Form 6-K SIERRA WIRELESS INC For: Dec 31

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of the

Securities Exchange Act of 1934

For the Month of March 2018

(Commission File. No. 000-30718).

SIERRA WIRELESS, INC.

(Translation of registrant’s name in English)

13811 Wireless Way

Richmond, British Columbia, Canada V6V 3A4

(Address of principal executive offices and zip code)

Registrant’s Telephone Number, including area code: 604-231-1100

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F:

Form 20-F | o | 40-F | ý | |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes: | o | No: | ý | |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes: | o | No: | ý | |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Sierra Wireless, Inc. | ||

By: | /s/ David G. McLennan | |

David G. McLennan, Chief Financial Officer and Secretary | ||

Date: March 7, 2018 | ||

INCORPORATION BY REFERENCE

This Report on Form 6-K is incorporated by reference into the Registration Statement on Form S-8 of the registrant, which was filed with the Securities and Exchange Commission on March 31, 2016 (File No. : 333-210315).

Sierra Wireless, Inc.

Financial Highlights

(Expressed in thousands of United States dollars, except as otherwise stated)

(Prepared in accordance with United States generally accepted accounting principles ("U.S. GAAP"))

Consolidated Statement of Operations Data

Years ended December 31, | 2017 | 2016 | 2015 | ||||||||

GAAP results | |||||||||||

Revenue | $ | 692,077 | $ | 615,607 | $ | 607,798 | |||||

Gross margin percentage | 33.9 | % | 35.4 | % | 31.9 | % | |||||

Total expenses | 235,306 | 196,395 | 183,741 | ||||||||

Earnings (loss) from operations | (359 | ) | 21,348 | 10,114 | |||||||

Net earnings (loss) | 4,135 | 15,385 | (2,674 | ) | |||||||

Basic and diluted net earnings (loss) per share (in dollars) | $ | 0.13 | $ | 0.48 | $ | (0.08 | ) | ||||

Non-GAAP results(1) | |||||||||||

Gross margin percentage | 34.0 | % | 33.3 | % | 32.0 | % | |||||

Total expenses | $ | 196,254 | $ | 174,991 | $ | 162,141 | |||||

Earnings from operations | 39,177 | 30,127 | 32,361 | ||||||||

Adjusted EBITDA | 54,194 | 43,919 | 42,911 | ||||||||

Net earnings | 34,136 | 21,969 | 25,774 | ||||||||

Basic and diluted net earnings per share (in dollars) | $ | 1.04 | $ | 0.68 | $ | 0.80 | |||||

Free cash flow | $ | (16,734 | ) | $ | 28,648 | $ | 1,724 | ||||

Revenue by segment | |||||||||||

OEM Solutions | $ | 555,887 | $ | 516,517 | $ | 523,366 | |||||

Enterprise Solutions | 101,535 | 71,486 | 63,072 | ||||||||

IoT Services | 34,655 | 27,604 | 21,360 | ||||||||

$ | 692,077 | $ | 615,607 | $ | 607,798 | ||||||

Revenue by geographical region | |||||||||||

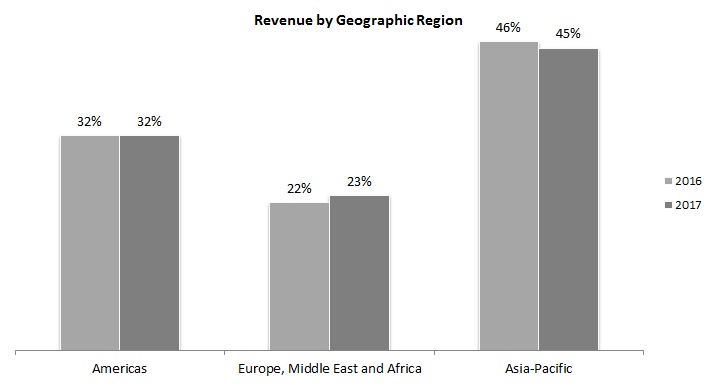

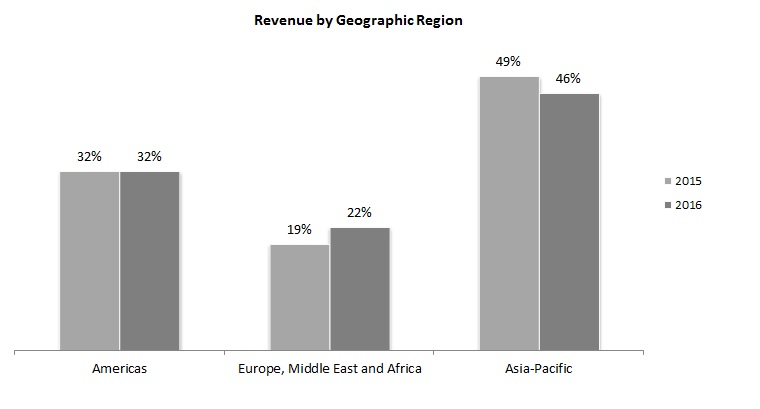

Americas | 32 | % | 32 | % | 32 | % | |||||

Europe, Middle East and Africa | 23 | % | 22 | % | 19 | % | |||||

Asia-Pacific | 45 | % | 46 | % | 49 | % | |||||

100 | % | 100 | % | 100 | % | ||||||

Consolidated Balance Sheet Data | |||||||||||

December 31, | 2017 | 2016 | 2015 | ||||||||

Cash and cash equivalents | $ | 65,003 | $ | 102,772 | $ | 93,936 | |||||

Long-term obligations | $ | 36,637 | $ | 32,654 | $ | 44,353 | |||||

Shareholders' equity | $ | 466,917 | $ | 361,584 | $ | 358,296 | |||||

Number of common shares outstanding | 35,861,510 | 31,859,960 | 32,337,201 | ||||||||

(1) Our non-GAAP financial measures exclude the impact of stock-based compensation expense and related social taxes, acquisition-related amortization, impairment, acquisition-related costs, integration costs, restructuring costs, certain other nonrecurring costs or recoveries, foreign exchange gains or losses on translation of balance sheet accounts, unrealized foreign exchange gains or losses on forward contracts, and certain tax adjustments. Adjusted EBITDA is defined as net earnings (loss) plus stock-based compensation expense and related social taxes, acquisition-related and integration costs, restructuring cost, impairment, certain other nonrecurring costs or recoveries, amortization, foreign exchange gains or losses on translation of certain balance sheet accounts, unrealized foreign exchange gains or losses on forward contracts, interest and income tax expense. Free cash flow is defined as cash flow from operating activities less capital expenditures and increases in intangibles. Non-GAAP financial measures do not have any standardized meaning prescribed by U.S. GAAP and therefore may not be comparable to similar measures presented by other companies. For further information, refer to "Non-GAAP Financial Measures" on page 31 of the Management's Discussion and Analysis in this Annual Report. | |||||||||||

Report to Shareholders

2017 was a strong year as revenue and profitability improved significantly. We also strengthened our strategic position in the Internet of Things (IoT) with the acquisition of Numerex just before year end.

Revenue in 2017 increased 12.4% to $692.1 million and adjusted EBITDA increased by 23.4% to $54.2 million on a year-over-year basis. Full year revenue in our OEM Solutions business increased 7.6% reflecting improved demand from existing customers and solid contribution from new programs. Enterprise Solutions revenue increased 42.0% in 2017, which included strong contributions from our telematics devices and AirLink networking solutions. Revenue in our IoT Services business (formerly Cloud and Connectivity Services) increased 25.5% in 2017 including a $3.1 million contribution from Numerex. Excluding revenue from Numerex, the organic growth rate in IoT Services was 14.2%. Our profitability improved year-over-year as non-GAAP earnings per share on a fully diluted basis rose 53% from $0.68 in 2016 to $1.04 in 2017.

On December 7, 2017 we closed the acquisition of Numerex, accelerating our IoT device-to-cloud strategy by adding established customers, proven solutions and recurring subscription-based revenue. The combination of Sierra Wireless and Numerex creates a clear global leader in IoT services and solutions. We are now deeply engaged in integration activities with a goal of capturing significant growth, cost and operational synergies.

Throughout the year, we launched many leading products across our lines of business, further bolstering our technology and market leadership position. Key product milestones achieved in 2017 included the launch of our first Ready to Connect devices with fully integrated Smart Connectivity and cloud management, industry leading Low Power Wide Area (LPWA) devices and the industry’s first LTE-Advanced Pro embedded cellular modules. Our new products and solutions address the needs of many emerging use cases and market segments in the IoT.

New customer program acquisition activity was solid in 2017 as we won numerous new programs across our three business segments, including the second largest design win in the company’s history with a large international automotive OEM customer.

As we look forward, we are the clear global leader in cellular connectivity solutions for the Internet of Things and our comprehensive product offering exposes us to a large and valuable market opportunity. We believe that we are better positioned than ever to capture a significant share of this opportunity. We also plan to continue to pursue acquisitions that support our device-to-cloud strategy and that help to accelerate long-term growth and value creation for our shareholders.

Jason W. Cohenour | ||

President and Chief Executive Officer | ||

Cautionary Note Regarding Forward-Looking Statements

Certain statements in this letter constitute forward-looking statements or forward-looking information and, in this regard, you should read carefully the "Cautionary Note Regarding Forward-Looking Statements" in the attached Management's Discussion & Analysis.

