Form 20-F Despegar.com, Corp. For: Dec 31

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 001-38209

Despegar.com, Corp.

(Exact Name of Registrant as Specified in its charter)

N/A

(Translation of Registrant’s name into English)

British Virgin Islands

(Jurisdiction of Incorporation or Organization)

Juana Manso 999

Ciudad Autónoma de Buenos Aires, Argentina C1107CBR

Telephone: +54 11 4894-3500

(Address of principal executive offices)

Juan Pablo Alvarado, General Counsel

Juana Manso 999

Ciudad Autónoma de Buenos Aires, Argentina C1107CBR

Telephone: +54 11 4894-3500

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Ordinary Shares, no par value | The New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

| At December 31, 2017 |

69,097,610 ordinary shares |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Note- Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Emerging growth company | ☒ | |||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☒

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Table of Contents

i

Table of Contents

ii

Table of Contents

| ITEM 16H. |

MINE SAFETY DISCLOSURE | 116 | ||||

| 116 | ||||||

| ITEM 17. |

FINANCIAL STATEMENTS | 116 | ||||

| ITEM 18. |

FINANCIAL STATEMENTS | 116 | ||||

| ITEM 19. |

EXHIBITS | 117 | ||||

iii

Table of Contents

INTRODUCTION

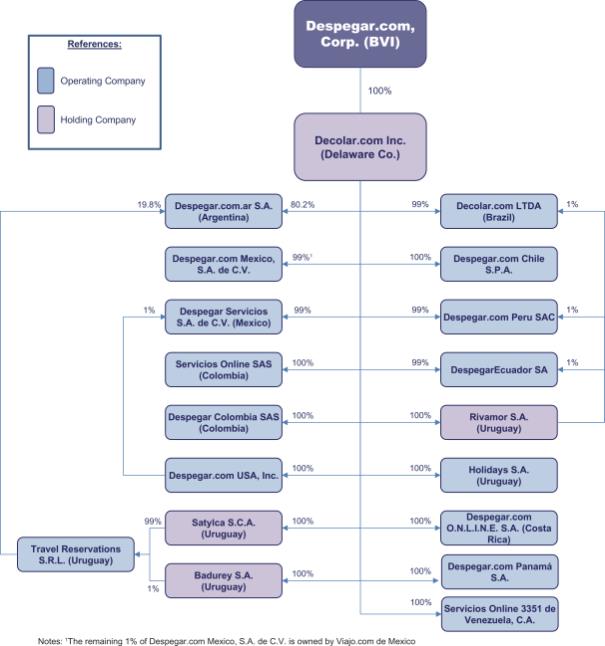

Unless the context suggests otherwise, references in this Annual Report to “Despegar,” the “Company,” “we” “us” and “our” are to Despegar.com, Corp., a business company incorporated in the British Virgin Islands (“BVI”), and its consolidated subsidiaries. Unless the context suggests otherwise, references to “Latin America” are to South America, Mexico, Central America and the Caribbean (except in the case of certain industry information from Euromonitor travel research for Latin America; as set forth below).

We were formed as a new business company in BVI on February 10, 2017. On May 3, 2017, the stockholders of our predecessor, Decolar.com, Inc., a Delaware corporation, exchanged their shares of Decolar.com, Inc. for ordinary shares of Despegar.com, Corp. to create a new BVI holding company. Following the exchange, our shareholders own shares of Despegar.com, Corp. and Decolar.com, Inc. is a wholly-owned subsidiary of Despegar.com, Corp. The audited consolidated financial statements as of December 31, 2017 and 2016, and for the three years ended December 31, 2017 to the extent related to the events and periods prior to May 3, 2017, included in this Annual Report are the consolidated financial statements of Decolar.com, Inc., which is our predecessor for accounting purposes, and other information contained in this Annual Report related to events and periods prior to May 3, 2017 is based on Decolar.com, Inc.

Financial Statements

The financial information contained in this Annual Report derives from our audited consolidated financial statements as of December 31, 2017 and 2016 and for the fiscal years ended December 31, 2017, 2016 and 2015. Our consolidated financial statements are prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) and presented in dollars.

Non-GAAP Financial Measures

This Annual Report includes certain references to Adjusted EBITDA, a non-GAAP financial measure. We define Adjusted EBITDA as net income / (loss) exclusive of financial income / (expense), income tax, depreciation, amortization and share-based compensation. See “Item 3. Key Information —A. Selected Financial Data — Other Financial and Operating Data” for a reconciliation of Adjusted EBITDA to net income / (loss). Adjusted EBITDA is not prepared in accordance with U.S. GAAP. Accordingly, you are cautioned not to place undue reliance on this information and should note that Adjusted EBITDA, as calculated by us, may differ materially from similarly titled measures reported by other companies, including our competitors.

Market Data

This Annual Report includes industry, market and competitive position data and forecasts that we have derived from independent consultant reports, publicly available information, industry publications, official government information and other third-party sources, including Euromonitor International, and GSM Association, as well as our internal data and estimates. Independent consultant reports, industry publications and other published sources generally indicate that the information contained therein was obtained from sources believed to be reliable. Although we believe that this information is reliable, the information has not been independently verified by us.

Certain data included in this Annual Report related to the Latin American travel industry and the Latin American online travel market includes the purchase of hotel and other travel products (such as airlines, car rentals, lodging and attractions) by inbound travelers traveling to Latin America, as well as corporate travel. Our customer base, however, is primarily comprised of consumers from Latin America traveling for leisure domestically within their own country of origin, to other countries in the Latin American region, and outside of Latin America. Additionally, Euromonitor travel research for Latin America only includes the following countries: Mexico, Brazil, Chile, Argentina, Colombia, Peru, Venezuela and Ecuador. Market data related solely to the travel trends of Latin American consumers is limited. As a result, certain market data included in this Annual Report is being provided to investors to give a general sense of the trends of our industry but such market data does not capture the travel trends of only our targeted customers. Accordingly, investors should not place undue reliance on the market information in this Annual Report.

1

Table of Contents

Information sourced to Euromonitor is from independent industry research carried out by Euromonitor International Limited as part of its annual Passport research. Euromonitor makes no warranties about the fitness of this intelligence for investment decisions.

Certain Operating Measures

This Annual Report includes certain references to number of transactions and gross bookings, both operating measures. Number of transactions is the total number of customer orders completed on our platform during a given period. Gross bookings is the aggregate purchase price of all travel products booked by our customers through our platform during a given period. For more information, see “Item 5. Operating and Financial Review and Prospects—A. Operating Results — Key Business Metrics.”

Currency Presentation

In this Annual Report, references to “dollars” and “$” are to the currency of the United States, references to “Brazilian real,” “Brazilian reais” and “R$” are to the currency of Brazil and references to “Argentine pesos” and “AR$” are to the currency of Argentina. See “Item 10. Additional Information — Exchange Controls” for information regarding historical exchange rates of Brazilian reais and Argentine pesos to dollars.

