Form 10-K SELLAS Life Sciences For: Dec 31

Tweet

Tweet Share

ShareUNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________________

FORM 10-K

________________________________

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to _________

Commission File Number: 001-33958

SELLAS Life Sciences Group, Inc.

(Exact name of registrant as specified in its charter)

________________________________

Delaware | 20-8099512 | |||

(State of incorporation) | (I.R.S. Employer Identification No.) | |||

15 West 38th Street, 10th Floor, New York, NY 10018

(Address of principal executive officers)

(917) 438-4353

(Registrant's telephone number, including area code)

Securities registered pursuant to Section (12(b) of the Exchange Act: | ||||

Title of Each Class | Name of Each Exchange on Which Registered | |||

Common Stock, $0.0001 Par Value per share | The Nasdaq Capital Market | |||

Securities registered pursuant to Section (12(g) of the Exchange Act: None | ||||

________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or other information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | o | Accelerated filer | o | Non-accelerated filer | x | |||||

Smaller reporting company | x | Emerging growth company | o | |||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes x No

The aggregate market value of the registrant's common stock, $0.0001 per value per share, held by non-affiliates of the registrant on June 29, 2018, the last business day of the registrant's most recently completed second fiscal quarter, was $14,425,577 (based on the closing sales price of the registrant's common stock on that date). Shares of the registrant's common stock held by each officer and director and each person who owns 5% or more of the outstanding common stock of the registrant have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes. As of March 21, 2019, SELLAS Life Sciences Group, Inc. had outstanding 23,176,475 shares of common stock, $0.0001 par value per share, exclusive of treasury shares.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required in Part III of this Annual Report on Form 10-K is incorporated from the registrant’s Proxy Statement for its 2019 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this Form 10-K, provided that if such Proxy Statement is not filed within such period, such information will be included in an amendment to this Form 10-K to be filed within such 120-day period.

SPECIAL NOTE REGARDING FORWARD LOOKING STATEMENTS

Some of the information contained in this annual report on Form 10-K may include forward-looking statements that reflect our current views with respect to our development programs, business strategy, business plan, financial performance and other future events. These statements include forward-looking statements both with respect to us, specifically, and our industry, in general. Such forward-looking statements include the words “expect,” “intend,” “plan,” “believe,” “project,” “estimate,” “may,” “should,” “anticipate,” “will” and similar statements of a future or forward-looking nature identify forward-looking statements.

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Forward-looking statements are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. There are or will be important factors that could cause actual results to differ materially from those indicated in these statements. These factors include, but are not limited to, those factors set forth in the sections entitled "Business - Overview - Recent Developments," “Risk Factors,” “Legal Proceedings,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in this annual report on Form 10-K, which you should review carefully. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

1

SELLAS LIFE SCIENCES GROUP, INC.

FORM 10-K - Annual Report

For the Year Ended December 31, 2018

TABLE OF CONTENTS

Page | |||

PART I | |||

Item 1 | |||

Item 1A | |||

Item 1B | |||

Item 2 | |||

Item 3 | |||

Item 4 | |||

PART II | |||

Item 5 | |||

Item 6 | |||

Item 7 | |||

Item 7A | |||

Item 8 | |||

Item 9 | |||

Item 9A | |||

Item 9B | |||

PART III | |||

Item 10 | |||

Item 11 | |||

Item 12 | |||

Item 13 | |||

Item 14 | |||

PART IV | |||

Item 15 | |||

Item 16 | |||

The names “SELLAS Life Sciences Group, Inc.,” “SELLAS,” the SELLAS logo, and other trademarks or service marks of SELLAS Life Sciences Group, Inc. appearing in this annual report on Form 10-K are the property of SELLAS Life Sciences Group, Inc. Other trademarks, service marks or trade names appearing in this prospectus are the property of their respective owners. We do not intend the use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of or by either, of these other companies.

Unless the context otherwise indicates, references in these notes to the “Company,” “we,” “us” or “our” refer to SELLAS Life Sciences Group, Inc. and its wholly owned subsidiaries.

PART I

ITEM 1. BUSINESS

Overview

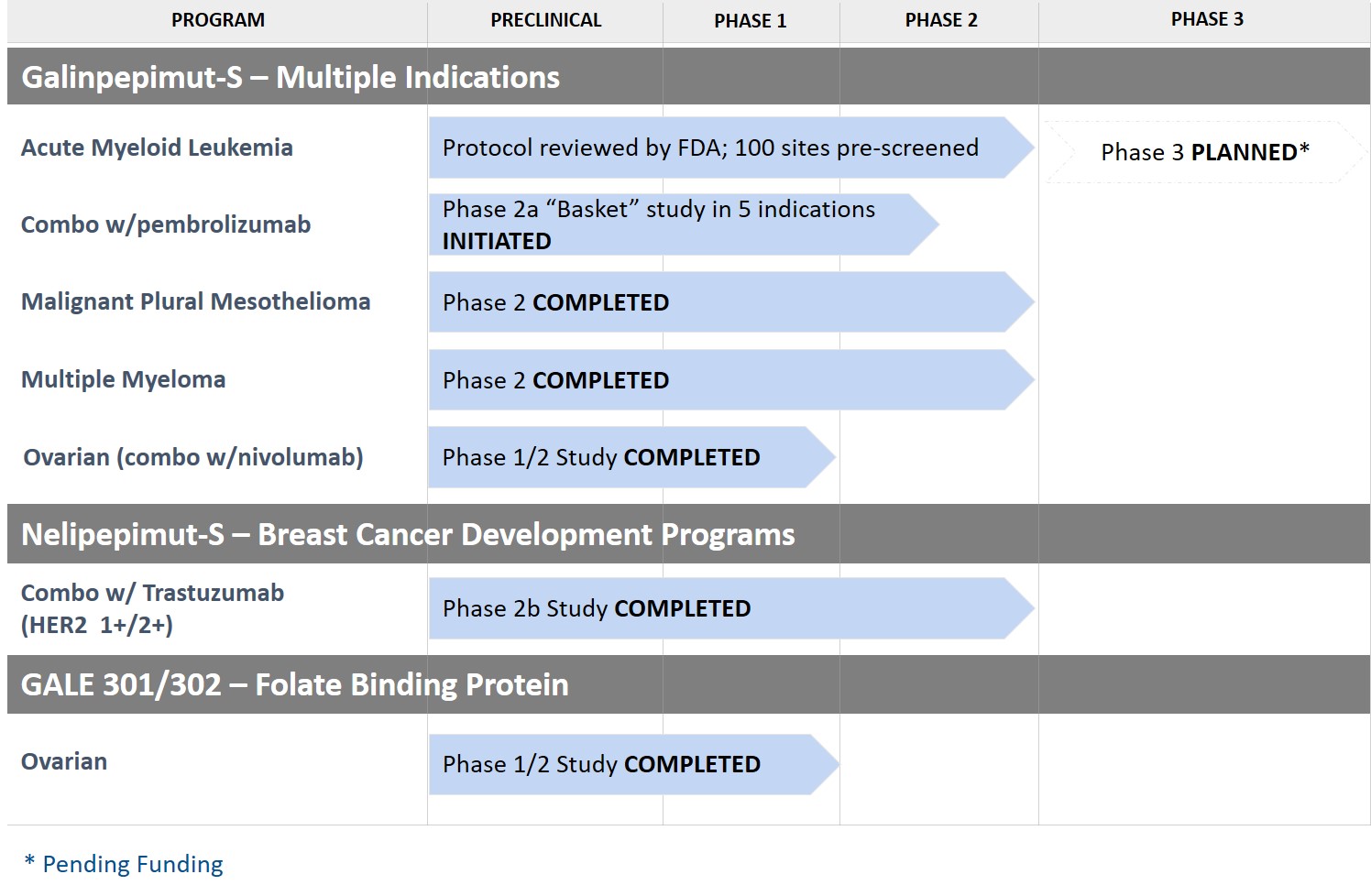

We are a clinical-stage biopharmaceutical company focused on developing novel cancer immunotherapeutics for a broad range of cancer indications. Our product candidates currently include galinpepimut-S and nelipepimut-S.

Galinpepimut-S, or GPS

Our lead product candidate, galinpepimut-S, or GPS, is a cancer immunotherapeutic agent licensed from Memorial Sloan Kettering Cancer Center, or MSK, that targets the Wilms tumor 1, or WT1, protein, which is present in 20 or more cancer types. Based on its mechanism of action as a directly immunizing agent, GPS has potential as a monotherapy or in combination with other immunotherapeutic agents to address a broad spectrum of hematologic, or blood, cancers and solid tumor indications.

In November 2018, following discussions with the U.S. Food and Drug Administration, or FDA, regarding a clinical trial design and biostatistical plan, we commenced preparations for a Phase 3 trial for GPS monotherapy in patients with acute myeloid leukemia, or AML, in the maintenance setting after achievement of their second complete remission, or CRem2, following successful completion of second-line antileukemic therapy. This trial is expected to serve as the basis for a Biologics License Application, or BLA, submission, subject to positive results. We are currently ready to start this Phase 3 trial, pending receipt of funding. The study is expected to enroll approximately 116 patients at approximately 50 clinical sites in the United States and Europe and is contemplated to have a planned interim safety and futility analysis after 80 events (deaths).

In December 2018, we initiated a Phase 1/2 multi-arm ("basket" type) clinical study of GPS in combination with Merck & Co., Inc.’s anti-PD-1 therapy, Keytruda® (pembrolizumab). We plan to enroll approximately 90 patients at up to 20 centers in the United States. The initial tumor types to be treated will be AML (in patients having achieved partial response as their best hematological response after four cycles of therapy with hypomethylating agents), and ovarian cancer (second or third line), to be followed by triple negative breast cancer, or TNBC, (second line), small cell lung cancer, or SCLC, (second line), and colorectal cancer (third or fourth line).

