Form DFAN14A Destination Maternity Filed by: Miller Nathan G

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

|

Filed by the Registrant

|

Filed by a Party other than the Registrant

|

Check the appropriate box:

|

|

Preliminary Proxy Statement

|

|

|

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

|

|

|

Definitive Proxy Statement

|

|

|

Definitive Additional Materials

|

|

|

Soliciting material Pursuant to §240.14a-12

|

|

Destination Maternity Corporation

|

|

(Name of Registrant as Specified In Its Charter)

|

|

|

|

Nathan G. Miller

Peter O’Malley

Holly N. Alden

Christopher B. Morgan

Marla A. Ryan

Anne-Charlotte Windal

|

|

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

|

Payment of Filing Fee (Check the appropriate box):

|

|

No fee required.

|

|

|

|

||

|

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11.

|

|

|

|

|

|

|

|

1)

|

Title of each class of securities to which transaction applies:

|

|

|

|

|

|

|

|

|

|

|

2)

|

Aggregate number of securities to which transaction applies:

|

|

|

|

|

|

|

|

|

|

|

3)

|

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

|

|

|

|

|

|

|

|

|

|

|

4)

|

Proposed maximum aggregate value of transaction:

|

|

|

|

|

|

|

|

|

|

|

5)

|

Total fee paid:

|

|

|

|

|

|

|

|

|

|

|

Fee paid previously with preliminary materials.

|

|

|

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

|

|

|

|

||

|

|

1)

|

Amount Previously Paid:

|

|

|

|

|

|

|

|

|

|

|

2)

|

Form, Schedule or Registration Statement No.:

|

|

|

|

|

|

|

|

|

|

|

3)

|

Filing Party:

|

|

|

|

|

|

|

|

|

|

|

4)

|

Date Filed:

