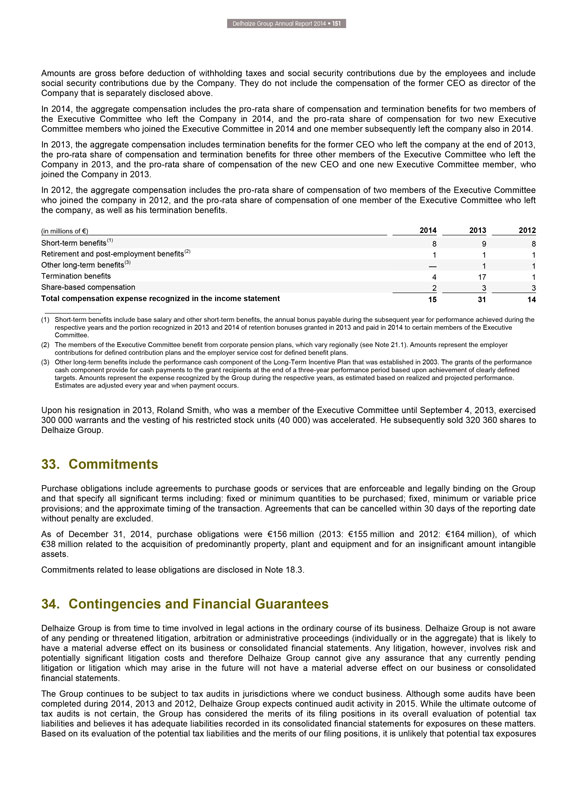

Form 6-K DELHAIZE GROUP For: Apr 13

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

Pursuant to Rule 13a-16 or 15d-16

under the Securities Exchange Act of 1934

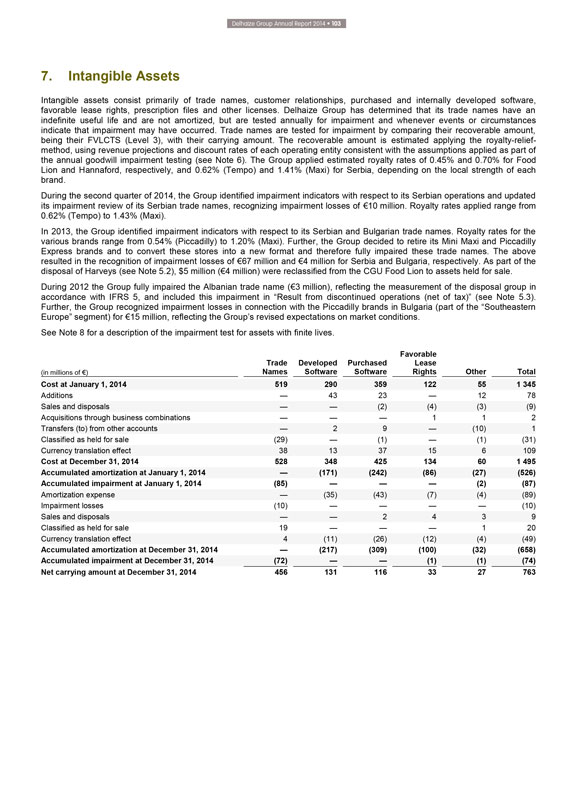

For the month of April, 2015

Commission File Number: 333-13302

ETABLISSEMENTS DELHAIZE FRÈRES

ET CIE “LE LION” (GROUPE DELHAIZE)

(Exact name of registrant as specified in its charter)*

DELHAIZE BROTHERS AND CO.

“THE LION” (DELHAIZE GROUP)

(Translation of registrant’s name into English)*

SQUARE MARIE CURIE 40

1070 BRUSSELS, BELGIUM

(Address of principal executive offices)

| * | The registrant’s charter (articles of association) specifies the registrant’s name in French, Dutch and English. |

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

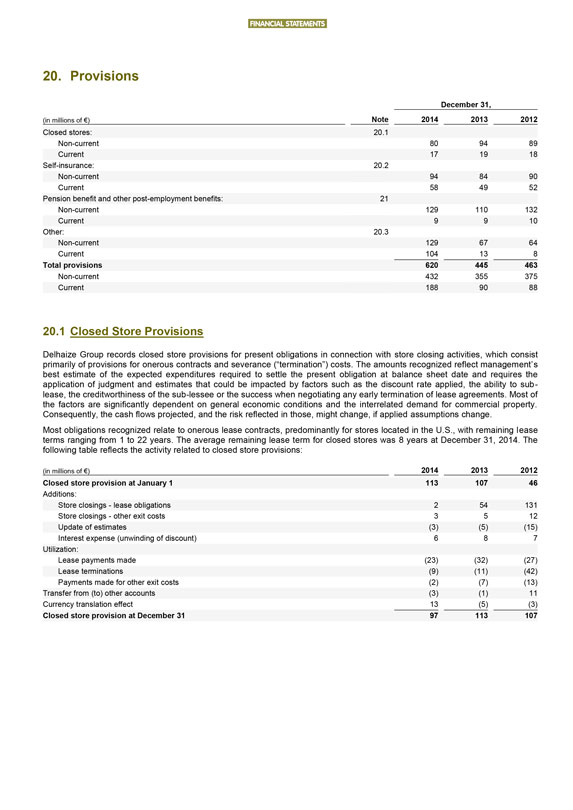

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ¨

ANNUAL REPORT 2014

DELHAIZE GROUP

DELHAIZE GROUP(1)

A LEADING FOOD

RETAILER

Delhaize Group has leading positions in food retailing in key markets. Our operating

companies have acquired these positions through distinct go-to-market strategies. The Group is committed to offer its customers a locally differentiated shopping experience, to deliver superior value and to maintain high social, environmental and

ethical standards. Our Group’s strength is supported by the close cooperation of its operating companies at both the regional and global levels.

Delhaize

Group is listed on both NYSE Euronext Brussels (ticker symbol: DELB) and the New York Stock Exchange (ticker symbol: DEG).

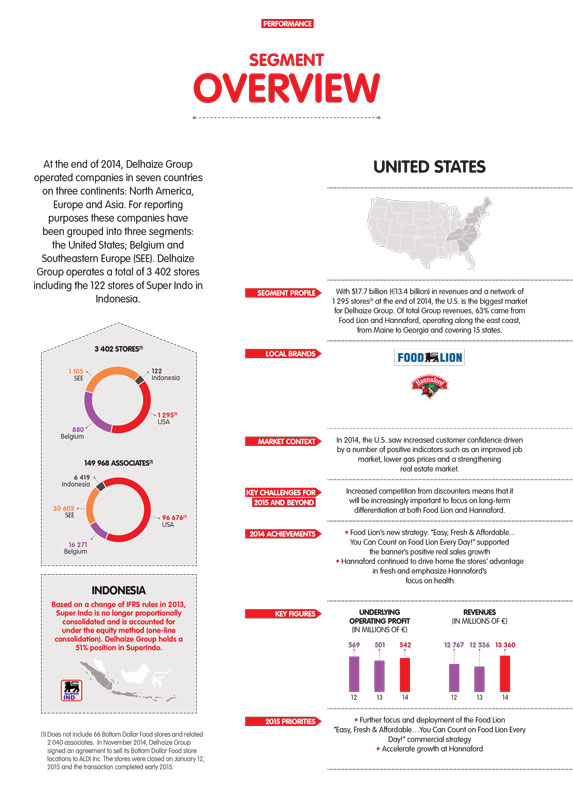

United States

Belgium & Luxembourg

Greece, Romania & Serbia

Indonesia

149 968

associates

3 402

stores

7

countries

Belgium, Luxembourg,

United States, Greece,

Romania, Serbia, Indonesia

€ 21.4B

revenues

€ 762 M

underlying operating profit

(1) As of December 31, 2014 unless otherwise indicated. Does not include 66 Bottom Dollar Food stores and 2 040 related associates.

02 Overview

02 Key figures

04 Interview with the Chairman of the Board of Directors and the Chief Executive Officer

08

Strategy

08 Retail Context and 2015 priorities

10 Strategic Framework

11 Our Purpose

12 Keeping our promises

14 Customers

18 Associates

21 Our Values

22 Communities

26 Shareholders

28 Shareholder Information

32 Performance(2)

32 Segment Overview

34 Financial Review

37 United States

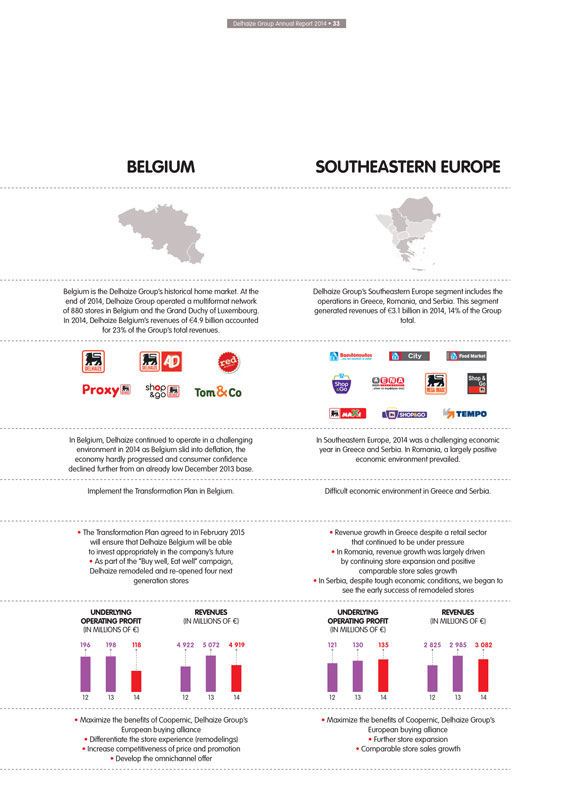

40 Belgium

42 Southeastern Europe

46 Governance(2)

46 Corporate Governance

58 Remuneration Report

64 Risk Factors(2)

71 Financial Statements(2)

168 Glossary

(2) These chapters contain the information

required by the Belgian Companies Code to

be included in the Management Report on the

consolidated financial statements

and constitute

in the aggregate such Management Report.

