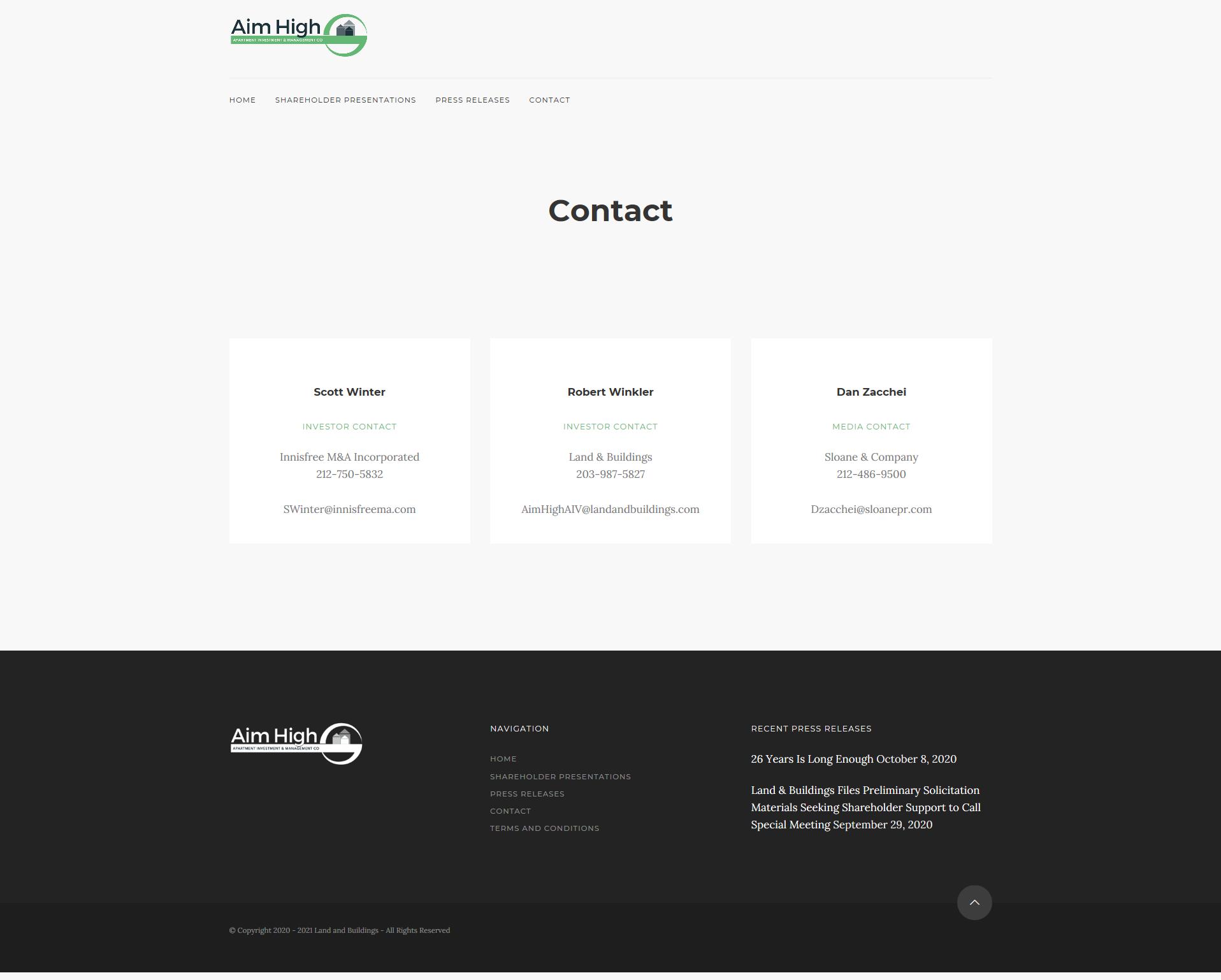

Form DFAN14A APARTMENT INVESTMENT & Filed by: Land & Buildings Investment Management, LLC

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of The Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☐ | Definitive Additional Materials |

| ☒ | Soliciting Material Under Rule 14a-12 |

| Apartment Investment and Management Company |

(Name of Registrant as Specified in Its Charter) |

Land & Buildings Capital Growth Fund, LP L & B Real Estate Opportunity Fund, LP L&B OPPORTUNITY FUND, LLC Land & Buildings GP LP Land & Buildings Investment Management, LLC Jonathan Litt Corey Lorinsky |

(Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ☐ | Fee paid previously with preliminary materials: |

☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Land & Buildings Investment Management, LLC, together with the other participants named herein (collectively, “Land & Buildings”), has made a preliminary filing with the Securities and Exchange Commission (“SEC”) of a solicitation statement and an accompanying GOLD request card to be used to solicit requests for the calling of a special meeting of shareholders of Apartment Investment and Management Company, a Maryland corporation (the “Company” or “Aimco”).

Item 1: On October 8, 2020, Jonathan Litt of Land & Buildings presented at the 13D Monitor Active-Passive Investor Summit, which included a discussion and presentation about the Company and its proposed plan to separate its business into two, separate and distinct, publicly traded companies, Apartment Income REIT and Aimco, through a reverse spin-off. A written transcript of the discussion is included below and a copy of the presentation is attached hereto as Exhibit 99.1 and is incorporated herein by reference.