|

|

|

|

|

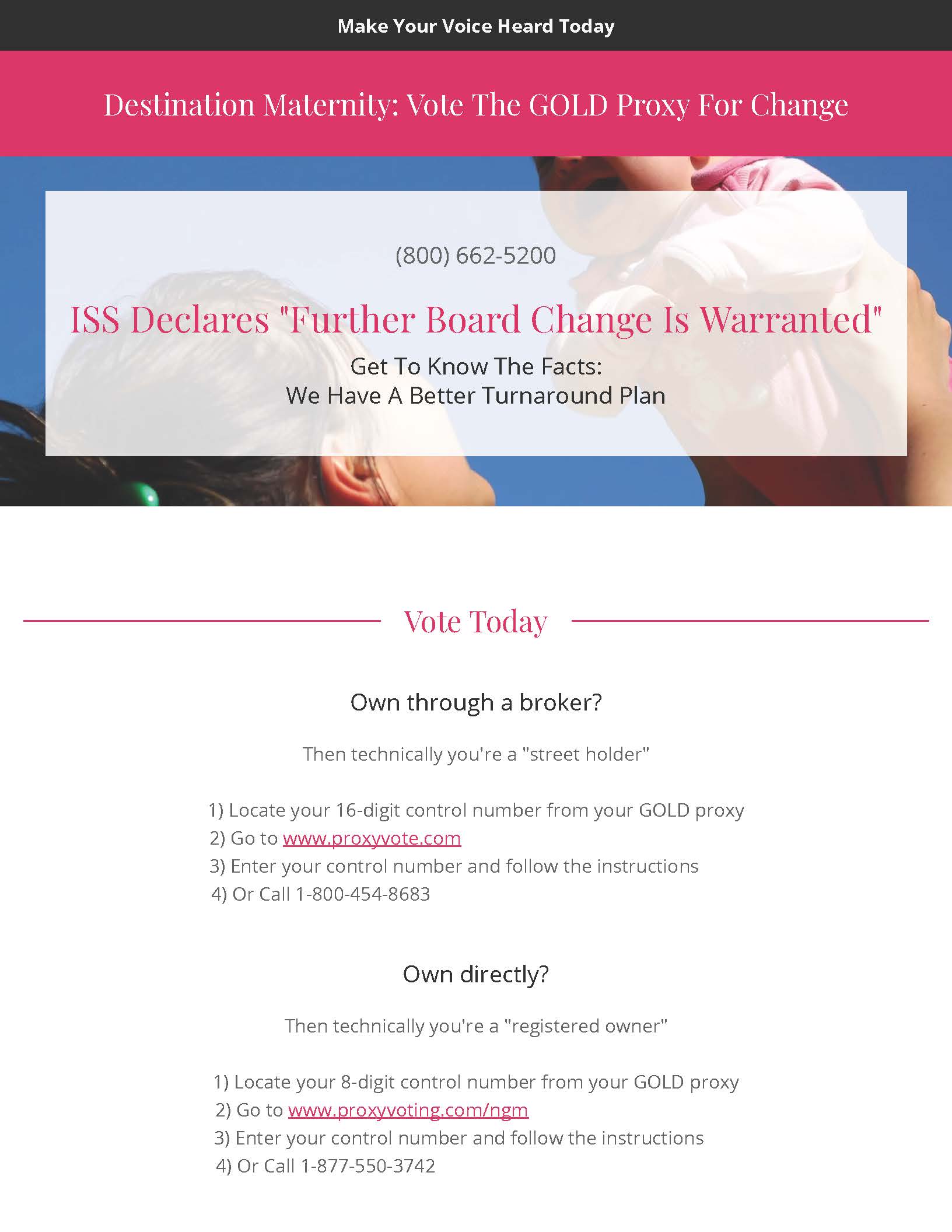

On May 15, 2018, the following materials were posted to www.destfacts.com:

Investor Group Comments on ISS Recommendation at Destination Maternity

NEW YORK--(BUSINESS WIRE)--May 11, 2018--Nathan G. Miller and Peter O’Malley (the “Investors”), collective holders of approximately 9% of the outstanding common stock of Destination Maternity Corporation (Nasdaq: DEST) (“Destination Maternity” or the “Company”), today released the following statement in regards to the recent report from Institutional Shareholder Services (ISS):