OVERVIEW

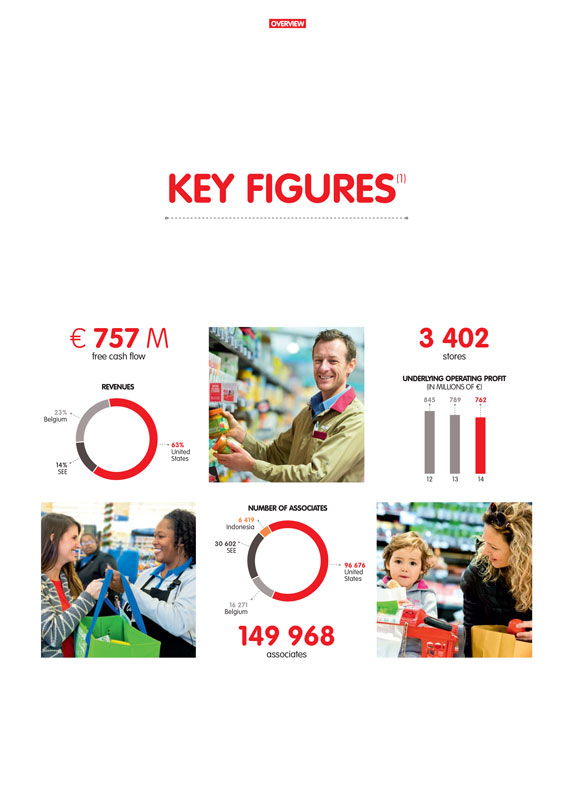

KEY FIGURES(1)

€ 757 M

free cash flow

REVENUES

23%

Belgium

63%

United

States

14%

SEE

3 402

stores

UNDERLYING OPERATING PROFIT

(IN MILLIONS OF €)

845 789 762

12 13 14

NUMBER OF ASSOCIATES

6 419

Indonesia

30 602

SEE

96 676

United

States

16 271

Belgium

149 968

associates

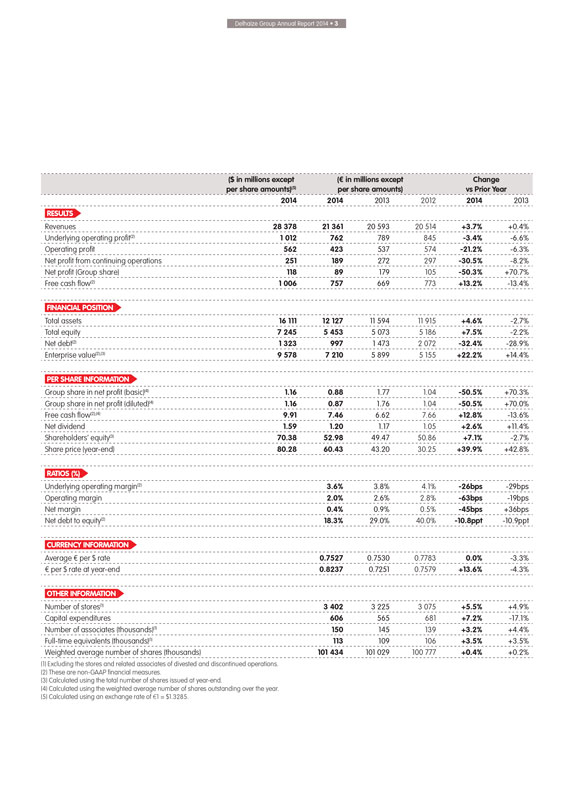

Delhaize Group Annual Report 2014 • 3

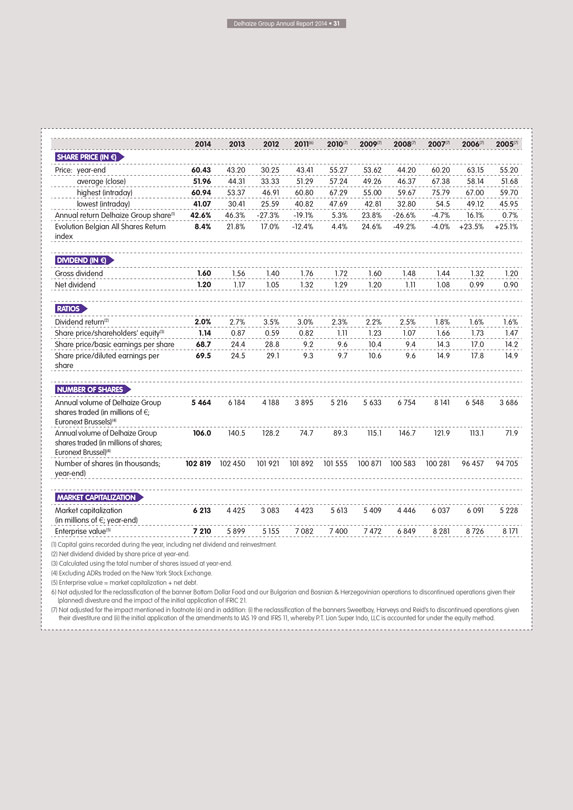

($ in

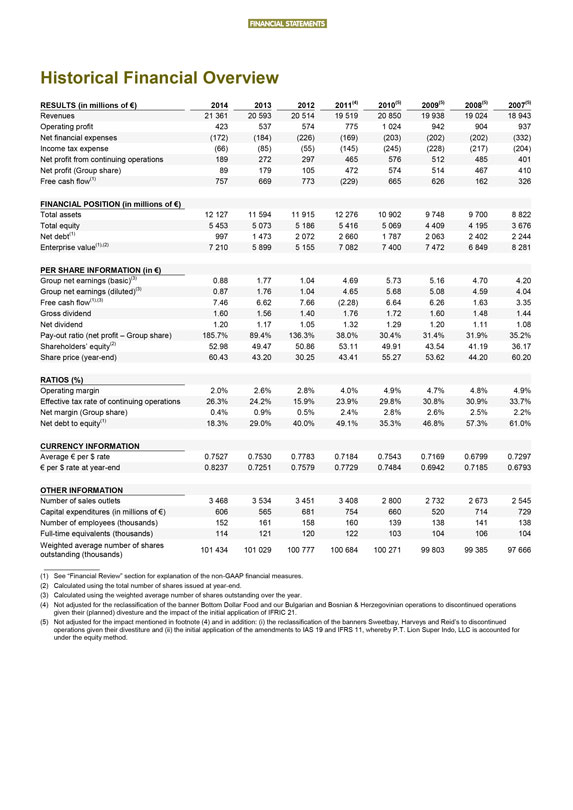

millions except per share amounts)(5) (€ in millions except per share amounts) Change vs Prior Year

2014 2014 2013 2012 2014 2013

RESULTS

Revenues 28 378 21 361 20 593 20 514 +3.7% +0.4%

Underlying operating profit(2) 1 012 762 789 845 -3.4% -6.6%

Operating profit 562 423 537 574

-21.2% -6.3%

Net profit from continuing operations 251 189 272 297 -30.5% -8.2%

Net profit (Group share) 118 89 179 105 -50.3% +70.7%

Free cash flow(2) 1 006

757 669 773 +13.2% -13.4%

FINANCIAL POSITION

Total assets 16 111 12 127 11

594 11 915 +4.6% -2.7%

Total equity 7 245 5 453 5 073 5 186 +7.5% -2.2%

Net

debt(2) 1 323 997 1 473 2 072 -32.4% -28.9%

Enterprise value(2),(3) 9 578 7 210 5 899 5 155 +22.2% +14.4%

PER SHARE INFORMATION

Group share in net profit (basic)(4) 1.16 0.88 1.77 1.04 -50.5% +70.3%

Group share in net profit (diluted)(4) 1.16 0.87 1.76 1.04 -50.5% +70.0%

Free

cash flow(2),(4) 9.91 7.46 6.62 7.66 +12.8% -13.6%

Net dividend 1.59 1.20 1.17 1.05 +2.6% +11.4%

Shareholders’ equity(3) 70.38 52.98 49.47 50.86 +7.1% -2.7%

Share price (year-end) 80.28

60.43 43.20 30.25 +39.9% +42.8%

RATIOS (%)

Underlying operating margin(2)

3.6% 3.8% 4.1% -26bps -29bps

Operating margin 2.0% 2.6% 2.8% -63bps -19bps

Net margin 0.4% 0.9% 0.5% -45bps +36bps

Net debt to equity(2) 18.3% 29.0%

40.0% -10.8ppt -10.9ppt

CURRENCY INFORMATION

Average € per $ rate 0.7527

0.7530 0.7783 0.0% -3.3%

€ per $ rate at year-end 0.8237 0.7251 0.7579 +13.6% -4.3%

OTHER INFORMATION

Number of stores(1) 3 402 3 225 3 075 +5.5% +4.9%

Capital expenditures 606 565 681 +7.2% -17.1%

Number of associates (thousands)(1) 150 145 139

+3.2% +4.4%

Full-time equivalents (thousands)(1) 113 109 106 +3.5% +3.5%

Weighted average number of shares (thousands) 101 434 101 029 100 777 +0.4% +0.2%

(1) Excluding the stores and related associates of divested and discontinued operations.

(2)

These are non-GAAP financial measures.

(3) Calculated using the total number of shares issued at year-end.

(4) Calculated using the weighted average number of shares outstanding over the year.

(5)

Calculated using an exchange rate of €1 = $1.3285.

OVERVIEW

WORKING TOGETHER TO BE PREFERRED BY OUR

CUSTOMERS

INTERVIEW WITH THE CHAIRMAN OF THE BOARD OF DIRECTORS AND THE CHIEF

EXECUTIVE OFFICER

In 2014 we introduced our new Strategic Framework. As a result, we are simpler, more transparent, and focused on providing a great, local

shopping experience.

What would you describe as the most important accomplishments at Delhaize Group in 2014?

Mats Jansson For me, 2014 was about Frans’ first year as CEO, developing the new strategy, and realizing continued progress in our U.S. operations. With Frans in place, the

Executive Committee took the opportunity to review our strategy and develop a new Strategic Framework. We felt it was critical to put our customers at the center of everything we do. In the U.S., where we have now seen nine consecutive quarters of

growth, we continue to be pleased by our efforts to maintain relevance. We did take the difficult decisions to announce the Transformation Plan in Belgium and in the fourth quarter of 2014 we agreed to the

Watch the interview of Frans Muller on annualreport.delhaizegroup.com

sale of our Bottom

Dollar Food locations in the U.S. We also exited from Bulgaria and Bosnia

& Herzegovina in 2014. These decisions are never easy, but we felt these decisions

were important in order to improve our focus. Frans Muller In March 2014, we developed, introduced and began to implement our new Strategic Framework across the Group. This Framework articulates our company’s Purpose. It also outlines the

Promise we make to all our stakeholders, the Principles we use to make decisions, our Sustainability Ambition as an organization, and the Values that embody who we are. Together, these elements function as the framework to serve our customers,

ensuring that we provide them with a great local shopping experience in stores and online.

