Form 10-Q On Deck Capital, Inc. For: Jun 30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(MARK ONE)

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2019

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number 001-36779

On Deck Capital, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 42-1709682 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1400 Broadway, 25th Floor

New York, New York 10018

(Address of principal executive offices)

(888) 269-4246

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock, par value $0.005 per share | ONDK | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ý NO ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data file required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). YES ý NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.:

Large accelerated filer | ¨ | Accelerated filer | x | |||

Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Emerging growth company | x | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | x | |||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO ý

The number of shares of the registrant’s common stock outstanding as of July 31, 2019 was 76,301,387.

On Deck Capital, Inc.

Table of Contents

Page | ||

PART I - FINANCIAL INFORMATION | ||

Item 1. | Financial Statements (Unaudited) | |

Unaudited Condensed Consolidated Balance Sheets | ||

Unaudited Condensed Consolidated Statements of Operations and Comprehensive Income | ||

Unaudited Condensed Consolidated Statements of Changes in Equity and Redeemable Noncontrolling Interest | ||

Unaudited Condensed Consolidated Statements of Cash Flows | ||

Notes to Unaudited Condensed Consolidated Financial Statements | ||

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | |

Item 4. | Controls and Procedures | |

PART II - OTHER INFORMATION | ||

Item 1. | Legal Proceedings | |

Item 1A | Risk Factors | |

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | |

Item 3. | Defaults Upon Senior Securities | |

Item 4. | Mine Safety Disclosures | |

Item 5. | Other Information | |

Item 6. | Exhibits | |

Signatures | ||

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

ON DECK CAPITAL, INC. AND SUBSIDIARIES

Unaudited Condensed Consolidated Balance Sheets

(in thousands, except share and per share data)

June 30, | December 31, | ||||||

2019 | 2018 | ||||||

Assets | |||||||

Cash and cash equivalents | $ | 58,744 | $ | 59,859 | |||

Restricted cash | 43,336 | 37,779 | |||||

Loans and finance receivables | 1,207,609 | 1,169,407 | |||||

Less: Allowance for credit losses | (145,739 | ) | (140,040 | ) | |||

Loans and finance receivables held for investment, net | 1,061,870 | 1,029,367 | |||||

Property, equipment and software, net | 17,088 | 16,700 | |||||

Other assets | 67,169 | 18,115 | |||||

Total assets | $ | 1,248,207 | $ | 1,161,820 | |||

Liabilities, mezzanine equity and stockholders' equity | |||||||

Liabilities: | |||||||

Accounts payable | $ | 5,819 | $ | 4,011 | |||

Interest payable | 2,687 | 2,385 | |||||

Debt | 841,602 | 816,231 | |||||

Accrued expenses and other liabilities | 65,135 | 36,708 | |||||

Total liabilities | 915,243 | 859,335 | |||||

Commitments and contingencies (Note 12) | |||||||

Mezzanine equity: | |||||||

Redeemable noncontrolling interest | 15,122 | — | |||||

Stockholders’ equity: | |||||||

Common stock—$0.005 par value, 1,000,000,000 shares authorized and 79,338,337 and 78,412,291 shares issued and 76,301,387 and 75,375,341 outstanding at June 30, 2019 and December 31 2018, respectively. | 401 | 396 | |||||

Treasury stock—at cost | (5,656 | ) | (5,656 | ) | |||

Additional paid-in capital | 508,630 | 502,003 | |||||

Accumulated deficit | (186,997 | ) | (196,959 | ) | |||

Accumulated other comprehensive loss | (1,894 | ) | (1,832 | ) | |||

Total On Deck Capital, Inc. stockholders' equity | 314,484 | 297,952 | |||||

Noncontrolling interest | 3,358 | 4,533 | |||||

Total stockholders' equity | 317,842 | 302,485 | |||||

Total liabilities, mezzanine equity and stockholders' equity | $ | 1,248,207 | $ | 1,161,820 | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

3

ON DECK CAPITAL, INC. AND SUBSIDIARIES

Unaudited Condensed Consolidated Statements of Operations and Comprehensive Income

(in thousands, except share and per share data)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2019 | 2018 | 2019 | 2018 | ||||||||||||

Revenue: | |||||||||||||||

Interest and finance income | $ | 105,641 | $ | 92,209 | $ | 211,440 | $ | 178,438 | |||||||

Other revenue | 4,605 | 3,247 | 8,781 | 7,158 | |||||||||||

Gross revenue | 110,246 | 95,456 | 220,221 | 185,596 | |||||||||||

Cost of revenue: | |||||||||||||||

Provision for credit losses | 42,951 | 33,293 | 86,242 | 69,586 | |||||||||||

Interest expense | 11,381 | 12,245 | 22,713 | 24,117 | |||||||||||

Total cost of revenue | 54,332 | 45,538 | 108,955 | 93,703 | |||||||||||

Net revenue | 55,914 | 49,918 | 111,266 | 91,893 | |||||||||||

Operating expense: | |||||||||||||||

Sales and marketing | 13,307 | 11,432 | 25,267 | 22,030 | |||||||||||

Technology and analytics | 16,681 | 12,799 | 33,487 | 23,806 | |||||||||||

Processing and servicing | 5,609 | 5,041 | 11,098 | 10,262 | |||||||||||

General and administrative | 16,353 | 16,034 | 30,382 | 33,759 | |||||||||||

Total operating expense | 51,950 | 45,306 | 100,234 | 89,857 | |||||||||||

Income (loss) from operations, before provision for income taxes | 3,964 | 4,612 | 11,032 | 2,036 | |||||||||||

Provision for income taxes | 1,796 | — | 3,536 | — | |||||||||||

Net income (loss) | 2,168 | 4,612 | 7,496 | 2,036 | |||||||||||

Less: Net income (loss) attributable to noncontrolling interest | (2,127 | ) | (1,016 | ) | (2,465 | ) | (1,535 | ) | |||||||

Net income (loss) attributable to On Deck Capital, Inc. common stockholders | $ | 4,295 | $ | 5,628 | $ | 9,961 | $ | 3,571 | |||||||

Net income (loss) per share attributable to On Deck Capital, Inc. common stockholders: | |||||||||||||||

Basic | $ | 0.06 | $ | 0.08 | $ | 0.13 | $ | 0.05 | |||||||

Diluted | $ | 0.05 | $ | 0.07 | $ | 0.13 | $ | 0.05 | |||||||

Weighted-average common shares outstanding: | |||||||||||||||

Basic | 76,137,751 | 74,385,446 | 75,840,604 | 74,182,929 | |||||||||||

Diluted | 78,901,601 | 78,288,267 | 79,013,757 | 77,786,748 | |||||||||||

Comprehensive income (loss): | |||||||||||||||

Net income (loss) | $ | 2,168 | $ | 4,612 | $ | 7,496 | $ | 2,036 | |||||||

Other comprehensive income (loss): | |||||||||||||||

Unrealized (loss) on derivative instrument | (124 | ) | — | (866 | ) | — | |||||||||

Foreign currency translation adjustment | 405 | (395 | ) | 771 | (508 | ) | |||||||||

Comprehensive income (loss) | 2,449 | 4,217 | 7,401 | 1,528 | |||||||||||

Less: Comprehensive income (loss) attributable to noncontrolling interests | (58 | ) | (179 | ) | (32 | ) | (229 | ) | |||||||

Less: Net income (loss) attributable to noncontrolling interest | (2,127 | ) | (1,016 | ) | (2,465 | ) | (1,535 | ) | |||||||

Comprehensive income (loss) attributable to On Deck Capital, Inc. common stockholders | $ | 4,634 | $ | 5,412 | $ | 9,898 | $ | 3,292 | |||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

ON DECK CAPITAL, INC. AND SUBSIDIARIES

Unaudited Condensed Consolidated Statements of Changes in Equity and Redeemable Noncontrolling Interest

(in thousands, except share data)

On Deck Capital, Inc.'s stockholders' equity | |||||||||||||||||||||||||||||||||||||||

Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Accumulated Other Comprehensive Income (Loss) | Total Stockholders' Equity | Noncontrolling interest | Total Equity | Redeemable Noncontrolling Interest | |||||||||||||||||||||||||||||||

Shares | Amount | ||||||||||||||||||||||||||||||||||||||

Balance at December 31, 2017 | 73,822,001 | $ | 386 | $ | 490,200 | $ | (224,047 | ) | $ | (5,656 | ) | $ | (52 | ) | $ | 260,831 | $ | 4,011 | $ | 264,842 | $ | — | |||||||||||||||||

Stock-based compensation | — | — | 3,122 | — | — | — | 3,122 | — | 3,122 | — | |||||||||||||||||||||||||||||

Issuance of common stock through vesting of restricted stock units and option exercises | 246,130 | 2 | 39 | — | — | — | 41 | — | 41 | — | |||||||||||||||||||||||||||||

Employee stock purchase plan | 196,360 | 1 | 918 | — | — | — | 919 | — | 919 | — | |||||||||||||||||||||||||||||

Tax withholding related to vesting of restricted stock units | — | — | (118 | ) | — | — | — | (118 | ) | — | (118 | ) | — | ||||||||||||||||||||||||||

Currency translation adjustment | — | — | — | — | — | (63 | ) | (63 | ) | (50 | ) | (113 | ) | — | |||||||||||||||||||||||||

