Form 10-K STAGE STORES INC For: Feb 03

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________

FORM 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 3, 2018

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to ______

Commission File No. 1-14035

Stage Stores, Inc.

(Exact Name of Registrant as Specified in Its Charter)

NEVADA (State or Other Jurisdiction of Incorporation or Organization) | 91-1826900 (I.R.S. Employer Identification No.) |

2425 WEST LOOP SOUTH, HOUSTON, TEXAS (Address of Principal Executive Offices) | 77027 (Zip Code) |

Registrant’s telephone number, including area code: (800) 579-2302

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Common Stock ($0.01 par value) | Name of each exchange on which registered New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 232.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | o | Accelerated filer | þ | |

Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company | o |

Emerging growth company | o | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

As of July 28, 2017 (the last business day of the registrant’s most recently completed second quarter), the aggregate market value of the voting and non-voting common stock of the registrant held by non-affiliates of the registrant was $52,166,748 (based upon the closing price of the registrant’s common stock as reported by the New York Stock Exchange on July 28, 2017).

As of March 23, 2018, there were 27,633,604 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement relating to the registrant’s Annual Meeting of Shareholders to be held on June 7, 2018, which will be filed within 120 days of the end of the registrant’s fiscal year ended February 3, 2018 (“Proxy Statement”), are incorporated by reference into Part III of this Form 10-K to the extent described therein.

2

TABLE OF CONTENTS | ||

Page | ||

3

References to a particular year are to Stage Stores, Inc.’s fiscal year, which is the 52- or 53-week period ending on the Saturday closest to January 31st of the following calendar year. For example, a reference to “2015” is a reference to the fiscal year ended January 30, 2016, “2016” is a reference to the fiscal year ended January 28, 2017 and “2017” is a reference to the fiscal year ended February 3, 2018. 2015 and 2016 each consisted of 52 weeks, while 2017 consisted of 53 weeks. Similarly, references to a particular quarter are to Stage Stores, Inc.’s fiscal quarters.

PART I

ITEM 1. BUSINESS

Our Business

Stage Stores, Inc. and its subsidiary (“we,” “us” or “our”) is a retailer, which operates specialty department stores and off-price stores. We offer our customers, referred to as “guests,” trend-right, moderately priced, name-brand apparel, accessories, cosmetics, footwear and home goods. As of February 3, 2018, we operated in 42 states through 777 department stores under the BEALLS, GOODY’S, PALAIS ROYAL, PEEBLES and STAGE nameplates and 58 GORDMANS off-price stores. We also operate an e-commerce website for our department store business. Our department stores are predominantly located in small towns and rural communities. Our off-price stores are predominantly located in mid-sized, non-rural Midwest markets.

Our History

Stage Stores, Inc. was formed in 1988 when the management of Palais Royal, together with several venture capital firms, acquired the family-owned Bealls and Palais Royal chains, both of which were originally founded in the 1920s. At the time of the acquisition, Palais Royal operated primarily larger stores, located in and around the Houston metropolitan area, while Bealls operated primarily smaller stores, principally located in rural Texas towns.

In 2003, we acquired Peebles Inc. (“Peebles”), a privately held, similarly small-market focused retail company headquartered in South Hill, Virginia. Our Peebles stores are located in the Mid Atlantic, Northeastern, Midwestern and Southeastern states.

In July 2009, we acquired the “Goody’s” name from Goody’s Family Clothing, Inc. through a bankruptcy auction. Our Goody’s stores are primarily located in the Southeastern and Midwestern states.

On April 7, 2017, we acquired select assets of Gordmans Stores, Inc. and its subsidiaries through a bankruptcy auction (“Gordmans Acquisition”). The results of the Gordmans stores that we operated from April 7, 2017 through February 3, 2018 are included in our consolidated statement of operations for fiscal year 2017 (see Note 15 to the consolidated financial statements). Our Gordmans stores are primarily located in the Midwestern states.

Competition

The department store and off-price retail markets are highly competitive and fragmented. We operate in a challenging macroeconomic and retail environment and have numerous competitors as further described in Item 1A, Risk Factors, of this Form 10-K. We believe the principal differentiating factors which allow us to compete for guests’ patronage include great values on name brand merchandise, assortments that appeal to our target guests, exceptional service in convenient locations, compelling advertising and promotions and an omni-channel shopping experience. We expect the strategic investments we have made and plan to continue to make will enable us to meet these guest expectations and leave us well positioned to compete in the future.

4

Stores

Store Openings and Closures. We added 58 Gordmans off-price stores in 2017 with the Gordmans Acquisition. We plan to open one new Gordmans store in early 2018. As part of a strategic evaluation of our department store portfolio in 2015, we announced a multi-year plan to close stores that we believe do not have the potential to meet our sales productivity and profitability standards. Since then, we have closed 81 stores, including 21 stores during 2017, and we expect to close approximately 30 stores in 2018. We continually review the profitability of each store and will consider closing a store if the expected store performance does not meet our financial standards. The closure of these stores is expected to improve our ability to effectively allocate capital, deliver higher sales productivity and be accretive to earnings.

Expansion, Relocation and Remodeling. During 2017, we completed 9 store remodels, relocations and expansions. Since 2015, we have updated over 200 stores representing approximately 45% of our sales base. We believe that our investment in these stores improves the store environment and helps us create an inviting and differentiated shopping experience. Our store remodels are designed to create a bright, fun and comfortable environment and include upgrades ranging from improved lighting, flooring, paint, fixtures, fitting rooms, visual merchandising and signage, to more extensive expansion projects.

Store count and selling square footage by nameplate are as follows:

Number of Stores | Selling Square Footage (in thousands) | |||||||||||||||||

January 28, 2017 | 2017 Activity Net Changes | February 3, 2018 | January 28, 2017 | 2017 Activity Net Changes | February 3, 2018 | |||||||||||||

Bealls | 188 | (7 | ) | 181 | 3,787 | (171 | ) | 3,616 | ||||||||||

Goody's | 223 | (6 | ) | 217 | 3,451 | (88 | ) | 3,363 | ||||||||||

Palais Royal | 49 | (3 | ) | 46 | 1,063 | (73 | ) | 990 | ||||||||||

Peebles | 187 | (2 | ) | 185 | 3,429 | (39 | ) | 3,390 | ||||||||||

Stage | 151 | (3 | ) | 148 | 2,858 | (80 | ) | 2,778 | ||||||||||

Gordmans | — | 58 | 58 | — | 2,825 | 2,825 | ||||||||||||

Total | 798 | 37 | 835 | 14,588 | 2,374 | 16,962 | ||||||||||||

Our department stores are predominantly located in small towns and rural communities. Utilizing a ten-mile radius from each store, approximately 61% of our department stores are located in communities with populations below 50,000 people, while an additional 24% of our department stores are located in communities with populations between 50,000 and 150,000 people. The remaining 15% of our department stores are located in higher-density markets with populations greater than 150,000 people, such as Houston, San Antonio and Lubbock, Texas.

Our Gordmans off-price stores are predominantly located in mid-sized, non-rural Midwest markets.

Omni-channel

In our ongoing effort to enhance the guest experience, we are focused on better connecting our department store and online channels. Below are few examples of how our department store and online channels intersect:

• | Our website gives guests the opportunity to preview merchandise online before making a purchase in our stores. |

• | Stores increase online sales by providing guests with the opportunity to view, touch and/or try on physical merchandise before ordering online. |

• | Most online purchases can easily be returned in our stores. |

• | In 2016, we introduced Buy Online, Ship-to-Store, which gives our guests the option to have online purchases shipped for free to a local store. |

• | In 2017, we introduced Web@POS, which gives our guests access to our expanded online assortments from within our stores. |

• | Style Circle Rewards® can be redeemed online or in stores regardless of where they are earned. |

• | Guests may apply most discounts to both online and in-store purchases. |

Providing our guests with the opportunity to engage with us through multiple channels is part of a cohesive business strategy that helps us build our brand loyalty. Guests that shop with us both online and in stores spend, on average, 3 times more than guests that shop only in our stores.