1

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS | |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS | |

OVERVIEW | |

Business Overview | |

Our Mission, Vision and Values | |

Our Strategy | |

Annual Overview - Financial Highlights | |

Outlook | |

CONSOLIDATED ANNUAL RESULTS OF OPERATIONS | |

Fiscal Year 2017 compared to Fiscal Year 2016 | |

Fiscal Year 2016 compared to Fiscal Year 2015 | |

SEGMENTED INFORMATION | |

FOURTH QUARTER OVERVIEW | |

SUMMARY OF QUARTERLY RESULTS OF OPERATIONS | |

LIQUIDITY AND CAPITAL RESOURCES | |

NON-GAAP FINANCIAL MEASURES | |

OFF-BALANCE SHEET ARRANGEMENTS | |

TRANSACTIONS BETWEEN RELATED PARTIES | |

CRITICAL ACCOUNTING POLICIES AND ESTIMATES | |

OUTSTANDING SHARE DATA | |

IMPACT OF ACCOUNTING PRONOUNCEMENTS AFFECTING CURRENT PERIOD | |

IMPACT OF ACCOUNTING PRONOUNCEMENTS AFFECTING FUTURE PERIODS | |

DISCLOSURE CONTROLS AND PROCEDURES | |

INTERNAL CONTROL OVER FINANCIAL REPORTING | |

LEGAL PROCEEDINGS | |

FINANCIAL RISK MANAGEMENT | |

RISKS AND UNCERTAINTIES | |

CONSOLIDATED FINANCIAL STATEMENTS | |

2

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) provides information for the years ended December 31, 2017, 2016 and 2015 and up to and including March 7, 2018. This MD&A should be read together with our audited consolidated financial statements and the accompanying notes for the year ended December 31, 2017 (“the consolidated financial statements”). The consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP” or "GAAP"). Except where otherwise specifically indicated, all amounts in this MD&A are expressed in United States dollars.

We have prepared this MD&A with reference to National Instrument 51-102 “Continuous Disclosure Obligations” of the Canadian Securities Administrators. Under the U.S./Canada Multijurisdictional Disclosure System, we are permitted to prepare this MD&A in accordance with the disclosure requirements of Canada, which requirements are different than those of the United States.

Certain statements in this MD&A constitute forward-looking statements or forward-looking information within the meaning of applicable securities laws. You should carefully read “Cautionary Note Regarding Forward-looking Statements” in this MD&A and should not place undue reliance on any such forward-looking statements.

Throughout this document, references are made to certain non-GAAP financial measures that are not measures of performance under U.S. GAAP. Management believes that these non-GAAP financial measures provide useful information to investors regarding the Company’s results of operations as they provide additional measures of its performance and assist in comparisons from one period to another. These non-GAAP financial measures do not have any standardized meaning prescribed by U.S. GAAP and are therefore unlikely to be comparable to similar measures presented by other issuers. These non-GAAP financial measures are defined and reconciled to their nearest GAAP measure in “Non-GAAP Financial Measures”.

In this MD&A, unless the context otherwise requires, references to "the Company", "Sierra Wireless", "we", "us" and "our" refer to Sierra Wireless, Inc. and its subsidiaries.

Additional information about the Company, including our most recent consolidated financial statements and our Annual Information Form, is available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

3

Cautionary Note Regarding Forward-looking Statements

This MD&A contains certain statements and information that are not based on historical facts and constitute forward-looking statements or forward-looking information within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and Canadian securities laws (collectively, “forward-looking statements”), including our business outlook for the short and longer term; statements regarding our strategy, plans and future operating performance; the Company’s liquidity and capital resources; the Company’s financial and operating objectives and strategies to achieve them; general economic conditions; expectations regarding the recent acquisition of Numerex Corp. ("Numerex"); estimates of our expenses, future revenues, non-GAAP earnings per share and capital requirements; our expectations regarding the legal proceedings we are involved in; statements with respect to the Company’s estimated working capital; expectations with respect to the adoption of IoT solutions; expectations in respect of our next generation Narrowband IoT; expectations regarding trends in the IoT market and wireless module market; expectations regarding product and price competition from other wireless device manufacturers and solution providers; and our ability to implement effective control procedures. Forward-looking statements are provided to help you understand our views of our short and longer term plans, expectations and prospects. We caution you that forward-looking statements may not be appropriate for other purposes.

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as “expects”, “is expected”, “anticipates”, “believes”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “potential”, “possible” or variations thereof or stating that certain actions, events, conditions or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements. Forward-looking statements are not promises or guarantees of future performance, they represent our current views and may change significantly. Forward-looking statements are based on a number of material assumptions, including, but not limited to, those listed below, which could prove to be significantly incorrect:

• | our ability to develop, manufacture and sell new products and services that meet the needs of our customers and gain commercial acceptance; |

• | our ability to continue to sell our products and services in the expected quantities at the expected prices and expected times; |

• | expected cost of goods sold; |

• | potential component supply constraints; |

• | our ability to win new business; |

• | our ability to integrate the business, operations and workforce of Numerex and to return the Numerex business to profitable growth and realize the expected benefits of the acquisition; |

• | our ability to integrate other acquired businesses and realize expected benefits; |

• | expected deployment of next generation networks by wireless network operators; |

• | our operations not being adversely disrupted by other developments, operating or regulatory risks; and |

• | expected tax rates and foreign exchange rates. |

4

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ significantly from those expressed or implied in our forward-looking statements, including, without limitation:

• | competition from new or established competitors or from those with greater resources; |

• | risks related to the recent acquisition of Numerex; |

• | disruption of, and demands on, our ongoing business and diversion of management's time and attention in connection with other acquisitions or divestitures; |

• | the loss of or significant demand fluctuations from any of our significant customers; |

• | cyber-attacks or other breaches of our information technology security; |

• | our financial results being subject to fluctuation; |

• | our ability to respond to changing technology, industry standards and customer requirements; |

• | our ability to attract or retain key personnel; |

• | risks related to infringement on intellectual property rights of others; |

• | our ability to obtain necessary rights to use software or components supplied by third parties; |

• | our ability to enforce our intellectual property rights; |

• | difficult or uncertain global economic conditions; |

• | our reliance on single source suppliers for certain components used in our products; |

• | failures of our products or services due to design flaws and errors, component quality issues, manufacturing defects or other quality issues; |

• | our dependence on a limited number of third party manufacturers; |

• | unanticipated costs associated with litigation or settlements; |

• | our dependence on mobile network operators to offer and promote acceptable wireless service programs; |

• | risks related to contractual disputes with counterparties; |

• | risks related to governmental regulation; |

• | risks related to the transmission, use and disclosure of user data and personal information; and |

• | risks inherent in foreign jurisdictions. |

This list is not exhaustive of the factors that may affect any of our forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and our actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to below under "Risks and Uncertainties" and those referred to in our other regulatory filings with the U.S. Securities and Exchange Commission (the "SEC") in the United States and the provincial securities commissions in Canada.

Our forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made, and we do not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations or opinions should change, except as required by applicable law. For the reasons set forth above, investors should not place undue reliance on forward-looking statements.

5

OVERVIEW

Business Overview

Sierra Wireless is an Internet of Things ("IoT") pioneer, empowering businesses and industries to transform and thrive in the connected economy. Customers start their IoT deployments with Sierra Wireless because we provide an integrated device-to-cloud solution comprised of embedded and networking solutions seamlessly connected with our IoT services. Original Equipment Manufacturers ("OEMs") and enterprises worldwide rely on our expertise in delivering fully-integrated solutions to reduce complexity, turn edge network data into intelligent decisions and get their connected products and services to market faster.

We operate our business under three reportable segments: (i) OEM Solutions; (ii) Enterprise Solutions; and (iii) IoT Services. Effective December 11, 2017, our former Cloud and Connectivity Services segment was renamed IoT Services to coincide with the acquisition of Numerex which is now included in our IoT Services segment.

OEM Solutions

As a leading embedded module vendor, we provide standards-based wireless technologies and support open source initiatives that help OEMs and system integrators get their products to market faster. We make it easy to embed cellular, Wi-Fi, Bluetooth and Global Navigation Satellite System ("GNSS") technologies, as well as manage connectivity, devices and data through our cloud platform. Our OEM Solutions segment includes embedded cellular modules, short range wireless modules, software and tools for OEM customers who integrate wireless connectivity into their products and solutions across a broad range of industries, including automotive, transportation, energy, enterprise networking, sales and payment, mobile computing, security, industrial monitoring, field services, smart home, healthcare and others. Within our OEM Solutions segment, our embedded wireless module product portfolio spans second generation ("2G"), third generation ("3G"), fourth generation ("4G") Long-Term Evolution ("LTE") and Low Power Wide Area ("LPWA") cellular technologies, short range modules focused on Bluetooth and Wi-Fi technologies and GNSS. Our broad product portfolio also includes cloud-based remote device and data management capability, as well as support for our embedded application framework called Legato which is an open source, Linux-based platform. We are also advancing our capabilities at the edge of the network to enable intelligent data orchestration through additional software that enhances our integrated IoT offering.