Net Income (loss) | — | — | — | (2,058 | ) | — | — | (2,058 | ) | (518 | ) | (2,576 | ) | — | |||||||||||||||||||||||||

Other | — | — | — | (1 | ) | — | (3 | ) | (4 | ) | — | (4 | ) | — | |||||||||||||||||||||||||

Balance-March 31, 2018 | 74,264,491 | $ | 389 | $ | 494,161 | $ | (226,106 | ) | $ | (5,656 | ) | $ | (118 | ) | $ | 262,670 | $ | 3,443 | $ | 266,113 | $ | — | |||||||||||||||||

Stock-based compensation | — | — | 2,712 | — | — | — | $ | 2,712 | — | $ | 2,712 | — | |||||||||||||||||||||||||||

Issuance of common stock through vesting of restricted stock units and option exercises | 376,513 | 2 | (2 | ) | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||

Employee stock purchase plan | — | — | 49 | — | — | — | 49 | — | 49 | — | |||||||||||||||||||||||||||||

Tax withholding related to vesting of restricted stock units | — | — | (323 | ) | — | — | — | (323 | ) | — | (323 | ) | — | ||||||||||||||||||||||||||

Investment by noncontrolling interests | — | — | — | — | — | — | — | 3,402 | 3,402 | — | |||||||||||||||||||||||||||||

Currency translation adjustment | — | — | — | — | — | (216 | ) | (216 | ) | (179 | ) | (395 | ) | — | |||||||||||||||||||||||||

Net Income (loss) | — | — | — | 5,628 | — | — | 5,628 | (1,016 | ) | 4,612 | — | ||||||||||||||||||||||||||||

Balance-June 30, 2018 | 74,641,004 | $ | 391 | $ | 496,597 | $ | (220,478 | ) | $ | (5,656 | ) | $ | (334 | ) | $ | 270,520 | $ | 5,650 | $ | 276,170 | $ | — | |||||||||||||||||

5

On Deck Capital, Inc.'s stockholders' equity | |||||||||||||||||||||||||||||||||||||||

Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Accumulated Other Comprehensive Income (Loss) | Total Stockholders' Equity | Noncontrolling interest | Total Equity | Redeemable Noncontrolling Interest | |||||||||||||||||||||||||||||||

Shares | Amount | ||||||||||||||||||||||||||||||||||||||

Balance at December 31, 2018 | 75,375,341 | $ | 396 | $ | 502,003 | $ | (196,959 | ) | $ | (5,656 | ) | $ | (1,832 | ) | $ | 297,952 | $ | 4,533 | $ | 302,485 | $ | — | |||||||||||||||||

Stock-based compensation | — | — | 2,743 | — | — | — | 2,743 | — | 2,743 | — | |||||||||||||||||||||||||||||

Issuance of common stock through vesting of restricted stock units and option exercises | 264,364 | 2 | 45 | — | — | — | 47 | — | 47 | — | |||||||||||||||||||||||||||||

Employee stock purchase plan | 267,688 | 1 | 1,659 | — | — | — | 1,660 | — | 1,660 | — | |||||||||||||||||||||||||||||

Tax withholding related to vesting of restricted stock units | — | — | (291 | ) | — | — | — | (291 | ) | — | (291 | ) | — | ||||||||||||||||||||||||||

Currency translation adjustment | — | — | — | — | — | 340 | 340 | 26 | 366 | — | |||||||||||||||||||||||||||||

Cash flow hedge | — | — | — | — | — | (742 | ) | (742 | ) | — | (742 | ) | — | ||||||||||||||||||||||||||

Net Income (loss) | — | — | — | 5,666 | — | — | 5,666 | (338 | ) | 5,328 | — | ||||||||||||||||||||||||||||

Balance-March 31, 2019 | 75,907,393 | $ | 399 | $ | 506,159 | $ | (191,293 | ) | $ | (5,656 | ) | $ | (2,234 | ) | $ | 307,375 | $ | 4,221 | $ | 311,596 | $ | — | |||||||||||||||||

Stock-based compensation | — | — | 2,965 | — | — | — | $ | 2,965 | $ | — | $ | 2,965 | — | ||||||||||||||||||||||||||

Issuance of common stock through vesting of restricted stock units and option exercises | 393,994 | 2 | 26 | — | — | — | 28 | — | 28 | — | |||||||||||||||||||||||||||||

Employee stock purchase plan | — | — | 335 | — | — | — | 335 | — | 335 | — | |||||||||||||||||||||||||||||

Tax withholding related to vesting of restricted stock units | — | — | (844 | ) | — | — | — | (844 | ) | — | (844 | ) | — | ||||||||||||||||||||||||||

Fair value of redeemable noncontrolling interest resulting from business combination | — | — | — | — | — | — | — | — | — | 16,444 | |||||||||||||||||||||||||||||

Currency translation adjustment | — | — | — | — | — | 463 | 463 | (49 | ) | 414 | (9 | ) | |||||||||||||||||||||||||||

Cash flow hedge | — | — | — | — | — | (124 | ) | (124 | ) | — | (124 | ) | — | ||||||||||||||||||||||||||

Other | — | — | (11 | ) | 1 | — | 1 | (9 | ) | — | (9 | ) | — | ||||||||||||||||||||||||||

Net Income (loss) | — | — | — | 4,295 | — | — | 4,295 | (814 | ) | 3,481 | (1,313 | ) | |||||||||||||||||||||||||||

Balance-June 30, 2019 | 76,301,387 | $ | 401 | $ | 508,630 | $ | (186,997 | ) | $ | (5,656 | ) | $ | (1,894 | ) | $ | 314,484 | $ | 3,358 | $ | 317,842 | $ | 15,122 | |||||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

6

ON DECK CAPITAL, INC. AND SUBSIDIARIES

Unaudited Condensed Consolidated Statements of Cash Flows

(in thousands)

Six Months Ended June 30, | |||||||

2019 | 2018 | ||||||

Cash flows from operating activities | |||||||

Net income (loss) | $ | 7,496 | $ | 2,036 | |||

Adjustments to reconcile net income (loss) to net cash provided by operating activities: | |||||||

Provision for credit losses | 86,242 | 69,586 | |||||

Depreciation and amortization | 3,574 | 4,218 | |||||

Amortization of debt issuance costs | 1,573 | 3,756 | |||||

Stock-based compensation | 6,331 | 6,004 | |||||

Amortization of net deferred origination costs | 35,277 | 26,499 | |||||

Changes in servicing rights, at fair value | 69 | 188 | |||||

Unfunded loan commitment reserve | 452 | 640 | |||||

Gain on lease termination | — | (1,481 | ) | ||||

Loss on disposal of fixed assets | 1,537 | 5,668 | |||||

Amortization of intangibles | 189 | — | |||||

Changes in operating assets and liabilities: | |||||||

Other assets | (9,595 | ) | (1,999 | ) | |||

Accounts payable | 1,499 | 1,413 | |||||

Interest payable | 302 | 244 | |||||

Accrued expenses and other liabilities | 1,613 | 1,992 | |||||

Net cash provided by operating activities | 136,559 | 118,764 | |||||

Cash flows from investing activities | |||||||

Purchases of property, equipment and software | (1,360 | ) | (695 | ) | |||

Capitalized internal-use software | (4,220 | ) | (2,464 | ) | |||

Originations of term loan, lines of credit and finance receivable, excluding rollovers into new originations | (1,029,348 | ) | (1,009,626 | ) | |||

Payments of net deferred origination costs | (33,505 | ) | (29,958 | ) | |||

Principal repayments of term loans, lines of credit and finance receivables | 946,025 | 865,537 | |||||

Purchase of loans | — | (801 | ) | ||||

Acquisition of shares in business combination | (3,004 | ) | $ | — | |||

Net cash used in investing activities | (125,412 | ) | (178,007 | ) | |||

Cash flows from financing activities | |||||||

Investments by noncontrolling interests | — | 3,403 | |||||

Tax withholding related to vesting of restricted stock units | (1,135 | ) | (441 | ) | |||

Proceeds from exercise of stock options and warrants | 71 | 39 | |||||

Issuance of common stock under employee stock purchase plan | 1,281 | 668 | |||||

Proceeds from the issuance of debt | 355,840 | 407,184 | |||||

Payments of debt issuance costs | (2,812 | ) | (3,748 | ) | |||

Repayments of debt principal | (359,392 | ) | (342,828 | ) | |||

Net cash (used in) provided by financing activities | (6,147 | ) | 64,277 | ||||

Effect of exchange rate changes on cash and cash equivalents | (558 | ) | (1,407 | ) | |||

Net increase in cash, cash equivalents and restricted cash | 4,442 | 3,627 | |||||

Cash, cash equivalents, and restricted cash at beginning of year | 97,638 | 114,824 | |||||

Cash, cash equivalents, and restricted cash at end of period | $ | 102,080 | $ | 118,451 | |||

7

Six Months Ended June 30, | |||||||

2019 | 2018 | ||||||

Reconciliation to amounts on consolidated balance sheets | |||||||

Cash and cash equivalents | $ | 58,744 | $ | 74,262 | |||

Restricted cash | 43,336 | 44,189 | |||||

Total cash, cash equivalents and restricted cash | $ | 102,080 | $ | 118,451 | |||

Supplemental disclosure of other cash flow information | |||||||

Cash paid for interest | $ | 20,038 | $ | 21,445 | |||

Supplemental disclosures of non-cash investing and financing activities | |||||||

Stock-based compensation included in capitalized internal-use software | $ | 109 | $ | 130 | |||

Unpaid principal balance of term loans rolled into new originations | $ | 198,319 | $ | 167,687 | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

8

ON DECK CAPITAL, INC. AND SUBSIDIARIES

Notes to Unaudited Condensed Consolidated Financial Statements

1. Organization and Summary of Significant Accounting Policies

On Deck Capital, Inc.’s principal activity is providing financing to small businesses located throughout the United States as well as Canada and Australia, through term loans and lines of credit, and additionally in Canada through merchant cash advances. We use technology and analytics to aggregate data about a business and then quickly and efficiently analyze the creditworthiness of the business using our proprietary credit-scoring model. We originate most of the loans in our portfolio and also purchase loans from an issuing bank partner. We subsequently transfer most of our loan volume into one of our wholly-owned subsidiaries for financing purposes.

