Form 8-K LEXINGTON REALTY TRUST For: Feb 20

Tweet

Tweet Share

ShareExhibit 99.1

LEXINGTON REALTY TRUST

QUARTERLY SUPPLEMENTAL INFORMATION

December 31, 2019

Table of Contents

This Quarterly Earnings Press Release and Quarterly Supplemental Information contains certain forward-looking statements which involve known and unknown risks, uncertainties or other factors not under the control of Lexington Realty Trust (“Lexington”), which may cause actual results, performance or achievements of Lexington and its subsidiaries to be materially different from the results, performance, or other expectations implied by these forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed under the headings “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Risk Factors” in Lexington’s periodic reports filed with the Securities and Exchange Commission, including, but not limited to, risks related to: (1) the authorization of Lexington’s Board of Trustees of future dividend declarations, (2) Lexington’s ability to achieve its estimates of net income attributable to common shareholders and Adjusted Company FFO available to all equity holders and unitholders – diluted for the year ending December 31, 2020, (3) the successful consummation of any lease, acquisition, build-to-suit, development project, disposition, financing or other transaction on the terms described herein or at all, (4) the failure to continue to qualify as a real estate investment trust, (5) changes in general business and economic conditions, including the impact of any new legislation, (6) competition, (7) increases in real estate construction costs, (8) changes in interest rates, (9) changes in accessibility of debt and equity capital markets, and (10) future impairment charges. Copies of the periodic reports Lexington files with the Securities and Exchange Commission are available on Lexington’s web site at www.lxp.com. Forward-looking statements, which are based on certain assumptions and describe Lexington’s future plans, strategies and expectations, are generally identifiable by use of the words “believes,” “expects,” “intends,” “anticipates,” “estimates,” “projects,” may,” “plans,” “predicts,” “will,” “will likely result,” “is optimistic,” “goal,” “objective” or similar expressions. Except as required by law, Lexington undertakes no obligation to revise those forward-looking statements to reflect events or circumstances after the occurrence of unanticipated events. Accordingly, there is no assurance that Lexington’s expectations will be realized.

| LEXINGTON REALTY TRUST | |

| TRADED: NYSE: LXP | |

| ONE PENN PLAZA, SUITE 4015 | |

| NEW YORK, NY 10119-4015 |

FOR IMMEDIATE RELEASE

LEXINGTON REALTY TRUST REPORTS FOURTH QUARTER 2019 RESULTS

New York, NY - February 20, 2020 - Lexington Realty Trust (“Lexington”) (NYSE: LXP), a real estate investment trust focused on single-tenant industrial real estate investments, today announced results for the fourth quarter and year ended December 31, 2019.

Fourth Quarter 2019 Highlights

| • | Generated Net Income attributable to common shareholders of $83.6 million, or $0.33 per diluted common share. |

| • | Generated Adjusted Company Funds From Operations available to all equityholders and unitholders - diluted (“Adjusted Company FFO”) of $52.4 million, or $0.20 per diluted common share. |

| • | Raised net proceeds of approximately $71.0 million by issuing approximately 6.6 million common shares through the ATM program. |

| • | Disposed of 10 properties for an aggregate gross sale price of $172.7 million. |

| • | Acquired six industrial properties for an aggregate cost of $264.1 million. |

| • | Invested an aggregate of approximately $15.0 million in three new industrial development projects. |

| • | Completed 2.2 million square feet of new leases and lease extensions. |

| • | Declared a quarterly common share/unit dividend/distribution of $0.105 per share/unit, an increase of 2.4%. |

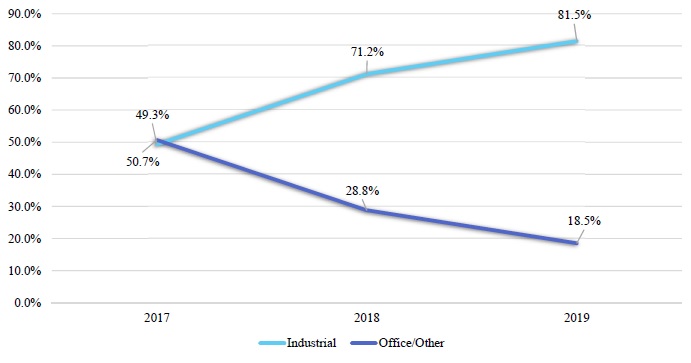

| • | Increased industrial portfolio to 81.5% of gross real estate assets. |

Full Year 2019 Highlights

| • | Generated Net Income attributable to common shareholders of $273.2 million, or $1.15 per diluted common share. |

| • | Generated Adjusted Company FFO of $196.6 million, or $0.80 per diluted common share. |

| • | Disposed of 22 properties for an aggregate gross sale price of $621.6 million. |

| • | Acquired 17 industrial properties for an aggregate cost of $703.8 million. |

| • | Invested an aggregate of $18.5 million in industrial development projects. |

| • | Increased total gross book value attributable to industrial assets from 71.2% to 81.5%. |

| • | Satisfied $199.2 million of secured debt at a weighted-average interest rate of 4.4%. |

| • | Extended the maturity of the revolving credit facility to 2023 and 2021 term loan to 2025, lowered the applicable margin rate and increased the commitment on the revolving credit facility, and swapped the LIBOR portion of the term loan interest rate to obtain a current fixed interest rate of 2.732% per annum. |

| • | Completed 6.4 million square feet of new leases and lease extensions, raising renewal Base Rents by 7.5%. |

3

Subsequent Events

| • | Acquired four industrial properties for an aggregate gross cost of approximately $195.0 million. |

Adjusted Company FFO is a non-GAAP financial measure. It and certain other non-GAAP financial measures are defined and reconciled later in this press release.

T. Wilson Eglin, Chief Executive Officer and President of Lexington Realty Trust, commented “Our excellent fourth quarter execution raised overall 2019 investment activity to more than $700 million of high-quality industrial assets. Further, property sales exceeded $620 million, and leasing volume was approximately six million square feet. Adding to our growth opportunities, we invested approximately $15 million during the quarter in three new development projects. We were also active on the capital markets front during the quarter, raising net proceeds of $71 million through our ATM program.

We continue to focus on becoming a single-tenant industrial REIT, having made tremendous progress thus far in repositioning our portfolio. At year-end, our industrial exposure represented nearly 82% of gross book value, and we are well-positioned to grow our industrial portfolio to 90% or more of gross book value by year-end 2020. As a result of all of these positive developments, we announced early in the fourth quarter an increase in our annualized dividend to $0.42 per share, with the intent of raising it steadily each year moving forward, subject to Board approval.”

FINANCIAL RESULTS

Revenues

For the quarter ended December 31, 2019, total gross revenues were $83.0 million, compared with total gross revenues of $88.2 million for the quarter ended December 31, 2018. The decrease was primarily attributable to a decrease in revenue due to property sales, partially offset by 2019 and 2018 property acquisitions.

Net Income Attributable to Common Shareholders

For the quarter ended December 31, 2019, net income attributable to common shareholders was $83.6 million, or $0.33 per diluted share, compared with net income attributable to common shareholders for the quarter ended December 31, 2018 of $23.8 million, or $0.10 per diluted share.

Adjusted Company FFO

For the quarter ended December 31, 2019, Lexington generated Adjusted Company FFO of $52.4 million, or $0.20 per diluted share, compared to Adjusted Company FFO for the quarter ended December 31, 2018 of $53.7 million, or $0.22 per diluted share.

4

Dividends/Distributions

As previously announced, during the fourth quarter of 2019, Lexington declared its quarterly common share/unit dividend/distribution for the quarter ended December 31, 2019 of $0.105 per common share/unit, an increase of 2.4%, which was paid on January 15, 2020 to common shareholders/unitholders of record as of December 31, 2019. Lexington previously declared a dividend of $0.8125 per share on its Series C Cumulative Convertible Preferred Stock (“Series C Preferred”) for the quarter ended December 31, 2019, which was paid February 18, 2020 to Series C Preferred shareholders of record as of January 31, 2020.

TRANSACTIONS

ACQUISITION TRANSACTIONS

| Property Type | Market | Sq. Ft. | Initial Basis ($000) | Approximate Lease Term (Yrs) | ||||||||||

| Industrial - warehouse/distribution | Greenville/Spartanburg, SC | 196,000 | $ | 16,817 | 5 | |||||||||

| Industrial - warehouse/distribution | Greenville/Spartanburg, SC | 177,320 | 15,583 | 6 | ||||||||||

| Industrial - warehouse/distribution | Phoenix, AZ | 186,336 | 21,020 | 7 | ||||||||||

| Industrial - warehouse/distribution | Phoenix, AZ | 801,424 | 67,079 | 11 | ||||||||||

| Industrial - warehouse/distribution | Chicago, IL | 1,034,200 | 49,348 | 10 | ||||||||||

| Industrial - warehouse/distribution | Greenville/Spartanburg, SC | 1,318,680 | 94,233 | 15 | ||||||||||

| 3,713,960 | $ | 264,080 | ||||||||||||

Including fourth quarter acquisition activity, consolidated 2019 acquisition activity totaled $703.8 million at aggregate weighted-average GAAP and cash capitalization rates of 5.8% and 5.4%, respectively.

DEVELOPMENT PROJECTS

| Project (% owned) | Market | Property

Type | Estimated | Estimated | GAAP Investment Balance as of 12/31/2019 ($000)(1) | Lexington | Estimated | |||||||||||||||

| Consolidated: | ||||||||||||||||||||||

| Fairburn (90%) | Atlanta, GA | Industrial | 910,000 | $ | 53,812 | $ | 10,088 | $ | 7,687 | 4Q 20 | ||||||||||||

| Rickenbacker (100%) | Columbus, OH | Industrial | 320,000 | 20,300 | 3,225 | 2,805 | 1Q 21 | |||||||||||||||

| $ | 74,112 | $ | 13,313 | $ | 10,492 | ||||||||||||||||

| Non-consolidated: | ||||||||||||||||||||||

| ETNA Park 70 (90%)(2) | Columbus, OH | Industrial | TBD | TBD | $ | 8,352 | $ | 8,644 | TBD | |||||||||||||

| ETNA Park 70 East (90%)(2) | Columbus, OH | Industrial | TBD | TBD | 4,310 | 4,351 | TBD | |||||||||||||||

| $ | 12,662 | $ | 12,995 | |||||||||||||||||||

| 1. | GAAP investment balance is in real estate under construction for consolidated projects and in investments in non-consolidated entities for non-consolidated projects. |

| 2. | Plans and specifications for completion have not been completed and the estimated square footage, project cost and completion date cannot be determined. |

5

PROPERTY DISPOSITIONS

| Primary Tenant | Location | Property | Gross | Annualized | Annualized NOI(1) ($000) | Month of Disposition | % | |||||||||||||||||

| Home Depot | Danville, VA | Other | $ | 4,650 | $ | 205 | $ | 276 | October | 100 | % | |||||||||||||

| Vacant | Watertown, NY | Other | 500 | (240 | ) | (244 | ) | October | 0 | % | ||||||||||||||

| Multi-Tenant | Indianapolis, IN | Office | 8,640 | 1,212 | 1,665 | November | 21 | % | ||||||||||||||||

| Multi-Tenant | Farmers Branch, TX | Office | 30,874 | 844 | 1,777 | November | 88 | % | ||||||||||||||||

| Vacant | Fairlea, WV | Other | 390 | (85 | ) | (86 | ) | November | 0 | % | ||||||||||||||

| Faurecia | Auburn Hills, MI | Office | 48,363 | 1,695 | 3,361 | December | 100 | % | ||||||||||||||||

| Multi-Tenant | Houston, TX | Office | 20,041 | (613 | ) | (477 | ) | December | 66 | % | ||||||||||||||

| Cummins | Columbus, IN | Office | 46,915 | 2,413 | 4,868 | December | 100 | % | ||||||||||||||||

| Mimeo | Memphis, TN | Industrial | 4,050 | 398 | 459 | December | 77 | % | ||||||||||||||||

| Alstom Power | Midlothian, VA | Office | 8,300 | 1,654 | 1,881 | December | 100 | % | ||||||||||||||||

| $ | 172,723 | $ | 7,483 | $ | 13,480 | |||||||||||||||||||

| 1. | Generally, quarterly period prior to sale annualized, excluding impairment charges. |

Including fourth quarter disposition activity, consolidated 2019 property disposition volume totaled $621.6 million at aggregate weighted-average GAAP and cash capitalization rates of 6.4% and 5.6%, respectively.

