Form 425 Dell Technologies Inc Filed by: Dell Technologies Inc

Filed by Dell Technologies Inc.

Pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-6 of the

Securities Exchange Act of 1934

Subject Company: Dell Technologies Inc.

(Commission File No. 001-37867)

| • | The following was posted to the LinkedIn account of Dell Technologies Inc. on December 6, 2018. |

Dells transformation is welcomed by many beleaguered IT managers& The Economist dives into Michael Dells vision for the future: https://dell.to/2AZgNLY. This contains information related to a proposed transaction for more &see moreMichael Dell plots his return to the public marketEconomist.com

| • | The following was posted to the Twitter account of Dell Technologies Inc. on December 6, 2018. |

| • | The following was posted to the Twitter account of Michael Dell on December 6, 2018. |

Dell Technologies @DellTech . 1m "Dell's transformation is welcomed by many beleaguered IT managers..." @TheEconomist

dives into @MichaelDell's vision for the future. This contains Information related to a proposed transaction - see dell.to/2UmLDHv Michael Dell plots his return to the public market The largest private tech firm has an updated vision for computing's

future economist.com

In depth look at @DellTech by @ VVVijayEconBiz. We are innovating at scale across our family of businesses to help our customers meet

opportunity head-on. Michael Dell plots his return to the public market The largest private tech firm has an updated vision for computings future economist.com

| • | The full text of The Economist article accessible through the link included in the posts above is reproduced below: |

Michael Dell plots his return to the public market

The largest private tech firm has an updated vision for computing’s future

Dec 6th 2018 | ROUND ROCK AND PALO ALTO

There are two ways to make money selling technology, goes an old industry saying: unbundling and bundling. Thanks to the spectacular rise in recent years of cloud-computing services from Amazon and Microsoft, many firms have shifted chunks of software, data and applications previously stored on in-house servers to the new “public cloud” infrastructure. Customers can now access a dizzying array of software and hardware offered as unbundled, cloud-based services.

Dizzying—but also bewildering. The typical chief technology officer (CTO) of a big firm, under pressure to take advantage of every computing advance from data-analytics to artificial intelligence to the internet of things (IoT), is faced with a mish-mash of information-technology options. The next big opportunity should therefore lie in simplifying this balkanised mess.

That insight lies at the heart of Michael Dell’s vision for the future of Dell Technologies, a giant it firm based in Texas. The billionaire founded Dell in his college dorm room at the University of Texas in 1984 and by the age of 27 he became the youngest-ever boss of a Fortune 500 company (Mark Zuckerberg was nearly 29 when Facebook first made the list, in 2013). Mr Dell revolutionised the business of personal computers (PCS) by selling directly to customers, adopting just-in-time manufacturing and lean, global supply chains that undercut rivals.

Now Mr Dell is pushing forward his next revolution. He is trying to save the ageing PC manufacturer from commoditisation by dramatically expanding its software and cloud offerings. He took Dell private in 2013 helped by Silver Lake Partners, a Californian private-equity firm, in a deal worth $24.4bn. At the time, Dell’s revenues and profits were tumbling as the PC market was squeezed by the rise of mobile devices and low-cost Asian manufacturers. Its prospects were rapidly darkening.

Away from the scrutiny of public markets, Mr Dell invested heavily ($13.6bn in research and development since 2013) to strengthen Dell’s capabilities in cutting-edge software and cloud integration. He pulled off the largest-ever tech acquisition, gobbling up EMC, a big American provider of data-storage devices and cloud-computing software, for $67bn in 2016.

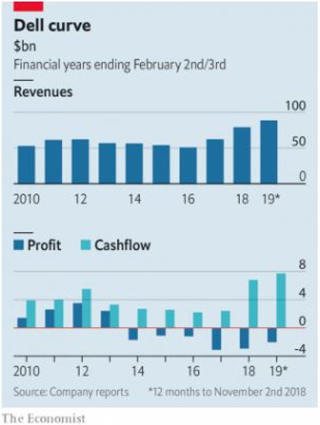

Very few firms have been able to pull off a corporate transformation, says Michael Cusumano of the MIT Sloan School of Management, but he thinks Mr Dell’s labours are starting to produce results. As a result of both ongoing investment and accounting charges related to the purchase of EMC, Dell continues to make losses (see chart) but its growth engine is at last fired up. On November 29th its quarterly results included a surge in revenues of 15%. The firm’s cashflow from operations leapt from $2.4bn in the fiscal year ending in February 2017 to $7.7bn in the four quarters to November 2nd 2018; losses fell.

