Form 485BPOS SUNAMERICA EQUITY FUNDS

Tweet

Tweet Share

ShareAs filed with the Securities and Exchange Commission on January 29, 2018

Securities Act File No. 033-08021

Investment Company Act File No. 811-04801

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | ☒ | |||

| PRE-EFFECTIVE AMENDMENT NO. | ☐ | |||

| POST-EFFECTIVE AMENDMENT NO. 74 | ☒ | |||

| and/or | ||||

| REGISTRATION STATEMENT | ☒ | |||

| UNDER | ||||

| THE INVESTMENT COMPANY ACT OF 1940 | ||||

| AMENDMENT NO. 69 |

(Check appropriate box or boxes)

SUNAMERICA EQUITY FUNDS

(Exact Name of Registrant as Specified in Charter)

Harborside 5

185 Hudson Street

Suite 3300

Jersey City, NJ 07311

(Address of Principal Executive Office) (Zip Code)

Registrant’s telephone number, including area code: (800) 858-8850

Kathleen D. Fuentes, Esq.

SunAmerica Asset Management, LLC

Harborside 5

185 Hudson Street

Suite 3300

Jersey City, NJ 07311

(Name and Address for Agent for Service)

Copy to:

Margery K. Neale, Esq.

Willkie Farr & Gallagher LLP

787 Seventh Avenue

New York, NY 10019

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective.

It is proposed that this filing will become effective (check appropriate box)

| ☒ | immediately upon filing pursuant to paragraph (b) |

| ☐ | on (date) pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | on (date) pursuant to paragraph (a)(1) |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) |

| ☐ | on (date) pursuant to paragraph (a)(2) of Rule 485. |

If appropriate, check the following box:

| ☐ | This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

SunAmerica Equity Funds

Prospectus

2018

aig.com/funds

THIS IS A PRIVACY STATEMENT AND NOT PART OF THE PROSPECTUS.

Privacy Statement

SunAmerica Asset Management, LLC (“SunAmerica”) collects nonpublic personal information about you from the following sources:

• Information we receive from you on applications or other forms; and

• Information about your AIG funds transactions with us or others, including your financial adviser.

SunAmerica will not disclose any nonpublic personal information about you or your account(s) to anyone unless one of the following conditions is met:

• SunAmerica received your prior written consent;

• SunAmerica believes the recipient is your authorized representative;

• SunAmerica is permitted by law to disclose the information to the recipient in order to service your account(s); or

• SunAmerica is required by law to disclose information to the recipient.

If you decide to close your account(s) or become an inactive customer, SunAmerica will adhere to the privacy policies and practices as described in this notice.

SunAmerica restricts access to your personal and account information to those employees who need to know that information to provide products or services to you. We maintain physical, electronic, and procedural safeguards to guard your nonpublic personal information.

| January 29, 2018 |

PROSPECTUS | |

AIG International Dividend Strategy Fund

AIG Japan Fund

| Class |

AIG International Dividend Strategy Fund: Ticker Symbols |

AIG Japan Fund: Ticker Symbols | ||

| A Shares |

SIEAX | SAESX | ||

| C Shares |

SIETX | SAJCX | ||

| I Shares |

NAOIX | — | ||

| W Shares |

SIEWX | SAJWX |

This Prospectus contains information you should know before investing, including information about risks. Please read it before you invest and keep it for future reference.

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

| 2 | ||||

| 7 | ||||

| 12 | ||||

| 13 | ||||

| 25 | ||||

| 25 | ||||

| 26 | ||||

| 26 | ||||

| 27 | ||||

| 30 | ||||

| 34 | ||||

| Financial Intermediary-Specific Sales Charge Waiver Policies |

A-1 |

Fund Highlights: AIG International Dividend Strategy Fund

INVESTMENT GOAL

The investment goal of the AIG International Dividend Strategy Fund (the “International Dividend Strategy Fund” or the “Fund”) is total return (including capital appreciation and current income).

FEES AND EXPENSES OF THE FUND

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the AIG fund complex. More information about these and other discounts is available from your financial professional and in the “Shareholder Account Information-Sales Charge Reductions and Waivers” section on page 13 of the Fund’s Prospectus, in the “Financial Intermediary-Specific Sales Charge Waiver Policies” section on page A-1 of the Fund’s Prospectus and in the “Additional Information Regarding Purchase of Shares” section on page 55 of the Fund’s statement of additional information (“SAI”). Class I shares are closed to new purchases.

| Class A | Class C | Class I | Class W | |||||||||||||

| Shareholder Fees |

||||||||||||||||

| Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) |

5.75% | None | None | None | ||||||||||||

| Maximum Deferred Sales Charge (Load) (as a percentage of the lesser of the amount redeemed or original purchase cost)(1) |

None | 1.00% | None | None | ||||||||||||

| Maximum Sales Charge (Load) Imposed on Reinvested Dividends |

None | None | None | None | ||||||||||||

| Maximum Account Fee |

None | None | None | None | ||||||||||||

| Annual Fund Operating Expenses |

||||||||||||||||

| Management Fees |

1.00% | 1.00% | 1.00% | 1.00% | ||||||||||||

| Distribution and/or Service (12b-1) Fees |

0.35% | 1.00% | — | — | ||||||||||||

| Other Expenses |

0.53% | 0.63% | 1.49% | 0.87% | ||||||||||||

| Total Annual Fund Operating Expenses Before Fee Waivers and/or Expense Reimbursement/(Recoupment) |

1.88% | 2.63% | 2.49% | 1.87% | ||||||||||||

| Fee Waivers and/or Expense Reimbursement/(Recoupment)(2),(3) |

-0.02% | 0.08% | 0.69% | 0.17% | ||||||||||||

| Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursement/(Recoupment)(2),(3) |

1.90% | 2.55% | 1.80% | 1.70% | ||||||||||||

| (1) | Purchases of Class A shares of $1 million or more will be subject to a contingent deferred sales charge (“CDSC”) on redemptions made within two years of purchase. The CDSC on Class C shares applies only if shares are redeemed within twelve months of their purchase. See pages 13-15 of the Prospectus for more information about the CDSCs. |

| (2) | Pursuant to an Expense Limitation Agreement, SunAmerica Asset Management, LLC (“SunAmerica” or the “Adviser”) is contractually obligated to waive its fees and/or reimburse expenses to the extent that the Total Annual Fund Operating Expenses exceed 1.90%, 2.55%, 1.80% and 1.70% for Class A, Class C, Class I and Class W shares, respectively. For purposes of the Expense Limitation Agreement, “Total Annual Fund Operating Expenses” shall not include extraordinary expenses (i.e., expenses that are unusual in nature and/or infrequent in occurrence, such as litigation), or acquired fund fees and expenses, brokerage commissions and other transactional expenses relating to the purchase and sale of portfolio securities, interest, taxes and governmental fees, and other expenses not incurred in the ordinary course of the Fund’s business. This agreement will continue in effect indefinitely, unless terminated by the Board of Trustees, including a majority of the trustees of the Board who are not “interested persons” of SunAmerica Equity Funds as defined in the Investment Company Act of 1940, as amended. |

| (3) | Any waivers and/or reimbursements made by SunAmerica pursuant to the Expense Limitation Agreement are subject to recoupment from the Fund within two years after the occurrence of the waiver and/or reimbursement, provided that the Fund is able to effect such payment to SunAmerica and remain in compliance with the expense cap in effect at the time the waivers and/or reimbursements occurred. |

| 2 |

EXAMPLE:

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions and the net expenses shown in the fee table, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

| AIG International Dividend Strategy Fund | ||||||||||||||||

| Class A Shares |

$ | 757 | $ | 1,138 | $ | 1,542 | $ | 2,669 | ||||||||

| Class C Shares |

358 | 794 | 1,355 | 2,885 | ||||||||||||

| Class I Shares |

183 | 566 | 975 | 2,116 | ||||||||||||

| Class W Shares |

173 | 536 | 923 | 2,009 | ||||||||||||

| You would pay the following expenses if you did not redeem your shares: |

||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

| AIG International Dividend Strategy Fund | ||||||||||||||||

| Class A Shares |

$ | 757 | $ | 1,138 | $ | 1,542 | $ | 2,669 | ||||||||

| Class C Shares |

258 | 794 | 1,355 | 2,885 | ||||||||||||

| Class I Shares |

183 | 566 | 975 | 2,116 | ||||||||||||

| Class W Shares |

173 | 536 | 923 | 2,009 | ||||||||||||

PORTFOLIO TURNOVER:

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 22% of the average value of its portfolio.