LEASING

During the fourth quarter of 2019, Lexington executed the following new and extended leases:

| LEASE EXTENSIONS | ||||||||||||||

| Location | Primary Tenant(1) | Prior Term | Lease Expiration Date | Sq. Ft. | ||||||||||

| Industrial | ||||||||||||||

| 1 | Antioch | TN | Wirtgen | 12/2019 | 12/2021 | 73,500 | ||||||||

| 2 | Laurens | SC | Michelin | 03/2020 | 01/2021 | 1,164,000 | ||||||||

| 3 | Austell | GA | Mars Wrigley | 05/2020 | 05/2025 | 604,852 | ||||||||

| 3 | Total industrial lease extensions | 1,842,352 | ||||||||||||

| NEW LEASES | ||||||||||||||

| Location | Lease Expiration Date | Sq. Ft. | ||||||||||||

| Industrial | ||||||||||||||

| 1 | Tampa | FL | RC Moore | 02/2023 | 229,605 | |||||||||

| 1 | Total industrial new leases | 229,605 | ||||||||||||

| Office | ||||||||||||||

| 1 | Phoenix | AZ | Valor IT | 07/2025 | 10,785 | |||||||||

| 2 | Lenexa | KS | Quest Diagnostics | 06/2030 | 77,484 | |||||||||

| 2 | Total office new leases | 88,269 | ||||||||||||

| 3 | Total new leases | 317,874 | ||||||||||||

| 6 | TOTAL NEW AND EXTENDED LEASES | 2,160,226 | ||||||||||||

| 1. | Leases greater than 10,000 square feet. |

As of December 31, 2019, Lexington's portfolio was 97.0% leased.

6

BALANCE SHEET/CAPITAL MARKETS

In the fourth quarter of 2019, Lexington issued approximately 6.6 million common shares under its ATM program raising net proceeds of approximately $71.0 million.

In the fourth quarter of 2019, Lexington satisfied $22.0 million of non-recourse debt. In addition, Lexington assumed $41.9 million of non-recourse debt in connection with the acquisition of a property in the Phoenix, Arizona market. The non-recourse debt has a fixed interest rate of 4.29% and matures in 2031.

As of December 31, 2019, Lexington did not have an outstanding balance under its unsecured revolving credit facility.

2020 EARNINGS GUIDANCE

Lexington estimates that its net income attributable to common shareholders per diluted common share for the year ended December 31, 2020 will be within an expected range of $0.95 to $0.98. Lexington estimates that its Adjusted Company FFO for the year ended December 31, 2020 will be within an expected range of $0.74 to $0.77 per diluted common share. This guidance is forward looking, excludes the impact of certain items and is based on current expectations.

FOURTH QUARTER 2019 CONFERENCE CALL

Lexington will host a conference call today February 20, 2020, at 8:30 a.m. Eastern Time, to discuss its results for the quarter ended December 31, 2019. Interested parties may participate in this conference call by dialing 1-844-825-9783 (U.S.), 1-412-317-5163 (International) or 1-855-669-9657 (Canada). A replay of the call will be available through May 20, 2020, at 1-877-344-7529 (U.S.), 1-412-317-0088 (International) or 1-855-669-9658 (Canada); pin code for all replay numbers is 10138613. A link to a live webcast of the conference call is available at www.lxp.com within the Investors section.

7

ABOUT LEXINGTON REALTY TRUST

Lexington Realty Trust (NYSE: LXP) is a publicly traded real estate investment trust (REIT) focused on single-tenant industrial real estate investments across the United States. Lexington seeks to expand its industrial portfolio through acquisitions, build-to-suit transactions, sale-leaseback transactions, development projects and other transactions, including acquisitions. For more information, including Lexington's Quarterly Supplemental Information package, or to follow Lexington on social media, visit www.lxp.com.

Contact:

Investor or Media Inquiries for Lexington Realty Trust:

Heather Gentry, Senior Vice President of Investor Relations

Lexington Realty Trust

Phone: (212) 692-7200 E-mail: [email protected]

This release contains certain forward-looking statements which involve known and unknown risks, uncertainties or other factors not under Lexington's control which may cause actual results, performance or achievements of Lexington to be materially different from the results, performance, or other expectations implied by these forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed under the headings “Management's Discussion and Analysis of Financial Condition and Results of Operations” and “Risk Factors” in Lexington's periodic reports filed with the Securities and Exchange Commission, including risks related to: (1) the authorization by Lexington's Board of Trustees of future dividend declarations, (2) Lexington's ability to achieve its estimates of net income attributable to common shareholders and Adjusted Company FFO for the year ending December 31, 2020, (3) the successful consummation of any lease, acquisition, build-to-suit, development project, disposition, financing or other transaction, (4) the failure to continue to qualify as a real estate investment trust, (5) changes in general business and economic conditions, including the impact of any legislation, (6) competition, (7) increases in real estate construction costs, (8) changes in interest rates, (9) changes in accessibility of debt and equity capital markets, and (10) future impairment charges. Copies of the periodic reports Lexington files with the Securities and Exchange Commission are available on Lexington's web site at www.lxp.com. Forward-looking statements, which are based on certain assumptions and describe Lexington's future plans, strategies and expectations, are generally identifiable by use of the words “believes,” “expects,” “intends,” “anticipates,” “estimates,” “projects”, “may,” “plans,” “predicts,” “will,” “will likely result,” “is optimistic,” “goal,” “objective” or similar expressions. Except as required by law, Lexington undertakes no obligation to publicly release the results of any revisions to those forward-looking statements which may be made to reflect events or circumstances after the occurrence of unanticipated events. Accordingly, there is no assurance that Lexington's expectations will be realized.

References to Lexington refer to Lexington Realty Trust and its consolidated subsidiaries. All interests in properties and loans are held, and all property operating activities are conducted, through special purpose entities, which are separate and distinct legal entities that maintain separate books and records, but in some instances are consolidated for financial statement purposes and/or disregarded for income tax purposes. The assets and credit of each special purpose entity with a property subject to a mortgage loan are not available to creditors to satisfy the debt and other obligations of any other person, including any other special purpose entity or affiliate. Consolidated entities that are not property owner subsidiaries do not directly own any of the assets of a property owner subsidiary (or the general partner, member of managing member of such property owner subsidiary), but merely hold partnership, membership or beneficial interests therein which interests are subordinate to the claims of the property owner subsidiary's (or its general partner's, member's or managing member's) creditors.

8

Non-GAAP Financial Measures - Definitions

Lexington has used non-GAAP financial measures as defined by the Securities and Exchange Commission Regulation G in this Quarterly Earnings Release and in other public disclosures.

Lexington believes that the measures defined below are helpful to investors in measuring our performance or that of an individual investment. Since these measures exclude certain items which are included in their respective most comparable measures under generally accepted accounting principles (“GAAP”), reliance on the measures has limitations; management compensates for these limitations by using the measures simply as supplemental measures that are weighed in balance with other GAAP measures. These measures are not necessarily indications of our cash flow available to fund cash needs. Additionally, they should not be used as an alternative to the respective most comparable GAAP measures when evaluating Lexington's financial performance or cash flow from operating, investing or financing activities or liquidity.

Company Funds Available for Distribution (“FAD”): FAD is calculated by making adjustments to Adjusted Company FFO (see below) for (1) straight-line adjustments, (2) lease incentive amortization, (3) amortization of above/below market leases, (4) lease termination payments, net, (5) non-cash interest, net, (6) non-cash charges, net, (7) cash paid for tenant improvements, and (8) cash paid for lease costs. Although FAD may not be comparable to that of other real estate investment trusts (“REITs”), Lexington believes it provides a meaningful indication of its ability to fund cash needs. FAD is a non-GAAP financial measure and should not be viewed as an alternative measurement of operating performance to net income, as an alternative to net cash flows from operating activities or as a measure of liquidity.

Funds from Operations (“FFO”) and Adjusted Company FFO: Lexington believes that Funds from Operations, or FFO, which is a non-GAAP measure, is a widely recognized and appropriate measure of the performance of an equity REIT. Lexington believes FFO is frequently used by securities analysts, investors and other interested parties in the evaluation of REITs, many of which present FFO when reporting their results. FFO is intended to exclude GAAP historical cost depreciation and amortization of real estate and related assets, which assumes that the value of real estate diminishes ratably over time. Historically, however, real estate values have risen or fallen with market conditions. As a result, FFO provides a performance measure that, when compared year over year, reflects the impact to operations from trends in occupancy rates, rental rates, operating costs, development activities, interest costs and other matters without the inclusion of depreciation and amortization, providing perspective that may not necessarily be apparent from net income.

The National Association of Real Estate Investment Trusts, or NAREIT, defines FFO as “net income (calculated in accordance with GAAP), excluding depreciation and amortization related to real estate, gains and losses from the sales of certain real estate assets, gains and losses from change in control and impairment write-downs of certain real estate assets and investments in entities when the impairment is directly attributable to decreases in value of depreciable real estate held by the entity. The reconciling items include amounts to adjust earnings from consolidated partially-owned entities and equity in earnings of unconsolidated affiliates to FFO.” FFO does not represent cash generated from operating activities in accordance with GAAP and is not indicative of cash available to fund cash needs.

Lexington presents FFO available to common shareholders and unitholders - basic and also presents FFO available to all equityholders and unitholders - diluted on a company-wide basis as if all securities that are convertible, at the holder's option, into Lexington’s common shares, are converted at the beginning of the period. Lexington also presents Adjusted Company FFO available to all equityholders and unitholders - diluted which adjusts FFO available to all equityholders and unitholders - diluted for certain items which we believe are not indicative of the operating results of Lexington's real estate portfolio. Lexington believes this is an appropriate presentation as it is frequently requested by security analysts, investors and other interested parties. Since others do not calculate these measures in a similar fashion, these measures may not be comparable to similarly titled measures as reported by others. These measures should not be considered as an alternative to net income as an indicator of Lexington’s operating performance or as an alternative to cash flow as a measure of liquidity.

GAAP and Cash Yield or Capitalization Rate: GAAP and cash yields or capitalization rates are measures of operating performance used to evaluate the individual performance of an investment. These measures are estimates and are not presented or intended to be viewed as a liquidity or performance measure that present a numerical measure of Lexington's historical or future financial performance, financial position or cash flows. The yield or capitalization rate is calculated by dividing the annualized NOI (as defined below, except GAAP rent adjustments are added back to rental income to calculate GAAP yield or capitalization rate) the investment is expected to generate (or has generated) divided by the acquisition/completion cost (or sale) price.

