in obtaining and maintaining IRB

approval of studies;

|

|

·

|

the duration of patient follow-up;

|

|

·

|

the efficacy and safety profile of a product candidate;

|

|

·

|

the costs and timing of obtaining regulatory approvals; and

|

|

·

|

the costs involved in enforcing or defending patent claims or other intellectual property rights.

|

|

·

|

delays in the development of manufacturing capabilities for our product candidates to enable their consistent

production at clinical trial scale;

|

|

·

|

delays in the commencement of clinical trials as a result of clinical trial holds or the need to obtain

additional information to complete an Investigational New Drug Application (IND);

|

|

·

|

delays in obtaining regulatory approval to commence new trials;

|

|

·

|

adverse safety events experienced during our clinical trials;

|

|

·

|

insufficient efficacy during trials leading to withdrawal of product candidate;

|

|

·

|

delays in obtaining clinical materials;

|

|

·

|

slower than expected patient recruitment for participation in clinical trials; and

|

|

·

|

delays in reaching agreement on acceptable clinical trial agreement terms with prospective sites or obtaining

institutional review board approval.

|

|

·

|

our clinical trials may produce negative or inconclusive results, and we may decide, or regulators may require

us, to conduct additional clinical and/or preclinical testing or to abandon programs;

|

|

·

|

the results obtained in earlier stage clinical testing may not be indicative of results in future clinical

trials;

|

|

·

|

clinical trial results may not meet the level of statistical significance required by the FDA or other

regulatory agencies;

|

|

·

|

enrollment in our clinical trials for our product candidates may be slower than we anticipate, resulting in

significant delays and additional expense;

|

|

·

|

we, or regulators, may suspend or terminate our clinical trials if the participating patients are being

exposed to unacceptable health risks; and

|

|

·

|

the effects of our product candidates on patients may not be the desired effects or may include undesirable

side effects or other characteristics that may delay or preclude regulatory approval or limit their commercial use, if approved.

|

|

·

|

the therapeutic endpoints chosen for evaluation;

|

|

·

|

the eligibility criteria defined in the protocol;

|

|

·

|

the perceived benefit of the investigational drug under study;

|

|

·

|

the size of the patient population required for analysis of the clinical trial’s therapeutic endpoints;

|

|

·

|

our ability to recruit clinical trial investigators and sites with the appropriate competencies and

experience;

|

|

·

|

our ability to obtain and maintain patient consents; and

|

|

·

|

competition for patients by clinical trial programs for other treatments.

|

|

·

|

variations in our quarterly operating results;

|

|

·

|

announcements that our revenue or income are below analysts’ expectations;

|

|

·

|

general economic slowdowns;

|

|

·

|

sales of large blocks of the Company’s Common Stock; and

|

|

·

|

announcements by us or our competitors of significant contracts, acquisitions, strategic partnerships, joint

ventures or capital commitments.

|

|

·

|

Eleven notes payable with

principal amounts totaling $1,613,000; and

|

|

·

|

Seventeen convertible notes

payable with principal amounts totaling $1,060,000.

|

|

·

|

Only two years of audited financial statements in addition to any required unaudited interim financial

statements with correspondingly reduced "Management's Discussion and Analysis of Financial Condition and Results of Operations" disclosure;

|

|

·

|

Reduced disclosure about our executive compensation arrangements;

|

|

·

|

Exemption from the auditor attestation requirement in the assessment of our internal control over financial

reporting.

|

Management’s efforts to remediate the material weakness included raising funds and seeking new resources to alleviate this material weakness and filing all necessary regulatory reports on a timely basis. Although management concluded that our internal controls over financial reporting were effective as of December 31, 2018, there can be no assurance that we will have the necessary resources to maintain effective controls in future periods.