PRINCIPAL INVESTMENT STRATEGIES AND TECHNIQUES OF THE FUND

The Fund’s principal investment strategies are value and international investing. The value oriented philosophy to which the Fund partly subscribes is that of investing in securities believed to be undervalued in the market. The selection criteria are usually calculated to identify stocks of companies with solid financial strength that have attractive valuations (e.g., as measured by low price earnings ratios) and that may have been generally overlooked by the market. The strategy of international investing involves investing substantially all of the Fund’s assets in foreign (non-U.S.) securities (“foreign securities”).

The principal investment technique of the Fund is to employ a “buy and hold” strategy with approximately 50 to 100 high dividend yielding equity securities selected annually from the Morgan Stanley Capital International All Country World Index ex-U.S. Index (“MSCI ACWI ex-U.S. Index”). At least 80% of the Fund’s net assets, plus any borrowings for investment purposes, will be invested in dividend yielding equity securities.

The Fund expects to invest primarily in common stocks, and to a lesser extent, preferred stocks, and may invest in companies of any size. In addition, the Fund is not limited in the amount it may invest in any one country, and its investments may include securities of emerging markets.

The selection criteria used by the Fund’s portfolio managers to identify high dividend yielding equity securities from the MSCI ACWI ex-U.S. Index will generally include dividend yield as well as a combination of factors that relate to profitability and valuation. Certain stocks in the MSCI ACWI ex-U.S. Index may be excluded as a result of liquidity screens applied during the selection process. The number of securities selected each year for inclusion in the Fund’s portfolio will be determined at the discretion of the portfolio managers and will depend on, among other things, the impact that the number of securities held is expected to have on the potential for overall dividend yield in the portfolio, as well as market conditions. While the securities selection process will take place on an annual basis, the portfolio managers may, from time to time, substitute certain securities for those selected for the Fund or reduce the position size of a portfolio security in between the annual rebalancings under certain limited circumstances. These circumstances will generally include where a security held by the Fund no longer meets the dividend yield criteria, when the value of a security becomes a disproportionately large percentage of the Fund’s holdings, or when the size of the Fund’s position in the security has the potential to create market liquidity or other issues in connection with the annual rebalancing or efficient management of the Fund, each at the discretion of the portfolio managers.

| 3 |

Fund Highlights: AIG International Dividend Strategy Fund

The Fund will be evaluated and adjusted at the discretion of the portfolio managers on an annual basis. The next annual consideration of the securities that meet the selection criteria will take place on or about October 1, 2018. Immediately after the Fund buys and sells securities in connection with the Fund’s annual rebalancing, it will hold approximately an equal value of each of the 50 to 100 securities. For example, the Fund would invest about 1/50th of its assets in each of the securities that make up its portfolio if the Fund were to select 50 securities. Thereafter, when an investor purchases shares of the Fund, the Adviser will generally invest additional funds in the pre-selected securities based on each security’s respective percentage of the Fund’s assets at the time.

The Fund employs a strategy to hold securities between its annual rebalancing, even if there are adverse developments concerning a particular security, an industry, the economy or the stock market generally. Due to changes in the market value of the securities held by the Fund, it is likely that the weighting of the stocks in its portfolio will fluctuate throughout the course of the year.

The principal investment strategies and principal investment techniques of the Fund may be changed without shareholder approval. You will receive at least 60 days’ notice of any change to the 80% investment policy set forth above.

PRINCIPAL RISKS OF INVESTING IN THE FUND

There can be no assurance that the Fund’s investment goal will be met or that the net return on an investment in the Fund will exceed what could have been obtained through other investment or savings vehicles. Shares of the Fund are not bank deposits and are not guaranteed or insured by any bank, government entity or the Federal Deposit Insurance Corporation. As with any mutual fund, there is no guarantee that the Fund will be able to achieve its investment goals. If the value of the assets of the Fund goes down, you could lose money.

The following is a summary description of the principal risks of investing in the Fund.

Market Volatility and Securities Selection. The Fund invests significantly in equity securities. As with any equity fund, the value of your investment in the Fund may fluctuate in response to stock market movements. In addition, the performance of the Fund may be subject to greater fluctuation when a smaller number of securities are held by the Fund and thus, the Fund’s risk may increase when it holds closer to 50 securities rather than closer to 100 securities. You should be aware that the performance of “value” stocks and “growth” stocks may rise or decline under varying market conditions — for example, “value” stocks may perform well under circumstances in which “growth” stocks in general have fallen. When investing in value stocks which are believed to be undervalued in the market, there is a risk that the market may not recognize a security’s intrinsic value for a long period of time, or that a security judged to be undervalued may actually be appropriately priced. In addition, individual securities selected for the Fund may underperform the market generally.

International Investing. When investing internationally, the value of your investment may be affected by fluctuating currency values, changing local and regional economic, political and social conditions, and greater market volatility. In addition, foreign securities may not be as liquid as domestic securities and are subject to settlement practices and regulatory and financial reporting standards that differ from those in the U.S. Also, while the Fund seeks to invest in a wide range of countries, volatility in a single country or region in which the Fund invests a significant portion of its assets may affect performance. In addition, the markets of emerging market countries are typically more volatile and potentially less liquid than more developed markets. Emerging market countries may have relatively unstable governments and may present the risk of nationalization of businesses, expropriation, confiscatory taxation or, in certain instances, reversion to closed market, centrally planned economies.

Small- and Mid-Market Capitalization. Stocks of small-cap companies, and to a lesser extent, mid-cap companies, may be more volatile than, and not as readily marketable as, those of larger companies.

Disciplined Strategy. The Fund will not deviate from its strategy (except to the extent necessary to comply with federal tax laws or other applicable laws). If the Fund is committed to a strategy that is unsuccessful, the Fund will not meet its investment goal. Because the Fund generally will not use certain hedging techniques available to other mutual funds to reduce stock market exposure, the Fund may be more susceptible to general market declines than other mutual funds.

Preferred Stock. The value of preferred stock will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of preferred stock. Preferred stock is also subject to credit risk, which is the possibility that an issuer of preferred stock will fail to make its dividend payments. Preferred stock is inherently more risky than the bonds and other debt instruments of the issuer, but typically less risky than its common stock. Preferred stock may be significantly less liquid than many other securities, such as U.S. Government securities, corporate debt and common stock.

| 4 |

PERFORMANCE INFORMATION*

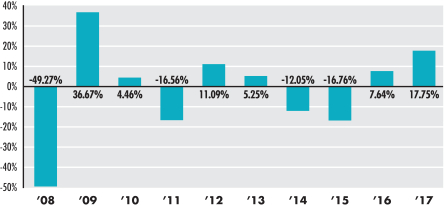

The following Risk/Return Bar Chart and Table illustrate the risks of investing in the Fund by showing changes in the Fund’s performance from calendar year to calendar year, and compare the Fund’s average annual returns to those of the MSCI ACWI ex-U.S. Index (Net), a broad measure of market performance. Sales charges are not reflected in the Bar Chart. If these amounts were reflected, returns would be less than those shown. However, the Table includes all applicable fees and sales charges. Past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Updated information on the Fund’s performance can be obtained by visiting www.aig.com/funds or can be obtained by phone at 800-858-8850, ext. 6003.

