Form 10-K TECH DATA CORP For: Jan 31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 31, 2019

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 0-14625

TECH DATA CORPORATION

(Exact name of Registrant as specified in its charter)

Florida | 59-1578329 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

5350 Tech Data Drive Clearwater, Florida | 33760 |

(Address of principal executive offices) | (Zip Code) |

Securities registered pursuant to Section 12(b) of the Act:

Common stock, par value $.0015 per share

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by a check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by a check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “accelerated filer”, “large accelerated filer”, “smaller reporting company”, and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x | Accelerated filer | ¨ |

Non-accelerated filer | ¨ | Smaller reporting company | ¨ |

Emerging growth company | ¨ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

Aggregate market value of the voting stock held by non-affiliates was $3,167,323,009 based on the reported last sale price of common stock on July 31, 2018 which is the last business day of the registrant’s most recently completed second fiscal quarter.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

Class | March 14, 2019 |

Common stock, par value $.0015 per share | 36,900,698 |

DOCUMENTS INCORPORATED BY REFERENCE

The registrant’s Proxy Statement for use at the Annual Meeting of Shareholders to be held on June 5, 2019, is incorporated by reference in Part III of this Form 10-K to the extent stated herein.

1

TABLE OF CONTENTS

ITEM 1. | ||

ITEM 1A. | ||

ITEM 1B. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

ITEM 5. | ||

ITEM 6. | ||

ITEM 7. | ||

ITEM 7A. | ||

ITEM 8. | ||

ITEM 9. | ||

ITEM 9A. | ||

ITEM 9B. | ||

ITEM 10 | ||

ITEM 11 | ||

ITEM 12 | ||

ITEM 13 | ||

ITEM 14. | ||

ITEM 15. | ||

ITEM 16. | ||

2

PART I

ITEM 1. Business.

In this report, we use the terms "Tech Data,” "we," "our," "us" or the “Company” to refer to Tech Data Corporation and its consolidated subsidiaries.

OVERVIEW | ||||

Tech Data Corporation is one of the world’s largest IT distribution and solutions companies. We serve a critical role in the center of the IT ecosystem, bringing products from the world's leading technology vendors to market, as well as helping customers create solutions best suited to maximize business outcomes for their end-user customers. Our customers include value-added resellers (“VARs”), direct marketers, retailers, corporate resellers and managed service providers ("MSPs") who support the diverse technology needs of end users.

Tech Data was incorporated in 1974 to market data processing supplies to end users of mini and mainframe computers. With the advent of microcomputer dealers, we made the transition to a wholesale technology distributor in 1983 by broadening our product line to include personal computer products and withdrawing entirely from end-user sales. We went public with the initial public offering of Tech Data’s stock in 1986 on the NASDAQ Stock Exchange.

From fiscal 1989 through fiscal 2008, we expanded geographically through the acquisition of several distribution companies in the Americas and Europe, strengthening our position in certain product and customer segments. From fiscal 2008 to fiscal 2017, we continued to expand geographically, and to further diversify our products and solutions portfolio through organic investments and acquisitions, primarily focused on the data center, mobility, and software product categories.

On February 27, 2017, we acquired all the outstanding shares of Avnet, Inc.'s ("Avnet") Technology Solutions business ("TS") for an aggregate purchase price of approximately $2.8 billion, comprised of approximately $2.5 billion in cash and 2,785,402 shares of Tech Data common stock. TS delivered data center hardware and software solutions and services and the TS acquisition strengthened our end-to-end solutions portfolio and deepened our value added capabilities in the data center and next-generation technologies. The total cash consideration payable to Avnet was subject to certain working capital and other adjustments, as determined through the process established in the interest purchase agreement. In August 2018, we executed a settlement agreement with Avnet, resulting in a final working capital adjustment of $120 million, which was paid to Avnet during the fiscal year ended January 31, 2019 (see further discussion in Note 5 of Notes to Consolidated Financial Statements).

VENDORS AND CUSTOMERS | ||||

Our value proposition to our vendors:

• | Access to highly fragmented markets - We provide our vendors access to large and highly fragmented markets such as the small- and medium-sized business (“SMB”) sector, which relies on VARs, our primary customer base, to gain access to and support for new technology. |

• | Variable-cost route to market - We serve as a variable, cost effective route to market for our vendors by providing them with access to resellers throughout the Americas, Europe and Asia Pacific. |

• | Logistics management - Our world class logistics capabilities enable us to efficiently bring technology products to market through one of our 22 strategically located logistics centers, by direct shipment from vendors to customers, or virtually through our Tech Data cloud marketplace. |

• | Services - We provide a comprehensive portfolio of services to our vendors, including integration services, supply chain management services, and field, depot and support services, such as field engineering, equipment installation, maintenance, repair and many others. |

We distribute and market hundreds of thousands of products from over 1,000 of the world’s leading technology hardware manufacturers and software publishers, as well as suppliers of next-generation technologies and delivery models such as converged and hyper-converged infrastructure, the cloud, security, analytics/Internet of things ("IoT"), and services. These products are typically purchased directly from the vendor on a non-exclusive basis. Conversely, our vendor agreements do not restrict us from selling similar products manufactured by competitors, nor do they require us to sell a specified quantity of product. As a result, we have the flexibility to terminate or curtail sales of one product line in favor of another due to technological change, pricing considerations, product availability, and customer demand or vendor distribution policies. Overall, we believe that our diversified and evolving product and solutions portfolio provides a solid platform for continued growth.

3

The following table provides a comparison of sales generated from products purchased from vendors that exceeded 10% of our consolidated net sales for fiscal 2019, 2018 and 2017 (as a percent of consolidated net sales):

2019 | 2018 | 2017 | |

Apple, Inc. | 16% | 17% | 21% |

HP Inc. | 11% | 11% | 14% |

Cisco Systems, Inc. | 11% | 11% | 10% |

Our value proposition to our customers:

• | End-to-end solutions - We help our customers create comprehensive, multi-vendor solutions from the world's leading technology vendors in order to maximize business outcomes for their end-user customers. |

• | Logistics management - Our robust order and logistics management systems enable us to fulfill customer orders quickly and efficiently through one of our 22 strategically located logistics centers, by direct shipment from the vendor, or virtually through our Tech Data cloud marketplace. |

• | Financing and inventory management - We provide our customers with access to flexible financing programs and inventory management for the technology products, services and solutions they acquire. |

• | Training and technical support - We provide our reseller customers a high level of training and technical support. |

• | Services - We provide our customers with complete customer management solutions, including customer acquisition, enablement and revenue-growth services, such as contract renewals and software license compliance, as well as product configuration/integration services. In addition, we provide our resellers access to a number of special promotions and marketing services on behalf of our vendors. |

We serve one of the largest bases of resellers throughout the Americas, Europe and Asia-Pacific. Our products are purchased directly from vendors in significant quantities and are marketed to an active reseller base of over 125,000 VARs, direct marketers, retailers, corporate resellers and MSPs. Our VAR customers, in many cases, rely on Tech Data as their principal source of technology products and the related financing for the products. VARs typically prefer not to invest the resources to establish a large number of direct purchasing relationships with vendors or stock significant product inventories. Direct marketers, retailers and corporate resellers may establish direct relationships with vendors for their highest volume products, but utilize distributors as the primary source for other product requirements and an alternative source for products acquired directly. Our customers rely on our expertise and resources to gain vital insights into emerging technologies and to help them capture growth opportunities in a rapidly changing technology landscape. No single customer accounted for more than 10% of our net sales during fiscal 2019, 2018 and 2017.

4

OUR STRATEGY | ||||

We believe technology is changing faster today than at any other point in our company’s history. Digital transformation is reshaping our industry, not only enabling businesses and consumers to engage in more ways than ever before, but changing the way technology is acquired and deployed. Because of this, hybrid models of IT delivery and consumption are emerging, as workloads shift across technology platforms and hardware and software-based solutions become increasingly combined. End-users are demanding solutions that drive business outcomes, and these solutions are end-to-end containing multiple products and software solutions from multiple vendors. As a result, customers are seeking greater integration of products, services and solutions that tie technologies together. Therefore, we believe an IT distribution and solutions company must be end-to-end, with deep capabilities across the computing continuum to manage the increasingly complex IT ecosystem and deliver the solutions and business outcomes the market desires. Our vision for the future is to be the vital link in the IT ecosystem that enables channel partners to bring to market the technology solutions the world needs to connect, learn and advance.