GPS was granted Orphan Drug Product Designations from the FDA as well as Orphan Medicinal Product Designations from the European Medicines Agency, or EMA, for GPS in AML, malignant pleural mesothelioma, or MPM, and multiple myeloma, or MM, as well as Fast Track Designation for AML, MPM, and MM from the FDA.

Nelipepimut-S or NPS

Nelipepimut-S, or NPS, is a cancer immunotherapy targeting the human epidermal growth factor receptor, or HER2, expressing cancers. Data presented in 2018 from our Phase 2b clinical trial of the combination of trastuzumab (Herceptin®) plus NPS in HER1/2+ breast cancer patients in the adjuvant setting to prevent recurrences showed a clinically and statistically significant improvement in the disease-free survival, or DFS, rate for the TNBC cohort at 24 months for patients treated with NPS plus trastuzumab of 92.6% compared to 70.2% for those treated with trastuzumab alone. In October 2018, the Data Safety Monitoring Board, or DSMB, unanimously concluded that the final analysis of the Phase 2b study data, with a median follow-up of 26 months, confirmed that TNBC patients should be the key target population for the development of trastuzumab plus NPS in the adjuvant setting in early-stage HER2 1+/2+ breast cancer patients. We are having ongoing discussions with the FDA in the first half of 2019 to define an optimal path for further development of the combination of NPS plus trastuzumab in TNBC and expect to complete these discussions the first half of 2019.

2

FBP-targeting bivalent vaccine (GALE-301/-302)

GALE-301 and GALE 302 are cancer immunotherapies that target the E39 peptide derived from the folate binding protein, or FBP. In a Phase 1/2a investigator sponsored trial, or IST, assessing GALE-301 in ovarian and endometrial cancers, we observed improvement in the 24-month DFS rate, in a small number of patients treated with the optimal dose. We are evaluating GALE-301/302 for potential internal development in a Phase 2 setting for ovarian cancer, strategic partnership, or other type of candidate rationalization.

The chart below summarizes the current status of our clinical development pipeline:

Recent Developments

In February 2019, we engaged Cantor Fitzgerald & Co. to explore a wide range of strategic alternatives to further our business plan, with the ultimate objective being an outcome that is in the best interest of shareholders. Such alternatives may include, but are not limited to, a sale of the Company, a business combination, a merger or reverse merger with another company, a strategic investment/financing or a funded collaboration or partnership. To the extent that this engagement results in a transaction, our business objectives may change depending upon the nature of the transaction. There can be no assurance that we will enter into any transaction as a result of the engagement.

On March 6, 2019, we entered into a Warrant Exercise Agreement, or the Exercise Agreement, with one of the holders of our warrants issued in July 2018. Pursuant to the Exercise Agreement, such holder agreed that it would cash exercise up to 3,800,000 of its warrants issued in July 2018 into shares of common stock at a reduced exercise price of $1.10 per share for any warrants exercised prior to May 31, 2019. In addition to reducing the exercise price of the warrants, the Exercise Agreement also provides for the issuance of new warrants to purchase up to an aggregate of approximately 3,800,000 shares of common stock at an exercise price of $1.40 per share, or New Warrants, to be issued on a share-for-share basis in an amount equal to the number of the warrants that are cash exercised by the holder by May 31, 2019. To date, the holder has exercised approximately 1.2 million warrants for gross proceeds of $1.3 million and approximately 1.2 million New Warrants were issued. We may receive aggregate gross proceeds of up to approximately $4.2 million from the cash exercise if all of the warrants under the Exercise Agreement are exercised.

3

Merger of SELLAS Life Sciences Group Ltd. and Galena Biopharma, Inc.

On December 29, 2017, we completed the business combination with the privately held Bermuda exempted company, Sellas Life Sciences Group Ltd., or Private SELLAS, in accordance with the terms of the Agreement and Plan of Merger and Reorganization, dated as of August 7, 2017 and amended November 5, 2017, or the Merger Agreement, among SELLAS Life Sciences Group, Inc., Sellas Intermediate Holdings I, Inc., Sellas Intermediate Holdings II, Inc., Galena Bermuda Merger Sub, Ltd., and Private SELLAS. We refer to this business combination throughout this annual report on Form 10-K as the Merger. Immediately after the Merger the former Private SELLAS shareholders owned approximately 67.5% of our fully diluted common stock, and the pre-Merger shareholders owned the remaining approximately 32.5%.

As a result of the Merger, our business is now substantially comprised of the business of Private SELLAS, and although we are considered the legal acquiror of Private SELLAS, for accounting purposes, Private SELLAS is considered to have acquired our company in the Merger. Consequently, the Merger is accounted for as a reverse acquisition. Upon completion of the Merger, we changed our name from “Galena Biopharma, Inc.” to “SELLAS Life Sciences Group, Inc.,” our common stock began trading on The Nasdaq Capital Market under a new ticker symbol “SLS” on January 2, 2018 and our financial statements became those of Private SELLAS.

As used in this annual report on Form 10-K, the words “we,” “us,” “our,” the “Company,” and “SELLAS” refer to SELLAS Life Sciences Group, Inc. and its consolidated subsidiaries following completion of the Merger.

4

The Cancer Immunotherapy Industry

Overview

Current treatments for cancer include surgery, radiation therapy, chemotherapy, hormone therapy, targeted therapy and immunotherapy. Cancer immunotherapy is an approach to cancer treatment that harnesses the body’s natural immune system response to fight and/or prevent tumor growth while keeping normal cells unaffected or delivering certain immune system components in order to inhibit the spread of cancer. In recent years, cancer immunotherapy drugs have emerged as a new mode of cancer treatment, alongside more established options such as surgery, chemotherapy, targeted therapy and radiation therapy.

Either as monotherapy or in combination therapies, immunotherapies may produce long-term remissions or even operational “cures” for cancers that have often been fatal until recently. A July 2016 report by Kelly Scientific Publications estimates that immunotherapies may eventually be used in as many as 60% of cases of advanced cancer. Additionally, a recent Allied Market Research report on the estimated entire market value of oncology drugs in 2020 suggests that cancer immunotherapies could represent up to 71% of that total value. Thus, cancer immunotherapy is an important and rapidly emerging field, which has led to exciting new clinical research studies and garnered the attention of investors, biotechnology and pharmaceutical companies, regulatory agencies, payors and hospital systems, cancer patients and their families and the general public at large.

Market

According to the 2018 “Global Oncology Trends” report by the IQVIA Institute, the global market for cancer drugs (including immunotherapy drugs) is expected to reach $200 billion by the end of 2022, growing at a compound annual growth rate, or CAGR of 10-13% between 2017 and 2022. According to a 2018 report by Data Bridge Market Research (Pune, India), MarketsandMarkets, the global cancer immunotherapy market is expected to reach $202.89 billion by 2025, growing at a CAGR of 14.1% during the forecast period of 2018 to 2025. Approximately 90% of the immunotherapy market is comprised of immune synapse modulators (which includes checkpoint inhibitors and immune synapse co-stimulators), which leaves approximately 10% for other major immunotherapies, which include peptide cancer active immunizers such as our product candidates, GPS and NPS.

Products/Pipeline

Galinpepimut-S (GPS)

Overview

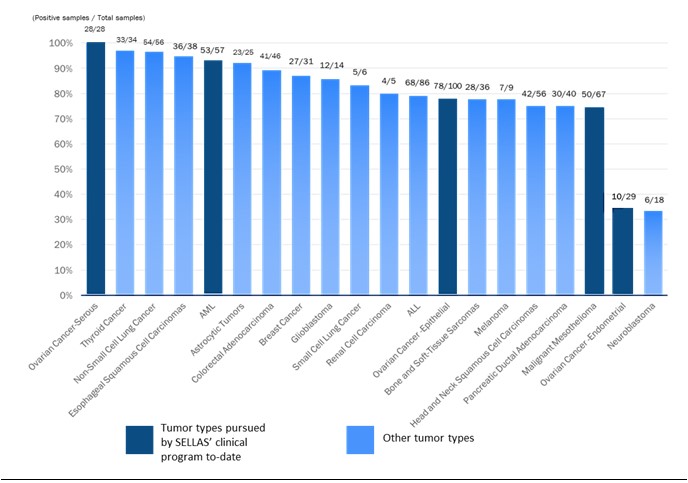

GPS is a WT1-targeting peptide-based cancer immunotherapeutic being developed as a monotherapy and in combination with other therapeutic agents to treat different types of cancers that result from uninhibited tumor cell growth. GPS targets malignancies and tumors characterized by an overexpression of the WT1 protein. The WT1 protein is one of the most widely expressed cancer proteins in multiple malignancies. A 2009 pilot project regarding the prioritization of cancer antigens (substances that evoke an immune response) conducted by the National Cancer Institute, or NCI, a division of the National Institutes of Health, or NIH, ranked the WT1 protein as a top priority for immunotherapy.

WT1 is a protein that resides in the cell’s nucleus and participates in the process of cancer formation and progression. As such, it is classified as an “oncogene.” WT1 plays a key role in the development of the kidneys in fetal life, but then almost disappears from normal organs and tissues. In a wide variety of cancers (20 or more cancer types), WT1 becomes detectable again in at least 50% of tumor pathology specimens in the cells of these cancers. WT1 appears in large amounts (i.e., becomes “overexpressed”) in numerous hematological malignancies, including AML, MM and CML, as well as in many solid malignancies such as MPM, gastrointestinal cancers (such as colorectal cancer), glioblastoma multiforme, TNBC, ovarian cancer and SCLC.