INTERNATIONAL DIVIDEND STRATEGY FUND (Class A)

|

During the period shown in the Bar Chart, the highest return for a quarter was 26.57% (quarter ended June 30, 2009) and the lowest return for a quarter was -26.18% (quarter ended December 31, 2008). |

| Average Annual Total Returns (as of the periods ended December 31, 2017) |

Past One Year |

Past Five Years |

Past Ten Years |

Class W Shares (Since Inception |

||||||||||||

| Class W | 17.97% | N/A | N/A | 2.16% | ||||||||||||

| Class I | 17.74% | -0.35% | -4.03% | N/A | ||||||||||||

| Class C | 15.97% | -1.13% | -4.76% | N/A | ||||||||||||

| Class A | 11.00% | -1.65% | -4.70% | N/A | ||||||||||||

| Return After Taxes on Distributions (Class A) | 10.47% | -2.07% | -4.96% | N/A | ||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares (Class A)1 | 7.23% | -1.03% | -3.21% | N/A | ||||||||||||

| MSCI ACWI ex-U.S. Index (Net) | 27.19% | 6.80% | 1.84% | 7.58% | ||||||||||||

| * | Effective July 2, 2012, the name of the Fund was changed to the SunAmerica International Dividend Strategy Fund (n/k/a AIG International Dividend Strategy Fund) and certain corresponding changes were made to the Fund’s investment strategy and techniques. Prior to this date, the Fund was managed as an international equity fund and employed a different strategy. The performance shown prior to July 2, 2012, represents the performance of the Fund as an international equity fund. Accordingly, this performance information does not reflect the management of the Fund in accordance with its current investment strategy and techniques. |

| 1 | When the return after taxes on distributions and sale of Fund shares is higher, it is because of realized losses. If realized losses occur upon the sale of Fund shares, the capital loss is recorded as a tax benefit, which increases the return. |

The after-tax returns shown were calculated using the historical highest individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. An investor’s actual after-tax returns depend on the investor’s tax situation and may differ from those shown in the above table. The after-tax returns shown are not relevant to investors who hold their shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class A. After-tax returns for other classes will vary.

INVESTMENT ADVISER

The Fund’s investment adviser is SunAmerica.

| 5 |

Fund Highlights: AIG International Dividend Strategy Fund

PORTFOLIO MANAGERS

| Name |

Portfolio Manager of the Fund Since |

Title | ||

| Timothy Pettee |

2013 | Lead Portfolio Manager, Senior Vice President and Chief Investment Strategist at SunAmerica | ||

| Andrew Sheridan |

2013 | Co-Portfolio Manager and Senior Vice President at SunAmerica | ||

| Timothy Campion |

2012 | Co-Portfolio Manager and Senior Vice President at SunAmerica |

For important information about purchase and sale of Fund shares, tax information and financial intermediary compensation, please turn to “Important Additional Information” on page 12 of the Prospectus.

| 6 |

Fund Highlights: AIG Japan Fund

INVESTMENT GOAL

The investment goal of the AIG Japan Fund (the “Japan Fund” or the “Fund”) is long-term capital appreciation.

FEES AND EXPENSES OF THE FUND

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the AIG fund complex. More information about these and other discounts is available from your financial professional and in the “Shareholder Account Information-Sales Charge Reductions and Waivers” section on page 13 of the Fund’s Prospectus, in the “Financial Intermediary-Specific Sales Charge Waiver Policies” section on page A-1 of the Fund’s Prospectus and in the “Additional Information Regarding Purchase of Shares” section on page 55 of the Fund’s statement of additional information (“SAI”).

| Class A | Class C | Class W | ||||||||||

| Shareholder Fees |

||||||||||||

| Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price) |

5.75% | None | None | |||||||||

| Maximum Deferred Sales Charge (Load) (as a percentage of the lesser of the amount redeemed or original purchase cost)(1) |

None | 1.00% | None | |||||||||

| Maximum Sales Charge (Load) Imposed on Reinvested Dividends |

None | None | None | |||||||||

| Maximum Account Fee |

None | None | None | |||||||||

| Annual Fund Operating Expenses |

||||||||||||

| Management Fees |

1.15% | 1.15% | 1.15% | |||||||||

| Distribution and/or Service (12b-1) Fees |

0.35% | 1.00% | — | |||||||||

| Other Expenses |

0.95% | 1.15% | 18.54% | |||||||||

| Total Annual Fund Operating Expenses Before Fee Waivers and/or Expense Reimbursement |

2.45% | 3.30% | 19.69% | |||||||||

| Fee Waivers and/or Expense Reimbursement(2),(3) |

0.55% | 0.75% | 17.99% | |||||||||

| Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursement(2),(3) |

1.90% | 2.55% | 1.70% | |||||||||

| (1) | Purchases of Class A shares of $1 million or more will be subject to a contingent deferred sales charge (“CDSC”) on redemptions made within two years of purchase. The CDSC on Class C shares applies only if shares are redeemed within twelve months of their purchase. See pages 13-15 of the Prospectus for more information about the CDSCs. |

| (2) | Pursuant to an Expense Limitation Agreement, SunAmerica Asset Management, LLC (“SunAmerica” or the “Adviser”) is contractually obligated to waive its fees and/or reimburse expenses to the extent that the Total Annual Fund Operating Expenses exceed 1.90%, 2.55% and 1.70% for Class A, Class C and Class W shares, respectively. For purposes of the Expense Limitation Agreement, “Total Annual Fund Operating Expenses” shall not include extraordinary expenses (i.e., expenses that are unusual in nature and/or infrequent in occurrence, such as litigation), or acquired fund fees and expenses, brokerage commissions and other transactional expenses relating to the purchase and sale of portfolio securities, interest, taxes and governmental fees, and other expenses not incurred in the ordinary course of the Fund’s business. This agreement will continue in effect indefinitely, unless terminated by the Board of Trustees, including a majority of the trustees of the Board who are not “interested persons” of SunAmerica Equity Funds as defined in the Investment Company Act of 1940, as amended. |

| (3) | Any waivers and/or reimbursements made by SunAmerica pursuant to the Expense Limitation Agreement are subject to recoupment from the Fund within two years after the occurrence of the waiver and/or reimbursement, provided that the Fund is able to effect such payment to SunAmerica and remain in compliance with the expense cap in effect at the time the waivers and/or reimbursements occurred. |

| 7 |

Fund Highlights: AIG Japan Fund

EXAMPLE:

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions and the net expenses shown in the fee table, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

| AIG Japan Fund | ||||||||||||||||

| Class A Shares |

$ | 757 | $ | 1,138 | $ | 1,542 | $ | 2,669 | ||||||||

| Class C Shares |

358 | 794 | 1,355 | 2,885 | ||||||||||||

| Class W Shares |

173 | 536 | 923 | 2,009 | ||||||||||||

| You would pay the following expenses if you did not redeem your shares: |

| |||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

| AIG Japan Fund | ||||||||||||||||

| Class A Shares |

$ | 757 | $ | 1,138 | $ | 1,542 | $ | 2,669 | ||||||||

| Class C Shares |

258 | 794 | 1,355 | 2,885 | ||||||||||||

| Class W Shares |

173 | 536 | 923 | 2,009 | ||||||||||||

PORTFOLIO TURNOVER:

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 115% of the average value of its portfolio.