|

2018 Fiscal Year

|

||||||||

|

High

|

Low

|

|||||||

|

First Quarter ended March 31, 2018

|

$

|

0.43

|

$

|

0.25

|

||||

|

Second Quarter ended June 30, 2018

|

$

|

0.85

|

$

|

0.42

|

||||

|

Third Quarter ended September 30, 2018

|

$

|

1.09

|

$

|

0.55

|

||||

|

Fourth Quarter ended December 31, 2018

|

$

|

0.75

|

$

|

0.45

|

||||

|

2017 Fiscal Year

|

||||||||

|

High

|

Low

|

|||||||

|

First Quarter ended March 31, 2017

|

$

|

0.53

|

$

|

0.35

|

||||

|

Second Quarter ended June 30, 2017

|

$

|

0.45

|

$

|

0.25

|

||||

|

Third Quarter ended September 30, 2017

|

$

|

0.40

|

$

|

0.30

|

||||

|

Fourth Quarter ended December 31, 2017

|

$

|

0.45

|

$

|

0.20

|

||||

|

·

|

Hematological malignancies (leukemias, lymphomas, etc.). One of the most effective treatments for these

conditions is SCT - stem cell transplantation (e.g. bone marrow transplantation). While the challenge finding donors for allogeneic (donor vs. patient derived) SCT can be addressed through haploidentical (partially mismatched donor)

transplants, is a risky and difficult procedure primarily because of potential conflicts between host and donor immune systems and also due to viral infections that often follow even successful SCT while the compromised new immune system

works to reconstitute itself by using the transplanted stem cells.

|

|

·

|

The broader set of cancers, including solid tumors, that can potentially be treated effectively using

genetically modified cells such as CAR-T cells, but also face efficacy and economic constraints due to limited persistence based on immune system issues (i.e., the need to be able to safely and efficiently deliver allogeneic CAR-T

therapy).

|

|

·

|

Organ failure and transplantation. A variety of conditions can be treated by the transplantation of vital

organs. However, transplantation is limited both by the insufficient supply of available donor organs and the need for lifelong, daily anti-reject treatments post-transplant.

|

|

·

|

Non-malignant hematological conditions (such as sickle cell anemia) which could, in many cases, also be

effectively treated by stem cell transplantation if the procedure could be made safer and more accessible by addressing conflicts between host and donor immune systems.

|

On February 7, 2019, MD Anderson submitted an IND application with respect to the Anti-Rejection, Anti-Viral Veto Cell to the FDA.

On February 19, 2019, we entered into an agreement with MD Andersen for the latter to perform cell production and conduct Phase I/II human clinical trials. In connection with that agreement, we committed to fund such work in the amount of approximately $2,000,000 over a two-year period beginning that same date.

Loss on Exchange of Warrants for Common Stock

During the year ended December 31, 2017, we recognized $38,393 of loss on exchange of warrants for common stock related to outstanding warrants exchanged in connection with a note extension during the period.|

December 31,

|

||||||||

|

2018

|

2017

|

|||||||

|

Cash

|

$

|

18,934

|

$

|

371,048

|

||||

|

Working capital deficiency

|

$

|

(4,920,171

|

)

|

$

|

(4,557,374

|

)

|

||

|

(1)

|

Due to a lack of financial resources, we were unable to file our annual reports on Form 10-K for the years

ended December 31, 2017 and December 31, 2016 and the quarterly reports on Form 10-Q for the periods ended March 31, 2017, June 30, 2017, September 30, 2017, March 31, 2018 and June 30, 2018 on a timely basis. Management evaluated the

lack of financial resources in its assessment of our reporting controls and procedures and has concluded that the control deficiency represented a material weakness.

|

|

Name

|

Age

|

Title(s)

|

||

|

Dennis Brown

|

69

|

Director (Chairman)

|

||

|

Itamar Shimrat

|

59

|

Chief Executive Officer, Chief Financial Officer and Director

|

||

|

Yoram Drucker

|

53

|

Director

|

||

|

David Zolty

|

69

|

Director

|

||

|

Ben Friedman

|

60

|

Director

|

| 1. |

any bankruptcy petition filed by or against such person or any business of which such person was a general partner or executive officer either at the time

of the bankruptcy or within two years prior to that time;

|

| 2. |

any conviction in a criminal proceeding or being subject to a pending criminal proceeding (excluding traffic violations and other minor offenses);

|

| 3. |

being subject to any order, judgment, or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction, permanently or