Enterprise Solutions

Our Enterprise Solutions segment provides secure networking solutions comprised of routers and gateways complemented by cloud-based or on-premise software for secure device and network management. Our networking solutions address a range of key segments within the mobility, industrial and enterprise markets.

Sierra Wireless AirLink gateways and routers have strong brand recognition with network operators, value added resellers and end customers. Our gateways and routers are known for their high reliability and technical capability in mission critical applications deployed in hostile environmental conditions. The gateways leverage Sierra Wireless' expertise in wireless technologies and offer the latest capabilities in LTE networking. The acquisition of GenX Mobile Incorporated ("GenX") in 2016 has added vehicle tracking (telematics) devices to our product portfolio, which are sold through large fleet management partners.

We sell our AirLink gateways and routers through channel partners in a two-tier distribution model worldwide. Our Enterprise Solutions team also includes a direct sales force and an expert technical team which engages with key customers in each of our target segments.

6

IoT Services

Our IoT Services segment enables the digital transformation of enterprises through integrated IoT services and comprises three main areas of operation: (i) our cloud services, which provide a secure and scalable cloud platform for deploying and managing IoT subscriptions, over-the-air updates, devices and applications; (ii) our global cellular connectivity services, which include our Smart SIM and core network platforms; and (iii) our managed broadband cellular services, which include a combination of hardware, high speed connectivity and cloud services. These cloud, connectivity and broadband services have been integrated to support our device-to-cloud strategy and enable worldwide IoT deployments by our customers. Our solution makes it simple to rapidly build and scale IoT applications while de-risking the deployment process. Sierra Wireless offers the broadest array of cloud and connectivity services to connect customers to the mobile network, manage devices and power their IoT services.

Our AirVantage cloud platform is used to collect, manage and process data from any number of connected devices. It allows our customers to centrally deploy and monitor IoT devices at the edge of the network, including configuring device settings and delivering firmware and embedded application updates remotely over the air. Our connectivity services offering, which includes our flexible Smart SIM technology, utilizes global, multi-operator subscriptions with unique benefits for IoT deployments including quality of service improvements and multi-operator network coverage. Our managed broadband services provide network connectivity solutions for distributed enterprises utilizing cellular broadband gateways, routers and advanced antennas.

We significantly advanced our device-to-cloud capabilities in 2015 by completing three acquisitions and rapidly expanding our IoT services business. These acquisitions included: Wireless Maingate AB ("Maingate"), a Sweden-based provider of IoT connectivity and data management services; Accel Networks LLC ("Accel"), a provider of secure managed cellular broadband connectivity services for distributed enterprises in North America and MobiquiThings SAS ("MobiquiThings"), a France-based mobile virtual network operator providing intelligent global connectivity services to the IoT marketplace. These businesses have been integrated into our IoT services segment, which now also includes the operations of Numerex, described below.

Acquisition of Numerex

On December 7, 2017, in accordance with the terms of the Agreement and Plan of Merger (the "Merger Agreement"), dated as of August 2, 2017, we acquired all of the outstanding shares of Numerex in a stock-for-stock merger transaction (the "Transaction") whereby Numerex stockholders received a fixed exchange ratio of 0.18 common shares of Sierra Wireless for each share of Numerex common stock. On closing of the Transaction, Sierra Wireless issued 3,580,832 common shares as merger consideration in exchange for all of the outstanding shares of Numerex common stock and certain outstanding Numerex equity awards and warrants. Concurrent with closing, approximately $20.2 million in the aggregate was paid to retire outstanding Numerex debt for total consideration of $97.5 million.

Numerex is a provider of enterprise solutions enabling IoT deployments. Numerex’s solutions produce new revenue streams and create operating efficiencies for its customers. Numerex provides its technology and services through its integrated platforms, which are generally sold on a subscription basis. Numerex offers a portfolio of managed end-to-end IoT solutions including smart devices, network connectivity and service applications capable of addressing the needs of a wide spectrum of vertical markets and industrial customers. Numerex’s mission is to empower enterprise operations with world-class, managed IoT solutions that are simple, scalable, and secure. We expect the acquisition of Numerex to expand our position as a leading global IoT pure-play and significantly increase our subscription-based recurring services revenue.

Numerex is now a wholly owned subsidiary of Sierra Wireless and its operations are being integrated with those of our IoT Services segment. For the period from December 8, 2017 to December 31, 2017, the results of the operations of Numerex have been consolidated into the Company's results and the balance sheet of Numerex as at

7

December 31, 2017 is consolidated with the balance sheet of Sierra Wireless. Numerex contributed $3.1 million in revenue and incurred a $1.5 million operating loss during the period from December 8, 2017 to December 31, 2017.

Other Acquisitions in 2017

During the second quarter, we acquired the technology assets of Flow Search Corp. ("FlowThings"), a small start-up based in Brooklyn, New York for total cash consideration of $0.2 million. The assets acquired provide a data orchestration platform for rapid application development at the edge and in the cloud. We believe this platform and the hiring of the FlowThings research and development ("R&D") team will help strengthen our device-to-cloud offering and accelerate time-to-market for our customers.

On March 31, 2017, we completed the acquisition of substantially all of the assets of the GNSS embedded module business of GlobalTop Technology Inc. ("GlobalTop") for total cash consideration of $3.1 million. GlobalTop is a Taiwan-based business that specializes in the development and manufacture of a wide variety of embedded GNSS modules and serves OEM customers around the world. GlobalTop's products and technologies are complementary to our OEM Solutions portfolio. The acquisition builds on our strategy to expand our embedded solution portfolio for OEM customers in the key IoT markets we serve.

We continue to seek opportunities to acquire or invest in businesses, products and technologies that help us drive our strategy forward and expand our position in the IoT market.

Our Mission, Vision and Values

Our mission is to be the IoT partner of choice for wireless device-to-cloud solutions and our vision is to empower businesses to reimagine their future in the connected world. Our core values are:

• | Innovation: We develop intelligent wireless solutions based on superior technology that provides value to our customers. |

• | Execution: We deliver on our commitments together as a team, and focus on quality and excellence in everything we do. |

• | Trust: We are responsive and collaborative with our customers to help them grow their businesses. |

8

Our Strategy

The global IoT market is growing significantly and new IoT applications are helping people and organizations to increase productivity, save energy costs, create new business models and provide value-added services to their customers. An integral factor in the growth of IoT applications is cellular connectivity, which enables the transmission of data from connected devices and machines, through advanced mobile networks and cloud services, to the enterprise or consumer. Cellular connectivity supports applications such as the connected car, the connected enterprise and the connected factory, as well as smart cities and the smart grid. Adoption of IoT solutions is driven by a number of factors including lower wireless connectivity costs, higher wireless connection speeds, new wireless technologies designed specifically for the IoT, new tools to simplify application development and higher levels of focus on data analytics, artificial intelligence and machine learning.

We believe these factors will continue to create attractive growth opportunities for the Company going forward. Based on third-party industry research, we are the global leader in embedded cellular wireless modules with 30% global market share (source: ABI Research, September 2017) and we are widely recognized as an innovation leader in the cellular IoT sector as well. We are also a leading provider of gateway and router solutions for industrial, enterprise and mobile applications, ranking as the worldwide market leader in shipment volume (source: IHS Research, December 2017). We have developed an IoT services platform that is tightly integrated with our devices and connectivity services.

Our corporate strategy is to drive growth and value creation by:

• | Solidifying our leadership position in IoT devices; |

• | Leveraging our leading position in IoT devices to build and scale our device-to-cloud solutions business; and |

• | Building a scalable company with the right systems, processes and talent to support our growth. |

In 2017, we continued to deliver on our corporate strategy by:

• | Launching our first embedded cellular modules for the LPWA market; |

• | Securing many new customer wins with global OEMs and enterprises, which significantly expanded our customer program pipeline; |

• | Closing and/or integrating a number of acquisitions including Numerex, GlobalTop and Blue Creation; |

• | Delivering on our Smart SIM technology, which enables Sierra Wireless to deliver highly differentiated connectivity services; and |

• | Strengthening our broader organizational capability, including new leadership for our IoT Services segment and additional go-to-market resources to support our continued revenue growth. |

We continue to seek opportunities to acquire or invest in businesses, products and technologies that accelerate our strategy and growth.

