Form N-CSRS BERNSTEIN SANFORD C FUND For: Mar 31

Tweet

Tweet Share

ShareTable of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21034

SANFORD C. BERNSTEIN FUND II, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: September 30, 2018

Date of reporting period: March 31, 2018

Table of Contents

ITEM 1. REPORTS TO STOCKHOLDERS.

Table of Contents

SANFORD C. BERNSTEIN FUND II, INC.

INTERMEDIATE DURATION INSTITUTIONAL PORTFOLIO

SEMI-ANNUAL REPORT

MARCH 31, 2018

Table of Contents

| 1 | ||||

| 3 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 29 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 51 |

Before investing in the Sanford C. Bernstein Fund II, Inc., a prospective investor should consider carefully the portfolio’s investment objectives and policies, charges, expenses and risks. These and other matters of importance to prospective investors are contained in the portfolio’s prospectus, an additional copy of which may be obtained by visiting our website at www.Bernstein.com and clicking on “Investments”, then “Mutual Fund Information—Prospectuses, SAIs and Shareholder Reports” or by calling your financial advisor or by calling Bernstein’s mutual fund shareholder help line at 212.756.4097. Please read the prospectus carefully before investing.

For performance information current to the most recent month-end, please visit our website at www.Bernstein.com and click on “Investments”, then “Mutual Fund Information—Mutual Fund Performance at a Glance”.

This shareholder report must be preceded or accompanied by the Sanford C. Bernstein Fund II, Inc. prospectus for individuals who are not shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit www.AllianceBernstein.com, or go to the Securities and Exchange Commission’s website at www.sec.gov, or call AllianceBernstein at 800.227.4618.

The Fund will file its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q is available on the Commission’s website at www.sec.gov. The Fund’s Form N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C.; information on the operation of the Public Reference Room may be obtained by calling 800.SEC.0330.

Investment Products Offered: · Are Not FDIC Insured · May Lose Value · Are Not Bank Guaranteed

Table of Contents

Portfolio Manager Commentary (Unaudited)

To Our Shareholders—May 15, 2018

On the following pages, you will find the 2018 semi-annual report for Sanford C. Bernstein Fund II, Inc.—Intermediate Duration Institutional Portfolio1 (the “Portfolio”). The semi-annual report covers the six- and 12-month periods ended March 31, 2018, and includes financial statements as well as notes to the financial statements, information about the recent performance of the Portfolio and a listing of the Portfolio’s holdings as of the period end.

Equity market returns decelerated during the six-month period ended March 31, 2018, as volatility resurfaced. Despite this, all regions of the world delivered positive returns for the period, with emerging-market equities remaining the top performer. Reflecting an increase in interest rates, both US taxable and tax-exempt bond returns were slightly negative.

Some slowing of stock returns seemed likely after a very strong 2017, when corporate earnings growth gained momentum and markets responded accordingly. Risk returned in 2018, with a correction in February interrupting the longest and calmest winning streak ever. Concerns about potentially rising inflation and interest rates, as well as risks around tariff wars, spurred heightened volatility, but we believe the global economy is strong enough that markets can withstand increased uncertainty.

Looking ahead, our return expectations remain below long-term averages. In our view, strong 2018 earnings growth has been largely priced in to stocks. We also anticipate that interest rates will climb gradually, potentially leading to subdued bond returns.

If you have any questions about your investments in the Portfolio, please contact your Bernstein Advisor by calling 212.756.4097, or visit www.Bernstein.com. As always, we are firmly dedicated to your investment success. Thank you for your continued interest in the Portfolio.

Sincerely,

Robert M. Keith

President and Chief Executive Officer

Sanford C. Bernstein Fund II, Inc.

| 1 | This performance discussion is intended as a general market commentary. |

Investment Objectives and Policies

The Portfolio seeks to provide safety of principal and a moderate to high rate of current income. The Portfolio seeks to maintain an average portfolio quality minimum of A, based on ratings given to the Portfolio’s securities by national rating agencies (or, if unrated, determined by AllianceBernstein L.P., the Portfolio’s investment adviser (the “Adviser”), to be of comparable quality). Many types of securities may be purchased by the Portfolio, including corporate bonds, notes, US government and agency securities, asset-backed securities, mortgage-related securities, bank loan debt, preferred stock and inflation-protected securities, as well as others. The Portfolio may also invest up to 25% of its total assets in fixed-income, non-US dollar denominated foreign securities, and may invest without limit in fixed-income, US dollar denominated foreign securities, in each case in developed- or emerging-market countries.

The Portfolio may use derivatives, such as options, futures contracts, forward contracts and swaps.

The Portfolio may invest up to 25% of its total assets in fixed-income securities rated below investment-grade (BB or below) by national rating agencies (commonly known as “junk bonds”). No more than 5% of the Portfolio’s total assets may be invested in fixed-income securities rated CCC by national rating agencies.

In managing the Portfolio, the Adviser may use interest rate forecasting to estimate the best level of interest rate risk at a given time. The Adviser may moderately shorten the average duration of the Portfolio when it expects interest rates to rise and modestly lengthen average duration when it anticipates that interest rates will fall.

The Portfolio seeks to maintain an effective duration of three to six years under normal market conditions. Duration is a measure that relates the expected price volatility of a security to changes in interest rates. The duration of a debt security is the weighted average term to maturity, expressed in years, of the present value of all future cash flows, including coupon payments and principal repayments.

(Portfolio Manager Commentary continued on next page)

| 2018 Semi-Annual Report | 1 |

Table of Contents

Portfolio Manager Commentary (continued)

The Adviser selects securities for purchase or sale based on its assessment of the securities’ risk and return characteristics as well as the securities’ impact on the overall risk and return characteristics of the Portfolio. In making this assessment, the Adviser takes into account various factors including the credit quality and sensitivity to interest rates of the securities under consideration and of the Portfolio’s other holdings.

The Portfolio may enter into foreign currency transactions on a spot (i.e., cash) basis or through the use of derivatives transactions, such as forward currency exchange contracts, currency futures and options thereon, and options on currencies. An appropriate hedge of currency exposure resulting from the Portfolio’s securities positions may not be available or cost effective, or the Adviser may determine not to hedge the positions, possibly even under market conditions where doing so could benefit the Portfolio.

| 2 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

Disclosures and Risks (Unaudited)

Benchmark Disclosures

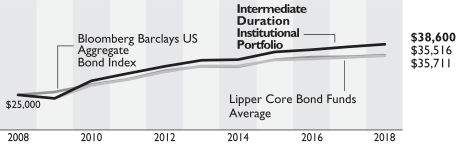

None of the following indices or averages reflects fees and expenses associated with the active management of a mutual fund portfolio. The Bloomberg Barclays US Aggregate Bond Index represents the performance of securities within the US investment-grade fixed-rate bond market, with index components for government and corporate securities, mortgage pass-through securities, asset-backed securities and commercial mortgaged-backed securities. The Lipper Core Bond Funds Average is the equal-weighted average returns of the portfolios in the relevant Lipper Inc. category; the average portfolios in a category may differ in composition from the Portfolio. The Lipper Core Bond Funds Average contains portfolios that invest primarily in investment-grade debt issues (rated in the top four grades) with dollar-weighted average maturities of five to ten years. An investor cannot invest directly in an index or average, and their results are not indicative of the performance for any specific investment, including the Portfolio.

A Word About Risk

The share price of the Portfolio will fluctuate and you may lose money. There is no guarantee that the Portfolio will achieve its investment objective.

Interest Rate Risk: This is the risk that changes in interest rates will affect the value of the Portfolio’s investments in fixed-income debt securities such as bonds and notes. The Portfolio may be subject to a greater risk of rising interest rates due to the current period of historically low rates and the effect of potential government fiscal policy initiatives and Federal Reserve and other central bank monetary initiatives, as well as the market reaction to those initiatives. Increases in interest rates may cause the value of the Portfolio’s investments to decline and this decrease in value may not be offset by higher income from new investments. The Portfolio may experience increased interest rate risk to the extent it invests in fixed-income securities with longer maturities or durations. A general rise in interest rates may cause investors to move out of fixed-income securities on a large scale, which could adversely affect the price and liquidity of fixed-income securities and could also result in increased redemptions from funds, such as the Portfolio, that invest largely in fixed-income securities.

Credit Risk: This is the risk that the issuer or the guarantor of a debt security, or the counterparty to a derivatives or other contract, will be unable or unwilling to make timely principal and/or interest payments, or to otherwise honor its obligations. The issuer or guarantor may default, potentially causing a loss of the full principal amount of a security and accrued interest. The degree of risk for a particular security may be reflected in its credit rating. The credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations. At times when credit risk is perceived to be greater, credit “spreads” (i.e., the difference between the yields on lower quality securities and the yields on higher quality securities) may get larger or “widen”. As a result, the values of the lower quality securities may go down more and they may become harder to sell and less liquid.

Duration Risk: The duration of a fixed-income security may be shorter than or equal to full maturity of the fixed-income security. Fixed-income securities with longer durations have more interest rate risk and will decrease in price as interest rates rise. For example, a fixed-income security with a duration of three years would be expected to decrease in value by approximately 3% if interest rates increase by 1%. Securities that have final maturities longer than their durations may be affected by increased credit spreads to a far greater degree than their durations would suggest, because they are exposed to credit risk until final maturity.

Inflation Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Portfolio’s assets can decline as can the value of the Portfolio’s distributions. This risk is significantly greater for fixed-income securities with longer maturities.

