Form S-1/A American Resources Corp

Tweet

Tweet Share

Share

As filed with the U.S. Securities and Exchange Commission on

February 14, 2019

Registration No. 333-226042

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington

D.C. 20549

FORM S-1/A

(Amendment No.

8)

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

-------------------------------------------

American Resources Corporation

(Exact

name of registrant as specified in its charter)

-----------------------------------------

|

Florida

|

1200

|

46-3914127

|

|

(State

or other jurisdiction of incorporation or

organization)

|

(Primary

Standard Industrial Classification Code Number)

|

(I.R.S.

Employer Identification Number)

|

-----------------------------------------

9002 Technology Lane

Fishers, IN 46038

Tel.: (317) 855-9926

(Address,

including zip code, and telephone number,

including

area code, of registrant’s principal executive

offices)

-----------------------------------------

Clifford J. Hunt

Law Office of Clifford J. Hunt, P.A.

8200 Seminole Boulevard

Seminole, Florida 33772

(727) 471-0444

(Name,

address, including zip code, and telephone number, including area

code, of agent for service)

-----------------------------------------

Copies

to:

|

Clifford

J. Hunt

Law

Office of Clifford J. Hunt, P.A.

8200

Seminole Boulevard

Seminole,

Florida 33772

(727)

471-0444

|

Mitchell

S. Nussbaum

Loeb

& Loeb LLP

345

Park Avenue

New

York, NY 10154

(212)

407-4000

|

----------------------------------------

Approximate date of commencement of proposed sale of the securities

to the public: As soon as practicable after the effective

date of this Registration Statement.

If any

of the securities being registered on this Form are to be offered

on a delayed or continuous basis pursuant to Rule 415 under the

Securities Act of 1933, check the following box: ☑

If this

Form is filed to register additional securities for an offering

pursuant to Rule 462(b) under the Securities Act, check the

following box and list the Securities Act registration statement

number of the earlier effective registration statement for the same

offering. ☐

If this

Form is a post-effective amendment filed pursuant to Rule 462(c)

under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier

effective registration statement for the same offering.

☐

If this

Form is a post-effective amendment filed pursuant to Rule 462(d)

under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier

effective registration statement for the same offering.

☐

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of

“large accelerated filer,” “accelerated

filer,” “smaller reporting company,” and

“emerging growth company” in Rule 12b-2 of the

Securities Exchange Act of 1934.

|

Large

accelerated filer ☐

|

Accelerated

filer ☐

|

|

Non-accelerated

filer ☐

|

Smaller

reporting company ☑

|

|

Emerging

Growth Company ☑

|

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 7(a)(2)(B) of the Securities Act. ☑

The

registrant hereby amends this Registration Statement on such date

or dates as may be necessary to delay its effective date until the

registrant shall file a further amendment that specifically states

that this Registration Statement shall thereafter become effective

in accordance with Section 8(a) of the Securities Act of 1933, as

amended, or until this Registration Statement shall become

effective on such date as the Securities and Exchange Commission,

acting pursuant to said Section 8(a), may determine.

THE INFORMATION IN THIS PROSPECTUS IS NOT COMPLETE AND MAY BE

CHANGED. WE MAY NOT SELL THESE SECURITIES UNTIL THE REGISTRATION

STATEMENT FILED WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION IS

EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES

AND WE ARE NOT SOLICITING OFFERS TO BUY THESE SECURITIES IN ANY

STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

SUBJECT TO COMPLETION, DRAFT DATED FEBRUARY 14, 2019

PRELIMINARY PROSPECTUS

1,000,000 Shares

American Resources Corporation

Class A Common Stock

______________________

This is a public offering of the Class A Common

stock (or also referred to as “common stock”) of

American Resources Corporation, a Florida corporation. Prior to

this offering, there has been limited public market for our common

stock on the OTC Markets under the ticker AREC. We are

selling up

to [

] shares

of common stock. There are no selling shareholders in this

offering.

Our

common stock is currently quoted on the OTC Market Group,

Inc.’s OTC Pink tier under the symbol “AREC”.

On February 13, 2019, the last reported sale price of our

common stock was $12.50 per share. We expect the public offering

price per share in this offering will be between $4.00 to $6.00. We

have applied to list our common stock on The NASDAQ Capital Market

under the symbol “AREC”. No assurance can be given that

our application will be approved.

We are an “emerging growth company” as

that term is used in the Jumpstart Our Business Startups Act

of 2012, and as such, we have

elected to take advantage of certain reduced public company

reporting requirements for this prospectus and future filings. See

“Risk Factors” and “Prospectus

Summary—Emerging Growth Company.”

Investing in our common stock involves risks. See “Risk

Factors” on page 7.

Neither

the Securities and Exchange Commission nor any state securities

commission has approved or disapproved of these securities or

determined if this prospectus is truthful or complete. Any

representation to the contrary is a criminal offense.

______________________

|

|

Per

Share

|

Total

|

|

Public offering

price

|

$ 6.00

|

$ 6,000,000$

|

|

Underwriting

discount(1)

|

$ 0.42

|

$ 420,000

|

|

Proceeds before

expenses

|

$ 5.58

|

$ 5,580,000

|

———————

(1) In addition to the

underwriting discount, we have agreed to issue to the

representative of the underwriters warrants to purchase a number of

shares of common stock equal to 7% of the total number of shares

being sold in the offering, including the over-allotments, if any,

and to reimburse the underwriters for expenses incurred by them.

See “Underwriting” beginning on page 51 of this

prospectus for additional information regarding total underwriter

compensation.

We have

granted the underwriters the option for a period of 45 days to

purchase additional shares of common stock (up to 15.0% of the

number of shares of common stock sold in the primary offering)

solely to cover over-allotments, if any (the

“Over-Allotment”).

The

underwriters expect to deliver our shares to purchasers in the

offering on or about February 14, 2019, subject to customary

closing conditions.

MAXIM GROUP, LLC

Lead Bookrunning Manager

The date of this prospectus

is February

14, 2019

TABLE OF CONTENTS

|

ABOUT THIS PROSPECTUS

|

4

|

|

OTHER INFORMATION

|

4

|

|

PROSPECTUS SUMMARY

|

5

|

|

RISK FACTORS

|

8

|

|

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING

STATEMENTS

|

41

|

|

USE OF PROCEEDS

|

44

|

|

CAPITALIZATION

|

45

|

|

INFORMATION WITH RESPECT TO THE REGISTRANT

|

46

|

|

DESCRIPTION OF PROPERTY

|

65

|

|

MARKET PRICE OF AND DIVIDENDS ON THE REGISTRANT'S COMMON EQUITY AND

RELATED STOCKHOLDER MATTERS

|

65

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

|

66

|

|

DIRECTORS AND EXECUTIVE OFFICERS

|

87

|

|

EXECUTIVE COMPENSATION

|

91

|

|

DESCRIPTION OF SECURITIES

|

93

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND

MANAGEMENT

|

96

|

|

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS, DIRECTOR

INDEPENDENCE

|

97

|

|

UNDERWRITING

|

99

|

|

DETERMINATION OF OFFERING PRICE

|

102

|

|

INTERESTS OF NAMED EXPERTS AND COUNSEL

|

103

|

|

WHERE YOU CAN FIND MORE INFORMATION

|

104

|

|

DISCLOSURE OF COMMISSION POSITION ON INDEMNIFICATION FOR SECURITIES

ACT LIABILITIES

|

104

|

|

INDEX TO FINANCIAL STATEMENTS

|

F-1

|

-----------------------------------------

You should rely only on the information contained in this

prospectus and any free writing prospectus prepared by us or on

behalf of us or the information to which we have referred you.

Neither we, nor the underwriters have authorized anyone to provide

you with information different from that contained in this

prospectus and any free writing prospectus. We take no

responsibility for, and can provide no assurance as to the

reliability of, any other information that others may give you. We

and the underwriters are offering to sell shares of common stock

and seeking offers to buy shares of common stock only in

jurisdictions where offers and sales are permitted. The information

in this prospectus is accurate only as of the date of this

prospectus, regardless of the time of delivery of this prospectus

or any sale of the common stock. Our business, financial condition,

results of operations and prospects may have changed since that

date.

This prospectus contains forward-looking statements that are

subject to a number of risks and uncertainties, many of which are

beyond our control. See “Risk Factors” and

“Cautionary Statement Regarding Forward-Looking

Statements.”

3

Certain

Terms Used in this Prospectus

All

references in this prospectus to:

●

“American

Resources Corporation,” the “Company,”

“ARC”, “AREC”, “us,”

“we,” “our,” or “ours” or like

terms when used in the present tense or prospectively refer to

American Resources Corporation and its subsidiaries, including its

wholly-owned subsidiary, Quest Energy Inc. American Resources

Corporation is the issuer in this offering.

●

“Common

shares,” “common stock” or “Common

Stock” refers to the Class A common stock of the Company, par

value $0.0001, as defined in the Company’s Articles of

Incorporation, as amended. There is no other class of common shares

of the Company authorized or issued other than the Class A common

stock. The term “stock” and “shares” are

used interchangeably.

●

“Coal mining

permits” refers to permits from Kentucky Department of

Natural Resources or Indiana Department of Natural Resources (as

the case may be) and includes permits for coal extraction,

processing, rail loading, and storage of refuse and/or

slurry.

●

Tons refer to short

tons, unless otherwise indicated.

●

We have not

classified the coal we control as either “proven” or

“probable” as defined in the United States Securities

and Exchange Commission Industry Guide 7, and as a result, do not

have any “proven” or “probable” reserves

under such definition and are classified as an “Exploration

Stage” pursuant to Industry Guide 7. Therefore, any

references to coal in this filing refers to an undetermined coal

deposit that has not been deemed proven or

probable.

You

should only rely on the information contained in this document or

to which we have referred you. We have not authorized anyone to

provide you with information otherwise. If anyone provides you with

different or inconsistent information, you should not rely on it.

We are not making an offer to sell these securities in any

jurisdiction where the offer or sale is not permitted.

OTHER INFORMATION

Our

website address is www.americanresourcescorp.com. We expect to make

our periodic reports and other information filed with or furnished

to the Securities Exchange Commission (“SEC”),

available free of charge through a link on our website as soon as

reasonably practicable after those reports and other information

are electronically filed with or furnished to the SEC. Information

on our website or any other website is not incorporated by

reference into, and does not constitute a part of, this

prospectus.

4

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in

this prospectus. You should read the entire prospectus carefully,

including the information under the headings “Risk

Factors,” “Cautionary Statement Regarding

Forward-Looking Statements” and “Management’s

Discussion and Analysis of Financial Condition and Results of

Operations” and the financial statements and the notes to

those financial statements appearing elsewhere in this prospectus.

The information presented in this prospectus assumes a public

offering price of $4.00 per common share.

About

Us

We are

a low-cost producer of primarily high-quality, metallurgical coal

in eastern Kentucky. We began our Company on October 2, 2013 and

changed our name from Natural Gas Fueling and Conversion Inc. to

NGFC Equities, Inc. on February 25, 2015, and then changed our name

from NGFC Equities, Inc. to American Resources Corporation on

February 17, 2017. On January 5, 2017, ARC executed a Share

Exchange Agreement between the Company and Quest Energy Inc., a

private company incorporated in the State of Indiana with offices

at 9002 Technology Lane, Fishers IN 46038, and due to the

fulfillment of various conditions precedent to closing of the

transaction, the control of the Company was transferred to the

Quest Energy shareholders on February 7, 2017 resulting in Quest

Energy becoming a wholly-owned subsidiary of ARC. Through its

wholly-owned subsidiary Quest Energy, which is an Indiana

corporation founded in June 2015, ARC was able to acquire coal

mining and coal processing operations, substantially all located in

eastern Kentucky. A majority of our domestic and international

target customer base includes blast furnace steel mills and coke

plants, as well as international metallurgical coal consumers,

domestic electricity generation utilities, and other industrial

customers.

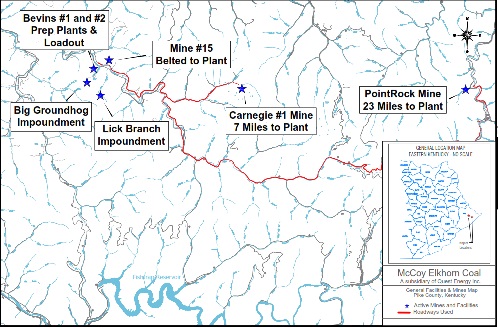

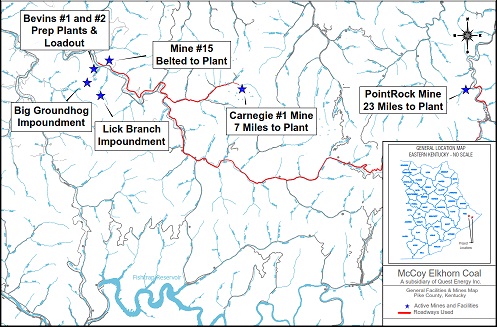

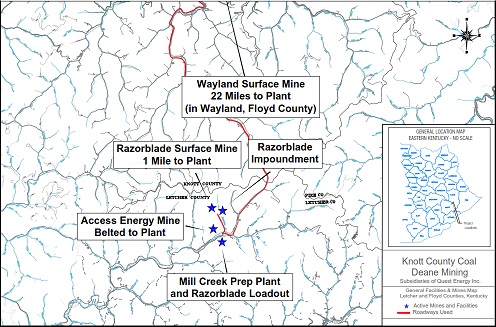

We

achieved initial commercial production of metallurgical coal in

September 2016 from our McCoy Elkhorn Mine #15 and from our McCoy

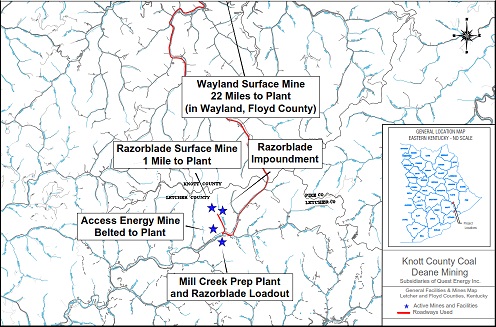

Elkhorn Carnegie 1 Mine in March 2017. In October 2017 we achieved

commercial production of thermal coal from our Deane Mining Access

Energy Mine and from our Deane Mining Razorblade Surface Mine in

May 2018. We believe that we will be able to take advantage of

recent increases in U.S. and global benchmark metallurgical and

thermal coal prices and intend to opportunistically increase the

amount of our projected production that is directed to the export

market to capture favorable differentials between domestic and

global benchmark prices. The Company commenced operations of two

out of four of its internally owned preparation plants in July of

2016 (Bevins #1 and Bevins #2 Prep Plants at McCoy Elkhorn), with a

third preparation plant commencing operation in October 2017 (Mill

Creek Prep Plant at Deane Mining).Pursuant to the definitions in

Paragraph (a) (4) of the Securities and Exchange Commission's

Industry Guide 7, our company and its business activities are

deemed to be in the exploration stage until mineral reserves are

defined on our properties.

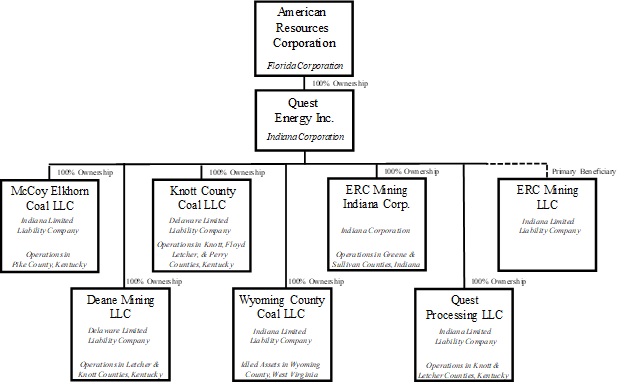

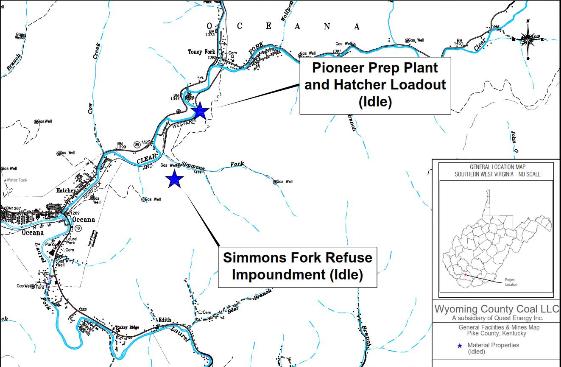

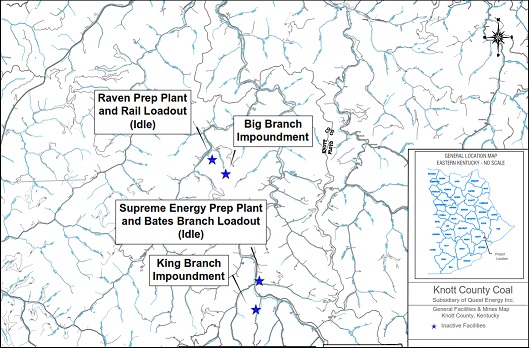

Current Projects

Quest

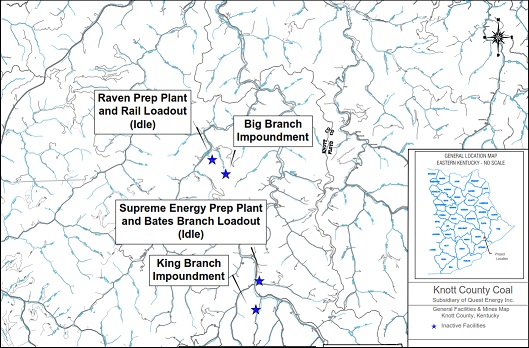

Energy has six coal mining and processing operating subsidiaries:

McCoy Elkhorn Coal LLC (doing business as McCoy Elkhorn Coal

Company, “McCoy Elkhorn”), Knott County Coal LLC

(“Knott County Coal”), Deane Mining LLC (“Deane

Mining”), ERC Mining Indiana Corporation (“ERC”),

Wyoming County Coal LLC (“Wyoming County Coal”), and

Quest Processing LLC (“Quest Processing”), all of which

are located in eastern Kentucky and West Virginia within the

Central Appalachian coal basin, with the exception of ERC Mining

Indiana Corporation, which is located in southwestern Indiana in

the Illinois coal basin. Below is an organizational and ownership

chart of our Company.

5

The

coal deposits under control by the Company generally comprise of

metallurgical coal (used for steel making), pulverized coal

injections (“PCI”, used in the steel making process)

and high-BTU, low sulfur, low moisture bituminous coal used for a

variety of uses within several industries, including industrial

customers, specialty products and thermal coal used for electricity

generation.

Emerging Growth Company

We are

an “emerging growth company” as defined in the

Jumpstart Our Business Startups Act (the “JOBS Act”).

For as long as we are an emerging growth company, unlike public

companies that are not emerging growth companies under the JOBS

Act, we will not be required to:

●

provide an

auditor’s attestation report on management’s assessment

of the effectiveness of our system of internal control over

financial reporting pursuant to Section 404(b) of the

Sarbanes-Oxley Act of 2002;

●

provide more than

two years of audited financial statements and related

management’s discussion and analysis of financial condition

and results of operations;

●

comply with any new

requirements adopted by the Public Company Accounting Oversight

Board (the “PCAOB”) requiring mandatory audit firm

rotation or a supplement to the auditor’s report in which the

auditor would be required to provide additional information about

the audit and the financial statements of the issuer;

●

provide certain

disclosure regarding executive compensation required of larger

public companies or hold stockholder advisory votes on the

executive compensation required by the Dodd-Frank Wall Street

Reform and Consumer Protection Act (the “Dodd-Frank

Act”); or

●

obtain stockholder

approval of any golden parachute payments not previously

approved.

We will

cease to be an emerging growth company upon the earliest

of:

●

the last day of the

fiscal year in which we have $1.0 billion or more in annual

revenues;

●

the date on which

we become a “large accelerated filer” (the fiscal

year-end on which the total market value of our common equity

securities held by non-affiliates is $700 million or more as of our

most recently completed second fiscal quarter);

●

the date on which

we issue more than $1.0 billion of non-convertible debt over a

three-year period; or

●

the last day of the

fiscal year following the fifth anniversary of our initial public

offering.

6

In

addition, Section 107 of the JOBS Act provides that an emerging

growth company can take advantage of the extended transition period

provided in Section 7(a)(2)(B) of the Securities Act of 1933, as

amended (the “Securities Act”), for complying with new

or revised accounting standards, but we intend to irrevocably opt

out of the extended transition period and, as a result, we will

adopt new or revised accounting standards on the relevant dates in

which adoption of such standards is required for other public

companies.

|

Total common stock offered by the Company

|

Up to 1,150,000 shares of Class A Common Stock, assuming the

underwriter’s Over-Allotment option is fully

exercised.

|

|

Use of proceeds

|

We expect to receive approximately $6,000,000

of gross proceeds, based upon the

offering price of $6.00 per share, and after deducting the underwriting

discount of $420,000,

we expect to receive approximately $5,580,000.

If the underwriters fully exercise their right to purchase

additional shares of common stock, we estimate that we will receive

gross proceeds of $6,900,000

from the sale of the common stock and net proceeds of

$4,278,000

after deducting $483,000

for underwriting discounts and commissions. The Company will use the proceeds of this offering

to fund organic and acquisitive growth and other uses as described

in the “Use of Proceeds” section. The Company will use

the proceeds, among other things, to initiate coal production on

certain permits the Company owns and act upon certain acquisition

opportunities, both those that are in close proximity to our

current operations and those that would create another

“hub” from which we can enhance business expansion. We

have not yet made final investment decisions with respect to any of

these potential projects and we cannot currently allocate specific

percentages of the net proceeds that we may use for the purposes

described above.