To achieve our vision, we have identified five key elements that we believe define an IT distribution and solutions company:

• | Global Footprint with Local Execution - Global footprint that ensures we can support our channel partners around the world, with the local knowledge it takes to be successful. |

• | End-to-End Portfolio - An end-to-end portfolio of products, services and solutions to enable channel partners to create the best business outcomes for their customers. |

• | Specialized Skills - Extensive solutions-oriented technical capabilities and deep domain knowledge that span the IT continuum, with the ability to deploy them within specific customer verticals. |

• | World-Class IT Systems - A common IT platform that ensures consistent global execution and delivers efficiency and speed for a superior customer experience. |

• | Financial Strength - Financial strength and flexibility to invest in next-generation technologies. |

These five key elements are the building blocks to Tech Data’s future and our strategic priorities are directly aligned with each of them. To strengthen our role at the center of the IT ecosystem well into the future, we are moving to higher value, focused on the following strategic priorities:

• | Invest in next-generation technologies and delivery models such as the cloud, security, analytics/IoT, and services. |

• | Strengthen our end-to-end portfolio of products, services and solutions. |

• | Transform our company digitally through greater automation, which we believe will enhance the customer experience, improve productivity and reduce costs. |

• | Optimize our global footprint by enhancing the operational efficiency and effectiveness of our businesses around the world. |

We believe our focus on these priorities will enable us to achieve our financial objectives of:

• | Growing faster than the industry in select markets by gaining profitable market share in key geographies within select product categories with leading vendors. |

• | Improving operating income by growing gross profit faster than operating costs. |

• | Delivering a return on invested capital above our weighted average cost of capital. |

PRODUCTS AND SERVICES | ||||

To enable a specialized approach to the market while maintaining the exceptional service levels that channel partners expect from us, we group our offerings into two primary solutions portfolios:

Endpoint Solutions Portfolio:

• | Our Endpoint Solutions portfolio primarily includes PC systems, mobile phones and accessories, printers, peripherals, supplies, endpoint technology software and consumer electronics. |

Advanced Solutions Portfolio:

• | Our Advanced Solutions portfolio primarily includes data center technologies such as storage, networking, servers, advanced technology software and converged and hyper-converged infrastructure. Our Advanced Solutions portfolio also includes our specialized solution businesses. |

Our next-generation technology solutions, along with our services offerings, span our Endpoint and Advanced Solutions portfolios.

5

SALES AND ELECTRONIC COMMERCE | ||||

Our sales team consists of field sales and inside sales representatives. Our sales representatives receive comprehensive training on our policies, procedures and the technical specifications of products, and attend additional training offered by our vendors. Field sales representatives are typically located in major metropolitan areas in their respective geographies and are supported by inside telemarketing sales teams covering a designated territory. Our team concept provides a strong personal relationship between us and our customers, who typically call our inside sales teams on dedicated telephone numbers or contact us through various electronic methods to place orders. If the product is in stock and the customer has available credit, customer orders are generally shipped the same day from the logistics center nearest the customer or the intended end user.

Customers often utilize our electronic ordering and information systems. Through our e-commerce website, customers can gain remote access to our information systems to place orders, or check order status, inventory availability and pricing. Certain larger customers have electronic data interchange ("EDI") services available whereby orders, order acknowledgments, invoices, inventory status reports, customized pricing information and other industry standard EDI transactions are generated online, which improves efficiency and timeliness for us and our customers.

We realize improved productivity, cost savings, and enhanced customer experience through automation and digitization, and we will continue to invest in and improve our digital ordering and information systems.

COMPETITION | ||||

We operate in a market characterized by intense competition, based on such factors as product availability, credit terms and availability, price, speed of delivery, effectiveness of information systems and e-commerce tools, ability to tailor solutions to customers' needs, quality and depth of product lines and training, as well as service and support provided by the distributor to the customer. We believe we are well equipped to compete effectively with other distributors in all of these areas.

We compete against several distributors in the Americas market, including Ingram Micro Inc. ("Ingram Micro"), Synnex Corp. ("Synnex"), and Arrow Electronics, Inc. (“Arrow”), along with some regional and local distributors. The competitive environment in Europe is more fragmented, with market share spread among several regional and local competitors such as ALSO Holding and Esprinet, as well as international distributors such as Ingram Micro, Westcon Group, Inc., and Arrow.

We also face competition from companies entering or expanding into the logistics and product fulfillment and e-commerce supply chain services market. Additionally, certain direct sales relationships between manufacturers, resellers and end-users continue to introduce change into the competitive landscape of our industry. As we expand our business into new areas, we may face increased competition from other distributors as well as vendors. However, we believe vendors will continue to sell their products through distributors such as Tech Data, due to our ability to provide them with access to our broad customer base and serve them in a highly cost-effective and efficient manner. Our logistics management capabilities, as well as our sales and marketing, credit and product management expertise, allow our vendors to expand their market coverage while lowering their selling, inventory and fulfillment costs.

EMPLOYEES | ||||

On January 31, 2019, we had over 14,000 employees (as measured on a full-time equivalent basis) in more than forty countries on five continents. Certain of our employees in various countries outside of the United States are subject to laws providing representation rights to employees through workers' councils. Our success depends on the talent and dedication of our employees and we strive to attract, hire, develop and retain outstanding employees. We believe significant benefits are realized from having a strong and seasoned management team with many years of experience in technology distribution and related industries. We consider relations with our employees to be good.

FOREIGN AND DOMESTIC OPERATIONS AND EXPORT SALES | ||||

We sell to customers in more than 100 countries throughout North America, South America, Europe, the Middle East, Africa and the Asia-Pacific region. Over the past several years, we have expanded our presence in certain existing markets and exited certain markets based upon our assessment of, among other factors, our earnings potential and the risk exposure in those markets, including foreign currency exchange, regulatory and political risks. To the extent we decide to close any of our operations, we may incur charges and operating losses related to such closures and recognize a portion of our accumulated other comprehensive income in connection with such a disposition. For information on our net sales, operating income and identifiable assets by geographic region, see Note 15 of Notes to Consolidated Financial Statements.

6

SEASONALITY | ||||

Our quarterly operating results have fluctuated significantly in the past and will likely continue to do so in the future as a result of currency fluctuations and seasonal variations in the demand for the products and services we sell. Narrow operating margins may magnify the impact of these factors on our quarterly operating results. Historical seasonal variations have included an increase in European demand during our fiscal fourth quarter and decreased demand in other fiscal quarters. The seasonal trend in Europe typically results in greater operating leverage, and therefore, lower SG&A as a percentage of net sales in the region and on a consolidated basis during the second half of our fiscal year, particularly in our fourth quarter.

ASSET MANAGEMENT | ||||

We manage our inventories in a manner that allows us to maintain sufficient quantities to achieve high order fill rates while attempting to stock only those products in high demand that have a rapid turnover rate. Our business, like that of other distributors, is subject to the risk that the value of inventory will be impacted adversely by suppliers’ price reductions or by technological changes affecting the usefulness or desirability of the products comprising the inventory. Our contracts with many of our vendors provide price protection and stock rotation privileges to reduce the risk of loss due to manufacturer price reductions and slow moving or obsolete inventory. In the event of a vendor price reduction, we generally receive a credit for the impact on products in inventory and we have the right to rotate a certain percentage of purchases, subject to certain limitations. Historically, price protection and stock rotation privileges, as well as our inventory management procedures, have helped reduce the risk of loss of inventory value.

We attempt to control losses on credit sales by closely monitoring customers’ creditworthiness through our IT systems, which contain detailed information on each customer’s payment history and other relevant information. In certain countries, we have obtained credit insurance that insures a percentage of the credit extended by us to certain customers against possible loss. The Company also has arrangements with certain finance companies that provide inventory financing facilities to our customers as an additional approach to mitigate credit risk. Certain of our vendors subsidize these financing arrangements for the benefit of our customers. We also sell products on a prepayment, credit card and cash-on-delivery basis.

7

ADDITIONAL INFORMATION AVAILABLE | ||||

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended. We therefore file our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Proxy Statements, and other documents with the Securities and Exchange Commission (the “SEC”). The SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements and other information.