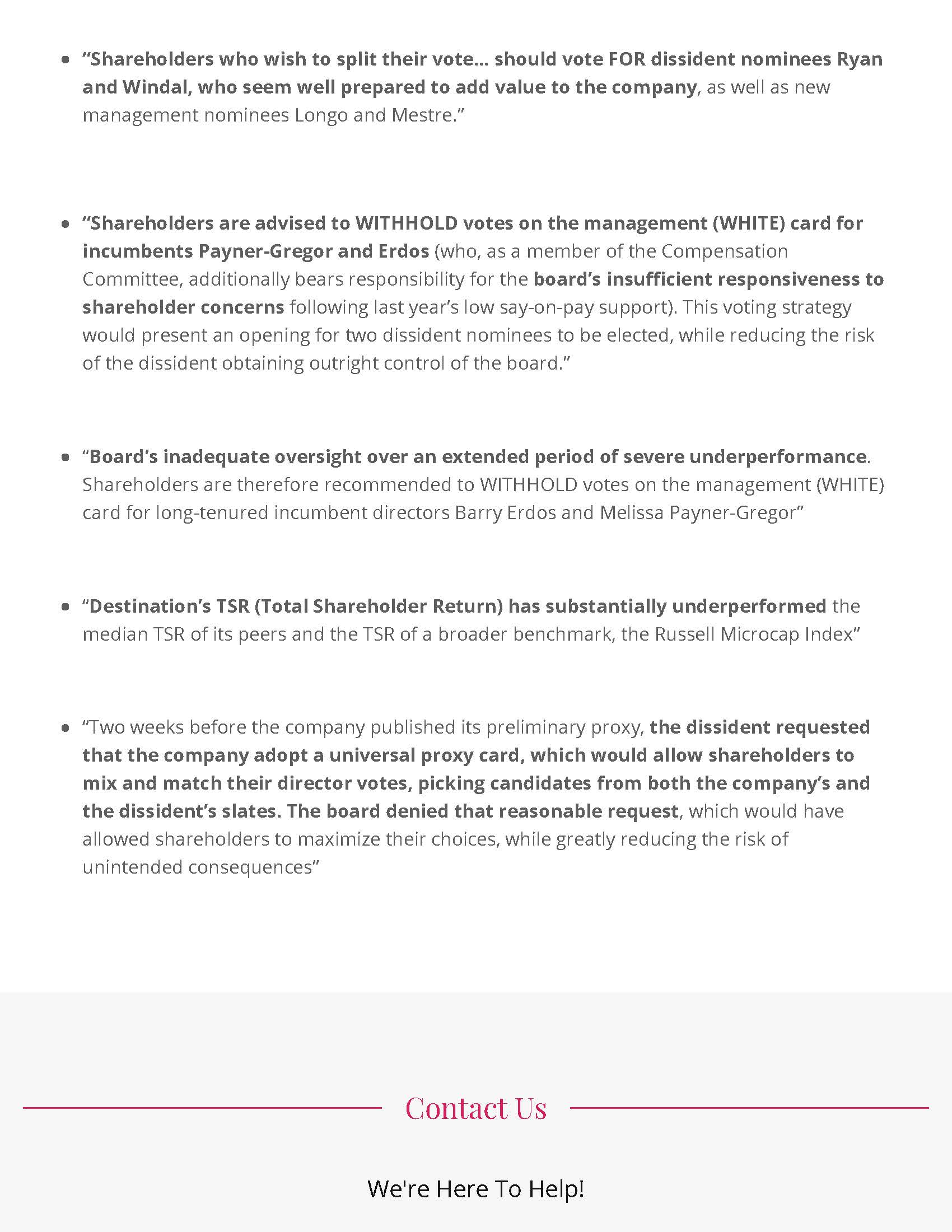

“We are pleased that ISS agreed with our argument that the chronic underperformance at Destination Maternity is emblematic of a company not living up to its potential, and that change at the board level is warranted.

However, we find it counterintuitive that while agreeing with these fundamental points, ISS refrained from recommending for our majority female slate, citing a lack of public board experience among our nominees as the primary justification. The reality is that Destination Maternity is a company where the absence of female board representation and leadership is in direct misalignment with the strategic goals, end customers and product selection that will ultimately determine whether DEST becomes a successful turnaround story, or yet another cautionary tale of mismanagement and missed opportunity.

Notably, before launching this proxy contest we proposed to the Company that they add to the Board two of our highly-qualified female nominees. They responded by adding two men.

The share of women on S&P 500 company boards rose merely 1 percentage point last year to 22 percent.1 If the argument - a chauvinist trope - continues to be that qualified women executives should not be added to boards because they have not previously served on boards, this embarrassing problem will not get solved. Board diversity cannot remain a ‘chicken or the egg’ situation.

As such, we believe that our highly-qualified nominees Holly N. Alden, Christopher B. Morgan, Marla A. Ryan and Anne-Charlotte Windal should be added to the Board of Directors of the Company in order to bring about the level of change needed to reverse the years of mismanagement and underperformance the Company has suffered.”

In its report, ISS noted the following:

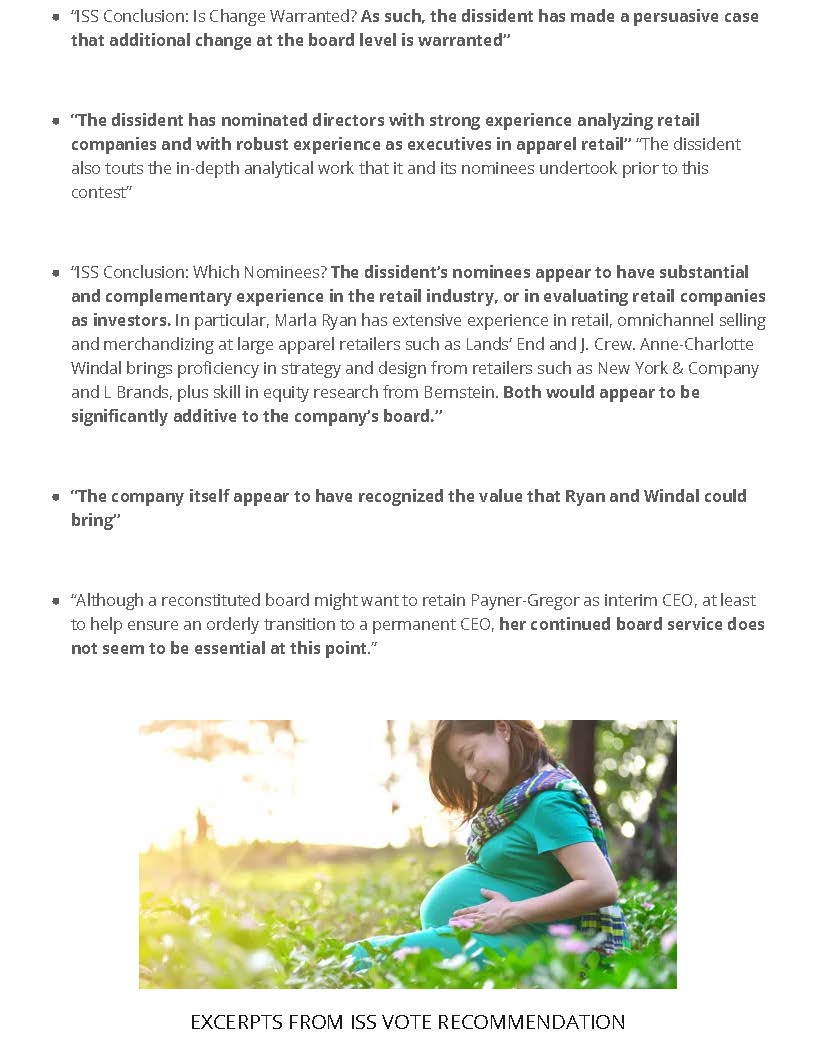

“The company’s dramatically negative shareholder returns and financial performance reflect a company falling well short of its potential.” “The long-tenured directors have presided over many years of abysmal financial performance and tremendous value destruction for shareholders.” “(T)he dissident has made a persuasive case that additional change at the board level is warranted.” “The dissident has nominated directors with strong experience analyzing retail companies and with robust experience as executives in apparel retail.”

1https://www.wsj.com/articles/how-to-get-more-women-in-the-boardroom-some-try-blunt-force-1524648602

View source version on businesswire.com:https://www.businesswire.com/news/home/20180511005382/en/

CONTACT: Morrow Sodali LLC

Tom Ball, 203-658-9368

KEYWORD: UNITED STATES NORTH AMERICA NEW YORK

INDUSTRY KEYWORD: PROFESSIONAL SERVICES BANKING FINANCE

SOURCE: Morrow Sodali LLC

Copyright Business Wire 2018.

PUB: 05/11/2018 10:24 AM/DISC: 05/11/2018 10:24 AM

http://www.businesswire.com/news/home/20180511005382/en

Gullane Capital Partners Announces Support for Activist Position of Destination Maternity

Hedge fund owning 3%+ of outstanding shares supports slated new board members

May 10, 2018 11:17 AM Eastern Daylight Time

MEMPHIS, Tenn.--(BUSINESS WIRE)--Gullane Capital Partners, a Memphis-based hedge fund that holds 3%+ ownership in Destination Maternity Corporation (Nasdaq: DEST), today announced its support of the GOLD proxy card issued by activist shareholders Nathan Miller and Peter O’ Malley calling on stockholders to vote in favor of four director nominees at the Company’s 2018 annual meeting, taking place on May 23, 2018.

Gullane Capital Partners Announces Support for Activist Position of Destination Maternity $DEST

Tweet this

“Destination Maternity’s existing board has been given ample time to fix DEST while watching the stock price fall over 80% in the past three years,” said Trip Miller, Managing Partner of Gullane Capital Partners, a value investor who is not affiliated with the activist shareholder group backing the GOLD proxy.

