Form DEFA14A Corporate Capital Trust,

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Pursuant to Rule 14a-12 |

CORPORATE CAPITAL TRUST, INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

| 1) | Title of each class of securities to which transaction applies: | |

| 2) | Aggregate number of securities to which transaction applies: | |

| 3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| 4) | Proposed maximum aggregate value of transaction: | |

| 5) | Total fee paid: | |

☐ Fee paid previously with preliminary materials:

☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| 1) | Amount Previously Paid: | |

| 2) | Form, Schedule or Registration Statement No.: | |

| 3) | Filing Party: | |

| 4) | Date Filed: | |

A copy of a presentation that was first used on September 12, 2017 by representatives of Corporate Capital Trust, Inc. in meetings with research analysts, existing investors and other parties is set forth below.

* * *

CONFIDENTIAL AND PROPRIETARY: For Investment Professionals Only Provided by Request Corporate Capital Trust, Inc. September 12, 2017

This presentation is for informational purposes only and is neither an offer to sell nor a solicitation of an offer to buy the securities described herein . Investing in Corporate Capital Trust is not suitable for all investors and they should carefully read the information in our Forms 10 - Q and 10 - K filings and in our other public filings before making an investment . Consider the investment objectives, risks, charges and expenses before deciding to invest in our shares of common stock . The information contained herein does not replace or supersede any information contained within the company’s 10 - K, 10 - Qs or other public filings . Corporate Capital Trust closed to new investors who purchase through the independent broker - dealer channel on Feb . 12 , 2016 . Corporate Capital Trust is currently advised by CNL Fund Advisors Company (CNL) and subadvised by KKR Credit Advisors (US) LLC (KKR Credit), affiliates of CNL Financial Group and KKR & Co . L . P . , respectively . The data and information presented are for informational purposes only . KKR Credit conducts its business through KKR Credit Advisors (US) LLC, an SEC - registered investment adviser, KKR Credit Advisors (Ireland), authorized and regulated by the Central Bank of Ireland, and KKR Credit Advisors (UK) LLP which is authorized and regulated by the Financial Conduct Authority in the United Kingdom . References to “KKR Capstone” or “Capstone” are to all or any of KKR Capstone Americas LLC, KKR Capstone EMEA LLP, KKR Capstone EMEA (International) LLP, KKR Capstone Asia Limited, and their affiliates, which are owned and controlled by their senior management . KKR Capstone is not a subsidiary or affiliate of KKR . KKR Capstone operates under several consulting agreements with KKR and uses the “KKR” name under license from KKR . References to operating executives, operating experts, or operating consultants are to employees of KKR Capstone and not to employees of KKR . In this presentation, the impact of initiatives in which KKR Capstone has been involved is based on KKR Capstone’s internal analysis and information provided by the applicable portfolio company . Impacts of such initiatives are estimates that have not been verified by a third party and are not based on any established standards or protocols . They may also reflect the influence of external factors, such as macroeconomic or industry trends, that are unrelated to the initiative presented . Participation of KKR Private Equity, KKR Capital Markets, and KKR Capstone personnel in the public investment process is subject to applicable law and inside information barrier policies and procedures, which may limit the involvement of KKR Private Equity, KKR Capital Markets, and KKR Capstone personnel in certain circumstances and KKR Credit’s ability to leverage such integration with KKR . Discussions with Senior Advisors and employees of KKR’s managed portfolio companies are also subject to the inside information barrier policies and procedures, which may restrict or limit discussions and/or collaborations with KKR Credit . Additional Information and Where to Find It : In connection with the matters described in this communication, the Company has filed relevant materials with the Securities and Exchange Commission (the “SEC”), including a definitive proxy statement on Schedule 14 A . The Company has mailed the definitive proxy statement and a proxy card to each stockholder entitled to vote at the stockholder meeting relating to such matters . STOCKHOLDERS OF THE COMPANY ARE URGED TO READ THESE MATERIALS (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO), AND ANY OTHER RELEVANT DOCUMENTS THAT THE COMPANY WILL FILE WITH THE SEC WHEN THEY BECOME AVAILABLE, BECAUSE THESE MATERIALS WILL CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY AND THE MATTERS DESCRIBED IN THIS COMMUNICATION . The definitive proxy statement and other relevant materials (when they become available), and any other documents filed by the Company with the SEC, may be obtained free of charge at the SEC’s website (http : //www . sec . gov), at the Company’s website (http : //www . corporatecapitaltrust . com/investor - resources), or by writing to the Company at 450 S . Orange Avenue, Orlando, Florida 32801 (telephone number 866 - 650 - 0650 ) . The information contained in this presentation is for informational purposes only and is not an offer to buy or the solicitation of an offer to sell any securities of the Company . The tender offer referenced herein will be made only pursuant to an offer to purchase, letter of transmittal and related materials (the “Tender Materials”) . The full details of the each of tender offer, including complete instructions on how to tender shares of common stock, will be included in the Tender Materials, which the Company will distribute to shareholders and file with the SEC upon the commencement of the tender offer . Shareholders are urged to carefully read the Tender Materials when they become available because they will contain important information, including the terms and conditions of the tender offer . The Tender Materials (when they become available), and any other documents filed by the Company with the SEC, may be obtained free of charge at the SEC’s website (http : //www . sec . gov), at the Company’s website (http : //www . corporatecapitaltrust . com/investor - resources), or by writing to the Company at 450 S . Orange Avenue, Orlando, Florida 32801 (telephone number 866 - 650 - 0650 ) . Participants in the Solicitation : The Company and its directors and officers may be deemed to be participants in the solicitation of proxies from the Company’s stockholders with respect to the matters described in this communication . Information about the Company’s directors and officers, as well as the identity of other potential participants, and their respective direct or indirect interests in such matters, by security holdings or otherwise, are set forth in the definitive proxy statement and other materials filed with SEC . 2 Important Information

3 Some of the statements in this presentation constitute “forward - looking statements” because they relate to future events or the future performance or financial condition of the company . These statements are based on the beliefs and assumptions of the company’s management and on the information currently available to management at the time of such statements . Although we believe that the expectations reflected in such forward - looking statements are based upon reasonable assumptions, our actual results could differ materially from those set forth in the forward - looking statements . Some factors that might cause such a difference include the following : persistent economic weakness at the global or national level, increased direct competition, changes in government regulations or accounting rules, changes in local, national and global capital market conditions, our ability to obtain or maintain credit lines or credit facilities on satisfactory terms, changes in interest rates, our ability to identify suitable investments, our ability to close on identified investments, our ability to maintain our qualification as a regulated investment company and as a business development company, the ability of our Advisors and their affiliates to attract and retain highly talented professionals, the ability of our Advisors to locate suitable borrowers for our loans, the ability of such borrowers to make payments under their respective loans, our ability to complete the listing of our shares of common stock on the New York Stock Exchange LLC (NYSE), our ability to complete the proposed related tender offer, and the price at which shares of our common stock may trade on the NYSE, which may be higher or lower than the purchase price in the proposed tender offer . Given these uncertainties, we caution you not to place undue reliance on such statements, which apply only as of the date hereof . Forward - looking statements generally can be identified by the words “believes,” “expects,” “intends,” “plans,” “estimates” or similar expressions that indicate future events . Important factors that could cause actual results to differ materially from the company’s expectations include those described above and disclosed in the company’s filings with the SEC, including the company’s annual report on Form 10 - K for the year ended December 31 , 2016 , which was filed with the SEC on March 20 , 2017 and the company’s quarterly reports subsequently filed on form 10 - Q . The company undertakes no obligation to update such statements to reflect subsequent events . Important Information & Forward Looking Statements