PRINCIPAL INVESTMENT STRATEGY AND TECHNIQUES OF THE FUND

The Fund’s principal investment strategy is country-specific investing. The strategy of country-specific investing involves investing in securities that focus on a particular country.

The principal investment technique of the Fund is active trading of securities of Japanese issuers and other investments that are tied economically to Japan (“Japanese companies”). Under normal circumstances, at least 80% of the Fund’s net assets, plus any borrowings for investment purposes, will be invested in Japanese companies. The Fund will invest primarily in common stocks and may invest in securities of companies of any size. The Fund may also invest in other equity securities, which include, without limitation, preferred stock, convertible securities, depositary receipts, rights and warrants.

In selecting investments for the Fund, the Fund’s subadviser, Wellington Management Company LLP (“Wellington Management”), will employ a contrarian investment process, which is based on valuation and behavioral finance principles applied to overlooked and misunderstood companies. In particular, the investment process incorporates traditional assessments of financial strength and management credibility with a disciplined approach to determining the current state of investor sentiment toward each industry and securities within the investment universe. The primary principle behind this process is that markets overreact to unexpected negative news, causing share prices to deeply undervalue near-term information.

The principal investment strategy and principal investment techniques of the Fund may be changed without shareholder approval. You will receive at least 60 days’ notice of any change to the 80% investment policy set forth above.

PRINCIPAL RISKS OF INVESTING IN THE FUND

There can be no assurance that the Fund’s investment goal will be met or that the net return on an investment in the Fund will exceed what could have been obtained through other investment or savings vehicles. Shares of the Fund are not bank deposits and are not guaranteed or insured by any bank, government entity or the Federal Deposit Insurance Corporation. As with any mutual fund, there is no guarantee that the Fund will be able to achieve its investment goal. If the value of the assets of the Fund goes down, you could lose money.

The following is a summary description of the principal risks of investing in the Fund.

Market Volatility and Securities Selection. The Fund invests significantly in equity securities. As with any equity fund, the value of your investment in the Fund may fluctuate in response to stock market movements. You should be aware that the performance of different types of equity securities may rise or decline under varying market conditions — for example, “value” stocks may perform well

| 8 |

under circumstances in which “growth” stocks in general have fallen. In addition, individual securities selected for the Fund may underperform the market generally. Moreover, while the Fund will seek to invest in securities that Wellington Management believes are misunderstood in the market or out-of-favor, there is a risk that the market may not recognize a security’s intrinsic value for a long period of time, or that a security judged to be attractively valued may actually be appropriately priced.

Geographic Concentration. Because the Fund concentrates its investments in Japan, the Fund’s performance is expected to be closely tied to social, political and economic conditions of that country. As a result, the Fund is likely to be more volatile than more geographically diverse international funds.

Japan Exposure. The Japanese economy faces a number of long-term problems, including massive government debt, the aging and shrinking of the population, an unstable financial sector and low domestic consumption. Japan has experienced natural disasters of varying degrees of severity, and the risks of such phenomena, and damage resulting therefrom, continue to exist. Japan has a growing economic relationship with China and other Southeast Asian countries, and thus Japan’s economy may also be affected by economic, political or social instability in those countries (whether resulting from local or global events).

International Investing. When investing internationally, the value of your investment may be affected by fluctuating currency values, changing local and regional economic, political and social conditions, and greater market volatility. In addition, foreign securities may not be as liquid as domestic securities and are subject to settlement practices and regulatory and financial reporting standards that differ from those in the U.S. In addition, the Fund’s performance may be affected by the broader Asian region, which includes emerging markets. Emerging markets are typically more volatile than more developed markets.

Small- and Mid-Market Capitalization. Stocks of small-cap companies, and to a lesser extent, mid-cap companies, may be more volatile than, and not as readily marketable as, those of larger companies.

Active Trading. As part of the Fund’s principal investment technique, the Fund may engage in active trading of its portfolio securities. Because the Fund may sell a security without regard to how long it has held the security, active trading may have tax consequences for certain shareholders, involving a possible increase in short-term capital gains or losses. Active trading may result in high portfolio turnover and correspondingly greater brokerage commissions and other transaction costs, which will be borne directly by the Fund and which will affect the Fund’s performance. During periods of increased market volatility, active trading may be more pronounced.

| 9 |

Fund Highlights: AIG Japan Fund

PERFORMANCE INFORMATION*

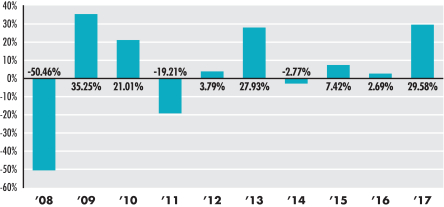

The following Risk/Return Bar Chart and Table illustrate the risks of investing in the Fund by showing changes in the Fund’s performance from calendar year to calendar year, and compare the Fund’s average annual returns to those of the Morgan Stanley Capital International (“MSCI”) Japan Index (Net), a broad measure of market performance. Sales charges are not reflected in the Bar Chart. If these amounts were reflected, returns would be less than those shown. However, the Table includes all applicable fees and sales charges. Past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Performance information with respect to the Fund’s Class W shares is not provided as these shares do not have a complete calendar year of performance. Updated information on the Fund’s performance can be obtained by visiting www.aig.com/funds or can be obtained by phone at 800-858-8850, ext. 6003.

JAPAN FUND (Class A)

|

During the period shown in the Bar Chart, the highest return for a quarter was 23.54% (quarter ended June 30, 2009) and the lowest return for a quarter was -27.29% (quarter ended September 30, 2008). |

| Average Annual Total Returns (as of the periods ended December 31, 2017) |

Past One Year |

Past Five Years |

Past Ten Years |

|||||||||

| Class C | 27.52% | 11.46% | 1.23% | |||||||||

| Class A | 22.06% | 10.86% | 1.31% | |||||||||

| Return After Taxes on Distributions (Class A) | 19.09% | 8.78% | -0.03% | |||||||||

| Return After Taxes on Distributions and Sale of Fund Shares (Class A)1 | 13.23% | 7.79% | 0.66% | |||||||||

| MSCI Japan Index (Net) | 23.99% | 11.16% | 3.17% | |||||||||

| * | Effective January 27, 2012, the name of the Fund was changed to the SunAmerica Japan Fund (n/k/a AIG Japan Fund) and certain corresponding changes were made to the Fund’s investment strategy and techniques. Prior to this date, the Fund was managed as an international small-cap fund. The performance shown prior to January 27, 2012 represents the performance of the Fund as an international small-cap fund. Accordingly, this performance information does not reflect the management of the Fund in accordance with its current investment strategy and techniques. |

| 1 | When the return after taxes on distributions and sale of Fund shares is higher, it is because of realized losses. If realized losses occur upon the sale of Fund shares, the capital loss is recorded as a tax benefit, which increases the return. |

The after-tax returns shown were calculated using the historical highest individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. An investor’s actual after-tax returns depend on the investor’s tax situation and may differ from those shown in the above table. The after-tax returns shown are not relevant to investors who hold their shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class A. After-tax returns for other classes will vary.

| 10 |

INVESTMENT ADVISER AND SUBADVISER

The Fund’s investment adviser is SunAmerica. The Fund is subadvised by Wellington Management.