Rounding

Certain figures included in this Annual Report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be exact arithmetic aggregations or percentages of the figures that precede them.

Trademarks

Our key trademarks are “Despegar.com,” “Decolar.com” and “Decolar.com.br.” Other trademarks or service marks appearing in this Annual Report are the property of their respective holders. Solely for the convenience of the reader, we refer to our brands in this Annual Report without the ® symbol, but these references are not intended to indicate in any way that we will not assert our rights to these brands to the fullest extent permitted by law.

Forward-Looking Statements

This Annual Report includes forward-looking statements, principally under the captions “Item 3. Key Information,” “Item 4. Information on the Company––Business Overview” and “Item 5. Operating and Financial Review and Prospects.” We have based these forward-looking statements largely on our current beliefs, expectations and projections about future events and financial trends affecting our business and our market. Many important factors, in addition to those discussed elsewhere in this Annual Report, could cause our actual results to differ substantially from those anticipated in our forward-looking statements, including:

| • | political, social and macroeconomic conditions in Latin America; |

| • | currency exchange rates and inflation; |

| • | current competition and the emergence of new market participants in our industry; |

| • | government regulation; |

| • | our expectations regarding the continued growth of internet usage and e-commerce in Latin America; |

| • | failure to maintain and enhance our brand recognition; |

| • | our ability to maintain and expand our supplier relationships; |

| • | our reliance on technology; |

| • | the growth in the usage of mobile devices and our ability to successfully monetize this usage; |

2

Table of Contents

| • | our ability to attract, train and retain executives and other qualified employees; |

| • | our ability to successfully implement our growth strategies; and |

| • | the other factors discussed under the caption “Item 3. Key Information—D. Risk Factors” in this Annual Report. |

We operate in a competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report. The words “believe,” “may,” “should,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “will,” “expect” and similar words are intended to identify forward-looking statements. Forward-looking statements include information concerning our possible or assumed future results of operations, business strategies, capital expenditures, financing plans, competitive position, industry environment, potential growth opportunities, the effects of future regulation and the effects of competition. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update publicly or to revise any forward-looking statements after we distribute this Annual Report because of new information, future events or other factors. In light of the risks and uncertainties described above, the future events and circumstances discussed in this Annual Report might not occur or come into existence and forward-looking statements are thus not guarantees of future performance. Considering these limitations, you should not make any investment decision in reliance on forward-looking statements contained in this Annual Report.

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

| A. | Selected Financial Data |

The following selected historical consolidated financial and other operating data should be read together with “Item 5. Operating and Financial Review and Prospects” and our consolidated financial statements included elsewhere in this Annual Report.

We derived the selected income statement, balance sheet and cash flow data as of December 31, 2017 and 2016 and for the three years ended December 31, 2017 from our audited consolidated financial statements which are included elsewhere in this Annual Report. We derived the selected balance sheet data as of December 31, 2015 from our audited consolidated financial statements which are not included in this Annual Report. Our consolidated financial statements are prepared and presented in accordance with U.S. GAAP in dollars. Our historical results do not necessarily indicate results expected for any future period.

Selected Income Statement Data

| Year Ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| (in thousands, except per share data) | ||||||||||||

| Revenue |

||||||||||||

| Air |

$ | 241,015 | $ | 205,721 | $ | 219,817 | ||||||

| Packages, Hotels and Other Travel Products |

282,925 | 205,441 | 201,894 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total revenue |

523,940 | 411,162 | 421,711 | |||||||||

| Cost of revenue |

142,479 | 126,675 | 154,213 | |||||||||

|

|

|

|

|

|

|

|||||||

| Gross profit |

381,461 | 284,487 | 267,498 | |||||||||

| Operating expenses |

||||||||||||

| Selling and marketing |

166,288 | 121,466 | 170,149 | |||||||||

| General and administrative |

72,626 | 64,683 | 78,181 | |||||||||

| Technology and product development |

71,308 | 63,251 | 73,535 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total operating expenses |

310,222 | 249,400 | 321,865 | |||||||||

|

|

|

|

|

|

|

|||||||

3

Table of Contents

| Year Ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| (in thousands, except per share data) | ||||||||||||

| Operating income / (loss) |

71,239 | 35,087 | (54,367 | ) | ||||||||

| Financial income |

2,389 | 8,327 | 10,797 | |||||||||

| Financial expense |

(19,268 | ) | (15,079 | ) | (23,702 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Income / (loss) before income taxes |

54,360 | 28,335 | (67,272 | ) | ||||||||

| Income tax expense |

11,994 | 10,538 | 18,004 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net income / (loss) |

$ | 42,366 | $ | 17,797 | $ | (85,276 | ) | |||||

|

|

|

|

|

|

|

|||||||

| Earnings / (loss) per share: |

||||||||||||

| Basic |

0.69 | 0.30 | (1.49 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Diluted |

0.69 | 0.30 | (1.49 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Weighted average shares outstanding: |

||||||||||||

| Basic |

61,457 | 58,518 | 57,078 | |||||||||

| Diluted |

61,548 | 58,609 | 57,186 | |||||||||

Selected Balance Sheet Data

| As of December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| (in thousands, except share data) | ||||||||||||

| Cash and cash equivalents(1) |

$ | 371,013 | $ | 75,968 | $ | 102,116 | ||||||

| Total assets |

738,694 | 353,710 | 348,215 | |||||||||

| Total liabilities |

520,736 | 435,973 | 431,348 | |||||||||

| Total shareholders’ equity/(deficit) attributable to Despegar |

217,958 | (82,263 | ) | (83,133 | ) | |||||||

| Common stock |

253,535 | 6 | 6 | |||||||||

| Number of Shares |

69,097 | 58,518 | 58,518 | |||||||||

| (1) | Excludes restricted cash and cash equivalents. See note 4 of our audited consolidated financial statements. |

Other Financial and Operating Data

We regularly review the following key metrics to evaluate our business, measure our performance, identify trends in our business, prepare financial projections and make strategic decisions.

| Year Ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| (in thousands) | ||||||||||||

| Operational |

||||||||||||

| Number of transactions |

||||||||||||

| By country |

||||||||||||

| Brazil |

3,713 | 2,924 | 3,620 | |||||||||

| Argentina |

2,264 | 1,798 | 1,787 | |||||||||

| Other |

3,079 | 2,490 | 2,298 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

9,056 | 7,212 | 7,705 | |||||||||

| By segment |

||||||||||||

| Air |

5,285 | 4,250 | 4,385 | |||||||||

| Packages, Hotels and Other Travel Products |

3,771 | 2,963 | 3,320 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

9,056 | 7,212 | 7,705 | |||||||||

| Gross bookings |

$ | 4,454,548 | $ | 3,260,234 | $ | 3,596,260 | ||||||

| Financial |

||||||||||||

| Adjusted EBITDA (unaudited) |

$ | 89,354 | $ | 48,585 | $ | (39,067 | ) | |||||

4

Table of Contents

Number of Transactions

The number of transactions for a period is an operating measure that represents the total number of customer orders completed on our platform in such period. We monitor the total number of transactions, as well as the number of transactions in each of our segments and the number of transactions with customers in each of Brazil, Argentina and the other countries in which we operate. The number of transactions is an important metric because it is an indicator of the level of engagement with our customers and the scale of our business from period to period but, unlike gross bookings and our financial metrics, the number of transactions is independent of the average selling price of each transaction, which can be significantly influenced by fluctuations in currency exchange rates.