4 The company and its directors and officers may be deemed to be participants in the solicitation of proxies from the company’s stockholders with respect to the matters described in this communication . Information about the company’s directors and officers, as well as the identity of other potential participants, and their respective direct or indirect interests in such matters, by security holdings or otherwise, are set forth in the definitive proxy statement and other materials filed with SEC . Risk Factors In addition to the other risk factors disclosed in our Forms 10 - K and 10 - Q, risks of investing in Corporate Capital Trust include : • Investing in Corporate Capital Trust may be considered speculative and involves a high degree of risk, including the risk of a substantial loss of investment . Other risks include a limited operating history, reliance on the advisors of the company, conflicts of interest, payment of substantial fees to the advisors of the company and its affiliates, limited liquidity, and liquidation at less than the original amount invested . Corporate Capital Trust is a long - term investment . Investing for short time periods makes losses more likely . See the Risk Factors section in our Forms 10 - K, 10 - Q and other public filings to read about the risks an investor should consider before buying shares of Corporate Capital Trust . There is no assurance the investment objectives will be met . • Corporate Capital Trust may extend loans to those with low credit quality and there may be limited information about those companies, which involves interest rate risk and financial market risk . Leverage can increase expenses and also volatility, which may magnify gains and losses . • Distributions are not guaranteed and subject to change . Future distributions may include a return of principal or borrowed funds, which may lower overall returns to the investor and may not be sustainable . We have borrowed funds to make investments, which increases the risks of investing in our shares . • An investment in Corporate Capital Trust is illiquid, which means that an investor will have limited ability to sell shares and should not expect to be able to sell their holdings until a liquidity event such as the proposed listing described herein . The board of directors must consider a liquidity event on or before Dec . 31 , 2018 , but there is no guarantee that any liquidity event will take place . Information Barrier Disclosure Participation of KKR Private Equity, KKR Capital Markets, and KKR Capstone personnel in the public markets investment process is subject to applicable law and inside information barrier policies and procedures, which may limit the involvement of such personnel in certain circumstances and KKR Credit’s ability to leverage such integration with KKR . Discussions with Senior Advisors and employees of the Firm’s managed portfolio companies are also subject to the inside information barrier policies and procedures, which may restrict or limit discussions and/or collaborations with KKR Credit . Assets Under Management References to “assets under management” or “AUM” represent the assets managed by KKR or its strategic partners as to which KKR is entitled to receive a fee or carried interest (either currently or upon deployment of capital) and general partner capital . KKR calculates the amount of AUM as of any date as the sum of : ( i ) the fair value of the investments of KKR's investment funds ; (ii) uncalled capital commitments from these funds, including uncalled capital commitments from which KKR is currently not earning management fees or carried interest ; (iii) the fair value of investments in KKR's co - investment vehicles ; (iv) the par value of outstanding CLOs (excluding CLOs wholly - owned by KKR) ; (v) KKR's pro - rata portion of the AUM managed by strategic partnerships in which KKR holds a minority ownership interest and (vi) the fair value of other assets managed by KKR . The pro - rata portion of the AUM managed by strategic partnerships is calculated based on KKR’s percentage ownership interest in such entities multiplied by such entity’s respective AUM . KKR’s calculation of AUM may differ from the calculations of other asset managers and, as a result, KKR’s measurements of its AUM may not be comparable to similar measures presented by other asset managers . KKR's definition of AUM is not based on the definitions of AUM that may be set forth in agreements governing the investment funds, vehicles or accounts that it manages and is not calculated pursuant to any regulatory definitions . Important Information

Senior Management 5 Todd Builione Member, KKR CEO of CCT Daniel P i etrzak Managing Director, KKR CIO of CCT Ryan Wilson Director, KKR COO / Associate PM of CCT • Joined KKR in January 2016 • Formerly a Managing Director and Co - Head of Structured Finance at Deutsche Bank • Prior experience includes Societe Generale and CIBC World Markets • B.S., Lehigh University • M.B.A., The Wharton School of the University of Pennsylvania • Joined KKR in 2013 • Formerly President of Highbridge Capital Management • Prior experience includes Goldman Sachs • B.S., Cornell University • J.D., Harvard Law School • Joined KKR in 2006 • Prior experience includes PwC • B.A., Wilfrid Laurier University • M.Acc ., University of Waterloo Thomas Murphy Director, KKR CFO of CCT • Joined KKR in 2009 • CFO of KKR Financial Holdings LLC (KFN) since 2015, Chief Accounting Officer of KFN 2009 - 2015 • Prior experience includes Countrywide Bank, Dell and Deloitte & Touche • B.A., University College Cork

Table of Contents 6 Overview of CCT 7 KKR Credit Platform 14 CCT’s Portfolio 22 Listing Details 28 Appendix – Historical Financials 32 Appendix – Case Studies 35

Overview of CCT 7

CCT Is An Industry Leading Business Development Company 8 Externally managed by KKR Credit • Leverages the full KKR platform • SEC exemptive relief • Strong alignment between KKR / CCT Significant scale with $4.4bn of assets • Focused on larger middle market companies • Typically sole or lead lender in originated credits • Scale can allow for more attractive funding Access to middle market direct lending opportunity • Stable recurring income generation • Established and diversified portfolio of 128 borrowers (1) • 71% of portfolio in senior secured investments (1) CCT is a business development company focused on making originated, senior secured loans to middle market companies Note: Please refer to “Important Information” at the beginning of this presentation for additional detail on the calculation of AUM and for further information on KKR’s inside information barrier policies and procedures, which may limit the involvement of personnel in certain investment pro cesses and discussions. 1) As of June 30, 2017.

Overview of KKR – A Leading Asset Management Platform Note: AUM and headcount as of June 30, 2017. Please refer to “Important Information” at the beginning of this presentation fo r a dditional detail on the calculation of AUM and for further information on KKR’s inside information barrier policies and procedures, which may limit the involvement of personnel in certain investme nt processes and discussions. KKR Capstone is not a subsidiary or affiliate of KKR. Please see Important Information for additional disclosure regarding KK R C apstone. Founded 1976 9 $148bn Assets Under Management Stakeholder Management (10 people) Client and Partner Group (~75 people) Global Macro and Asset Allocation (7 people) KKR Global Institute (3 people) KKR Capstone (~50 people) $15bn Internal Balance Sheet Largely Invested Alongside Clients ~370 Investment Professionals 19 Offices Globally Private Equity & Real Assets ~270 investment professionals ($85bn AUM) KKR Credit ~100 investment professionals ($39bn AUM) Capital Markets ~40 capital markets professionals (86 lead - left / active book - run transactions) HF Partnerships ($24bn AUM)

