Form N-CSR/A FPA U.S. Core Equity For: Dec 31

Tweet

Tweet Share

Share

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03896

fpa U.S. Core Equity FUND, inc.

(Exact name of registrant as specified in charter)

11601 WILSHIRE BLVD., STE. 1200

LOS ANGELES, CALIFORNIA 90025

(Address of principal executive offices)(Zip code)

| (Name and Address of Agent for Service) |

Copy to:

|

|

J. RICHARD ATWOOD, PRESIDENT FPA U.S. CORE EQUITY FUND, INC. 11601 WILSHIRE BLVD., STE. 1200 LOS ANGELES, CALIFORNIA 90025

|

MARK D. PERLOW, ESQ. DECHERT LLP ONE BUSH STREET, STE. 1600 SAN FRANCISCO, CA 94104

|

Registrant’s telephone number, including area code: (310) 473-0225

Date of fiscal year end: December 31

Date of reporting period: December 31, 2021

Item 1: Report to Shareholders.

| (a) | The Report to Shareholders is attached herewith. |

Annual Report

Distributor:

UMB DISTRIBUTION SERVICES, LLC

235 West Galena Street

Milwaukee, Wisconsin 53212

December 31, 2021

FPA U.S. Core Equity Fund, Inc.

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

Introduction1

In 2021, the FPA U.S. Core Equity Fund, Inc.'s ("Fund") performance was 22.86% (24.23% before fees and expenses), while the S&P 500 Index ("Index" or "S&P 500") returned 28.71%.

While the Fund's performance trailed that of the index in 2021, I am very pleased with the absolute return especially after posting such strong absolute and relative performance in 2019 and 2020. Taken together, the Fund's annualized return over the past three years is 27.18% (28.68% before fees and expenses), which compares favorably to the Index's 26.07% return. Considering most active equity managers underperform the Index in most years, I take great pride in having delivered attractive relative performance over the past few years. And this performance was achieved as a diversified U.S. equity Fund, which I believe is an important factor when considering how much risk is acceptable while seeking to deliver long-term capital growth.

Despite trailing in 2021, I believe we have created a better version of the Index by overweighting what I think is good, eliminating what is bad and adding other high quality foreign and U.S. companies that are not in the Index. What is worth noting is that we achieved favorable results over the past three years in a well-thought-out manner with an approximate 40% overlap with the Index over this time.

The Fund's trailing performance for 2021 is mostly attributable to having none or less than average exposure to the best performing sectors for the year such as Energy (up 46.54%), Real Estate (up 44.31%) and Financials (up 34.30%) coupled with having greater than average exposure to underperforming sectors such as Communication Services (up 21.70%) and Consumer Discretionary (up 23.64%).

I was not surprised to see Energy and Financials rebound from somewhat depressed 2020 levels as the U.S. and global economy began to recover in 2021. In my closing remarks for the Fund's fourth quarter 2020 commentary I said, "The biggest thing we struggle with in managing the portfolio is that a lot of the companies we like the most generally do not have the cheapest valuations at the moment, whereas the companies with the lowest valuations typically do not have businesses in which we wish to invest for the long-term. At the same time, for lack of a better term, 'cash is trash' in a world where the monetary 'printing presses' seem unabated as more fiat currency continues to flood the economy and interest rates remain near historical lows. Given the current choices, we choose to remain diversified to mitigate risk and to invest in high-quality businesses even if we do not love the current valuations."

I would not be surprised to see Energy or Financials outperform the Index again in 2022, but I would be surprised to see these sectors outperform the Index over the long-term. Over the long-term, revenue and earnings growth are typically the greatest factors in determining stock price returns. I believe the sectors the Fund has the greatest current exposure to, which are Information Technology and Communication Services, are likely to continue to exhibit above average growth whereas sectors such as Energy and Financials are less likely to do so. Therefore, a large part of my focus remains identifying companies within favorable sectors that are more likely to produce sustainable, above average revenue and earnings growth over time and then hopefully purchase them at attractive prices.

Even though the 10-year U.S. Treasury yield increased from approximately 0.9% to 1.5% in 2021, it remains near historical lows. I believe secularly growing mid- to large-capitalization companies trading at compelling valuations will continue to be a favorable place to invest for the long-term — especially relative to U.S. Treasuries and other investment alternatives.

1 Past performance in not a guarantee, nor is it indicative, of future results.

1

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

Portfolio Commentary

During the fourth quarter, I continued to make some changes to the portfolio to seek to best position it for future success. To that end I eliminated 25 positions that made up 7.1% of the September 30, 2021 portfolio, increased the weighting of the 82 remaining positions by 1.1% to 93.4%, and added nine new positions representing 5.4% of the December 31, 2021 portfolio. These new positions are in companies I have been following and that were on our wish list to purchase. Most are not at full position sizes yet due to valuation, and thus we are prepared to add to them should we get the opportunity.

As of December 31, 2021, the Fund was invested in 91 companies (77 of which are disclosed), including 56 disclosed investments that are in the S&P 500, which made up 85.0% of the portfolio. Moreover, the 56 disclosed positions in common with the Index made up 40.5% of the S&P 500's weighting as of December 31, 2021. A majority of the 56 positions were overweight in the Fund relative to the Index. The Fund's remaining 21 disclosed investments were large-cap foreign and U.S. companies. Combined, those 21 companies made up 8.9% of the portfolio.

In terms of geography, 90.1% of the disclosed portfolio was in U.S. companies, while 3.7% was in foreign equities, as of December 31, 2021. By market capitalization, 93.0% of the disclosed portfolio was invested in large-cap companies with market values above $10 billion, with about 67% invested in mega-caps (companies with market values above $200 billion). The Fund's weighted average market cap was approximately $955 billion, while the Fund's median market cap was approximately $81 billion.

Regarding portfolio concentration, the Fund's top five positions made up 41.7% of the Fund compared to approximately 24.3% for the S&P 500. The Fund's top 10 positions made up 49.9% of the portfolio versus 29.0% for the Index. Over time, our goal is to reduce the weighting of some of the Fund's largest positions and to increase some of the Fund's smallest ones as our conviction grows.

From an industry exposure standpoint, the portfolio had investments in nine of the 11 sectors in the S&P 500. Combined, those nine sectors made up approximately 94% of the S&P 500. Relative to the S&P 500, the portfolio is overweight information technology, communication services and consumer discretionary, and underweight financials, health care, industrials, consumer staples, real estate, and materials. At the end of the quarter, the Fund did not have any investments in utilities and energy. Collectively, those three sectors made up approximately 6% of the S&P 500.

2

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

|

Sector |

FPA U.S. Core Equity Fund |

S&P 500 |

|||||||||

|

Information Technology |

36.1 |

% |

28.7 |

% |

|||||||

|

Communication Services |

24.1 |

% |

10.0 |

% |

|||||||

|

Consumer Discretionary |

17.9 |

% |

12.0 |

% |

|||||||

|

Health Care |

10.9 |

% |

13.1 |

% |

|||||||

|

Financials |

5.7 |

% |

11.3 |

% |

|||||||

|

Industrials |

2.1 |

% |

7.8 |

% |

|||||||

|

Consumer Staples |

1.3 |

% |

6.1 |

% |

|||||||

|

Real Estate |

0.6 |

% |

2.7 |

% |

|||||||

|

Materials |

0.1 |

% |

2.5 |

% |

|||||||

|

Energy |

0.0 |

% |

3.4 |

% |

|||||||

|

Utilities |

0.0 |

% |

2.5 |

% |

|||||||

|

Total |

98.9 |

% |

100.0 |

% |

|||||||

|

Cash and equivalents (net of liabilities) |

1.1 |

% |

|||||||||

Source: FPA, Capital IQ. As of December 31, 2021. Totals might not add up to 100% due to rounding. Portfolio composition will change due to ongoing management of the Fund.

Compared to the broader market, we believe the Fund's portfolio is of higher quality and has greater potential for revenue and earnings growth.2

2 The portfolio manager believes a high-quality company is one that is able to generate a return on capital in excess of its cost of capital for sustained periods of time.