Delhaize Group Annual Report 2014 • 5

Why did

the Board and the Executive Committee find it important to review Delhaize Group’s strategy?

MJ I believe that we have an obligation to review the strategy

every year and, with Frans on board, this represented a unique opportunity to do a deeper review of our strategy. It is important to look at our strategy from a commercial perspective to ensure its continued relevance, to understand the areas where

we can improve, and to ensure our business is sustainable. One of the benefits of having worked in the retail industry for many years is that I have seen strategic plans discussed and put into action. Putting a new strategy in place is an ambitious

process and with our new, clear, and transparent strategy, we are well positioned in 2015 to further implement it successfully and to pursue profitable growth in all our markets.

FM As the new CEO I took the opportunity to lead our in-depth strategic review in order for us to understand the facts, assess the current situation, and to build on our strengths,

such as our store network, our people, our fresh food competence and our private brands. It also allowed us to identify and further focus on our core businesses. We had to make some tough decisions in 2014, but our new Strategic Framework has helped

us to remain focused on attractive markets in terms of size, growth, and profitability and be competitive in markets where we have the capabilities and strengths to win.

How does the strategy influence day-to-day management and priorities of the different operating companies within Delhaize Group?

MJ By refining our strategy, we are focusing our execution efforts to deliver our core promises to our stakeholders. We have four key stakeholders – customers, associates,

communities, and shareholders - and we use our new strategy to deliver value to each in a profitable, respectful and sustainable way. FM Our Promise to our

customers is to provide a great local shopping experience, in stores and online. With the customer as our primary focus, we are re-defining the words used in our Strategic Framework: “preferred”, “local” and “working

together”. We want to ensure that, by providing excellent products at reasonable prices in a compelling and logical store environment, customers choose us as their preferred supermarket. We also understand that local is important. Customers

want stores that are conveniently located. They want the store staffed with people from their community – people they know and who reflect the local culture and values. Finally, working together means that we want to work as teams in the

stores, across functions within operating companies, and across the Group as a whole. We want to continuously share best practices to ensure that we are operating our customers’ preferred local supermarket. “Customer focus” is just a

buzzword if we do not measure whether we are delivering on our Promise. For this reason, we are putting specific performance metrics in place to measure our success and understand how we are delivering on our promises. For example, to measure how

our customers perceive us we will use a Net Promoter Score, which is determined by asking our customers if they would recommend us to their friends and family. And we can’t deliver for our customers without the engagement of our associates.

Therefore, we will also be using a new Associate Engagement Survey to measure with our associates how rewarding their work is, because we believe that engaged associates will, in turn, delight customers.

“Our new Strategic Framework puts our customers at the center of everything we do and provides a roadmap for a winning business.

Through these and other key performance indicators - discussed in more detail on page

13 - we

are making ourselves accountable to our customers, our associates, our communities, and ultimately our shareholders.

In your first full year at the company, what

did you find most exciting about Delhaize Group in 2014? What has pleased you most in the past year?

FM What excited me most about Delhaize Group in 2014 was what

I found in meeting with the various associates and visiting our stores in the U.S., Belgium and Luxembourg, Southeastern Europe, and Indonesia. I found talented associates with strong values and ethics, strong brands with local leadership, and

excellent front-line management, all combining to serve about 20 million customers per week. After all, it is the people – our customers as well as our talented associates – who make our business successful.

I am also very proud of our strong fundamentals. We are number one or number two in most of our local markets. These markets, in which we have such a strong position, represent no

less than 75% of our total Group sales. Above all, I am enthusiastic about and proud of our Executive team – Pierre, Kevin, Kostas, and Marc – and the work we have accomplished together. With these and the other executives across the

Group, we have deep experience and a collective knowledge. It is my job to make sure that we harness and focus this collective knowledge and experience in service of driving Delhaize Group’s continued performance.

Mats Jansson,

Chairman of the

Board of Directors of

Delhaize Group

OVERVIEW

“We have terrific and locally robust

brands and we are number one or number two in most of our markets.

Could you talk about what decisions the Executive Committee took in 2014 and how Delhaize Group

thinks about capital discipline?

MJ As a result of our refined strategic thinking, our goals and how we will accomplish them are now clearer. The organization is

simpler. Our structure is focused on our core business and is more transparent. The priorities for the Group are more defined than ever before. In 2014, the Executive Committee set the foundation to create a winning business by combining hard facts

with our passion for retail.

FM I am convinced that an organization has to be focused on a limited number of high-impact priorities. In keeping with this

philosophy, in late 2013 and continuing into 2014 we identified which markets and banners were core to us and then made strategic decisions to exit non-core banners and markets. We have further strengthened our balance sheet through strong operating

performance and by improving working capital and capital expenditure discipline. In the past three years we have reduced our net debt by more than 50%. Today, we are present in seven countries with approximately 63% of our revenues generated in the

United States. Operations in Belgium and Luxembourg represent around 23% of the Group’s revenues and those in Southeastern Europe represent around 14%.

Our

five core banners at Delhaize Group are Food Lion and Hannaford (U.S.), Delhaize Le Lion (Belgium and Luxembourg), Alfa Beta (Greece), and Delhaize Serbia (Serbia). These five banners will be the focus of our capital spending during the coming

years. Consistent with our strategy, we are focusing on our key formats of supermarket and convenience.

Frans Muller, President and Chief Executive Officer of

Delhaize Group

MJ While we are seeing growth, it is still mixed across our operations, which is why we are focusing on core markets where we believe we can win.

The environment remains highly competitive and we believe that winning will require us to push differentiation within our formats to increase relevance to our customers.

FM Our growth is indeed being led largely by our progress at Delhaize America. At Food Lion, the team continues to build momentum with its “Easy, Fresh &

Affordable” strategy. Food Lion’s comparable store sales growth is among the best it has delivered during the past decade and that performance is providing optimism as we look ahead. At Hannaford, the team continues to deliver results.

They

2015 PRIORITIES

Create value in line with our peers;

Leverage skills of our associates & work on capability gaps;

Align IT and business

priorities;

Achieve progress on 2020 sustainability goals;

Accelerate share

of online sales.

have maintained their strong market position and are building on this strength. In Belgium, the uncertainty caused by the announcement of the

Transformation Plan has negatively impacted revenues, but will improve our competitiveness going forward. In Greece, despite tough economic conditions, we continued to expand the store network and gain market share. In Serbia, while we have

experienced deflation, we have nevertheless been able to increase share in the food retail channel, and in Romania, Mega Image continued to profitably expand in Bucharest. In Indonesia, we continued to see strong comparable store sales growth at

Super Indo.

Sustainability will receive increased attention at Delhaize Group. How does sustainability fit into the new Strategic Framework?

FM For Delhaize Group, sustainability is about being the preferred supermarket for our customers, being a good employer, being an integral part of the local community, and being a

high-integrity partner for our suppliers. It is a guidebook to being a great company. We want to be known as a company where people enjoy working, customers love shopping, and vendors value doing business with us. Integrity and sustainability are

synonyms at Delhaize Group, and are embedded in our core Values.

MJ Sustainability is at the heart of how we run our business. In order to concretely measure our

performance, we will continue to monitor our progress against our 2020 Sustainability Goals. We have work to do to keep further integrating sustainability into how we operate and we are committed to an ambitious target, a Supergood sustainability

strategy that underpins everything we do.

FM Our 2020 Sustainability Goals are ambitious and include: 100% of our stores and warehouses donating food that is close

to expiration to feed people in our local communities; all Delhaize Group companies will have leading Healthy Associates programs; refrigerants will be 80% ozone friendly; our recycling rate in stores and distribution centers

Delhaize Group Annual Report 2014 • 7

increasing from 54% currently to 80% by 2020; achieving a 20% reduction in greenhouse gas emissions by 2020 against a 2008 baseline through continued energy

reduction use and better refrigerants; employing a more diverse and inclusive team of associates to better serve our local neighborhoods; and offering the most sustainable private brands.

Looking forward, what is the outlook for 2015 and how does this fit into your strategic thinking?

FM I see opportunities in making our banners more competitive and being more cost-conscious as a Group, with the overall goal of creating value in line with our peers. At the same

time we will never compromise on our focus on the customers: providing them with a great local shopping experience at a reasonable price.

Following the

streamlining of our portfolio in 2013 and 2014, we aim in 2015 to support growth opportunities at all our banners. At Food Lion, we will further refine and deploy our Easy, Fresh & Affordable strategy in 160 additional stores, and at

Hannaford, we have the ambition to accelerate growth. In Belgium, we are looking to implement the Transformation Plan, improving our customer offer, modernizing our network and further developing our online channel. In Southeastern Europe and

Indonesia we will continue to expand. Across Europe we intend to maximize the potential benefits of Coopernic, our new European buying alliance. Finally, we remain disciplined with respect to capital allocation.

What is the largest opportunity for 2015 and beyond?

FM I believe the company has a solid base

from which I have had the good fortune to start. We have terrific and locally robust brands, and we are number one or number two in most of our local markets. However, in order to build on these positions, we need to continue to focus on our core

markets in order to further differentiate our value proposition. We will also be more commercially aggressive in 2015, as we aim to better communicate our offer and our strengths to our customers. I am convinced these efforts, coupled with our push

into digital and omni-channel food retailing provide us with a positive outlook for Delhaize Group.

MJ We are facing challenges, including slow growth and

increasing consolidation in the markets where we operate. In order to remain relevant in our markets and pursue growth, we need to continue to bring cost levels down while at the same time maximizing the potential of our assets and refusing to

compromise in terms of delivering an excellent product to our customers. We need to mobilize the energy of our associates. Our biggest asset as a company is our people and their energy. We need to work harder to engage them, capture their creativity

and innovation while at the same time work to support their personal development.

What will Delhaize Group look like in five years’ time?

MJ In all our markets we want to look back in five years’ time having gained market share, being recognized as a top employer, and having reached or exceeded our 2020

sustainability targets. We expect to have high operating efficiency, at all steps in the supply chain and

to have increased return on invested capital (ROIC).

FM We want to be in a leadership position in all of our core markets. We want to have delighted customers. But to do this we have work to do on our IT systems and

infrastructure to ensure that they are up to date and can support future growth. We want to be able to deliver on customer expectations with our digital and online platform, and accelerate our share of online sales. Above all we want to be in

sustainable leading positions vis-à-vis our customers, our associates, and our suppliers. We want to lead in creating value for our shareholders.