9

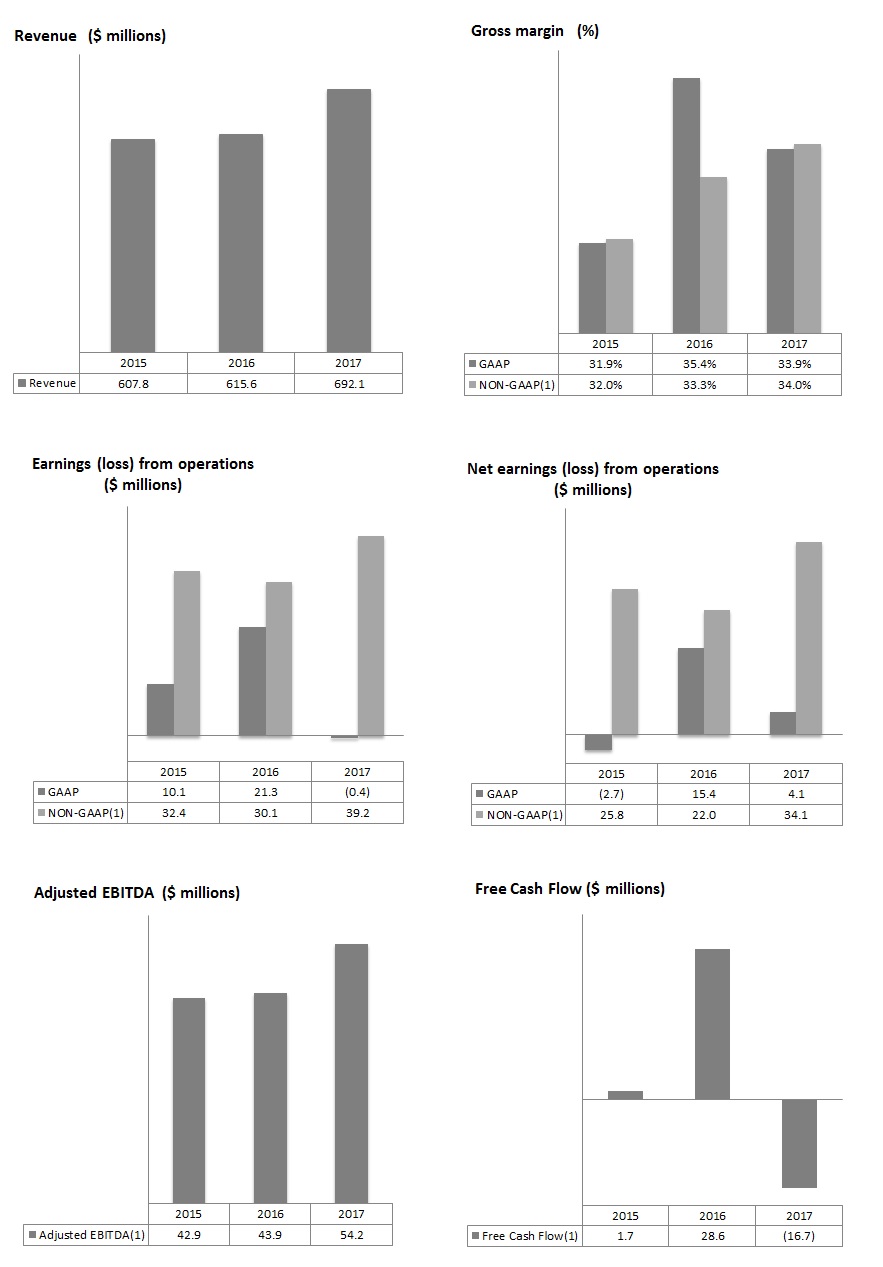

Annual Overview — Financial Highlights

Our 2017 revenue was $692.1 million, up from $615.6 million in 2016. The increase in revenue was driven by solid year-over-year growth in each of our three reportable segments: our OEM Solutions segment experienced growth from automotive and enterprise customers (including mobile computing); our Enterprise Solutions segment revenues grew as a result of the acquired GenX business and the continuing ramp of new AirLink gateway and router products; and our IoT Services segment revenues grew as a result of subscriber expansion.

Gross margin was 33.9% in 2017 compared to 35.4% in 2016. In 2016, gross margin was favorably impacted by a change in estimate of our Intellectual Property ("IP") royalty accrual ("Change in Estimate") (see Royalty obligations under "Critical Accounting Policies and Estimates" below) and two legal settlements. On a comparable year-over-year basis these items added 210 basis points to gross margin in 2016 compared to 2017. In 2017, gross margin benefited from product cost reductions that were partially offset by unfavorable product mix.

Net earnings decreased in 2017 compared to the prior year due to the above mentioned Change in Estimate, higher operating expenses driven by growth in the business, the added cost structure of acquired businesses, transaction and integration costs associated with acquisitions and an asset impairment, partially offset by foreign exchange gains on balance sheet items and lower income taxes.

Foreign exchange rate changes in 2017 increased our foreign currency denominated revenue by $0.9 million and operating expenses by $1.6 million compared to 2016.

GAAP

• | Revenue increased by $76.5 million, or 12.4%, compared to 2016. |

• | Gross margin was 33.9%, down 150 basis points from 2016. |

• | Loss from operations was $0.4 million compared to earnings from operations of $21.3 million in 2016. |

• | Net earnings decreased by $11.3 million, or $0.35 per share, compared to 2016. |

• | Cash and cash equivalents were $65.0 million at the end of the year, down $37.8 million compared to December 31, 2016, primarily reflecting usage of cash for working capital, and acquisition-related activities which included approximately $20.2 million for retiring outstanding Numerex debt. |

Non-GAAP(1)

• | Gross margin was 34.0%, up 70 basis points from 2016 as a result of component cost savings and lower manufacturing costs, partially offset by unfavorable product mix within our Enterprise Solutions segment. |

• | Operating earnings increased by $9.1 million, or 30.0%, compared to 2016, as a result of higher revenue and gross margin, partially offset by higher operating expenses driven by growth in the business and the added cost structure of acquired businesses. |

• | Adjusted EBITDA increased by $10.3 million, or 23.4%, compared to 2016. |

• | Net earnings increased by $12.2 million, or 55.4%, compared to 2016, mainly driven by growth in the business and lower income taxes. |

(1)Non-GAAP financial measures exclude the impact of stock-based compensation expense and related social taxes, acquisition-related amortization, impairment, acquisition-related costs, integration costs, restructuring costs, certain other nonrecurring costs or recoveries, foreign exchange gains or losses on translation of balance sheet accounts, unrealized foreign exchange gains or losses on forward contracts and certain tax adjustments. Refer to the section titled "Non-GAAP Financial Measures" for additional details and reconciliations to the applicable GAAP financial measures.

10

Select Annual Financial Highlights

(1)Non-GAAP financial measures exclude the impact of stock-based compensation expense and related social taxes, acquisition-related amortization, impairment, acquisition-related costs, integration costs, restructuring costs, certain other nonrecurring costs or recoveries, foreign exchange gains or losses on translation of balance sheet accounts, unrealized foreign gains or losses on forward contracts and certain tax adjustments. Refer to the section titled "Non-GAAP Financial Measures" for additional details and reconciliations to the applicable GAAP financial measures.

11

Selected Annual Financial information:

(In thousands of U.S. dollars, except where otherwise stated) | 2017 | 2016 | 2015 | |||||||||

Statement of Operations data: | ||||||||||||

Revenue | $ | 692,077 | $ | 615,607 | $ | 607,798 | ||||||

Gross Margin | ||||||||||||

- GAAP | $ | 234,947 | $ | 217,743 | $ | 193,855 | ||||||

- Non-GAAP (1) | 235,431 | 205,118 | 194,502 | |||||||||

Gross Margin % | ||||||||||||

- GAAP | 33.9 | % | 35.4 | % | 31.9 | % | ||||||

- Non-GAAP (1) | 34.0 | % | 33.3 | % | 32.0 | % | ||||||

Earnings (loss) from operations | ||||||||||||

- GAAP | $ | (359 | ) | $ | 21,348 | $ | 10,114 | |||||

- Non-GAAP (1) | 39,177 | 30,127 | 32,361 | |||||||||

Adjusted EBITDA | $ | 54,194 | $ | 43,919 | $ | 42,911 | ||||||

Net earnings (loss) | ||||||||||||

- GAAP | $ | 4,135 | $ | 15,385 | $ | (2,674 | ) | |||||

- Non-GAAP (1) | 34,136 | 21,969 | 25,774 | |||||||||

Revenue by Segment: | ||||||||||||

OEM Solutions | $ | 555,887 | $ | 516,517 | $ | 523,366 | ||||||

Enterprise Solutions | 101,535 | 71,486 | 63,072 | |||||||||

IoT Services | 34,655 | 27,604 | 21,360 | |||||||||

Share and per share data: | ||||||||||||

Basic and diluted earnings (loss) per share (in dollars) | ||||||||||||

- GAAP | $ | 0.13 | $ | 0.48 | $ | (0.08 | ) | |||||

- Non-GAAP (1) | $ | 1.04 | $ | 0.68 | $ | 0.80 | ||||||

Common shares (in thousands) | ||||||||||||

At period-end | 35,862 | 31,860 | 32,337 | |||||||||

Weighted average - basic | 32,356 | 32,032 | 32,166 | |||||||||

Weighted average - diluted | 32,893 | 32,335 | 32,166 | |||||||||

Balance sheet data (end of period): | ||||||||||||

Cash and cash equivalents | $ | 65,003 | $ | 102,772 | $ | 93,936 | ||||||

Total assets | 689,106 | 578,459 | 546,332 | |||||||||

Total long-term obligations | 36,637 | 32,654 | 44,353 | |||||||||

(1)Non-GAAP financial measures exclude the impact of stock-based compensation expense and related social taxes, acquisition-related amortization, impairment, acquisition-related costs, integration costs, restructuring costs, certain other nonrecurring costs or recoveries, foreign exchange gains or losses on translation of balance sheet accounts, unrealized foreign exchange gains or losses on forward contracts and certain tax adjustments. Refer to the section titled "Non-GAAP Financial Measures" for additional details and reconciliations to the applicable GAAP financial measures.