PORTFOLIO MANAGER

| Name |

Portfolio Manager of the |

Title | ||

| Jun Y. Oh |

2012 | Senior Managing Director and Portfolio Manager affiliated with Wellington Management and located outside the U.S. |

For important information about purchase and sale of Fund shares, tax information and financial intermediary compensation, please turn to “Important Additional Information” on page 12 of the Prospectus.

| 11 |

Important Additional Information

PURCHASE AND SALE OF FUND SHARES

Each Fund’s initial investment minimums generally are as follows:

| CLASS A

AND CLASS C SHARES |

CLASS I SHARES | CLASS W SHARES | ||||

| Minimum Initial Investment | • non-retirement account: $500 • retirement account: $250 • dollar cost averaging: $500 to open; you must invest at least $25 a month. |

Closed to new purchases. | $50,000 | |||

| Minimum Subsequent Investment | • non-retirement account: $100 • retirement account: $25 |

N/A | N/A | |||

You may purchase or sell shares of each Fund each day the New York Stock Exchange is open. Purchase and redemption requests are executed at the Fund’s next net asset value to be calculated after the Fund or its agents receives your request in good order. You should contact your broker, financial adviser or financial institution, or, if you hold your shares through the Fund, you should contact the Fund by phone at 800-858-8850, by regular mail (AIG Funds c/o DST Asset Manager Solutions, Inc. (“DST”), PO Box 219186, Kansas City, MO 64121-9186), by express, certified and registered mail (AIG Funds c/o DST, 330 West 9th Street, Kansas City, MO 64105-1514), or via the Internet at www.aig.com/funds.

TAX INFORMATION

Each Fund’s dividends and distributions are subject to federal income taxes and will be taxed as ordinary income or capital gains, unless you are a tax-exempt investor or are investing through a retirement plan, in which case you may be subject to federal income tax upon withdrawal from such tax-deferred arrangements.

PAYMENTS TO BROKER/DEALERS AND OTHER FINANCIAL INTERMEDIARIES

If you purchase a Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend a Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

| 12 |

Shareholder Account Information

SELECTING A SHARE CLASS

Each Fund offers a number of classes of shares through this Prospectus, which may include: Class A, Class C, Class I and Class W shares.

Each class of shares has its own cost structure, so you can choose the one best suited to your investment needs. Your broker or financial adviser can help you determine which class is right for you.

| Class A | Class C | Class I | Class W | |||

| • Front-end sales charges, as described below. There are several ways to reduce these charges, also described on page 14. • Lower annual expenses than Class C shares. |

• No front-end sales charges, all your money goes to work for you right away. • Higher annual expenses than Class A shares. • Deferred sales charge on shares you sell within twelve months of purchase, as described on page 14. • Effective March 1, 2018, automatic conversion to Class A shares approximately ten years after purchase. |

• Closed to new purchases; however, existing investors may continue to purchase shares through reinvestments of dividends and capital gains distributions. • No sales charges. • Lower annual expenses than Class A or C shares. |

• Offered exclusively through advisory fee-based programs sponsored by certain financial intermediaries, such as brokerage firms, investment advisers, financial planners, third-party administrators, insurance companies, and any other institutions having a selling, administration or any similar agreement with the Fund, whose use of Class W shares will depend on the structure of the particular advisory fee-based program. • No sales charges. • Lower annual expenses than Class A or C shares. | |||

CALCULATION OF SALES CHARGES

Class A. Sales charges are as follows:

| Sales Charges | Concession to Dealers | |||||||||||

| Your Investment | % of Offering Price |

% of Net Amount Invested |

% of Offering Price |

|||||||||

| Less than $50,000 |

5.75% | 6.10% | 5.00% | |||||||||

| $50,000 but less than $100,000 |

4.75% | 4.99% | 4.00% | |||||||||

| $100,000 but less than $250,000 |

3.75% | 3.90% | 3.00% | |||||||||

| $250,000 but less than $500,000 |

3.00% | 3.09% | 2.50% | |||||||||

| $500,000 but less than $1,000,000 |

2.00% | 2.04% | 1.75% | |||||||||

| $1,000,000 or more* |

None | None | 1.00% | |||||||||

| * | Purchases of $1,000,000 or more are subject to a concession to dealers of up to 1.00%. |

Investments of $1 million or more: Class A shares are offered with no front-end sales charge with respect to investments of $1 million or more. However, a 1% CDSC is imposed on any shares you sell within one year of purchase and a 0.50% CDSC is charged on any shares you sell after the first year and within the second year after purchase.

Class C. Shares are offered at their net asset value per share (“NAV”), without any front-end sales charge. However, there is a CDSC of 1% on shares you sell within 12 months after purchase.

Determination of CDSC. The CDSC is based on the original purchase cost or the current market value of the shares being sold, whichever is less. There is no CDSC on shares you purchase through reinvestment of dividends. To keep your CDSC as low as possible, each time you place a request to sell shares, we will first sell any shares in your account that are not subject to a CDSC. If there are not enough of these shares available, we will sell shares that have the lowest CDSC.

For purposes of the CDSC, we count all purchases made during a calendar month as having been made on the FIRST day of that month.

SALES CHARGE REDUCTIONS AND WAIVERS

To receive a waiver or a reduction in sales charges under the programs described below, the shareholder must notify the Funds’ transfer agent (the “Transfer Agent”) (or financial intermediary through which shares are being purchased) at the time of purchase or notify the Transfer Agent at the time of redeeming shares for those reductions or waivers that apply to CDSCs. Such notification must be provided in writing by the shareholder (or other financial intermediary through which shares are being purchased). In addition, a shareholder must provide certain information and records to the Fund as described below under “Information and records to be provided to the Fund.”

| 13 |

Shareholder Account Information

The availability of certain sales charge waivers and reductions will depend on whether you purchase your shares through a financial intermediary or directly through a Fund. Financial intermediaries may have different policies and procedures regarding the availability of front-end sales charge waivers and reductions or CDSC waivers, as referenced below. For waivers and reductions not available through a particular financial intermediary, shareholders will have to purchase Fund shares through another financial intermediary or directly through a Fund to receive these waivers or reductions. If Merrill Lynch is your financial intermediary, please see the section entitled “Financial Intermediary-Specific Sales Charge Waiver Policies” on page A-1 of this Prospectus for additional information about sales charge waivers and reductions that may be available to you.

Reduction in Sales Charges for Certain Investors of Class A shares. Various individuals and institutions may be eligible to purchase Class A shares at reduced sales charge rates under the programs described below. Each Fund reserves the right to modify or cease offering these programs at any time without prior notice.

| • | Rights of Accumulation. A purchaser of Fund shares may qualify for a reduced sales charge by combining a current purchase (or combined purchases as described below) with shares previously purchased and still owned, provided the cumulative value of such shares (valued at cost or current net asset value, whichever is higher) amounts to $50,000 or more. In determining the shares previously purchased, the calculation will include, in addition to other Class A shares of the particular Fund that were previously purchased, shares of the other classes of the same Fund, as well as shares of any class of any other Fund or of any of the other Funds advised by SunAmerica, as long as such shares were sold with a sales charge at the time of purchase or acquired in exchange for shares purchased with a sales charge. |

| • | Letter of Intent. A reduction of sales charges is also available to an investor who, pursuant to a written Letter of Intent, establishes a total investment goal in Class A shares of one or more Funds to be achieved through any number of investments over a thirteen-month period, of $50,000 or more. Each investment in such Funds made during the period will be subject to a reduced sales charge applicable to the goal amount. The initial purchase must be at least 5% of the stated investment goal and shares totaling 5% of the dollar amount of the Letter of Intent will be held in escrow by the Transfer Agent, in the name of the investor. |

| • | Combined Purchases. In order to take advantage of reductions in sales charges that may be available to you when you purchase Fund shares, you must inform the Transfer Agent if you have entered into a Letter of Intent or right of accumulation and if there are other accounts in which there are holdings eligible to be aggregated with your purchase. To receive a reduced front-end sales charge, you or your financial intermediary must inform the Fund at the time of your purchase of Fund shares, that you believe you qualify for a discount. If you purchased shares through a financial intermediary, you may need to provide certain records, such as account statements for accounts held by family members or accounts you hold at another broker-dealer or financial intermediary, in order to verify your eligibility for reduced sales charges. |