Please read “Use of Proceeds.”

|

|

Dividend policy

|

While we have not paid any dividends on our common stock since our

inception, our longer-term objective is to pay dividends in order

to enhance stockholder returns when the Board of Directors deems

such action as in the best interest of its shareholders. Please

read “Dividend Policy.”

|

|

Listing and trading symbol

|

Currently our stock is listed on the OTC Markets OTC Pink

tier under the ticker “AREC”. We have applied for a

listing on the NASDAQ Capital Market under the symbol

“AREC”.

|

|

Risk factors

|

You should carefully read and consider the information set forth

under the heading “Risk Factors” and all other

information set forth in this prospectus before deciding to invest

in our common stock.

|

The

information above does not include 4,000,000 shares of Class A

Common Stock reserved for issuance pursuant to the Employee

Incentive Stock Option Plan, 636,830 of which are issued as of the

date of this document.

7

RISK FACTORS

Investing in our common stock involves risks. You should carefully

consider the information in this prospectus, including the matters

addressed under “Cautionary Statement Regarding

Forward-Looking Statements,” and the following risks before

making an investment decision. The trading price of our common

stock could decline and our ability to pay dividends may be reduced

due to any of these risks, and you may lose all or part of your

investment.

Risks Associated with Small Company Size and Liquidity

Risks

As a start-up or development stage company, our business and

prospects are difficult to evaluate because we have a very limited

operating history and our business model is evolving, an investment

in us is considered a high-risk investment whereby you could lose

your entire investment.

We have

recently commenced operations and, therefore, we are considered a

“start-up” or “development stage” company.

We have had limited income from the sale of the coal from our

mining operations. We will incur significant expenses in order to

implement our business plan. As an investor, you should be aware of

the difficulties, delays and expenses normally encountered by an

enterprise in its development stage, many of which are beyond our

control, including unanticipated developmental expenses, and

advertising and marketing expenses. We cannot assure you that our

proposed business plan will materialize or prove successful, or

that we will ever be able to operate profitably. If we cannot

operate profitably, you could lose your entire

investment.

We have limited assets, have incurred operating losses and have

limited current sources of revenue.

We

have limited assets and limited revenues since our inception in

2015. Since our inception, we have incurred annual

operating losses. As of the end of the 9 months ending

on September 30, 2018, our unaudited net loss from operations was

$8,869,858. We have only recently started generating

revenue and such revenue is concentrated among a small number of

customers and a small number of operations. We can provide no

assurance that any of our current or future assets will produce any

material revenues for our stockholders, or that any such business

will operate on a profitable basis.

Our results of operations have not resulted in profitability and we

may not be able to achieve profitability going

forward.

We

have had net losses in each quarter since our inception. We expect

that we will continue to incur net losses for the foreseeable

future. We may incur significant losses in the future for a number

of reasons, including the other risks described in this prospectus,

and we may encounter unforeseen expenses, difficulties,

complications, delays and other unknown events. Accordingly, we may

not be able to achieve or maintain profitability. Our business is

early development stage, consisting of the development, marketing,

and sale of our coal. There is no assurance that even if we

successfully implement our business plan, that we will be able to

curtail our losses. Further, as we are a development

stage enterprise, we expect that net losses and the working capital

deficiency will continue. If we incur additional significant

operating losses, our stock price may decline, perhaps

significantly.

8

We have yet to achieve positive cash flow and, given our projected

funding needs, our ability to generate positive cash flow is

uncertain.

We

have had unaudited negative cash flow from operating activities of

$4,076,157 for the 9 months ending on September 30, 2018. We

anticipate that we will continue to have negative cash flow from

operating and investing activities for the foreseeable future as we

expect to incur increased coal mining development expenses and make

significant capital expenditures in our efforts to commence mining

operations at our various permit sites. Our business also will at

times require significant amounts of working capital to support our

growth, particularly as we acquire infrastructure and equipment to

support our new mining operations. An inability to generate

positive cash flow for the foreseeable future may adversely affect

our ability to raise needed capital for our business on reasonable

terms, diminish supplier or customer willingness to enter into

transactions with us, and have other adverse effects that may

decrease our long-term viability. There can be no assurance we will

achieve positive cash flow in the foreseeable future.

We may need access to additional financing, which may not be

available to us on acceptable terms or at all, and there is a

substantial doubt about our ability to continue as a going concern.

If we cannot access additional financing when we need it and on

acceptable terms, our business, prospects, financial condition,

operating results and ability to continue as a going concern could

be adversely affected.

Our

growth-oriented business plan to mine and sell coal from our

various permits and facilities will require significant continued

capital investment. Our independent registered public accounting

firm for the fiscal year ended December 31, 2016 and December 31,

2017, has included an explanatory paragraph in their opinion that

accompanies our audited consolidated financial statements as of and

for those years indicating that our current liquidity position

raises substantial doubt about our ability to continue as a going

concern. If we are unable to improve our liquidity position, we may

not be able to continue as a going concern. The accompanying

consolidated financial statements do not include any adjustments

that might result if we are unable to continue as a going concern

and, therefore, be required to realize our assets and discharge our

liabilities other than in the normal course of business which could

cause investors to suffer the loss of all or a substantial portion

of their investment. We cannot be certain that additional financing

will be available to us on favorable terms when required, or at

all, particularly given that we do not now have a committed credit

facility with any government or financial institution. If we cannot

obtain additional financing when we need it and on terms acceptable

to us, our business, prospects, financial condition, operating

results and ability to continue as a going concern could be

adversely affected.

We do not have any existing bank credit facilities. Our ability to

obtain such financing may be limited and if we are unable to secure

such financing, our profitability may be adversely

affected.

We

do not have any existing bank credit facilities. Our ability to

obtain such financing may be limited as banks and other financial

institutions may be reluctant to extend credit to businesses they

perceive as lacking prolonged operating histories, an industry that

may be politically undesirable, and limited information relating to

revenues and costs upon which they can evaluate the merits and

risks of any such credit extension. Our inability to secure bank

credit facilities (or some other form of cash/liquid injection) may

have an adverse effect on our results of operations. Due to our

limited operating history and limited assets, and the lag often

existing between commencing business operations and profitability,

in the absence of such bank financing, we may be forced to rely

solely on revenues generated from our business operations in order

to support our company, which revenues may not be sufficient to

meet our operating and administrative expenses. If we do not have

sufficient cash to meet our expenses, whether from revenues or bank

credit, we may have to curtail or cease business

operations.

9

We have identified several material weaknesses in our internal

control over financial reporting. If our remediation of these

material weaknesses is not effective, or if we experience

additional material weaknesses in the future or otherwise fail to

maintain an effective system of internal control over financial

reporting in the future, we may not be able to accurately or timely

report our financial condition or results of operations, which may

adversely affect investor confidence in us and, as a result, the

value of our securities.

In

connection with the audit of our financial statements beginning on

page F-1, the Company identified several material weaknesses in its

internal control over financial reporting. A material weakness is

defined as a deficiency, or a combination of deficiencies, in

internal control over financial reporting, such that there is a

reasonable possibility that a material misstatement of the

Company’s financial statements will not be prevented or

detected on a timely basis. Below are the material weakness

identified:

●

Insufficient number

of staff performing the accounting and financial reporting

functions; and

●

Lack of timely

reconciliations;

Neither

we nor our independent registered public accounting firm has

performed an evaluation of our internal control over financial

reporting in accordance with Section 404 of the Sarbanes-Oxley Act.