In October 2018, we announced the launch of ODX, a wholly-owned subsidiary that helps banks digitize their small business lending process. ODX offers a combination of software, analytic insights, and professional services that allow banks to bring their small business lending process online.

In April 2019, we combined our Canadian operations with Evolocity Financial Group, or Evolocity, to create a new holding company in which we own a 58.5% majority interest. We have accounted for this transaction as a business combination and have consolidated the financial position and results of operations of the holding company. The noncontrolling interest has been classified as mezzanine equity because it was deemed to be a redeemable noncontrolling interest. See Note 2 for further discussion.

Basis of Presentation and Principles of Consolidation

We prepare our consolidated financial statements and footnotes in accordance with accounting principles generally accepted in the United States of America, or GAAP, as contained in the Financial Accounting Standards Board, or FASB, Accounting Standards Codification, or ASC. All intercompany transactions and accounts have been eliminated in consolidation. When used in these notes to consolidated financial statements, the terms "we," "us," "our" or similar terms refer to On Deck Capital, Inc. and its consolidated subsidiaries.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires us to make estimates and assumptions that affect the reported amounts in the consolidated financial statements and accompanying notes. Significant estimates include allowance for credit losses, stock-based compensation expense, capitalized software development costs, interest rate cap, the useful lives of long-lived assets, our effective income tax rate and valuation allowance for deferred tax assets. We base our estimates on historical experience, current events and other factors we believe to be reasonable under the circumstances. These estimates and assumptions are inherently subjective in nature; actual results may differ from these estimates and assumptions.

Recently Adopted Accounting Standards

In August 2017, the FASB issued ASU 2017-12, Derivatives and Hedging: Targeted Improvements to Accounting for Hedging Activities, which improves the financial reporting of hedging relationships to better portray the economic results of an entity's risk management activities in its financial statements and make certain targeted improvements to simplify the application of the hedge accounting guidance. The amendments in this update better align an entity's risk management activities and financial reporting for hedging relationships through changes to both the designation and measurement guidance for qualifying hedging relationships and presentation of hedge results. The effective date for the standard is for fiscal years beginning after December 15, 2018. We elected to early adopt this ASU in fiscal year 2018. See Note 10 for a discussion of our derivatives.

In February 2016, the FASB issued ASU 2016-02, Leases, which creates ASC 842, Leases, and supersedes ASC 840, Leases. ASU 2016-02 requires lessees to recognize a right-of-use asset and lease liability for all leases with terms of more than 12 months. The new standard is effective for annual reporting periods beginning after December 15, 2018, including interim periods within that reporting period. In July 2018, the FASB issued ASU No. 2018-11, Leases (Topic 842): Targeted Improvements. We elected the prospective transition option provided by the ASU that would not require earlier periods to be restated upon adoption. We elected the package of practical expedients afforded under the standard which permit an entity not to: (i) reassess whether existing or expired contracts are or contain a lease, (ii) reassess the lease classification, and (iii) reassess any initial direct costs for any existing leases. Our operating lease commitments, which were primarily real estate leases, were recognized as a $37.5 million lease liability when we adopted the new standard. The balance, which is included in Other Liabilities on the Consolidated Balance Sheet, is $36.5 million at June 30, 2019. We simultaneously recognized a $37.5 million right-of-use asset when we adopted the standard. Our right-of-use asset was partially offset by $10.1 million of existing deferred rent and lease incentives resulting in a net right-of-use asset of $27.6 million which is included in Other Assets on the Consolidated Balance Sheet. At June 30, 2019 the balance was $26.7 million. Our total operating lease cost for the three months ended June 30, 2019 was $1.5 million and allocated

9

within operating expenses. The weighted average remaining lease term was 6.8 years and we utilized a weighted average discount rate of approximately 7%.

Recent Accounting Pronouncements Not Yet Adopted

In June 2016, the FASB issued ASU 2016-13, Measurement of Credit Losses on Financial Instruments. ASU 2016-13 will change the impairment model and how entities measure credit losses for most financial assets. The standard requires entities to use the new expected credit loss impairment model which will replace the incurred loss model used today. The new guidance will be effective for annual reporting periods beginning after December 15, 2019. Early adoption is permitted, although we do not intend to do so. We are currently assessing the impact that the adoption of this guidance will have on our consolidated financial statements.

In January 2017, the FASB issued ASU 2017-04, Intangibles-Goodwill and Other: Simplifying the Test for Goodwill Impairment, which eliminates the requirement to determine the fair value of individual assets and liabilities of a reporting unit to measure goodwill impairment. Under the amendments in the new ASU, goodwill impairment testing will be performed by comparing the fair value of the reporting unit with its carrying amount and recognizing an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value. The new standard will become effective for annual reporting periods beginning after December 12, 2019. Early adoption is permitted, although we do not intend to do so. We are currently evaluating the impact the new standard may have on our disclosures, but we do not expect it to have a material impact.

In August 2018, the FASB issued ASU 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework-Changes to the Disclosure Requirements for Fair Value Measurement, which modifies disclosure requirements for fair value measurements under ASC 820, Fair Value Measurement. The new guidance will be effective for annual reporting periods beginning after December 15, 2019. We are currently evaluating the impact the new standard may have on our disclosures, but we do not expect it to have a material impact.

Revision of Prior Period Financial Statements

During the second quarter of 2019, we identified an immaterial error in our historical financial statements relating to the accrual of commissions on a portion of our renewal loans. The aggregate amount of the under-accrual was $2.4 million, approximately 90% of which relates to 2015 and subsequent periods, and represents less than 1%, of our total stockholders’ equity at March 31, 2019. The amount of the error in each of the impacted annual and interim periods was less than 1% of total commissions paid for such period.

In accordance with the SEC’s SAB No. 99, “Materiality,” and SAB No. 108, “Considering the Effects of Prior Year Misstatements when Quantifying Misstatements in Current Year Financial Statements,” we evaluated the error and concluded that the impact was not material to our financial statements for any prior annual or interim period. Accordingly, we have revised our previously reported financial information to correct the immaterial error contained in our Quarterly Report on Form 10-Q for the three-months ended and six-months ended June 30, 2018. We will also revise previously reported financial information for this immaterial error in our future filings, as applicable.

A summary of revisions to certain previously reported financial information is presented in Note 11.

2. Business Combination

On April 1, 2019, we combined our Canadian operations with Evolocity Financial Group, or Evolocity, a Montreal-based online small business lender. The purpose of the transaction was to accelerate the growth of our Canadian operations and to enable us to provide a broader range of financing options to Canadian small businesses nationwide. In the transaction, Evolocity contributed its business to a holding company, and we contributed our Canadian business plus cash to that holding company such that we own a 58.5% majority interest in the holding company. The remainder is owned by former Evolocity stockholders. The Company has accounted for this transaction as a business combination.

The transaction has a preliminary purchase price for accounting purposes of approximately $16.7 million. Our provisional valuation of the assets acquired and liabilities assumed, including but not limited to loans, intangible assets and goodwill, is preliminary and the fair values are subject to change within the measurement period of up to one year from the business combination date. Goodwill arising from the business combination is not amortized, but is subject to impairment testing at least annually or more frequently if there is an indicator of impairment.

10

The following table summarizes the preliminary fair value of the assets acquired and liabilities assumed in connection with the business combination (in thousands):

Fair Value | |||

Loans and finance receivables | $ | 37,454 | |

Intangibles and other assets (1) | 2,860 | ||

Debt and other liabilities | (34,437 | ) | |

Goodwill (1) | 10,844 | ||

Net assets acquired | $ | 16,721 | |

(1) Goodwill, and Intangibles and other assets were included in Other Assets on the Consolidated Balance Sheet as of June 30, 2019.

We consolidate the financial position and results of operations of the holding company.

As part of this business combination, the noncontrolling interest was deemed to be a redeemable noncontrolling interest. These interests are classified as mezzanine equity and measured at the greater of fair value at the end of each reporting period or the historical cost basis of the noncontrolling interest adjusted for cumulative earnings allocations.

