Form 424B2 GOLDMAN SACHS GROUP INC

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-239610

BlackRock® Dynamic Factor Index Supplement No. 10 to the Prospectus and the Prospectus Supplement, each as may be amended from time to time, that form a part of Registration Statement No. 333-239610

|

|

GS Finance Corp. Medium-Term Notes, Series E Medium-Term Notes, Series F guaranteed by The Goldman Sachs Group, Inc. BlackRock® Dynamic Factor Index Supplement No. 10 Notes Linked to the Performance of the BlackRock® Dynamic Factor Index |

GS Finance Corp. may from time to time offer and sell notes, the payments and performance of which will be linked to the BlackRock® Dynamic Factor Index (the “index”). The index measures the extent to which the performance of the combination of an equity ETF basket composed of up to five equity ETFs, a fixed income ETF basket composed of up to three fixed income ETFs and a cash constituent (together with the ETFs, the underlying assets) outperforms the sum of the return on 3-month USD LIBOR plus an additional 0.65% per annum fee (accruing daily). The weights of the ETFs within the equity ETF basket are determined based on three common economic measures (factors) – “economic regime”, “value” and “momentum”, while the weights of the ETFs within the fixed income ETF basket are determined based on how medium-term interest rates are trending. The relative weights of the equity ETF basket, the fixed income ETF basket and the cash constituent that compose the index are determined based on measures of volatility using the past returns of the ETFs (i.e., the degree of variation in past returns given the various weightings of these components). The equity ETF basket rebalances monthly and the fixed income ETF basket rebalances on each index business day. Allocations of the index among the equity ETF basket, the fixed income ETF basket and the cash constituent are determined on each index business day with a goal of limiting volatility (i.e., the degree of variation in the past returns) to no more than 5%.

As a result of such allocations, the index may include limited exposure to the ETFs and may allocate a significant portion of its exposure to the cash constituent, the return on which will be less than the sum of the return on 3-month USD LIBOR plus 0.65% per annum. In recent months, a very significant portion (up to 85.5%) of the index has been allocated to the cash constituent. The greater the percentage of the index allocated to the cash constituent, the higher the return that will be required on the ETFs in order to have a return on your investment.

Because the index measures the performance of the selected underlying assets less the sum of the return on 3-month USD LIBOR plus 0.65% per annum (accruing daily), on any day such underlying assets must outperform the return on 3-month USD LIBOR plus 0.65% per annum for the index level to increase.

The accompanying prospectus and the accompanying prospectus supplement, each as may be amended from time to time, that form a part of Registration Statement No. 333-239610, describes some of the terms that may apply generally to the notes, including any notes you purchase. A separate pricing supplement, which we refer to as the applicable pricing supplement and, if specified in the applicable pricing supplement, a separate product supplement, which we refer to as the applicable product supplement, will describe additional terms that apply to your notes.

This index supplement contains the following:

|

● |

A summary overview of the index. You should read this summary overview in conjunction with (i) the more detailed description of index to be set forth in the applicable pricing supplement and (ii) the descriptions of the index’s underlying assets (including the ETFs) set forth herein. |

|

• |

Certain risks applicable to the index’s ETFs. You should read these risks in conjunction with the risks and considerations described in the applicable pricing supplement (including risks and considerations relating to the index itself, the particular notes being offered thereby and certain other matters), the applicable product supplement, if any, the accompanying prospectus supplement and the accompanying prospectus. |

|

• |

A description of the index’s underlying assets. |

Your investment in the notes involves certain risks. See “Additional Risk Factors Specific to the Notes” beginning on page S-9 to read about investment risks relating to the notes.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this index supplement no. 10, the applicable pricing supplement, the applicable product supplement, if any, the accompanying prospectus supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

The notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

GS Finance Corp. may use this index supplement in the initial sale of the notes. In addition, Goldman Sachs & Co. LLC (GS&Co.), or any other affiliate of GS Finance Corp., may use this index supplement in a market-making transaction in a note after its initial sale. Unless GS Finance Corp. or its agent informs the purchaser otherwise in the confirmation of sale, this index supplement is being used in a market-making transaction.

|

|

Goldman Sachs & Co. LLC BlackRock® Dynamic Factor Index Supplement No. 10 dated November 24, 2020. |

The Notes Are Part of a Series

The notes are part of a series of debt securities that we may issue under our indenture from time to time. The notes are “indexed debt securities”, as defined in the accompanying prospectus. The applicable pricing supplement will specify whether the series is entitled “Medium-Term Notes, Series E” or “Medium-Term Notes, Series F.” The notes will be fully and unconditionally guaranteed by The Goldman Sachs Group, Inc. We describe terms that apply generally to all medium-term notes of the applicable series in “Description of Notes We May Offer” and “Description of Debt Securities We May Offer” in the accompanying prospectus supplement for the applicable series of medium-term notes and the accompanying prospectus, respectively. The applicable pricing supplement will describe any additions or changes to the terms of the notes being offered thereby.

Please note that the information about the settlement or trade dates, issue price, underwriting discounts or commissions and net proceeds to us in the applicable pricing supplement relates only to the initial issuances and sales of your notes. If you have purchased your notes in a market-making transaction after any initial issuance and sale, any such relevant information about the sale to you will be provided in a separate confirmation of sale.

Specific Terms Will Be Described in the Applicable Pricing Supplement and the Applicable Product Supplement, If Any

The specific terms of your notes will be described in the applicable pricing supplement and the applicable product supplement, if any, accompanying this index supplement. The terms described therein are in addition to those described herein and in the accompanying prospectus and the accompanying prospectus supplement.

S-2

|

Please note that this section constitutes only a brief overview of the index. The index will be described in more detail in the applicable pricing supplement. You should not invest in the notes without also reading the applicable pricing supplement in full, including the sections entitled “The Index” and “Additional Risk Factors Specific to Your Notes” (including risks and considerations relating to the index, the particular notes being offered thereby and certain other matters). Neither this section, the section entitled “Additional Risks Factors Specific to the ETFs” nor any other information in this index supplement is intended to be a substitute for the information relating to the index, including the risk factors relating to the index, set forth in the applicable pricing supplement. |

The BlackRock® Dynamic Factor Index (the index) measures the extent to which the performance of the combination of an equity ETF basket composed of five equity ETFs, a fixed income ETF basket composed of three fixed income ETFs and a cash constituent (together with the ETFs, the underlying assets) outperforms the sum of the return on a notional interest rate (3-month USD LIBOR) plus 0.65% per annum (accruing daily). The weights of the ETFs within the equity ETF basket are determined based on three common economic measures (factors) — “economic regime”, “value” and “momentum”, while the weights of the ETFs and within the fixed income ETF basket are determined based on how medium-term interest rates are trending. The relative weights of the equity ETF basket, the fixed income ETF basket and the cash constituent that compose the index are determined based on measures of volatility using the past returns of the ETFs (i.e., the degree of variation in past returns given the various weightings of these components).