5

Merchandising

We offer a well-edited selection of moderately priced, branded merchandise within distinct merchandise categories of women’s, men’s and children’s apparel, accessories, cosmetics, footwear and home goods that reflect current styles and trends through our department stores, off-price stores and e-commerce website.

The following table sets forth the distribution of net sales among our various merchandise categories:

Fiscal Year | |||||||||||||||

2017 | 2016 | 2015 | |||||||||||||

Merchandise Category | Department Stores | Off-price Stores | Total Company | ||||||||||||

Women’s | 35 | % | 29 | % | 34 | % | 37 | % | 38 | % | |||||

Men’s | 17 | 13 | 17 | 17 | 17 | ||||||||||

Children's | 11 | 12 | 11 | 12 | 11 | ||||||||||

Apparel | 63 | % | 54 | % | 62 | % | 66 | % | 66 | % | |||||

Footwear | 14 | % | 2 | % | 12 | % | 13 | % | 13 | % | |||||

Accessories | 7 | 9 | 8 | 7 | 7 | ||||||||||

Cosmetics/Fragrances | 11 | 5 | 10 | 10 | 10 | ||||||||||

Home/Gifts/Other | 5 | 30 | 8 | 4 | 4 | ||||||||||

Non-apparel | 37 | % | 46 | % | 38 | % | 34 | % | 34 | % | |||||

100 | % | 100 | % | 100 | % | 100 | % | 100 | % | ||||||

Our merchandise mix in our department stores offers more apparel categories, while our off-price stores carry a larger selection of home goods. Merchandise mix may also vary from store to store to accommodate differing demographic, regional and climate characteristics. Our buying and planning team uses technology tools such as size pack optimization, which allow us to better fulfill guest needs by tailoring size assortments by store.

Approximately 82% of sales in our department stores consist of national brands such as Adidas, Calvin Klein, Carters, Chaps, Clinique, Dockers, Estee Lauder, G by Guess, Izod, Jessica Simpson, Levi’s, Nike, Nine West and Skechers, while the remaining 18% of sales are private label merchandise. Our off-price stores offer national brands purchased opportunistically bringing greater value to our guests.

Our department store private label portfolio brands are developed and sourced through agreements with third party vendors. We believe our private label and exclusive brands offer a compelling mix of style, quality and value.

Merchandise Distribution

We distribute merchandise to our department stores through our distribution centers located in Jacksonville, Texas, and Jeffersonville, Ohio and to our Gordmans off-price stores through our distribution center in Omaha, Nebraska. In December 2017, we closed our South Hill, Virginia, distribution center, as part of our strategy to increase the efficiency of our distribution network. Operations from the Virginia distribution center have been transferred to our distribution centers in Texas and Ohio. E-commerce orders are predominantly filled from our distribution center in Jacksonville, Texas and to a lesser extent, from our distribution center in Jeffersonville, Ohio, select stores and directly from our vendors. We contract with third party carriers to deliver merchandise to our stores and to our guests in the fulfillment of online orders. Guests also have the option to pick up an online order in a local store through our Buy Online, Ship-to-Store program.

6

Marketing

Our marketing strategy is designed to establish and reward brand loyalty. The strategy supports each store’s position as the destination for desirable styles and national brands at an attractive value in a comfortable and welcoming environment. Our marketing strategy leverages (i) insights from brand and guest research, (ii) identified guest purchase history and (iii) emerging technology and trends in retail marketing. We use a multi-media advertising approach, including broadcast media, digital media, mobile media, direct mail, and to a lesser degree, newspaper inserts.

Our department stores and off-price stores are similar in many respects. However, our department stores offer deeper, more curated assortments with sales driven by high-low promotions. Conversely, our Gordmans off-price stores offer every day value in a “treasure hunt” environment with sales driven by holidays, back-to-school, and other calendar events.

We consider our private label credit card program, and our loyalty programs, Style Circle Rewards® and gRewardsTM, to be vital components of our business because these programs (i) enhance guest loyalty, (ii) allow us to identify and regularly contact our best guests and (iii) create a comprehensive database that enables us to implement targeted and personalized marketing messages. On average, private label credit cardholders and loyalty members visit our stores more frequently, spend more annually, and are less likely to attrite than non-loyalty guests. In our department stores, private label credit card purchases represented 49%, 47% and 44% of our sales in 2017, 2016 and 2015, respectively. In our Gordmans off-price stores, we acquired a historically underpenetrated private label credit card program and implemented best practices developed in our department stores, which we expect to drive future growth. In 2017, we relaunched the value proposition for Style Circle Rewards® and our private label credit card in conjunction with launching gRewardsTM. We ended 2017 with 7.4 million Style Circle Rewards® members and 0.8 million gRewardsTM members. These programs allow us to better understand and respond to our guests’ shopping habits and are powerful tools to drive higher transaction value and frequency of visits.

Brand image is an important part of our marketing program. Our principal trademarks, including the BEALLS, GOODY’S, PALAIS ROYAL, PEEBLES, STAGE and GORDMANS, have been registered with the U.S. Patent and Trademark Office. We have also registered trademarks used in connection with our private label merchandise. We regard our trademarks and their protection as important to our success.

We maintain a connection to the communities we serve and operate a giving campaign in the markets we serve called 30 Days of Giving under our Community Counts program. In 2017, through our Community Counts program and other efforts like our Bears that Care program and Hurricane Harvey relief efforts, we helped raise approximately $3.0 million for our communities.

Guest Service

We strive to provide exceptional guest service. To ensure consistency of execution, each sales associate is evaluated based on the attainment of specific guest service standards, such as offering a friendly greeting, providing prompt assistance, helping open private label credit card accounts, thanking guests and inviting return visits. We also conduct guest satisfaction surveys to measure and monitor attainment of service expectations. The results of guest surveys are used to provide feedback to reinforce and improve store service. Additionally, we have various programs in place to recognize our sales associates for providing outstanding guest service.

7

Information Systems

We support our business by using multiple, highly integrated systems in areas such as merchandising, store operations, distribution, sales promotion, asset protection, personnel management, store design and accounting. Our core merchandising systems assist in planning, ordering, allocating and replenishing merchandise assortments for each store, based on specific characteristics and recent sales trends. Our replenishment/fulfillment system allows us to maintain planned levels of in-stock positions in basic items such as jeans and undergarments. In addition, a fully integrated warehouse management system is in place in all three distribution centers.

Our assortment planning system allows us to create guest-centric assortments aligned to sales strategies. The system also facilitates cleaner seasonal transitions and fresher merchandise in stores. We continue to expand the utilization and effectiveness of our merchandise planning system to maximize the generation of sales and gross margin.

We utilize a point-of-sale (“POS”) platform with bar code scanning, electronic credit authorization, instant credit, a returns database and gift card processing in all our stores. The POS platform allows us to capture guest specific sales data for use in our merchandising, marketing and loss prevention systems, while servicing our guests. The POS platform also manages coupon and deal-based pricing, which streamlines the checkout process and improves store associate adherence to promotional markdown policies.

In 2017, we implemented new systems to facilitate our Web@POS and Buy Online, Ship-to-Store programs as part of our strategy to better connect our department store and online channels. Web@POS provides guests access to our online merchandise assortments from within our department stores. Buy Online, Ship-to-Store provides our guests the ability to buy certain merchandise on our website and have it shipped to a store for pick-up. We also continue to invest in enhancements to improve the performance of our e-commerce website.

Our Employees

At February 3, 2018, we employed approximately 14,500 full-time and part-time employees, referred to as “associates.” Employment levels vary during the year as we traditionally hire additional sales associates and increase the hours of part-time sales associates during peak seasonal selling periods. We offer a broad range of company-paid benefits to our associates. Eligibility for and the level of benefits vary depending on associates' full-time or part-time status, compensation level, date of hire and/or length of service. Company-paid benefits include a 401(k) plan, deferred compensation plans, medical and dental plans, disability insurance, paid vacation, life insurance and merchandise discounts. We consider our relationship with our associates to be good, and there are no collective bargaining agreements in effect with respect to any of our associates.