Gross Bookings

Gross bookings is an operating measure that represents the aggregate purchase price of all travel products booked by our customers through our platform during a given period. We generate substantially all of our revenue from commissions and other incentive payments paid by our suppliers and service fees paid by our customers for transactions through our platform, and, as a result, we monitor gross bookings as an important indicator of our ability to generate revenue.

Adjusted EBITDA

We define Adjusted EBITDA as net income / (loss) exclusive of financial income / (expense), income tax, depreciation, amortization and share-based compensation.

We believe that Adjusted EBITDA, a non-GAAP financial measure, provides useful supplemental information to investors about us and our results. Adjusted EBITDA is among the measures used by our management team to evaluate our financial and operating performance and make day-to-day financial and operating decisions. In addition, Adjusted EBITDA is frequently used by securities analysts, investors and other parties to evaluate companies in the online travel industry. We also believe that Adjusted EBITDA is helpful to investors because it provides additional information about trends in our core operating performance prior to considering the impact of capital structure, depreciation, amortization, and taxation on our results.

Adjusted EBITDA should not be considered in isolation or as a substitute for other measures of financial performance reported in accordance with U.S. GAAP. Adjusted EBITDA has limitations as an analytical tool, including:

| • | Adjusted EBITDA does not reflect changes in, including cash requirements for, our working capital needs or contractual commitments; |

| • | Adjusted EBITDA does not reflect our financial expenses, or the cash requirements to service interest or principal payments on our indebtedness, or interest income or other financial income; |

| • | Adjusted EBITDA does not reflect our income tax expense or the cash requirements to pay our income taxes; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated or amortized often will need to be replaced in the future, and Adjusted EBITDA does not reflect any cash requirements for these replacements; |

| • | although share-based compensation is a non-cash charge, Adjusted EBITDA does not consider the potentially dilutive impact of share-based compensation; and |

| • | other companies may calculate Adjusted EBITDA differently, limiting its usefulness as a comparative measure. |

5

Table of Contents

We compensate for the inherent limitations associated with using Adjusted EBITDA through disclosure of these limitations, presentation of our consolidated financial statements in accordance with U.S. GAAP and reconciliation of Adjusted EBITDA to the most directly comparable U.S. GAAP measure, net income / (loss).

The table below provides a reconciliation of our net income / (loss) to Adjusted EBITDA:

| Year Ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| (in thousands) | ||||||||||||

| Net income / (loss) |

$ | 42,366 | $ | 17,797 | $ | (85,276 | ) | |||||

| Add (deduct): |

||||||||||||

| Financial expense / (income), net |

17,879 | 6,752 | 12,905 | |||||||||

| Income tax expense |

11,994 | 10,538 | 18,004 | |||||||||

| Depreciation expense |

5,075 | 5,089 | 5,152 | |||||||||

| Amortization of intangible assets |

8,751 | 7,835 | 9,287 | |||||||||

| Share-based compensation expense |

4,289 | 574 | 861 | |||||||||

|

|

|

|

|

|

|

|||||||

| Adjusted EBITDA |

$ | 89,354 | $ | 48,585 | $ | (39,067 | ) | |||||

|

|

|

|

|

|

|

|||||||

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

You should carefully consider the risks described below, in addition to the other information contained in this Annual Report. We also may face additional risks and uncertainties that are not presently known to us, or that as of the date of this Annual Report we deem immaterial, which may impair our business, financial condition and results of operations. If any of these events occur, the trading price of our ordinary shares could decline. In general, you take more risk when you invest in the securities of issuers with operations in emerging markets such as Latin American countries than when you invest in the securities of issuers in the United States and other developed markets. The information in this Risk Factors section includes forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of numerous factors, including those described in “Forward-Looking Statements.”

Risks Related to Our Business

We are subject to the risks generally associated with doing business in Latin America.

Our business serves the Latin American travel industry and substantially all of our revenue is derived in Latin American countries. Substantially all of our operations are located in Latin America. Moreover, we have significant revenue from Brazil and Argentina as well as other Latin American countries: in 2017, Brazil accounted for 41% of our transactions and Argentina accounted for 25%. As a result, we are subject to the risks generally associated with doing business in the region, including:

| • | political, social and macroeconomic instability; |

| • | cycles of severe economic downturns; |

| • | currency devaluations and fluctuations; |

6

Table of Contents

| • | periods of high inflation; |

| • | availability, quality and level of usage of the internet and e-commerce; |

| • | high levels of credit risk, fraud and lack of secure payment methods; |

| • | uncertainty or changes in governmental regulation, including applicable to travel services operations and internet and e-commerce services; |

| • | uncertainty or changes in tax laws and regulations; |

| • | limited access to financing, both for companies and for consumers; |

| • | exchange and capital controls; |

| • | limited infrastructure, including in the travel and technology sectors; |

| • | adverse labor conditions and difficulties in hiring, training and retaining qualified personnel; |

| • | the challenges of doing business across a region with multiple languages, different currencies and regulatory regimes that varies from country to country; and |

| • | the impact of adverse global conditions in the region. |

Any of these risks could have a material adverse effect on our business, financial condition and results of operations. For more information, see “—Risks Related to Latin America.”

General declines or disruptions in the travel industry may adversely affect our business and results of operations.

Our business is significantly affected by the trends that occur in the travel industry. As the travel industry is highly sensitive to business and personal discretionary spending levels, it tends to decline during general economic downturns. Trends or events that tend to reduce travel and are likely to reduce our revenue include:

| • | terrorist attacks or threats of terrorist attacks or wars; |

| • | fluctuations in currency exchange rates; |

| • | health-related risks, such as an outbreak of the Zika virus, H1N1 influenza, Ebola virus, yellow fever, avian flu or any other serious contagious diseases; |

| • | increased prices in the airline ticketing, hotel, or other travel-related sectors; |

| • | significant changes in oil prices; |

| • | travel-related strikes or labor unrest, bankruptcies or liquidations; |

| • | travel-related accidents or the grounding of aircraft due to safety concerns; |

| • | political unrest; |

| • | high levels of crime; |

| • | natural disasters or severe weather conditions, including volcanic eruptions, hurricanes, flooding or earthquakes; |

| • | changes in immigration policy; and |

7

Table of Contents

| • | travel restrictions or other security procedures implemented in connection with any major events, particularly those that affect travel by Latin Americans within their respective countries, across the region and outbound from the region to the rest of the world. |

We could be severely and adversely affected by declines or disruptions in the travel industry and, in many cases, have little or no control over the occurrence of such events. Such events could result in a decrease in demand for our travel services. Any decrease in demand, depending on the scope and duration, could significantly and adversely affect our business and financial performance over the short and long term.