Dell curve$bnFinancial years ending February 2nd/3rdRevenues2010 12 14 16 18 19* 0 50 100Profit Cashflow2010 12 14 16 18 19 -4 0 4 8Source Company reports*12 months to November 2nd 2018 The Economist

On its current trajectory, Dell looks set to achieve annual revenues this year of just over $90bn, up from roughly $80bn last year. Dell’s hope is that its investments in cloud computing and software, which offer far higher margins than the PC business, will soon return it to profitability.

A good example is Dell’s crown jewel: VMware, a pioneer in virtualisation software, which allows software to run on multiple machines seamlessly. It is a publicly traded and profitable entity with a hip campus in Palo Alto, California. Since Dell got hold of most of VMware through the EMC acquisition, investors have been able to own a piece of Dell itself through DVMT, a special tracking stock that is meant to reflect Dell’s ownership stake in VMware.

Soon they should be able to buy into all of Dell directly. Shareholders will gather on December 11th in Round Rock, Texas, at Dell’s unpretentious headquarters, to vote on a complex proposal that would allow the firm to pull off something resembling a reverse merger (the acquisition of a listed firm by a privately held one that is keen to go public without the hassle of a conventional initial public offering).

This plan, announced in July, involves converting DVMT shares into new Dell shares to be publicly traded. DVMT investors could accept the new Dell shares at a given conversion ratio or cash out (though a cap on cash available means those choosing the latter may have to receive a mix). VMware said then that it would pay out a special one-time dividend of $11bn, with Dell to use its share of the dividend (about $9bn) to help fund the transaction. In an initial proposal, Mr Dell and Silver Lake offered a deal that implied a value for DVMT of about $22bn, including $9bn in cash.

After noisy objections from Carl Icahn, an activist investor (who also made trouble back in 2013 about the price at which Dell went private), they revised the terms last month to reflect a value of some $24bn for DVMT, some $14bn of it in cash. If the resolution passes, as expected, Dell will soon trade on the New York Stock Exchange.

The real challenge begins after the vote. Mr Dell’s plan to emphasise software in future contains three bets. The first is to be the best all-in-one provider of bundled IT. That may not be easy. Norman White of the NYU Stern School of Business observes that combining a commoditised hardware business with an innovative software business is particularly hard to do. And IBM’s $34bn acquisition in October of Red Hat, a provider of open-source software, which it plans to sell alongside hardware, could make Big Blue a potent rival.

Still, Dell’s transformation is welcomed by many beleaguered IT managers. The chief information officer of a big British bank that spends over $50m a year on Dell kit says he values its ability to provide “converged infrastructure” that bundles multiple IT components such as servers, data-storage units, networking switches and the software to make all this gear work together, into a single package. Cheekily, Mr Dell promises customers to be the “one throat to choke” in case things go awry.

Mr Dell’s second big bet is on the rise of a “hybrid” cloud which allows customers to blend their out-of-house and in-house IT. Companies are growing nervous about putting all of their sensitive customer and business data on third-party clouds. Lonne Jaffe, a former IBM man now at Insight, a venture-capital company, insists that hybrid clouds are the future.

The public cloud promoted by Amazon and Microsoft will remain a force to reckon with. Dell cannot invest as much in innovation, and is sure to face ruthless price competition from Amazon. Still, Dell may be catching a wave big enough to carry several firms. Last year Gartner, a consultancy, predicted a “massive shift toward hybrid infrastructure”, with 90% of companies using hybrid clouds by 2020.

A third bet is on “edge” computing. As countries roll out 5G networks and firms put smart sensors into everything, the IoT should arrive. Mr Dell says it will make demands that the public cloud cannot satisfy. If an autonomous vehicle (AV) senses it is about to hit a deer on a country road, he asks, must it wait for software housed in a distant public cloud to give it permission to stop? It is an unlikely scenario but one Dell is using to promote its IoT division.

One of Dell’s big customers says the answer is obvious. “Decisions must be taken absolutely in real time, a car is a data centre on wheels,” says Simon Bolton, chief information officer of Jaguar Land Rover (JLR), an Indian-owned carmaker. The answer is edge computing, which allows the car to have a lot of computing power in the boot. JLR has long used Dell desktop computers, EMC storage devices and VM ware software. Now it is using other bits of the firm’s kit (cyber-security software, for example) as it develops edge-computing systems.

Last year, Dell created a new division devoted to the IoT. It has promised to invest $1bn in research and development over three years. Its venture-capital arm has invested in Graphcore, a British startup developing AI process super-fast chip, which enjoys very low latency (the time it takes for data to get to their destination), is ideal for use in AVs. Graphcore is bringing these AI chips to market by putting them into Dell hardware, which the latter’s legions of salesmen will promote to big corporate customers normally out of a startup’s reach.

In the end, the success of Dell’s new strategies depends greatly on the person at the top. Sceptics wonder if he is yesterday’s man. Others worry that his firm’s recent growth spurt may be unsustainable, and question how long it will take for him to return the firm to profitability. It remains to be seen if he can blend the aggressive sales culture at Round Rock with a softer, innovation-focused ethos in Palo Alto.

