Form 485BPOS DELAWARE GROUP FOUNDATIO

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE

COMMISSION

WASHINGTON, D.C. 20549

FORM N-1A

File No. 333-38801

File

No. 811-08457

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | /X/ | |

| Pre-Effective Amendment No. _______ | / / | |

| Post-Effective Amendment No. 48 | /X/ | |

| and/or | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | /X/ | |

| Amendment No. 48 |

(Check appropriate box or boxes)

| DELAWARE GROUP FOUNDATION FUNDS |

| (Exact Name of Registrant as Specified in Charter) |

| 2005 Market Street, Philadelphia, Pennsylvania | 19103-7094 | ||

| (Address of Principal Executive Offices) | (Zip Code) | ||

| Registrant’s Telephone Number, including Area Code: | (800) 523-1918 |

| David F. Connor, Esq., 2005 Market Street, Philadelphia, PA 19103-7094 |

| (Name and Address of Agent for Service) |

| Approximate Date of Proposed Public Offering: | July 30, 2018 |

It is proposed that this filing will become effective (check appropriate box):

| /X/ | immediately upon filing pursuant to paragraph (b) | ||||

| / / | on (date) pursuant to paragraph (b) | ||||

| / / | 60 days after filing pursuant to paragraph (a)(1) | ||||

| / / | on (date) pursuant to paragraph (a)(1) | ||||

| / / | 75 days after filing pursuant to paragraph (a)(2) | ||||

| / / | on (date) pursuant to paragraph (a)(2) of Rule 485. | ||||

| If appropriate, check the following box: | |

| / / | this post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

--- C O N T E N T S ---

This Post-Effective Amendment No. 48 to Registration File No. 333-38801 includes the following:

| 1. | Facing Page | ||

| 2. | Contents Page | ||

| 3. | Part A – Prospectus | ||

| 4. | Part B – Statement of Additional Information | ||

| 5. | Part C – Other Information | ||

| 6. | Signatures | ||

| 7. | Exhibits | ||

Prospectus

Delaware Foundation® Moderate Allocation Fund

Multi-asset mutual fund

|

Nasdaq ticker symbols | |

|

Class A |

DFBAX |

|

Class C |

DFBCX |

|

Class R |

DFBRX |

|

Institutional Class |

DFFIX |

July 30, 2018

The US Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this Prospectus.

Any representation to the contrary is a criminal offense.

Get shareholder reports and prospectuses online instead of in the mail.

Visit delawarefunds.com/edelivery.

Table of contents

|

Fund summary

| |

|

Delaware Foundation® Moderate Allocation Fund

| |

|

How we manage the Fund

| |

|

Our principal investment strategies

| |

|

The securities in which the Fund typically invests

| |

|

Other investment strategies

| |

|

The risks of investing in the Fund

| |

|

Disclosure of portfolio holdings information

| |

|

Who manages the Fund

| |

|

Investment manager and sub-advisor

| |

|

Portfolio managers

| |

|

Manager of managers structure

| |

|

Who’s who

| |

|

About your account

| |

|

Investing in the Fund

| |

|

Choosing a share class

| |

|

Dealer compensation

| |

|

Payments to intermediaries

| |

|

How to reduce your sales charge

| |

|

Buying Class A shares at net asset value

| |

|

Waivers of contingent deferred sales charges

| |

|

How to buy shares

| |

|

Calculating share price

| |

|

Fair valuation

| |

|

Retirement plans

| |

|

Document delivery

| |

|

Inactive accounts

| |

|

How to redeem shares

| |

|

Low balance accounts

| |

|

Investor services

| |

|

Frequent trading of Fund shares (market timing and disruptive trading)

| |

|

Dividends, distributions, and taxes

| |

|

Certain management considerations

| |

|

Financial highlights

| |

|

Additional information

|

Fund summary

Delaware Foundation® Moderate Allocation Fund

Effective as of the close of business on July 27, 2018, Delaware Foundation Conservative Allocation Fund merged into Delaware Foundation Moderate Allocation Fund.

What is the Fund’s investment objective?

Delaware Foundation Moderate Allocation Fund seeks capital appreciation with current income as a secondary objective.

What are the Fund’s fees and expenses?

The table below describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales-charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in Delaware Funds® by Macquarie. More information about these and other discounts is available from your financial intermediary, in the Fund’s Prospectus under the section entitled “About your account,” and in the Fund’s statement of additional information (SAI) under the section entitled “Purchasing Shares.”

Shareholder fees (fees paid directly from your investment)

Class |

A | C | R | Inst. | ||||||||

Maximum sales charge (load) imposed on purchases as a percentage of offering price

|

5.75% | none | none | none | ||||||||

Maximum contingent deferred sales charge (load) as a percentage of original purchase price or redemption price, whichever is lower

|

none | 1.00% | 1 |

none | none | |||||||

Annual fund operating expenses (expenses that you pay each year as a percentage of the value of your investment)

Class |

A | C | R | Inst. | ||||||||

Management fees

|

0.65% | 0.65% | 0.65% | 0.65% | ||||||||

Distribution and service (12b-1) fees

|

0.24% | 1.00% | 0.50% | none | ||||||||

Other expenses2

|

0.28% | 0.28% | 0.28% | 0.28% | ||||||||

Total annual fund operating expenses

|

1.17% | 1.93% | 1.43% | 0.93% | ||||||||

Fee waivers and expense reimbursements

|

(0.03%) | 3 |

(0.03%) | 3 |

(0.03%) | 3 |

(0.03%) | 3 |

||||

Total annual fund operating expenses after fee waivers and expense reimbursements

|

1.14% | 1.90% | 1.40% | 0.90% | ||||||||

1 |

Class C shares redeemed within one year of purchase are subject to a 1.00% contingent deferred sales charge (CDSC). |

2 |

“Other expenses” have been restated to reflect future lower operating expenses. |

3 |

The Fund’s investment manager, Delaware Management Company (Manager), has contractually agreed to waive all or a portion of its investment advisory fees and/or pay/reimburse expenses (excluding any 12b-1 fees, taxes, interest, acquired fund fees and expenses, short sale dividend and interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) in order to prevent total annual fund operating expenses from exceeding 0.90% of the Fund’s average daily net assets from July 27, 2018 through July 29, 2019. These waivers and reimbursements may only be terminated by agreement of the Manager and the Fund. Additionally, the Fund’s Class A shares are subject to a blended 12b-1 fee of 0.10% on all shares acquired prior to June 1, 1992, and 0.25% on all shares acquired on or after June 1, 1992. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. In addition, the example shows expenses for Class C shares, assuming those shares were not redeemed at the end of those periods. The example also assumes that your investment has a 5% return each year and reflects the Manager’s expense waivers and reimbursements for the 1-year contractual period and the total operating expenses without waivers for years 2 through 10. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Class |

A | (if not | C | R | Inst. | ||||||||||

1 year

|

$685 | $193 | $293 | $143 | $92 | ||||||||||

3 years

|

$922 | $603 | $603 | $449 | $293 | ||||||||||

5 years

|

$1,179 | $1,039 | $1,039 | $779 | $512 | ||||||||||

10 years

|

$1,911 | $2,251 | $2,251 | $1,710 | $1,140 | ||||||||||

1

Fund summary

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 93% of the average value of its portfolio.

What are the Fund’s principal investment strategies?