Net Operating Income (“NOI”): NOI is a measure of operating performance used to evaluate the individual performance of an investment. This measure is not presented or intended to be viewed as a liquidity or performance measure that presents a numerical measure of Lexington's historical or future financial performance, financial position or cash flows. Lexington defines NOI as operating revenues (rental income (less GAAP rent adjustments and lease termination income), and other property income) less property operating expenses. Other REITs may use different methodologies for calculating NOI, and accordingly, Lexington's NOI may not be comparable to other companies. Because NOI excludes general and administrative expenses, interest expense, depreciation and amortization, acquisition-related expenses, other nonproperty income and losses, and gains and losses from property dispositions, it provides a performance measure that, when compared year over year, reflects the revenues and expenses directly associated with owning and operating commercial real estate and the impact to operations from trends in occupancy rates, rental rates, and operating costs, providing a perspective on operations not immediately apparent from net income. Lexington believes that net income is the most directly comparable GAAP measure to NOI.

# # #

9

LEXINGTON REALTY TRUST AND CONSOLIDATED SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited and in thousands, except share and per share data)

| Three months ended December 31, | Twelve months ended December 31, | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||

| Gross revenues: | ||||||||||||||||

| Rental revenue | $ | 81,564 | $ | 87,251 | $ | 320,622 | $ | 395,339 | ||||||||

| Other revenue | 1,472 | 932 | 5,347 | 1,632 | ||||||||||||

| Total gross revenues | 83,036 | 88,183 | 325,969 | 396,971 | ||||||||||||

| Expense applicable to revenues: | ||||||||||||||||

| Depreciation and amortization | (35,977 | ) | (38,498 | ) | (147,594 | ) | (168,191 | ) | ||||||||

| Property operating | (11,052 | ) | (9,614 | ) | (42,018 | ) | (42,675 | ) | ||||||||

| General and administrative | (7,133 | ) | (7,763 | ) | (30,785 | ) | (31,662 | ) | ||||||||

| Non-operating income | 335 | 893 | 2,262 | 1,859 | ||||||||||||

| Interest and amortization expense | (14,380 | ) | (16,656 | ) | (65,095 | ) | (79,880 | ) | ||||||||

| Debt satisfaction gains (charges), net | 10 | (368 | ) | (4,517 | ) | (2,596 | ) | |||||||||

| Impairment charges | (2,974 | ) | (4,953 | ) | (5,329 | ) | (95,813 | ) | ||||||||

| Gains on sales of properties | 74,227 | 13,336 | 250,889 | 252,913 | ||||||||||||

| Income before provision for income taxes and equity in earnings (losses) of non-consolidated entities | 86,092 | 24,560 | 283,782 | 230,926 | ||||||||||||

| Provision for income taxes | (271 | ) | (402 | ) | (1,379 | ) | (1,728 | ) | ||||||||

| Equity in earnings (losses) of non-consolidated entities | (398 | ) | 1,516 | 2,890 | 1,708 | |||||||||||

| Net income | 85,423 | 25,674 | 285,293 | 230,906 | ||||||||||||

| Less net income attributable to noncontrolling interests | (192 | ) | (266 | ) | (5,383 | ) | (3,491 | ) | ||||||||

| Net income attributable to Lexington Realty Trust shareholders | 85,231 | 25,408 | 279,910 | 227,415 | ||||||||||||

| Dividends attributable to preferred shares – Series C | (1,572 | ) | (1,572 | ) | (6,290 | ) | (6,290 | ) | ||||||||

| Allocation to participating securities | (85 | ) | (40 | ) | (395 | ) | (287 | ) | ||||||||

| Net income attributable to common shareholders | $ | 83,574 | $ | 23,796 | $ | 273,225 | $ | 220,838 | ||||||||

| Net income attributable to common shareholders – per common share basic | $ | 0.34 | $ | 0.10 | $ | 1.15 | $ | 0.93 | ||||||||

| Weighted-average common shares outstanding – basic | 248,943,975 | 233,963,608 | 237,642,048 | 236,666,375 | ||||||||||||

| Net income attributable to common shareholders – per common share diluted | $ | 0.33 | $ | 0.10 | $ | 1.15 | $ | 0.93 | ||||||||

| Weighted-average common shares outstanding – diluted | 252,939,590 | 238,292,912 | 237,934,515 | 240,810,990 | ||||||||||||

10

LEXINGTON REALTY TRUST AND CONSOLIDATED SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

As of December 31,

(In thousands, except share and per share data)

| 2019 | 2018 | |||||||

| (unaudited) | ||||||||

| Assets: | ||||||||

| Real estate, at cost | $ | 3,320,574 | $ | 3,090,134 | ||||

| Real estate - intangible assets | 409,756 | 419,612 | ||||||

| Investments in real estate under construction | 13,313 | — | ||||||

| Real estate, gross | 3,743,643 | 3,509,746 | ||||||

| Less: accumulated depreciation and amortization | 887,629 | 954,087 | ||||||

| Real estate, net | 2,856,014 | 2,555,659 | ||||||

| Assets held for sale | — | 63,868 | ||||||

| Operating lease right-of-use assets, net | 38,133 | — | ||||||

| Cash and cash equivalents | 122,666 | 168,750 | ||||||

| Restricted cash | 6,644 | 8,497 | ||||||

| Investments in non-consolidated entities | 57,168 | 66,183 | ||||||

| Deferred expenses, net | 18,404 | 15,937 | ||||||

| Rent receivable – current | 3,229 | 3,475 | ||||||

| Rent receivable – deferred | 66,294 | 58,692 | ||||||

| Other assets | 11,708 | 12,779 | ||||||

| Total assets | $ | 3,180,260 | $ | 2,953,840 | ||||

| Liabilities and Equity: | ||||||||

| Liabilities: | ||||||||

| Mortgages and notes payable, net | $ | 390,272 | $ | 570,420 | ||||

| Term loans payable, net | 297,439 | 298,733 | ||||||

| Senior notes payable, net | 496,870 | 496,034 | ||||||

| Trust preferred securities, net | 127,396 | 127,296 | ||||||

| Dividends payable | 32,432 | 48,774 | ||||||

| Liabilities held for sale | — | 386 | ||||||

| Operating lease liabilities | 39,442 | — | ||||||

| Accounts payable and other liabilities | 29,925 | 30,790 | ||||||

| Accrued interest payable | 7,897 | 4,523 | ||||||

| Deferred revenue - including below market leases, net | 20,350 | 20,531 | ||||||

| Prepaid rent | 13,518 | 9,675 | ||||||

| Total liabilities | 1,455,541 | 1,607,162 | ||||||

| Commitments and contingencies | ||||||||

| Equity: | ||||||||

| Preferred shares, par value $0.0001 per share; authorized 100,000,000 shares: | ||||||||

| Series C Cumulative Convertible Preferred, liquidation preference $96,770; 1,935,400 shares issued and outstanding | 94,016 | 94,016 | ||||||

| Common shares, par value $0.0001 per share; authorized 400,000,000 shares, 254,770,719 and 235,008,554 shares issued and outstanding in 2019 and 2018, respectively | 25 | 24 | ||||||

| Additional paid-in-capital | 2,976,670 | 2,772,855 | ||||||

| Accumulated distributions in excess of net income | (1,363,676 | ) | (1,537,100 | ) | ||||

| Accumulated other comprehensive income (loss) | (1,928 | ) | 76 | |||||

| Total shareholders’ equity | 1,705,107 | 1,329,871 | ||||||

| Noncontrolling interests | 19,612 | 16,807 | ||||||

| Total equity | 1,724,719 | 1,346,678 | ||||||

| Total liabilities and equity | $ | 3,180,260 | $ | 2,953,840 | ||||

11

LEXINGTON REALTY TRUST AND CONSOLIDATED SUBSIDIARIES

EARNINGS PER SHARE

(Unaudited and in thousands, except share and per share data)

| Three Months Ended December 31, | Twelve Months Ended December 31, | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||

| EARNINGS PER SHARE: | ||||||||||||||||

| Basic: | ||||||||||||||||

| Net income attributable to common shareholders | $ | 83,574 | $ | 23,796 | $ | 273,225 | $ | 220,838 | ||||||||

| Weighted-average common shares outstanding - basic | 248,943,975 | 233,963,608 | 237,642,048 | 236,666,375 | ||||||||||||

| Net income attributable to common shareholders - per common share basic | $ | 0.34 | $ | 0.10 | $ | 1.15 | $ | 0.93 | ||||||||

| Diluted: | ||||||||||||||||

| Net income attributable to common shareholders - basic | $ | 83,574 | $ | 23,796 | $ | 273,225 | $ | 220,838 | ||||||||

| Impact of assumed conversions | (34 | ) | 21 | — | 2,528 | |||||||||||

| Income from continuing operations attributable to common shareholders | $ | 83,540 | $ | 23,817 | $ | 273,225 | $ | 223,366 | ||||||||

| Weighted-average common shares outstanding - basic | 248,943,975 | 233,963,608 | 237,642,048 | 236,666,375 | ||||||||||||

| Effect of dilutive securities: | ||||||||||||||||

| Unvested share-based payment awards and options | 639,178 | 723,120 | 292,467 | 528,495 | ||||||||||||

| Operating Partnership Units | 3,356,437 | 3,606,184 | — | 3,616,120 | ||||||||||||

| Weighted-average common shares outstanding - diluted | 252,939,590 | 238,292,912 | 237,934,515 | 240,810,990 | ||||||||||||

| Net income attributable to common shareholders - per common share diluted | $ | 0.33 | $ | 0.10 | $ | 1.15 | $ | 0.93 | ||||||||

12

LEXINGTON REALTY TRUST AND CONSOLIDATED SUBSIDIARIES

ADJUSTED COMPANY FUNDS FROM OPERATIONS & FUNDS AVAILABLE FOR DISTRIBUTION

(Unaudited and in thousands, except share and per share data)

| Three Months Ended December 31, | Twelve Months Ended December 31, | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||

| FUNDS FROM OPERATIONS: | ||||||||||||||||

| Basic and Diluted: | ||||||||||||||||

| Net income attributable to common shareholders | $ | 83,574 | $ | 23,796 | $ | 273,225 | $ | 220,838 | ||||||||

| Adjustments: | ||||||||||||||||

| Depreciation and amortization | 35,323 | 37,819 | 144,792 | 164,261 | ||||||||||||

| Impairment charges - real estate | 2,974 | 4,953 | 5,329 | 95,813 | ||||||||||||

| Noncontrolling interests - OP units | (34 | ) | 22 | 4,376 | 2,528 | |||||||||||

| Amortization of leasing commissions | 654 | 679 | 2,802 | 3,930 | ||||||||||||

| Joint venture and noncontrolling interest adjustment | 2,249 | 2,567 | 9,449 | 4,063 | ||||||||||||

| Gains on sales of properties, including non-consolidated entities and net of tax | (74,211 | ) | (14,821 | ) | (255,048 | ) | (254,269 | ) | ||||||||

| FFO available to common shareholders and unitholders - basic | 50,529 | 55,015 | 184,925 | 237,164 | ||||||||||||

| Preferred dividends | 1,572 | 1,572 | 6,290 | 6,290 | ||||||||||||

| Amount allocated to participating securities | 85 | 40 | 395 | 287 | ||||||||||||

| FFO available to all equityholders and unitholders - diluted | 52,186 | 56,627 | 191,610 | 243,741 | ||||||||||||

