Form 424B2 WELLS FARGO & COMPANY/MN

Filed Pursuant to Rule 424(b)(2)

Registration No. 333-221324

| Product Supplement No. EQUITY INDICES SUN-1 (To Series S Prospectus Supplement dated January 24, 2018 and Prospectus dated April 27, 2018) April 27, 2018 |

|

Market-Linked Step Up Notes Linked to One or More Equity Indices

| • | Market-Linked Step Up Notes (the “notes”) are senior unsecured debt securities issued by Wells Fargo & Company (“Wells Fargo”). Any payments due on the notes, including any repayment of principal, will be subject to the credit risk of Wells Fargo. |

| • | The notes do not guarantee the return of principal at maturity, and we will not pay interest on the notes. Instead, the return on the notes will be based on the performance of an underlying “Market Measure,” which will be an equity index or a basket of equity indices. |

| • | The notes provide an opportunity to receive the greater of a fixed return or a return based on the positive performance of the Market Measure. However, you will be exposed to any negative performance of the Market Measure below the Threshold Value (as defined below) on a 1-to-1 basis. If specified in the applicable term sheet, your notes may be subject to an automatic call, which will limit your return to a fixed amount if the notes are called. |

| • | If the value of the Market Measure does not change or increases from its Starting Value to its Ending Value up to and including the Step Up Value (each as defined below), you will receive at maturity a cash payment per unit (the “Redemption Amount”) that equals the principal amount plus the Step Up Payment (as defined below). If the Ending Value is greater than the Step Up Value, you will receive a return on the notes equal to the percentage increase in the value of the Market Measure from the Starting Value to the Ending Value or, if applicable, a multiple of that percentage increase. |

| • | If the value of the Market Measure decreases from its Starting Value to its Ending Value but not below the Threshold Value, then the Redemption Amount will equal the principal amount. However, if the Ending Value is less than the Threshold Value, you will be subject to 1-to-1 downside exposure to the decrease of the Market Measure below the Threshold Value. In such a case, you may lose all or a significant portion of the principal amount of your notes. |

| • | If specified in the applicable term sheet, your notes may be subject to an automatic call prior to maturity. In that case, the notes will be automatically called if the Observation Level on any Observation Date is greater than or equal to the Call Level (each as defined below). If the notes are automatically called, you will receive a cash payment per unit (the “Call Amount”) on the applicable Call Settlement Date (as defined below) that equals the principal amount plus the applicable Call Premium (as defined below). |

| • | This product supplement describes the general terms of the notes, the risk factors to consider before investing, the general manner in which they may be offered and sold, and other relevant information. |

| • | For each offering of the notes, we will provide you with a pricing supplement (which we refer to as a “term sheet”) that will describe the specific terms of that offering, including the specific Market Measure, the Step Up Value, the Step Up Payment, the Threshold Value, and certain related risk factors, and if the notes are subject to an automatic call, the Call Level, the Call Amount and the Call Premium for each Observation Date, the Observation Dates and the Call Settlement Dates. The term sheet will identify, if applicable, any additions or changes to the terms specified in this product supplement. |

| • | The notes will be issued in denominations of whole units. Unless otherwise set forth in the applicable term sheet, each unit will have a principal amount of $10. The term sheet may also set forth a minimum number of units that you must purchase. |

| • | Unless otherwise specified in the applicable term sheet, the notes will not be listed on a securities exchange or quotation system. |

| • | Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”) and one or more of its affiliates may act as our agents to offer the notes and will act in a principal capacity in such role. |

The notes are not deposits or other obligations of a depository institution and are not insured by the Federal Deposit Insurance Corporation, the Deposit Insurance Fund or any other governmental agency of the United States or any other jurisdiction.

The notes have complex features and investing in the notes involves risks not associated with an investment in conventional debt securities. Potential purchasers of notes should consider the information in “Risk Factors” beginning on page PS-7 of this product supplement. You may lose all or a significant portion of your investment in the notes.

None of the Securities and Exchange Commission (the “SEC”), any state securities commission, or any other regulatory body has approved or disapproved of these securities or passed upon the adequacy or accuracy of this product supplement, the prospectus supplement, or the prospectus. Any representation to the contrary is a criminal offense.

Merrill Lynch & Co.

| Page | ||||

| PS-3 | ||||

| PS-7 | ||||

| PS-18 | ||||

| PS-19 | ||||

| PS-28 | ||||

| PS-33 | ||||

| PS-40 | ||||

PS-2

The information in this “Summary” section is qualified in its entirety by the more detailed explanation set forth elsewhere in this product supplement, the prospectus supplement, and the prospectus, as well as the applicable term sheet. Neither we nor MLPF&S have authorized any other person to provide you with any information different from the information set forth in these documents. If anyone provides you with different or inconsistent information about the notes, you should not rely on it.

Key Terms:

| General: | The notes are senior debt securities issued by Wells Fargo, and are not guaranteed or insured by the FDIC or secured by collateral. They rank equally with all of our other unsecured senior debt from time to time outstanding. Any payments due on the notes, including any repayment of principal, are subject to our credit risk.

The return on the notes will be based on the performance of a Market Measure and there is no guaranteed return of principal at maturity. Therefore, you may lose all or a significant portion of your investment if the notes are not automatically called prior to maturity, if applicable, and the value of the Market Measure decreases from the Starting Value to an Ending Value that is less than the Threshold Value.

Each issue of the notes will mature on the date set forth in the applicable term sheet, unless, if applicable, the notes are automatically called on an earlier date. You should be aware that if the automatic call feature applies to your notes, it may shorten the term of an investment in the notes, and you must be willing to accept that your notes may be called prior to maturity.

You will not receive any interest payments. | |

| Market Measure: |

The Market Measure may consist of one or more of the following:

• U.S. broad-based equity indices;

• U.S. sector or style-based equity indices;

• non-U.S. or global equity indices; or

• any combination of the above.

The Market Measure may consist of a group, or “Basket,” of the foregoing. We refer to each equity index included in any Basket as a “Basket Component.” If the Market Measure to which your notes are linked is a Basket, the Basket Components will be set forth in the applicable term sheet. | |

| Market Measure Performance: |

The performance of the Market Measure will be measured according to the percentage change of the Market Measure from its Starting Value to its Ending Value or, if applicable, its Observation Level.

Unless otherwise specified in the applicable term sheet:

The “Starting Value” will equal the closing level of the Market Measure on the date | |

PS-3

| when the notes are priced for initial sale to the public (the “pricing date”).

If the Market Measure consists of a Basket, the Starting Value will be equal to 100. See “Description of the Notes—Basket Market Measures.”

The “Threshold Value” will be a value of the Market Measure that equals a specified percentage (100% or less) of the Starting Value. The Threshold Value will be determined on the pricing date and set forth in the term sheet. If the Threshold Value is equal to 100% of the Starting Value, you will be exposed to any decrease in the value of the Market Measure from the Starting Value to the Ending Value on a 1-to-1 basis, and you may lose all of your investment in the notes.

The “Ending Value” will equal the closing level of the Market Measure on the calculation day (as defined below).

If the applicable term sheet specifies that the notes will be subject to an automatic call:

The “Call Level” will be a value of the Market Measure that equals a specified percentage of the Starting Value.