Miller continued, “We believe the four new proposed directors are highly qualified to restore long term value to DEST and encourage other shareholders to take action.”

To learn more about Gullane Capital Partners, visit www.gullanecapitalpartners.com.

About Gullane Capital Partners, LLC

Founded in 2002, Gullane Capital LLC is the investment advisor to the Gullane Capital Partners, LLC fund and separately managed accounts. We are value investors following the teachings of Ben Graham, Warren Buffett, and Charlie Munger. Gullane Capital LLC utilizes a concentrated, disciplined value investing philosophy to manage partner capital for the long term.Gullane focuses exclusively on bottom up proprietary research of publicly traded securities across the capital structure, with no market cap, industry, or geographic restrictions. We define risk as permanent capital loss, not short-term market volatility.

Contacts

Gregory FCA for Gullane Capital Partners

Amy Lash, 610-228-2806

Battle over board seats at Destination Maternity heats up

Reuters Staff

BOSTON (Reuters) - One of Destination Maternity Corp’s largest investors on Monday accused the retailer of “governance shenanigans” and asked it to clarify exactly how many directors will be elected at the annual meeting, a regulatory filing shows.

In the last two weeks the company has increased and then decreased the size of its board, creating what investor Nathan G. Miller calls confusion and worse for investors, he wrote to the Moorestown, New Jersey-based company on Monday, according to the filing.

Investors like Miller who are pushing for changes at corporations around the country have a short time to nominate dissident investors and company lawyers force them to follow strict nomination rules for their slates to be valid. Industry analysts say Destination Maternity’s shifts in board size are unusual and raise questions for investors.

Miller, whose NGM Asset Management owns 7.8 percent of the company’s stock and is pushing it to add female directors, said the back-and-forth is leaving investors in the dark about how many people will eventually oversee how the company operates.

On April 3, the company increased the board to six directors from four. Then it cut the board back to five directors on April 12 when one of the recently appointed directors quit after only nine days on the job, the filing says.

Another board member then said he would not run again, but the company did not reduce the size of the board, saying it would do so only after the 2018 annual meeting began, the filing says.

We “are concerned that these governance shenanigans are an attempt to gain an improper advantage in the election of directors at the 2018 annual meeting of stockholders,” Miller wrote, demanding an “unequivocal statement regarding the maximum number of Board seats that are up for election.”

The annual meeting is scheduled for May 23, according to a Feb. 28 statement by the company.

Miller asked the company to use a universal proxy card so investors can choose directors from both the management and dissident slates. The company refused to use it.

Both Miller and a representative for Destination Maternity declined to comment.

Destination Maternity’s stock lost 3.6 percent to $2.59 in Nasdaq trading on Monday.

Reporting by Svea Herbst-Bayliss; Editing by Dan Grebler

Destination Maternity faces second proxy battle in as many years

By Natalie Kostelni – Reporter, Philadelphia Business Journal

May 4, 2018, 7:31am EDT

Destination Maternity Corp., which faced a proxy battle over its board last year, is set for a repeat this year as an activist shareholder pushes for a new slate of directors amid accusations that the company is up to “ governance shenanigans” to thwart new members from joining its board.

The company, which reported two weeks ago a $10.2 million loss, or 73 cents a share, for its fiscal fourth quarter and a $21 million, or $1.57 a share loss for the year, has been struggling for several years and has left it vulnerable to take over attempts and pressure for a change in leadership. The most recent proxy battle comes from Nathan G. Miller of NGM Asset Management, which owns 7.8 percent of the company.

In a scathing letter sent April 16 to the Moorestown, N.J., clothing company and filed with the Securities and Exchange Commission, Miller details a timeline of uncertainty surrounding the company including: how it increased its board to six directors from four on April 3; reduced the board to five directors on April 12; saw another newly appointed director resign after just nine days; and yet another board member decline to stand for re-election.