3. Net Income (Loss) Per Common Share

Basic and diluted net income (loss) per common share is calculated as follows (in thousands, except share and per share data):

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2019 | 2018 | 2019 | 2018 | ||||||||||||

Numerator: | |||||||||||||||

Net Income (loss) | $ | 2,168 | $ | 4,612 | $ | 7,496 | $ | 2,036 | |||||||

Less: Net income (loss) attributable to noncontrolling interest | (2,127 | ) | (1,016 | ) | (2,465 | ) | (1,535 | ) | |||||||

Net income (loss) attributable to On Deck Capital, Inc. common stockholders | $ | 4,295 | $ | 5,628 | $ | 9,961 | $ | 3,571 | |||||||

Denominator: | |||||||||||||||

Weighted-average common shares outstanding, basic | 76,137,751 | 74,385,446 | 75,840,604 | 74,182,929 | |||||||||||

Net income (loss) per common share, basic | $ | 0.06 | $ | 0.08 | $ | 0.13 | $ | 0.05 | |||||||

Effect of dilutive securities | 2,763,850 | 3,902,821 | 3,173,153 | 3,603,819 | |||||||||||

Weighted-average common shares outstanding, diluted | 78,901,601 | 78,288,267 | 79,013,757 | 77,786,748 | |||||||||||

Net income (loss) per common share, diluted | $ | 0.05 | $ | 0.07 | $ | 0.13 | $ | 0.05 | |||||||

Anti-dilutive securities excluded | 6,747,782 | 5,174,846 | 5,591,794 | 5,351,219 | |||||||||||

The difference between basic and diluted net income per common share has been calculated using the Treasury Stock Method based on the assumed exercise of outstanding stock options, the vesting of restricted stock units, or RSUs, performance restricted stock units, or PRSUs, and the issuance of stock under our employee stock purchase plan. Changes in the average market price of our stock can impact when stock equivalents are considered dilutive or anti-dilutive. The following common share equivalent securities have been included in the calculation of dilutive weighted-average common shares outstanding:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||

Dilutive Common Share Equivalents | 2019 | 2018 | 2019 | 2018 | |||||||

Weighted-average common shares outstanding | 76,137,751 | 74,385,446 | 75,840,604 | 74,182,929 | |||||||

RSUs and PRSUs | 489,080 | 1,018,066 | 755,731 | 768,172 | |||||||

Stock options | 2,274,770 | 2,860,430 | 2,413,951 | 2,830,587 | |||||||

Employee stock purchase plan | — | 24,325 | 3,471 | 5,060 | |||||||

Total dilutive common share equivalents | 78,901,601 | 78,288,267 | 79,013,757 | 77,786,748 | |||||||

11

The following common share equivalent securities were excluded from the calculation of diluted net income per share attributable to common stockholders. Their effect would have been antidilutive for the three and six months ended June 30, 2019 and 2018.

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||

2019 | 2018 | 2019 | 2018 | ||||||||

Anti-Dilutive Common Share Equivalents | |||||||||||

Warrants to purchase common stock | — | 22,000 | — | 22,000 | |||||||

RSUs and PRSUs | 2,361,583 | 429,942 | 1,633,192 | 600,632 | |||||||

Stock options | 4,176,551 | 4,722,904 | 3,958,602 | 4,728,587 | |||||||

Employee stock purchase plan | 209,648 | — | — | — | |||||||

Total anti-dilutive common share equivalents | 6,747,782 | 5,174,846 | 5,591,794 | 5,351,219 | |||||||

4. Interest Income

Interest income was comprised of the following components for the three and six months ended June 30, 2019 and 2018 (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2019 | 2018 | 2019 | 2018 | ||||||||||||

Interest and finance income | $ | 122,799 | $ | 106,090 | $ | 246,234 | $ | 204,845 | |||||||

Amortization of net deferred origination costs | (17,451 | ) | (13,913 | ) | (35,344 | ) | (26,459 | ) | |||||||

Interest and finance income, net | 105,348 | 92,177 | 210,890 | 178,386 | |||||||||||

Interest on deposits and investments | 293 | 32 | 550 | 52 | |||||||||||

Total interest and finance income | $ | 105,641 | $ | 92,209 | $ | 211,440 | $ | 178,438 | |||||||

5. Loans and Finance Receivables Held for Investment and Allowance for Credit Losses

Loans and finance receivables held for investment consisted of the following as of June 30, 2019 and December 31, 2018 (in thousands):

June 30, 2019 | December 31, 2018 | ||||||

Term loans | $ | 936,053 | $ | 956,755 | |||

Lines of credit | 238,105 | 188,199 | |||||

Other loans and finance receivables (1) | 10,964 | — | |||||

Total Unpaid Principal Balance | 1,185,122 | 1,144,954 | |||||

Net deferred origination costs | 22,487 | 24,453 | |||||

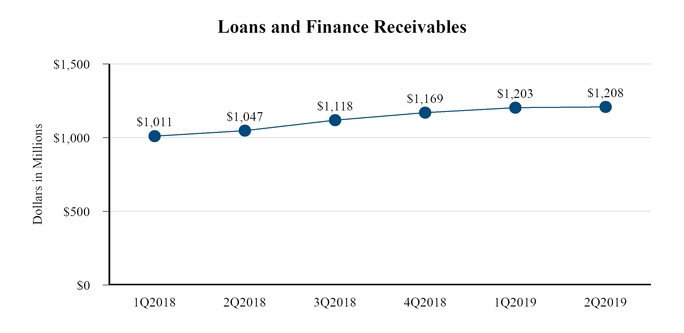

Total loans and finance receivables held for investment | $ | 1,207,609 | $ | 1,169,407 | |||

(1) | Includes secured equipment loans and merchant cash advances. |

As part of the business combination with Evolocity, on April 1, 2019 we purchased $37.5 million of term loans and finance receivables. During the six months ended June 30, 2018, we paid $0.8 million to purchase term loans that we previously sold to a third party. No loans from third parties were purchased during 2019.

We include both loans we originate and loans funded by our issuing bank partner and later purchased by us as part of our originations. During the three months ended June 30, 2019 and 2018 we purchased loans from our issuing bank partner in the amount of $95.5 million and $109.3 million, respectively. During the six months ended June 30, 2019 and 2018 we purchased loans from our issuing bank partner in the amount of $207.1 million and $248.5 million, respectively.

12

The change in the allowance for credit losses for the three and six months ended June 30, 2019 and 2018 consisted of the following (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2019 | 2018 | 2019 | 2018 | ||||||||||||

Balance at beginning of period | $ | 147,406 | $ | 118,921 | $ | 140,040 | $ | 109,015 | |||||||

Recoveries of previously charged off amounts | 4,523 | 3,206 | 8,437 | 6,551 | |||||||||||

Loans and finance receivables charged off | (49,141 | ) | (31,362 | ) | (88,980 | ) | (61,094 | ) | |||||||

Provision for credit losses | 42,951 | 33,293 | 86,242 | 69,586 | |||||||||||

Allowance for credit losses at end of period | $ | 145,739 | $ | 124,058 | $ | 145,739 | $ | 124,058 | |||||||

When loans and finance receivables are charged off, we typically continue to attempt to recover amounts from the respective borrowers and guarantors, including, when we deem it appropriate, through formal legal action. Alternatively, we may sell previously charged-off loans to a third-party debt collector. The proceeds from these sales are recorded as a component of the recoveries of loans previously charged off. We did not sell any previously charged-off loans for the three and six months ended June 30, 2019. For the three and six months ended June 30, 2018 loans sold accounted for $0.2 million and $0.7 million of recoveries of loans previously charged off.

As of June 30, 2019 and December 31, 2018, our off-balance sheet credit exposure related to the undrawn line of credit balances was $282.2 million and $264.2 million, respectively. The related reserve on unfunded loan commitments was $6.3 million and $5.9 million as of June 30, 2019 and December 31, 2018, respectively. Net adjustments to the liability for unfunded loan commitments are included in general and administrative expense.

The following table contains information, on a combined basis, regarding the unpaid principal balance we originated related to non-delinquent, paying and non-paying delinquent loans and finance receivables as of June 30, 2019 and December 31, 2018 (in thousands):

June 30, 2019 | December 31, 2018 | ||||||

Current loans and finance receivables | $ | 1,060,465 | $ | 1,031,449 | |||

Delinquent: paying (accrual status) | 52,735 | 54,427 | |||||

Delinquent: non-paying (non-accrual status) | 71,922 | 59,078 | |||||

Total | $ | 1,185,122 | $ | 1,144,954 | |||

The portion of the allowance for credit losses attributable to current loans and finance receivables was $70.5 million and $85.7 million as of June 30, 2019 and December 31, 2018, respectively, while the portion of the allowance for credit losses attributable to delinquent loans and finance receivables was $75.3 million and $54.3 million as of June 30, 2019 and December 31, 2018, respectively.