The following is a summary of the index components:

|

• |

An equity ETF basket with components that are weighted to provide exposure to three common economic measures (factors) — “economic regime”, “value” (which is composed of a “cash flow from operations to price” signal and a “forward earnings yield” signal) and “momentum”. For purposes of calculating the index, a signal is a measurement of a specified economic measure that is used to determine the components of the equity and fixed income ETF baskets. Each month, the allocation to the five equity ETFs in the equity ETF basket is rebalanced based primarily on the characteristics of each equity ETF as measured by each of the three common factors and the volatility of the returns of each equity ETF. The five equity ETFs are as follows: |

|

|

o |

iShares® MSCI USA Momentum Factor ETF (MTUM); |

|

|

o |

iShares® MSCI USA Size Factor ETF (SIZE); |

|

|

o |

iShares® MSCI USA Quality Factor ETF (QUAL); |

|

|

o |

iShares® MSCI USA Value Factor ETF (VLUE); and |

|

|

o |

iShares® MSCI USA Min Vol Factor ETF (USMV). |

|

• |

A fixed income ETF basket with components that are weighted based on a rates momentum signal which measures how medium-term interest rates are trending. On each index index business day, the allocation to the fixed income ETFs in the fixed income ETF basket is rebalanced, with 50% allocated to the iShares® 7-10 Year Treasury Bond ETF and the remaining 50% allocated to one of the other fixed income ETFs (other than during periods when a transition is being effected between the iShares® 1-3 Year Treasury Bond ETF and the iShares® 20+ Year Treasury Bond ETF). The three fixed income ETFs are as follows: |

|

|

o |

iShares® 1-3 Year Treasury Bond ETF (SHY); |

|

|

o |

iShares® 7-10 Year Treasury Bond ETF (IEF); and |

|

|

o |

iShares® 20+ Year Treasury Bond ETF (TLT). |

|

• |

A cash constituent that reflects the notional returns accruing to a hypothetical investor from an investment in a notional money market account that accrues interest at 3-month USD LIBOR, calculated in accordance with the Act/360 day count convention (i.e., using the actual number of days in the relevant accrual period divided by 360). |

Allocations of the index among the equity ETF basket, the fixed income ETF basket and the cash constituent are determined on each index business day according to the following volatility control procedures:

|

• |

First, to the extent that the volatility (i.e., the degree of variation in the past returns) of the equity ETF basket exceeds the target volatility of 5%, the fixed income ETF basket is assigned a positive weight, and the weight of the equity ETF basket is reduced by the amount needed to achieve the 5% volatility target. For purposes of calculating volatility in this portion of the volatility control procedures, the volatility contribution of the fixed income ETF basket is not taken into account. |

|

• |

Second, to the extent that the historically realized volatility of a weighted four asset portfolio consisting of the equity ETF basket and the three fixed income ETFs exceeds the 5% volatility target, the index will make an allocation to the cash constituent, and the weights of the equity ETF basket and fixed income ETFs will be ratably reduced. |

How the volatilities used to make allocations of the index among its components are calculated, including over what time periods historical data is employed and the method of calculation, is described in greater detail below.

S-3

|

• |

an “underlying asset” is one of the ETFs or the cash constituent that is eligible for inclusion in the index on an index business day; |

|

• |

an “ETF” is one of the ETFs that is eligible for inclusion in the index on an index business day; and |

|

• |

an “index business day” is a day on which the New York Stock Exchange is open for regular trading. |

BlackRock Index Services, LLC (“Index Services” or the “index administrator”), a subsidiary of BlackRock, Inc., designs, sponsors, calculates, administers and publishes the index.

S-4

As of November 12, 2020, the following chart sets forth the weighting of each underlying asset and the hypothetical and historical average percentage weightings of the underlying assets, the highest percentage weightings of the underlying assets and the percentage of index business days with positive weightings for the underlying assets from January 1, 2015 to November 12, 2020. The chart uses historical information from October 31, 2019 (the index launch date) to November 12, 2020 and hypothetical data from January 1, 2015 to October 31, 2019. The hypothetical data is based on the historical levels of the underlying assets and uses the same methodology that is used to calculate the index. As a result, the following chart does not reflect the global financial crisis which began in 2008, which had a materially negative impact on certain of the underlying assets. You should not take the historical information or hypothetical data as an indication of the future performance of the index.

|

Underlying Asset |

Weighting (as of November 12, 2020)* |

Average Weighting (as of November 12, 2020)* |

Highest Weighting (as of November 12, 2020)* |

Percentage of Index Business Days When Underlying Asset is Included in the Index (as of November 12, 2020)* |

|

iShares® MSCI USA Momentum Factor ETF |

5.14% |

9.3% |

41.1% |

94.8% |

|

iShares® MSCI USA Quality Factor ETF |

0.00% |

9.6% |

33.1% |

76.3% |

|

iShares® MSCI USA Size Factor ETF |

4.36% |

8.5% |

46.4% |

91.3% |

|

iShares® MSCI USA Min Vol Factor ETF |

1.06% |

5.2% |

24.7% |

83.1% |

|

iShares® MSCI USA Value Factor ETF |

2.05% |

4.8% |

26.3% |

62.3% |

|

iShares® 1-3 Year Treasury Bond ETF |

0.00% |

5.2% |

38.7% |

22.7% |

|

iShares® 7-10 Year Treasury Bond ETF |

19.68% |

23.0% |

40.0% |

100.0% |

|

iShares® 20+ Year Treasury Bond ETF |

19.68% |

17.7% |

40.0% |

79.2% |

|

Cash Constituent |

48.03% |

16.6% |

85.5% |

81.2% |

*Current weighting information is updated from time to time by the index administrator at blackrock.com/us/individual/products/309029/blackrock-dynamic-factor-index. We are not incorporating by reference the website or any material it includes in this index supplement.

S-5

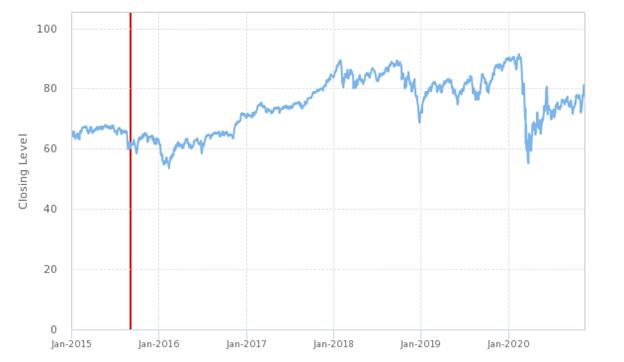

Index Allocations Among Asset Classes

The following chart sets forth the daily allocation on each index business day among each asset class (equity, fixed income and cash constituent) from January 1, 2015 to November 12, 2020, using the historical index information and hypothetical index data described above. (In the chart, this historical information can be found to the right of the vertical solid line marker.) You should not take the historical information or hypothetical data as an indication of the future performance of the index.

S-6

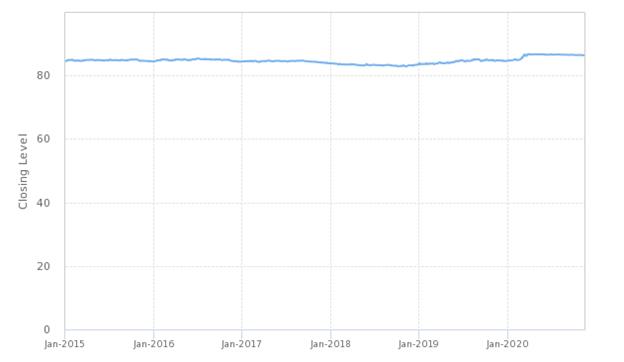

Allocation of Equity ETF Basket

The following chart sets forth the daily allocation on each index business day within the equity ETF basket among the equity ETFs from January 1, 2015 to November 12, 2020, using the historical index information and hypothetical index data described above. (In the chart, historical information can be found to the right of the vertical solid line marker.) You should not take the historical information or hypothetical data as an indication of the future performance of the index.

S-7

Allocation of Fixed Income ETF Basket

The following chart sets forth the daily allocation on each index business day within the fixed income ETF basket among the fixed income ETFs from January 1, 2015 to November 12, 2020, using the historical index information and hypothetical index data described above. (In the chart, historical information can be found to the right of the vertical solid line marker.) You should not take the historical information or hypothetical data as an indication of the future performance of the index.

S-8

Additional Risk Factors Specific to the ETFs

|

The following risks relate only to the ETFs underlying the index. For risks and considerations relating to the index itself and certain other matters, see the applicable pricing supplement. You should carefully review all of the risks and considerations herein and in the applicable pricing supplement, the applicable product supplement, if any, the accompanying prospectus supplement and the accompanying prospectus. An investment in your notes is subject to the risks described below as well as the risks and considerations described in the applicable pricing supplement, the applicable product supplement, if any, the accompanying prospectus supplement and the accompanying prospectus. Your notes are a riskier investment than ordinary debt securities. Also, your notes are not equivalent to investing directly in any underlying asset or the assets held by any ETF or in notes that bear interest at the notional interest rate. You should carefully consider whether the offered notes are appropriate given your particular circumstances. |

Risks related to all of the ETFs

The ETFs Are Passively Managed to Track an Index and May Not Perform as Well as an Actively Managed Fund or Another Investment

The ETFs are not actively managed and may be affected by a general decline in the assets tracked by their underlying indices. Each passively managed ETF invests in assets included in, or representative of, the underlying index. These ETFs’ investment advisors do not attempt to take defensive positions under any market conditions, including during declining markets. This means, among other things, that the investment advisor typically will not sell a particular holding just because it is performing poorly. Instead, the ETF seeks to track the index regardless of whether the index level is increasing or decreasing. As a result, shares of the passively managed ETFs may not perform as well as an investment in actively managed ETFs or a basket comprised solely of actively managed ETFs or some other investment that seeks to outperform a benchmark or market.