See discussion under “Consolidated Annual Results of Operations” for factors that have caused period to period variations.

12

Key highlights for the year ended December 31, 2017:

• | We entered into a joint business relationship with PwC Canada to help enterprises around the world develop and launch transformative IoT services and new business models. |

OEM Solutions

• | Volkswagen selected our AirPrime AR Series modules with our Legato embedded software platform for its next generation of connected cars. Our automotive solutions will deliver high-speed cellular connectivity for the Volkswagen Car-Net platform. |

• | We were recently selected by Nauto, Inc. ("Nauto") as the wireless connectivity solution for the North American launch of Nauto's flagship artificial intelligence-powered auto network. |

• | We launched the world's first 'plug-and-play' cellular modules and routers with pre-integrated global connectivity, IoT operation management and security. |

• | We delivered early modules for Telstra Corporation Limited's upcoming LTE Cat-M1 network to Landis+Gyr, enabling their industry-first live Cat-M1 smart meter trial. |

• | We announced one of the industry's first global, dual-mode LPWA cellular modules. Our AirPrime WP77 smart wireless modules simplify LPWA deployments for customers developing products that need to seamlessly connect to different LPWA technologies. |

• | In collaboration with industry leaders and developers, we announced mass-market availability of the mangOH Red open-source hardware platform to drive the next phase of IoT commercialization. |

• | We announced the industry's first global LTE-Advanced Pro cellular modules, enabling the world's fastest IoT applications for the mobile computing, networking, and industrial segments. |

• | We announced the BX Series Wi-Fi and Bluetooth combo modules with built-in cloud services and security features. The AirPrime BX Series now provides AirVantage cloud services and secure boot in our CF3 form factor to enable scalable Wi-Fi/Bluetooth solutions optimized for industrial IoT applications. |

• | Testing is underway for our next-generation Narrowband IoT ("NB-IoT") embedded cellular modules which are expected to be certified for T-Mobile's NB IoT network in early 2018. |

• | Recently, our mangOH Red open source hardware platform has been recognized with the IoT Breakthrough Award for IoT Development Tool of the Year. |

• | We announced the industry's smallest, lowest power, multi-mode LPWA cellular modules targeted at rapidly growing markets in asset tracking and connected industrial equipment, smart city, healthcare, agriculture and wearables. |

Enterprise Solutions

• | We announced that our industry-leading AirLink MP70 LTE-Advanced vehicle routers now support the most advanced, integrated vehicle telemetry, inertial navigation, and driver behavior features to improve fleet operations and vehicle maintenance. |

• | We signed a distribution agreement with Ingram Micro Inc., one of the largest technology distributors in the world. Through this agreement, Ingram Micro is authorized to distribute our complete AirLink |

13

portfolio of networking solutions, including cellular routers, gateways, and management services to its channel partners in the United States.

• | We announced the release of the AirLink Connection Manager (ACM) 2.0 VPN appliance for vehicle networking use cases. |

IoT Services

• | We announced support for Google Cloud IoT Core, a fully managed service that allows users to easily and securely connect and manage devices at global scale, through integration of our AirVantage IoT Platform with Google Could services. |

• | We announced that Nube has selected our device-to-cloud IoT solution and Microsoft Azure Cloud Services to reinvent consumer gas delivery. |

Outlook

In the first quarter of 2018, we expect revenue to be in the range of $181 million to $189 million and non-GAAP earnings per share to be in the range of $0.04 to $0.10. Our guidance for the first quarter of 2018 includes a full quarter of Numerex following the acquisition of the company on December 7, 2017. We expect the first quarter of 2018 to be impacted by some unusual and mainly non-recurring items, including higher one-time costs related to a Numerex network upgrade and customer migration, and tight component supply constraining revenue and adding to cost of goods sold.

Additionally, with the integration of Numerex, we have commenced various efficiency and effectiveness initiatives. These initiatives are focused on capturing synergies as we integrate Numerex and efficiency gains in other areas of our business. The initiatives being undertaken are expected to reduce cost of goods sold, as well as on-going operating expenses. As a result of implementing these initiatives, we are targeting a quarterly non-GAAP operating expense run rate of $56.5 million in the fourth quarter of 2018, down from approximately $59 million in non-GAAP operating expense that is included in our guidance for the first quarter of 2018. We expect these initiatives will result in a one-time non-GAAP restructuring charge of approximately $4.5 million.

We believe that the market for wireless IoT solutions has strong long-term growth prospects. We anticipate strong long-term growth in the number of devices being wirelessly connected, driven by key enablers, such as lower wireless connectivity costs, faster wireless connection speeds, new wireless technologies designed specifically for the IoT, new devices and tools to simplify the development of IoT applications, and increased focus and investment from large ecosystem players. More importantly, we see emerging customer demand in many of our target verticals driven by increasing recognition of the value created by deploying IoT solutions, such as new revenue streams and cost efficiencies.

14

Key factors that we expect will affect our results in the near term are:

• | the strength of our competitive position in the market; |

• | the timely ramp up of sales of our new products recently launched or currently under development; |

• | our ability to integrate Numerex's business, operations and workforce with ours and our ability to return the Numerex business to profitable growth and to realize the anticipated benefits of the acquisition; |

• | contributions to our operating results from the other acquisitions we completed in 2015, 2016 and 2017; |

• | the level of success our customers achieve with sales of connected solutions; |

• | fluctuations in customer demand and inventory levels, particularly large customers; |

• | our ability to manage component supply issues when they arise; |

• | our ability to attract and retain effective channel partners; |

• | the timely launch and ramp up of new customer programs; |

• | our ability to secure future design wins with both existing and new customers; |

• | the end-of-life of existing customer programs; |

• | manufacturing capacity at our various manufacturing sites; |

• | our ability to manage component and product quality compliance; |

• | fluctuations in foreign exchange rates; |

• | general economic conditions in the markets we serve; and |

• | seasonality in demand. |

We expect that product and price competition from other wireless device manufacturers and solution providers will continue to play a role in the IoT market. As a result of these factors, we may experience volatility in our results on a quarter-to-quarter basis. Gross margin percentage may fluctuate from quarter-to-quarter depending on product and customer mix, average selling prices and product costs.

See "Cautionary Note Regarding Forward-Looking Statements".

15

CONSOLIDATED ANNUAL RESULTS OF OPERATIONS

(In thousands of U.S. dollars, except where otherwise stated) | 2017 | 2016 | 2015 | |||||||||||||||||

$ | % of Revenue | $ | % of Revenue | $ | % of Revenue | |||||||||||||||

Revenue | 692,077 | 100.0 | % | 615,607 | 100.0 | % | 607,798 | 100.0 | % | |||||||||||

Cost of goods sold | 457,130 | 66.1 | % | 397,864 | 64.6 | % | 413,943 | 68.1 | % | |||||||||||

Gross margin | 234,947 | 33.9 | % | 217,743 | 35.4 | % | 193,855 | 31.9 | % | |||||||||||

Expenses | ||||||||||||||||||||

Sales and marketing | 75,594 | 10.9 | % | 64,242 | 10.4 | % | 54,144 | 8.9 | % | |||||||||||

Research and development | 83,361 | 12.0 | % | 73,077 | 11.9 | % | 74,020 | 12.2 | % | |||||||||||

Administration | 42,904 | 6.2 | % | 40,956 | 6.7 | % | 40,321 | 6.6 | % | |||||||||||

Restructuring | 1,076 | 0.2 | % | — | — | % | 951 | 0.2 | % | |||||||||||

Acquisition-related and integration | 8,195 | 1.2 | % | 843 | 0.1 | % | 1,945 | 0.3 | % | |||||||||||

Impairment | 3,668 | 0.5 | % | — | — | % | — | — | % | |||||||||||

Amortization | 20,508 | 3.0 | % | 17,277 | 2.8 | % | 12,360 | 2.0 | % | |||||||||||

235,306 | 34.0 | % | 196,395 | 31.9 | % | 183,741 | 30.2 | % | ||||||||||||

Earnings (loss) from operations | (359 | ) | (0.1 | )% | 21,348 | 3.5 | % | 10,114 | 1.7 | % | ||||||||||

Foreign exchange gain (loss) | 7,550 | (1,736 | ) | (11,843 | ) | |||||||||||||||

Other income | 67 | 83 | 115 | |||||||||||||||||

Earnings (loss) before income taxes | 7,258 | 19,695 | (1,614 | ) | ||||||||||||||||

Income tax expense | 3,123 | 4,310 | 1,060 | |||||||||||||||||

Net earnings (loss) | 4,135 | 15,385 | (2,674 | ) | ||||||||||||||||

Net earnings (loss) per share - basic and diluted (in dollars) | 0.13 | 0.48 | (0.08 | ) | ||||||||||||||||

16

Fiscal Year 2017 Compared to Fiscal Year 2016

Revenue

Revenue increased by $76.5 million, or 12.4%, in 2017 compared to 2016. The increase was driven by contributions from each of our three reportable segments which all experienced solid year-over-year growth:

• | OEM Solutions experienced notable year-over-year increases in automotive and enterprise segment module sales; |

• | Enterprise Solutions experienced a strong contribution from fleet management products and other mobile and industrial gateway products; and |

• | IoT Services experienced solid subscriber additions and contribution from Numerex which was acquired late in the year. |

Our geographic revenue mix for the years ended December 31, 2017 and 2016 was as follows:

During the years ended December 31, 2017 and 2016, no customer accounted for more than 10% of our aggregated revenue.