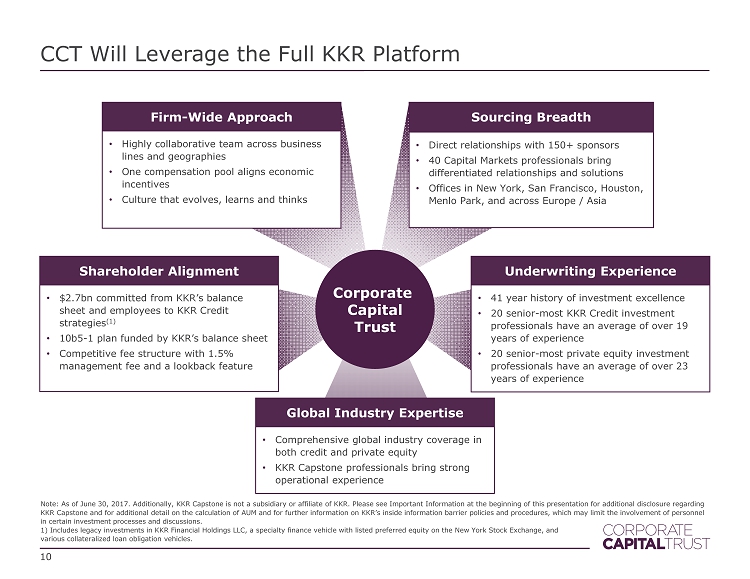

CCT Will Leverage the Full KKR Platform 10 Note: As of June 30, 2017. Additionally, KKR Capstone is not a subsidiary or affiliate of KKR. Please see Important Informati on at the beginning of this presentation for additional disclosure regarding KKR Capstone and for additional detail on the calculation of AUM and for further information on KKR’s inside information barrier policies and pro cedures, which may limit the involvement of personnel in certain investment processes and discussions. 1) Includes legacy investments in KKR Financial Holdings LLC, a specialty finance vehicle with listed preferred equity on the Ne w York Stock Exchange, and various collateralized loan obligation vehicles. Global Industry Expertise • Comprehensive global industry coverage in both credit and private equity • KKR Capstone professionals bring strong operational experience Underwriting Experience • 41 year history of investment excellence • 20 senior - most KKR Credit investment professionals have an average of over 19 years of experience • 20 senior - most private equity investment professionals have an average of over 23 years of experience Sourcing Breadth • Direct relationships with 150+ sponsors • 40 Capital Markets professionals bring differentiated relationships and solutions • Offices in New York, San Francisco, Houston, Menlo Park, and across Europe / Asia Shareholder Alignment • $2.7bn committed from KKR’s balance sheet and employees to KKR Credit strategies (1) • 10b5 - 1 plan funded by KKR’s balance sheet • Competitive fee structure with 1.5% management fee and a lookback feature Firm - Wide Approach • Highly collaborative team across business lines and geographies • One compensation pool aligns economic incentives • Culture that evolves, learns and thinks Corporate Capital Trust

Potentially Attractive Environment for Middle Market Direct Lending Private Equity Dry Powder Continues to Drive Strong Demand for Middle Market Lending… 5,000 6,000 7,000 8,000 9,000 10,000 11,000 0% 10% 20% 30% 40% 50% 60% 70% 80% 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 # US FDIC Banks Bank Market Share - US Lev. Loans Bank Market Share - US Lev. Loans # US FDIC Banks Source: Federal Deposit Insurance Corporation, S&P as of 12/31/2016 . Source: Prequin , as of July 1, 2017. $580bn $0 $100 $200 $300 $400 $500 $600 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 7/2017 11 … While Banks Have Retreated from Loan Market

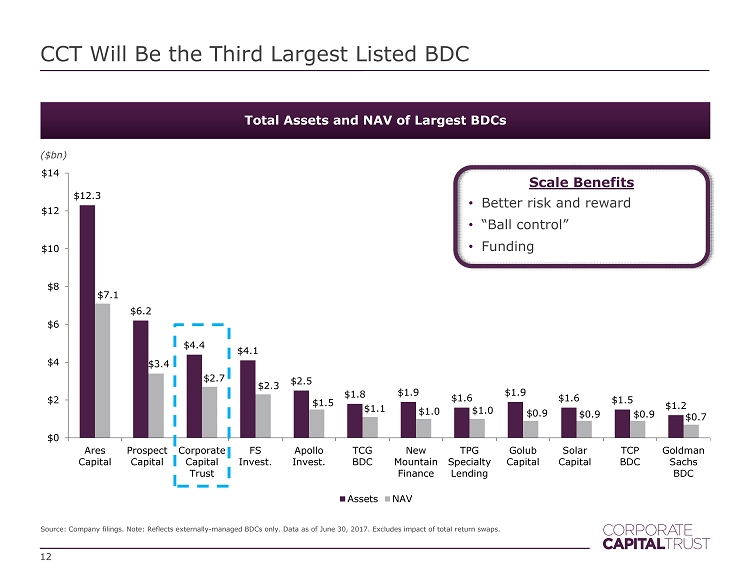

Total Assets and NAV of Largest BDCs ($ bn ) $12.3 $6.2 $4.4 $4.1 $2.5 $1.8 $1.9 $1.6 $1.9 $1.6 $1.5 $1.2 $7.1 $3.4 $2.7 $2.3 $1.5 $1.1 $1.0 $1.0 $0.9 $0.9 $0.9 $0.7 $0 $2 $4 $6 $8 $10 $12 $14 Ares Capital Prospect Capital Corporate Capital Trust FS Invest. Apollo Invest. TCG BDC New Mountain Finance TPG Specialty Lending Golub Capital Solar Capital TCP BDC Goldman Sachs BDC Assets NAV CCT Will Be the Third Largest Listed BDC Source: Company filings. Note : Reflects externally - managed BDCs only. Data as of June 30, 2017. Excludes impact of total return swaps. 12 Scale Benefits • “Ball control” • Funding • Better risk and reward

$0.1 $0.9 $2.3 $3.0 $4.0 $4.4 $4.4 CCT Is Mature and Scaled with $4.4bn of Assets Note: Gross assets as of June 30, 2017. Gross assets as of 2011 - 2016 year - end. 2011 2012 2013 2014 2015 2016 2017 Q2 CCT Gross Assets 13 May 2013 Granted SEC exemptive relief August 2016 First investment in JV with Conway Capital April 2017 Commenced plans to list and for KKR to become sole investment advisor March 2014 Received investment grade credit rating (BBB - ) from S&P 1.5% Mgmt Fee At Listing 20% Performance Fee 7% Hurdle Rate October 2016 Closed equity offering (>70k investors) July 2011 Commenced fundraising and investment operations June / August 2017 $245mm unsecured notes at a fixed 5% rate

KKR Credit Platform 14

Attributes (1) ~100 dedicated investment professionals across 8 cities in 7 countries ~750 issuers on the KKR Credit platform KKR balance sheet and employees have committed approximately $2.7bn to our credit strategies (2) $0 $5 $10 $15 $20 $25 $30 $35 $40 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 (June 30) Leveraged Credit Private Credit Special Situations KKR Credit – Global Credit Platform 15 1) As of June 30, 2017. 2) Includes legacy investments in KKR Financial Holdings LLC, a specialty finance vehicle with listed preferred equity on the Ne w Y ork Stock Exchange, and various collateralized loan obligation vehicles. $39.4bn KKR Credit Assets Under Management $20.8bn Leveraged Credit • Leveraged Loans • High Yield Bonds • Opportunistic Credit • CLOs $10.1bn Private Credit • Direct Lending • Asset - Backed Lending • Subordinated Debt • Revolving Credit $8.5bn Special Situations • Deep Value • Distressed • Event - Driven KKR Credit AUM Growth ($ bn ) (1)