The “Observation Level” will equal the closing level of the Market Measure on the applicable Observation Date. The “Observation Dates” will be set forth in the applicable term sheet, subject to postponement in the event of Market Disruption Events (as defined below). The final Observation Date will be prior to the calculation day. See “Description of the Notes—Automatic Call.”

If the Market Measure consists of a Basket, the Ending Value will be the value of the Basket on the calculation day, and if applicable, each Observation Level will be the value of the Basket on the applicable Observation Date, determined as described in “Description of the Notes—Basket Market Measures—Observation Level or Ending Value of the Basket.”

If a Market Disruption Event occurs and is continuing on the calculation day or an Observation Date, if applicable, or if certain other events occur, the calculation agent will determine the Ending Value or, if applicable, the Observation Level as set forth in the section “Description of the Notes—Automatic Call,” “—The Starting Value, the Observation Level and the Ending Value—Ending Value,” and “—Basket Market Measures—Observation Level or Ending Value of the Basket.” | ||

| Step Up Value: | A value of the Market Measure that is a specified percentage (over 100%) of the Starting Value, as set forth in the applicable term sheet. | |

| Step Up Payment: |

A dollar amount that will be equal to a percentage of the principal amount. This percentage will equal the percentage by which the Step Up Value is greater than the Starting Value. The Step Up Payment will be determined on the pricing date and set forth in the applicable term sheet. | |

| Redemption Amount at Maturity: |

Unless the notes are subject to an automatic call and are automatically called prior to the maturity date, at maturity, you will receive a Redemption Amount that is greater than the principal amount if the value of the Market Measure does not change or increases from the Starting Value to the Ending Value. If the value of the Market Measure decreases from the Starting Value to the Ending Value but not below the | |

PS-4

| Threshold Value, you will receive a Redemption Amount equal to the principal amount. If the Ending Value is less than the Threshold Value, you will be subject to 1-to-1 downside exposure to the decrease in the value of the Market Measure below the Threshold Value, and will receive a Redemption Amount that is less than the principal amount. If the Threshold Value is equal to 100% of the Starting Value, the Redemption Amount could be zero.

Any payments due on the notes, including any repayment of principal, are subject to our credit risk as issuer of the notes.

The Redemption Amount, denominated in U.S. dollars, will be calculated as follows:

If specified in the term sheet, your notes may provide at maturity a leveraged return if the Ending Value is greater than the Step Up Value. In this case, a Participation Rate (as defined below) will be specified in the term sheet. | ||

| Participation Rate: |

The Participation Rate, if applicable, will be set forth in the applicable term sheet and is the rate at which investors participate in any increase in the value of the Market Measure if the Ending Value is greater than the Step Up Value. | |

| Automatic Call Prior to Maturity: |

If specified in the applicable term sheet, your notes may be subject to an automatic call. In that case, the notes will be automatically called on an Observation Date if the Observation Level of the Market Measure on that Observation Date is greater than or equal to the Call Level. If the notes are not automatically called, the payment at maturity will be determined as set forth under “Redemption Amount at Maturity” above. | |

| Call Amount: | If your notes are subject to an automatic call and are called on an Observation Date, you will receive the Call Amount applicable to that Observation Date. The Call Amount will be equal to the principal amount per unit plus the applicable “Call Premium.” Each Call Premium will be a percentage of the principal amount and will be set forth in the applicable term sheet. The Call Amount, if payable, will be payable | |

PS-5

| on the applicable “Call Settlement Date” set forth in the applicable term sheet. | ||

| Principal at Risk: |

You may lose all or a significant portion of the principal amount of the notes. Further, if you sell your notes prior to maturity, you may find that the market value per note is less than the price that you paid for the notes. | |

| Calculation Agents: |

The calculation agents will make all determinations associated with the notes. Unless otherwise set forth in the applicable term sheet, we or one of our affiliates may act as the calculation agent, or we may appoint MLPF&S or one of its affiliates to act as calculation agent for the notes. Alternatively, we (or one of our affiliates) and MLPF&S (or one of its affiliates) may act as joint calculation agents for the notes. See the section entitled “Description of the Notes—Role of the Calculation Agent.” | |

| Agents: | MLPF&S and one or more of its affiliates will act as our agents in connection with each offering of the notes and will receive an underwriting discount based on the number of units of notes sold. None of the agents is your fiduciary or adviser solely as a result of the making of any offering of the notes, and you should not rely upon this product supplement, the term sheet, or the accompanying prospectus or prospectus supplement as investment advice or a recommendation to purchase the notes. | |

| Listing: | Unless otherwise specified in the applicable term sheet, the notes will not be listed on a securities exchange or quotation system. | |

This product supplement relates only to the notes and does not relate to any equity index that comprises the Market Measure described in any term sheet. You should read carefully the entire prospectus, prospectus supplement, and product supplement, together with the applicable term sheet, to understand fully the terms of your notes, as well as the tax and other considerations important to you in making a decision about whether to invest in any notes. In particular, you should review carefully the section in this product supplement entitled “Risk Factors,” which highlights a number of risks of an investment in the notes, to determine whether an investment in the notes is appropriate for you. If information in this product supplement is inconsistent with the prospectus or prospectus supplement, this product supplement will supersede those documents. However, if information in any term sheet is inconsistent with this product supplement, that term sheet will supersede this product supplement. For example, we may offer notes in which the Step Up Payment will be paid if the Ending Value equals or exceeds the Threshold Value. You should carefully review the applicable term sheet to understand the specific terms of your notes.

Neither we nor any agent is making an offer to sell the notes in any jurisdiction where the offer or sale is not permitted. This product supplement and the accompanying prospectus supplement and prospectus are not an offer to sell these notes to anyone, and are not soliciting an offer to buy these notes from anyone, in any jurisdiction where the offer or sale is not permitted.

Certain capitalized terms used and not defined in this product supplement have the meanings ascribed to them in the prospectus supplement and prospectus. Unless otherwise indicated or unless the context requires otherwise, all references in this product supplement to “we,” “us,” “our,” or similar references are to Wells Fargo.

You are urged to consult with your own attorneys and business and tax advisers before making a decision to purchase any notes.

PS-6

Your investment in the notes is subject to investment risks, many of which differ from those of a conventional debt security. Your decision to purchase the notes should be made only after carefully considering the risks, including those discussed below, together with the risk information in the applicable term sheet, in light of your particular circumstances. The notes are not an appropriate investment for you if you are not knowledgeable about the material terms of the notes or investments in equity or equity-based securities in general.

General Risks Relating to the Notes

Your investment may result in a loss; there is no guaranteed return of principal. There is no fixed principal repayment amount on the notes at maturity. The return on the notes will be based on the performance of the Market Measure and therefore, you may lose all or a significant portion of your investment if the notes are not automatically called, if applicable, and if the value of the Market Measure decreases from the Starting Value to an Ending Value that is less than the Threshold Value. If the Threshold Value is equal to 100% of the Starting Value, the Redemption Amount could be zero.

Your return on the notes may be less than the yield on a conventional fixed or floating rate debt security of comparable maturity. There will be no periodic interest payments on the notes as there would be on a conventional fixed-rate or floating-rate debt security having the same maturity. Any return that you receive on the notes may be less than the return you would earn if you purchased a conventional debt security with the same maturity date. As a result, your investment in the notes may not reflect the full opportunity cost to you when you consider factors, such as inflation, that affect the time value of money.