In light of the material weaknesses that were identified, we

believe that it is possible that additional material weaknesses and

control deficiencies may have been identified if such an evaluation

had been performed.

The

Company is working to remediate the material weaknesses, has taken

steps to enhance the internal control environment, and plans to

take additional steps to remediate the material weaknesses.

Specifically, we are:

●

seeking technically

competent staff with appropriate experience;

●

designing

additional controls around identification, documentation and

application of technical accounting guidance regarding

reconciliation of account discrepancies.

The

actions that we are taking are subject to ongoing senior management

review as well as audit committee oversight. Although we plan to

complete this remediation process as quickly as possible, we cannot

at this time estimate how long it will take, and our efforts may

not be successful in remediating these material weaknesses. In

addition, we will incur additional costs in improving our internal

control over financial reporting. If we are unable to successfully

remediate these material weaknesses or if we identify additional

material weaknesses, we may not detect errors on a timely basis.

This could harm our operating results, cause us to fail to meet our

SEC reporting obligations or NASDAQ Capital Market listing

requirements on a timely basis, adversely affect our reputation,

cause our stock price to decline or result in inaccurate financial

reporting or material misstatements in our annual or interim

financial statements.

In

addition to the remediation efforts related to the material

weaknesses described above, we are in the process of designing and

implementing the internal control over financial reporting required

to comply with Section 404 of the Sarbanes Oxley Act. This process

will be time consuming, costly and complicated. If during the

evaluation and testing process, we identify one or more other

material weaknesses in our internal control over financial

reporting, our management will be unable to assert that our

internal control over financial reporting is effective. Even if our

management concludes that our internal control over financial

reporting is effective, our independent registered public

accounting firm may conclude that there are material weaknesses

with respect to our internal controls or the level at which our

internal controls are documented, designed, implemented or

reviewed. If we are unable to assert that our internal control over

financial reporting is effective, or when required in the future,

if our independent registered public accounting firm is unable to

express an opinion as to the effectiveness of our internal control

over financial reporting, investors may lose confidence in the

accuracy and completeness of our financial reports and the market

price of our securities could be adversely affected, and we could

become subject to investigations by the stock exchange on which our

securities are listed, the SEC, or other regulatory authorities,

which could require additional financial and management

resources.

10

We have never declared or paid a cash dividend on our common shares

nor will we in the foreseeable future.

You

will not receive dividend income from an investment in the shares

and as a result, the purchase of the shares should only be made by

an investor who does not expect a dividend return on the

investment.

Our Series B

preferred stock, however, received an 8.0% annual dividend, of

which an accrued amount is recorded of $104,157, as of September

30, 2018, and continued to accrue to the Series B preferred stock

holder at the same rate until all Series B preferred stock was

converted to common stock on November 7, 2018. On November 8, 2018,

we filed an amendment to the company’s Articles of

Incorporation that eliminated the Series B preferred stock and

created a new Series C preferred stock. The Series C preferred

stock accrues a 10.0% annual dividend, compounded annually, of

which no amount has been recorded yet as being

accrued.

With

the potential exception of the Series C preferred stock dividend

referenced above, we currently intend to retain future earnings, if

any, to finance the operation and expansion of our business.

Accordingly, investors who anticipate the need for immediate income

from their investments by way of cash dividends should refrain from

purchasing any of our securities. As we do not intend to declare

dividends in the future, you may never see a return on your

investment and you indeed may lose your entire

investment.

We will incur professional fees in connection with being a

reporting company under the Securities Exchange Act of 1934, as

amended.

Our

Company is subject to the reporting requirements of the 1934 Act

and as such, we are required to file 10-Ks, 10-Qs and 8-Ks and

other reports with the Securities and Exchange Commission. We will

incur professional fees (i.e., attorney, auditors and filing

agents) in connection with the preparation and filing of such

reports and we currently anticipate such costs to range from

$25,000 to $50,000 per year. If we are unable to file such reports,

we will be delinquent in our filings which could adversely affect

the marketability of the Shares.

The failure to comply with the internal control evaluation and

certification requirements of Section 404 of Sarbanes-Oxley Act

could harm our operations and our ability to comply with our

periodic reporting obligations.

As a

reporting company under the 1934 Act, we are required to comply

with the internal control evaluation and certification requirements

of Section 404 of the Sarbanes-Oxley Act of 2002. We are in the

process of determining whether our existing internal controls over

financial reporting systems are compliant with Section 404. This

process may divert internal resources and will take a significant

amount of time, effort and expense to complete. If it is determined

that we are not in compliance with Section 404, we may be required

to implement new internal control procedures and reevaluate our

financial reporting. We may experience higher than anticipated

operating expenses as well as outside auditor fees during the

implementation of these changes and thereafter. Further, we may

need to hire additional qualified personnel in order for us to be

compliant with Section 404. If we are unable to implement these

changes effectively or efficiently, it could harm our operations,

financial reporting or financial results and could result in our

being unable to obtain an unqualified report on internal controls

from our independent auditors, which could adversely affect our

ability to comply with our periodic reporting obligations under the

1934 Act.

11

Future sales of restricted shares could decrease the price a

willing buyer would pay for shares of our common stock, could cause

our price to decline and could impair our ability to raise

capital.

Future

sales of common stock by existing shareholders or a new issuance by

the Company under exemptions from registration or through a

subsequent registered offering could materially adversely affect

the market price of our common stock and could materially impair

our future ability to raise capital through an offering of equity

securities. We are unable to predict the effect, if any, that

market sales of these shares, or the availability of these shares

for future sale, will have on the prevailing market price of our

common stock at any given time.

You may not be able to resell any shares you

purchased.

There

is an extremely limited trading market for our common stock at

present. There is no assurance that any trading market will be

present. This means that it may be hard or impossible for you to

find a willing buyer for your shares should you decide to sell them

in the future.

Risks Related to Our Business

The majority of our properties have not yet been developed into

producing coal mines and, if we experience any development delays

or cost increases, our business, financial condition, and results

of operations could be adversely affected.

We have

not yet completed our development plan and do not expect to have

full annual production from all of our properties until sometime in

the future. We expect to incur significant capital expenditures

until we have completed the development of our properties. In

addition, the development of our properties involves numerous

regulatory, environmental, political and legal uncertainties that

are beyond our control and that may cause delays in, or increase

the costs associated with, their completion. Accordingly, we may

not be able to complete the development of the properties on

schedule, at the budgeted cost or at all, and any delays beyond the

expected development periods or increased costs above those

expected to be incurred could have a material adverse effect on our

business, financial condition, results of operations, cash flows

and ability to pay dividends to our common

stockholders.

In

connection with the development of our properties, we may encounter

unexpected difficulties, including the following:

●

shortages of

materials or delays in delivery of materials;

●

unexpected

operational events;

●

facility or

equipment malfunctions or breakdowns;

●

unusual or

unexpected adverse geological conditions;

●

cost

overruns;

●

failure to obtain,

or delays in obtaining, all necessary governmental and third-party

rights-of-way, easements, permits, licenses and approvals for the

development, construction and operation of one or more of our

properties;

●

weather conditions

and other catastrophes, such as explosions, fires, floods and

accidents;

●

difficulties in

attracting a sufficient skilled and unskilled workforce, increases

in the level of labor costs and the existence of any labor

disputes; and

●

local and general

economic and infrastructure conditions.