There is No Affiliation Between Us and Any Issuer of Assets Held by Any ETF or Any Sponsor of Any ETF

GS&Co. and one or more of our other affiliates may act, from time to time, as authorized participants in the distribution of shares of ETFs, and, at any time, may hold shares of ETFs. We are not affiliated with the issuers of the assets held by the ETFs, the underlying index sponsors or the ETF sponsors or investment advisors. However, our affiliates may currently or from time to time in the future own securities of, or engage in business with, the ETFs, their sponsors, their investment advisors, the sponsors of the underlying indexes or the issuers of assets held by the ETFs. Nevertheless, neither we nor any of our affiliates has verified the accuracy or the completeness of any information about the ETFs, the investment advisors or the issuers of assets held by the ETFs, and we have consulted only publicly available sources of information about them. You, as an investor in the notes, should make your own investigation into the ETFs, the investment advisors and the issuers of the assets held by the ETFs. See “The Underlying Assets” below for additional information about the ETFs.

None of the ETF sponsors, the sponsors of the underlying indexes, the ETFs’ investment advisors and the issuers of assets held by the ETFs are involved in the offering of your notes in any way and none of them have any obligation of any sort with respect to your notes. Thus, none of the ETF sponsors, the sponsors of the underlying indexes, the ETFs’ investment advisors and the issuers of assets held by the ETFs have any obligation to take your interests into consideration for any reason, including in taking any corporate actions that might adversely affect the level of an index or making any investment decision for the ETFs.

The Policies of the ETF Sponsors and/or Investment Advisor, and the Policies of Any Sponsor of an Underlying Index Tracked by an ETF, Could Affect the Level of the Index

Any ETF sponsor or investment advisor may from time to time be called upon to make certain decisions or judgments with respect to the implementation of the strategy of the ETF’s investment advisor concerning additions, deletions or substitutions of securities or assets held by the ETF, the manner in which changes affecting the underlying index, if any, are reflected in the ETF, the means of executing trading on behalf of an ETF, and the best means of tracking an underlying index, if any. The ETF sponsor’s or investment advisor’s decisions or judgments could affect the market price of the shares of the ETF and may adversely affect the level of the index.

In addition, the sponsor of an underlying index tracked by an ETF is responsible for the design and maintenance of such underlying index. The policies of the sponsor of such underlying index concerning the calculation of the underlying index, including decisions regarding the addition, deletion or substitution of the assets included in the underlying index, could affect the level of the underlying index and, consequently, could affect the market price of shares of the ETF and could adversely affect the level of the index, the amount payable on your notes and the market value of your notes.

S-9

There is No Assurance That an Active Trading Market Will Continue for the ETFs or That There Will Be Liquidity in Any Such Trading Market; Further, Each ETF is Subject to Management Risks, Securities Risks, Lending Risks and Custody Risks

Although all of the shares of the ETFs are listed for trading on Cboe BZX Exchange, Inc. (Cboe BZX), NYSE Arca, Inc. (NYSE Arca) or the NASDAQ Stock Market (NASDAQ) and a number of similar products have been traded on the Cboe BZX, NYSE Arca, NASDAQ or other securities exchanges for varying periods of time, there is no assurance that an active trading market will continue for the ETFs or that there will be liquidity in any such trading market.

In addition, each ETF is subject to management risk, which is the risk that an ETF’s investment advisor’s investment strategy, the implementation of which is subject to a number of constraints, may not produce the intended results. In addition, each investment advisor is permitted to engage in securities lending with respect to a portion of the applicable ETF’s total assets, which could subject such ETF to the risk that the borrower of such loaned securities fails to return the securities in a timely manner or at all.

Further, each ETF is subject to custody risk, which refers to the risks in the process of clearing and settling trades and the holding of securities by local banks, agents and depositories. Low trading volumes and volatile prices in less developed markets make trades harder to complete and settle, and governments or trade groups may compel local agents to hold securities in designated depositories that are not subject to independent evaluation. The less developed a country’s securities market is, the greater the likelihood of custody problems.

Further, each ETF is subject to listing standards adopted by Cboe BZX, NYSE Arca or NASDAQ, as applicable. There can be no assurance that an ETF will continue to meet the applicable listing requirements, or that an ETF will not be delisted.

The ETFs May Be Subject to Pricing Dislocations and Other Market Forces, Which May Adversely Affect the Level of the Index

Even if the net asset value of an ETF’s assets is increasing, the market price of its shares may not. Shares of an ETF may trade in the secondary market at times when the ETF does not accept orders to purchase or redeem shares. At such times, shares may trade in the secondary market with more significant premiums or discounts than might be experienced at times when the ETF accepts purchase and redemption orders. Further, from time to time, an authorized participant, a third party investor, an ETF advisor, an affiliate of an ETF advisor or a fund may invest in an ETF and hold its investment for a specific period of time in order to facilitate commencement of an ETF’s operations or for the ETF to achieve size or scale, which could negatively impact such ETF. In addition, shares of each ETF trade at prices at, above or below the most recent net asset value of the ETF’s assets. The trading prices of an ETF’s shares fluctuate continuously throughout trading hours based on market supply and demand rather than the net asset value. The trading prices of the ETF’s shares may deviate significantly from the ETF’s net asset value during periods of market volatility, and disruptions due to creations and redemptions of the ETF’s shares by authorized participants (or disruptions due to the lack of authorized participants able to create or redeem the ETF’s shares) or the existence of extreme market volatility may result in trading prices for shares of the ETF that differ significantly from its net asset value. If any of these dislocations were to occur, the level of the index, the amount payable on your notes and the market value of your notes may be adversely affected.

The Values of the ETFs May Not Completely Track the Level of the Indices Underlying Such ETFs

Although the trading characteristics and valuations of the shares of an ETF will usually mirror to some extent the characteristics and valuations of the underlying index, the value of the shares of an ETF may not completely track the level of the underlying index. One of the common reasons this occurs is that an index is a theoretical financial calculation of the performance of certain assets, but an ETF holds an actual investment portfolio. The value of a share of the ETF may reflect transaction costs and fees incurred or imposed by the investment advisor of the ETF as well as the costs to the ETF to buy and sell its assets. These costs and fees are not included in the calculation of the underlying index. Additionally, because an ETF may not actually hold all of the assets that comprise the underlying index, and may invest in securities that are not part of the underlying index, the ETF may not closely track the performance of the underlying index. Some additional reasons for these tracking differences are described under “The Underlying Assets” below. As a result of these tracking differences, the index may not perform as well as an investment linked directly to the underlying indices of the ETFs.

The ETFs May Be Subject to Global or Regional Financial Risks, Which May Adversely Affect the Level of the Index

Many of the ETFs invest wholly or substantially in regionally-focused debt or equity securities. If a financial crisis occurs in a region, or if there is another global financial crisis such as the one experienced beginning in 2007/2008, any number (if not all) of the ETFs may be severely affected, which may adversely affect the level of the index.

S-10

Risks related to ETFs concentrated in the Information Technology sector

Certain ETFs Are Concentrated in the Information Technology Sector and Do Not Provide Diversified Exposure

Certain ETFs hold assets that are concentrated in the Information Technology sector, which means the ETFs are more likely to be more adversely affected by any negative performance of the Information Technology sector than ETFs that have more diversified holdings across a number of sectors. Market or economic factors impacting technology companies and companies that rely heavily on technological advances could have a major effect on the value of the ETFs’ investments. The value of stocks of technology companies and companies that rely heavily on technology are particularly vulnerable to rapid changes in technology product cycles, rapid product obsolescence, government regulation and competition, both domestically and internationally, including competition from foreign competitors with lower production costs. Stocks of technology companies and companies that rely heavily on technology, especially those of smaller, less-seasoned companies, tend to be more volatile than the overall market. Technology companies are heavily dependent on patent and intellectual property rights, the loss or impairment of which may adversely affect profitability. Additionally, companies in the Information Technology sector may face dramatic and often unpredictable changes in growth rates and competition for the services of qualified personnel.