5

The following figure shows the ratio of samples testing positive for WT1 to those testing negative for WT1 in a number of different malignancies.

WT1 EXPRESSION FREQUENCY ACROSS VARIOUS CANCERS

(Positive samples / Total samples)

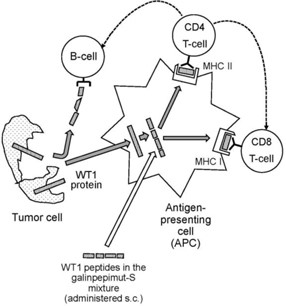

Mechanism of Action in Immune System

GPS is a multi-peptide product that has been modified to enhance the degree and duration of the immune response against the WT1 protein. The modification is based on the fact that two of the four peptides in the peptide mixture comprising GPS are deliberately mutated in a single amino acid residue. These mutated peptides are recognized by the immune system as non-self-entities and are therefore less likely to induce immune tolerance. After administration of these mutated peptides, the patients become immunized against the corresponding native versions of these peptides (which are expressed by the tumor cells), and thus, are able to cross-react against them, which concept is called the heteroclitic principle.

6

We believe that GPS has a mechanism of action that involves direct activation of the patient’s immune system specifically and solely against the WT1 protein. Although the immune system is designed to identify foreign or abnormal proteins expressed on tumor cells, this process is often defective in cancer patients. Typically, patients harboring WT1-positive malignancies have very few or no T cells specifically reactive or responsive to, and therefore activated by, WT1. T cells are involved in both sensing and killing abnormal cells, in addition to coordinating the activation of other cells in an immune response. T cells can be classified into two major subsets, CD4 cells and CD8 cells. CD8 cells are characterized by a CD8 protein on their cell surface that allow them to recognize, bind and kill cells infected by cancer cells. CD4 cells, known as helper T cells, are critical to providing the signals necessary for sustained CD8 cell responses and are also capable of exerting direct anti-tumor activity. GPS is designed to elicit both CD4 and CD8 cell immune responses. We believe that the activation of CD8 cells by GPS could lead to direct cancer cell killing, or cytotoxicity, and the eventual establishment of immunologic memory against a WT1-expressing cancer. This occurs by two mechanisms: (i) conversion of some of the activated CD8 cells to CD8 memory cells, and (ii) activation of CD4 cells and the eventual creation of CD4 terminal effective memory cells.

We believe that, with respect to the conversion of activated CD8 cells, the GPS stimulated CD8 cells transform into cytotoxic T-lymphocytes, or CTLs, which are expected to be able to attack and destroy specifically WT1-positive cancer cells. Each CTL typically destroys one WT1-positive cancer cell, but they have been shown to be able to kill up to 10 to 20 WT1-positive cancer cells. Further, with respect to the activation of CD4 cells, we believe that CD4 cells are stimulated to produce WT1-specific, helper T cells, which are able to in turn activate CTLs and B cells. The B-cells “helped” by the helper T cells produce antibodies to specific WT1 epitopes. The anti-cancer effect is considered to be a result of a combination of all of the above actions, as well as possible additional, less clear mechanisms involving other immune cell types (e.g., natural killer cells) that are not as widely understood.

The following diagram illustrate GPS’ mechanism of action:

GPS cannot be administered to patients in a water-soluble form, and so it is given under the skin, or subcutaneously. If administered on its own, GPS would rapidly degrade and would not have the opportunity to activate the immune system. Therefore, GPS is mixed with Montanide™, a commercially available, non-specific immune adjuvant composed of a natural metabolizable oil and a very refined emulsifier, creating a dense emulsion. Montanide is co-administered with GPS by subcutaneous injection to optimally activate cellular and humoral immune responses in vaccinated patients. Additionally, prior to the administration of GPS, patients receive another immune adjuvant, granulocyte-macrophage colony-stimulating factor, or GM-CSF, to non-specifically stimulate and activate antigen-presenting cells, or APCs, in the vicinity of the subcutaneous injection of GPS.

7

After subcutaneous injection, the WT1 peptides within GPS disperse locally underneath the injection site and at local lymph nodes and are ingested by APCs. Digested peptide fragments are then presented on the surface of APCs to CD8 and CD4 lymphocytes while simultaneously associated on the cell membrane with major histocompatibility complexes, or MHC, human leukocyte antigen, or HLA molecules. This process activates the CD4 and CD8 cells and sensitizes them to the key 25 epitopes of WT1, thus initiating the process of short- and long-term T-cell-mediated immunity against WT1.

8

Key Features

The following table summarizes the key features of GPS:

Key features of an Optimal Cancer Active Immunizer Therapeutic | GPS Properties and Clinical Strategy | |

Selecting the right target antigen and epitopes within that antigen | Four peptides and 25 epitopes selected optimally with the objective of ensuring: - optimal MHC complex presentation; - specificity across different HLA types; - production of both CD4 and CD8 activated cells; and - the ability to apply the heteroclitic principle, as described above, to overcome tolerance. | |

Optimal T-cell engagement leading to cancer cell destruction | Immune response data from the final analysis of the Phase I clinical study of GPS in MM in 12 evaluable patients that were presented at the 44th Annual Meeting of the European Society for Blood and Marrow Transplantation, or EBMT, in 2018 (Dr. Kohne et al.) showed 75% frequency of either CD8+ or CD4+ responses to an all-pool mixture of WT1-derived antigens after completion of the 12 vaccinations per the study protocol. This evidence of multi-epitope, broad cross-reactivity along the full-length of the WT1 protein is suggestive of epitope spreading, as it emerged across epitopes against which the patients were not specifically immunized. These data corroborate the results of an earlier analysis in mid-2017 and strongly suggest stimulation of T cells towards intracellular antigen fragments from GPS-induced destruction of tumor cells, which effect is a hallmark of an effective vaccine, e.g., that it is targeting the right epitopes chosen by design. | |

Overcoming the barriers of an adverse/immunosuppressive tumor micro-environment, or TME | The GPS monotherapy clinical studies are in the setting of complete remission, or CRem, and minimal residual disease, or MRD, whereby no bulky or measurable tumor deposits exist. This is typically seen after successful frontline therapy in select cancer types for which such debulking standard therapies exist (e.g., AML or MPM). In these settings, the tumor micro-environment, or TME, is substantially absent. We are also pursuing combination therapy with checkpoint inhibitors in tumor settings whereby measurable disease exists, as contemporaneous checkpoint inhibition would abrogate the immunosuppressive effects of the TME. | |

Overcoming or mitigating immune tolerance | Heteroclitic peptides are those in which mutations have been deliberately introduced in the amino acid sequence. The use of heteroclitic peptide in an active immunizer, such as GPS, increases immunogenicity without changes in the antigenicity profile, as well as strengthens MHC binding of the peptide to produce cytotoxic CD8 cells that continue to recognize the corresponding native peptide sequence. This is believed to be a key factor differentiating GPS from essentially all previously developed peptide vaccines, and applies a highly innovative technology platform, peptide heteroclicity, in a clinical late-stage cancer immunotherapeutic candidate product. | |

Addressing the broadest possible candidate patient population | GPS has activity across multiple HLA types that could allow treatment of a vast majority of global patient populations harboring WT1-positive malignancies. | |

9

Potential Key Differentiators

GPS’ potential key differentiators as compared to other active immunization or vaccine-type approaches, as well as compared to immunotherapy approaches more generally, are as follows:

• | heteroclitic peptides may offer increased immune response and less potential for tolerance; |

• | multivalent oligopeptide mixture potentially drives differentiated immunotherapeutic efficacy, targeting 25 key epitopes of WT1; |

• | potentially applicable to 20 or more cancer types worldwide and the vast majority of HLA types; |

• | CRem or MRD status (after initial tumor debulking with preceding standard therapy) is the preferred setting for GPS monotherapy; |

• | not directly competitive with current clinical standard of care therapies, but rather believed to complement them in the maintenance setting; |

• | potential for combination approaches with other cancer immunotherapies, due to tolerable adverse event profile; |

• | anticipated cost-effective manufacturing; allogeneic, “off-the-shelf,” vialed subcutaneously administered drug that is not patient-specific; and |

• | positive Phase 2 clinical data on effectiveness (based on overall survival, or OS, in AML and progression-free survival, or PFS, in MM) with good tolerability and a favorable safety profile. |

Development Program for GPS

GPS has the potential as a monotherapy or in combination with other immunotherapeutic agents to address a broad spectrum of hematologic, or blood, cancers and solid tumor indications. We are currently exploring the potential role for GPS in both monotherapy and combination therapy environments:

• | GPS monotherapy: Phase 2 clinical trials of GPS as monotherapy for AML, MPM and MM have been completed and we are planning (pending funding availability) a Phase 3 registrational trial in AML. |

• | GPS combination therapy: A Phase 1/2a clinical trial of GPS in combination with nivolumab (Opdivo®) for ovarian cancer has been completed. The clinical trial was independently sponsored by MSK. In December 2018, we initiated a Phase 1/2 multi-arm ("basket" type) clinical trial of GPS in combination with the anti-PD-1 therapy Keytruda (pembrolizumab) in collaboration with a Merck & Co., Inc., Kenilworth, N.J., U.S. subsidiary (known as MSD outside the United States and Canada), or Merck. The purpose of the basket trial is to determine if the administration of GPS in combination with pembrolizumab has the potential to demonstrate clinical activity in the presence of macroscopic disease, where monotherapy with either agent would have a more limited effect. |