If we

are unable to complete or are substantially delayed in completing

the development of any of our properties, our business, financial

condition, results of operations cash flows and ability to pay

dividends to our common stockholders could be adversely

affected.

Because we have limited operating history and have not yet

generated significant revenues or operating cash flows, you may

have difficulty evaluating our ability to successfully implement

our business strategy.

Because

of our limited operating history, the operating performance of our

properties and our business strategy have not yet been proven. As a

result, our historical financial statements do not provide a

meaningful basis to evaluate our operations or our ability to

achieve our business strategy. Therefore, it may be difficult for

you to evaluate our business and results of operations to date and

assess our future prospects.

In

addition, we may encounter risks and difficulties experienced by

companies whose performance is dependent upon newly-constructed or

newly-acquired assets, such as any one of our properties failing to

perform as expected, having higher than expected operating costs,

having lower than expected customer revenues, or suffering

equipment breakdown, failures or operational errors. We may be less

successful in achieving a consistent operating level capable of

generating cash flows from our operations as compared to a company

whose major assets have had longer operating histories. In

addition, we may be less equipped to identify and address operating

risks and hazards in the conduct of our business than those

companies whose major assets have had longer operating

histories.

12

We have limited operating history and our future performance is

uncertain.

We are

an early stage enterprise and will continue to be so until

commencement of substantial production from our coal properties. We

have only recently commenced limited production at one of our

properties. We have generated substantial net losses and negative

cash flows from operating activities since our inception and expect

to continue to incur substantial net losses as we continue our mine

development program. We face challenges and uncertainties in

financial planning as a result of the unavailability of historical

data and uncertainties regarding the nature, scope and results of

our future activities. New companies must develop successful

business relationships, establish operating procedures, hire staff,

install management information and other systems, establish

facilities and obtain licenses, as well as take other measures

necessary to conduct their intended business activities. We may not

be successful in implementing our business strategies or in

completing the development of the infrastructure necessary to

conduct our business as planned. In the event that one or more of

our mine development programs are not completed or are delayed or

terminated, our operating results will be adversely affected and

our operations will differ materially from the activities described

in this prospectus. As a result of industry factors or factors

relating specifically to us, we may have to change our methods of

conducting business, which may cause a material adverse effect on

our results of operations, financial condition and ability to pay

dividends to our common stockholders.

13

We will likely depend on a limited number of customers for a

significant portion of our revenues.

We will

likely depend on a limited number of customers for a significant

portion of our revenues. The failure to obtain additional customers

or the loss of all or a portion of the revenues attributable to any

customer as a result of competition, creditworthiness, inability to

negotiate extensions or replacement of contracts or otherwise,

could have a material adverse effect on our business, financial

condition, results of operations, cash flows and ability to pay

dividends to our common stockholders.

We expect that our customer base will be highly dependent on a

small number of customers.

The

majority of all of the coal that we produce, or plan to produce, is

sold to steel producers. Therefore, demand for our coal will be

highly correlated to the steel industry. The steel industry’s

demand for metallurgical coal is affected by a number of factors

including the cyclical nature of that industry’s business,

technological developments in the steel-making process and the

availability of substitutes for steel such as aluminum, composites

and plastics. A significant reduction in the demand for steel

products would reduce the demand for metallurgical coal, which

would have a material adverse effect upon our business, cash flows

and results of operations. Similarly, if less expensive ingredients

could be used in substitution for metallurgical coal in the

integrated steel mill process, the demand for metallurgical coal

would materially decrease, which would also materially adversely

affect demand for our metallurgical coal.

We do not expect to enter into long-term sales contracts for our

coal and as a result we will be exposed to fluctuations in market

pricing.

Sales

commitments for our coal typically are not long-term in nature and

are generally no longer than one year in duration. Many coal

transactions in the U.S. are done on a calendar year basis, where

both prices and volumes are fixed in the third and fourth quarter

for the following calendar year. Globally the market is evolving to

shorter term pricing. Some annual contracts have shifted to

quarterly contracts and growing volumes are being sold on an

indexed basis, where prices are determined by averaging the leading

spot indexes reported in the market. As a result, once we commence

operations and enter into agreements with customers, we will be

subject to fluctuations in market pricing. We will not be protected

from oversupply or market conditions where we cannot sell our coal

at economic prices. Metallurgical coal has been an extremely

volatile commodity over the past ten years and prices may become

volatile again in the future given the recent rapid increase. There

can be no assurances we will be able to mitigate such conditions as

they arise. Any sustained failure to be able to market our coal

during such periods would have a material adverse effect on our

business, results of operations, cash flows and ability to pay

dividends to our common stockholders.

Product alternatives may reduce demand for our

products.

The

majority of our coal production in the near term will be comprised

of metallurgical coal or pulverized coal injection (PCI), both

which typically command a price premium over the majority of other

forms of coal because of its use in blast furnaces for steel

production. Metallurgical coal has specific physical and chemical

properties, which are necessary for efficient blast furnace

operation. Steel producers are continually investigating

alternative steel production technologies with a view to reducing

production costs. The steel industry has increased utilization of

electric arc furnaces or pulverized coal injection processes, which

reduce or eliminate the use of furnace coke, an intermediate

product produced from metallurgical coal and, in turn, generally

decreases the demand for metallurgical coal. Many alternative

technologies are designed to use lower quality coals or other

sources of carbon instead of higher cost high-quality metallurgical

coal. While conventional blast furnace technology has been the most

economic large-scale steel production technology for a number of

years, and emergent technologies typically take many years to

commercialize, there can be no assurance that over the longer term

competitive technologies not reliant on metallurgical coal could

emerge which could reduce the demand and price premiums for

metallurgical coal.

Moreover, we may

produce and market other coal products, such as thermal coal, which

are also subject to alternative competition. Alternative

technologies are continually being investigated and developed in

order to reduce production costs or minimize environmental or

social impact. If competitive technologies emerge that use other

materials in place of our products, demand and price for our

products might fall.

We face uncertainties in estimating our economically recoverable

coal deposits, and inaccuracies in our estimates could result in

lower than expected revenues, higher than expected costs and

decreased profitability.

Coal is

economically recoverable when the price at which coal can be sold

exceeds the costs and expenses of mining and selling the coal.

Forecasts of our future performance are based on, among other

things, estimates of our recoverable coal deposits. We base our

coal deposit information on geologic data, coal ownership

information and current and proposed mine plans. We have not

independently verified any of the coal deposit information,

including coal qualities within the coal deposit areas, coal

heights, and deposit boundaries, and our information comes

primarily from previously prepared reports by prior management and

other third parties. Coal deposit estimates are periodically

updated to reflect past coal production, if any, new drilling

information, other geologic or mining data, and changes to coal

price expectations or the cost of production and sale. There are

numerous uncertainties inherent in estimating quantities and

qualities of coal and costs to mine coal, including many factors

beyond our control. As a result, estimates of economically

recoverable coal deposits are by their nature uncertain. Some of

the factors and assumptions that can impact economically

recoverable coal deposits estimates include:

14

●

geologic and mining

conditions;

●

historical

production from the area compared with production from other

producing areas;

●

the assumed effects

of environmental and other regulations and taxes by governmental

agencies;

●

our ability to

obtain, maintain and renew all required permits;

●

future improvements

in mining technology;

●

assumptions related

to future prices; and

●

future operating

costs, including the cost of materials, and capital

expenditures.

Each of

the factors that impacts coal deposit estimation may vary

considerably from the assumptions used in estimating such deposits.

For these reasons, estimates of coal deposits may vary

substantially. Actual production, revenues and expenditures with

respect to our future coal deposits will vary from estimates, and

these variances may be material. As a result, our estimates may not

accurately reflect our actual future coal deposits.

Our inability to acquire additional coal deposits that are

economically recoverable may have a material adverse effect on our

future profitability.

Our

profitability depends substantially on our ability to mine, in a

cost-effective manner, coal deposits that possess the quality

characteristics that prospective customers desire. Because our coal

deposits will decline as we mine our coal, our future profitability

depends upon our ability to acquire additional coal deposits that

are economically recoverable to replace the coal deposits we will

produce. If we fail to acquire or develop sufficient additional

coal deposits over the long term to replace the coal deposits

depleted by our production, our existing deposits could eventually

be exhausted.

The status of our idled mines, our lack of operating history and

multiple coal quality levels and inability to send test shipments

to our prospective customers may negatively impact our ability to

develop our initial customer base.

As a

company with limited operating history and several idled,

non-producing mines, our potential customer base is also uncertain.

Our ability to commence operations and begin shipments to customers

will be impacted by any potential mine rehabilitation work or

start-up timing and costs.

Deterioration in the global economic conditions in any of the

industries in which prospective customers operate, a worldwide

financial downturn, such as the 2008-2009 financial crisis, or

negative credit market conditions could have a material adverse

effect on our business, financial condition, results of operations,

cash flows and ability to pay dividends to our common

stockholders.

Economic conditions

in the industries in which most of our prospective customers

operate, such as steelmaking and electric power generation,

substantially deteriorated in recent years and reduced the demand

for coal. According to the US Energy Information Agency

(“EIA”), total thermal and metallurgical coal

production in the Central Appalachian Basin is expected to

gradually decline. A deterioration of economic conditions in our

prospective customers’ industries could cause a decline in

demand for and production of metallurgical coal. Renewed or

continued weakness in the economic conditions of any of the

industries served by prospective customers could have a material

adverse effect on our business, financial condition, results of

operations, cash flows and ability to pay dividends to our common

stockholders. For example:

●

demand for

metallurgical coal depends on domestic and foreign steel demand,

which if weakened would negatively impact our revenues, margins and

profitability;

●

the tightening of

credit or lack of credit availability to prospective customers

could adversely affect our ability to collect our trade

receivables; and

●

our ability to

access the capital markets may be restricted at a time when we

intend to raise capital for our business, including for capital

improvements and exploration and/or development of coal

deposits.

Prices for coal are volatile and can fluctuate widely based upon a

number of factors beyond our control, including oversupply relative

to the demand available for our coal and weather. A substantial or

extended decline in the prices we receive for our coal could

adversely affect our business, results of operations, financial

condition, cash flows and ability to pay dividends to our common

stockholders.

Our

financial results will be significantly affected by the prices we

receive for our coal and depend, in part, on the margins that we

will receive on sales of our coal. Our margins will reflect the

price we receive for our coal over our cost of producing and

transporting our coal. Prices and quantities under U.S. domestic

metallurgical coal sales contracts are generally based on

expectations of the next year’s coal prices at the time the

contract is entered into, renewed, extended or re-opened, Pricing

in the global seaborne market is typically negotiated quarterly,

however, increasingly the market is moving towards shorter term

pricing models. The expectation of future prices for coal depends

upon many factors beyond our control, including the

following:

15

●

the market price

for coal;

●

overall domestic

and global economic conditions, including the supply of and demand

for domestic and foreign coal, coke and steel;

●

the consumption

pattern of industrial consumers, electricity generators and

residential users;

●

weather conditions

in our markets that affect the demand for thermal coal or that

affect the ability to produce metallurgical coal;

●

competition from

other coal suppliers;

●

technological

advances affecting energy consumption;

●

the costs,

availability and capacity of transportation

infrastructure;

●

the impact of

domestic and foreign governmental laws and regulations, including

environmental and climate change regulations and regulations

affecting the coal mining industry, and delays in the receipt of,

failure to receive, failure to maintain or revocation of necessary

governmental permits; and

●

increased

utilization by the steel industry of electric arc furnaces or

pulverized coal injection processes, which reduce or eliminate the

use of furnace coke, an intermediate product produced from

metallurgical coal, and generally decrease the demand for

metallurgical coal.

Metallurgical coal

has been an extremely volatile commodity over the past 10 years, as

steel production growth in Asia underpinned demand growth, while

the market experienced two supply shocks from flooding events in

Australia’s Queensland and a third in 2016 caused by a

reduction in Chinese domestic production. The first severe flooding

sent global metallurgical coal prices from $98 per MT in 2007 to

$305 per MT in 2008. A second round of flooding disrupted the

Australian supply chain in 2011, and prices jumped from $129 per MT

to $330 per MT. The temporary supply disruptions caused major price

spikes, which, while short-lived, resulted in a period of elevated

prices, before declining once supply normalized, and production

growth that high prices incentivized eventually came online. The

slow decline in global prices since 2011 forced high-cost U.S.

suppliers who could not compete in the export market to reduce

output. Any decline in the prices of and demand for coal could have

a material adverse effect on our business, financial condition,

results of operations, cash flows and ability to pay dividends to

our common stockholders.

Increased competition or a loss of our competitive position could

adversely affect sales of, or prices for, our coal, which could

impair our profitability. In addition, foreign currency

fluctuations could adversely affect the competitiveness of our coal

abroad.

We will

compete with other producers primarily on the basis of coal

quality, delivered costs to the customer and reliability of supply.

We expect to compete primarily with U.S. coal producers and with

some Canadian coal producers for sales of metallurgical coal to

domestic steel producers and, to a lesser extent, thermal coal to

electric power generators. We also expect to compete with both

domestic and foreign coal producers for sales of metallurgical coal

in international markets. Certain of these coal producers may have

greater financial resources and larger coal deposit bases than we

do. We expect to sell coal to the seaborne metallurgical coal

market, which is significantly affected by international demand and

competition.

We

cannot assure you that competition from other producers will not

adversely affect us in the future. The coal industry has

experienced consolidation over the past 10 years, including

consolidation among some of our major competitors. We cannot assure

you that the result of current or further consolidation in the coal

industry, or the reorganization through bankruptcy of competitors

with large legacy liabilities, will not adversely affect us. A

number of our competitors have idled production over the last year

in light of lower metallurgical coal prices in 2015 and the first

half of 2016. The recent increase in coal prices in 2017 and 2018

could encourage existing producers to expand capacity or could

encourage new producers to enter the market.

16

In

addition, we face competition from foreign producers that sell

their coal in the export market. Potential changes to international

trade agreements, trade concessions, foreign currency fluctuations

or other political and economic arrangements may benefit coal

producers operating in countries other than the United States.