Seasonality

Our business, like many other retailers, is subject to seasonal influences with a significant portion of sales and income typically realized during the last quarter of our fiscal year. Working capital requirements fluctuate during the year and generally reach their highest levels during the third and fourth quarters. Because of the seasonality of our business, results from any quarter are not necessarily indicative of the results that may be achieved for a full fiscal year.

8

Available Information

We make available, free of charge, through the “Investor Relations” section of our website (corporate.stage.com)

under the “Financial Reports” caption, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934, as amended (“Exchange Act”) as soon as reasonably practicable after we file such material with, or furnish it to, the Securities and Exchange Commission (“SEC”). In this Form 10-K, we incorporate by reference certain information from parts of our Proxy Statement for our 2018 Annual Meeting of Shareholders (“Proxy Statement”).

Also in the “Investor Relations” section of our website (corporate.stage.com) under the “Corporate Governance” and “Financial Reports” captions, the following information relating to our corporate governance may be found: Corporate Governance Guidelines; charters of our Board of Directors’ Audit, Compensation, and Corporate Governance and Nominating Committees; Code of Ethics and Business Conduct; Code of Ethics for Senior Officers; Chief Executive Officer and Chief Financial Officer certifications related to our SEC filings; and transactions in our securities by our directors and executive officers. The Code of Ethics and Business Conduct applies to all of our directors and employees. The Code of Ethics for Senior Officers applies to our Chief Executive Officer, Chief Financial Officer, Controller and other individuals performing similar functions, and contains provisions specifically applicable to the individuals serving in those positions. We intend to post amendments to and waivers from, if any, our Code of Ethics and Business Conduct (to the extent applicable to our directors and executive officers) and our Code of Ethics for Senior Officers in the “Investor Relations” section of our website (corporate.stage.com) under the “Corporate Governance” caption. We will provide any of the foregoing information without charge upon written request to our Secretary. The contents of our websites are not part of this report.

9

ITEM 1A. RISK FACTORS

Cautionary Statement Concerning Forward-Looking Statements for Purposes of the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995

The Private Securities Litigation Reform Act of 1995 (“Act”) provides a safe harbor for forward-looking statements to encourage companies to provide prospective information, so long as those statements are identified as forward-looking and are accompanied by meaningful cautionary statements identifying important factors that may cause actual results to differ materially from those discussed in the statements. We wish to take advantage of the “safe harbor” provisions of the Act.

Certain statements in this report are forward-looking statements within the meaning of the Act, and such statements are intended to qualify for the protection of the safe harbor provided by the Act. The words “anticipate,” “estimate,” “expect,” “objective,” “goal,” “project,” “intend,” “plan,” “believe,” “will,” “should,” “may,” “target,” “forecast,” “guidance,” “outlook,” and similar expressions generally identify forward-looking statements. Similarly, descriptions of our objectives, strategies, plans, goals or targets are also forward-looking statements. Forward-looking statements relate to the expectations of management as to future occurrences and trends, including statements expressing optimism or pessimism about future operating results or events and projected sales, earnings, capital expenditures and business strategy.

Forward-looking statements are based upon a number of assumptions and factors concerning future conditions that may ultimately prove to be inaccurate and could cause actual results to differ materially from those in the forward-looking statements. Forward-looking statements that are made herein and in other reports and releases are not guarantees of future performance and actual results may differ materially from those discussed in such forward-looking statements as a result of various factors. These factors include, but are not limited to, the ability for us to maintain normal trade terms with vendors, the ability for us to comply with the various covenant requirements contained in the Revolving Credit Facility agreement (as defined in “Liquidity and Capital Resources”), the demand for apparel, and other factors. The demand for apparel and sales volume can be affected by significant changes in economic conditions, including an economic downturn, employment levels in our markets, consumer confidence, energy and gasoline prices, the value of the Mexican peso, and other factors influencing discretionary consumer spending. Other factors affecting the demand for apparel and sales volume include unusual weather patterns, an increase in the level of competition, competitors’ marketing strategies, changes in fashion trends, changes in the average cost of merchandise purchased for resale, availability of product on normal payment terms and the failure to achieve the expected results of our merchandising and marketing plans as well as our store opening or relocation plans. Additional assumptions, factors and risks concerning future conditions are discussed in the Risk Factors section of this Form 10-K, and may be discussed from time to time in our other filings with the SEC, including Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Most of these factors are difficult to predict accurately and are generally beyond our control.

Forward-looking statements are and will be based upon management’s then-current views and assumptions regarding future events and operating performance, and are applicable only as of the dates of such statements. Although management believes the expectations expressed in forward-looking statements are based on reasonable assumptions within the bounds of our knowledge, forward-looking statements, by their nature, involve risks, uncertainties and other factors, any one or a combination of which could materially affect our business, financial condition, results of operations or liquidity.

Readers should carefully review this Form 10-K in its entirety, including, but not limited to our financial statements and the accompanying notes, and the risks and uncertainties described in this Item 1A. Readers should consider these risks, uncertainties and other factors carefully in evaluating forward-looking statements. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date they are made. Forward-looking statements contained in this Form 10-K are made as of the date of this Form 10-K. We undertake no obligation to publicly update forward-looking statements whether as a result of new information, future events or otherwise. Readers are advised, however, to consult any further disclosures we make on related subjects in our public announcements and SEC filings.

Our ability to achieve the results contemplated by forward-looking statements is subject to a number of factors, any one, or a combination, of which could materially affect our business, financial condition, results of operations, or liquidity. Described below are certain risk factors that management believes are applicable to our business and the industry in which we operate. There may also be additional risks that are presently immaterial or unknown.

10

Competitive and Operational Risks

We face significant competition in the retail apparel industry, which may adversely affect our sales and profitability. The retail apparel business is highly competitive. We compete with local, regional, national and online retailers, including department, specialty and discount stores, direct-to-consumer businesses and other forms of retail commerce. The Internet and evolving technologies in retail have led to increased competition as there are fewer barriers to entry and consumers are able to quickly and conveniently comparison shop. We compete on many factors, such as merchandise assortment, advertising, price, quality, convenience, guests’ shopping experience, store environment, service, loyalty programs and credit availability. Unanticipated changes in the pricing and other practices of our competitors may create downward pressure on prices and lower demand for our products, which may adversely impact our sales and profitability.

If we are unable to successfully execute our strategies, our operating performance may be significantly impacted. There is a risk that we will be unable to meet our operating performance targets and goals if our strategies and initiatives are unsuccessful. Our ability to develop and execute our strategic plan and to execute the business activities associated with our strategic and operating plans may impact our ability to meet our operating performance targets.

Our failure to anticipate and respond to changing guest preferences in a timely manner may adversely affect our operations. Our success depends, in part, upon our ability to anticipate and respond to changing consumer preferences and fashion trends in a timely manner. We attempt to stay abreast of emerging lifestyles and consumer preferences affecting our merchandise. However, any sustained failure on our part to identify and respond to such trends may have a material and adverse effect on our business, financial condition and cash flows.

Failure to successfully operate our Gordmans stores as an off-price retailer, or to grow the Gordmans off-price business as planned may adversely affect our results of operations and financial condition. We operated 58 Gordmans off-price stores during 2017, following the Gordmans Acquisition on April 7, 2017. During 2017, we progressed with converting the Gordmans stores into a true off-price retailer by eliminating promotions and implementing pricing that is competitive with the off-price industry. We view Gordmans as a key growth opportunity for our business. If we are not able to successfully operate the Gordmans stores as an off-price retailer, or grow the Gordmans off-price business as planned, the anticipated scale and profitability may not be realized fully or at all, or may take longer to realize than expected, which may adversely affect our results of operations and financial condition.