Our business and results of operations may be adversely affected by macroeconomic conditions.

Consumer purchases of discretionary items generally decline during periods of recession and other periods in which disposable income is adversely affected. As a substantial portion of travel expenditure, for both business and leisure, is discretionary, the travel industry tends to experience weak or reduced demand during economic downturns.

General adverse economic conditions, including the possibility of recessionary conditions in Latin America or a worldwide economic slowdown, would adversely impact our business, financial condition and results of operations. Past weakness and uncertainty in the global economy and in Latin America have negatively impacted consumer spending patterns and demand for travel services and may continue to do so in the future. For example, consumer spending patterns and demand for travel services were negatively impacted by the 2008-2009 global financial crisis that arose in the United States, as well as the recession in Brazil of 2015-2016 and the Argentine financial crisis of 2001-2002 and recession of 2016.

As an intermediary in the travel industry, a significant portion of our revenue is affected by prices charged by our travel suppliers. During periods of poor economic conditions, airlines and hotels tend to reduce rates or offer discounted sales to stimulate demand, thereby reducing our commission-based income. A slowdown in economic conditions may also result in a decrease in transaction volumes and adversely affect our revenue, including our consumer fee-based income. It is difficult to predict the effects of the uncertainty in global economic conditions. If economic conditions decline globally or in Latin America, our business, financial condition and results of operations could be adversely impacted.

We are exposed to fluctuations in currency exchange rates.

Because we conduct our business outside the United States and receive almost all of our revenue in currencies other than the dollar, but report our results in dollars, we face exposure to adverse movements in currency exchange rates. The currencies of certain countries where we operate, including Brazil and Argentina, have historically experienced significant devaluations. For example, in December 2015, the Argentine government let the Argentine peso float freely, after several years of controlling foreign exchange rates, resulting in a significant devaluation. The results of operations in the countries where we operate are exposed to foreign exchange rate fluctuations as the financial results of the applicable subsidiaries are translated from the local currency into dollars upon consolidation. If the dollar weakens against foreign currencies, the translation of these foreign-currency-denominated transactions will typically result in increased revenue and operating expenses, and our revenue and operating expenses will typically decrease if the dollar strengthens. Moreover, if the dollar strengthens against the foreign currencies of countries in which we operate, the purchasing power of our customers from those countries could be negatively affected by potentially increased prices in local currencies, and we could experience a reduction in the demand for our travel services.

Additionally, foreign exchange exposure also arises from pre-pay transactions, where we accept upfront payments for bookings in the customer’s home currency, but payment to the hotel is not due until after the customer checks out, and is paid by us in the hotel’s home currency. We are therefore exposed to foreign exchange risk between the time of the initial reservation and the time when the hotel is paid.

We minimize our foreign currency exposures by managing natural hedges, netting our current assets and current liabilities in similarly denominated foreign currencies, and managing short term loans and investments for hedging purposes. Additionally, from time to time we enter into derivative transactions. However, depending on the size of the exposures and the relative movements of exchange rates, if we choose not to hedge or fail to hedge effectively our exposure, we could experience a material adverse effect on our consolidated financial statements and financial condition.

8

Table of Contents

We have incurred operating losses in the past and may experience earnings declines or net losses in the future.

We have incurred operating losses in the past, though in the years ended December 31, 2017 and 2016 we had positive net income. We cannot assure you that we can sustain profitability or avoid net losses in the future. Our ability to remain profitable depends on various factors, including our ability to generate additional transaction volume and revenue and control our costs and expenses. We may incur significant losses in the future for a number of reasons, including the other risks described in this Annual Report, and we may further encounter unforeseen expenses, difficulties, complications, delays and other unknown events. If our costs and expenses increase at a more rapid rate than our revenue, we may not be able to sustain profitability and may incur losses.

If we are unable to maintain or increase consumer traffic to our sites and our conversion rates, our business and results of operations would be harmed.

Our ability to generate revenue depends, in part, on our ability to attract consumers to our platform. If we fail to maintain or increase consumer traffic and our conversion rates, our ability to grow our revenue could be negatively affected. We expect that our efforts to maintain or increase traffic are likely to include, among other things, significant increases to our marketing expenditures. We cannot assure you that any increases in our expenses will be successful in generating additional consumer traffic.

There are many factors that could negatively affect user retention, growth, and engagement, including if:

| • | we fail to offer compelling products; |

| • | users increasingly engage with competing products instead of ours; |

| • | we fail to introduce new and exciting products and services or those we introduce are poorly received; |

| • | our websites or mobile apps fail to operate effectively on the iOS and Android mobile operating systems; |

| • | we do not provide a compelling user experience; |

| • | we are unable to combat spam or other hostile or inappropriate usage on our products, or if our anti-fraud measures are too conservative and we reject too many bona fide transactions; |

| • | there are changes in user sentiment about the quality or usefulness of our existing products; |

| • | there are concerns about the privacy implications, safety, or security of our products; |

| • | our suppliers decide to discontinue the offering of their products through our platform; |

| • | technical or other problems frustrate the user experience, particularly if those problems prevent us from delivering our products in a fast and reliable manner; |

| • | we fail to provide adequate service to our customers and suppliers; |

| • | we or other companies in our industry are the subject of adverse media reports or other negative publicity; or |

| • | we do not maintain our brand image or our reputation is damaged. |

Any decrease to user retention, growth, or engagement could render our products less attractive to consumers and would seriously harm our business.

9

Table of Contents

We operate in a highly competitive and evolving market, and pressure from existing and new companies may adversely affect our business and results of operations.

The travel market in Latin America and worldwide is intensely competitive and rapidly evolving. Factors affecting our competitive success include, among other things, price, availability and breadth of choice of travel services and products, brand recognition, customer service, fees charged to travelers, ease of use, accessibility, consumer payment options and reliability. We currently compete with both established and emerging providers of travel services and products, including regional offline travel agency chains and tour operators, global OTAs with presence in Latin America and smaller, country-specific online and offline travel agencies and tour operators. In addition, our customers have the option to book travel directly with airlines, hotels and other travel service providers who are increasingly focused on further refining their online offerings. Large, established internet search engines have also launched applications offering travel itineraries in destinations around the world, and meta-search companies who can aggregate travel search results also compete against us for customers. In addition, we face price competition from new entrants that offer discounted rates and other incentives from time to time, as well as social media channels that market travel products and experiences. Some of our competitors have significantly greater financial and other resources than us. From time to time we may be required to reduce service fees and revenue margins in order to compete effectively and maintain or gain customers, brand awareness and supplier relationships.