10

Targeted Indications

GPS Monotherapy for Acute Myeloid Leukemia (AML)

Current AML Treatment Therapies

AML is an aggressive and highly lethal blood cancer characterized by the rapid growth of abnormal white blood cells that build up in the bone marrow and interfere with the production of normal blood cells. Its symptoms include fatigue, shortness of breath, bruising and bleeding, and increased risk of infection. The cause of AML is unknown, and the disease is typically fatal within weeks or months if untreated. AML most commonly affects adults, and its incidence increases with age. Until recently, the overall treatment landscape for AML had remained static for decades, as numerous targeted and antiproliferative agents were unsuccessful in according meaningful long-term clinical benefits, including increments in survival. Standard treatments included chemotherapy as well as hypomethylating agents, or HMAs, while select patients could have also undergone a hematopoietic, or blood-forming, stem cell transplant, or allo-HSCT. Recently approved agents that target mutations of the isocitrate dehydrogenase, or IDH, type-1 and -2 proteins and the FMS-like tyrosine-protein kinase, or FLT3, proteins, as well as the novel fixed-combination of chemotherapy Vyxeos and the CD33-targeting antibody-drug conjugate gemtuzumab ozogamicin, as well as the B-cell lymphoma 2 (bcl-2) inhibitor venetoclax, have led to modest incremental improved patient outcomes. Nonetheless, the goal of upfront therapy for AML is to achieve a state of CRem. CRem is defined per consensus criteria by the European Leukemia Net, whereby the hematologic and clinical features of the disease are no longer detected. Other than a successful completion of an allo-HSCT in AML, we are not aware of any therapies that have shown any meaningful long-term benefit after patients achieve a CRem status. Without allo-HSCT, once the disease relapses, second-line therapies can be given, but these have shown very limited positive clinical impact to date and their benefit is transitory; eventually AML patients who do not undergo an allo-HSCT generally succumb to AML or complications associated with it.

The AML indication was chosen for first-in-human clinical studies of GPS for the following reasons:

• | AML presents a clinical setting in which CRem status can be achieved with standard upfront therapy; |

the high degree of unmet medical need in AML and the absence of an effective maintenance therapy over the decades after initial upfront induction until and immediately after achievement of CRem status, particularly in patients older than 60 years of age;

the almost universal expression of WT1 in leukemic blasts, which are AML’s malignant cells, as well as leukemic stem cells, or LSCs, cells that are or become extremely resistant to standard chemotherapy or targeted agent approaches and which can be realistically eradicated only with immunotherapy methods (including allo-HSCT). LSCs have been shown to be susceptible to targeting by cytotoxic T cells (CD8 and CD4 cells) stimulated against leukemia-associated antigens and we predicted this would be the case for GPS;

• | the fact that WT1 has been associated with the actual development of leukemia; |

• | the positive correlation between the level of expression of WT1 and the prognosis in AML; |

• | the fact that the level of expression of WT1 can be followed over time in patients during and after therapy, including immunotherapy, as a method of monitoring for MRD; |

• | early evidence from mouse models that vaccination with peptides against select WT1 antigenic epitopes leads to detection of immune response; |

• | early evidence that human immunocytes sensitized ex-vivo to peptides contained in GPS were able to recognize naturally presented WT1 peptides on the surface of several leukemia cell lines; |

• | early anecdotal (at the time) clinical data showing antileukemic activity of WT1 monovalent vaccines in the Japanese population (albeit restricted to HLA-A*2401 type), as well as a dendritic cell vaccine in the Netherlands (independent of HLA haplotype); |

11

• | a predictive assumption of very low to negligible degree of clinical toxicity with a WT1-targeted immunotherapy such as GPS, due to the fact that WT1 in normal, non-cancerous, tissues is both expressed at extremely low levels and limited in number of organs and tissues, but also due to the fact that WT1 fragments, or peptide epitopes, in normal cells are presented to host APCs in a different manner than are WT1 fragments produced in cancer cells; of note, WT1 expression in normal tissues of adults is limited to the podocyte layer of the glomerulus (kidney), Sertoli cells (testis), granulosa cells (ovary), decidual cells (uterus), mesothelial cells (peritoneum, pleura), mammary duct and lobule (breast), and blood-forming (hematopoietic) progenitor cells (CD34+ cells in the bone marrow); and |

• | the advent of modern immunotherapeutics in cancer and the promise of an innovative, off-the-shelf immunotherapy for AML, a disease that has historically been associated with dearth of deep and sustained responses to checkpoint inhibitors. |

GPS has been granted Fast Track and Orphan Drug designations by the FDA for the treatment of AML.

AML Clinical Data

In an initial pilot clinical trial in AML, a total of nine adult patients of all ages with de novo AML were treated with upfront standard chemotherapy and were able to achieve their first complete remission, or CRem1. Administration of GPS resulted in a median OS that was at least 35 months from the time of GPS administration. In this study, specifically for patients who were 60 years and older (n=5), median OS was at least 33 months from the time of GPS administration or approximately 43 months from the time of initial AML diagnosis. The mean time of follow-up was 30 months from the time of diagnosis at the time of this analysis for all patients. Of the eight patients tested for immunologic response, seven, or 87.5%, demonstrated a WT1-specific immune response.

In a subsequent Phase 2 clinical trial in AML, a total of 22 adult patients of all ages with de novo AML were treated with upfront standard chemotherapy and were able to achieve CRem1. Most patients also received one to four cycles of “consolidation” chemotherapy per standard AML treatment guidelines. GPS was then administered within three months from the completion of the consolidation chemotherapy regimen in up to 12 total doses: six initial doses (priming immunization) followed by six additional “booster” immunizations over a total period of up to 15 months to qualifying patients (i.e., patients who were clinically stable and did not show disease recurrence after the first six injections). This Phase 2 clinical trial met its primary endpoint of an actual OS rate of at least 34%, measured three years into the clinical trial (i.e., percentage of patients alive after three years of follow-up). An actual OS rate of 47.4% was demonstrated at three years post-GPS treatment, exceeding historical published data of OS of 20% to 25% by 2.4- to 1.9-fold (or 240% to 190%), respectively.

GPS administration was also shown to improve OS in comparison to historical data in patients in CRem1. Administration of GPS resulted in a median OS that was poised to exceed 67.6 months from the time of initial AML diagnosis in patients of all ages, which represents a substantial improvement compared to best standard therapy. Only five of the 22 patients underwent allo-HSCT and an ad hoc statistical analysis failed to show a significant effect of the transplant upon OS (either in median survival times or survival rates at specific landmark time-points). In this study, the patients’ median age was 64 years old. The most frequent toxicities were mild to moderate local skin reactions and inflammation, as well as fatigue, which were self-limited and responded to local supportive measures and analgesics. None of the patients developed significant serious or high grade systemic adverse reactions (including anaphylaxis) attributable to GPS. GPS elicited WT1-specific immune responses in 88% of patients, including CD4 and CD8 T-cell responses. Further, the heteroclitic principle was confirmed, in that immune responses were seen against the native version of the two mutated WT1 peptides within the GPS mixture. The results showed a trend in improved clinical outcomes in patients who mounted an immune response with GPS compared to those patients who did not. Importantly, a preplanned subgroup analysis for the cohort of 13 patients within the clinical trial who were 60 years of age or older demonstrated a median OS of 35.3 months from time of initial diagnosis. Comparable historical populations have a median OS ranging from 9.5 to 15.8 months from initial diagnosis, which represents a 2.25 to 3.75-fold improvement in OS associated with GPS therapy in the CR1 maintenance setting as contrasted to these historical cohorts of broadly comparable patients.

12

An additional Phase 2 clinical trial of GPS was performed at the H. Lee Moffitt Cancer Center & Research Institute, or Moffitt. This Phase 2 trial included 10 AML patients who had received first-line therapy for their disease, who then experienced relapse and were subsequently treated with second-line chemotherapy and achieved a CRem2. This group of patients had a more advanced disease in comparison to those treated in the Phase 2 clinical trial discussed above, and typically demonstrated a historical OS of less than ~8 months, even with post-CRem2 allo-HSCT. In the Moffitt trial, the efficacy of GPS (measured as median OS from the time of administration of a maintenance therapy to immediately after achievement of CRem2) was compared with that of “watchful waiting” in a cohort of 15 contemporaneously treated (but not matched by randomization) broadly comparable patients treated by the same clinical team at Moffitt. GPS administration resulted in a median OS of 16.3 months (495 days) compared to 5.4 months (165 days) from the time of achievement of CRem2. This was a statistically significant difference (P=0.0175). Two of 14 AML patients demonstrated relapse-free survival of more than one year. Both such patients were in CRem2 at time of GPS administration, with duration of their remission exceeding duration of their CRem1, strongly suggesting a potential benefit based on immune response mechanisms. GPS was well-tolerated in this clinical trial.