Inflation-Protected Securities Risk: The terms of inflation-protected securities provide for the coupon and/or maturity value to be adjusted based on changes in an inflation index. Decreases in the inflation rate or in investors’ expectations about inflation could cause these securities to underperform non-inflation-adjusted securities on a total-return basis. In addition, these securities may have limited liquidity in the secondary market.

Foreign (Non-US) Securities Risk: Investments in foreign securities entail significant risks in addition to those customarily associated with investing in US securities. These risks include risks related to adverse market, economic, political and regulatory factors and social instability, all of which could disrupt the financial markets in which the Portfolio invests and adversely affect the value of the Portfolio’s assets.

(Disclosures and Risks continued on next page)

| 2018 Semi-Annual Report | 3 |

Table of Contents

Disclosures and Risks (continued)

Emerging-Markets Securities Risk: The risks of investing in foreign (non-US) securities are heightened with respect to issuers in emerging-market countries, because the markets are less developed and less liquid and there may be a greater amount of economic, political and social uncertainty, and these risks are even more pronounced in “frontier” markets, which are investable markets with lower total market capitalization and liquidity than the more developed emerging markets. In addition, the value of the Portfolio’s investments may decline because of factors such as unfavorable or unsuccessful government actions and reduction of government or central bank support

Derivatives Risk: The Portfolio may use derivatives as direct investments to earn income, enhance return and broaden portfolio diversification, which entail greater risk than if used solely for hedging purposes. In addition to other risks such as the credit risk of the counterparty, derivatives involve the risk that changes in the value of the derivative may not correlate with relevant assets, rates or indices. Derivatives may be illiquid and difficult to price or unwind, and small changes may produce disproportionate losses for the Portfolio. Certain derivatives have the potential for unlimited loss, regardless of the size of the initial investment. Assets required to be set aside or posted to cover or secure derivatives positions may themselves go down in value, and these collateral and other requirements may limit investment flexibility. Some derivatives involve leverage, which can make the Portfolio more volatile and can compound other risks. Use of derivatives may have different tax consequences for the Portfolio than an investment in the underlying security, and such differences may affect the amount, timing and character of income distributed to shareholders. The US government and foreign governments are in the process of adopting and implementing regulations governing derivatives markets, including mandatory clearing of certain derivatives, margin, reporting and registration requirements. The ultimate impact of the regulations remains unclear. Additional regulation may make derivatives more costly, limit their availability or utility, otherwise adversely affect their performance, or disrupt markets.

Mortgage-Related Securities Risk: Mortgage-related securities represent interests in “pools” of mortgages, including consumer loans or receivables held in trust. Mortgage-related securities are subject to credit, interest rate, prepayment and extension risks. These securities also are subject to risk of default on the underlying mortgage, particularly during periods of economic downturn. Small movements in interest rates (both increases and decreases) may quickly and significantly reduce the value of certain mortgage-related securities.

Prepayment and Extension Risk: Prepayment risk is the risk that a loan, bond or other security might be called or otherwise converted, prepaid or redeemed before maturity. If this happens, particularly during a time of declining interest rates or credit spreads, the Portfolio will not benefit from the rise in market price that normally accompanies a decline in interest rates, and may not be able to invest the proceeds in securities providing as much income, resulting in a lower yield to the Portfolio. Conversely, extension risk is the risk that as interest rates rise or spreads widen, payments of securities may occur more slowly than anticipated by the market. If this happens, the values of these securities may go down because their interest rates are lower than current market rates and they remain outstanding longer than anticipated.

Subordination Risk: The Portfolio may invest in securities that are subordinated to more senior securities of an issuer, or which represent interests in pools of such subordinated securities. Subordinated securities will be disproportionately affected by a default or even a perceived decline in creditworthiness of the issuer. Subordinated securities are more likely to suffer a credit loss than non-subordinated securities of the same issuer, any loss incurred by the subordinated securities is likely to be proportionately greater, and any recovery of interest or principal may take more time.

Management Risk: The Portfolio is subject to management risk because it is an actively managed investment portfolio. The Adviser will apply its investment techniques and risk analyses in making investment decisions for the Portfolio, but these techniques, analyses and decisions may not work as intended or may not produce the desired results. In some cases, derivatives and other investment techniques may be unavailable or the Adviser may determine not to use them, possibly even under market conditions where their use could benefit the Portfolio. In addition, the Adviser may change the Portfolio’s investment strategies or policies from time to time. Those changes may not lead to the results intended by the Adviser and could have an adverse on effect the value or performance of the Portfolio.

Liquidity Risk: Liquidity risk exists when particular investments are difficult to purchase or sell, possibly preventing the Portfolio from selling out of these illiquid or relatively less liquid securities at an advantageous price. Over

(Disclosures and Risks continued on next page)

| 4 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

Disclosures and Risks (continued)

recent years, regulatory changes have led to reduced liquidity in the marketplace, and the capacity of dealers to make markets in fixed-income securities has been outpaced by the growth in the size of the fixed-income markets. Liquidity risk may be magnified in a rising interest rate environment, where the value and liquidity of fixed-income securities generally go down. Derivatives and securities involving substantial market and credit risk tend to involve greater liquidity risk. Illiquid securities and relatively less liquid securities may also be difficult to value.

Redemption Risk: The Portfolio may experience heavy redemptions that could cause the Portfolio to liquidate its assets at inopportune times or at a loss or depressed value, which could cause the value of your investment to decline. Redemption risk is heightened during periods of overall market turmoil.

Foreign Currency Risk: This is the risk that changes in foreign (non-US) currency exchange rates may negatively affect the value of the Portfolio’s investments or reduce the returns of the Portfolio. For example, the value of the Portfolio’s investments in foreign securities and foreign currency positions may decrease if the US dollar is strong (i.e., gaining value relative to other currencies) and other currencies are weak (i.e., losing value relative to the US dollar).

Actions by a Few Major Investors: In certain countries, volatility may be heightened by actions of a few major investors. For example, substantial increases or decreases in cash flows of mutual funds investing in these markets could significantly affect local securities prices and, therefore, share prices of the Portfolio.

Market Risk: The Portfolio is subject to market risk, which is the risk that bond prices in general may decline over short or extended periods. In the past decade, financial markets in the United States, Europe and elsewhere have experienced increased volatility, decreased liquidity and heightened uncertainty. These market conditions may recur from time to time and have an adverse impact on various securities markets. The US government and the Federal Reserve, as well as certain foreign governments and central banks, have taken steps to support financial markets. Other governments have tried to support markets by buying stocks and through other market interventions. Government intervention may not work as intended, particularly if the efforts are perceived by investors as being unlikely to achieve the desired results. The Federal Reserve has reduced its market support activities and has begun raising interest rates. Further Federal Reserve or other US or non-US governmental or central bank actions, including interest rate increases or decreases, could negatively affect financial markets generally, increase market volatility and reduce the value and liquidity of securities in which the Portfolio invests.

Current political uncertainty surrounding the European Union (“EU”) and its membership may increase market volatility. The United Kingdom has voted to withdraw from the EU, and one or more other countries may withdraw from the EU and/or abandon the Euro, the common currency of the EU. The financial instability of some countries in the EU, together with the risk of that financial instability impacting other more stable countries, may increase the risk of investing in companies in Europe and worldwide. In addition, policy and legislative changes in the United States and in other countries are affecting many aspects of financial regulation, and may in some instances contribute to decreased liquidity and increased volatility in the financial markets. The impact of these changes, and the practical implications for market participants, may not be fully known for some time.

Economies and financial markets throughout the world are becoming increasingly interconnected. Economic, financial or political events, trading and tariff arrangements, terrorism, natural disasters and other circumstances in one country or region could have profound impacts on global economies or markets. As a result, whether or not the Portfolio invests in securities of issuers located in or with significant exposure to countries experiencing economic and financial difficulties, the value and liquidity of the Portfolios’ investments may be negatively affected.

Lower-rated Securities Risk: Lower-rated securities, or junk bonds/high-yield securities, are subject to greater risk of loss of principal and interest and greater market risk than higher-rated securities. The capacity of issuers of lower-rated securities to pay interest and repay principal is more likely to weaken than is that of issuers of higher-rated securities in times of deteriorating economic conditions or rising interest rates.

Portfolio Turnover Risk: The Portfolio’s investment strategies may result in high portfolio turnover. The Portfolio generally buys portfolio securities with the intention of holding them for investment. However, when market conditions or other circumstances warrant, securities may be purchased and sold without regard to the length of time held. From time to time, the Portfolio may engage in active short-term trading to

(Disclosures and Risks continued on next page)

| 2018 Semi-Annual Report | 5 |

Table of Contents

Disclosures and Risks (continued)

seek short-term profits during periods of fluctuating interest rates or for other reasons. This trading may increase the Portfolio’s rate of turnover and the incidence of short-term capital gain taxable as ordinary income. A higher rate of portfolio turnover may increase transaction costs, which must be borne by the Portfolio and its shareholders.

These risks are discussed in further detail in the Portfolio’s prospectus.

An Important Note About Historical Performance

Except as noted, returns do not reflect the deduction of taxes that a shareholder would pay on portfolio distributions or the redemption of portfolio shares. All fees and expenses related to the operation of the Portfolio have been deducted.

The performance shown in this report represents past performance and does not guarantee future results. Performance information is as of the dates shown. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by visiting www.Bernstein.com or by calling 212.756.4097. The investment return and principal value of an investment in the Portfolio will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost.