Ongoing Monitoring & Risk Management • Full quarterly re - underwriting of every credit, supplemented with portfolio - level risk analysis • Hands - on investor when required, leveraging KKR operational and work - out teams Investment Approval Process • Private Credit Investment Committee serves as decision - making group • Unanimous decisions • Additional approvals required at CCT level Due Diligence / Underwriting • Intense and consistent underwriting process • “Private equity” - style due diligence; leverages investment and operational teams across KKR • Typically sole or lead lender; allows “ball control” in documentation and structural protections Initial Screening • Private Credit Investment Committee evaluates early - stage opportunities • Provides “go” or “no - go” decision; structure, pricing, and key diligence item views KKR Credit’s Investment Process Sourcing / Origination • 35 private credit originators and underwriters in New York, San Francisco, London and Dublin • Opportunities sourced from: 150+ sponsors covered, financial intermediaries, corporate relationships, ~750 issuers on KKR Credit platform • Deep industry and regional relationships across the KKR platform Note: Participation of KKR Private Equity, KKR Capital Markets, and KKR Capstone personnel in the public markets investment pro cess is subject to applicable laws, including the 1940 Act, and inside information barrier policies and procedures, which may limit the involvement of such personnel in certain circumstances and K KR Credit’s ability to leverage such integration with KKR. Discussions with Senior Advisors and employees of the KKR’s managed portfolio companies are also subject to the inside information barrier policies and procedures, which may restrict or limit discussions and/or collaborations with KKR Credit. 1 5 4 3 2 16

KKR Credit’s Origination Platform is Broad 17 Global Sponsor Coverage • Our size and underwriting capability appealing to sponsors • Viewed as solution providers given our capital markets expertise • Several sponsors consider us a preferred financing partner Global Corporates & Non - Sponsors • Cross - sales from KKR Credit & Private Equity direct relationships • Also sourced through financial advisors, banks with no balance sheet, and brokers • Family office and private bank relationships further enhance deal flow Incremental Channels • May include proactive refinancings within portfolio, failed syndications, and club deals • Wall Street relationships expand opportunity set, particularly in choppier capital markets • Benefit from the impact of regulation on financial institutions Global, Diversified Private Credit Sourcing Platform

Proprietary Sourcing Rigorous Screening The “KKR Advantage” Scale of KKR Private Credit Platform Drives Investment Opportunities KKR Private Credit’s large opportunity set is funneled through a rigorous screening and approval process Note: Reflects 2016 sourcing process for KKR Private Credit. 2016 Total Evaluated Opportunities 700 Total Screening Committee 350 (50% of Evaluated) Completed and Funded 37 (5% of Evaluated) Total Discussed at Private Credit Investment Committee 160 (23% of Evaluated) 18

Deep experience in valuation, structuring, deal tactics and execution Unanimous investment decisions required Iterative, interactive, and open dialogue focused on key issues Committee drives quarterly portfolio review process and re - underwrites each position Highly Experienced Private Credit Investment Committee Note: Please refer to “Important Information” at the beginning of this presentation for further information on KKR’s inside i nfo rmation barrier policies and procedures, which may limit the involvement of personnel in certain investment processes and discussions. The Company may use a ny one or none of the diligence processes described above. Daniel Pietrzak Matthieu Boulanger Nat Zilkha Chris Sheldon Marc Ciancimino 20 years of industry experience 18 years of industry experience 18 years of industry experience 19 years of industry experience 20 years of industry experience Co - Head of Private Credit Co - Head of Private Credit Co - Head of KKR Credit Co - Head of Special Situations Head of U.S. Leveraged Credit European Private Credit 19 Attributes

CCT Sits Alongside KKR Credit’s Other Client Accounts CCT shareholders have the same deal flow access to KKR Credit investment opportunities as institutional investors, receiving a pro rata allocation of deals that fit CCT’s mandate (1) 20 Note: Fee terms between funds may vary. 1) Pro rata allocation decisions are based on a variety of factors, including but not limited to, available capital, demand size , i nvestment suitability, deal - specific considerations, and portfolio management. Investment Process & Deal Allocation Senior Secured Loan Screened KKR Credit Deal Team Due Diligence Private Credit Investment Committee

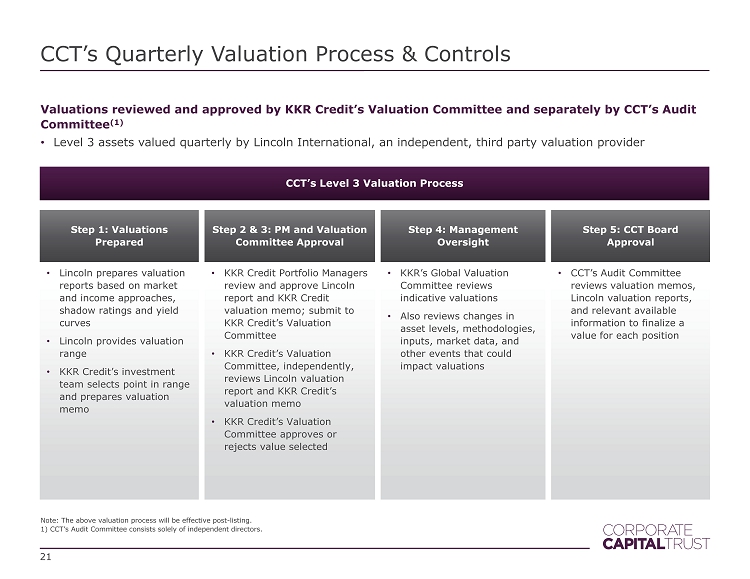

CCT’s Quarterly Valuation Process & Controls Valuations reviewed and approved by KKR Credit’s Valuation Committee and separately by CCT’s Audit Committee (1) • Level 3 assets valued quarterly by Lincoln International, an independent, third party valuation provider 21 Note: The above valuation process will be effective post - listing. 1) CCT’s Audit Committee consists solely of independent directors. Step 1: Valuations Prepared • Lincoln prepares valuation reports based on market and income approaches, shadow ratings and yield curves • Lincoln p rovides valuation range • KKR Credit’s investment team selects point in range and prepares valuation memo CCT’s Level 3 Valuation Process Step 2 & 3: PM and Valuation Committee Approval • KKR Credit Portfolio Managers review and approve Lincoln report and KKR Credit valuation memo ; submit to KKR Credit’s Valuation Committee • KKR Credit’s Valuation Committee, independently, reviews Lincoln valuation report and KKR Credit’s valuation memo • KKR Credit’s Valuation Committee approves or rejects value selected Step 4: Management Oversight • KKR’s Global Valuation Committee reviews indicative valuations • Also reviews changes in asset levels, methodologies, inputs, market data, and other events that could impact valuations Step 5: CCT Board Approval • CCT’s Audit Committee reviews valuation memos, Lincoln valuation reports, and relevant available information to finalize a value for each position

CCT’s Portfolio 22

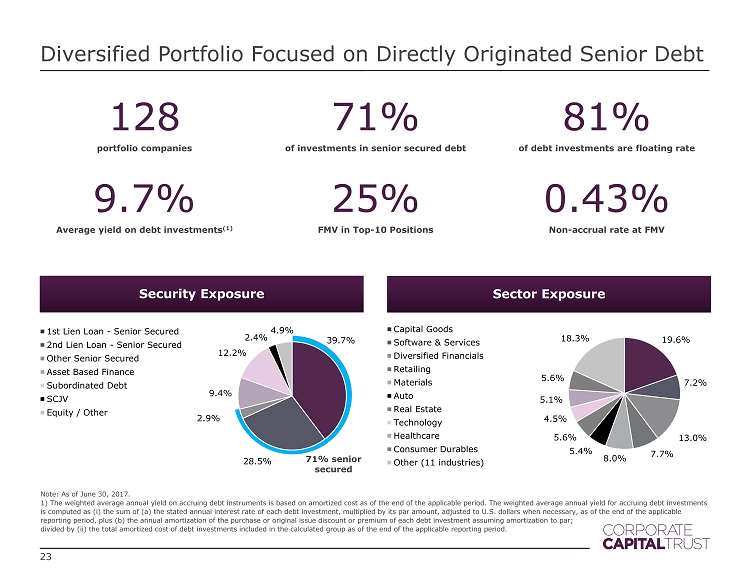

39.7% 28.5% 2.9% 9.4% 12.2% 2.4% 4.9% 1st Lien Loan - Senior Secured 2nd Lien Loan - Senior Secured Other Senior Secured Asset Based Finance Subordinated Debt SCJV Equity / Other Diversified Portfolio Focused on Directly Originated Senior Debt Note: As of June 30, 2017. 1) The weighted average annual yield on accruing debt instruments is based on amortized cost as of the end of the applicable per iod. The weighted average annual yield for accruing debt investments is computed as (i) the sum of (a) the stated annual interest rate of each debt investment, multiplied by its par amount, adju ste d to U.S. dollars when necessary, as of the end of the applicable reporting period, plus (b) the annual amortization of the purchase or original issue discount or premium of each debt investm ent assuming amortization to par; divided by (ii) the total amortized cost of debt investments included in the calculated group as of the end of the applicable re porting period. 19.6% 7.2% 13.0% 7.7% 8.0% 5.4% 5.6% 4.5% 5.1% 5.6% 18.3% Capital Goods Software & Services Diversified Financials Retailing Materials Auto Real Estate Technology Healthcare Consumer Durables Other (11 industries) Security Exposure 128 portfolio companies 71% of investments in senior secured debt 81% of debt investments are floating rate 9.7% Average yield on debt investments (1) 25% FMV in Top - 10 Positions 0.43% Non - accrual rate at FMV 23 71% senior secured Sector Exposure

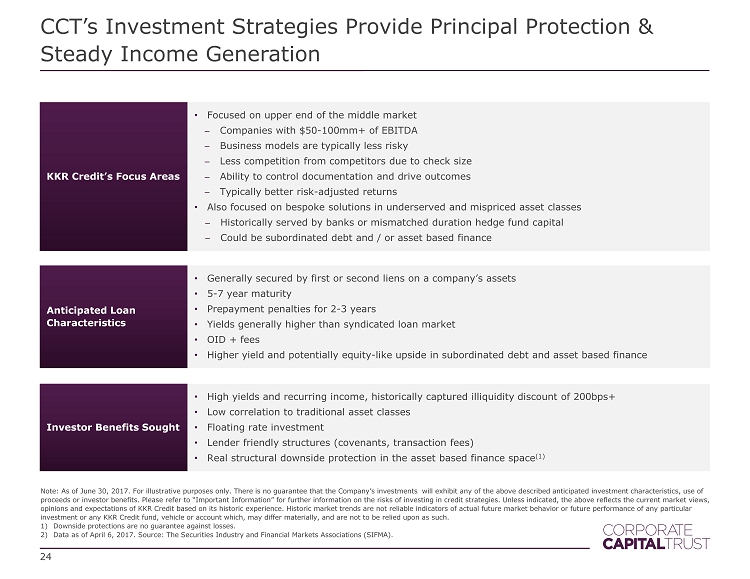

CCT’s Investment Strategies Provide Principal Protection & Steady Income Generation KKR Credit’s Focus Areas • Focused on upper end of the middle market ̶ Companies with $50 - 100mm+ of EBITDA ̶ Business model s are typically less risky ̶ Less competition from competitors due to check size ̶ Ability to control documentation and drive outcomes ̶ Typically better risk - adjusted returns • Also focused on bespoke solutions in underserved and mispriced asset classes ̶ Historically served by banks or mismatched duration hedge fund capital ̶ Could be subordinated debt and / or asset based finance 24 Note: As of June 30, 2017. For illustrative purposes only. There is no guarantee that the Company’s investments will exhibit an y of the above described anticipated investment characteristics, use of proceeds or investor benefits. Please refer to “Important Information” for further information on the risks of investing in c red it strategies. Unless indicated, the above reflects the current market views, opinions and expectations of KKR Credit based on its historic experience. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment or any KKR Credit fund, vehicle or account which, may differ materially, and are not to be relied upon as such. 1) Downside protections are no guarantee against losses. 2) Data as of April 6, 2017. Source: The Securities Industry and Financial Markets Associations ( SIFMA ). Anticipated Loan Characteristics • Generally secured by first or second liens on a company’s assets • 5 - 7 year maturity • Prepayment penalties for 2 - 3 years • Yields generally higher than syndicated loan market • OID + fees • Higher yield and potentially equity - like upside in subordinated debt and asset based finance Investor Benefits Sought • High yields and recurring income, historically captured illiquidity discount of 200bps+ • Low correlation to traditional asset classes • Floating rate investment • Lender friendly structures (covenants, transaction fees ) • Real structural downside protection in the asset based finance space (1)

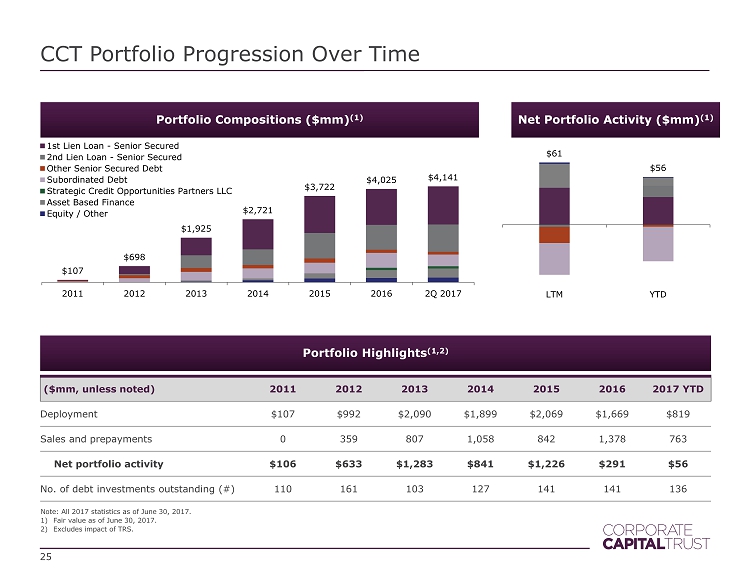

CCT Portfolio Progression Over Time Note: All 2017 statistics as of June 30, 2017. 1) Fair value as of June 30, 2017. 2) Excludes impact of TRS. Portfolio Highlights (1,2) ($mm, unless noted) 2011 2012 2013 2014 2015 2016 2017 YTD Deployment $107 $992 $2,090 $1,899 $2,069 $1,669 $819 Sales and prepayments 0 359 807 1,058 842 1,378 763 Net portfolio activity $106 $633 $1,283 $841 $1,226 $291 $56 No. of debt investments outstanding (#) 110 161 103 127 141 141 136 Portfolio Compositions ($mm) (1) 25 $107 $698 $1,925 $2,721 $3,722 $4,025 $4,141 2011 2012 2013 2014 2015 2016 2Q 2017 1st Lien Loan - Senior Secured 2nd Lien Loan - Senior Secured Other Senior Secured Debt Subordinated Debt Strategic Credit Opportunities Partners LLC Asset Based Finance Equity / Other $61 $56 LTM YTD Net Portfolio Activity ($mm) (1)