| Debt satisfaction (gains) charges, net, including non-consolidated entities | (9 | ) | 368 | 4,773 | 2,596 | |||||||||||

| Other(1) | 202 | (3,305 | ) | 202 | (10,038 | ) | ||||||||||

| Adjusted Company FFO available to all equityholders and unitholders - diluted | 52,379 | 53,690 | 196,585 | 236,299 | ||||||||||||

| FUNDS AVAILABLE FOR DISTRIBUTION: | ||||||||||||||||

| Adjustments: | ||||||||||||||||

| Straight-line rents | (3,656 | ) | (4,722 | ) | (14,502 | ) | (20,968 | ) | ||||||||

| Lease incentives | 293 | 227 | 1,191 | 1,686 | ||||||||||||

| Amortization of above/below market leases | (269 | ) | (28 | ) | (443 | ) | 285 | |||||||||

| Lease termination payments, net | 25 | (309 | ) | (1,095 | ) | (1,234 | ) | |||||||||

| Non-cash interest, net | 563 | 854 | 2,709 | 4,209 | ||||||||||||

| Non-cash charges, net | 1,577 | 1,611 | 6,410 | 6,810 | ||||||||||||

| Tenant improvements | (2,885 | ) | (1,608 | ) | (7,817 | ) | (8,271 | ) | ||||||||

| Lease costs | (3,743 | ) | (1,448 | ) | (14,367 | ) | (4,522 | ) | ||||||||

| Joint venture and non-controlling interest adjustment | (63 | ) | (449 | ) | (3,794 | ) | (505 | ) | ||||||||

| Company Funds Available for Distribution | $ | 44,221 | $ | 47,818 | $ | 164,877 | $ | 213,789 | ||||||||

| Per Common Share and Unit Amounts | ||||||||||||||||

| Basic: | ||||||||||||||||

| FFO | $ | 0.20 | $ | 0.23 | $ | 0.77 | $ | 0.99 | ||||||||

| Diluted: | ||||||||||||||||

| FFO | $ | 0.20 | $ | 0.23 | $ | 0.78 | $ | 0.99 | ||||||||

| Adjusted Company FFO | $ | 0.20 | $ | 0.22 | $ | 0.80 | $ | 0.96 | ||||||||

| Weighted-Average Common Shares | ||||||||||||||||

| Basic: | ||||||||||||||||

| Weighted-average common shares outstanding - basic EPS | 248,943,975 | 233,963,608 | 237,642,048 | 236,666,375 | ||||||||||||

| Operating partnership units(2) | 3,356,437 | 3,606,184 | 3,490,147 | 3,616,120 | ||||||||||||

| Weighted-average common shares outstanding - basic FFO | 252,300,412 | 237,569,792 | 241,132,195 | 240,282,495 | ||||||||||||

| Diluted: | ||||||||||||||||

| Weighted-average common shares outstanding - diluted EPS | 252,939,590 | 238,292,912 | 237,934,515 | 240,810,990 | ||||||||||||

| Unvested share-based payment awards | 36,516 | — | 22,813 | — | ||||||||||||

| Operating partnership units(1) | — | — | 3,490,147 | — | ||||||||||||

| Preferred shares - Series C | 4,710,570 | 4,710,570 | 4,710,570 | 4,710,570 | ||||||||||||

| Weighted-average common shares outstanding - diluted FFO | 257,686,676 | 243,003,482 | 246,158,045 | 245,521,560 | ||||||||||||

| (1) | "Other" primarily consisted of transaction related costs in 2019 and the acceleration of below-market lease intangible accretion in 2018. |

| (2) | Includes OP units other than OP units held by Lexington. |

13

LEXINGTON REALTY TRUST AND CONSOLIDATED SUBSIDIARIES

RECONCILIATION OF NON-GAAP MEASURES

(UNAUDITED)

2020 EARNINGS GUIDANCE

| Twelve

Months Ended December 31, 2020 | ||||||||

| Range | ||||||||

| Estimated: | ||||||||

| Net income attributable to common shareholders per diluted common share(1) | $ | 0.95 | $ | 0.98 | ||||

| Depreciation and amortization | 0.62 | 0.62 | ||||||

| Impact of capital transactions | (0.83 | ) | (0.83 | ) | ||||

| Estimated Adjusted Company FFO per diluted common share | $ | 0.74 | $ | 0.77 | ||||

| (1) | Assumes all convertible securities are dilutive. |

14

LEXINGTON REALTY TRUST

2019 Fourth Quarter Investments / Capital Recycling Summary

PROPERTY INVESTMENTS

| Property Type | Market | Square Feet | Initial Basis ($000) | Month Closed | Primary Lease Expiration | |||||||||||||||

| 1 | Industrial - Warehouse/distribution | Greenville/Spartanburg | SC | 196,000 | $ | 16,817 | October | 01/2024 | ||||||||||||

| 2 | Industrial - Warehouse/distribution | Greenville/Spartanburg | SC | 177,320 | 15,583 | October | 04/2025 | |||||||||||||

| 3 | Industrial - Warehouse/distribution | Phoenix | AZ | 186,336 | 21,020 | October | 09/2026 | |||||||||||||

| 4 | Industrial - Warehouse/distribution | Phoenix | AZ | 801,424 | 67,079 | November | 09/2030 | |||||||||||||

| 5 | Industrial - Warehouse/distribution | Chicago | IL | 1,034,200 | 49,348 | December | 09/2029 | |||||||||||||

| 6 | Industrial - Warehouse/distribution | Greenville/Spartanburg | SC | 1,318,680 | 94,233 | December | 12/2034 | |||||||||||||

| 6 | TOTAL PROPERTY INVESTMENTS | 3,713,960 | $ | 264,080 | ||||||||||||||||

CAPITAL RECYCLING

PROPERTY DISPOSITIONS

| Primary Tenant | Location | Property Type | Gross Disposition Price ($000) | Annualized Net Income ($000) (1) | Annualized NOI ($000)(1)(2) | Month of Disposition | % Leased | Gross Disposition Price PSF | ||||||||||||||||||

| 1 | Home Depot | Danville | VA | Other | $ | 4,650 | $ | 205 | $ | 276 | October | 100 | % | $ | - | |||||||||||

| 2 | Vacant | Watertown | NY | Other | 500 | (240 | ) | (244 | ) | October | 0 | % | 4.14 | |||||||||||||

| 3 | Multi-Tenant | Indianapolis | IN | Office | 8,640 | 1,212 | 1,665 | November | 21 | % | 61.26 | |||||||||||||||

| 4 | Multi-Tenant | Farmers Branch | TX | Office | 30,874 | 844 | 1,777 | November | 88 | % | 170.50 | |||||||||||||||

| 5 | Vacant | Fairlea | WV | Other | 390 | (85 | ) | (86 | ) | November | 0 | % | 4.29 | |||||||||||||

| 6 | Faurecia | Auburn Hills | MI | Office | 48,363 | 1,695 | 3,361 | December | 100 | % | 173.97 | |||||||||||||||

| 7 | Multi-Tenant | Houston | TX | Office | 20,041 | (613 | ) | (477 | ) | December | 66 | % | 128.96 | |||||||||||||

| 8 | Cummins | Columbus | IN | Office | 46,915 | 2,413 | 4,868 | December | 100 | % | 120.26 | |||||||||||||||

| 9 | Mimeo | Memphis | TN | Industrial | 4,050 | 398 | 459 | December | 77 | % | 28.91 | |||||||||||||||

| 10 | Alstom Power | Midlothian | VA | Office | 8,300 | 1,654 | 1,881 | December | 100 | % | 83.79 | |||||||||||||||

| 10 | TOTAL PROPERTY DISPOSITIONS | $ | 172,723 | $ | 7,483 | $ | 13,480 | |||||||||||||||||||

| Footnotes | |

| (1) | Generally, quarterly period prior to sale annualized, excluding impairment charges. |

| (2) | See definitions of non-GAAP measures and reconciliations to applicable GAAP measures in this document. |

| 15 |

LEXINGTON REALTY TRUST

12/31/2019

DEVELOPMENT PROJECTS

| GAAP | Lexington | ||||||||||||||||||

| Estimated | Investment Balance | Amount Funded | Estimated | ||||||||||||||||

| Project | Property | Estimated | Project Cost | as of 12/31/19 | as of 12/31/19 | Completion | |||||||||||||

| (% owned) | Market | Type | Sq. Ft. | ($000) | ($000) (1) | ($000) | Date | ||||||||||||

| Consolidated | |||||||||||||||||||

| 1 | Fairburn (90%) | Atlanta, GA | Industrial | 910,000 | $ | 53,812 | $ | 10,088 | $ | 7,687 | 4Q 2020 | ||||||||

| 2 | Rickenbacker (100%) | Columbus, OH | Industrial | 320,000 | 20,300 | 3,225 | 2,805 | 1Q 2021 | |||||||||||

| 2 | Total Consolidated Development | $ | 74,112 | $ | 13,313 | $ | 10,492 | ||||||||||||

| Non - Consolidated | |||||||||||||||||||

| 1 | Etna Park 70 (90%) (2) | Columbus, OH | Industrial | TBD | TBD | $ | 8,352 | $ | 8,644 | TBD | |||||||||

| 2 | Etna Park 70 East (90%) (2) | Columbus, OH | Industrial | TBD | TBD | 4,310 | 4,351 | TBD | |||||||||||

| 2 | Total Non-Consolidated Development | $ | 12,662 | $ | 12,995 | ||||||||||||||

| 4 | Total Development Projects | $ | 25,975 | $ | 23,487 | ||||||||||||||

| Footnotes | |

| (1) | GAAP investment balance is in real estate under construction for consolidated projects and in investments in non-consolidated entities for non-consolidated projects. |

| (2) | Plans and specifications for completion have not been completed and the estimated square footage, project cost and completion date cannot be determined. |

| 16 |

LEXINGTON REALTY TRUST

2019 Fourth Quarter Financing Summary

DEBT RETIRED

| Location | Tenant | Property Type | Face / Satisfaction ($000) | Rate | Maturity Date | ||||||||||

| 1 | Oakland, ME | T-Mobile USA | Office | $ | 7,939 | 5.930 | % | 10/2020 | |||||||

| 2 | Lenexa, KS | Quest Diagnostics | Office | 7,777 | 6.270 | % | 12/2019 | ||||||||

| 3 | Lavonia, GA | TI Automotive | Industrial | 6,297 | 5.460 | % | 12/2020 | ||||||||

| 3 | Total Mortgage Debt | $ | 22,013 | ||||||||||||

PROPERTY LEVEL FINANCING (1)

| Location | Tenant (3) | Property Type | Face ($000) | Fixed Rate | Maturity Date | |||||||||

| Goodyear, AZ (2) | Undisclosed | Industrial | $ | 41,877 | 4.290 | % | 08/2031 |

| Footnotes | |

| (1) | Also, a 20% owned joint venture incurred an additional $7.3 million of secured debt. |

| (2) | Assumed mortgage at acquisition. |

| (3) | Lease restricts certain disclosures. |

| 17 |

LEXINGTON REALTY TRUST

2019 Fourth Quarter Leasing Summary

LEASE EXTENSIONS

| Tenant (1) | Location | Prior Term | Lease Expiration Date | Sq. Ft. | New Base Rent Per Annum ($000)(2)(3) | Prior Base Rent Per Annum ($000) | New Cash Base Rent Per Annum ($000)(2)(3) | Prior Cash Base Rent Per Annum ($000)(3) | |||||||||||||||||