Investors should consider the investment objectives, risks, charges and expenses of the Portfolio carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit www.Bernstein.com, click on “Investments”, then “Mutual Fund Information—Prospectuses, SAIs and Shareholder Reports”, or call Bernstein’s mutual fund shareholder help line at 212.756.4097 or contact your Bernstein Advisor. Please read the prospectus and/or summary prospectus carefully before investing.

| 6 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

Historical Performance (Unaudited)

Intermediate Duration Institutional Portfolio vs. Its Benchmark and Lipper Average

| TOTAL RETURNS | AVERAGE ANNUAL TOTAL RETURNS |

|||||||||||||||||||||

| THROUGH MARCH 31, 2018 | PAST SIX MONTHS |

PAST 12 MONTHS |

PAST FIVE YEARS |

PAST 10 YEARS |

SINCE INCEPTION |

INCEPTION DATE | ||||||||||||||||

| Intermediate Duration Institutional Portfolio1 |

-0.76 | % | 1.71 | % | 2.37 | % | 4.44 | % | 4.62 | % | 5/17/2002 | |||||||||||

| Bloomberg Barclays US Aggregate Bond Index |

-1.08 | % | 1.20 | % | 1.82 | % | 3.63 | % | 4.34 | % | ||||||||||||

| Lipper Core Bond Funds Average |

-1.11 | % | 1.12 | % | 1.65 | % | 3.57 | % | ||||||||||||||

| 1 | There are no sales charges associated with an investment in the Portfolio. Total returns and average annual returns are therefore the same. |

The current prospectus table shows the total annual operating expense ratio for the Portfolio as 0.54%, gross of any fee waivers or expense reimbursements. Contractual fee waivers and/or expense reimbursements limit the annual operating expense ratio to 0.45%. These waivers/reimbursements may not be terminated before January 29, 2019, and may be extended by the Adviser for additional one-year terms. Absent reimbursements or waivers, performance would have been lower. The Financial Highlights section of this report sets forth expense ratio data for the current reporting period; the expense ratio shown above may differ from the expense ratio in the Financial Highlights section since they are based on different time periods.

| Growth of a $25,000 Investment in the Portfolio | ||||||||

The chart illustrates the total value of an assumed $25,000 minimum investment as compared to the performance of the Portfolio’s benchmark and Lipper Average for the 10-year period ended March 31, 2018.

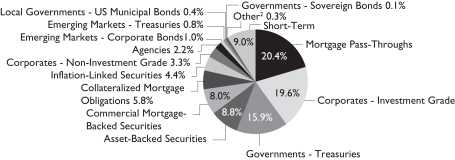

Portfolio Summary—March 31, 2018 (Unaudited)

| Security Type Breakdown1 | ||||||||

|

||||||||

| 1 | All data are as of March 31, 2018. The Portfolio’s security type breakdown is expressed as a percentage of total investments and may vary over time. The Portfolio also enters into derivative transactions, which may be used for hedging or investment purposes (see “Schedule of Investments” section of the report for additional details). |

| 2 | “Other” represents less than 0.1% in Common Stocks, Emerging Markets—Sovereigns and Quasi-Sovereigns. |

See Disclosures, Risks and Note about Historical Performance on pages 3-6.

| 2018 Semi-Annual Report | 7 |

Table of Contents

Expense Example—March 31, 2018 (Unaudited)

As a shareholder of the Fund, you incur various types of costs including management fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses—The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes—The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| BEGINNING ACCOUNT VALUE OCTOBER 1, 2017 |

ENDING ACCOUNT VALUE MARCH 31, 2018 |

EXPENSES PAID DURING PERIOD* |

ANNUALIZED EXPENSE RATIO* |

|||||||||||||

| SCB Intermediate Duration Institutional Portfolio |

||||||||||||||||

| Actual |

$ | 1,000 | $ | 992.40 | $ | 2.24 | 0.45 | % | ||||||||

| Hypothetical** |

$ | 1,000 | $ | 1,022.69 | $ | 2.27 | 0.45 | % | ||||||||

| * | Expenses are equal to the classes’ annualized expense ratios, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

| ** | Assumes 5% annual return before expenses. |

| 8 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

Sanford C. Bernstein Fund II, Inc.

Schedule of Investments

Intermediate Duration Institutional Portfolio

March 31, 2018 (Unaudited)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| MORTGAGE PASS-THROUGHS–22.0% | ||||||||||||

| Agency ARMs–0.0% | ||||||||||||

| Federal Home Loan Mortgage Corp. |

U.S.$ | 1 | $ | 577 | ||||||||

| Series 2007 |

1 | 1,362 | ||||||||||

| Federal National Mortgage Association |

2 | 2,338 | ||||||||||

| 3.579%, 3/01/37(a) |

2 | 2,356 | ||||||||||

|

|

|

|||||||||||

| 6,633 | ||||||||||||

|

|

|

|||||||||||

| Agency Fixed Rate 15-Year–1.8% | ||||||||||||

| Federal National Mortgage Association |

7,805 | 7,659,607 | ||||||||||

| Series 2017 |

4,743 | 4,654,036 | ||||||||||

|

|

|

|||||||||||

| 12,313,643 | ||||||||||||

|

|

|

|||||||||||

| Agency Fixed Rate 30-Year–20.2% | ||||||||||||

| Federal Home Loan Mortgage Corp. Gold |

53 | 58,294 | ||||||||||

| Series 2007 |

324 | 354,724 | ||||||||||

| Series 2016 |

3,045 | 3,152,890 | ||||||||||

| Series 2017 |

2,302 | 2,381,022 | ||||||||||

| Federal National Mortgage Association |

902 | 987,011 | ||||||||||

| Series 2004 |

820 | 897,097 | ||||||||||

| Series 2005 |

875 | 957,778 | ||||||||||

| Series 2006 |

179 | 195,421 | ||||||||||

| Series 2007 |

215 | 235,471 | ||||||||||

| Series 2008 |

1 | 1,341 | ||||||||||

| Series 2009 |

39 | 42,287 | ||||||||||

| Series 2010 |

1,372 | 1,421,660 | ||||||||||

| 5.00%, 6/01/40 |

36 | 39,309 | ||||||||||

| Series 2013 |

U.S.$ | 4,858 | $ | 5,028,398 | ||||||||

| Series 2015 |

5,115 | 5,007,971 | ||||||||||

| Series 2017 |

7,910 | 7,931,480 | ||||||||||

| Series 2018 |

48,540 | 48,668,731 | ||||||||||

| 4.00%, 4/01/48, TBA |

29,132 | 29,892,165 | ||||||||||

| 4.50%, 4/01/48, TBA |

27,130 | 28,405,956 | ||||||||||

| Government National Mortgage Association |

3,276 | 3,234,050 | ||||||||||

|

|

|

|||||||||||

| 138,893,056 | ||||||||||||

|

|

|

|||||||||||

| Other Agency Fixed Rate Programs–0.0% | ||||||||||||

| Federal National Mortgage Association |

123 | 133,492 | ||||||||||

|

|

|

|||||||||||

| Total Mortgage Pass-Throughs (cost $151,709,968) |

151,346,824 | |||||||||||

|

|

|

|||||||||||

| CORPORATES–INVESTMENT GRADE–21.2% | ||||||||||||

| Financial Institutions–11.4% | ||||||||||||

| Banking–9.5% | ||||||||||||

| ABN AMRO Bank NV |

269 | 275,685 | ||||||||||

| American Express Co. |

34 | 32,945 | ||||||||||

| Banco Santander SA |

1,200 | 1,194,876 | ||||||||||

| 5.179%, 11/19/25 |

800 | 834,648 | ||||||||||

| Bank of America Corp. |

1,810 | 1,771,194 | ||||||||||

| 3.824%, 1/20/28 |

1,835 | 1,816,852 | ||||||||||

| 4.20%, 8/26/24 |

56 | 56,762 | ||||||||||

| 5.00%, 5/13/21 |

10 | 10,533 | ||||||||||

| 5.875%, 1/05/21 |

35 | 37,536 | ||||||||||

| Series G |

905 | 878,547 | ||||||||||

| Bank of Tokyo-Mitsubishi UFJ Ltd. (The) |

700 | 689,269 | ||||||||||

| Banque Federative du Credit Mutuel SA |

705 | 696,131 | ||||||||||

| Barclays PLC |

200 | 192,944 | ||||||||||

| 4.375%, 1/12/26 |

200 | 201,012 | ||||||||||

| BB&T Corp. |

588 | 583,078 | ||||||||||

| BNP Paribas SA |

989 | 976,321 | ||||||||||

| 3.80%, 1/10/24(b) |

552 | 551,034 | ||||||||||

| Series E |

EUR | 476 | 599,833 | |||||||||

| 2018 Semi-Annual Report | 9 |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| BPCE SA |

U.S.$ | 575 | $ | 565,587 | ||||||||

| 5.70%, 10/22/23(b) |

379 | 406,171 | ||||||||||

| Capital One Financial Corp. |

1,725 | 1,663,417 | ||||||||||

| 4.75%, 7/15/21 |

90 | 93,893 | ||||||||||

| Citigroup, Inc. |

2,105 | 2,054,817 | ||||||||||

| 3.875%, 3/26/25 |

1,575 | 1,556,163 | ||||||||||

| 3.887%, 1/10/28 |

500 | 496,695 | ||||||||||

| Citizens Bank NA/Providence RI |

500 | 492,005 | ||||||||||

| Commonwealth Bank of Australia/New York NY |

420 | 414,212 | ||||||||||

| Compass Bank |

1,785 | 1,732,467 | ||||||||||

| 5.50%, 4/01/20 |

1,537 | 1,595,990 | ||||||||||

| Cooperatieve Rabobank UA |

443 | 446,978 | ||||||||||

| 4.375%, 8/04/25 |

1,044 | 1,054,116 | ||||||||||

| 6.875%, 3/19/20(b) |

EUR | 100 | 138,533 | |||||||||

| Cooperatieve Rabobank UA/NY |

U.S.$ | 698 | 689,114 | |||||||||

| Credit Agricole SA/London |

600 | 595,188 | ||||||||||

| 3.375%, 1/10/22(b) |

680 | 675,315 | ||||||||||

| 4.125%, 1/10/27(b) |

402 | 401,373 | ||||||||||

| Credit Suisse Group Funding Guernsey Ltd. |

1,440 | 1,443,600 | ||||||||||

| 4.55%, 4/17/26 |

1,095 | 1,119,802 | ||||||||||

| Fifth Third Bancorp |

41 | 41,155 | ||||||||||

| Goldman Sachs Group, Inc. (The) |

1,483 | 1,431,125 | ||||||||||

| 3.75%, 5/22/25–2/25/26 |

731 | 722,217 | ||||||||||

| 3.85%, 7/08/24 |

2,115 | 2,124,602 | ||||||||||

| 5.75%, 1/24/22 |

510 | 551,570 | ||||||||||

| Series D |

1,203 | 1,274,506 | ||||||||||

| Series G |

130 | 135,218 | ||||||||||

| HSBC Bank USA, NA |

680 | 704,079 | ||||||||||

| HSBC Holdings PLC |

200 | 199,462 | ||||||||||

| 4.00%, 3/30/22 |

90 | 92,168 | ||||||||||

| 4.041%, 3/13/28 |

3,035 | 3,025,015 | ||||||||||

| 5.10%, 4/05/21 |

255 | 268,336 | ||||||||||

| HSBC USA, Inc. |

300 | 297,450 | ||||||||||

| JPMorgan Chase & Co. |

1,895 | 1,845,578 | ||||||||||

| 3.54%, 5/01/28 |

2,740 | 2,678,049 | ||||||||||

| 3.625%, 5/13/24 |

436 | 434,221 | ||||||||||

| 4.35%, 8/15/21 |

20 | 20,695 | ||||||||||

| 4.40%, 7/22/20 |

U.S.$ | 455 | $ | 468,777 | ||||||||

| 4.50%, 1/24/22 |

45 | 46,816 | ||||||||||

| 4.625%, 5/10/21 |

60 | 62,551 | ||||||||||

| KeyBank NA/Cleveland OH |

1,000 | 986,410 | ||||||||||

| Lloyds Banking Group PLC |

200 | 193,388 | ||||||||||

| 4.375%, 3/22/28 |

393 | 396,906 | ||||||||||

| 4.65%, 3/24/26 |

364 | 366,592 | ||||||||||

| Manufacturers & Traders Trust Co. |

1,000 | 985,600 | ||||||||||

| Mitsubishi UFJ Financial Group, Inc. |

286 | 286,420 | ||||||||||

| Morgan Stanley |

2,205 | 2,134,594 | ||||||||||

| 3.625%, 1/20/27 |

175 | 171,239 | ||||||||||

| 5.625%, 9/23/19 |

1,098 | 1,139,428 | ||||||||||

| 7.25%, 4/01/32 |

55 | 72,783 | ||||||||||

| Series F |

335 | 338,641 | ||||||||||

| Series G |

39 | 39,409 | ||||||||||

| 5.50%, 7/24/20–7/28/21 |

2,018 | 2,132,851 | ||||||||||

| 6.625%, 4/01/18 |

205 | 205,000 | ||||||||||

| Nationwide Building Society |

1,580 | 1,520,545 | ||||||||||

| PNC Bank NA |

250 | 247,868 | ||||||||||

| PNC Financial Services Group, Inc. (The) |

228 | 236,685 | ||||||||||

| Santander Holdings USA, Inc. |

1,525 | 1,510,177 | ||||||||||

| Santander Issuances SAU |

EUR | 400 | 536,151 | |||||||||

| Santander UK Group Holdings PLC |

U.S.$ | 1,448 | 1,420,169 | |||||||||

| State Street Corp. |

45 | 46,070 | ||||||||||

| UBS AG |

EUR | 135 | 182,727 | |||||||||

| UBS AG/Stamford CT |

U.S.$ | 1,584 | 1,778,753 | |||||||||

| UBS Group Funding Switzerland AG |

836 | 841,426 | ||||||||||

| US Bancorp |

723 | 738,357 | ||||||||||

| Wells Fargo & Co. |

1,445 | 1,421,085 | ||||||||||

|

|

|

|||||||||||

| 65,387,500 | ||||||||||||

|

|

|

|||||||||||

| Finance–0.3% | ||||||||||||

| GE Capital International Funding Co. Unlimited Co. |

200 | 195,496 | ||||||||||

| Synchrony Financial |

1,735 | 1,640,651 | ||||||||||

|

|

|

|||||||||||

| 1,836,147 | ||||||||||||

|

|

|

|||||||||||

| 10 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Insurance–0.9% | ||||||||||||

| American International Group, Inc. |

U.S.$ | 792 | $ | 802,573 | ||||||||

| Anthem, Inc. |

33 | 32,633 | ||||||||||

| Coventry Health Care, Inc. |

165 | 174,887 | ||||||||||

| Guardian Life Insurance Co. of America (The) |

1,268 | 1,291,712 | ||||||||||

| Hartford Financial Services Group, Inc. (The) |

86 | 90,120 | ||||||||||

| Massachusetts Mutual Life Insurance Co. |

7 | 11,014 | ||||||||||

| MetLife Capital Trust IV |

970 | 1,228,136 | ||||||||||

| MetLife, Inc. |

75 | 74,175 | ||||||||||

| 4.75%, 2/08/21 |

350 | 364,798 | ||||||||||

| 10.75%, 8/01/39 |

25 | 39,475 | ||||||||||

| Nationwide Mutual Insurance Co. |

377 | 607,743 | ||||||||||

| New York Life Global Funding |

703 | 691,415 | ||||||||||

| Prudential Financial, Inc. |

86 | 89,126 | ||||||||||

| Reliance Standard Life Global Funding II |

80 | 79,761 | ||||||||||

| Swiss Re America Holding Corp. |

35 | 41,666 | ||||||||||

| XLIT Ltd. |

EUR | 415 | 513,813 | |||||||||

| 6.25%, 5/15/27 |

U.S.$ | 195 | 224,381 | |||||||||

|

|

|

|||||||||||

| 6,357,428 | ||||||||||||

|

|

|

|||||||||||

| REITS–0.7% | ||||||||||||

| American Tower Corp. |

30 | 31,280 | ||||||||||

| HCP, Inc. |

2 | 2,100 | ||||||||||

| Healthcare Trust of America Holdings LP |

205 | 200,660 | ||||||||||

| Host Hotels & Resorts LP |

48 | 47,407 | ||||||||||

| Trust F/1401 |

970 | 980,912 | ||||||||||

| Welltower, Inc. |

3,410 | 3,407,204 | ||||||||||

|

|

|

|||||||||||

| 4,669,563 | ||||||||||||

|

|

|

|||||||||||

| 78,250,638 | ||||||||||||

|

|

|

|||||||||||

| Industrial–9.3% | ||||||||||||

| Basic–0.9% | ||||||||||||

| Anglo American Capital PLC |

U.S.$ | 200 | $ | 199,734 | ||||||||

| Barrick North America Finance LLC |

15 | 15,576 | ||||||||||

| Dow Chemical Co. (The) |

15 | 14,738 | ||||||||||

| 4.125%, 11/15/21 |

30 | 30,870 | ||||||||||

| 4.375%, 11/15/42 |

87 | 86,883 | ||||||||||

| 7.375%, 11/01/29 |

220 | 286,961 | ||||||||||

| Eastman Chemical Co. |

496 | 501,421 | ||||||||||

| Glencore Funding LLC |

502 | 504,470 | ||||||||||

| LYB International Finance BV |

330 | 334,940 | ||||||||||

| LyondellBasell Industries NV |

996 | 1,093,777 | ||||||||||

| Minsur SA |

397 | 426,279 | ||||||||||

| Mosaic Co. (The) |

405 | 425,481 | ||||||||||

| Sociedad Quimica y Minera de Chile SA |

1,043 | 1,039,089 | ||||||||||

| Vale Overseas Ltd. |

900 | 1,058,580 | ||||||||||

| Yamana Gold, Inc. |

395 | 407,435 | ||||||||||

|

|

|

|||||||||||

| 6,426,234 | ||||||||||||

|

|

|

|||||||||||

| Capital Goods–0.2% | ||||||||||||

| Embraer Netherlands Finance BV |

1,025 | 1,083,015 | ||||||||||

| General Electric Co. |

372 | 368,261 | ||||||||||

|

|

|

|||||||||||

| 1,451,276 | ||||||||||||

|

|

|

|||||||||||

| Communications—Media–0.8% | ||||||||||||

| Charter Communications Operating LLC/Charter Communications Operating Capital |

470 | 479,367 | ||||||||||

| Comcast Corp. |

17 | 16,957 | ||||||||||

| 5.15%, 3/01/20 |

83 | 86,463 | ||||||||||

| Cox Communications, Inc. |

463 | 446,693 | ||||||||||

| Time Warner Cable LLC |

30 | 30,179 | ||||||||||

| 4.125%, 2/15/21 |

1,990 | 2,012,507 | ||||||||||

| 4.50%, 9/15/42 |

505 | 442,734 | ||||||||||

| 5.00%, 2/01/20 |

90 | 92,423 | ||||||||||

| Time Warner, Inc. |

80 | 79,841 | ||||||||||

| 2018 Semi-Annual Report | 11 |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| 3.60%, 7/15/25 |

U.S.$ | 1,285 | $ | 1,249,919 | ||||||||

| 4.875%, 3/15/20 |

714 | 738,126 | ||||||||||

|

|

|

|||||||||||

| 5,675,209 | ||||||||||||

|

|

|

|||||||||||

| Communications—Telecommunications–1.2% | ||||||||||||

| AT&T Corp. |

53 | 70,866 | ||||||||||

| AT&T, Inc. |

2,860 | 2,757,326 | ||||||||||

| 3.60%, 2/17/23 |

105 | 105,503 | ||||||||||

| 3.90%, 8/14/27 |

140 | 140,811 | ||||||||||

| 4.125%, 2/17/26 |

2,087 | 2,099,960 | ||||||||||

| 5.15%, 2/14/50 |

700 | 706,300 | ||||||||||

| 7.00%, 10/01/25(b) |

135 | 159,801 | ||||||||||

| British Telecommunications PLC |

69 | 100,536 | ||||||||||

| Crown Castle Towers LLC |

543 | 562,206 | ||||||||||

| New Cingular Wireless Services, Inc. |

20 | 27,792 | ||||||||||

| Rogers Communications, Inc. |

CAD | 256 | 207,268 | |||||||||

| Sprint Spectrum Co. LLC/Sprint Spectrum Co. II LLC/Sprint Spectrum Co. III LLC |

U.S.$ | 1,380 | 1,385,547 | |||||||||

| Verizon Communications, Inc. |

90 | 99,496 | ||||||||||

| Vodafone Group PLC |

15 | 15,521 | ||||||||||

|

|

|

|||||||||||

| 8,438,933 | ||||||||||||

|

|

|

|||||||||||

| Consumer Cyclical—Automotive–1.2% | ||||||||||||

| Ford Motor Credit Co. LLC |

748 | 741,956 | ||||||||||

| 3.664%, 9/08/24 |

1,727 | 1,665,484 | ||||||||||

| 5.00%, 5/15/18 |

1,984 | 1,989,317 | ||||||||||

| 5.875%, 8/02/21 |

1,145 | 1,221,452 | ||||||||||

| General Motors Co. |

665 | 667,973 | ||||||||||

| General Motors Financial Co., Inc. |

1,411 | 1,412,679 | ||||||||||

| 3.25%, 5/15/18 |

91 | 91,067 | ||||||||||

| 4.00%, 1/15/25 |

374 | 369,639 | ||||||||||

| 4.30%, 7/13/25 |

275 | 275,239 | ||||||||||

|

|

|

|||||||||||

| 8,434,806 | ||||||||||||

|

|

|

|||||||||||

| Consumer Non-Cyclical–1.5% | ||||||||||||

| Ahold Finance USA LLC |

120 | 145,063 | ||||||||||

| Baxalta, Inc. |

15 | 14,964 | ||||||||||

| Becton Dickinson and Co. |

355 | 348,897 | ||||||||||

| Biogen, Inc. |

11 | 11,113 | ||||||||||

| 4.05%, 9/15/25 |

1,471 | 1,505,186 | ||||||||||

| Bunge Ltd. Finance Corp. |

U.S.$ | 93 | $ | 98,800 | ||||||||

| CVS Health Corp. |

830 | 836,856 | ||||||||||

| 4.30%, 3/25/28 |

830 | 834,499 | ||||||||||

| Kimberly-Clark Corp. |

35 | 35,948 | ||||||||||

| Medtronic, Inc. |

1,841 | 1,842,473 | ||||||||||

| Mylan NV |

EUR | 1,074 | 1,371,046 | |||||||||

| Reynolds American, Inc. |

U.S.$ | 300 | 322,023 | |||||||||

| Sigma Alimentos SA de CV |

221 | 212,989 | ||||||||||

| Tyson Foods, Inc. |

353 | 351,228 | ||||||||||

| 3.95%, 8/15/24 |

1,211 | 1,220,325 | ||||||||||

| 4.50%, 6/15/22 |

179 | 185,628 | ||||||||||

| Zimmer Biomet Holdings, Inc. |

694 | 686,755 | ||||||||||

| Zoetis, Inc. |

479 | 482,703 | ||||||||||

|

|

|

|||||||||||

| 10,506,496 | ||||||||||||

|

|

|

|||||||||||

| Energy–1.7% | ||||||||||||

| Anadarko Finance Co. |

20 | 25,522 | ||||||||||

| Apache Corp. |

20 | 20,217 | ||||||||||

| Cenovus Energy, Inc. |

77 | 74,187 | ||||||||||

| 5.70%, 10/15/19 |

332 | 343,388 | ||||||||||

| ConocoPhillips Holding Co. |

85 | 108,502 | ||||||||||

| Ecopetrol SA |

558 | 550,858 | ||||||||||

| Encana Corp. |

830 | 840,914 | ||||||||||

| Energy Transfer LP |

809 | 816,402 | ||||||||||

| Energy Transfer Partners LP |

100 | 97,844 | ||||||||||

| 4.65%, 6/01/21 |

324 | 333,182 | ||||||||||

| Energy Transfer Partners LP/Regency Energy Finance Corp. |

251 | 253,902 | ||||||||||

| Enterprise Products Operating LLC |

95 | 94,763 | ||||||||||

| 5.20%, 9/01/20 |

691 | 723,062 | ||||||||||

| Hess Corp. |

1,180 | 1,154,760 | ||||||||||

| Kinder Morgan Energy Partners LP |

218 | 217,457 | ||||||||||

| 4.15%, 3/01/22 |

260 | 264,248 | ||||||||||

| 6.85%, 2/15/20 |

18 | 19,127 | ||||||||||

| 12 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Kinder Morgan, Inc./DE |

U.S.$ | 645 | $ | 670,355 | ||||||||

| Marathon Petroleum Corp. |

48 | 50,663 | ||||||||||

| Noble Energy, Inc. |

927 | 933,387 | ||||||||||

| 4.15%, 12/15/21 |

557 | 569,811 | ||||||||||

| Occidental Petroleum Corp. |

20 | 20,016 | ||||||||||

| Phillips 66 |

131 | 136,093 | ||||||||||

| Plains All American Pipeline LP/PAA Finance Corp. |

1,411 | 1,342,115 | ||||||||||

| Sabine Pass Liquefaction LLC |

811 | 842,159 | ||||||||||

| Spectra Energy Partners LP |

20 | 19,284 | ||||||||||

| 4.60%, 6/15/21 |

145 | 149,656 | ||||||||||

| TransCanada PipeLines Ltd. |

10 | 10,187 | ||||||||||

| Valero Energy Corp. |

6 | 6,361 | ||||||||||

| Williams Partners LP |

30 | 29,600 | ||||||||||

| 4.125%, 11/15/20 |

784 | 796,795 | ||||||||||

|

|

|

|||||||||||

| 11,514,817 | ||||||||||||

|

|

|

|||||||||||

| Other Industrial–0.2% | ||||||||||||

| Alfa SAB de CV |

915 | 951,028 | ||||||||||

|

|

|

|||||||||||

| Services–0.4% | ||||||||||||

| Expedia Group, Inc. |

1,225 | 1,138,417 | ||||||||||

| S&P Global, Inc. |

1,170 | 1,228,161 | ||||||||||

| Total System Services, Inc. |

21 | 20,979 | ||||||||||

|

|

|

|||||||||||

| 2,387,557 | ||||||||||||

|

|

|

|||||||||||

| Technology–1.1% | ||||||||||||

| Agilent Technologies, Inc. |

47 | 48,964 | ||||||||||

| Broadcom Corp./Broadcom Cayman Finance Ltd. |

309 | 304,028 | ||||||||||

| 3.875%, 1/15/27 |

671 | 652,990 | ||||||||||

| Dell International LLC/EMC Corp. |

1,560 | 1,653,351 | ||||||||||

| 6.02%, 6/15/26(b) |

246 | 264,785 | ||||||||||

| DXC Technology Co. |

35 | 43,183 | ||||||||||

| Fidelity National Information Services, Inc. |

2 | 2,136 | ||||||||||

| Hewlett Packard Enterprise Co. |

1,206 | 1,189,695 | ||||||||||

| 3.60%, 10/15/20 |

20 | 20,186 | ||||||||||

| HP, Inc. |

U.S.$ | 11 | $ | 11,159 | ||||||||

| KLA-Tencor Corp. |

1,265 | 1,320,015 | ||||||||||

| Lam Research Corp. |

566 | 559,474 | ||||||||||

| Motorola Solutions, Inc. |

107 | 105,463 | ||||||||||

| 7.50%, 5/15/25 |

46 | 54,736 | ||||||||||

| Seagate HDD Cayman |

687 | 669,275 | ||||||||||

| VMware, Inc. |

539 | 518,302 | ||||||||||

| Xerox Corp. |

22 | 21,749 | ||||||||||

|

|

|

|||||||||||

| 7,439,491 | ||||||||||||

|

|

|

|||||||||||

| Transportation—Services–0.1% | ||||||||||||

| Adani Ports & Special Economic Zone Ltd. |

925 | 922,687 | ||||||||||

|

|

|

|||||||||||

| 64,148,534 | ||||||||||||

|

|

|

|||||||||||

| Utility–0.5% | ||||||||||||

| Electric–0.5% | ||||||||||||

| Berkshire Hathaway Energy Co. |

108 | 137,986 | ||||||||||

| Duke Energy Carolinas LLC |

42 | 43,160 | ||||||||||

| Exelon Corp. |

30 | 29,736 | ||||||||||

| Exelon Generation Co. LLC |

919 | 916,169 | ||||||||||

| Israel Electric Corp., Ltd. |

1,117 | 1,163,076 | ||||||||||

| Pacific Gas & Electric Co. |

55 | 54,035 | ||||||||||

| 6.05%, 3/01/34 |

104 | 123,833 | ||||||||||

| Sempra Energy |

105 | 107,765 | ||||||||||

| TECO Finance, Inc. |

730 | 756,002 | ||||||||||

| Union Electric Co. |

30 | 30,963 | ||||||||||

| Wisconsin Electric Power Co. |

23 | 23,545 | ||||||||||

|

|

|

|||||||||||

| 3,386,270 | ||||||||||||

|

|

|

|||||||||||

| Natural Gas–0.0% | ||||||||||||

| NiSource, Inc. |

16 | 16,462 | ||||||||||

|

|

|

|||||||||||

| 3,402,732 | ||||||||||||

|

|

|

|||||||||||

| Total Corporates—Investment Grade (cost $145,550,772) |

145,801,904 | |||||||||||

|

|

|

|||||||||||

| 2018 Semi-Annual Report | 13 |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| GOVERNMENTS—TREASURIES–17.2% | ||||||||||||