The following table shows an aging analysis of the unpaid principal balance related to loans and finance receivables by delinquency status as of June 30, 2019 and December 31, 2018 (in thousands):

June 30, 2019 | December 31, 2018 | ||||||

By delinquency status: | |||||||

Current loans and finance receivables | $ | 1,060,465 | $ | 1,031,449 | |||

1-14 calendar days past due | 23,798 | 27,655 | |||||

15-29 calendar days past due | 15,518 | 14,665 | |||||

30-59 calendar days past due | 23,931 | 21,470 | |||||

60-89 calendar days past due | 18,162 | 19,031 | |||||

90 + calendar days past due | 43,248 | 30,684 | |||||

Total unpaid principal balance | $ | 1,185,122 | $ | 1,144,954 | |||

13

6. Debt

The following table summarizes our outstanding debt as of June 30, 2019 and December 31, 2018 (in thousands):

Outstanding | |||||||||||||

Type | Maturity Date | Weighted Average Interest Rate at June 30, 2019 | June 30, 2019 | December 31, 2018 | |||||||||

Debt: | |||||||||||||

OnDeck Asset Securitization Trust II | Securitization | April 2022 | (1) | 3.8% | $ | 225,000 | $ | 225,000 | |||||

OnDeck Account Receivables Trust 2013-1 | Revolving | March 2022 | (2) | 4.2% | 111,827 | 117,664 | |||||||

Receivable Assets of OnDeck, LLC | Revolving | September 2021 | (3) | 4.8% | 101,453 | 113,631 | |||||||

OnDeck Asset Funding II LLC | Revolving | August 2022 | (4) | 5.4% | 110,202 | 109,568 | |||||||

Prime OnDeck Receivable Trust II | Revolving | March 2022 | (5) | 4.4% | 108,949 | 108,816 | |||||||

Loan Assets of OnDeck, LLC | Revolving | October 2022 | (6) | 4.2% | 98,469 | 100,000 | |||||||

Corporate Debt | Revolving | January 2021 | 5.4% | 20,000 | — | ||||||||

Other Agreements | Various | Various | (7) | 6.8% | (8) | 72,909 | (9) | 47,318 | |||||

4.6% | 848,809 | 821,997 | |||||||||||

Deferred debt issuance cost | (7,207 | ) | (5,766 | ) | |||||||||

Total Debt | $ | 841,602 | $ | 816,231 | |||||||||

(1) | The period during which new loans may be purchased under this securitization transaction expires in March 2020. |

(2) | The period during which new borrowings may be made under this facility expires in March 2021. |

(3) | The period during which new borrowings of Class A revolving loans may be made under this debt facility expires in December 2020. The $19.7 million of Class B borrowing capacity matures in December 2019. |

(4) | The period during which new borrowings may be made under this facility expires in August 2021. |

(5) | The period during which new borrowings may be made under this facility expires in March 2021. |

(6) | The period during which new borrowings may be made under this debt facility expires in April 2022. |

(7) | The periods during which new borrowings may be made under the various agreements expire between September 2019 and June 2020. Maturity dates range from September 2019 through December 2022. |

(8) | Weighted average interest rate as of June 30, 2019 reflects the credit facilities assumed as a part of the combination with Evolocity Financial Group. |

(9) | Outstanding amounts as of June 30, 2019 reflects the credit facilities assumed as a part of the combination with Evolocity Financial Group. |

Certain of our loans held for investment are pledged as collateral for borrowings in our funding debt facilities. These loans totaled $1.0 billion and $1.0 billion as of June 30, 2019 and December 31, 2018, respectively. Our corporate debt facility is collateralized by substantially all of our assets.

7. Fair Value of Financial Instruments

Assets and Liabilities Measured at Fair Value on a Recurring Basis Using Significant Unobservable Inputs

We evaluate our financial assets and liabilities subject to fair value measurements on a recurring basis to determine the appropriate level at which to classify them for each reporting period. Our interest rate cap is reported at fair value utilizing Level 2 inputs. The fair value is determined using third party valuations that are based on discounted cash flow analysis using observed market inputs.

14

The following tables present information about our assets and liabilities that are measured at fair value on a recurring basis as of June 30, 2019 and December 31, 2018 (in thousands):

June 30, 2019 | |||||||||||||||

Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Assets: | |||||||||||||||

Interest rate cap | — | 41 | — | 41 | |||||||||||

Total assets | $ | — | $ | 41 | $ | — | $ | 41 | |||||||

December 31, 2018 | |||||||||||||||

Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Assets: | |||||||||||||||

Interest rate cap | $ | — | $ | 1,253 | $ | — | $ | 1,253 | |||||||

Total assets | $ | — | $ | 1,253 | $ | — | $ | 1,253 | |||||||

There were no transfers between levels for the three months ended June 30, 2019 and December 31, 2018.

Assets and Liabilities Disclosed at Fair Value

Because our loans and finance receivables and fixed-rate debt are not measured at fair value, we are required to disclose their fair value in accordance with ASC 825. Due to the lack of transparency and comparable loans and finance receivables, we utilize an income valuation technique to estimate fair value. We utilize industry-standard modeling, such as discounted cash flow models, to arrive at an estimate of fair value and may utilize third-party service providers to assist in the valuation process. This determination requires significant judgments to be made. The following tables summarize the carrying value and fair value of our loans held for investment and fixed-rate debt (in thousands):

June 30, 2019 | |||||||||||||||||||

Carrying Value | Fair Value | Level 1 | Level 2 | Level 3 | |||||||||||||||

Assets: | |||||||||||||||||||

Loans and finance receivables, net | $ | 1,061,870 | $ | 1,191,009 | $ | — | $ | — | $ | 1,191,009 | |||||||||

Total assets | $ | 1,061,870 | $ | 1,191,009 | $ | — | $ | — | $ | 1,191,009 | |||||||||

Liabilities: | |||||||||||||||||||

Fixed-rate debt | $ | 240,238 | $ | 236,026 | $ | — | $ | — | $ | 236,026 | |||||||||

Total fixed-rate debt | $ | 240,238 | $ | 236,026 | $ | — | $ | — | $ | 236,026 | |||||||||

December 31, 2018 | |||||||||||||||||||

Carrying Value | Fair Value | Level 1 | Level 2 | Level 3 | |||||||||||||||

Assets: | |||||||||||||||||||

Loans and finance receivables, net | $ | 1,029,367 | $ | 1,155,464 | $ | — | $ | — | $ | 1,155,464 | |||||||||

Total assets | $ | 1,029,367 | $ | 1,155,464 | $ | — | $ | — | $ | 1,155,464 | |||||||||

Liabilities: | |||||||||||||||||||

Fixed-rate debt | $ | 232,972 | $ | 226,965 | $ | — | $ | — | $ | 226,965 | |||||||||

Total fixed-rate debt | $ | 232,972 | $ | 226,965 | $ | — | $ | — | $ | 226,965 | |||||||||

15

8. Income Taxes

For interim periods, the income tax provision is comprised of tax on ordinary income provided at the most recent estimated annual effective tax rate, adjusted for the tax effect of discrete items. We use an estimated annual effective tax rate which is based on expected annual income and statutory tax rates to determine our quarterly provision for income taxes. Certain significant or unusual items are separately recognized in the quarter in which they occur and can be a source of variability in the effective tax rates from quarter to quarter.

Our provision for income taxes for the three and six months ended June 30, 2019 was $1.8 million and $3.5 million, representing an estimated quarterly effective income tax rate of 45% for the three months ended June 30, 2019 and a year to date effective income tax rate of 32%. The effective income tax rate for the full year 2018 was 0% due to the availability of net operating loss carryforwards. A valuation allowance of $37.6 million was recorded against our net deferred tax assets of approximately $42.7 million as of June 30, 2019 resulting in a net deferred tax asset of approximately $5.0 million.

9. Stock-Based Compensation and Employee Benefit Plans

Options

The following is a summary of option activity for the six months ended June 30, 2019:

Number of Options | Weighted- Average Exercise Price | Weighted- Average Remaining Contractual Term (in years) | Aggregate Intrinsic Value (in thousands) | ||||||||||

Outstanding at January 1, 2019 | 7,932,782 | $ | 5.86 | — | — | ||||||||

Exercised | (389,335 | ) | $ | 2.63 | — | — | |||||||

Expired | (508,557 | ) | $ | 11.24 | — | — | |||||||

Outstanding at June 30, 2019 | 7,034,890 | $ | 5.65 | 5.5 | $ | 9,043 | |||||||

Exercisable at June 30, 2019 | 6,093,122 | $ | 5.63 | 5.1 | $ | 9,043 | |||||||

Vested or expected to vest as of June 30, 2019 | 6,984,662 | $ | 5.65 | 5.5 | $ | 9,043 | |||||||

Total compensation cost related to nonvested option awards not yet recognized as of June 30, 2019 was $1.9 million and will be recognized over a weighted-average period of 2.1 years. The aggregate intrinsic value of employee options exercised during the six months ended June 30, 2019 and 2018 was $1.4 million and $2.0 million, respectively.

16

Restricted Stock Units

The following table is a summary of activity in RSUs and PRSUs for the six months ended June 30, 2019:

Number of RSUs and PRSUs | Weighted-Average Grant Date Fair Value | |||||

Unvested at January 1, 2019 | 3,307,561 | $ | 6.00 | |||

RSUs and PRSUs granted | 1,984,378 | $ | 5.64 | |||

RSUs and PRSUs vested | (585,312 | ) | $ | 6.57 | ||

RSUs and PRSUs forfeited/expired | (294,195 | ) | $ | 5.78 | ||

Unvested at June 30, 2019 | 4,412,432 | $ | 5.78 | |||

Expected to vest after June 30, 2019 | 3,594,305 | $ | 5.76 | |||

As of June 30, 2019, there was $16 million of unrecognized compensation cost related to unvested RSUs and PRSUs, which is expected to be recognized over a weighted-average period of 2.8 years.