62.8% 3.1% 6.7% 27.4% 1st Lien Loan 2nd Lien Loan Senior Secured Bonds Subordinated Debt CCT’s JV Offers Key Investor Benefits CCT launched a joint venture with Conway Capital (1) in Q3 2016 As of Q2 2017, $98.1mm was invested by CCT; total equity was $112.1mm • Seeks to invest capital in middle - market loans, broadly syndicated loans, equity, and warrants • Key Portfolio Benefits – Attractive risk - adjusted returns on equity. Mid - teens ROE target – Increased asset diversification – Ability to commit to larger deal sizes – Access to partner’s pipeline and due diligence capability Key Terms of the Partnership: • CCT and Conway share voting 50% / 50% • Equity ownership 87.5% / 12.5% • CCT provides day - to - day administrative oversight 19.2% 11.0% 9.2% 11.1% 10.2% 6.3% 11.4% 6.0% 5.4% 10.3% Software & Services Retailing Consumer Services Healthcare Commercial Services Technology Capital Goods Transportation Materials Other 66.0% 34.0% Floating rate Fixed rate Fixed / Floating Sector Exposure Security Exposure 26 Note: As of June 30, 2017. 1) Conway Capital is an affiliate of Guggenheim Life and Annuity Company and Delaware Life Insurance Company.

$1,601 $1,791 $ 1,480 $1,875 $472 $579 $ 475 $425 $2,073 $2,370 $1,955 $2,300 2015 2016 Q2 2017 Target Total funded debt ($mm) Capacity Cash (mm) $54.0 $127.0 $44.0 $20.0 GAAP debt/equity 0.55x 0.59x 0.54x 0.75x CCT Funding Overview Note: As of June 30, 2017. 1) Peer group includes AINV, PSEC, SLRC, PNNT, MCC, FSIC, FSC, NMFC, ARCC, TSLX, TCPC, GSBD, and GBDC. 2) Includes impact of TRS. As of June 30, 2017. 3) Comprised of outstanding principal less unaccreted original discount and deferred financing costs. 4) CCT issued $ 140mm of unsecured notes in Q2 2017 and an additional $105m of unsecured notes in Q3 2017. Leverage over Time (2) 27 CCT has $ 475m of dry powder through diversified, long - dated debt facilities that are ~80bps cheaper than peers (1) $0 $0 $384 $330 $629 $137 2017 2018 2019 2020 2021 2022 Maturity Profile ($mm) Key Funding Vehicles ($mm) Counterparty Committed Drawn (3) Maturity Weighted Avg Rate Senior secured RCF $928 $629 2021 3.41% Term Loan 387 384 2019 4.50% J.P. Morgan facility 300 240 2020 4.39% SMBC facility 200 90 2020 3.10% Unsecured Bond 140 (4) 137 2022 5.00% Total $1,955 $1,480 3.98% Maturity Profile ($mm)

Listing Details 28

CCT Listing Details Company Name Corporate Capital Trust, Inc. Exchange / Ticker NYSE:CCT Anticipated Timing Q4 2017 29 As of June 30, 2017. Fee Structure On Listing 1.5% management fee on assets 20% incentive fee on income; subject to a 7% hurdle and 4 quarter look - back 20% incentive fee on capital gains; net of all unrealized and realized losses Net Asset Value Per Share (1) $8.92 Shares Outstanding (1) 308,243,000 – all shares will be listed Distribution Rate Current annualized distribution rate of $0.715 per share; ~8% yield on 6/30 NAV Two special dividends of $0.045 per share expected to be distributed post - listing Subject to approval by the Board of Directors Post - listing Tender Tender expected at listing; terms and size to be announced Post - tender Share Purchases KKR - sponsored 10b5 - 1 Plan expected post - tender; terms and size to be announced

Management Fee • CCT’s management fee will drop from 2.0% to 1.5% What Changes Are Being Made At Listing? 30 Investment Advisor • CNL has served as CCT’s investment advisor and KKR Credit as sub - advisor • Post - listing, KKR Credit will be sole investment advisor Board of Directors & Special Advisory Committee • Special Advisory Committee to the Board will be formed ̶ Daniel Pietrzak, CIO of CCT, and Chirag Bhavsar, CFO of CNL, serving as representatives of KKR Credit and CNL, respectively • Tom Sittema , CEO of CNL, will step down from the Board of Directors Charter Amendments to Organizational Documents • CCT will make changes to its charter and bylaws to bring it in line with listed peers

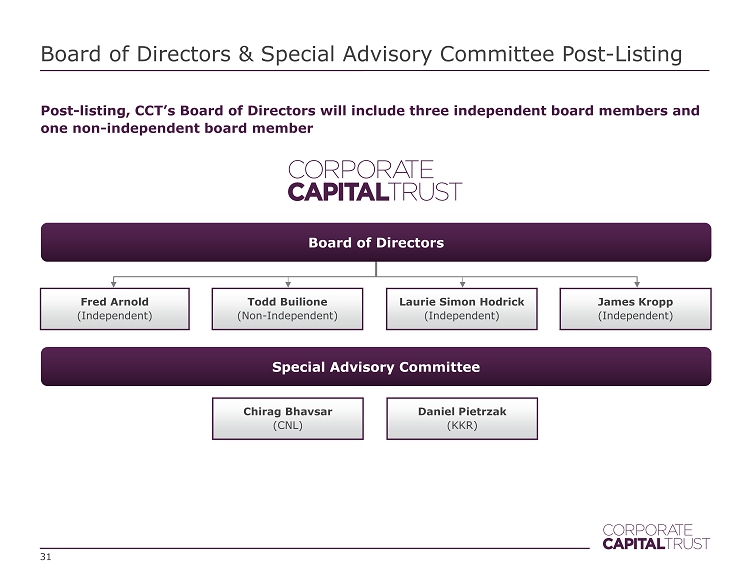

Board of Directors & Special Advisory Committee Post - Listing 31 Fred Arnold (Independent) Todd Builione (Non - Independent) Laurie Simon Hodrick (Independent) James Kropp (Independent) Board of Directors Special Advisory Committee Post - listing, CCT’s Board of Directors will include three independent board members and one non - independent board member Chirag Bhavsar ( CNL ) Daniel Pietrzak ( KKR )

Appendix – Historical Financials 32

Historical Quarterly Operating Results Detail ($mm, except per share) 1Q 2016 2Q 2016 3Q 2016 4Q 2016 1Q 2017 2Q 2017 Investment income Interest from investments $77.6 $85.2 $85.2 $89.9 $83.7 $79.0 Payment - in - kind interest income 8.4 5.8 2.2 3.1 3.5 4.0 Fee income 0.7 2.6 5.0 5.4 2.6 5.6 Dividend and other income 2.2 4.8 5.1 3.4 3.0 11.8 Total investment income $88.9 $98.4 $97.4 $101.8 $92.8 $100.5 Operating expenses Investment advisory fees $19.7 $20.0 $21.4 $21.6 $20.8 $20.9 Interest expense 11.5 12.0 13.5 14.6 14.1 15.2 Performance - based incentive fees 2.7 10.8 5.8 4.9 0.9 4.7 Offering expenses 0.8 0.7 0.4 0.4 0.2 0.1 G&A / other 2.9 2.8 3.2 3.5 4.1 6.4 Total operating expenses $37.5 $46.2 $44.2 $45.1 $40.2 $47.4 Net investment income before taxes $51.3 $52.2 $53.7 $56.7 $52.7 $53.1 Income taxes, including excise taxes – – (0.0) (3.3) – (0.2) Net investment income $51.3 $52.2 $53.2 $53.4 $52.5 $52.9 NII / share $0.17 $0.17 $0.17 $0.18 $0.17 $0.17 Annualized NII return on NAV 7.9% 7.9% 7.8% 7.7% 7.6% 7.6% Distributions declared / share $0.20 $0.20 $0.20 $0.20 $0.20 $0.20 Net asset value / share $8.62 $8.81 $8.97 $8.93 $9.00 $8.92 Weighted average shares outstanding 298.1 304.8 306.9 304.5 309.3 308.4 33