3

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

|

FPA U.S. Core Equity Fund |

S&P 500 |

||||||||||

|

Large Capitalization Holdings % of Portfolio |

90.1 |

% |

99.4 |

% |

|||||||

|

Top 5 Holdings % of Portfolio |

41.7 |

% |

24.3 |

% |

|||||||

|

Top 10 Holdings % of Portfolio |

49.9 |

% |

29.0 |

% |

|||||||

|

Foreign Securities % of Portfolio |

3.7 |

% |

0.0 |

% |

|||||||

| 12-Month Forward P/E3 |

29.1 |

x |

20.9 |

x |

|||||||

|

Price/Book4 |

9.1 |

x |

4.8 |

x |

|||||||

|

Return on Equity5 |

29.7 |

% |

18.8 |

% |

|||||||

|

EPS Growth Forecast (2-year, median) |

13.5 |

% |

9.0 |

% |

|||||||

|

Revenue Growth Historical (2-year, $-weighted median) |

27.5 |

% |

16.1 |

% |

|||||||

|

Revenue Growth Forecast (2-year, median) |

17.8 |

% |

14.7 |

% |

|||||||

|

Debt/Equity6 |

0.5 |

x |

0.9 |

x |

|||||||

|

Median Market Capitalization7 (billions) |

$ |

80.9 |

$ |

34.0 |

|||||||

|

Weighted Average Market Cap (billions) |

$ |

955.2 |

$ |

665.2 |

|||||||

Source: FPA, Capital IQ. Data as of December 31, 2021. Fund statistics for '% of Portfolio' holdings are based on net assets. Portfolio composition will change due to ongoing management of the Fund.

3 The forward price-to-earnings (P/E) ratio is derived by dividing the price of the stock by the estimated one year of future per-share earnings and is used as a relative value comparison for a company's shares. Forward P/E numbers are estimates and subject to change.

4 Price/Book ratio is the current closing price of the stock divided by the latest quarter's book value per share.

5 Return on Equity measures a portfolio company's profitability by dividing net income before taxes less preferred dividends by the value of stockholders' equity.

6 Debt/Equity (D/E) Ratio is calculated by dividing a company's total liabilities by its shareholder equity. These numbers are available on the balance sheet of a company's financial statements. The ratio is used to evaluate a company's financial leverage.

7 Market Cap, short for market capitalization, refers to the total dollar market value of a company's outstanding shares.

4

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

2021 Winners and Losers8

|

Winners |

Performance Contribution |

Losers |

Performance Contribution |

||||||||||||

|

Alphabet |

4.62 |

% |

Adidas AG |

-0.54 |

% |

||||||||||

|

Microsoft |

4.40 |

% |

Tencent |

-0.39 |

% |

||||||||||

|

Apple |

2.33 |

% |

PayPal |

-0.37 |

% |

||||||||||

|

Meta Platforms |

1.55 |

% |

Activision Blizzard |

-0.26 |

% |

||||||||||

|

NVIDIA |

1.43 |

% |

Autodesk |

-0.22 |

% |

||||||||||

One of the year's biggest losers was Tencent. Chinese technology stocks took a beating throughout the year (the KraneShares CSI China Internet ETF (ARCX: KWEB) declined 52.53% between the period 1/1/2021 and 12/31/2021) due to various Chinese government actions that began in November 2020 with the suspension of Ant Group's IPO. Next came guidelines to root out monopolistic practices in the internet industry, which was followed by an investigation into monopolistic practices at Alibaba. On April 10, 2021, Alibaba was fined a record $2.8 billion after regulators concluded the company abused its market position. On April 12, 2021, Ant was ordered to transform itself into a financial holdings company that will be supervised more like a bank. Then on April 29, 2021, regulators imposed similar curbs on the fintech arms of 13 firms, including Tencent and Meituan. On July 2, 2021, China's internet watchdog started a cybersecurity review of Didi two days after its U.S. IPO and ordered the firm to halt new user registrations. On July 9, 2021, new rules were proposed that requires companies with more than one million users to get cybersecurity clearance when seeking public market listings in other countries. On July 24, 2021, China's cabinet banned companies teaching school curriculum from making profits, raising capital, or going public. A week later Tencent and Alibaba began taking steps to open their platforms after regulators asked 25 companies to stop blocking links to their rivals. On August 17, 2021, President Xi Jinping re-emphasized the need for Common Prosperity, echoing remarks he first made at the 2017 Communist Party national congress, by requiring the adjustment of "excessive income" indicating the potential for higher taxes or the expectation of more charity contributions from the rich and corporations. Two weeks later China's media regulator issued rules limiting the amount of time children can play video games and slowed down approvals for new titles.9 This was particularly painful for Tencent, which has a large video game business.

Our investment thesis behind Tencent was that it is a very good company with market leading businesses trading at an attractive valuation given tremendous growth opportunities. These growth opportunities exist largely because of China's robust economic growth thanks to its budding technology industry as well as its emerging middle class that is increasingly adopting these technology advances. We knew the political risk of investing in China and as a result we put a self-imposed five percent exposure limit to Chinese equities, which we never hit.

8 Reflects top contributors and top detractors to the Fund's performance based on contribution-to-return. Contribution is presented gross of investment management fees, transactions costs, and Fund operating expenses, which if included, would reduce the returns presented. This is not a recommendation for a specific security and these securities may not be in the Fund at the time you receive this report. The information provided does not reflect all positions purchased, sold or recommended by FPA during the quarter. A copy of the methodology used and a list of every holding's contribution to the overall Fund's performance during the quarter is available by contacting FPA at [email protected]. The portfolio holdings as of the most recent quarter-end may be obtained at www.fpa.com. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities listed. For a full list of holdings and weights by percentage of total assets please view the holdings report at the end of this Commentary.

Past performance is no guarantee, nor is it indicative, of future results.

9 https://www.bloomberg.com/graphics/2021-china-tech-crackdown-one-year/

5

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

As the political environment worsened throughout the year, we trimmed the Fund's exposure to Chinese equities. In hindsight we should have trimmed the Fund's exposure more aggressively than we did. In total, Chinese equity exposure cost the Fund 0.54% in 2021.

In prior Commentaries I discussed our affinity for FAAAM (Facebook, Alphabet, Amazon, Apple and Microsoft), which are our top five positions. Since Facebook renamed itself Meta Platforms, I am renaming this MAAAM. MAAAM largely delivered for the Fund in 2021 with the exception of Amazon as it saw growth slow down a bit in its core e-commerce operations as retail stores increasingly reopened throughout the world and presented more competition for Amazon compared to 2020. Nonetheless we are very optimistic regarding Amazon's future.

Looking at Amazon's various businesses and the disclosure it gives to investors shows just how much it is investing into them, particularly within e-commerce. While this depresses current profits, these investments serve to further distance itself from the competition, which I think should bode well for future revenue and earnings as it continues to take market share. Amazon's non-Amazon Web Services (AWS) businesses collectively broke even on $95 billion in revenue in the third quarter of 2021 compared to an approximate $2.7 billion operating profit on $85 billion in revenue in the third quarter of 2020.

Digging a little deeper into its non-AWS sub segments reveals some interesting takeaways. Of the approximate $10 billion non-AWS revenue growth, about $8 billion was in its highest margin businesses that include third-party seller services, subscription services, and advertising services. At the same time, its worldwide shipping costs increased approximately $3 billion or 20% compared to the 8% growth in paid units.10 Amazon has been investing a tremendous amount into its in-house delivery services by having more local warehouses that allow it to deliver increasingly more items at a faster pace — and ultimately potentially at a lower cost as it gains more local density and leverages these expenses. No other company is attempting to do what Amazon is doing here. My view is that these investments will further enhance its economic moat. As such I believe Amazon will deliver above average investment returns over the long-term.

Closing

We are optimistic that the Fund will generate good absolute and relative returns compared to the S&P 500 going forward.

We look forward to delivering value for our fellow shareholders. Thank you for your confidence and continued support.