The focus

we apply to the segments and markets in which we want to compete will be applied to everything we do, by everyone in our company and will be integrated company-wide into the incentive targets for our officers. We believe this focus will benefit all

our stakeholders. Because our focus is our customer and we will operate our customers’ preferred local supermarkets!

STRATEGY

RETAIL CONTEXT

AND 2015 PRIORITIES

In 2014 we reformulated our strategy (see page 10) to face a retail

marketplace that today is more competitive than ever. We see three main external competitive trends that impact and shape the food retail industry today. These trends and our response are discussed on the following pages.

Delhaize Group Annual Report 2014 • 9

“Our goal is to be known as the best in fresh, with an efficient yet innovative assortment, delivering the best shopping experience at the best everyday

value.

First, large format stores, particularly hypermarkets are being challenged. Several large players are experiencing a slowdown of comparable store sales

(CSS) in their core large formats. Thus they are developing smaller formats as well as on-line alternatives to try to revive growth. Second, the rise of the discounters has progressed unabated. Thirdly, as the number of channels proliferates –

discount, traditional, hypermarket, club, dollar, online – the blurring of boundaries between formats continues. Food retailers are joining other industries in developing, testing, and refining different business models to adapt to both new

consumer demands as well as a changing competitive landscape. The result is that shoppers no longer distinguish between formats; they only want their favorite products at the best prices. In addition, and because of these trends, margins in the

retail sector are increasingly being squeezed.

Our response to these trends is to refine and update our formats and intensify our e-commerce efforts while

continuing to invest in the customer proposition. Our goal is to be known as the best in fresh, with an efficient yet innovative assortment, delivering the best shopping experience at the best everyday value.

Our sustainability strategy is called “Supergood”. Our Supergood strategy is in response to other trends we see impacting food retail:

Increasing consumer demand for transparency about our products; for example, where they are from and how they are produced.

Health trends including the increase of diet-related diseases (obesity, diabetes, malnutrition) impacting customer health needs and expectations.

Increasing pressure on both agriculture and oceanic resources impacts price and availability of our products; for example, the increasing global demand for food, decreasing

availability of water, diminishing soil quality, and climate change impacts such as droughts and storms.

So, to prepare us to stay competitive in this changing

world, we established the Supergood 2020 strategy. On the path to meeting our 2020 goals, we are changing how we do business – from how we design and source our private brand products, to how we foster healthy living among our customers and

associates.

Being a Supergood company underpins the way we operate and is simply good business: our Supergood ambition is to delight our customers and energize our

associates by helping them live happier and eat healthier in thriving local communities.

The following pages show our strategy in action across our markets as we

meet today’s challenges and prepare for those we will face tomorrow.

2015 PRIORITIES

Put the customer back at the center

Provide a great local shopping experience in stores and

on-line

Engage great people

Develop a strong performance culture

Offer development opportunities

Connect with communities

Support thriving communities

Improve our offer of nutritious, sustainable, and affordable

private brands

Empower healthy and sustainable living

Create value in line with our peers

Support growth opportunities

Realize operating excellence

and efficiencies

Maximize our assets’ potential and return

Align our information technology (IT) and

business priorities

Concretely, in the U.S., we will be further focusing and careful rolling out the Food Lion “Easy, Fresh & Affordable... You Can

Count on Food Lion Every Day!” commercial strategy.

We will also continue to accelerate growth at Hannaford. In order to realize operating excellence and

efficiencies, we will implement the Transformation Plan in Belgium and maximize the benefits of Coopernic, our European buying alliance. In Southeastern Europe and Indonesia, we remain focused on further store expansion and comparable store sales

growth.

STRATEGY

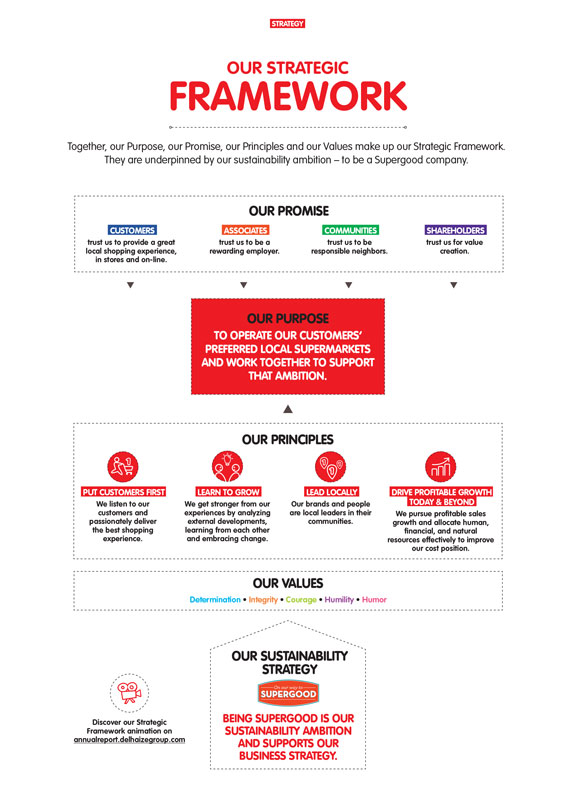

OUR STRATEGIC

FRAMEWORK

Together, our Purpose, our Promise, our Principles and our Values make up our

Strategic Framework. They are underpinned by our sustainability ambition – to be a Supergood company.

OUR PROMISE

CUSTOMERS

trust us to provide a great local shopping experience, in stores and on-line.

ASSOCIATES

trust us to be a rewarding employer.

COMMUNITIES

trust us to be responsible neighbors.

SHAREHOLDERS

trust us for value creation.

OUR PURPOSE

TO OPERATE OUR CUSTOMERS’

PREFERRED LOCAL SUPERMARKETS

AND WORK TOGETHER TO SUPPORT

THAT AMBITION.

OUR PRINCIPLES

PUT CUSTOMERS FIRST

We listen to our customers and passionately deliver the best shopping

experience.

LEARN TO GROW

We get stronger from our experiences by analyzing

external developments, learning from each other and embracing change.

LEAD LOCALLY

Our brands and people are local leaders in their communities.

DRIVE PROFITABLE GROWTH TODAY

& BEYOND

We pursue profitable sales growth and allocate human, financial, and natural resources effectively to improve our cost position.

OUR VALUES

Determination • Integrity • Courage • Humility • Humor

Discover our Strategic Framework animation on annualreport.delhaizegroup.com

OUR SUSTAINABILITY STRATEGY

On our way to

SUPERGOOD

BEING SUPERGOOD IS OUR SUSTAINABILITY AMBITION AND SUPPORTS OUR BUSINESS STRATEGY.

Delhaize Group Annual Report 2014 • 11

OUR

PURPOSE

To operate our customers’ preferred local supermarkets and work

together to support that ambition.

Our Purpose is why we exist and how we are currently delivering. Each word in our Purpose is important; below we have

highlighted four terms: preferred, local, supermarket and working together. Each term is linked to our promises which are described on the following pages.

Our

brands and people are local leaders in their communities. What makes us LOCAL is that:

Our stores are conveniently located.

We provide local produce when it is in season.

Our stores are staffed with people from the

local community; our staff reflects the culture and values of the community and we work together to give back to the community.

INTRODUCING OUR STRATEGIC FRAMEWORK

“In March 2014, we developed, introduced and began to implement our new Strategic Framework across the Group. This Framework articulates our company’s

Purpose. It also outlines the Promise we make to all our stakeholders, the Principles we use to make decisions, our Sustainability Ambition as an organization, and the Values that embody who we are. Together, these elements function as the framework

to serve our customers, ensuring that we provide to them a great local shopping experience in stores and online.”

We listen to our customers and passionately

deliver the best shopping experience. Customers PREFER us because:

Our food is very fresh, priced right and is available across a number of channels.

Our employees are always at our clients’ service and helpful; customer satisfaction is constantly tracked.

There is always follow-up to customer queries.

We address customers’ concerns on

sustainability; for example, we strive to provide private brand products that are delicious, sustainable and affordable.

We deliver on our core business, that of

selling groceries, by pursuing profitable sales growth and allocating human, financial, and natural resources effectively to improve our cost position.

Our

SUPERMARKETS :

Focus on selling a wide range of food products.

Stock

excellent private brand products.

Provide a convenient and pleasant shopping experience.

We get stronger from our experiences by analyzing external development, learning from each other and

embracing change. Our goal as

Delhaize Group is to work together

to support being our customers’

preferred local supermarket.

WORKING TOGETHER means:

Being an innovator.

Sharing best practices and learning from each other.

Realizing benefits of scale.

STRATEGY

KEEPING OUR

PROMISES

Our Promise is what we are doing as Delhaize Group to achieve our Purpose. In this

section, we show how we are keeping our promises to our stakeholders and how we are measuring them.

The Delhaize Group team passionately serves local customers

tasty, nutritious, and affordable foods. We operate friendly, neighborhood supermarkets in diverse local markets, living shared values, enriching thriving communities, and growing profitably as a Group.

We skillfully balance the needs of our customers, associates, communities and shareholders in a respectful, sustainable, and profitable way. This results in being the preferred

local supermarket.

Discover more about our Strategic Framework on annualreport.delhaizegroup.com

CUSTOMERS

ASSOCIATES

COMMUNITIES

SHAREHOLDERS

Delhaize Group Annual Report 2014 • 13

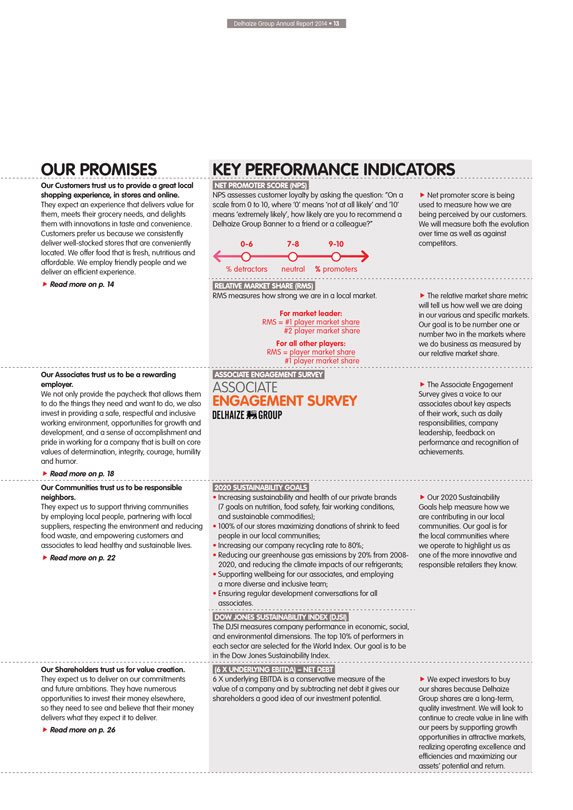

OUR

PROMISES

Our Customers trust us to provide a great local shopping experience, in stores and online.