Our principal Internet address is www.techdata.com. We make available free of charge, through our website, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports, as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. Information on Tech Data’s website is not incorporated into this Form 10-K or the Company’s other securities filings and is not a part of them.

EXECUTIVE OFFICERS | ||||

The following table sets forth the name, age and title of each of the persons who were serving as executive officers of Tech Data as of March 20, 2019:

Name | Age | Title | ||

Richard T. Hume | 59 | Chief Executive Officer | ||

Charles V. Dannewitz | 64 | Executive Vice President, Chief Financial Officer | ||

Beth E. Simonetti | 53 | Executive Vice President, Chief Human Resources Officer | ||

John A. Tonnison | 50 | Executive Vice President, Chief Information Officer | ||

David R. Vetter | 59 | Executive Vice President, Chief Legal Officer | ||

Joseph H. Quaglia | 54 | President, Americas | ||

Patrick Zammit | 52 | President, Europe | ||

Michael Rabinovitch | 49 | Senior Vice President, Chief Accounting Officer and Controller | ||

Richard T. Hume, Chief Executive Officer, joined the Company in March 2016 as Executive Vice President, Chief Operating Officer. In June 2018, the Company's Board of Directors (the “Board”) appointed Mr. Hume as Chief Executive Officer. Prior to joining the Company, Mr. Hume was employed for more than thirty years at IBM. Most recently, from January 2015 to February 2016, Mr. Hume served as General Manager and Chief Operating Officer of Infrastructure and Outsourcing. Prior to that position, from January 2012 to January 2015, Mr. Hume served as General Manager, Europe where he led IBM’s multi-brand European organization. From 2008 to 2011, Mr. Hume served as General Manager, Global Business Partners, directing the growth and channel development initiatives for IBM’s Business Partner Channel. Mr. Hume holds a Bachelor of Science degree in Accounting from Pennsylvania State University.

Charles V. Dannewitz, Executive Vice President, Chief Financial Officer, joined the Company in February 1995 as Vice President of Taxes. He was promoted to Senior Vice President of Taxes in March 2000, and assumed responsibility for worldwide treasury operations in July 2003. In February 2014, he was appointed Senior Vice President, Chief Financial Officer, Americas. In June 2015, he was promoted to Executive Vice President, Chief Financial Officer. Prior to joining the Company, Mr. Dannewitz was employed by Price Waterhouse from 1981 to 1995, most recently as a tax partner. Mr. Dannewitz is a Certified Public Accountant and holds a Bachelor of Science degree in Accounting from Illinois Wesleyan University.

Beth E. Simonetti, Executive Vice President, Chief Human Resources Officer, joined the company in September 2015 as Senior Vice President, Chief Human Resources Officer and was promoted to Executive Vice President in January 2017. Prior to joining Tech Data, Ms. Simonetti served as Senior Vice President, Human Resources at Baker & Taylor, Inc. since 2010. Previously, she was an executive search consultant and was with Cardinal Health for 12 years in various HR leadership positions. Ms. Simonetti holds a Bachelor of Science degree from Miami University in Ohio and a Masters of Hospital and Health Services Administration from Ohio State University.

John A. Tonnison, Executive Vice President, Chief Information Officer, joined the Company in March 2001 as Vice President, Worldwide E-Business and was promoted to Senior Vice President of IT Americas in December 2006. In February 2010, he was appointed Executive Vice President, Chief Information Officer. Prior to joining the Company, Mr. Tonnison held executive management positions in the U.S., United Kingdom and Germany with Computer 2000, Technology Solutions Network and Mancos Computers. Mr. Tonnison was educated in the United Kingdom and became a U.S. citizen in 2006.

David R. Vetter, Executive Vice President, Chief Legal Officer, joined the Company in June 1993 as Vice President, General Counsel and was promoted to Corporate Vice President, General Counsel in April 2000. In March 2003, he was promoted to Senior Vice President, and effective July 2003, was appointed Secretary. In January 2017, Mr. Vetter was promoted to Executive Vice President, Chief Legal Officer. Prior to joining the Company, Mr. Vetter was employed by the law firm of Robbins, Gaynor & Bronstein, P.A. from 1984 to 1993, most recently as a partner. Mr. Vetter is a member of the Florida Bar Association and holds Bachelor of Arts degrees in English and Economics from Bucknell University and a Juris Doctorate Degree from the University of Florida.

Joseph H. Quaglia, President, Americas, joined the Company in May 2006 as Vice President, East and Government Sales and was promoted to Senior Vice President of U.S. Marketing in November 2007. In February 2012, he was appointed to the additional role of

8

President, TDMobility and he was promoted to President, Americas in November 2013. Prior to joining the Company, Mr. Quaglia held senior management positions with CA Technologies, StorageNetworks Inc. and network software provider Atabok. Mr. Quaglia holds a Bachelor of Science degree in Computer Science from Indiana State University and an M.B.A. from Butler University.

Patrick Zammit, President, Europe, joined the Company in February 2017 through Tech Data's acquisition of Avnet’s Technology Solutions business as President, Europe. Prior to his appointment at the Company, Mr. Zammit was employed for more than twenty years at Avnet, Inc. Most recently, from January 2015 to January 2017, Mr. Zammit served as Global President of Avnet Technology Solutions. Prior to that position, from October 2006 until January 2015, Mr. Zammit served as President of Avnet Electronics Marketing EMEA. From 1993 to 2006, Mr. Zammit served in management positions of increasing responsibilities. Prior to joining Avnet, Mr. Zammit was employed by Arthur Andersen from 1989 to 1993. Mr. Zammit holds a Masters in Business Administration equivalent from Paris Business School ESLSCA.

Michael Rabinovitch, Senior Vice President, Chief Accounting Officer and Controller, joined the Company in March 2018 as Senior Vice President, Chief Accounting Officer and Controller. Prior to joining Tech Data, Mr. Rabinovitch was employed at Office Depot, Inc. from January 2015 to February 2018, where he served as Senior Vice President, Finance and Chief Accounting Officer beginning in March 2017 and Vice President of Finance, North America from January 2015 to March 2017. Prior to joining Office Depot, Inc., Mr. Rabinovitch was the Executive Vice President and Chief Financial Officer of Birks Group, a North American manufacturer and retailer of fine jewelry and luxury timepieces, from 2005 through 2014. Prior to joining Birks Group, Mr. Rabinovitch was Vice President of Finance of Claire’s Stores, Inc., a specialty retailer of fashion jewelry and accessories, from 1999 to 2005. Prior to joining Claire’s Stores, Inc., Mr. Rabinovitch was Vice President of Accounting and Corporate Controller at an equipment leasing company and spent five years with Price Waterhouse. Mr. Rabinovitch is a licensed Certified Public Accountant (inactive) and holds Bachelor of Science degrees in Accounting and Finance from Florida State University.

9

ITEM 1A. Risk Factors.

The following are certain risk factors that could affect our business, financial position and results of operations. These risk factors should be considered in connection with evaluating the forward-looking statements contained in this Annual Report on Form 10-K because these factors could cause the actual results and conditions to differ materially from those projected in the forward-looking statements. Before you buy our common stock or other securities, you should know that making such an investment involves risks, including the risks described below. The risks that have been highlighted below are not the only risks of our business. If any of the risks actually occur, our business, financial condition or results of operations could be negatively affected. In that case, the trading price of our common stock or other securities could decline, and you may lose all or part of your investment. Risk factors that could cause actual results to differ materially from our forward-looking statements are as follows:

Our ability to earn profit is more challenging when sales slow from a down economy as a result of gross profit declining faster than cost reduction efforts taking effect.

Adverse economic conditions may result in lower demand for the products and services we sell. When we experience a rapid decline in demand for products we experience more difficulty in achieving the gross profit and operating profit we desire due to the lower sales and increased pricing pressure. The economic environment may also result in changes in vendor terms and conditions, such as rebates, cash discounts and cooperative marketing efforts, which may also result in downward pressure on our gross profit. As a result, there is pressure to reduce the cost of operations in order to maximize operating profits. To the extent we cannot reduce costs to offset such decline in gross profits, our operating profits typically deteriorate. The benefits from cost reductions may also take longer to fully realize and may not fully mitigate the impact of the reduced demand or changes in vendor terms and conditions. Should we experience a decline in operating profits or not achieve the planned level of growth in operations of previously acquired companies, the valuations we develop for purposes of our goodwill impairment test may be adversely affected, potentially resulting in impairment charges. Deterioration in the financial and credit markets heightens the risk of customer bankruptcies and delays in payment. Future deterioration in the credit markets could result in reduced availability of credit insurance to cover customer accounts. This, in turn, may result in our reducing the credit lines we provide to customers, thereby having a negative impact on our net sales, gross profits and net income.

