Form S-1 Jaguar Health, Inc.

Tweet

Tweet Share

Share

Use these links to rapidly review the document

TABLE OF CONTENTS

As filed with the Securities and Exchange Commission on September 12, 2018.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

JAGUAR HEALTH, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

2834 (Primary Standard Industrial Classification Code Number) |

46-2956775 (I.R.S. Employer Identification Number) |

201 Mission Street, Suite 2375

San Francisco, California 94105

(415) 371-8300

(Address, including zip code, and telephone number, including area code, of registrant's principal executive office)

Lisa A. Conte

Chief Executive Officer and President

Jaguar Health, Inc.

201 Mission Street, Suite 2375

San Francisco, California 94105

(415) 371-8300

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

Donald C. Reinke, Esq. Reed Smith LLP 101 Second Street, Suite 1800 San Francisco, California 94105 (415) 543-8700 |

Robert F. Charron, Esq. Ellenoff Grossman & Schole LLP 1345 Avenue of the Americas New York, NY 10105 (212) 370-1300 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o |

Smaller reporting company ý Emerging growth company ý |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ý

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered(1) |

Proposed Maximum Aggregate Offering Price(2)(3) |

Amount of Registration Fee(3) |

||

|---|---|---|---|---|

Common Stock, par value $0.0001 per share |

$11,500,000 | $ | ||

Pre-funded warrants to purchase shares of common stock and common stock issuable upon exercise thereof |

— | — | ||

Underwriter warrants to purchase shares of common stock issuable upon exercise thereof(4) |

$1,150,000 | |||

Total |

$12,650,000 | $1,574.93 | ||

|

||||

- (1)

- Pursuant

to Rule 416 under the Securities Act of 1933, as amended, the securities being registered hereunder include such indeterminate number of additional

securities as may be issuable to prevent dilution resulting from stock splits, stock dividends or similar transactions.

- (2)

- The

proposed maximum aggregate offering price of the common stock proposed to be sold in the offering will be reduced on a dollar-for-dollar basis based on the

aggregate offering price of the pre-funded warrants offered and sold in the offering, and therefore the proposed aggregate maximum offering price of the common stock and pre-funded warrants (including

the common stock issuable upon exercise of the pre-funded warrants), if any, is $11,500,000.

- (3)

- Estimated

solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) of the Securities Act of 1933, as amended. Includes

the offering price of any additional securities that the underwriter has the option to purchase.

- (4)

- Represents warrants issuable to H.C. Wainwright & Co., LLC (the "Underwriter's Warrants") to purchase a number of shares of common stock equal to 8% of the number of shares of Common Stock and pre-funded warrants being offered at an exercise price equal to 125% of the public offering price. Resales of the Underwriter's Warrants on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, are registered hereby. Resales of shares of common stock issuable upon exercise of the Underwriter's Warrants are also being similarly registered on a delayed or continuous basis hereby. See "Underwriting."

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED SEPTEMBER 12, 2018

PRELIMINARY PROSPECTUS

Shares of Common Stock

Pre-Funded Warrants to Purchase Shares of Common Stock

We are offering shares of our common stock. We are also offering to certain purchasers whose purchase of shares of common stock in this offering would otherwise result in the purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding common stock immediately following the consummation of this offering, the opportunity to purchase, if any such purchaser so chooses, pre-funded warrants, in lieu of shares of common stock that would otherwise result in such purchaser's beneficial ownership exceeding 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding common stock. The purchase price of each pre-funded warrant will be equal to the price per share at which shares of common stock are sold to the public in this offering, minus $0.01, and the exercise price of each pre-funded warrant will be $0.01 per share. This offering also relates to the shares of common stock issuable upon exercise of any pre-funded warrants sold in this offering. The pre-funded warrants will be exercisable immediately and may be exercised at any time until all of the pre-funded warrants are exercised in full. For each pre-funded warrant we sell, the number of shares of common stock we are offering will be decreased on a one-for-one basis. Our common stock is listed on The NASDAQ Capital Market under the symbol "JAGX." On September 10, 2018, the last reported sale price of our common stock was $0.66 per share.

We are an "emerging growth company" as that term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings.

Our business and an investment in our securities involves a high degree of risk. See "Risk Factors" beginning on page 7 of this prospectus for a discussion of information that you should consider before investing in our securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

||||||

| |

Per Share |

Per Pre-funded Warrant |

Total |

|||

|---|---|---|---|---|---|---|

Public offering price |

$ | $ | $ | |||

Underwriting discounts and commissions(1) |

$ | $ | $ | |||

Proceeds, before expenses, to us |

$ | $ | $ | |||

|

||||||

- (1)

- See "Underwriting" beginning on page 120 of this prospectus for a description of compensation payable to the underwriter.

The offering is being underwritten on a firm commitment basis. We have granted the underwriter an option for a period of 30 days from the date of this prospectus to purchase up to an additional shares of our common stock (15% of the number of shares of common stock and pre-funded warrants sold in this offering) at the public offering price, less the underwriting discounts and commissions, to cover over-allotments, if any. If the underwriter exercises this option in full, the total underwriting discounts and commissions payable by us will be $ , and the total proceeds to us, before expenses, will be $ .

The underwriter expects to deliver the shares and pre-funded warrants against payment therefor on or about , 2018.

Sole Book-Running Manager

H.C. Wainwright & Co.

, 2018

We have not, and the underwriter has not, authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under the circumstances and in the jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date. We are not, and the underwriter is not, making an offer of these securities in any jurisdiction where such offer is not permitted.

For investors outside the United States: we have not, and the underwriter has not, done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of securities and the distribution of this prospectus outside the United States.

Jaguar Health, our logo, Napo Pharmaceuticals, Mytesi, Canalevia, Equilevia and Neonorm are our trademarks that are used in this prospectus. This prospectus also includes trademarks, tradenames and service marks that are the property of other organizations. Solely for convenience, trademarks and tradenames referred to in this prospectus appear without the ©, ® or ™ symbols, but those references are not intended to indicate that we will not assert, to the fullest extent under applicable law, our rights or that the applicable owner will not assert its rights, to these trademarks and tradenames.

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, especially the section in this prospectus titled "Risk Factors" appearing elsewhere in this prospectus the information incorporated by reference herein, including our financial statements and notes in our annual report on Form 10-K for 2017 and quarterly reports on Form 10-Q, before making an investment decision.

As used in this prospectus, references to "Jaguar," "we," "us" or "our" refer to Jaguar Health, Inc.

Overview

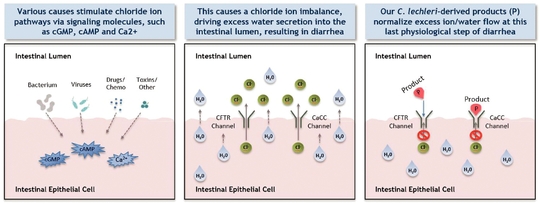

We are a commercial stage pharmaceutical company focused on developing novel, sustainably derived gastrointestinal products on a global basis. Our wholly-owned subsidiary, Napo Pharmaceuticals, Inc. ("Napo"), focuses on developing and commercializing proprietary human gastrointestinal pharmaceuticals for the global marketplace from plants used traditionally in rainforest areas. Our Mytesi (crofelemer) product is a first-in-class anti-secretory agent, approved by the U.S. Food and Drug Administration ("FDA") for the symptomatic relief of noninfectious diarrhea in adults with HIV/AIDS on antiretroviral therapy. The full launch of Mytesi began in April 2018—with the support of a full complement of patient and healthcare practitioner programs—when Napo's direct sales force of 18 sales representatives, a national sales director and one regional sales director became fully deployed.

Jaguar was founded in San Francisco, California as a Delaware corporation on June 6, 2013. The Company was a majority-owned subsidiary of Napo until the close of the Company's initial public offering on May 18, 2015. On July 31, 2017 with the merger of Jaguar and Napo, Napo began operating as a wholly-owned subsidiary of Jaguar focused on human health and the ongoing commercialization of, and development of follow-on indications for, Mytesi.

We believe that Jaguar is poised to realize a number of value adding events—including continued commercial growth of Mytesi for the current HIV-diarrhea indication, an expanded pipeline of human follow-on indications, and a second-generation anti-secretory agent, upon which to build global partnerships. As previously announced, Jaguar, through Napo, now controls commercial rights for Mytesi for all indications, territories and patient populations globally, and crofelemer manufacturing is being conducted at a new, multimillion-dollar commercial manufacturing facility that has been FDA-inspected and approved. Additionally, several of the drug product candidates in Jaguar's Mytesi pipeline are backed by Phase 2 and/or proof of concept evidence from completed human clinical trials. The current approved indication in HIV-related diarrhea is a chronic approval, with a safety package that supports chronic use of Mytesi for follow-on indications as well.

Mytesi is a novel, first-in-class anti-secretory agent which has a basic normalizing effect locally on the gut, and this mechanism of action has the potential to benefit multiple gastrointestinal disorders. Mytesi is in development for multiple possible follow-on indications, including cancer therapy-related diarrhea; orphan-drug indications for infants and children with congenital diarrheal disorders and short bowel syndrome (SBS); supportive care for inflammatory bowel disease (IBD); irritable bowel syndrome (IBS); and as a second-generation anti-secretory agent for use in cholera patients. Mytesi has received orphan-drug designation for SBS.

Corporate Information

We were incorporated in the State of Delaware on June 6, 2013. Our principal executive offices are located at 201 Mission Street, Suite 2375, San Francisco, CA 94015 and our telephone number is (415) 371-8300. Our website address is www.jaguar.health. The information contained on, or that can

1

be accessed through, our website is not part of this prospectus. Our voting common stock is listed on the NASDAQ Capital Market and trades under the symbol "JAGX." On July 31, 2017, we completed the acquisition of Napo (the "Merger") pursuant to the Agreement and Plan of Merger, dated March 31, 2017, by and among the Company, Napo, Napo Acquisition Corporation, and Napo's representative (the "Merger Agreement").

Emerging Growth Company Information

We are an "emerging growth company," as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and we may take advantage of certain exemptions and relief from various reporting requirements that are applicable to other public companies that are not "emerging growth companies." In particular, while we are an "emerging growth company" (i) we will not be required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act, (ii) we will be subject to reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and (iii) we will not be required to hold nonbinding advisory votes on executive compensation or stockholder approval of any golden parachute payments not previously approved. In addition, the JOBS Act provides that an emerging growth company can delay its adoption of any new or revised accounting standards, but we have irrevocably elected not to avail ourselves of this exemption and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies. In addition, investors may find our common stock less attractive if we rely on the exemptions and relief granted by the JOBS Act. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may decline and/or become more volatile.

We may remain an "emerging growth company" until as late as December 31, 2020 (the fiscal year-end following the fifth anniversary of the closing of our initial public offering, which occurred on May 18, 2015), although we may cease to be an "emerging growth company" earlier under certain circumstances, including (i) if the market value of our common stock that is held by non-affiliates exceeds $700.0 million as of any June 30, in which case we would cease to be an "emerging growth company" as of December 31 of such year, (ii) if our gross revenue exceeds $1.07 billion in any fiscal year or (iii) if we issue more than $1.0 billion of non-convertible debt over a three-year period.

Risks Associated with Our Business and this Offering

Our business and our ability to implement our business strategy are subject to numerous risks, as more fully described in the section of this prospectus entitled "Risk Factors" and under similarly titled headings of the documents incorporated herein by reference. You should read these risks before you invest in our securities

2

Common stock offered by us |

shares | |

Pre-funded warrants offered by us in this offering |

We are also offering to certain purchasers whose purchase of shares of common stock in this offering would otherwise result in the purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding common stock immediately following the consummation of this offering, the opportunity to purchase, if such purchasers so choose, pre-funded warrants, in lieu of shares of common stock that would otherwise result in any such purchaser's beneficial ownership exceeding 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding common stock. Each pre-funded warrant will be exercisable for one share of our common stock. The purchase price of each pre-funded warrant will equal the price per share at which the shares of common stock are being sold to the public in this offering, minus $0.01, and the exercise price of each pre-funded warrant will be $0.01 per share. The pre-funded warrants will be exercisable immediately and may be exercised at any time until all of the pre-funded warrants are exercised in full. This offering also relates to the shares of common stock issuable upon exercise of any pre-funded warrants sold in this offering. For each pre-funded warrant we sell, the number of shares of common stock we are offering will be decreased on a one-for-one basis. |

|

Option to purchase additional shares |

The underwriter has an option within 30 days of the date of this prospectus to purchase up to additional shares of our common stock in this offering. |

|

Common stock to be outstanding after this offering |

shares of common stock, assuming no sale of any pre-funded warrants (or shares of common stock if the underwriter exercises in full its option to purchase additional shares of common stock, assuming no sale of pre-funded warrants). |

|

Use of proceeds |

We estimate the net proceeds from this offering will be approximately $ million (or $ million if the underwriter exercises its option to purchase additional shares in full), based on an assumed public offering price of $ per share, the last reported sale price of our common stock on The Nasdaq Capital Market on , 2018, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

|

|

We intend to use the net proceeds from this offering, together with our existing cash and cash equivalents, for general corporate purposes and working capital. See "Use of Proceeds." |

|

Dividend policy |

We have not paid or declared any dividends on our common stock. For more information, see the section titled "Dividend policy." |

3

Risk factors |

You should read the section titled "Risk Factors" beginning on page 7 of this prospectus and other information included in this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

|

National Securities Exchange Listing |

Our common stock is listed on the NASDAQ Capital Market under the symbol "JAGX." We do not intend to list the pre-funded warrants on any securities exchange or nationally recognized trading system. |

The number of shares of our common stock to be outstanding after this offering is based on 8,736,579 shares of voting common stock and 40,301,237 shares of nonvoting common shares outstanding as of June 30, 2018 and assumes the sale and issuance by us of shares of common stock in this offering and excludes, as of June 30, 2018:

- •

- 3,314,955 shares of common stock issuable upon conversion of outstanding preferred stock as of June 30, 2018 with a weighted-average

conversion price of $2.775 per share;

- •

- 2,704,692 shares of common stock issuable upon exercise of outstanding options as of June 30, 2018 with a weighted-average exercise

price of $6.40 per share;

- •

- 402,348 shares of common stock reserved for future issuance under our 2014 Stock Incentive Plan as of June 30, 2018;

- •

- 209,531 shares of common stock issuable upon exercise of outstanding inducement options as of June 30, 2018 with a weighted-average

exercise price of $1.75 per share;

- •

- 392,904 shares of common stock issuable upon exercise of outstanding restricted stock unit awards, or RSUs, as of June 30, 2018;

- •

- 270,761 shares of common stock issuable upon exercise of outstanding warrants as of June 30, 2018 with a weighted-average exercise price of $16.35 per share;

The number of shares of common stock outstanding after the offering also does not include the following:

- •

- 866,524 shares of common stock issued after June 30, 2018;

- •

- Up to 720,721 shares of common stock issuable upon conversion of outstanding convertible promissory notes in the aggregate principal amount of

$10,000,000 issued after June 30, 2018, convertible at a price of $13.875 per share ;

- •

- 38,675 shares of common stock issuable pursuant to a convertible promissory note issued to Chicago Venture Partners, L.P. ("CVP"), in

the aggregate principal amount of $580,127, convertible at a price of $15 per share of common stock;

- •

- 670,586 shares of common stock, issuable upon exercise of a warrant issued on August 28, 2018 to Pacific Capital Management, LLC

with an exercise price that is the lower of (i) $0.85 per share and (ii) the average of the closing sales price of the common stock for the 30 consecutive trading days

commencing on September 4, 2018;

- •

- 185,417 shares of common stock issuable upon exercise of warrants issued on September 11, 2018 to L2 Capital, LLC with an

exercise price of $0.90 per share;

- •

- 33,918 shares of common stock issuable upon exercise of warrants issued on September 11, 2018 to Charles C. Conte with an exercise price of $1.23 per share;

4

- •

- Up to 706,765 shares of common stock issuable upon conversion of a convertible promissory note delivered to L2 Capital, LLC on

September 11, 2018 in the aggregate principal amount of $445,000 with an exercise price of $0.85 per share; and

- •

- Up to 176,691 shares of common stock issuable upon conversion of a convertible promissory note delivered to Charles C. Conte on September 11, 2018 in the aggregate principal amount of $111,250 with an exercise price of $0.85 per share.

5

Summary Consolidated Financial Data

You should read the following summary consolidated financial data together with our consolidated financial statements and the notes to those consolidated financial statements appearing in our Annual Report on Form 10-K for the fiscal year ended December 31, 2017 and our Quarterly Report on Form 10-Q for the period ended June 30, 2018, which are incorporated by reference in this prospectus. We have derived the consolidated statement of operations data for the years ended December 31, 2017 and 2016 from our audited consolidated financial statements. The consolidated statement of operations data for the six months ended June 30, 2017 and 2018 and the consolidated balance sheet data as of June 30, 2018 have been derived from our unaudited consolidated financial statements incorporated by reference to our Quarterly Report of Form 10-Q for the quarter ended June 30, 2018 and have been prepared on the same basis as the audited consolidated financial statements. Our historical results are not necessarily indicative of the results that may be expected in the future, and our results for any interim period are not necessarily indicative of results that may be expected for any full year.

| |

Year Ended December 31, | Six Months Ended June 30, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2016 | 2017 | 2017 | 2018 | |||||||||

Product revenue |

$ | 141,523 | $ | 1,485,114 | $ | 135,989 | $ | 1,510,813 | |||||

Collaboration revenue |

— | 2,876,072 | 1,582,942 | 177,389 | |||||||||

| | | | | | | | | | | | | | |

Total revenue |

141,523 | 4,361,186 | 1,718,931 | 1,688,202 | |||||||||

Operating Expenses |

|||||||||||||

Cost of product revenue |

51,966 | 880,405 | 40,907 | 1,072,185 | |||||||||

Research and development expense |

7,206,864 | 4,269,455 | 2,182,243 | 2,362,752 | |||||||||

Sales and marketing expense |

485,440 | 3,083,739 | 280,143 | 4,402,452 | |||||||||

General and administrative expense |

5,983,238 | 11,247,647 | 5,441,493 | 6,058,148 | |||||||||

Impairment of goodwill |

— | 16,827,000 | — | — | |||||||||

Impairment of indefinite-lived intangible assets |

— | 2,300,000 | — | — | |||||||||

| | | | | | | | | | | | | | |

Total operating expenses |

13,727,508 | 38,608,246 | 7,944,786 | 13,895,537 | |||||||||

Loss from operations |

(13,585,985 | ) | (34,247,060 | ) | (6,225,855 | ) | (12,207,335 | ) | |||||

Interest expense |

(985,549 | ) | (1,209,632 | ) | (336,201 | ) | (1,313,824 | ) | |||||

Other income/(expense) |

(11,046 | ) | 88,549 | 1,448 | 312,704 | ||||||||

Change in fair value of warrants |

(43,200 | ) | 695,341 | 247,321 | (145,365 | ) | |||||||

Loss on extinguishment of debt |

(108,000 | ) | (477,054 | ) | (207,713 | ) | — | ||||||

| | | | | | | | | | | | | | |

Net loss before income tax |

(14,733,780 | ) | (35,149,856 | ) | (6,521,000 | ) | (13,353,820 | ) | |||||

Income tax benefit |

— | 13,181,242 | — | — | |||||||||

| | | | | | | | | | | | | | |

Net loss and comprehensive loss |

$ | (14,733,780 | ) | $ | (21,968,614 | ) | $ | (6,521,000 | ) | $ | (13,353,820 | ) | |

Deemed dividend attributable to preferred stock |

(995,000 | ) | |||||||||||

Net loss attributable to common shareholders |

$ | (14,733,780 | ) | $ | (21,968,614 | ) | $ | (6,521,000 | ) | $ | (14,348,820 | ) | |

Net loss per share, basic and diluted |

$ | (5.09 | ) | $ | (30.09 | ) | $ | (6.78 | ) | $ | (1.43 | ) | |

Weighted-average common shares outstanding, basic and diluted |

2,895,729 | 730,079 | 961,821 | 10,010,862 | |||||||||

6

Investing in our securities involves a high degree of risk. You should carefully consider the risks described below, as well as the other information in this prospectus and incorporated by reference herein, including our financial statements and the related notes, before deciding whether to invest in our common stock. The occurrence of any of the events or developments described below could harm our business, financial condition, results of operations and prospects. In such an event, the market price of our common stock could decline, and you may lose all or part of your investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may harm our business, financial condition, results of operations and prospects.

Risks Related to Our Financial Position and Need for Additional Capital

We have a limited operating history, expect to incur further losses as we grow and may be unable to achieve or sustain profitability. Our independent registered public accounting firm has expressed substantial doubt about our ability to continue as a going concern.

From the date of our formation in June 2013, until the consummation of the Napo merger on July 31, 2017, our operations have been primarily limited to the research and development of our animal prescription drug product candidate, Canalevia, to treat various forms of diarrhea in dogs, our non-prescription product, Neonorm Calf, to help dairies and calf farms proactively retain fluid in calves, the ongoing commercialization of Neonorm Foal, our antidiarrheal for newborn horses, and Equilevia, our product for total gut health in high-performance equine athletes. Since the consummation of the Merger on July 31, 2017, our operations have been primarily focused on research, development and the ongoing commercialization of our lead prescription drug product candidate, Mytesi, which is approved by the U.S. FDA for the symptomatic relief of noninfectious diarrhea in adults with HIV/AIDS on antiretroviral therapy. As a result, we have limited meaningful historical operations upon which to evaluate our business and prospects or to successfully overcome the risks and uncertainties frequently encountered by companies in emerging fields such as the gastrointestinal health industry in general. We also have not generated any material revenue to date, and expect to continue to incur significant research and development and other expenses. Our net loss and comprehensive loss for the year ended December 31, 2017 was $22.0 million. As of June 30, 2018, we had an accumulated deficit of $75.8 million. We expect to continue to incur losses for the foreseeable future, which will increase significantly from historical levels as we expand our product development activities, seek necessary approvals for our human and veterinary drug product candidates, conduct species-specific formulation studies for our non-prescription products and begin commercialization activities. Even if we succeed in developing and broadly commercializing one or more of our products or product candidates beyond Mytesi, we expect to continue to incur losses for the foreseeable future, and we may never become profitable. If we fail to achieve or maintain profitability, then we may be unable to continue our operations at planned levels and be forced to reduce or cease operations.

As more fully discussed in Note 1 to our consolidated financial statements for the year ended December 31, 2017 and the quarter ended June 30, 2018, we believe there is substantial doubt about our ability to continue as a going concern as we do not currently have sufficient cash resources to fund our operations through August 13, 2019, or one year from the filing date of our Form 10-Q. Our financial statements do not include any adjustments that may result from the outcome of this uncertainty. If we are unable to continue as a viable entity, our stockholders may lose their entire investment.

We currently generate limited revenue from the sale of products and may never become profitable.

We are a natural-products pharmaceuticals company focused on the development and commercialization of novel, sustainably derived gastrointestinal products for human prescription use

7

primarily and also for animals on a global basis. Napo, our wholly-owned subsidiary, began the commercial pre-launch activities of our first FDA approved product, Mytesi, in February 2017. Accordingly, we have only generated limited revenue from product sales. There is no guarantee that our ongoing commercialization efforts for Neonorm Calf for preweaned dairy calves in the United States and Neonorm Foal for newborn horses in the United States will be successful or that we will be able to generate a consistent revenue stream from the sale of any of these products in the future. Further, in order to commercialize our other prescription drug product candidates, we must receive regulatory approval from the FDA in the United States and other regulatory agencies in various jurisdictions. Other than Mytesi, we have not yet received any regulatory approvals for our prescription drug product candidates. In addition, certain of our non-prescription products, such as Neonorm Calf, may be subject to regulatory approval outside the United States prior to commercialization in other countries. Accordingly, until and unless we receive any necessary regulatory approvals, we cannot market or sell our products in many regions. Moreover, even if we receive the necessary approvals, we may not be successful in generating revenue from sales of our products as we do not have any meaningful experience marketing or distributing our products. Accordingly, we may never generate any material revenue from our operations.

Raising additional capital may cause dilution to our stockholders, including purchasers of our common stock in this offering, restrict our operations or require us to relinquish rights to our technologies or product candidates.

Unless and until we can generate a substantial amount of revenue from our products or product candidates, we expect to finance our future cash needs through public or private equity offerings, debt financings or collaborations, licensing arrangements and government funding arrangements. In addition, we may seek additional capital due to favorable market conditions or strategic considerations, even if we believe that we have sufficient funds for our current or future operating plans.

To the extent that we raise additional capital through the sale of common stock, convertible securities or other equity securities, your ownership interest may be materially diluted, and the terms of these securities could include liquidation or other preferences and anti-dilution protections that could adversely affect your rights as a stockholder. In addition, debt financing, if available, would result in increased fixed payment obligations and may involve agreements that include restrictive covenants that limit our ability to take specific actions, such as incurring additional debt, making capital expenditures or declaring dividends, which could adversely affect our ability to conduct our business. In addition, securing additional financing would require a substantial amount of time and attention from our management and may divert a disproportionate amount of their attention away from day-to-day activities, which may adversely affect our management's ability to oversee the development of our product candidates.

If we raise additional funds through collaborations, strategic alliances or marketing, distribution or licensing arrangements with third parties, we may have to relinquish valuable rights to our technologies, future revenue streams or product candidates or grant licenses on terms that may not be favorable to us.

Our ability to continue as a going concern requires that we obtain sufficient funding to finance our operations.

Our ability to continue as a going concern requires that we obtain sufficient funding to finance our operations. If we are unable to obtain sufficient funding, our business, prospects, financial condition and results of operations will be materially and adversely affected and we may be unable to continue as a going concern. If we are unable to continue as a going concern, we may have to liquidate our assets and may receive less than the value at which those assets are carried on our audited financial statements, and it is likely that investors will lose all or a part of their investment. If we seek additional

8

financing to fund our business activities in the future and there remains substantial doubt about our ability to continue as a going concern, investors or other financing sources may be unwilling to provide additional funding to us on commercially reasonable terms or at all.

We expect to incur significant additional costs as we continue commercialization efforts for current prescription drug candidates, or other product candidates, and undertake the clinical trials necessary to obtain any necessary regulatory approvals, which will increase our losses.

We commenced sales of Neonorm for preweaned dairy calves in the United States under the brand name Neonorm Calf at the end of 2014, and Napo commenced sales of Mytesi for adults with HIV/AIDS on antiretroviral therapy in February 2017. We will need to continue to invest in developing our internal and third-party sales and distribution network and outreach efforts to key opinion leaders in the gastrointestinal health industry, including physicians, as applicable. We will also need to conduct clinical trials for Mytesi in order to broaden Mytesi to additional indications.

We are actively identifying additional products for development and commercialization, and will continue to expend substantial resources for the foreseeable future to develop Mytesi, a second generation anti-secretory agent, and Canalevia for the MUMS indication of chemotherapy-induced diarrhea in dogs. These expenditures will include costs associated with:

- •

- identifying additional potential prescription drug product candidates and non-prescription products;

- •

- formulation studies;

- •

- conducting pilot, pivotal and toxicology studies;

- •

- completing other research and development activities;

- •

- payments to technology licensors;

- •

- maintaining our intellectual property;

- •

- obtaining necessary regulatory approvals;

- •

- establishing commercial supply capabilities; and

- •

- sales, marketing and distribution of our commercialized products.

We also may incur unanticipated costs in connection with developing and commercializing our products. Because the outcome of our development activities and commercialization efforts is inherently uncertain, the actual amounts necessary to successfully complete the development and commercialization of our current or future products and product candidates may be greater than we anticipate.

Because we anticipate incurring significant costs for the foreseeable future, if we are not successful in broadly commercializing any of our current or future products or product candidates or raising additional funding, including potential business development and/or strategic partnerships, to pursue our research and development efforts, we may never realize the benefit of our development efforts and our business may be harmed.

9

We will need to raise substantial additional capital in the future in the event that we conduct clinical trials for new indications and we may be unable to raise such funds when needed and on acceptable terms, which would force us to delay, limit, reduce or terminate one or more of our product development programs.

We are forecasting continued losses and negative cash flows as we continue to fund our operating and marketing activities and research and development programs, and we will not have sufficient cash on hand to fund our operating plan through March 31, 2019 and to complete the development of all the current products in our pipeline, or any additional products we may identify. We will need to seek additional funds sooner than planned through public or private equity or debt financings or other sources such as strategic collaborations. Any such financings or collaborations may result in dilution to our stockholders, the imposition of debt covenants and repayment obligations or other restrictions that may harm our business or the value of our common stock. We may also seek from time to time to raise additional capital based upon favorable market conditions or strategic considerations such as potential acquisitions or potential license arrangements.

Our future capital requirements depend on many factors, including, but not limited to:

- •

- the scope, progress, results and costs of researching and developing our current and future prescription drug product candidates and

non-prescription products;

- •

- the timing of, and the costs involved in, obtaining any regulatory approvals for our current and any future products;

- •

- the number and characteristics of the products we pursue;

- •

- the cost of manufacturing our current and future products and any products we successfully commercialize;

- •

- the cost of commercialization activities for Mytesi, Neonorm, Equilevia and Canalevia, if approved, including sales, marketing and distribution

costs;

- •

- the expenses needed to attract and retain skilled personnel;

- •

- the costs associated with being a public company;

- •

- our ability to establish and maintain strategic collaborations, distribution or other arrangements and the financial terms of such agreements;

and

- •

- the costs involved in preparing, filing, prosecuting, maintaining, defending and enforcing possible patent claims, including litigation costs and the outcome of any such litigation.

Additional funds may not be available when we need them on terms that are acceptable to us, or at all. If adequate funds are not available to us on a timely basis, we may be required to delay, limit, reduce or terminate one or more of our product development programs or future commercialization efforts.

We are substantially dependent on the success of our current lead prescription drug product candidate, Mytesi, and cannot be certain that necessary approvals will be received for planned Mytesi follow-on indications or that these product candidates will be successfully commercialized, either by us or any of our partners.

Other than Mytesi, we currently do not have regulatory approval for any of our prescription drug product candidates, including Canalevia. Our current efforts are primarily focused on the ongoing commercialization of Mytesi, and development efforts related to Mytesi and Canalevia. With regard to Mytesi, we are focused on the commercial launch of the product in the United States as well as on development efforts related to a follow-on indication for Mytesi in CTD, an important supportive care indication for patients undergoing cancer treatment. Mytesi is also in development for rare disease indications for infants and children with congenital diarrheal disorders and short bowel syndrome; for

10

IBS (Mytesi has demonstrated benefit to IBS-D patients in published Phase 2 studies); for supportive care for IBD; and as a second-generation anti-secretory agent for use in cholera patients. Mytesi has received orphan-drug designation for SBS. Accordingly, our near term prospects, including our ability to generate material product revenue, obtain any new financing if needed to fund our business and operations or enter into potential strategic transactions, will depend heavily on the success of Mytesi and potential follow-on indications.

Substantial time and capital resources have been previously devoted by third parties in the development of crofelemer, the active pharmaceutical ingredient, or API, in Mytesi and Canalevia, and the development of the botanical extract used in Equilevia and Neonorm. Both crofelemer and the botanical extract used in Equilevia and Neonorm were originally developed at Shaman Pharmaceuticals, Inc. ("Shaman"), by certain members of our management team, including Lisa A. Conte, our chief executive officer and president, and Steven R. King, Ph.D., our executive vice president of sustainable supply, ethnobotanical research and intellectual property and secretary. Shaman spent significant development resources before voluntarily filing for bankruptcy in 2001 pursuant to Chapter 11 of the U.S. Bankruptcy Code. The rights to crofelemer and the botanical extract used in Equilevia and Neonorm, as well as other intellectual property rights, were subsequently acquired by Napo from Shaman in 2001 pursuant to a court approved sale of assets. Ms. Conte founded Napo in 2001 and was the current interim chief executive officer of Napo and a member of Napo's board of directors prior to the Merger. While at Napo, certain members of our management team, including Ms. Conte and Dr. King, continued the development of crofelemer. In 2005, Napo entered into license agreements with Glenmark and Luye Pharma Group Limited for rights to various human indications of crofelemer in certain territories as defined in the respective license agreements with these licensees. Subsequently, after expending significant sums developing crofelemer, including trial design and on-going patient enrollment in the final pivotal Phase 3 trial for crofelemer for non-infectious diarrhea in adults with HIV/AIDS on antiretroviral therapy, in late 2008, Napo entered into a collaboration agreement with Salix Pharmaceuticals, Inc., or Salix, for development and commercialization rights to certain indications worldwide and certain rights in North America, Europe, and Japan, to crofelemer for human use. In January 2014, Jaguar entered into the Napo License Agreement pursuant to which Jaguar acquired an exclusive worldwide license to Napo's intellectual property rights and technology, including crofelemer and the botanical extract used in Equilevia and Neonorm, for all veterinary treatment uses and indications for all species of animals. In February 2014, most of the executive officers of Napo, and substantially all Napo's employees, became Jaguar's employees. In March 2016, Napo settled with Salix for the return of all commercial rights to crofelemer. Following the merger of Jaguar and Napo in July 2017, Napo became Jaguar's wholly-owned subsidiary. If we are not successful in the development and commercialization of Mytesi, Neonorm, Equilevia and Canalevia, our business and our prospects will be harmed.

The successful development and commercialization of Mytesi, Equilevia and Neonorm, and, if approved, Canalevia will depend on a number of factors, including the following:

- •

- our ability to demonstrate to the satisfaction of the FDA and any other regulatory bodies, the safety and efficacy of Canalevia for

chemotherapy-induced diarrhea in dogs;

- •

- our ability and that of our contract manufacturers to manufacture supplies of Mytesi, Neonorm, Equilevia and Canalevia

- •

- our ability to successfully continue commercial efforts associated with Mytesi, whether alone or in collaboration with others;

- •

- our ability to successfully launch Canalevia, assuming approval is obtained, and Equilevia, whether alone or in collaboration with others;

11

- •

- the availability, perceived advantages, relative cost, relative safety and relative efficacy of our prescription drug product candidates and

non-prescription products compared to alternative and competing treatments;

- •

- the acceptance of our prescription drug product candidates and non-prescription products as safe and effective by physicians, veterinarians,

patients, animal owners and the human and animal health community, as applicable;

- •

- our ability to achieve and maintain compliance with all regulatory requirements applicable to our business; and

- •

- our ability to obtain and enforce our intellectual property rights and obtain marketing exclusivity for our prescription drug product candidates and non-prescription products, and avoid or prevail in any third-party patent interference, patent infringement claims or administrative patent proceedings initiated by third parties or the U.S. Patent and Trademark Office ("USPTO").

Many of these factors are beyond our control. Accordingly, we may not be successful in developing or commercializing Mytesi, Neonorm, Equilevia, Canalevia or any of our other potential products. If we are unsuccessful or are significantly delayed in developing and commercializing Mytesi, Neonorm, Equilevia, Canalevia or any of our other potential products, our business and prospects will be harmed and you may lose all or a portion of the value of your investment in our common stock.

If we are not successful in identifying, licensing, developing and commercializing additional product candidates and products, our ability to expand our business and achieve our strategic objectives could be impaired.

Although a substantial amount of our efforts is focused on the commercial performance of Mytesi, a key element of our strategy is to identify, develop and commercialize a portfolio of products to serve the gastrointestinal health market. Most of our potential products are based on our knowledge of medicinal plants. Our current focus is primarily on product candidates whose active pharmaceutical ingredient or botanical extract has been successfully commercialized or demonstrated to be safe and effective in human or animal trials. In some instances, we may be unable to further develop these potential products because of perceived regulatory and commercial risks. Even if we successfully identify potential products, we may still fail to yield products for development and commercialization for many reasons, including the following:

- •

- competitors may develop alternatives that render our potential products obsolete;

- •

- an outside party may develop a cure for any disease state that is the target indication for any of our planned or approved drug products;

- •

- potential products we seek to develop may be covered by third-party patents or other exclusive rights;

- •

- a potential product may on further study be shown to have harmful side effects or other characteristics that indicate it is unlikely to be

effective or otherwise does not meet applicable regulatory criteria;

- •

- a potential product may not be capable of being produced in commercial quantities at an acceptable cost, or at all; and

- •

- a potential product may not be accepted as safe and effective by physicians, veterinarians, patients, animal owners, key opinion leaders and other decision-makers in the gastrointestinal health market, as applicable.

While we are developing specific formulations, including flavors, methods of administration, new patents and other strategies with respect to our current potential products, we may be unable to

12

prevent competitors from developing substantially similar products and bringing those products to market earlier than we can. If such competing products achieve regulatory approval and commercialization prior to our potential products, our competitive position may be impaired. If we fail to develop and successfully commercialize other potential products, our business and future prospects may be harmed and we will be more vulnerable to any problems that we encounter in developing and commercializing our current potential products.

Mytesi faces significant competition from other pharmaceutical companies, both for its currently approved indication and for planned follow-on indications, and our operating results will suffer if we fail to compete effectively.

The development and commercialization of products for human gastrointestinal health is highly competitive and our success depends on our ability to compete effectively with other products in the market. During the ongoing commercialization of Mytesi for its currently approved indication, and during the future commercialization of Mytesi for any planned follow-on indications, if such follow-on indications receive regulatory approval, we expect to compete with major pharmaceutical and biotechnology companies that operate in the gastrointestinal space, such as Sucampo AG, Takeda Pharmaceuticals, Allergan, Inc., Ironwood Pharmaceuticals, Inc., Synergy Pharmaceuticals Inc., Heron Therapeutics, Inc., Sebela Pharmaceuticals, Inc. and Salix Pharmaceuticals.

Many of our competitors and potential competitors in the human gastrointestinal space have substantially more financial, technical and human resources than we do. Many also have more experience in the development, manufacture, regulation and worldwide commercialization of human gastrointestinal health products.

For these reasons, we cannot be certain that we and Mytesi can compete effectively.

We may be unable to obtain, or obtain on a timely basis, regulatory approval for our existing or future human or animal prescription drug product candidates under applicable regulatory requirements, which would harm our operating results.

The research, testing, manufacturing, labeling, approval, sale, marketing and distribution of human and animal health products are subject to extensive regulation. We are typically not permitted to market our prescription drug product candidates in the United States until we receive approval of the product from the FDA through the filing of an NDA or NADA, as applicable. To gain approval to market a prescription drug, we must provide the FDA with safety and efficacy data from pivotal trials that adequately demonstrate that our prescription drug product candidates are safe and effective for the intended indications. Likewise, to gain approval to market an animal prescription drug for a particular species, we must provide the FDA with safety and efficacy data from pivotal trials that adequately demonstrate that our prescription drug product candidates are safe and effective in the target species (e.g. dogs) for the intended indications. In addition, we must provide manufacturing data evidencing that we can produce our product candidates in accordance with cGMP. For the FDA, we must also provide data from toxicology studies, also called target animal safety studies, and in some cases environmental impact data. In addition to our internal activities, we will partially rely on contract research organizations ("CROs"), and other third parties to conduct our toxicology studies and for certain other product development activities. The results of toxicology studies, other initial development activities, and/or any previous studies in humans or animals conducted by us or third parties may not be predictive of future results of pivotal trials or other future studies, and failure can occur at any time during the conduct of pivotal trials and other development activities by us or our CROs. Our pivotal trials may fail to show the desired safety or efficacy of our prescription drug product candidates despite promising initial data or the results in previous human or animal studies conducted by others. Success of a prescription drug product candidate in prior animal studies, or in the treatment of humans, does not ensure success in subsequent studies. Clinical trials in humans and pivotal trials in animals

13

sometimes fail to show a benefit even for drugs that are effective because of statistical limitations in the design of the trials or other statistical anomalies. Therefore, even if our studies and other development activities are completed as planned, the results may not be sufficient to obtain a required regulatory approval for a product candidate.

Regulatory authorities can delay, limit or deny approval of any of our prescription drug product candidates for many reasons, including:

- •

- if they disagree with our interpretation of data from our pivotal studies or other development efforts;

- •

- if we are unable to demonstrate to their satisfaction that our product candidate is safe and effective for the target indication and, if

applicable, in the target species;

- •

- if they require additional studies or change their approval policies or regulations;

- •

- if they do not approve of the formulation, labeling or the specifications of our current and future product candidates; and

- •

- if they fail to approve the manufacturing processes of our third-party contract manufacturers.

Further, even if we receive a required approval, such approval may be for a more limited indication than we originally requested, and the regulatory authority may not approve the labeling that we believe is necessary or desirable for successful commercialization.

Any delay or failure in obtaining any necessary regulatory approval for the intended indications of our human or animal product candidates would delay or prevent commercialization of such product candidates and would harm our business and our operating results.

The results of our earlier studies of Mytesi may not be predictive of the results in any future clinical trials and species-specific formulation studies, respectively, and we may not be successful in our efforts to develop or commercialize line extensions of Mytesi.

Our product pipeline includes a number of potential indications of Mytesi, our lead prescription product. The results of our studies and other development activities and of any previous studies conducted by us or third parties may not be predictive of future results of these clinical studies and formulation studies, respectively. Failure can occur at any time during the conduct of these trials and other development activities. Even if our formulation/clinical studies and other development activities are completed as planned, the results may not be sufficient to pursue a particular line extension for Mytesi. Further, even if we obtain promising results from our clinical trials, we may not successfully commercialize any line extension. Because line extensions are developed for a particular market, we may not be able to leverage our experience from the commercial launch of Mytesi in new markets. If we are not successful in developing and successfully commercializing these line extension products, we may not be able to grow our revenue and our business may be harmed.

Development of prescription drug products is inherently expensive, time-consuming and uncertain, and any delay or discontinuance of our current or future pivotal trials would harm our business and prospects.

Development of prescription drug products for human and animal gastrointestinal health remains an inherently lengthy, expensive and uncertain process, and our development activities may not be successful. We do not know whether our current or planned pivotal trials for any of our product candidates will begin or conclude on time, and they may be delayed or discontinued for a variety of reasons, including if we are unable to:

- •

- address any safety concerns that arise during the course of the studies;

14

- •

- complete the studies due to deviations from the study protocols or the occurrence of adverse events;

- •

- add new study sites;

- •

- address any conflicts with new or existing laws or regulations; or

- •

- reach agreement on acceptable terms with study sites, which can be subject to extensive negotiation and may vary significantly among different sites.

Further, we may not be successful in developing new indications for Mytesi and may be subject to the same regulatory regime as prescription drug products in jurisdictions outside the United States. Any delays in completing our development efforts will increase our costs, delay our development efforts and approval process and jeopardize our ability to commence product sales and generate revenue. Any of these occurrences may harm our business, financial condition and prospects. In addition, factors that may cause a delay in the commencement or completion of our development efforts may also ultimately lead to the denial of regulatory approval of our product candidates which, as described above, would harm our business and prospects.

We will partially rely on third parties to conduct our development activities. If these third parties do not successfully carry out their contractual duties, we may be unable to obtain regulatory approvals or commercialize our current or future human or animal product candidates on a timely basis, or at all.

We will partially rely upon CROs to conduct our toxicology studies and for other development activities. We intend to rely on CROs to conduct one or more of our planned pivotal trials. These CROs are not our employees, and except for contractual duties and obligations, we have limited ability to control the amount or timing of resources that they devote to our programs or manage the risks associated with their activities on our behalf. We are responsible for ensuring that each of our studies is conducted in accordance with the development plans and trial protocols presented to regulatory authorities. Any deviations by our CROs may adversely affect our ability to obtain regulatory approvals, subject us to penalties or harm our credibility with regulators. The FDA and foreign regulatory authorities also require us and our CROs to comply with regulations and standards, commonly referred to as good clinical practices ("GCPs"), or good laboratory practices ("GLPs"), for conducting, monitoring, recording and reporting the results of our studies to ensure that the data and results are scientifically valid and accurate.

Agreements with CROs generally allow the CROs to terminate in certain circumstances with little or no advance notice. These agreements generally will require our CROs to reasonably cooperate with us at our expense for an orderly winding down of the CROs' services under the agreements. If the CROs conducting our studies do not comply with their contractual duties or obligations, or if they experience work stoppages, do not meet expected deadlines, or if the quality or accuracy of the data they obtain is compromised, we may need to secure new arrangements with alternative CROs, which could be difficult and costly. In such event, our studies also may need to be extended, delayed or terminated as a result, or may need to be repeated. If any of the foregoing were to occur, regulatory approval, if required, and commercialization of our product candidates may be delayed and we may be required to expend substantial additional resources.

Even if we obtain regulatory approval for planned follow-on indications of Mytesi, or for Canalevia or our other product candidates, they may never achieve market acceptance. Further, even if we are successful in the ongoing commercialization of Mytesi, we may not achieve commercial success.

If we obtain necessary regulatory approvals for planned follow-on indications of Mytesi or for Canalevia or our other product candidates, such products may still not achieve market acceptance and

15

may not be commercially successful. Market acceptance of Mytesi and Canalevia, and any of our other products depends on a number of factors, including:

- •

- the safety of our products as demonstrated in our target human and animal studies;

- •

- the indications for which our products are approved or marketed;

- •

- the potential and perceived advantages over alternative treatments or products, including generic medicines and competing products currently

prescribed by physicians or veterinarians, as applicable, and, in the case of animal products, products approved for use in humans that are used extra-label in animals;

- •

- the acceptance by physicians, veterinarians, companion animal owners and production animal owners, as applicable, of our products as safe and

effective;

- •

- the cost in relation to alternative treatments and willingness on the part of physicians, veterinarians, patients and animal owners, as

applicable, to pay for our products;

- •

- the prevalence and severity of any adverse side effects of our products;

- •

- the relative convenience and ease of administration of our products; and

- •

- the effectiveness of our sales, marketing and distribution efforts.

Any failure by Mytesi, Canalevia and Equilevia or any of our other products to achieve market acceptance or commercial success would harm our financial condition and results of operations.

Human and animal gastrointestinal health products are subject to unanticipated post-approval safety or efficacy concerns, which may harm our business and reputation.

The success of our commercialization efforts will depend upon the perceived safety and effectiveness of human and animal gastrointestinal health products, in general, and of our products, in particular. Unanticipated safety or efficacy concerns can subsequently arise with respect to approved prescription drug products, such as Mytesi, or non-prescription products, such as Neonorm, which may result in product recalls or withdrawals or suspension of sales, as well as product liability and other claims. Any safety or efficacy concerns, or recalls, withdrawals or suspensions of sales of our products could harm our reputation and business, regardless of whether such concerns or actions are justified.

Future federal and state legislation may result in increased exposure to product liability claims, which could result in substantial losses.

Under current federal and state laws, companion and production animals are generally considered to be the personal property of their owners and, as such, the owners' recovery for product liability claims involving their companion and production animals may be limited to the replacement value of the animal. Companion animal owners and their advocates, however, have filed lawsuits from time to time seeking non-economic damages such as pain and suffering and emotional distress for harm to their companion animals based on theories applicable to personal injuries to humans. If new legislation is passed to allow recovery for such non-economic damages, or if precedents are set allowing for such recovery, we could be exposed to increased product liability claims that could result in substantial losses to us if successful. In addition, some horses can be worth millions of dollars or more, and product liability for horses may be very high. While we currently have product liability insurance, such insurance may not be sufficient to cover any future product liability claims against us.

16

If we fail to retain current members of our senior management, or to identify, attract, integrate and retain additional key personnel, our business will be harmed.

Our success depends on our continued ability to attract, retain and motivate highly qualified management and scientific personnel. We are highly dependent upon our senior management, particularly Lisa A. Conte, our president and Chief Executive Officer. The loss of services of any of our key personnel would cause a disruption in our ability to develop our current or future product pipeline and commercialize our products and product candidates. Although we have offer letters with these key members of senior management, such agreements do not prohibit them from resigning at any time. We currently do not maintain "key man" life insurance on any of our senior management team. The loss of Ms. Conte or other members of our current senior management could adversely affect the timing or outcomes of our current and planned studies, as well as the prospects for commercializing our products.

In addition, competition for qualified personnel in the human and animal gastrointestinal health fields is intense, because there are a limited number of individuals who are trained or experienced in the field. We will need to hire additional personnel as we expand our product development and commercialization activities. Even if we are successful in hiring qualified individuals, as we are a growing organization, we do not have a track record for integrating and retaining individuals. If we are not successful in identifying, attracting, integrating or retaining qualified personnel on acceptable terms, or at all, our business will be harmed.

We are dependent on two suppliers for the raw material used to produce the active pharmaceutical ingredient in Mytesi and Canalevia and the botanical extract in Neonorm and Equilevia. The termination of either of these contracts would result in a disruption to product development and our business will be harmed.

The raw material used to manufacture Mytesi, Canalevia, Neonorm and Equilevia is crude plant latex ("CPL"), derived from the Croton lechleri tree, which is found in countries in South America, principally Peru. The ability of our contract suppliers to harvest CPL is governed by the terms of their respective agreements with local government authorities. Although CPL is available from multiple suppliers, we only have contracts with two suppliers to obtain CPL and arrange the shipment to our contract manufacturer. Accordingly, if our contract suppliers do not or are unable to comply with the terms of our respective agreements, and we are not able to negotiate new agreements with alternate suppliers on terms that we deem commercially reasonable, it may harm our business and prospects. The countries from which we obtain CPL could change their laws and regulations regarding the export of the natural products or impose or increase taxes or duties payable by exporters of such products. Restrictions could be imposed on the harvesting of the natural products or additional requirements could be implemented for the replanting and regeneration of the raw material. Such events could have a significant impact on our cost and ability to produce Mytesi, Canalevia, Neonorm, Equilevia and anticipated line extensions.

We are dependent upon third-party contract manufacturers, both for the supply of the active pharmaceutical ingredient in Mytesi and Canalevia and the botanical extract in Neonorm and Equilevia, as well as for the supply of finished products for commercialization.

We have contracted with third parties for the formulation of API and botanical extract into finished products for our studies. We have also entered into memorandums of understanding with Indena S.p.A. for the manufacture of CPL received from our suppliers into the API in Canalevia to support our regulatory filings, as well as the botanical extract in Neonorm and agreed to negotiate a commercial supply agreement. Indena S.p.A. has never manufactured either such ingredient to commercial scale. Glenmark is the current manufacturer of crofelemer, the active API in Canalevia, for Mytesi, and the manufacturer on file for the NDA to which we have a right of reference. As announced in October of 2015, we have entered an agreement with Patheon, a provider of drug

17

development and delivery solutions, under which Patheon provides enteric-coated tablets to us. We also may contract with additional third parties for the formulation and supply of finished products, which we will use in our planned studies and commercialization efforts.

We will be dependent upon our contract manufacturers for the supply of the API in Mytesi and Canalevia. We currently have sufficient quantities of the botanical extract used in Neonorm and Equilevia to support initial commercialization of Neonorm and Equilevia. However, we will require additional quantities of the botanical extract if our ongoing commercialization of Neonorm or our commercial launch of Equilevia is successful. If we are not successful in reaching agreements with third parties on terms that we consider commercially reasonable for manufacturing and formulation, or if our contract manufacturer and formulator are not able to produce sufficient quantities or quality of API, botanical extract or finished product under their agreements, it could delay our plans and harm our business prospects.

The facilities used by our third-party contractors are subject to inspections, including by the FDA, and other regulators, as applicable. We also depend on our third-party contractors to comply with cGMP. If our third-party contractors do not maintain compliance with these strict regulatory requirements, we and they will not be able to secure or maintain regulatory approval for their facilities, which would have an adverse effect on our operations. In addition, in some cases, we also are dependent on our third-party contractors to produce supplies in conformity to our specifications and maintain quality control and quality assurance practices and not to employ disqualified personnel. If the FDA or a comparable foreign regulatory authority does not approve the facilities of our third-party contractors if so required, or if it withdraws any such approval in the future, we may need to find alternative manufacturing or formulation facilities, which could result in delays in our ability to develop or commercialize our human and animal products, if at all. We and our third-party contractors also may be subject to penalties and sanctions from the FDA and other regulatory authorities for any violations of applicable regulatory requirements. The USDA and the European Medicines Agency (the "EMA"), employ different regulatory standards than the FDA, so we may require multiple manufacturing processes and facilities for the same human or animal product candidate or any approved product. We are also exposed to risk if our third-party contractors do not comply with the negotiated terms of our agreements, or if they suffer damage or destruction to their facilities or equipment.

If we are unable to establish sales capabilities on our own or through third parties, we may not be able to market and sell our current or future human or animal products and product candidates, if approved, and generate product or other revenue.

We currently have limited sales, marketing or distribution capabilities, and prior to Napo's launch of Mytesi for the symptomatic relief of noninfectious diarrhea in adults with HIV/AIDS on antiretroviral therapy, and our launch of Neonorm for preweaned dairy calves, we had no experience in the sale, marketing and distribution of human or animal health products. There are significant risks involved in building and managing a sales organization, including our potential inability to attract, hire, retain and motivate qualified individuals, generate sufficient sales leads, provide adequate training to sales and marketing personnel and effectively oversee a geographically dispersed sales and marketing team. Any failure or delay in the development of our internal sales, marketing and distribution capabilities and entry into adequate arrangements with distributors or other partners would adversely impact the commercialization of Mytesi, Neonorm, Equilevia and, if approved, Canalevia. If we are not successful in commercializing Mytesi, Neonorm, Equilevia, Canalevia or any of our other line extension products, either on our own or through one or more distributors, or in generating upfront licensing or other fees, we may never generate significant revenue and may continue to incur significant losses, which would harm our financial condition and results of operations.

18

Changes in distribution channels for animal health prescription drugs may make it more difficult or expensive to distribute our animal health prescription drug products.

In the United States, animal owners typically purchase their animal health prescription drugs from their local veterinarians who also prescribe such drugs. There is a trend, however, toward increased purchases of animal health prescription drugs from Internet-based retailers, "big-box" retail stores and other over-the-counter distribution channels, which follows an emerging shift in recent years away from the traditional veterinarian distribution channel. It is also possible that animal owners may come to rely increasingly on Internet-based animal health information rather than on their veterinarians. We currently expect to market our animal health prescription drugs directly to veterinarians, so any reduced reliance on veterinarians by animal owners could harm our business and prospects by making it more difficult or expensive for us to distribute our animal health prescription drug products.