temporarily enjoining him from or otherwise limiting his involvement in any type of business, securities or banking activities or to be associated with any person practicing in banking or securities activities;

|

| 4. |

being found by a court of competent jurisdiction in a civil action, the SEC or the Commodity Futures Trading Commission to have violated a Federal or state

securities or commodities law, and the judgment has not been reversed, suspended, or vacated;

|

| 5. |

being subject of, or a party to, any Federal or state judicial or administrative order, judgment decree, or finding, not subsequently reversed, suspended or

vacated, relating to an alleged violation of any Federal or state securities or commodities law or regulation, any law or regulation respecting financial institutions or insurance companies, or any law or regulation prohibiting mail

or wire fraud or fraud in connection with any business entity; or

|

| 6. |

being subject of or party to any sanction or order, not subsequently reversed, suspended, or vacated, of any self-regulatory organization, any registered

entity or any equivalent exchange, association, entity or organization that has disciplinary authority over its members or persons associated with a member.

|

|

Name and

|

Stock

|

Option

|

All Other

|

||||||||||||||||||||||

|

Principal Position

|

Year

|

Salary

|

Bonus

|

Awards

|

Awards

|

Compensation

|

Total

|

||||||||||||||||||

|

Itamar Shimrat

|

2018

|

$

|

165,625

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

165,625

|

||||||||||||

|

Chief Executive Officer

|

2017

|

$

|

179,064

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

179,064

|

||||||||||||

|

Option Awards

|

Stock Awards

|

||||||||||||||||||||||||||||||||

|

Equity

|

|||||||||||||||||||||||||||||||||

|

incentive

|

|||||||||||||||||||||||||||||||||

|

plan

|

|||||||||||||||||||||||||||||||||

|

Equity

|

awards:

|

||||||||||||||||||||||||||||||||

|

incentive

|

Market or

|

||||||||||||||||||||||||||||||||

|

Equity

|

plan

|

payout

|

|||||||||||||||||||||||||||||||

|

incentive

|

awards:

|

value of

|

|||||||||||||||||||||||||||||||

|

plan awards:

|

Number of

|

unearned

|

|||||||||||||||||||||||||||||||

|

Number of

|

Number of

|

Number of

|

Number

|

Market

|

unearned

|

shares,

|

|||||||||||||||||||||||||||

|

securities

|

securities

|

securities

|

of shares

|

value of

|

shares,

|

units or

|

|||||||||||||||||||||||||||

|

underlying

|

underlying

|

underlying

|

or units of

|

shares of

|

units or

|

other

|

|||||||||||||||||||||||||||

|

unexercised

|

unexercised

|

unexercised

|

Option

|

Option

|

stock that

|

units

|

other rights

|

rights

|

|||||||||||||||||||||||||

|

options

|

options

|

unearned

|

exercise

|

expiration

|

have not

|

that have

|

that have

|

that have

|

|||||||||||||||||||||||||

|

Name

|

exercisable

|

unexercisable

|

options

|

price

|

date

|

vested

|

not vested

|

not vested

|

not vested

|

||||||||||||||||||||||||

|

Itamar Shimrat

|

750,000

|

-

|

-

|

$

|

0.75

|

11/10/2019

|

-

|

$

|

-

|

-

|

$

|

-

|

|||||||||||||||||||||

|

Change in

|

|||||||||||||||||||||||||

|

Present Value

|

|||||||||||||||||||||||||

|

and

|

|||||||||||||||||||||||||

|

Fees

|

Nonqualified

|

||||||||||||||||||||||||

|

Earned or

|

Deferred

|

||||||||||||||||||||||||

|

Paid In

|

Stock

|

Option

|

Compensation

|

All Other

|

|||||||||||||||||||||

|

Year

|

Salary

|

Awards

|

Awards

|

Earnings

|

Compensation

|

Total

|

|||||||||||||||||||

|

Dennis Brown

|

2018

|

$ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||||

|

Yoram Drucker

|

2018

|

$ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||||

|

David Zolty

|

2018

|

$ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||||

|

Ben Friedman

|

2018

|

$ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||||

|

As of March 27, 2019

|

|||||||||

|

Name and Address of Beneficial Owner (10)