Gross margin

Gross margin was 33.9% of revenue in 2017, compared to 35.4% in 2016. In 2016 gross margin was favorably impacted by the Change in Estimate and two legal settlements. On a comparable year-over-year basis these items added 210 basis points to gross margin in 2016 compared to 2017. In 2017, gross margin benefited from product cost reductions that were partially offset by unfavorable product mix. Gross margin included stock-based compensation expense and related social taxes of $0.5 million and $0.4 million in 2017 and 2016, respectively.

Sales and marketing

Sales and marketing expenses increased by $11.4 million, or 17.7%, in 2017, compared to 2016, primarily as a result of targeted investments in our go-to-market capabilities to drive growth, costs added as a result of acquisitions and the unfavorable impact of foreign exchange. Sales and marketing expenses included stock-based compensation and related social taxes of $2.5 million in 2017, compared to $1.7 million in 2016.

Research and development

R&D expenses increased by $10.3 million, or 14.1%, in 2017, compared to 2016. The increase in R&D expenses was primarily due to costs associated with new product development programs, the unfavorable impact of foreign exchange and additional expenses added as a result of acquisitions.

17

R&D expenses included stock-based compensation and related social taxes of $2.0 million in 2017, compared to $1.4 million in 2016. R&D expenses also included acquisition-related amortization of $0.4 million in 2017, compared to $0.5 million in 2016.

Administration

Administration expenses increased by $1.9 million, or 4.8%, in 2017, compared to 2016, primarily due to higher stock-based compensation expense and the unfavorable impact of foreign exchange, partially offset by lower bad debt expense. Administration expenses included stock-based compensation expense and related social taxes of $5.3 million in 2017, compared to $4.1 million in 2016.

Restructuring

Restructuring costs were $1.1 million in 2017. These costs are related to the relocation of our IoT Services customer support operations from Sweden to France and the United States.

Acquisition-related and integration

Acquisition-related and integration costs increased by $7.4 million in 2017, compared to 2016. The increase was primarily due to the acquisition of Numerex, integration activities and higher accruals of acquisition-related contingent consideration.

Impairment

We recorded an impairment of $3.7 million related to an intangible asset recorded on the acquisition of Maingate. The resulting change, which was recorded in the first quarter of 2017, was due to the decision to terminate a service offering that has now been superseded by a more technologically advanced offering in our integrated IoT Services business.

Amortization

Amortization expense increased by $3.2 million, or 18.7%, in 2017, compared to 2016 primarily due to higher acquisition-related amortization. Amortization expense in 2017 included $15.1 million of acquisition-related amortization compared to $11.6 million in 2016.

Foreign exchange gain (loss)

Foreign exchange gain was $7.6 million in 2017, compared to a loss of $1.7 million in 2016. This gain was primarily the result of an increase in the value of the Euro compared to the U.S. dollar.

Income tax expense (recovery)

Income tax expense was $3.1 million in 2017, compared to $4.3 million in 2016. This decrease was due to a recovery related to the impairment charge in the first quarter of 2017 and a shift of earnings between jurisdictions.

Net earnings (loss)

Net earnings were $4.1 million in 2017, compared to $15.4 million in 2016. The decrease of $11.3 million in net earnings reflects decreased earnings from operations as a result of higher operating expenses driven by growth in the business, the added cost structure of acquired businesses, transaction and integration costs associated with acquisitions and an asset impairment, partially offset by foreign exchange gains on balance sheet items and lower income tax expense.

Net earnings in 2017 included stock-based compensation expense and related social taxes of $10.4 million and acquisition-related amortization of $15.1 million. Net earnings in 2016 included stock-based compensation expense and related social taxes of $7.6 million and acquisition-related amortization of $12.1 million.

18

Weighted average number of shares

The weighted average basic and diluted shares outstanding were 32.4 million and 32.9 million, respectively, for the year ended December 31, 2017 and 32.0 million and 32.3 million for the year ended December 31, 2016.

The number of shares outstanding was 35.9 million at December 31, 2017, compared to 31.9 million at December 31, 2016. The increase in the number of shares outstanding was primarily due to the shares issued for the acquisition of Numerex.

Fiscal Year 2016 Compared to Fiscal Year 2015

Revenue

Revenue increased by $7.8 million, or 1.3%, in 2016 compared to 2015. The increase was mainly driven by contributions from businesses acquired in 2016 and 2015 and higher revenues from our new Enterprise gateway products, partially offset by weaker revenues in our OEM Solutions segment.

Our geographic revenue mix for the years ended December 31, 2016 and 2015 was as follows:

During the years ended December 31, 2016 and 2015, no customer accounted for more than 10% of our aggregated revenue.

Gross margin

Gross margin was 35.4% of revenue in 2016, compared to 31.9% in 2015. The significant increase in gross margin was due to the favorable impact on cost of goods sold of the Change in Estimate, product cost reductions in our OEM Solutions segment, improved margins in our Enterprise Solutions segment and the favorable impact of cost recoveries as a result of two legal settlements received in the first half of 2016. Gross margin included stock-based compensation expense and related social taxes of $0.4 million and $0.6 million in 2016 and 2015, respectively.

Sales and marketing

Sales and marketing expenses increased $10.1 million, or 18.7%, in 2016, compared to 2015, primarily as a result of targeted investments to strengthen our go-to-market capability and costs added as a result of the acquisitions undertaken in 2015 and 2016. Sales and marketing expenses included stock-based compensation and related social taxes of $1.7 million in 2016, compared to $2.2 million in 2015.

19

Research and development

R&D expenses decreased by $0.9 million, or 1.3%, in 2016, compared to 2015. The decrease in R&D expenses was primarily due to lower costs related to development parts and certification fees, lower acquisition-related amortization costs and the favorable impact of foreign exchange. This was partially offset by higher compensation costs and additional expenses associated with acquired businesses.

R&D expenses included stock-based compensation and related social taxes of $1.4 million in 2016, compared to $1.5 million in 2015. R&D expenses also included acquisition-related amortization of $0.5 million in 2016, compared to $1.3 million in 2015.

Administration

Administration expenses increased by $0.6 million, or 1.6%, in 2016, compared to 2015, primarily due to higher compensation costs, including certain termination expenses, partially offset by lower professional fees, stock-based compensation expense and the favorable impact of foreign exchange. Administration expenses included stock-based compensation expense and related social taxes of $4.1 million in 2016, compared to $5.3 million in 2015.

Restructuring

Restructuring costs were $nil in 2016. Restructuring costs in 2015 were related to the implementation of a plan to realign responsibilities within our Enterprise Solutions segment to reflect the evolution of our business and to provide dedicated focus on our enterprise gateways and recently acquired IoT services businesses.

Acquisition-related and integration

Acquisition-related and integration costs decreased by $1.1 million in 2016, compared to 2015. The decrease was primarily due to the lower level of acquisition and integration activities and a decrease in the fair value of acquisition-related contingent consideration.

Amortization

Amortization expense increased by $4.9 million, or 39.8%, in 2016, compared to 2015 primarily due to higher acquisition-related amortization driven by the acquisitions undertaken in 2015 and reflects a change in the estimate of the useful life of some of our assets, including assets related to our office relocation in France. Amortization expense in 2016 included $11.6 million of acquisition-related amortization compared to $8.4 million in 2015.

Foreign exchange gain (loss)

Foreign exchange loss was $1.7 million in 2016, compared to a loss of $11.8 million in 2015. The foreign exchange loss in 2015 included the impact of an unrealized loss of $6.2 million on revaluation of a Euro denominated loan ("Intercompany Loan") to a self-sustaining subsidiary. We classified the Intercompany Loan as a net investment in a foreign subsidiary in the second quarter of 2015 when we determined the loan was permanent. As a result, the foreign exchange gain or loss from revaluation of the Intercompany Loan, since that time, is being recognized in other comprehensive income.

Income tax expense (recovery)

Income tax expense was $4.3 million in 2016, compared to $1.1 million in 2015. The additional expense was due to higher earnings and the impact of a shift of earnings between jurisdictions.

Net earnings (loss)

Net earnings were $15.4 million in 2016, compared to a net loss of $2.7 million in 2015. The increase in net earnings reflects improved earnings from operations as a result of the Change in Estimate and lower foreign exchange losses partially offset by higher income tax expenses.

20

Net earnings in 2016 included stock-based compensation expense and related social taxes of $7.6 million and acquisition-related amortization of $12.1 million. Net loss in 2015 included stock-based compensation expense and related social taxes of $9.7 million and acquisition-related amortization of $9.7 million.

Weighted average number of shares

The weighted average basic and diluted shares outstanding were 32.0 million and 32.3 million, respectively, for the year ended December 31, 2016 and 32.2 million for the year ended December 31, 2015.

The number of shares outstanding was 31.9 million at December 31, 2016, compared to 32.3 million at December 31, 2015. The decrease in the number of shares outstanding was primarily due to the impact of share repurchases made under our Normal Course Issuer Bid ("NCIB") program (refer to "Liquidity and Capital Resources" section below), partially offset by issuance of common shares as a result of stock option exercises and restricted share unit releases.