The Fund seeks to achieve its objectives by investing in a combination of underlying securities representing a variety of asset classes and investment styles. The Manager uses an active allocation approach when selecting investments for the Fund. In striving to meet its objectives, the Fund will typically target about 60% of its net assets in equity securities and about 40% of its net assets in fixed income securities. Allocations for the Fund may vary within the ranges shown in the table below. The Fund may invest 10% to 60% of net assets in foreign securities, and up to 15% of net assets in emerging market securities. Following are the strategic policy weights for the Fund’s net assets, as they may be invested in broad and narrow asset classes, and various investment styles, and the permitted range of variation around those weights.

Equity asset class: 60% policy weight (40-70% range)

What are the principal risks of investing in the Fund?

Investing in any mutual fund involves the risk that you may lose part or all of the money you invest. Over time, the value of your investment in the Fund will increase and decrease according to changes in the value of the securities in the Fund’s portfolio. The Fund’s principal risks include:

Market risk — The risk that all or a majority of the securities in a certain market — such as the stock or bond market — will decline in value because of factors such as adverse political or economic conditions, future expectations, investor confidence, or heavy institutional selling.

Company size risk — The risk that investments in small- and/or medium-sized companies may be more volatile than those of larger companies because of limited financial resources or dependence on narrow product lines.

2

Foreign risk — The risk that foreign securities (particularly in emerging markets) may be adversely affected by political instability, changes in currency exchange rates, inefficient markets and higher transaction costs, foreign economic conditions, the imposition of economic or trade sanctions, or inadequate or different regulatory and accounting standards.

Fixed income risk — The risk that bonds may decrease in value if interest rates increase; an issuer may not be able to make principal and interest payments when due; a bond may be prepaid prior to maturity; and, in the case of high yield bonds (“junk bonds”), such bonds may be subject to an increased risk of default, a more limited secondary market than investment grade bonds, and greater price volatility. Interest rate changes are influenced by a number of factors, such as government policy, monetary policy, inflation expectations, and the supply and demand of bonds. Bonds and other fixed income securities with longer maturities or duration generally are more sensitive to interest rate changes. A fund may be subject to a greater risk of rising interest rates due to the current period of historically low interest rates.

Forward foreign currency risk — The use of forward foreign currency contracts may substantially change a fund’s exposure to currency exchange rates and could result in losses to a fund if currencies do not perform as the portfolio manager expects. The use of these investments as a hedging technique to reduce a fund’s exposure to currency risks may also reduce its ability to benefit from favorable changes in currency exchange rates.

Real estate industry risk — This risk includes, among others: possible declines in the value of real estate; risks related to general and local economic conditions; possible lack of availability of mortgage funds; overbuilding; extended vacancies of properties; increases in competition, property taxes, and operating expenses; changes in zoning laws; costs resulting from the cleanup of, and liability to third parties resulting from, environmental problems; casualty for condemnation losses; uninsured damages from floods, earthquakes, or other natural disasters; limitations on and variations in rents; and changes in interest rates.

Derivatives risk — Derivatives contracts, such as futures, forward foreign currency contracts, options, and swaps, may involve additional expenses (such as the payment of premiums) and are subject to significant loss if a security, index, reference rate, or other asset or market factor to which a derivatives contract is associated, moves in the opposite direction from what the portfolio manager anticipated. When used for hedging, the change in value of the derivatives instrument may also not correlate specifically with the currency, rate, or other risk being hedged, in which case a fund may not realize the intended benefits. Derivatives contracts are also subject to the risk that the counterparty may fail to perform its obligations under the contract due to, among other reasons, financial difficulties (such as a bankruptcy or reorganization).

Leveraging risk — The risk that certain fund transactions, such as reverse repurchase agreements, short sales, loans of portfolio securities, and the use of when-issued, delayed delivery or forward commitment transactions, or derivatives instruments, may give rise to leverage, causing a fund to be more volatile than if it had not been leveraged, which may result in increased losses to the fund.

Liquidity risk — The possibility that securities cannot be readily sold within seven calendar days at approximately the price at which a fund has valued them.

Government and regulatory risk — The risk that governments or regulatory authorities may take actions that could adversely affect various sectors of the securities markets and affect fund performance.

Active management and selection risk — The risk that the securities selected by a fund’s management will underperform the markets, the relevant indices, or the securities selected by other funds with similar investment objectives and investment strategies. The securities and sectors selected may vary from the securities and sectors included in the relevant index.

The Manager is an indirect wholly owned subsidiary of Macquarie Group Limited (MGL). Other than Macquarie Bank Limited (MBL), a subsidiary of MGL and an affiliate of the Manager, none of the entities noted are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise. The Fund is governed by US laws and regulations.

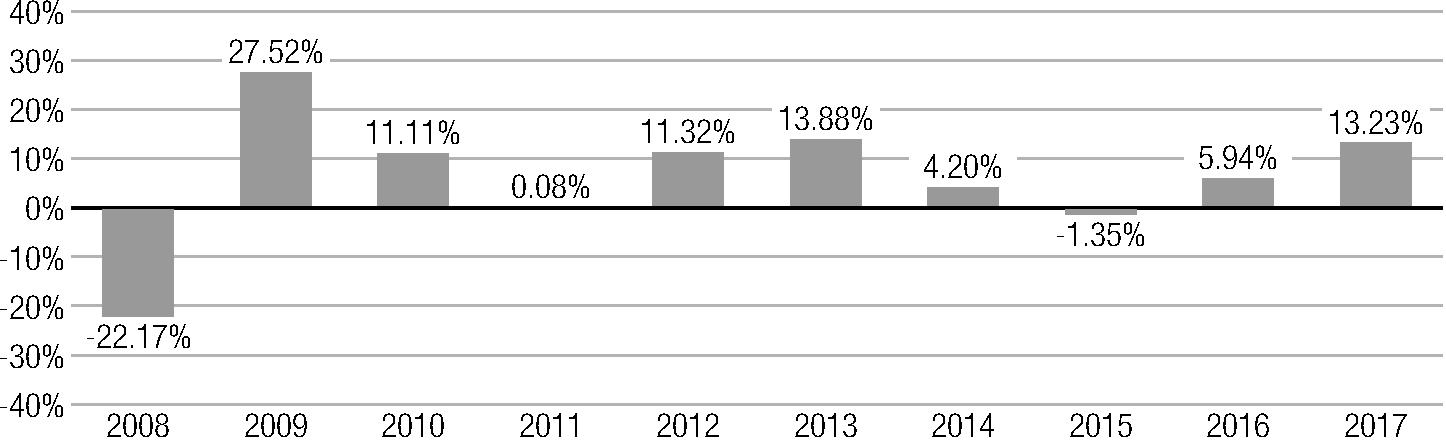

How has Delaware Foundation® Moderate Allocation Fund performed?

The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year and by showing how the Fund’s average annual total returns for the 1-, 5-, and 10-year periods compare with those of a broad measure of market performance. The Fund’s past performance (before and after taxes) is not necessarily an indication of how it will perform in the future. The returns reflect any expense caps in effect during these periods. The returns would be lower without the expense caps. You may obtain the Fund’s most recently available month-end performance by calling 800 523-1918 or by visiting our website at delawarefunds.com/performance.

Prior to mid-September 2008, the Fund operated as a fund of funds, investing primarily in other Delaware Funds. Since mid-September 2008, the Fund has been restructured to invest directly in securities representing a variety of asset classes and investment styles (Restructuring). The historical returns prior to that time do not reflect the Restructuring.