If the notes are subject to an automatic call and are called prior to maturity, your investment return will be limited to the return represented by the Call Premium. If the notes are subject to an automatic call, and if the Observation Level of the Market Measure on an Observation Date is greater than or equal to the specified Call Level, we will automatically call the notes. If the notes are automatically called, your return will be limited to the applicable Call Premium, regardless of the extent of the increase in the value of the Market Measure.

Any positive return on your investment may be less than a comparable investment directly in the Market Measure. Unless otherwise set forth in the applicable term sheet, the Ending Value and the Observation Levels, if applicable, of the Market Measure will not reflect the value of dividends paid, or distributions made, on the securities included in the Market Measure or any other rights associated with those securities. Thus, any return on the notes will not reflect the return you would realize if you actually owned the securities underlying the Market Measure.

Additionally, the Market Measure may consist of one or more equity indices calculated in a non-U.S. currency, which include components traded in such non-U.S. currency. If the value of that currency strengthens against the U.S. dollar during the term of your notes, you may not obtain the benefit of that increase, which you would have received if you had owned the securities included in the index or indices.

Reinvestment Risk. If the notes are subject to an automatic call and are automatically called prior to maturity, the term of the notes will be short. There is no guarantee that you would be able to reinvest the proceeds from an investment in the notes at a comparable return for a similar level of risk in the event the notes are called prior to maturity.

PS-7

The notes are subject to our credit risk. The notes are our obligations and are not, either directly or indirectly, an obligation of any third party. Any amounts payable under the notes are subject to our creditworthiness, and you will have no ability to pursue the issuers of any securities represented by the Market Measure for payment. As a result, our actual and perceived creditworthiness may affect the value of the notes and, in the event we were to default on our obligations, you may not receive any amounts owed to you under the terms of the notes.

The estimated value of the notes will be determined by our affiliate’s pricing models, which may differ from those of MLPF&S or other dealers.

The estimated value of the notes will be set forth in the applicable term sheet and will be determined for us by our affiliate, Wells Fargo Securities, LLC (“WFS”), using its proprietary pricing models and related market inputs and assumptions. Based on these pricing models and related market inputs and assumptions, WFS will determine an estimated value for the notes by estimating the value of the combination of hypothetical financial instruments that would replicate the payout on the notes, which combination will consist of a non-interest bearing, fixed-income bond (the “debt component”) and one or more derivative instruments underlying the economic terms of the notes (the “derivative component”).

The estimated value of the debt component will be based on a reference interest rate, determined by WFS as of a date near the time of calculation, that will generally track our secondary market rates. The reference interest rate to be used in the calculation of the estimated value of the debt component may be higher or lower than our secondary market rates at the time of that calculation. Because the reference interest rate is generally higher than the assumed funding rate that is used to determine the economic terms of the notes, using the reference interest rate to value the debt component will generally result in a lower estimated value of the notes than if we had used the assumed funding rate. WFS will calculate the estimated value of the derivative component based on a proprietary derivative-pricing model, which will generate a theoretical price for the derivative instruments that constitute the derivative component based on various inputs including, but not limited to, market measure performance; interest rates; volatility of the market measure; correlation among basket components (if applicable); time remaining to maturity; dividend yields on the securities included in or held by the market measure; currency exchange rates (if applicable); volatility of currency exchange rates (if applicable); and correlation between currency exchange rates and the market measure (if applicable). These inputs may be market-observable or may be based on assumptions made by WFS in its discretion.

The estimated value of the notes will not be an independent third-party valuation and certain inputs to these models may be determined by WFS in its discretion. WFS’s views on these inputs may differ from those of MLPF&S and other dealers, and WFS’s estimated value of the notes may be higher, and perhaps materially higher, than the estimated value of the notes that would be determined by MLPF&S or other dealers in the market. WFS’s models and its inputs and related assumptions may prove to be wrong and therefore not an accurate reflection of the value of the notes.

The estimated value of the notes on the pricing date, based on WFS’s proprietary pricing models, will be less than the public offering price. The public offering price of the notes will include certain costs that are borne by you. Because of these costs, the estimated value of the notes on the pricing date will be less than the public offering price. The costs included in the public offering price will relate to selling, structuring, hedging and issuing the notes, as well as to our funding considerations for debt of this type. The costs related to selling, structuring, hedging and issuing the notes will include the underwriting discount, the

PS-8

projected profit that our hedge counterparty (which may be MLPF&S or one of its affiliates) will expect to realize for assuming risks inherent in hedging our obligations under the notes and hedging and other costs relating to the offering of the notes. Our funding considerations will be reflected in the fact that we will determine the economic terms of the notes based on an assumed funding rate that will generally be lower than our secondary market rates. If the costs relating to selling, structuring, hedging and issuing the notes were lower, or if the assumed funding rate we will use to determine the economic terms of the securities were higher, the economic terms of the notes would be more favorable to you and the estimated value would be higher.

The public offering price you pay for the notes will exceed the initial estimated value. If you attempt to sell the notes prior to maturity, their market value may be lower than the price you paid for them and lower than the initial estimated value. This is due to, among other things, the assumed funding rate used to determine the economic terms of the notes, and the inclusion in the public offering price of the underwriting discount and the estimated cost of hedging our obligations under the notes (which includes a hedging related charge as described in the applicable term sheet). These factors, together with customary bid ask spreads, other transaction costs and various credit, market and economic factors over the term of the notes, including changes in the level of the Market Measure, are expected to reduce the price at which you may be able to sell the notes in any secondary market and will affect the value of the notes complex and unpredictable ways.

The initial estimated value does not represent the price at which we, MLPF&S or any of our respective affiliates would be willing to purchase your notes in any secondary market (if any exists) at any time. The value of your notes at any time after issuance will vary based on many factors that cannot be predicted with accuracy, including the performance of the Market Measure, our creditworthiness and changes in market conditions. MLPF&S has advised us that any repurchases by them or their affiliates are expected to be made at prices determined by reference to their pricing models and at their discretion, and these prices will include MLPF&S’s trading commissions and mark-ups. If you sell your notes to a dealer other than MLPF&S in a secondary market transaction, the dealer may impose its own discount or commission.

We cannot assure you that there will be a trading market for your notes. If a secondary market exists, we cannot predict how the notes will trade, or whether that market will be liquid or illiquid. The development of a trading market for the notes will depend on various factors, including our financial performance and changes in the value of the Market Measure. The number of potential buyers of your notes in any secondary market may be limited. There is no assurance that any party will be willing to purchase your notes at any price in any secondary market.

We anticipate that one or more of the agents will act as a market-maker for the notes, but none of them is required to do so and may cease to do so at any time. Any price at which an agent may bid for, offer, purchase, or sell any of the notes may be higher or lower than the applicable public offering price, and that price may differ from the values determined by pricing models that it may use, whether as a result of dealer discounts, mark-ups, or other transaction costs. These bids, offers, or transactions may affect the prices, if any, at which the notes might otherwise trade in the market. In addition, if at any time any agent were to cease acting as a market-maker for any issue of the notes, it is likely that there would be significantly less liquidity in that secondary market. In such a case, the price at which those notes could be sold likely would be lower than if an active market existed.