Respectfully submitted,

Gregory R. Nathan

Portfolio Manager

January 2022

10 https://s2.q4cdn.com/299287126/files/doc_financials/2021/q3/Q3-2021-Earnings-Release.pdf

6

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

Important Disclosures

This Commentary is for informational and discussion purposes only and does not constitute, and should not be construed as, an offer or solicitation for the purchase or sale of any securities, products or services discussed, and neither does it provide investment advice. Any such offer or solicitation shall only be made pursuant to the Fund's Prospectus, which supersedes the information contained herein in its entirety. This Commentary does not constitute an investment management agreement or offering circular.

The views expressed herein and any forward-looking statements are as of the date of this publication and are those of the portfolio management team. Future events or results may vary significantly from those expressed and are subject to change at any time in response to changing circumstances and industry developments. This information and data has been prepared from sources believed reliable, but the accuracy and completeness of the information cannot be guaranteed and is not a complete summary or statement of all available data.

Portfolio composition will change due to ongoing management of the Fund. References to individual securities or sectors are for informational purposes only and should not be construed as recommendations by the Fund, the portfolio manager, the Adviser, or the distributor. It should not be assumed that future investments will be profitable or will equal the performance of the security or sector examples discussed. The portfolio holdings as of the most recent quarter-end may be obtained at www.fpa.com.

Future events or results may vary significantly from those expressed and are subject to change at any time in response to changing circumstances and industry developments. The information and data contained herein has been prepared from sources believed reliable, but the accuracy and completeness of the information cannot be guaranteed and is not a complete summary or statement of all available data.

The information contained herein is not complete, may change, and is subject to, and is qualified in its entirety by, the more complete disclosures, risk factors, and other information contained in the Fund's Prospectus and Statement of Additional Information. The information is furnished as of the date shown. No representation is made with respect to its completeness or timeliness. The information is not intended to be, nor shall it be construed as, investment advice or a recommendation of any kind.

Certain statements contained in this presentation may be forward-looking and/or based on current expectations, projections, and information currently available. Actual events or results may materially differ from those we anticipate, or the actual performance of any investments described herein may differ from those reflected or contemplated in such forward-looking statements, due to various risks and uncertainties. We cannot assure future results and disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Such statements may or may not be accurate over the long-term. Statistical data or references thereto were taken from sources which we deem to be reliable, but their accuracy cannot be guaranteed.

The reader is advised that the Fund's investment strategy includes active management with corresponding changes in allocations from one period of time to the next. Therefore, any data with respect to investment allocations as of a given date is of limited use and may not be reflective of the portfolio manager's more general views with respect to proper geographic, instrument and/or sector allocations. The data is presented for indicative purposes only and, as a result, may not be relied upon for any purposes whatsoever.

Investments, including investments in mutual funds, carry risks and investors may lose principal value. Capital markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. The Fund may purchase foreign securities, including American Depository

7

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

Receipts (ADRs) and other depository receipts, which are subject to interest rate, currency exchange rate, economic and political risks; these risks may be heightened when investing in emerging markets. Foreign investments, especially those of companies in emerging markets, can be riskier, less liquid, harder to value, and more volatile than investments in the United States. Adverse political and economic developments or changes in the value of foreign currency can make it more difficult for the Fund to value the securities. Differences in tax and accounting standards, difficulties in obtaining information about foreign companies, restrictions on receiving investment proceeds from a foreign country, confiscatory foreign tax laws, and potential difficulties in enforcing contractual obligations, can all add to the risk and volatility of foreign investments.

Small and mid-cap stocks involve greater risks and may fluctuate in price more than larger company stocks. Groups of stocks, such as value and growth, go in and out of favor which may cause certain funds to underperform other equity funds.

Value style investing presents the risk that the holdings or securities may never reach their full market value because the market fails to recognize what the portfolio manager considers the true business value or because the portfolio manager has misjudged those values. In addition, value style investing may fall out of favor and underperform growth or other styles of investing during given periods.

In making any investment decision, you must rely on your own examination of the Fund, including the risks involved in an investment. Investments mentioned herein may not be suitable for all recipients and in each case, potential investors are advised not to make any investment decision unless they have taken independent advice from an appropriately authorized advisor. An investment in any security mentioned herein does not guarantee a positive return as securities are subject to market risks, including the potential loss of principal. You should not construe the contents of this document as legal, tax, investment or other advice or recommendations.

Please refer to the Fund's Prospectus for a complete overview of the primary risks associated with the Fund.

Index / Other Definitions

The Fund will be less diversified than the indices noted herein, and may hold non-index securities or securities that are not comparable to those contained in an index. Indices may hold positions that are not within the Fund's investment strategy. Indices are unmanaged and do not reflect any commissions or fees which would be incurred by an investor purchasing the underlying securities and which would reduce the performance in an actual account. An investor cannot invest directly in an index.

The S&P 500 Index includes a representative sample of 500 hundred companies in leading industries of the U.S. economy. The index focuses on the large-cap segment of the market, with over 80% coverage of U.S. equities, but is also considered a proxy for the total market.

The Fund is distributed by UMB Distribution Services, LLC, 235 W. Galena Street, Milwaukee, WI, 53212.

8

FPA U.S. CORE EQUITY FUND, INC.

LETTER TO SHAREHOLDERS

(Continued)

The discussions of Fund investments represent the views of the Fund's managers at the time of this report and are subject to change without notice. References to individual securities are for informational purposes only and should not be construed as recommendations to purchase or sell individual securities. While the Fund's managers believe that the Fund's holdings are value stocks, there can be no assurance that others will consider them as such. While the Fund's managers believe that the Fund's holdings are value stocks, there can be no assurance that others will consider them as such. Further, investing in value stocks presents the risk that value stocks may fall out of favor with investors and underperform growth stocks during given periods.

FORWARD LOOKING STATEMENT DISCLOSURE

As mutual fund managers, one of our responsibilities is to communicate with shareholders in an open and direct manner. Insofar as some of our opinions and comments in our letters to shareholders are based on our current expectations, they are considered "forward-looking statements" which may or may not prove to be accurate over the long term. While we believe we have a reasonable basis for our comments and we have confidence in our opinions, actual results may differ materially from those we anticipate. You can identify forward-looking statements by words such as "believe," "expect," "may," "anticipate," and other similar expressions when discussing prospects for particular portfolio holdings and/or the markets, generally. We cannot, however, assure future results and disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Further, information provided in this report should not be construed as a recommendation to purchase or sell any particular security.

9

FPA U.S. CORE EQUITY FUND, INC.

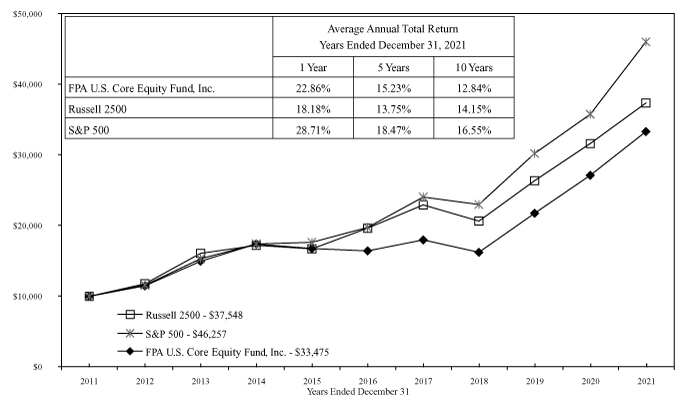

HISTORICAL PERFORMANCE

(Unaudited)

Change in Value of a $10,000 Investment in FPA U.S. Core Equity Fund, Inc. vs. Russell 2500 Index and S&P 500 for the Ten Years Ended December 31, 2021

The Russell 2500 Index consists of the 2,500 smallest companies in the Russell 3000 total capitalization universe. This index is considered a measure of small to medium capitalization stock performance. The Standard & Poor's 500 Composite Index (S&P 500) is an unmanaged index that is generally representative of the U.S. stock market. The indexes do not reflect any commissions, fees or other expenses of investing which would be incurred by an investor purchasing the stocks it represents. The performance of the Fund and of the Indexes is computed on a total return basis which includes reinvestment of all distributions. It is not possible to invest directly in an index.

A new strategy for FPA U.S. Core Equity Fund, Inc. was implemented beginning on September 1, 2015. The returns above include performance of the previous managers prior to that date. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. This data represents past performance and investors should understand that investment returns and principal values fluctuate, so that when you redeem your investment may be worth more or less than its original cost. Current month-end performance data can be obtained by visiting the website at www.fpa.com or by calling toll-free, 1-800-982-4372. Information regarding the Fund's expense ratio and redemption fees can be found on page 20. The Prospectus details the Fund's objective and policies, sales charges, and other matters of interest to prospective investors. Please read the Prospectus carefully before investing. The Prospectus may be obtained by visiting the website at www.fpa.com, by email at [email protected], toll-free by calling 1-800-982-4372 or by contacting the Fund in writing.

10

FPA U.S. CORE EQUITY FUND, INC.

PORTFOLIO SUMMARY

December 31, 2021

|

Common Stocks |

98.8 |

% |

|||||||||

|

Internet Media |

16.9 |

% |

|||||||||

|

Infrastructure Software |

11.1 |

% |

|||||||||

|

Communications Equipment |

7.9 |

% |

|||||||||

|

E-Commerce Discretionary |

7.2 |

% |

|||||||||

|

Information Technology Services |

7.0 |

% |

|||||||||

|

Consumer Finance |

5.5 |

% |

|||||||||

|

Other Common Stocks |

5.0 |

% |

|||||||||

|

Apparel, Footwear & Accessory Design |

4.2 |

% |

|||||||||

|

Application Software |

3.7 |

% |

|||||||||

|

Entertainment Content |

3.5 |

% |

|||||||||

|

Managed Care |

3.5 |

% |

|||||||||

|

Home Products Stores |

3.4 |

% |

|||||||||

|

Life Science Equipment |

2.7 |

% |

|||||||||

|

Retailing |

2.0 |

% |

|||||||||

|

Medical Devices |

2.0 |

% |

|||||||||

|

Cable & Satellite |

1.6 |

% |

|||||||||

|

Insurance Brokers |

1.5 |

% |

|||||||||

|

Health Care Services |

1.4 |

% |

|||||||||

|

Private Equity |

1.2 |

% |

|||||||||

|

Specialty Pharmaceuticals |

1.0 |

% |

|||||||||

|

Managed Health Care |

1.0 |

% |

|||||||||

|

Industrials |

0.8 |

% |

|||||||||

|

Automotive Retailers |

0.7 |

% |

|||||||||

|

Courier Services |

0.6 |

% |

|||||||||

|

Commercial & Residential Building Equipment & Systems |

0.6 |

% |

|||||||||

|

Institutional Brokerage |

0.5 |

% |

|||||||||

|

Internet Based Services |

0.5 |

% |

|||||||||

|

Household Products |

0.5 |

% |

|||||||||

|

Restaurants |

0.4 |

% |

|||||||||

|

Investment Management |

0.3 |

% |

|||||||||

|

Health Care Facilities |

0.3 |

% |

|||||||||

|

Entertainment Facilities |

0.3 |

% |

|||||||||

|

Short-term Investments |

1.0 |

% |

|||||||||

|

Other Assets And Liabilities, Net |

0.2 |

% |

|||||||||

|

Net Assets |

100.0 |

% |

|||||||||

11

FPA U.S. CORE EQUITY FUND, INC.

PORTFOLIO OF INVESTMENTS

December 31, 2021

|

COMMON STOCKS |

Shares |

Fair Value |

|||||||||

|

INTERNET MEDIA — 16.9% |

|||||||||||

|

Alphabet, Inc. Class C(a) |

2,694 |

$ |

7,795,331 |

||||||||

|

Match Group, Inc.(a) |

1,891 |

250,085 |

|||||||||

|

MercadoLibre, Inc. (Argentina)(a) |

105 |

141,582 |

|||||||||

|

Meta Platforms, Inc. Class A(a) |

15,993 |

5,379,246 |

|||||||||

|

Spotify Technology SA (Sweden)(a) |

535 |

125,206 |

|||||||||

|

$ |

13,691,450 |

||||||||||

|

INFRASTRUCTURE SOFTWARE — 11.1% |

|||||||||||

|

Microsoft Corp. |

25,787 |

$ |

8,672,684 |

||||||||

|

Zscaler, Inc.(a) |

1,095 |

351,856 |

|||||||||

|

$ |

9,024,540 |

||||||||||

|

COMMUNICATIONS EQUIPMENT — 7.9% |

|||||||||||

|

Apple, Inc. |

34,327 |

$ |

6,095,445 |

||||||||

|

Shopify, Inc. Class A (Canada)(a) |

135 |

185,948 |

|||||||||

|

Universal Music Group NV (Netherlands) |

4,500 |

126,954 |

|||||||||

|

$ |

6,408,347 |

||||||||||

|

E-COMMERCE DISCRETIONARY — 7.2% |

|||||||||||

|

Amazon.com, Inc.(a) |

1,750 |

$ |

5,835,095 |

||||||||

|

INFORMATION TECHNOLOGY SERVICES — 7.0% |

|||||||||||

|

Accenture PLC Class A (Ireland) |

3,165 |

$ |

1,312,051 |

||||||||

|

Autodesk, Inc.(a) |

4,050 |

1,138,819 |

|||||||||

|

Crowdstrike Holdings, Inc. Class A(a) |

1,055 |

216,011 |

|||||||||

|

IHS Markit Ltd. (Britain) |

2,376 |

315,818 |

|||||||||

|

Intuit, Inc. |

555 |

356,987 |

|||||||||

|

MSCI, Inc. |

480 |

294,091 |

|||||||||

|

NVIDIA Corp. |

4,425 |

1,301,437 |

|||||||||

|

Palantir Technologies, Inc. Class A(a) |

6,500 |

118,365 |

|||||||||

|

QUALCOMM, Inc. |

3,270 |

597,985 |

|||||||||

|

S&P Global, Inc. |

70 |

33,035 |

|||||||||

|

$ |

5,684,599 |

||||||||||

|

CONSUMER FINANCE — 5.5% |

|||||||||||

|

American Express Co. |

3,500 |

$ |

572,600 |

||||||||

|

Mastercard, Inc. Class A |

3,625 |

1,302,535 |

|||||||||

|

PayPal Holdings, Inc.(a) |

6,820 |

1,286,116 |

|||||||||

|

Visa, Inc. A Shares |

6,010 |

1,302,427 |

|||||||||

|

$ |

4,463,678 |

||||||||||

12

FPA U.S. CORE EQUITY FUND, INC.

PORTFOLIO OF INVESTMENTS (Continued)

December 31, 2021

|

COMMON STOCKS — Continued |

Shares |

Fair Value |

|||||||||

|

APPAREL, FOOTWEAR & ACCESSORY DESIGN — 4.2% |

|||||||||||

|

Adidas AG (Germany) |

4,942 |

$ |

1,424,621 |

||||||||

|

Kering SA (France) |

410 |

329,970 |

|||||||||

|

LVMH Moet Hennessy Louis Vuitton SE (France) |

413 |

341,836 |

|||||||||

|

NIKE, Inc. Class B |

7,815 |

1,302,526 |

|||||||||

|

$ |

3,398,953 |

||||||||||

|

APPLICATION SOFTWARE — 3.7% |

|||||||||||

|

Activision Blizzard, Inc. |

6,693 |

$ |

445,285 |

||||||||

|

Adobe, Inc.(a) |

2,225 |

1,261,709 |

|||||||||

|

salesforce.com, Inc.(a) |

5,125 |

1,302,416 |

|||||||||

|

$ |

3,009,410 |

||||||||||

|

ENTERTAINMENT CONTENT — 3.5% |

|||||||||||

|

Netflix, Inc.(a) |

2,141 |

$ |

1,289,824 |

||||||||

|

Take-Two Interactive Software, Inc.(a) |

1,360 |

241,699 |

|||||||||

|

Walt Disney Co.(a) |

8,395 |

1,300,302 |

|||||||||

|

$ |

2,831,825 |

||||||||||

|

MANAGED CARE — 3.5% |

|||||||||||

|

Anthem, Inc. |

1,915 |

$ |

887,679 |

||||||||

|

Apollo Global Management, Inc. |

8,400 |

608,412 |

|||||||||

|

UnitedHealth Group, Inc. |

2,595 |

1,303,053 |

|||||||||

|

$ |

2,799,144 |

||||||||||

|

HOME PRODUCTS STORES — 3.4% |

|||||||||||

|

Estee Lauder Cos., Inc. Class A |

897 |

$ |

332,069 |

||||||||

|

Home Depot, Inc. |

3,195 |

1,325,957 |

|||||||||

|

Lowe's Cos., Inc. |

4,300 |

1,111,464 |

|||||||||

|

$ |

2,769,490 |

||||||||||

|

LIFE SCIENCE EQUIPMENT — 2.7% |

|||||||||||

|

Danaher Corp. |

2,134 |

$ |

702,107 |

||||||||

|

Illumina, Inc.(a) |

368 |

140,002 |

|||||||||

|

Thermo Fisher Scientific, Inc. |

1,969 |

1,313,796 |

|||||||||

|

$ |

2,155,905 |

||||||||||

|

RETAILING — 2.0% |

|||||||||||

|

AutoZone, Inc.(a) |

255 |

$ |

534,579 |

||||||||

|

Etsy, Inc.(a) |

525 |

114,944 |

|||||||||

|

Sherwin-Williams Co. |

275 |

96,844 |

|||||||||

|

Sprouts Farmers Market, Inc.(a) |

12,850 |

381,388 |

|||||||||

|

Ulta Beauty, Inc.(a) |

1,280 |

527,795 |

|||||||||

|

$ |

1,655,550 |

||||||||||

13

FPA U.S. CORE EQUITY FUND, INC.

PORTFOLIO OF INVESTMENTS (Continued)

December 31, 2021

|

COMMON STOCKS — Continued |

Shares |

Fair Value |

|||||||||

|

MEDICAL DEVICES — 2.0% |

|||||||||||

|

Abbott Laboratories |

3,829 |

$ |

538,893 |

||||||||

|

Edwards Lifesciences Corp.(a) |

1,818 |

235,522 |

|||||||||

|

Intuitive Surgical, Inc.(a) |

1,776 |

638,117 |

|||||||||

|

Stryker Corp. |

815 |

217,947 |

|||||||||

|

$ |

1,630,479 |

||||||||||

|

CABLE & SATELLITE — 1.6% |

|||||||||||

|

Comcast Corp. Class A |

25,870 |

$ |

1,302,037 |

||||||||

|

INSURANCE BROKERS — 1.5% |

|||||||||||

|

Aon PLC Class A |

2,045 |

$ |

614,645 |

||||||||

|

Willis Towers Watson PLC (Britain) |

2,400 |

569,976 |

|||||||||

|

$ |

1,184,621 |

||||||||||

|

HEALTH CARE SERVICES — 1.4% |

|||||||||||

|

IQVIA Holdings, Inc.(a) |

3,385 |

$ |

955,044 |

||||||||

|

Moody's Corp. |

385 |

150,373 |

|||||||||

|

$ |

1,105,417 |

||||||||||

|

PRIVATE EQUITY — 1.2% |

|||||||||||

|

Blackstone, Inc. Class A |

4,146 |

$ |

536,451 |

||||||||

|

KKR & Co., Inc. Class A |

6,174 |

459,963 |

|||||||||

|

$ |

996,414 |

||||||||||

|

SPECIALTY PHARMACEUTICALS — 1.0% |

|||||||||||

|

Cigna Corp. |

870 |

$ |

199,778 |

||||||||

|

Zoetis, Inc. |

2,405 |

586,892 |

|||||||||

|

$ |

786,670 |

||||||||||

|

MANAGED HEALTH CARE — 1.0% |

|||||||||||

|

Humana, Inc. |

1,678 |

$ |

778,357 |

||||||||

|

INDUSTRIALS — 0.8% |

|||||||||||

|

Airbus SE ADR (France)(a) |

16,800 |

$ |

536,088 |

||||||||

|

Trimble, Inc.(a) |

1,425 |

124,246 |

|||||||||

|

$ |

660,334 |

||||||||||

|

AUTOMOTIVE RETAILERS — 0.7% |

|||||||||||

|

O'Reilly Automotive, Inc.(a) |

848 |

$ |

598,883 |

||||||||

|

COURIER SERVICES — 0.6% |

|||||||||||

|

FedEx Corp. |

2,040 |

$ |

527,626 |

||||||||

14

FPA U.S. CORE EQUITY FUND, INC.

PORTFOLIO OF INVESTMENTS (Continued)

December 31, 2021

|

COMMON STOCKS — Continued |

Shares |

Fair Value |

|||||||||

|

COMMERCIAL & RESIDENTIAL BUILDING EQUIPMENT & SYSTEMS — 0.6% |

|||||||||||

|

Avalara, Inc.(a) |

1,220 |

$ |

157,514 |

||||||||

|

Honeywell International, Inc. |

1,540 |

321,106 |

|||||||||

|

$ |

478,620 |

||||||||||

|

INSTITUTIONAL BROKERAGE — 0.5% |

|||||||||||

|

Morgan Stanley |

4,160 |

$ |

408,346 |

||||||||

|

INTERNET BASED SERVICES — 0.5% |

|||||||||||

|

GoDaddy, Inc. Class A(a) |

4,534 |

$ |

384,755 |

||||||||

|

HOUSEHOLD PRODUCTS — 0.5% |

|||||||||||

|

Constellation Brands, Inc. Class A |

451 |

$ |

113,187 |

||||||||

|

L'Oreal SA (France) |

550 |

261,084 |

|||||||||

|

$ |

374,271 |

||||||||||

|

RESTAURANTS — 0.4% |

|||||||||||

|

Starbucks Corp. |

2,910 |

$ |

340,383 |

||||||||

|

INVESTMENT MANAGEMENT — 0.3% |

|||||||||||

|

BlackRock, Inc. |

305 |

$ |

279,246 |

||||||||

|

HEALTH CARE FACILITIES — 0.3% |

|||||||||||

|

HCA Healthcare, Inc. |

965 |

$ |

247,928 |

||||||||

|

ENTERTAINMENT FACILITIES — 0.3% |

|||||||||||

|

Electronic Arts, Inc. |

1,800 |

$ |

237,420 |

||||||||

|

OTHER COMMON STOCKS — 5.0%(a)(b) |

$ |

4,049,299 |

|||||||||

| TOTAL COMMON STOCKS — 98.8% (Cost $38,602,200) |

$ |

80,099,092 |

|||||||||

| TOTAL INVESTMENT SECURITIES — 98.8% (Cost $38,602,200) |

$ |

80,099,092 |

|||||||||

15

FPA U.S. CORE EQUITY FUND, INC.

PORTFOLIO OF INVESTMENTS (Continued)

December 31, 2021

|

SHORT-TERM INVESTMENTS — 1.0% |

Principal Amount |

Fair Value |

|||||||||

|

State Street Bank Repurchase Agreement — 0.00% 1/3/2022 (Dated 12/31/2021, repurchase price of $793,000, collateralized by $845,300 principal amount U.S. Treasury Notes — 0.625% 2027, fair value $808,945)(c) |

$ |

793,000 |

$ |

793,000 |

|||||||

| TOTAL SHORT-TERM INVESTMENTS (Cost $793,000) |

$ |

793,000 |

|||||||||

| TOTAL INVESTMENTS — 99.8% (Cost $39,395,200) |

$ |

80,892,092 |

|||||||||

|

Other assets and liabilities, net — 0.2% |

127,230 |

||||||||||

|

NET ASSETS — 100.0% |

$ |

81,019,322 |

|||||||||

(a) Non-income producing security.

(b) As permitted by U.S. Securities and Exchange Commission regulations, "Other" Common Stocks include holdings in their first year of acquisition that have not previously been publicly disclosed.

(c) Security pledged as collateral (See Note 7 of the Notes to Financial Statements).

See accompanying Notes to Financial Statements.

16

FPA U.S. CORE EQUITY FUND, INC.