3

Fund summary

Calendar year-by-year total return (Class A)

As of June 30, 2018, the Fund’s Class A shares had a calendar year-to-date return of -0.55%. During the periods illustrated in this bar chart, Class A’s highest quarterly return was 13.72% for the quarter ended June 30, 2009, and its lowest quarterly return was -10.65% for the quarter ended Sept. 30, 2011. The maximum Class A sales charge of 5.75%, which is normally deducted when you purchase shares, is not reflected in the highest/lowest quarterly returns or in the bar chart. If this fee were included, the returns would be less than those shown. The average annual total returns in the table below do include the sales charge.

Average annual total returns for periods ended December 31, 2017

|

1 year | 5 years | 10 years | ||||||

Class A return before taxes

|

6.68% | 5.77% | 4.98% | ||||||

Class A return after taxes on distributions

|

4.53% | 3.90% | 3.78% | ||||||

Class A return after taxes on distributions and sale of Fund shares

|

4.95% | 4.14% | 3.68% | ||||||

Class C return before taxes

|

11.38% | 6.20% | 4.80% | ||||||

Class R return before taxes

|

12.99% | 6.73% | 5.31% | ||||||

Institutional Class return before taxes

|

13.58% | 7.28% | 5.84% | ||||||

S&P 500® Index (reflects no deduction for fees, expenses, or taxes)

|

21.83% | 15.79% | 8.50% | ||||||

Bloomberg Barclays US Aggregate Index (reflects no deduction for fees, expenses, or taxes)

|

3.54% | 2.10% | 4.01% | ||||||

After-tax performance is presented only for Class A shares of the Fund. The after-tax returns for other Fund classes may vary. Actual after-tax returns depend on the investor’s individual tax situation and may differ from the returns shown. After-tax returns are not relevant for shares held in tax-advantaged investment vehicles such as employer-sponsored 401(k) plans and individual retirement accounts (IRAs). The after-tax returns shown are calculated using the highest individual federal marginal income tax rates in effect during the periods presented and do not reflect the impact of state and local taxes.

Who manages the Fund?

Investment manager

Delaware Management Company, a series of Macquarie Investment Management Business Trust (a Delaware statutory trust)

|

Portfolio managers |

Title with Delaware Management Company |

Start date on the Fund |

|

Paul Grillo, CFA |

Senior Vice President, Chief Investment Officer — Diversified Income |

September 2008 |

|

Sharon Hill, Ph.D. |

Senior Vice President, Head of Equity Quantitative Research and Analytics — Macquarie Investment Management, Americas |

September 2008 |

|

Francis X. Morris |

Executive Director, Chief Investment Officer — Core Equity |

May 2004 |

|

Babak “Bob” Zenouzi |

Senior Vice President, Chief Investment Officer — Real Estate Securities and Income Solutions (RESIS) |

September 2008 |

4

Sub-advisor

Jackson Square Partners, LLC (JSP) (Large-cap growth investment sleeve)

|

Portfolio managers |

Title with JSP |

Start date on the Fund |

|

Jeffrey S. Van Harte, CFA |

Chairman, Chief Investment Officer |

May 2014 |

|

Christopher J. Bonavico, CFA |

Portfolio Manager, Research Analyst |

May 2014 |

|

Christopher M. Ericksen, CFA |

Portfolio Manager, Research Analyst |

May 2014 |

|

Daniel J. Prislin, CFA |

Portfolio Manager, Research Analyst |

May 2014 |

Purchase and redemption of Fund shares

You may purchase or redeem shares of the Fund on any day that the New York Stock Exchange (NYSE) is open for business (Business Day). Shares may be purchased or redeemed: through your financial advisor; through the Fund’s website at delawarefunds.com; by calling 800 523-1918; by regular mail (c/o Macquarie Investment Management, P.O. Box 9876, Providence, RI 02940-8076); by overnight courier service (c/o Delaware Service Center, 4400 Computer Drive, Westborough, MA 01581-1722); or by wire.

For Class A and Class C shares, the minimum initial investment is generally $1,000 and subsequent investments can be made for as little as $100. The minimum initial investment for IRAs, Uniform Gifts/Transfers to Minors Act accounts, direct deposit purchase plans, and automatic investment plans is $250 and through Coverdell Education Savings Accounts is $500, and subsequent investments in these accounts can be made for as little as $25. For Class R and Institutional Class shares (except those shares purchased through an automatic investment plan), there is no minimum initial purchase requirement, but certain eligibility requirements must be met. The eligibility requirements are described in the Prospectus under “Choosing a share class” and on the Fund’s website. We may reduce or waive the minimums or eligibility requirements in certain cases.

Tax information

The Fund’s distributions generally are taxable to you as ordinary income, capital gains, or some combination of both, unless you are investing through a tax-advantaged arrangement, such as a 401(k) plan or an IRA, in which case your distributions may be taxed as ordinary income when withdrawn from the tax-advantaged account.

Payments to broker/dealers and other financial intermediaries

If you purchase shares of the Fund through a broker/dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker/dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

5

How we manage the Fund

The Manager takes a disciplined approach to investing, combining investment strategies and risk-management techniques that it believes can help shareholders meet their goals.

Our principal investment strategies

The Fund relies on active asset allocation and invests in a diversified portfolio of securities of different investment classes and styles as it strives to attain its objective(s).

By allocating its investments across several different asset classes and styles, the Fund offers broad diversification while seeking to produce the desired risk-return profile. The potential benefits of such a strategy are threefold:

1. Offering two types of diversification: first, by using multiple investment styles to identify investment opportunities; and, second, by investing in a broadly diversified number of individual securities;

2. Access to the investment expertise of multiple portfolio managers and analysts who focus on each of the underlying investment styles; and

3. A professional portfolio manager who makes asset allocation decisions.

The Manager believes that the Fund is an efficient way to provide active asset allocation services to meet the needs of investors through different stages of their life and their accumulation of wealth. Our active asset allocation strategy begins with an evaluation of three key factors:

This information is used to determine how much of the Fund will be allocated to each asset class. The Manager then selects the appropriate investment styles for investment. The Manager has identified a select group of investment styles that are appropriate for the allocation strategy of the Fund. Each style is listed below along with its investment strategies:

US large-cap core

In managing the large-cap core investment sleeve (style) for the Fund, the Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities or market sectors that the Manager believes are the best investments for the Fund. The large-cap core investment sleeve (style) employs a bottom-up security selection utilizing quantitative screens, fundamental research, and risk control to evaluate stocks based on both growth and value characteristics. The Manager typically uses a quantitative screen that ranks the attractiveness of an investment based on a combination of valuation measures, earnings expectations, cash flow, and balance sheet quality. In further evaluating the attractiveness of an investment, the Manager consider factors such as business conditions in the company’s industry and its competitive position in that industry. The Manager conducts fundamental research on all investments, which often includes reviewing US Securities and Exchange Commission (SEC) filings, examining financial statements, and meeting with top-level company executives. When constructing the large-cap core investment sleeve (style), the Manager applies controls to ensure that the sleeve (style) has acceptable risk characteristics. These characteristics include, but are not limited to, size, valuation, growth, yield, and earnings consistency. This risk profile is then compared to the benchmark index to ensure the large-cap core investment sleeve (style) does not have any unintended risk exposure. The Manager strives to identify stocks of large companies that it believes offer above-average opportunities for long-term price appreciation based on: (1) attractive valuations; (2) growth prospects; and (3) strong cash flow. The large-cap core investment sleeve (style) will generally invest primarily in the common stock of companies with market capitalizations of at least $2 billion at the time of purchase.