Further, we may also face increased competition from new entrants in our industry. We cannot assure you that we will be able to successfully compete against existing or new competitors. If we are not able to compete effectively, our business, financial condition and results of operations may be adversely affected.

Some travel suppliers are seeking to decrease their reliance on distribution intermediaries like us by promoting direct distribution channels. Many airlines, hotels, car rental companies and tour operators have call centers and have established their own travel distribution websites and mobile applications. From time to time, travel suppliers offer advantages, such as bonus loyalty awards and lower transaction fees or discounted prices, when their services and products are purchased from supplier-related channels. We also compete with competitors which may offer less content, functionality and marketing reach but at a relatively lower cost to suppliers. If our access to supplier-provided content or features were to be diminished either relative to our competitors or in absolute terms or if we are unable to compete effectively with travel supplier-related channels or other competitors, our business could be materially and adversely affected.

If we are unable to maintain existing, and establish new, arrangements with travel suppliers, our business may be adversely affected.

Our business is dependent on our ability to maintain our relationships and arrangements with existing suppliers, such as airlines, global distribution system (GDS), service providers, hotels, hotel consolidators and destination services companies, car rental companies, bus operators, cruise companies and travel assistance providers, as well as our ability to establish and maintain relationships with new travel suppliers. In addition, the hotel and other lodging products that we offer through our platform for all countries outside Latin America are provided to us exclusively by affiliates of Expedia and Expedia is the preferred provider to us of hotel and other lodging products in Latin America pursuant to a lodging outsourcing agreement (the “Expedia Outsourcing Agreement”). In the event the Expedia Outsourcing Agreement is terminated, we may be required to pay a $125.0 million termination fee. For more information on our relationships with Expedia, see “Item 7. Major Shareholders and Related Party Transactions — B. Related Party — Relationship with Expedia.” Adverse changes in key arrangements with our suppliers, including an inability of any key travel supplier to fulfill its payment obligation to us in a timely manner, increasing industry consolidation or our inability to enter into or renew arrangements with these parties on favorable terms, if at all, could reduce the amount, quality, pricing and breadth of the travel services and products that we are able to offer, which could adversely affect our business, financial condition and results of operations. For example, American Airlines discontinued our access to its inventory from July 2013 to March 2016, until a mutually satisfactory settlement was reached and American Airlines resumed supplying us with airline tickets.

In addition, adverse economic developments affecting the travel industry could also adversely impact our ability to maintain our existing relationships and arrangements with one or more of our suppliers. We cannot assure you that our agreements or arrangements with our travel suppliers or travel-related service providers will continue or that our travel suppliers or travel-related service providers will not further reduce commissions, terminate our contracts, make their products or services unavailable to us as part of exclusive arrangements with our competitors or default on or dispute their payment or other obligations towards us, any of which could

10

Table of Contents

reduce our revenue and margins or may require us to initiate legal or arbitral proceedings to enforce their contractual payment obligations, which may adversely affect our business, financial condition and results of operations.

We rely on the value of our brands, and any failure to maintain or enhance consumer awareness of our brands could adversely affect our business and results of operations.

We believe continued investment in our brand is critical to retain and expand our business. We believe that our brands are well recognized in the Latin American travel market. We have invested in developing and promoting our brand since our inception and expect to continue to spend on maintaining the value of our brands to enable us to compete against increased spending by competitors and to allow us to expand into new services or increase our penetration in certain markets where our brands are less well known.

We cannot assure you that we will be able to successfully maintain or enhance consumer awareness of our brands. Even if we are successful in our branding efforts, such efforts may not be cost-effective. Our marketing costs may also increase as a result of inflation in media pricing. If we are unable to maintain or enhance consumer awareness of our brands and generate demand in a cost-effective manner, it would negatively impact our ability to compete in the travel industry and would have a material adverse effect on our business, financial condition and results of operations.

We rely on information technology to operate our business and maintain our competitiveness, and any failure to adapt to technological developments or industry trends could adversely affect our business.

We depend on the use of sophisticated information technology and systems, for search and reservation for airline tickets, hotels, and any of the other products that we offer on our platform, as well as payments, refunds, customer relationship management, communications and administration. As our operations grow in both size and scope, we must continuously improve and upgrade our systems and infrastructure to improve services, features and functionality, while maintaining the reliability and integrity of our systems and infrastructure in a cost-effective manner. Our future success also depends on our ability to upgrade our services and infrastructure ahead of rapidly evolving consumer demands while continuing to improve the performance, features and reliability of our service in response to competitive offerings.

We may not be able to maintain or replace our existing systems or introduce new technologies and systems as quickly as our competitors, in a cost-effective manner or at all. We may also be unable to devote adequate financial resources to develop or acquire new technologies and systems in the future.

We may not be able to use new technologies effectively, or we may fail to adapt our websites, mobile apps, transaction processing systems and network infrastructure to meet consumer requirements or emerging industry standards, comply with government regulation or prevent fraud or security breaches. If we face material delays in introducing new or enhanced solutions, our customers may forego the use of our services in favor of those of our competitors. Any of these events could have a material adverse effect on our business, financial condition and results of operations.

Some of our airline suppliers (including our GDS service providers) may reduce or eliminate the commission and other compensation they pay to us for the sale of airline tickets and this could adversely affect our business and results of operations.

In our air business, we generate revenue through commissions and incentive payments from airline suppliers (including our GDS service providers) and service fees charged to our customers. Our airline suppliers (including our GDS service providers) may reduce or eliminate the commissions, incentive payments or other compensation they pay to us. To the extent any of our airline suppliers (including our GDS service providers) reduce or eliminate the commissions, incentive payments or other compensation they pay to us, our revenue may be reduced unless we are able to adequately mitigate such reduction by increasing the service fee we charge to our customers or increasing our transaction volume in a sustainable manner. However, any increase in service fees may also result in a loss of potential customers. In addition, our arrangement with the airlines that supply airline tickets to us may limit the amount of service fee that we are able to charge our customers. Our business would also be negatively impacted if competition or regulation in the Latin American travel industry causes us to have to reduce or eliminate our service fees.

11

Table of Contents

Our business and results of operations could be adversely affected if one or more of our major travel suppliers suffers a deterioration in its financial condition or restructures its operations.

As we are an intermediary in the travel industry, a substantial portion of our revenue is affected by the prices charged by our suppliers, including airlines, GDS service providers, hotels, destination service providers, car rental suppliers, tour operators, supply aggregators (such as other OTAs), cruise operators, bus service providers and travel assistance providers, and the volume of products offered by our suppliers. As a result, if one or more of our major suppliers suffers a deterioration in its financial condition or restructures its operations, it could adversely affect our business, financial condition and results of operations. Accordingly, our business may be negatively affected by adverse changes in the markets in which our suppliers operate.