They expect an experience that delivers value for them, meets their grocery needs, and delights them with innovations in taste and convenience. Customers prefer us because we

consistently deliver well-stocked stores that are conveniently located. We offer food that is fresh, nutritious and affordable. We employ friendly people and we deliver an efficient experience.

Read more on p. 14

Our Associates trust us to be a rewarding employer.

We not only provide the paycheck that allows them to do the things they need and want to do, we also invest in providing a safe, respectful and inclusive working environment,

opportunities for growth and development, and a sense of accomplishment and pride in working for a company that is built on core values of determination, integrity, courage, humility and humor.

Read more on p. 18

Our Communities trust us to be responsible neighbors.

They expect us to support thriving communities by employing local people, partnering with local suppliers, respecting the environment and reducing food waste, and empowering

customers and associates to lead healthy and sustainable lives.

Read more on p. 22

Our Shareholders trust us for value creation.

They expect us to deliver on our commitments and

future ambitions. They have numerous opportunities to invest their money elsewhere, so they need to see and believe that their money delivers what they expect it to deliver.

Read more on p. 26

KEY PERFORMANCE INDICATORS

NET PROMOTER SCORE (NPS)

NPS assesses customer loyalty by asking the question: “On a

scale from 0 to 10, where ‘0’ means ‘not at all likely’ and ‘10’ means ‘extremely likely’, how likely are you to recommend a Delhaize Group Banner to a friend or a colleague?”

0-6 7-8 9-10

% detractors neutral % promoters

RELATIVE MARKET SHARE (RMS)

RMS measures how strong we are in a local market.

For market leader:

RMS = #1 player market share

#2 player market share

For all other players:

RMS = player market share

#1 player market share

ASSOCIATE ENGAGEMENT SURVEY

ASSOCIATE

ENGAGEMENT SURVEY

DELHAIZE GROUP

2020 SUSTAINABILITY GOALS

Increasing sustainability and health of our private brands (7 goals

on nutrition, food safety, fair working conditions, and sustainable commodities);

100% of our stores maximizing donations of shrink to feed people in our local

communities;

Increasing our company recycling rate to 80%;

Reducing our

greenhouse gas emissions by 20% from 2008-2020, and reducing the climate impacts of our refrigerants;

Supporting wellbeing for our associates, and employing a more

diverse and inclusive team;

Ensuring regular development conversations for all associates.

DOW JONES SUSTAINABILITY INDEX (DJSI)

The DJSI measures company performance in economic,

social, and environmental dimensions. The top 10% of performers in each sector are selected for the World Index. Our goal is to be in the Dow Jones Sustainability Index.

(6 X UNDERLYING EBITDA) – NET DEBT

6 X underlying EBITDA is a conservative measure of the

value of a company and by subtracting net debt it gives our shareholders a good idea of our investment potential.

Net promoter score is being used to measure how

we are being perceived by our customers. We will measure both the evolution over time as well as against competitors.

The relative market share metric will tell us

how well we are doing in our various and specific markets. Our goal is to be number one or number two in the markets where we do business as measured by our relative market share.

The Associate Engagement Survey gives a voice to our associates about key aspects of their work, such as daily responsibilities, company leadership, feedback on performance and

recognition of achievements.

Our 2020 Sustainability Goals help measure how we are contributing in our local communities. Our goal is for the local communities

where we operate to highlight us as one of the more innovative and responsible retailers they know.

We expect investors to buy our shares because Delhaize Group

shares are a long-term, quality investment. We will look to continue to create value in line with our peers by supporting growth opportunities in attractive markets, realizing operating excellence and efficiencies and maximizing our assets’

potential and return.

STRATEGY

CUSTOMERS

TRUST US TO PROVIDE A GREAT LOCAL SHOPPING EXPERIENCE

IN STORES AND ONLINE

Customers choose to shop at our local banners because they feel warmly welcomed and are delighted to find tasty products that are affordable, healthy and sustainable.

more than

20 M

customers served

weekly in our stores

around the world

REVENUES BY

SEGMENT

23%

Belgium

14%

SEE

63%

United

States

As we move forward into 2015, our aim is to continue to provide our customers with a delightful shopping experience. Our stores are conveniently located. Shopping is efficient and

technology is used to make shopping easier, not only at the point of sale but also to ensure that stores are well-stocked with both high-quality good-value food and non-food products. The following pages illustrate how we keep our Promise to our

customers.

Delhaize Group Annual Report 2014 • 15

PUT

CUSTOMERS FIRST

Our customers trust us to provide a range of tasty, fresh, nutritious and affordable food products, available at their convenience, in stores and

online. Delivering this Promise depends on managing a complex value chain to consistently provide thousands of quality products at good value. This is critical to our success as a business to deliver on our Purpose of operating customers’

preferred local supermarkets.

Alfa Beta (AB, Greece) launches “The joy from giving only the best”

Alfa Beta’s new fresh strategy aims to further improve customers’ experience in Greece and reinforce AB’s established position as the every day food expert. As part

of the fresh strategy, AB aims to further differentiate offerings, with the main focus on three pillars: freshness and variety; guaranteed quality; and fresh ideas.

More specifically:

New products from local and well known bakeries have been

introduced in-store to further strengthen the already appealing assortment in the bakery department;

“Fish Day” every Wednesday has introduced customers

already familiar with the quality of the fresh fish offered to great, new offers in both specific products and whole categories;

The fresh strategy has contributed

to Alfa Beta’s overall positive sales growth and market share gain.

Together, Mega Image’s “Wine Gallery” and a new on-line wine platform offer

a specialized service around wine to better meet customer needs

In 2014, Mega Image opened the Wine Gallery, its first wine “shop-in-a-shop” concept

store, in Bucharest. The concept wine store offers around 900 different wines as well as a choice of spirits and gourmet products associated with wine consumption. Mega Image is also launching an online platform that aims to build a community of

people interested in wines and delicacies, through direct interaction between Mega Image specialists and users in the online forum.

Mega Image is launching an

online platform that aims to build a community of people interested in wines and delicacies:

http://www.stamdevorba.ro

±900

different wines offered by Mega Image’s concept wine store

In Serbia in 2014 we increased our offer of private label products to our customers.

LEARN TO

GROW

We find innovative solutions and share them to benefit our customers. Customers want to be delighted by the shopping experience. Technology-based solutions

offer a way to make the shopping experience not only more efficient but also more pleasant.

Delhaize Belgium begins to test payment by smartphone

In recent years, the proliferation of smartphones and tablets has transformed the shopping experience. In 2014, as part of capital investment in IT and e-commerce to benefit

customers, Delhaize Belgium began to test payments by smartphone, in partnership with a leader in e-payments. When all of a customer’s products are scanned, a QR (machine-readable) code appears on the screen of the payment terminal at checkout.

Via a specific application, customers can scan the code, enter their pin number and thereby confirm the transaction. During the test phase, the system will be evaluated and adapted to provide the optimal user-friendly experience for the customer.

STRATEGY

BRINGING SUPERGOOD PRIVATE BRANDS TO OUR

CUSTOMERS

Part of delivering on our Supergood strategy means providing the tastiest, healthiest and most sustainable private brands. Through our actions to meet

our 2020 Supergood goals, we are making our food more nutritious by reducing salt, fat and sugar content; providing clear nutritional labelling; ensuring complete food safety; and aiming for private brands in 2020 that contain 100% sustainable

seafood, palm oil, wood and paper, and are verified to be from suppliers who provide fair and decent working conditions.

New customer portals launched in Greece

and Romania

The new portal for Alfa Beta Plus card holders launched online allows AB Plus card holders to link their card to an account and have access to their

personal info online along with the ability to track their points, tickets and vouchers. Customers can also order an AB plus card online, ask for a new card if the card is lost, and even donate points to charity. Mega Image in Romania introduced its

first e-commerce solution. Customers can order their favorite products from Mega Image online, with different possibilities for delivery, including home delivery and pick up in-store.

Super Indo mobile site tampil dengan wajah baru & lebih bersahabat.

new

www.superindo.co.id

In 2014, Super Indo re-launched their mobile site to provide an efficient

and up to the minute experience.

10

local Serbian

farmers supported

through a Delhaize

Group Sustainability

Innovation Fund

project

LEAD LOCALLY

Our customers want to know where their food is coming from. They want local produce when it is in season. They appreciate being able to buy food from local producers and being

served by employees who live locally.

Delhaize Group works with local farmers to deliver sustainable products to our customers

In 2013 and continuing into 2014, we launched a series of projects with local farmers to deliver sustainable products as part of our Supergood strategy.

In Romania, we were the first retailer to work closely with small family farms, supporting them with seeds and technical advice to grow specific varieties of vegetables in ways

that maximize the harvest and minimize the environmental impact. Their products are ultimately sold in Mega Image stores as part of the “Gusturi Romanesti” private label. This has deepened our relationship with the farmers and helps us to

promote sustainable agricultural practices in Romania.

In Serbia, we are supporting small scale agriculture to encourage young people to stay working on their

family farms and to help farmers understand and comply with sustainable farming practices. For example, Delhaize Serbia’s fruit and vegetables project, winner of the Delhaize Group Sustainability Innovation Fund award in 2013, helped 10 local

farmers produce sustainable fruits and vegetables. In 2014, these were sold exclusively at Maxi stores for the same price as other produce and were well received by customers. Based on this success, Delhaize Serbia plans to further develop the

project in 2015 and will look at extending the assortment, to include products that are available all year round, such as carrots and potatoes.

These pilots are a

model for future partnerships, to introduce more fruit, vegetables, dairy and meat products into stores from local, sustainably managed farms.

Delhaize Group Annual Report 2014 • 17

DRIVE

PROFITABLE GROWTH TODAY AND BEYOND

We are always looking to innovate and respond to industry dynamics and trends to ensure that our business remains profitable

while we provide the best in fresh to our customers.

Food Lion’s “Easy, Fresh & Affordable…You Can Count on Food Lion Every Day!” Strategy

During the course of 2014, Food Lion began deploying a new, easier shopping experience for customers. In all Food Lion stores, the company enhanced its assortment

offering to customers. In addition, all associates were provided with new customer-centric training to enable customers to count on Food Lion for great service every day.