Stock-based compensation expense related to stock options, RSUs, PRSUs and the employee stock purchase plan are included in the following line items in our accompanying consolidated statements of operations for the three months and six months ended June 30, 2019 and 2018 (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2019 | 2018 | 2019 | 2018 | ||||||||||||

Sales and marketing | $ | 474 | $ | 505 | $ | 1,033 | $ | 1,040 | |||||||

Technology and analytics | 889 | 657 | 1,717 | 1,253 | |||||||||||

Processing and servicing | 49 | 94 | 139 | 201 | |||||||||||

General and administrative | 1,836 | 1,538 | 3,442 | 3,510 | |||||||||||

Total | $ | 3,248 | $ | 2,794 | $ | 6,331 | $ | 6,004 | |||||||

10. Derivatives and Hedging

We are subject to interest rate risk in connection with borrowings under our debt agreements which are subject to variable interest rates. In December 2018 we entered into an interest rate cap, which is a derivative instrument, to manage our interest rate risk on a portion of our variable-rate debt. We do not use derivatives for speculative purposes. The interest rate cap is designated as a cash flow hedge. In exchange for our up-front premium, we would receive variable amounts from a counterparty if interest rates rise above the strike rate on the contract. The interest rate cap agreement is for a notional amount of $300 million and has a maturity date of January 2021.

For derivatives designated and that qualify as cash flow hedges of interest rate risk, the changes in the fair value of the derivative are recorded in Accumulated Other Comprehensive Income, or AOCI, and subsequently reclassified into interest expense in the same period(s) during which the hedged transaction affects earnings. Gains and losses on the derivative representing hedge components excluded from the assessment of effectiveness are recognized over the life of the hedge on a systematic and rational basis, as documented at hedge inception in accordance with our accounting policy election. The earnings recognition of excluded components is presented in interest expense. Amounts reported in AOCI related to derivatives will be reclassified to interest expense as interest payments are made on our variable-rate debt. We estimate that $1.0 million will be reclassified as an increase to interest expense over the next 12 months.

The table below presents the fair value of our derivative financial instruments as well as their classification on the Balance Sheet as of June 30, 2019 and December 31, 2018 (in thousands):

Derivative Type | Classification | June 30, 2019 | December 31, 2018 | |||||||

Assets: | ||||||||||

Interest rate cap agreement | Other Assets | $ | 41 | $ | 1,253 | |||||

17

The table below presents the effect of cash flow hedge accounting on AOCI as of June 30, 2019 and December 31, 2018 (in thousands):

June 30, 2019 | December 31, 2018 | ||||||

Amount Recognized in OCI on Derivative: | |||||||

Interest rate cap agreement | $ | 866 | $ | 456 | |||

The table below presents the effect of our derivative financial instruments on the Statement of Operations and Comprehensive Income as of three and six months ended June 30, 2019 and 2018 (in thousands):

Location and Amount of Gain or (Loss) Recognized in Income on Cash Flow Hedging Relationships | ||||||||||||||||

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

2019 | 2018 | 2019 | 2018 | |||||||||||||

Interest expense | $ | (204 | ) | $ | — | $ | (338 | ) | $ | — | ||||||

11. Revision of Prior Period Financial Statements

We revised prior period financial statements to correct an immaterial error related to the channel attribution of certain loans and the commissions associated with those loans. Commissions become due upon the closing of a loan. Those commissions are capitalized as a component of the loan balance and are amortized as an adjustment to interest income over the life of the loan. A summary of those revisions is as follows:

Revised Consolidated Balance Sheet as of December 31, 2018 (in thousands):

As Reported | Adjustment | As Revised | |||||||||

Loans and finance receivables | $ | 1,169,157 | $ | 250 | $ | 1,169,407 | |||||

Total assets | $ | 1,161,570 | $ | 250 | $ | 1,161,820 | |||||

Accrued expenses and other liabilities | $ | 34,654 | $ | 2,054 | $ | 36,708 | |||||

Total liabilities | $ | 857,281 | $ | 2,054 | $ | 859,335 | |||||

Accumulated deficit | $ | (195,155 | ) | $ | (1,804 | ) | $ | (196,959 | ) | ||

Total On Deck Capital, Inc. stockholders' equity | $ | 299,756 | $ | (1,804 | ) | $ | 297,952 | ||||

Total stockholders' equity | $ | 304,289 | $ | (1,804 | ) | $ | 302,485 | ||||

Revised Consolidated Statements of Operations and Comprehensive Income (in thousands):

Three Months Ended June 30, 2018 | Six Months Ended June 30, 2018 | ||||||||||

As Reported | Adjustment | As Revised | As Reported | Adjustment | As Revised | ||||||

Interest and finance income | $92,371 | $(162) | $92,209 | $178,740 | $(302) | $178,438 | |||||

Gross revenue | $95,618 | $(162) | $95,456 | $185,898 | $(302) | $185,596 | |||||

Net revenue | $50,080 | (1) | $(162) | $49,918 | $92,195 | (1) | $(302) | $91,893 | |||

Income (loss) from operations, before provision for income taxes | $4,774 | (1) | $(162) | $4,612 | $2,338 | (1) | $(302) | $2,036 | |||

Net income (loss) | $4,774 | $(162) | $4,612 | $2,338 | $(302) | $2,036 | |||||

(1) Includes a prior period reclassification to include interest expense as funding costs.

There was no impact to earnings per share for any period presented.

18

Revised Consolidated Statements of Cash Flows

We revised our condensed consolidated statement of cash flows for the six months ended June 30, 2018 to reflect the correction of the error, which had no impact to net cash provided by operating activities, net cash used in investing activities and net cash provided by financing activities in the period.

12. Commitments and Contingencies

Concentrations of Credit Risk

Financial instruments that potentially subject us to significant concentrations of credit risk consist principally of cash, cash equivalents, restricted cash and loans. We hold cash, cash equivalents and restricted cash in accounts at regulated domestic financial institutions in amounts that exceed or may exceed FDIC insured amounts and at non-U.S. financial institutions where deposited amounts may be uninsured. We believe these institutions to be of acceptable credit quality and we have not experienced any related losses to date.

We are exposed to default risk on loans we originate and hold and that we purchase from our issuing bank partner. We perform an evaluation of each customer's financial condition and during the term of the customer's loan(s), we have the contractual right to limit a customer's ability to take working capital loans or other financing from other lenders that may cause a material adverse change in the financial condition of the customer.

Contingencies

From time to time we are subject to legal proceedings and claims in the ordinary course of business. The results of such matters cannot be predicted with certainty. However, we believe that the final outcome of any such current matters will not result in a material adverse effect on our consolidated financial condition, consolidated results of operations or consolidated cash flows.

13. Subsequent Events

On July 19, 2019, we increased the commitment under our corporate revolving debt facility by $20 million to an aggregate commitment amount of $105 million. The facility's interest rate of 1-month LIBOR plus 3.0% and the final maturity date in January 2021 did not change.

19

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

You should read the following discussion and analysis of our financial condition and results of operations together with our unaudited condensed consolidated financial statements and the related notes, and other financial information included elsewhere in this report. Some of the information contained in this discussion and analysis, including information with respect to our plans and strategy for our business, includes forward-looking statements that involve risks and uncertainties. You should review the “Cautionary Note Regarding Forward-Looking Statements” and Part II - Item 1A. Risk Factors sections of this report for a discussion of important factors that could cause actual results to differ materially from the results described in, or implied by, the forward-looking statements contained in the following discussion and analysis.

20

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and other legal authority. These forward-looking statements concern our operations, economic performance, financial condition, goals, beliefs, future growth strategies, objectives, plans and current expectations.

Forward-looking statements appear throughout this report including in Part I - Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations, Part II - Item 1. Legal Proceedings and Part II - Item 1A. Risk Factors. Forward-looking statements can generally be identified by words such as “will,” “enables,” “expects,” "intends," "may," “allows,” "plan," “continues,” “believes,” “anticipates,” “estimates” or similar expressions.

Forward-looking statements are neither historical facts nor assurances of future performance. They are based only on our current beliefs, expectations and assumptions regarding the future of our business, anticipated events and trends, the economy and other future conditions. As such, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and in many cases outside our control. Therefore, you should not rely on any of these forward-looking statements. Our expected results may not be achieved, and actual results may differ materially from our expectations.