In particular, as a substantial portion of our revenue depends on our sales of airline flights, we could be adversely affected by changes in the airline industry, including consolidation or bankruptcies and liquidations, and in many cases, we will have no control over such changes. Any consolidation in the airline industry in the future would result in fewer airlines with potentially more bargaining power with respect to the commissions and incentive payments or other fees they pay to intermediaries. Events or weaknesses specific to the airline industry that could negatively affect our business include air fare fluctuations, airport, airspace and landing fee increases, seat capacity constraints, removal of destinations or flight routes, travel-related strikes or labor unrest, imposition of taxes or surcharges by regulatory authorities and fuel price volatility. While decreases in prices for flights and other travel products generally increase demand, such price decreases generally also have a negative effect on the commissions we earn, particularly in our non-flight business, which is more dependent on commissions than our flight business. The overall effect of a price increase or decrease is therefore uncertain.

In the past several years, several major airlines have filed for bankruptcy, recently exited bankruptcy, or discussed publicly the risk of bankruptcy. In addition, some of these airlines have merged, or discussed merging, with other airlines. If one of our major airline suppliers merges or consolidates with, or is acquired by, another company that either does not participate in the GDS systems we use, or that participates in such systems but at substantially lower levels, the surviving company may elect not to make supply available to us or may elect to do so at lower levels than the previous supplier. Similarly, in the event that one of our major airline suppliers voluntarily or involuntarily declares bankruptcy and is subsequently unable to successfully emerge from bankruptcy, and we are unable to replace such supplier, our business would be adversely affected. Further consolidation of one or more of the major airlines could result in further capacity reductions, a reduction in the number of airline tickets available for booking on our website and increased air fares, which may have a negative impact on demand for travel products.

We are subject to payments-related fraud risks.

We are held liable for accepting fraudulent bookings on our platform and other bookings for which payment is successfully disputed by the cardholder, both of which lead to the reversal of payments received by us for such bookings (referred to as a “chargeback”). Our results of operations may be negatively affected by our acceptance of fraudulent bookings made using credit cards, as occurred in 2015, when there was an increase in fraud in the Latin American travel industry, particularly in Brazil. In the fourth quarter of 2015, we experienced an increase in attempted fraudulent transactions in Brazil, resulting in both the first quarter of 2016 and the fourth quarter of 2015 in an increase in fraud expense in the form of chargebacks. We also experienced a decrease in gross bookings in both quarters, as we imposed more restrictive anti-fraud protocol in response to the uptick in fraudulent transactions that resulted in more rejections of legitimate transactions. Our ability to detect and combat fraud, which has become increasingly common and sophisticated, may be negatively impacted by the adoption of new payment methods, the emergence and innovation of new technology platforms, including smartphones, tablets and other mobile devices, and our expansion, including into geographies with a history of elevated fraudulent activity. If we are unable to effectively combat fraud on our platform or if we otherwise experience increased levels of chargebacks, our results of operations could be materially adversely affected.

We have agreements with companies that process customer credit and debit card transactions for the facilitation of customer bookings of travel services from our travel suppliers. These agreements allow these processing companies, under certain conditions, to hold an amount of our cash (referred to as a “holdback”) or require us to otherwise post security equal to a portion of bookings that have been processed by such companies. These processing companies may be entitled to a holdback or suspension of processing services upon the occurrence of specified events, including material adverse changes in our financial condition. Moreover, there can be no assurances that the rates we pay for the processing of customer credit and debit card transactions will not increase, which could reduce our revenue thereby adversely affecting our business and financial performance.

12

Table of Contents

Moreover, credit card networks, such as Visa and MasterCard, have adopted rules and regulations that apply to all merchants which process and accept credit cards and include the Payment Card Industry Data Security Standards (“PCI DSS”). Under these rules, we are required to adopt and implement internal controls over the use, storage and security of card data. We are currently PCI DSS certified and in compliance with PCI DSS. We assess our compliance with PCI DSS rules on a periodic basis and make necessary improvements to our internal controls as needed. Failure to comply may prevent us from processing or accepting credit cards.

In addition, when onboarding suppliers to our platform, we may fail to identify falsified or stolen supplier credentials, which may result in fraudulent bookings or unauthorized access to personal or confidential information of users of our websites and mobile applications. A fraudulent supplier scheme could also result in negative publicity and damage to our reputation, and could cause users of our websites and mobile applications to lose confidence in the quality of our services. Any of these events would have a negative effect on the value of our brands, which could have an adverse impact on our financial performance.

Any system interruption, security breaches or lack of sufficient redundancy in our information systems may harm our businesses.

We rely on information technology systems, including the internet and third-party hosted services, to support a variety of business processes including booking transactions, and activities and to store sensitive data, including our proprietary business information and that of our suppliers, personally identifiable information and other information of our customers and employees and data with respect to invoicing and the collection of payments, accounting and procurement activities. In addition, we rely on our information technology systems to process financial information and results of operations for internal reporting purposes and to comply with financial reporting, legal, and tax requirements. The risk of a cybersecurity-related attack, intrusion, or disruption, including by criminal organizations, hacktivists, foreign governments, and terrorists, is persistent. We have experienced and may in the future experience system interruptions that make some or all of these systems unavailable or prevent us from efficiently fulfilling orders or providing services to third parties. Interruptions of this nature could include security intrusions and attacks on our systems for fraud or service interruption. Significant interruptions, outages or delays in our internal systems, or systems of third parties that we rely upon—including multiple co-location providers for data centers, cloud computing providers for application hosting, and network access providers—and network access, or deterioration in the performance of such systems, would impair our ability to process transactions, decrease our quality of service that we can offer to our customers, damage our reputation and brands, increase our costs and/or cause losses.

Potential security breaches to our systems or the systems of our service providers, whether resulting from internal or external sources, could significantly harm our business. We devote significant resources to network security, monitoring and testing, employee training, and other security measures, but we cannot assure you that these measures will prevent all possible security breaches or attacks. A party, whether internal or external, that is able to circumvent our security systems could misappropriate customer or employee information, proprietary information or other business and financial data or cause significant interruptions in our operations. We may need to expend significant resources to protect against security breaches or to address problems caused by breaches, and reductions in website availability could cause a loss of substantial business volume during the occurrence of any such incident. Because the techniques used to sabotage security change frequently, often are not recognized until launched against a target and may originate from less regulated and remote areas around the world, we may be unable to proactively address these techniques or to implement adequate preventive measures. We have obtained cyberinsurance, however we cannot assure you that our insurance will be sufficient to protect against our losses or will cover all potential incidents. Moreover, security breaches could result in negative publicity and damage to our reputation, exposure to risk of loss or litigation and possible liability due to regulatory penalties and sanctions or pursuant to our contractual arrangements with payment card processors for associated expenses and penalties. Security breaches could also cause customers and potential users and our suppliers to lose confidence in our security, which would have a negative effect on the value of our brands. Failure to adequately protect against attacks or intrusions, whether for our own systems or those of our suppliers, could expose us to security breaches that could have an adverse impact on our financial performance. For example, in 2014, hackers breached our system security and accessed credit card information from customers who had made purchases through our platform, representing approximately 663,000 unique credit card numbers.