Waivers for Certain Investors for Class A shares. The following individuals and institutions may purchase Class A shares without front-end sales charges. The Funds reserve the right to modify or to cease offering these programs at any time.

| • | Financial planners, institutions, broker-dealer representatives or registered investment advisers utilizing fund shares in fee-based investment programs under an agreement with AIG Capital Services, Inc. (“ACS” or the “Distributor”). The financial planner, financial institution or broker-dealer must have a supplemental selling agreement with ACS and charge its client(s) an advisory fee based on the assets under management on an annual basis. |

| • | Participants in certain employer-sponsored benefit plans. The front-end sales charge is waived with respect to shares purchased by employer-sponsored retirement plans that offer a Fund as an investment vehicle, including qualified and nonqualified retirement plans, deferred compensation plans and other employer-sponsored retirement, savings or benefit plans, such as defined benefit plans, 401(k) plans, 457 plans, 403(b) plans, and other pension, educational and profit-sharing plans, but not IRAs. |

| • | Current or retired officers and Trustees of the Trust, and full-time employees of SunAmerica and its affiliates, as well as family members of the foregoing. |

| • | Selling brokers and their employees and sales representatives and their families (i.e., members of a family unit comprised of husband, wife, and minor children). |

| • | Registered management investment companies that are advised by SunAmerica. |

| • | Financial intermediaries who have entered into an agreement with the Distributor to offer shares through a no-load network or platform, or through self-directed investment brokerage accounts, that may or may not charge a transaction fee to its customers. |

Waivers for Certain Investors for Class C Shares. Under the following circumstances, the CDSC may be waived on redemption of Class C Shares. The Funds reserve the right to modify or cease offering these programs at any time without prior notice.

| • | Within one year of the shareholder’s death or becoming legally disabled (individual and spousal joint tenancy accounts only). |

| • | Taxable distributions to participants made by qualified retirement plans or retirement accounts (not including rollovers) for which AIG Fund Services, Inc. (“AFS” or the “Servicing Agent”) serves as fiduciary and in which the plan participant or account holder has attained the age of 59 1/2 at the time the redemption is made. |

| 14 |

| • | To make payments through the Systematic Withdrawal Plan (subject to certain conditions). |

| • | Eligible participant distributions from employer-sponsored retirement plans that meet the eligibility criteria set forth above under “Waivers for Certain Investors for Class A shares,” such as distributions due to death, disability, financial hardship, loans, retirement and termination of employment, or any return of excess contributions. |

| • | Involuntary redemptions (e.g., closing of small accounts described under Shareholder Account Information). |

Sales Charge Arrangements and Waivers. The Funds and ACS offer other opportunities to purchase shares without sales charges under the programs described below. The Funds reserve the right to modify or cease offering these programs at any time without prior notice.

| • | Dividend Reinvestment. Dividends and/or capital gains distributions received by a shareholder from a Fund will automatically be reinvested in additional shares of the Fund and share class without sales charge, at the NAV in effect on the payable date. Alternatively, dividends and distributions may be reinvested in any retail fund distributed by ACS. Or, you may receive amounts in excess of $10.00 in cash if you elect in writing not less than five business days prior to the payment date. You will need to complete the relevant part of the Account Application to elect one of these other options. |

| • | Exchange of Shares. Shares of the Funds may be exchanged for the same class of shares of one or more other retail funds distributed by ACS at NAV at the time of exchange. Please refer to “Additional Investor Services” in this Prospectus for more details about this program. In addition, in connection with advisory fee-based programs sponsored by certain financial intermediaries, and subject to the conditions set forth in the Funds’ SAI, shareholders may exchange their shares (i) from Class A or Class C shares of a Fund into Class W shares of the same Fund and (ii) from Class W shares of a Fund into Class A shares of the same Fund. Please refer to “Exchange Privilege” in the SAI for more details about these types of exchanges and the corresponding sales charge arrangements. |

| • | Reinstatement Privilege. Within one year of a redemption of certain Class A and Class C shares of a Fund, the proceeds of the sale may be invested in the same share class of any Fund or in the same share class of any other retail fund distributed by ACS without a sales charge. A shareholder may use the reinstatement privilege only one time after selling such shares. If you paid a CDSC when you sold your shares, we will credit your account with the dollar amount of the CDSC at the time of sale. This may impact the amount of gain or loss recognized on the previous sale, for tax purposes. All accounts involved must be registered in the same name(s). |

Information and records to be provided to the Fund. You may be asked to provide supporting account statements or other information to allow us to verify your eligibility to receive a reduction or waiver of sales charge.

For more information regarding the sales charge reductions and waivers described above, please visit our website at www.aig.com/funds. The section entitled “Financial Intermediary-Specific Sales Charge Waiver Policies” on page A-1 of this Prospectus and the Funds’ SAI also contain additional information about the sales charges and certain reductions and waivers.

DISTRIBUTION AND SERVICE FEES

Each class of shares (other than Class I and Class W) of each Fund has its own plan of distribution pursuant to Rule 12b-1 (“Rule 12b-1 Plans”) that provides for distribution and account maintenance fees (collectively, “Rule 12b-1 Fees”) (payable to ACS) based on a percentage of average daily net assets, as follows:

| Class | Distribution Fee | Account Maintenance Fee | ||||||||

| A | 0.10% | up to 0.25% | ||||||||

| C | 0.75% | up to 0.25% | ||||||||

Because Rule 12b-1 Fees are paid out of a Fund’s assets on an ongoing basis, over time these fees will increase the cost of your investment and may cost you more than paying other types of sales charges.

In addition, ACS is paid a fee of 0.25% and 0.15% of average daily net assets of Class I shares and Class W shares, respectively, in compensation for providing additional shareholder services to Class I and Class W shareholders.

OPENING AN ACCOUNT (Classes A and C)

| 1. | Read this Prospectus carefully. |

| 2. | Determine how much you want to invest. The minimum initial investments for the Funds are as follows: |

| • | non-retirement account: $500 |

| • | retirement account: $250 |

| • | dollar cost averaging: $500 to open; you must invest at least $25 a month. |

| 15 |

Shareholder Account Information

The minimum subsequent investments for the Funds are as follows:

| • | non-retirement account: $100 |

| • | retirement account: $25 |

| • | The minimum initial and subsequent investments may be waived for certain fee-based programs and/or group plans held in omnibus accounts. |

| 3. | Complete the appropriate parts of the Account Application, carefully following the instructions. If you have any questions, please contact your broker or financial adviser or call Shareholder Services at 800-858-8850. |

| 4. | Complete the appropriate parts of the Supplemental Account Application. By applying for additional investor services now, you can avoid the delay and inconvenience of having to submit an additional application if you want to add services later. |

| 5. | Make your initial investment using the chart on the next page. You can also initiate any purchase, exchange or sale of shares through your broker or financial adviser. |

As part of your application, you are required to provide information regarding your personal identification under anti-money laundering laws, including the USA PATRIOT Act of 2001, as amended (the “PATRIOT Act”). If we are unable to obtain the required information, your application will not be considered to be in good order, and it therefore cannot be processed. Your application and any check or other deposit that accompanied your application will be returned to you. Applications must be received in good order under the PATRIOT Act requirements and as otherwise required in this Prospectus in order to receive that day’s net asset value. In addition, applications received in good order are nevertheless subject to customer identification verification procedures under the PATRIOT Act. We may ask to see your driver’s license or other identifying documents. We may share identifying information with third parties for the purpose of verification. If your identifying information cannot be verified within a reasonable time after receipt of your application, the account will not be processed or, if processed, the Funds reserve the right to redeem the shares purchased and close the account. If a Fund closes an account in this manner, the shares will be redeemed at the net asset value next calculated after the Fund decides to close the account. In these circumstances, the amount redeemed may be less than your original investment and may have tax implications. Consult with your tax adviser for details. Non-resident aliens will not be permitted to establish an account through the check and application process at the Transfer Agent.