Important factors that could cause or contribute to such differences include risks relating to: (1) our ability to achieve consistent profitability in the future in light of our prior loss history and competition; (2) our growth strategies, including the introduction of new products or features, expanding our platform to other lenders through ODX, maintaining ODX’s current clients or losing a significant ODX client, expansion into international markets, offering equipment financing and our ability to effectively manage and fund our growth; (3) possible future acquisitions of complementary assets, businesses, technologies or products with the goal of growing our business, and the integration of any such acquisitions including Evolocity Financial Group; (4) any material reduction in our interest rate spread and our ability to successfully mitigate this risk through interest rate hedging or raising interest rates or other means; (5) worsening economic conditions that may result in decreased demand for our loans or services and increase our customers’ default rates; (6) supply and demand driven changes in credit and increases in the availability of capital for our competitors that negatively impacts our loan pricing; (7) our ability to accurately assess creditworthiness and forecast and reserve for loan losses; (8) our ability to prevent or discover security breaches, disruption in service and comparable events that could compromise confidential information held in our data systems or adversely impact our ability to service our loans; (9) incorrect or fraudulent information provided to us by customers causing us to misjudge their qualifications to receive a loan; (10) the effectiveness of our efforts to identify, manage and mitigate our credit, market, liquidity, operational and other risks associated with our business and strategic objectives; (11) our ability to continue to innovate or respond to evolving technological changes and protect our intellectual property; (12) our reputation and possible adverse publicity about us or our industry; (13) failure of operating controls, including customer or partner experience degradation, and related legal expenses, increased regulatory cost, significant fraud losses and vendor risk; (14) changes in federal or state laws or regulations, or judicial decisions involving licensing or supervision of commercial lenders, interest rate limitations, the enforceability of choice of law provisions in loan agreements, the validity of bank sponsor partnerships, the use of brokers or other significant changes; (15) risks associated with pursuing a bank charter, either de novo or in a transaction, and risks associated with either failing to obtain or obtaining a bank charter; and other risks, including those described in Part I - Item 1A. Risk Factors in our Annual Report on Form 10-K for the year ended December 31, 2018, Part II - Item 1A. Risk Factors in this report and other documents that we file with the Securities and Exchange Commission, or SEC, from time to time which are or will be available on the SEC website at www.sec.gov.

Except as required by law, we undertake no duty to update any forward-looking statements. Readers are also urged to carefully review and consider all of the information in this report, as well as the other documents we make available through the SEC’s website.

In this report, when we use the terms “OnDeck,” the “Company,” “we,” “us” or “our,” we are referring to On Deck Capital, Inc. and its consolidated subsidiaries, and when we use the term "ODX" we are referring to our wholly-owned subsidiary ODX, LLC, in each case unless the context requires otherwise.

OnDeck, the OnDeck logo, OnDeck Score, OnDeck Marketplace, ODX and other trademarks or service marks of OnDeck appearing in this report are the property of OnDeck. Trade names, trademarks and service marks of other companies appearing in this report are the property of their respective holders, including FICO®, a registered trademark of Fair Issac Corporation and Chase Business Quick Capital®, a registered trademark of JPMorgan Chase Bank, National Association. We have generally omitted the ® and TM designations, as applicable, for the trademarks used in this report.

21

Overview

We are a leading online small business lender. We make it efficient and convenient for small businesses to access financing. Enabled by our proprietary technology and analytics, we aggregate and analyze thousands of data points from dynamic, disparate data sources to assess the creditworthiness of small businesses rapidly and accurately. Small businesses can apply for financing on our website in minutes and, using our loan decision process, including our proprietary OnDeck Score®, we can make a funding decision immediately and, if approved, fund as fast as 24 hours. We have originated more than $12 billion of loans since we made our first loan in 2007.

We have offered term loans since we made our first loan in 2007, lines of credit since 2013 and this year have begun offering equipment finance loans and, in Canada, merchant cash advances through Evolocity Financial Group with whom we combined operations on April 1, 2019. Our term loans range from $5,000 to $500,000, have maturities of 3 to 36 months and feature fixed dollar repayments. Our lines of credit range from $6,000 to $100,000, and are generally repayable within 6 or 12 months of the date of the most recent draw. We are generally targeting equipment finance loans from $5,000 to $150,000, with maturities of 2 to 5 years as we develop this offering, although we may offer larger loans in cases we deem appropriate. Qualified customers may have multiple financings with us concurrently, which we believe provides opportunities for repeat business, as well as increased value to our customers.

We originate loans throughout the United States, Canada and Australia, although, to date, the majority of our revenue has been generated in the United States. These loans are originated through our direct marketing channel, including direct mail, our outbound sales team, our social media and other online marketing channels; referrals from our strategic partner channel, including small business-focused service providers, payment processors, and other financial institutions; and through independent funding advisor program partners, or FAPs, who advise small businesses on available funding options.

We generate the majority of our revenue through interest income and fees earned on the loans we make to our customers. We earn interest on the balance outstanding and lines of credit are subject to a monthly fee unless the customer makes a qualifying minimum draw, in which case the fee is waived for the first six months. The balance of our other revenue primarily comes from our servicing and other fee income, most of which consists of marketing fees from our issuing bank partner, fees generated by ODX, and monthly fees earned from lines of credit.

We rely on a diversified set of funding sources for the loans we make to our customers. Our primary source of this financing has historically been debt facilities with various financial institutions and securitizations. We have also used proceeds from operating cash flow to fund loans in the past and continue to finance a portion of our outstanding loans with these funds. As of June 30, 2019, we had $848.8 million of debt principal outstanding and $1.2 billion total borrowing capacity.

Recent Developments

On April 1, 2019, we combined our Canadian operations with Evolocity Financial Group, or Evolocity, a Montreal-based online small business lender. The purpose of the transaction was to accelerate the growth of our Canadian operations and to enable us to provide a broader range of financing options to Canadian small businesses nationwide. In the transaction, Evolocity contributed its business to a holding company, and we contributed our Canadian business plus cash to that holding company such that we own a 58.5% majority interest in the holding company. The remainder is owned by former Evolocity stockholders. The financial position and results of operations of Evolocity as of and for the three months ended June 30, 2019 are included in our consolidated financial statements and other financial data contained within this quarterly report on Form 10-Q.

On July 29, 2019 we made several important announcments. We announced that our Board of Directors authorized the repurchase of up to $50 million of common stock with the shares to be retained in Treasury and available for possible reissuance. Any share repurchases under the program will be made from time to time in the open market, in privately negotiated transactions or otherwise. The timing and amount of any share repurchases will be subject to market conditions and other factors as we may determine. The repurchase authorization expires August 31, 2020, however, we may suspend, modify or discontinue the program at any time in our discretion without prior notice.

We also announced that JPMorgan Chase Bank, National Association, informed us that effective August 3, 2019, they no longer intend to originate new small business loans through our platform. We will continue to service the loans they previously originated through our platform and be entitled to receive related servicing revenue for up to two years. We recorded a charge of approximately $0.9 million during the three months ended June 30, 2019 related to the impairment of certain capitalized software built for and dedicated to their originations.

Additionally, we announced that we decided to pursue obtaining a bank charter, either de novo or through a transaction.

22

Key Financial and Operating Metrics

We regularly monitor a number of metrics in order to measure our current performance and project our future performance. These metrics aid us in developing and refining our growth strategies and making strategic decisions.

As of or for the Three Months Ended June 30, | As of or for the Six Months Ended June 30, | ||||||||||||||

2019 | 2018 | 2019 | 2018 | ||||||||||||

(dollars in thousands) | (dollars in thousands) | ||||||||||||||

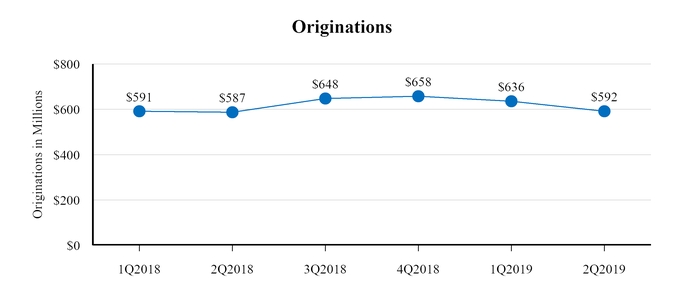

Originations | $ | 591,848 | $ | 586,728 | $ | 1,227,354 | $ | 1,177,313 | |||||||