Failure to successfully operate our e-commerce website or fulfill guest expectations may adversely impact our business and sales. Our e-commerce platform provides another channel to generate sales. We believe that our e-commerce website will drive incremental sales by providing existing guests another opportunity to shop with us and allowing us to reach new guests. If we do not successfully meet the challenges of operating an e-commerce website or fulfilling guest expectations, our business and sales may be adversely affected.

Our failure to attract, develop and retain qualified employees may negatively impact the results of our operations. We strive to have well-trained and motivated sales associates provide guests with exceptional service. Our success depends in part upon our ability to attract, develop and retain a sufficient number of qualified employees, including store, service and administrative personnel. Competition for key personnel in the retail industry is intense and our future success will depend on our ability to recruit, train and retain our senior executives and other qualified personnel.

11

Supply Chain and Distribution Risks

Risks associated with our vendors from whom our products are sourced may have a material adverse effect on our business and financial condition. Our merchandise is sourced from a variety of domestic and international vendors. All of our vendors must comply with applicable laws, including our required standards of conduct. Political or financial instability, trade restrictions, tariffs, currency exchange rates, transport capacity and costs and other factors relating to foreign trade, the ability to access suitable merchandise on acceptable terms and the financial viability of our vendors are beyond our control and may adversely impact our performance.

Risks associated with our carriers, shippers and other providers of merchandise transportation services may have a material adverse effect on our business and financial condition. Our vendors rely on shippers, carriers and other merchandise transportation service providers (collectively “Transportation Providers”) to deliver merchandise from their manufacturers, both in the United States and abroad, to the vendors’ distribution centers in the United States. Transportation Providers are also responsible for transporting merchandise from their vendors’ distribution centers to our distribution centers. We also rely on Transportation Providers to transport merchandise from our distribution centers to our stores and to our guests in the case of online sales. However, if work slowdowns, stoppages, weather or other disruptions affect the transportation of merchandise between the vendors and their manufacturers, especially those manufacturers outside the United States, between the vendors and us, or between us and our e-commerce guests, our business, financial condition and cash flows may be adversely affected.

Financial and Liquidity Risks

Our dependence upon cash flows and net earnings generated during the fourth quarter, including the holiday season, may have a disproportionate impact on our results of operations. The seasonal nature of the retail industry causes a heavy dependence on earnings in the fourth quarter. A large fluctuation in economic or weather conditions occurring during the fourth quarter may adversely impact our earnings. In preparation for our peak season, we may carry a significant amount of inventory in advance. If, however, we do not manage inventory appropriately or guest preferences change we may need to increase markdowns or promotional sales to dispose of inventory which will negatively impact our financial results.

Failure to obtain merchandise product on normal trade terms may adversely impact our business, financial condition and cash flows. We are highly dependent on obtaining merchandise product on normal trade terms. Failure to meet our performance objectives may cause key vendors and factors to become more restrictive in granting trade credit. The tightening of credit, such as a reduction in our lines of credit or payment terms from the vendor or factor community, may have a material adverse impact on our business, financial condition and cash flows. We are also highly dependent on obtaining merchandise at competitive and predictable prices. If we experience rising prices related to our merchandise, whether due to cost of materials, inflation, transportation costs, or otherwise, our business, financial condition and cash flows may be adversely and materially affected.

There can be no assurance that our liquidity will not be affected by changes in macroeconomic conditions. Due to our operating cash flow and availability under the Revolving Credit Facility, we continue to believe that we have the ability to meet our financing needs for the foreseeable future. However, there can be no assurance that our liquidity will not be materially and adversely affected by changes in macroeconomic conditions.

12

The Revolving Credit Facility contains covenants that may impose operating restrictions and limits our borrowing capacity to the value of certain of our assets. The Revolving Credit Facility agreement contains covenants which, among other things, restrict (i) the amount of additional debt or capital lease obligations, (ii) the payment of dividends, and (iii) the repurchase of common stock under certain circumstances. A violation of any of these covenants may permit the lenders to restrict our ability to further access loans and letters of credit and may require the immediate repayment of any outstanding loans. Our failure to comply with these covenants may have a material adverse effect on our capital resources, financial condition, results of operations and liquidity. In addition, any material or adverse developments affecting our business may significantly limit our ability to meet our obligations as they become due or to comply with the various covenant requirements contained in the Revolving Credit Facility agreement. In addition, borrowings under the Revolving Credit Facility are limited to the availability under a borrowing base that is determined principally on eligible inventory, and our inventory, cash and cash equivalents are pledged as collateral under the Revolving Credit Facility. In the event of any material decrease in the amount of or appraised value of our inventory, our borrowing capacity would decrease, which may adversely impact our business and liquidity. In the event of a default that is not cured or waived, the lenders’ commitment to extend further credit under the Revolving Credit Facility may be terminated, our outstanding obligations may become immediately due and payable, outstanding letters of credit may be required to be cash collateralized, and remedies may be exercised against the collateral. If we are unable to borrow under the Revolving Credit Facility, we may not have the necessary cash resources for our operations and, if any event of default occurs, there is no assurance that we would have the cash resources available to repay such accelerated obligations, refinance such indebtedness on commercially reasonable terms, or at all, or cash collateralize our letters of credit, which would have a material adverse effect on our business, financial condition, results of operations and liquidity.

The inability or unwillingness of one or more lenders to fund their commitment under the Revolving Credit Facility may have a material adverse impact on our business and financial condition. We use the Revolving Credit Facility to provide financing for working capital, capital expenditures and other general corporate purposes, as well as to support our outstanding letters of credit requirements. The lenders under the Revolving Credit Facility are: Wells Fargo Bank, National Association, JPMorgan Chase Bank, N.A., Regions Bank, Bank of America, N.A. and SunTrust Bank. Notwithstanding that we may be in full compliance with all covenants contained in the Revolving Credit Facility, the inability or unwillingness of one or more of those lenders to fund their commitment under the Revolving Credit Facility may have a material adverse impact on our business and financial condition.

Changes in our private label credit card program may adversely affect our sales and/or profitability. Our private label credit card (“PLCC”) program facilitates sales and generates additional revenue under our profit sharing agreement with the unrelated third party which owns the PLCC accounts receivable. PLCC sales represented 49% of total department stores sales in 2017, and PLCC guests spend more on average than non-PLCC guests. We receive a share of the net finance charges, late fees, other cardholder fees, write-offs, and operating expenses generated by the program. Changes in credit granting standards maintained by the third party, which may be due to macroeconomic trends, could impact our ability to generate new PLCC accounts. Changes in guest payment patterns could impact profit sharing by impacting fee income, write-offs and operating expense. If the sales or profit share that we receive from the PLCC decreases due to economic, legal, social, or other factors that we cannot control or predict, our operating results, financial condition and cash flows may be adversely affected.

Unexpected costs may arise from our current insurance program and our financial performance may be affected. Our insurance coverage is subject to deductibles, self-insured retentions, limits of liability and similar provisions that we believe are prudent based on the dispersion of our operations. However, we may incur certain types of losses that we cannot insure or that we believe are not economically reasonable to insure, such as losses due to acts of war, employee and certain other crime and some natural disasters. If we incur these losses and they are material, our business could suffer. Certain material events, including property losses caused by various natural disasters and other types of casualties, may result in sizable losses for the insurance industry and adversely impact the availability of adequate insurance coverage or result in excessive premium increases. To offset negative cost trends in the insurance market, we may elect to self-insure, accept higher deductibles or reduce the amount of coverage in response to these market changes. In addition, we self-insure a portion of expected losses under our workers’ compensation, general liability and group health insurance programs. Unanticipated changes in any applicable actuarial assumptions and management estimates underlying our recorded liabilities for these losses, including potential increases in medical and indemnity costs, could result in materially different amounts of expense than expected under these programs, which may have a material adverse effect on our financial condition and results of operations. Although we continue to maintain property insurance for catastrophic events, we are self-insured for losses up to the amount of our deductibles. If we experience a greater number of self-insured or uninsured losses than we anticipate or excessive premium increases, our financial performance may be adversely affected.