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2021

|

ASSETS |

|||||||

|

Investment securities — at fair value (identified cost $38,602,200) |

$ |

80,099,092 |

|||||

|

Short-term investments — repurchase agreements |

793,000 |

||||||

|

Cash |

20,434 |

||||||

|

Foreign currencies at value (identified cost $214) |

216 |

||||||

|

Receivable for: |

|||||||

|

Investment securities sold |

2,326,595 |

||||||

|

Dividends and interest |

8,578 |

||||||

|

Capital Stock sold |

133 |

||||||

|

Prepaid expenses and other assets |

8,794 |

||||||

|

Total assets |

83,256,842 |

||||||

|

LIABILITIES |

|||||||

|

Payable for: |

|||||||

|

Investment securities purchased |

2,056,872 |

||||||

|

Advisory fees |

48,728 |

||||||

|

Capital Stock repurchased |

2,400 |

||||||

|

Accrued expenses and other liabilities |

129,520 |

||||||

|

Total liabilities |

2,237,520 |

||||||

|

NET ASSETS |

$ |

81,019,322 |

|||||

|

SUMMARY OF SHAREHOLDERS' EQUITY |

|||||||

|

Capital Stock — par value $0.01 per share; authorized 25,000,000 shares; 5,064,894 outstanding shares |

$ |

50,649 |

|||||

|

Additional Paid-in Capital |

35,561,816 |

||||||

|

Distributable earnings |

45,406,857 |

||||||

|

NET ASSETS |

$ |

81,019,322 |

|||||

|

NET ASSET VALUE |

|||||||

|

Offering and redemption price per share |

$ |

16.00 |

|||||

See accompanying Notes to Financial Statements.

17

FPA U.S. CORE EQUITY FUND, INC.

STATEMENT OF OPERATIONS

For the Year Ended December 31, 2021

|

INVESTMENT INCOME |

|||||||

|

Dividends (net of foreign taxes withheld of $4,727) |

$ |

402,843 |

|||||

|

Total investment income |

402,843 |

||||||

|

EXPENSES |

|||||||

|

Advisory fees |

550,192 |

||||||

|

Legal fees |

111,929 |

||||||

|

Transfer agent fees and expenses |

71,509 |

||||||

|

Director fees and expenses |

60,243 |

||||||

|

Filing fees |

35,054 |

||||||

|

Custodian fees |

28,719 |

||||||

|

Audit and tax services fees |

21,525 |

||||||

|

Reports to shareholders |

17,638 |

||||||

|

Other professional fees |

5,073 |

||||||

|

Administrative services fees |

3,176 |

||||||

|

Other |

413 |

||||||

|

Total expenses |

905,471 |

||||||

|

Net investment loss |

(502,628 |

) |

|||||

|

NET REALIZED AND UNREALIZED GAIN (LOSS) |

|||||||

|

Net realized gain (loss) on: |

|||||||

|

Investments |

8,872,776 |

||||||

|

Investments in foreign currency transactions |

(1,314 |

) |

|||||

|

Net change in unrealized appreciation (depreciation) of: |

|||||||

|

Investments |

7,558,282 |

||||||

|

Translation of foreign currency denominated amounts |

519 |

||||||

|

Net realized and unrealized gain |

16,430,263 |

||||||

|

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS |

$ |

15,927,635 |

|||||

See accompanying Notes to Financial Statements.

18

FPA U.S. CORE EQUITY FUND, INC.

STATEMENTS OF CHANGES IN NET ASSETS

|

Year Ended December 31, 2021 |

Year Ended December 31, 2020 |

||||||||||

|

INCREASE (DECREASE) IN NET ASSETS |

|||||||||||

|

Operations: |

|||||||||||

|

Net investment loss |

$ |

(502,628 |

) |

$ |

(448,607 |

) |

|||||

|

Net realized gain |

8,871,462 |

3,987,614 |

|||||||||

|

Net change in unrealized appreciation |

7,558,801 |

12,760,238 |

|||||||||

|

Net increase in net assets resulting from operations |

15,927,635 |

16,299,245 |

|||||||||

|

Distributions to shareholders |

(6,172,342 |

) |

(2,152,118 |

) |

|||||||

|

Capital Stock transactions: |

|||||||||||

|

Proceeds from Capital Stock sold |

1,640,846 |

3,061,340 |

|||||||||

|

Proceeds from shares issued to shareholders upon reinvestment of dividends and distributions |

5,510,185 |

1,908,860 |

|||||||||

|

Cost of Capital Stock repurchased |

(9,842,822 |

) |

(16,356,042 |

) |

|||||||

|

Net decrease from Capital Stock transactions |

(2,691,791 |

) |

(11,385,842 |

) |

|||||||

|

Total change in net assets |

7,063,502 |

2,761,285 |

|||||||||

|

NET ASSETS |

|||||||||||

|

Beginning of Year |

73,955,820 |

71,194,535 |

|||||||||

|

End of Year |

$ |

81,019,322 |

$ |

73,955,820 |

|||||||

|

CHANGE IN CAPITAL STOCK OUTSTANDING |

|||||||||||

|

Shares of Capital Stock sold |

106,893 |

245,236 |

|||||||||

|

Shares issued to shareholders upon reinvestment of dividends and distributions |

355,334 |

141,266 |

|||||||||

|

Shares of Capital Stock repurchased |

(641,013 |

) |

(1,268,932 |

) |

|||||||

|

Change in Capital Stock outstanding |

(178,786 |

) |

(882,430 |

) |

|||||||

See accompanying Notes to Financial Statements.

19

FPA U.S. CORE EQUITY FUND, INC.

FINANCIAL HIGHLIGHTS

Selected Data for Each Share of Capital Stock Outstanding Throughout Each Year

|

Year Ended December 31 |

|||||||||||||||||||||||

|

2021 |

2020 |

2019 |

2018 |

2017 |

|||||||||||||||||||

|

Per share operating performance: |

|||||||||||||||||||||||

|

Net asset value at beginning of year |

$ |

14.10 |

$ |

11.62 |

$ |

8.84 |

$ |

9.91 |

$ |

9.09 |

|||||||||||||

|

Income from investment operations: |

|||||||||||||||||||||||

|

Net investment income (loss)(a) |

(0.10 |

) |

(0.08 |

) |

(0.02 |

) |

— |

(b) |

0.01 |

||||||||||||||

|

Net realized and unrealized gain (loss) on investment securities |

3.26 |

2.94 |

3.03 |

(0.95 |

) |

0.86 |

|||||||||||||||||

|

Total from investment operations |

3.16 |

2.86 |

3.01 |

(0.95 |

) |

0.87 |

|||||||||||||||||

|

Less distributions: |

|||||||||||||||||||||||

|

Dividends from net investment income |

— |

— |

(0.01 |

) |

(0.02 |

) |

(0.05 |

) |

|||||||||||||||

|

Distributions from net realized capital gains |

(1.26 |

) |

(0.38 |

) |

(0.22 |

) |

(0.10 |

) |

— |

||||||||||||||

|

Total distributions |

(1.26 |

) |

(0.38 |

) |

(0.23 |

) |

(0.12 |

) |

(0.05 |

) |

|||||||||||||

|

Redemption fees |

— |

— |

— |

— |

— |

(b) |

|||||||||||||||||

|

Net asset value at end of year |

$ |

16.00 |

$ |

14.10 |

$ |

11.62 |

$ |

8.84 |

$ |

9.91 |

|||||||||||||

|

Total investment return(c) |

22.86 |

% |

24.80 |

% |

34.16 |

% |

(9.81 |

)% |

9.52 |

% |

|||||||||||||

|

Ratios/supplemental data: |

|||||||||||||||||||||||

|

Net assets, end of year (in 000's) |

$ |

81,019 |

$ |

73,956 |

$ |

71,195 |

$ |

61,928 |

$ |

86,212 |

|||||||||||||

|

Ratio of expenses to average net assets: |

|||||||||||||||||||||||

|

Before reimbursement from Adviser |

1.16 |

% |

1.34 |

% |

1.43 |

% |

1.37 |

% |

1.22 |

% |

|||||||||||||

|

After reimbursement from Adviser |

1.16 |

% |

1.22 |

% |

1.22 |

% |

1.20 |

% |

1.13 |

% |

|||||||||||||

|

Ratio of net investment income to average net assets: |

|||||||||||||||||||||||

|

Before reimbursement from Adviser |

(0.64 |

)% |

(0.75 |

)% |

(0.36 |

)% |

(0.19 |

)% |

0.05 |

% |

|||||||||||||

|

After reimbursement from Adviser |

(0.64 |

)% |

(0.63 |

)% |

(0.15 |

)% |

(0.02 |

)% |

0.14 |

% |

|||||||||||||

|

Portfolio turnover rate |

23 |

% |

60 |

% |

25 |

% |

79 |

% |

137 |

% |

|||||||||||||

(a) Per share amount is based on average shares outstanding.