Risks related to the iShares® MSCI USA Momentum Factor ETF

Momentum Securities Risk

The iShares® MSCI USA Momentum Factor ETF tracks an underlying index that is designed to measure the performance of an equity momentum strategy by emphasizing stocks with high price momentum. Stocks that have previously exhibited high momentum characteristics may not experience positive momentum in the future or may experience more volatility than the market as a whole. The underlying index sponsor may be unsuccessful in creating an underlying index that emphasizes momentum securities. In addition, there may be periods when the momentum style of investing is out of favor and the investment performance of the iShares® MSCI USA Momentum Factor ETF may suffer.

The iShares® MSCI USA Momentum Factor ETF Recently Changed the Index it Tracks

The iShares® MSCI USA Momentum Factor ETF will generally invest in the securities included in the index it tracks, but may invest in cash, cash equivalents and other securities not included in the index. Previously, the iShares® MSCI USA Momentum Factor ETF tracked the MSCI USA Momentum Index, but, beginning on November 23, 2020, the iShares® MSCI USA Momentum Factor ETF began tracking the MSCI USA Momentum SR Variant Index. Any historical information about the performance of the iShares® MSCI USA Momentum Factor ETF for any period before November 23, 2020 was during a period in which the iShares® MSCI USA Momentum Factor ETF tracked a different index, and therefore should not be considered information relevant to how the iShares® MSCI USA Momentum Factor ETF will perform as it tracks the MSCI USA Momentum SR Variant Index.

The performance of the MSCI USA Momentum SR Variant Index may deviate from the performance of the MSCI USA Momentum Index as a result of its different rebalancing mechanics. Such divergence in performance may occur during any period that includes a rebalancing (whether scheduled or ad-hoc), and may be particularly acute during periods characterized by more frequent ad-hoc rebalancing or market volatility.

The Index Which the iShares® MSCI USA Momentum Factor ETF Tracks Is a New Index Without a Historical Track Record

The MSCI USA Momentum SR Variant Index was launched on May 19, 2020. The index sponsor of the MSCI USA Momentum SR Variant Index has published hypothetical historical information regarding the historical performance of the MSCI USA Momentum SR Variant Index prior to May 19, 2020. Because the MSCI USA Momentum SR Variant Index was not published during those periods, these levels should not be relied upon when making your investment decision.

Risks related to the iShares® MSCI USA Quality Factor ETF

Quality Stocks Risk

The iShares® MSCI USA Quality Factor ETF tracks an underlying index that is designed to measure historical and expected high returns on equity, stable earnings growth and low debt-to-asset ratio. However, there is no guarantee that the past performance of these stocks will continue. The underlying index sponsor may be unsuccessful in creating an underlying index that reflects the quality of individual stocks. Companies that issue these stocks may not be able to sustain consistently high returns on equity, earnings and growth year after year and may need to borrow money or issue debt despite their prior history. Earnings, growth and other measures of a stock’s quality can be adversely affected by market, regulatory, political, environmental and other factors. The price of a stock also may be affected by factors other than those factors considered by the underlying index sponsor. The degree to which these factors affect a stock’s

S-11

performance can be difficult to predict.

Risks related to the iShares® MSCI USA Size Factor ETF

Low Size Risk

The iShares® MSCI USA Size Factor ETF tracks an underlying index that is designed to select equity securities based on certain investment style factors, including low size. Low size companies are those that are on the smaller end of the market capitalization range of securities in the MSCI USA Index. Low size is not a capitalization range similar to large, mid- and small capitalization companies, but rather a factor score determined by a security’s relative position within the market capitalization range of the MSCI USA Index.

Low size companies may be more volatile than those of larger companies, and therefore, the iShares® MSCI USA Size Factor ETF’s share price may be more volatile than those of funds that invest a larger percentage of their assets in stocks issued by larger capitalization companies. Stock prices of low size companies are more vulnerable to adverse business and economic developments. Securities of low size companies may be thinly traded, making it difficult for the iShares® MSCI USA Size Factor ETF to buy and sell them. In addition, low size companies may be less financially stable than larger, more established companies and may depend on a small number of essential personnel, making these companies more vulnerable to experiencing adverse effects due to the loss of personnel. Low size companies also may have less diverse product lines than those of larger capitalization companies and are more susceptible to adverse developments concerning their products.

Risks related to the iShares® MSCI USA Min Vol Factor ETF

Volatility Risk

The value of the securities in the iShares® MSCI USA Min Vol Factor ETF’s portfolio may fluctuate, sometimes rapidly and unpredictably. The value of a security may fluctuate due to factors affecting markets generally or particular industries. This volatility may affect the iShares® MSCI USA Min Vol Factor ETF’s net asset value. Although the underlying index was created by the underlying index sponsor to seek lower volatility than the MSCI USA Index, and the iShares® MSCI USA Min Vol Factor ETF’s name reflects the name of the underlying index as provided by the underlying index sponsor, there is no guarantee that the underlying index sponsor will be successful in creating an underlying index that minimizes volatility, and there is a risk that the iShares® MSCI USA Min Vol Factor ETF may experience more than minimum volatility. Securities in the iShares® MSCI USA Min Vol Factor ETF’s portfolio may be subject to price volatility, and their prices may not be any less volatile than the market as a whole, and could be more volatile. Events or financial circumstances affecting individual securities or sectors may increase the volatility of the iShares® MSCI USA Min Vol Factor ETF.

Risks related to the iShares® MSCI USA Value Factor ETF

Value Risk

The iShares® MSCI USA Value Factor ETF tracks an underlying index that is designed to measure the performance of securities in the MSCI USA Index that, in the aggregate, have value characteristics and relatively lower valuations relative to the large- and mid-cap U.S. equity market. Value securities are those issued by companies that may be perceived as undervalued. Value securities may fail to appreciate for long periods of time and may never realize their full potential value. The underlying index sponsor may be unsuccessful in creating an underlying index that emphasizes undervalued securities. Value securities have generally performed better than non-value securities during periods of economic recovery (although there is no assurance that they will continue to do so). Value securities may go in and out of favor over time.

Risks related to ETFs holding U.S. government debt securities

Your Investment is Subject to Concentration Risks

Certain of the ETFs invest in U.S. Treasury bonds that are all obligations of the United States, including the iShares® 1-3 Year Treasury Bond ETF, the iShares® 7-10 Year Treasury Bond ETF and the iShares® 20+ Year Treasury Bond ETF. In addition, the iShares® 20+ Year Treasury Bond ETF invests in securities with a similar remaining time to maturity. As a result, these ETFs are concentrated in the performance of bonds issued by a single issuer and having the same general tenor and terms. Although your investment in the notes will not result in the ownership or other direct interest in the U.S. Treasury bonds held by any ETF, the return on your investment in the notes will be subject to certain risks similar to those associated with direct investment in a U.S. Treasury bonds. This increases the risk that any downgrade of the credit ratings of the U.S. government from its current ratings, any increase in risk that the U.S. Treasury may default on its obligations by the market (whether for credit or legislative process reasons) or any other market events that create a

S-12

decrease in demand for U.S. Treasury bonds would significantly adversely affect such ETFs and may adversely affect the level of the index. In addition, to the extent that any such decrease in demand is more concentrated in particular U.S. Treasury bond maturities, the ETFs that are concentrated in those maturities could be severely affected, which may adversely affect the level of the index.