| Industrial | |||||||||||||||||||||||||

| 1 | Wirtgen | Antioch | TN | 12/2019 | 12/2021 | 73,500 | $ | 184 | $ | 216 | $ | 184 | $ | 216 | |||||||||||

| 2 | Michelin | Laurens | SC | 03/2020 | 01/2021 | 1,164,000 | 3,594 | 3,594 | 3,594 | 3,594 | |||||||||||||||

| 3 | Mars Wrigley | Austell | GA | 05/2020 | 05/2025 | 604,852 | 4,406 | 2,590 | 4,235 | 3,587 | |||||||||||||||

| 3 | Total Industrial Lease Extensions | 1,842,352 | $ | 8,184 | $ | 6,400 | $ | 8,013 | $ | 7,397 | |||||||||||||||

| 3 | TOTAL EXTENDED LEASES | 1,842,352 | $ | 8,184 | $ | 6,400 | $ | 8,013 | $ | 7,397 | |||||||||||||||

NEW LEASES

| Tenant (1) | Location | Lease Expiration Date | Sq. Ft. | New Base Rent Per Annum ($000)(2)(3) | New Cash Base Rent Per Annum ($000)(2)(3) | |||||||||||||

| Industrial | ||||||||||||||||||

| 1 | RC Moore (4) | Tampa | FL | 02/2023 | 229,605 | $ | 1,152 | $ | 1,160 | |||||||||

| 1 | Total Industrial New Leases | 229,605 | $ | 1,152 | $ | 1,160 | ||||||||||||

| Office | ||||||||||||||||||

| 1 | Valor IT | Phoenix | AZ | 07/2025 | 10,785 | $ | 215 | $ | 187 | |||||||||

| 2 | Quest Diagnostics (5) | Lenexa | KS | 06/2030 | 77,484 | 1,013 | 1,103 | |||||||||||

| 2 | Total Office New Leases | 88,269 | $ | 1,228 | $ | 1,290 | ||||||||||||

| 3 | TOTAL NEW LEASES | 317,874 | $ | 2,380 | $ | 2,450 | ||||||||||||

| 6 | TOTAL NEW AND EXTENDED LEASES | 2,160,226 | $ | 10,564 | $ | 10,463 | ||||||||||||

| 18 |

LEXINGTON REALTY TRUST

2019 Fourth Quarter Leasing Summary

NEW VACANCY (6)

| Prior Lease | 2019 | 2019 | ||||||||||||||||

| Expiration | Base Rent | Cash Rent | ||||||||||||||||

| Former Tenant | Location | Date | Sq. Ft. | ($000)(3) | ($000)(3) | |||||||||||||

| Industrial | ||||||||||||||||||

| Michelin | Moody | AL | 12/2019 | 595,346 | $ | 1,408 | $ | 1,450 | ||||||||||

| Footnotes | |

| (1) | Leases greater than 10,000 square feet. |

| (2) | Assumes twelve months rent from the later of 1/1/20 or lease commencement/extension, excluding free rent periods as applicable. |

| (3) | See definitions of non-GAAP measures and reconciliations to applicable GAAP measures in this document. |

| (4) | Prior tenant terminated lease 12/11/19; new tenant (RC Moore) will lease building effective 1/1/20. |

| (5) | Previous tenant lease expired and sub-lease tenant (Quest Diagnostics) entered into a direct lease. |

| (6) | Excludes multi-tenant properties, disposed properties and non-consolidated investments. |

| 19 |

LEXINGTON REALTY TRUST

12/31/2019

($000)

Other Revenue Data

| Base Rent | ||||||||||||

| Twelve months ended | ||||||||||||

| Asset Class | 12/31/19 (1) | 12/31/19 Percentage | 12/31/18 Percentage | |||||||||

| Industrial | $ | 194,485 | 75.5 | % | 65.4 | % | ||||||

| Office/Other | 63,274 | 24.5 | % | 34.6 | % | |||||||

| $ | 257,759 | 100.0 | % | 100.0 | % | |||||||

| Base Rent | ||||||||||||

| Twelve months ended | ||||||||||||

| Credit Ratings (2) | 12/31/19 (1) | 12/31/19 Percentage | 12/31/18 Percentage | |||||||||

| Investment Grade | $ | 125,509 | 48.7 | % | 39.1 | % | ||||||

| Non-Investment Grade | 60,016 | 23.3 | % | 19.0 | % | |||||||

| Unrated | 72,234 | 28.0 | % | 41.9 | % | |||||||

| $ | 257,759 | 100.0 | % | 100.0 | % | |||||||

| Weighted-Average Lease Term - Cash Basis | As of 12/31/19 | As of 12/31/18 | ||

| 8.4 years | 8.9 years |

Rent Estimates for Current Assets

| Year | Base Rent (3) | Cash Base Rent (3) | Difference | |||||||||

| 2020 | $ | 279,385 | $ | 265,202 | $ | (14,183 | ) | |||||

| 2021 | 259,213 | 250,661 | (8,552 | ) | ||||||||

Footnotes

| (1) | Twelve months ended 12/31/2019 Base Rent recognized for consolidated properties owned as of 12/31/2019. |

| (2) | Credit ratings are based upon either tenant, guarantor or parent/ultimate parent. Historical comparison was not adjusted for subsequent tenant entity changes and multi-tenant was generally reflected as unrated. |

| (3) | Amounts assume (1) lease terms for non-cancellable periods only, (2) no new or renegotiated leases are entered into after 12/31/2019, and (3) no properties are sold or acquired after 12/31/2019. |

20

LEXINGTON REALTY TRUST

Other Revenue Data (Continued)

12/31/2019

($000)

Same-Store NOI (1)

| Twelve months ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| Total Cash Base Rent | $ | 214,081 | $ | 216,563 | ||||

| Tenant Reimbursements | 22,044 | 17,791 | ||||||

| Property Operating Expenses | (28,226 | ) | (22,924 | ) | ||||

| Same-Store NOI | $ | 207,899 | $ | 211,430 | ||||

| Change in Same-Store NOI (2) | (1.7 | )% | ||||||

| Same-Store Percent Leased (3) | As of 12/31/19 | As of 12/31/18 | ||||||

| 96.7 | % | 98.5 | % | |||||

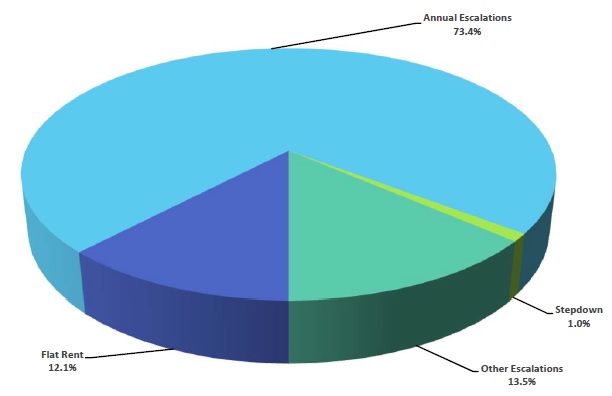

Lease Escalation Data (4)

Footnotes

| (1) | NOI is on a consolidated cash basis excluding properties acquired and sold in 2019 and 2018 and properties subject to mortgage loans in default at December 31, 2019. |

| See definitions of non-GAAP measures and reconciliations to applicable GAAP measures in this document. |

| (2) | Change in Same-Store NOI was breakeven excluding single-tenant property vacancies. |

| (3) | Excludes properties acquired or sold in 2019 and 2018 and properties subject to mortgage loans in default at December 31, 2019. |

| (4) | Based on twelve months consolidated Cash Base Rents for single-tenant leases (properties greater than 50% leased to a single tenant) owned as of December 31, 2019. Excludes parking operations and rents from prior tenants. |

21

LEXINGTON REALTY TRUST

Portfolio Detail By Asset Class

12/31/2019

($000, except square footage)

| Asset Class | YE 2017 (1) | YE 2018 (1)(2) | YE 2019 | |||||||||

| Industrial | ||||||||||||

| % of Cost (3) | 49.3 | % | 71.2 | % | 81.5 | % | ||||||

| % of ABR (4) | 44.3 | % | 65.4 | % | 75.5 | % | ||||||

| % Leased | 99.9 | % | 96.3 | % | 97.9 | % | ||||||

| Wtd. Avg. Lease Term (5) | 10.5 | 9.7 | 8.3 | |||||||||

| Mortgage Debt | $ | 193,529 | $ | 206,006 | $ | 109,939 | ||||||

| % Investment Grade (4) | 28.4 | % | 31.6 | % | 45.9 | % | ||||||

| Square Feet | 36,071,422 | 41,447,962 | 48,742,014 | |||||||||

| Office/Other | ||||||||||||

| % of Cost (3) | 50.7 | % | 28.8 | % | 18.5 | % | ||||||

| % of ABR (4)(6) | 55.7 | % | 34.6 | % | 24.5 | % | ||||||

| % Leased | 96.0 | % | 87.1 | % | 85.8 | % | ||||||

| Wtd. Avg. Lease Term (5) | 7.9 | 7.2 | 8.5 | |||||||||

| Mortgage Debt | $ | 503,539 | $ | 369,508 | $ | 283,933 | ||||||

| % Investment Grade (4) | 49.4 | % | 53.2 | % | 57.3 | % | ||||||

| Square Feet | 12,542,640 | 6,111,588 | 3,876,294 | |||||||||

| Construction in progress (7) | $ | 4,219 | $ | 1,840 | $ | 15,208 | ||||||

Footnotes

| (1) | Office and Other properties combined. |

| (2) | Pataskala, Ohio property reclassed to Industrial from Office/Other. |

| (3) | Based on gross book value of real estate assets; excludes held for sale assets. |

| (4) | Percentage of Base Rent, for consolidated properties owned as of each respective period. |

| (5) | Cash basis. |

| (6) | YE 2018 excludes the acceleration of below-market lease intangible accretion on one Kmart asset. |

| (7) | Includes development classified as real estate under construction on a consolidated basis. |

22

LEXINGTON REALTY TRUST

12/31/2019

As a Percent of Gross Book Value (1)

Portfolio Composition (2)

Footnotes

| (1) | Based on gross book value of real estate assets as of 12/31/2019. |

| (2) | Based on gross book value of real estate assets as of 12/31/2019, 12/31/2018 and 12/31/2017, as applicable and excludes held for sale assets. |

23

LEXINGTON REALTY TRUST

12/31/2019

($000)

The purpose of providing the following information is to enable readers to derive their own estimates of net asset value. This information is not intended to be an asset-by-asset or enterprise valuation.