Seventy-six stores so far have been remodeled as part of our “Easy, Fresh & Affordable…You Can Count on Food Lion Every Day!” strategy. In its remodeled stores,

Food Lion further expanded its assortment to include items such as a new Taste of Inspirations premium line of deli meats and cheeses along with some grab and go items, which make it easy for customers to figure out what items to purchase. In

addition, Food Lion changed the customer check-out process by making it easy for the customer to move quickly through check-out. Also, the company enhanced its meat and produce departments. Customer feedback about the remodeled stores has been

positive; as a result this strategy will be further evaluated and carefully rolled out across approximately 160 Food Lion stores in 2015.

Delhaize Belgium and

Luxembourg launched the “Buy well/Eat well” campaign

The launch in 2014 by Delhaize Belgium and Luxembourg of the new commercial strategy “Buy

well/Eat well” throughout the store network was accompanied by the launch of two pilot stores in April and two pilot stores in October of 2014 centered around this new concept. The stores are particularly focused on offering fresh foods from

the company’s private brands and providing customers with an efficient checkout experience. There have been marked customer satisfaction improvements. In 2015, Delhaize Belgium will continue to invest in its commercial strategy, focusing on

providing fresh products, a varied assortment, and a seamless and easy shopping experience while continuing to offer the best price and quality products to our customers.

In 2014, Delhaize Belgium and Luxembourg launched the new commercial strategy “Buy well/Eat well”.

Discover more on http://fr.delhaize.be/action/bien-acheter-bien-manger

In 2014, Hannaford

continued to serve all members of the community by increasing Hannaford’s commitment to providing products that are locally relevant and increasing community involvement.

STRATEGY

ASSOCIATES

TRUST US TO BE A REWARDING EMPLOYER

Our stores employ diverse associates; we pay our

associates a fair wage and we provide an environment that is much more than just about money.

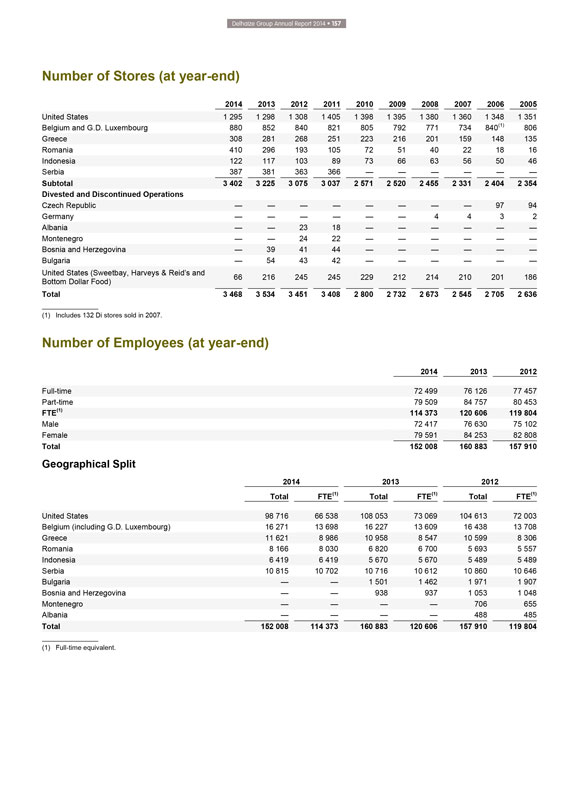

3 402(1) stores

7 countries

149 968(1) associates

We have 149 968 associates across Delhaize Group companies. We provide a safe environment that is respectful and inclusive, one that offers associates development opportunities and

a sense of accomplishment in a job well done. The following pages illustrate how we keep our Promise to our associates and include a discussion of our Values which outline who we are as a Group and who we want to be – to our customers, to our

communities, and to each other.

Delhaize Group Annual Report 2014 • 19

PUT

CUSTOMERS FIRST

Healthy lifestyles are an important part of our Supergood ambition to help our customers and associates live happier and eat healthier. We realize

that health and wellness cover areas from fitness and nutrition to managing chronic disease and that there is no “one-size-fits-all” approach. Alongside our nutritional innovations in our private brands, we continually test approaches to

changing behavior towards adopting healthy habits, launch pilot programs in partnership with health experts, and experiment with new tools.

Providing health and

wellness support online and in-store

At Hannaford in the U.S., we continue to offer free in-store and online dietician classes, consultations, and nutrition

demonstrations to help customers better understand nutrition. Delhaize Belgium provides online food coaching, monthly nutrition tips and answers to frequently asked questions on healthy eating topics including salt, gluten, lactose-intolerance,

diabetes, weight-loss plans and recommended daily quantities of staple foods.

“Our stores welcome diverse customers and associates; we work hard to ensure our

associate diversity reflects our local communities.

Food Lion associates have been empowered by new customer-centric training to make decisions in the moment to

benefit customers.

LEARN TO GROW

We learn to grow by listening to our

associates who provide feedback annually via the Associate Engagement Survey. We also ensure that we continue to grow as a company, for example, by making use of available technology in innovative ways to improve the way we work.

Super Indo uses technology to deliver employee training on site

Super Indo has installed

kiosks in over 100 of Super Indo’s 122 stores to provide e-training to store associates and management trainees. As well as reducing traveling costs, the kiosks provide accessible and up-to-date training for Super Indo associates.

(1) Does not include 66 Bottom Dollar Food Stores and related 2 040 associates. In November 2014, Delhaize Group signed an agreement to sell its Bottom Dollar Food Store locations

to ALDI Inc. The stores were closed on January 12, 2015 and the transaction completed early 2015.

“YOU CAN COUNT ON FOOD LION EVERY DAY!”

As part of its “Easy, Fresh & Affordable” strategy, Food Lion has committed to delivering a new customer and associate experience. Food Lion

educated all of its 64 000 retail associates with new “Count on Me” customer-centric training. The training engages and empowers associates to make decisions in the moment to best serve customers by knowing what to do, making it easy,

doing their part, and caring.

STRATEGY

PARTNERING WITH LOCAL ORGANIZATIONS WHO

SHARE OUR VALUES

In 2014, Delhaize Serbia sponsored the Serbian Olympic Team for Sochi and will continue this support for athletes heading to Rio de Janeiro in

2016. We share our Values with athletes and their healthy lifestyles are part of what we aim to support as a Group.

LEAD LOCALLY

Because we put customers first, we tailor our stores to unique, local characteristics in their communities to make them attractive to local shoppers. How we staff our stores is

crucial to this effort. Community outreach is key to leading locally. Some of our associates volunteer in their local communities and we partner with organizations whose values mirror ours.

AB Volunteer Day

Over the past four years Alfa Beta has organized an Alfa Beta Volunteer Day

where employees come together on a common project to create a positive impact on Greek society and the environment. Each year, the Volunteer Day has brought together employees with members of the local community on an activity agreed among each

store’s employees. Activities have included: collecting food and clothing to benefit a local school and an orphanage; a football match to benefit a nursing home; and removing trash from a local forest. Participation has nearly doubled over the

four years the Volunteer Day has taken place. Nearly 2 700 employees participated in 2011; in 2014, more than 5 000 Alfa Beta employee participated.

DRIVE

PROFITABLE GROWTH TODAY AND BEYOND

In order to drive profitable growth today and beyond, feedback from our associates, who are on the “front-lines” in

our stores is crucial to our continuing success.

The Associate Engagement Survey

The Associate Engagement Survey (AES) lets associates provide confidential feedback via a third party about key aspects of their work, such as daily responsibilities, company

leadership, feedback on performance, and recognition of achievements. While associates were not surveyed in all locations in 2014, a plan is in place to survey associates in all locations in 2015.

The AES findings help us identify gaps and opportunities for associate growth and development, allowing the company to better focus resources to achieve our goals and build on our

success. The survey is another step on the path to fostering a highly engaged workforce – associates working together to support our Purpose of operating our customers’ preferred local supermarkets and delivering our Promise to our four

key groups of stakeholders: customers, associates, communities and shareholders.

more than 5 000

AB associates participated in the 2014 AB Volunteer Day

BEING A SUPERGOOD EMPLOYER

Being Supergood means that our stores welcome associates from a variety of backgrounds, ethnicities, those with disabilities and across generations. We focus on activating

diversity and inclusion programs in all companies and provide all associates with performance dialogues. Healthy lifestyles are a key part of our Supergood ambition; our goal by 2020 is for 100% of our companies to promote good nutrition, physical

and mental health, and safety at work through health-related programs for our associates. One example of our healthy associates’ program in action is in Serbia where Delhaize Serbia has negotiated with private medical clinics and health centers

to provide associates with discounts for medical services, educational workshops, and other offerings.

Delhaize Group Annual Report 2014 • 21

OUR

VALUES

Our Values represent “who” we are and want to be –

for

our customers and for each other.

DETERMINATION

When we talk about

determination, we are talking about a commitment to perform, even if barriers stand in our way. We know we can count on each other to perform his or her role to achieve our goals together. We are accountable and we deliver.

INTEGRITY

Integrity means that we are authentic. We are honest with ourselves and with others.

We are fair and principled towards our colleagues, our suppliers, our customers, and our communities. We stick to our word. We do things the right way, every day.

COURAGE

Courage is required to take the road less traveled. We dare to

challenge ourselves, each other and our competitors. We are commercially aggressive.

HUMILITY

If we are going to Learn to Grow, we should better be humble. Because the humble person is inspired to teach and to learn from others, as well as to be alert to external

developments. We always look for ways to serve others and respect the role each of us plays in delivering on our commitments.

HUMOR

Finally, finding the humor of the situation helps to put things in perspective and enables us to appreciate both our successes and our setbacks. And while work is serious, humor

keeps us from taking ourselves too seriously. Humor makes work enjoyable while sparking creativity and innovation. Humor makes us different.

STRATEGY

COMMUNITIES

TRUST US TO BE RESPONSIBLE NEIGHBORS

In each community where we operate, we aim to serve our

local communities by being an attractive local employer, engaging local suppliers, respecting the environment, reducing food waste and empowering healthy and sustainable living.

3 402(1) stores in 7 countries

EVOLUTION OF CAPEX

(IN MILLIONS OF €)

565 606

13 14

We serve the communities where we operate stores by striving to provide products and

services that are clearly linked to their local communities. Our stores employ local people and also support their local neighborhoods to be healthier, greener and thriving.