|

Amount and Nature

of

Beneficial Ownership (1)

|

Percentage of

Class (2)

|

|||||||

|

Directors and Officers:

|

|||||||||

|

Yoram Drucker, Director

|

1,125,004

|

(3)

|

4.22

|

%

|

|||||

|

Itamar Shimrat, Chief Executive Officer, Chief Financial Officer and Director

|

1,337,311

|

(4)

|

4.99

|

%

|

|||||

|

David Zolty, Director

|

1,168,318

|

(5)

|

4.47

|

%

|

|||||

|

Ben Friedman, Director (6)

|

4,383,344

|

(7)

|

16.80

|

%

|

|||||

|

Dennis Brown, Director (Executive Chairman)

|

200,000

|

(8)

|

*

|

||||||

|

All directors and executive officers as a group (5 persons)

|

8,213,977

|

29.80

|

%

|

||||||

|

Yeda Research & Development Co. Ltd.

P.O. Box 95

Rehovot, 76100, Israel

|

1,308,684

|

(9)

|

4.99

|

%

|

|||||

| * |

less than 1%

|

| (1) |

Beneficial ownership is determined in accordance with the rules of the SEC and generally includes voting or

investment power with respect to securities. Shares of common stock subject to options or warrants currently exercisable or convertible, or exercisable or convertible within 60 days of March27, 2019 are deemed outstanding for computing

the percentage of the person holding such option or warrant but are not deemed outstanding for computing the percentage of any other person.

|

| (2) |

Based on 26,077,611 shares issued and outstanding as of March 27, 2019.

|

| (3) |

Includes a five-year warrant to purchase 550,000 shares of common stock with an exercise price of $0.75 per share.

|

| (4) |

Includes 762,307 shares of a five-year warrant to purchase 750,000 shares of

common stock with an exercise price of $0.75 per share, which warrant is subject to

a 4.99% conversion limitation.

|

| (5) |

Includes warrants to purchase a total of 72,500 shares of common stock with an exercise price of $0.75 per share.

|

| (6) |

Mr. Friedman’s beneficial ownership includes shares beneficially owned by his wife, Phyllis Friedman.

|

| (7) |

Excludes a five-year warrant to purchase 50,000 shares of common stock with an exercise price of $0.75 per share, which warrant is subject to a 4.99%

conversion limitation.

|

| (8) |

Includes a five-year warrant to purchase 100,000 shares of common stock with an exercise price of $0.75 per share.

|

| (9) |

Includes 148,722 shares of a five-year warrant to purchase 1,995,376 shares of common stock with an exercise price

of $0.001 per share, which warrant is subject to a 4.99% conversion limitation.

|

| (10) |

Except as otherwise indicated, the address of each beneficial owner is c/o Cell Source, Inc., 57 West 57th Street, Suite 400, New York, New York 10019.

|

|

2018

|

2017

|

|||||||

|

Audit Fees

|

$

|

185,900

|

$

|

73,000

|

||||

|

Tax fees

|

--

|

--

|

||||||

|

All other fees

|

--

|

--

|

||||||

|

$

|

185,900

|

$

|

73,000

|

|||||

|

Exhibit

Number

|

Description

|

|

|

2.1 (1)

|

Share Exchange Agreement, dated June 30, 2014, by and between Cell Source, Ltd., and Ticket to See, Inc.

|

|

|

3.1 (1)

|

Articles of Association of Cell Source Limited, dated August 14, 2011, as amended on November 11, 2013

|

|

|

3.2 (2)

|

Articles of Incorporation of Ticket to See, Inc., dated June 6, 2012

|

|

|

3.3 (3)

|

Certificate of Amendment to Articles of Incorporation of Ticket to See, Inc., dated June 23, 2014

|

|

|

3.3 (4)

|

Certificate of Amendment to Articles of Incorporation of Ticket to See, Inc., dated May 20, 2014

|

|

|

3.4 (2)

|

Bylaws of Cell Source, Inc., dated June 6, 2012

|

|

|

3.5 (18)

|

Certificate of Designation with respect to Series A Preferred Stock dated November 14, 2016