Our competitors can take more market share by reducing prices on vendor products that contribute the most to our profitability.

The technology distribution industry is characterized by intense competition, based primarily on product availability, credit terms and availability, price, effectiveness of information systems and e-commerce tools, speed of delivery, ability to tailor specific solutions to customer needs, quality and depth of product lines and training, service and support. Our customers are not required to purchase any specific volume of products from us and may move business if pricing is reduced by competitors, resulting in lower sales. As a result, we must be extremely flexible in determining when to reduce prices to maintain market share and sales volumes and when to allow our sales volumes to decline to maintain the quality of our profitability. We compete with a variety of regional, national and international wholesale distributors, some of which may have greater financial resources than us.

We are dependent on internal information and telecommunications systems, and any failure of these systems, including system security breaches, data protection breaches or other cybersecurity attacks, may negatively impact our business and results of operations.

Cyber-attacks and other tactics designed to gain access to and exploit sensitive information by breaching mission critical systems of large organizations are constantly evolving and have been increasing in sophistication in recent years. High profile security breaches leading to unauthorized release of sensitive information have occurred with increasing frequency at a number of major U.S. companies, despite widespread recognition of the cyber-attack threat and improved data protection methods. In addition, regulations related to data protection, including the European Union’s General Data Protection Regulation (“GDPR”) which took effect in May 2018, create a range of new compliance obligations for the Company. While to date we have not experienced a significant data loss, significant compromise or any material financial losses related to cybersecurity attacks, our systems, those of our customers, and those of our third-party service providers are under constant threat. Cybercrime, including phishing, social engineering, attempts to overload our servers with denial-of-service attacks, or similar disruptions from unauthorized access to our systems, could cause us critical data loss or the disclosure or use of personal or other confidential information. Outside parties may attempt to fraudulently induce employees to disclose personally identifiable information or other confidential information which could expose us to a risk of loss or misuse of this information.

We are dependent on internal information and telecommunications systems, and we are vulnerable to failure of these systems, including through system security breaches, data protection breaches or other cybersecurity attacks. If these events occur, the unauthorized disclosure, loss or unavailability of data and disruption to our business may have a material adverse effect on our reputation and harm our relationships with vendors and customers. Additionally, these events may lead to financial losses from remedial actions, or potential liability from fines, including in relation to noncompliance with the GDPR, as well as possible litigation and punitive damages. Failures of our internal information or telecommunications systems may prevent us from taking customer orders, shipping products and billing customers. Sales may also be impacted if our customers are unable to access our pricing and product availability information. The occurrence of any of these events could have a material adverse impact on our business and results of operations.

10

We may not be able to ship products if our third party shipping companies cease operations temporarily or permanently.

We rely on arrangements with independent shipping companies for the delivery of our products from vendors and to customers. The failure or inability of these shipping companies to deliver products or the unavailability of their shipping services, even temporarily, may have an adverse effect on our business and our operating results.

Natural disasters may negatively impact our business and results of operations.

Certain of our facilities, including our corporate headquarters in Clearwater, Florida, are located in geographic areas that heighten our exposure to hurricanes, tropical storms and other severe weather events. Future weather events could cause severe damage to our property and technology and could cause major disruptions to our operations. We carry property damage and business interruption insurance; however, there can be no assurance that such insurance would be adequate to cover any losses we may incur. As such, a hurricane, tropical storm or severe weather event may have an adverse effect on our business, financial condition or results of operations.

If our vendors do not continue to provide price protection for inventory we purchase from them, our profit from the sale of that inventory may decline.

It is very typical in our industry that the value of inventory will decline as a result of price reductions by vendors or technological obsolescence. It is the policy of many of our vendors to protect distributors from the loss in value of inventory due to technological change or the vendors' price reductions. Some vendors, however, may be unwilling or unable to pay us for price protection claims or products returned to them under purchase agreements. Moreover, industry practices are sometimes not embodied in written agreements and do not protect us in all cases from declines in inventory value. No assurance can be given that such practices to protect distributors will continue, that unforeseen new product developments will not adversely affect us or that we will be able to successfully manage our existing and future inventories.

Failure to obtain adequate product supplies from our largest vendors, or terminations of a supply or services agreement, or a significant change in vendor terms or conditions of sale by our largest vendors may negatively affect our financial condition or results of operations.

A significant percentage of our revenues are from products we purchase from certain vendors, such as Apple, Inc., HP Inc. and Cisco Systems, Inc. These vendors have significant negotiating power over us and rapid, significant or adverse changes in sales terms and conditions, such as reducing the amount of price protection and return rights as well as reducing the level of purchase discounts and rebates they make available to us, may reduce the profit we can earn on these vendors' products and result in loss of revenue and profitability. Our gross profit could be negatively impacted if we are unable to pass through the impact of these changes to our customers or cannot develop systems to manage ongoing vendor programs. Additionally, changes in vendor payment terms could negatively impact our financial condition. Our standard vendor distribution agreement permits termination without cause by either party upon 30 days notice. The loss of a relationship with any of our key vendors, a change in their strategy (such as increasing direct sales), the merger or reorganization of significant vendors or significant changes in terms on their products may adversely affect our business.

We conduct business in countries outside of the U.S., which exposes us to fluctuations in foreign currency exchange rates that result in losses in certain periods.

Approximately 61%, 62% and 65% of our net sales in fiscal 2019, 2018 and 2017 were generated in countries outside of the U.S., which exposes us to fluctuations in foreign currency exchange rates. We may enter into short-term forward exchange or option contracts to hedge this risk. Nevertheless, volatile foreign currency exchange rates increase our risk of loss related to products purchased in a currency other than the currency in which those products are sold. While we maintain policies to protect against fluctuations in currency exchange rates, extreme fluctuations have resulted in our incurring losses in some countries. Furthermore, our local competitors in certain markets may have different purchasing models that provide them reduced foreign currency exposure compared to us. This may result in market pricing that we cannot meet without significantly lower profit on sales. In addition, we may be exposed to foreign exchange risk that may occur as a result of the United Kingdom's (“U.K.”) potential withdrawal from the European Union, commonly referred to as "Brexit". Brexit may adversely affect global economic and market conditions and could contribute to volatility in the foreign exchange markets, which we may be unable to effectively manage through our foreign exchange risk management program.

The translation of the financial statements of foreign operations into U.S. dollars is also impacted by fluctuations in foreign currency exchange rates, which may positively or negatively impact our results of operations. In addition, the value of our equity investment in foreign countries may fluctuate based upon changes in foreign currency exchange rates. These fluctuations, which are recorded in a cumulative translation adjustment account, may result in losses in the event a foreign subsidiary is sold or closed at a time when the foreign currency is weaker than when we made investments in the country. The realization of any or all of these risks could have a significant adverse effect on our financial results.

11

We have international operations which expose us to risks associated with conducting business in multiple jurisdictions.

Our international operations are subject to other risks such as the imposition of governmental controls, export license requirements, restrictions on the export of certain technology, political instability, trade restrictions, tariff changes, uncertainty surrounding the implementation and effects of Brexit, difficulties in staffing and managing international operations, changes in the interpretation and enforcement of laws (in particular related to items such as duty and taxation), difficulties in collecting accounts receivable, longer collection periods, the impact of local economic conditions and practices, uncertainties arising from local business practices and cultural considerations, and enforcement of the Foreign Corrupt Practices Act, or similar laws of other jurisdictions. Recently, the U.S. government imposed tariffs on certain products imported into the U.S. and the Chinese government imposed tariffs on certain products imported into China, which have increased the prices of many of the products that the company purchases from its suppliers. The new tariffs, along with any additional tariffs or trade restrictions that may be implemented by the U.S. or other countries, could result in further increased prices. While the company intends to pass price increases on to our customers, the effect of tariffs on prices may impact sales and results of operations. There can be no assurance that these and other factors will not have an adverse effect on our business.