ETFs Holding U.S. Government Bonds May Change in Unexpected Ways

The indexes to which ETFs holding U.S. Treasury bonds tend to be linked tend to have very limited public disclosure about the underlying indexes. The index sponsors of these indexes retain discretion to make changes to the indexes at any time. The lack of detailed information about the indexes and how their constituents may change in the future creates the risk that the indexes could change in the future to perform much differently from the way they would perform if such changes were not made. If the indexes are changed in unexpected ways, the ETFs holding such bonds would similarly change to better reflect the indexes. The performance of the ETFs holding such bonds could be adversely affected in that case, which could adversely affect your investment in the notes.

Risks related to ETFs holding debt securities

Your Investment is Subject to Income Risk and Interest Rate Risk

The income of ETFs that invest in debt securities, or “bonds,” may decline when interest rates fall. This decline can occur because the ETF must invest in lower-yielding bonds as bonds in its portfolio fall outside the time to maturity limits required by the ETF’s investment objective or are called, bonds in the underlying index are substituted or the ETF otherwise needs to purchase additional bonds. In addition, an increase in interest rates may cause the value of the fixed rate bonds held by an ETF to decrease, may lead to heightened volatility in the fixed income markets and may adversely affect the liquidity of certain fixed income bonds. Securities with longer durations tend to be more sensitive to interest rate changes, usually making them more volatile than securities with shorter durations. If any of these events occur, the shares of the ETFs invested in bonds and the level of the index could be adversely affected.

Risks related to the iShares® 1-3 Year Treasury Bond ETF

The iShares® 1-3 Year Treasury Bond ETF Previously Changed the Index it Tracks

The iShares® 1-3 Year Treasury Bond ETF will generally invest in the securities included in the index it tracks, but may invest in cash, cash equivalents and other securities not included in the index. Previously, the iShares® 1-3 Year Treasury Bond ETF tracked the Barclays U.S. 1-3 Year Treasury Bond Index, but, beginning on April 1, 2016, the iShares® 1-3 Year Treasury Bond ETF began tracking the ICE U.S. Treasury 1-3 Year Bond Index. Any historical performance of the iShares® 1-3 Year Treasury Bond ETF for any period before April 1, 2016 was during a period in which the iShares® 1-3 Year Treasury Bond ETF tracked a different index, and therefore should not be considered information relevant to how the iShares® 1-3 Year Treasury Bond ETF will perform as it tracks the ICE U.S. Treasury 1-3 Year Bond Index.

The Index Which the iShares® 1-3 Year Treasury Bond ETF Tracks Is a Relatively New Index With a Limited Historical Track Record

The ICE U.S. Treasury 1-3 Year Bond Index was launched on December 31, 2015. The index sponsor of the ICE U.S. Treasury 1-3 Year Bond Index has published hypothetical historical information regarding the historical performance of ICE U.S. Treasury 1-3 Year Bond Index prior to December 31, 2015. Because the ICE U.S. Treasury 1-3 Year Bond Index was not published during those periods, these levels should not be relied upon when making your investment decision.

Risks related to the iShares® 7-10 Year Treasury Bond ETF

The iShares® 7-10 Year Treasury Bond ETF Previously Changed the Index it Tracks

The iShares® 7-10 Year Treasury Bond ETF will generally invest in the securities included in the index it tracks, but may invest in cash, cash equivalents and other securities not included in the index. Previously, the iShares® 7-10 Year Treasury Bond ETF tracked the Barclays U.S. 7-10 Year Treasury Bond Index, but, beginning on April 1, 2016, the iShares® 7-10 Year Treasury Bond ETF began tracking the ICE U.S. Treasury 7-10 Year Bond Index. Any historical performance of the iShares® 7-10 Year Treasury Bond ETF for any period before April 1, 2016 was during a period in which the iShares® 7-10 Year Treasury Bond ETF tracked a different index, and therefore should not be considered information relevant to how the iShares® 7-10 Year Treasury Bond ETF will perform as it tracks the ICE U.S. Treasury 7-10 Year Bond Index.

The Index Which the iShares® 7-10 Year Treasury Bond ETF Tracks Is a Relatively New Index With a Limited Historical Track Record

The ICE U.S. Treasury 7-10 Year Bond Index was launched on December 31, 2015. The index sponsor of the ICE U.S. Treasury 7-10 Year Bond Index has published hypothetical historical information regarding the historical performance of

S-13

ICE U.S. Treasury 7-10 Year Bond Index prior to December 31, 2015. Because the ICE U.S. Treasury 7-10 Year Bond Index was not published during those periods, these levels should not be relied upon when making your investment decision.

Risks related to the iShares® 20+ Year Treasury Bond ETF

The iShares® 20+ Year Treasury Bond ETF Previously Changed the Index it Tracks

The iShares® 20+ Year Treasury Bond ETF will generally invest in the securities included in the index it tracks, but may invest in cash, cash equivalents and other securities not included in the index. Previously, the iShares® 20+ Year Treasury Bond ETF tracked the Barclays U.S. 20+ Year Treasury Bond Index, but, beginning on April 1, 2016, the iShares® 20+ Year Treasury Bond ETF began tracking the ICE U.S. Treasury 20+ Year Bond Index. Any historical information about the performance of the iShares® 20+ Year Treasury Bond ETF for any period before April 1, 2016 was during a period in which the iShares® 20+ Year Treasury Bond ETF tracked a different index, and therefore should not be considered information relevant to how the iShares® 20+ Year Treasury Bond ETF will perform as it tracks the ICE U.S. Treasury 20+ Year Bond Index.

The Index Which the iShares® 20+ Year Treasury Bond ETF Tracks Is a Relatively New Index With a Limited Historical Track Record

The ICE U.S. Treasury 20+ Year Bond Index was launched on December 31, 2015. The index sponsor of the ICE U.S. Treasury 20+ Year Bond Index has published hypothetical historical information regarding the historical performance of ICE U.S. Treasury 20+ Year Bond Index prior to December 31, 2015. Because the ICE U.S. Treasury 20+ Year Bond Index was not published during those periods, these levels should not be relied upon when making your investment decision.

S-14

THE UNDERLYING ASSETS

The defined terms provided in the description of each underlying asset apply only in the description in which they are used. Unless otherwise indicated, these definitions are not intended to be used in other sections of this index supplement.

The underlying asset descriptions below are provided in the following order:

|

ASSET CLASS |

ASSET CLASS MINIMUM WEIGHT |

ASSET CLASS MAXIMUM |

UNDERLYING |

TICKER |

|

Equities |

0% |

100% |

iShares® MSCI USA Momentum Factor ETF |

MTUM |

|

iShares® MSCI USA Size Factor ETF |

SIZE |

|||

|

iShares® MSCI USA Quality Factor ETF |

QUAL |

|||

|

iShares® MSCI USA Value Factor ETF |

VLUE |

|||

|

iShares® MSCI USA Min Vol Factor ETF |

USMV |

|||

|

Fixed Income |

0% |

100% |

iShares® 1-3 Year Treasury Bond ETF |

SHY |

|

iShares® 7-10 Year Treasury Bond ETF |

IEF |

|||

|

iShares® 20+ Year Treasury Bond ETF |

TLT |

|||

|

Cash Constituent |

0% |

100% |

Notional Interest Rate (3-month USD LIBOR) |

N/A |

Some Common Concepts

Each description of an ETF provides information about the particular structure (type of entity) of that ETF. Each of the ETFs files information with the SEC. Information provided to or filed with the SEC can be inspected and copied at the public reference facilities maintained by the SEC or through the SEC’s website at sec.gov. The descriptions below will provide the “CIK number” for each of the ETFs, which is an identifying number that will assist you in finding information about the ETFs filed with the SEC.

Each of the ETFs also has certain concepts in common with most or all of the other ETFs. We have described some of these common concepts below.

Investment Objective

The investment objective of most ETFs is to achieve investment results that correspond generally to the price and yield performance, before fees and expenses, of a particular index. That type of ETF, sometimes called a “tracking ETF,” uses a passive or indexing approach to try to achieve the ETF’s investment objective. The investment advisor to the ETF does not try to beat the index; the ETF tracks and does not seek temporary defensive positions when markets decline or appear overvalued. This means, among other things, that a tracking ETF typically will not sell a particular holding just because it is performing poorly. Instead, the ETF seeks to track the index regardless of whether the index level is increasing or decreasing. The descriptions below will indicate the investment objective of each ETF and will indicate which index a particular ETF tracks if it is a tracking ETF. The description also will state how much of the ETF’s assets generally will be invested in the securities in the index and what else the ETF may invest in. The descriptions also will state the strategy the investment advisor uses to track the index.