If you invest in a Fund through your dealer, broker or financial adviser, your dealer, broker or financial adviser may charge you a transaction-based fee or other fees for its services in connection with the purchase or redemption of Fund shares. These fees are in addition to those imposed by the Fund and its affiliates. You should ask your dealer, broker or financial adviser about applicable fees.

Investment Through Financial Institutions. Dealers, brokers, financial advisers or other financial institutions (collectively, “Financial Institutions” or “Financial Intermediaries”) may impose charges, limitations, minimums and restrictions in addition to or different from those applicable to shareholders who invest in the Funds directly. Accordingly, the net yield and/or return to investors who invest through Financial Institutions may be less than an investor would receive by investing in the Funds directly. Financial Institutions may also set deadlines for receipt of orders that are earlier than the order deadline of the Funds due to processing or other reasons. An investor purchasing through a Financial Institution should read this Prospectus in conjunction with the materials provided by the Financial Institution describing the procedures under which Fund shares may be purchased and redeemed through the Financial Institution. For any questions concerning the purchase or redemption of Fund shares through a Financial Institution, please call your Financial Institution or the Funds (toll free) at (800) 858-8850.

| 16 |

HOW TO BUY SHARES (Classes A and C)

Buying Shares Through Your Financial Institution

You may generally open an account and buy Class A and C shares through any Financial Institution. Your Financial Institution will place your order on your behalf. You may purchase additional shares in a variety of ways, including through your Financial Institution or by sending your check or wire directly to the Fund or its agents as described below under “Adding to an Account.” The Funds will generally not accept new accounts that are not opened through a Financial Institution except for accounts opened by current and former Trustees and other individuals who are affiliated with, or employed by an affiliate of, the Funds or any fund distributed by the Distributor, selling brokers and their employees and sales representatives, family members of these individuals and certain other individuals at the discretion of the Funds or their agents as described below under “Opening an Account.”

Buying Shares Through the Funds

| Opening an Account |

Adding to an Account |

By check

| • Make out a check for the investment amount, payable to the Fund or to AIG Funds. An account cannot be opened with a Fund check. • Deliver the check and your completed Account Application (and Supplemental Account Application, if applicable) to:

(via regular mail) AIG Funds c/o DST PO Box 219186 Kansas City, MO 64121-9186

(via express, certified and registered mail) AIG Funds c/o DST 330 W 9th St. Kansas City, MO 64105-1514

• All purchases must be in U.S. dollars. Cash, money orders and/or travelers checks will not be accepted. A $25.00 fee will be charged for all checks returned due to insufficient funds. • Accounts can only be opened by check by a non-resident alien or on funds drawn from a non-U.S. bank if they are processed through a brokerage account or the funds are drawn from a U.S. branch of a non-U.S. bank. A personal check from an investor should be drawn from the investor’s bank account. In general, starter checks, cash equivalents, stale-dated or post-dated checks will not be accepted. |

• Make out a check for the investment amount, payable to the Fund or to AIG Funds. Shares cannot be purchased with a Fund check. • Include the stub from your Fund statement or a note specifying the Fund name, your share class, your account number and the name(s) in which the account is registered. • Indicate the Fund and account number in the memo section of your check. • Deliver the check and your stub or note to your broker or financial adviser, or mail them to:

(via regular mail) AIG Funds c/o DST PO Box 219186 Kansas City, MO 64121-9186

(via express, certified and registered mail) AIG Funds c/o DST 330 W 9th St. Kansas City, MO 64105-1514 | |

By wire

| • Fax your completed application to AIG Fund Services, Inc. at 816-218-0519. • Obtain your account number by calling Shareholder Services at 800-858-8850. • Instruct your bank to wire the amount of your investment to:

DST Boston, MA ABA #0110-00028 DDA # 99029712

ATTN: (include name of Fund and share class).

FBO: (include account number and name(s) in which the acct. is registered).

Your bank may charge a fee to wire funds. |

• Instruct your bank to wire the amount of your investment to:

DST Boston, MA ABA #0110-00028 DDA # 99029712

ATTN: (include name of Fund and share class).

FBO: (include account number and name(s) in which the acct. is registered).

Your bank may charge a fee to wire funds. | |

To open or add to an account using dollar cost averaging, see “Additional Investor Services.”

| 17 |

Shareholder Account Information

HOW TO SELL SHARES (Classes A and C)

Selling Shares Through Your Financial Institution

You can sell shares through your Financial Institution or through the Funds as described below under “Selling Shares Through the Funds.” Shares held for you in your various Financial Institution’s name must be sold through the Financial Institution.

Selling Shares Through the Funds

By mail

| Send your request to:

(via regular mail) AIG Funds c/o DST PO Box 219186 Kansas City, MO 64121-9186

(via express, certified and registered mail) AIG Funds c/o DST 330 West 9th Street Kansas City, MO 64105-1514 |

Your request should include:

• Your name • Fund name, share class and account number • The dollar amount or number of shares to be redeemed • Any special payment instructions • The signature of all registered owners exactly as the account is registered, and • Any special documents required to assure proper authorization

On overnight mail redemptions, a $25 fee will be deducted from your account. | |

By phone

| • Call Shareholder Services at 800-858-8850 between 8:30 a.m. and 6:00 p.m. Eastern time on most business days. • Or, for automated 24-hour account access call FastFacts at 800-654-4760. |

||

By wire

| If banking instructions exist on your account, this may be done by calling Shareholder Services at 800-858-8850 between 8:30 a.m. and 6:00 p.m. (Eastern time) on most business days. Otherwise, you must provide, in writing, the following information:

• Fund name, share class and account number you are redeeming • Bank or Financial Institution name • ABA routing number • Account number, and • Account registration |

If the account registration at your bank is different than your account at SunAmerica, your request must be Medallion Guaranteed. A notarization is not acceptable.

Minimum amount to wire money is $250. A $15 fee per fund will be deducted from your account. | |

By Internet

| Visit our website at www.aig.com/funds, and select the “Click Here for Secure Login” hyperlink (generally not available for retirement accounts). | Proceeds for all transactions will normally be sent on the business day after the trade date. Additional documents may be required for certain transactions. | |

To sell shares through a systematic withdrawal plan, see “Additional Investor Services.”

Certain Requests Require a Medallion Guarantee:

To protect you and the Funds from fraud, the following redemption requests must be in writing and include a Medallion Guarantee (although there may be other situations that also require a Medallion Guarantee) if:

| • | Redemptions of $100,000 or more |

| • | The proceeds are to be payable other than as the account is registered |

| • | The redemption check is to be sent to an address other than the address of record |

| 18 |

| • | Your address of record has changed within the previous 30 days |

| • | Shares are being transferred to an account with a different registration |

| • | Someone (such as an Executor) other than the registered shareholder(s) is redeeming shares (additional documents may be required). |

You can generally obtain a Medallion Guarantee from the following sources:

| • | A broker or securities dealer |

| • | A federal savings, cooperative or other type of bank |

| • | A savings and loan or other thrift institution |

| • | A credit union |

| • | A securities exchange or clearing agency |

A notary public CANNOT provide a Medallion Guarantee.

OPENING AN ACCOUNT, BUYING AND SELLING SHARES (Class W)

Class W shares of the Funds are offered exclusively for sale through advisory fee-based programs sponsored by certain Financial Intermediaries and any other institutions having agreements with the Funds, whose use of Class W shares will depend on the structure of the particular advisory fee-based program. The minimum initial investment for Class W shares of the Funds is $50,000 and there is no minimum subsequent investment. The minimum initial investment for Class W shares may be waived for certain fee-based programs. Inquiries regarding the purchase, redemption or exchange of Class W shares or the making or changing of investment choices should be directed to your financial adviser.