13

Economic Conditions, Business Disruption and Other External Risks

An economic downturn or decline in consumer confidence may negatively impact our business and financial condition. Our results of operations are sensitive to changes in general economic and political conditions that impact consumer discretionary spending, such as employment levels, taxes, energy and gasoline prices and other factors influencing consumer confidence. We have extensive operations in the South Central, Southeastern, Midwestern and Mid-Atlantic states. Many stores are located in small towns and rural environments that are substantially dependent upon the local economy. We also have concentrations of stores in areas where the local economy is heavily dependent on the oil and gas industry, particularly in portions of Texas, Louisiana, Oklahoma and New Mexico. A decline in crude oil prices and/or oil or gas exploration may negatively impact employment in those communities, resulting in reduced consumer confidence and discretionary spending. Additionally, approximately 3% of our stores contributing approximately 6% of our 2017 sales are located in cities that either border Mexico or are in close proximity to Mexico. A devaluation of the Mexican peso will reduce the purchasing power of those guests who are citizens of Mexico. In such an event, revenues attributable to these stores could be reduced. In early 2017, 2016 and 2015, we experienced pressure on our business in areas that are heavily dependent on the oil industry and near the Mexican border. If those pressures continue or there is an additional economic downturn or decline in consumer confidence, particularly in the South Central, Southeastern, Midwestern and Mid-Atlantic states and any state from which we derive a significant portion of our net sales (such as Texas or Louisiana), our business, financial condition and cash flows will be negatively impacted and such impact may be material.

We are subject to payment-related risks that may increase our operating costs, expose us to fraud or theft, subject us to potential liability and potentially disrupt our business. We accept payments using a variety of methods, including cash, checks, credit cards, debit cards, and gift cards, and we may offer new payment options over time. Acceptance of these payment options subjects us to rules, regulations, contractual obligations and compliance requirements, including payment network rules and operating guidelines, data security standards and certification requirements and rules governing electronic funds transfers. These requirements may change over time or be reinterpreted, making compliance more difficult or costly. We rely on third parties to provide payment processing services and pay interchange and other fees, which may increase over time and raise our operating costs. On October 1, 2015, the payment cards industry began shifting liability for certain debit and credit card transactions to retailers who do not accept Europay, MasterCard and Visa (“EMV”) chip technology transactions. We have not yet implemented EMV chip technology. Implementation of the EMV chip technology and receipt of final certification is subject to the time availability of third-party service providers and may require upgrades to our systems and hardware. Further, we may experience a decrease in transaction volume if we cannot process transactions for cardholders whose card issuer has migrated entirely from magnetic strip to EMV chip enabled cards. Until we are able to fully implement and certify the EMV chip technology in our stores, we may be liable for chargebacks related to counterfeit transactions generated through EMV chip enabled cards, which could negatively impact our operational results, financial position and cash flows.

Unusual weather patterns or natural disasters may negatively impact our financial condition. Our business depends, in part, on normal weather patterns in our markets. We are susceptible to unseasonable and severe weather conditions, including natural disasters, such as hurricanes and tornadoes. Any unusual or severe weather, especially in states such as Texas and Louisiana, may have a material and adverse impact on our business, financial condition and cash flows. In addition, our business, financial condition and cash flow may be adversely affected if the businesses of our key vendors or their merchandise manufacturers, shippers, carriers and other merchandise transportation service providers, including those outside of the United States, are disrupted due to severe weather, such as, but not limited to, hurricanes, typhoons, tornadoes, tsunamis or floods.

An event adversely affecting any of our buying, distribution or other corporate facilities may result in reduced revenues. Our buying, distribution and other corporate operations are in highly centralized locations. Our operations may be materially and adversely affected if a catastrophic event (such as, but not limited to, fire, hurricanes, tornadoes or floods) or other disruption impacts the access or use of these facilities. While we have contingency plans that would be implemented in such an event, there are no assurances that we would be successful in obtaining alternative servicing facilities in a timely manner.

War, acts of terrorism, Mexican border violence, public health issues and natural disasters may create uncertainty and may result in reduced revenues. We cannot predict, with any degree of certainty, what effect, if any, war, acts of terrorism, Mexican border violence, public health issues and natural disasters, if any, will have on us, our operations, the other risk factors discussed herein and the forward-looking statements we make in this Form 10-K. However, the consequences of these events may have a material adverse effect on our business, financial condition and cash flows.

14

The price of our common stock as traded on the New York Stock Exchange may be volatile. Our stock price may fluctuate substantially due to factors beyond our control, including but not limited to, general economic and stock market conditions, risks relating to our business and industry as discussed above, strategic actions by us or our competitors, variations in our quarterly operating performance and investor perceptions of the investment opportunity associated with our common stock relative to other investment alternatives.

Legal and Regulatory Risks

Changes in the regulatory or administrative landscape could adversely affect our financial condition and results of operations. Laws and regulations at the local, state, federal and international levels frequently change, and the ultimate cost of compliance cannot be precisely estimated. In addition, we cannot predict the impact that may result from changes in the regulatory or administrative landscape. Any changes in regulations, the imposition of additional regulations, or the enactment of any new or more stringent legislation that impacts employment and labor, trade, product safety, transportation and logistics, health care, tax, privacy, operations, or environmental issues, among others, could have an adverse impact on our financial condition and results of operations.

Our business may be materially and adversely affected by changes to fiscal and tax policies. A number of factors influence our effective income tax rate, including changes in tax law and related regulations, interpretation of existing laws, and our ability to sustain our reporting positions on examination. Changes in any of those factors could change our effective tax rate, which could adversely affect our results of operations.

We may be subject to periodic litigation and regulatory proceedings which may adversely affect our business and financial performance. From time to time, we are involved in lawsuits and regulatory proceedings. Due to the inherent uncertainties of such matters, we may not be able to accurately determine the impact on us of any future adverse outcome of such matters. The ultimate resolution of these matters may have a material adverse impact on our financial condition, results of operations and liquidity. In addition, regardless of the outcome, these matters may result in substantial cost to us and may require us to devote substantial attention and resources to defend ourselves.

If our trademarks are successfully challenged, the outcome of those disputes may require us to abandon one or more of our trademarks. We regard our trademarks and their protection as important to our success. However, we cannot be sure that any trademark held by us will provide us a competitive advantage or will not be challenged by third parties. Although we intend to vigorously protect our trademarks, the cost of litigation to uphold the validity and prevent infringement of trademarks can be substantial and the outcome of those disputes may require us to abandon one or more of our trademarks.

Technology Infrastructure, Data Security and Privacy Risks

A disruption of our information technology systems may have a material adverse impact on our business and financial condition. We are heavily dependent on our information technology systems for day-to-day business operations, including sales, warehousing, distribution, purchasing, inventory control, merchandise planning and replenishment, and financial systems. Certain of our information technology support functions are performed by third-parties in overseas locations. While we believe that we are diligent in selecting the vendors that assist us in maintaining the reliability and integrity of our information technology systems, failure by any of these third-parties to implement and/or manage our information systems and infrastructure effectively and securely could result in future disruptions, service outages, service failures or unauthorized intrusions. Despite our precautionary efforts, our information technology systems are vulnerable to damage or interruption from, among other things, natural or man-made disasters, technical malfunctions, inadequate systems capacity, power outages, computer viruses and security breaches, which may require significant investment to fix or replace, and we may suffer loss of critical data and interruptions or delays to our operations in the interim. In addition, as part of our normal course of business, we collect, process and retain sensitive and confidential guest information. Potential risks include, but are not limited to, the following: (i) an intrusion by a hacker, (ii) the introduction of malware (virus, Trojan horse, spyware), (iii) hardware failure, (iv) outages due to software defects and (v) human error. Although we run anti-virus and anti-spyware software and take other steps to ensure that our information technology systems will not be disabled or otherwise disrupted, there are no assurances that disruptions will not occur. The consequences of a disruption, depending on the severity, may have a material adverse effect on our business and financial condition and may expose us to civil, regulatory and industry actions and possible judgments, fees and fines.