Changes in tax laws or tax rulings in the jurisdictions in which we operate may materially impact our financial position and results of operations. The Organization for Economic Cooperation and Development has been working on the Base Erosion and Profit Sharing Project, and has issued and will continue to issue, guidelines and proposals that may change various aspects of the existing framework under which our tax obligations are determined in many of the countries in which we do business. Certain countries are evaluating their tax policies and regulations, which could affect international business and may have an adverse effect on our overall tax rate, along with increasing the complexity, burden and cost of tax compliance. For example, on December 22, 2017, the U.S. federal government enacted the U.S. Tax Cuts and Jobs Act (“U.S. Tax Reform”) which significantly revised U.S. corporate income tax law by, among other things, reducing the U.S. federal corporate income tax rate from 35% to 21% and implementing a modified territorial tax system that includes a one-time transition tax on deemed repatriated earnings of foreign subsidiaries (see Note 9 of Notes to Consolidated Financial Statements for further discussion). Additional changes in the U.S. tax regime or in how U.S. multinational corporations are taxed on foreign earnings, including changes in how existing tax laws are interpreted or enforced, could adversely affect our business, financial condition or results of operations.

In addition, while our labor force in the U.S. is currently non-union, employees of certain other subsidiaries are subject to collective bargaining or similar arrangements. We do business in certain foreign countries where labor disruption is more common than is experienced in the U.S. and some of the freight carriers we use are unionized. A labor strike by a group of our employees, one of our freight carriers, one of our vendors, a general strike by civil service employees or a governmental shutdown could have an adverse effect on our business. Many of the products we sell are manufactured in countries other than the countries in which our logistics centers are located. The inability to receive products into the logistics centers because of government action or labor disputes at critical ports of entry may have an adverse effect on our business.

12

We have incurred substantial indebtedness that may impact our financial position and subject us to financial and operating restrictions, decrease our access to capital, and / or increase our borrowing costs, which may adversely affect our operations and financial results.

Our business requires substantial capital to operate and to finance accounts receivable and product inventory that are not financed by trade creditors. We have historically relied upon cash generated from operations, bank credit lines, trade credit from vendors, accounts receivable purchase agreements, proceeds from public offerings of our common stock and proceeds from debt offerings to satisfy our capital needs and to finance growth. The incurrence of debt under our Senior Notes and other credit facilities subject us to financial and operating covenants, which may limit our ability to borrow and our flexibility in responding to our business needs.

As of January 31, 2019, we had approximately $1.4 billion of total debt. If we are not able to maintain compliance with stated financial covenants or if we breach other covenants in any debt agreement, we could be in default under such agreement. Such a default may allow our creditors to accelerate the related debt and may result in the acceleration of any other debt to which a cross acceleration or cross-default provision applies. Our overall leverage and terms of our financing could, among other things:

• | limit our ability to obtain additional financing in the future for working capital, capital expenditures, acquisitions or for general corporate purposes; |

• | make it more difficult to satisfy our obligations under the terms of our debt; |

• | limit our ability to refinance our debt on terms acceptable to us or at all; |

• | make it more difficult to obtain trade credit from vendors; |

• | limit our flexibility to plan for and adjust to changing business and market conditions and repurchase shares of our common stock; and |

• | increase our vulnerability to general adverse economic and industry conditions. |

Changes in our credit rating or other market factors may increase our interest expense or other costs of capital.

Certain of our financing instruments involve variable rate debt, thus exposing us to the risk of fluctuations in interest rates. In addition, the interest rate payable on the 3.70% Senior Notes and the 4.95% Senior Notes (each as defined herein) and certain other credit facilities would be subject to adjustment from time to time if our credit rating is downgraded. The U. K.’s Financial Conduct Authority, which regulates LIBOR, announced that it intends to phase out LIBOR by the end of 2021. The U.S. Federal Reserve has begun publishing a Secured Overnight Funding Rate (“SOFR”), which is intended to replace U.S. dollar LIBOR. Plans for alternative reference rates for other currencies have also been announced. At this time, we cannot predict how markets will respond to these proposed alternative rates or the effect of any changes to LIBOR or the discontinuation of LIBOR. If LIBOR is no longer available or if our lenders have increased costs due to changes in LIBOR, we may experience potential increases in interest rates on our variable rate debt, which could adversely impact our interest expense, results of operations and cash flows.

We cannot predict what losses we might incur in litigation matters, regulatory enforcement actions and contingencies that we may be involved with from time to time.

We cannot predict what losses we might incur from litigation matters, regulatory enforcement actions and contingencies that we may be involved with from time to time. There are various other claims, lawsuits and pending actions against us. We do not expect that the ultimate resolution of these matters will have a material adverse effect on our consolidated financial position. However, the resolution of certain of these matters could be material to our operating results for any particular period, depending on the level of income for such period. We can make no assurances that we will ultimately be successful in our defense of any of these matters.

13

ITEM 1B. Unresolved Staff Comments.

Not applicable.

ITEM 2. Properties.

Our executive offices are located in Clearwater, Florida. As of January 31, 2019, we operated a total of 22 logistics centers and a number of smaller stocking locations to provide our customers timely delivery of products. These logistic centers are located in the following principal markets: The Americas - 10, Europe - 10, and Asia-Pacific - 2.

As of January 31, 2019, we leased or owned approximately 9.0 million square feet of space. We own approximately 2.6 million square feet of our facilities in the Americas and lease the majority of our facilities and office space in other regions. Our facilities are well maintained and are adequate to conduct our current business. We do not anticipate significant difficulty in renewing our leases as they expire or securing replacement facilities.

ITEM 3. Legal Proceedings.

Prior to fiscal 2004, one of our subsidiaries, located in Spain, was audited in relation to various value added tax (“VAT”) matters and received notices of assessment related to fiscal years 1994 through 2001 that alleged the subsidiary did not properly collect and remit VAT. The Spanish subsidiary appealed these assessments beginning in March 2010. The matters related to fiscal years 1996 through 2001 were resolved during fiscal 2016. During fiscal 2017, the Spanish National Appellate Court issued an opinion upholding the assessments for fiscal years 1994 and 1995. We appealed this opinion to the Spanish Supreme Court, however, certain of the amounts assessed were not eligible to be appealed to the Spanish Supreme Court. As a result, we increased our accrual for costs associated with this matter by $2.6 million during fiscal 2017, including $1.5 million recorded in "value added tax assessments" and $1.1 million recorded in "interest expense" in the Consolidated Statement of Income.

During fiscal 2018, the Spanish Supreme Court issued a decision upholding the assessment for fiscal years 1994 and 1995. As a result, we increased our accrual for costs associated with this matter by $2.1 million, including $1.2 million recorded in "value added tax assessments" and $0.9 million recorded in "interest expense" in the Consolidated Statement of Income. As of January 31, 2018, we had recorded a liability of approximately $10.7 million for the entire amount of the remaining assessments, including various penalties and interest. During fiscal 2019, we paid the assessed amounts and recorded a benefit in interest expense of $0.9 million to adjust our accrual for estimated interest costs to the final assessed amount.

In December 2010, in a non-unanimous decision, a Brazilian appellate court overturned a 2003 trial court which had previously ruled in favor of our Brazilian subsidiary related to the imposition of certain taxes on payments abroad related to the licensing of commercial software products, commonly referred to as “CIDE tax”. We estimate the total exposure related to CIDE tax, including interest, was approximately $20.4 million at January 31, 2019. The Brazilian subsidiary has appealed the unfavorable ruling to the Supreme Court and Superior Court, Brazil's two highest appellate courts. Based on the legal opinion of outside counsel, we believe that the chances of success on appeal of this matter are favorable and the Brazilian subsidiary intends to vigorously defend its position that the CIDE tax is not due. Accordingly, we have not recorded an accrual for the total estimated CIDE tax exposure. However, due to the lack of predictability of the Brazilian court system, we have concluded that it is reasonably possible that the Brazilian subsidiary may incur a loss up to the total exposure described above. We believe the resolution of this litigation will not be material to our consolidated net assets or liquidity.