13

Table of Contents

In addition, we cannot assure you that our backup systems or contingency plans will sustain critical aspects of our operations or business processes in all circumstances, many other systems are not fully redundant and our disaster recovery or business continuity planning may not be sufficient. Fire, flood, power loss, telecommunications failure, break-ins, earthquakes, acts of war or terrorism, acts of God, computer viruses, electronic intrusion attempts from both external and internal sources and similar events or disruptions may damage or impact or interrupt computer or communications systems or business processes at any time. Although we have put measures in place to protect certain portions of our facilities and assets, any of these events could cause system interruption, delays and loss of critical data, and could prevent us from providing services to our customers and/or third parties for a significant period of time. Remediation may be costly and we may not have adequate insurance to cover such costs. Moreover, the costs of enhancing infrastructure to attain improved stability and redundancy may be time consuming and expensive and may require resources and expertise that are difficult to obtain.

Our ability to attract, train and retain executives and other qualified employees, particularly highly-skilled IT professionals, is critical to our business and future growth.

Our business and future success is substantially dependent on the continued services and performance of our key executives, senior management and skilled personnel, particularly personnel with experience in our industry and our information technology and systems. Any of these individuals may choose to terminate their employment with us at any time and we cannot assure you that we will be able to retain these employees or find adequate replacements, if at all. The specialized skills we require can be difficult, time-consuming and expensive to acquire and/or develop and, as a result, these skills are often in short supply. A lengthy period of time may be required to hire and train replacement personnel when skilled personnel depart our company. Our ability to compete effectively depends on our ability to attract new employees and to retain and motivate our existing employees. We may be required to increase our levels of employee compensation more rapidly than in the past to remain competitive in attracting the quality of employees that our business requires. Competition for these personnel is intense, and we cannot assure you that we will be able to successfully attract, integrate, train, retain, motivate and manage sufficiently qualified personnel. If we do not succeed in attracting well-qualified employees or retaining or motivating existing employees, our business and prospects for growth could be adversely affected.

In addition, we compete for talented individuals not only with other companies in our industry but also with companies in other industries, such as software services, engineering services and financial services companies, among others, and there is a limited pool of individuals who have the skills and training needed to help us grow our company. High attrition rates of qualified personnel could have an adverse effect on our ability to expand our business, as well as cause us to incur greater personnel expenses and training costs.

Moreover, while we sometimes require our senior management to sign non-compete agreements, typically for a period of one year following termination, we cannot assure you that our former employees will not compete with us in the future. In addition, these non-compete agreements may be difficult to enforce in certain Latin-American jurisdictions.

We rely on third-party systems and service providers and any disruption or adverse change in their businesses could have a material adverse effect on our business.

We currently rely on a variety of third-party systems, service providers and software companies, including the GDS and other electronic central reservation systems used by airlines, various channel managing systems and reservation systems used by other suppliers, as well as other technologies used by payment gateway providers. In particular, we rely on third parties for:

| • | the hosting of our websites; |

| • | certain software underlying our technology platform; |

| • | transportation ticketing agencies to issue transportation tickets and travel assistance products, confirmations and deliveries; |

| • | third-party local tour operators to deliver on-site services to our packaged-tour customers; |

14

Table of Contents

| • | assistance in conducting searches for airfares and process air ticket bookings; |

| • | processing hotel reservations for hotels not connected to our management system; |

| • | processing credit card, debit card and net banking payments; |

| • | providing computer infrastructure critical to our business; and |

| • | providing customer relationship management (CRM) services. |

Any interruption or deterioration in performance of these third-party systems and services could have a material adverse effect on our business. Further, the information provided to us by certain of these third-party systems may not always be accurate due to either technical glitches or human error, and we may incur monetary and/or reputational loss as a result.

Our success is also dependent on our ability to maintain our relationships with these third-party systems and service providers. In the event our arrangements with any of these third parties are impaired or terminated, we may not be able to find an adequate alternative source of systems support on a timely basis or on commercially reasonable terms, which could result in significant additional costs or disruptions to our business. Any security breach at one of these companies could also affect our customers and harm our business.

We rely on banks or payment processors to collect payments from customers and facilitate payments to suppliers, and changes to credit card association fees, rules or practices may adversely affect our business.

We rely on banks or payment processors to process collections and payments, and we pay a fee for this service. In the countries where we operate, the number of processors is limited so there is little or no competition among processors. From time to time, credit card associations may increase the interchange fees that they charge for each transaction using one of their cards.

For certain payment methods, including credit cards, we pay transaction and other fees, which may increase over time and raise our operating costs, lowering profitability. We rely on third parties to provide payment processing services and it could disrupt our business if these companies become unwilling or unable to provide these services to us. If we fail to comply with these third-party servicers’ rules or requirements, or if our data security systems are breached or compromised (similar to the increase in fraud attempts we experienced in the fourth quarter of 2015 in Brazil), we may be liable for chargebacks, credit card issuing banks’ costs, fines and higher transaction fees and we may lose our ability to accept credit card payments from our customers, process electronic funds transfers, or facilitate other types of online payments. If any of these situations were to occur, our business and results of operations could be adversely affected.

Our business depends on the availability of credit cards and financing options for consumers.

Our business is highly dependent on the availability of credit cards and financing options for consumers. In 2017, 2016 and 2015, substantially all our net sales were derived from payments effected through credit cards. Moreover, approximately 55% of transactions in the year ended December 31, 2017 were paid by installment, using credit cards. As a result, the continued growth of our business is also partially dependent on the expansion of credit card penetration in Latin America, which may never reach a percentage similar to more developed countries for reasons that are beyond our control, such as low credit availability for a significant portion of the population in such countries. The provision of credit cards and other consumer financing depends on the product offerings at local and regional banks operating in the countries we serve. In the past, banking systems in Latin America have suffered disruptions and significantly limited availability and increased cost of consumer credit. Banks may also change their product offerings that they provide to consumers, or may change the availability or costs of such products, due to credit, regulations or other reasons beyond our control. For example, Argentina recently enacted regulations requiring vendors to disclose to customers the full price of items purchased by installment plan, including implicit financing costs. Furthermore, in Argentina, the rules that govern the credit card business provide for variable caps on the interest rates that financial entities may charge clients and the fees that they may charge merchants. Moreover, general legal provisions exist pursuant to which courts could decrease the interest rates and fees agreed upon by the parties on the grounds that they are excessively high.