Historical Quarterly Balance Sheet ($mm, except per share) 1Q 2016 2Q 2016 3Q 2016 4Q 2016 1Q 2017 2Q 2017 Assets Total investments, at fair value $3,637.1 $4,013.2 $4,062.7 $4,025.3 $3,935.0 $4,141.1 Cash (1) 99.1 133.7 43.9 146.6 52.7 130.5 Collateral on deposit with custodian 120.0 110.0 95.0 95.0 105.0 – Dividends and interest receivable 48.9 49.0 55.8 53.5 48.7 46.4 Receivable for investments sold 8.3 76.0 24.4 49.3 7.4 25.6 Principal receivable 6.6 3.1 5.6 2.9 5.0 10.0 Unrealized appreciation on derivatives 3.9 13.4 19.8 42.5 40.4 9.1 Prepaid and other expense (2) 8.1 41.6 13.6 15.5 12.4 25.0 Total assets $3,932.0 $4,440.0 $4,320.8 $4,430.7 $4,206.7 $4,387.6 Liabilities Revolving credit facilities $865.0 $1,243.8 $1,046.1 $1,219.0 $998.5 $959.0 Term loan payable, net 387.1 386.4 385.8 385.2 384.6 384.0 Unsecured notes payable, net – – – – – 137.2 Repurchase agreement payable – 24.7 25.0 23.5 23.8 – Payable for investments purchased 18.1 43.5 77.8 22.2 2.4 120.2 Unrealized depreciation on derivatives 34.2 20.7 11.6 0.3 2.4 18.7 Accrued fees (3) 9.3 17.6 12.7 12.2 8.0 11.6 Deferred tax liability – – – 2.0 2.4 – Other accrued expenses and liabilities 3.8 3.8 3.6 7.0 5.3 7.0 Total liabilities $1,317.4 $1,740.6 $1,562.7 $1,671.4 $1,427.4 $1,637.7 Net assets $2,614.5 $2,699.5 $2,758.1 $2,759.3 $2,779.2 $2,749.9 Net asset value per share $8.62 $8.81 $8.97 $8.93 $9.00 $8.92 Debt/equity 0.5x 0.6x 0.5x 0.6x 0.5x 0.5x 1) Includes Cash, Cash denominated in foreign currency, and Restricted cash. 2) Includes Receivables from advisors, Deferred offering expenses, Prepaid and other deferred expenses, and Repurchase agreement re ceivables (2Q 2016 only ). 3) Includes Accrued performance - based incentive fees, Accrued investment advisory fees, and Accrued directors’ fees. 34

Appendix – Case Studies The companies shown on pages 39 - 41 represent a cross - sample of executed transactions in the last 18 months, and CCT would seek t o participate in similar transactions going forward. The transactions identified are not representative of all of the securities purchased or sold by CCT, and it should not be assume d t hat the investment in the companies identified was or will be profitable. Please refer to “Important Information” for further information on KKR’s inside information barrier policies and procedures, whi ch may limit the involvement of personnel in certain investment processes and discussions. Past performance is no guarantee of future results. 35

The KKR Advantage in Practice: CCT Case Studies Case Study 1: AM General Investment Date December 2016 Purpose Refinancing Security First Lien Term Loan Industry Autos Leverage 1.9x Interest Rate L+725bps LIBOR Floor 1.00% OID 98.5 Structuring Fee 1.50% Call Protection NC - 1, 103, 102, 101 Additional Terms • 10% per annum hard amortization • 50% excess cash flow sweep (with step - downs) • Maximum total first lien leverage ratio; maximum total leverage ratio Company Overview • American heavy vehicle manufacturer • Producer / primary servicer of U.S. military Humvees • N.A.’s only independent contract manufacturer of automobiles, SUVs and trucks • Sponsor has owned the Company for 12 years; demonstrates commitment to the business /conviction in the long - term investment opportunity through cycles Investment Thesis • Diverse mix of businesses: military and commercial vehicle production, service parts, logistics services, and engine and transmission production • Significant revenue and earnings visibility; >60% of 2017E revenue in backlog from existing orders • Large installed base provides further visibility through parts orders / replacement cycle • Low leverage and contractual deleveraging via amortization • In process of signing $2+ billion Sole Source contract for international orders; AMG is only logical provider KKR Advantage • Reviewed investment opportunity with General Petraeus who was able to advise on the importance of the platform and key considerations for diligence • Held calls with third - party experts (both military and commercial) to assess industry dynamics • KKR Credit had underwritten investment and was able to move quickly when bank syndicated deal failed; KCM was able to distribute the second lien below KKR’s investment Case Study 2: New Enterprise Stone & Lime Investment Date July 2016 Purpose Refinancing Security First Lien Term Loan Industry Industrials Leverage 4.6x Interest Rate L + 800bps LIBOR Floor 1.00% OID 99 Structuring Fee 1.50% Call Protection 104.5, 102.25, 100 at T+50 to 104.5 Additional Terms • Minimum EBITDA and Capital Expenditures covenants Company Overview • Family - owned, vertically integrated aggregates supplier and heavy highway construction contractor in PA. Business segments include: − Construction materials (aggregates, hot mix asphalt, ready mix concrete) − Heavy / highway construction − Traffic safety services • Significant hard assets; 42 quarries, 30 asphalt plants, 17 concrete plants and 2bn tons of aggregate reserves Investment Thesis • Key end markets driven by the non - residential construction cycle; KKR’s outlook is favorable, and Company should benefit from increased spending • Pennsylvania transportation bill expected to increase spending by the commonwealth by $2 - 3bn/year; Company well - positioned as bridges, roads and highways are a key focus • Meaningful asset coverage in a downside scenario given strategic location of quarries and scarcity of those assets KKR Advantage • Company initially introduced to KKR Credit by KKR PE team • KKR Credit has invested in the Company since 2011 • KKR Credit granted exclusive look at transaction given goodwill with management, familiarity with company, and ability to act in size • Significant diligence of regulatory environment including the Highway Bill at the federal level and the PA Transportation Bill at the state level 36