In June 2013, we were the subject of a document seizure by the French Autorité de la Concurrence (Competition Authority), following allegations of anticompetitive distribution practices in the French market for the products of one of our suppliers. In October 2018, the Competition Authority delivered a notification des griefs (statement of objections) to the Company, stating that the Competition Authority is pursuing charges against the Company in this matter. The Competition Authority has taken similar action against our supplier and another of its distributors. At this time, we cannot determine the likelihood of loss or reasonably estimate the range of any loss arising from this proceeding.

We are subject to various other legal proceedings and claims arising in the ordinary course of business. Our management does not expect that the outcome in any of these other legal proceedings, individually or collectively, will have a material adverse effect on our financial condition, results of operations, or cash flows.

ITEM 4. Mine Safety Disclosures.

Not applicable.

14

PART II

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is traded on the NASDAQ Stock Market, Inc. (“NASDAQ”) under the symbol “TECD.” We have not paid cash dividends since fiscal 1983 and the Board of Directors has no current plans to institute a cash dividend payment policy in the foreseeable future. As of March 14, 2019, there were 193 holders of record.

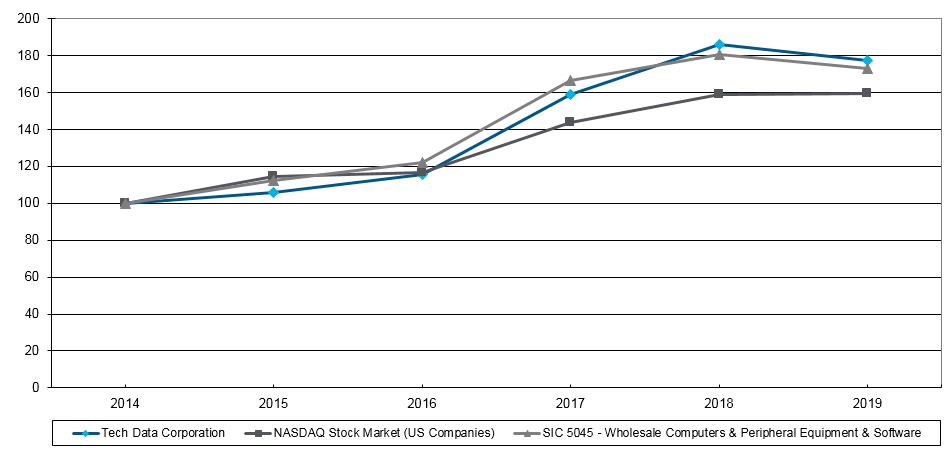

STOCK PERFORMANCE CHART

The five-year stock performance chart below assumes an initial investment of $100 on February 1, 2014 and compares the cumulative total return for Tech Data, the NASDAQ Stock Market (U.S.) Index, and the Standard Industrial Classification, or SIC, Code 5045 – Computer and Peripheral Equipment and Software. The comparisons in the table are provided in accordance with SEC requirements and are not intended to forecast or be indicative of possible future performance of our common stock.

Comparison of Cumulative Total Return

Assumes Initial Investment of $100 on February 1, 2014

Among Tech Data Corporation,

NASDAQ Stock Market (U.S.) Index and SIC Code 5045

2014 | 2015 | 2016 | 2017 | 2018 | 2019 | ||||||

Tech Data Corporation | 100 | 106 | 116 | 159 | 186 | 177 | |||||

NASDAQ Stock Market (U.S.) Index | 100 | 115 | 117 | 144 | 159 | 159 | |||||

SIC Code 5045 – Computer and Peripheral Equipment and Software | 100 | 112 | 122 | 167 | 181 | 173 | |||||

Securities Authorized for Issuance under Equity Compensation Plans

Information regarding the Securities Authorized for Issuance under Equity Compensation Plans can be found under Item 12 of this Report.

Unregistered Sales of Equity Securities

None.

15

Issuer Purchases of Equity Securities

On October 2, 2018, the Company's Board of Directors authorized a share repurchase program for up to $200.0 million of the

Company's common stock. During the year ended January 31, 2019, there were 1,429,154 shares repurchased by the Company at an average price of $74.89 per share, for a total cost, including expenses, of approximately $107.0 million under the program. As of January 31, 2019, the Company had approximately $93.0 million available for future repurchases of its common stock under the authorized share repurchase program.

The following table presents information with respect to purchases of common stock by the Company under the share repurchase program during the quarter ended January 31, 2019:

Issuer Purchases of Equity Securities | ||||||||||||||

Period | Total number of shares purchased | Average price paid per share | Total number of shares purchased as part of a publicly announced plan or program | Maximum dollar value of shares that may yet be purchased under the plan or programs | ||||||||||

November 1 - November 30, 2018 | 421,833 | $ | 73.97 | 421,833 | $ | 125,000,053 | ||||||||

December 1 - December 31, 2018 | 297,368 | 82.47 | 297,368 | 100,475,560 | ||||||||||

January 1 - January 31, 2019 | 88,513 | 84.74 | 88,513 | 92,975,378 | ||||||||||

Total | 807,714 | $ | 78.28 | 807,714 | ||||||||||

Subsequent to January 31, 2019, the Company’s Board of Directors authorized the repurchase of up to an additional $100.0 million of the Company's common stock.

16

ITEM 6. Selected Financial Data.

The following table sets forth certain selected consolidated financial data. This information should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and our consolidated financial statements and notes thereto appearing elsewhere in this Annual Report.

FIVE-YEAR FINANCIAL SUMMARY | |||||||||||||||||||

Year ended January 31: | 2019 | 2018 (1) | 2017 | 2016 | 2015 | ||||||||||||||

(in thousands, except per share data) | (As Adjusted) (2) | (As Adjusted) (2) | |||||||||||||||||

Income statement data: | |||||||||||||||||||

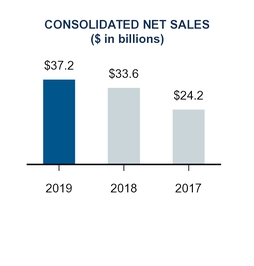

Net sales | $ | 37,238,950 | $ | 33,597,841 | $ | 24,193,697 | $ | 26,379,783 | $ | 27,670,632 | |||||||||

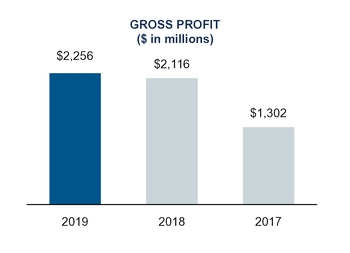

Gross profit | 2,255,899 | 2,115,621 | 1,301,927 | 1,286,661 | 1,393,954 | ||||||||||||||

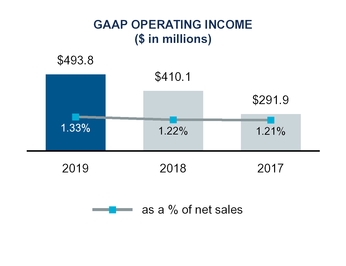

Operating income (3) (4) (5) (6) | 493,802 | 410,079 | 291,902 | 401,428 | 267,635 | ||||||||||||||

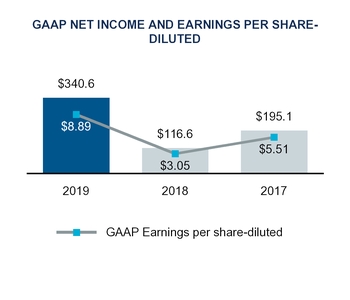

Net income (7) | $ | 340,580 | $ | 116,641 | $ | 195,095 | $ | 265,736 | $ | 175,172 | |||||||||

Earnings per share—basic | $ | 8.94 | $ | 3.07 | $ | 5.54 | $ | 7.40 | $ | 4.59 | |||||||||

Earnings per share—diluted | $ | 8.89 | $ | 3.05 | $ | 5.51 | $ | 7.36 | $ | 4.57 | |||||||||

Dividends per common share | — | — | — | — | — | ||||||||||||||

Balance sheet data: | |||||||||||||||||||

Working capital (8) | $ | 2,085,889 | $ | 2,095,573 | $ | 2,701,472 | $ | 1,889,415 | $ | 1,834,997 | |||||||||

Total assets | 12,986,552 | 12,920,359 | 8,118,934 | 6,358,288 | 6,136,725 | ||||||||||||||