TRANSACTION POLICIES (All Funds and All Classes)

Valuation of shares. The NAV for each Fund and class is determined each Fund business day at the close of regular trading on the New York Stock Exchange (“NYSE”) (generally 4:00 p.m., Eastern Time) by dividing the net assets of each class by the number of such class’s outstanding shares. The NAV for each Fund also may be calculated on any other day in which the Adviser determines that there is sufficient liquidity in the securities held by the Fund. As a result, the value of each Fund’s shares may change on days when you will not be able to purchase or redeem your shares. Securities for which market quotations are readily available are valued at their market price as of the close of regular trading on the NYSE, unless, in accordance with pricing procedures approved by the Board of Trustees, the market quotations are determined to be unreliable. Securities and other assets for which market quotations are not readily available or unreliable are valued at fair value in accordance with pricing procedures periodically reviewed and approved by the Board. There is no single standard for making fair value determinations, which may result in prices that vary from those of other funds. In addition, there can be no assurance that fair value pricing will reflect actual market value and it is possible that the fair value determined for a security may differ materially from the value that could be realized upon the sale of the security.

Investments in registered investment companies that do not trade on an exchange are valued at the end of the day NAV. Investments in registered investment companies that trade on an exchange are valued at the last sales price or official closing price as of the close of the customary trading session on the exchange where the security principally traded. The prospectus for any such open-end funds should explain the circumstances under which these funds use fair value pricing and the effects of using fair value pricing.

As of the close of regular trading on the NYSE, securities traded primarily on securities exchanges outside of the United States are valued at the last sale price on such exchanges on the day of valuation, or if there is no sale on the day of valuation, at the last-reported bid price. If a security’s price is available from more than one exchange, a Fund will use the exchange that is the primary market for the security. However, depending on the foreign market, closing prices may be up to 15 hours old when they are used to price the Fund’s shares, and the Fund may determine that certain closing prices do not reflect the fair value of the securities. This determination will be based on review of a number of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. If a Fund determines that closing prices do not reflect the fair value of the securities, the Fund will adjust the previous closing prices in accordance with pricing procedures approved by the Board to reflect what it believes to be the fair value of the securities as of the close of regular trading on the NYSE. The Funds may also fair value securities in other situations, for example, when a particular foreign market is closed but a Fund is open. For foreign equity securities and foreign equity futures contracts, a Fund uses an outside pricing service to provide it with closing market prices and information used for adjusting those prices.

The Funds may invest to a large extent in securities that are primarily listed on foreign exchanges that trade on weekends or other days when the Funds do not price their shares. As a result, the value of the Funds’ shares may change on days when the Funds are not open for purchase or redemptions.

| 19 |

Shareholder Account Information

Buy and sell prices. When you buy Class A or C shares, you pay the NAV plus any applicable sales charges, as described above. When you sell Class A or C shares, you receive the NAV minus any applicable CDSCs. Class I shares of the International Dividend Strategy Fund are closed to new purchases. When you sell Class I shares of the International Dividend Strategy Fund, you receive NAV. When you buy Class W shares, you pay the NAV. When you sell Class W shares, you receive the NAV.

Execution of requests. Each Fund is open on those days when the NYSE is open for regular trading (“Fund business day”). We execute buy and sell requests at the next NAV to be calculated after the Fund receives your request in good order. Each Fund has authorized one or more Financial Institutions, or their agents, to receive purchase or redemption orders on its behalf. A purchase, exchange or redemption order is in “good order” when a Fund, ACS, a Financial Institution or their respective agents, as applicable, receive all required information, including properly completed and signed documents. If a Fund, ACS, a Financial Institution or their respective agents receive your order before a Fund’s close of business (generally 4:00 p.m., Eastern Time), you will receive that day’s closing price. If a Fund, ACS, a Financial Institution or their respective agents receive your order after that time, you will receive the next business day’s closing price. The Funds reserve the right to reject any order to buy shares.

Certain qualified Financial Institutions may transmit an investor’s purchase or redemption order to the Funds’ Transfer Agent after the close of regular trading on the NYSE on a Fund business day, on the day the order is received from the investor, as long as the investor has placed the order with the Financial Institution by the close of regular trading on the NYSE on that day. The investor will then receive the NAV of the Fund’s shares determined by the close of regular trading on the NYSE on the day the order was placed with the qualified Financial Institution. Orders received after such time will not result in execution until the following Fund business day. Financial Institutions are responsible for instituting procedures to ensure that purchase and redemption orders by their respective clients are processed expeditiously.

The processing of sell requests and payment of proceeds may generally not be postponed for more than seven days, except when the NYSE is closed (other than weekends or holidays), when trading on the NYSE is restricted, or as permitted by the Securities and Exchange Commission (“SEC”). The Funds and their agents reserve the right to “freeze” or “block” (that is, disallow any further purchases or redemptions from any account) or suspend account services in certain instances as permitted or required by applicable laws and regulations, including applicable anti-money laundering regulations. Examples of such instances include, but are not limited to: (i) where an accountholder appears on the list of “blocked” entities and individuals maintained pursuant to Office of Foreign Assets Control regulations; (ii) where a Fund or its agents detect suspicious activity or suspect fraudulent or illegal activity; or (iii) when certain notifications have been received by a Fund or its agents that there is a dispute between the registered or beneficial account owners.

If a Fund determines that it would be detrimental to the best interests of the remaining shareholders of the Fund to make payment of redemption proceeds wholly or partly in cash, the Fund may pay the redemption price by a distribution in kind of securities from the Fund in lieu of cash. However, the Japan Fund has made an election that requires it to pay a certain portion of redemption proceeds in cash.

At various times, a Fund may be requested to redeem shares for which it has not yet received good payment. A Fund may delay or cause to be delayed the mailing of a redemption check until such time as good payment (e.g., wire transfer or certified check drawn on a United States bank) has been collected for the purchase of such shares, which will not exceed 15 days.

Under normal circumstances, each Fund expects to meet redemption requests by using cash or cash equivalents in its portfolio or by selling portfolio assets to generate cash. During periods of stressed market conditions, a Fund may be more likely to limit cash redemptions and may determine to pay redemption proceeds by borrowing under a line of credit and/or transferring portfolio securities in-kind to you in lieu of cash. If a Fund pays redemption proceeds by transferring portfolio securities in-kind to you, you may pay transaction costs to dispose of the securities, and you may receive less for them than the price at which they were valued for purposes of redemption.

Telephone transactions. For your protection, telephone requests are recorded in order to verify their accuracy. In addition, Shareholder Services will take measures to verify the identity of the caller, such as asking for name, account number, social security or other taxpayer ID number and other relevant information. If appropriate measures are not taken, the Fund is responsible for any losses that may occur to any account due to an unauthorized telephone call. Also for your protection, telephone transactions are not permitted on accounts whose names or addresses have changed within the past 30 days. At times of peak activity, it may be difficult to place requests by phone. During these times, consider sending your request in writing.

Exchanges. You may exchange shares of a Fund for shares of the same class of any other retail fund distributed by ACS. Such exchange will generally constitute a taxable event for U.S. federal income tax purposes. Before making an exchange, you should review a copy of the prospectus of the fund into which you would like to exchange. All exchanges are subject to applicable minimum investment requirements. A Systematic Exchange Program is described under “Additional Investor Services.”

If you exchange shares that were purchased subject to a CDSC, the CDSC schedule will continue to apply following the exchange. In determining the CDSC applicable to shares being sold after an exchange, we will take into account the length of time you held those shares prior to the exchange.

| 20 |