Delhaize Group Annual Report 2014 • 23

PUT

CUSTOMERS FIRST

We work hard to be local at every step of the purchasing process for our customers. Our stores are staffed with associates from the local community

and aim to reflect the culture and values of the community. Our local community engagement is a key way we differentiate ourselves from our competitors.

Hannaford’s cookbook “30 Days on $200”(2) promotes healthy eating for one person on a budget

Hannaford supported the publication of a cookbook entitled “30 Days on $200”. The cookbook provides a shopping list, recipes built with these groceries, a 30-day meal

planner, money-saving tips, and other resources for healthy eating on a very limited budget.

“What we think is so powerful about this cookbook is that it

helps people to make the most of their food and to stretch limited budgets,” said a member of the grocer’s Healthy Living Team. “Hannaford is proud to support this project because it is such a great fit with our Values of encouraging

healthy choices, supporting the community and increasing access to nutritious food.”

Alfa Beta introduces new bio products and product lines to better meet

customer needs

Alfa Beta in Greece continues to put customers first and emphasize local production by introducing new bio products and product lines. As well as

lactose free products, this included the introduction of new wines specially selected by Alfa Beta wine experts and offered exclusively in Alfa Beta stores.

(1)

Does not include 66 Bottom Dollar Food Stores. In November 2014, Delhaize Group signed an agreement to sell its Bottom Dollar Food Store locations to ALDI Inc. The stores were closed on January 12, 2015 and the transaction completed early 2015.

(2) Prices are estimates from 2014 and are subject to change.

LEARN TO GROW

We continuously strive to further limit the impact of our activities on the environment and use innovation to meet our 2020 Supergood goals. We research, analyze

and apply innovation to improve the nutritional value and sustainability of our private brands.

Sourcing sustainable seafood and being a responsible neighbor

The value of the retail market for sustainable seafood is growing, and increased use of sustainable fisheries management is beginning to improve the future for

fish stocks and marine ecosystems. To meet customer demand, our goal is to ensure our private brand seafood products are fully traceable to the fishery or farm of origin and 90% from sustainable sources by 2020.

In 2009, both Delhaize Belgium and Delhaize America launched their commitments to meet ambitious sustainable seafood targets by 2012, which they achieved. These commitments include

policies on full traceability and responsible harvesting of fresh seafood products, including partnering with organiza-

BEING SUPERGOOD BY HELPING LOCAL

COMMUNITIES

Being Supergood means we will help local communities to thrive by innovating to minimize our impacts on the environment, such as the amount of energy

we use, the amount and type of refrigerants we use, and the amount of waste we produce. This helps address global challenges like climate change, improves local environments, and delivers cost savings for our business. Meeting our Supergood ambition

also means we will lead locally by improving the nutritional value and sustainability of customers’ favorite private brands.

90%

private brand seafood products from sustainable sources by 2020

Hannaford’s cookbook

“30 Days on $200” promotes healthy eating for one person on a budget.

STRATEGY

tions to improve fisheries. In

collaboration with fishermen in northern Greece and WWF, Alfa Beta launched its commitment to sustainable fishing practices in 2013. This is the first time this kind of program is being implemented in the Mediterranean Sea. Super Indo in Indonesia

also launched in 2014 its sustainable seafood sourcing guidelines and plan for 2020.

Super Indo leads locally in recycling

Delhaize Group has been recycling waste in our stores for decades, and now Super Indo has taken this to new heights. The banner is leading locally as the first supermarket in

Indonesia to make a natural fertilizer on site from leftover fruit and vegetables. Forty-six stores across the country now have their own composting facility to reduce and recycle food waste. No chemicals are used in the process and customers can

take home the natural fertilizer free of cost to use in their gardens.

DELHAIZE GROUP’S 2020 SUSTAINABILITY GOALS

Our 2020 Supergood (Sustainability) Goals in the areas of zero waste and greenhouse gas emissions include the following:

80% of our waste will be recycled;

100% of stores and warehouses will have food donation

programs in place to maximize the amount of surplus food that is donated to food recovery charities;

20% reduction in CO2 -equivalent emissions per m2 of sales

area (against a 2008 baseline);

and refrigerants will be 80% ozone-friendly and with a reduced average global warming potential.

+ € 41 M

spent in capex in 2014

46

Super Indo stores have facilities to recycle food waste

Our sustainable seafood commitments include full traceability and responsible harvesting of fresh seafood.

Delhaize Group Annual Report 2014 • 25

LEAD

LOCALLY

Being an integral part of our local communities is central to who we are as a company and giving back is important for all of our stakeholders.

Innovative projects from Delhaize Group associates propose local and sustainable solutions to everyday problems

In July 2013, the jury of Delhaize Group’s Sustainability Innovation Fund selected eight sustainability projects that began implementation in 2014. The project highlighted

below is only one example of the projects implemented through the Sustainability Innovation Fund in 2014.

Delhaize America (DA) develops a sustainable strategy

around the Nature’s Place product range

Proposed by members of Delhaize America’s “Our Brands” team this project aims to identify consumer

needs, purchasing habits and concerns about sustainable grocery products. In 2014, Delhaize America’s “Our Brands” department ran a survey with different groups of customers (DA and non-DA consumers) to identify expectations in terms

of sustainability for the Nature’s Place brand and made changes to meet customer expectations where possible. For example, the survey showed that customers expect packaging to be made from recycled material and/or to be easily recyclable. As a

result, the team decided to partner with GreenBlue, an organization that will help identify peers’ practices, advise on packaging redesign, and clarify the environmental impact of the current packaging material.

DRIVE PROFITABLE GROWTH TODAY AND BEYOND

We invest locally. In 2013 we spent

€565 million in capex and we increased this spend to €606 million in 2014. And, as neighborhoods evolve, we drive growth by providing stores that meet the needs of those who live there.

Proxy Delhaize goes urban to meet local needs

Proxy Urban Delhaize is a new store format

concept introduced in Belgium in 2014 which grew out of the successful Proxy Delhaize.

Proxy Delhaize is a neighborhood store, independently owned and often open

on Sundays but with access to Delhaize’s operational expertise. Proxy Urban Delhaize stocks about 50% of Delhaize brands with a focus on fresh products and speedy checkout. It attracts two types of customers, both office workers who work in the

area, and local residents who use it when they need a few items quickly.

Delhaize Group associates are an integral part of their local communities.

ENGAGING DIALOGUE WITH SUSTAINABILITY STAKEHOLDERS

As part of its ambition to be a Supergood

company, Delhaize Group organized a sustainability stakeholder event: “Sustainability and private brands” in December 2014. The half-day workshop in Brussels was attended by representatives from private brand suppliers, non-governmental

organizations (NGOs), and external advisors. The majority of the workshop was conducted through both small and large-group discussions to identify where we can improve our approach and also how we can engage better with suppliers and customers on

sustainability. Organizing meetings like this is part of our ongoing work to engage in dialogue with key external stakeholders. It helps us stay aware of our stakeholders’ opinions and how sustainability issues are evolving for our industry and

our customers.

The positive feedback and ideas from stakeholders as well as from top management will help us to strengthen our projects to increase the health,

sustainability, and affordability of our private brands in the future.

STRATEGY

SHAREHOLDERS

TRUST US FOR VALUE CREATION

We pursue profitable sales growth and allocate human, financial,

and natural resources effectively to improve our cost position.

REVENUES(1) (IN BILLIONS OF €)

20.5 20.6 21.4

12 13 14(1)

UNDERLYING OPERATING PROFIT(1) (IN MILLIONS OF €)

845 789 762

12 13 14(1)

(1) Including 53rd week in the United States.

We meet this Promise by delivering on commitments to our shareholders, creating value by growing and expanding our business. We exercise discipline in resource allocation and use

our scale to reduce our costs in order to ensure profitable and sustainable growth. By doing so, we expect our shares to earn an attractive return for our shareholders. The following pages illustrate how we keep this Promise to our shareholders and

ensure that they are confident that Delhaize Group shares are a good investment.

PUT CUSTOMERS FIRST

Putting customers first is at the heart of our business and the way we accelerate organic growth, while improving our price position and perception. Our approach to e-commerce is

how we differentiate ourselves from our competitors and provide our customers with an easy and convenient way to shop using new and innovative tools.

Hannaford-to-Go

Hannaford focused in 2014 on expanding its e-commerce

capabilities by taking its successful Hannaford-to-Go online ordering system from the pilot stage to roll-out. In 2014, this curbside pick-up service expanded from two stores to 11 in three states. The growth in this service lays a foundation for

further growth in the service across Hannaford’s market area in 2015.

LEARN TO GROW

Joining Coopernic to generate cost savings

We have joined Coopernic, the European buying

alliance, to generate additional cost savings beginning in January 2015. This is expected to lead to further efficiencies in the areas of private brand innovation and development; improved commercial terms with international suppliers; and synergies

in non-food procurement. Our customers will benefit from the cost savings we generate.

Delhaize Group Annual Report 2014 • 27

LEAD

LOCALLY

Renovation of Alfa Beta flagship store

In 2014, there has been a vast

rethinking of product categories with Alfa Beta introducing new concepts as well as new product lines. More specifically, the renovation of our Elliniko store (Athens), one of the largest Alfa Beta stores, established a whole new store concept:

Products in bulk such as dry nuts, premium chocolate, coffee and tea as well as the usual categories of products, adding a significant competitive advantage;

A newly developed special beverage area in the same store accommodates an extensive assortment from Greek and international vineyards and even has a controlled

temperature room to store premium wines as well as a vending machine for testing wines;

An on-site bakery and an in-store pastry shop that offers a wide range of

custom recipes and extremely fresh products;

Unprecedented varieties of local and imported cheese, various deli products as well as marinated fresh fish and meat

with a strong relationship between quality and price.

Our new distribution center in Serbia will strengthen operational efficiency and improve Delhaize

Serbia’s ability to provide the best in fresh products to customers.

DOW JONES SUSTAINABILITY INDEX

The Dow Jones Sustainability Index measures company performance in economic, social, and environmental dimensions. The top 10% of performers in each sector are selected for the

World Index. Our efforts were recognized during the previous two years and therefore we made it into the DJSI. In 2014 however, we fell short. In 2015, our goal is to get back in the DJSI, recognized again as a leader in our sector. In order to do

so we will be using the DJSI more clearly as a benchmark tool to identify improvements in how we manage environmental and social topics across the business. Our investors will benefit as being a sustainable retailer positions us for stronger future

business performance.