SEGMENTED INFORMATION

OEM Solutions

% change | ||||||||||||||||||

(In thousands of U.S. dollars, except where otherwise stated) | 2017 | 2016 | 2015 | 2017 vs 2016 | 2016 vs 2015 | |||||||||||||

Revenue | $ | 555,887 | $ | 516,517 | $ | 523,366 | 7.6 | % | (1.3 | )% | ||||||||

Cost of goods sold | 384,872 | 349,921 | 371,559 | 10.0 | % | (5.8 | )% | |||||||||||

Gross margin | $ | 171,015 | $ | 166,596 | $ | 151,807 | 2.7 | % | 9.7 | % | ||||||||

Gross margin % | 30.8 | % | 32.3 | % | 29.0 | % | ||||||||||||

Non-GAAP (1) | ||||||||||||||||||

Gross Margin | $ | 171,402 | $ | 154,988 | $ | 152,368 | 10.6 | % | 1.7 | % | ||||||||

Gross Margin % | 30.8 | % | 30.0 | % | 29.1 | % | ||||||||||||

(1) See section titled "Non-GAAP Financial Measures" for additional details and a reconciliation to the applicable GAAP financial measure.

Fiscal Year 2017 compared to 2016

Revenue increased by $39.4 million, or 7.6%, in 2017, compared to 2016. This increase was primarily due to strong demand from automotive and enterprise customers and programs.

In 2016, gross margin was favorably impacted by the Change in Estimate and a legal settlement. On a comparable year over year basis these items added 190 basis points to gross margin in 2016 compared to 2017. In 2017, gross margin benefited from product cost reductions that were partially offset by unfavorable product mix.

Our non-GAAP gross margin percentage of 30.8% increased in comparison to 2016 reflecting the impact of cost reduction programs, including lower manufacturing and component costs, partially offset by unfavorable product mix principally driven by the ramp up of a new high volume automotive program at lower gross margin which replaced an existing program that went end of life.

21

Fiscal Year 2016 compared to 2015

Revenue decreased by $6.8 million, or 1.3%, in 2016, compared to 2015. This decrease was primarily due to demand softness from certain established customers and programs, partially offset by contribution from new programs.

Higher gross margin percentage in 2016 compared to the prior year reflects a $12.9 million reduction of cost of goods sold, representing the portion of the Change in Estimate that is attributable to our OEM Solutions segment. In addition, our cost reduction initiatives during the year, together with the reimbursement of $1.9 million in certain legal costs pursuant to a favorable arbitration decision on a contract dispute with an IP licensor, of which $1.7 million was attributable to our OEM Solutions segment, also had a positive impact on the gross margin.

Our non-GAAP gross margin percentage of 30.0% excludes $11.7 million of the Change in Estimate attributable to OEM Solutions related to the one-time reduction in our accrued royalties obligations effective October 1, 2016. The $1.2 million balance of the Change in Estimate attributable to the OEM Solutions segment is included in non-GAAP gross margin as it relates to products sold during the fourth quarter of 2016.

Enterprise Solutions

% change | ||||||||||||||||||

(In thousands of U.S. dollars, except where otherwise stated) | 2017 | 2016 | 2015 | 2017 vs 2016 | 2016 vs 2015 | |||||||||||||

Revenue | $ | 101,535 | $ | 71,486 | $ | 63,072 | 42.0 | % | 13.3 | % | ||||||||

Cost of goods sold | 53,014 | 31,537 | 29,945 | 68.1 | % | 5.3 | % | |||||||||||

Gross margin | $ | 48,521 | $ | 39,949 | $ | 33,127 | 21.5 | % | 20.6 | % | ||||||||

Gross margin % | 47.8 | % | 55.9 | % | 52.5 | % | ||||||||||||

Non-GAAP (1) | ||||||||||||||||||

Gross Margin | $ | 48,593 | $ | 38,913 | $ | 33,192 | 24.9 | % | 17.2 | % | ||||||||

Gross Margin % | 47.9 | % | 54.4 | % | 52.6 | % | ||||||||||||

(1) See section titled "Non-GAAP Financial Measures" for additional details and a reconciliation to the applicable GAAP financial measure.

Fiscal Year 2017 compared to 2016

Revenue increased by $30.0 million, or 42.0%, in 2017, compared to 2016 mainly driven by revenue from fleet management products acquired from GenX in 2016 and the growth in sales of gateway products, including the RV50 and MG90, which were launched in the latter half of 2016 and ramped up during 2017.

Gross margin percentage decreased in 2017 in comparison to 2016. In 2016, gross margin was favorably impacted by the Change in Estimate and two legal settlements. On a comparable year over year basis these items added 390 basis points to gross margin in 2016 compared to 2017. In 2017, gross margin percentage was unfavorably impacted by the inclusion of lower margin fleet management revenues from GenX, partially offset by product cost reductions.

Our non-GAAP gross margin percentage of 47.9% decreased in comparison to 2016 because of the unfavorable product mix noted above.

22

Fiscal Year 2016 compared to 2015

Revenue increased by $8.4 million, or 13.3%, in 2016, compared to 2015 mainly driven by revenue from the acquisition of GenX and the impact of new AirLink gateway product introductions in 2016.

Gross margin increased in 2016, reflecting a $1.5 million reduction of cost of goods sold, representing the portion of the Change in Estimate that is attributable to our Enterprise Solutions segment. In addition, a $1.9 million recovery from a legal settlement with a supplier related to a component quality issue received in the first quarter of 2016 and improved product mix resulting from increased sales of higher margin gateway products, also had a positive impact on our Enterprise Solutions segment gross margin.

Our non-GAAP gross margin percentage of 54.4% excludes $1.3 million of the Change in Estimate attributable to Enterprise Solutions related to the one-time reduction in our accrued royalties obligations effective October 1, 2016. The $0.2 million balance of the Change in Estimate attributable to the Enterprise Solutions segment is included in non-GAAP gross margin as it relates to products sold during the fourth quarter of 2016.

IoT Services

% change | ||||||||||||||||||

(In thousands of U.S. dollars, except where otherwise stated) | 2017 | 2016 | 2015 | 2017 vs 2016 | 2016 vs 2015 | |||||||||||||

Revenue | $ | 34,655 | $ | 27,604 | $ | 21,360 | 25.5 | % | 29.2 | % | ||||||||

Cost of goods sold | 19,244 | 16,406 | 12,439 | 17.3 | % | 31.9 | % | |||||||||||

Gross margin | $ | 15,411 | $ | 11,198 | $ | 8,921 | 37.6 | % | 25.5 | % | ||||||||

Gross margin % | 44.5 | % | 40.6 | % | 41.8 | % | ||||||||||||

Non-GAAP (1) | ||||||||||||||||||

Gross Margin | $ | 15,436 | $ | 11,217 | $ | 8,942 | 37.6 | % | 25.4 | % | ||||||||

Gross Margin % | 44.5 | % | 40.6 | % | 41.9 | % | ||||||||||||

(1) See section titled "Non-GAAP Financial Measures" for additional details and a reconciliation to the applicable GAAP financial measure.

Fiscal Year 2017 compared to 2016

Revenue increased by $7.1 million, or 25.5%, in 2017, compared to 2016 as a result of continuing subscriber growth and the inclusion of Numerex revenue which was acquired late in the year.

Gross margin increased in 2017 due to favorable mix from cloud and connectivity services and the fact that there were several one-time charges to cost of sales in 2016 that reduced gross margin compared to 2017.

Fiscal Year 2016 compared to 2015

Revenue increased by $6.2 million, or 29.2%, in 2016, compared to 2015 mainly as a result of the inclusion of a full year of revenue resulting from the acquisitions of Maingate, MobiquiThings and Accel in 2015.

Gross margin percentage was slightly lower in 2016 due to the increased revenue impact of Accel's broadband services, which have gross margins that are lower than the average gross margin for IoT Services.