Revolving credit loans and current maturities of long-term debt, net | 110,368 | 132,661 | 373,123 | 18,063 | 13,303 | ||||||||||||||

Long-term debt, less current maturities | 1,300,554 | 1,505,248 | 989,924 | 348,608 | 351,576 | ||||||||||||||

Total shareholders' equity | 2,936,723 | 2,921,492 | 2,169,888 | 2,005,755 | 1,960,143 | ||||||||||||||

(1) | During fiscal 2018, we completed the acquisition of TS (see Note 5 of Notes to Consolidated Financial Statements for further discussion). |

(2) | We adopted Accounting Standards Update No. 2014-09, “Revenue from Contracts with Customers (Topic 606)” during fiscal 2019 using the full retrospective transition method and adjusted results from fiscal 2017 and 2018 (see Note 1 of Notes to Consolidated Financial Statements for further discussion). Results from periods prior to fiscal 2017 have not been recast for the adoption of this standard. |

(3) | During fiscal 2019, 2018 and 2017, we recorded acquisition, integration and restructuring expenses of $45.4 million, $136.3 million and $29.0 million, respectively, associated with the acquisition of TS. During fiscal 2019, we also recorded restructuring expenses of $42.5 million associated with the Global Business Optimization Program (see Note 6 of Notes to Consolidated Financial Statements for further discussion). |

(4) | During fiscal 2019, we recorded goodwill impairment expense of $47.4 million related to our Asia-Pacific reporting unit (see Note 4 of Notes to Consolidated Financial Statements for further discussion). |

(5) | During fiscal 2019, 2018, 2017, 2016 and 2015, we recorded gains of $15.4 million, $41.3 million, $4.1 million, $98.4 million and $5.1 million, respectively, associated with legal settlements, net of attorney fees and expenses (see Note 1 of Notes to Consolidated Financial Statements for further discussion). |

(6) | During fiscal 2015, we recorded restatement and remediation related expenses of $22.0 million related to the restatement of certain of our consolidated financial statements and other financial information from fiscal 2009 to fiscal 2013. |

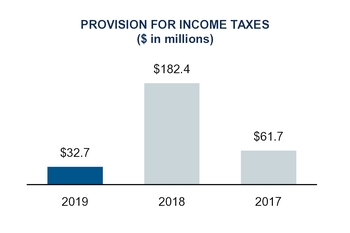

(7) | During fiscal 2019 and 2018, we recorded income tax benefits/(expenses) of $49.2 million and ($95.4) million related to the impact of the enactment of U.S. Tax Reform. During fiscal 2019, 2018, 2017 and 2015, we also recorded income tax benefits/(expenses) of $6.0 million, $(1.2) million, $12.5 million and $19.2 million, respectively, related to changes in deferred tax valuation allowances (see Note 9 of Notes to Consolidated Financial Statements for further discussion). |

(8) | Working capital represents total current assets less total current liabilities in the Consolidated Balance Sheet. |

17

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

FORWARD-LOOKING STATEMENTS | ||||

This Annual Report on Form 10-K, including this Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”), contains forward-looking statements, as described in the “safe harbor” provision of the Private Securities Litigation Reform Act of 1995. These statements involve a number of risks and uncertainties and actual results could differ materially from those projected. These forward-looking statements regarding future events and the future results of Tech Data Corporation (“Tech Data,” “we,” “our,” “us” or the “Company”) are based on current expectations, estimates, forecasts, and projections about the industries in which we operate and the beliefs and assumptions of our management. Words such as “expects,” “anticipates,” “targets,” “goals,” “projects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” variations of such words, and similar expressions are intended to identify such forward-looking statements. In addition, any statements that refer to our future financial performance, our anticipated growth and trends in our businesses, and other characterizations of future events or circumstances, are forward-looking statements. Readers are cautioned that these forward-looking statements are only predictions and are subject to risks, uncertainties, and assumptions. Therefore, actual results may differ materially and adversely from those expressed in any forward-looking statements. Readers are referred to the cautionary statements and important factors discussed in Item 1A, "Risk Factors" in this Annual Report on Form 10-K for the year ended January 31, 2019 for further information with respect to important risks and other factors that could cause actual results to differ materially from those in the forward-looking statements. We undertake no obligation to revise or update publicly any forward-looking statements for any reason.

OVERVIEW | ||||

Tech Data is one of the world’s largest IT distribution and solutions companies. Tech Data serves a critical role in the center of the IT ecosystem, bringing products from the world's leading technology vendors to market, as well as helping our customers create solutions best suited to maximize business outcomes for their end-user customers. Our customers include value-added resellers, direct marketers, retailers, corporate resellers and managed service providers who support the diverse technology needs of end users.

On February 27, 2017, we acquired Avnet, Inc's. (“Avnet”) Technology Solutions business ("TS"). TS delivered data center hardware and software solutions and services and the TS acquisition strengthened our end-to-end solutions and deepened our value added capabilities in the data center and next-generation technologies. We acquired TS for an aggregate purchase price of approximately $2.8 billion, comprised of approximately $2.5 billion in cash and 2,785,402 shares of the Company's common stock. In August 2018, we entered into a settlement agreement with Avnet to finalize the TS purchase price (see Note 5 of Notes to Consolidated Financial Statements for further discussion), which resulted in the recognition of a gain of $9.6 million during the year ended January 31, 2019. Additionally, as part of the settlement agreement, we reached agreement with Avnet on the final geographic allocation of the purchase price for tax reporting purposes which resulted in the recognition of a deferred tax asset in the United States ("U.S.") for future tax deductions related to the amortization of goodwill for tax purposes. The recognition of the deferred tax asset in the U.S. resulted in an income tax benefit of $13.0 million for the fiscal year ended January 31, 2019.

Due to the timing of the completion of the TS acquisition, the results of operations for the fiscal year ended January 31, 2019 include an additional month of TS operations, as compared to the fiscal year ended January 31, 2018, which impacts comparability between periods.

On December 22, 2017, the U.S. federal government enacted the U.S. Tax Cuts and Jobs Act ("U.S. Tax Reform") which significantly revised U.S. corporate income tax law by, among other things, reducing the U.S. federal corporate income tax rate from 35% to 21% and implementing a modified territorial tax system that includes a one-time transition tax on deemed repatriated earnings of foreign subsidiaries. In fiscal 2018, we recorded income tax expenses of $95.4 million, which represented our reasonable estimate of the impact of the enactment of U.S. Tax Reform. The amounts recorded include income tax expenses of $101.1 million for the one-time transition tax and a net income tax benefit of $5.7 million related to the remeasurement of net deferred tax liabilities as a result of the change in the U.S. federal corporate income tax rate. During the fiscal year ended January 31, 2019, we finalized our analysis of the impact of the enactment of U.S. Tax Reform and decreased our estimate of the one-time transition tax by $49.2 million, primarily due to further analysis of earnings and profits of our foreign subsidiaries and the utilization of foreign tax credits (see Note 9 of Notes to Consolidated Financial Statements for further discussion).

RECENT ACCOUNTING PRONOUNCEMENTS | ||||

Effective February 1, 2018, we adopted the requirements of Accounting Standards Update 2014-09, "Revenue from Contracts with Customers." See Note 1 of Notes to Consolidated Financial Statements for the discussion on recent accounting pronouncements, including the impacts of the adoption of the new revenue recognition accounting standard.