| Singapore–0.5% | ||||||||||||

| Singapore Government Bond |

SGD | 4,995 | $ | 3,790,911 | ||||||||

|

|

|

|||||||||||

| United States–16.7% | ||||||||||||

| U.S. Treasury Bonds |

U.S.$ | 187 | 160,997 | |||||||||

| 2.50%, 2/15/46–5/15/46 |

1,446 | 1,315,739 | ||||||||||

| 2.75%, 8/15/42–11/15/47 |

2,344 | 2,242,677 | ||||||||||

| 2.875%, 5/15/43–11/15/46 |

603 | 592,734 | ||||||||||

| 3.00%, 11/15/44–5/15/47 |

3,422 | 3,440,078 | ||||||||||

| 3.125%, 2/15/43-8/15/44 |

330 | 340,067 | ||||||||||

| 3.375%, 5/15/44 |

246 | 264,174 | ||||||||||

| 3.625%, 8/15/43–2/15/44 |

893 | 1,000,085 | ||||||||||

| 3.75%, 11/15/43 |

295 | 336,991 | ||||||||||

| 4.375%, 2/15/38 |

1,577 | 1,939,834 | ||||||||||

| 4.50%, 2/15/36 |

2,349 | 2,902,236 | ||||||||||

| 4.75%, 2/15/37 |

1,525 | 1,952,000 | ||||||||||

| 6.125%, 11/15/27 |

2,066 | 2,656,101 | ||||||||||

| 6.25%, 5/15/30 |

386 | 523,151 | ||||||||||

| 7.125%, 2/15/23 |

4,028 | 4,867,586 | ||||||||||

| 7.50%, 11/15/24 |

52 | 67,291 | ||||||||||

| U.S. Treasury Notes |

938 | 896,114 | ||||||||||

| 1.25%, 12/31/18 |

11,689 | 11,617,770 | ||||||||||

| 1.375%, 2/29/20–5/31/21 |

25,630 | 25,034,062 | ||||||||||

| 1.50%, 1/31/19–5/31/20 |

642 | 634,768 | ||||||||||

| 1.50%, 11/30/19(e) |

2,695 | 2,662,155 | ||||||||||

| 1.625%, 6/30/19–5/15/26 |

4,070 | 3,811,228 | ||||||||||

| 1.75%, 10/31/20–5/31/22 |

9,528 | 9,244,605 | ||||||||||

| 1.875%, 4/30/22–7/31/22 |

8,463 | 8,240,797 | ||||||||||

| 2.00%, 12/31/21–8/15/25 |

14,113 | 13,670,388 | ||||||||||

| 2.125%, 8/31/20–5/15/25 |

3,260 | 3,198,904 | ||||||||||

| 2.25%, 11/15/25–8/15/27 |

1,738 | 1,666,478 | ||||||||||

| 2.375%, 8/15/24–5/15/27 |

6,615 | 6,493,871 | ||||||||||

| 2.50%, 8/15/23 |

297 | 295,608 | ||||||||||

| 2.75%, 11/15/23–2/15/24 |

2,060 | 2,072,597 | ||||||||||

| 3.75%, 11/15/18 |

328 | 330,978 | ||||||||||

|

|

|

|||||||||||

| 114,472,064 | ||||||||||||

|

|

|

|||||||||||

| Total Governments—Treasuries (cost $120,400,577) |

118,262,975 | |||||||||||

|

|

|

|||||||||||

| ASSET-BACKED SECURITIES–9.5% | ||||||||||||

| Autos—Fixed Rate–5.3% | ||||||||||||

| Ally Auto Receivables Trust |

318 | 317,589 | ||||||||||

| Ally Master Owner Trust |

182 | 181,818 | ||||||||||

| Americredit Automobile Receivables Trust |

325 | 324,663 | ||||||||||

| AmeriCredit Automobile Receivables Trust |

U.S.$ | 740 | $ | 736,946 | ||||||||

| Avis Budget Rental Car Funding AESOP LLC |

2,535 | 2,538,045 | ||||||||||

| Series 2016-1A, Class A |

742 | 739,407 | ||||||||||

| Bank of The West Auto Trust |

144 | 144,143 | ||||||||||

| California Republic Auto Receivables Trust |

176 | 176,079 | ||||||||||

| CarMax Auto Owner Trust |

85 | 84,965 | ||||||||||

| Chrysler Capital Auto Receivables Trust |

172 | 171,572 | ||||||||||

| CPS Auto Receivables Trust |

142 | 141,427 | ||||||||||

| Series 2017-D, Class A |

1,591 | 1,583,712 | ||||||||||

| CPS Auto Trust |

318 | 317,254 | ||||||||||

| Drive Auto Receivables Trust |

160 | 159,558 | ||||||||||

| Series 2017-3, Class B |

1,730 | 1,721,669 | ||||||||||

| DT Auto Owner Trust |

365 | 363,877 | ||||||||||

| Series 2018-1A, Class A |

1,770 | 1,768,963 | ||||||||||

| Exeter Automobile Receivables Trust |

520 | 552,027 | ||||||||||

| Series 2016-3A, Class A |

169 | 167,897 | ||||||||||

| Series 2017-2A, Class A |

488 | 486,324 | ||||||||||

| Series 2017-3A, Class A |

1,465 | 1,457,268 | ||||||||||

| Fifth Third Auto Trust |

1,028 | 1,025,526 | ||||||||||

| First Investors Auto Owner Trust |

279 | 278,207 | ||||||||||

| Flagship Credit Auto Trust |

620 | 669,677 | ||||||||||

| 14 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Series 2016-4, Class A2 |

U.S.$ | 635 | $ | 632,628 | ||||||||

| Series 2016-4, Class D |

570 | 572,326 | ||||||||||

| Series 2017-3, Class A |

770 | 764,878 | ||||||||||

| Series 2017-4, Class A |

705 | 699,495 | ||||||||||

| Ford Credit Auto Owner Trust |

2,407 | 2,393,527 | ||||||||||

| Series 2016-1, Class A |

1,232 | 1,211,682 | ||||||||||

| Ford Credit Floorplan Master Owner Trust |

1,755 | 1,733,119 | ||||||||||

| Series 2016-1, Class A1 |

55 | 54,557 | ||||||||||

| Series 2017-1, Class A1 |

1,275 | 1,255,831 | ||||||||||

| GM Financial Automobile Leasing Trust |

627 | 626,902 | ||||||||||

| GMF Floorplan Owner Revolving Trust |

1,078 | 1,076,717 | ||||||||||

| Harley-Davidson Motorcycle Trust |

304 | 303,146 | ||||||||||

| Series 2015-2, Class A3 |

32 | 31,495 | ||||||||||

| Hertz Vehicle Financing II LP |

669 | 668,654 | ||||||||||

| Series 2015-2A, Class A |

924 | 920,468 | ||||||||||

| Series 2015-2A, Class C |

600 | 598,698 | ||||||||||

| Series 2018-1A, Class A |

710 | 702,387 | ||||||||||

| Hertz Vehicle Financing LLC |

3,204 | 3,197,954 | ||||||||||

| Santander Drive Auto Receivables Trust |

678 | 676,695 | ||||||||||

| Westlake Automobile Receivables Trust |

44 | 44,186 | ||||||||||

| Series 2018-1A, Class A1 |

541 | 541,357 | ||||||||||

| Wheels SPV 2 LLC |

1,325 | 1,308,902 | ||||||||||

|

|

|

|||||||||||

| 36,124,217 | ||||||||||||

|

|

|

|||||||||||

| Other ABS—Fixed Rate–2.1% | ||||||||||||

| CLUB Credit Trust |

U.S.$ | 1,413 | $ | 1,409,590 | ||||||||

| CNH Equipment Trust |

648 | 647,036 | ||||||||||

| Series 2015-A, Class A4 |

1,217 | 1,210,968 | ||||||||||

| Marlette Funding Trust |

71 | 71,259 | ||||||||||

| Series 2017-1A, Class A |

321 | 320,768 | ||||||||||

| Series 2017-2A, Class A |

602 | 600,689 | ||||||||||

| Series 2017-3A, Class A |

482 | 480,305 | ||||||||||

| Series 2017-3A, Class B |

415 | 411,339 | ||||||||||

| Series 2018-1A, Class A |

1,404 | 1,402,362 | ||||||||||

| Prosper Marketplace Issuance Trust |

360 | 358,930 | ||||||||||

| SBA Tower Trust |

1,340 | 1,317,448 | ||||||||||

| SoFi Consumer Loan Program LLC |

349 | 349,195 | ||||||||||

| Series 2016-3, Class A |

446 | 445,048 | ||||||||||

| Series 2017-2, Class A |

591 | 592,169 | ||||||||||

| Series 2017-5, Class A2 |

1,475 | 1,452,730 | ||||||||||

| Series 2017-6, Class A2 |

1,380 | 1,364,752 | ||||||||||

| SoFi Consumer Loan Program Trust |

1,686 | 1,680,093 | ||||||||||

| Volvo Financial Equipment LLC |

12 | 12,375 | ||||||||||

|

|

|

|||||||||||

| 14,127,056 | ||||||||||||

|

|

|

|||||||||||

| Credit Cards—Fixed Rate–1.6% | ||||||||||||

| Barclays Dryrock Issuance Trust |

100 | 98,908 | ||||||||||

| Series 2015-2, Class A |

100 | 99,919 | ||||||||||

| Series 2015-4, Class A |

1,130 | 1,125,583 | ||||||||||

| Capital One Multi-Asset Execution Trust |

1,063 | 1,060,524 | ||||||||||

| 2018 Semi-Annual Report | 15 |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Chase Issuance Trust |

U.S.$ | 200 | $ | 193,990 | ||||||||

| GE Capital Credit Card Master Note Trust |

2,042 | 2,036,766 | ||||||||||

| Synchrony Credit Card Master Note Trust |

1,802 | 1,795,852 | ||||||||||

| Series 2016-1, Class A |

100 | 99,538 | ||||||||||

| World Financial Network Credit Card Master Trust |

1,398 | 1,392,228 | ||||||||||

| Series 2017-B, Class A |

1,300 | 1,286,626 | ||||||||||

| Series 2018-A, Class A |

2,100 |

|

2,098,275

|

| ||||||||

|

|

|

|||||||||||

| 11,288,209 | ||||||||||||

|

|

|

|||||||||||

| Autos—Floating Rate–0.3% | ||||||||||||

| BMW Floorplan Master Owner Trust |

1,949 | 1,951,102 | ||||||||||

|

|

|

|||||||||||

| Credit Cards—Floating Rate–0.2% | ||||||||||||

| World Financial Network Credit Card Master Trust |

1,375 | 1,375,198 | ||||||||||

|

|

|

|||||||||||

| Home Equity Loans—Floating Rate–0.0% | ||||||||||||

| Asset Backed Funding Certificates Trust |

158 | 158,702 | ||||||||||

| Wells Fargo Home Equity Trust Mortgage Pass-Through Certificates |

81 | 78,965 | ||||||||||

|

|

|

|||||||||||

| 237,667 | ||||||||||||

|

|

|

|||||||||||

| Home Equity Loans—Fixed Rate–0.0% | ||||||||||||

| Credit-Based Asset Servicing & Securitization LLC |

108 | 109,375 | ||||||||||

|

|

|

|||||||||||

| Total Asset-Backed Securities (cost $65,410,007) |

65,212,824 | |||||||||||

|

|

|

|||||||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES–8.6% | ||||||||||||

| Non-Agency Fixed Rate CMBS–7.0% | ||||||||||||

| BHMS Commercial Mortgage Trust |

U.S.$ | 1,705 | $ | 1,683,091 | ||||||||

| CCUBS Commercial Mortgage Trust |

2,005 | 1,988,949 | ||||||||||

| CFCRE Commercial Mortgage Trust |

2,808 | 2,742,088 | ||||||||||

| CGRBS Commercial Mortgage Trust |

2,495 | 2,500,892 | ||||||||||

| Citigroup Commercial Mortgage Trust |

1,468 | 1,443,381 | ||||||||||

| Series 2015-GC35, Class A4 |

630 | 642,877 | ||||||||||

| Series 2016-C1, Class A4 |

2,409 | 2,360,940 | ||||||||||

| Series 2016-GC36, Class A5 |

705 | 709,071 | ||||||||||

| Series 2018-B2, Class A4 |

1,200 | 1,242,456 | ||||||||||

| Commercial Mortgage Trust |

889 | 749,686 | ||||||||||

| Series 2013-CR6, Class A2 |

37 | 36,630 | ||||||||||

| Series 2013-SFS, Class A1 |

695 | 671,682 | ||||||||||

| Series 2014-UBS5, Class A4 |

1,925 | 1,978,110 | ||||||||||

| Series 2015-CR24, Class A5 |

730 | 741,251 | ||||||||||

| Series 2015-CR25, Class A4 |

200 | 203,254 | ||||||||||

| Series 2015-LC21, Class XA |

2,919 | 111,787 | ||||||||||

| Series 2015-PC1, Class A5 |

226 | 232,177 | ||||||||||

| CSAIL Commercial Mortgage Trust |

675 | 674,058 | ||||||||||

| Series 2015-C3, Class A4 |

1,165 | 1,177,904 | ||||||||||

| Series 2015-C4, Class A4 |

1,641 | 1,683,128 | ||||||||||

| GS Mortgage Securities Corp. II |

2,361 | 2,352,991 | ||||||||||

| GS Mortgage Securities Trust |

1,499 | 1,457,017 | ||||||||||

| Series 2013-GC16, Class A2 |

103 | 103,484 | ||||||||||

| 16 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

| JP Morgan Chase Commercial Mortgage Securities Trust |

U.S.$ | 330 | $ | 331,957 | ||||||||

| Series 2011-C5, Class D |

224 | 219,917 | ||||||||||

| Series 2012-C6, Class E |

712 | 628,946 | ||||||||||

| JPMBB Commercial Mortgage Securities Trust |

472 | 424,608 | ||||||||||

| Series 2014-C22, Class XA |

6,485 | 285,416 | ||||||||||

| Series 2015-C30, Class A5 |

725 | 741,609 | ||||||||||

| Series 2015-C31, Class A3 |

1,903 | 1,939,369 | ||||||||||

| Series 2015-C32, Class C |

1,000 | 993,830 | ||||||||||

| LB-UBS Commercial Mortgage Trust |

421 | 333,383 | ||||||||||

| LSTAR Commercial Mortgage Trust |

86 | 85,395 | ||||||||||

| Series 2015-3, Class A2 |

961 | 952,277 | ||||||||||

| Series 2016-4, Class A2 |

1,099 | 1,065,745 | ||||||||||

| Morgan Stanley Bank of America Merrill Lynch Trust |

2,266 | 140,057 | ||||||||||

| Morgan Stanley Capital I Trust |

619 | 613,687 | ||||||||||

| Series 2016-UB12, Class A4 |

1,105 | 1,110,367 | ||||||||||

| UBS Commercial Mortgage Trust |

1,320 | 1,359,844 | ||||||||||

| UBS Commercial Mortgage Trust |

2,100 | 2,173,509 | ||||||||||

| UBS-Barclays Commercial Mortgage Trust |

2,348 | 2,317,013 | ||||||||||

| Wells Fargo Commercial Mortgage Trust |

|

|||||||||||

| Series 2014-LC16, Class XA |

3,917 | 195,836 | ||||||||||

| Series 2015-SG1, Class C |

975 | 947,401 | ||||||||||

| Series 2016-NXS6, Class C |

1,030 | 1,022,371 | ||||||||||

| WF-RBS Commercial Mortgage Trust |

|

|||||||||||

| Series 2013-C14, Class A5 |

U.S.$ | 1,419 | $ | 1,423,264 | ||||||||

| Series 2013-C15, Class A4 |

115 | 119,643 | ||||||||||

| Series 2014-C20, Class A2 |

1,201 | 1,203,312 | ||||||||||

|

|

|

|||||||||||

| 48,115,660 | ||||||||||||

|

|

|

|||||||||||

| Non-Agency Floating Rate CMBS–1.6% | ||||||||||||

| BAMLL Commercial Mortgage Securities Trust |

2,435 | 2,440,495 | ||||||||||

| BX Trust |

1,625 | 1,626,013 | ||||||||||

| Credit Suisse Mortgage Trust |

393 | 395,913 | ||||||||||

| Great Wolf Trust |

1,261 | 1,262,729 | ||||||||||

| H/2 Asset Funding NRE |

465 | 464,935 | ||||||||||

| JP Morgan Chase Commercial Mortgage Securities Trust |

1,379 | 1,375,183 | ||||||||||

| Morgan Stanley Capital I Trust |

|

|||||||||||

| Series 2015-XLF2, Class AFSA |

458 | 457,528 | ||||||||||

| Series 2015-XLF2, Class SNMA |

418 | 416,017 | ||||||||||

| RETL |

686 | 689,220 | ||||||||||

| Starwood Retail Property Trust |

1,935 | 1,934,544 | ||||||||||

|

|

|

|||||||||||

| 11,062,577 | ||||||||||||

|

|

|

|||||||||||

| Agency CMBS–0.0% | ||||||||||||

| Federal Home Loan Mortgage Corp. Multifamily |

|

|||||||||||

| Series K010, Class A1 |

10 | 9,771 | ||||||||||

| 2018 Semi-Annual Report | 17 |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Series K011, Class A1 |

U.S.$ | 22 | $ | 21,956 | ||||||||

| Series K021, Class A1 |

57 | 55,925 | ||||||||||

| Series K025, Class A1 |

89 | 87,122 | ||||||||||

| Federal Home Loan Mortgage Corp. Multifamily Structured Pass-Through Certificates |

78 | 78,912 | ||||||||||

|

|

|

|||||||||||

| 253,686 | ||||||||||||

|

|

|

|||||||||||

| Total Commercial Mortgage-Backed Securities |

|

59,431,923 | ||||||||||

|

|

|

|||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS–6.3% | ||||||||||||

| Risk Share Floating Rate–4.1% | ||||||||||||

| Bellemeade Re II Ltd. |

308 | 314,077 | ||||||||||

| Federal Home Loan Mortgage Corp. Structured Agency Credit Risk Debt Notes |

2,254 | 2,507,643 | ||||||||||

| Series 2014-DN3, Class M3 |

748 | 816,006 | ||||||||||

| Series 2014-DN4, Class M3 |

253 | 282,481 | ||||||||||

| Series 2014-HQ3, Class M3 |

933 | 1,038,944 | ||||||||||

| Series 2015-DNA1, Class M3 |

305 | 339,848 | ||||||||||

| Series 2015-DNA2, Class M2 |

863 | 879,169 | ||||||||||

| Series 2015-HQ1, Class M3 |

250 | 269,865 | ||||||||||

| Series 2015-HQ2, Class M2 |

227 | 232,645 | ||||||||||

| Series 2015-HQA1, Class M2 |

758 | 772,967 | ||||||||||

| Series 2016-DNA1, Class M2 |

250 | 256,427 | ||||||||||

| Series 2016-DNA2, Class M3 |

U.S.$ | 1,000 | $ | 1,147,993 | ||||||||

| Series 2016-DNA4, Class M2 |

250 | 252,798 | ||||||||||

| Series 2016-HQA2, Class M2 |

250 | 255,219 | ||||||||||

| Series 2018-HQA1, Class M2 |

106 | 105,757 | ||||||||||

| Federal National Mortgage Association |

|

|||||||||||

| Series 2014-C03, Class 1M2 |

585 | 625,909 | ||||||||||

| Series 2014-C04, Class 2M2 |

398 | 447,226 | ||||||||||

| Series 2015-C01, Class 1M2 |

531 | 583,037 | ||||||||||

| Series 2015-C01, Class 2M2 |

560 | 608,274 | ||||||||||

| Series 2015-C02, Class 1M2 |

866 | 950,474 | ||||||||||

| Series 2015-C02, Class 2M2 |

565 | 609,566 | ||||||||||

| Series 2015-C03, Class 1M2 |

998 | 1,135,006 | ||||||||||

| Series 2015-C03, Class 2M2 |

1,041 | 1,163,659 | ||||||||||

| Series 2015-C04, Class 1M2 |

331 | 383,575 | ||||||||||

| Series 2015-C04, Class 2M2 |

1,007 | 1,134,098 | ||||||||||

| Series 2016-C01, Class 1M2 |

1,131 | 1,363,297 | ||||||||||

| Series 2016-C01, Class 2M2 |

849 | 1,018,954 | ||||||||||

| Series 2016-C02, Class 1M2 |

925 | 1,107,272 | ||||||||||

| Series 2016-C03, Class 2M2 |

2,103 | 2,466,816 | ||||||||||

| 18 | Sanford C. Bernstein Fund II, Inc. |

Table of Contents

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Series 2016-C05, Class 2M2 |

U.S.$ | 2,105 | $ | 2,348,685 | ||||||||

| Series 2018-C01, Class 1M2 |

1,310 | 1,326,883 | ||||||||||

| JP Morgan Madison Avenue Securities Trust |

209 | 227,311 | ||||||||||

| Wells Fargo Credit Risk Transfer Securities Trust |

730 | 821,243 | ||||||||||

| Series 2015-WF1, Class 2M2 |

206 | 241,472 | ||||||||||

|

|

|

|||||||||||

| 28,034,596 | ||||||||||||

|

|

|

|||||||||||

| Agency Floating Rate–1.3% | ||||||||||||

| Federal Home Loan Mortgage Corp. REMICs |

4,182 | 705,670 | ||||||||||

| Series 4693, Class SL |

3,733 | 707,865 | ||||||||||

| Series 4727, Class SA |

2,901 | 545,199 | ||||||||||

| Federal National Mortgage Association REMICs |

2,055 | 388,824 | ||||||||||

| Series 2012-70, Class SA |

3,644 | 717,076 | ||||||||||

| Series 2016-106, Class ES |

3,992 | 697,364 | ||||||||||

| Series 2017-16, Class SG |

3,905 | 712,185 | ||||||||||

| Series 2017-73, Class SA |

4,316 | 856,137 | ||||||||||

| Series 2017-97, Class LS |

2,727 | 523,056 | ||||||||||

| Series 2017-97, Class SW |

3,047 | 575,367 | ||||||||||

| Government National Mortgage Association |

U.S.$ | 3,394 | $ | 593,125 | ||||||||

| Series 2017-43, Class ST |

4,865 | 793,637 | ||||||||||

| Series 2017-65, Class ST |

4,271 | 762,091 | ||||||||||

|

|

|

|||||||||||

| 8,577,596 | ||||||||||||

|

|

|

|||||||||||

| Non-Agency Fixed Rate–0.7% | ||||||||||||

| Alternative Loan Trust |

147 | 141,795 | ||||||||||

| Series 2005-57CB, Class 4A3 |

322 | 287,347 | ||||||||||

| Series 2006-24CB, Class A16 |

665 | 576,619 | ||||||||||

| Series 2006-28CB, Class A14 |

465 | 389,308 | ||||||||||

| Series 2006-J1, Class 1A13 |

376 | 342,784 | ||||||||||

| Chase Mortgage Finance Trust |

207 | 185,435 | ||||||||||

| Citigroup Mortgage Loan Trust, Inc. |

319 | 321,782 | ||||||||||

| Countrywide Home Loan Mortgage Pass-Through Trust |

348 | 297,921 | ||||||||||

| Series 2006-13, Class 1A19 |

156 | 132,255 | ||||||||||

| Credit Suisse Mortgage Trust |

643 | 524,213 | ||||||||||

| First Horizon Alternative Mortgage Securities Trust |

551 | 462,885 | ||||||||||

| JP Morgan Alternative Loan Trust |

231 | 206,856 | ||||||||||

| JP Morgan Mortgage Trust |

282 | 246,433 | ||||||||||

| RBSSP Resecuritization Trust |

913 | 801,783 | ||||||||||

| Residential Funding Mortgage Securities I Trust |

8 | 7,733 | ||||||||||

| 2018 Semi-Annual Report | 19 |

Table of Contents

Schedule of Investments (continued)

| Principal Amount (000) | U.S. $ Value | |||||||||||

| Wells Fargo Mortgage Backed Securities Trust |

U.S.$ | 147 | $ | 146,743 | ||||||||

|

|

|

|||||||||||

| 5,071,892 | ||||||||||||

|

|

|

|||||||||||

| Non-Agency Floating Rate–0.2% | ||||||||||||

| Deutsche Alt-A Securities Mortgage Loan Trust |

1,411 | 870,934 | ||||||||||

| HomeBanc Mortgage Trust |

494 | 438,387 | ||||||||||

|

|

|

|||||||||||

| 1,309,321 | ||||||||||||

|

|

|

|||||||||||

| Agency Fixed Rate–0.0% | ||||||||||||

| Federal National Mortgage Association Grantor Trust |

323 | 301,331 | ||||||||||

|

|

|

|||||||||||

| Total Collateralized Mortgage Obligations (cost $41,310,152) |

43,294,736 | |||||||||||

|

|

|

|||||||||||

| INFLATION-LINKED SECURITIES–4.8% | ||||||||||||

| Japan–0.9% | ||||||||||||

| Japanese Government CPI Linked Bond |

JPY | 641,181 | 6,409,341 | |||||||||

|

|

|

|||||||||||

| United States–3.9% | ||||||||||||

| U.S. Treasury Inflation Index |

U.S.$ | 16,198 | 16,174,856 | |||||||||

| 0.375%, 7/15/25 (TIPS) |

10,450 | 10,316,321 | ||||||||||

|

|

|

|||||||||||

| 26,491,177 | ||||||||||||

|

|

|

|||||||||||

| Total Inflation-Linked Securities (cost $32,805,393) |

32,900,518 | |||||||||||

|

|

|

|||||||||||

| CORPORATES—NON-INVESTMENT GRADE–3.6% | ||||||||||||

| Industrial–2.0% | ||||||||||||

| Basic–0.2% | ||||||||||||

| ArcelorMittal |

100 | 105,296 | ||||||||||

| NOVA Chemicals Corp. |

645 | 648,696 | ||||||||||

| SPCM SA |

533 | 517,959 | ||||||||||

|

|

|

|||||||||||

| 1,271,951 | ||||||||||||

|

|

|

|||||||||||

| Communications—Media–0.3% | ||||||||||||

| Altice France SA/France |

EUR | 274 | 343,465 | |||||||||

| CCO Holdings LLC/CCO Holdings Capital Corp. |

|

U.S.$ |

|

906 | 869,090 | |||||||

| CSC Holdings LLC |

U.S.$ | 235 | $ | 245,121 | ||||||||

| Ziggo Secured Finance BV |

262 | 246,125 | ||||||||||

|

|

|

|||||||||||

| 1,703,801 | ||||||||||||

|

|

|

|||||||||||

| Communications—Telecommunications–0.3% | ||||||||||||

| CenturyLink, Inc. |

136 | 137,002 | ||||||||||

| Sprint Capital Corp. |