Additionally, North American steel producers face competition from

foreign steel producers, which could adversely impact the financial

condition and business of our prospective customers. We cannot

assure you that we will be able to compete on the basis of price or

other factors with companies that in the future may benefit from

favorable foreign trade policies or other arrangements. Coal is

sold internationally in U.S. dollars and, as a result, general

economic conditions in foreign markets and changes in foreign

currency exchange rates may provide our foreign competitors with a

competitive advantage. If our competitors’ currencies decline

against the U.S. dollar or against our prospective foreign

customers’ local currencies, those competitors may be able to

offer lower prices for coal to prospective customers. Furthermore,

if the currencies of our prospective overseas customers were to

significantly decline in value in comparison to the U.S. dollar,

those prospective customers may seek decreased prices for the coal

we sell to them. Consequently, currency fluctuations could

adversely affect the competitiveness of our coal in international

markets, which could have a material adverse effect on our

business, financial condition, results of operations and cash

flows.

Our business involves many hazards and operating risks, some of

which may not be fully covered by insurance. The occurrence of a

significant accident or other event that is not fully insured could

adversely affect our business, results of operations, financial

condition, cash flows and ability to pay dividends to our common

stockholders.

Our

mining operations, including our preparation and transportation

infrastructure, are subject to many hazards and operating risks. In

particular, underground mining and related processing activities

present inherent risks of injury to persons and damage to property

and equipment. Our mines are subject to a number of operating risks

that could disrupt operations, decrease production and increase the

cost of mining for varying lengths of time, thereby adversely

affecting our operating results. In addition, if coal production

declines, we may not be able to produce sufficient amounts of coal

to deliver under future sales contracts. Our inability to satisfy

contractual obligations could result in prospective customers

initiating claims against us. The operating risks that may have a

significant impact on our future coal operations

include:

●

variations in

thickness of the layer, or seam, of coal;

●

adverse geologic

conditions, including amounts of rock and other natural materials

intruding into the coal seam, that could affect the stability of

the roof and the side walls of the mine;

●

environmental

hazards;

●

mining and

processing equipment failures and unexpected maintenance

problems;

●

fires or

explosions, including as a result of methane, coal, coal dust or

other explosive materials, or other accidents;

●

inclement or

hazardous weather conditions and natural disasters or other force

majeure events;

●

seismic activities,

ground failures, rock bursts or structural cave-ins or

slides;

●

delays in moving

our mining equipment;

●

railroad delays or

derailments;

●

security breaches

or terroristic acts; and

●

other hazards or

occurrences that could also result in personal injury and loss of

life, pollution and suspension of operations.

Any of

these risks could adversely affect our ability to conduct

operations or result in substantial loss to us as a result of

claims for:

●

personal injury or

loss of life;

●

damage to and

destruction of property, natural resources and equipment, including

our coal properties and our coal production or transportation

facilities;

●

pollution,

contamination and other environmental damage to our properties or

the properties of others;

●

potential legal

liability and monetary losses;

●

regulatory

investigations, actions and penalties;

●

suspension of our

operations; and

●

repair and

remediation costs.

17

In

addition, the total cost of coal sold, and overall coal production

may be adversely affected by various factors.

Although we

maintain insurance for a number of risks and hazards, we may not be

insured or fully insured against the losses or liabilities that

could arise from a significant accident in our future coal

operations. We may elect not to obtain insurance for any or all of

these risks if we believe that the cost of available insurance is

excessive relative to the risks presented. In addition, pollution,

contamination and environmental risks generally are not fully

insurable. Moreover, a significant mine accident or regulatory

infraction could potentially cause a mine shutdown. The occurrence

of an event that is not fully covered by insurance could have a

material adverse effect on our business, financial condition,

results of operations, cash flows and ability to pay dividends to

our common stockholders.

In

addition, if any of the foregoing changes, conditions or events

occurs and is not determined to be a force majeure event, any

resulting failure on our part to deliver coal to the purchaser

under contract could result in economic penalties, suspension or

cancellation of shipments or ultimately termination of the

agreement, any of which could have a material adverse effect on our

business, financial condition, results of operations, cash flows

and ability to pay dividends to our common

stockholders.

Depending on future acquisitions, our operations could be

exclusively located in a single geographic region, making us

vulnerable to risks associated with operating in a single

geographic area.

Initially,

substantially all of our operations will be conducted in a single

geographic region in the eastern United States in the Commonwealth

of Kentucky. The geographic concentration of our operations may

disproportionately expose us to disruptions in our operations if

the region experiences severe weather, transportation capacity

constraints, constraints on the availability of required equipment,

facilities, personnel or services, significant governmental

regulation or natural disasters. If any of these factors were to

impact the region in which we operate more than other coal

producing regions, our business, financial condition, results of

operations and cash flows will be adversely affected relative to

other mining companies that have a more geographically diversified

asset portfolio.

In

addition, some scientists have warned that increasing

concentrations of greenhouse gases (“GHGs”) in the

Earth’s atmosphere may produce climate changes that have

significant physical effects, such as increased frequency and

severity of storms, droughts and floods and other climatic events.

If these warnings are correct, and if any such effects were to

occur in areas where we or our customers operate, they could have

an adverse effect on our assets and operations.

The availability and reliability of transportation facilities and

fluctuations in transportation costs could affect the demand for

our coal or impair our ability to supply coal to prospective

customers.

Transportation

logistics will play an important role in allowing us to supply coal

to prospective customers. Any significant delays, interruptions or

other limitations on the ability to transport our coal could

negatively affect our operations. Delays and interruptions of rail

services because of accidents, failure to complete construction of

rail infrastructure, infrastructure damage, lack of rail or port

capacity, weather-related problems, governmental regulation,

terrorism, strikes, lock-outs, third-party actions or other events

could impair our ability to supply coal to customers and adversely

affect our profitability. In addition, transportation costs

represent a significant portion of the delivered cost of coal and,

as a result, the cost of delivery is a critical factor in a

customer’s purchasing decision. Increases in transportation

costs, including increases resulting from emission control

requirements and fluctuations in the price of locomotive diesel

fuel and demurrage, could make our coal less competitive, which

could have a material adverse effect on our business, financial

condition, results of operations, cash flows and ability to pay

dividends to our common stockholders.

18

Any significant downtime of our major pieces of mining equipment,

including any preparation plant, could impair our ability to supply

coal to prospective customers and materially and adversely affect

our results of operations.

We

currently and in the future, will depend on several major pieces of

mining equipment to produce and transport our coal, including, but

not limited to, underground continuous mining units and coal

conveying systems, surface mining equipment such as augers,

highwall miners, front-end loaders and coal over burden haul

trucks, preparation plant and related facilities, conveyors and

transloading facilities. If any of these pieces of equipment or

facilities suffered major damage or were destroyed by fire,

abnormal wear, flooding, incorrect operation or otherwise, we may

be unable to replace or repair them in a timely manner or at a

reasonable cost, which would impact our ability to produce and

transport coal and materially and adversely affect our business,

results of operations, financial condition and cash flows.

Moreover, the Mine Safety and Health Administration

(“MSHA”) and other regulatory agencies sometimes make

changes with regards to requirements for pieces of equipment. For

example, in 2015, MSHA promulgated a new regulation requiring the

implementation of proximity detection devices on all continuous

mining machines. Such changes could cause delays if manufacturers

and suppliers are unable to make the required changes in compliance

with mandated deadlines.

If

either our preparation plants, or train loadout facilities, or

those of a third-party processing or loading our coal, suffer

extended downtime, including major damage, or is destroyed, our

ability to process and deliver coal to prospective customers would

be materially impacted, which would materially adversely affect our

business, results of operations, financial condition and cash flows

and our ability to pay dividends to our common

stockholders.

If customers do not enter into, extend or honor contracts with us,

our profitability could be adversely affected.

We have

entered into a limited number of contracts for the sale of our