US mid- and large-cap growth

In managing the mid- and large-cap growth investment sleeve (style) for the Fund, the Manager researches individual companies that it believes have long-term capital appreciation potential and are expected to grow faster than the US economy. The Fund invests primarily in common stocks and, though it has the flexibility to invest in companies of all sizes, the Fund generally focuses on medium- and large-size companies. Using a bottom-up approach, the Manager looks for companies that it believes: (1) have large end-market potential, dominant business models, and strong free cash flow generation; (2) demonstrate operational efficiencies; (3) have planned well for capital allocation; and (4) have governance policies that tend to be favorable to shareholders. There are a number of catalysts that might increase a company’s potential for free cash flow growth. The Manager’s disciplined, research-intensive selection process is designed to identify catalysts such as: (1) management changes; (2) new products; (3) structural changes in the economy; or (4) corporate restructurings and turnaround situations. The Fund maintains a diversified portfolio representing a number of different industries. Such an approach helps to minimize the impact that any one security or industry could have on the Fund if it were to experience a period of slow or declining growth.

6

US large-cap value

In managing the large-cap value investment sleeve (style) for the Fund, the Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities that it believes are the best investments for the Fund. The large-cap value investment sleeve (style) invests primarily in securities of large-capitalization companies that it believes have long-term capital appreciation potential. The Manager follows a value-oriented investment philosophy in selecting stocks for the Fund using a research-intensive approach that considers factors such as: (1) a security price that reflects a market valuation that is judged to be below the estimated present or future value of the company; (2) favorable earnings prospects and dividend yield potential; (3) the financial condition of the issuer; and (4) various qualitative factors. The Manager may sell a security if it no longer believes the security will contribute to meeting the Fund’s investment objective. In considering whether to sell a security, the Manager may evaluate, among other things, the factors listed above, the condition of the US economy, the condition of non-US economies, and changes in the condition and outlook in the issuer’s industry sector.

US small-cap core

In managing the small-cap core investment sleeve (style) for the Fund, the Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities or market sectors that it believes are the best investments for the Fund. The Manager strives to identify stocks of small companies that it believes offers above-average opportunities for long-term price appreciation based on: (1) attractive valuations; (2) growth prospects; and (3) strong cash flow. The small-cap core investment sleeve (style) employs a bottom-up security selection process utilizing quantitative screens, fundamental research, and risk control to evaluate stocks based on both growth and value characteristics. The Manager typically uses a quantitative screen that ranks the attractiveness of an investment based on a combination of valuation measures, earnings expectations, cash flow, and balance sheet quality. In further evaluating the attractiveness of an investment, the Manager considers factors such as business conditions in the company’s industry and its competitive position in that industry. The Manager conducts fundamental research on all investments, which often includes reviewing SEC filings, examining financial statements, and meeting with top-level company executives. When constructing the sleeve (style), the Manager applies controls to ensure the sleeve (style) has acceptable risk characteristics. These characteristics include, but are not limited to, size, valuation, growth, yield, and earnings consistency. This risk profile is then compared to the benchmark index to ensure the sleeve (style) does not have any unintended risk exposure. From time to time, this sleeve may also invest in convertible securities, futures contracts, options on futures contracts, and warrants.

US small-cap growth

In managing the small-cap growth investment sleeve (style) for the Fund, the Manager seeks to invest primarily in common stocks and generally focuses on small-sized companies that address large market opportunities. The Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities or market sectors that it believes are the best investments for the sleeve (style). The Manager believes, over the long run, earnings growth determines stock price movements and companies with the strongest gains in profitability should enjoy share performance that exceeds the broad market averages, provided that the earnings are of high quality and likely to continue. To locate these high growth investment opportunities, the Manager utilizes a top-down thematic overlay combined with bottom-up, fundamental research. From a top-down perspective, the Manager seeks to identify, at an early stage, major demand trends that are believed to be creating powerful investment opportunities. Once the trends have been identified, the Manager creates investment themes as a means for organizing research efforts. The Manager studies the industries that fit within its themes to assess the competitive landscape and begins to analyze specific companies. From a bottom-up perspective, the Manager conducts extensive fundamental analysis of the businesses that appear to have a competitively advantaged position within these fast growing industries. At this stage, it is critical for the Manager to understand the nature of competition and develop a model for the type of company that will succeed in the given industry. The Manager seeks companies that have current earnings growth rates that are significantly higher than the overall market.

US small-cap value

In managing the small-cap value investment sleeve (style) for the Fund, the Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities or market sectors that it believes are the best investments for the sleeve (style). The Manager strives to identify small companies that it believes offer above-average opportunities for long-term price appreciation because their current stock prices do not appear to accurately reflect the companies' underlying value or future earnings potential. The Manager's focus will be on value stocks, defined as stocks whose prices are historically low based on a given financial measure such as profit, book value, or cash flow. Companies may be undervalued for many reasons. They may be unknown to stock analysts, they may have experienced poor earnings, or their industry may be in the midst of a period of weak growth. The Manager will carefully evaluate the financial strength of a company, the nature of its management, any developments affecting the company or its industry, anticipated new products or services, possible management changes, projected takeovers, or technological breakthroughs. Using this extensive analysis, the Manager's goal is to pinpoint the companies within the universe of undervalued stocks, whose true value is likely to be recognized and rewarded with a rising stock price in the future. Because there is added risk when investing in smaller companies, which may still be in their early developmental stages, the portfolio managers maintain a well-diversified portfolio, typically holding a mix of different stocks, representing a wide array of industries.

7

How we manage the Fund

International value

In managing the international value investment sleeve (style) for the Fund, the Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities or market sectors that it believes are the best investments for the Fund. The Manager uses a value strategy, investing primarily in equity securities which provide the potential for capital appreciation. In selecting foreign stocks, the portfolio management team’s philosophy is based on the concept that adversity creates opportunity and that transitory problems can be overcome by well-managed companies. The team uses an approach that combines quantitative, valuation-based screening at the early stages followed by comprehensive company and industry-specific research. The team’s philosophy and process are based on the concept that valuation screens serve solely as a starting point in the creation of a portfolio of undervalued stocks because accounting measures only approximate the intrinsic value of any company. The team’s investment universe segmentation prioritizes its research and its bottom-up contrarian investment style seeks to identify mispriced securities. The international value investment sleeve (style) may purchase securities in any foreign country, developed or emerging. A representative list of the countries where the sleeve may invest includes: Australia, Brazil, Canada, China, Finland, France, Germany, Hong Kong, Italy, Japan, Luxembourg, the Netherlands, Singapore, Spain, Sweden, Switzerland, Taiwan, and the United Kingdom. While this is a representative list, the sleeve may also invest in countries not listed here. The Manager maintains a long-term focus, seeking companies that it believes will perform well over the next three to five years.

International growth

In managing the international growth investment sleeve (style) for the Fund, the Manager seeks to invest primarily in equity securities that provide the potential for capital appreciation. Such an investment approach would commonly be described as a growth strategy. The Manager may purchase securities in any foreign, developed, or emerging country, relying on a combination of top-down and bottom-up analysis of individual companies. Its analysis will generally focus on valuation, growth prospects, capital structure, and industry position, together with economic, political, and regulatory conditions. Alternatively, the Fund may invest in exchange traded instruments which provide exposure to equities fitting the international growth investment style.

International small-cap growth

In managing the international small-cap growth investment sleeve (style) for the Fund, the Manager invests in small capitalization non-US companies with earnings growth due to positive fundamental change, with evidence of a sustainable catalyst and timeliness in terms of positive relative price strength that we believe will offer superior returns over time. The team operates under the following beliefs: fundamental research is the foundation of any investment decision, market participants tend to underestimate the magnitude and/or duration of earnings growth driven by change, and companies undergoing positive sustainable fundamental change will likely exhibit rising relative price strength.

The Manager utilizes screens and fundamental qualitative analysis in its research and security selection process in order to ensure a good alignment/validation of investment research and investment performance. Investment screens are used to help identify stocks with the desired liquidity and growth characteristics that may be undergoing positive fundamental change. The fundamental research focuses on identifying the positive change, the sustainability of the change and the risks related to the investment thesis. The Manager evaluates and compares the market’s growth assumptions to the Manager’s growth assumptions.

The Manager incorporates top-down analysis to govern the magnitude of over and underweights with respect to geographic and sector positioning. The analysis consists of evaluating many factors such as economic momentum, liquidity, market performance, valuations and political risks. The Manager also uses various multi-factor risk management systems to measure, monitor and manage the sleeve’s (style) security-specific and systematic risk exposure. The sleeve invests in non-US companies across the small-cap universe including emerging markets.

Emerging markets

In managing the emerging markets investment sleeve (style) for the Fund, the Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities or market sectors that it believes are the best investments for the Fund. The Manager invests primarily in a broad range of equity securities of companies located in emerging market countries. Emerging market countries include those currently considered to be developing by the World Bank, the United Nations or the countries’ governments. These countries typically are located in the Asia-Pacific region, Eastern Europe, the Middle East, Central and South America, and Africa.

Although the Manager invests primarily in companies from countries considered to be emerging, it will also invest in companies that are not in emerging countries: (1) if the portfolio manager believes that the performance of a company or its industry will be influenced by opportunities in the emerging markets; (2) to maintain exposure to industry segments where the portfolio manager believes there are not satisfactory investment opportunities in emerging countries; and (3) if the portfolio manager believes there is the potential for significant benefit to the sleeve. The team believes that although market price and intrinsic business value are positively correlated in the long run, short-term divergences can emerge. The Manager seeks to take advantage of these divergences through a fundamental, bottom-up approach. The Manager invests in securities of companies with sustainable franchises when they are trading at a discount to the Manager’s intrinsic value estimate for that security. The Manager defines sustainable franchises as those companies with potential to earn excess returns above their cost of capital over the long-run. Sustainability analysis involves identification of a company’s source of competitive advantage and the ability of its management to maximize its return potential. The Manager prefers companies with large market opportunities in which to deploy capital, providing

8

opportunities to grow faster than the overall economy. Intrinsic value assessment is quantitatively determined through a variety of valuation methods including discounted cash flow, replacement cost, private market transaction, and multiples analysis.

Emerging markets small-cap

In managing the emerging markets small-cap investment sleeve (style) for the Fund, the Manager invests in small capitalization companies located in or with economic ties to emerging markets with earnings growth due to positive fundamental change, with evidence of a sustainable catalyst and timeliness in terms of positive relative price strength that we believe will offer superior returns over time. The team operates under the following beliefs: fundamental research is the foundation of any investment decision, market participants tend to underestimate the magnitude and/or duration of earnings growth driven by change, and companies undergoing positive sustainable fundamental change will likely exhibit rising relative price strength.

The Manager utilizes screens and fundamental qualitative analysis in its research and security selection process in order to ensure a good alignment/validation of investment research and investment performance. Investment screens are used to help identify stocks with the desired liquidity and growth characteristics that may be undergoing positive fundamental change. The fundamental research focuses on identifying the positive change, the sustainability of the change and the risks related to the investment thesis. The Manager evaluates and compares the market’s growth assumptions to the Manager’s growth assumptions.

The Manager incorporates top-down analysis to govern the magnitude of over and underweights with respect to geographic and sector positioning. The analysis consists of evaluating many factors such as economic momentum, liquidity, market performance, valuations and political risks. The Manager also uses various multi-factor risk management systems to measure, monitor and manage the sleeve’s (style) security-specific and systematic risk exposure.

Emerging markets opportunities

In managing the emerging markets opportunities sleeve (style) for the Fund, the Manager invests in companies located in or with economic ties to emerging markets with earnings growth due to positive fundamental change, with evidence of a sustainable catalyst and timeliness in terms of positive relative price strength that we believe will offer superior returns over time. The team operates under the following beliefs: fundamental research is the foundation of any investment decision, market participants tend to underestimate the magnitude and/or duration of earnings growth driven by change, and companies undergoing positive sustainable fundamental change will likely exhibit rising relative price strength.

The Manager utilizes screens and fundamental qualitative analysis in its research and security selection process in order to ensure a good alignment/validation of investment research and investment performance. Investment screens are used to help identify stocks with the desired liquidity and growth characteristics that may be undergoing positive fundamental change. The fundamental research focuses on identifying the positive change, the sustainability of the change and the risks related to the investment thesis. The Manager evaluates and compares the market’s growth assumptions to the Manager’s growth assumptions.

The Manager incorporates top-down analysis to govern the magnitude of over and underweights with respect to geographic and sector positioning. The analysis consists of evaluating many factors such as economic momentum, liquidity, market performance, valuations and political risks. The Manager also uses various multi-factor risk management systems to measure, monitor and manage the sleeve’s (style) security-specific and systematic risk exposure.

Global real estate securities

In managing the global real estate securities investment sleeve (style) for the Fund, the Manager researches individual companies and analyzes economic and market conditions, seeking to identify the securities or market sectors that it believes are the best investments for the Fund. The Manager invests in securities issued by US and non-US companies in the real estate and real estate-related sectors. A company in the real estate sector (such as a real estate operating or service company) generally derives at least 50% of its revenue from real estate or has at least 50% of its assets in real estate. The Manager will allocate the assets among companies in various regions and countries throughout the world, including the US and developed, developing, and emerging market non-US countries. Therefore, the Fund may at times have a significant investment in real estate companies organized or located outside the US. Conversely, under certain market conditions, the Manager may shift more of the investments to US companies. The Fund may invest in securities issued in any currency and may hold foreign currency.

The Manager’s investment strategy is based on both a top-down and a bottom-up assessment of countries and specific markets. From a top-down perspective, the Manager considers each region’s economy, including current economic conditions, interest rates, job growth, and capital flows. The Manager’s bottom-up analysis is based on a relative valuation methodology that is focused on both real estate valuations and security-level research with disciplined portfolio management. Real estate factors that are important to our analysis include supply/demand, vacancy rates, and rental growth in a particular market. This market-by-market research is coupled with an overview of a company’s financials, cash flow, dividend growth rates, and management strategy. In addition, the Manager considers selling a security based generally on the following disciplines: a security reaching our targeted price ranges; relative pricing of a security versus other investment opportunities; or a negative change in how it views a security’s fundamentals.

9

How we manage the Fund

Diversified fixed income

In selecting fixed income securities for the Fund, the Manager takes a disciplined approach to investing, combining investment strategies and risk management techniques that it believes can help shareholders meet their goals. The Manager analyzes economic and market conditions, seeking to identify the securities or market sectors that it thinks are the best investments for the Fund. The fixed income investment sleeve (style) allocates its investments principally among the US investment grade, US high yield, international developed markets, and emerging markets sectors.