“As a result of these governance shenanigans, the stockholders of the company are left in a state of uncertainty in which even the most basic details regarding the election of directors at the 2018 annual meeting remain unknown,” Miller wrote.

Prior to that, Miller had proposed a merger transaction in which shareholders would receive $2.75 in cash and the company would go private, according to an SEC filing made by Miller. A confidentially agreement was drawn up and Miller, his firm and Destination discussed the potential of a transaction with Guggenheim and other various potential financing sources. Not long thereafter, Miller decided not to pursue a deal because of Destination’s “poor financial performance and liquidity issues,” SEC documents said.

In an open letter to shareholders issued Thursday, Miller along with another investor that gives them a combined 9 percent ownership stake in the company, urged them to consider their slate of directors and proposed turnaround plan at the annual meeting scheduled for May 23 at its headquarters. Among the issues Miller cited included the company’s stock price declining by 84 percent to $2.385 from $15.44; book value falling by 67 percent to $2.95 from $9.25; and revenues dropping by 21 percent to $406 million from $517 million.

In a letter dated May 1, Melissa Payner-Gregor, the company’s interim CEO, urged shareholders to vote for its recommended slate of incumbent directors. “The election of the Miller Group’s nominees would replace every member of your board with directors who lack institutional knowledge of your company and other requisite skills for effective service on your board,” Payner-Gregor wrote. “The board has serious concerns that the Miller Group’s candidates would have a negative impact on Destination Maternity’s future growth plans, as the collective

experience and relevant expertise of these individuals pale in comparison to the decades of corporate leadership and board experience in the retail and apparel industry represented on your board.”

Payner-Gregor said two outside proxy solicitation firms had been retained and that shareholders may hear from either regarding how they intend to vote.

“With a strong team in place and a solid infrastructure upon which to grow, the company is focused on improving performance, achieving profitable growth and maximizing stockholder value,” she said, adding that by voting for her suggested nominees, the company will be on a path to turnaround.

Last year, Orchestra-Prémaman S.A. waged a proxy battle to get its nominees put on the board and Destination Maternity narrowly won. Last month, the New Jersey company named an executive from the French clothing retailer to its board and entered into a support agreement with it and its affiliates.

The company in 2013 received $40 million in corporate welfare from the state’s Grow N.J. economic development program to relocate its headquarters to New Jersey from Philadelphia.

Exhibit C

Nathan G. Miller

c/o NGM Asset Management, LLC

27 Pine Street, Suite 700

New Canaan, CT 06840

April 16, 2018

Via Federal Express

Board of Directors

Destination Maternity Corporation

232 Strawbridge Drive

Moorestown, NJ 08057

Ladies and Gentlemen:

We are writing to express our concern regarding the recent actions by the board of directors (the “Board”) and management of Destination Maternity Corporation (the “Company”) to manipulate the composition of the Board. We are well past the director nominating deadline and are concerned that these governance shenanigans are an attempt to gain an improper advantage in the election of directors at the 2018 annual meeting of stockholders of the Company (the “2018 Annual Meeting”).

On March 30, 2018, we requested that the Board act in the interest of all of the Company’s stockholders by committing to the use of a universal proxy card that would include all of the nominees proposed, regardless of who proposed such nominees. On April 4, 2018, despite the fact that universal proxy cards have been used successfully in electoral contests involving large companies with shares listed on the New York Stock Exchange, the Company notified us that it had rejected the use of a universal proxy card because its use could create “significant risk of confusion that could result in disenfranchisement of certain stockholders.”