| Consolidated properties twelve month net operating income (NOI) (1) | ||||

| Industrial | $ | 167,797 | ||

| Office/Other | 57,891 | |||

| Total Net Operating Income | $ | 225,688 | ||

| Lexington's share of non-consolidated twelve month NOI (1) | ||||

| NNN OFFICE JV | ||||

| Office | $ | 10,312 | ||

| OTHER JV | ||||

| Other | $ | 1,490 | ||

| Other income | ||||

| Advisory fees | $ | 3,918 | ||

| In service assets not fairly valued by capitalized NOI method (1) | ||||

| Wholly-owned assets acquired in 2019 | $ | 690,720 | ||

| Wholly-owned assets less than 70% leased | $ | 42,391 | ||

| Add other assets: | ||||

| Construction in progress | $ | 1,895 | ||

| Developable land | 12,995 | |||

| Development investment at cost incurred | 10,492 | |||

| Cash and cash equivalents | 122,666 | |||

| Restricted cash | 6,644 | |||

| Accounts receivable | 3,229 | |||

| Other assets | 11,708 | |||

| Total other assets | $ | 169,629 | ||

| Liabilities: | ||||

| Corporate level debt (face amount) | $ | 929,120 | ||

| Mortgages and notes payable (face amount) | 393,872 | |||

| Dividends payable | 32,432 | |||

| Accounts payable, accrued expenses and other liabilities | 51,340 | |||

| Preferred stock, at liquidation value | 96,770 | |||

| Lexington's share of non-consolidated mortgages (face amount) | 89,418 | |||

| Total deductions | $ | 1,592,952 | ||

| Common shares & OP units at 12/31/2019 | 257,956,216 |

Footnotes

| (1) | NOI for the existing property portfolio at December 31, 2019, excludes NOI related to assets undervalued by a capitalized NOI method and assets held for sale. Assets undervalued by a capitalized NOI method are identified generally by occupancies under 70% and assets acquired in 2019. For assets in this category an NOI capitalization approach is not appropriate, and accordingly, Lexington's net book value has been used. See definitions of non-GAAP measures and reconciliations to applicable GAAP measures in this document. |

24

LEXINGTON REALTY TRUST

Consolidated Portfolio Concentration

12/31/2019

| Markets (1) | Percent of Base Rent as of 12/31/19 (2) | |||||

| 1 | Houston, TX | 11.4 | % | |||

| 2 | Memphis, TN | 7.1 | % | |||

| 3 | New York, NY | 4.3 | % | |||

| 4 | Atlanta, GA | 4.1 | % | |||

| 5 | Detroit, MI | 4.0 | % | |||

| 6 | Nashville, TN | 3.8 | % | |||

| 7 | Dallas, TX | 3.5 | % | |||

| 8 | Philadelphia, PA | 2.9 | % | |||

| 9 | San Jose, CA | 2.6 | % | |||

| 10 | Jackson, MS | 2.4 | % | |||

| 11 | St. Louis, MO | 2.4 | % | |||

| 12 | Phoenix, AZ | 2.2 | % | |||

| 13 | Cincinnati, OH | 2.1 | % | |||

| 14 | Columbus, OH | 1.9 | % | |||

| 15 | Kansas City, MO | 1.7 | % | |||

| 16 | Champaign, IL | 1.6 | % | |||

| 17 | Charlotte, NC | 1.6 | % | |||

| 18 | Spartanburg, SC | 1.6 | % | |||

| 19 | Jackson, TN | 1.5 | % | |||

| 20 | Richmond, VA | 1.5 | % | |||

| Total Consolidated Portfolio Concentration (3) | 64.1 | % | ||||

| Footnotes | |

| (1) | Markets are based on a Core Based Statistical Area, which is the official term for a functional region based around an urban center of at least 10,000 people, based on standards published by the Office of Management and Budget (OMB) in 2000. These standards are used to replace the definitions of metropolitan areas that were defined in 1990. |

| (2) | Twelve months ended 12/31/2019 Base Rent recognized for consolidated properties owned as of 12/31/2019. |

| (3) | Total shown may differ from detailed amounts due to rounding. |

25

LEXINGTON REALTY TRUST

Portfolio Concentration - Industrial

12/31/2019

| Markets (1) | Percent of Base Rent as of 12/31/19 (2) | |||||

| 1 | Memphis, TN | 9.5 | % | |||

| 2 | Houston, TX | 7.4 | % | |||

| 3 | Detroit, MI | 5.3 | % | |||

| 4 | Atlanta, GA | 5.1 | % | |||

| 5 | Nashville, TN | 5.0 | % | |||

| 6 | Jackson, MS | 3.2 | % | |||

| 7 | St. Louis, MO | 3.2 | % | |||

| 8 | Cincinnati, OH | 2.7 | % | |||

| 9 | New York, NY | 2.6 | % | |||

| 10 | Dallas, TX | 2.6 | % | |||

| 11 | Columbus, OH | 2.5 | % | |||

| 12 | Champaign, IL | 2.2 | % | |||

| 13 | Spartanburg, SC | 2.1 | % | |||

| 14 | Jackson, TN | 2.0 | % | |||

| 15 | Richmond, VA | 2.0 | % | |||

| 16 | Winchester, VA | 2.0 | % | |||

| 17 | Greenville, SC | 1.9 | % | |||

| 18 | Chicago, IL | 1.9 | % | |||

| 19 | Indianapolis, IN | 1.8 | % | |||

| 20 | Shreveport, LA | 1.8 | % | |||

| Total Industrial Portfolio Concentration (3) | 66.7 | % | ||||

| Footnotes | |

| (1) | Markets are based on a Core Based Statistical Area, which is the official term for a functional region based around an urban center of at least 10,000 people, based on standards published by the Office of Management and Budget (OMB) in 2000. These standards are used to replace the definitions of metropolitan areas that were defined in 1990. |

| (2) | Twelve months ended 12/31/2019 Base Rent recognized for consolidated industrial properties owned as of 12/31/2019. |

| (3) | Total shown may differ from detailed amounts due to rounding. |

26

LEXINGTON REALTY TRUST

Portfolio Concentration - Office/Other

12/31/2019

| Markets (1) | Percent of Base Rent as of 12/31/19 (2) | |||||

| 1 | Houston, TX | 23.6 | % | |||

| 2 | San Jose, CA | 10.5 | % | |||

| 3 | Philadelphia, PA | 10.1 | % | |||

| 4 | New York, NY | 9.3 | % | |||

| 5 | Charlotte, NC | 6.5 | % | |||

| 6 | Dallas, TX | 6.3 | % | |||

| 7 | Washington, DC | 4.9 | % | |||

| 8 | Kansas City, MO | 4.8 | % | |||

| 9 | Phoenix, AZ | 3.9 | % | |||

| 10 | Miami, FL | 3.5 | % | |||

| 11 | Sarasota, FL | 3.0 | % | |||

| 12 | Baton Rouge, LA | 1.8 | % | |||

| 13 | McAllen, TX | 1.6 | % | |||

| 14 | Augusta, ME | 1.5 | % | |||

| 15 | Orlando, FL | 1.4 | % | |||

| 16 | Knoxville, TN | 1.4 | % | |||

| 17 | Atlanta, GA | 1.3 | % | |||

| 18 | Baltimore, MD | 1.0 | % | |||

| 19 | Florence, SC | 0.9 | % | |||

| 20 | Tucson, AZ | 0.9 | % | |||

| Total Office/Other Portfolio Concentration (3) | 98.3 | % | ||||

| Footnotes | |

| (1) | Markets are based on a Core Based Statistical Area, which is the official term for a functional region based around an urban center of at least 10,000 people, based on standards published by the Office of Management and Budget (OMB) in 2000. These standards are used to replace the definitions of metropolitan areas that were defined in 1990. |

| (2) | Twelve months ended 12/31/2019 Base Rent recognized for consolidated office/other properties owned as of 12/31/2019. |

| (3) | Total shown may differ from detailed amounts due to rounding. |

27

LEXINGTON REALTY TRUST

Tenant Industry Diversification - Industrial Assets (1)

12/31/2019

Footnotes

| (1) | Twelve months ended 12/31/2019 Base Rent recognized for consolidated properties owned as of 12/31/2019. |

28

LEXINGTON REALTY TRUST

Tenant Industry Diversification - Office/Other Assets (1)

12/31/2019

Footnotes

| (1) | Twelve months ended 12/31/2019 Base Rent recognized for consolidated properties owned as of 12/31/2019. |

29

LEXINGTON REALTY TRUST

12/31/2019

Top 15 Tenants

| Tenants (1) | Property Type | Lease Expirations | Number of Leases | Sq. Ft. Leased | Sq.

Ft. Leased as a Percent of Consolidated Portfolio (2)(3) | Base Rent as of 12/31/2019 ($000) | Percent of Base Rent as of 12/31/2019 ($000) (2)(4) | |||||||||||||||

| Dow | Office | 2036 | 1 | 664,100 | 1.3 | % | $ | 14,850 | 5.9 | % | ||||||||||||

| Nissan | Industrial | 2027 | 2 | 2,971,000 | 5.8 | % | 12,760 | 5.0 | % | |||||||||||||

| Dana | Industrial | 2021-2026 | 7 | 2,053,359 | 4.0 | % | 9,941 | 3.9 | % | |||||||||||||

| Undisclosed (5) | Industrial | 2031-2035 | 3 | 1,090,383 | 2.1 | % | 7,139 | 2.8 | % | |||||||||||||

| Watco | Industrial | 2038 | 1 | 132,449 | 0.3 | % | 6,773 | 2.7 | % | |||||||||||||

| Xerox | Office | 2023 | 1 | 202,000 | 0.4 | % | 6,642 | 2.6 | % | |||||||||||||

| Morgan Lewis (6) | Office | 2024 | 1 | 289,432 | 0.6 | % | 5,655 | 2.2 | % | |||||||||||||

| Amazon | Industrial | 2026-2030 | 3 | 2,515,492 | 4.9 | % | 5,637 | 2.2 | % | |||||||||||||

| Undisclosed (5) | Industrial | 2023-2027 | 3 | 2,132,290 | 4.2 | % | 5,527 | 2.2 | % | |||||||||||||

| FedEx | Industrial | 2023 & 2028 | 2 | 292,021 | 0.6 | % | 5,479 | 2.2 | % | |||||||||||||

| Hamilton Beach | Industrial | 2021 & 2026 | 2 | 1,645,436 | 3.2 | % | 4,948 | 2.0 | % | |||||||||||||

| Asics | Industrial | 2030 | 1 | 855,878 | 1.7 | % | 4,388 | 1.7 | % | |||||||||||||

| Spitzer | Industrial | 2035 | 2 | 449,895 | 0.9 | % | 4,344 | 1.7 | % | |||||||||||||

| Vista Outdoor | Industrial | 2034 | 1 | 813,126 | 1.6 | % | 4,195 | 1.7 | % | |||||||||||||

| Wells Fargo | Office | 2024 | 2 | 338,301 | 0.7 | % | 4,101 | 1.6 | % | |||||||||||||

| 32 | 16,445,162 | 32.2 | % | $ | 102,379 | 40.5 | % | |||||||||||||||

| Footnotes | |

| (1) | Tenant, guarantor or parent. |

| (2) | Total shown may differ from detailed amounts due to rounding. |

| (3) | Excludes vacant square feet. |

| (4) | Twelve months ended 12/31/2019 Base Rent recognized for consolidated properties owned as of 12/31/2019, excluding rent from prior tenants. |

| (5) | Lease restricts certain disclosures. |

| (6) | Includes parking operations. |

30

LEXINGTON REALTY TRUST

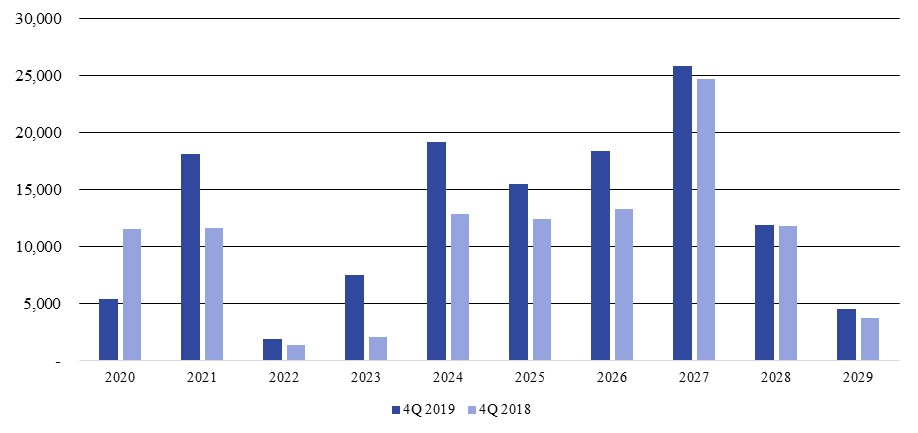

Lease Rollover Schedule - Consolidated Industrial Properties

12/31/2019

($000)