Unless otherwise stated in the term sheet, we will not list the notes on any securities exchange or quotation system. Even if an application were made to list your notes, we cannot

PS-9

assure you that the application will be approved or that your notes will be listed and, if listed, that they will remain listed for their entire term. The listing of the notes on any securities exchange or quotation system will not necessarily ensure that a trading market will develop, and if a trading market does develop, that there will be liquidity in the trading market.

Payment on the notes will not reflect changes in the value of the Market Measure other than on the calculation day or the relevant Observation Date, if applicable. Changes in the value of the Market Measure during the term of the notes other than on the calculation day, or the relevant Observation Date, if applicable, will not be reflected in the calculation of the Redemption Amount or the determination of whether the notes will be automatically called, if applicable. To make that calculation or determination, the calculation agent will refer only to the value of the Market Measure on the calculation day, or the relevant Observation Date, if applicable. No other values of the Market Measure will be taken into account. As a result, even if the value of the Market Measure has increased at certain times during the term of the notes, your notes will not be called if the Observation Level on each Observation Date is less than the Call Level, if applicable, and you will receive a Redemption Amount that is less than the principal amount if the Ending Value is less than the Threshold Value.

If your notes are linked to a Basket, changes in the levels of one or more of the Basket Components may be offset by changes in the levels of one or more of the other Basket Components. The Market Measure of your notes may be a Basket. In such a case, changes in the levels of one or more of the Basket Components may not correlate with changes in the levels of one or more of the other Basket Components. The levels of one or more Basket Components may increase, while the levels of one or more of the other Basket Components may decrease or not increase as much. Therefore, in calculating the value of the Market Measure at any time, increases in the level of one Basket Component may be moderated or wholly offset by decreases or lesser increases in the levels of one or more of the other Basket Components. If the weightings of the applicable Basket Components are not equal, adverse changes in the levels of the Basket Components which are more heavily weighted could have a greater impact upon your notes.

The respective publishers of the applicable indices may adjust those indices in a way that affects their levels, and these publishers have no obligation to consider your interests. Unless otherwise specified in the term sheet, we, the agents and our respective affiliates have no affiliation with any publisher of an index to which your notes are linked (each, an “Index Publisher”). Consequently, we have no control of the actions of any Index Publisher. The Index Publisher can add, delete, or substitute the components included in that index or make other methodological changes that could change its level. A new security included in an index may perform significantly better or worse than the replaced security, and the performance will impact the level of the applicable index. Additionally, an Index Publisher may alter, discontinue, or suspend calculation or dissemination of an index. Any of these actions could adversely affect the value of your notes. The Index Publishers will have no obligation to consider your interests in calculating or revising any index.

Exchange rate movements may impact the value of the notes. If any security included in a Market Measure is traded in a currency other than U.S. dollars and, for purposes of the applicable index, is converted into U.S. dollars, then the value of the Market Measure may depend in part on the relevant exchange rates. If the value of the U.S. dollar strengthens against the currencies of that index, the level of the applicable index may be adversely affected and any payment on the notes may be reduced. Exchange rate movements may be particularly impacted by existing and expected rates of inflation and interest rate levels; political, civil or military unrest; the balance of payments between countries; and the extent of governmental

PS-10

surpluses or deficits in the countries relevant to the applicable index and the United States. All of these factors are in turn sensitive to the monetary, fiscal, and trade policies pursued by the governments of those countries and the United States and other countries important to international trade and finance.

If you attempt to sell the notes prior to maturity, their market value, if any, will be affected by various factors that interrelate in complex ways, and their market value may be less than the principal amount. The notes are not designed to be short-term trading instruments. The limited protection against the risk of losses provided by the Threshold Value, if any, will only apply if you hold the notes to maturity. You have no right to have your notes redeemed at your option prior to maturity. If you wish to liquidate your investment in the notes prior to maturity, your only option would be to sell them. At that time, there may be an illiquid market for your notes or no market at all. Even if you were able to sell your notes, there are many factors outside of our control that may affect their market value, some of which, but not all, are stated below. The impact of any one factor may be offset or magnified by the effect of another factor. The following paragraphs describe a specific factor’s expected impact on the market value of the notes, assuming all other conditions remain constant.

| • | Value of the Market Measure. We anticipate that the market value of the notes prior to maturity generally will depend to a significant extent on the value of the Market Measure. In general, it is expected that the market value of the notes will decrease as the value of the Market Measure decreases, and increase as the value of the Market Measure increases. However, as the value of the Market Measure increases or decreases, the market value of the notes is not expected to increase or decrease at the same rate. If you sell your notes when the value of the Market Measure is less than, or not sufficiently above, the Starting Value, or, if applicable, the Call Level, then you may receive less than the principal amount of your notes. |

In addition, if the notes are subject to an automatic call, because the amount payable on the notes upon an automatic call will not exceed the applicable Call Amount, we do not expect that the notes will trade in any secondary market prior to any Observation Date at a price that is greater than the applicable Call Amount.

| • | Volatility of the Market Measure. Volatility is the term used to describe the size and frequency of market fluctuations. Increases or decreases in the volatility of the Market Measure may have an adverse impact on the market value of the notes. Even if the value of the Market Measure increases after the applicable pricing date, if you are able to sell your notes before their maturity date, you may receive substantially less than the amount that would be payable at maturity or upon an automatic call, if applicable, based on that value because of the anticipation that the value of the Market Measure will continue to fluctuate until the notes are automatically called, if applicable, or the calculation day. |

| • | Economic and Other Conditions Generally. The general economic conditions of the capital markets in the United States, as well as geopolitical conditions and other financial, political, regulatory, and judicial events and related uncertainties that affect stock markets generally, may affect the value of the Market Measure and the market value of the notes. If the Market Measure includes one or more indices that have returns that are calculated based upon securities prices in one or more non-U.S. markets (a “non-U.S. Market Measure”), the value of your notes may also be affected by similar events in the markets of the relevant foreign countries. |

| • | Interest Rates. We expect that changes in interest rates will affect the market value of the notes. In general, if U.S. interest rates increase, we expect that the market value of the notes will decrease, and conversely, if U.S. interest rates decrease, we expect that the |

PS-11

| market value of the notes will increase. In general, we expect that the longer the amount of time that remains until maturity, the more significant the impact of these changes will be on the value of the notes. In the case of non-U.S. Market Measures, the level of interest rates in the relevant foreign countries may also affect their economies and in turn the value of the non-U.S. Market Measure, and, thus, the market value of the notes may be adversely affected. |

| • | Dividend Yields. In general, if cumulative dividend yields on the securities included in the Market Measure increase, we anticipate that the market value of the notes will decrease; conversely, if those dividend yields decrease, we anticipate that the market value of your notes will increase. |

| • | Exchange Rate Movements and Volatility. If the Market Measure of your notes includes any non-U.S. Market Measures, changes in, and the volatility of, the exchange rates between the U.S. dollar and the relevant non-U.S. currency or currencies could have a negative impact on the value of your notes, and any payment on the notes may depend in part on the relevant exchange rates. In addition, the correlation between the relevant exchange rate and any applicable non-U.S. Market Measure reflects the extent to which a percentage change in that exchange rate corresponds to a percentage change in the applicable non-U.S. Market Measure, and changes in these correlations may have a negative impact on the value of your notes. |

| • | Our Creditworthiness. Our actual and perceived creditworthiness may affect the value of the notes. |

| • | Time to Maturity or, if Applicable, the Next Observation Date. There may be a disparity between the market value of the notes prior to maturity, or if applicable, prior to an Observation Date, and their value at maturity or as of the next Observation Date, if applicable. This disparity is often called a time “value,” “premium,” or “discount,” and reflects expectations concerning the value of the Market Measure during the term of the notes. As the time to maturity, or if applicable, the next Observation Date, decreases, this disparity may decrease, such that the value of the notes will approach the expected Redemption Amount to be paid at maturity, or if applicable, the Call Amount to be paid at the next Call Settlement Date. |