|

|

|

10.1 (1)

|

Form of Subscription Agreement

|

|

|

10.2 (1)

|

Form of Registration Rights Agreement

|

|

|

10.3 (1)

|

Form of Investor Warrant

|

|

|

10.4 (1)

|

Form of Consultant Warrant(8)

|

|

|

10.5 (1)

|

Form of Researcher Company Warrant

|

|

|

10.6 (1)

|

Form of Company Warrant

|

|

|

10.7 (1)

|

Form of Lockup Agreement (included in Exhibit 2.1)

|

|

|

10.8 (1)

|

Research and License Agreement by and between Yeda Research and Development Company Limited and Cell Source

Limited, dated October 3, 2011

|

|

|

10.9 (1)

|

Amendment to Research and License Agreement

|

|

|

10.10 (1)

|

Evaluation and Exclusive Option Agreement by and between Yeda Research and Development Company Limited and Cell

Source Limited, dated Oct. 3, 2011 (included in Exhibit 10.7)

|

|

|

10.11 (1)

|

Amendment dated April 1, 2014 to Evaluation and Exclusive Option Agreement by and between Yeda Research and

Development Company Limited and Cell Source Limited

|

|

|

10.12 (1)

|

Second Amendment dated June 22, 2014 to Evaluation and Exclusive Option Agreement by and between Yeda Research and

Development Company Limited and Cell Source Limited

|

|

|

10.13 (1)

|

Consulting Agreement by and between Cell Source Limited and Professor Yair Reisner

|

|

|

10.14 (6)

|

Form of Amendment No. 1 to Registration Rights Agreement

|

|

|

10.15 (7)

|

Bridge Funding Agreement

|

|

|

10.16 (5)

|

Third Amendment dated June 22, 2014 to Evaluation and Exclusive Option Agreement by and between Yeda Research and

Development Company Limited and Cell Source Limited

|

|

|

10.17 (8)

|

Form of Consulting Agreement pursuant to which the Company issued warrants to purchase an aggregate of 2,000,000

shares of the Company’s common stock

|

|

|

10.18 (9)

|

Form of Promissory Note issued to the Company’s Chief Executive Officer

|

|

|

10.19(10)

|

Form of March 2015 Promissory Note

|

|

|

10.20(10)

|

Form of March 2015 Warrant

|

|

|

10.21(11)

|

Form of Note Amendment Letter Agreement

|

|

|

10.22(11)

|

Form of May 2015 Note

|

|

|

10.23(11)

|

Form of May 2015 Warrant

|

|

|

10.24(12)

|

Form of Advisory/Consulting Agreement

|

|

|

10.25(13)

|

Zolty Promissory Note

|

|

|

10.26(13)

|

Zolty Warrant

|

|

|

10.27(13)

|

Form of July 2015 Convertible Promissory Note

|

|

|

10.28(13)

|

Form of July 2015 Warrant

|

|

10.29(15)

|

Form of Bridge Note Subscription Agreement

|

|

|

10.30(15)

|

Form of Convertible Note

|

|

|

10.31(15)

|

Form of March 2016 Note

|

|

|

10.32(15)

|

Form of March 2016 Warrant

|

|

|

10.33(18)

|

Form of July 2016 Warrants

|

|

|

10.34(18)

|

Second Amendment to Research and License Agreement dated as of November 28, 2016 between the Company and Yeda

Research and Development Company Limited

|

|

|

10.35(18)

|

Third Amendment to Research and License Agreement dated as of March 29, 2018 between the Company and Yeda Research

and Development Company Limited

|

|

|

10.36(18)

|

Fourth Amendment to Research and License Agreement dated as of March 30, 2018 between the Company and Yeda Research

and Development Company Limited

|

|

|

10.37(16)

|

Convertible Note due July 27, 2016

|

|

|

10.38(17)

|

Promissory Note dated May 10, 2016

|

|

|

10.39(19) *

|

Sponsored Research Agreement dated November 28, 2018 between The University of Texas M.D. Anderson Cancer Center and Cell Source

Limited

|

|

| 10.40(19) * |