In managing the assets allocated to the investment grade sector, the Manager will invest principally in debt obligations issued or guaranteed by the US government, its agencies or instrumentalities, and by US corporations. The corporate debt obligations in which the Fund may invest include bonds, notes, debentures, and commercial paper of US companies. The US government securities in which the Manager may invest include a variety of securities which are issued or guaranteed as to the payment of principal and interest by the US government, and by various agencies or instrumentalities which have been established or sponsored by the US government. The investment grade sector of the assets may also be invested in mortgage-backed securities issued or guaranteed by the US government, its agencies or instrumentalities, or by government-sponsored corporations.

Other mortgage-backed securities in which the Fund may invest are issued by certain private, nongovernment entities. The Fund may also invest in securities which are backed by assets such as receivables on home equity and credit card loans, automobile, mobile home, recreational vehicle, and other loans, wholesale dealer floor plans, and leases.

In managing the assets allocated to the US high yield sector, the Fund will invest the assets that are allocated to the domestic high yield sector primarily in those securities having a liberal and consistent yield and those tending to reduce the risk of market fluctuations. The Manager may invest in domestic corporate debt obligations, including notes, which may be convertible or nonconvertible, commercial paper, units consisting of bonds with stock or warrants to buy stock, attached debentures, convertible debentures, zero coupon bonds, and pay-in-kind securities. The Fund will invest in both rated and unrated bonds. The rated bonds that the Fund may purchase in this sector will generally be rated lower than BBB- by Standard & Poor’s (S&P) and Baa3 by Moody’s Investors Service, Inc. (Moody’s), or similarly rated by another nationally recognized statistical rating organization (NRSRO). Unrated bonds may be more speculative in nature than rated bonds.

In managing the assets allocated to the international developed markets sector, the Manager invests primarily in fixed income securities of issuers organized or having a majority of their assets or deriving a majority of their operating income in international developed markets. These fixed income securities may include foreign government securities, debt obligations of foreign companies, and securities issued by supranational entities. A supranational entity is an entity established or financially supported by the national governments of one or more countries to promote reconstruction or development. Examples of supranational entities include, among others, the International Bank for Reconstruction and Development (more commonly known as the World Bank), the European Central Bank, the European Investment Bank, the Inter-American Development Bank, and the Asian Development Bank. The international developed markets sector will be subject to certain risks, including, but not limited to, the risk that securities within this sector may be adversely affected by political instability, changes in currency exchange rates, foreign economic conditions, or inadequate regulatory and accounting standards.

In managing the assets allocated to emerging markets sector, the Manager may purchase securities of issuers in any foreign country, developed and underdeveloped. These investments may include direct obligations of issuers located in emerging markets countries. As with the international sector, the fixed income securities in the emerging markets sector may include foreign government securities, debt obligations of foreign companies, and securities issued by supranational entities. In addition to the risks associated with investing in all foreign securities, emerging markets debt is subject to specific risks, particularly those that result from emerging markets generally being less stable, politically and economically, than developed markets. There is substantially less publicly available information about issuers in emerging markets than there is about issuers in developed markets, and the information that is available tends to be of a lesser quality. Also, emerging markets are typically less mature, less liquid, and subject to greater price volatility than are developed markets.

Once the Manager selects appropriate investments for the Fund, it continually monitors the market and economic environments and the risk-reward profiles of each asset class. The Manager actively adjusts the Fund, striving to meet its investment objective(s).

The Fund’s investment objectives are nonfundamental. This means that the Fund’s Board of Trustees (Board) may change an objective without obtaining shareholder approval. If an objective were changed, the Fund would notify shareholders at least 60 days before the change became effective.

The securities in which the Fund typically invests

Please see the Fund’s SAI for additional information about certain of the securities described below as well as other securities in which the Fund may invest.

10

|

Common stocks |

Common stocks are securities that represent shares of ownership in a corporation. Stockholders may participate in a corporation’s profits through its distribution of dividends to stockholders, proportionate to the number of shares they own.

How the Fund uses them: The Fund focuses a portion of its net investments on common stocks.

|

Corporate bonds |

Corporate bonds are bonds, notes, or debentures issued by corporations and other business organizations.

How the Fund uses them: The Fund may invest in corporate bonds rated in one of the four highest categories by an NRSRO (for example, at least BBB by S&P or Baa by Moody’s), or deemed equivalent consistent with its investment objectives and policies. For bonds rated below investment grade, please see “High yield fixed income securities (junk bonds)” below.

|

High yield fixed income securities (junk bonds) |

High yield fixed income securities are debt obligations rated lower than BBB- by S&P, Baa3 by Moody’s, or similarly rated by another NRSRO or, if unrated, of comparable quality. These securities are often referred to as “junk bonds” and are considered to be of poor standing and predominantly speculative.

How the Fund uses them: The Fund may invest in high yield fixed income securities up to 25% of its net assets.

Emphasis is typically on those rated BB or Ba by an NRSRO. The Manager carefully evaluates an individual company’s financial situation, its management, the prospects for its industry, and the technical factors related to its bond offering. The Manager’s goal is to identify those companies that it believes will be able to repay their debt obligations in spite of poor ratings. The Fund may invest in unrated bonds if the Manager believes their credit quality is comparable to the rated bonds in which the Fund is permitted to invest. Unrated bonds may be more speculative in nature than rated bonds.

|

Convertible securities |

Convertible securities are usually preferred stocks or corporate bonds that can be exchanged for a set number of shares of common stock at a predetermined price. These securities offer higher appreciation potential than nonconvertible bonds and greater income potential than nonconvertible preferred stocks.

How the Fund uses them: The Fund may invest a portion of its assets in convertible securities in any industry consistent with its investment objectives and policies.

|

Mortgage-backed securities (MBS) |

MBS are fixed income securities that represent pools of mortgages, with investors receiving principal and interest payments as the underlying mortgage loans are paid back. Many are issued and guaranteed against default by the US government or its agencies or instrumentalities, such as Freddie Mac, Fannie Mae, and Ginnie Mae. Others are issued by private financial institutions, with some fully collateralized by certificates issued or guaranteed by the US government or its agencies or instrumentalities.

How the Fund uses them: The Fund may invest in mortgage-backed securities issued or guaranteed by the US government, its agencies, or instrumentalities or by government-sponsored corporations consistent with their investment objectives and policies.

|

Collateralized mortgage obligations (CMOs) and real estate mortgage investment conduits (REMICs) |

CMOs are privately issued mortgage-backed bonds whose underlying value is the mortgages that are collected into different pools according to their maturity. They are issued by US government agencies and private issuers. REMICs are privately issued mortgage-backed bonds whose underlying value is a fixed pool of mortgages secured by an interest in real property. Like CMOs, REMICs offer different pools according to the underlying mortgages’ maturities.

How the Fund uses them: The Fund may invest in CMOs and REMICs consistent with its investment objectives and policies. Illiquid stripped mortgage securities together with any other illiquid investments will not exceed the Fund’s limit on illiquid securities. In addition, subject to certain quality and collateral limitations, the Fund may invest up 10% of net assets in CMOs and REMICs issued by private entities that are not collateralized by securities issued or guaranteed by the US government, its agencies, or instrumentalities.

|

Asset-backed securities (ABS) |

ABS are bonds or notes backed by accounts receivable, including home equity, automobile, or credit loans.

How the Fund uses them: The Fund may invest in ABS.