However, despite the Board’s professed sensitivity to the risk of confusing the Company’s stockholders, the Board and management of the Company have since engaged in a series of actions that would confuse even the most sophisticated of stockholders, a background of which is summarized below:

|

·

|

On April 3, 2018, after the deadline had passed for nominating candidates for election to the Board at the 2018 Annual Meeting, the Company announced that the size of the Board would be increased to six directors and that Pierre-André Mestre and Jean-Claude Jacomin would be appointed to fill the newly created vacancies pursuant to an agreement with Orchestra-Prémaman (“Orchestra”), a stockholder of the Company.

|

|

·

|

On April 12, 2018, in response to the Company’s expansion of the Board and pursuant to our rights as a stockholder under the Company’s bylaws, we notified the Company of our intention to nominate two additional individuals in addition to the three individuals we had previously identified for election to the Board at the 2018 Annual Meeting (collectively, the “Nominees”).

|

|

·

|

Later on April 12, 2018, the Company announced that Mr. Jacomin, who had been appointed to the Board only nine days earlier, had resigned as a member of the Board. Further, the Company announced that the size of the Board had been decreased from six to five directors. To further complicate matters, the Company stated that Orchestra would continue to have a right to name a substitute individual to replace Mr. Jacomin on the Board pursuant to Orchestra’s agreement with the Company. The Company has not announced who Orchestra intends to designate or when Orchestra will exercise this right, creating uncertainty as to both the Company’s slate of directors for election at the 2018 Annual Meeting and the number of directors that will be elected at the 2018 Annual Meeting.

|

|

·

|

On April 13, 2018, the Company announced for the third time in a two week period that the composition of the Board would change because Michael J. Blitzer would not be standing for reelection to the Board at the 2018 Annual Meeting. Instead of immediately reducing the size of the Board accordingly, as was done following Mr. Jacomin’s resignation, the Company announced that the size of the Board would only decrease from five to four directors upon the commencement of the 2018 Annual Meeting.

|

|

·

|

Later on April 13, 2018, Barry Erdos, the Chairman of the Board, sent a letter to Marla A. Ryan and Anne-Charlotte Windal, two of the Nominees. Despite having previously (i) rejected the use of a universal proxy card in which the stockholders of the Company would have the opportunity to vote for both Ms. Ryan and Ms. Windal and (ii) stated that neither individual was endorsed by the Board, Mr. Erdos asked Ms. Ryan and Ms. Windal if they would consider being added to the Company’s slate of nominees for election at the 2018 Annual Meeting.

|

As a result of these governance shenanigans, the stockholders of the Company are left in a state of uncertainty in which even the most basic details regarding the election of directors at the 2018 Annual Meeting remain unknown. First, with its size changing from day to day, it is unclear what the size of the Board will be as of the 2018 Annual Meeting and afterwards. Second, the composition of the Company’s slate remains in flux, despite the fact that the Company has filed their preliminary proxy statement and the deadline to nominate directors has long since passed. Third, it is unclear whether Orchestra will appoint a new director pursuant to their agreement with the Company, and whether the Company will allow Orchestra to designate such director after the 2018 Annual Meeting, disenfranchising the stockholders of their right to vote on such director’s election to the Board.

For the benefit of all the stockholders of the Company, we ask that the Board refrain from engaging in any further manipulation of the Board’s composition and immediately clarify the uncertainties they have created. Accordingly, we are requesting that you provide us with an unequivocal statement regarding (i) the maximum number of Board seats that are up for election at the 2018 Annual Meeting, (ii) the maximum number of individuals we can nominate for election at the 2018 Annual Meeting and (iii) the maximum number of candidates we can include

2

on our proxy card for election at the 2018 Annual Meeting. In addition, the Board should clarify whether it intends to circumvent stockholder democracy by allowing Orchestra to wait until after the 2018 Annual Meeting to exercise their right to designate a second director. Board seats are not an entitlement, despite the fact that the Board has been treating them as such, and we believe any Orchestra designee should be on the ballot for the 2018 Annual Meeting so that all directors can be held accountable to stockholders of the Company. Immediate clarification of the foregoing uncertainties is necessary in order to remedy the confusion that the Board and the management of the Company has already caused and avoid the disenfranchisement that would result in the absence of clarification. It is our sincere hope that we can engage in a fair and transparent electoral contest going forward and that the merits of the nominees and their competing visions for the Company-not manipulation of the corporate electoral process-is what determines the outcome of the election.

Very truly yours,

|

/s/ Nathan G. Miller

|

||||

|

Nathan G. Miller

|

||||

3