(b) Rounds to less than $0.01 per share.

(c) Return is based on net asset value per share, adjusted for reinvestment of distributions, and does not reflect deduction of the sales charge.

See accompanying Notes to Financial Statements.

20

FPA U.S. CORE EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS

December 31, 2021

NOTE 1 — Significant Accounting Policies

FPA U.S. Core Equity Fund (the "Fund", formerly known as FPA U.S. Value Fund, Inc.) is registered under the Investment Company Act of 1940, as a diversified, open-end, management investment company. The Fund's primary investment objective is long-term growth of capital. Current income is a secondary consideration. The Fund qualifies as an investment company pursuant to Financial Accounting Standard Board (FASB) Accounting Standards Codification (ASC) No. 946, Financial Services — Investment Companies. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements.

A. Security Valuation

The Fund's investments are reported at fair value as defined by accounting principles generally accepted in the United States of America, ("U.S. GAAP"). The Fund generally determines its net asset value as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open. Further discussion of valuation methods, inputs and classifications can be found under Disclosure of Fair Value Measurements.

B. Securities Transactions and Related Investment Income

Securities transactions are accounted for on the date the securities are purchased or sold. Dividend income and distributions to shareholders are recorded on the ex-dividend date. Interest income and expenses are recorded on an accrual basis. Market discounts and premiums on fixed income securities are amortized over the expected life of the securities using effective interest rate method. Realized gains or losses are based on the specific identification method. The books and records of the Fund are maintained in U.S. dollars as follows: (1) the foreign currency fair value of investment securities, and other assets and liabilities stated in foreign currencies, are translated using the daily spot rate; and (2) purchases, sales, income and expenses are translated at the rate of exchange prevailing on the respective dates of such transactions. The resultant exchange gains and losses are included in net realized or net unrealized gain (loss) in the statement of operations.

C. Use of Estimates

The preparation of the financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported. Actual results could differ from those estimates.

NOTE 2 — Risk Considerations

Investing in the Fund may involve certain risks including, but not limited to, those described below.

Market Risk: Because the values of the Fund's investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund or the Fund could underperform other investments.

Common Stocks and Other Securities: The prices of common stocks and other securities held by the Fund may decline in response to certain events taking place around the world, including; those directly involving companies whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional or global political, social or economic instability; and currency, interest rate and commodity price fluctuations. In addition, the emphasis on a value-oriented investment approach by the Fund's investment adviser, First Pacific Advisors, LP ("Adviser"), generally results in the Fund's portfolio being invested primarily in medium or smaller sized companies. Smaller companies may be subject to a greater degree of change in earnings and business prospects than larger, more established companies, and smaller companies are often more reliant on key products or personnel than larger companies. Also, securities of smaller companies are traded

21

FPA U.S. CORE EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (Continued)

in lower volumes than those issued by larger companies and may be more volatile than those of larger companies. The Fund's foreign investments are subject to additional risks such as, foreign markets could go down or prices of the Fund's foreign investments could go down because of unfavorable changes in foreign currency exchange rates, foreign government actions, social, economic or political instability or other factors that can adversely affect investments in foreign countries. These factors can also make foreign securities less liquid, more volatile and harder to value than U.S. securities. In light of these characteristics of smaller companies and their securities, the Fund may be subjected to greater risk than that assumed when investing in the equity securities of larger companies.

Sector Risk: To the extent the Fund invests more heavily in particular sectors, its performance will be especially sensitive to developments that significantly affect those sectors. Individual sectors may be more volatile, and may perform differently, than the broader market. The following summarizes the risks associated with investing in certain sector(s) in which the Fund is more heavily invested:

◼ Information Technology Sector Risk: Companies in the information technology sector face intense competition, both domestically and internationally, which may have an adverse effect on their profit margins. Companies in this sector may have limited product lines, markets, financial resources or personnel. The products of information technology companies may face obsolescence due to rapid technological developments, frequent new product introduction, unpredictable changes in growth rates and competition for the services of qualified personnel. Companies in the information technology sector are heavily dependent on patent and intellectual property rights. The loss or impairment of these rights may adversely affect the profitability of these companies.

Repurchase Agreements: Repurchase agreements permit the Fund to maintain liquidity and earn income over periods of time as short as overnight. Repurchase agreements held by the Fund are fully collateralized by U.S. Government securities, or securities issued by U.S. Government agencies, or securities that are within the three highest credit categories assigned by established rating agencies (Aaa, Aa, or A by Moody's or AAA, AA or A by Standard & Poor's) or, if not rated by Moody's or Standard & Poor's, are of equivalent investment quality as determined by the Adviser. Such collateral is in the possession of the Fund's custodian. The collateral is evaluated daily to ensure its fair value equals or exceeds the current fair value of the repurchase agreements including accrued interest. In the event of default on the obligation to repurchase, the Fund has the right to liquidate the collateral and apply the proceeds in satisfaction of the obligation.

The Fund may enter into repurchase agreements, under the terms of a Master Repurchase Agreement ("MRA"). The MRA permits the Fund, under certain circumstances including an event of default (such as bankruptcy or insolvency), to offset payables and/or receivables under the MRA with collateral held and/or posted to the counterparty and create one single net payment due to or from the Fund. However, bankruptcy or insolvency laws of a particular jurisdiction may impose restrictions on or prohibitions against such a right of offset in the event of a MRA counterparty's bankruptcy or insolvency. Pursuant to the terms of the MRA, the Fund receives securities as collateral with a fair value in excess of the repurchase price to be received by the Fund upon the maturity of the repurchase transaction. Upon a bankruptcy or insolvency of the MRA counterparty, the Fund recognizes a liability with respect to such excess collateral to reflect the Fund's obligation under bankruptcy law to return the excess to the counterparty. Repurchase agreements outstanding at the end of the period are listed in the Fund's Portfolio of Investments.

Many countries have experienced outbreaks of infectious illnesses in recent decades, including swine flu, avian influenza, SARS and, more recently, COVID-19. The global outbreak of COVID-19 in early 2020 has resulted in various disruptions, including travel and border restrictions, quarantines, supply chain disruptions,

22

FPA U.S. CORE EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (Continued)

lower consumer demand and general market uncertainty. The full effects, duration and costs of the COVID-19 pandemic are impossible to predict, and the circumstances surrounding the COVID-19 pandemic will continue to evolve, including the risk of future increased rates of infection due to low vaccination rates and/or the lack of effectiveness of current vaccines against new variants. Similar consequences could arise as a result of the spread of other infectious diseases. Management will continue to monitor the impact COVID-19 has on the Fund and reflect the consequences as appropriate in the Fund's accounting and financial reporting.

NOTE 3 — Purchases and Sales of Investment Securities

Cost of purchases of investment securities (excluding short-term investments) aggregated $17,485,505 for the year ended December 31, 2021. The proceeds and cost of securities sold resulting in net realized gains of $8,872,776 aggregated $27,460,748 and $18,587,972, respectively, for the year ended December 31, 2021.

NOTE 4 — Federal Income Tax

No provision for federal income tax is required because the Fund has elected to be taxed as a "regulated investment company" under the Internal Revenue Code (the "Code") and intends to maintain this qualification and to distribute each year to its shareholders, in accordance with the minimum distribution requirements of the Code, its taxable net investment income and taxable net realized gains on investments.

Distributions paid to shareholders are based on net investment income and net realized gains determined on a tax reporting basis, which may differ from financial reporting. For federal income tax purposes, the Fund had the following components of distributable earnings at December 31, 2021:

|

Unrealized appreciation |

$ |

41,102,538 |

|||||

|

Undistributed capital gains |

4,511,079 |

||||||

|

Other temporary differences |

(206,760 |

) |

|||||

The tax status of distributions paid during the fiscal years ended December 31, 2021 and 2020 were as follows:

|

2021 |

2020 |

||||||||||

|

Dividends from ordinary income |

$ |

— |

$ |

— |

|||||||

|

Distributions from long-term capital gains |

6,172,342 |

2,152,118 |

|||||||||

The Fund utilizes the provisions of federal income tax laws that provide for the carryforward of capital losses for prior years, offsetting such losses against any future realized capital gains. The Fund did not generate or utilize capital losses during the current tax year.

The cost of investment securities held at December 31, 2021 was $39,789,395 for federal income tax purposes. Gross unrealized appreciation and depreciation for all investment at December 31, 2021, for federal income tax purposes was $41,253,905 and $151,208, respectively resulting in net unrealized appreciation of $41,102,697. As of and during the year ended December 31, 2021, the Fund did not have any liability for unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year, the Fund did not incur any interest or penalties. The statute of limitations remains open for the last 3 years, once a return is filed. No examinations are in progress at this time.

During the year ended December 31, 2021, the Fund reclassified $226,722 to Paid in Capital from Distributable Earnings to align financial reporting to tax reporting. These permanent differences are primarily

23

FPA U.S. CORE EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (Continued)

due to net operating losses and distributions made in connection with redemption of fund shares adjustments. Net assets were not affected by these reclassifications.

NOTE 5 — Advisory Fees and Other Affiliated Transactions

Pursuant to an Investment Advisory Agreement (the "Agreement"), advisory fees were paid by the Fund to First Pacific Advisors, LP (the "Adviser"). Under the terms of this Agreement, the Fund pays the Adviser a monthly fee calculated at the annual rate of 0.75% of the first $50 million of the Fund's average daily net assets and 0.65% of the average daily net assets in excess of $50 million. The Agreement obligates the Adviser to reduce its fee to the extent necessary to reimburse the Fund for any annual expenses (exclusive of interest, taxes, the cost of brokerage and research services, legal expenses related to portfolio securities, and extraordinary expenses such as litigation) in excess of 1.5% of the first $30 million and 1% of the remaining average net assets of the Fund for the year.

For the year ended December 31, 2021, the Fund paid aggregate fees and expenses of $60,243 to all Directors who are not affiliated persons of the Adviser. Certain officers of the Fund are also officers of the Adviser.

NOTE 6 — Disclosure of Fair Value Measurements

The Fund uses the following methods and inputs to establish the fair value of its assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued each day at the official closing price of, or the last reported sale price on, the exchange or market on which such securities principally are traded, as of the close of business on that day. If there have been no sales that day, equity securities are generally valued at the last available bid price. Securities that are unlisted and fixed-income and convertible securities listed on a national securities exchange for which the over-the-counter ("OTC") market more accurately reflects the securities' value in the judgment of the Fund's officers, are valued at the most recent bid price. Short-term corporate notes with maturities of 60 days or less at the time of purchase are valued at amortized cost.

Securities for which representative market quotations are not readily available or are considered unreliable by the Adviser are valued as determined in good faith under procedures adopted by the authority of the Fund's Board of Directors. Various inputs may be reviewed in order to make a good faith determination of a security's value. These inputs include, but are not limited to, the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations of investments that would have been used had greater market activity occurred.

The Fund classifies its assets based on three valuation methodologies. Level 1 values are based on quoted market prices in active markets for identical assets. Level 2 values are based on significant observable market inputs, such as quoted prices for similar assets and quoted prices in inactive markets or other market observable inputs as noted above including spreads, cash flows, financial performance, prepayments, defaults, collateral, credit enhancements, and interest rate volatility. Level 3 values are based on significant unobservable inputs that reflect the Fund's determination of assumptions that market participants might reasonably use in valuing the

24

FPA U.S. CORE EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (Continued)

assets. The valuation levels are not necessarily an indication of the risk associated with investing in those securities. The following table presents the valuation levels of the Fund's investments as of December 31, 2021:

|

Investments |

Level 1 |

Level 2 |

Level 3 |

Total |

|||||||||||||||

|

Common Stocks |

|||||||||||||||||||

|

Internet Media |

$ |

13,691,450 |

— |

— |

$ |

13,691,450 |

|||||||||||||

|

Infrastructure Software |

9,024,540 |

— |

— |

9,024,540 |

|||||||||||||||

|

Communications Equipment |

6,408,347 |

— |

— |

6,408,347 |

|||||||||||||||

|

E-Commerce Discretionary |

5,835,095 |

— |

— |

5,835,095 |

|||||||||||||||

|

Information Technology Services |

5,684,599 |

— |

— |

5,684,599 |

|||||||||||||||

|

Consumer Finance |

4,463,678 |

— |

— |

4,463,678 |

|||||||||||||||

|

Apparel, Footwear & Accessory Design |

3,398,953 |

— |

— |

3,398,953 |

|||||||||||||||

|

Application Software |

3,009,410 |

— |

— |

3,009,410 |

|||||||||||||||

|

Entertainment Content |

2,831,825 |

— |

— |

2,831,825 |

|||||||||||||||

|

Managed Care |

2,799,144 |

— |

— |

2,799,144 |

|||||||||||||||

|

Home Products Stores |

2,769,490 |

— |

— |

2,769,490 |

|||||||||||||||

|

Life Science Equipment |

2,155,905 |

— |

— |

2,155,905 |

|||||||||||||||

|

Retailing |

1,655,550 |

— |

— |

1,655,550 |

|||||||||||||||

|

Medical Devices |

1,630,479 |

— |

— |

1,630,479 |

|||||||||||||||

|

Cable & Satellite |

1,302,037 |

— |

— |

1,302,037 |

|||||||||||||||

|

Insurance Brokers |

1,184,621 |

— |

— |

1,184,621 |

|||||||||||||||

|

Health Care Services |

1,105,417 |

— |

— |

1,105,417 |

|||||||||||||||

|

Private Equity |

996,414 |

— |

— |

996,414 |

|||||||||||||||

|

Specialty Pharmaceuticals |

786,670 |

— |

— |

786,670 |

|||||||||||||||

|

Managed Health Care |

778,357 |

— |

— |

778,357 |

|||||||||||||||

|

Industrials |

660,334 |

— |

— |

660,334 |

|||||||||||||||

|

Automotive Retailers |

598,883 |

— |

— |

598,883 |

|||||||||||||||

|

Courier Services |

527,626 |

— |

— |

527,626 |

|||||||||||||||

|

Commercial & Residential Building Equipment & Systems |

478,620 |

— |

— |

478,620 |

|||||||||||||||

|

Institutional Brokerage |

408,346 |

— |

— |

408,346 |

|||||||||||||||

|

Internet Based Services |

384,755 |

— |

— |

384,755 |

|||||||||||||||

|

Household Products |

374,271 |

— |

— |

374,271 |

|||||||||||||||

|

Restaurants |

340,383 |

— |

— |

340,383 |

|||||||||||||||

|

Investment Management |

279,246 |

— |

— |

279,246 |

|||||||||||||||

|

Health Care Facilities |

247,928 |

— |

— |

247,928 |

|||||||||||||||

|

Entertainment Facilities |

237,420 |

— |

— |

237,420 |

|||||||||||||||

|

Other Common Stocks |

4,049,299 |

— |

— |

4,049,299 |

|||||||||||||||

|

Short-Term Investment |

— |

$ |

793,000 |

— |

793,000 |

||||||||||||||

|

$ |

80,099,092 |

$ |

793,000 |

— |

$ |

80,892,092 |

|||||||||||||

25

FPA U.S. CORE EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (Continued)

Transfers of investments between different levels of the fair value hierarchy are recorded at fair value as of the end of the reporting period. There were no significant transfers into or out of Level 3 during the year ended December 31, 2021.