Transcript

Raymond Ko (Head of Strategic Transactions Group Americas at Societe Generale):

So our next and last speaker is Jon Litt of Land and Buildings. Jon is the Founder of Land and Buildings, which was originally founded in the Summer of 2008 to take advantage of opportunities uncovered by the global property bubble. He has since built Land and Buildings into a prominent activist hedge fund in the real estate space. Prior to the founding of Land and Buildings, Jon has experience as both a sell-side and buy-side analyst having achieved top rankings from Greenwich Associates and is a frequent contributor to CNBC, the Wall Street Journal and other industry publications. Jon, the floor is yours.

Jonathan Litt (Founder and CIO at Land & Buildings):

Great, thanks Raymond. And thank you to the 13D team for having us on and for doing an excellent job in a COVID world of executing this conference. I am here today to talk about Aimco. Aimco is an apartment REIT. Lauren talked a bit about the excellent fundamentals in the apartment industry. And this is a company in which I have been involved with since its IPO in 1994. It certainly says that I’m old. But you know what, 26 years is long enough. This company has underperformed for 26 years and we will explain more inside. We think there is 75% upside to the stock from its current share price and we think in the next 12 to 24 months shareholders should be able to earn that upside.

Specifically, we are here today because Aimco in September proposed a transaction in which they are spinning off 90% of the apartments the company owns into a new entity in a taxable transaction. They've cleverly gone through the Maryland laws to figure out a way to do this without seeking shareholder approval. We have asked them to seek shareholder approval and they have refused. We have filed with the SEC materials to call a special meeting so that we can have an advisory vote on the merits of this spin.

The company says their net asset value is $58. That is 75% above current price. We don't take issue with this, we agree, but not only do we agree as recently as yesterday, Blackstone, KKR and Starwood were at a conference and they stated that apartments are at the top of their shopping list. Starwood said there's wild bidding for apartments. They went on to say that the value of apartments is up from pre COVID levels. Blackstone gave an example. If they put an asset on the market in Phoenix, they would have 20 bids and values in excess of pre COVID levels. Blackstone went on to say that today they can finance apartments at the low 2% range with 70 to 75% leverage. KKR said that there is a disconnect between private market valuations and public market valuations of apartments. Blackstone during the COVID sell off bought 11 REITs in the public markets. They have sold six and they own five today. Three of them are apartments. One of them is Aimco. Aimco would be a Scooby Snack for Blackstone. There is little doubt in my mind of Blackstone and the other private equity players have a serious interest in acquiring a company such as Aimco. It lines up consistently with their portfolios and they clearly have the cash to do it.

It is also with little doubt in my mind that the Chairman and CEO of this company has made it clear to its advisors that they are not interested in selling. Instead, they are going to do this transaction, which is going to destroy shareholder value as they outlined in their own materials and cause investors to incur a material tax while the Chairman and CEO ownership in this company is in a different class of securities, which will not incur that tax.

This company has persistently and consistently underperformed in the public markets. For 26 years, for one year for three years and five years. This spin that they are proposing creates significant conflicts of interest with the Chairman and CEO and shareholders. Post spin he will own interests in this company that will create a situation where he does not want to sell assets, but where shareholders may want to see assets sold. He does not want to sell it because of his tax consequences. Furthermore, he will now be Chairman and CEO of both companies, double-dipping on compensation and likely we will see his options re-written on a tax-favorable will basis in Newco.

We believe this long tenured board is out of touch with market conditions and it is unlikely the directors considered a sale of the company or change in leadership as options to maximize value for all shareholders.

Why we are here today? We believe that shareholders should have a say in the spin of 90% of the company. We are in the process of calling a special meeting for that advisory vote. The portfolio is well diversified in 17 states, 32,000 class B apartments.

Let's look at the numbers. Terry Considine, the Chairman and CEO, has been there since its IPO 26 years ago - the company has underperformed its proxy peers by 907%. In the last one, three and five years it has underperformed. But it gets worse. Their Proxy Compensation Peers it has underperformed and yet this board has approved $30 million in compensation to Considine the last five years. The company has also underperformed all REITs in a similar timeframe.

Under this Board's leadership, the company has traded at a material discount to NAV the last five years while its competitors have traded at or above net asset value. We know what the value of these assets are. The company sold an interest in properties for a 4% cap rate.

This board is old. Five of the nine directors have been together for 10 years. Both ISS and Green Street have issues with the governance and the board of this company will be the board of the new company.

Do not just take our word for it. Look at what the analytical community is saying. Michael Bilerman downgraded the company to a sell after this deal was announced. He said, it is like trading a quarter for two dimes. I could not say it better. He polled investors and clients asking them if they thought this would add value. 72% said no. They asked shareholders if they want to vote on their transaction. 90% said yes. This company is not a case of good-co and bad-co it is a case of bad-co and worse-co.

The company is deliberately delaying our special meeting requests in order to stifle shareholder voices by delaying the record date to November 4th. And what is the rush? They announced this deal in September. Are they trying to avoid having this go to a shareholder vote at its annual meeting?

In closing, this spin could destroy value as they themselves have disclosed in their materials. We think this needs to be put to a vote and we believe that they should evaluate all strategical alternatives, including a sale of the company and a change in leadership. The value of this company is 75% above where the shares are trading today and we believe that should be achieved in the next 12 to 24 months. Thank you.

Item 2: Also on October 8, 2020, Land & Buildings posted the following materials to https://aimhighaiv.com/: