Form DEFA14A Delek US Holdings, Inc.

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

☐ | Preliminary Proxy Statement | |||||||

☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |||||||

☐ | Definitive Proxy Statement | |||||||

☐ | Definitive Additional Materials | |||||||

| ☒ | Soliciting Material Pursuant to § 240.14a-12 | |||||||

DELEK US HOLDINGS, INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

☒ | No fee required. | ||||||||||||||||||||||

☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||||||||||||||||||||||

| (1) | Title of each class of securities to which transaction applies: ____________________________________ | ||||||||||||||||||||||

| (2) | Aggregate number of securities to which transaction applies: ____________________________________ | ||||||||||||||||||||||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): _______________________________ | ||||||||||||||||||||||

| (4) | Proposed maximum aggregate value of transaction: ___________________________________________ | ||||||||||||||||||||||

| (5) | Total fee paid: _________________________________________________________________________ | ||||||||||||||||||||||

☐ | Fee paid previously with preliminary materials. | ||||||||||||||||||||||

☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||||||||||||||||||||||

| (1) | Amount Previously Paid: _________________________________________________________________ | ||||||||||||||||||||||

| (2) | Form, Schedule or Registration Statement No.: _______________________________________________ | ||||||||||||||||||||||

| (3) | Filing Party: ___________________________________________________________________________ | ||||||||||||||||||||||

| (4) | Date Filed: ____________________________________________________________________________ | ||||||||||||||||||||||

Delek Responds to Public Statements by CVR Energy

BRENTWOOD, Tenn., March 3, 2021 – The Board of Directors of Delek US Holdings, Inc. (NYSE: DK) ("Delek") today issued an open letter to its shareholders in response to recent public statements made by CVR Energy, Inc. ("CVR"), a majority owned subsidiary of Icahn Enterprises L.P. and competitor of Delek. The full text of the letter follows:

Dear Fellow Shareholder:

Delek US Holdings, Inc.’s (“Delek”) Board of Directors and management team are committed to delivering value for shareholders. Over the last year, we have taken decisive action to further strengthen our operations and position the business to deliver significantly enhanced cash flow in 2021 and beyond.

As you may know, almost a year ago, at the beginning of the COVID lockdowns and in the midst of a dramatic decline in energy demand and global economic conditions, one of our competitors, CVR Energy, Inc. (“CVR”), a company controlled by Carl Icahn1, took an approximately 15% ownership position in our Company at severely depressed prices. CVR’s stated reason for acquiring the shares was its belief that Delek was undervalued and a potential consolidation target.

From the time of CVR’s initial filing in March 2020, neither CVR nor Icahn contacted us regarding their position or their views on the Company. Then, on January 14, 2021, CVR management published a letter indicating that, contrary to their prior public statements, CVR had no interest in acquiring Delek and, instead, outlined a series of strategic and operational initiatives that CVR wanted Delek to pursue. In the same letter, CVR disclosed their plans to replace three Delek directors with their nominees. CVR, our competitor, also announced they were pursuing an activist campaign focused on pushing Delek to undertake actions that would directly benefit CVR’s competitive positioning.

CVR management published another letter on March 1, 2021. The letter described CVR’s demands for non-public information and included spurious claims related to our CEO’s interest in Delek Logistics’ (“DKL”) general partner (“DKL GP”), a matter of public record for nearly eight years.

DELEK’S TRACK RECORD OF STRONG PERFORMANCE

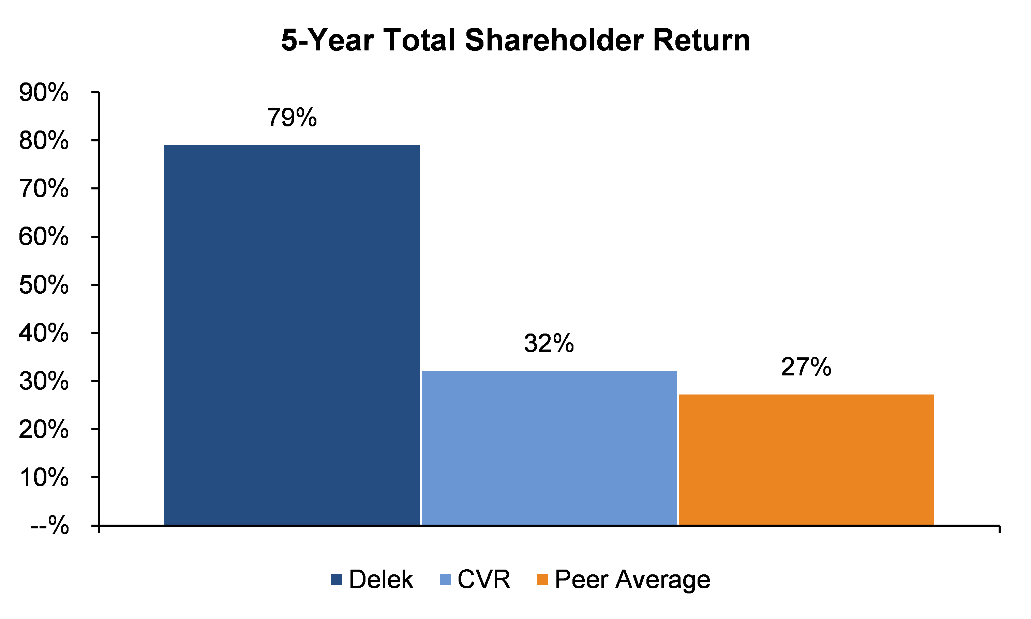

By executing our long-term strategy, Delek has built an integrated portfolio of assets located in strategically important geographies, which provide significant value for shareholders, customers and partners. We have strengthened our competitive position and laid the groundwork for continued future growth. This strategy has delivered value for our shareholders, as demonstrated by a five-year total shareholder return (TSR) of 79% compared to 27% for the average of our peers, including CVR2, over the same period. We find it odd that CVR is urging Delek to adopt a business strategy closer to its own, given CVR’s track record of substantial underperformance relative to Delek.

1 As of 12/31/20, Icahn Enterprises owned 70.8% of CVR’s common stock.

2 As of 3/2/21; peer set includes: CVR Energy, Inc., HollyFrontier Corporation, Marathon Petroleum Corporation, Par Pacific Holdings, Inc., PBF Energy Inc., Phillips 66 and Valero Energy Corporation. Based on peer groups used by Wall Street Research. Total Shareholder Return calculated based on price performance of stock over given time period and assumes all dividends are reinvested.

Recent highlights of our performance include:

•Since the completion of our merger with Alon USA Energy, Inc. (“Alon”) in 2017 (the "Alon Acquisition"3) , we have divested non-core assets with high operating expenses (Bakersfield, Paramount, Long Beach refineries, and western US asphalt terminals) and divested or did not renew leases for underperforming retail sites as part of a continuous evaluation process to optimize our portfolio. These efforts have resulted in cash inflows of $278 million, and reductions in on-going annual expenses of $77 million.

•Delek’s midstream investments yielded benefits in 2020 including the drop down of the Big Spring gathering system to DKL. Our indirect Wink to Webster Pipeline investment should begin generating cash flow by the end of 2021 and over the next ten years, we expect Wink to Webster to generate a return in excess of our midstream target IRR of 15%. We project midstream EBITDA4 to grow to $370 - $395 million by 2023. Our strategy and structure has driven DKL's success – it is one of the best performing refining logistics master limited partnerships ("MLPs"), generating a five-year total unitholder return of 117% relative to the 0% total unitholder return of its peers5, while continuously increasing distributions and maintaining competitive debt and coverage multiples.

Delek has also consistently returned significant capital to shareholders to drive returns. Since 2017, we returned more than $570 million through the repurchase of shares (~32% of current market capitalization) and paid more than

3 Refers to Delek’s acquisition of the outstanding shares of Alon, previously a separate SEC registrant under the ticker NYSE:ALJ, which was effective as of July 1, 2017, and which included net assets and operations associated with the Big Spring Refinery, the Krotz Springs Refinery and the Retail Operations (thereafter, Delek’s “Retail Segment”), as well as certain asphalt operations, non-operating refinery assets and controlling interest in a renewables facility.

4 See the definition of EBITDA in the 'Non-GAAP Disclosures' Section at the end of this communication.

5 As of 3/2/21; peer set includes: Enterprise Products Partners L.P., Holly Energy Partners, L.P., Magellan Midstream Partners, L.P., MPLX LP, Plains All American Pipeline, L.P., PBF Logistics LP and Phillips 66 Partners LP. Total Shareholder Return calculated based on price performance of stock over given time period and assumes all dividends are reinvested.

3

$280 million in dividends. In 2019 alone, prior to the COVID-19 pandemic, we returned to shareholders ~$265 million, or approximately 10% of Delek’s market capitalization at that time6, the highest amongst our peers.

Our Board and management team are focused on prudent balance sheet management, and execution was particularly critical in 2020, as the world grappled with COVID-19, commodity price volatility and demand shocks. We took decisive action to protect our balance sheet and financial flexibility, ensure employee safety, and stabilize our business, while maintaining customer satisfaction. These actions, which are expected to improve 2021 cost structure by over $225 million versus 2019, and capital spending by approximately $275 million versus 2019, included:

•Achieving a reduction in our 2020 operating expense structure relative to 2019 of more than $120 million, with a further $70 million decrease in controllable costs budgeted for 2021 (assuming reduced Krotz operations)

•Achieving a reduction in our 2020 G&A expense relative to 2019 of more than $25 million, with a further $10 million decrease budgeted for 2021

•Achieving a reduction in planned capital expenditures of $189 million, or 44% relative to 2019, with a further $85 million, or 35% reduction, expected in 2021, resulting in a new capital spending range of $150 to $160 million for this year

Through the implementation of innovative new technologies and systems, we expect to achieve further reductions going forward, as well as significant operational efficiencies.

DELEK’S BOARD OF DIRECTORS IS HIGHLY QUALIFIED, ENGAGED, AND DIVERSE

Delek’s Board of Directors is comprised of eight highly experienced, engaged, and diverse directors, seven of whom are independent and each of whom has a track record that demonstrates his or her ability to drive value for shareholders. Each director is actively engaged in overseeing the Company’s continued growth and success, and brings unique expertise and experience to support the Company’s long-term strategy.

The Board composition reflects a commitment to regular refreshment and increasing diversity, with three directors joining the Board since February 2019, and an average independent director tenure of 4.3 years, well below the S&P average of 7.9 years7. Two of the last three directors added were women, marking significant progress on Delek’s stated goal of having female and/or traditionally underrepresented individuals comprise thirty percent of the Board by 2022.

Delek’s Board thoroughly evaluated CVR’s director nominees and unanimously determined that adding these nominees is not in the best interest of shareholders. None of the nominees offer experience and skills that we believe are meaningfully different than our current Board. The addition of the CVR nominees to our Board would not advance our goals with respect to Board composition, including enhancing our diversity profile, a priority for us in our ongoing refreshment efforts. In fact, we believe their common backgrounds would reduce the overall diversity of perspective and experience that is currently reflected on our Board. It was also apparent from our interviews with each nominee that they each maintain personal relationships with CVR’s CEO, David Lamp, which raises serious concerns regarding their independence and commitment to acting in the interests of all Delek shareholders.

6 Based on full-year average 2019 market capitalization.

7 Source: 2020 Spencer Stuart Board Index.

4

| Board Composition Highlights | ||||||||||||||

| ~88% | 63% | 3 | ~4.3 yrs | 25% | ||||||||||

| Independent Directors | Petroleum and Refining Experience | Independent Directors Added Since February 2019 | Average Tenure of Independent Directors | Gender Diverse | ||||||||||

In addition to driving the execution of Delek’s long-term strategy, our Board has actively engaged in enhancing and expanding our Environmental, Social, and Governance (“ESG”) initiatives, and these efforts are bearing fruit. This strong commitment to transparency in our ESG practices, informed by the various frameworks, such as SASB (Sustainability Accounting Standards Board) and TCFD (Task Force on Climate-Related Financial Disclosures), has been recognized by our investors and major proxy advisors.

Our commitment to shareholder value, diversity and ESG principles is embedded in our mission, vision, and core values, and helps drive long-term value creation for shareholders.

OUR OBSERVATIONS REGARDING CVR’S BUSINESS PROPOSALS

The business proposals outlined in CVR’s letter are ideas that have been a part of our continuous internal evaluation process to identify value creation strategies. Our observations regarding CVR’s suggested actions are summarized below:

•Refineries: Our Krotz Springs and El Dorado refineries faced challenges in the low margin environment experienced in 2020. We believe the margin environment will progressively improve through 2021, as COVID-19 vaccine distribution impacts the reopening of the US and world economies, and demand for our products rebounds. On a mid-cycle basis, each facility generates free cash flow with optionality and opportunity to capitalize on market spikes. Through efficiency and cost reduction initiatives, we have lowered the operating cost structure at both of these facilities. We continuously review the strategic value of these refineries and believe that retaining these assets as operated refineries provides significant value and potential upside for Delek shareholders.

•Renewable Diesel: Like many of our peers, we are continuously reviewing opportunities to produce renewable diesel. We have an established position in the conventional biodiesel market, and operate three Company-owned facilities with more than 40 million gallons per year of biodiesel production. In addition, Delek was the operating partner in Alt-Air, one of the first US refinery conversions to renewable diesel. As a result, we have developed knowledge and expertise in this area. We have efforts underway to study the conversion of our facilities to enable the production of renewable diesel, both with and without continuing fuels production. We already established a ‘capital light’ approach to renewable diesel by retaining a low-cost option of $13.3 million to acquire a one-third economic interest in GCE Holdings Acquisitions, which indirectly owns the Bakersfield, CA renewable diesel refinery with an annual capacity of up to 220 million gallons. The option extends beyond January 2022, when the facility is expected to be commissioned and its production capability has been demonstrated, thereby reducing risk to a Delek investment. We will continue to evaluate the business and move forward with further investment if the economics are attractive.

5

•Retail: With respect to CVR’s proposal to sell our retail convenience store network, we would point out that Delek has a track record of prudent strategic actions in this area of our business. Delek developed the MAPCO Express convenience store chain into a strong southeastern US business, and sold the business in 2016 at a multiple of approximately 12.7 times forecasted store-level EBITDA8. The proceeds from that sale were a key component in developing adequate liquidity to proceed with the acquisition of Alon. Since the MAPCO Express sale, market multiples for retail have remained strong, and we believe this trend will continue for some time.

We inherited Alon’s retail chain as a result of the 2017 Alon Acquisition. Since then, through the rationalization of the store portfolio and the implementation of our proven retail programs, the Adjusted Retail Contribution Margin9 has doubled from approximately $29 million in 2016 (pre-Alon Acquisition) to $47 million in 2020. In addition to implementing our programs and divesting or not renewing leases of approximately 50 locations (which generated ~$20 million in cash proceeds), we have constructed three new-to-industry (“NTI”) stores which outperform our legacy stores in terms of expected Adjusted Retail Contribution Margin by 4.8x. Through further build-out of NTI stores, we have the potential (capital dependent) to achieve more than $100 million in Adjusted Retail Contribution Margin by 2025 as the NTI stores mature. We forecast an IRR above 25% on retail growth capital expenditures, representing one of the more attractive opportunities to which we can allocate capital. Furthermore, the retail segment provides a natural fuel short for Delek’s refining segment and enhances cash flow stability. We continue to evaluate holding versus selling with the assistance of outside advisors, but we believe there are additional growth opportunities for the retail segment.

•Delek Logistics: CVR also proposed that we utilize proceeds from a sale of our retail business to purchase the publicly-held units of DKL. These publicly-held units reflect approximately 20% of the outstanding equity of DKL, and have a market value today of approximately $322 million10. The distributions to the public units are approximately $32 million per year based on DKL’s current quarterly distribution per unit of $0.91 and current public units outstanding. DKL has increased its distribution per unit every quarter since it went public in November 2012 and is guiding toward an additional 5% increase in 2021. Buying in these units is not a prudent use of capital compared to alternative uses of capital available to the Company. DKL provides both an alternative source of financing and could also serve as an acquisition currency. Given the strength of DKL's equity, we believe it could be used to fund further midstream growth by taking advantage of depressed MLP equity prices and distressed industry players, as the calculus of ‘build-vs-buy’ has flipped in the past year to favor acquisition over construction.

Unlike many of our MLP peers, DKL has doubled its EBITDA11 in the past three years from $115 million in 2017 to $245 million in 2020, while increasing distributions, increasing coverage, and improving the leverage ratio. Our actions in 2020 further highlight the value and flexibility of the Delek /

8 Based on midpoint of pre-disposition EBITDA guidance provided for MAPCO Express retail assets.

9 Refer to the 'Non-GAAP Disclosures' Section at the end of this communication for a description of our non-GAAP measures as well as a reconciliation to their most comparable GAAP financial measure.

10 As of 3/2/21.

11 Refer to the 'Non-GAAP Disclosures' Section at the end of this communication for a description of our non-GAAP measures as well as a reconciliation to their most comparable GAAP financial measure.

6

DKL structure. In March 2020, Delek contributed its Big Spring gathering system to DKL for $146 million of consideration comprised of $100 million of cash and 5.0 million DKL common units valued at approximately $9.10 per unit at that time. The cash consideration provided liquidity at the Delek level during a period of significant uncertainty early in the pandemic, and the value of equity consideration received has increased over 4x since the time of the transaction. The end result is a contribution EBITDA multiple of approximately 9x12. While we continuously review the merits of our structure, we currently believe maintaining DKL as a standalone midstream-focused MLP aligns with our strategy of growing the midstream business.

OUR OBSERVATIONS REGARDING CVR’S COMPENSATION CLAIMS

Several weeks after publishing the business proposals, CVR made claims regarding the compensation of Delek’s CEO, focused primarily on his interest in DKL GP. The original grant of DKL GP interests took place nearly eight years ago, was disclosed in our proxy statement that year, and was designed to incentivize Mr. Yemin, as Chairman and CEO of Delek and DKL, to increase the value of DKL.

Under Mr. Yemin’s management, DKL outperformed, resulting in a total return of more than 233% TSR13 since the IPO. The largest beneficiary of the performance was Delek, as majority owner of DKL, and by extension the shareholders of Delek. This outperformance at DKL was achieved in the same environment in which Delek outperformed its refining peers, leading one industry analyst to name Delek’s CEO as ‘the best bang for the buck’ among its peers14.

In August 2020, Delek and DKL eliminated the incentive distribution rights ("IDRs") in a transaction that was similar to those that have been executed by most MLPs.The transaction was approved by the Conflicts Committee of the DKL GP, which was comprised solely of independent directors and the sale of the GP interests held by Mr. Yemin and members of management was approved by the independent, disinterested members of the Delek Board.

The amount of the consideration received reflected the appreciation in the value of the DKL GP interests over an approximately eight-year period since they were issued. Notably, the market responded well to the elimination of the IDRs, and the associated improvements in DKL’s cost of capital, with unit price appreciation of 7%15.

Our compensation framework is designed based on a pay-for-performance philosophy. Over the last three years, we have consistently received strong support from our shareholders on say-on-pay (over 96%)16.

CONCERNS REGARDING CVR COMMENTS ABOUT DELEK’S STRATEGY

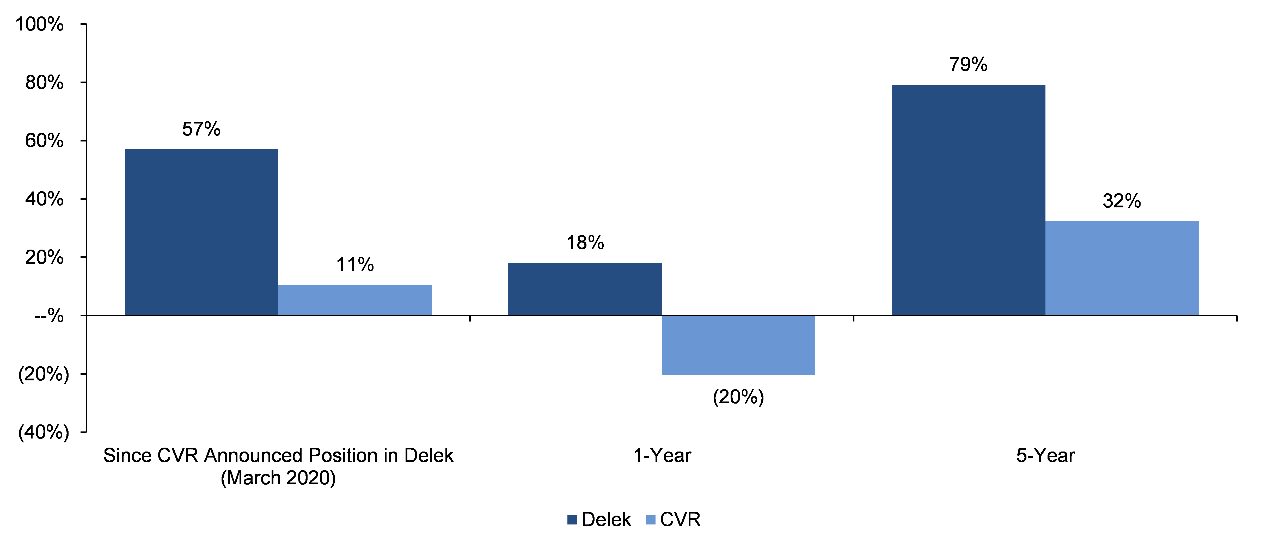

CVR’s letter and prior public comments from its executives state that Delek should abandon its strategy and shift to an approach that is more in line with our competitor CVR’s objectives. From a performance perspective, Delek’s strategy has driven significant outperformance relative to CVR on a TSR basis over both the short and longer-term.

12 As of 3/2/21.

13 Total Shareholder Return calculated based on price performance of stock from 11/12/12 to 3/2/21 and assumes all dividends are reinvested.

14 Paul Sankey, Mizuho Research (9/11/2019); Permission to use quotation was neither sought nor obtained.

15 Unit price appreciation measured from 8/13/20 to 3/2/21.

16 Calculated as (Votes For / (Votes For + Votes Against)).

7

Since CVR announced its position in Delek, Delek has delivered a TSR of 57% versus 11% for CVR17. Over a 1- and 5-year period, Delek’s TSR has outperformed CVR’s by 38% and 47%, respectively18.

While CVR is calling for the divestiture of our retail segment, its management has publicly stated repeatedly, over a long period of time and as recently as January 2021, its aspirations to have its own retail business:

“Strategic Priorities:…continue to evaluate building a wholesale/retail business…” – CVR January 2021 Investor Presentation

“On our last call, I outlined our strategic objectives for 2019. A recap of those objectives are:…continue to increase our internally generated RINs and reduce our RIN exposure, this includes increasing biodiesel blending as well as continuing to explore building a wholesale and retail business…” – David Lamp, CVR’s CEO, on Q1 2019 earnings call

“We believe CVR Energy is well positioned for 2019 and beyond. To achieve our mission, our strategic objectives are:…continue to increase our internally generated RINs and reduce our RIN [exposure], this includes increasing our biodiesel blending as well as continuing to explore building a wholesale and retail business…” – David Lamp, CVR’s CEO, on Q4 2018 earnings call

“In addition to running our facilities reliably safe and environmentally compliant, a recap of our objectives are; one, build a wholesale/retail business to reduce our RIN exposure…” – David Lamp, CVR’s CEO, on Q2 2018 earnings call

“As discussed in our last call, I outlined our strategic objectives for 2018. We continue to develop these initiatives, and as we move forward, I will provide updates. A recap of our objectives are:…build a wholesale/retail business to reduce our RIN exposure…” – David Lamp, CVR’s CEO, on Q1 2018 earnings call

“To achieve our mission, the strategic initiatives and objectives for 2018 are:…to build a wholesale/retail business to reduce our RIN exposure…” – David Lamp, CVR’s CEO, on Q4 2017 earnings call

17 Represents TSR performance 3/20/20 to 3/2/21.

18 As of 3/2/21.

8

The contradictory position that Delek should sell its retail business while CVR is expressing interest in building such a business suggests CVR may be motivated by short-term monetary gain rather than a desire to create long-term value for Delek shareholders.

CVR also proposed eliminating our supply and trading activities. Supply and trading is a small but highly integrated part of Delek that generates value for our other businesses. Supply and trading is a low-cost business that has historically dampened gross margin volatility. Our other non-refining businesses provide additional diversification resulting in lower volatility and margin enhancements, such as crude gathering connected to refineries, asphalt marketing (including the use of proprietary tire rubber technology), and fuel exports to Mexico to maximize netbacks. Supply and trading is a direct competitor with CVR in several markets, including crude oil purchasing/gathering in Oklahoma and West Texas and light products marketing in Oklahoma and Arkansas. We believe that the elimination of our supply and trading business would provide CVR competitive advantages that otherwise would not exist.

CVR proposed that Delek close its Krotz Springs and El Dorado refineries. The El Dorado refinery supplies light products into markets where CVR is a direct competitor. As with CVR’s proposed elimination of supply and trading activities, the closure of the El Dorado refinery would create an immediate and meaningful competitive advantage to CVR at the detriment of DK shareholders.

Finally, with respect to cost reductions, we have taken proactive actions that have led to G&A expense savings of over $25 million in 2020 (off a base level of $275 million in 2019) and operating expense savings of $120 million (off a base of $682 million in 2019). We expect to further reduce operating and G&A expenses in 2021 by $70 million and $10 million, respectively.

DELEK’S RECOMMENDATIONS

Delek has a reputation for engaging with shareholders and analysts with respect to value-creating ideas and constructive proposals. While we welcome feedback from all shareholders, we respectfully note that CVR is not like any other Delek shareholder. We believe the actions demanded by CVR, a direct competitor of Delek, could benefit CVR’s competing business rather than creating value for Delek’s shareholders. Delek’s Board carefully evaluated CVR’s nominees and unanimously determined that adding them to the Delek Board is not in the best interests of Delek shareholders. Our Board will continue to evaluate actions in the best interest of all Delek shareholders – not just CVR.

We believe we have the right strategy in place to enhance shareholder value – the continued execution of our long-term strategic plan that is underpinned by a rigorous and disciplined capital allocation framework. We are also confident that we have the right team in place to deliver on this plan. We look forward to an ongoing dialogue with all shareholders, including CVR, as we continue delivering for shareholders.

As always, we will keep you informed of our progress and thank you for your support.

Sincerely,

Your Board of Directors

9

Evercore is acting as financial advisor and Skadden, Arps, Slate, Meagher, & Flom LLP is acting as legal advisor to Delek.

About Delek US Holdings, Inc.

Delek US Holdings, Inc. is a diversified downstream energy company with assets in petroleum refining, logistics, asphalt, renewable fuels and convenience store retailing. The refining assets consist of refineries operated in Tyler and Big Spring, Texas, El Dorado, Arkansas and Krotz Springs, Louisiana with a combined nameplate crude throughput capacity of 302,000 barrels per day.

The logistics operations consist of Delek Logistics Partners, LP (NYSE: DKL) ("Delek Logistics"). Delek US and its affiliates also own the general partner and an approximate 80 percent limited partner interest in Delek Logistics. Delek Logistics is a growth-oriented master limited partnership focused on owning and operating midstream energy infrastructure assets.

The convenience store retail business operates approximately 253 convenience stores in central and west Texas and New Mexico.

Information about Delek US Holdings, Inc. can be found on its website (www.delekus.com), investor relations webpage (ir.delekus.com), news webpage (www.delekus.com/news) and its Twitter account (@DelekUSHoldings).

10

Additional Information:

Delek, its directors and certain of its executive officers and employees may be deemed to be participants in the solicitation of proxies from the company’s shareholders in connection with the matters to be considered at the Company’s 2021 Annual Meeting. Delek intends to file a proxy statement and a white proxy card with the SEC in connection with any such solicitation of proxies from the Company’s shareholders. DELEK SHAREHOLDERS ARE STRONGLY ENCOURAGED TO READ ANY SUCH PROXY STATEMENT AND ACCOMPANYING WHITE PROXY CARD WHEN THEY BECOME AVAILABLE AS THEY WILL CONTAIN IMPORTANT INFORMATION.

Information regarding the ownership of the Company’s stock and other securities by the Company’s directors and executive officers is included in SEC filings on Forms 3, 4, and 5, which can be found through the Company’s website (http://www.delekus.com) in the section “Investors” or through the SEC’s website at www.sec.gov. Information can also be found in the Company’s other SEC filings, including the Company’s Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. More detailed and updated information regarding the identity of potential participants, and their direct or indirect interests, by security holdings or otherwise, will be set forth in the proxy statement and other materials to be filed with the SEC in connection with the Company’s 2021 Annual Meeting. Shareholders will be able to obtain any proxy statement, any amendments or supplements to the proxy statement and other documents filed by Delek with the SEC for no charge at the SEC’s website at www.sec.gov. Copies will also be available at no charge on the Company’s website at http://www.delekus.com.

Non-GAAP Disclosures:

Our management uses certain "non-GAAP" operational measures to evaluate our operating segment performance and non-GAAP financial measures to evaluate past performance and prospects for the future to supplement our financial information presented in accordance with U.S. GAAP (United States generally accepted accounting principles). These financial and operational non-GAAP measures are important factors in assessing our operating results and profitability and include:

•Earnings before interest, taxes, depreciation and amortization ("EBITDA") - calculated as net income before net interest expense, income tax expense, depreciation and amortization expense, including amortization of customer contract intangible assets (with respect to DKL EBITDA).

•Adjusted Retail Contribution Margin – calculated or reported (with respect to Delek) contribution margin (or revenue less cost of materials and other and operating expenses) less estimated general and administrative expenses specific to the segment (and excluding allocations of corporate general and administrative expenses), adjusted to include gain (loss) from disposal of property and equipment. While this measure does not exactly represent EBITDA, it may be considered a reasonably comparable measure to EBITDA, a commonly used metric in the retail market, in that it includes all identified material cash income and expense items, and excludes depreciation, amortization, interest and income taxes. This definition of Adjusted Retail Contribution Margin is specific to this release only and the exhibits referenced herein, and may not correlate to the use of the term ‘Adjusted Contribution Margin’ or 'Adjusted Segment Contribution Margin' as a non-GAAP measure in other of our filings with the SEC. Accordingly, always refer to the respective Non-GAAP Disclosures section, included in each of our filings that contain non-GAAP measures, for more information

11

regarding the use of and definition of non-GAAP measures and terms, as they relate to that specific SEC filing.

We believe these non-GAAP measures are useful to investors, lenders, ratings agencies and analysts to assess our financial results and ongoing performance in certain segments because, when reconciled to their most comparable GAAP financial measure, they provide important information regarding trends that may aid in evaluating our performance as well improved relevant comparability between periods, to peers or to market metrics.

Non-GAAP measures have important limitations as analytical tools, because they exclude some, but not all, items that affect contribution margin, operating income (loss), and net income (loss). These measures should not be considered substitutes for their most directly comparable U.S. GAAP financial measures. Additionally, because the non-GAAP measures referenced above may be defined differently by other companies in its industry, Delek's definition may not be comparable to similarly titled measures of other companies. See the accompanying tables below for a reconciliation of these non-GAAP measures to the most directly comparable GAAP measures.

| Delek Logistics Partners, LP | |||||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation of Amounts Reported Under U.S. GAAP | |||||||||||||||||||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | ||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation of Net Income to EBITDA: | |||||||||||||||||||||||||||||||||||||||||||||||

| Net income | $ | 159.3 | $ | 96.7 | $ | 90.2 | $ | 69.4 | |||||||||||||||||||||||||||||||||||||||

| Add: | |||||||||||||||||||||||||||||||||||||||||||||||

| Income tax expense | 0.2 | 1.0 | 0.5 | (0.2) | |||||||||||||||||||||||||||||||||||||||||||

| Depreciation and amortization | 35.7 | 26.7 | 26.0 | 21.9 | |||||||||||||||||||||||||||||||||||||||||||

| Amortization of customer contract intangible assets | 7.2 | 7.2 | 6.0 | — | |||||||||||||||||||||||||||||||||||||||||||

| Interest expense, net | 42.9 | 47.3 | 41.3 | 23.9 | |||||||||||||||||||||||||||||||||||||||||||

| EBITDA | $ | 245.3 | $ | 178.9 | $ | 164.0 | $ | 115.0 | |||||||||||||||||||||||||||||||||||||||

| Retail Segment | |||||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation of Amounts Reported Under U.S. GAAP | |||||||||||||||||||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Period from July 1, 2017 to December 31, 2017 | ||||||||||||||||||||||||||||||||||||||||||||||

| 2020 | 2019 | 2018 | |||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation of Contribution Margin to Adjusted Retail Contribution Margin: | |||||||||||||||||||||||||||||||||||||||||||||||

| Contribution Margin | $ | 67.6 | $ | 58.5 | $ | 58.9 | $ | 26.8 | |||||||||||||||||||||||||||||||||||||||

| Less: | |||||||||||||||||||||||||||||||||||||||||||||||

| General and administrative expenses | 20.5 | 23.8 | 23.2 | 9.8 | |||||||||||||||||||||||||||||||||||||||||||

| Add: | |||||||||||||||||||||||||||||||||||||||||||||||

| Gain on sale of assets | 0.1 | 3.0 | 1.2 | — | |||||||||||||||||||||||||||||||||||||||||||

| Adjusted Retail Contribution Margin | $ | 47.2 | $ | 37.7 | $ | 36.9 | $ | 17.0 | |||||||||||||||||||||||||||||||||||||||

12

Retail Segment - Pre-Acquisition (a) | |||||||||||||||||||||||

| Reconciliation of Amounts Reported Under U.S. GAAP | |||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||

| Period from January 1, 2017 to June 30, 2017 | Year Ended December 31, 2016 | ||||||||||||||||||||||

| Net revenue | $ | 398.6 | $ | 731.7 | |||||||||||||||||||

| Operating costs and expenses (excluding depreciation and amortization): | |||||||||||||||||||||||

| Cost of materials | 325.9 | 588.8 | |||||||||||||||||||||

| Selling, general and administrative expenses | 54.6 | 114.3 | |||||||||||||||||||||

| Total operating costs and expenses | 380.5 | 703.1 | |||||||||||||||||||||

| Gain on sale of assets | 1.1 | 0.4 | |||||||||||||||||||||

| Adjusted Retail Contribution Margin | $ | 19.2 | $ | 29.0 | |||||||||||||||||||

(a) For the annual period ended December 31, 2016, the Pre-acquisition Alon Adjusted Retail Contribution Margin was derived from the Annual Report on Form 10-K filed by Alon and incorporated by reference into Delek’s 2016 Annual Report on Form 10-K (when Alon was a significant equity method investment of Delek), and for the six months ended June 30, 2017, the Pre-acquisition Alon Adjusted Retail Contribution Margin was derived from Exhibit 99.3 Alon Supplemental Information, filed as an exhibit to Delek’s Form 8-K filed on August 3, 2017 related to the significant acquisition of Alon. In those respective filings, Alon did not present Contribution Margin as a GAAP measure for its retail segment (as defined by Alon, which is not believed to be materially different from Delek’s definition and, therefore, hereafter also referred to as “Retail Segment”). As a result, we have calculated Adjusted Retail Contribution Margin for the Retail Segment for the pre-acquisition periods using the income statement items that were disclosed for the Retail Segment by Alon. Note that the pre-acquisition period presentation of Adjusted Retail Contribution Margin is based on accounting policies as elected and applied by Alon, which may differ from accounting policies used post-acquisition by Delek and reflected in Delek’s post-acquisition Adjusted Retail Contribution Margin.

For further information: Investor Relations Contact: Blake Fernandez, Senior Vice President of Investor Relations and Market Intelligence, 615-224-1312 OR Public Relations Contacts: Michael Freitag / Tim Lynch / Andrew Squire - Joele Frank, Wilkinson Brimmer Katcher, 212-355-4449.

13

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Delek US (DK) PT Raised to $26 at Morgan Stanley

- Montrose Environmental (MEG) Announces Pricing of Public Offering of Shares

- Delek Logistics Partners, LP Announces Proposed Offering of $200 Million of Additional 8.625% Senior Notes Due 2029

Create E-mail Alert Related Categories

SEC FilingsRelated Entities

S3Sign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!