Trading and hedging activities by us, the agents, and our respective affiliates may affect your return on the notes and their market value. We, the agents, and our respective affiliates may buy or sell the securities included in the Market Measure, futures or options contracts or exchange-traded instruments on the Market Measure or its component securities, or other listed or over the counter derivative instruments linked to the Market Measure or its component securities. We, the agents and our respective affiliates may execute such purchases or sales for our own or their own accounts, for business reasons, or in connection with hedging our obligations under the notes. These transactions could affect the value of these securities and, in turn, the value of a Market Measure in a manner that could be adverse to your investment in the notes. On or before the applicable pricing date, any purchases or sales by us, the agents, and our respective affiliates, or others on our or their behalf (including for the purpose of hedging anticipated exposure) may increase the value of a Market Measure or its component securities. Consequently, the values of that Market Measure or the securities included in that Market Measure may decrease subsequent to the pricing date of an issue of the notes, adversely affecting the market value of the notes.

We, the agents, or one or more of our respective affiliates may also engage in hedging activities that could increase the value of the Market Measure on the applicable pricing date. In addition, these activities, including the unwinding of a hedge, may decrease the market

PS-12

value of your notes prior to maturity, including on the calculation day, or if applicable, on each Observation Date, and may reduce any payment on the notes. The agents, or one or more of their respective affiliates may purchase or otherwise acquire a long or short position in the notes, and may hold or resell the notes. For example, the agents may enter into these transactions in connection with any market making activities in which they engage. We cannot assure you that these activities will not adversely affect the value of the Market Measure or the market value of your notes prior to maturity, or any payment on the notes.

Our trading, hedging and other business activities, and those of the agents or one or more of our respective affiliates, may create conflicts of interest with you. We, the agents, or one or more of our respective affiliates may engage in trading activities related to the Market Measure and to securities included in the Market Measure that are not for your account or on your behalf. We, the agents, or one or more of our respective affiliates also may issue or underwrite other financial instruments with returns based upon the applicable Market Measure. These trading and other business activities may present a conflict of interest between your interest in the notes and the interests we, the agents and our respective affiliates may have in our proprietary accounts, in facilitating transactions, including block trades, for our or their other customers, and in accounts under our or their management. These trading and other business activities, if they influence the value of the Market Measure or secondary trading in your notes, could be adverse to your interests as a beneficial owner of the notes.

We, the agents, and our respective affiliates expect to enter into arrangements or adjust or close out existing transactions to hedge our obligations under the notes. We, the agents, or our respective affiliates also may enter into hedging transactions relating to other notes or instruments that we or they issue, some of which may have returns calculated in a manner related to that of a particular issue of the notes. We may enter into such hedging arrangements with one or more of our subsidiaries or affiliates, or with one or more of the agents or their affiliates. Such a party may enter into additional hedging transactions with other parties relating to the notes and the applicable Market Measure. This hedging activity is expected to result in a profit to those engaging in the hedging activity, which could be more or less than initially expected, or the hedging activity could also result in a loss. We, the agents, and our respective affiliates will price these hedging transactions with the intent to realize a profit, regardless of whether the value of the notes increases or decreases, whether the notes will be automatically called, if applicable, or whether the Redemption Amount on the notes is more or less than the principal amount of the notes. Any profit in connection with such hedging activities will be in addition to any other compensation that we, the agents, and our respective affiliates receive for the sale of the notes, which creates an additional incentive to sell the notes to you.

There may be potential conflicts of interest involving the calculation agent. We may appoint and remove the calculation agent. We or one of our affiliates may be the calculation agent or act as joint calculation agent for the notes and, as such, will determine the Starting Value, the Step Up Value, the Threshold Value, the Ending Value, the Redemption Amount and, if applicable, the Call Level and each Observation Level and whether the notes will be automatically called. Under some circumstances, these duties could result in a conflict of interest between our status as issuer and our responsibilities as calculation agent. These conflicts could occur, for instance, in connection with the calculation agent’s determination as to whether a Market Disruption Event has occurred, or in connection with judgments that the calculation agent would be required to make if the publication of an index is discontinued. See the sections entitled “Description of the Notes—Market Disruption Events,” “—Adjustments to an Index,” and “—Discontinuance of an Index.” The calculation agent will be required to carry out its duties in good faith and using its reasonable judgment. However, because we or one of our affiliates may serve as the calculation agent, potential conflicts of interest could arise. In

PS-13

addition, we may appoint MLPF&S or one of its affiliates to act as the calculation agent or as joint calculation agent for the notes. As the calculation agent or joint calculation agent, MLPF&S or one of its affiliates will have discretion in making various determinations that affect your notes. The exercise of this discretion by the calculation agent could adversely affect the value of your notes and may present the calculation agent with a conflict of interest of the kind described under “—Trading and hedging activities by us, the agents, and our respective affiliates may affect your return on the notes and their market value” and “—Our trading, hedging and other business activities, and those of the agents or one or more of our respective affiliates, may create conflicts of interest with you” above.

The U.S. federal tax consequences of an investment in the notes are unclear. There is no direct legal authority regarding the proper U.S. federal tax treatment of the notes, and we do not plan to request a ruling from the Internal Revenue Service (the “IRS”). Consequently, significant aspects of the tax treatment of the notes are uncertain, and the IRS or a court might not agree with the treatment of the notes as prepaid derivative contracts that are “open transactions” for U.S. federal income tax purposes. If the IRS were successful in asserting an alternative treatment of the notes, the tax consequences of ownership and disposition of the notes might be materially and adversely affected. Even if the treatment of the notes as prepaid derivative contracts that are “open transactions” is respected, a note that is linked to a Market Measure that includes underlying equity interests in certain types of entities (including exchange-traded funds, real estate investment trusts and partnerships) may be subject to adverse treatment under the “constructive ownership” rules.

Section 871(m) of the Internal Revenue Code of 1986, as amended (the “Code”), imposes a withholding tax of up to 30% on “dividend equivalents” paid or deemed paid to non-U.S. investors with respect to certain financial instruments linked to U.S. equities. This withholding regime generally applies to financial instruments that substantially replicate the economic performance of one or more U.S. equities, as determined based on tests set forth in the applicable regulations. The Section 871(m) regime requires complex calculations to be made with respect to financial instruments linked to U.S. equities, and its application to a specific issue of notes may be uncertain. Accordingly, even if we determine that certain notes are not subject to Section 871(m), the IRS could challenge our determination and assert that withholding is required in respect of those notes. Moreover, the application of Section 871(m) to a note may be affected if a non-U.S. investor enters into other transactions relating to a market measure. Non-U.S. investors should consult their tax advisers regarding the application of Section 871(m) in their particular circumstances. If withholding applies to the notes, neither we nor our agents (including MLPF&S) will be required to pay any additional amounts with respect to amounts withheld.