11

How we manage the Fund

|

Real estate investment trusts (REITs) |

REITs are pooled investment vehicles that invest primarily in income-producing real estate or real estate-related loans or interests. REITs are generally classified as equity REITs, mortgage REITs, or a combination of equity and mortgage REITs. Equity REITs invest the majority of their assets directly in real property and derive income primarily from the collection of rents. Equity REITs can also realize capital gains by selling properties that have appreciated in value. Mortgage REITs invest the majority of their assets in real estate mortgages and derive income from the collection of interest payments.

How the Fund uses them: The Fund may invest in shares of REITs consistent with its investment objectives and policies.

|

US government securities |

US government securities are direct US obligations that include bills, notes, and bonds, as well as other debt securities, issued by the US Treasury, and securities of US government agencies or instrumentalities. US Treasury securities are backed by the “full faith and credit” of the United States. Securities issued or guaranteed by federal agencies and US government-sponsored instrumentalities may or may not be backed by the “full faith and credit” of the US. In the case of securities not backed by the “full faith and credit” of the US, investors in such securities look principally to the agency or instrumentality issuing or guaranteeing the obligation for ultimate repayment.

How the Fund uses them: The Fund may invest in US government securities for temporary purposes or otherwise, as is consistent with its investment objectives and policies.

|

Foreign securities |

Foreign securities are securities of issuers which are classified by index providers, or by the investment manager applying internally consistent guidelines, as being assigned to countries outside the United States. Investments in foreign securities include investments in American depositary receipts (ADRs), European depositary receipts (EDRs), and global depositary receipts (GDRs). ADRs are receipts issued by a depositary (usually a US bank) and EDRs and GDRs are receipts issued by a depositary outside of the US (usually a non-US bank or trust company or a foreign branch of a US bank). Depositary receipts represent an ownership interest in an underlying security that is held by the depositary. Generally, the underlying security represented by an ADR is issued by a foreign issuer and the underlying security represented by an EDR or GDR may be issued by a foreign or US issuer. Sponsored depositary receipts are issued jointly by the issuer of the underlying security and the depositary, and unsponsored depositary receipts are issued by the depositary without the participation of the issuer of the underlying security. Generally, the holder of the depositary receipt is entitled to all payments of interest, dividends, or capital gains that are made on the underlying security.

How the Fund uses them: The Fund may invest in foreign securities directly or indirectly through ADRs, EDRs, and GDRs.

Determinations to purchase depositary receipts will be based on relevant factor(s) in the portfolio managers’ sole discretion.

|

Repurchase agreements |

A repurchase agreement is an agreement between a buyer of securities, such as a fund, and a seller of securities, in which the seller agrees to buy the securities back within a specified time at the same price the buyer paid for them, plus an amount equal to an agreed-upon interest rate. Repurchase agreements are often viewed as equivalent to cash.

How the Fund uses them: Typically, the Fund uses repurchase agreements as a short-term investment for its cash positions or for temporary defensive purposes. In order to enter into these repurchase agreements, the Fund must have collateral of at least 102% of the repurchase price. The Fund will only enter into repurchase agreements in which the collateral is composed of US government securities. At the Manager’s discretion, the Fund may invest overnight cash balances in short-term discount notes issued or guaranteed by the US government, its agencies or instrumentalities or government-sponsored corporations.

|

Restricted securities |

Restricted securities are privately placed securities whose resale is restricted under US securities laws.

How the Fund uses them: The Fund may invest in privately placed securities, including those that are eligible for resale only among certain institutional buyers without registration, commonly known as “Rule 144A Securities.” Restricted securities that are determined to be illiquid may not exceed the Fund’s limit on investments in illiquid securities.

|

Illiquid securities |

Illiquid securities are securities that do not have a ready market and cannot be readily sold within seven calendar days at approximately the price at which a fund has valued them. Illiquid securities include repurchase agreements maturing in more than seven calendar days.

How the Fund uses them: The Fund may invest up to 15% of its net assets in illiquid securities.

12

|

Short-term debt or money market instruments |

These instruments include: (1) time deposits, certificates of deposit, and banker's acceptances issued by US banks; (2) time deposits and certificates of deposit issued by foreign banks; (3) commercial paper with the highest quality rating; (4) short-term debt obligations with the highest quality rating; (5) US government securities; and (6) repurchase agreements collateralized by those instruments.

How the Fund uses them: The Fund may invest in these instruments either as a means to achieve its investment objective or, more commonly, as temporary defensive investments or pending investment in the Fund’s principal investment securities. When investing all or a significant portion of the Fund’s assets in these instruments, the Fund may not be able to achieve its investment objective.

|

Time deposits |

Time deposits are nonnegotiable deposits maintained in a banking institution for a specified period of time at a stated interest rate.

How the Fund uses them: The Fund will not purchase time deposits maturing in more than seven days, and time deposits maturing from two business days through seven calendar days will not exceed 15% of its total assets.

|

When-issued and delayed-delivery securities |

In these transactions, instruments are purchased with payment and delivery taking place in the future in order to secure what is considered to be an advantageous yield or price at the time of the transaction. The payment obligations and the interest rates that will be received are each fixed at the time a fund enters into the commitment and no interest accrues to a fund until settlement. Thus, it is possible that the market value at the time of settlement could be higher or lower than the purchase price if the general level of interest rates has changed.

How the Fund uses them: The Fund may purchase securities on a when-issued or delayed-delivery basis. The Fund may not enter into when-issued commitments exceeding, in the aggregate, 15% of the market value of its total assets less liabilities other than the obligations created by these commitments. The Fund will designate cash or securities in amounts sufficient to cover its obligations, and will value the designated assets daily.

|

Securities lending transactions |

These transactions involve the loan of securities owned by a fund to qualified dealers and investors for their use relating to short-sales or other securities transactions. These transactions may generate additional income for a fund.

How the Fund uses them: The Fund may loan up to 25% of its assets to qualified broker/dealers or institutional investors.

|

Zero coupon and payment-in-kind (PIK) bonds |

Zero coupon bonds are debt obligations that do not entitle the holder to any periodic payments of interest prior to maturity or a specified date when the securities begin paying current interest, and therefore are issued and traded at a discount from their face amounts or par values. PIK bonds pay interest through the issuance to holders of additional securities.

How the Fund uses them: The Fund may invest in fixed income securities, including zero coupon bonds and PIK bonds, consistent with its investment objectives and policies. The market prices of these bonds are generally more volatile than the market prices of securities that pay interest periodically and are likely to react to changes in interest rates to a greater degree than interest-paying bonds having similar maturities and credit quality. The bonds may have certain tax consequences which, under certain conditions, could be adverse to the Fund.

|

Futures and options |

Futures contracts are agreements for the purchase or sale of a security or a group of securities at a specified price, on a specified date. Unlike purchasing an option, a futures contract must be executed unless it is sold before the settlement date.

Options represent a right to buy or sell a swap agreement, a futures contract, or a security or a group of securities at an agreed-upon price at a future date. The purchaser of an option may or may not choose to go through with the transaction. The seller of an option, however, must go through with the transaction if the purchaser exercises the option.

Certain options and futures may be considered illiquid.

How the Fund uses them: The Fund may invest in futures, options, and closing transactions related thereto. These activities will be entered into for hedging purposes and to facilitate the ability to quickly deploy into the market the Fund’s cash, short-term debt securities, and other money market instruments at times when the Fund’s assets are not fully invested. The Fund may only enter into these transactions for hedging purposes if it is consistent with its respective investment objective(s) and policies. The Fund may not engage in such transactions to the extent that obligations resulting from these activities, in the

13

How we manage the Fund

aggregate, exceed 75% of its assets. In addition, the Fund may enter into futures contracts, purchase or sell options on futures contracts, trade in options on foreign currencies, and enter into closing transactions with respect to such activities to hedge or “cross hedge” the currency risks associated with their investments.