The ETFs that track an equity index seek to track the performance of the “total return” version of such index. A total return index represents the total return earned in a portfolio that tracks the price return index and reinvests dividend income in the overall index, not in the specific stock paying the dividend. The difference between the price return calculation and the total return calculation of an index is that, with respect to the price return calculation, changes in the index level reflect changes in stock prices, whereas with respect to the total return calculation of the index, changes in the index level reflect both movements in stock prices and the reinvestment of dividend income. In addition, some of the ETFs track an index that is calculated on a net daily total return basis, which tracks the price return index and reinvests dividend income in the overall index, except that the dividend income is reinvested net of certain withholding taxes. Notwithstanding an ETF’s investment objective to track the performance of the total return version of an index, the return on your notes will not reflect any dividends paid on the ETF shares, on the securities purchased by the ETF or on the securities that comprise the index such ETF tracks. See “Additional Risk Factors Specific to Your Notes — You Have No Shareholder Rights or Rights to Receive Any Shares or Units of Any ETF, or Any Assets Held by Any ETF or the Cash Constituent” in the applicable pricing supplement.

Tracking Error

In the case of a tracking ETF, as described above, the difference between the performance of the ETF over a period of time and the performance of the index over such period of time is called the “tracking error” over that period of time. This is typically measured as the difference between the ETF’s returns and the index returns over the same period of time. This is also sometimes referred to as the “correlation” between the index and the tracking ETF. An index and ETF are

S-15

perfectly correlated if the correlation is 1.00 (i.e., the tracking error is 0.00%). Tracking errors can result for a variety of reasons, but one of the common reasons is that an index is a theoretical financial calculation of the performance of certain assets, but an ETF holds an actual investment portfolio. The descriptions below will discuss some of the additional reasons for tracking errors in the ETFs. The ETFs provide information about the performance of the index and the performance of the ETF for the same period. In some cases, the ETFs assume reinvestment of share distributions when calculating the performance of the market price of the shares.

Creation Units

Prior to trading in the secondary market, shares of an ETF are issued at net asset value to certain institutional investors (typically market makers or other broker-dealers) only in large block-size units, known as creation units. As a practical matter, only institutions, market makers or large investors purchase or redeem creation units. Except when aggregated in creation units (or upon the liquidation of the ETF), shares of an ETF are not redeemable securities. The descriptions below will describe the size of the creation units for each ETF. For most investors, the important thing to know is that redemptions of creation units may cause temporary dislocations in tracking errors for tracking ETFs.

Investment Advisor

Each of the ETFs has an investment advisor. Depending on the structure of the ETF, there may be other key roles with respect to that ETF. Those roles and the entities that perform them will be described below.

Net Asset Value and Share Prices

Each of the ETFs calculates a net asset value, or NAV, at the end of each trading day. This value represents the value of the ETF’s assets less any applicable fees and expenses. The actual trading price of an ETF’s shares or units in the secondary market generally differs (and may deviate significantly during periods of market volatility) from the ETF’s daily net asset value. This is because the trading price is affected by market forces such as supply and demand, economic conditions and other factors. For purposes of your notes and the index, the trading prices of the shares or units of the ETFs included in the calculation of the index will be based on the trading prices alone and not the NAV or any indicative values.

S-16

iShares® MSCI USA Momentum Factor ETF

The shares of the iShares® MSCI USA Momentum Factor ETF (the “ETF”) are issued by iShares® Trust, a registered investment company.

|

• |

The ETF is a tracking ETF that seeks investment results which correspond generally to the price and yield performance, before fees and expenses, of the MSCI USA Momentum SR Variant Index (the “index”). Prior to November 23, 2020, the ETF tracked the MSCI USA Momentum Index. |

|

• |

The ETF’s investment advisor is BlackRock Fund Advisors (“BFA”). |

|

• |

The ETF’s shares trade on the Cboe BZX under the ticker symbol “MTUM”. |

|

• |

The iShares® Trust’s SEC CIK Number is 0001100663. |

|

• |

The ETF’s inception date was April 16, 2013. |

|

• |

The ETF’s shares are issued or redeemed only in creation units of 50,000 shares or multiples thereof. |

Effective August 17, 2020, the name of the ETF changed from the iShares® Edge MSCI USA Momentum Factor ETF to the iShares® MSCI USA Momentum Factor ETF.

We obtained the following fee information from the iShares® website without independent verification. The investment advisor is paid a management fee from the ETF based on a percentage of the ETF’s average daily net assets, at the annual rate of 0.15%. BFA may from time to time voluntarily waive and/or reimburse fees or expenses in order to limit total annual ETF operating expenses (excluding acquired fund fees and expenses, if any). Any such voluntary waiver or reimbursement may be eliminated by BFA at any time. As of September 30, 2020, the aggregate expense ratio of the ETF was 0.15% per annum.

For additional information regarding iShares® Trust or BFA, please consult the reports (including the Annual Report to Shareholders on Form N-CSR for the fiscal year ended July 31, 2020) and other information iShares® Trust files with the SEC. In addition, information regarding the ETF, including its top portfolio holdings, may be obtained from other sources including, but not limited to, press releases, newspaper articles, other publicly available documents, and the iShares® website at us.ishares.com/product_info/fund/overview/MTUM.htm. We are not incorporating by reference the website, the sources listed above or any material they include in this index supplement.

Investment Objective

The ETF seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the index. The ETF’s investment objective and the index may be changed without the approval of BFA’s shareholders.

The following table displays the top holdings and weightings by industry sector of the ETF. (Sector designations are determined by the ETF sponsor using criteria it has selected or developed. Index and ETF sponsors may use very different standards for determining sector designations. In addition, many companies operate in a number of sectors, but are listed in only one sector and the basis on which that sector is selected may also differ. As a result, sector comparisons between indices or ETFs with different sponsors may reflect differences in methodology as well as actual differences in the sector composition of the indices or ETFs.) We obtained the information in the tables below from the ETF website without independent verification.

S-17

iShares® MSCI USA Momentum Factor ETF Top Ten Holdings as of November 12, 2020

|

ETF Stock Issuer |

Percentage (%) |

|

APPLE INC |

6.21% |

|

TESLA INC |

6.10% |

|

AMAZON COM INC |

5.18% |

|

MICROSOFT CORP |

4.78% |

|

NVIDIA CORP |

4.59% |

|

JOHNSON & JOHNSON |

3.80% |

|

UNITEDHEALTH GROUP INC |

3.52% |

|

ADOBE INC |

2.93% |

|

ALPHABET INC CLASS C |

2.65% |

|

ALPHABET INC CLASS A |

2.54% |

|

Total |

42.30% |

iShares® MSCI USA Momentum Factor ETF Weighting by Sector as of November 12, 2020*

|

Sector |

Percentage (%) |

|

Information Technology |

32.09% |

|

Health Care |

29.22% |

|

Communication |

10.92% |

|

Industrials |

1.32% |

|

Consumer Discretionary |

13.49% |

|

Financials |

3.37% |

|

Utilities |

1.43% |

|

Consumer Staples |

3.22% |

|

Materials |

1.06% |

|

Real Estate |

3.72% |

|

Cash and/or Derivatives |

0.16% |

|

Total |

100.00% |

* Percentages may not sum to 100% due to rounding.

Representative Sampling

BFA uses a representative sampling indexing strategy to manage the ETF. This strategy involves investing in a representative sample of securities that collectively has an investment profile similar to that of the index. The securities selected are expected to have, in the aggregate, investment characteristics (based on factors such as market capitalization and industry weightings), fundamental characteristics (such as return variability and yield) and liquidity measures similar to those of the index.