15

Table of Contents

We rely on various banks to provide financing to our customers who elect to use an installment plan payment option. Some of our competitors also offer installment plans and may offer installment plans with more attractive terms. If we are not able to offer a competitive selection of installment plan financing at competitive rates, our business and results of operations could be adversely affected. Moreover, our agreements with local banks allow us to offer installment payment plans without assuming collection risk from the customer and receive payment in full (provided we choose not to factor such installment payments). We cannot assure you that local banks will not change their credit practices in the future. If our arrangements with local banks are impaired or terminated, our business and results of operations could be adversely affected.

Furthermore, as secure methods of payment for e-commerce transactions have not been widely adopted in certain emerging markets, consumers and other merchants may have relatively low confidence in the integrity of e-commerce transactions and remote payment mechanisms, which may have a material and adverse effect on our business prospects or limit our growth.

Our business could be negatively affected by changes in search engine algorithms and dynamics or other traffic-generating arrangements.

We increasingly utilize internet search engines such as Google, principally through the purchase of travel-related keywords, to generate a significant portion of the traffic to our websites. Search engines frequently update and change the algorithms that determine the placement and display of results of a user’s search. It is possible that any such update could negatively affect us or may negatively affect us relative to our competitors. We have developed search engine management tools to bid more efficiently on portfolios of travel-related keywords and we have a search engine management team dedicated to reviewing the return of investment of all biddings.

In addition, a significant amount of traffic is directed to our websites through participation in pay-per-click and display advertising campaigns on search engines, including Google, and travel metasearch engines, including TripAdvisor and Trivago. A search or metasearch engine could, for competitive or other purposes, adopt emerging technologies, such as voice, or alter its search algorithms or results, any of which could cause us to place lower in search query results, or exclude our website from the search query results. If a major search engine changes its algorithms or results in a manner that negatively affects the search engine ranking, paid or unpaid, of our websites, or if competitive dynamics impact the costs or effectiveness of search engine optimization, search engine marketing or other traffic-generating arrangements in a negative manner, this may have a material and adverse effect on our business and financial performance. In addition, certain metasearch engines have added or may add various forms of direct or assisted booking functionality to their sites. To the extent such functionality is promoted at the expense of traditional paid listings, this may reduce the amount of traffic to our websites or those of our affiliates.

Changes in internet browser functionality could result in a decrease in our overall revenue.

Some of our services and marketing activities rely on cookies, which are placed on individual browsers when users visit websites. We use these cookies to optimize our marketing campaigns, to better understand our users’ preferences and to detect and prevent fraudulent activity. Users can block or delete cookies through their browsers or “adblocking” software or apps. The most common internet browsers allow users to modify their browser settings to prevent cookies from being accepted by their browsers, or are set to block third-party cookies by default. Increased use of methods, software or apps that block cookies, or diminished interest of users resulting from our use of such marketing activities, may adversely affect our business, financial condition and results of operations.

Our business depends on the continued growth of e-commerce and the availability and reliability of the internet in Latin America.

The market for e-commerce is developing in Latin America. Our future revenue depends substantially on Latin American consumers’ widespread acceptance and use of the internet as a way to conduct commerce. The use of and interest in the internet (particularly as a way to conduct commerce) has grown rapidly since our inception and we cannot assure you that this acceptance, interest and use will continue. For us to grow our user base successfully, more consumers must accept and use new ways of conducting business and exchanging information.

16

Table of Contents

The price of personal computers and/or mobile devices and internet access may limit our potential growth in countries with low levels of internet penetration and/or high levels of poverty. In addition, the infrastructure for the internet may not be able to support continued growth in the number of internet users, their frequency of use or their bandwidth requirements.

The internet could lose its viability due to delays in telecommunications technological developments, or due to increased government regulation. If telecommunications services change or are not sufficiently available to support the internet, response times would be slower, which would adversely affect use of the internet and our service in particular. Moreover, lack of investment in mobile infrastructure in Latin America may limit the expansion of our mobile business, which is one of our key growth strategies.

Growth of e-commerce transactions in Latin America may be impeded by the lack of secure payment methods.

As secure methods of payment for e-commerce transactions have not been widely adopted in Latin America, both consumers and merchants may have a relatively low confidence level in the integrity of e-commerce transactions. Consumer confidence can be adversely affected by incidents of fraud and security breaches, including generally in the marketplace, which is beyond our control. Moreover, although we are PCI DSS certified, most of our suppliers with which we share information are not. The continued growth of e-commerce in the region will depend on consumers’ confidence in the safety of online payment methods.

Our future success depends on our ability to expand and adapt our operations in a cost-effective and timely manner.

We plan to continue to expand our operations by developing and promoting new and complementary services and increasing our penetration in our markets. Moreover, we expect our customer base to expand as income levels and access to internet and banking services, such as credit card issuances, increase in Latin America. We may not succeed at expanding our operations in a cost-effective or timely manner, and our expansion efforts may not have the same or greater overall market acceptance as our current services. Furthermore, any new service that we launch that is not favorably received by consumers could damage our reputation and diminish the value of our brands. To expand our operations we will also need to spend significant amounts on development, operations and other resources, and this may place a strain on our management, financial and operational resources. Similarly, a lack of market acceptance of these services or our inability to generate satisfactory revenue from any expanded services to offset their cost could have a material adverse effect on our business, financial condition and results of operations.

We may not be successful in implementing our growth strategies.

Our growth strategies involve expanding our service and product offerings, enhancing our service platforms and potentially pursuing acquisitions or other strategic opportunities.

Our success in implementing our growth strategies could be affected by:

| • | our ability to attract customers in a cost-effective manner, including in markets where we have lower brand awareness or operational history; |

| • | our ability to improve the competitiveness of our product offerings including by expanding the number of suppliers and negotiating fares and rates with existing and potential suppliers; |

| • | our ability to market and cross-sell our travel services and products to facilitate the expansion of our business; |

| • | our ability to compete effectively with existing and new entrants to the Latin American travel industry; |

| • | our ability to expand and promote our mobile platform and make it user-friendly; |

| • | our ability to build required technology; |

17

Table of Contents

| • | our ability to expand our businesses through strategic acquisitions and successfully integrate such acquisitions; |

| • | the general condition of the global economy (particularly in Latin America) and continued growth in demand for travel services, particularly online; |

| • | the growth of the internet and mobile technology as a medium for commerce in Latin America; and |

| • | changes in the regulatory environments where we operate. |

Many of these factors are beyond our control and we cannot assure you that we will succeed in implementing our strategies. Even if we are successful in executing our growth strategies, our different businesses may not grow at the same rate or with a uniform effect on our revenue and profitability.

Acquisitions could present risks and disrupt our ongoing business.