BEING SUPERGOOD BY DOING GOOD BUSINESS

Our Supergood

goals, especially in the areas of sustainable private brands and zero waste help us to uncover new sales opportunities and push us to operate more efficiently. Being Supergood is, quite simply, good business.

DRIVE PROFITABLE GROWTH TODAY AND BEYOND

Opening a new distribution center in Serbia

Our new distribution center (DC) in Serbia, which opened in November 2014, will strengthen our operational efficiency and profitability and provide fresh products

to our customers. Delhaize Group invested €50 million in the construction of the distribution center. A key priority for the distribution center was to transfer our international experience and knowledge in this area to the Serbian market

and through this continue running our operations at the highest standards. The DC will serve around 800 suppliers and employ 750 people by 2020; around 400 associates worked in the DC at the end of 2014. In line with our Supergood sustainability

strategy, the distribution center was built with environmentally-responsible construction materials, energy efficient heating and cooling systems, LED lights and motion sensor systems – part of our commitment to buildings with lower

environmental footprints.

STRATEGY

SHAREHOLDER

INFORMATION

Delhaize Group shares trade on NYSE Euronext Brussels under the symbol DELB.

American Depositary Shares (ADS) are traded on the New York Stock Exchange under the symbol DEG.

ADSs are evidenced by American Depositary Receipts (ADRs).

Information on delhaize group’s share price can be found on the websites of Delhaize Group (www.delhaizegroup.com), NYSE Euronext Brussels (www. euronext.com)

and the New York Stock Exchange (www.nyse.com). Detailed information on trading activity and share prices can also be found in the financial section of many newspapers.

Share Performance in 2014

On December 31, 2014, the closing price of Delhaize

Group’s ordinary share on NYSE Euronext Brussels was €60.43, an increase of 39.9% compared to €43.20 a year earlier. During the same period, the Euro Stoxx 50 index increased by 1.2% and the Bel20 index increased by 12.4%. The FTSE

Eurofirst 300 Food and Drug Retailers Index decreased by 23.8% in 2014. In 2014, Delhaize Group shares traded on NYSE Euronext Brussels at an average closing price of €51.96 and an average daily trading volume of 415 986 shares.

Since April 7, 2014, 4 Delhaize Group ADRs trade for 1 Delhaize Group share (before that, 1 Delhaize Group ADR traded for 1 Delhaize Group share). On December 31, 2014,

the closing price of Delhaize Group’s ADRs on the New York Stock Exchange was $18.12, 22.0% higher than the closing price on December 31, 2013 ($59.42 or $14.86 adjusted for the 4:1 ADR ratio split). In the same period, the S&P 500

index increased by 11.4%, and the S&P 500 Food and Staples Retailing Index increased by 21.0%. From April 7, 2014 (the date of the ADR ratio split) to December 31, 2014, the average daily trading volume of Delhaize Group ADRs was 64

855.

Equity Indices

On December 31, 2014, Delhaize Group’s shares

were included in the following major stock indices: BEL20, Euronext 100 and the Dow Jones Stoxx 600.

SHARE PRICE EVOLUTION (2014 - IN €)

Delhaize Group share (DELB) EURONEXT 100

70 65 60 55 50 45 40 35 30

J F M A M J J A S O N D

SHARE PRICE EVOLUTION (2014 - IN $)

Delhaize Group ADR (DEG) S&P 500

20 19 18 17 16 15 14 13 12

J F M A M J J A S O N D

Delhaize Group Annual Report 2014 • 29

On

December 31, 2014, the weight of Delhaize Group shares in the BEL20 index was 6.5%. Delhaize Group shares represented the 7th largest constituent in the index.

On December 31, 2014, the weight of Delhaize Group in the Euronext 100 index was 0.31%. Delhaize Group represented the 76th largest constituent in the index.

Dividend

The dividend policy of Delhaize Group is to pay out approximately

35% of underlying Group share in net profit from continuing operations.

At the Ordinary Shareholders’ Meeting to be held on May 28, 2015, the Board of

Directors will therefore propose the payment of a gross dividend of €1.60 per share, compared to €1.56 the previous year. After deduction of 25% Belgian withholding tax, this will result in a net dividend of €1.20 per share

(€1.17 the prior year).

The net dividend of €1.20 per share will be payable to owners of ordinary shares against coupon no. 53. The Delhaize Group

shares will start trading ex-coupon on June 2, 2015 (opening of the market). The record date (i.e. the date at which shareholders are entitled to the dividend) is June 3, 2015 (closing of the market) and the payment date is June 4,

2015. The payment will be made at the registered office of the Company (rue Osseghem / Osseghemstraat 53, 1080 Brussels, Belgium) as well as through all Belgian financial institutions.

For shares held through a share account, the bank or broker will automatically handle the dividend payment.

The payment of the dividend to the ADR holders will be made through Citibank.

Type of Delhaize

Group Shares

Delhaize shares can be held in two different forms: dematerialized form or registered shares. Dematerialized shares are shares that can only be

represented by entries into an account in the book of a depositary institution. Registered shares are shares that can only

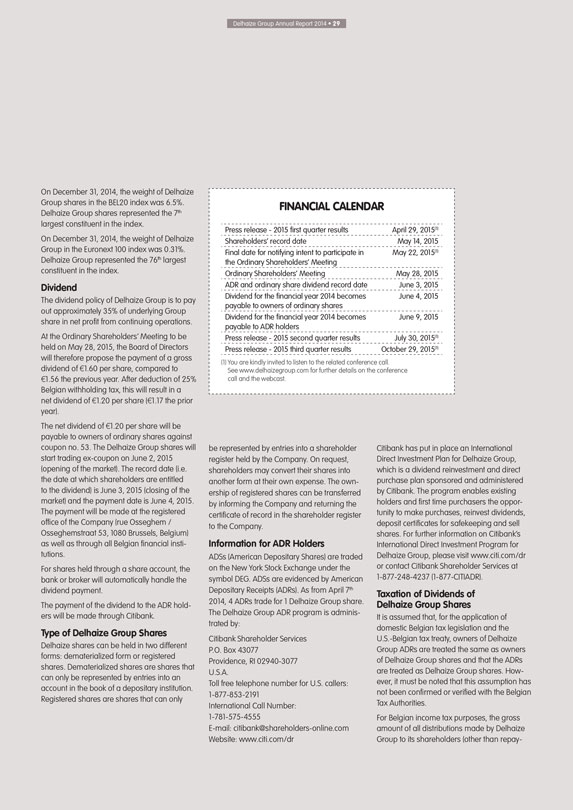

FINANCIAL CALENDAR

Press release - 2015 first quarter results April 29, 2015(1)

Shareholders’ record date

May 14, 2015

Final date for notifying intent to participate in the Ordinary Shareholders’ Meeting May 22, 2015(1)

Ordinary Shareholders’ Meeting May 28, 2015

ADR and ordinary share dividend record date

June 3, 2015

Dividend for the financial year 2014 becomes payable to owners of ordinary shares June 4, 2015

Dividend for the financial year 2014 becomes payable to ADR holders June 9, 2015

Press release

- 2015 second quarter results July 30, 2015(1)

Press release - 2015 third quarter results October 29, 2015(1)

(1) You are kindly invited to listen to the related conference call. See www.delhaizegroup.com for further details on the conference call and the webcast.

be represented by entries into a shareholder register held by the Company. On request, shareholders may convert their shares into another form at their own expense. The ownership

of registered shares can be transferred by informing the Company and returning the certificate of record in the shareholder register to the Company.

Information

for ADR Holders

ADSs (American Depositary Shares) are traded on the New York Stock Exchange under the symbol DEG. ADSs are evidenced by American Depositary

Receipts (ADRs). As from April 7th 2014, 4 ADRs trade for 1 Delhaize Group share. The Delhaize Group ADR program is administrated by:

Citibank Shareholder

Services

P.O. Box 43077

Providence, RI 02940-3077

U.S.A.

Toll free telephone number for U.S. callers:

1-877-853-2191

International Call Number:

1-781-575-4555

E-mail: [email protected]

Website: www.citi.com/dr

Citibank has put in place an International Direct Investment Plan for

Delhaize Group, which is a dividend reinvestment and direct purchase plan sponsored and administered by Citibank. The program enables existing holders and first time purchasers the opportunity to make purchases, reinvest dividends, deposit

certificates for safekeeping and sell shares. For further information on Citibank’s International Direct Investment Program for Delhaize Group, please visit www.citi.com/dr or contact Citibank Shareholder Services at 1-877-248-4237

(1-877-CITIADR).

Taxation of Dividends of Delhaize Group Shares

It is assumed

that, for the application of domestic Belgian tax legislation and the U.S.-Belgian tax treaty, owners of Delhaize Group ADRs are treated the same as owners of Delhaize Group shares and that the ADRs are treated as Delhaize Group shares. However, it

must be noted that this assumption has not been confirmed or verified with the Belgian Tax Authorities.

For Belgian income tax purposes, the gross amount of all

distributions made by Delhaize Group to its shareholders (other than repay-

STRATEGY

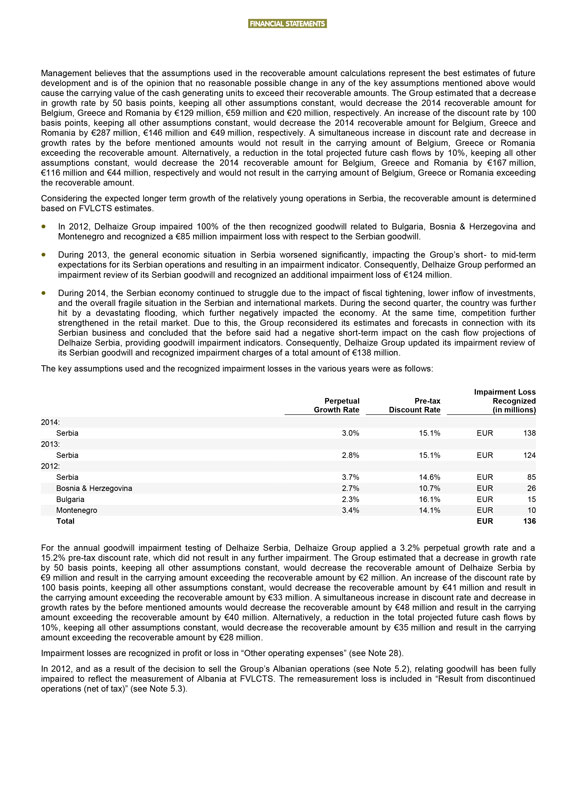

€ 1.60 gross dividend for 2014