18

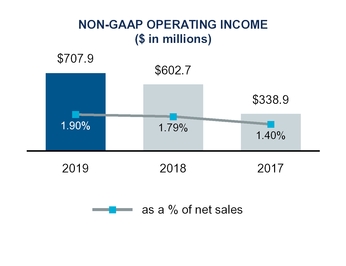

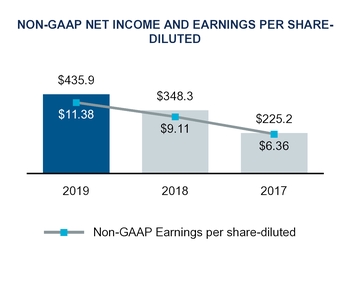

NON-GAAP FINANCIAL INFORMATION | ||||

In addition to disclosing financial results that are determined in accordance with generally accepted accounting principles in the U.S. (“GAAP”), the Company also discloses certain non-GAAP financial information. Certain of these measures are presented as adjusted for the impact of changes in foreign currencies (referred to as “impact of changes in foreign currencies”). Removing the impact of the changes in foreign currencies provides a framework for assessing our financial performance as compared to prior periods. The impact of changes in foreign currencies is calculated by using the exchange rates from the prior year comparable period applied to the results of operations for the current period. The non-GAAP financial measures presented in this document include:

• | Net sales, as adjusted, which is defined as net sales adjusted for the impact of changes in foreign currencies; |

• | Gross profit, as adjusted, which is defined as gross profit as adjusted for the impact of changes in foreign currencies; |

• | Selling, general and administrative expenses (“SG&A”), as adjusted, which is defined as SG&A as adjusted for the impact of changes in foreign currencies; |

• | Non-GAAP operating income, which is defined as operating income as adjusted to exclude acquisition, integration and restructuring expenses; goodwill impairment; legal settlements and other, net; gain on disposal of subsidiary; value added tax assessments; tax indemnifications; and acquisition-related intangible assets amortization expense; |

• | Non-GAAP net income, which is defined as net income as adjusted to exclude acquisition, integration and restructuring expenses; goodwill impairment; legal settlements and other, net; gain on disposal of subsidiary; tax indemnifications; value added tax assessments and related interest expense; acquisition-related intangible assets amortization expense; acquisition-related financing expenses; the income tax effects of these adjustments; change in deferred tax valuation allowances and the impact of U.S. Tax Reform; |

• | Non-GAAP earnings per share-diluted, which is defined as earnings per share-diluted as adjusted to exclude the per share impact of acquisition, integration and restructuring expenses; goodwill impairment; legal settlements and other, net; gain on disposal of subsidiary; value added tax assessments and related interest expense; tax indemnifications; acquisition-related intangible assets amortization expense; acquisition-related financing expenses; the income tax effects of these adjustments; change in deferred tax valuation allowances and the impact of U.S. Tax Reform. |

Management believes that providing this additional information is useful to the reader to assess and understand our financial performance as compared with results from previous periods. Management also uses these non-GAAP measures to evaluate performance against certain operational goals. However, analysis of results on a non-GAAP basis should be used as a complement to, and in conjunction with, data presented in accordance with GAAP. Additionally, because these non-GAAP measures are not calculated in accordance with GAAP, they may not necessarily be comparable to similarly titled measures reported by other companies.

19

RESULTS OF OPERATIONS | ||||

The following table sets forth our Consolidated Statement of Income as a percentage of net sales.

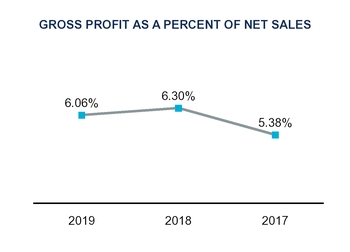

Year ended January 31: | 2019 | 2018 | 2017 | ||||||||

Net sales | 100.00 | % | 100.00 | % | 100.00 | % | |||||

Cost of products sold | 93.94 | 93.70 | 94.62 | ||||||||

Gross profit | 6.06 | 6.30 | 5.38 | ||||||||

Operating expenses: | |||||||||||

Selling, general and administrative expenses | 4.43 | 4.79 | 4.07 | ||||||||

Acquisition, integration and restructuring expenses | 0.23 | 0.41 | 0.12 | ||||||||

Goodwill impairment | 0.13 | — | — | ||||||||

Legal settlements and other, net | (0.04 | ) | (0.12 | ) | (0.02 | ) | |||||

Value added tax assessments | — | — | — | ||||||||

Gain on disposal of subsidiary | (0.02 | ) | — | — | |||||||

4.73 | 5.08 | 4.17 | |||||||||

Operating income | 1.33 | 1.22 | 1.21 | ||||||||

Interest expense | 0.29 | 0.33 | 0.15 | ||||||||

Other expense (income), net | 0.04 | — | — | ||||||||

Income before income taxes | 1.00 | 0.89 | 1.06 | ||||||||

Provision for income taxes | 0.09 | 0.54 | 0.25 | ||||||||

Net income | 0.91 | % | 0.35 | % | 0.81 | % | |||||

20

NET SALES | ||||

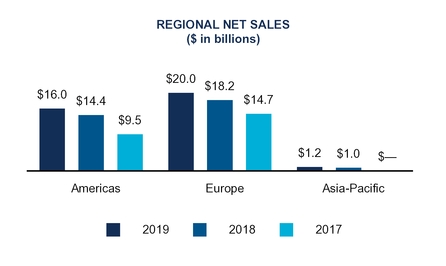

The following tables summarize our net sales and change in net sales by geographic region for the fiscal years ended January 31, 2019, 2018 and 2017 (in billions):

Year ended January 31: | 2019 | 2018 | $ Change | % Change | ||||||||||

(in millions) | ||||||||||||||

Consolidated net sales, as reported | $ | 37,239 | $ | 33,598 | $ | 3,641 | 10.8% | |||||||

Impact of changes in foreign currencies | (238 | ) | — | (238 | ) | |||||||||

Consolidated net sales, as adjusted | $ | 37,001 | $ | 33,598 | $ | 3,403 | 10.1% | |||||||

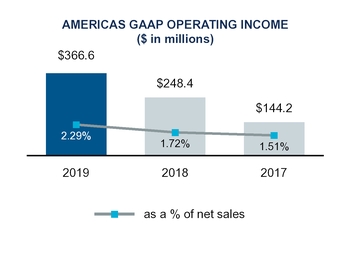

Americas net sales, as reported | $ | 16,041 | $ | 14,419 | $ | 1,622 | 11.2% | |||||||

Impact of changes in foreign currencies | 45 | — | 45 | |||||||||||

Americas net sales, as adjusted | $ | 16,086 | $ | 14,419 | $ | 1,667 | 11.6% | |||||||

Europe net sales, as reported | $ | 20,026 | $ | 18,148 | $ | 1,878 | 10.3% | |||||||

Impact of changes in foreign currencies | (314 | ) | — | (314 | ) | |||||||||

Europe net sales, as adjusted | $ | 19,712 | $ | 18,148 | $ | 1,564 | 8.6% | |||||||

Asia-Pacific net sales, as reported | $ | 1,172 | $ | 1,031 | $ | 141 | 13.7% | |||||||

Impact of changes in foreign currencies | 31 | — | 31 | |||||||||||

Asia-Pacific net sales, as adjusted | $ | 1,203 | $ | 1,031 | $ | 172 | 16.7% | |||||||

2019 - 2018 NET SALES COMMENTARY | ||||

AMERICAS

• | The increase in Americas net sales, as adjusted, of approximately $1.7 billion is primarily due to growth in data center products, software products and personal computer systems, including the impact of an additional month of TS operations due to the timing of the completion of the acquisition in the prior year. |

EUROPE

• | The increase in Europe net sales, as adjusted, of approximately $1.6 billion is primarily due to growth in data center, software and mobility products, including the impact of an additional month of TS operations due to the timing of the completion of the acquisition in the prior year. The impact of changes in foreign currencies is primarily due to the strengthening of the euro against the U.S. dollar. |

ASIA-PACIFIC

• | The increase in Asia-Pacific net sales, as adjusted, of $172 million is primarily due to growth in data center products and the impact of an additional month of TS operations due to the timing of the completion of the acquisition in the prior year. |

21

Year ended January 31: | 2018 | 2017 | $ Change | % Change | ||||||||||

(in millions) | ||||||||||||||

Consolidated net sales, as reported | $ | 33,598 | $ | 24,194 | $ | 9,404 | 38.9% | |||||||

Impact of changes in foreign currencies | (542 | ) | — | (542 | ) | |||||||||

Consolidated net sales, as adjusted | $ | 33,056 | $ | 24,194 | $ | 8,862 | 36.6% | |||||||

Americas net sales, as reported | $ | 14,419 | $ | 9,526 | $ | 4,893 | 51.4% | |||||||

Impact of changes in foreign currencies | (27 | ) | — | (27 | ) | |||||||||

Americas net sales, as adjusted | $ | 14,392 | $ | 9,526 | $ | 4,866 | 51.1% | |||||||

Europe net sales, as reported | $ | 18,148 | $ | 14,668 | $ | 3,480 | 23.7% | |||||||

Impact of changes in foreign currencies | (506 | ) | — | (506 | ) | |||||||||