The U.S. Treasury Department and the IRS have requested comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar financial instruments and have indicated that such transactions may be the subject of future regulations or other guidance. In addition, members of Congress have proposed legislative changes to the tax treatment of derivative contracts. Any legislation, Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the notes, possibly with retroactive effect.

Both U.S. and non-U.S. investors should read carefully the section of this product supplement entitled “United States Federal Tax Considerations” and consult their tax advisers regarding the U.S. federal tax consequences of an investment in the notes, as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

PS-14

Risks Relating to the Market Measures

You must rely on your own evaluation of the merits of an investment linked to the applicable Market Measure. In the ordinary course of business, we, the agents, and our respective affiliates may have expressed views on expected movements in a Market Measure or the securities included in the Market Measure, and may do so in the future. These views or reports may be communicated to our clients and clients of these entities. However, these views are subject to change from time to time. Moreover, other professionals who deal in markets relating to a Market Measure may at any time have significantly different views from our views and the views of these entities. For these reasons, you are encouraged to derive information concerning a Market Measure and its component securities from multiple sources, and you should not rely on our views or the views expressed by these entities.

You will have no rights as a security holder, you will have no rights to receive any of the securities represented by the Market Measure, and you will not be entitled to dividends or other distributions by the issuers of these securities. The notes are our debt securities. They are not equity instruments, shares of stock, or securities of any other issuer. Investing in the notes will not make you a holder of any of the securities represented by the Market Measure. You will not have any voting rights, any rights to receive dividends or other distributions, or any other rights with respect to those securities. As a result, the return on your notes may not reflect the return you would realize if you actually owned those securities and received the dividends paid or other distributions made in connection with them. Additionally, the levels of certain indices reflect only the prices of the securities included in that index and do not take into consideration the value of dividends paid on those securities. Your notes will be paid in cash and you have no right to receive any of these securities.

If the Market Measure to which your notes are linked includes equity securities traded on foreign exchanges, your return may be affected by factors affecting international securities markets. The value of securities traded outside of the U.S. may be adversely affected by a variety of factors relating to the relevant securities markets. Factors which could affect those markets, and therefore the return on your notes, include:

| • | Market Liquidity and Volatility. The relevant foreign securities markets may be less liquid and/or more volatile than U.S. or other securities markets and may be affected by market developments in different ways than U.S. or other securities markets. |

| • | Political, Economic, and Other Factors. The prices and performance of securities of companies in foreign countries may be affected by political, economic, financial, and social factors in those regions. Direct or indirect government intervention to stabilize a particular securities market and cross-shareholdings in companies in the relevant foreign markets may affect prices and the volume of trading in those markets. In addition, recent or future changes in government, economic, and fiscal policies in the relevant jurisdictions, the possible imposition of, or changes in, currency exchange laws, or other laws or restrictions, and possible fluctuations in the rate of exchange between currencies, are factors that could negatively affect the relevant securities markets. The relevant foreign economies may differ from the U.S. economy in economic factors such as growth of gross national product, rate of inflation, capital reinvestment, resources, and self-sufficiency. |

In particular, many emerging nations are undergoing rapid change, involving the restructuring of economic, political, financial and legal systems. Regulatory and tax environments may be subject to change without review or appeal, and many emerging markets suffer from underdevelopment of capital markets and tax systems. In addition,

PS-15

in some of these nations, issuers of the relevant securities face the threat of expropriation of their assets, and/or nationalization of their businesses. The economic and financial data about some of these countries may be unreliable.

| • | Publicly Available Information. There is generally less publicly available information about foreign companies than about U.S. companies that are subject to the reporting requirements of the SEC. In addition, accounting, auditing, and financial reporting standards and requirements in foreign countries differ from those applicable to U.S. reporting companies. |

Unless otherwise set forth in the applicable term sheet, we and the agents do not control any company included in any Market Measure and have not verified any disclosure made by any other company. We, the agents, or our respective affiliates currently, or in the future, may engage in business with companies included in a Market Measure, and we, the agents, or our respective affiliates may from time to time own securities of companies included in a Market Measure. However, none of us, the agents, or any of our respective affiliates has the ability to control the actions of any of these companies or has undertaken any independent review of, or made any due diligence inquiry with respect to, any of these companies, unless (and only to the extent that) the securities of us, the agents, or our respective affiliates are represented by that Market Measure. In addition, unless otherwise set forth in the applicable term sheet, none of us, the agents, or any of our respective affiliates is responsible for the calculation of any index represented by a Market Measure. Unless otherwise specified therein, any information in the applicable term sheet regarding the Market Measure will be derived from publicly available information. You should make your own investigation into the Market Measure.

Unless otherwise set forth in the applicable term sheet, none of the Index Publishers, their affiliates, or any companies included in the Market Measure will be involved in any offering of the notes or will have any obligation of any sort with respect to the notes. As a result, none of those companies will have any obligation to take your interests as holders of the notes into consideration for any reason, including taking any corporate actions that might affect the value of the securities represented by the Market Measure or the value of the notes.

Our business activities and those of the agents relating to the companies represented by a Market Measure or the notes may create conflicts of interest with you. We, the agents, and our respective affiliates, at the time of any offering of the notes or in the future, may engage in business with the companies represented by a Market Measure, including making loans to, equity investments in, or providing investment banking, asset management, or other services to those companies, their affiliates, and their competitors.

In connection with these activities, any of these entities may receive information about those companies that we will not divulge to you or other third parties. We, the agents, and our respective affiliates have published, and in the future may publish, research reports on one or more of these companies. The agents may also publish research reports relating to our or our affiliates’ securities, including the notes. This research is modified from time to time without notice and may express opinions or provide recommendations that are inconsistent with purchasing or holding your notes. Any of these activities may affect the value of the Market Measure and, consequently, the market value of your notes. None of us, the agents, or our respective affiliates makes any representation to any purchasers of the notes regarding any matters whatsoever relating to the issuers of the securities included in a Market Measure. Any prospective purchaser of the notes should undertake an independent investigation of the companies included in a Market Measure to a level that, in its judgment, is appropriate to make an informed decision regarding an investment in the notes. The composition of the

PS-16

Market Measure does not reflect any investment recommendations from us, the agents, or our respective affiliates.

Historical levels of the Market Measure should not be taken as an indication of the future performance of the Market Measure during the term of the notes. Accordingly, any historical or hypothetical values of the Market Measure do not provide an indication of the future performance of the Market Measure.

Other Risk Factors Relating to the Applicable Market Measure

The applicable term sheet may set forth additional risk factors as to the Market Measure that you should review prior to purchasing the notes.

PS-17

We will use the net proceeds we receive from each sale of the notes for the purposes described in the accompanying prospectus under “Use of Proceeds” and the prospectus supplement under “Supplemental Use of Proceeds.” In addition, we expect that we or our affiliates may use a portion of the net proceeds to hedge our obligations under the notes.

PS-18

General

Each issue of the notes will be part of a series of medium-term notes entitled “Medium-Term Notes, Series S” that will be issued under the indenture, as amended and supplemented from time to time. The indenture is described more fully in the prospectus and prospectus supplement. The following description of the notes supplements and, to the extent it is inconsistent with, supersedes the description of the general terms and provisions of the notes and debt securities set forth under the headings “Description of Notes” in the prospectus supplement. These documents should be read in connection with the applicable term sheet.