The ETF generally will invest at least 90% of its assets in the component securities of the index and may invest up to 10% of its assets in certain futures, options and swap contracts, cash and cash equivalents, including shares of money market funds advised by BFA or its affiliates, as well as in securities not included in the index, but which BFA believes will help the ETF track the index. The ETF may temporarily invest a lesser amount in the component securities of the index outside of normal circumstances, such as when the index rebalances during periods of high volatility in the markets for the component securities. Also, the ETF may lend securities representing up to one-third of the value of the ETF’s total assets (including the value of the collateral received).

Tracking Error

The performance of the ETF and the index may vary due to a variety of factors, including differences between the securities and other instruments held in the ETF’s portfolio and those included in the index, pricing differences, transaction costs incurred by the ETF, the ETF’s holding of uninvested cash, differences in timing of the accrual of or the valuation of dividends or interest, the requirements to maintain pass-through tax treatment, portfolio transactions carried out to minimize the distribution of capital gains to shareholders, acceptance of custom baskets, changes to the index or the costs to the ETF of complying with various new or existing regulatory requirements. Tracking error also may result because the ETF incurs fees and expenses, while the index does not. BFA expects that, over time, the ETF’s tracking error will not exceed 5%. The ETF’s use of a representative sampling indexing strategy can be expected to produce a larger tracking error than would result if the ETF used a replication indexing strategy in which an ETF invests in substantially all of the securities in its index in approximately the same proportions as in the index.

S-18

As of October 31, 2020, iShares® reported the following average annual returns on the market price of the ETF’s shares and the MSCI USA Momentum Index. The market price of the ETF’s shares takes into account distributions on the shares and the returns shown account for changes in the mid-point of the bid and ask prices at 4:00 p.m., Eastern time on the relevant date. ETF shares: 1 year, 19.25 %; 3 years, 13.49%; 5 years, 15.55%; since inception, 15.72 %; MSCI USA Momentum Index: 1 year, 19.46%; 3 years, 13.76%; 5 years, 15.80%; since ETF inception, 15.97%.

Industry Concentration Policy

The ETF will concentrate its investments (i.e., hold 25% or more of its total assets) in a particular industry or group of industries to approximately the same extent that the index is concentrated.

The MSCI USA Momentum SR Variant Index

The MSCI USA Momentum SR Variant Index aims to reflect the performance of the MSCI USA Momentum Index (for purposes of the descriptions of the MSCI USA Momentum SR Variant Index, the “reference index”), except that the MSCI USA Momentum SR Variant Index is rebalanced by staggering changes in the number of security shares due to rebalancing in equal proportion over three business days ending on the effective date of the reference index rebalancing, whereas the reference index implements the entire rebalancing on the effective date. Please read “Additional Risk Factors Specific to the ETFs—Risks related to the iShares® MSCI USA Momentum Factor ETF – The iShares® MSCI USA Momentum Factor ETF Recently Changed the Index it Tracks” on S-11. For more information about the reference index, see “The MSCI USA Momentum Index” below.

The MSCI USA Momentum SR Variant Index is calculated, published and disseminated daily by MSCI through numerous data vendors, on the MSCI website and in real time on Bloomberg Financial Markets and Reuters Limited. The MSCI USA Momentum SR Variant Index was launched on May 19, 2020. Additional information about the MSCI USA Momentum SR Variant Index is available on the following website: msci.com/index-methodology. We are not incorporating by reference the website, the sources listed above or any material they include in this index supplement.

Rebalancing of the MSCI USA Momentum SR Variant Index

The MSCI USA Momentum SR Variant Index is rebalanced by staggering the changes in the number of shares of securities due to rebalancing in equal proportions over three days: T-2, T-1 and T (where “T” is the effective date of the rebalancing of the reference index, T-1 is the preceding business day, and T-2 is the second preceding business day). In case any of the three consecutive business days ending in business day T is preceded by a scheduled exchange holiday (any day on which any exchange on which any security in the MSCI USA Momentum SR Variant Index is listed has a trading holiday (either full or partial)), the start date of the staggering will be advanced to ensure that the implementation continues to be staggered over three business days (which may be non-consecutive), none of which are preceded by a scheduled exchange holiday. The pro forma MSCI USA Momentum SR Variant Index in general is announced nine business days before T (T-9), where T is the effective date of the rebalancing of the reference index.

Other than with respect to the staggered implementation of rebalancings, the MSCI USA Momentum SR Variant Index generally follows the rebalancing schedule of the reference index. The reference index’s scheduled rebalancings occur semi-annually, usually as of the close of the last business day of May and November, coinciding with the May and November semi-annual index review of the reference index (which reference index rebalancing day would serve as the reference date for the staggered rebalancing of the MSCI USA Momentum SR Variant Index, as described below). In addition, the MSCI USA Momentum SR Variant Index generally will be subject to ad-hoc rebalancing if a trigger condition for an ad-hoc rebalancing of the reference index is satisfied, but such ad-hoc rebalancing will also be implemented on a staggered basis (i.e., over three business days). For more information about the rebalancing schedule and trigger conditions for ad-hoc rebalancings of the reference index, see “The MSCI USA Momentum Index—Maintenance of the MSCI USA Momentum Index” below.

For each day of staggering, the number of shares for each security included in the MSCI USA Momentum SR Variant Index equals the sum of (i) the number of shares of such security in the reference index effective on the particular date of staggering plus (ii) the product of (a) the difference between the targeted number of shares of such security that will be in the reference index on the effective date of the reference index’s rebalancing date (T), adjusted for changes to the overall number of shares due to corporate events (spinoffs, mergers, etc.), minus the actual number of shares of such security in the reference index on the particular date of staggering multiplied by (b) the quotient of N divided 3, where N is the nth day of staggering (e.g., t-2 is the first day of staggering). The number of shares of a security in the reference index effective on a particular date of staggering is calculated as the product of the end of day number of shares of the security as of the close of trading on the prior business day as adjusted for certain corporate events as described in “The MSCI USA Momentum Index—Maintenance of the MSCI USA Momentum Index—Corporate Events” below.

S-19

Maintenance of the MSCI USA Momentum SR Variant Index

Except as otherwise specified below, the MSCI USA Momentum SR Variant Index is generally maintained on the same basis as the reference index.

Corporate Events

Corporate event treatment for the MSCI USA Momentum SR Variant Index depends on whether the effective date of the event falls within the staggering period (T-2, T-1, T), or outside the staggering period.

The general treatment of corporate events effective outside the staggering period in the MSCI USA Momentum SR Variant Index aims to minimize turnover outside of index reviews. The methodology aims to appropriately represent an investor’s participation in an event based on relevant deal terms and pre-event weighting of the index constituents that are involved. Further, changes in index market capitalization that occur as a result of corporate event implementation will be offset by a corresponding change in the variable weighting factor of the constituent. Additionally, if the frequency of index reviews in the MSCI USA Index is greater than the frequency of index reviews in the MSCI USA Momentum SR Variant Index, the changes made to the MSCI USA Index during intermediate index reviews will be neutralized in the MSCI USA Momentum SR Variant Index.

For more information about the treatment of common corporate events, see “The MSCI USA Momentum Index— Maintenance of the MSCI USA Momentum Index—Corporate Events” below. No new securities will be added (except where noted below in “The MSCI USA Momentum Index— Maintenance of the MSCI USA Momentum Index—Corporate Events”) to the MSCI USA Momentum SR Variant Index outside of the staggering period. MSCI USA Index deletions will be reflected simultaneously in the MSCI USA Momentum SR Variant Index.

Events effective in MSCI USA Momentum SR Variant Index during the staggering period incorporate the event implementation in the reference index. The impact of an event on the MSCI USA Momentum SR Variant Index depends on the type of event and calculation date of the index.

The MSCI USA Momentum Index

The MSCI USA Momentum Index is designed to measure the performance of an equity momentum strategy by emphasizing stocks with high price momentum, while maintaining reasonably high trading liquidity and investment capacity and moderate index turnover, each as determined by MSCI Inc. (“MSCI”). The MSCI USA Momentum Index’s constituent stocks exhibit relatively higher momentum characteristics than its traditional market capitalization weighted parent index, the MSCI USA Index. The MSCI USA Index includes U.S. large- and mid-capitalization stocks, as defined by MSCI. For more information about the MSCI USA Index, see “The MSCI USA Index” below.