| Year | Number of Leases Expiring | Base Rent as of 12/31/2019 | Percent of Base Rent as of 12/31/2019 | Percent of Base Rent as of 12/31/2018 | ||||||||||||

| 2020 | 4 | $ | 5,363 | 2.8 | % | 6.2 | % | |||||||||

| 2021 | 13 | 18,136 | 9.4 | % | 6.3 | % | ||||||||||

| 2022 | 2 | 1,907 | 1.0 | % | 0.7 | % | ||||||||||

| 2023 | 8 | 7,468 | 3.9 | % | 1.1 | % | ||||||||||

| 2024 | 16 | 19,168 | 9.9 | % | 7.0 | % | ||||||||||

| 2025 | 13 | 15,476 | 8.0 | % | 6.7 | % | ||||||||||

| 2026 | 11 | 18,392 | 9.5 | % | 7.2 | % | ||||||||||

| 2027 | 9 | 25,835 | 13.4 | % | 13.4 | % | ||||||||||

| 2028 | 4 | 11,855 | 6.2 | % | 6.4 | % | ||||||||||

| 2029 | 3 | 4,507 | 2.3 | % | 2.0 | % | ||||||||||

| Thereafter | 25 | 64,634 | 33.5 | % | 39.6 | % | ||||||||||

| Total (1) | 108 | $ | 192,741 | 100.0 | % | |||||||||||

Footnotes

| (1) | Total shown may differ from detailed amounts due to rounding. |

31

LEXINGTON REALTY TRUST

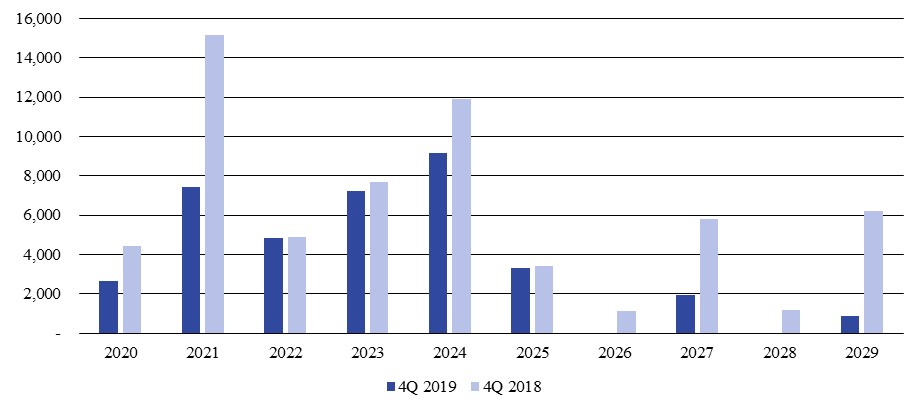

Lease Rollover Schedule - Consolidated Office/Other Properties

12/31/2019

($000)

| Year | Number of Leases Expiring | Base Rent as of 12/31/2019 | Percent of Base Rent as of 12/31/2019 | Percent of Base Rent as of 12/31/2018 | ||||||||||||

| 2020 | 30 | $ | 2,643 | 4.3 | % | 4.8 | % | |||||||||

| 2021 | 9 | 7,451 | 12.1 | % | 16.6 | % | ||||||||||

| 2022 | 3 | 4,837 | 7.9 | % | 5.3 | % | ||||||||||

| 2023 | 3 | 7,201 | 11.7 | % | 8.4 | % | ||||||||||

| 2024 | 5 | 9,180 | 14.9 | % | 13.0 | % | ||||||||||

| 2025 | 5 | 3,320 | 5.4 | % | 3.7 | % | ||||||||||

| 2026 | 0 | - | 0.0 | % | 1.2 | % | ||||||||||

| 2027 | 3 | 1,956 | 3.2 | % | 6.4 | % | ||||||||||

| 2028 | 0 | - | 0.0 | % | 1.3 | % | ||||||||||

| 2029 | 1 | 881 | 1.4 | % | 6.8 | % | ||||||||||

| Thereafter | 8 | 24,053 | 39.1 | % | 21.0 | % | ||||||||||

| Total (1) | 67 | $ | 61,522 | 100.0 | % | |||||||||||

Footnotes

| (1) | Total shown may differ from detailed amounts due to rounding and does not include parking operations. |

32

LEXINGTON REALTY TRUST

Property Leases and Vacancies - Consolidated Portfolio - 12/31/2019

| Year of Lease Expiration | Date of Lease Expiration | Property Location | City | State | Note | Primary Tenant, Guarantor, or Parent | Sq. Ft. Leased or Available (1) | Base Rent as of 12/31/2019 ($000) (2) | Cash Base Rent as of 12/31/2019($000) (2) | 12/31/2019 Debt Balance ($000) | Debt Maturity | |||||||||||||||||||||

| INDUSTRIAL PROPERTIES | ||||||||||||||||||||||||||||||||

| Single-tenant | ||||||||||||||||||||||||||||||||

| 2020 | 6/30/2020 | 1650-1654 Williams Rd. | Columbus | OH | -- | ODW Logistics | 772,450 | 1,347 | 1,347 | - | - | |||||||||||||||||||||

| 12/19/2020 | 1901 Ragu Dr. | Owensboro | KY | 5 | Unilever | 443,380 | 1,493 | 1,288 | - | - | ||||||||||||||||||||||

| 12/31/2020 | 2203 Sherrill Dr. | Statesville | NC | -- | Geodis America | 639,800 | 2,493 | 2,537 | - | - | ||||||||||||||||||||||

| 2021 | 1/31/2021 | 101 Michelin Dr. | Laurens | SC | -- | Michelin | 1,164,000 | 3,745 | 3,745 | - | - | |||||||||||||||||||||

| 3/31/2021 | 2455 Premier Row | Orlando | FL | -- | Walgreen Co. | 205,016 | 786 | 508 | - | - | ||||||||||||||||||||||

| 5/31/2021 | 291 Park Center Dr. | Winchester | VA | -- | Kraft Heinz | 344,700 | 1,422 | 1,451 | - | - | ||||||||||||||||||||||

| 6/30/2021 | 11624 S. Distribution Cv. | Olive Branch | MS | -- | Hamilton Beach | 1,170,218 | 3,789 | 3,189 | - | - | ||||||||||||||||||||||

| 9/30/2021 | 3820 Micro Dr. | Millington | TN | -- | Ingram Micro | 701,819 | 1,812 | 1,874 | - | - | ||||||||||||||||||||||

| 10/25/2021 | 6938 Elm Valley Dr. | Kalamazoo | MI | -- | Dana | 150,945 | 1,747 | 2,027 | - | - | ||||||||||||||||||||||

| 11/30/2021 | 2880 Kenny Biggs Rd. | Lumberton | NC | -- | Quickie Manufacturing | 423,280 | 1,356 | 1,459 | - | - | ||||||||||||||||||||||

| 12/31/2021 | 191 Arrowhead Dr. | Hebron | OH | -- | Owens Corning | 250,410 | 573 | 573 | - | - | ||||||||||||||||||||||

| 200 Arrowhead Dr. | Hebron | OH | -- | Owens Corning | 400,522 | 916 | 916 | - | - | |||||||||||||||||||||||

| 3686 South Central Ave. | Rockford | IL | -- | Pierce Packaging | 93,000 | 321 | 321 | - | - | |||||||||||||||||||||||

| 2022 | 3/31/2022 | 5417 Campus Dr. | Shreveport | LA | -- | Tire Rack | 257,849 | 1,343 | 1,403 | - | - | |||||||||||||||||||||

| 8/31/2022 | 50 Tyger River Dr. | Duncan | SC | -- | Plastic Omnium | 221,833 | 564 | 336 | - | - | ||||||||||||||||||||||

| 2023 | 2/28/2023 | 3102 Queen Palm Dr. | Tampa | FL | 8 | RC Moore | 229,605 | 1,081 | 1,303 | - | - | |||||||||||||||||||||

| 7670 Hacks Cross Rd. | Olive Branch | MS | -- | MAHLE Industries | 268,104 | 906 | 902 | - | - | |||||||||||||||||||||||

| 5/31/2023 | 6495 Polk Ln. | Olive Branch | MS | 13 | Undisclosed | 151,691 | 344 | 330 | - | - | ||||||||||||||||||||||

| 8/31/2023 | 10535 Red Bluff Rd. | Pasadena | TX | -- | Unis | 257,835 | 1,231 | 1,199 | - | - | ||||||||||||||||||||||

| 3737 Duncanville Rd. | Dallas | TX | -- | Owens Corning | 510,440 | 1,175 | 1,134 | - | - | |||||||||||||||||||||||

| 10/31/2023 | 493 Westridge Pkwy. | McDonough | GA | -- | Carlstar | 676,000 | 1,777 | 1,694 | - | - | ||||||||||||||||||||||

| 12/31/2023 | 120 Southeast Pkwy. Dr. | Franklin | TN | -- | United Technologies | 289,330 | 735 | 735 | - | - | ||||||||||||||||||||||

| 675 Gateway Blvd. | Monroe | OH | -- | Blue Buffalo | 143,664 | 219 | 209 | - | - | |||||||||||||||||||||||

| 2024 | 1/31/2024 | 1285 W. State Road 32 | Lebanon | IN | -- | Continental Tire | 741,880 | 2,286 | 2,383 | - | - | |||||||||||||||||||||

| 6495 Polk Ln. | Olive Branch | MS | 13 | Undisclosed | 118,211 | 291 | 276 | - | - | |||||||||||||||||||||||

| 70 Tyger River Dr. | Duncan | SC | -- | BMW | 408,000 | 1,367 | 1,310 | - | - | |||||||||||||||||||||||

| 33 |

LEXINGTON REALTY TRUST

Property Leases and Vacancies - Consolidated Portfolio - 12/31/2019

| Year of Lease Expiration | Date of Lease Expiration | Property Location | City | State | Note | Primary Tenant, Guarantor, or Parent | Sq. Ft. Leased or Available (1) | Base Rent as of 12/31/2019 ($000) (2) | Cash Base Rent as of 12/31/2019($000) (2) | 12/31/2019 Debt Balance ($000) | Debt Maturity | |||||||||||||||||||||

| INDUSTRIAL PROPERTIES | ||||||||||||||||||||||||||||||||

| 2024 | 1/31/2024 | 231 Apple Valley Road | Duncan | SC | 13 | Undisclosed | 120,680 | 141 | 133 | - | - | |||||||||||||||||||||

| 3/31/2024 | 1520 Lauderdale Memorial Hwy. | Cleveland | TN | -- | General Electric | 851,370 | 2,658 | 2,648 | - | - | ||||||||||||||||||||||

| 4/30/2024 | 113 Wells St. | North Berwick | ME | -- | United Technologies | 993,685 | 1,798 | 1,739 | - | - | ||||||||||||||||||||||