The maturity date of the notes and the aggregate principal amount of each issue of the notes will be stated in the term sheet. If the scheduled maturity date is not a business day, we will make the required payment on the next business day, and no interest will accrue as a result of such delay.

We will not pay interest on the notes. The notes do not guarantee the return of principal at maturity. The notes will be payable only in U.S. dollars.

Unless subject to an automatic call and automatically called prior to the maturity date, the notes will mature on the date set forth in the applicable term sheet. Prior to the maturity date, the notes are not redeemable at our option or repayable at the option of any holder. The notes are not subject to any sinking fund. The notes are not subject to the defeasance provisions described in the prospectus supplement under the caption “Description of Notes.”

We will issue the notes in denominations of whole units. Unless otherwise set forth in the applicable term sheet, each unit will have a principal amount of $10. The CUSIP number for each issue of the notes will be set forth in the applicable term sheet. You may transfer the notes only in whole units.

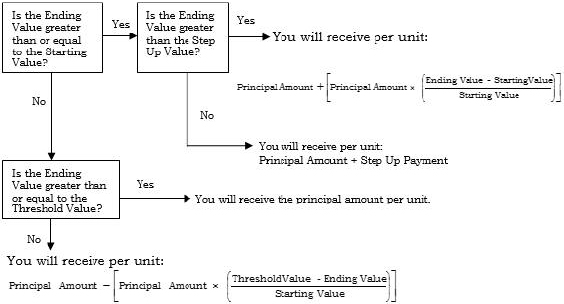

Payment at Maturity

If the notes are not subject to an automatic call or if the notes are subject to an automatic call but are not called, then at maturity, subject to our credit risk as issuer of the notes, you will receive a Redemption Amount, denominated in U.S. dollars. The “Redemption Amount” will be calculated as follows:

| • | If the Ending Value is greater than the Step Up Value, then the Redemption Amount will equal: |

| Principal Amount + | Principal Amount × | Ending Value – Starting Value | ||||||||||||||||||||||||

| Starting Value |

If specified in the applicable term sheet, your notes may provide a leveraged return at maturity if the Ending Value is greater than the Step Up Value. In this case, a Participation Rate will be specified in the term sheet.

PS-19

| • | If the Ending Value is greater than or equal to the Starting Value but is equal to or less than the Step Up Value, then the Redemption Amount will equal: |

Principal Amount + Step Up Payment

| • | If the Ending Value is less than the Starting Value, but is greater than or equal to the Threshold Value, then the Redemption Amount will equal the principal amount. |

| • | If the Ending Value is less than the Threshold Value, then the Redemption Amount will equal: |

| Principal Amount – | Principal Amount × | Threshold Value – Ending Value | ||||||||||||||||||||||||

| Starting Value |

The Redemption Amount will not be less than zero.

The “Step Up Value” will be a value of the Market Measure that is a specified percentage (over 100%) of the Starting Value, as set forth in the applicable term sheet.

The “Step Up Payment” will be a dollar amount that will be equal to a percentage of the principal amount. This percentage will equal the percentage by which the Step Up Value is greater than the Starting Value. The Step Up Payment will be determined on the pricing date and set forth in the applicable term sheet.

The “Threshold Value” will be a value of the Market Measure that equals a specified percentage of the Starting Value, which will be less than or equal to 100%. The Threshold Value will be determined on the pricing date and set forth in the term sheet. If the Threshold Value is equal to 100% of the Starting Value, then the Redemption Amount for the notes will be less than the principal amount if there is any decrease in the value of the Market Measure from the Starting Value to the Ending Value, and you may lose all of your investment in the notes.

The “Participation Rate”, if applicable, is the rate at which investors participate in any increase in the value of the Market Measure if the Ending Value is greater than the Step Up Value.

Each term sheet will provide examples of Redemption Amounts based on a range of hypothetical Ending Values.

The term sheet will set forth information as to the specific Market Measure, including information as to the historical values of the Market Measure. However, historical values of the Market Measure are not indicative of its future performance or the performance of your notes.

An investment in the notes does not entitle you to any ownership interest, including any voting rights, dividends paid, or other distributions made, in the securities of any of the companies included in a Market Measure.

Automatic Call

If specified in the applicable term sheet, the notes may be subject to an automatic call. In that case, the notes will be called, in whole but not in part, if the Observation Level of the Market Measure on any Observation Date is greater than or equal to the Call Level set forth in the applicable term sheet.

PS-20

The “Call Level” will be a value of the Market Measure that equals a specified percentage of the Starting Value.

The “Observation Dates” will be set forth in the applicable term sheet, subject to postponement in the event of Market Disruption Events. The final Observation Date will be prior to the calculation day.

If the notes are automatically called on an Observation Date, for each unit of the notes that you own, we will pay you on the related Call Settlement Date the Call Amount applicable to that Observation Date. The “Call Amount” will be equal to the principal amount plus the applicable Call Premium. The “Call Premium” will be a percentage of the principal amount.

The Observation Dates and the related Call Amounts and Call Premiums will be specified in the applicable term sheet.

If the notes are automatically called on an Observation Date, we will redeem the notes and pay the applicable Call Amount on the applicable Call Settlement Date. Each “Call Settlement Date” will occur on approximately the fifth business day after the applicable Observation Date, subject to postponement as described below.

If a scheduled Observation Date is determined by the calculation agent not to be a Market Measure Business Day (as defined below) by reason of an extraordinary event, occurrence, declaration, or otherwise, or if there is a Market Disruption Event on that day, the applicable Observation Date will be the immediately succeeding Market Measure Business Day during which no Market Disruption Event occurs or is continuing; provided that the Observation Level will not be determined on a date later than the fifth scheduled Market Measure Business Day after the scheduled Observation Date, and if that fifth day is not a Market Measure Business Day, or if there is a Market Disruption Event on that date, the calculation agent will determine (or, if not determinable, estimate) the Observation Level in a manner which the calculation agent considers commercially reasonable under the circumstances on that fifth scheduled Market Measure Business Day.

If, due to a Market Disruption Event or otherwise, a scheduled Observation Date is postponed, the relevant Call Settlement Date will be postponed to approximately the fifth business day following the Observation Date as postponed, unless otherwise specified in the applicable term sheet.

Unless otherwise specified in the term sheet, a “business day” means any day, other than Saturday or Sunday, that is neither a legal holiday nor a day on which banking institutions are authorized or required by law or regulation to close in New York, New York.

The Starting Value, the Observation Level and the Ending Value

Starting Value

Unless otherwise specified in the term sheet, the “Starting Value” will be the closing level of the Market Measure on the pricing date.

Observation Level

If applicable, the “Observation Level” will equal the closing level of the Market Measure on the applicable Observation Date.

PS-21

Ending Value

The “Ending Value” will equal the closing level of the Market Measure on the calculation day.

The “calculation day” means a Market Measure Business Day shortly before the maturity date on which a Market Disruption Event has not occurred. The calculation day will be set forth in the term sheet.

Unless otherwise specified in the applicable term sheet, a “Market Measure Business Day” means a day on which (1) the New York Stock Exchange (the “NYSE”) and The Nasdaq Stock Market, or their successors, are open for trading and (2) the applicable index or any successor is calculated and published.