The MSCI USA Momentum Index is calculated, published and disseminated daily by MSCI through numerous data vendors, on the MSCI website and in real time on Bloomberg Financial Markets and Reuters Limited. The MSCI USA Momentum Index was launched on February 15, 2013. Additional information about the MSCI USA Momentum Index is available on the following website: msci.com/index-methodology. We are not incorporating by reference the website, the sources listed above or any material they include in this index supplement.

Construction of the MSCI USA Momentum Index

The MSCI USA Momentum Index selects a predetermined number of constituent securities with the highest risk-adjusted price momentum from the MSCI USA Index. With respect to a security, MSCI defines risk-adjusted price momentum as (i) the excess return over 6- and 12-month time periods over the risk-free rate divided by (ii) the annualized standard deviation of weekly returns over the past three years. The 6- and 12-month risk-adjusted price momentum calculations are then capped/floored at +/-3 standard deviations and translated into an average momentum score. MSCI uses an algorithm to determine the number of constituent securities to be selected from the MSCI USA Index for inclusion in the MSCI USA Momentum Index with an aim to attain a high exposure to the momentum factor while maintaining sufficient market capitalization and number of securities coverage. The number of components is evaluated semi-annually. The weight of each constituent security in the MSCI USA Momentum Index is determined based on the product of the constituent security’s momentum score and its market capitalization weight in the MSCI USA Index, as further adjusted to, among others, mitigate the impact of stock-specific risk. Additionally, each individual constituent security is capped at 5%.

MSCI USA Momentum Index rebalancings occur semi-annually, usually as of the close of the last business day of May and November, coinciding with the May and November semi-annual index review of the MSCI USA Index. The pro forma Momentum Indexes are in general announced nine business days before the effective date.

Calculate Momentum Values

In order to calculate the momentum score for each security in the MSCI USA Index, the first step is to calculate the 6-month price momentum and the 12-month price momentum on the rebalancing date for that security as follows:

S-20

|

• |

“12-month price momentum” equals (i) the quotient of (a) the price of the security one month prior to the rebalancing date divided by (b) the price of the security 13 months prior to the rebalancing date, minus (ii) 1, minus (iii) the 3-month treasury bill rate on the rebalancing date |

If the 12-month price momentum is not available, only the 6-month price momentum is used to calculate the momentum score. However, if the 6-month price momentum is not available on the rebalancing date, the momentum score will not be calculated and the security is not eligible for inclusion in the MSCI USA Momentum Index.

Calculate Risk-Adjusted Momentum Value

Second, for each security, the 6-month price momentum is used to calculate the 6-month risk-adjusted price momentum, and the 12-month price momentum is used to calculate the 12-month risk-adjusted price momentum, as follows:

|

• |

“6-month risk-adjusted price momentum” equals (i) 6-month risk-adjusted price momentum divided by (ii) the annualized standard deviation of weekly USD price returns over the preceding three years |

|

• |

“12-month risk-adjusted price momentum” equals (i) 12-month risk-adjusted price momentum divided by (ii) the annualized standard deviation of weekly USD price returns over the preceding three years |

Calculate Z-Scores

Third, for each security, the 6-month risk-adjusted price momentum and the 12-month risk-adjusted price momentum are standardized into z-scores as follows:

|

• |

“6-month momentum z-score” equals the number of standard deviations the 6-month risk-adjusted price momentum is from the average 6-month risk-adjusted price momentum for all of the securities in the MSCI USA Index |

|

• |

“12-month momentum z-score” equals the number of standard deviations the 12-month risk-adjusted price momentum 12-month risk-adjusted price momentum for all of the securities in the MSCI USA Index |

Calculate Momentum Score

Fourth, the 6-month momentum z-score and 12-month momentum z-score are combined in equal proportions to arrive at a single combined momentum z-score as follows:

|

(i) |

if both the 6-month momentum z-score and the 12-month momentum z-score is available, “combined momentum z-score” equals (i) the product of 0.5 times 6-month risk-adjusted price momentum plus (ii) the product of 0.5 times 12-month risk-adjusted price momentum, 9 or |

|

(ii) |

if the 12-month momentum z-score is not available, “combined momentum z-score” equals the 6-month risk-adjusted price momentum. |

Fifth, the combined momentum z-score is then standardized by calculating the standardized momentum z-score. The standardized momentum z-score equals the number of standard deviations the combined momentum z-score is from the average of the combined momentum z-scores for all of the securities in the MSCI USA Index. The standardinzing momentum z-score is then winsorized at +/- 3, i.e., a standardized momentum z-score above 3 is capped at 3 standard deviations and a combined momentum z-score below -3 is floored at -3 standard deviations.

Sixth, the momentum score is then computed from the momentum z-scores as follows:

|

(i) |

If the standardized z-score is greater than or equal to 0, the “momentum score” equals 1 plus the momentum z-score; or |

|

(ii) |

If the momentum z-score is less than 0, the “momentum score” equals the quotient of (i) 1 divided by (ii) the difference of 1 minus the momentum z-score. |

Security Selection

The number of securities targeted for inclusion in the MSCI USA Momentum Index at initial construction and upon each rebalancing is determined based on certain rules relating to free-float market capitalization (market price per share multiplied by the number of shares held by non-controlling interests) and numbers of constituent securities as described below.

S-21

Initial Construction. The number of securities targeted for inclusion in the MSCI USA Momentum Index at initial construction (or on any semi-annual rebalancing when the initial construction methodology is required to be applied, as described below under the caption “—Rebalancing”) is determined by (i) ranking each constituent security in the MSCI USA Index according to its momentum z-score (before applying any cap or floor, and using such securities’ weights in the MSCI USA Index if multiple securities have the same score) and (ii) applying the following rules in order of priority:

|

• |

if the MSCI USA Index has 25 or fewer constituent securities on the relevant date, each constituent security in the MSCI USA Index is included as a constituent security in the MSCI USA Momentum Index; or |

|

• |

if 25 or fewer of the highest ranking MSCI USA Index constituent securities account for at least 30% of the MSCI USA Index’s free-float market capitalization, the target number of MSCI USA Momentum Index constituent securities will be 25, subject to the rounding rules; or |

|

• |

if 25 of the highest ranking MSCI USA Index constituent securities DO NOT account for at least 30% of the MSCI USA Index’s free-float market capitalization, but the top 10% of the highest ranking MSCI USA Index constituent securities DO account for at least 30% of the MSCI USA Index’s free-float market capitalization, the number of constituent securities constituting the top 10% of the highest ranking MSCI USA Index constituent securities, after rounding, is the number of securities targeted for inclusion in the MSCI USA Momentum Index; or |

|

• |

if the number of top ranking MSCI USA Index constituent securities accounting for 30% of the MSCI USA Index’s free-float market capitalization, after rounding, account for less than 40% of the total number of MSCI USA Index constituent securities, such rounded number is the number of securities targeted for inclusion in the MSCI USA Momentum Index; or |

|

• |

if the number of top ranking MSCI USA Index constituent securities accounting for 30% of the MSCI USA Index’s free-float market capitalization, after rounding, account for 40% or more of the total number of MSCI USA Index constituent securities, eliminate each of the lowest ranking MSCI USA Index constituent securities from such rounded number until the number of those remaining account for 40% or less of the total number of MSCI USA Index constituent securities; and |

|

|

o |

if the remaining MSCI USA Index constituent securities account for at least 20% of the MSCI USA Index’s free-float market capitalization, the number of such remaining MSCI USA Index constituent securities, after rounding, is the number of securities targeted for inclusion in the MSCI USA Momentum Index; or |

|

|

o |

if the remaining MSCI USA Index constituent securities account for less than 20% of the MSCI USA Index’s free-float market capitalization, add back the next highest ranking MSCI USA Index constituent securities previously eliminated until the MSCI USA Momentum Index’s constituent securities account for at least 20% of the MSCI USA Index’s free-float market capitalization and such number of MSCI USA Index constituent securities, after rounding, is the number of securities targeted for inclusion in the MSCI USA Momentum Index. |

Where indicated above, the following rounding conventions apply:

|

• |