Use of these strategies can increase the operating costs of the Fund and can lead to loss of principal.

|

Forward foreign currency contracts |

A fund may invest in securities of foreign issuers and may hold foreign currency. In addition, a fund may enter into contracts to purchase or sell foreign currencies at a future date (a “forward foreign currency” contract or “forward” contract). A forward contract involves an obligation to purchase or sell a specific currency at a future date, which may be any fixed number of days from the date of the contract, agreed upon by the parties, at a price set at the time of the contract.

How the Fund uses them: Although the Fund values its assets daily in terms of US dollars, it does not intend to convert its holdings of foreign currencies into US dollars on a daily basis. The Fund is permitted to, however, from time to time, purchase or sell foreign currencies and/or engage in forward foreign currency contracts in order to facilitate or expedite settlement of portfolio transactions and to minimize currency value fluctuations. The Fund may also enter into forward contracts to “lock in” the price of a security it has agreed to purchase or sell, in terms of US dollars or other currencies in which the transaction will be consummated.

|

Interest rate swap, index swap, and credit default swap agreements |

In an interest rate swap, a fund receives payments from another party based on a variable or floating interest rate, in return for making payments based on a fixed interest rate. An interest rate swap can also work in reverse with a fund receiving payments based on a fixed interest rate and making payments based on a variable or floating interest rate.

In an index swap, a fund receives gains or incurs losses based on the total return of a specified index, in exchange for making interest payments to another party. An index swap can also work in reverse with a fund receiving interest payments from another party in exchange for movements in the total return of a specified index.

In a credit default swap, a fund may transfer the financial risk of a credit event occurring (a bond default, bankruptcy, or restructuring, for example) on a particular security or basket of securities to another party by paying that party a periodic premium; likewise, a fund may assume the financial risk of a credit event occurring on a particular security or basket of securities in exchange for receiving premium payments from another party.

Interest rate swaps, index swaps, and credit default swaps may be considered illiquid.

How the Fund uses them: The Fund may use interest rate swaps to adjust its sensitivity to interest rates or to hedge against changes in interest rates. Index swaps may be used to gain exposure to markets that the Fund invests in, such as the corporate bond market. The Fund may also use index swaps as a substitute for futures or options contracts if such contracts are not directly available to the Fund on favorable terms. The Fund may enter into credit default swaps in order to hedge against a credit event, to enhance total return, or to gain exposure to certain securities or markets.

At times when the Manager anticipates adverse conditions, the Manager may want to protect gains on securities without actually selling them. The Manager might use swaps to seek to neutralize the effect of any price declines without selling a bond or bonds.

If the Fund has any financial obligation under a swap agreement, it will designate cash and liquid assets sufficient to cover the obligation and will value the designated assets daily as long as the obligation is outstanding. Use of these strategies can increase the operating costs of the Fund and can lead to loss of principal.

|

Investment company securities |

Any investments in investment company securities, including exchange-traded funds (ETFs), will be limited by the Investment Company Act of 1940, as amended (the “1940 Act”) and would involve a payment of the pro rata portion of their expenses, including advisory fees, of such other investment companies. Under the current 1940 Act limitations, without an exemption a fund may not: (i) own more than 3% of the voting stock of another investment company; (ii) invest more than 5% of a fund’s total assets in the shares of any one investment company; or (iii) invest more than 10% of a fund’s total assets in shares of other investment companies. These percentage limitations also apply to a fund’s investment in an unregistered investment company.

The SEC has granted exemptive orders to various iShares funds and their investment advisors that permit the Fund to invest in these funds beyond the limitations described above, subject to certain conditions.

How the Fund uses them: The Fund may invest in investment companies to the extent that it helps it achieve its investment objective(s).

14

|

Equity linked securities |

Equity linked securities are privately issued derivatives securities that have a return component based on the performance of a single security, a basket of securities, or an index.

How the Fund uses them: The Fund may invest up to 10% of its net assets in equity linked securities. Equity linked securities may be considered illiquid and are subject to the Fund’s limitation on illiquid securities. In some instances, investments in equity linked securities may also be subject to the Fund’s limitation on investments in investment companies.

|

Bank loans and other indebtedness |

A bank loan represents an interest in a loan or other direct indebtedness, such as an assignment, that entitles the acquiror of such interest to payments of interest, principal, and/or other amounts due under the structure of the loan or other direct indebtedness. In addition to being structured as secured or unsecured loans, such investments could be structured as novations or assignments or represent trade or other claims owed by a company to a supplier.

How the Fund uses them: The Fund may invest in bank loans that meet the credit standards established by the portfolio managers. The portfolio managers perform their own independent credit analysis on each borrower and on the collateral securing each loan. The portfolio managers consider the nature of the industry in which the borrower operates, the nature of the borrower’s assets, and the general quality and creditworthiness of the borrower. The Fund may invest in bank loans in order to enhance total return, to effect diversification, or to earn additional income. The Fund will not use bank loans for reasons inconsistent with its investment objective(s).

|

Short sales |

Short sales are transactions in which a fund sells a security it does not own and, at the time the short sale is effected, the fund incurs an obligation to replace the security borrowed no matter what its price may be at the time the fund delivers it to the lender.

How the Fund uses them: The Manager may establish short positions in exchange traded funds in the fixed income portion of the Fund in an attempt to isolate, manage, or reduce the risk of individual securities positions held by the Fund, of a decline in a particular market sector to which the Fund has significant exposure, or of the exposure to securities owned by the Fund in the aggregate. Such short sales may also be implemented in an attempt to manage the duration of the Fund's holdings. There is no assurance that any such short sales will achieve their intended objective(s). The Manager will not engage in short sales for speculative purposes.

The Manager may also engage in short sales “against the box” in the equity portion of the Fund.

Other investment strategies

|

Borrowing from banks |

The Fund may borrow money from banks as a temporary measure for extraordinary or emergency purposes or to facilitate redemptions. The Fund will be required to pay interest to the lending banks on the amounts borrowed. As a result, borrowing money could result in the Fund being unable to meet its investment objective. The Fund will not borrow money in excess of one-third of the value of its total assets.

|

Initial public offerings (IPOs) |

Under certain market conditions, the Fund may invest in companies at the times of their IPOs. Companies involved in IPOs generally have limited operating histories, and prospects for future profitability are uncertain. Prices of IPOs may also be unstable because of the absence of a prior public market, the small number of shares available for trading, and limited investor information. IPOs may be sold within 12 months of purchase. This may result in increased short-term capital gains, which will be taxable to shareholders as ordinary income.

|

Temporary defensive positions |

In response to unfavorable market conditions, the Fund may make temporary investments in cash or cash equivalents or other high-quality, short-term instruments. These investments may not be consistent with the Fund’s investment objective. To the extent that the Fund holds such instruments, it may be unable to achieve its investment objective.

15

How we manage the Fund

The risks of investing in the Fund

Investing in any mutual fund involves risk, including the risk that you may receive little or no return on your investment, and the risk that you may lose part or all of the money you invest. Before you invest in the Fund, you should carefully evaluate the risks. Because of the nature of the Fund, you should consider your investment to be a long-term investment that typically provides the best results when held for a number of years. The information below describes the principal risks you assume when investing in the Fund. Please see the SAI for a further discussion of these risks and other risks not discussed here.

|

Market risk |