Portfolio Yield (a) | 35.0 | % | 36.1 | % | 35.3 | % | 35.8 | % | |||||||

Cost of Funds Rate | 5.5 | % | 6.6 | % | 5.4 | % | 6.7 | % | |||||||

Net Interest Margin (a) | 29.0 | % | 28.2 | % | 29.3 | % | 28.1 | % | |||||||

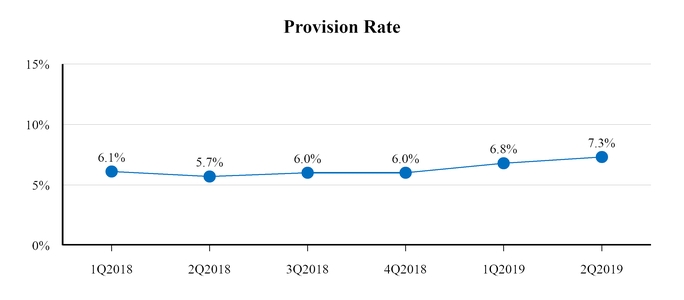

Provision Rate | 7.3 | % | 5.7 | % | 7.0 | % | 5.9 | % | |||||||

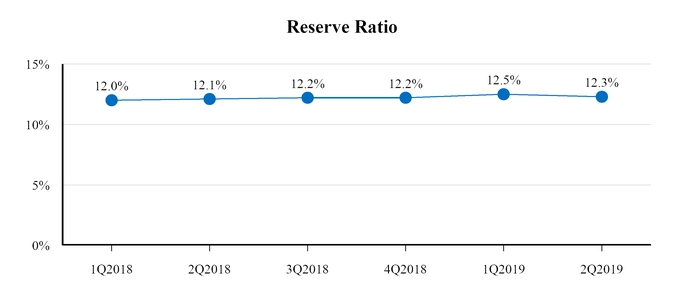

Reserve Ratio | 12.3 | % | 12.1 | % | 12.3 | % | 12.1 | % | |||||||

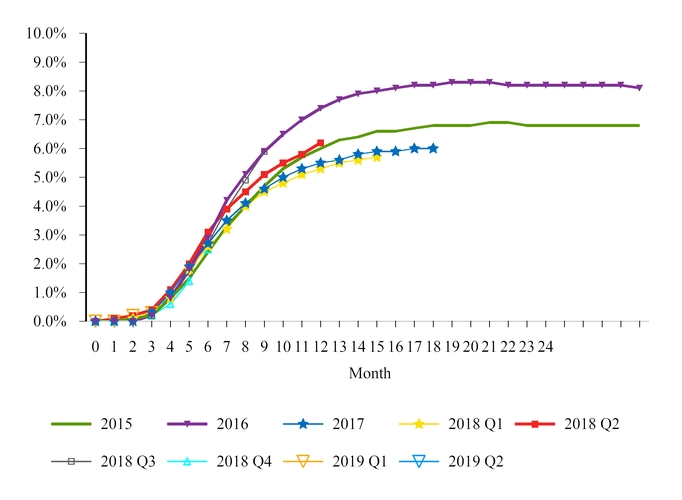

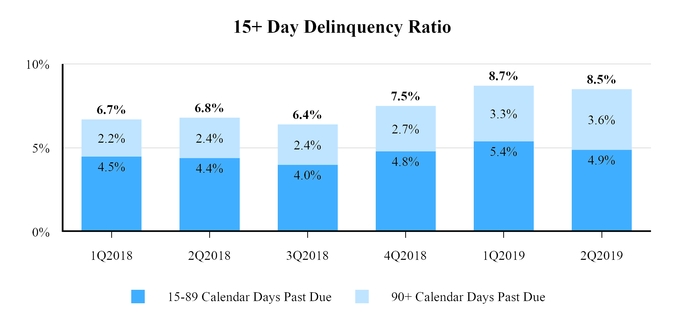

15+ Day Delinquency Ratio | 8.5 | % | 6.8 | % | 8.5 | % | 6.8 | % | |||||||

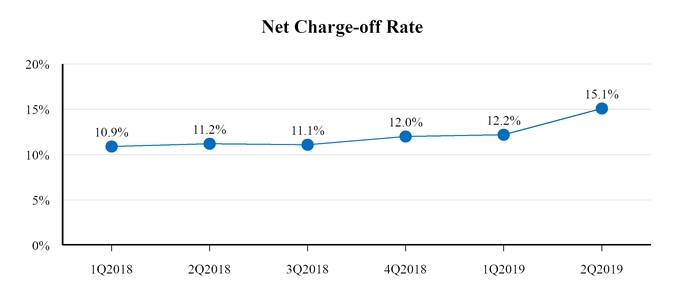

Net Charge-off Rate | 15.1 | % | 11.2 | % | 13.6 | % | 11.1 | % | |||||||

Efficiency Ratio (a) | 47.1 | % | 47.5 | % | 45.5 | % | 48.4 | % | |||||||

Adjusted Efficiency Ratio* (a) | 44.2 | % | 43.1 | % | 42.6 | % | 41.7 | % | |||||||

Return on Assets (a) | 1.4 | % | 2.2 | % | 1.6 | % | 0.7 | % | |||||||

Adjusted Return On Assets* (a) | 2.2 | % | 3.7 | % | 2.5 | % | 3.1 | % | |||||||

Return on Equity (a) | 5.5 | % | 8.4 | % | 6.5 | % | 2.7 | % | |||||||

Adjusted Return On Equity* (a) | 8.8 | % | 14.7 | % | 9.8 | % | 12.1 | % | |||||||

(a) The prior period metrics have been updated to reflect the impact of the revision. We believe the impact of the revision to each affected KPI is not meaningful with no impact being greater than 20 basis points. See Note 1 of Notes to Unaudited Condensed Consolidated Financial Statements.

*Non-GAAP measure. Refer to "Non-GAAP Financial Measures" below for an explanation and reconciliation to GAAP.

Originations

Originations represent the total principal amount of Loans made during the period plus the total amount advanced on other finance receivables. Many of our repeat term loan customers renew their term loans before their existing term loan is fully repaid. In accordance with industry practice, originations of such repeat term loans are presented as the full renewal loan principal, rather than the net funded amount, which would be the renewal term loan’s principal net of the Unpaid Principal Balance on the existing term loan. Loans referred to, and funded by, our issuing bank partner and later purchased by us are included as part of our originations.

Unpaid Principal Balance represents the total amount of principal outstanding on Loans held for investment, plus outstanding advances relating to other finance receivables and the amortized cost of loans purchased from other than our issuing bank partner at the end of the period. It excludes net deferred origination costs, allowance for credit losses and any loans sold or held for sale at the end of the period.

Portfolio Yield

Portfolio Yield is the rate of return we achieve on Loans and finance receivables outstanding during a period. It is calculated as annualized Interest and finance income on Loans and finance receivables including amortization of net deferred origination costs divided by average loans and finance receivables. Annualization is based on 365 days per year and is calendar day-adjusted. Loans and finance receivables represents the sum of term loans, lines of credit, equipment finance loans and finance receivables. Portfolio Yield replaces our previous metric, Loan Yield in order to include other finance receivables.

Net deferred origination costs in Loans and finance receivables held for investment and loans held for sale consist of deferred origination fees and costs. Deferred origination fees include fees paid up front to us by customers when Loans and finance receivables are originated and decrease the carrying value of Loans and finance receivables, thereby increasing Portfolio Yield. Deferred origination costs are limited to costs directly attributable to originating loans and finance receivables such as commissions,

23

vendor costs and personnel costs directly related to the time spent by the personnel performing activities related to originations and increase the carrying value of loans and finance receivables, thereby decreasing Portfolio Yield.

Recent pricing trends are discussed under the subheading “Key Factors Affecting Our Performance - Pricing.”

Cost of Funds Rate

Cost of Funds Rate is calculated as interest expense divided by average debt outstanding for the period. For periods of less than one year, the metric is annualized based on four quarters per year and is not business day or calendar day-adjusted.

Net Interest Margin

Net Interest Margin is calculated as annualized net interest and finance income divided by average Interest Earning Assets. Net interest and finance income represents Interest and finance receivable income less Interest expense during the period. Annualization is based on 365 days per year and is calendar day-adjusted. Interest and finance receivable income is net of fees on loans held for investment and loans held for sale. Interest expense is the interest expense, fees, and amortization of deferred debt issuance costs we incur in connection with our debt facilities. Interest Earning Assets represents the sum of Loans and finance receivables plus Cash and cash equivalents plus Restricted cash.

Reserve Ratio

Reserve Ratio is our allowance for credit losses at the end of the period divided by the Unpaid Principal Balance at the end of the period.

Provision Rate

Provision Rate equals the provision for credit losses for the period divided by originations for the period. Because we reserve for probable credit losses inherent in the portfolio upon origination, this rate is significantly impacted by the expectation of credit losses for the period’s originations volume. This rate is also impacted by changes in loss expectations for loans and finance receivables originated prior to the commencement of the period. All other things equal, an increased volume of loan rollovers and line of credit repayments and re-borrowings in a period will reduce the Provision Rate.

The Provision Rate is not directly comparable to the net cumulative lifetime charge-off ratio because (i) the Provision Rate reflects estimated losses at the time of origination while the net cumulative lifetime charge-off ratio reflects actual charge-offs, (ii) the Provision Rate includes provisions for losses on Loans and finance receivables while the net cumulative lifetime charge-off ratio reflects only charge-offs related to term loans and (iii) the Provision Rate for a period reflects the provision for losses related to all loans and finance receivables held for investment while the net cumulative lifetime charge-off ratio reflects lifetime charge-offs of term loans related to a particular cohort of term loans.

15+ Day Delinquency Ratio

15+ Day Delinquency Ratio equals the aggregate Unpaid Principal Balance for our Loans that are 15 or more calendar days contractually passed due and for our finance receivables that are 15 or more payments behind schedule as a percentage of the Unpaid Principal Balance at the end of the period. The Unpaid Principal Balance for our loans and finance receivables that are 15 or more calendar days or payments past due includes Loans and finance receivables that are paying and non-paying. Because term and line of credit loans require daily and weekly repayments, excluding weekends and holidays, they may be deemed delinquent more quickly than loans from traditional lenders that require only monthly payments. 15+ Day Delinquency Ratio is not annualized, but reflects balances at the end of the period.

Net Charge-off Rate

Net Charge-off Rate is calculated as our annualized net charge-offs for the period divided by the average Unpaid Principal Balance outstanding during the period. Net charge-offs are charged-off loans and finance receivables in the period, net of recoveries of prior charged-off loans and finance receivables in the period. For periods of less than one year, the metric is annualized based on four quarters per year and is not business day or calendar day-adjusted.

Efficiency Ratio

Efficiency Ratio is a measure of operating efficiency and is calculated as Total operating expense for the period divided by Gross revenue for the period.

Adjusted Efficiency Ratio