| 11555 Silo Dr. | Olive Branch | MS | -- | Olam Cotton | 927,742 | 1,681 | 1,258 | - | - | |||||||||||||||||||||||

| 5/31/2024 | 901 East Bingen Point Way | Bingen | WA | -- | Boeing | 124,539 | 2,636 | 2,637 | - | - | ||||||||||||||||||||||

| 7225 Goodson Rd. | Union City | GA | -- | Interface Americas | 370,000 | 745 | 698 | - | - | |||||||||||||||||||||||

| 7/31/2024 | 5795 North Blackstock Road | Spartanburg | SC | -- | Wal-Mart | 341,660 | 1,672 | 1,623 | - | - | ||||||||||||||||||||||

| 231 Apple Valley Road | Duncan | SC | 13 | Undisclosed | 75,320 | 88 | 88 | - | - | |||||||||||||||||||||||

| 9/30/2024 | 1621 Veterans Memorial Pkwy. E | Lafayette | IN | -- | Caterpillar | 309,400 | 1,215 | 1,204 | - | - | ||||||||||||||||||||||

| 10/31/2024 | 43955 Plymouth Oaks Blvd. | Plymouth | MI | -- | Tower Automotive | 311,612 | 1,591 | 1,542 | - | - | ||||||||||||||||||||||

| 2115 East Belt Line Rd. | Carrollton | TX | -- | L.E. Klein | 58,202 | 229 | 153 | - | - | |||||||||||||||||||||||

| 12/31/2024 | 749 Southrock Dr. | Rockford | IL | -- | Jacobson Warehouse | 150,000 | 638 | 600 | - | - | ||||||||||||||||||||||

| 2025 | 4/30/2025 | 235 Apple Valley Road | Duncan | SC | 13 | Undisclosed | 177,320 | 219 | 205 | - | - | |||||||||||||||||||||

| 5/31/2025 | 7875 White Road SW | Austell | GA | -- | Mars Wrigley | 604,852 | 1,407 | 1,853 | - | - | ||||||||||||||||||||||

| 6/30/2025 | 10000 Business Blvd. | Dry Ridge | KY | -- | Dana | 336,350 | 1,346 | 1,346 | - | - | ||||||||||||||||||||||

| 4010 Airpark Dr. | Owensboro | KY | -- | Metalsa / Dana | 211,598 | 1,208 | 1,208 | - | - | |||||||||||||||||||||||

| 730 North Black Branch Rd. | Elizabethtown | KY | -- | Metalsa / Dana | 167,770 | 537 | 537 | - | - | |||||||||||||||||||||||

| 750 North Black Branch Rd. | Elizabethtown | KY | -- | Metalsa / Dana | 539,592 | 2,838 | 2,838 | - | - | |||||||||||||||||||||||

| 301 Bill Bryan Blvd. | Hopkinsville | KY | -- | Metalsa / Dana | 424,904 | 1,687 | 1,687 | - | - | |||||||||||||||||||||||

| 7/14/2025 | 590 Ecology Ln. | Chester | SC | -- | Boral Limited | 420,597 | 1,798 | 2,391 | 5,763 | 08/2025 | ||||||||||||||||||||||

| 7/31/2025 | 7005 Cochran Rd. | Glenwillow | OH | -- | Royal Appliance | 458,000 | 2,061 | 2,101 | - | - | ||||||||||||||||||||||

| 5352 Performance Way | Whitestown | IN | -- | LaCrosse | 380,000 | 1,250 | 1,091 | - | - | |||||||||||||||||||||||

| 12/31/2025 | 1700 47th Ave North | Minneapolis | MN | -- | Owens Corning | 18,620 | 550 | 550 | - | - | ||||||||||||||||||||||

| 2026 | 3/30/2026 | 121 Technology Dr. | Durham | NH | 12 | Heidelberg | 500,500 | 2,537 | 2,479 | - | - | |||||||||||||||||||||

| 3/31/2026 | 633 Garrett Pkwy. | Lewisburg | TN | -- | Calsonic Kansei | 310,000 | 1,288 | 1,286 | - | - | ||||||||||||||||||||||

| 4/30/2026 | 16811 W. Commerce Dr. | Goodyear | AZ | -- | Blue Buffalo | 540,349 | 2,444 | 1,161 | - | - | ||||||||||||||||||||||

| 6/30/2026 | 351 Chamber Dr. | Chillicothe | OH | 16 | Kitchen Collection | 475,218 | 1,159 | 1,164 | - | - | ||||||||||||||||||||||

| 34 |

LEXINGTON REALTY TRUST

Property Leases and Vacancies - Consolidated Portfolio - 12/31/2019

| Year of Lease Expiration | Date of Lease Expiration | Property Location | City | State | Note | Primary Tenant, Guarantor, or Parent | Sq. Ft. Leased or Available (1) | Base Rent as of 12/31/2019 ($000) (2) | Cash Base Rent as of 12/31/2019($000) (2) | 12/31/2019 Debt Balance ($000) | Debt Maturity | |||||||||||||||||||||

| INDUSTRIAL PROPERTIES | ||||||||||||||||||||||||||||||||

| 2026 | 9/30/2026 | 900 Industrial Blvd. | Crossville | TN | -- | Dana | 222,200 | 578 | 578 | - | - | |||||||||||||||||||||

| 3931 Lakeview Corporate Dr. | Edwardsville | IL | -- | Amazon.com | 769,500 | 2,696 | 2,588 | - | - | |||||||||||||||||||||||

| 9494 W. Buckeye Rd. | Tolleson | AZ | -- | CHEP | 186,336 | 236 | 218 | - | - | |||||||||||||||||||||||

| 10/31/2026 | 10345 Philipp Pkwy. | Streetsboro | OH | -- | L'Oreal USA | 649,250 | 2,725 | 2,788 | - | - | ||||||||||||||||||||||

| 5001 Greenwood Rd. | Shreveport | LA | -- | Libbey | 646,000 | 2,165 | 2,229 | - | - | |||||||||||||||||||||||

| 11/30/2026 | 250 Rittenhouse Cir. | Bristol | PA | -- | Estée Lauder | 241,977 | 1,146 | 1,182 | - | - | ||||||||||||||||||||||

| 736 Addison Rd. | Erwin | NY | -- | Corning | 408,000 | 1,418 | 1,425 | - | - | |||||||||||||||||||||||

| 2027 | 1/31/2027 | 27200 West 157th St. | New Century | KS | -- | Amazon.com | 446,500 | 1,240 | 1,090 | - | - | |||||||||||||||||||||

| 2/28/2027 | 554 Nissan Pkwy. | Canton | MS | -- | Nissan | 1,466,000 | 6,200 | 6,037 | - | - | ||||||||||||||||||||||

| 4/30/2027 | 16407 Applewhite Rd. | San Antonio | TX | 13 | Undisclosed | 849,275 | 2,994 | 2,822 | - | - | ||||||||||||||||||||||

| 200 Sam Griffin Rd. | Smyrna | TN | -- | Nissan | 1,505,000 | 6,560 | 6,325 | - | - | |||||||||||||||||||||||

| 6/30/2027 | 1501 Nolan Ryan Expy. | Arlington | TX | -- | Arrow Electronics | 74,739 | 406 | 405 | - | - | ||||||||||||||||||||||

| 8/31/2027 | 600 Gateway Blvd. | Monroe | OH | -- | Hayneedle | 994,013 | 1,227 | 1,004 | - | - | ||||||||||||||||||||||

| 9/30/2027 | 1550 Hwy 302 | Byhalia | MS | -- | McCormick | 615,600 | 2,451 | 2,416 | - | - | ||||||||||||||||||||||

| 10/31/2027 | 201 James Lawrence Rd. | Jackson | TN | -- | Kellogg | 1,062,055 | 3,944 | 3,753 | - | - | ||||||||||||||||||||||

| 12/31/2027 | 10590 Hamilton Ave. | Cincinnati | OH | -- | Hillman Group | 264,598 | 813 | 813 | - | - | ||||||||||||||||||||||

| 2028 | 1/31/2028 | 490 Westridge Pkwy. | McDonough | GA | -- | Georgia-Pacific | 1,121,120 | 3,737 | 3,458 | - | - | |||||||||||||||||||||

| 3/31/2028 | 29-01-Borden Ave./29-10 Hunters Point Ave. | Long Island City | NY | -- | FedEx | 140,330 | 5,135 | 5,128 | 36,449 | 03/2028 | ||||||||||||||||||||||

| 8/31/2028 | 1420 Greenwood Rd. | McDonough | GA | -- | United States Cold Storage | 296,972 | 2,170 | 2,160 | - | - | ||||||||||||||||||||||

| 9/30/2028 | 904 Industrial Rd. | Marshall | MI | -- | Tenneco | 246,508 | 813 | 743 | - | - | ||||||||||||||||||||||

| 2029 | 7/31/2029 | 8500 Nail Rd. | Olive Branch | MS | -- | Sephora | 716,080 | 2,751 | 2,603 | - | - | |||||||||||||||||||||

| 9/30/2029 | 6255 East Minooka Road | Minooka | IL | -- | Kellogg | 1,034,200 | 16 | 14 | - | - | ||||||||||||||||||||||

| 11/24/2029 | 318 Pappy Dunn Blvd. | Anniston | AL | -- | IAC Group | 276,782 | 1,740 | 1,671 | - | - | ||||||||||||||||||||||

| 2030 | 3/31/2030 | 549 Wingo Rd. | Byhalia | MS | -- | Asics | 855,878 | 4,388 | 4,174 | - | - | |||||||||||||||||||||

| 5/31/2030 | 359 Gateway Dr. | Lavonia | GA | -- | TI Automotive | 133,221 | 799 | 997 | - | - | ||||||||||||||||||||||

| 4015 Lakeview Corporate Dr. | Edwardsville | IL | -- | Spectrum | 1,017,780 | 3,460 | 2,739 | - | - | |||||||||||||||||||||||

| 6/30/2030 | 2601 Bermuda Hundred Rd. | Chester | VA | 14 | Philip Morris | 1,034,470 | 3,851 | 3,807 | - | - | ||||||||||||||||||||||

| 35 |

LEXINGTON REALTY TRUST

Property Leases and Vacancies - Consolidated Portfolio - 12/31/2019

| Year of Lease Expiration | Date of Lease Expiration | Property Location | City | State | Note | Primary Tenant, Guarantor, or Parent | Sq. Ft. Leased or Available (1) | Base Rent as of 12/31/2019 ($000) (2) | Cash Base Rent as of 12/31/2019 ($000) (2) | 12/31/2019 Debt Balance ($000) | Debt Maturity | |||||||||||||||||||||

| INDUSTRIAL PROPERTIES | ||||||||||||||||||||||||||||||||

| 2030 | 6/30/2030 | 700 Gateway Blvd. | Monroe | OH | -- | Amazon.com | 1,299,492 | 1,701 | 1,535 | - | - | |||||||||||||||||||||

| 9/30/2030 | 255 143rd Ave. | Goodyear | AZ | 13 | Undisclosed | 801,424 | 389 | 351 | 41,877 | 08/2031 | ||||||||||||||||||||||

| 2031 | 10/31/2031 | 1020 W. Airport Rd. | Romeoville | IL | -- | ARYZTA | 188,166 | 3,640 | 3,463 | - | - | |||||||||||||||||||||

| 12/18/2031 | 80 Tyson Dr. | Winchester | VA | 13 | Undisclosed | 400,400 | 2,368 | 2,109 | - | - | ||||||||||||||||||||||