15

A security breach that results in unauthorized disclosure of guest, employee, vendor or our company information may adversely impact our business, reputation and financial condition. In the standard course of business, we receive, process and store information about our guests, employees, vendors and our business, some of which is entrusted to third-party service providers and vendors. We also work with third-party service providers and vendors that provide technology, systems and services that we use in connection with the receipt, storage and transmission of this information. Hardware, software or applications obtained from third parties may contain defects in design or manufacture or other problems that could unexpectedly compromise our information security. We rely on commercially available systems, software, tools (including encryption technology) and monitoring to provide security and oversight for processing, transmission, storage and the protection of confidential information. Despite the security measures we have in place, our facilities and systems (and those of our vendors and third-party service providers) may be vulnerable to security breaches, acts of vandalism and theft, computer viruses, misplaced or lost data, programming and/or human errors, or other similar events. Our employees, contractors, vendors or third-party service providers may attempt to circumvent our security measures in order to misappropriate such information, and may purposefully or inadvertently cause a breach involving such information. Additionally, unauthorized parties may attempt to gain access to our systems or facilities through fraud, trickery, or other means of deceit. We have programs in place to detect, contain, respond to and report (internally and externally) data security incidents. However, because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently, we may be unable to anticipate these techniques or implement adequate preventive measures to safeguard against or timely disclose all data security breaches or misuses of data. Our management and Board of Directors regularly evaluate the risks associated with information security and our efforts to mitigate those risks. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential guest, employee or company information may severely damage our reputation, cause us to incur significant remediation costs, increase our information security protection costs, expose us to the risks of legal proceedings (including fines or other regulatory sanctions in excess of our insurance limits), disrupt our operations, attract a substantial amount of negative media attention, damage our guest and vendor relationships, increase our insurance premiums, damage our competitiveness, and otherwise have a material adverse impact on our reputation, stock price, business, operating results, financial condition and cash flows.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

16

ITEM 2. PROPERTIES

Our stores are primarily located in strip shopping centers. We own six of our stores and lease the balance. The majority of leases, which are typically for an initial 10-year term and often with two renewal options of five years each, provide for our payment of base rent plus expenses, such as common area maintenance, utilities, taxes and insurance. Certain leases provide for contingent rents that are not measurable at inception. These contingent rents are primarily based on a percentage of sales that are in excess of a predetermined level. Our stores range in size from approximately 5,000 to 73,000 selling square feet, with the average being approximately 18,000 selling square feet for department stores and approximately 49,000 selling square feet for off-price stores. At February 3, 2018, we operated 835 stores, in 42 states located within 5 regions, as follows:

Number of Stores | Number of Stores | |||||

South Central Region | Midwestern Region | |||||

Arkansas | 23 | Illinois | 11 | |||

Louisiana | 50 | Indiana | 30 | |||

Oklahoma | 34 | Iowa | 11 | |||

Texas | 220 | Kansas | 13 | |||

327 | Michigan | 17 | ||||

Mid-Atlantic & Northeastern Region | Minnesota | 2 | ||||

Delaware | 3 | Missouri | 20 | |||

Maryland | 6 | Nebraska | 3 | |||

New Jersey | 5 | North Dakota | 4 | |||

Pennsylvania | 32 | Ohio | 30 | |||

Virginia | 35 | South Dakota | 2 | |||

West Virginia | 10 | Wisconsin | 8 | |||

Massachusetts | 2 | 151 | ||||

New Hampshire | 1 | Northwestern & Southwestern Region | ||||

New York | 19 | Arizona | 7 | |||

Vermont | 4 | Colorado | 8 | |||

117 | Idaho | 5 | ||||

Southeastern Region | Nevada | 4 | ||||

Alabama | 27 | New Mexico | 19 | |||

Florida | 6 | Oregon | 4 | |||

Georgia | 33 | Utah | 4 | |||

Kentucky | 34 | Wyoming | 1 | |||

Mississippi | 21 | 52 | ||||

North Carolina | 24 | |||||

South Carolina | 19 | |||||

Tennessee | 24 | Total Stores | 835 | |||

188 | ||||||

17

We own a distribution center in Jacksonville, Texas and lease distribution centers in Jeffersonville, Ohio and Omaha, Nebraska. The distribution centers in Texas and Ohio support our department store business, and the distribution center in Nebraska supports our off-price store business. Our distribution centers have the following square footages:

Location | Square Footage |

Jacksonville, Texas | 437,000 |

Jeffersonville, Ohio | 202,000 |

Omaha, Nebraska | 350,000 |

989,000 | |

We also lease a 176,000 square foot facility in Jacksonville, Texas to provide capacity expansion for our growing e-commerce business.

We own a 162,000 square-foot distribution center building located in South Hill, Virginia that is no longer used and is currently held for sale.

We lease our corporate office building located in Houston, Texas.

Our properties are in good condition and are suitable for their intended purpose.

ITEM 3. LEGAL PROCEEDINGS

No response is required under Item 103 of Regulation S-K.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

18

PART II

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market and Dividend Information

Our common stock trades on the New York Stock Exchange under the symbol “SSI”. The following table sets forth the high and low market prices per share of our common stock as reported by the New York Stock Exchange and the amount of cash dividends per common share we paid during each quarter in 2017 and 2016:

Fiscal Year | |||||||||||||||||||||||

2017 | 2016 | ||||||||||||||||||||||

High | Low | Dividend | High | Low | Dividend | ||||||||||||||||||

1st Quarter | $ | 3.00 | $ | 1.80 | $ | 0.15 | $ | 9.00 | $ | 6.60 | $ | 0.15 | |||||||||||

2nd Quarter | 2.94 | 1.72 | 0.05 | 7.57 | 4.44 | 0.15 | |||||||||||||||||

3rd Quarter | 2.43 | 1.45 | 0.05 | 6.56 | 4.97 | 0.15 | |||||||||||||||||

4th Quarter | 2.22 | 1.61 | 0.05 | 5.88 | 2.72 | 0.15 | |||||||||||||||||

We paid aggregate cash dividends in 2017 and 2016 of $8.5 million and $16.7 million, respectively. The declaration and payment of future quarterly cash dividends remain subject to the review and discretion of our Board of Directors (“Board”). Future determinations to pay dividends will continue to be evaluated in light of our results of operations, cash flow and financial condition, as well as meeting certain criteria under the Revolving Credit Facility (as defined in “Liquidity and Capital Resources”) and other factors deemed relevant by our Board.

Holders

As of the close of trading on the New York Stock Exchange on March 23, 2018 there were approximately 231 holders of record of our common stock.

19

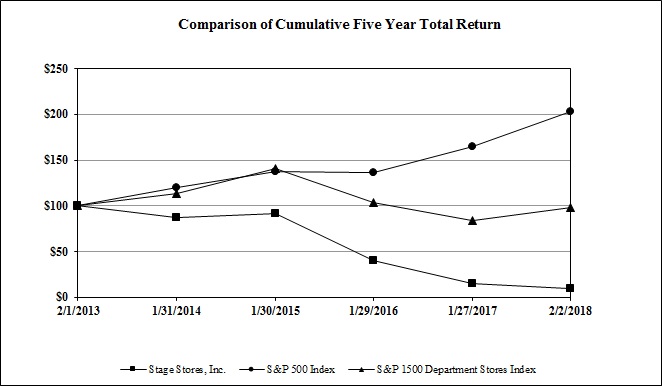

Performance Graph

The annual changes for the five-year period shown in the following graph are based on the assumption that $100 had been invested in each of our common stock, the S&P 500 Index and the S&P 1500 Department Stores Index on February 1, 2013 (the last trading date of 2012), and that all quarterly dividends were reinvested at the closing prices of the dividend payment dates. Subsequent measurement points are the last trading days of 2013, 2014, 2015, 2016 and 2017. The total cumulative dollar returns shown on the graph represent the value that such investments would have had on February 2, 2018 (the last trading date of 2017). The calculations exclude trading commissions and taxes. The stock price performance on the following graph and table is not necessarily indicative of future stock price performance.