Mr Dell is confident that his bets will pay off. He notes that a public listing would “absolutely give us an acquisition currency,” one that he intends to put to use as Dell shoots toward $100bn in annual revenues. He has managed to defy naysayers in the past. In 2015, Meg Whitman, then the boss of HP Enterprise, a rival IT firm, predicted that the takeover of EMC would prove an “enormous distraction” to Dell. In a headline the same year, Wired, a magazine, said the PC was dead and not coming back—Dell’s PC sales have been rising. Accepting the scrutiny of Wall Street again will doubtless mean plenty more such provocations. Over to you, Mr Dell.

No Offer or Solicitation

This communication does not constitute an offer to sell or a solicitation of an offer to sell or a solicitation of an offer to buy any securities or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended, and otherwise in accordance with applicable law.

Additional Information and Where to Find It

This communication is being made in respect of the proposed merger of a wholly-owned subsidiary of the Company with and into the Company, with the Company as the surviving entity, pursuant to which each share of Class V common stock of the Company will, at the election of the holder, convert into the right to receive shares of Class C common stock of the Company or cash, without interest, and each existing share of Class A common stock, Class B common stock and Class C common stock of the Company will be unaffected by the merger and remain outstanding. The proposed transaction requires the approval of a majority of the aggregate voting power of the outstanding shares of Class A common stock, Class B common stock and Class V common stock other than those held by affiliates of the Company, in each case, voting as a separate class, and all outstanding shares of common stock of the Company, voting together as a single class, and will be submitted to stockholders for their consideration. The Company has filed a registration statement on Form S-4 (File No. 333-226618). The registration statement was declared effective by the SEC on October 19, 2018, and a definitive proxy statement/prospectus was mailed on or about October 23, 2018 to each holder of Class A common stock, Class B common stock, Class C common stock and Class V common stock entitled to vote at the special meeting in connection with the proposed transaction. The Company also filed a supplement to the definitive proxy statement/prospectus on November 26, 2018, which was mailed on or about November 26, 2018 to each holder of Class A common stock, Class B common stock, Class C common stock and Class V common stock entitled to vote at the special meeting in connection with the proposed transaction. INVESTORS ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS, THE SUPPLEMENT AND ANY OTHER DOCUMENTS RELATING TO THE TRANSACTION FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. You may get these documents, when available, for free by visiting EDGAR on the SEC website at www.sec.gov or by visiting the Company’s website at http://investors.delltechnologies.com.

Participants in the Solicitation

The Company and its consolidated subsidiaries and their directors, executive officers and other members of their management and employees, and Silver Lake Technology Management, L.L.C. and its managing partners and employees, may be deemed to be participants in the solicitation of proxies from the stockholders of the Company in favor of the proposed merger and the other transactions contemplated by the amended merger agreement, including the exchange of shares of Class V common stock of the Company for shares of Class C common stock of the Company or cash. Information concerning persons who may be considered participants in such solicitation under the rules of the SEC, including a description of their direct or indirect interests, by security holdings or otherwise, is set forth in the aforementioned proxy statement/prospectus and the supplement that have been filed with the SEC.

Dell Technologies Inc. Disclosure Regarding Forward-Looking Statements

This communication contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The words “may,” “will,” “anticipate,” “estimate,” “expect,” “intend,” “plan,” “aim,” “seek,” and similar expressions as they relate to the Company or its management are intended to identify these forward-looking statements. All statements by the Company regarding its expected financial position, revenues, cash flows and other operating results, business strategy, legal proceedings, and similar matters are forward-looking statements. The expectations expressed or implied in these forward-looking statements may not turn out to be correct. The Company’s results could be materially different from its expectations because of various risks, including but not limited to: (i) the failure to consummate or delay in consummating the proposed transaction, including the failure to obtain the requisite stockholder approvals or the failure of VMware to pay the special dividend or any inability of the Company to pay the cash consideration to Class V holders; (ii) the risk as to the trading price of Class C common stock to be issued by the Company in the proposed transaction relative to the trading price of shares of Class V common stock and VMware, Inc. common stock; and (iii) the risks discussed in the “Risk Factors” section of the registration statement on Form S-4 (File No. 333-226618) that has been filed with the SEC and declared effective, the risks discussed in the “Update to Risk Factors” section of the supplement to the definitive proxy statement/prospectus that has been filed with the SEC, as well as the Company’s periodic and current reports filed with the SEC. Any forward-looking statement speaks only as of the date as of which such statement is made, and, except as required by law, the Company undertakes no obligation to update any forward-looking statement after the date as of which such statement was made, whether to reflect changes in circumstances or expectations, the occurrence of unanticipated events, or otherwise.