The KKR Advantage in Practice: CCT Case Studies Case Study 4: NBG Home Investment Date April 2017 Purpose Acquisition Financing Security First Lien Term Loan, Second Lien Term Loan, Equity Co - Invest Industry Home Furnishings Leverage First Lien: 3.4x; Second Lien: 4.3x Interest Rate First Lien: L+550bps; Second Lien: L+975bps LIBOR Floor 1.00% OID First Lien: 98; Second Lien: 98.5 Structuring Fee Second Lien: 1.50% Call Protection First Lien: 101; Second Lien: 103/102/101 Additional Terms • Covenant - lite first lien Company Overview • Designer, manufacturer and distributor of affordable home décor products • Sells through mass market (Target, Walmart), specialty ( HomeGoods , Michael’s), home improvement (Home Depot, Lowe’s) and online (Amazon) distributors Investment Thesis • Diversified customer base; no customer >10% of sales • End markets have been recession resistant • Market driven more by remodel / repairs than new homes due to the low price points and frequent replacement cycles • Affordable home décor is a large / attractive market; $16bn in size • Sponsor specializes in retail investments; extensive experience in retail distribution and sourcing KKR Advantage • Early call from Sycamore to provide complete financing solution • KKR Credit proposed a differentiated solution: covenant - lite first and second lien term loan • KCM acted as Joint Lead Arranger and Joint Bookrunner on the $260mm syndicated first lien term loan while KKR Credit provided the entire second lien term loan Case Study 3: Three Sixty Group Investment Date March 2017 Purpose Acquisition Financing Security First Lien Term Loan Industry Consumer Discretionary Leverage 4.3x Interest Rate L + 700bps LIBOR Floor 1.00% OID 1.50% Structuring Fee 1.00% Call Protection 102, 101 Additional Terms • 2.5% mandatory amortization • 50% excess cash flow sweep (with step - downs) • Total net leverage ratio, limitations on acquisitions and incremental debt Company Overview • Designer, sourcer and seller of high - velocity consumer products to 70,000+ U.S. retail stores • Products sourced and sold to customers at price advantage, often 30 - 50% below competitors • Low price position and unique merchandise program selling approach across categories result in improved sell - through and profitability for retail customers Investment Thesis • Company’s merchandising programs let retailers improve profitability in hard - to - manage product categories without in - house sourcing costs • Long - term customer relationships; serves some of the largest retailers in the US • Consistent track record of expansion and brand portfolio • Sponsor is making an equity investment and has experience managing consumer companies KKR Advantage • KKR Credit evaluated financing for Sponsor’s initial acquisition in October 2015, thus was familiar with the Company and its product offerings • KKR has long running relationship with the Sponsor and was invited in Q1 2017 to provide acquisition financing which led to an opportunity to replace the incumbent lender • KKR leveraged its broad experience in the retail and consumer sector to conduct channel checks and validate the Company’s value proposition and brand perception 37

The KKR Advantage in Practice: CCT Case Studies Case Study 6: Toorak Capital Partners Investment Date August 2016 Purpose Purchase residential real estate bridge loans Security Asset - backed finance Industry US Residential Real Estate LTV 50 - 75% against underlying real estate Company Overview • KKR Credit and Toorak Capital Partners LLC established a differentiated loan aggregation platform in Q3 2016 • Focused on residential bridge loans – loans made to professional residential rehab specialists • Short dated loans (7 month avg life) with attractive coupons (8% – 12%), and an average size of ~$200k • 12+ distinct originators partners across the country Investment Thesis • Strong downside protection; purchasing first lien mortgages capped at a maximum of 75% loan to value • Majority of the originators agreed to hold a first loss risk retention exposure in the loan pools • First loss piece substantially enhances KKR Credit’s downside protection beyond the low LTV on the loans • Opportunity is scalable; current size of residential bridge lending market is $15.0bn+ and we have indications for $800mm+ of actionable origination volume • Outsourcing the ongoing loan due diligence, document custodian and loan servicing functions to best - in - class third party providers helps execution and mitigates operational risks • Toorak is largest capital provider to the residential bridge lending industry • 16 - 18% expected return on a short duration asset KKR Advantage • Longstanding relationship with management team • Formed a detailed and constructive global macro view on US housing market • Structured partnership to ensure alignment of interest • Diligenced originators on - boarded at launch; continue to conduct due diligence on each originator in tandem with Clayton Holdings, a professional loan due diligence company • KKR’s internal knowledge of mortgage finance informed its views around investing in the transaction • KKR Credit has two of three board seats and controls all decisions around originator eligibility criteria Case Study 5: PQ Corporation & Eco Services Investment Date May 2016 Purpose Acquisition Financing Security Senior Unsecured Notes Industry Specialty Chemicals Leverage 5.8x Interest Rate L + 1075bps LIBOR Floor 1.00% OID 98 Structuring Fee 0.00% Call Protection NC - 2, 104, 102 Additional Terms • Covenant - lite first lien Company Overview • PQ Corp is a global producer of specialty inorganic performance chemicals and catalysts • Operates in three distinct segments: performance chemicals, catalysts, and specialty glass materials • Eco Services is a leading sulfuric acid manufacturer in the US; #1 market share in sulfuric acid regeneration and the virgin acid merchant market • In August 2015, the Companies announced that they were form a leading global producer of inorganic specialty materials and catalysts Investment Thesis • Adds a complimentary business line to existing product offerings and provides stability through cycles via differentiation and margin stability • Large percentage of sales contracts have automatic pass - through features for raw materials and input costs • Exposure to defensive industries (personal care, cleaning products, tires, gasoline) creates greater volume stability in market downturns • No single end market makes of a significant percentage of sales – largest end market is <18% of overall sales KKR Advantage • Diligence advantage, as KKR Credit had an existing position in the credit • Ability to move quickly to participate in the transaction before the rest of the capital structure launched in the syndicated markets • Capital available to fill market need due to leverage lending guidelines in the US 38

Additional Information and Where to Find It

In connection with the matters described in this communication, the Company has filed relevant materials with the Securities and Exchange Commission (the “SEC”), including a definitive proxy statement on Schedule 14A. The Company has mailed the definitive proxy statement and a proxy card to each stockholder entitled to vote at the stockholder meeting relating to such matters. STOCKHOLDERS OF THE COMPANY ARE URGED TO READ THESE MATERIALS (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO), AND ANY OTHER RELEVANT DOCUMENTS THAT THE COMPANY WILL FILE WITH THE SEC WHEN THEY BECOME AVAILABLE, BECAUSE THESE MATERIALS WILL CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY AND THE MATTERS DESCRIBED IN THIS COMMUNICATION. The definitive proxy statement and other relevant materials (when they become available), and any other documents filed by the Company with the SEC, may be obtained free of charge at the SEC’s website (http://www.sec.gov), at the Company’s website (http://www.corporatecapitaltrust.com/investor-resources), or by writing to the Company at 450 S. Orange Avenue, Orlando, Florida 32801 (telephone number 866-650-0650).

Participants in the Solicitation

The Company and its directors and officers may be deemed to be participants in the solicitation of proxies from the Company’s stockholders with respect to the matters described in this communication. Information about the Company’s directors and officers, as well as the identity of other potential participants, and their respective direct or indirect interests in such matters, by security holdings or otherwise, are set forth in the definitive proxy statement and other materials filed with SEC.

Forward Looking Statements

The information in this communication may include “forward-looking statements.” These statements are based on the beliefs and assumptions of the Company’s management and on the information currently available to management at the time of such statements. Forward-looking statements generally can be identified by the words “believes,” “expects,” “intends,” “plans,” “estimates” or similar expressions that indicate future events. Important factors that could cause actual results to differ materially from the Company’s expectations include those disclosed in the Company’s filings with the SEC, including the Company’s annual report on Form 10-K for the year ended December 31, 2016, which was filed with the SEC on March 20, 2017. The Company undertakes no obligation to update such statements to reflect subsequent events.

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Irish Residential Properties Sub-Fund 1: Form 8.3 - Irish Residential Properties REIT PLC

- Nykredit Realkredit A/S upgrades full-year guidance, and Nykredit Bank raises deposit rates

- Update on the acquisition of a block of 71.9% of Believe's share capital and launch of a simplified tender offer for 100% of Believe's share capital.

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!