Date | Stage Stores, Inc. | S&P 500 Index | S&P 1500 Department Stores Index | |||

2/1/2013 | $100.00 | $100.00 | $100.00 | |||

1/31/2014 | 87.26 | 120.30 | 113.28 | |||

1/30/2015 | 91.55 | 137.42 | 141.17 | |||

1/29/2016 | 39.80 | 136.50 | 103.65 | |||

1/27/2017 | 14.68 | 164.99 | 84.00 | |||

2/2/2018 | 9.96 | 202.66 | 98.61 | |||

20

Stock Repurchase Program

On March 7, 2011, our Board approved a stock repurchase program (“2011 Stock Repurchase Program”), which authorizes us to repurchase up to $200.0 million of our outstanding common stock. The 2011 Stock Repurchase Program will expire when we have exhausted the authorization, unless terminated earlier by our Board. Through February 3, 2018, we repurchased approximately $141.6 million of our outstanding common stock under the 2011 Stock Repurchase Program. Also in March 2011, our Board authorized us to repurchase shares of our outstanding common stock equal to the amount of the proceeds and related tax benefits from the exercise of stock options, stock appreciation rights (“SARs”) and other equity grants. Purchases of shares of our common stock may be made from time to time, either on the open market or through privately negotiated transactions, and are financed by our existing cash, cash flow and other liquidity sources, as appropriate.

The table below sets forth information regarding our repurchases of our common stock during the fourth quarter of 2017:

ISSUER PURCHASES OF EQUITY SECURITIES | ||||||||||||||

Period | Total Number of Shares Purchased (a) | Average Price Paid Per Share (a) | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs (b) | ||||||||||

October 29, 2017 to November 25, 2017 | 10,686 | $ | 1.89 | — | $ | 58,351,202 | ||||||||

November 26, 2017 to December 30, 2017 | 12,056 | 1.94 | — | 58,351,202 | ||||||||||

December 31, 2017 to February 3, 2018 | 8,089 | 1.77 | — | 58,351,202 | ||||||||||

Total | 30,831 | $ | 1.88 | — | ||||||||||

(a) Although we did not repurchase any of our common stock during the fourth quarter of 2017 under the 2011 Stock Repurchase Program:

• | We reacquired 4,445 shares of our common stock from certain employees to cover tax withholding obligations from the vesting of restricted stock at a weighted average acquisition price of $1.88 per share; and |

• | The trustee of the grantor trust established by us for the purpose of holding assets under our deferred compensation plan purchased an aggregate of 26,386 shares of our common stock in the open market at a weighted average price of $1.88 in connection with the option to invest in our stock under the deferred compensation plan and reinvestment of dividends paid on our common stock held in trust in the deferred compensation plan. |

(b) Reflects the $200.0 million authorized under the 2011 Stock Purchase Program, less the $141.6 million repurchased as of February 3, 2018 using our existing cash, cash flow and other liquidity sources since March 2011.

21

ITEM 6. SELECTED FINANCIAL DATA

The following sets forth selected consolidated financial data for the periods indicated. Financial results for 2017 are based on a 53-week period. Financial results for 2016, 2015, 2014 and 2013 are based on a 52-week period. The selected consolidated financial data should be read in conjunction with our Consolidated Financial Statements included herein. All amounts are stated in thousands, except for per share data, percentages and number of stores.

Fiscal Year | |||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

Statement of operations data: | |||||||||||||||||||

Net sales | $ | 1,592,275 | $ | 1,442,718 | $ | 1,604,433 | $ | 1,638,569 | $ | 1,609,481 | |||||||||

Cost of sales and related buying, occupancy and distribution expenses | 1,228,780 | 1,144,666 | 1,208,002 | 1,188,763 | 1,172,995 | ||||||||||||||

Gross profit | 363,495 | 298,052 | 396,431 | 449,806 | 436,486 | ||||||||||||||

Selling, general and administrative expenses | 406,206 | 356,064 | 387,859 | 386,104 | 393,126 | ||||||||||||||

Interest expense | 7,680 | 5,051 | 2,977 | 3,002 | 2,744 | ||||||||||||||

(Loss) income from continuing operations before income tax | (50,391 | ) | (63,063 | ) | 5,595 | 60,700 | 40,616 | ||||||||||||

Income tax (benefit) expense | (13,068 | ) | (25,166 | ) | 1,815 | 22,847 | 15,400 | ||||||||||||

(Loss) income from continuing operations | (37,323 | ) | (37,897 | ) | 3,780 | 37,853 | 25,216 | ||||||||||||

Loss from discontinued operations, net (a) | — | — | — | (7,003 | ) | (8,574 | ) | ||||||||||||

Net (loss) income | $ | (37,323 | ) | $ | (37,897 | ) | $ | 3,780 | $ | 30,850 | $ | 16,642 | |||||||

Adjusted net (loss) income (non-GAAP) (b) | $ | (23,037 | ) | $ | (24,078 | ) | $ | 16,182 | $ | 37,853 | $ | 39,986 | |||||||

Basic (loss) earnings per share data: | |||||||||||||||||||

Continuing operations | $ | (1.37 | ) | $ | (1.40 | ) | $ | 0.12 | $ | 1.18 | $ | 0.78 | |||||||

Discontinued operations(a) | — | — | — | (0.22 | ) | (0.27 | ) | ||||||||||||

Basic (loss) earnings per share | $ | (1.37 | ) | $ | (1.40 | ) | $ | 0.12 | $ | 0.96 | $ | 0.51 | |||||||

Basic weighted average shares outstanding | 27,510 | 27,090 | 31,145 | 31,675 | 32,034 | ||||||||||||||

Diluted (loss) earnings per share data: | |||||||||||||||||||

Continuing operations | $ | (1.37 | ) | $ | (1.40 | ) | $ | 0.12 | $ | 1.18 | $ | 0.77 | |||||||

Discontinued operations (a) | — | — | — | (0.22 | ) | (0.26 | ) | ||||||||||||

Diluted (loss) earnings per share | $ | (1.37 | ) | $ | (1.40 | ) | $ | 0.12 | $ | 0.96 | $ | 0.51 | |||||||

Adjusted diluted (loss) earnings per share (non-GAAP) (b) | $ | (0.85 | ) | $ | (0.89 | ) | $ | 0.51 | $ | 1.18 | $ | 1.22 | |||||||

Diluted weighted average shares outstanding | 27,510 | 27,090 | 31,188 | 31,763 | 32,311 | ||||||||||||||

Gross profit and SG&A as a percentage of sales: | |||||||||||||||||||

Gross profit margin | 22.8 | % | 20.7 | % | 24.7 | % | 27.5 | % | 27.1 | % | |||||||||

Selling, general and administrative expense rate | 25.5 | % | 24.7 | % | 24.2 | % | 23.6 | % | 24.4 | % | |||||||||

Cash flow and other data: | |||||||||||||||||||

Capital expenditures | $ | 38,630 | $ | 74,257 | $ | 90,695 | $ | 70,580 | $ | 61,263 | |||||||||

Construction allowances from landlords | 1,228 | 7,079 | 3,444 | 5,538 | 4,162 | ||||||||||||||

Business acquisition | 36,144 | — | — | — | — | ||||||||||||||

Stock repurchases | — | — | 41,587 | 2,755 | 31,367 | ||||||||||||||

Cash dividends per share | 0.30 | 0.60 | 0.58 | 0.53 | 0.48 | ||||||||||||||

22

Fiscal Year | |||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

Store data: | |||||||||||||||||||

Comparable sales (decline) growth (c) | (3.6 | )% | (8.8 | )% | (2.0 | )% | 1.4 | % | (1.5 | )% | |||||||||

Store openings (d) | 58 | — | 3 | 18 | 28 | ||||||||||||||

Store closings (d) | 21 | 37 | 23 | 12 | 10 | ||||||||||||||

Number of stores open at end of period (d) | 835 | 798 | 834 | 854 | 848 | ||||||||||||||

Total selling area square footage at end of period (d) | 16,962 | 14,588 | 15,130 | 15,409 | 15,313 | ||||||||||||||

February 3, | January 28, | January 30, | January 31, | February 1, | |||||||||||||||

2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||||||

Balance sheet data: | |||||||||||||||||||

Working capital | $ | 298,616 | $ | 296,091 | $ | 344,880 | $ | 299,279 | $ | 293,995 | |||||||||

Total assets | 806,406 | 786,989 | 848,099 | 824,677 | 810,837 | ||||||||||||||

Debt obligations | 183,335 | 170,163 | 165,723 | 47,388 | 63,225 | ||||||||||||||

Stockholders' equity | 344,114 | 380,160 | 429,753 | 475,930 | 454,444 | ||||||||||||||

(a) Discontinued operations reflect the results of Steele’s, which was divested in 2014.

