Form DEFA14A NATIONAL INSTRUMENTS

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________________

SCHEDULE 14A

(RULE 14a-101)

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

____________________________________

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

|

☐

|

|

Preliminary Proxy Statement

|

|

☐

|

|

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

|

|

☐

|

|

Definitive Proxy Statement

|

|

☒

|

|

Definitive Additional Materials

|

|

☐

|

|

Soliciting Material Pursuant to §240.14a-12

|

National Instruments Corporation

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

|

☒

|

|

No fee required.

|

||

|

☐

|

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11.

|

||

|

|

(1)

|

|

Title of each class of securities to which transaction applies:

|

|

|

|

(2)

|

|

Aggregate number of securities to which transaction applies:

|

|

|

|

(3)

|

|

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

|

|

|

|

(4)

|

|

Proposed maximum aggregate value of transaction:

|

|

|

|

(5)

|

|

Total fee paid:

|

|

|

☐

|

|

Fee paid previously with preliminary materials.

|

||

|

☐

|

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

|

||

|

|

(1)

|

|

Amount Previously Paid:

|

|

|

|

(2)

|

|

Form, Schedule or Registration Statement No.:

|

|

|

|

(3)

|

|

Filing Party:

|

|

|

|

(4)

|

|

Date Filed:

|

|

Revised Supplemental CEO Compensation Information April 30, 2018

National Instruments CEO Transition in 2017 National Instruments founder, Dr. James Truchard, retired from the CEO position in January 2017.Dr. Truchard was receiving $1 per year salary at his own request.He was replaced by Alex Davern, only the second CEO to lead the company since its founding in 1976.A change in CEO compensation up from $1 per year to reasonable compensation for the CEO position was necessary.The 2017 CEO compensation includes a one-time award of RSUs (“Initial Grant”) which will not repeat in 2018 or 2019. 2

National Instruments CEO Compensation One-time Initial Grant for new CEOwas 62% of total comp in 2017 One-time Initial Grant does not repeat *From NI proxy statements New CEO Equity Compensation 3

NI Executive Compensation Philosophy Total compensation opportunities should be competitiveTotal compensation should be related to NI’s performanceTotal compensation should be related to individual performanceEquity rewards help executives think like stockholdersNI’s overall amount of equity awards should be related to its revenue growthThe same compensation programs should generally apply to both executives and non-executive employees whenever possible 2017 New CEO Total CompensationHighly variable 4

$1.29BILLION REVENUEIN 2017 Continuous INVESTMENT IN R&D 35,000+ CUSTOMERS WORLDWIDE Long-Term Track Record of Growth Revenue in millions USD NI at a Glance Founded in 1976Global Operations in more than 50 countries Approximately 7,300 employeesBroad customer base, more than 35,000 companies served annually Diversity with no industry >15% of revenue 5

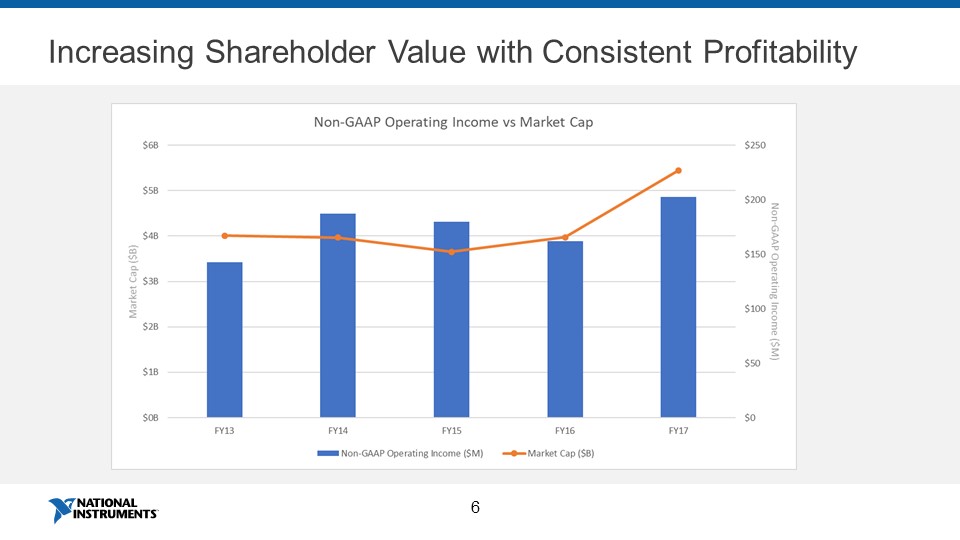

Increasing Shareholder Value with Consistent Profitability 6

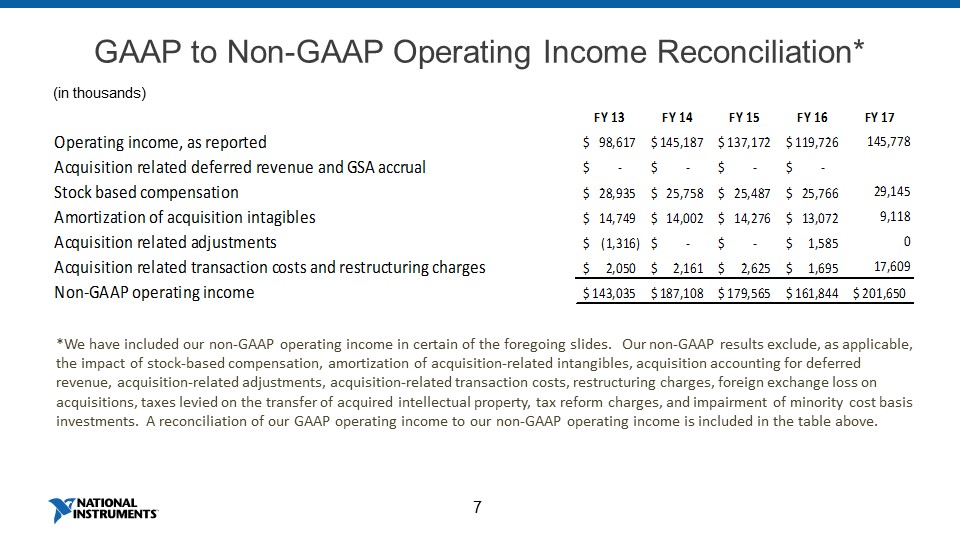

GAAP to Non-GAAP Operating Income Reconciliation* 7 *We have included our non-GAAP operating income in certain of the foregoing slides. Our non-GAAP results exclude, as applicable, the impact of stock-based compensation, amortization of acquisition-related intangibles, acquisition accounting for deferred revenue, acquisition-related adjustments, acquisition-related transaction costs, restructuring charges, foreign exchange loss on acquisitions, taxes levied on the transfer of acquired intellectual property, tax reform charges, and impairment of minority cost basis investments. A reconciliation of our GAAP operating income to our non-GAAP operating income is included in the table above. (in thousands)

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Verra Mobility appoints Cate Prescott as Chief People Officer

- Bloom Energy Appoints Daniel Berenbaum as Chief Financial Officer

- Sherritt Corrects Misleading Information Announced by SC2 Inc. an Affiliate of Seablinc Canada Inc., a Significant Supplier to Sherritt’s Moa Joint Venture

Create E-mail Alert Related Categories

SEC FilingsSign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!