If the scheduled calculation day is determined by the calculation agent not to be a Market Measure Business Day by reason of an extraordinary event, occurrence, declaration, or otherwise, or if there is a Market Disruption Event on that day, the calculation day will be the immediately succeeding Market Measure Business Day during which no Market Disruption Event occurs or is continuing; provided that the Ending Value will be determined (or, if not determinable, estimated) by the calculation agent in a commercially reasonable manner on a date no later than the second scheduled Market Measure Business Day prior to the maturity date, regardless of the occurrence of a Market Disruption Event on that day.

If the Market Measure consists of a Basket, the Starting Value, each Observation Level, if applicable, and the Ending Value of the Basket will be determined as described in “—Basket Market Measures.”

Market Disruption Events

For an index, “Market Disruption Event” means one or more of the following events, as determined by the calculation agent in its sole discretion:

| (A) | the suspension of or material limitation on trading, in each case, for more than two consecutive hours of trading, or during the one-half hour period preceding the close of trading, on the primary exchange where the securities included in an index trade (without taking into account any extended or after-hours trading session), in 20% or more of the securities which then compose the index or any successor index; and |

| (B) | the suspension of or material limitation on trading, in each case, for more than two consecutive hours of trading, or during the one-half hour period preceding the close of trading, on the primary exchange that trades options contracts or futures contracts related to the index (without taking into account any extended or after-hours trading session), whether by reason of movements in price otherwise exceeding levels permitted by the relevant exchange or otherwise, in options contracts or futures contracts related to the index, or any successor index. |

For the purpose of determining whether a Market Disruption Event has occurred:

| (1) | a limitation on the hours in a trading day and/or number of days of trading will not constitute a Market Disruption Event if it results from an announced change in the regular business hours of the relevant exchange; |

| (2) | a decision to permanently discontinue trading in the relevant futures or options |

PS-22

| contracts related to the index, or any successor index, will not constitute a Market Disruption Event; |

| (3) | a suspension in trading in a futures or options contract on the index, or any successor index, by a major securities market by reason of (a) a price change violating limits set by that securities market, (b) an imbalance of orders relating to those contracts, or (c) a disparity in bid and ask quotes relating to those contracts will constitute a suspension of or material limitation on trading in futures or options contracts related to the index; |

| (4) | a suspension of or material limitation on trading on the relevant exchange will not include any time when that exchange is closed for trading under ordinary circumstances; and |

| (5) | if applicable to indices with component securities listed on the NYSE, for the purpose of clause (A) above, any limitations on trading during significant market fluctuations under NYSE Rule 80B, or any applicable rule or regulation enacted or promulgated by the NYSE or any other self-regulatory organization or the SEC of similar scope as determined by the calculation agent, will be considered “material.” |

Adjustments to an Index

After the applicable pricing date, an Index Publisher may make a material change in the method of calculating an index or in another way that changes the index such that it does not, in the opinion of the calculation agent, fairly represent the level of the index had those changes or modifications not been made. In this case, the calculation agent will, at the close of business in New York, New York, on each date that the closing level is to be calculated, make adjustments to the index. Those adjustments will be made in good faith as necessary to arrive at a calculation of a level of the index as if those changes or modifications had not been made, and calculate the closing level of the index, as so adjusted.

Discontinuance of an Index

After the pricing date, an Index Publisher may discontinue publication of an index to which an issue of the notes is linked. The Index Publisher or another entity may then publish a substitute index that the calculation agent determines, in its sole discretion, to be comparable to the original index (a “successor index”). If this occurs, the calculation agent will substitute the successor index as calculated by the relevant Index Publisher or any other entity and calculate each Observation Level, if applicable, and/or the Ending Value as described under “—The Starting Value, the Observation Level and the Ending Value” or “—Basket Market Measure,” as applicable. If the calculation agent selects a successor index, the calculation agent will give written notice of the selection to the trustee, to us and to the holders of the notes.

PS-23

If an Index Publisher discontinues publication of the index before the calculation day or, if applicable, an Observation Date, and the calculation agent does not select a successor index, then on the day that would otherwise be the calculation day, or if applicable, an Observation Date, until the earlier to occur of:

| • | the occurrence of an automatic call, if applicable; |

| • | the determination of the Ending Value; or |

| • | a determination by the calculation agent that a successor index is available, |

the calculation agent will compute a substitute level for the index in accordance with the procedures last used to calculate the index before any discontinuance. The calculation agent will make available to holders of the notes information regarding those levels by means of Bloomberg L.P., Thomson Reuters, a website, or any other means selected by the calculation agent in its reasonable discretion.

If a successor index is selected or the calculation agent calculates a level as a substitute for an index, the successor index or level will be used as a substitute for all purposes, including for the purpose of determining whether a Market Disruption Event exists.

Notwithstanding these alternative arrangements, any modification or discontinuance of the publication of any index to which your notes are linked may adversely affect trading in the notes.

Basket Market Measures

If the Market Measure to which your notes are linked is a Basket, the Basket Components will be set forth in the term sheet. We will assign each Basket Component a weighting (the “Initial Component Weight”) so that each Basket Component represents a percentage of the Starting Value of the Basket on the pricing date. We may assign the Basket Components equal Initial Component Weights, or we may assign the Basket Components unequal Initial Component Weights. The Initial Component Weight for each Basket Component will be stated in the term sheet.

Determination of the Component Ratio for Each Basket Component

The “Starting Value” of the Basket will be equal to 100. We will set a fixed factor (the “Component Ratio”) for each Basket Component on the pricing date, based upon the weighting of that Basket Component. The Component Ratio for each Basket Component will equal:

| • | the Initial Component Weight (expressed as a percentage) for that Basket Component, multiplied by 100; divided by |

| • | the closing level of that Basket Component on the pricing date. |

Each Component Ratio will be rounded to eight decimal places.

The Component Ratios will be calculated in this way so that the Starting Value of the Basket will equal 100 on the pricing date. The Component Ratios will not be revised subsequent to their determination on the pricing date, except that the calculation agent may in its good faith judgment adjust the Component Ratio of any Basket Component in the event that Basket Component is materially changed or modified in a manner that does not, in the opinion of the calculation agent, fairly represent the value of that Basket Component had those material changes or modifications not been made.

PS-24

The following table is for illustration purposes only, and does not reflect the actual composition, Initial Component Weights, or Component Ratios, which will be set forth in the term sheet.

Example: The hypothetical Basket Components are Index ABC, Index XYZ, and Index RST, with their Initial Component Weights being 50.00%, 25.00% and 25.00%, respectively, on a hypothetical pricing date:

| Basket Component |

Initial Component Weight |

Hypothetical Closing Level(1) |

Hypothetical Component Ratio(2) |

Initial Basket Value Contribution |

||||||||

| Index ABC |

50.00% | 500.00 | 0.10000000 | 50.00 | ||||||||

| Index XYZ |

25.00% | 2,420.00 | 0.01033058 | 25.00 | ||||||||

| Index RST |

25.00% | 1,014.00 | 0.02465483 | 25.00 | ||||||||

| Starting Value |

100.00 | |||||||||||

| (1) | This column sets forth the hypothetical closing level of each Basket Component on the hypothetical pricing date. |

| (2) | The hypothetical Component Ratio for each Basket Component equals its Initial Component Weight (expressed as a percentage) multiplied by 100, and then divided by the hypothetical closing level of that Basket Component on the hypothetical pricing date, with the result rounded to eight decimal places. |