(b) See Reconciliation of Non-GAAP Financial Measures on page 24 for additional information and reconciliation to the most directly comparable U.S. GAAP financial measure.

(c) Comparable sales for 2017 were measured over the 52-week period and exclude the last week of 2017.

(d) Fiscal 2017 reflects the addition of Gordmans off-price stores. The fiscal 2016 year-end store count includes one store that was relocated during the year after being temporarily closed in 2015, and was excluded from the 2015 year-end store count. Fiscal 2013 and 2014 exclude Steele’s, which was divested in 2014.

23

Reconciliation of Non-GAAP Financial Measures

To provide additional transparency, we have disclosed the results of operations for the years presented on a basis in conformity with accounting principles generally accepted in the United States of America (“GAAP”) and on a non-GAAP basis to show earnings excluding certain items presented below. We believe this supplemental financial information enhances an investor’s understanding of our financial performance as it excludes those items which impact comparability of operating trends. The non-GAAP financial information should not be considered in isolation or viewed as a substitute for net income, cash flow from operations, diluted earnings per common share or other measures of performance as defined by GAAP. Moreover, the inclusion of non-GAAP financial information as used herein is not necessarily comparable to other similarly titled measures of other companies due to the potential inconsistencies in the method of presentation and items considered. The following tables set forth the supplemental financial information and the reconciliation of GAAP disclosures to non-GAAP financial measures (in thousands, except diluted earnings per share):

Fiscal Year | |||||||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

Net (loss) income (GAAP) | $ | (37,323 | ) | $ | (37,897 | ) | $ | 3,780 | $ | 30,850 | $ | 16,642 | |||||||

Loss from discontinued operations, net of tax benefit of $4,228 and $5,237, respectively (GAAP)(a) | — | — | — | 7,003 | 8,574 | ||||||||||||||

(Loss) income from continuing operations (GAAP) | (37,323 | ) | (37,897 | ) | 3,780 | 37,853 | 25,216 | ||||||||||||

Business acquisition costs (pretax)(b) | 9,059 | — | — | — | — | ||||||||||||||

South Hill distribution center closure (pretax)(c) | 828 | — | — | — | — | ||||||||||||||

Pension settlement (pretax)(d) | 438 | — | 748 | — | — | ||||||||||||||

Store closures, impairments and other strategic initiatives (pretax)(e) | 2,608 | 21,256 | 12,186 | — | — | ||||||||||||||

Severance charges associated with workforce reductions (pretax)(f) | — | 1,632 | 1,885 | — | — | ||||||||||||||

Consolidation of corporate headquarters (pretax)(g) | — | 110 | 3,538 | — | — | ||||||||||||||

South Hill Consolidation related charges (pretax)(h) | — | — | — | — | 23,789 | ||||||||||||||

Income tax impact of above adjustments(i) | (4,979 | ) | (9,179 | ) | (5,955 | ) | — | (9,019 | ) | ||||||||||

Valuation allowance on net deferred tax assets(j) | 6,077 | — | — | — | — | ||||||||||||||

Tax Act(k) | 255 | — | — | — | — | ||||||||||||||

Adjusted net income (loss) (non-GAAP) | $ | (23,037 | ) | $ | (24,078 | ) | $ | 16,182 | $ | 37,853 | $ | 39,986 | |||||||

Diluted (loss) earnings per share (GAAP) | $ | (1.37 | ) | $ | (1.40 | ) | $ | 0.12 | $ | 0.96 | $ | 0.51 | |||||||

Loss from discontinued operations (GAAP)(a) | — | — | — | (0.22 | ) | (0.26 | ) | ||||||||||||

Diluted (loss) earnings per share from continuing operations (GAAP) | (1.37 | ) | (1.40 | ) | 0.12 | 1.18 | 0.77 | ||||||||||||

Business acquisition costs (pretax)(b) | 0.33 | — | — | — | — | ||||||||||||||

South Hill distribution center closure (pretax)(c) | 0.03 | — | — | — | — | ||||||||||||||

Pension settlement (pretax)(d) | 0.02 | — | 0.02 | — | — | ||||||||||||||

Store closures, impairments and other strategic initiatives (pretax)(e) | 0.09 | 0.78 | 0.39 | — | — | ||||||||||||||

Severance charges associated with workforce reductions (pretax)(f) | — | 0.06 | 0.06 | — | — | ||||||||||||||

Consolidation of corporate headquarters (pretax)(g) | — | — | 0.11 | — | — | ||||||||||||||

South Hill Consolidation related charges (pretax)(h) | — | — | — | — | 0.73 | ||||||||||||||

Income tax impact of above adjustments(i) | (0.18 | ) | (0.33 | ) | (0.19 | ) | — | (0.28 | ) | ||||||||||

Valuation allowance on net deferred tax assets(j) | 0.22 | — | — | — | — | ||||||||||||||

Tax Act(k) | 0.01 | — | — | — | — | ||||||||||||||

Adjusted diluted (loss) earnings per share (non-GAAP) | $ | (0.85 | ) | $ | (0.89 | ) | $ | 0.51 | $ | 1.18 | $ | 1.22 | |||||||

24

Fiscal Year | |||||||||||

2017 | 2016 | 2015 | |||||||||

Net (loss) income (GAAP) | $ | (37,323 | ) | $ | (37,897 | ) | $ | 3,780 | |||

Interest expense | 7,680 | 5,051 | 2,977 | ||||||||

Income tax (benefit) expense | (13,068 | ) | (25,166 | ) | 1,815 | ||||||

EBIT (Non-GAAP) | (42,711 | ) | (58,012 | ) | 8,572 | ||||||

Business acquisition costs (pretax)(b) | 9,059 | — | — | ||||||||

South Hill distribution center closure (pretax)(c) | 828 | — | — | ||||||||

Pension settlement charge (pretax)(d) | 438 | — | 748 | ||||||||

Store closures, impairments and other (pretax)(e) | 2,608 | 21,256 | 12,186 | ||||||||

Severance charges associated with workforce reduction (pretax)(f) | — | 1,632 | 1,885 | ||||||||

Consolidation of corporate headquarters (pretax)(g) | — | 110 | 3,538 | ||||||||

Adjusted EBIT (non-GAAP) | $ | (29,778 | ) | $ | (35,014 | ) | $ | 26,929 | |||

(a) Discontinued operations reflect the results of Steele’s, which was divested in 2014. |

(b) Reflects acquisition and integration related costs associated with the Gordmans Acquisition (see Note 15 to the consolidated financial statements). |

(c) Reflects charges associated with the closure of our distribution center in South Hill, Virginia. |

(d) Reflects non-cash charges as a result of pension lump sum distributions exceeding interest cost. |

(e) Charges in 2017 reflect impairment charges and store closure costs. Charges in 2016 reflect impairment charges recognized as a result of deteriorating operating performance of our stores and costs related to our strategic store closure plan and other initiatives announced in 2015. Charges in 2015 reflect our strategic store closure plan, and primarily consist of impairment charges, as well as fixture moving costs and lease termination charges and other strategic initiatives. |