23

FOURTH QUARTER OVERVIEW

Consolidated Results of Operations:

Three months ended December 31, | ||||||||||||||

(in thousands of U.S. dollars, except where otherwise stated) | 2017 | 2016 | ||||||||||||

% of | % of | |||||||||||||

$ | Revenue | $ | Revenue | |||||||||||

Revenue | 183,533 | 100.0 | % | 163,021 | 100.0 | % | ||||||||

Cost of goods sold | 121,719 | 66.3 | % | 94,225 | 57.8 | % | ||||||||

Gross margin | 61,814 | 33.7 | % | 68,796 | 42.2 | % | ||||||||

Expenses | ||||||||||||||

Sales and marketing | 20,456 | 11.2 | % | 17,048 | 10.4 | % | ||||||||

Research and development | 21,828 | 11.9 | % | 18,047 | 11.1 | % | ||||||||

Administration | 11,379 | 6.2 | % | 9,708 | 6.0 | % | ||||||||

Restructuring | 245 | 0.1 | % | — | — | % | ||||||||

Acquisition-related and integration | 4,792 | 2.6 | % | 376 | 0.2 | % | ||||||||

Amortization | 6,073 | 3.3 | % | 4,372 | 2.7 | % | ||||||||

64,773 | 35.3 | % | 49,551 | 30.4 | % | |||||||||

Earnings (loss) from operations | (2,959 | ) | (1.6 | )% | 19,245 | 11.8 | % | |||||||

Foreign exchange gain (loss) | 1,267 | (3,547 | ) | |||||||||||

Other income | 38 | 2 | ||||||||||||

Earnings (loss) before income taxes | (1,654 | ) | 15,700 | |||||||||||

Income tax expense (recovery) | 1,876 | (18 | ) | |||||||||||

Net earnings (loss) | (3,530 | ) | 15,718 | |||||||||||

Net earnings (loss) per share - Basic and diluted (in dollars) | (0.11 | ) | 0.49 | |||||||||||

GAAP:

• | In the fourth quarter of 2017, revenue increased by $20.5 million, or 12.6%, compared to the same period of 2016 primarily as a result of higher sales of telematics devices, gateways and routers, module sales to automotive and enterprise customers and a contribution from Numerex, which we acquired on December 7, 2017. |

• | Gross margin was 33.7% in the fourth quarter of 2017, which represents a more normalized level compared to the same period of 2016 when gross margin of 42.2% was favorably impacted as a result of a $13.0 million (800 basis point) reduction of cost of goods sold as a result of the Change in Estimate effective October 1, 2016. In the fourth quarter of 2017, gross margin was slightly lower than the normalized 2016 gross margin due to unfavorable mix in our OEM segment driven by the ramp up of a new high volume automotive program at lower gross margin which replaced a previous program and in our Enterprise segment driven by lower gross margin from telematics products, partially offset by favorable mix due to a larger IoT Services contribution. |

• | Earnings from operations decreased by $22.2 million in the fourth quarter of 2017 compared to the fourth quarter of 2016 as a result of lower gross margin, higher operating expenses as a result of continued targeted investments in our go-to-market capabilities, the impact of unfavorable foreign exchange on operating expenses and added costs as a result of recent acquisitions. |

24

• | Net earnings decreased by $19.2 million in the fourth quarter of 2017, compared to the fourth quarter of 2016. Lower operating income in the fourth quarter of 2017 was partially offset by foreign exchange gains on balance sheet items, partially offset by higher income tax expense. |

• | Cash and cash equivalents at the end of the fourth quarter of 2017 were $65.2 million, a decrease of $9.0 million compared to $74.2 million at the end of the third quarter of 2017. The decrease in cash was mainly due to the acquisition of Numerex and capital expenditures, partially offset by cash flows from operating activities. |

NON-GAAP(1):

• | Gross margin was 33.8% in the fourth quarter of 2017, compared to 34.3% in the fourth quarter of 2016. The decrease in gross margin was primarily attributable to the impact of unfavorable mix in our OEM segment driven by the ramp up of a new high volume automotive program at lower gross margin which replaced a previous program that went end of life and lower gross margin from telematics products in our Enterprise segment, partially offset by favorable mix due to a larger IoT Services contribution. |

• | Earnings from operations decreased by $2.3 million compared to the fourth quarter of 2016 due to higher operating expenses, partially offset by higher revenues and gross margin. |

• | Adjusted EBITDA decreased by $1.5 million compared to the fourth quarter of 2016. This decrease mainly reflects lower earnings from operations and higher amortization expense in the fourth quarter of 2017. |

• | Net earnings increased by $0.4 million, compared to the fourth quarter of 2016. This increase was mainly due to lower income tax expense partially offset by the lower earnings from operations. |

(1)Non-GAAP financial measures exclude the impact of stock-based compensation expense and related social taxes, acquisition-related amortization, impairment, acquisition-related costs, integration costs, restructuring costs, certain other nonrecurring costs or recoveries, foreign exchange gains or losses on translation of balance sheet accounts, unrealized foreign exchange gains or losses on forward contracts and certain tax adjustments. Refer to the section titled "Non-GAAP Financial Measures" for additional details and reconciliations to the applicable GAAP financial measures.

25

SUMMARY OF QUARTERLY RESULTS OF OPERATIONS

The following tables highlight selected financial information for each of the eight most recent quarters that, in management’s opinion, have been prepared on a basis consistent with the audited consolidated financial statements for the year ended December 31, 2017. The selected financial information presented below reflects all adjustments, consisting primarily of normal recurring adjustments, which are, in the opinion of management, necessary for a fair presentation of results for the interim periods. These results are not necessarily indicative of results for any future period. You should not rely on these results to predict future performance.

(In thousands of U.S. dollars, except where otherwise stated) | 2017 | 2016 | |||||||||||||||||||||||||||||||

Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | Q2 | Q1 | ||||||||||||||||||||||||||

Revenue | $ | 183,533 | $ | 173,241 | $ | 173,510 | $ | 161,793 | $ | 163,021 | $ | 153,560 | $ | 156,229 | $ | 142,797 | |||||||||||||||||

Cost of goods sold | 121,719 | 115,466 | 113,813 | 106,132 | 94,225 | 104,192 | 103,465 | 95,982 | |||||||||||||||||||||||||

Gross margin | 61,814 | 57,775 | 59,697 | 55,661 | 68,796 | 49,368 | 52,764 | 46,815 | |||||||||||||||||||||||||

Gross margin % | 33.7 | % | 33.3 | % | 34.4 | % | 34.4 | % | 42.2 | % | 32.1 | % | 33.8 | % | 32.8 | % | |||||||||||||||||

Expenses | |||||||||||||||||||||||||||||||||

Sales and marketing | 20,456 | 18,127 | 18,844 | 18,167 | 17,048 | 15,519 | 16,046 | 15,629 | |||||||||||||||||||||||||

Research and development | 21,828 | 21,525 | 20,531 | 19,477 | 18,047 | 18,015 | 18,237 | 18,778 | |||||||||||||||||||||||||

Administration | 11,379 | 10,560 | 10,579 | 10,386 | 9,708 | 11,435 | 10,286 | 9,527 | |||||||||||||||||||||||||

Restructuring | 245 | 199 | 259 | 373 | — | — | — | — | |||||||||||||||||||||||||

Acquisition-related and integration | 4,792 | 2,077 | 875 | 451 | 376 | 34 | 59 | 374 | |||||||||||||||||||||||||

Impairment | — | — | — | 3,668 | — | — | — | — | |||||||||||||||||||||||||

Amortization | 6,073 | 5,049 | 4,760 | 4,626 | 4,372 | 4,418 | 4,725 | 3,762 | |||||||||||||||||||||||||

64,773 | 57,537 | 55,848 | 57,148 | 49,551 | 49,421 | 49,353 | 48,070 | ||||||||||||||||||||||||||

Earnings (loss) from operations | (2,959 | ) | 238 | 3,849 | (1,487 | ) | 19,245 | (53 | ) | 3,411 | (1,255 | ) | |||||||||||||||||||||

Foreign exchange gain (loss) | 1,267 | 1,667 | 3,517 | 1,099 | (3,547 | ) | 590 | (1,071 | ) | 2,292 | |||||||||||||||||||||||

Other income (expense) | 38 | 32 | (12 | ) | 9 | 2 | 23 | 32 | 26 | ||||||||||||||||||||||||

Earnings (loss) before income taxes | (1,654 | ) | 1,937 | 7,354 | (379 | ) | 15,700 | 560 | 2,372 | 1,063 | |||||||||||||||||||||||

Income tax expense (recovery) | 1,876 | 710 | 705 | (168 | ) | (18 | ) | 2,329 | 1,654 | 345 | |||||||||||||||||||||||

Net earnings (loss) | $ | (3,530 | ) | $ | 1,227 | $ | 6,649 | $ | (211 | ) | $ | 15,718 | $ | (1,769 | ) | $ | 718 | $ | 718 | ||||||||||||||

Earnings (loss) per share - GAAP in dollars | |||||||||||||||||||||||||||||||||

Basic | $ | (0.11 | ) | $ | 0.04 | $ | 0.21 | $ | (0.01 | ) | $ | 0.49 | $ | (0.06 | ) | $ | 0.02 | $ | 0.02 | ||||||||||||||

Diluted | $ | (0.11 | ) | $ | 0.04 | $ | 0.20 | $ | (0.01 | ) | $ | 0.49 | $ | (0.06 | ) | $ | 0.02 | $ | 0.02 | ||||||||||||||

Weighted average number of shares (in thousands) | |||||||||||||||||||||||||||||||||

Basic | 33,136 | 32,200 | 32,167 | 31,909 | 31,962 | 32,043 | 31,966 | 32,156 | |||||||||||||||||||||||||

Diluted | 33,136 | 32,735 | 32,766 | 31,909 | 32,367 | 32,043 | 32,430 | 32,500 | |||||||||||||||||||||||||

26

Our quarterly results may fluctuate from quarter-to-quarter, driven by variation in sales volume, product mix and the combination of variable and fixed operating expenses, as well as from the impact of acquisitions completed in the quarter. The impact of significant items incurred during the first three interim periods of the year ended December 31, 2017 are discussed in more detail and disclosed in our quarterly reports and management’s discussion and analysis. Certain of the factors that affected our quarterly results are listed below.

• | In the fourth quarter of 2017, net earnings decreased by $4.8 million, compared to the third quarter of 2017, primarily due to lower earnings from operations as a result of increased operating expenses and higher acquisition and integration related expenses, as well as higher income tax expenses compared to the third quarter of 2017. |