13

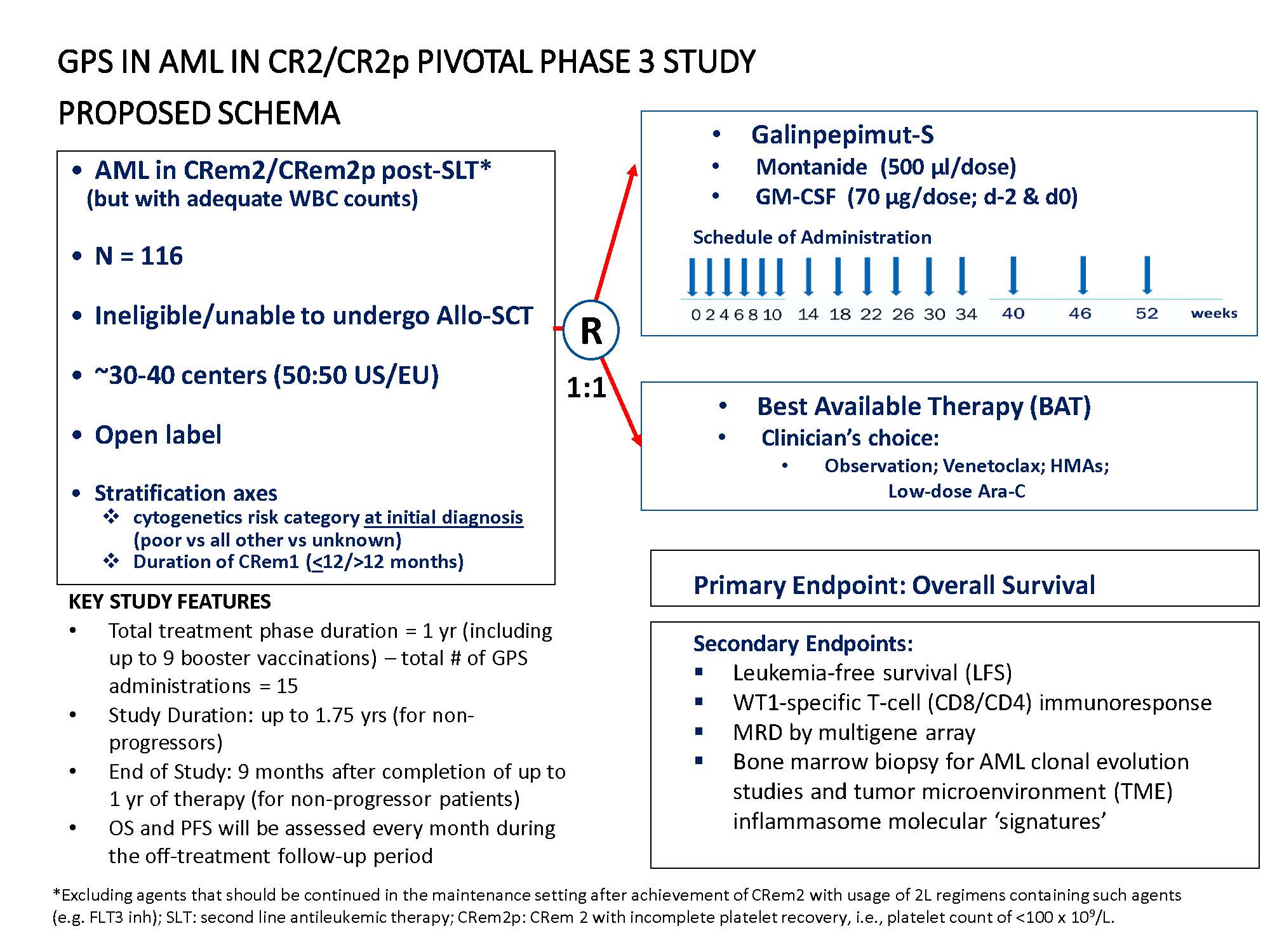

AML Planned Phase 3 Clinical Trial

We are planning a Phase 3 registrational study for GPS in AML pending funding availability. This study is planned to be a 1:1 randomized, open-label study comparing GPS in the maintenance setting to investigators’ choice of best available treatment, or BAT, in adult AML adult patients (age >18 yrs) who have achieved their second hematologic (morphological) complete remission, with or without thrombocytopenia (CRem2/CRem2p; with “p” designating platelets), after second-line antileukemic therapy and who are deemed ineligible for or unable to undergo allo-HSCT. This study will serve as the basis for a biologics license application, or BLA, submission, subject to positive results.

The Phase 3 study is expected to enroll approximately 116 patients at approximately 50 clinical sites in the United States and Europe. The primary endpoint is OS and secondary endpoints include leukemia-free survival, antigen-specific T-cell immune response dynamics over time and rates of achievement of MRD negativity. The study will have a planned interim safety and futility analysis after 80 events (deaths). The key features and schema of this study are shown in the following graphic:

14

GPS Monotherapy in Other Indications

Malignant Pleural Mesothelioma (MPM)

MPM is an asbestos-related cancer that forms on the protective tissues that cover many of the internal organs. The most common area affected is the lining of the lungs and abdomen, though it can also form around the lining of the heart. Most cases are traced to job-related exposures to asbestos and it can take approximately 40 years between exposure and cancer formation. Symptoms may include shortness of breath, a swollen abdomen, chest wall pain, cough, feeling tired, and weight loss. MPM is generally resistant to radiation and chemotherapy, and long-term survival is rare, even in cases where aggressive upfront debulking multimodality therapy (i.e., extirpative surgery, chemotherapy and in some cases radiotherapy, often described as “trimodality therapy” when used to treat MPM) are used.

A randomized, double-blind, placebo-controlled Phase 2 clinical trial in MPM patients enrolled a total of 41 patients at MSK and M.D. Anderson Cancer Center. Data from this Phase 2 clinical trial was presented in 2016. Based on an initial analysis of 40 patients who were eligible at the time with a median follow-up of 16.3 months, a median OS of 24.8 months was seen for GPS-treated MPM patients, compared to a median OS of 16.6 months for patients in the control arm. For patients with a basic reproductive ratio tumor resection and subsequent treatment with GPS, a significant survival benefit was observed compared to those who received a placebo, with a median OS of 39.3 months compared to 24.8 months (HR: 0.415) in favor of GPS. In a subsequent analysis for the entire cohort (n=41) in August 2016, with a median follow-up of 17.2 months, a median OS of 22.8 months was observed for GPS-treated MPM patients, compared to a median OS of 18.3 months for patients in the control arm. In the datasets from both of these analyses, GPS was shown to induce WT1-specific CD8 and CD4 T-cell activation. There were no clinically significant severe adverse events in this study.

Multiple Myeloma (MM)

MM is a cancer formed by malignant plasma cells, and its cause is unknown. The overgrowth of plasma cells in the bone marrow crowds out normal blood-forming cells, causing low blood counts and anemia (a shortage of red blood cells). MM can also cause a shortage of platelets (cells responsible for normal blood clotting) and lead to increased bleeding and bruising, along with problems fighting infections due to low white cell counts and/or lower levels of infection-fighting antibodies. MM causes a host of organ problems and symptoms, including fatigue, bone pain, fractures, circulatory problems (in small vessels of the brain, eye retina, heart, bowel, etc.) and kidney failure. Treatment for MM includes chemotherapy, glucocorticoids, drugs that modulate the immune system (immunomodulatory drugs, or IMiDs), radiation and autologous stem cell transplants, or ASCTs. The prognosis in MM is highly variable and depends on numerous risk factors, some related to the biology of the disease, others to the host (e.g., age and functional status). Consequently, median survival can vary from up to at least 15 years in non-high-risk patients who achieve CRems, as defined by the International Myeloma Working Group, or IMWG, criteria, to approximately three years (from time of initial treatment) in patients with MM who achieve less than partial response, or PR, after ASCT. There are patients with MM who fare even more poorly than described above. For example, those in the immediately aforementioned group who also have high-risk cytogenetics at baseline may survive on average less than three years. Similarly, patients who are ineligible for ASCT and are managed only with chemotherapy and long-term IMiD maintenance (with up to nine cycles of lenalidomide) who also achieve less than CRems and remain MRD-positive demonstrate a three-year OS rate of only about 55%; these landmark three-year OS rates decrease by approximately 40 to 50% in patients who also have high-risk cytogenetics at baseline. Despite significant therapeutic advances in the management of MM, the prognosis of patients with high-risk cytogenetics at the time of diagnosis remains quite poor, even when they successfully complete an ASCT, particularly if such patients continue to have evidence of MRD.

15

We have reported comprehensive final data from a Phase 2 study for GPS in 19 patients with MM. All non-progression events were confirmed and remained ongoing as of the time of the latest presentation (median follow-up at 20 months for survivors). The data indicate promising clinical activity among MM patients with high-risk cytogenetics at initial diagnosis who also remain MRD(+) after successful frontline therapy (induction regimen followed by ASCT). This subgroup of MM patients, when serially assessed per IMWG criteria, typically relapse/progress within 12 to 14 months after ASCT, even when they receive maintenance therapy with IMiDs such as thalidomide or proteasome inhibitors such as bortezomib. Of note, 18 of the 19 patients received lenalidomide maintenance starting after the first three GPS administrations following ASCT; the remaining single patient received bortezomib under the same schedule. All patients had evidence of at least MRD after ASCT, while 15 of the 19 also had high-risk cytogenetics at diagnosis. Combined, these characteristics typically result in low PFS rates that do not exceed 12 to 14 months following ASCT, even while on maintenance therapy with IMiDs or proteasome inhibitors, which are the current standards of care. As of June 2017, median PFS with GPS was 23.6 months, while median OS had not been reached. Our results compare favorably with an unmatched cohort of broadly comparable MM patients with high-risk cytogenetics published by the Spanish PETHEMA group from the PETHEMA Network No. 2005-001110-41 trial. Our GPS therapy demonstrated a 1.87-fold increase in median PFS, as well as a 1.34-fold increase in the PFS rate at 18 months compared to the aforementioned historical cohort, which included MM patients with high-risk cytogenetics and MRD(+) post-ASCT and on continuous intensive maintenance with thalidomide +/- bortezomib. The safety profile was devoid of grade 3/4/5 treatment-related adverse events. Immune response data showed that up to 91% of patients had successfully developed T-cell (CD8 or CD4) reactivity to any of the four peptides within the GPS mixture, while up to 64% of patients demonstrated immune response positivity (CD4/CD8) against more than one WT1 peptide (multivalent responses). Moreover, multifunctional cross-epitope T-cell reactivity was observed in 75% of patients to antigenic epitopes against which hosts were not specifically immunized, in a pattern akin to epitope spreading. Further, a distinctive link was shown between the evolution of immune responses and changes in clinical response status (achievement of CR/very good partial response clinical status per IMWG criteria) over time following treatment with GPS, with each patient being used as his or her own control for each longitudinal comparison. This association has not been previously described for a peptide vaccine in MM. We believe that these results offer mechanistic underpinnings for immune activation against WT1 in patients with aggressive, high-risk MM, and support the potential antimyeloma activity of GPS.

GPS Combination Therapy with PD-1 blocker (nivolumab) for Ovarian Cancer

Epithelial cancer of the ovary, or ovarian cancer, is a relatively common gynecologic cancer that develops insidiously, and hence is associated with vague or no symptoms that would urge patients to seek medical attention. Not surprisingly, most women with ovarian cancer present with advanced (at least locally or regionally, and often systemically spread) disease. Ovarian cancer is managed with initial surgical resection followed by platinum-based chemotherapy. During the past decade, incremental advances in chemotherapy, and the introduction of targeted therapies (such as poly-ADP-ribose polymerase inhibitors and several others) and specially formulated compounds (such as liposomal anthracyclines) have resulted in improved survival and in more effective treatment of relapsed disease. In addition, a better understanding of genetic risk factors, along with aggressive screening, has permitted a tailored approach to preventive strategies, such as bilateral salpingo-oophorectomy in selected women along in specific patient populations genetically predisposed to this cancer (such as those harboring genetic alterations of the BRCA gene family). Although a complete clinical remission following initial chemotherapy can be anticipated for many patients, a review of “second-look” laparotomy, when it was often performed as a matter of routine care, indicates that less than 50% of patients are actually free of disease. Furthermore, nearly half of patients with a negative “second-look” procedure relapse and require additional treatment. Many patients will achieve a CRem2 clinical response with additional chemotherapy. However, almost all patients will relapse after a short remission interval of nine to 11 months. Effective strategies, such as introduction of novel immunotherapies, to prolong remission or to prevent relapse are required, as subsequent remissions are of progressively shorter duration until chemotherapy resistance broadly develops, leading to eventual disease-related demise.

16

Ovarian cancer represents an intriguing opportunity to study both the clinical and immunologic effects of GPS in another solid tumor. Additionally, therapeutic targeting of WT1 through immune pathways has largely not been pursued by others to date for this indication and ovarian cancer remains “incurable” once it advances and becomes disseminated, even in the face of significant advances in the field. Ovarian cancer was chosen as a target indication for the following reasons:

• | ovarian cancer presents a clinical setting whereby MRD status can be achieved with standard upfront therapy both immediately after first line therapy, but also after effective debulking of the “first relapse.” The latter subgroup of patients (after successful second line treatment/first salvage, lacking demonstrable macroscopic residual disease) would be optimal candidates for GPS therapy, as no standard maintenance therapy exists for such patients and the subsequent relapse patterns and metrics are known and predictable; |

• | the high levels of expression of WT1 in ovarian cancer cells. In fact, WT1 expression is so frequent that pathologists routinely use immunohistochemical stains for WT1 (with a standardized convention for describing expression and determining as “positive” or “negative”) to help distinguish epithelial ovarian cancers from other tumors; |

• | preliminary evidence that WT1 expression may be linked to prognosis in ovarian cancer and that it may play an anti-apoptotic role in ovarian cancer cell lines; |

• | the high degree of unmet medical need in ovarian cancer patients after first (or subsequent) successful “salvage” debulking therapy and the absence of effective therapies for such patients; and |

• | a predictive assumption of very low to negligible degree of clinical toxicity with a WT1-targeted immunotherapy such as GPS due to the fact that WT1 in normal, non-cancerous tissues is both expressed at extremely low levels and limited in number of organs and tissues, but also due to the fact that WT1 fragments, or peptide epitopes, in normal cells are presented to host APCs in a different manner than are WT1 fragments produced in cancer cells. |

GPS was studied in combination with nivolumab, a PD-1 immune checkpoint inhibitor, in an open-label, non-randomized Phase 1/pilot clinical trial, which was independently sponsored by MSK. The aim of the study was to evaluate the safety and efficacy of this combination in patients with WT1-expressing (WT1+) recurrent ovarian, fallopian tube or primary peritoneal cancer who were in second or greater clinical remission (after their successful first or subsequent “salvage” therapy). Eligible patients were devoid of macroscopic residual or recurrent disease, i.e., were free of locally or distantly metastatic deposits detectable by imaging modalities (CT, MRI and/or PET scan). This Phase 1/pilot clinical trial enrolled 11 patients with recurrent ovarian cancer who were in second or greater clinical remission at MSK, of whom 10 were evaluable. Patients enrolled in the clinical trial received the combination therapy during the clinical trial’s 14-week treatment period. Individuals who had not progressed by the end of this period also received a maintenance course of GPS. In this study, treatment was continued until disease progression or toxicity. Information on the primary endpoint of this clinical trial, which was the safety of repeated GPS administrations, for a total of six doses, in combination with seven infusions of nivolumab was presented at the ASCO 2018 annual meeting (O’Cearbhaill RE, et al). The secondary endpoint of the study was immune response, and the exploratory endpoints included landmark one-year PFS rate compared to historical controls and correlative analyses between clinical and immune responses. Exploratory efficacy interim data from this pilot trial showed that GPS, when combined with a PD-1 inhibitor, in this case nivolumab, demonstrated PFS of 64% at one year in an intent to treat the group of 11 evaluable patients with WT1+ ovarian cancer in second or greater remission. Among patients who received at least three doses of GPS in combination with nivolumab, PFS at one year was 70% (7/10). The historical rates with best standard treatment do not exceed 50% in this disease setting. The most common adverse events were Grade 1 or 2, including fatigue and injection site reactions. Dose limiting toxicity, or DLT, was observed in one patient, following the second dose of the combination. No additional adverse event burden was observed for the combination as compared to nivolumab monotherapy. The combination induced a high frequency of T- and B-cell immune responses.

17

GPS Combination Therapy with PD1 blocker (pembrolizumab) for Other Cancers

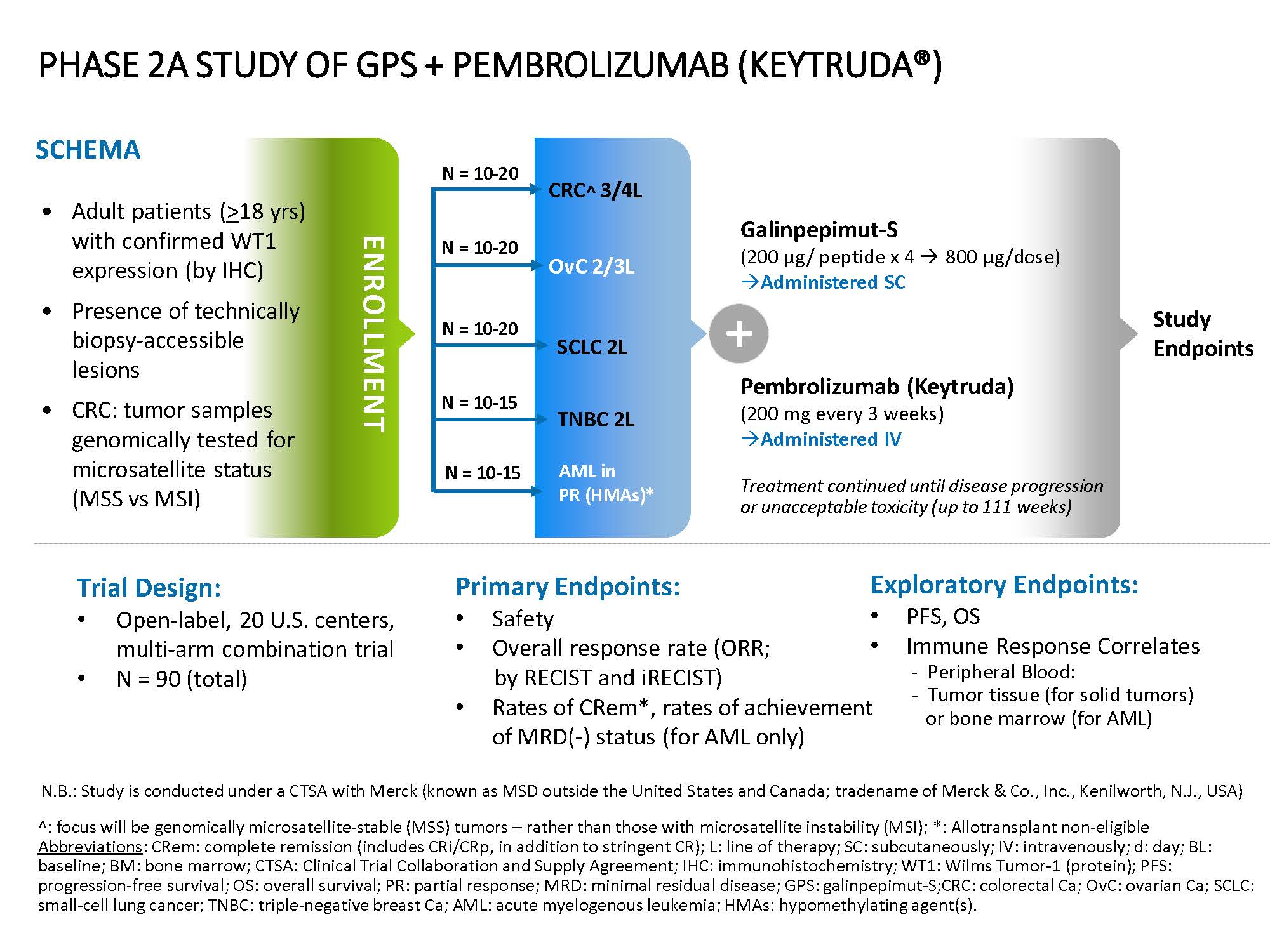

Given the potential immunobiologic and pharmacodynamic synergy between GPS and an immune check-point inhibitor (e.g., PD1 blocker), we entered into a Phase 1/2 Clinical Trial Collaboration and Supply Agreement with Merck (known as MSD outside the United States and Canada), to assess the efficacy and safety of GPS in combination with Merck’s anti-PD-1 therapy pembrolizumab with exploratory long-term follow-up for OS and safety. This is a Phase 1/2 open-label, non-comparative, multicenter, multi-arm study of patients with WT1-positive advanced cancers, including both hematologic malignancies and solid tumors. The initial tumor types to be treated are AML (patients unable to attain deeper morphological response than PR on hypomethylating agents and who are either ineligible for or unable to undergo allo-HSCT and ovarian cancer (second or third line), to be followed by TNBC (second line), SCLC (second line), and colorectal cancer (third or fourth line). This clinical study was initiated in December 2018 and we plan to enroll approximately 90 patients in up to 20 centers in the United States only.

The purpose of this five-arm “basket” trial is to determine if the administration of GPS in combination with pembrolizumab has the potential to demonstrate clinical activity in the presence of macroscopic disease, where monotherapy with either agent would have a more limited effect. The negative influence of TME factors on the immune response is predicted to be mitigated by PD1 inhibition (by pembrolizumab), thus allowing the patients’ own immune cells to invade and destroy cancerous growth deposits specifically sensitized against WT1 (by concomitantly-administered GPS). The key features and schema of this study are shown in the graphic below:

18

NPS (nelipepimut-S)

Our other cancer immunotherapy product, NPS, utilizes a targeted approach and is being developed to potentially: (i) prevent secondary recurrence of HER2, positive breast cancer and (ii) prevent ductal carcinoma in situ, or DCIS, from becoming invasive breast cancer. Our programs for NPS primarily target patients in the adjuvant, or after-surgery, setting who have relatively healthy immune systems but may still have residual disease. MRD, or micrometastases, that are undetectable by current radiographic scanning technologies, can result in breast cancer recurrence.

NPS is the immunodominant nonapeptide derived from the extracellular domain of the HER2 protein, a well-established and validated target for therapeutic intervention in breast and gastric carcinomas. The NPS vaccine is combined with GM-CSF (Sargramostim) for injection in between the layers of the skin epidermis, i.e., intradermal administration. Data has shown that an increased presence of circulating tumor cells, or CTCs, may predict reduced DFS, and OS, suggesting a presence of isolated micrometastases, not detectable clinically, but, over time, can lead to recurrence of cancer, most often in distant sites. After binding to the specific HLA molecules on antigen presenting cells, the NPS sequence stimulates specific cytotoxic T-lymphocytes, or CTLs, causing significant clonal expansion. These activated CTLs recognize, neutralize and destroy, through cell lysis, HER2 expressing cancer cells, including occult cancer cells and micrometastatic foci. The nelipepimut immune response can also generate CTLs to other immunogenic peptides through inter- and intra-antigenic epitope spreading.

NPS Therapy for Breast Cancer

According to NCI, over 260,000 women in the United States are diagnosed with breast cancer annually. While improved diagnostics and targeted therapies have decreased breast cancer mortality in the United States, metastatic breast cancer remains incurable. Approximately 75% to 80% of breast cancer patients test positive for some increased amount of the HER2 receptor, which is associated with disease progression and decreased survival. Only approximately 20% to 30% of all breast cancer patients have a HER2-directed, approved treatment option, i.e., trastuzumab, available after their initial standard of care. The patients are defined as having tumors demonstrating a level of HER2 expression of 3+ by immunohistochemistry, or IHC, (HER2 IHC 3+), or HER2 IHC 2+ but also being positive by HER2 gene amplification by fluorescence in situ hybridization, or FISH. This leaves the majority of breast cancer patients with low-to-intermediate HER2 expression by IHC (IHC 1+, 2+ by IHC) with tumors that are not HER2-amplified by FISH ineligible for targeted therapy with trastuzumab and without an effective targeted treatment option to prevent cancer recurrence.

In April 2018 we announced positive interim data from the prospective, randomized, single-blinded, controlled Phase 2b IST clinical trial of trastuzumab +/- NPS in HER2 1+/2+ breast cancer patients in the adjuvant setting to prevent recurrences. A pre-specified interim analysis, conducted by the DSMB of the efficacy and safety data for the study in an overall population of 275 patients as well as the two primary study target patient populations (node-positive and TNBC) after a median follow-up of 19 months, demonstrated:

• | a clinically meaningful difference in median DFS in favor of the active arm (NPS + trastuzumab), a primary endpoint of the study, with hazard ratios of 0.67 and 0.61 in the intent to treat, or ITT, and modified ITT, or mITT, populations (i.e., those who received at least one dose of vaccine or control) as well as a 34.9% and 39.5% reduction in relative risk of recurrence in the active versus control arms in the ITT and mITT populations, respectively; |

• | a clinically meaningful and also statistically significant difference between the two arms in the cohort of patients (n= 98) with TNBC, with a hazard ratio of 0.26 and a p-value of 0.023 in favor of the NPS + trastuzumab combination with a 70.4% reduction in relative risk of recurrence in the active arm versus control; |

• | a clinically meaningful and statistically significant difference between the two arms in favor of the combination in the cohort of patients not receiving hormonal therapy (n = 110), with a hazard ratio of 0.24 and a p-value of 0.009 with a 74.1% reduction in relative risk of recurrence in the active arm versus control; |

• | no notable differences between treatment arms; and |

19

• | that the addition of NPS to trastuzumab did not result in any additional cardiotoxicity compared to trastuzumab alone. |

Based on these results, the DSMB recommended that we expeditiously seek regulatory guidance from the FDA for further development of the combination of GPS plus trastuzumab for TNBC.

In October 2018, we announced the following final data at the 26-month median follow-up of the NPS +/- trastuzumab Phase 2b trial for the TNBC cohort, which confirmed the previously reported positive data:

• | clinically and statistically significant efficacy in the TNBC cohort, with a p-value of 0.013 and a 75.2% reduction in risk of relapse or death; |

• | clinically meaningful difference in median DFS in favor of the active arm (patients treated with NPS + trastuzumab) in the TNBC cohort at 24 months for patients of 92.6% compared to 70.2% for those treated with trastuzumab alone; and |

• | in all HER2 low-expressing breast cancer patients, the DFS rate was also in favor of the NPS plus trastuzumab combination (89.8%) as compared to trastuzumab alone (83.8%). |

The DSMB, in October 2018, unanimously concluded that the final analysis of the Phase 2b study data with a median follow-up of 26 months confirmed that TNBC patients should be the key target population for the development of trastuzumab plus NPS in the adjuvant setting in early-stage HER2 1+/2+ breast cancer patients and again recommended that we expeditiously seek regulatory guidance for further development for TNBC.

In November and December 2018 we announced the following positive data from a preplanned secondary efficacy analysis across HLA allele subgroups from the Phase 2b IST study:

• | the data analysis confirmed the therapeutic potential of NPS in patients with early-stage TNBC in the adjuvant setting across HLA types A-02, -03, -24 and -26, which cover approximately 80-85% of the North American/European populations and 86-90% of Asian/Pacific basin populations; |

• | in the subgroup of TNBC patients with the HLA-A24+ allele type, which is highly prevalent in the Asian population, treated with the combination of NPS and trastuzumab (n=47), the p-value is 0.003 with a 90.6% relative reduction in risk of relapse or death at 24 months and a hazard ratio of 0.08 in favor of the active (combination) arm; |

• | TNBC patients with the HLA-A24+ allele type had a significant improvement in DFS both by log-rank and landmark (24 month) analysis despite the lowest predicted binding potential between the E75 (NPS) antigen and this HLA-type; and |

• | a clinically meaningful and statistically significant decrease in the number of clinically detectable relapses in the TNBC cohort with the combination of trastuzumab and NPS (7.5%) versus trastuzumab alone (27.3%) (p=0.004). |

In a Type C meeting with the FDA in late 2018, we discussed several key points of the clinical and regulatory strategy for NPS in combination with trastuzumab for TNBC, a registration-enabling Phase 3 trial design and biostatistical plan. We expect a further meeting in the first half of 2019 to reach agreement for a final development program for NPS in TNBC.

20

Our second IST for NPS plus trastuzumab is a Phase 2 study in high-risk HER2 3+ breast cancer patients who are defined as patients with HER2 3+ (“classic” HER2+) breast cancer who have completed neoadjuvant therapy with an approved regimen that includes trastuzumab and who have failed to achieve a pathological complete response, meaning they have microscopic evidence of residual disease at the time of their primary surgery and are therefore at an increased risk of disease recurrence. The protocol for this study specified that the patients also should be HLA A2+ or HLA A3+. This multi-center, prospective, randomized, single-blinded Phase 2 clinical trial is fully enrolled with 100 patients actively participating. The rationale for this study is based on the fact that HER2 3+ patients with high risk features are known to have higher recurrence rates than all other HER2 3+ breast cancer patients. Eligible patients are being randomized to receive NPS + GM-CSF + trastuzumab or trastuzumab + GM-CSF alone. The primary endpoint of the study is DFS. Funding for this trial was awarded through the Congressionally Directed Medical Research Program, funded through the Department of Defense, via a breast cancer research program breakthrough award. In February 2017, the DSMB reported that there were no safety concerns with the trial and the trial is not futile. The pre-specified interim safety analysis was also completed on 50 patients and demonstrated that the combination is well tolerated with no increased cardiotoxicity associated with giving NPS in combination with trastuzumab. The recommendation from the DSMB was to continue the HER2 3+ trial unmodified. Top-line data is expected by the end of 2019.

NPS was previously granted Fast Track designation by the FDA for the adjuvant treatment of patients with early stage breast cancer with low to intermediate HER2 expression following standard of care upfront therapy (surgery plus chemotherapy +/- radiotherapy).

NPS for Ductal Carcinoma In Situ of the Breast (DCIS)

DCIS is defined by the NCI as a noninvasive condition in which abnormal cells are found in the lining of a breast duct and have not spread outside the duct to other tissues in the breast. DCIS is the most common type of breast neoplasm with malignant potential. In some cases, DCIS may become invasive cancer and spread to other tissues, and at this time, there is no way to know which lesions could become invasive. Current treatment options for DCIS include breast-conserving surgery and radiation therapy with or without tamoxifen, breast-conserving surgery without radiation therapy, or total mastectomy with or without tamoxifen. According to the American Cancer Society, in the United States, there were over 60,000 diagnoses of DCIS in 2015. We are supporting a Phase 2 IST to evaluate women diagnosed with DCIS who are HLA-A2+ or A3+ positive, who express HER2 at IHC 1+, 2+, or 3+ levels, and who are pre or post-menopausal. This clinical study was initiated in February 2018. Patients are being randomized to one of two arms: NPS plus GM-CSF or GM-CSF alone. The trial is sponsored and operationalized by the NCI, studying NPS’s potential clinical effects in earlier stage disease. The trial has an immunological (rather than clinical) endpoint evaluating NPS peptide-specific cytotoxic T lymphocyte (CTL; CD8+ T-cell) response in vaccinated patients.

FBP-targeting bivalent vaccine (GALE-301 and GALE-302)

GALE-301 and GALE-302 are cancer immunotherapies that target the E39 peptide derived from FBP receptor-alpha. FBP is a well-validated therapeutic target that is highly over-expressed in ovarian, endometrial and breast cancers, and is the source of immunogenic peptides that can stimulate CTLs to recognize and destroy FBP-expressing cancer cells. Current treatments after surgery for these diseases are principally with platinum-based chemotherapeutic agents. These patients suffer a high recurrence rate and most relapse with an extremely poor prognosis. GALE-301 and GALE-302 are immunogenic peptides that consist of a peptide derived from FBP combined with GM-CSF for the prevention of cancer recurrence in the adjuvant setting. GALE-301 is the E39 peptide, while GALE-302 is an attenuated version of this peptide, known as J65 (or E39’; E39-prime).

21

In a Phase 1/2a IST, assessing GALE-301 in ovarian and endometrial cancers, we observed improvement in the 24-month DFS in a small number of patients treated with the optimal dose. Patients receiving the highest dose of E39 vaccine showed a 24-month DFS of 77.9% compared to 40% for the patients in the control arm. We are evaluating GALE-301/302 for potential internal development in a Phase 2 setting for ovarian cancer, strategic partnership, or other types of product rationalizations.

In June 2016, the FDA granted two Orphan Drug Product Designations for the treatment (including prevention of recurrence) of ovarian cancer: one for GALE-301 (E39) and one for GALE-302 (J65).

Strategic Collaborations and License Agreements

Exclusive License Agreement-Memorial Sloan Kettering Cancer Center

In September 2014, we entered into a license agreement with Memorial Sloan Kettering Cancer Center, or MSK, under which we were granted an exclusive license to develop and commercialize MSK’s WT1 peptide vaccine technology. The MSK original license agreement was first amended in October 2015, further amended in August 2016, amended and restated in May 2017 and again amended and restated in October 2017. In connection with the entry of the original license agreement and its amendments, MSK was issued or assigned an aggregate of 4,846 ordinary shares of Private SELLAS common stock for the year ended December 31, 2017. These common stock shares were converted into our common stock shares upon the Merger.

Under the terms of the current amended and restated MSK license agreement, we agreed to pay minimum royalty payments in the amount of $0.1 million each year commencing in 2015 and research funding costs of $0.2 million in each year and for three years commencing in January 2016. We also agreed to pay MSK a mid-six digit amount over a one year period in exchange for MSK’s agreement to further amend and restate the MSK license agreement in October 2017. In addition, to the extent certain development and commercial milestones are achieved, we also agreed to pay MSK up to $17.4 million in aggregate milestone payments for each licensed product, and for each additional patent licensed product, up to $2.8 million in additional milestone payments. We also agreed to pay MSK a tiered royalty in the mid-single digits in the event of commercial sales of any licensed products and agreed to raise $25.0 million in gross proceeds no later than December 31, 2018. We raised this amount from the proceeds received from the sale of our Series A Convertible Preferred stock in March 2018 and our underwritten public offering of shares of common stock, pre-funded warrants to purchase shares of common-stock, and warrants to purchase shares of common stock in July 2018. Under the terms of the agreement, we achieved a clinical development milestone at the end of the fourth quarter of 2018, triggering a $0.5 million payment in the first quarter of 2019.

Unless terminated earlier in accordance with its terms, the MSK license agreement as amended and restated, will continue on a country-by-country and licensed product-by-licensed product basis, until the later, of: (a) expiration of the last valid claim embracing such licensed product; (b) expiration of any market exclusivity period granted by law with respect to such licensed product; or (c) ten years from the first commercial sale in such country.

Merck & Co., Inc. Clinical Trial Collaboration and Supply Agreement

In September 2017, we entered into a clinical trial collaboration and supply agreement through a Merck subsidiary, whereby we agreed with the Merck subsidiary to collaborate on a clinical program to evaluate GPS as it is administered in combination with their PD1 blocker pembrolizumab in a Phase 1/2 clinical trial enrolling patients in up to five cancer indications, including both hematologic malignancies and solid tumors.

The Phase 1/2 clinical trial utilizes a combination of GPS plus pembrolizumab in patients with WT1+ relapsed or refractory tumors. Specifically, the study is designed to explore the following cancer indications: AML, ovarian, triple-negative breast, small cell lung, and colorectal (arm enriched in but not exclusive to patients with microsatellite instability-low tumors). This study will assess the efficacy and safety of the combination, comparing overall response rates and immune response markers achieved with the combination compared to prespecified rates based on those seen with pembrolizumab alone in comparable patient populations. This trial was initiated in December 2018.

22

Advaxis, Inc. Research and Development Collaboration Agreement

In February 2017, we entered into a research and development collaboration agreement with Advaxis whereby we agreed to collaborate on a research program to evaluate, through a “proof of principle” trial or trials (“PoP Clinical Trial”), a clinical candidate comprised of the combination of Advaxis’ proprietary Lm-based antigen delivery technology and GPS. Unless terminated earlier in accordance with its terms, the Advaxis agreement will expire upon the earlier of: (a) completion of the PoP Clinical Trial or (b) a decision by the parties to cease further development of the clinical candidate.

The Advaxis agreement provides for cost-sharing between the parties, with Advaxis being responsible for the costs of performing the research activities and filing any investigational new drug, or IND, cost-sharing for preparation of the IND, and we being responsible for the costs (exclusive of product costs) of conducting the PoP Clinical Trial. We also agreed to make certain non-refundable milestone payments to Advaxis having an aggregate amount of up to $108.0 million, upon meeting certain clinical, regulatory and commercial milestones. In addition, if net sales exceed certain targets, we agreed to make non-refundable sales milestone payments up to $250.0 million and royalty payments based on specific royalty rates, with a maximum rate capped at a percentage rate in the low teens if net sales exceed $1.0 billion.

The University of Texas M. D. Anderson Cancer Center and The Henry M. Jackson Foundation for the Advancement of Military Medicine, Inc. License Agreement

In September 2006, we acquired rights and assumed obligations under a license agreement among Apthera, Inc., our wholly owned subsidiary, the University of Texas M.D. Anderson Cancer Center, or MDACC, and the Henry M. Jackson Foundation for the Advancement of Military Medicine, Inc., or HJF, which grants exclusive worldwide rights to a U.S. patent covering the nelipepimut-S peptide and several U.S. and foreign patents and patent applications covering methods of using the peptide as a vaccine. Under the license agreement we agreed to pay MDACC and HJF up to $3.8 million in aggregate milestone payments to the extent certain development and commercial milestones are reached and a $0.2 million annual maintenance fee. We also agreed to pay MDACC and HJF a tiered royalty in the mid-single digits in the event of any commercial sales of licensed products.

Manufacturing

We do not own or operate manufacturing facilities for the production of our product candidates, nor do we have plans to develop our own manufacturing operations in the foreseeable future. We currently depend on third-party contract manufacturers for all of our required raw materials, active pharmaceutical ingredients, and finished product candidate for our clinical trials. We do not have any current contractual arrangements for the manufacture of commercial supplies of any product candidates. We currently employ internal resources and third-party consultants to manage our manufacturing contractors.

Sales and Marketing